89100 merged williams analyst...

TRANSCRIPT

We make energy happen.®

© 2017 The Williams Companies, Inc. All rights reserved.

Williams Analyst Day

May 11, 2017

NYSE: WMB

NYSE: WPZ

williams.com

WE MAKE ENERGY HAPPEN

2017 Analyst Day May 11, 2017

2 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17

Forward-Looking Statements

INTRO & AGENDA

> The reports, filings, and other public announcements of The Williams Companies, Inc. (Williams) and Williams Partners L.P. (WPZ) may contain or incorporate by reference statements that do not directly or exclusively relate to historical facts. Such statements are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements relate to anticipated financial performance, management’s plans and objectives for future operations, business prospects, outcome of regulatory proceedings, market conditions and other matters. We make these forward-looking statements in reliance on the safe harbor protections provided under the Private Securities Litigation Reform Act of 1995. All statements, other than statements of historical fact, included in this document that address activities, events or developments that we expect, believe or anticipate will exist or may occur in the future, are forward-looking statements. Forward-looking statements can be identified by various forms of words such as “anticipates,” “believes,” “seeks,” “could,” “may,” “should,” “continues,” “estimates,” “expects,” “forecasts,” “intends,” “might,” “goals,” “objectives,” “targets,” “planned,” “potential,” “projects,” “scheduled,” “will,” “assumes,” “guidance,” “outlook,” “in service date” and other similar expressions. These forward-looking statements are based on management’s beliefs and assumptions and on information currently available to management and include, among others, statements regarding:

– Levels of cash distributions by WPZ with respect to limited partner interests; – Levels of dividends to Williams stockholders; – Future credit ratings of Williams, WPZ and their affiliates; – Amounts and nature of future capital expenditures; – Expansion and growth of Williams’ business and operations; – Financial condition and liquidity; – Business strategy; – Cash flow from operations or results of operations; – Seasonality of certain business components; – Natural gas, natural gas liquids, and olefins prices, supply, and demand; and – Demand for our services.

> Forward-looking statements are based on numerous assumptions, uncertainties and risks that could cause future events or results to be materially different from those stated or implied in this document. Many of the factors that will determine these results are beyond our ability to control or predict. Specific factors that could cause actual results to differ from results contemplated by the forward-looking statements include, among others, the following:

– Whether WPZ will produce sufficient cash flows to provide the level of cash distributions that Williams expects; – Whether Williams is able to pay current and expected levels of dividends; – Whether WPZ elects to pay expected levels of cash distributions and Williams elects to pay expected levels of dividends; – Whether we will be able to effectively execute our financing plan including the receipt of anticipated levels of proceeds from planned asset sales; – Whether Williams will be able to effectively manage the transition in its board of directors and management as well as successfully execute its business restructuring; – Availability of supplies, including lower than anticipated volumes from third parties served by our midstream business, and market demand; – Volatility of pricing including the effect of lower than anticipated energy commodity prices and margins; – Inflation, interest rates, and general economic conditions (including future disruptions and volatility in the global credit markets and the impact of these events on customers and

suppliers); – The strength and financial resources of our competitors and the effects of competition; – Whether we are able to successfully identify, evaluate and timely execute capital projects and other investment opportunities in accordance with our forecasted capital

expenditures budget; – Our ability to successfully expand our facilities and operations; – Development of alternative energy sources;

3 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17

INTRO & AGENDA

Forward-Looking Statements, cont.

– The impact of operational and developmental hazards and unforeseen interruptions, and the availability of adequate insurance coverage for such interruptions; – The impact of existing and future laws, regulations, the regulatory environment, environmental liabilities, and litigation, as well as our ability to obtain permits and achieve

favorable rate proceeding outcomes; – Williams’ costs and funding obligations for defined benefit pension plans and other postretirement benefit plans; – WPZ’s allocated costs for defined benefit pension plans and other postretirement benefit plans sponsored by its affiliates; – Changes in maintenance and construction costs; – Changes in the current geopolitical situation; – Our exposure to the credit risk of our customers and counterparties; – Risks related to financing, including restrictions stemming from debt agreements, future changes in credit ratings as determined by nationally-recognized credit rating agencies

and the availability and cost of capital; – The amount of cash distributions from and capital requirements of our investments and joint ventures in which we participate; – Risks associated with weather and natural phenomena, including climate conditions and physical damage to our facilities; – Acts of terrorism, including cybersecurity threats and related disruptions; and – Additional risks described in our filings with the Securities and Exchange Commission (SEC).

> Given the uncertainties and risk factors that could cause our actual results to differ materially from those contained in any forward-looking statement, we caution investors not to unduly rely on our forward-looking statements. We disclaim any obligations to and do not intend to update the above list or announce publicly the result of any revisions to any of the forward-looking statements to reflect future events or developments.

> In addition to causing our actual results to differ, the factors listed above and referred to below may cause our intentions to change from those statements of intention set forth in this document. Such changes in our intentions may also cause our results to differ. We may change our intentions, at any time and without notice, based upon changes in such factors, our assumptions, or otherwise.

> Because forward-looking statements involve risks and uncertainties, we caution that there are important factors, in addition to those listed above, that may cause actual results to differ materially from those contained in the forward-looking statements. For a detailed discussion of those factors, see Part I, Item 1A. Risk Factors in Williams’ and WPZ’s Annual Reports on Form 10-K filed with the SEC on February 22, 2017.

4 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17

Agenda

INTRO & AGENDA

Continental Breakfast/Registration

Welcome and Introductions John Porter

CEO Perspective Alan Armstrong

Operations Micheal Dunn

Break

Atlantic-Gulf Rory Miller

West Walter Bennett

Break (Box Lunches)

Northeast G&P Jim Scheel

Financial Outlook Don Chappel

Closing Remarks Alan Armstrong

NYSE: WMB

NYSE: WPZ

williams.com

WE MAKE ENERGY HAPPEN

CEO Perspective Alan Armstrong, President and Chief Executive Officer

2 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Strategic Focus

Clear Vision Drives Transformation to Energy Infrastructure Leader

CEO PERSPECTIVE

Guiding Principle

Strategy remains focused on natural gas volumes

> North American natural gas to remain globally cost-advantaged, low volatility fuel for long-term

> Increase fee-based revenue

> Reduce commodity exposure

Large-scale, competitive positions generate long-term value

> Strong competitive advantages

> Provides attractive incremental investment opportunity

> Positioned to capture growth and operate efficiently

3 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Williams: Unmatched Assets, Uniquely Positioned to Serve Growing Natural Gas Demand

CEO PERSPECTIVE

Positioned for Long-term,

Sustainable Growth

Advantaged Assets Connect to

Opportunities in Stable Natural

Gas Market

Focus on Execution, Delivering on Our

Commitments

4 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Our Organization is Energized, Passionate and Focused on Shareholder Value Creation

CEO PERSPECTIVE

Our Imperatives

Safety > Operating safely in everything we do, every day

> Continuing to develop a best-in-class safety culture

Growth > Exercising capital discipline while pursuing attractive growth opportunities that leverage advantaged asset base

Efficiency > Streamlining organization around an even more focused strategy

> Driving continuous improvement in operating margin ratio

Execution > Meeting all of our sanctioned project cost, quality and timeline commitments

Financial Performance

> Driving long-term, sustainable distribution growth with strong coverage and credit profile

5 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Advantaged Asset Positions & Stable Natural Gas Market Drive Predictable Growth

6 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Source: EIA historical monthly prices, Wood Mackenzie forecasted monthly prices, NYMEX forward curve

U.S. Natural Gas: Stable, Low Volatility Investment vs. Global Commodity Market

CEO PERSPECTIVE

$0

$5

$10

$15

$20

$25

$120

$0

$30

$60

$90

$150 Forecast �

U.S. Natural Gas Revolution

Hurricane Katrina

Natural Gas Henry Hub Spot Price- Wood Mackenzie

Henry Hub Forward Curve

WTI Crude Oil Price- Wood Mackenzie

WTI Forward Curve

$/MMBtu $/Bbl

Speculative Bubble

Financial Crisis

Polar Vortex

OPEC Policy

Change

Less Predictable

Steady Trend

7 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Sources: Wood Mackenzie; historical Henry Hub natural gas price per the EIA

Natural Gas Demand, Not Price, Driving Williams’ Growth

CEO PERSPECTIVE

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

0102030405060708090

100110

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

$/MM

Btu

Bcf

/d $3.01

$4.37

$2.49

North American Natural Gas Demand by Sector (2010–2021)

Residential/ Commercial

Industrial Power Generation

LNG Exports

Mexico Exports

Transport/ Other

Henry Hub Price

8 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Source: Wood Mackenzie

LNG Impact: Exports Increasing Rapidly; Williams Contracted to Continued Volume Growth

CEO PERSPECTIVE

= Williams Partners long-term contract for firm transport to LNG supply

0

2,000

4,000

6,000

8,000

10,000

12,000

MM

cf/d

Sabine Pass Cove Point Cameron Freeport

Corpus Christi Elba Island Annual Average

Gulf Trace: 1,200 MMcf/d

Atlantic Sunrise: 350 MMcf/d

Gulf Connector: 75 MMcf/d

Gulf Connector: 400 MMcf/d

(Forecasted LNG Export Volumes)

U.S. LNG Export Volumes Reach 2.2 Bcf/d in Apr. 2017, Up from 1.4 Bcf/d in Dec. 2016

9 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Source: Wood Mackenzie

Williams Capturing Current and Future LNG Export Volumes

CEO PERSPECTIVE

Contracted

Market Access

Contracted

with 4 of 6 LNG Facilities In-service or Under

Construction (~2Bcf/d)

