9/8/2015 erldc: posoco 1 renewable energy g chakraborty dgm(mo), erldc renewable energy g...

TRANSCRIPT

04/19/23 ERLDC: POSOCO 1

Renewable Energy

G ChakrabortyDGM(MO), ERLDC

Renewable Energy

G ChakrabortyDGM(MO), ERLDC

04/19/23 ERLDC: POSOCO 2

Contents

• Indian Power Sector – At Present

- Factors compel us to worry• Drivers for alternative Energy Source

– Legal provision– Emerging Renewable Scenario– International Position– Wind and Solar potential in India

• Need for REC Mechanism• Integration of Renewables • Implementation of RRF• Future Scenario

Region wise Installed Generating Capacity

Captive generating capacity as on 31st March 2011 = 34,445 MW

Source: CEA website

NPTI, Bangalore

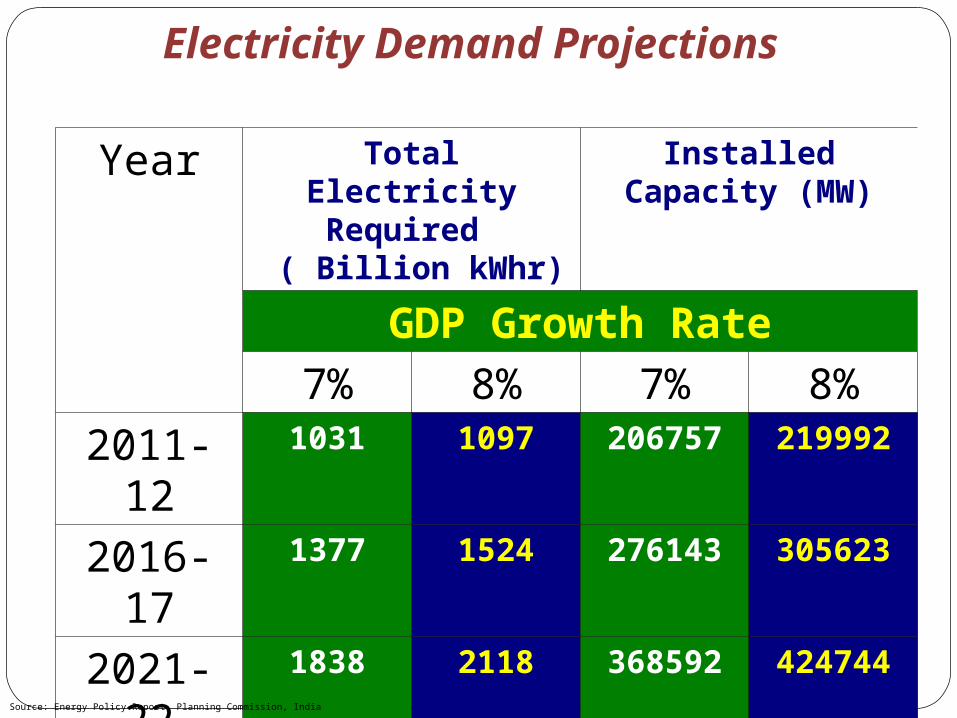

Electricity Demand Projections

Year Total Electricity Required ( Billion kWhr)

Installed Capacity (MW)

GDP Growth Rate

7% 8% 7% 8%2011-12 1031 1097 206757 219992

2016-17 1377 1524 276143 305623

2021-22 1838 2118 368592 424744

2026-27 2397 2866 480694 574748

2031-32 3127 3880 627088 778095

Source: Energy Policy Report, Planning Commission, India

India’s Oil Balance

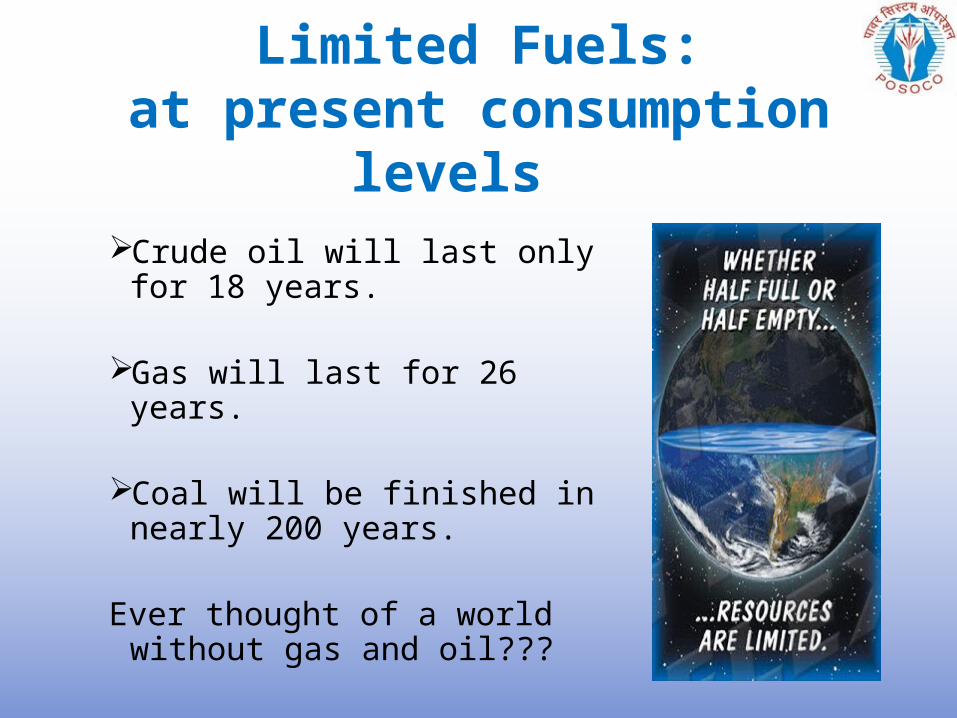

Limited Fuels:at present consumption levels

Crude oil will last only for 18 years.

Gas will last for 26 years.

Coal will be finished in nearly 200 years.

Ever thought of a world without gas and oil???

Factors which compel us to worry

C l i m a t e h a s c h a n g e d a n d c o n t i n u e s t o c h a n g e . .

– G l o b a l m e a n t e m p e r a t u r e h a s i n c r e a s e d 0 . 5 - 1 o F

– G l o b a l s e a l e v e l h a s r i s e n 4 - 1 0 i n c h e s – G l o b a l p r e c i p i t a t i o n o v e r l a n d h a s

i n c r e a s e d 1 %

– P r o j e c t e d t e m p e r a t u r e i n c r e a s e o f 3 . 6 o F b y 2 1 0 0 ( 1 . 8 - 6 . 3 o F )

– P r o j e c t e d s e a l e v e l r i s e o f 2 0 i n c h e s b y 2 1 0 0 ( 6 - 3 8 i n c h e s )

– L i k e l y i n c r e a s e i n p r e c i p i t a t i o n i n t e n s i t y

0.75 0.760.86

1.83

0.65

3.24

0.21

1.08

CO

2 RELEA

SE,

GIG

A T

ON

S

OECD

USA

CHINA

INDIA

Ref : World Energy Council Report, 1994

1990 2050

GLOBAL CARBON DI-OXIDE EMISSION

Potential Impacts

Climate Impacts in South Asia

AFG BLD BHU IND PAK NEP MAL

Sea Level Rise - Very High

- Modest Low - Very High

Glacier

Melt

High High High High High High --

Temp Increase Very High

High Very High

High High Very High Modest

Flooding

Worsens

? Very

High

Likely High High High High (SLR)

Drought

More Frequent

? High some areas

? High Very High

? Possible --

Drivers for Alternate energy sources

Oil crisis in 1970s. Limited natural Resources (Oil, Coal). Energy Security. International mandate for development of CDM technologies and to

reduce Carbon/Sulpher/Green House Gas emissions, phase out fossil fuel generation and develop alternate Energy sources. IPCC(Inter-governmental Panel for Climate Change) under

UNEP(1998) UNFCCC Rio De Janeiro 1992 Kyoto protocol 1997 Copenhagen Summit 2009

Indian initiatives NAPCC (National Action Plan for Climate Change) JNNSM (Jawaharlal Nehru National Solar Mission)

HYDRO RESOURCES

COAL BELT

MUMBAI

DELHI

CHENNAIBANGALORE

KOLKATA

RESOURCES ARE FAR AWAY FROM LOAD CENTERS.

