9 15am rodney lester

TRANSCRIPT

Insurance Development and Investment in Emerging Markets

Rodney Lester, World Bank Group Consultant

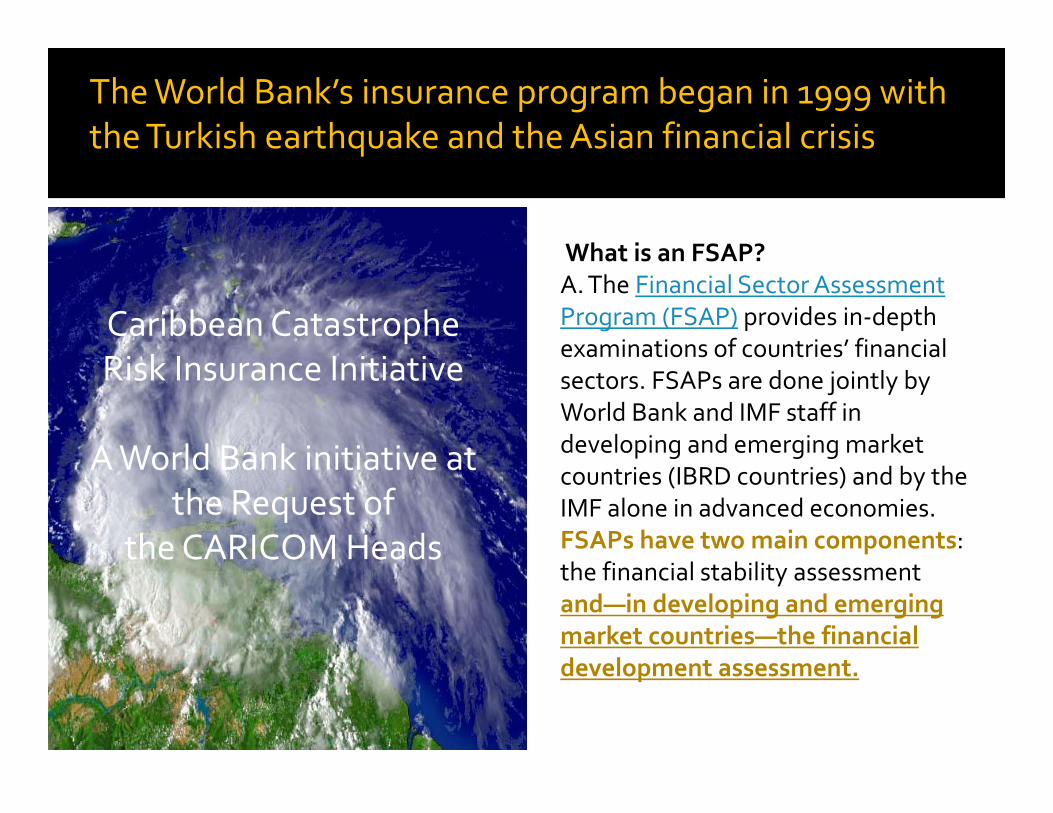

Caribbean Catastrophe Risk Insurance Initiative

A World Bank initiative at the Request of

the CARICOM Heads

What is an FSAP?A. The Financial Sector Assessment Program (FSAP) provides in‐depth examinations of countries’ financial sectors. FSAPs are done jointly by World Bank and IMF staff in developing and emerging market countries (IBRD countries) and by the IMF alone in advanced economies. FSAPs have two main components: the financial stability assessment and—in developing and emerging market countries—the financial development assessment.

The World Bank’s insurance program began in 1999 with the Turkish earthquake and the Asian financial crisis

EMs have provided most recent economic growth ‐ underemployed factors of production still exist in many EMs (esp. low cost labor).

Still growing middle classes in EMs – although very country specific –China versus Eq. Guinea.

Some EMs will need to face up to growing fiscal gaps –e.g. medical insurance in the ME.

New distribution strategies being pioneered in EMs as they leapfrog with communications tech. – cell ‘phones in Kenya.