Market Access to Other 2

10 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Increased Industrial Demand to Support Ongoing Williams Growth

CEO PERSPECTIVE

0

1,000

2,000

3,000

4,000

5,000

6,000

2017 2018 2019 2020 2021

MM

cf/d

Other Methanol Fertilizers Chemicals Ethylene

50 identified projects

included

Includes modeled growth from

additional, smaller sub-sectors

~600 Mbpd of ethane for

ethylene feedstock

represents ~1.7 Bcf/d natural gas*

Incremental North American Gas Demand From Industrial Facilities Through 2021 by Sector/End Product

Source: Wood Mackenzie & WMB analysis *Incremental 1.7 Bcf/d of natural gas applies to all demand sectors and is not limited to the industrial sector

11 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Source: Wood Mackenzie

Williams Well Positioned to Serve Growing Industrial Uses

CEO PERSPECTIVE

50 Industrial Projects Driving

Natural Gas Demand Through 2021

12 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

*Source: EIA

Williams’ Opportunities to Capture Power Generation Demand Continue

CEO PERSPECTIVE

> Current Projects: Dalton Expansion, Hillabee Phase 1&2, Virginia Southside II

> Power sector continues making long-term investments

– 2017-2021: Additional 88 plants expected to come on line*

> Williams’ assets in close proximity to expected power generation expansion, especially in Northeast and Transco

Well More Than Half of Future Gas-fired Capacity Through 2021 to Be Sited in States Served by Transco

13 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Source: EIA

Natural Gas-fired Power Generation Projects Overlap Williams’ Advantaged Asset Footprint

CEO PERSPECTIVE

54 of 88 Projects

Located in Transco Corridor Totaling 33.6 Gigawatts in Nameplate Capacity

14 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Note: Chart excludes Canada, Alaska, West Coast, Rockies, Barnett, Gulf Coast conventional and GOM production that amounts to a decline of 2.5 Bcf/d through 2021; CV=Cotton Valley Source: Wood Mackenzie

Williams Positioned to Benefit from Significant Opportunities in Best Plays

CEO PERSPECTIVE

23.2

4.5

9.3

4.8 5.0

37.9

7.7 9.6

8.2 6.1

0

10

20

30

40

Northeast Eagle Ford Mid-Con Permian Haynesville + CV

Bcf

/d

+14.7 Bcf/d

+3.2 Bcf/d

+0.3 Bcf/d +3.4

Bcf/d +1.1 Bcf/d

Northeast Accounts for

More Than 70% of N.A.

Growth

Natural Gas Forecasted Production by Region (2016–2021)

15 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Note: CV = Cotton Valley Source: Wood Mackenzie NACPAT

Continued Growth Driven by Position in Most Economic and Largest Remaining Undrilled Gas-directed Reserves

CEO PERSPECTIVE

0

100

200

300

400

500

600

< $2.50 < $3.00 < $3.50 < $4.00 < $4.50 over $4.50

Marcellus Utica Haynesville + CV Remaining Gulf Coast US - Mid-Continent US - Rocky Mountains

Tcfe

Gas-directed Breakevens by U.S. Region ~425 Tcfe Under $4.00 Cumulative Remaining Risked Reserves

Northeast Has ~75% of

the Remaining Risked Reserves

Under $4

16 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Focus on Execution, Delivering on Our Commitments

17 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

CEO PERSPECTIVE

18 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Large, Complex Projects Now Driving Predictable Revenues, Sustainable Returns

CEO PERSPECTIVE

Placed $1.6+ Billion of Transco Projects in Service > Mobile Bay South III, CPV Woodbridge, Rockaway Lateral,

Northeast Connector, Virginia Southside, Leidy SE, Gulf Trace

Placed $1.4+ Billion of Deepwater Gulf of Mexico Projects in Service > Keathley Canyon Connector, Kodiak, Gulfstar One (Tubular

Bells & Gunflint)

Other Major Projects > Northeast Expansions, Bucking Horse Plant, Bayou Ethane

& Texas Belle Pipelines

19 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Ongoing Execution in Current Regulatory/ Political Environment

CEO PERSPECTIVE

Proactively communicating the tremendous value of U.S. natural gas

Executing robust campaigns to support major projects, especially Atlantic Sunrise > Industry-leading digital/social media

> TV, radio and print advertising

> Significant political, grassroots and community advocacy

> Win-win partnerships with key stakeholders

Progress on the federal landscape, realistic about opposition, especially at the local level

20 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Business Model Execution Strong Through Challenging 2015 – 1Q 2017 Period

CEO PERSPECTIVE

Operational & Financial Performance

> New record Transco peak-day volumes & Northeast G&P volumes

> Win-win G&P contract renegotiations (Dry Utica, Haynesville, Barnett & Mid-con)

> Intensified focus on streamlining the organization and reducing costs – 15% headcount reduction; SG&A/O&M costs down ~$130 MM; improving operating

margin ratio

> Delivered 8% WPZ Adjusted EBITDA growth 2016 vs. 2015

Repositioned for Continued, Sustainable, Long-term Growth

> Strengthened credit metrics; Focused on strong sustainable coverage

> Allocating capital to fee-based assets, away from commodity-exposed, consistent with large scale natural gas strategy

> ~$3.3 Billion Monetizations: Canada, Marcellus-for-Permian and Geismar* transactions

> Removed need for equity to fund attractive growth portfolio

*Geismar transaction expected to close in Summer of 2017. Adjusted EBITDA is a non-GAAP financial measure. A reconciliation of all non-GAAP financial measures used in this presentation to their nearest GAAP financial measures is included at the back of this presentation.

21 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

1 Adjusted EBITDA is a non-GAAP financial measure. A reconciliation of WPZ Adjusted EBITDA to Net Income is included at the back of this presentation. 2 WPZ Peers Include: BWP, ENBL, EPD, ETP, KMI, MMP, PAA, SEP and TRP 3 Historical EBITDA based on reporting disclosure for peer companies except for PAA and SEP in Q1’17 which are based on CapitalIQ consensus estimate as of May 4, 2017. Results reported in $ Canadian are translated to $US based on average exchange rate for each quarter per Capital IQ.

Proven Strategy Demonstrates Resiliency Through Challenging Markets

CEO PERSPECTIVE

Attractive Adjusted EBITDA1 Performance vs. Peers2,3

60

85

110

135

Q1 '15 Q2 '15 Q3 '15 Q4 '15 Q1 '16 Q2 '16 Q3 '16 Q4 '16 1Q'17

WPZ Peer A Peer B Peer C Peer D Peer E Peer F Peer G Peer H Peer I

High-quality fee-based revenue, drives peer-leading stability

and WPZ Adjusted EBITDA growth

WMB: Highly liquid, institutional-friendly option

to invest in WPZ’s underlying business

Fully contracted, fee-based expansion projects, advantaged

assets underpin Williams expected growth

WPZ

22 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Today’s Speakers: Deep Dive on Williams’ Commitment to Sustainable, Long-term Growth

CEO PERSPECTIVE

Don Chappel

Chief Financial Officer

Micheal Dunn

Chief Operating Officer

Rory Miller

Senior Vice President,

Atlantic-Gulf

Jim Scheel

Senior Vice President,

Northeast G&P

Walter Bennett Senior Vice

President, West

Focus on operational excellence

Investing in the future of America’s

fastest growing interstate pipeline

Long-term contracts, steady volumes driving

consistent revenues

Assets positioned to

capture significant opportunities

Financial positioning to

provide long-term, sustainable growth

23 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 A-

Williams: Best Basin Positions, Preeminent Market Access, Unmatched Scale

CEO PERSPECTIVE

Positioned for Long-term,

Sustainable Growth

Advantaged Assets Connect to

Opportunities in Stable Natural

Gas Market

Focus on Execution, Delivering on Our

Commitments

WE MAKE ENERGY HAPPEN

NYSE: WMB

NYSE: WPZ

williams.com

Operations Micheal Dunn, Chief Operating Officer

2 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 B-

Williams: Focused on Operational Excellence

Safety is the Number One

Company Imperative

Continuously Improving the

Reliability of Our Operations

Disciplined Project Execution and Cost

Management

OPERATIONS

3 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 B-

Williams’ Operations Team

OPERATIONS

Operating Areas

Operations Support

Walter Bennett West

Rory Miller Atlantic-Gulf

Jim Scheel Northeast G&P

John Seldenrust Engineering Services

Mark Cluff Safety and Ops. Discipline

Larry Larsen Central Services

Brian Letzkus Information Systems

4 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 B-

> Safety is an Imperative – The safety of our employees and assets

is our highest priority – Commitment to asset and pipeline

integrity programs – Process safety and pipeline integrity

enables our assets to be most reliable for our customers

> Continuous Improvement Safety Culture – Robust safety metrics help us ensure we

are focused on continuously improving – Continuous safety improvement focus

yields reliability benefits

Safety Focus

OPERATIONS

TIER 1 LOPC Events

of Greater Consequence

TIER 2 LOPC Events

of Lesser Consequence

TIER 3 Challenges to Safety Systems

TIER 4 Operating Discipline and Management

System Performance Indicators

5 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 B-

Reliability

OPERATIONS

> Performance – Strong Preventive Maintenance

Performance – Asset Performance Monitoring /

Optimization

> Predictability – Predictive Failure Analysis – Condition-Based Maintenance

> Continuous Improvement – Reliability programs include embedded

improvement processes – Dedicated team to share operational

lessons learned

Real-Time Gathering System Optimization

6 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 B-

Williams Project Excellence

OPERATIONS

Williams Project Life Cycle (PLC)