NECESSITATES LONG TRANSMISSION LINKS FOR EVACUATION

SOURCES OF RESOURCES

HIGH POWER CORRIDOR AT 765 KV

WIND ZONES

GAS RESOURCES

The Ex-President’s Message: Independence

Cut down energy losses Utilize technologies to

provide a diverse supply of environmentally friendly energy

“We must achieve Energy Independence by 2030”, including a cut down in ALL sectors

Increase the power generated through renewable energy sources from 5% to 25%

This is the nation’s “first and highest priority”

Ex-President A.P.J. Abdul Kalam

(Rocket Scientist)

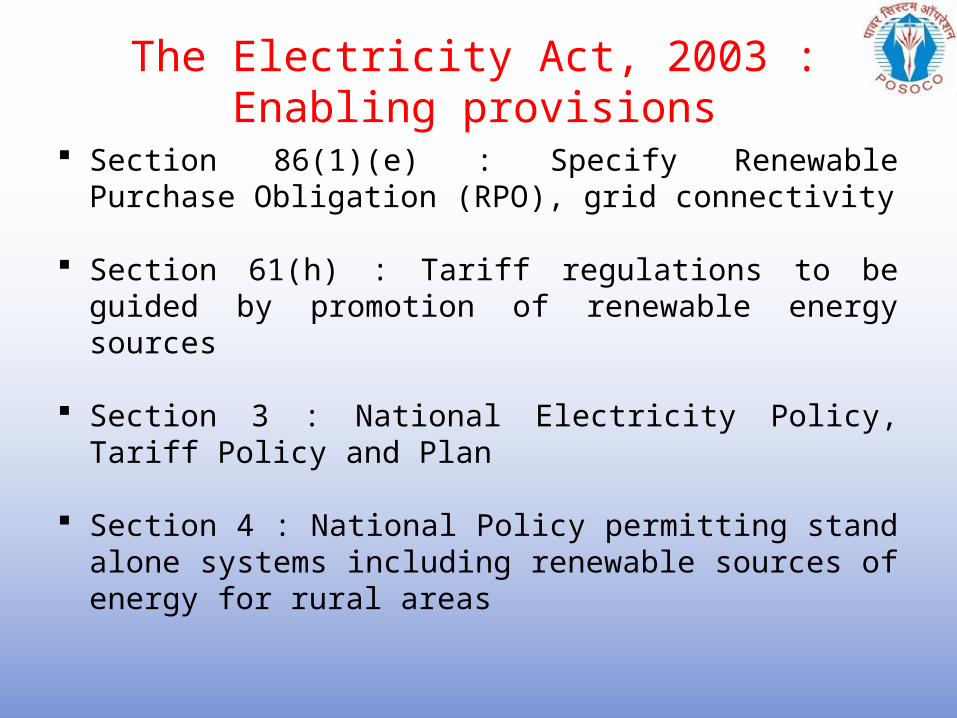

The Electricity Act, 2003 : Enabling provisions

Section 86(1)(e) : Specify Renewable Purchase Obligation (RPO), grid connectivity

Section 61(h) : Tariff regulations to be guided by promotion of renewable energy sources

Section 3 : National Electricity Policy, Tariff Policy and Plan

Section 4 : National Policy permitting stand alone

systems including renewable sources of energy for rural areas

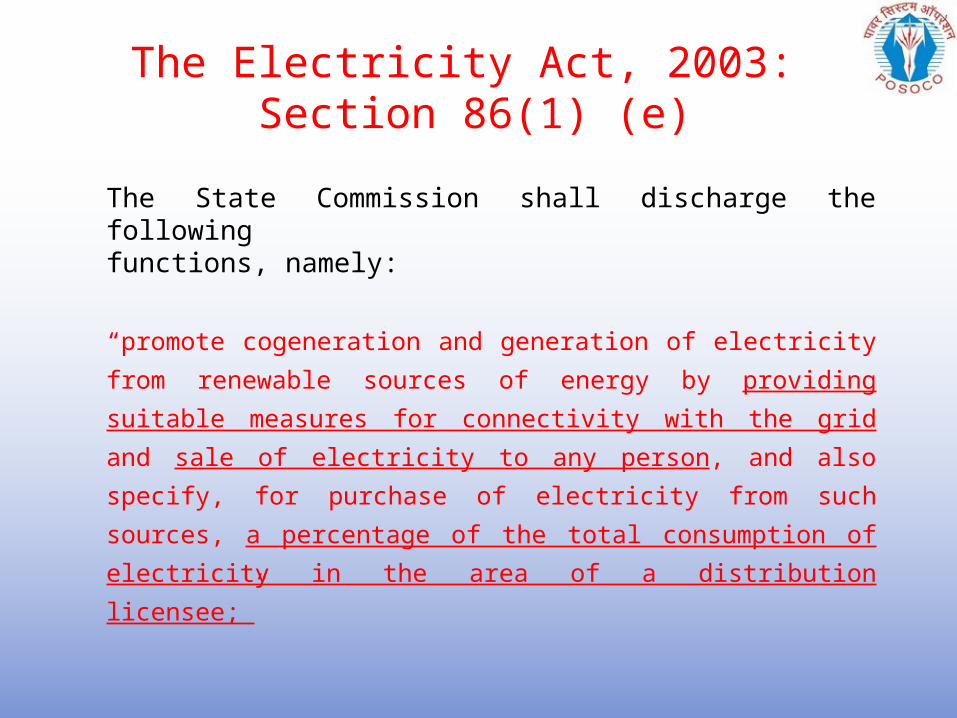

The Electricity Act, 2003: Section 86(1) (e)

The State Commission shall discharge the following functions, namely:

“promote cogeneration and generation of electricity from

renewable sources of energy by providing suitable measures

for connectivity with the grid and sale of electricity to any

person, and also specify, for purchase of electricity from such

sources, a percentage of the total consumption of electricity

in the area of a distribution licensee;”

The Electricity Act, 2003: Section 61(h)

The Appropriate Commission shall subject to the provisions of this Act, specify the terms and conditions for the determination of tariff, and in doing so, shall be guided by the following, namely:

(h) the promotion of co-generation and generation of electricity from renewable sources of energy

National Electricity Policy: 2005• Urgent need for promotion of non-conventional and

renewable sources of energy.

• Efforts need to be made to reduce the capital cost of such projects.

• Adequate promotional measures would have to be taken for development of technologies and sustained growth of these sources.

• SERCs to provide suitable measures for connectivity with grid and fix percentage of purchase from Renewable sources.

• Progressively such share of electricity need to be increased.

Tariff Policy:2006• Appropriate Commission shall fix RPO and

SERCs shall fix tariff.