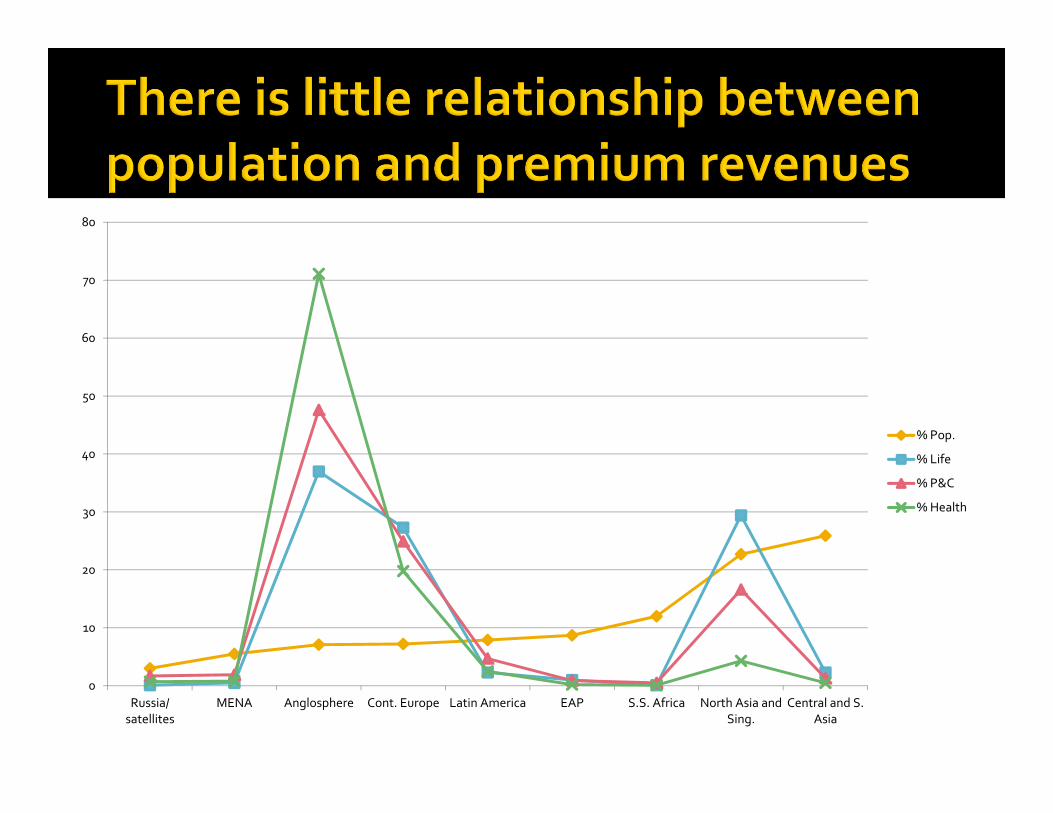

0

10

20

30

40

50

60

70

80

Russia/satellites

MENA Anglosphere Cont. Europe Latin America EAP S.S. Africa North Asia andSing.

Central and S.Asia

% Pop.

% Life

% P&C

% Health

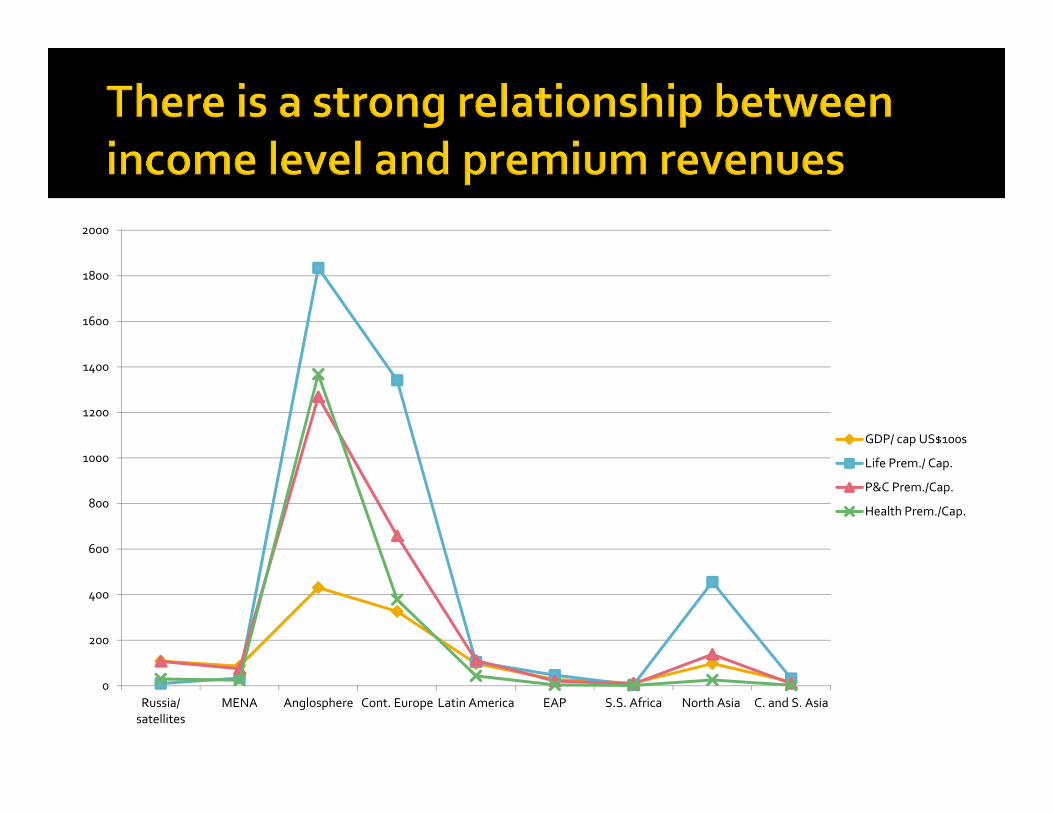

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Russia/satellites

MENA Anglosphere Cont. Europe Latin America EAP S.S. Africa North Asia C. and S. Asia

GDP/ cap US$100s

Life Prem./ Cap.

P&C Prem./Cap.

Health Prem./Cap.

