9 july 2011 workshop on service tax priyajit ghosh

TRANSCRIPT

9 July 2011

Workshop on Service tax Workshop on Service tax

Priyajit GhoshPriyajit Ghosh

22

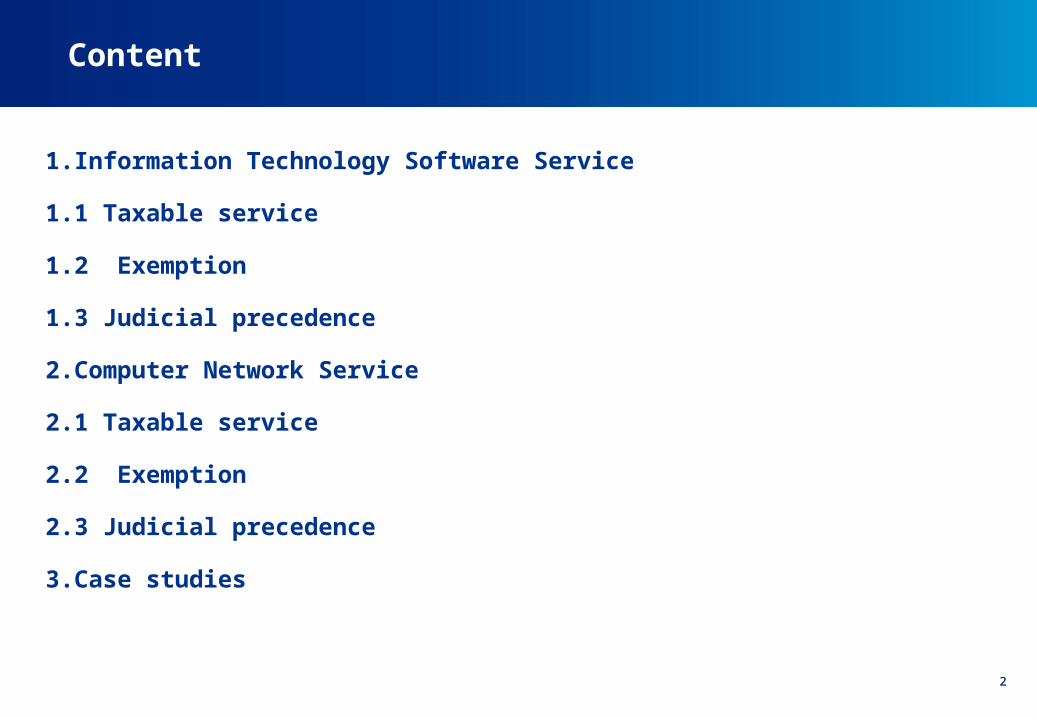

Content

1. Information Technology Software Service

1.1 Taxable service

1.2 Exemption

1.3 Judicial precedence

2. Computer Network Service

2.1 Taxable service

2.2 Exemption

2.3 Judicial precedence

3. Case studies

33

Information Technology Software Service

Date of taxability & definition

“Information technology software” defined as any representation of instructions, data, sound or image, including source code and object code, recorded in a machine readable form, and capable of being manipulated or providing interactivity to a user, by means of a computer or an automatic data processing machine or any other device or equipment

While introducing the Finance Bill, 2008, the Finance Minister in his Budget Speech stated:“I propose to increase the excise duty on packaged software from 8 per cent to 12 per cent to bring it on par with customised software which will attract a service tax of 12 per cent.”“I propose to bring under the service tax net customised software, to bring it on par with packaged software and other IT services”

Taxable service means any service liable to service tax if services provided or to be provided to any person, by any other person in relation to information technology software (for use in the course, or furtherance of business or commerce – Omitted 2010)