• In future Discoms to procure Renewable Energy through competitive bidding within suppliers offering same type of RE.

• In long-term, RE technologies need to compete with all other sources in terms of full costs.

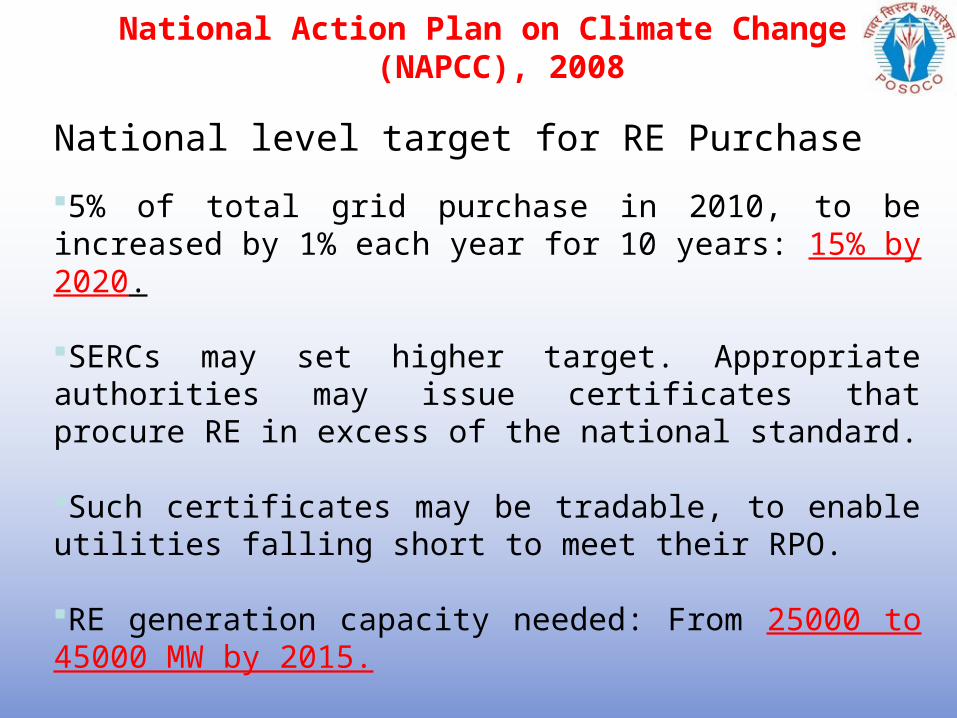

National Action Plan on Climate Change (NAPCC), 2008

National level target for RE Purchase

5% of total grid purchase in 2010, to be increased by 1% each year for 10 years: 15% by 2020.

SERCs may set higher target. Appropriate authorities may issue certificates that procure RE in excess of the national standard.

Such certificates may be tradable, to enable utilities falling short to meet their RPO.

RE generation capacity needed: From 25000 to 45000 MW by 2015.

National Solar Mission, 2009

Mission aims to achieve grid tariff parity by 2022 through Bundling of solar

power with un-allocated quota of central stations by NVVNL for resale to utilities

To deploy 20 million solar lighting systems for rural areas by 2022

Large scale utilization R&D, Local manufacturing In addition,100 MW capacity distributed

small grid connected power plants during Phase - 1.

MW

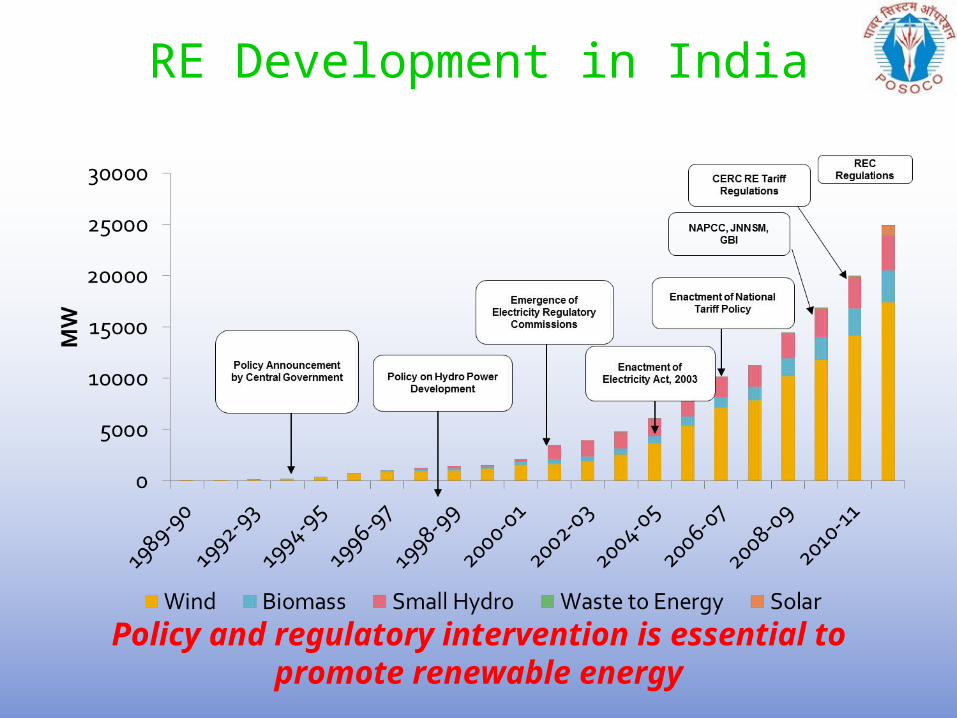

RE Development in India

Policy and regulatory intervention is essential to promote renewable energy

Various types of Renewable Energy• Wind

– On shore– Off shore

• Solar– Solar PV (Photo Voltaic, Concentrated PhotoVoltaic)– Solar Thermal (Solar Concentrated, Parabolic trough/dish, Fresnel

collector, Heliostat & Solar Tower receiver, Solar updraft receiver) • Small Hydel (upto 25 MW)• Biomass

– Bagasse (the dry fibrous waste that is left after sugarcane has been processed)

– rice husk, cotton stalk, mustard stalk, groundnut shell, coconut fronds, waste cotton stalks, roots of trees, cane trash, poultry litter etc.)

• Co - generation• Municipal Solid waste• Geo -Thermal• Hydro kinetics

– Tidal power – Wave technology

Wind MapWind MapSolar MapSolar MapBoth Solar and wind Both Solar and wind concentration are concentration are geographically samegeographically same