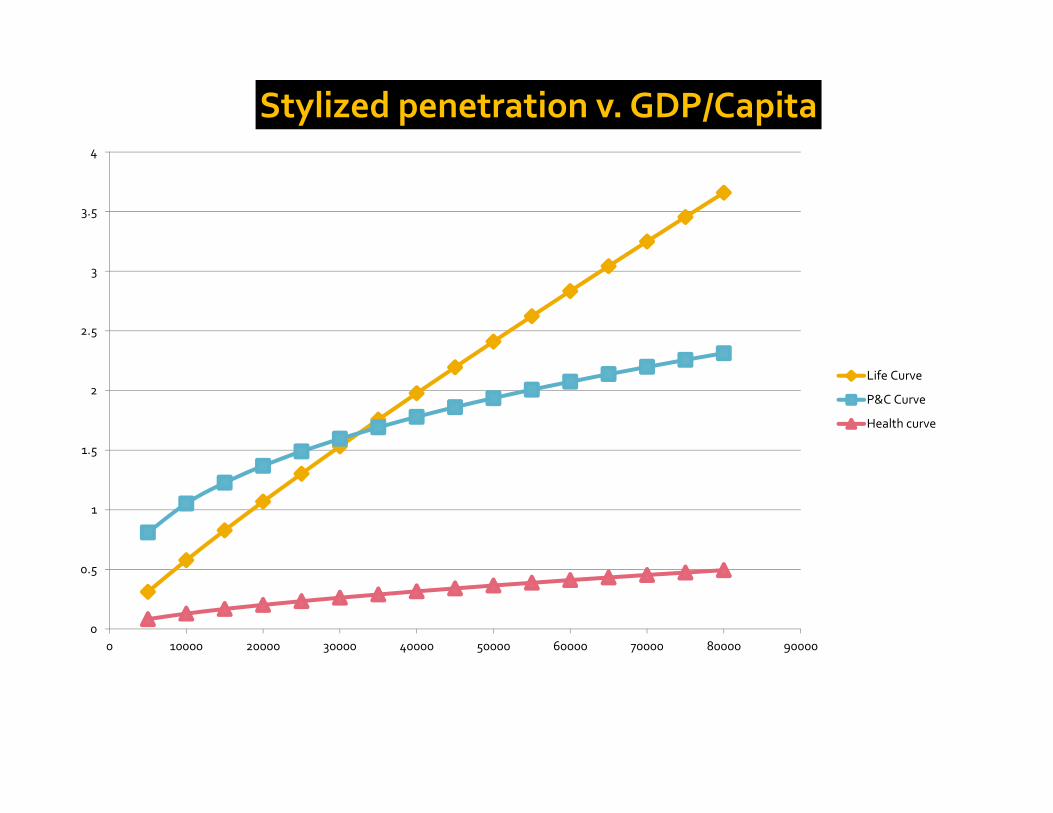

0

0.5

1

1.5

2

2.5

3

3.5

4

0 10000 20000 30000 40000 50000 60000 70000 80000 90000

Stylized penetration v. GDP/Capita

Life Curve

P&C Curve

Health curve

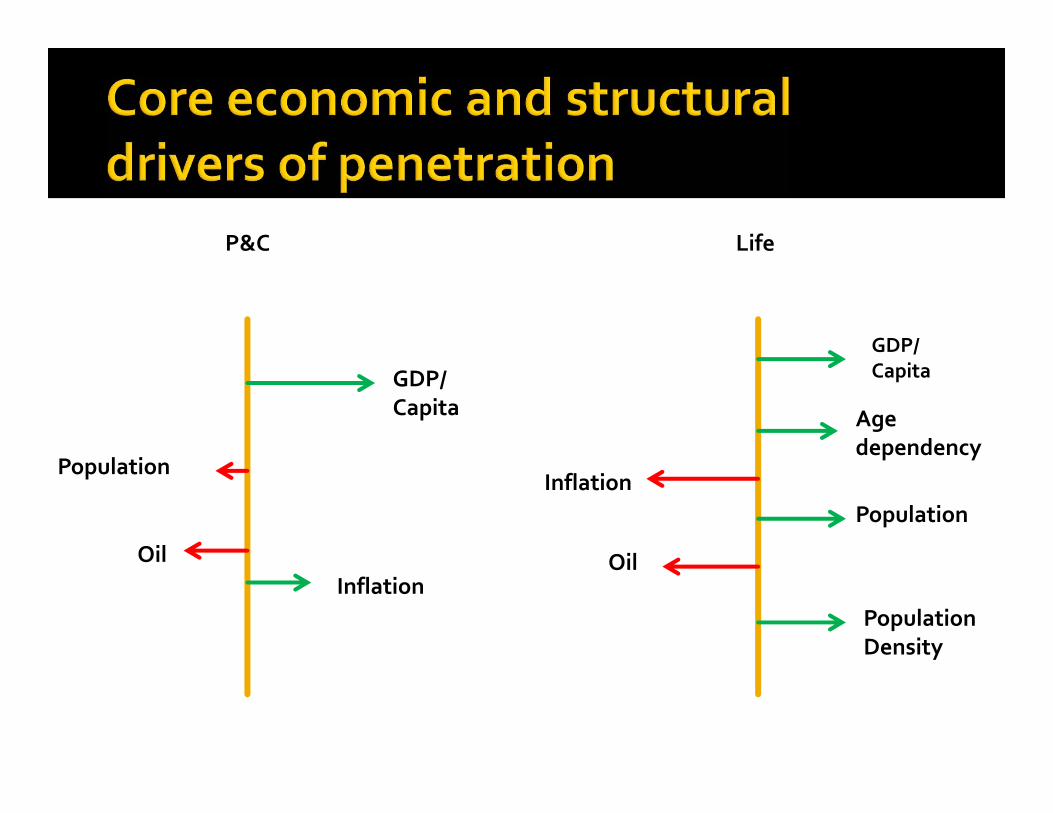

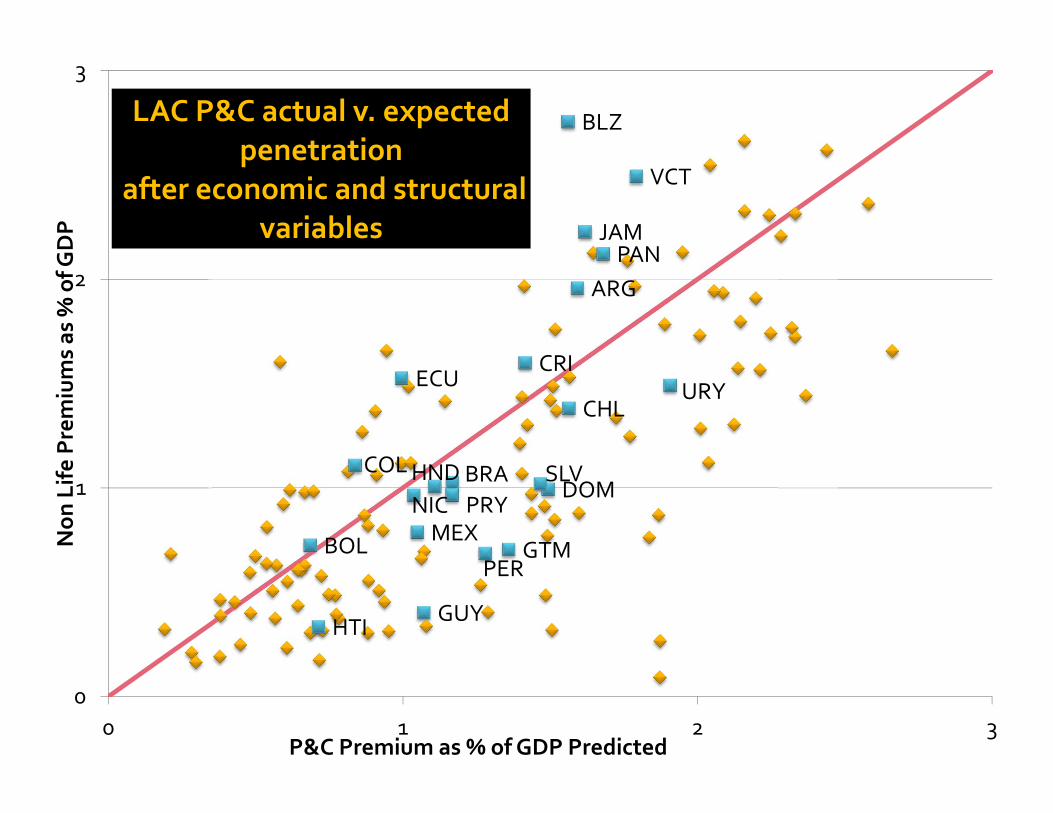

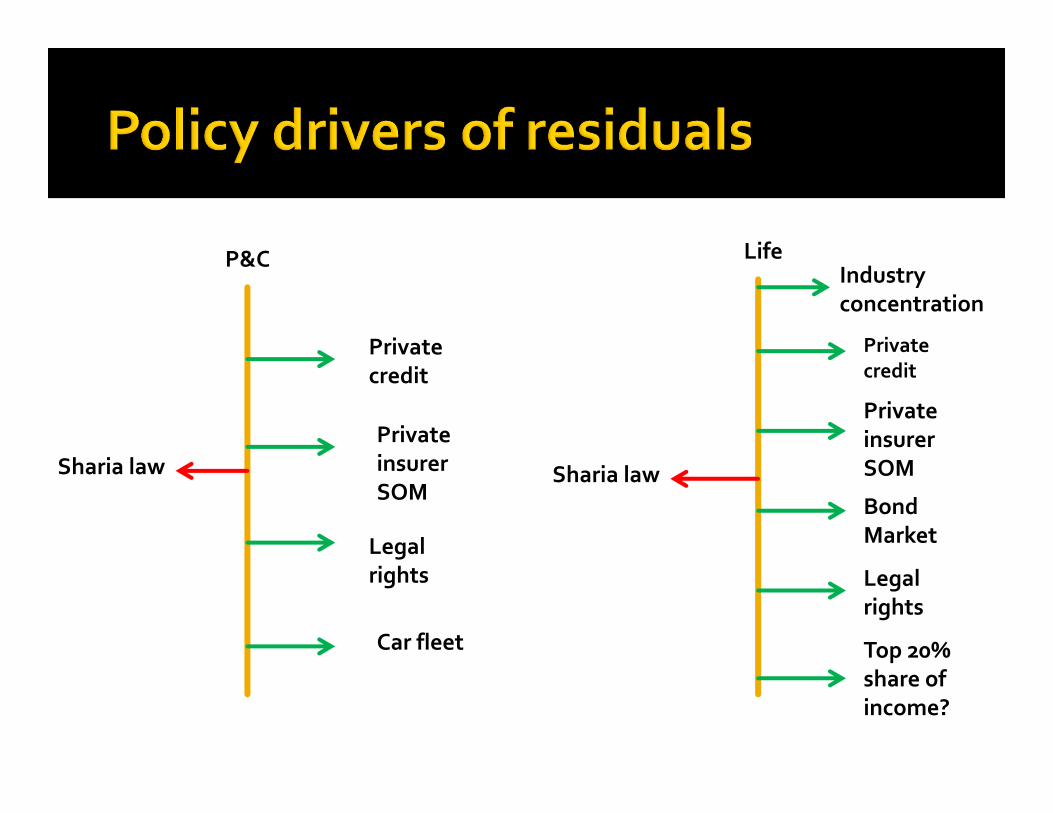

P&C Life

GDP/ Capita

Population

Population Density

Inflation

GDP/ Capita

Inflation

Population

OilOil

Age dependency

MEX

PANARG

BRA

CRI

VCT

DOMCOL

JAM

BLZ

PER

ECU

SLV

GTM

PRYHNDNIC

GUY

BOL

HTI