The taxable service made effective from 16 May 2008

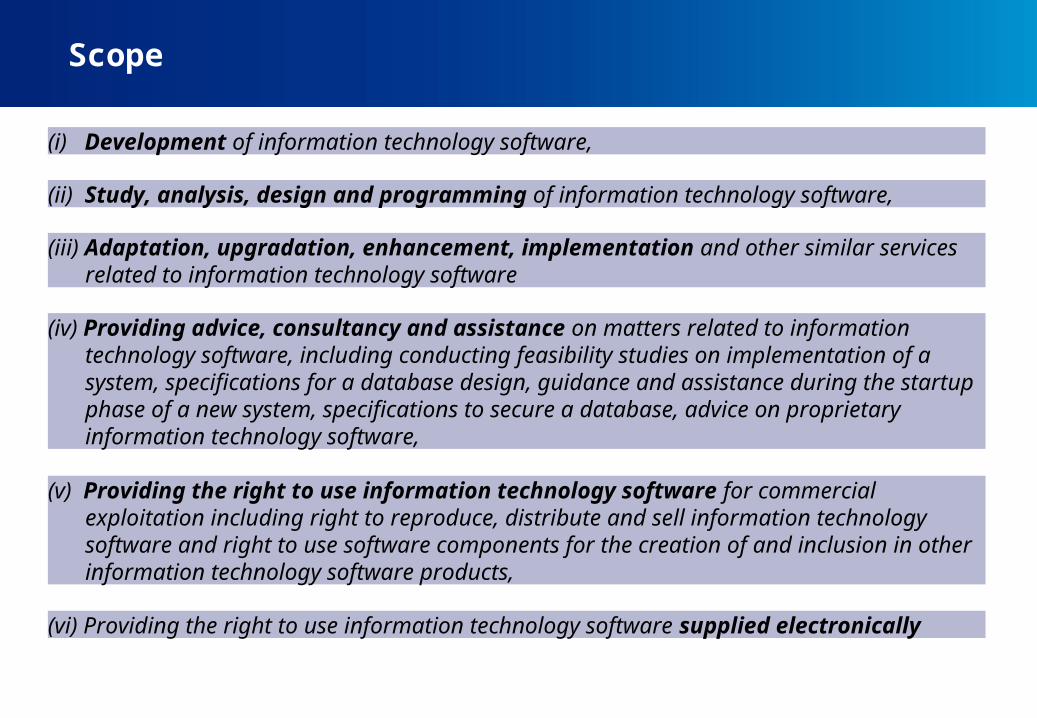

Scope

(i) Development of information technology software,

(ii) Study, analysis, design and programming of information technology software,

(iii) Adaptation, upgradation, enhancement, implementation and other similar services related to information technology software

(iv) Providing advice, consultancy and assistance on matters related to information technology software, including conducting feasibility studies on implementation of a system, specifications for a database design, guidance and assistance during the startup phase of a new system, specifications to secure a database, advice on proprietary information technology software,

(v) Providing the right to use information technology software for commercial exploitation including right to reproduce, distribute and sell information technology software and right to use software components for the creation of and inclusion in other information technology software products,

(vi) Providing the right to use information technology software supplied electronically

Current exemption

Particular Remarks

Notification No. 53/2010-ST dated 21 December 2010

Exemption Exemption from payment of service tax for packaged or canned software

Condition • Value of the packaged or canned software (procured domestically or imported) has been determined under section 4A of the Central Excise Act, 1994 (i.e. MRP based valuation);

• Appropriate duties of excise and customs (including CVD) paid

Export of service: Recipient is located outside India and payment is received in convertible foreign exchange