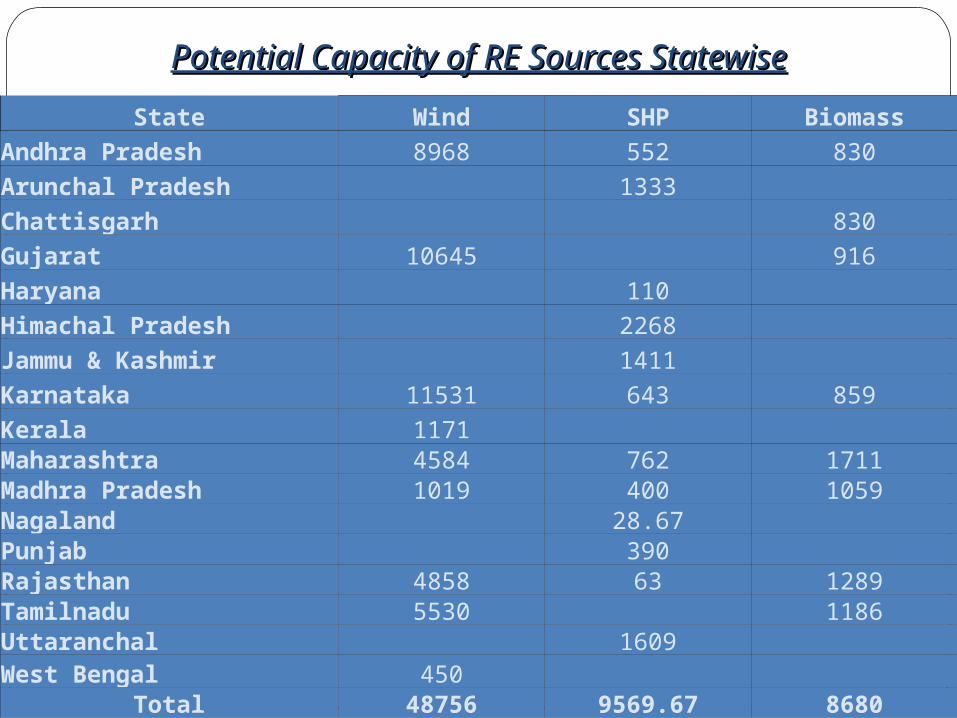

Potential Capacity of RE Sources StatewisePotential Capacity of RE Sources Statewise

State Wind SHP BiomassAndhra Pradesh 8968 552 830Arunchal Pradesh 1333 Chattisgarh 830Gujarat 10645 916Haryana 110 Himachal Pradesh 2268 Jammu & Kashmir 1411 Karnataka 11531 643 859Kerala 1171 Maharashtra 4584 762 1711Madhra Pradesh 1019 400 1059Nagaland 28.67 Punjab 390 Rajasthan 4858 63 1289Tamilnadu 5530 1186Uttaranchal 1609 West Bengal 450

Total 48756 9569.67 8680

Renewable Energy sources (RES)Renewable Energy Installed

CapacityPotential

Wind Power 16179.00 48561

Small Hydro Power 3300.13 14292

Biomass Power 1142.60 8680

Bagasse Cogeneration

1952.53 5000

Waste to Power 73.66 7000

Solar Power (SPV) 481.48 200000

Total 23129.40 283533

Capacities in MW as on31.01.12

Source: MNRE

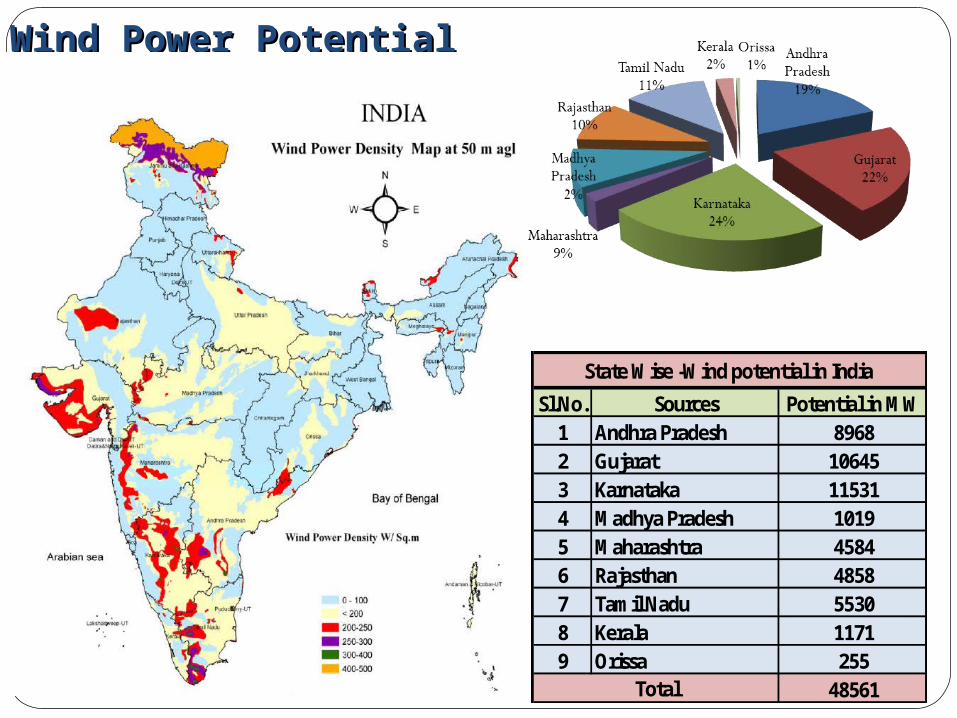

Wind Power Potential Wind Power Potential

Sl.No. Sources Potential in MW1 Andhra Pradesh 89682 Gujarat 106453 Karnataka 115314 Madhya Pradesh 10195 Maharashtra 45846 Rajasthan 48587 Tamil Nadu 55308 Kerala 11719 Orissa 255

48561Total

State Wise -Wind potential in India

Wind Energy Installed Capacity, INDIA

10240MW

Growth of Wind Capacity(By end 2012)

2,599

5,912

12,210

25,104

44,733

62,733

75,564

11,603

16,819

25,170

35,159

40,200

46,919

60,007

20,62222,247

23,90325,777

27,21429,060

31,332

11,630

15,14516,740

19,14920,676 21,674 22,796

6,2707,850

9,58710,925

13,064

16,08418,421

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2006 2007 2008 2009 2010 2011 2012

IC in

MW

China United States Germany Spain India

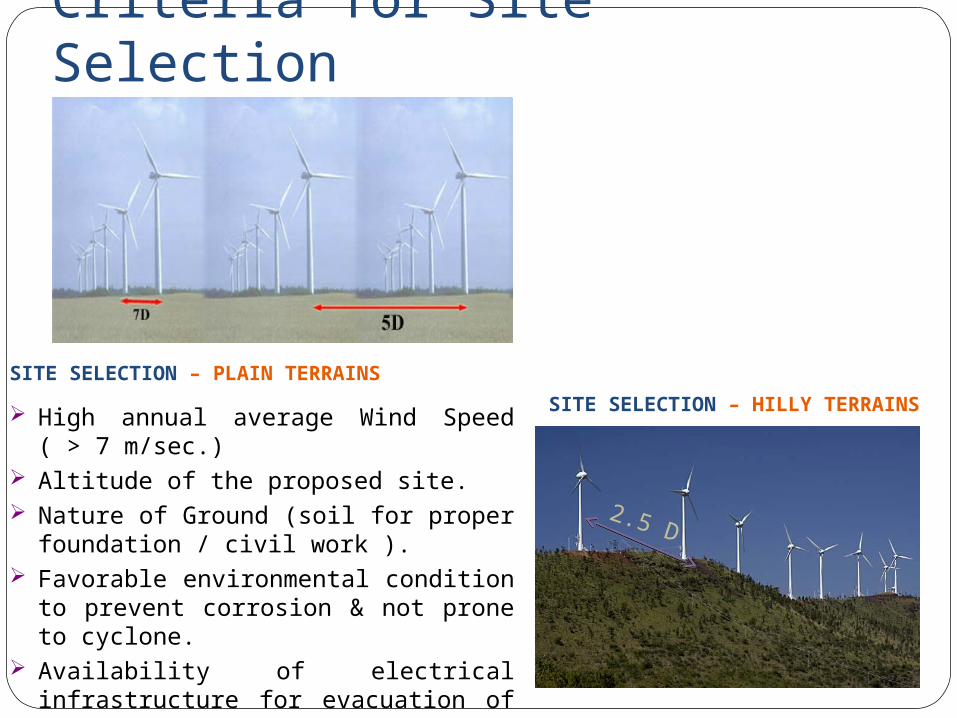

Criteria for Site Selection

2.5 D

SITE SELECTION – PLAIN TERRAINS

SITE SELECTION – HILLY TERRAINS High annual average Wind Speed ( > 7 m/sec.)