Commercial and FP&A

Development

Execution

Operations

Discover G0 Select G1 Define G2 Deliver G3 Integrate G4 G5

Decide to Initiate

Decide to Proceed

Decide to Continue

Decide to Sanction

Decide to Handover

Decide to Closeout

7 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 B-

Project Execution Excellence

OPERATIONS

> Disciplined Front End Processes – Well established Project Life Cycle process

– Improved cost estimates & schedules

> Well Orchestrated Project Execution – Highly capable teams led by experienced Project Managers

– Strong permitting and public outreach efforts

> Carefully Coordinated Startups & Handoffs – Improved commissioning processes

> Leadership Engagement in Project Governance – Robust project controls and project reporting cadence

> Multi-Year Efforts Are Paying Off – Leidy Southeast (AG, On Budget; On Time)

– Cabot 5th Expansion (NE, Below Budget, On Time)

– Gulf Trace (AG, Below Budget, 5 months early)

– In-flight projects show similar trends

Williams’ Project Management is Based On:

Gulf Trace Station 44

8 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 B-

Coming Soon: About $1.5 Billion of Regulated Expansions with Full 2017 ISD Nearing Completion

OPERATIONS

> Transco – Gulf Trace – ~1.2 Bcf/d expansion serving Cheniere Sabine Pass LNG export terminal placed in

service under budget and ahead of schedule

> Transco – Dalton Expansion – 0.4 Bcf/d Power Gen Southern Market Expansion – construction continues – expect full

in-service 3Q 2017 – on time

> Transco – Hillabee Phase 1 – 0.8 Bcf/d Power Gen Southern Market Expansion – construction continues – expect

partial service 2Q, full service 3Q 2017 – on time

> Transco – New York Bay Expansion – 0.1 Bcf/d Northern Market Expansion – expect in-service 4Q 2017 – on time

> Transco – Virginia South Side Phase II – 0.3 Bcf/d Power Gen Southern Market Expansion – expect in-service 4Q 2017 – on time

9 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 B-

Atlantic Sunrise & Susquehanna Supply Hub Expansion: Key Energy Infrastructure

OPERATIONS

> Atlantic Sunrise: – ~$2.6B1 (100%) Forecasted CapEx; 1.7 Bcf/d Fully Committed;

15-year Binding Firm-Transportation Agreements

– Project Status: • FERC order received Feb 3, 2017 • Full project target in-service date: mid-2018 (financial plan further

risks cash flows by ~6 months, which results in a phased approach)

– Early Mainline Service (Station 195 to Station 85) • Reversals at six Transco stations • Add compression at one Transco station • Construction began on March 16, 2017

– Early Initial Service on Central Penn Line • 186 miles of new pipeline • Add compression at two Transco stations • Subject to certain environmental construction windows

– Full Project In-Service • Two new compressor stations on Central Penn Line

> Northeast G&P: Susquehanna Supply Hub Expansion: – Major expansion allowing Cabot to fulfill 850,000 Dth/d firm

Commitment to Atlantic Sunrise

– 49,000 new horsepower at two new compression facilities and 59 miles of 12” and 24” pipelines

– Key takeaway project expected to drive additional gathering volumes in the region

Atlantic Sunrise 1.7 MMDth/d Mid 2018

Cove Point LNG

1 As per FERC filing.

10 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 B-

1 Excludes Constitution which is appealing the denial of a required permit, and is not included in financial forecast.

Steady Progress on Over $4 Billion of Projects in the Pipeline with Post-2017 In-Service Dates

OPERATIONS

FERC Certificate Application Filed

FERC Certificate

Major Construction Activities

In-Service

REGULATORY MILESTONES FOR FULLY CONTRACTED REGULATED EXPANSIONS1

Other Federal / State / Local Permits

Gulf Connector Filed 8/16

St. James Supply Filed 2/17

NE Supply Enhancement

Filed 3/17

Hillabee Ph 2 Received 2/16

Garden State Began 2/17

Atlantic Sunrise Began 3/17

11 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 B-

Sharp Focus on Key Performance Indicator: Operating Margin Percentage

OPERATIONS

> OM% neutralizes diversity in practice among peers in classification of expenses e.g., O&M vs. G&A

> Measured on a GAAP basis for comparison to peers

> Cost efficiency metric designed to measure the percentage of profits impacting the bottom line

> Strong and consistent year-over-year improvement

$ in millions

Operating Margin %1 Performance

53%

57% 60%

45%

50%

55%

60%

65%

$0

$1,500

$3,000

$4,500

$6,000

2014 2015 2016

Gross Margin Operating Margin OM%

> Combination of growth in gross margin and sharp focus on cost efficiency expected to drive increase in operating margin %

> 2017: streamlining operating areas, closing OKC office

~13% Improvement in Operating Margin % from 2014 to 2016

Positioned to Continue Improvement

1 Gross Margin = Total revenues less related product costs expressed here as an absolute amount. Operating Margin % = operating margin / gross margin. Operating margin = gross margin less operating and maintenance costs and selling, general and administrative expenses. Depreciation and amortization expense, impairment charges and other expenses not associated with operating the business are excluded. Operating Margin % is a non-GAAP financial measure. A reconciliation to the most relevant GAAP measure is included in this presentation.

12 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 B-

Williams: Focused on Operational Excellence

OPERATIONS

Safety is the Number One

Company Imperative

Continuously Improving the

Reliability of Our Operations

Disciplined Project Execution and Cost

Management

WE MAKE ENERGY HAPPEN

NYSE: WMB

NYSE: WPZ

williams.com

Atlantic – Gulf Rory Miller, Senior Vice President

2 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

Connecting the Best Markets to World’s Lowest-cost Supplies

ATLANTIC – GULF

Executing on $7 Billion in

Projects, Doubling Transco Capacity

20+ Demand-driven Interstate Projects

in Development

New Deepwater Investment Cycle

Underway

3 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

In service. *Wood Mackenzie 2H 2016 forecasted demand growth through 2021 in states which Transco passes through. **Assuming successful and prompt resolution of permit litigation.

$7 Billion in Interstate Pipeline Expansions Inked and Underway

ATLANTIC – GULF

Leidy Southeast (0.5 Bcf/d)

Virginia Southside II (0.3 Bcf/d) Rock Springs Expansion

(0.2 Bcf/d)

Dalton Expansion (0.4 Bcf/d)

Hillabee Phase 1&2 (1.0 Bcf/d)

Atlantic Sunrise (1.7 Bcf/d)

Constitution** (0.7 Bcf/d)

Bcf/d

Williams New/Recent Project Capacity 7.4

*Forecasted Demand Growth 13.7

St. James Supply (0.2 Bcf/d)

Gulf Trace (1.2 Bcf/d)

New York Bay Expansion (0.1 Bcf/d)

Gulf Connector (0.5 Bcf/d)

Northeast Supply Enhancement

(0.4 Bcf/d)

Garden State Expansion (0.2 Bcf/d)

20+ Additional Projects in

Development

4 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

1 In-service dates for projects not yet in service represent expected in-service dates. Expected in-service dates assume timely receipt of all necessary regulatory approvals. Constitution, which is appealing the denial of a required permit, is not included in financial forecast.

2 Excludes impact of any early in-service revenues. 3 Targeting partial service to begin 2H 2017, full-in service mid 2018; financial plan further risks cash flows by approximately six months.

Strong EBITDA Projected from Current Project Slate

ATLANTIC – GULF

Transco Project Return Profile – Projects Placed In-service1

2015–2016 20172 2018–2020

Growth Capital Placed In-service ($ B)

$1.5 $1.5 $4.0

Full-year Run Rate Modified EBITDA ($ B)

~ $0.25 ~ $0.25 ~ $0.65

Projects Mobile Bay South 3 CPV Woodbridge

NE Connector Rockaway Lateral Leidy Southeast

Virginia Southside Rock Springs

Garden State I Gulf Trace

Dalton Hillabee (Ph. 1)

Virginia Southside II NY Bay Expansion

St. James Supply Gulf Connector

NE Supply Enhancement Hillabee (Ph. 2) Garden State II

Atlantic Sunrise3

5 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

Note: Includes all system deliveries and all zones. 1 Contracted Incremental Expansion Projects include: Gulf Trace: 1.2 MMDt/d (placed in-service Feb 1, 2017); Hillabee Phase 1 and 2: 1.0 MMDt/d; Dalton: 0.4 MMDt/d; Garden State: 0.2

MMDt/d; Virginia Southside 2: 0.3 MMDt/d; NY Bay Expansion: 0.1 MMDt/d; Atlantic Sunrise: 1.7 MMDt/d; Gulf Connector: 0.5 MMDt/d; NE Supply Enhancement 0.4 MMDt/d; St James Supply: 0.2 MMDt/d.