CHLURY

0

1

2

3

0 1 2 3

Non Life Premiums as % of G

DP

LAC P&C actual v. expected penetration

after economic and structural variables

P&C Premium as % of GDP Predicted

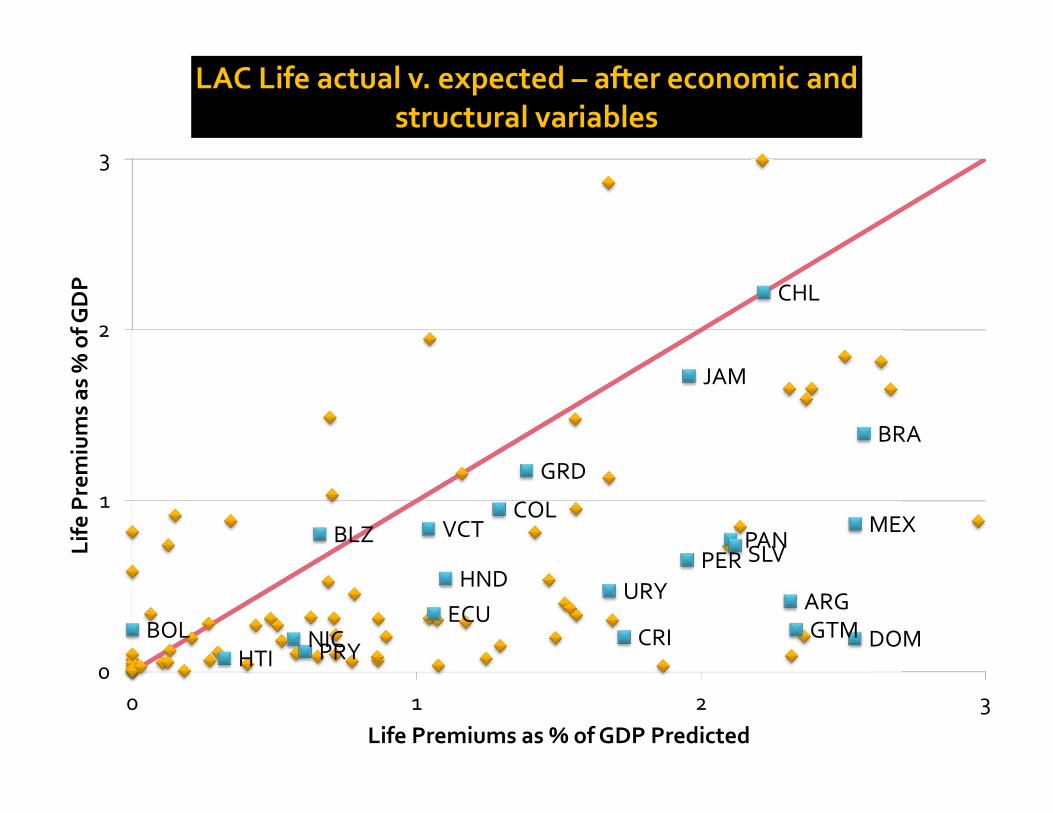

MEXPAN

ARG

GRD

BRA

CRI

VCT

DOM

COL

JAM

BLZPER

ECU

SLV

GTMPRY

HND

NICBOLHTI

CHL

URY

0

1

2

3

0 1 2 3

Life Premiums as % of G

DP

Life Premiums as % of GDP Predicted

LAC Life actual v. expected – after economic and structural variables

P&C Life

Private credit

Private insurer SOM

Top 20% share of income?