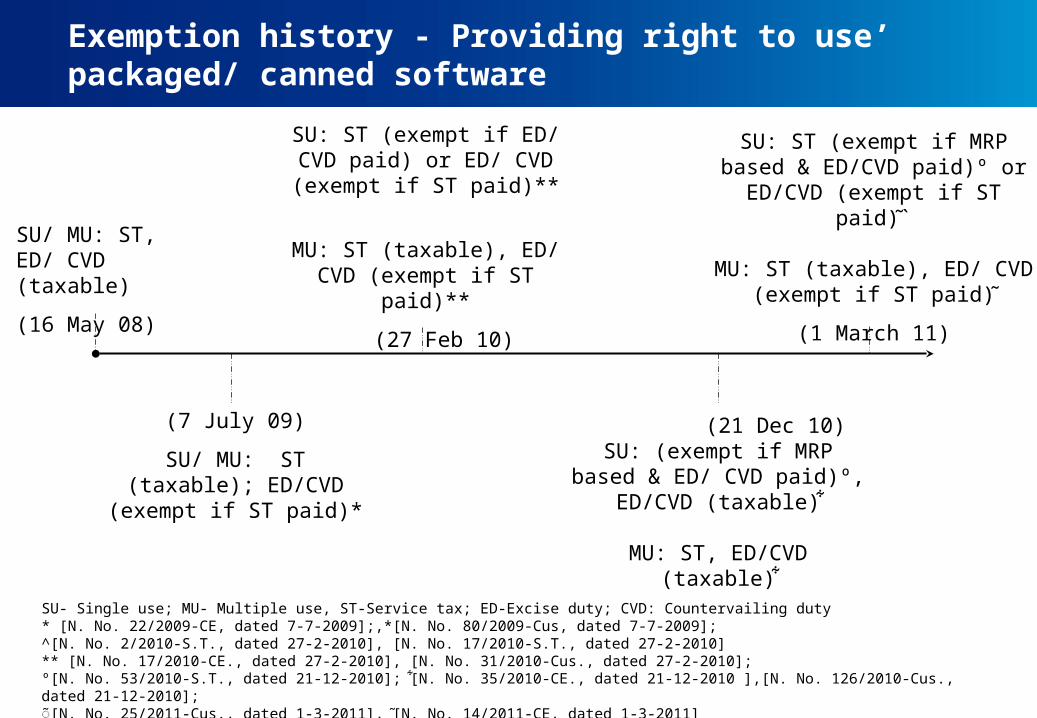

Exemption history - Providing right to use’ packaged/ canned software

SU/ MU: ST, ED/ CVD (taxable)

(16 May 08)

SU- Single use; MU- Multiple use, ST-Service tax; ED-Excise duty; CVD: Countervailing duty* [N. No. 22/2009-CE, dated 7-7-2009];,*[N. No. 80/2009-Cus, dated 7-7-2009];^[N. No. 2/2010-S.T., dated 27-2-2010], [N. No. 17/2010-S.T., dated 27-2-2010]** [N. No. 17/2010-CE., dated 27-2-2010], [N. No. 31/2010-Cus., dated 27-2-2010];º[N. No. 53/2010-S.T., dated 21-12-2010]; G[N. No. 35/2010-CE., dated 21-12-2010 ],[N. No. 126/2010-Cus., dated 21-12-2010];I͂ [N. No. 25/2011-Cus., dated 1-3-2011], I[N. No. 14/2011-CE, dated 1-3-2011]

(7 July 09)

SU/ MU: ST (taxable); ED/CVD (exempt if ST

paid)*

SU: ST (exempt if ED/ CVD paid) or ED/ CVD (exempt if

ST paid)**

MU: ST (taxable), ED/ CVD (exempt if ST paid)**

(27 Feb 10)

(21 Dec 10)SU: (exempt if MRP based &

ED/ CVD paid)º, ED/CVD (taxable)G

MU: ST, ED/CVD (taxable)G

SU: ST (exempt if MRP based & ED/CVD paid)º or ED/CVD

(exempt if ST paid)I`

MU: ST (taxable), ED/ CVD (exempt if ST paid)I

(1 March 11)

Key areas of dispute

Whether up-gradation, adaption, etc. of software is liable to tax under the category of MMR service or ITS service

Whether packaged/ canned software liable to VAT or service tax

Whether provision of manpower to provide IT enabled services liable to tax under MRSA service or ITS service

Infotech Software Dealers Association vs Union of India

Facts of the case• Petitioner is an association of software resellers • Master End User License Agreement entered between Microsoft Developer Network

Subscription Program (‘MSDN’) and member of Association (‘distributor’) under which˗ Ownership and rights over original software is retained by MSDN ˗ Limited rights of software distribution is provided to end user

• Writ Petition filed by an association to declare levy of service tax on ITS service as null and void, ultra vires and unconstitutional

Contention of the assessee• The Supreme Court in the case of Tata Consultancy Services Vs. State of Andhra

Pradesh held that software is goods, hence all transactions relating to software would amount to sale of goods

• Association never intended to provide service, transaction is always to sale of a software as goods. There is an absence of service element