2 Sum of Heating Degree Days for Mid Atlantic plus South Atlantic regions.

Transco: Doubling Contracted Capacity Since 2010

ATLANTIC – GULF

Transco Peak Day Volumes and Contracted Capacity1 vs Heating Degree Days2

8.5 8.6 8.9 9.5 9.6

10.1 10.1

11.5 11.7

14.5

16.4 17.1

17.7

0

1,000

2,000

3,000

4,000

5,000

6,000

8

10

12

14

16

18

20

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Jan-F

eb H

DD

2 M

MD

t/d

Contracted Capacity Peak Day Jan-Feb HDD

6 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

Interconnects Reflect Unique Position of Transco, a Transportation Network Unlike Any Other

ATLANTIC – GULF

0

1

2

3

4

5

6

7

8

2012 2013 2014 2015 2016 2017+

Des

ign

Cap

acit

y (B

cf/d

)

Bi-directional Delivery Receipt

22 Bcf/d

Since 2012

Annual Installed Interconnect Capacity on Transco Paid for by Others

7 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

Atlantic Sunrise: Largest-ever Transco Expansion Unlocks Low-cost Supplies for Major Markets

ATLANTIC – GULF

Atlantic Sunrise 1.7 MMDth/d Mid 2018

> In 2019, Atlantic Sunrise expected to account for ~25% of Eastern Interstates’ Modified EBITDA

> Fee based revenue for early in-service in 2018

– Early mainline service ~ $4.5 million/month

– Central Penn line ~ $24 million/month

> When project is fully in service, fee-based revenue will be $35 million/month

Atlantic Sunrise

Remainder of the Eastern Interstates

Cove Point LNG

8 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

Dalton Expansion: On Track for On-schedule Delivery

ATLANTIC – GULF

Starts at Station 210

Ends at Holmesville,

MS

115 Miles Greenfield

Lateral

> Conservation success story

> Target in-service date: July 2017

– Monthly fee-based revenue of approximately $6 million

> 448 MDth/d

> Customer: AGL, Oglethorpe

> Early mainline service April 2017: ~ $4 million/month fee based revenue

9 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

205

200

River Road

Rockaway Delivery Point 207

210

195

Narrows

0

207

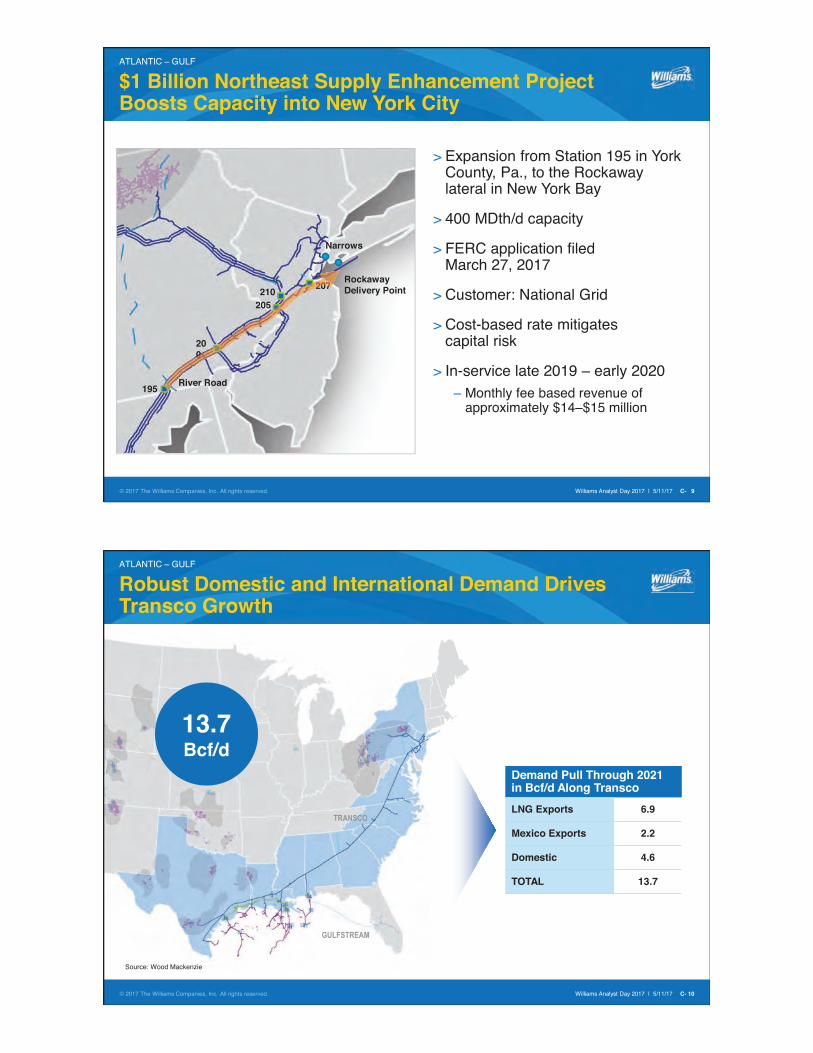

$1 Billion Northeast Supply Enhancement Project Boosts Capacity into New York City

ATLANTIC – GULF

> Expansion from Station 195 in York County, Pa., to the Rockaway lateral in New York Bay

> 400 MDth/d capacity

> FERC application filed March 27, 2017

> Customer: National Grid

> Cost-based rate mitigates capital risk

> In-service late 2019 – early 2020 – Monthly fee based revenue of

approximately $14–$15 million

10 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

Robust Domestic and International Demand Drives Transco Growth

ATLANTIC – GULF

Demand Pull Through 2021 in Bcf/d Along Transco

LNG Exports 6.9

Mexico Exports 2.2

Domestic 4.6

TOTAL 13.7

Transco Growth

13.7 Bcf/d

TRANSCO

GULFSTREAM

Source: Wood Mackenzie

11 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

Transco Plays a Key Role in Connecting Low-cost LNG to Global Gas Markets

ATLANTIC – GULF

The gas demand to serve LNG export facilities along

Transco is expected to grow by ~7 Bcf/d through 2021*

> A pipeline reversal to deliver gas to the Sabine Pass Liquefaction Facility 2

> Provides 1.2 Bcf/d of incremental capacity to Transco

> In service Feb. 2017

Gulf Trace

> Will deliver 75 MMcf/d to Freeport’s liquefaction project by the second half of 2018

> Will deliver 400 MMcf/d to Cheniere’s Corpus Christi liquefaction terminal in 2019

Gulf Connector

> 350 MMcf/d capacity to serve Cove Point

Atlantic Sunrise

*Wood Mackenzie

Cove Point

Elba Island

Sabine Pass

ee Cameron aPFreeport FreeepFree

Corpus Christi

12 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

Gulf Trace: Early in Service, Under Budget

ATLANTIC – GULF

13 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

Pursuing 20+ Different Demand-Driven Expansion Opportunities Across Eastern Interstates

ATLANTIC – GULF

> Potential projects are primarily demand pull and along existing corridor

– Power generation

– Industrial demand

– LDC demand

– LNG / Mexican exports

> In final negotiations on three projects

7 in the Northeast

4 in the Mid-Atlantic

10 in the Southeast

& Gulf

14 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

0

50

100

150

200

250

300

Plant Gas Usage at6,800 Btu/kWh,100% Utilization

Plant Gas Usage at65% Utilization

Plant Gas Usage at50% Utilization

Contracted Capacityon Transco

MM

cf/d

Source: WMB analysis

Natural Gas: First Choice for New Power Plants

ATLANTIC – GULF

Transco’s Virginia Southside II Expansion Project to Serve Proposed Gas-fired Power Plant in Greensville County, VA

Transco’s Virginia Southside II Contracted Capacity vs. Potential Power Plant Gas Burn

15 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

Investing in the Future of America’s Fastest Growing Interstate Gas Pipeline

ATLANTIC – GULF

> Fulfilling obligation to customers, shareholders and public to modernize system

> Defined Transco modernization program to upgrade and/or replace HP/compression and pipeline facilities

> Evaluating various capital recovery methods allowable under FERC policy

– Modernization tracker vs. rate case

> Customer education and participation

> Rate case milestones – Filing date: August 31, 2018

– Base period: June 1, 2017 – May 31, 2018

– Test period: June 1, 2018 – Feb. 28, 2019

– Effective date: March 1, 2019

16 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

Right Assets, Right Skills Provide Strong Competitive Advantage for New Gulf of Mexico Investment Cycle

ATLANTIC – GULF

Perdido

Salina

Perdido

Salina

17 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

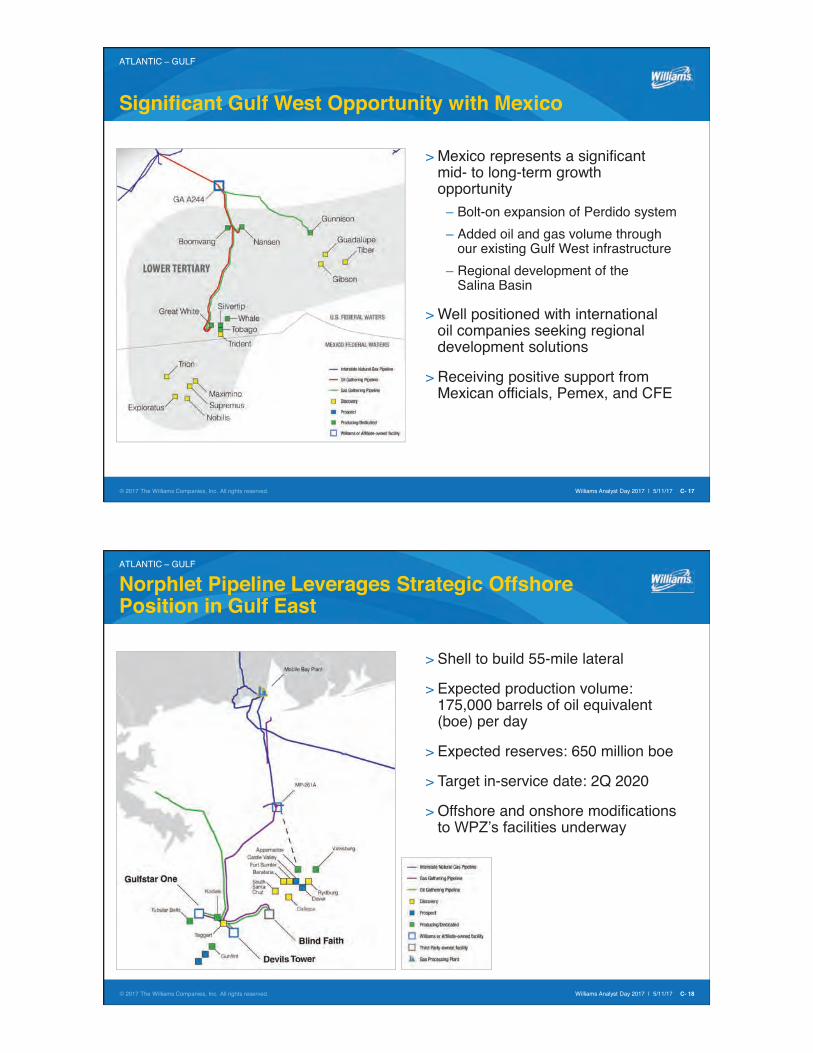

Significant Gulf West Opportunity with Mexico

ATLANTIC – GULF

> Mexico represents a significant mid- to long-term growth opportunity

– Bolt-on expansion of Perdido system

– Added oil and gas volume through our existing Gulf West infrastructure

– Regional development of the Salina Basin

> Well positioned with international oil companies seeking regional development solutions