Sharia law

Private credit

Legal rights

Sharia lawPrivate insurer SOM

Car fleet

Bond Market

Legal rights

Industry concentration

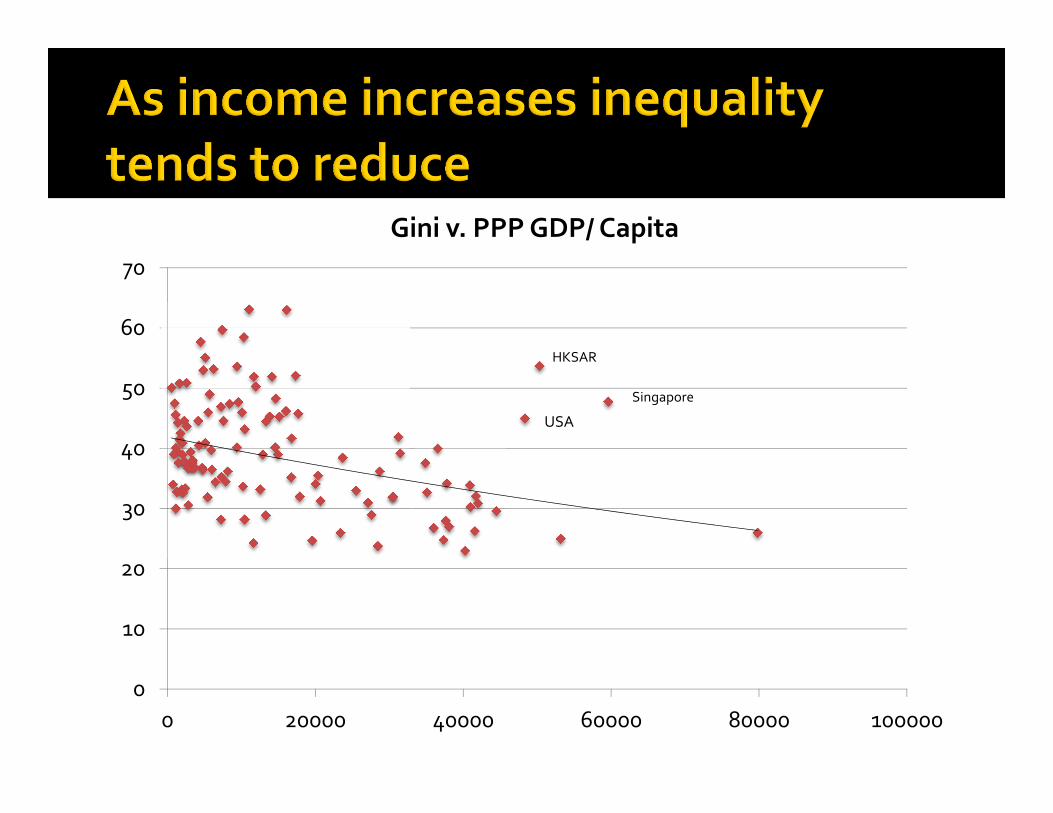

0

10

20

30

40

50

60

70

0 20000 40000 60000 80000 100000

Gini v. PPP GDP/ Capita

HKSAR

Singapore

USA

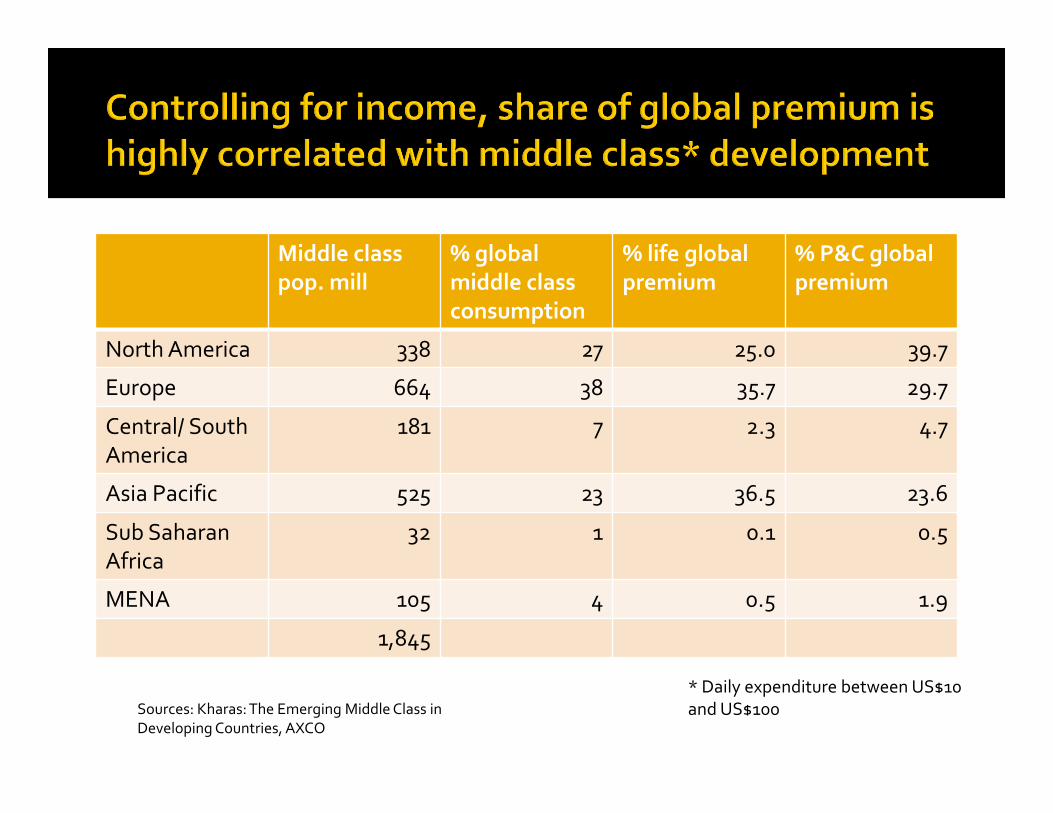

Middle class pop. mill

% global middle class consumption

% life global premium

% P&C global premium

North America 338 27 25.0 39.7

Europe 664 38 35.7 29.7

Central/ South America

181 7 2.3 4.7

Asia Pacific 525 23 36.5 23.6

Sub Saharan Africa

32 1 0.1 0.5

MENA 105 4 0.5 1.9

1,845

Sources: Kharas: The Emerging Middle Class in Developing Countries, AXCO

* Daily expenditure between US$10 and US$100

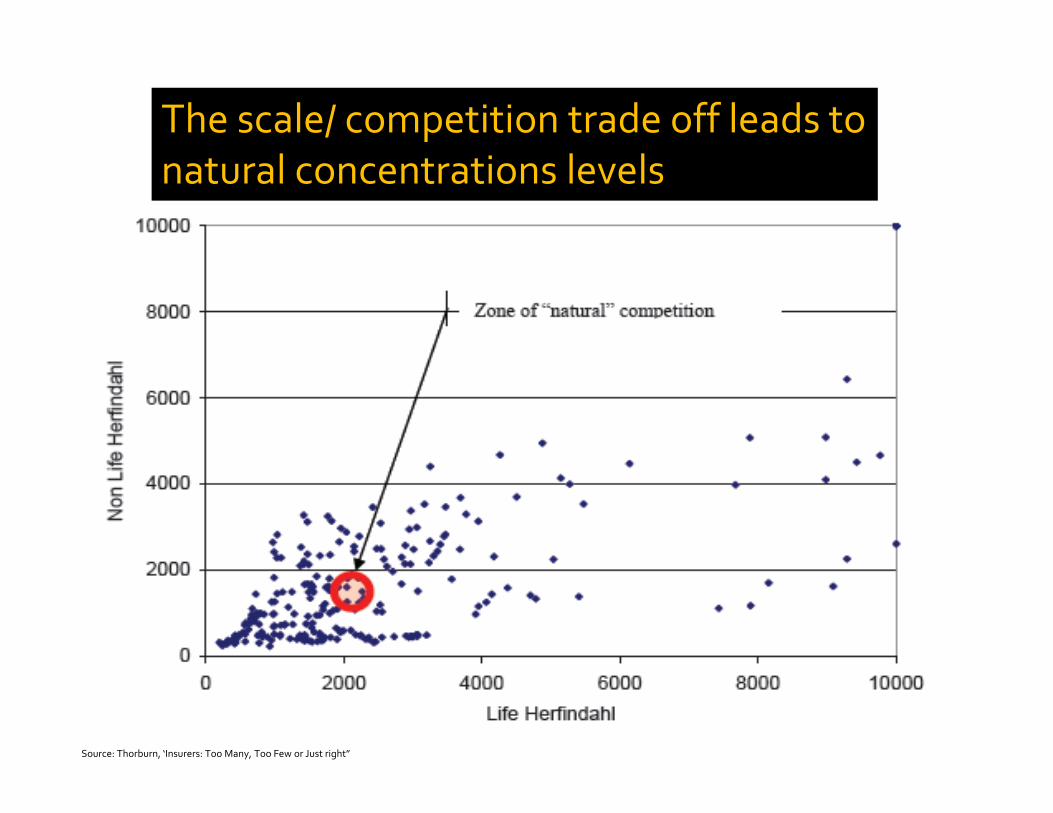

The scale/ competition trade off leads to natural concentrations levels

Source: Thorburn, ‘Insurers: Too Many, Too Few or Just right”