• State Government can levy VAT where software qualify as goods

Contention of the revenue• There is no element of sale involved when standardized software is supplied to end user

by means of End User License Agreement

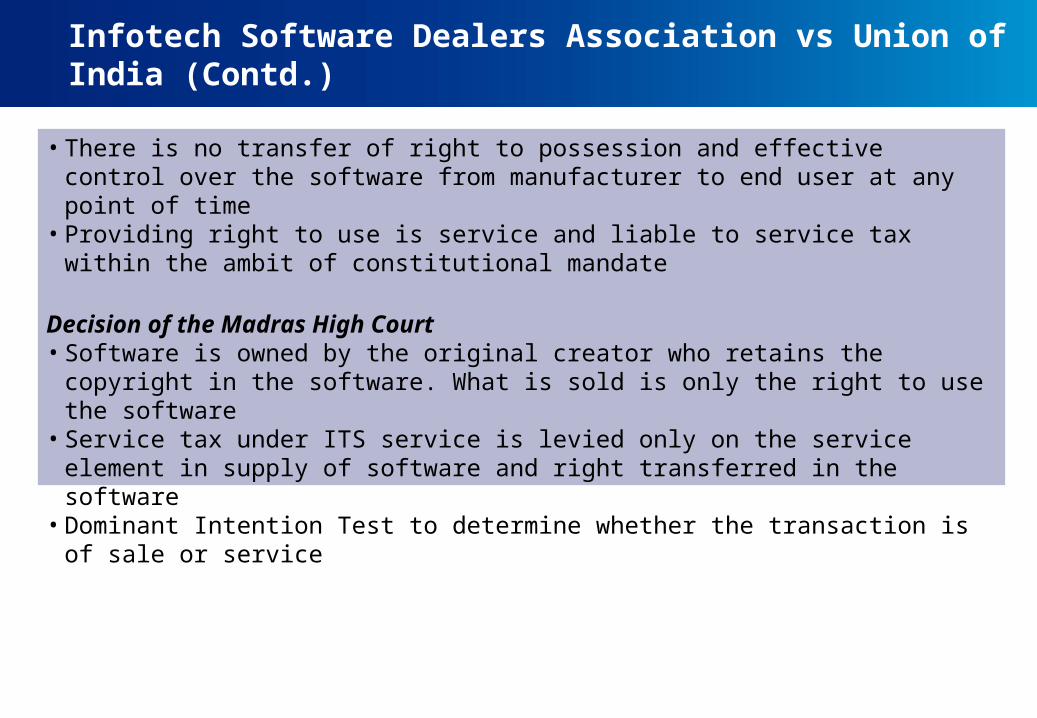

Infotech Software Dealers Association vs Union of India (Contd.)

• There is no transfer of right to possession and effective control over the software from manufacturer to end user at any point of time

• Providing right to use is service and liable to service tax within the ambit of constitutional mandate

Decision of the Madras High Court• Software is owned by the original creator who retains the copyright in the software.

What is sold is only the right to use the software• Service tax under ITS service is levied only on the service element in supply of software

and right transferred in the software• Dominant Intention Test to determine whether the transaction is of sale or service