> Receiving positive support from Mexican officials, Pemex, and CFE

18 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

Norphlet Pipeline Leverages Strategic Offshore Position in Gulf East

ATLANTIC – GULF

> Shell to build 55-mile lateral

> Expected production volume: 175,000 barrels of oil equivalent (boe) per day

> Expected reserves: 650 million boe

> Target in-service date: 2Q 2020

> Offshore and onshore modifications to WPZ’s facilities underway

19 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

Continued Opportunity on Discovery System

ATLANTIC – GULF

> Strategically located in the deepwater, Keathley Canyon Connector (KCC) continues to provide long-term growth opportunities

> Discovery’s joint venture structure allows for the allocation of project risk and capital (60% Williams)

> Discoveries along the KCC corridor include over 1 TCF of gas reserves

20 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 C-

Connecting the Best Low-Cost Supplies to the Best Global Markets

ATLANTIC – GULF

Executing on $7 Billion in

Projects, Doubling Transco Capacity

20+ Demand-driven Interstate Projects

in Development

New Deepwater Investment Cycle

Underway

WE MAKE ENERGY HAPPEN

NYSE: WMB

NYSE: WPZ

williams.com

West Walter Bennett, Senior Vice President

2 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 D-

Large Portfolio of Efficient Operations Positioned to Produce Long-term Sustainable Cash Flows

WEST

Large Portfolio of Reliable Assets

Connect Supplies to Opportunities

Positioned for Long-term Stability

and Growth Opportunities

Strong Focus on Cash Flow and

Operational Discipline

3 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 D-

Portfolio of Reliable Assets

WEST

Asset Type Key Asset Characteristics

Interstate Gas Pipeline

~3,900 pipeline miles

3.8 MMdth/d reserved capacity

366 delivery points

Gas Gathering

12,774 pipeline miles

8.8 Bcf/d inlet

capacity

22,000+ receipt points

Gas Processing

7 plant sites

4.2 Bcf/d inlet

capacity

189 Mbpd NGL production

capacity

Interstate NGL Pipeline

1,096 pipeline miles

255 Mbpd transport capacity

17 receipt points

NGL Services

~50 Mbpd fractionation

capacity

~20 MMbbls storage capacity

8 pipeline interconnects

& truck/rail terminal

OVERLAND PASS

NORTHWEST

4 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 D-

Rockies Basins

Western Canada Sedimentary Basin

Clay Basin

Jackson Prairie

Plymouth

Avista Cascade Intermountain Gas Northwest Natural Puget Sound Energy Sierra / Southwest Gas

Northwest Pipeline: Giving End-market Consumers Reliable Access to Low-cost Gas Supply

WEST

> Low-cost, primary service provider in the Pacific Northwest

– ~3,900-mile system with 3.8 Bcf/d peak design capacity

– Access to 120 Bcf of storage along pipeline, high injection and delivery capability in market area

– Primary Washington high pressure gas delivery west of Cascade Mountains

> Bi-directional design – Flexibility: Canadian gas to market and

Rockies gas to market – Cheapest supply drives flow patterns

> Prolific supply sources – U.S. sources: Greater Green River,

Piceance, San Juan – Canadian sources: Montney, Western

Canadian Sedimentary Basin

> Significant market options – 366 delivery points totaling 9.7 Bcf/d of

delivery capacity

Critical Existing Infrastructure – Fully Contracted Demand Charge Revenue

5 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 D-

Note: Population density data per US Census Bureau Census 2010 Summary File 1 population by census tract.

Unrivaled Position in Pacific Northwest Market: Current Demand and Potential Future Growth

WEST

Scale, Flexibility, and Location Create Competitive Advantages

Boise

Portland

Seattle

Spokane

Tacoma

e

Olympia

In 2016 Northwest Pipeline Supplied 89% of Washington Demand and 100% of Seattle/Tacoma Demand

Pacific Northwest Advantaged for Asian Export Markets:

> Methanol > LNG

Pacific Northwest’s Current Primary Market Areas:

> Seattle > Tacoma > Portland > Spokane > Boise

6 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 D-

1 Capacity is long-term, maximum rate, Rate schedule TF-1 capacity as of 12/31/2016.

Exceptional Contract Profile Demonstrates Strength of Access to Market Demand

WEST

Majority of Customers Have Strong Investment Grade Ratings

Northwest Pipeline Contract Base Predominately “Demand Pull” Customers

Northwest Pipeline Revenue Predominately Demand Charges

76%

17%

6% 1%

Firm Capacity1 by Customer Type

Utilities/LDC MarketerEnd-User Producer

95%

5%

2016 Revenue by Type

Demand Charge Throughput Revenue

7 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 D-

9.4 9.4 9.9

10.5 9.7

9.2

10.1 9.5

0

2

4

6

8

10

12

Northwest Pipeline Average Remaining Contract Life (Years) History

Reliability, Customer Satisfaction, and Location Advantage Drive Continued Contract Renewals

WEST

> Continued customer renewals reflect critical nature of Northwest Pipeline infrastructure

> Exceptional system reliability

– 2016 – 99.9%

– 2015 – 100%

– 2014 – 99.9%

> Top 10 percent of all interstate pipelines for customer service1

1 2017 Mastio Survey

8 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 D-

New Demand Drives Contracted Expansion Opportunities

WEST

$75 Million Capital Investment Opportunity at Attractive Regulated Pipeline Returns

North Seattle Lateral Upgrade

> Will provide up to 196 MDth/d of incremental firm lateral capacity to Puget’s Seattle market area – Anticipated FERC certificate filing: May 2017

– Anticipated in-service: November 2019

Kalama Lateral

> Will serve NW Innovation Works’ proposed methanol plant for export to markets in China – 320 MDth/d new firm lateral capacity

– FERC certificate received: April 2016

– Anticipated in-service: Late 2020

9 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 D-

Potential Expansion Opportunities Due to Local and Global Demand Sources

WEST

Mainline Expansion

> Sumas Express: Market driven expansion(s) to serve increases in LDC, electric generation, and/or industrial firm transportation needs from British Columbia

LNG Export

> Island Gas Connector: Deliver British Columbia natural gas to Steelhead LNG’s proposed facilities on Vancouver Island

> Jordan Cove/Pacific Connector: Investment opportunity to partner with Veresen

Regional Coal Conversions

> Planned coal plant retirements by 2025 drive increased natural gas demand for power generation

10 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 D-

Key Producer Customers

Provide Large Acreage

Dedications

Partnering with Customers

Under Long-term Contracts

> Long-term acreage dedications, low contract risk

> Aim to maximize production volume and minimize cost

Cash Flows > Long-term stable cash flows from portfolio of assets

Large-scale West Gathering, Processing & NGL Assets Aligned with Significant Hydrocarbon Reserves

WEST

Strong Portfolio of Customers Active Across Range of Supply Areas

OVERLAND PASS

NORT

HWES

T

11 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 D-

1 Anadarko volumes exclude SCOOP and STACK. 2 Eagle Ford includes Black Oil, Hawkville Condensate, Maverick Condensate and Maverick Oil sub-plays. 3 Haynesville volumes include Caspiana Core, Greenwood-Waskom and Spider sub-plays.