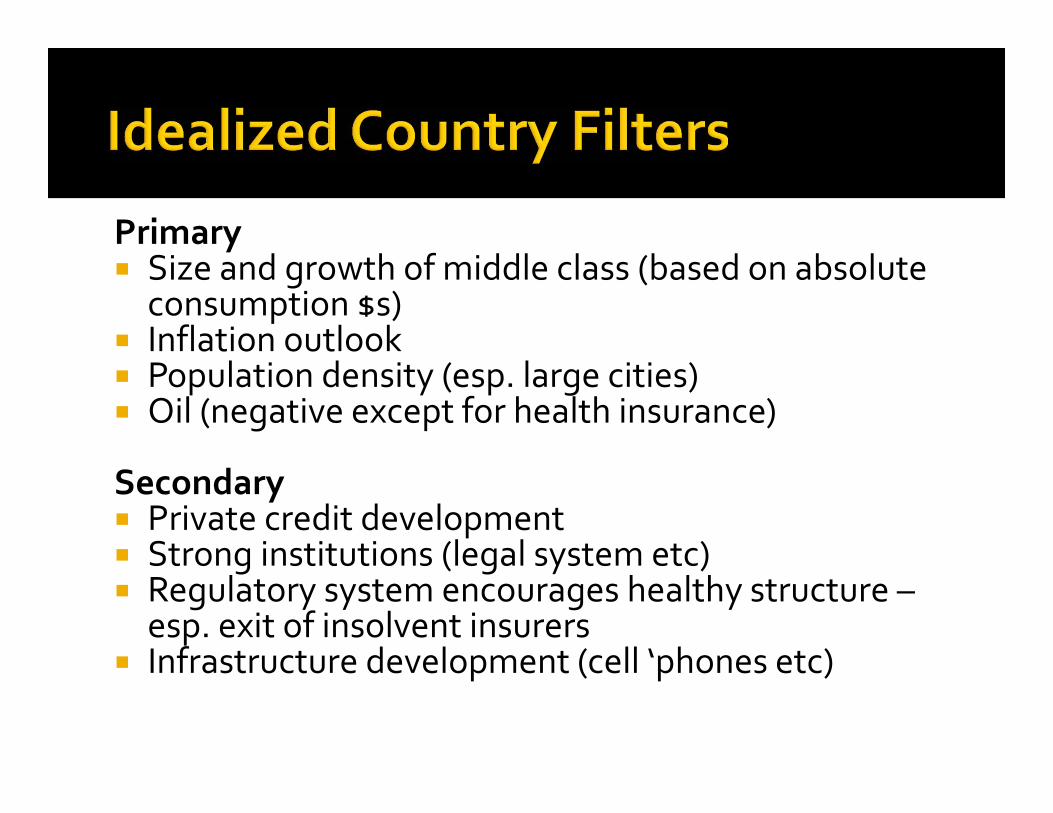

Primary Size and growth of middle class (based on absolute consumption $s)

Inflation outlook Population density (esp. large cities) Oil (negative except for health insurance)

Secondary Private credit development Strong institutions (legal system etc) Regulatory system encourages healthy structure –esp. exit of insolvent insurers

Infrastructure development (cell ‘phones etc)