Altitude of the proposed site. Nature of Ground (soil for proper

foundation / civil work ). Favorable environmental condition to

prevent corrosion & not prone to cyclone.

Availability of electrical infrastructure for evacuation of electricity generated .

Solar in India : Potential & Prospects

1. India receives the highest global solar radiation on a horizontal surface. According to solar energy experts, India has considerable scope for solar energy production. India is bestowed with solar irradiation ranging from 4-7 kWh/ sq. m/ day across the country.

2. The desert areas in India have the solar radiation required for CSP(concentrating solar power technology) production. A 60 km x 60 km area can produce 1,00,000 MW of power. India has a desert area of 2,08,110 Sq Kms in Rajasthan and Gujarat. Even if India uses only 15,000 Sq. Kms of the desert, it can produce 3,00,000 MW of power.

3. Government of India is currently envisaging large-scale expansion of solar power capacity by 2022.

Country-wise Solar PV installed Capacity

32,509

16,987

8,043 7,6656,704

4,214 3,843

2,291 1,831 1,427

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Germany Italy China UnitedStates

Japan Spain France Australia UnitedKingdom

India

IC (M

W)

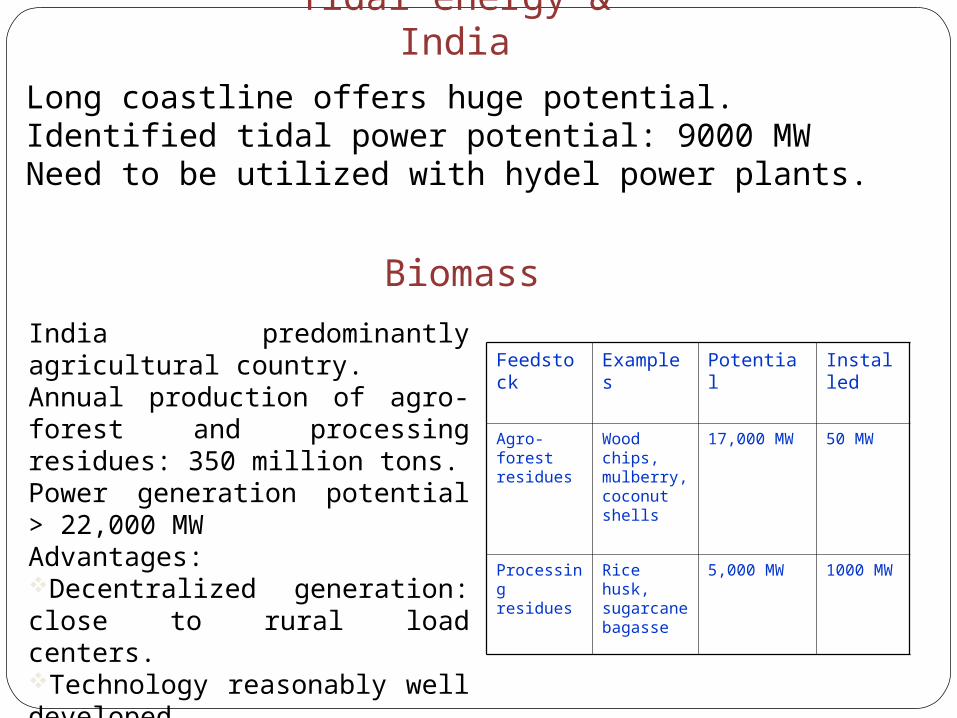

Tidal energy & India

Long coastline offers huge potential.Identified tidal power potential: 9000 MW Need to be utilized with hydel power plants.

India predominantly agricultural country.Annual production of agro-forest and processing residues: 350 million tons.Power generation potential > 22,000 MWAdvantages:Decentralized generation: close to rural load centers.Technology reasonably well developedEnvironment friendly: No net CO2 No net CO2 emissions

Biomass

Feedstock Examples Potential Installed

Agro-forest residues

Wood chips, mulberry, coconut shells

17,000 MW 50 MW

Processing residues

Rice husk, sugarcane bagasse

5,000 MW 1000 MW

Geothermal energy & India

Yet to be tapped .

Potential capacity over 10000 MW .

Puga valley in Ladakh has an

experimental 1 KW generator in

geothermal field .

North-western Himalayas & Western

coast are considered Geothermal areas.

Typical arrangement of an Small Hydro Power station

SHP station on a canal

SHP station on a riverSmall Hydro & India

Potential capacity over 10000 MW.

Non polluting, high prime mover efficiency, low operational cost

Availabilty - seasonal and intermittent

Integration issues of WindIntegration issues of Wind

• Planning criterion for RE

• Variability and Intermittency

• Forecasting and Scheduling

• SCADA / telemetry

• Network related Problems and Congestion

• Protection

• Commercial mechanism implementation

Planning Transmission system for RE

At lower penetration RE treated as an energy rather than capacity addition.

As the penetration of the RE increases, RE treated in terms of MW capacity.

Network development and O&M up to the pooling station by the wind developer. beyond the pooling station by the Distribution

licensee.

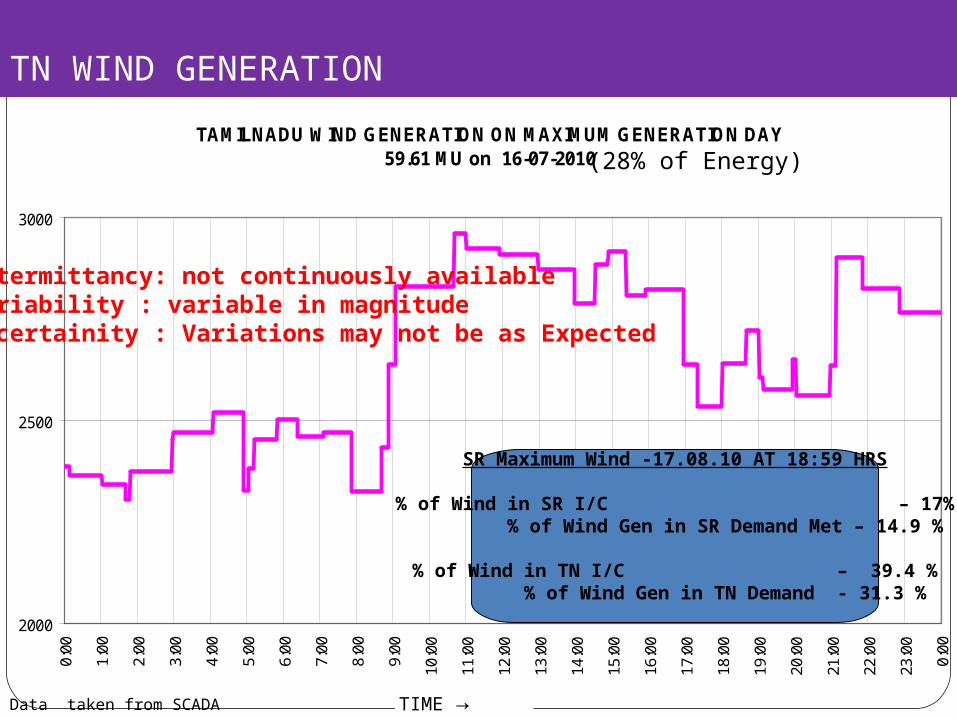

TN WIND GENERATION

TAMILNADU WIND GENERATION ON MAXIMUM GENERATION DAY 59.61 MU on 16-07-2010

2000

2500

3000

0:00

1:00

2:00

3:00

4:00

5:00

6:00

7:00

8:00

9:00

10:0

0

11:0

0

12:0

0

13:0

0

14:0

0

15:0

0

16:0

0

17:0

0

18:0

0

19:0

0

20:0

0

21:0

0

22:0

0

23:0

0

0:00

TIME ?Data taken from SCADA TIME →

(28% of Energy)