Wood Mackenzie Forecast Points to Stable Volumes from West G&P Portfolio

WEST

2016–2026 Composite CAGR of (0.2)%

0

2

4

6

8

10

12

14

16

18

20

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026Nat

ura

l Gas

Pro

du

ctio

n (

Bcf

/d)

Areas with Williams West G&P Assets

Anadarko Eagle Ford Fort WorthGreater Green River Haynesville PiceancePowder River Basin San Juan

1 2

3

Factors Driving West G&P Volumes Across Portfolio Include:

> Available infrastructure

> Proximity to growing markets

> New technologies unlocking new resources, improving economics of established reserves

> Regionally focused producers

Wood Mackenzie Production Forecast (Bcf/d):

12 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 D-

1 Excludes Cotton Valley production; 2 Wood Mackenzie NACPAT; 3 Chesapeake Analyst Day, 10/20/2016 noted 1,425 undrilled locations, after effect of announced acreage sales; 4 Chesapeake Guidance, 2/23/2017

Haynesville – Significant Footprint in Most Economic Dry Gas Basin Outside of Northeast

WEST

Proximity to Demand Growth and Infrastructure Ready

Henry Hub Henry

Texas Louisiana

Key Customers

> Chesapeake > Exco

Service Offering, Assets &

Competitive Position

> Gathering, compression & treating

> 1.7 Bcf/d of gathering capacity; 598 miles of pipeline

> Largest gatherer in Louisiana Haynesville Shale1

Basin Attributes and

Customer Activities Driving Growth

> Largest, most economic remaining gas reserves outside of Northeast

� ~40 Tcfe recoverable at <$3.50 Henry Hub2

> Significant existing infrastructure > Proximity to Gulf Coast markets and multiple

pipeline takeaway options > Strong recent well results: ROTC 1H and CA

1H wells IP ~40 MMcf/d with 10,000’ laterals > Chesapeake ~1,400 undrilled locations3;

2017 expecting 3 rigs, 30-35 Spuds & 32-37 TILs in 20174

> Pursuing additional business in close proximity to our assets

> Optimizing system capabilities to meet expected growth

13 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 D-

1 50% owner and operator; 2 Wood Mackenzie NACPAT; 3 45% IRR assumes $10 mm well cost, $3 Henry Hub and $55 WTI; BP Upstream Field Trip 2016, “Lower 48 deep dive” June 2016; 4 Ultra Petroleum press release, March 15, 2017; 5 Chesapeake Investor Presentations, 1/20/2017 and 2/14/2017

Wyoming – Regionally Focused Producers Concentrate on Prolific Oil, Gas and NGL Reserves

WEST

Largest Gas Processor in Wyoming; Producer Economics Improving

OVERLAND PASS

NORT

HWES

T

Key Customers

> BP > Ultra Petroleum > Chesapeake

Service Offering, Assets &

Competitive Position

> Gathering & Processing > SW Wyoming gathering & Opal processing > Wamsutter gathering & Echo

Springs processing > Jackalope gathering & Bucking Horse

processing1 > Largest gas processor in Wyoming

Basin Attributes and

Customer Activities Driving Growth

> Rich gas & oil directed drilling > Greater Green River contains 15.4 Tcfe

recoverable at <$3.50 Henry Hub2

> Introduction of horizontal drilling and enhanced completion techniques

> Exploration of stacked pay resource > BP horizontal wells delivering up to 45% IRR;

~2,000 horizontal locations identified3

> Ultra Petroleum expects 245 new gross Wyoming wells in 20174

> Chesapeake ~2,600 risked locations; 2017 expecting 2 rigs; 25-30 wells; 28-33 TILs5

14 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 D-

1 Wood Mackenzie NACPAT, range of break-evens for Black Oil sub-play for Chesapeake and other customers; 2 Chesapeake IR Presentation 1/20/2017; 3 Chesapeake IR Presentation 2/14/2017; 4 Chesapeake 1Q’17 Earnings Presentation, 5/4/2017

Eagle Ford Shale: Well-positioned for Growth Expected From Announced Drilling Activity

WEST

175+ New Wells Expected in Eagle Ford in 2017

Key Customers

> Chesapeake > EOG

Service Offering, Assets &

Competitive Position

> Gathering, treating & compression

> 0.7 Bcf/d gathering capacity; 135 MMcf/d treating capacity; 1,010 miles of pipeline

> Premier sour gas gatherer and treater in Eagle Ford Shale

Basin Attributes and

Customer Activities Driving Growth

> Oil directed drilling, with associated gas

> Break-evens range from $35–$65 WTI1

> Proximity to Gulf Coast crude markets and gas demand growth

> Chesapeake expects to be active

� >4,000 Eagle Ford locations2

� Expect average lateral length >10,000’ 3 � 5 to 7 rigs, 175-195 Spuds and 155-175 TILs in

20174

> Increasing customer diversification > Expanding gathering and treating capacity

for expected growth

15 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 D-

1 Capacity varies with NGL component make-up.

Downstream NGL Assets Provide Attractive Markets for Liquids Production from West G&P Assets

WEST

121 152 164 169 185 202 201 197 204

OPPL Volumes (Mbpd) C3+ Ethane

OVERLAND PASS

NO

RT

HW

ES

T

Overland Pass

Pipeline

> Mixed NGL pipeline, nominal capacity 255 Mbpd1

> Attractive path to market for Williams Wyoming and Rockies NGL production

> Access to DJ, Bakken and Powder River volumes

> Steady volume performance through commodity cycle

> Exploring expansion opportunity to serve growing western volumes

Mid-Continent Frac and Storage

> 50% interest in and operator of ~100 Mbpd fractionator

> ~20 MMbbls of underground storage (Mixed and purity NGLs and specialty products)

> 8 pipeline interconnects; active truck and rail terminals

> Component of integrated G&P solution for West producers

> Supplies Mid-continent demand sources: crop-drying, refining and fuels, petchem, and Canadian diluent

16 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 D-

Large Portfolio of Efficient Operations Positioned to Produce Long-term Sustainable Cash Flows

WEST

Large Portfolio of Reliable Assets

Connect Supplies to Opportunities

Positioned for Long-term Stability

and Growth Opportunities

Strong Focus on Cash Flow and

Operational Discipline

NYSE: WMB

NYSE: WPZ

williams.com

WE MAKE ENERGY HAPPEN

Northeast G&P Jim Scheel, Senior Vice President

2 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

Williams in the Northeast: Well-positioned for More Significant Growth

Foundational, Large-scale Assets

Established in Best Acreage

Demand vs. Takeaway Capacity:

Key Issue Being Addressed

Positioned for Even More Significant

Growth

NORTHEAST G&P

3 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

Foundational Assets in Place

NORTHEAST G&P

Large-scale Position Spanning Marcellus/Utica Wet/Dry Gas

4 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

Foundational Assets in Place

NORTHEAST G&P

Largest Gathering Footprint in NE Pennsylvania Dry Gas

> Large-scale supply hubs in the heart of highly productive/low cost dry-gas Marcellus

> 5.7 Bcf/d of gathering capacity with extensive, reliable, robust delivery point capabilities

> Production in supply hubs has access to Northeast, Canadian, Southeast, Mid-Atlantic, and Gulf Coast markets.

> Acreage dedications covering most of Susquehanna, Bradford counties from top-tier producers

BRADFORD SUPPLY HUB

SUSQUEHANNA SUPPLY HUB

5 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

1 Gathering and processing statistics for Utica Supply Hub do not include Blue Racer. 2 Non-operated joint venture.

Foundational Assets in Place

NORTHEAST G&P

Powerful Combination of Assets in SW Marcellus/Utica Wet/Dry Gas

> Extensive acreage dedications and long-term contracts liquids-rich Marcellus and dry Utica

> 1.5 Bcf/d of gathering capacity in dry/wet gas

> 800+ MMcf/d processing capacity

> 120,000+ bpd fractionation and de-ethanization capacity

> Extensive CHK acreage dedication in both the liquids-rich and dry windows of the Utica

> 1.2 Bcf/d of gathering capacity in dry/wet systems

> 800 MMcf/d of processing capacity

> 135,000 bpd fractionation capacity

UTICA SUPPLY HUB1

> Cardinal Gathering > Flint Gathering > Utica East Ohio (UEO)2

OHIO RIVER SUPPLY HUB

> Ohio River Midstream > Laurel Mtn Midstream > Marcellus South

BLUE RACER MIDSTREAM2

6 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

Established, Large-scale Position Creates Advantages

NORTHEAST G&P

> Best-in-Class Operational Efficiency – Consistently moving 98%+ of available gas

– Planning with producers to efficiently optimize system capacities

– Focused on driving down cost structure

– Resolved geotechnical challenges

> Efficient Incremental Capital Investment

– All critical gathering infrastructure is in place

– Volume expansions focused primarily on compression and processing expansions

– Producers often providing well connects to core gathering system

– Timing capital to correspond to rig activity

> Speed-to-Market Advantage – Deploying standardized compression,

dehydration and processing

– Responsive to customers’ production schedules

7 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

Customer Base Has Evolved

NORTHEAST G&P

> Consolidation in E&P space means more stable, high-quality producer customers

> Producers have significantly increased their efficiency in the past few years as they continue to gain better understanding of basin

– Wells per pad increasing

– Cost to drill decreasing

8 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

Source: Wood Mackenzie Note: Chart excludes Canada, Alaska, West Coast, Rockies, Barnett, Gulf Coast conventional and GOM production that amounts to a decline of 2.5 Bcf/d through 2021

Williams Positioned to Benefit from Significant Opportunities in Best Plays

NORTHEAST G&P

23.2

4.5

9.3

4.8 5.0

37.9

7.7 9.6

8.2 6.1

0

10

20

30

40

Northeast Eagle Ford Mid-Con Permian Haynesville + CV

Bcf

/d

+14.7 Bcf/d

+3.2 Bcf/d

+0.3 Bcf/d +3.4

Bcf/d +1.1 Bcf/d

Northeast Accounts for

More Than 70% of N.A.