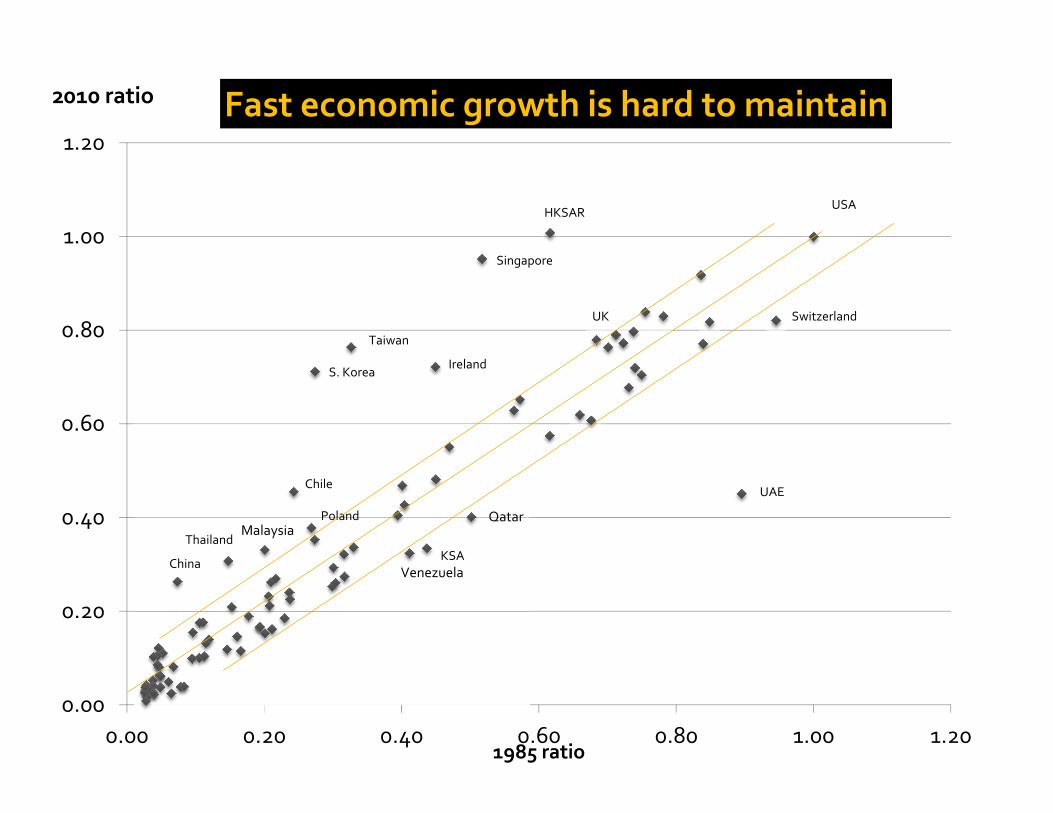

0.00

0.20

0.40

0.60

0.80

1.00

1.20

0.00 0.20 0.40 0.60 0.80 1.00 1.20

2010 ratio

1985 ratio

Fast economic growth is hard to maintain

HKSAR

UAE

MalaysiaQatar

VenezuelaChina

USA

Taiwan

S. Korea

Singapore

Chile

Ireland

Thailand

Switzerland

KSA

Poland

UK

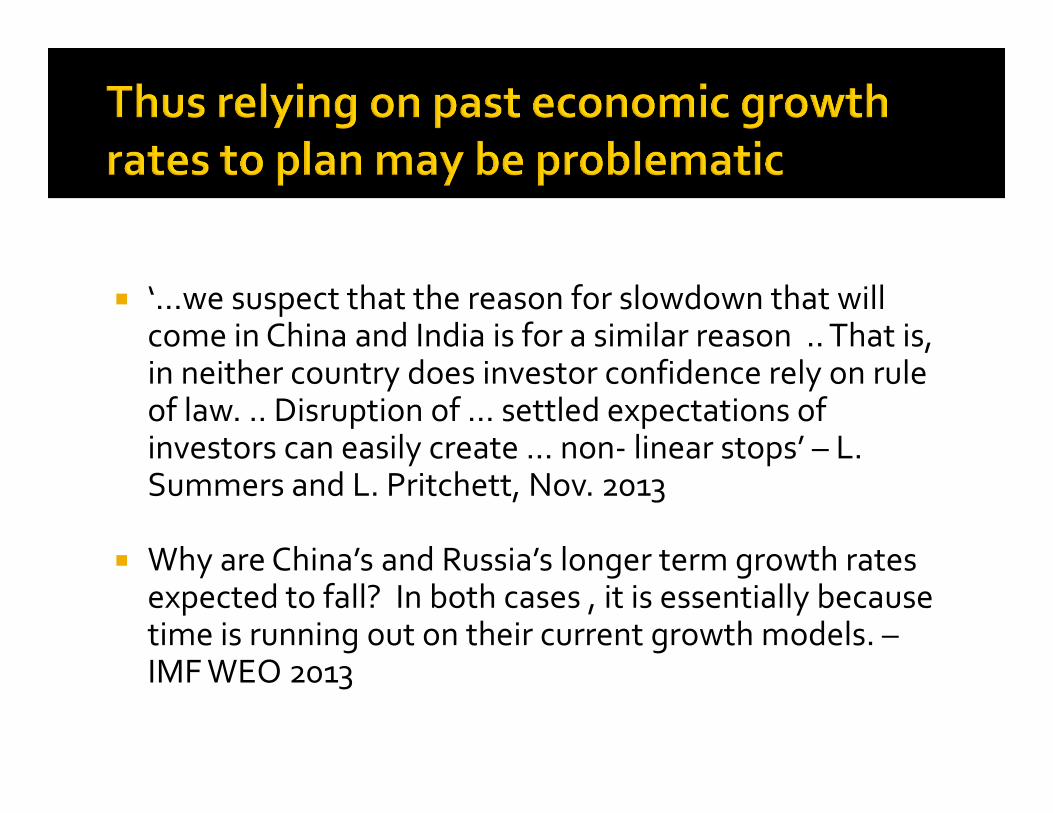

‘…we suspect that the reason for slowdown that will come in China and India is for a similar reason .. That is, in neither country does investor confidence rely on rule of law. .. Disruption of … settled expectations of investors can easily create … non‐ linear stops’ – L. Summers and L. Pritchett, Nov. 2013