Judicial precedence: ITS service vs MMR service

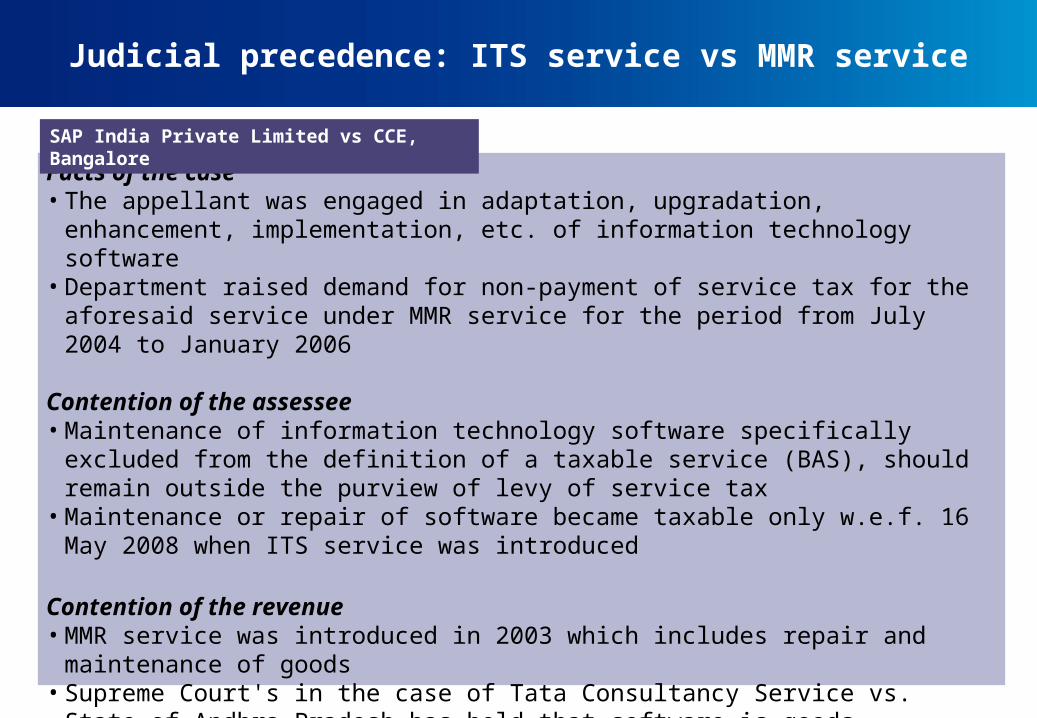

Facts of the case• The appellant was engaged in adaptation, upgradation, enhancement, implementation,

etc. of information technology software• Department raised demand for non-payment of service tax for the aforesaid service

under MMR service for the period from July 2004 to January 2006

Contention of the assessee• Maintenance of information technology software specifically excluded from the definition

of a taxable service (BAS), should remain outside the purview of levy of service tax• Maintenance or repair of software became taxable only w.e.f. 16 May 2008 when ITS

service was introduced

Contention of the revenue• MMR service was introduced in 2003 which includes repair and maintenance of goods• Supreme Court's in the case of Tata Consultancy Service vs. State of Andhra Pradesh

has held that software is goods• In view of circular no. 81/2/2005-S.T., dated 07 October 2005 maintenance or repair or

servicing of software is liable to service tax under MMR service

SAP India Private Limited vs CCE, Bangalore

Judicial precedence: ITS service vs MMR service (Contd..)

Decision of the CESTAT• The services rendered by the appellant i.e. up gradation, enhancement, implementation

are expressly covered under the definition of ITS service which was made taxable w.e.f. 16 May 2008 only

• Such service is not to be subjected to levy of service tax under any other service• It is settled law that a new taxable service covered by specific entry under will not attract

levy of service tax under any pre-existing entry in view of Karnataka High Court's judgment in Commissioner Vs. Turbotech Precision Engineering Pvt. Ltd

Cognizant Tech. Solutions (I) Pvt. Ltd. vs Comm. (LTU), Chennai

Facts of the case• Appellant entered into a contract with its customer to provide certain biometric services • In terms of contract, appellant will provide adequate staff to provide services to its

customer, and customer will support appellant to recruit and train the staff for its work• Department raised demand for aforesaid service under manpower recruitment service

Contention of the assessee• Services provided is in the nature of ITS service which at the material time was

excluded from levy of Service tax• The recruited employees works under management of appellants and from premises of

appellants and it cannot be said that manpower has been supplied to its customer

Contention of the revenue• Services would be liable to service tax under manpower recruitment service as the

appellants have recruited entire staff only on the basis of requirement of its customer

Decision of the CESTAT• The manpower so recruited is deployed under the responsibility of the appellants and

are paid for by the appellants

Cognizant Tech. Solutions (I) Pvt. Ltd. vs Comm.(LTU) Chennai (Contd..)

• Nature of services required to be provided by the appellants are in the nature of information technology services as the same relates to data management

• Therefore, appellants are not liable to pay Service tax in respect of the services provided by them to customer under manpower recruitment service