Growth

Natural Gas Forecasted Production by Region (2016–2021)

9 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

Source: Wood Mackenzie Note: Sub-plays with flat production growth were excluded from the chart

Key Marcellus/Utica Sub-plays Driving Northeast Growth Through 2021

NORTHEAST G&P

Wood Mackenzie Marcellus and Utica Production Outlook by Sub-play (2016–2021)

6.8

6.1

4.8

3.3 3.0 2.8

2.5

1.1 0.7 0.7

0.2 0

1

2

3

4

5

6

7

8

Bradford Area Lean Gas Core WV Rich Gas SusquehannaCore

Greene DryGas

Southwest RichGas

WV Dry Gas Rich Gas Core Southern WetGas

AlleghenyMountains

Condensate

Bcf

/d

2016 2017 2018 2019 2020 2021

Utica Marcellus

+2.5 Bcf/d

+4.2 Bcf/d

+3.2 Bcf/d

+1.5 Bcf/d

+0.2 Bcf/d +1.2

Bcf/d +1.9 Bcf/d

+0.3 Bcf/d +0.2

Bcf/d

-0.3 Bcf/d

-0.2 Bcf/d

Marcellus/Utica Sub-plays that Represent

+14.7 Bcf/d of Projected Growth by 2021

10 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

Source: Wood Mackenzie

Wood Mackenzie Marcellus Shale Sub-plays

NORTHEAST G&P

8

3

4

5

6

15

14

1. Susquehanna Core 2. Bradford Area 3. Northeast PA 4. Lycoming Area 5. Central PA 6. High Plateau 7. Allegheny Mountains 8. Pittsburgh Area 9. Greene Dry Gas 10. Southwest Rich Gas 11. Rich Gas Core 12. WV Dry Gas 13. WV Rich Gas 14. Big Sandy Field Area 15. Ohio 16. New York

Highlighted sub-plays are the key growth plays listed on Slide 9

16

1

9

2

7

10

11

12

13

11 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

Source: Wood Mackenzie

Wood Mackenzie Utica Shale Sub-plays

NORTHEAST G&P

9

4

3

2 11

10

7

5

1. Lean Gas Core 2. Lean Gas 3. Lean Gas Frontier 4. Tioga County 5. Northern Wet Gas 6. Southern Wet Gas 7. Condensate Core 8. Condensate 9. Condensate Frontier 10. Western Oil 11. Lean Gas SWPA

Highlighted sub-plays are the key growth plays listed on Slide 9

6 1

8

12 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

Source: Wood Mackenzie Marcellus Shale Sub-play Boundaries

Bradford/Susquehanna Supply Hubs Ideally Situated in the Core of NE Marcellus Dry Gas…

NORTHEAST G&P

BRADFORD SUPPLY HUB

SUSQUEHANNA SUPPLY HUB

PENNSYLVANIA

NEW YORK

1

2

3

WOOD MACKENZIE NE MARCELLUS SUB-PLAYS

Susquehanna Core 1

Bradford Area 2

Northeast PA 3

13 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

Source: Wood Mackenzie Marcellus Shale Sub-play Boundaries

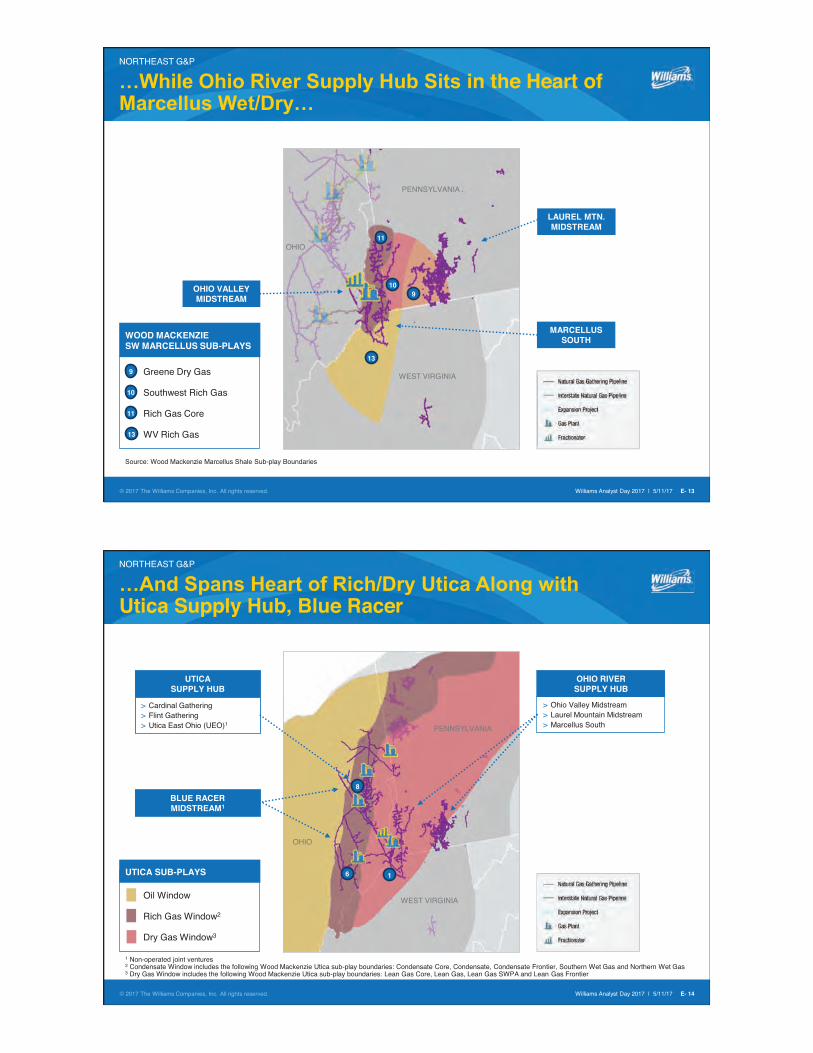

…While Ohio River Supply Hub Sits in the Heart of Marcellus Wet/Dry…

NORTHEAST G&P

LAUREL MTN. MIDSTREAM

OHIO VALLEY MIDSTREAM

MARCELLUS SOUTH WOOD MACKENZIE

SW MARCELLUS SUB-PLAYS

OHIO

PENNSYLVANIA

WEST VIRGINIA

9

Greene Dry Gas 9

10

Southwest Rich Gas 10

Rich Gas Core 11

WV Rich Gas 13

13

11

14 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

1 Non-operated joint ventures 2 Condensate Window includes the following Wood Mackenzie Utica sub-play boundaries: Condensate Core, Condensate, Condensate Frontier, Southern Wet Gas and Northern Wet Gas 3 Dry Gas Window includes the following Wood Mackenzie Utica sub-play boundaries: Lean Gas Core, Lean Gas, Lean Gas SWPA and Lean Gas Frontier

…And Spans Heart of Rich/Dry Utica Along with Utica Supply Hub, Blue Racer

NORTHEAST G&P

OHIO RIVER SUPPLY HUB

> Ohio Valley Midstream > Laurel Mountain Midstream > Marcellus South

OHIO

PENNSYLVANIA

WEST VIRGINIA

UTICA SUPPLY HUB

> Cardinal Gathering > Flint Gathering > Utica East Ohio (UEO)1

BLUE RACER MIDSTREAM1

1 6

8

UTICA SUB-PLAYS

Oil Window

Rich Gas Window2

Dry Gas Window3

15 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

Source: Wood Mackenzie Note: Sub-plays with flat production growth were excluded from the chart

Williams’ Unique NE Position: Exposed to 100 Percent of Projected Marcellus/Utica Growth

NORTHEAST G&P

6.8

6.1

4.8

3.3 3.0 2.8

2.5

1.1 0.7 0.7

0.2 0

1

2

3

4

5

6

7

8

Bradford Area Lean Gas Core WV Rich Gas SusquehannaCore

Greene DryGas

Southwest RichGas

WV Dry Gas Rich Gas Core Southern WetGas

AlleghenyMountains

Condensate

Bcf

/d

2016 2017 2018 2019 2020 2021Utica Marcellus

+2.5 Bcf/d

+4.2 Bcf/d

+3.2 Bcf/d

+1.5 Bcf/d

+0.2 Bcf/d +1.2

Bcf/d +1.9 Bcf/d

+0.3 Bcf/d +0.2

Bcf/d

-0.3 Bcf/d

-0.2 Bcf/d

Wood Mackenzie Marcellus and Utica Production Outlook by Sub-play (2016–2021)

Williams assets/dedications in sub-play

W W W W W W W W W W W

W

100% Assets/Dedications

Exposed to Sub-Plays Encompassing

Of Projected Marcellus/ Utica Growth through 2021

16 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

+15 23 � 38 +2

15 � 17

+5 37 � 42

+11 26 � 37

1 Size of bubble indicates magnitude of 2021 production or demand Source: Wood Mackenzie 2H 2016, excludes impact of net Canadian imports

Northeast Supplies Catalyst for Transco Expansions

NORTHEAST G&P

Tremendous Marcellus-Utica Resources Critical to Industry Growth, U.S. Economy

+2 12 � 14

+1 11 � 12

Regional Production change, 2016 to 2021 (Bcf/d)1

Regional Demand change, 2016 to 2021 (Bcf/d)1

17 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

Source: Wood Mackenzie 1 Note: Constitution, which is appealing the denial of a required permit, is not included in financial forecast.