SR Maximum Wind -17.08.10 AT 18:59 HRS

% of Wind in SR I/C – 17% % of Wind Gen in SR Demand Met – 14.9 %

% of Wind in TN I/C – 39.4 % % of Wind Gen in TN Demand - 31.3 %

Intermittancy: not continuously availableVariability : variable in magnitudeUncertainity : Variations may not be as Expected

MAX WIND DAY:KARNATAKA 13/07/2011 MAX WIND DAY:KARNATAKA 13/07/2011 – 22.31 MU GENERATED, – 22.31 MU GENERATED,

15.7% OF TOTAL STATE CONSUMPTION15.7% OF TOTAL STATE CONSUMPTION

WIND GENERATION IN MW

FREQUENCY

MAX: 1400 MW, MIN 1050 MW

Need for Accurate Forecasting

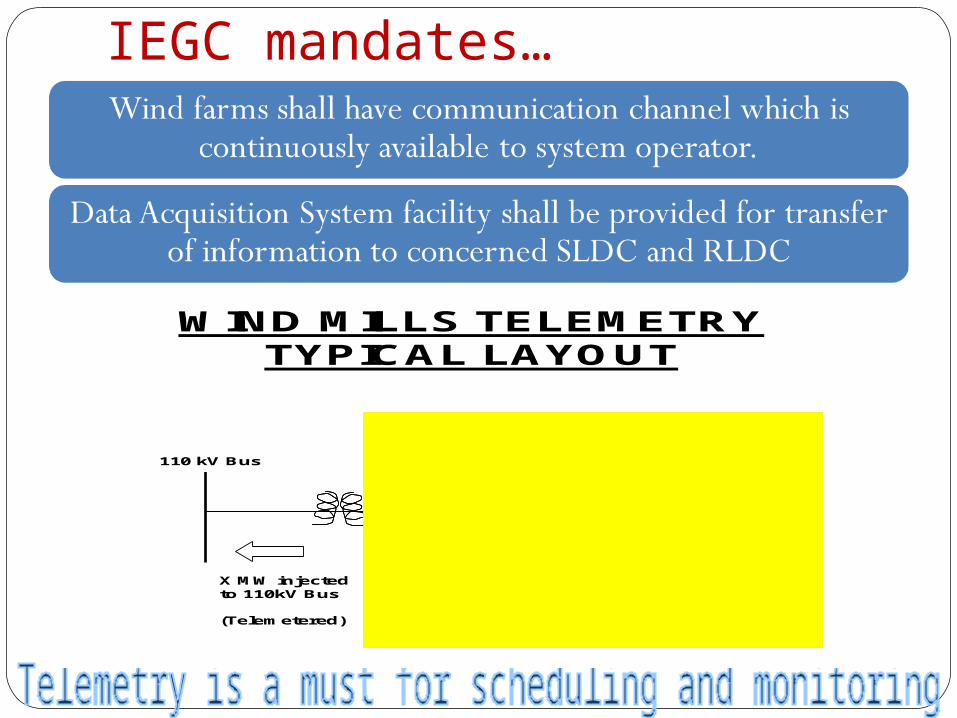

IEGC mandates…

WIND MILLS TELEMETRY TYPICAL LAYOUT

110 kV Bus

33kV or 11 kV Bus

LOADS

Untelemetered

X MW injectedto 110kV Bus

(Telemetered)

WIND MILLS

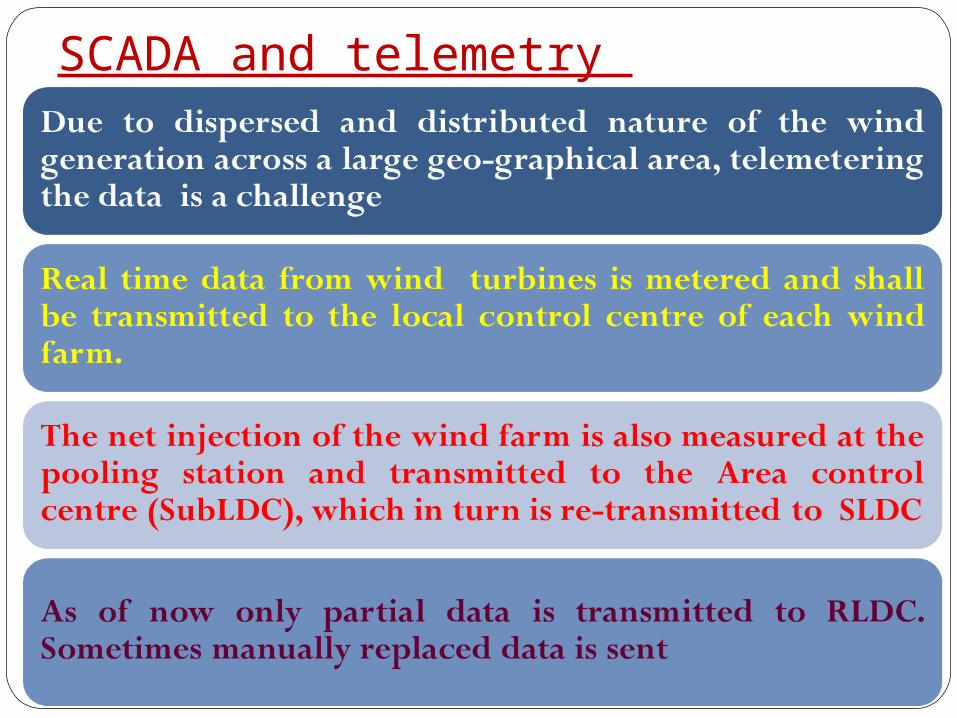

SCADA and telemetry

Protection requirements for RE

Efforts of Indian Regulators and policy makers

• Creation of Power Market post ABT, Open Access, Power Exchange

• ‘Cost-plus’ return on investment thro’ preferential tariff or Feed In Tariff (FIT)

• Solar power is exempted from sharing transmission charges and losses

• Accelerated Depreciation (AD) or Generation Based Incentive (GBI) @50 paise/unit

• Capital/ interest subsidy, concessional excise and customs duties etc.