1515

Computer Network Service

Date of taxability & definition

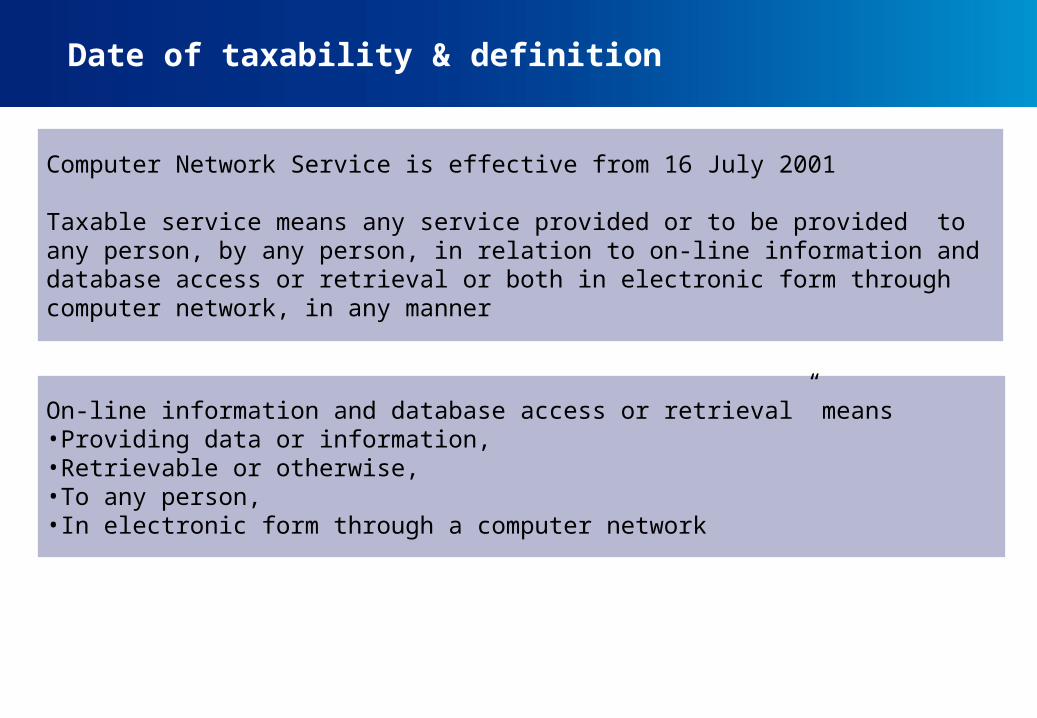

On-line information and database access or retrieval” means •Providing data or information, •Retrievable or otherwise, •To any person, •In electronic form through a computer network

Computer Network Service is effective from 16 July 2001

Taxable service means any service provided or to be provided to any person, by any person, in relation to on-line information and database access or retrieval or both in electronic form through computer network, in any manner

Scope – TRU Circular

TRU Circular (circular no. B-II/I/2000-TRU, dated 9 July 2001)

• Generally two categories of service providers are involved in providing online information and data access or retrieval services. These are

˗ Internet Service Providers such as VSNL, MTNL, Dishnet etc.˗ Website Operators such as Taxindiaonline.com, CIIonline.com etc.

• Following Services are specifically excluded from the scope :˗ Inter connectivity services provided by one ISP to another ISP˗ E-Commerce transactions˗ Service provided by cyber-café services˗ Newsletter publishing companies