New Takeaway Capacity Connects NE to Best Markets Across the Country…

NORTHEAST G&P

> Adair SW/ Lebanon Ex. (0.3 Bcf/d) > Leach Xpress: (1.5 Bcf/d) > Lebanon West- Ph. 2 (0.13 Bcf/d) > Mountaineer Express: (1.4 Bcf/d) > Nexus Pipeline: (1.3 Bcf/d) > Rex Zone 3 Cap. Enh. (0.8 Bcf/d) > Rover Pipeline: (3.25 Bcf/d) > Utica Access (0.21 Bcf/d)

> Atlantic Coast Pipeline: (1.5 Bcf/d) > Atlantic Sunrise (1.7 Bcf/d) > Dalton Expansion (0.4 Bcf/d) > Mountain Valley: (2.0 Bcf/d) > WB Xpress: (0.5 Bcf/d)

+2 15 � 17

+10 23 � 33

+2 12 � 14

+2 14 � 16

Regional Production change, 2016 to 2021 (Bcf/d)

Regional Demand change, 2016 to 2021 (Bcf/d)

> Access South (0.32 Bcf/d) > Gulf Markets Expansions (0.35 Bcf/d) > Broad Run Ex. (0.2 Bcf/d)

+15 23� 38

> Access Northeast (0.5 Bcf/d) > Atlantic Bridge (0.15 Bcf/d) > Constitution Pipeline (0.7 Bcf/d)1

> CPV Valley Lateral Project (0.13 Bcf/d) > Equitrans Expansion Project (0.6 Bcf/d) > Garden State Expansion (0.2 Bcf/d) > Leidy South (0.5 Bcf/d) > Millennium Eastern System Upgrade (0.2 Bcf/d) > New Market Project (0.1 Bcf/d) > New York Bay Expansion (0.1 Bcf/d) > Northeast Supply Enhancement (0.4 Bcf/d) > Northern Access 2016 (0.15 Bcf/d) > Orion Expansion Project (0.14 Bcf/d) > PennEast (1.1 Bcf/d) > South to North (0.3 Bcf/d) > Susquehanna West (0.15 Bcf/d) > Triad Expansion Project (0.18 Bcf/d) > WB Xpress (0.8 Bcf/d)

>>>>>>>>>>>>>>>>>>>>>>>>

Northeast Pipeline Projects (2016–2021) ~22 Bcf/d of Incremental Capacity

18 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

Source: EIA

…While Northeast Gas-Fired Power Generation Growth Will Drive Incremental Local Demand

NORTHEAST G&P

17,800 MW Announced Capacity Through 2021 Could Drive ~1–2 Bcf/d of Incremental Demand within Northeast

Planned gas-fired electric generation additions by electric utilities and independent power producers

19 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

Partially owned system volumes are shown at 100%. Note: Excludes volumes for all non-operated assets.

Substantial Growth Through ’14; 2015–16 Constrained by Market, Takeaway Capacity

NORTHEAST G&P

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2012 2013 2014 2015 2016 2017

Bcf

/d

Dry Gas Wet Gas

Gathering Volume Growth Through 1Q 2017 Average Gathered Volumes (Bcf/d)

20 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

1 Source for total Utica and Marcellus volume: Energy Information Administration, average daily production for 1Q 2017. 2 Partially owned gathering system volumes are shown at 100%.

Leading Gathering Position in Preeminent Gas Basin in North America

NORTHEAST G&P

34% Marcellus & Utica

Gathered Volumes2

Utica Supply Hub2

Blue Racer Midstream2

Bradford Supply Hub2

Susquehanna Supply Hub Ohio Valley Midstream

Marcellus South2

Laurel Mountain Midstream2

Non-Williams

Total Marcellus/Utica Average Gathered Volumes (Bcf/d) – 1Q 20171

21 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

2016 2021

* Includes 100% of consolidated assets and operated equity-method investments. Excludes non-operated equity-method investments.

Northeast Poised for Significant Value Creation

NORTHEAST G&P

Northeast Modified EBITDA/MCF Growing on Higher Volume

Target: 2016 ~37 cents 2021 ~50-55 cents

> Using Wood Mackenzie’s ‘16-’21 volume CAGR we could see 2021 Modified EBITDA around $2 billion

> Volume growth could require annual growth capital of ~$500MM

WILLIAMS 2016

ACTUAL

Gat

her

ed V

olu

mes

(M

Mcf

/d) 63%

53%

73%

Wood Mackenzie Marcellus/Utica growth rate of 63% applied to 2016 actuals:

> 4.0 Bcf/d of growth

> CAGR of 10.3%

22 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 E-

Northeast – Ideally Positioned in Preeminent Growth Basin in North America

NORTHEAST G&P

Foundational, Large-scale Assets in the Best Acreage

Demand vs. Takeaway Capacity:

Key Issue Being Addressed

Positioned for Even More Significant

Growth

WE MAKE ENERGY HAPPEN

NYSE: WMB

NYSE: WPZ

williams.com

Williams and Williams Partners Financial Outlook Don Chappel, Chief Financial Officer

2 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 F-

Williams and Williams Partners: Focused on Peer Leading Value Creation and Financial Discipline

WILLIAMS AND WILLIAMS PARTNERS FINANCIAL OUTLOOK

Growing Distributable Cash Flow per Unit /

Share and Sustaining Strong Cash Coverage

Focused on Projects within Our Competitively Advantaged Asset Base

Offering Attractive Financial Return

Retaining Cash Flow While Maintaining a

Strong Balance Sheet and Funding Growth with Low-Cost Debt

3 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 F-

Positioned for Long-Term, Sustainable Growth with Disciplined Capital Allocation and Financial Policies

WILLIAMS AND WILLIAMS PARTNERS FINANCIAL OUTLOOK

Compelling Market Fundamentals

> Clear line of sight to continued strong growth in natural gas demand driven by LNG exports, industrial, LDCs, power generation, Mexican exports and other

> Best supply basins respond to demand growth with relief of infrastructure constraints

Premier Assets

> Nation’s largest and fastest growing interstate gas pipeline system, Transco, with unrivaled proximity to growing Mid-Atlantic, Southeast and Gulf Coast demand centers

> Largest gas gatherer in fastest growing basins (Marcellus and Utica; currently almost 7 Bcf/d) > Steady, high-quality revenues from large-scale West operations and unique footprint and

capabilities in Atlantic Gulf’s Gulf of Mexico operations

Immaterial Direct Commodity Exposure

> Pro Forma for Geismar sale, 97% of WPZ’s gross margin expected from fee-based revenues in 2017

Focused on Lower-Risk, Competitively

Advantaged Projects with Attractive

Financial Returns

> 64% of 2017–2019 growth capex is projected to be spent on regulated growth projects backed by long-term contracts with low credit risk customers that will also drive volumes on G&P systems

> 27% of 2017–2019 growth capex is forecasted to be spent on Northeast G&P projects that will drive volume growth

Strong Financial Outlook

> WPZ expects to fund planned growth capex with retained cash flow, asset sale proceeds, and low-cost debt

> No new equity issuances required to fund WPZ planned growth capex for the next several years > Improved balance sheet and ample liquidity have strengthened the WPZ credit profile, solidifying

its investment grade credit rating > Streamlining the organization and aggressively managing costs > Attractive cash distribution/dividend growth and strong, sustainable coverage

4 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 F-

WPZ 2016 Proportionate Share of Total Revenues of Equity Investments Have Increased 178% (23% CAGR) Since 2011

Completing Transformation to Stable, Predictable Cash Flows

WILLIAMS AND WILLIAMS PARTNERS FINANCIAL OUTLOOK

WPZ Fee-based Revenues Increased ~$2.7 Billion, 2016 NGL Margins ~3% of Gross Margin

Note: Fee-based Revenue Presented Above Excludes Equity Method Investments Such as Gulfstream, Appalachian Midstream, Discovery, OPPL, UEOM, BRM/Caiman II, and LMM

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000 2014

> Access Acquisition > Gulfstar One > OVM De-ethanizer > OVM Processing &

Frac expansions > Ohio Valley Ethane

Pipeline

2015 > Buckinghorse Plant > Geismar Expansion > Mobile Bay South III > CPV Woodbridge > Leidy Southeast > VA Southside > Bayou Ethane 2013

> Mid-Atlantic Connector > Mid-South Expansion

Ph. II > NE Supply Link > Canadian Ethane

Recovery

2011 > Perdido Norte /

Markham Plant Expansion

> Gulfstream Ph. V > Station 85 North II > Mobile Bay South II

2012 > Cabot Gathering

Acquisition > Springville > Laser NE Gathering > OVM Acquisition > Boreal Pipeline > Mid-South Expansion Ph. I

2016 > NE Connector &

Rockaway > Rock Springs > Susquehanna

Supply Hub > Utica Supply Hub > Kodiak > Gunflint

NGL Margins Fee Revenues Olefins Margins

($ in millions)

5 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 F-

0

100

200

300

400

500

600

700

80001

/02…

02/0

2…03

/02…

04/0

2…05

/02…

06/0

2…07

/02…

08/0

2…

09/0

2…10

/02…

11/0

2…12

/02…

01/0

2…

02/0

2…03

/02…

04/0

2…05

/02…

06/0

2…07

/02…

08/0

2…

09/0

2…10

/02…

11/0

2…12

/02…

01/0

2…

02/0

2…03

/02…

$0.0

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

$1.4

Ind

ex Valu

e $ B

illio

ns

WPZ Adjusted EBITDA Alerian Energy Infrastructure Index (AMEI)(1)

This slide contains non-GAAP financial measures. A reconciliation of all non-GAAP financial measures used in this presentation to their nearest GAAP financial measures is included at the back of this presentation. 1 Price-return basis index.

WPZ Steady Predictable EBITDA Through Commodity and Financial Market Volatility

WILLIAMS AND WILLIAMS PARTNERS FINANCIAL OUTLOOK

2015: $4.1 Billion 2016: $4.4 Billion

2017

($ Billions) Q1 '15 Q2 '15 Q3 '15 Q4 '15 Q1 '16 Q2 '16 Q3 '16 Q4 '16 Q1 '17

Adjusted EBITDA $0.9 $1.0 $1.1 $1.1 $1.1 $1.1 $1.2 $1.1 $1.1

1

6 © 2017 The Williams Companies, Inc. All rights reserved. Williams Analyst Day 2017 | 5/11/17 F-