• UI upto +/-30% socialised

• RE Sources Not evenly distributed across India• Inhibits the SERCs of potential deficit states from high

RPO• Potential rich states

• Already set higher RPO, still avenues left for new plants

• Very high cost of generation from RE sources (discourages local DISCOM to purchase beyond RPO)

• REC to address the mismatch between availability of RE sources and the requirement of RPO

Government Initiative: National Action Plan Government Initiative: National Action Plan on Climate Change (NAPCC), 2008on Climate Change (NAPCC), 2008

04/19/23

National level target for RE Purchase

5%of total grid purchase in 2010, to be increased by 1% each year

for 10 years: 15% by 2020

SERCs may set higher target

Appropriate authorities may issue certificates that procure RE in excess of

the national standard

Such certificates may be tradable, to enable utilities falling short to

meet their RPO

RE generation capacity needed: From 18000 to 45500 MW by FY2015

Eligibility of Wind Farms/Solar Generators for RECEligibility of Wind Farms/Solar Generators for REC

Wind farms – 10 MW and above and Solar plants - 5MW and above, connected at 33 KV and above :

• Connectivity details to concerned SLDC/RLDC

• Declaration about agreement if any

• Provide details of Contracts and Contracted path to the concerned SLDC RLDCRPC

• Generation forecast with periodic updates to SLDC/RLDC

• To provide Data Acquisition System (DAS) facility to SLDC/RLDC

Energy

Generation

GREEN ATTRIBUTE

GREEN ATTRIBUTE

ELECTRICITYELECTRICITY

RENEWABLE ENERGY

CERTIFICATE

SOLAR CERTIFICATE

NON-SOLAR CERTIFICATE

Options for DISCOMs to fulfill RPOOptions for DISCOMs to fulfill RPO

RPO

Buy Power @ Preferential Tariff

Buy REC

What is RPO ?

Obligation to purchase Renewable Energy directly through power purchase

or indirectly through purchase of Renewable energy Certificate

Renewable Purchase Obligation specified by SERC. It will :

Incentivise the RE generator

Reduce the Geographical imbalances in RE spread

NLDC 55

Electricity Component

* Self consumption by CPPs based upon renewable generation are eligible for RECs

RE Generation*

Sale at Preferential

TariffREC Component

Obligated Entities / Voluntary Buyers

Distribution Company/ Third Party Sale/ Power Exchange

Obligated Entities

ACCREDITATION

REGISTRATION

ISSUANCE

TRADE & REDEMPTION

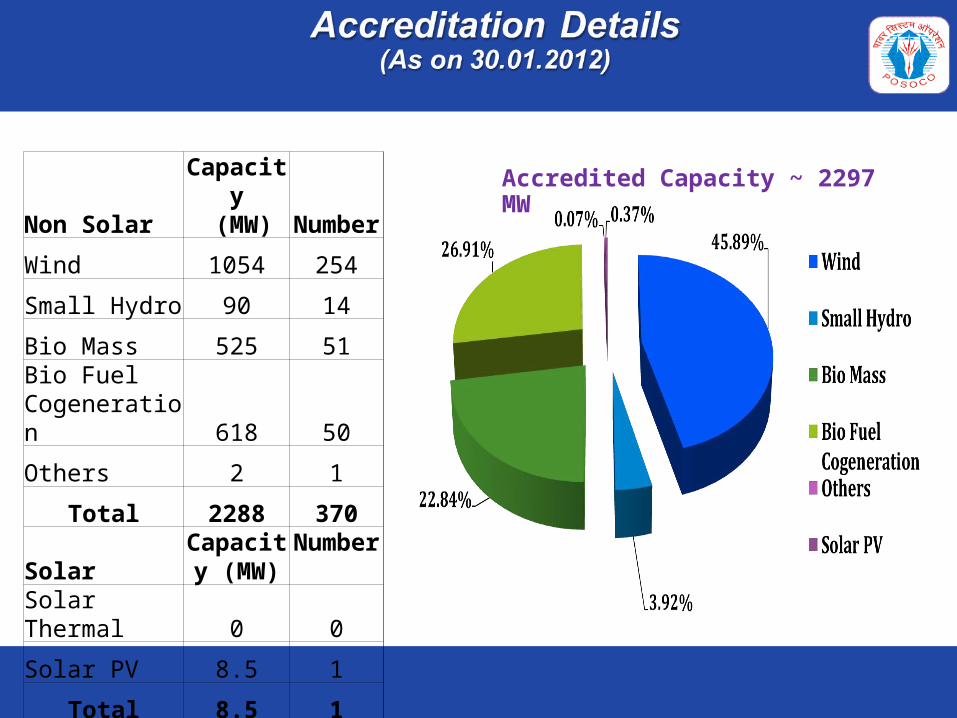

Non SolarCapacity (MW) Number

Wind 1054 254

Small Hydro 90 14

Bio Mass 525 51Bio Fuel Cogeneration 618 50

Others 2 1

Total 2288 370

SolarCapacity

(MW) Number

Solar Thermal 0 0

Solar PV 8.5 1

Total 8.5 1

Accredited Capacity ~ 2297 MW

Non SolarCapacity

(MW) NumberWind 900 204Small Hydro 88 13Bio Mass 446 38Bio Fuel Cogeneration 606 49Urban & Municipal Waste 0 0