Exemption

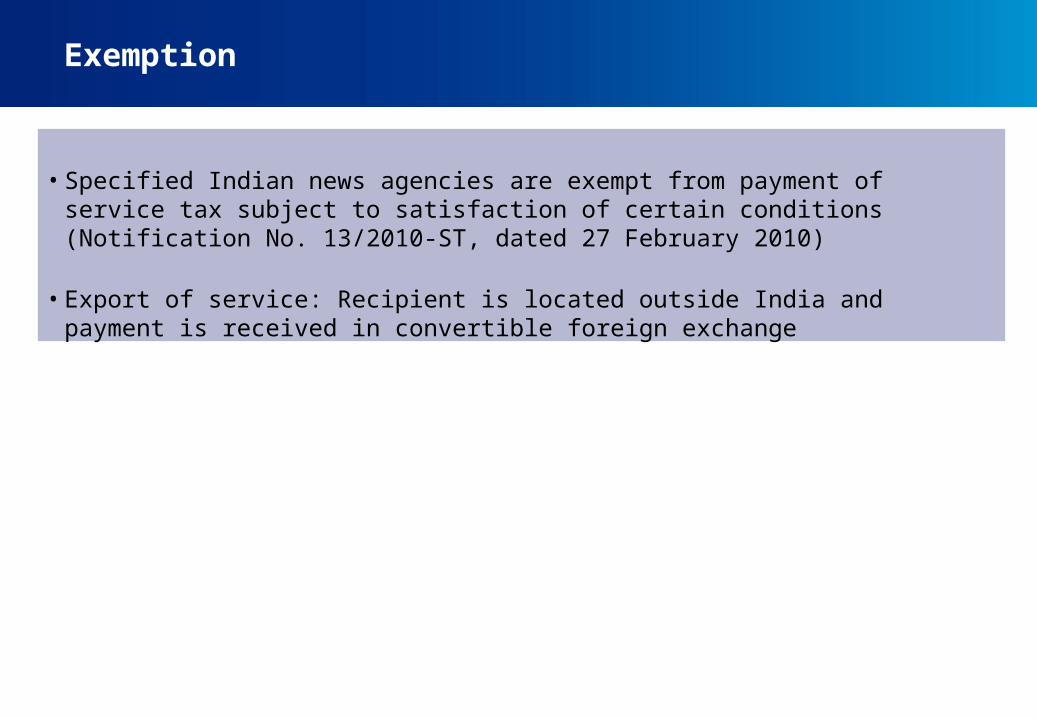

• Specified Indian news agencies are exempt from payment of service tax subject to satisfaction of certain conditions (Notification No. 13/2010-ST, dated 27 February 2010)

• Export of service: Recipient is located outside India and payment is received in convertible foreign exchange

Bharat Matrimony Com. Pvt. Ltd. vs CST, Chennai

Facts of the case• Appellant are engaged in business of providing matrimonial service from portals/

websites• Appellant gives access to its customers of on-line information and database (which

includes profile and pictures of other customers) and charges fees for such access• Department raised demand for the aforesaid services under ‘online information and

database access or retrieval’ service

Decision of the tribunal• Services provided by the appellant to its customers would come within the scope of

taxable service under category of ‘online information and database access or retrieval’ service

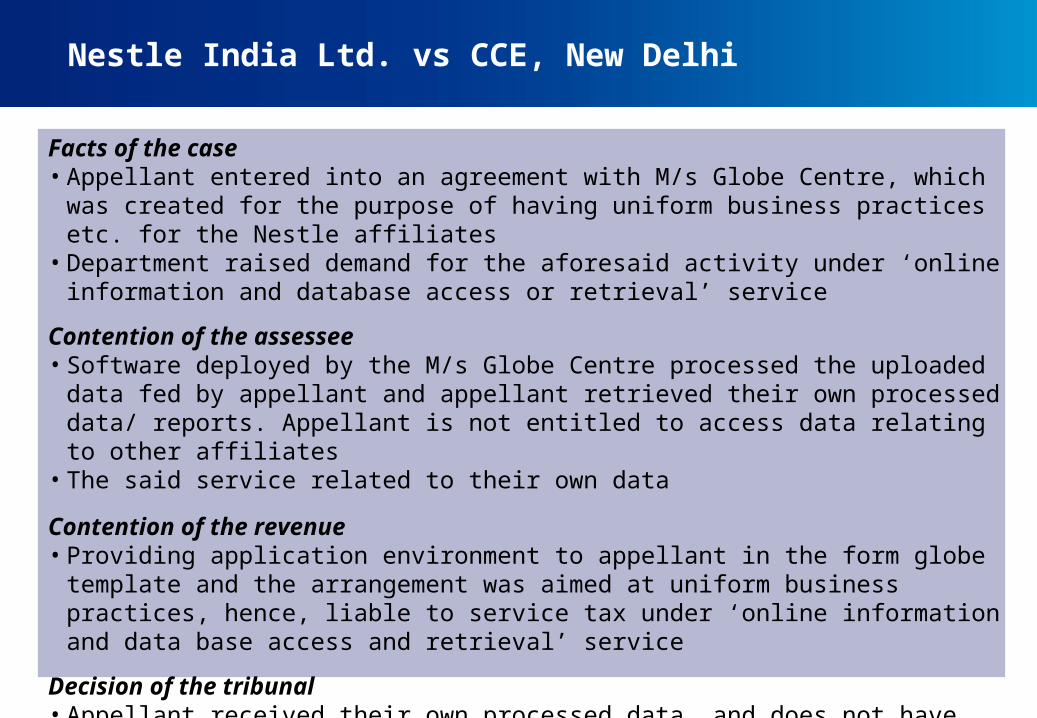

Nestle India Ltd. vs CCE, New Delhi

Facts of the case• Appellant entered into an agreement with M/s Globe Centre, which was created for the

purpose of having uniform business practices etc. for the Nestle affiliates • Department raised demand for the aforesaid activity under ‘online information and

database access or retrieval’ service

Contention of the assessee• Software deployed by the M/s Globe Centre processed the uploaded data fed by

appellant and appellant retrieved their own processed data/ reports. Appellant is not entitled to access data relating to other affiliates