Why are China’s and Russia’s longer term growth rates expected to fall? In both cases , it is essentially because time is running out on their current growth models. –IMF WEO 2013

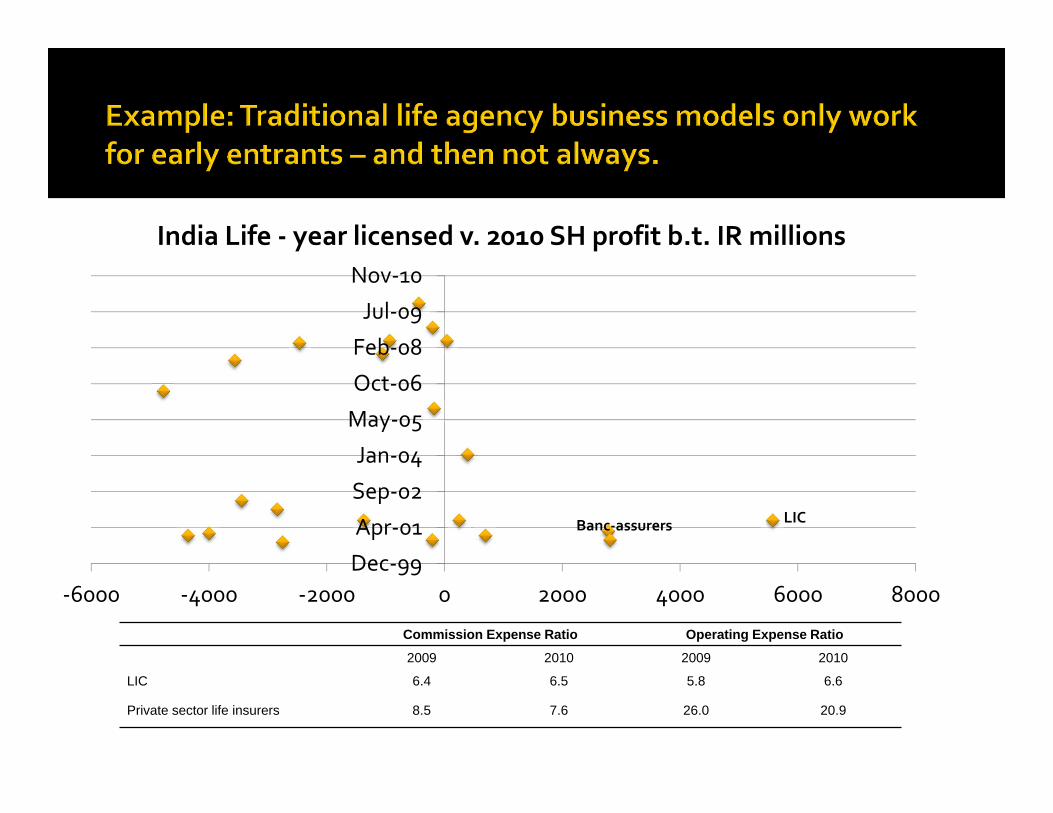

Commission Expense Ratio Operating Expense Ratio

2009 2010 2009 2010

LIC 6.4 6.5 5.8 6.6

Private sector life insurers 8.5 7.6 26.0 20.9

Dec‐99

Apr‐01

Sep‐02

Jan‐04

May‐05

Oct‐06

Feb‐08

Jul‐09

Nov‐10

‐6000 ‐4000 ‐2000 0 2000 4000 6000 8000

India Life ‐ year licensed v. 2010 SH profit b.t. IR millions

Banc‐assurers LIC