Total 2039 304

SolarCapacity

(MW) Number Solar Thermal 0 0Solar PV 0 0

Total 0 0

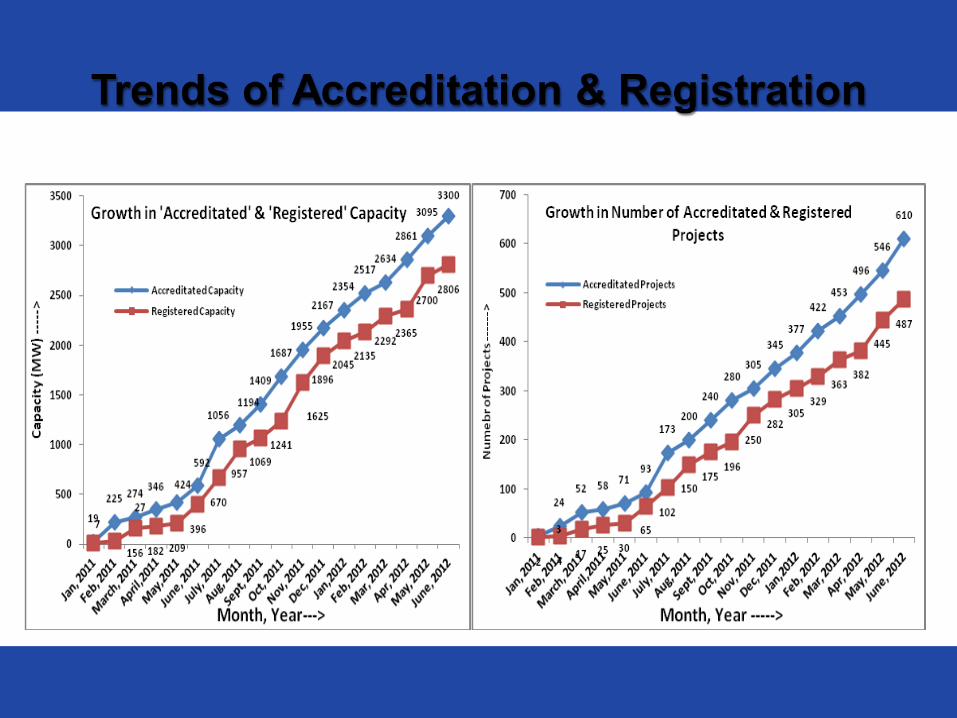

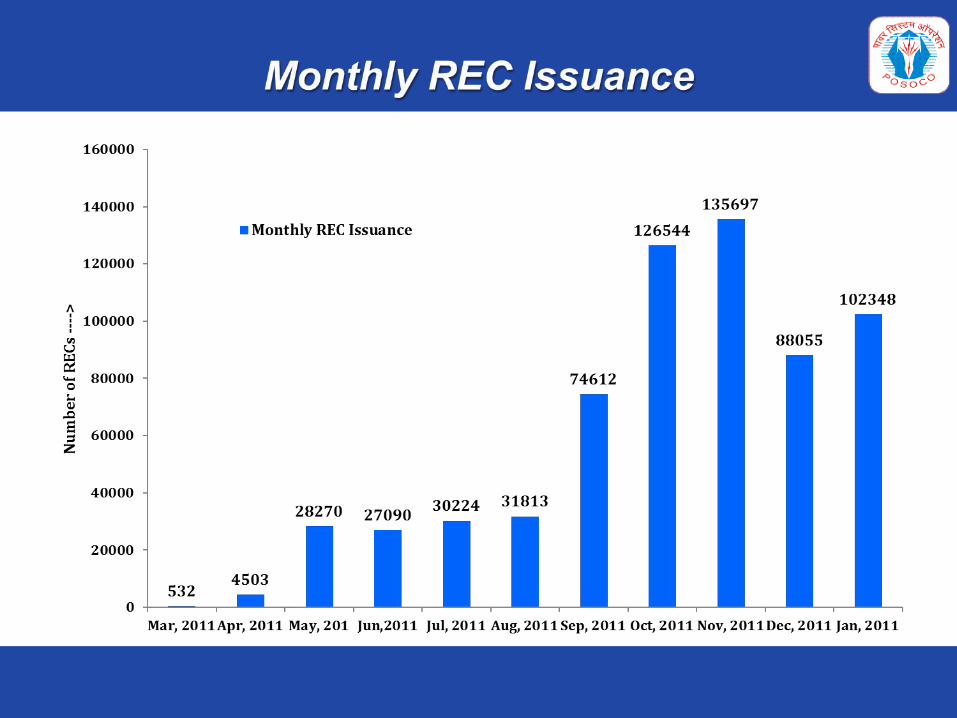

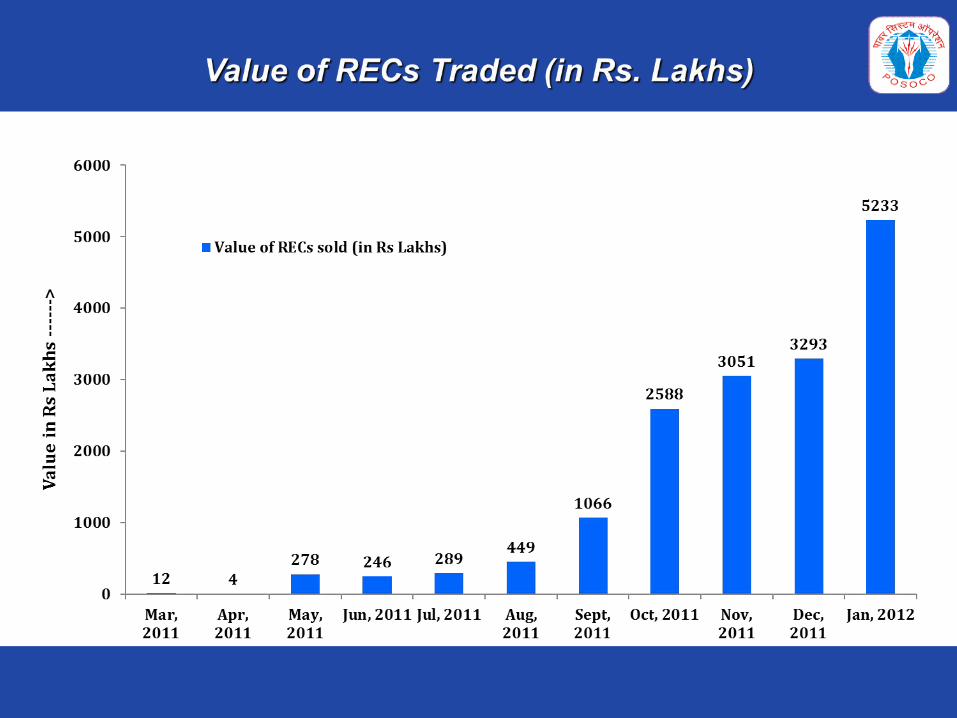

Registered Capacity Surpassed CERC estimate of most optimistic scenario in REC Fees and Charges Order

Registered Capacity ~ 2039 MW

Measures under implementation stage :Measures under implementation stage :

• Forecasting and Scheduling of Grid connected wind and Solar

generators

• Eligible generators would be required to forecast their generation

with a minimum accuracy of + 30%.

• Any deviation upto + 30% will not have any cost implication to the

Renewable Energy generator.

• The RE generator can enter in to contract to supply power to any

entity located any where in the country under Short Term Open

Access at a price negotiated bilaterally.

Approach thro’ Renewable Regulatory Fund:Approach thro’ Renewable Regulatory Fund:

• Achieve better generation prediction using weather forecasting tools

• Immune wind generators from paying deviation in UI charges up to a certain level of variation

• No UI charges payable/receivable by Solar Generator

• Socialise the deviation charges arrived due to variations amongst different state utilities

• Develop a self sustaining mechanism towards better acceptance of intermittent generation

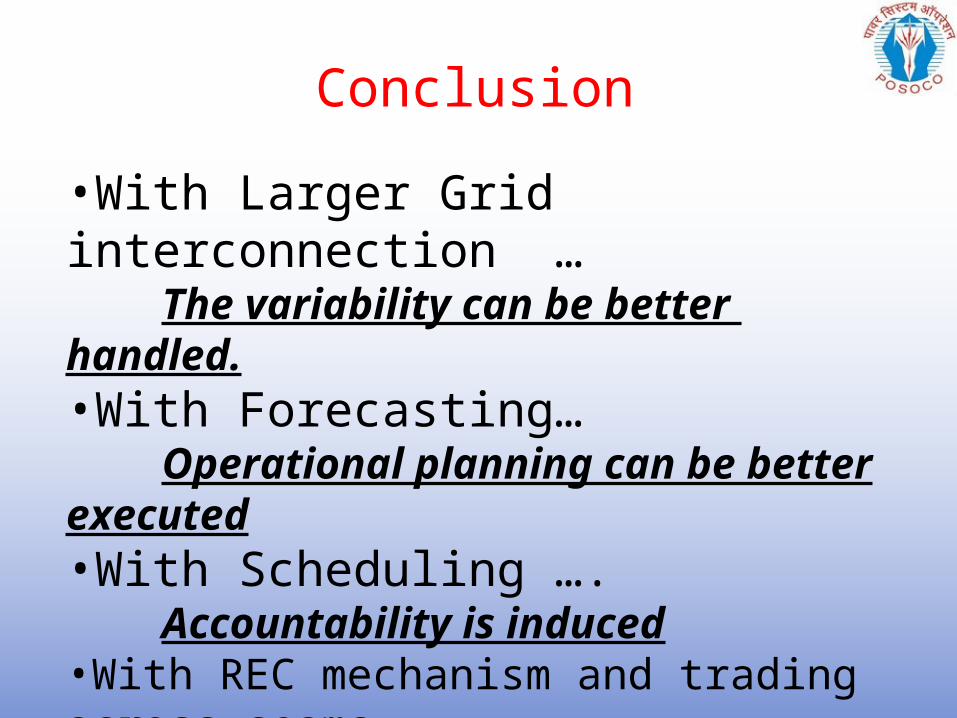

Conclusion

•With Larger Grid interconnection …

The variability can be better handled.•With Forecasting…

Operational planning can be better executed•With Scheduling ….

Accountability is induced•With REC mechanism and trading across seams…

RE will be an attractive business

Thank You