• The said service related to their own data

Contention of the revenue• Providing application environment to appellant in the form globe template and the

arrangement was aimed at uniform business practices, hence, liable to service tax under ‘online information and data base access and retrieval’ service

Decision of the tribunal• Appellant received their own processed data, and does not have access of other

affiliates data, hence not liable to service tax

Dewsoft Overseas Pvt. Ltd. vs CST, New Delhi

Facts of the case• Appellants provide Computer education via “online” through an interactive website• Department raised demand for the aforesaid activities under ‘online information and

data base access and retrieval’ service

Contention of the assessee• The service being provided by the appellant is e-learning-online education through an

interactive website which is nothing but commercial training or coaching through electronic media which includes conducting online tests and issuing certificates

Contention of the revenue• Interactive process involved in importing online education is covered under the category

of ‘online information and database access or retrieved services’

Decision of the tribunal• Online coaching or teaching, includes providing library access to the students, is an

interactive process and the same cannot be compared with mere “online information and database access or retrieval” and covered under commercial training or coaching

2222

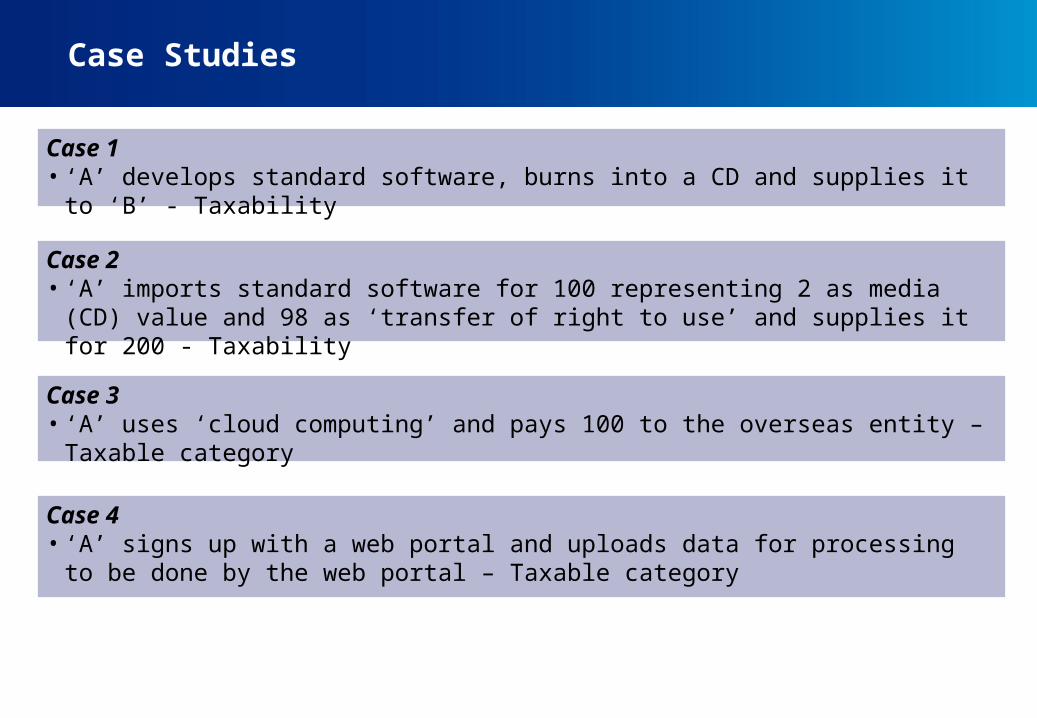

Case Studies

Case Studies

Case 1• ‘A’ develops standard software, burns into a CD and supplies it to ‘B’ - Taxability

Case 2• ‘A’ imports standard software for 100 representing 2 as media (CD) value and 98 as

‘transfer of right to use’ and supplies it for 200 - Taxability

Case 3• ‘A’ uses ‘cloud computing’ and pays 100 to the overseas entity – Taxable category

Case 4• ‘A’ signs up with a web portal and uploads data for processing to be done by the web

portal – Taxable category

THANK YOU

Presenter: Priyajit Ghosh

Mail: [email protected]

The views in this presentation are personal views of the Presenter. Further, the information contained is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although, the endeavor is to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such / this information without appropriate professional advice which is possible only after a thorough examination of facts / particular situation.