9th annual new york value investing...

TRANSCRIPT

9th annual new yorkvalue investing congress

•September 16, 2013 • New York, NY

Where do we go from here?Mark A. Boyar, Boyar Value Group

www.ValueInvestingCongress.com

Mark Boyar www.BoyarValueGroup.com

Where Do We Go From Here?Thoughts on navigating a stock picker's market.

Mark Boyar www.BoyarValueGroup.com

Mark Boyar www.BoyarValueGroup.com

Disclaimer

The statistical and other information contained in this presentation has been obtained from sources wedeem to be reliable, but we cannot guarantee its entire accuracy or completeness.

The information presented is not intended to be an offer to sell or the solicitation of an offer to purchaseany security or investment product. This presentation may not be published or re-distributed without theprior written consent of Boyar’s Intrinsic Value Research LLC. Investors should bear in mind that pastperformance of any investments described herein are for illustrative purposes only and are notnecessarily indicative of future results.

This presentation may contain, or may be deemed to contain, “forward-looking” statements, which arestatements other than statements of historical facts. By their nature, forward-looking statements involverisks and uncertainties because they relate to events and depend on circumstances that may or may notoccur in the future. The future of investment results of the investments described herein may vary fromthe results expressed in, or implied by, any forward looking statements included in this presentation,possibly to a material degree.

Affiliated companies, clients, and employees of Boyar’s Intrinsic Value Research own shares inMSG, and SKS. The presentation represents the views of Boyar’s Intrinsic Value Research as of9/16/2013 and is subject to change at anytime without notice.

Mark Boyar www.BoyarValueGroup.com

About Mark Boyar

Mark A. Boyar has been a securities analyst since 1968.

Mr. Boyar began publishing Asset Analysis Focus in 1975.Approximately 40% of the companies profiled in this publicationhave been acquired or liquidated – the vast majority atsignificantly higher prices than when originally profiled.

Boyar’s annual Forgotten Forty publication advanced 28% in2012 and has outperformed the S&P 500 significantly over thepast 10 years.

Mr. Boyar began publishing Boyar’s Micro Cap Focus in 2010.The stocks contained in this publication have increased by anaverage of 78.5% compared to an advance of 28.8% for theRussell Microcap value index.

Since 1983, Mr. Boyar has been formally managing money forboth institutions and high-net-worth individuals through BoyarAsset Management.

Mark Boyar www.BoyarValueGroup.com

A LOOK BACK AT MY SPEECH AT THE 2013 VIC IN LAS VEGAS

History Does Not Repeat ItselfBut It Sure Does RhymeLessons learned from 40 years

in the investment business.

Mark Boyar www.BoyarValueGroup.com

LESSON #1:You can purchase thebest company in theworld, but if you do notbuy it at a reasonableprice, you will notcompound your capitalat an acceptable rateof return.

Mark Boyar www.BoyarValueGroup.com

Lesson #1

These were companies that were:• Impervious to any economic downturn

• “One decision” stocks (buy at any price, no need to sell)

The 1960s produced a group of stocks that were affectionately dubbed the “Nifty Fifty.”

Examples of Nifty Fifty stocks included:

Mark Boyar www.BoyarValueGroup.com

Lesson #1

Nifty Fifty S&P 500

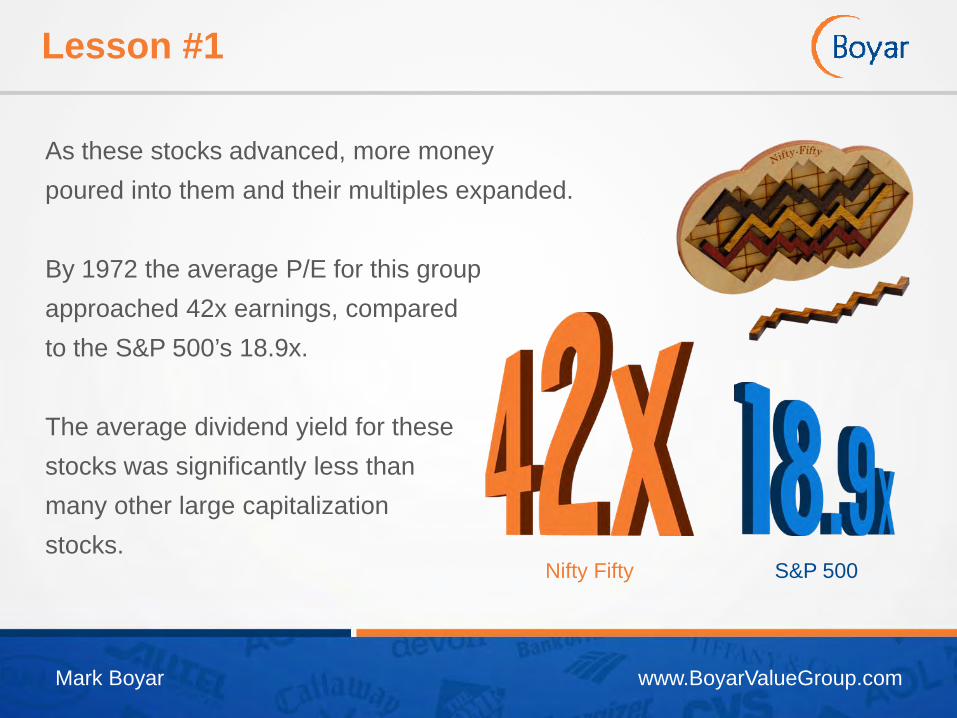

As these stocks advanced, more money poured into them and their multiples expanded.

By 1972 the average P/E for this group approached 42x earnings, compared to the S&P 500’s 18.9x.

The average dividend yield for these stocks was significantly less than many other large capitalizationstocks.

Mark Boyar www.BoyarValueGroup.com

Lesson #1

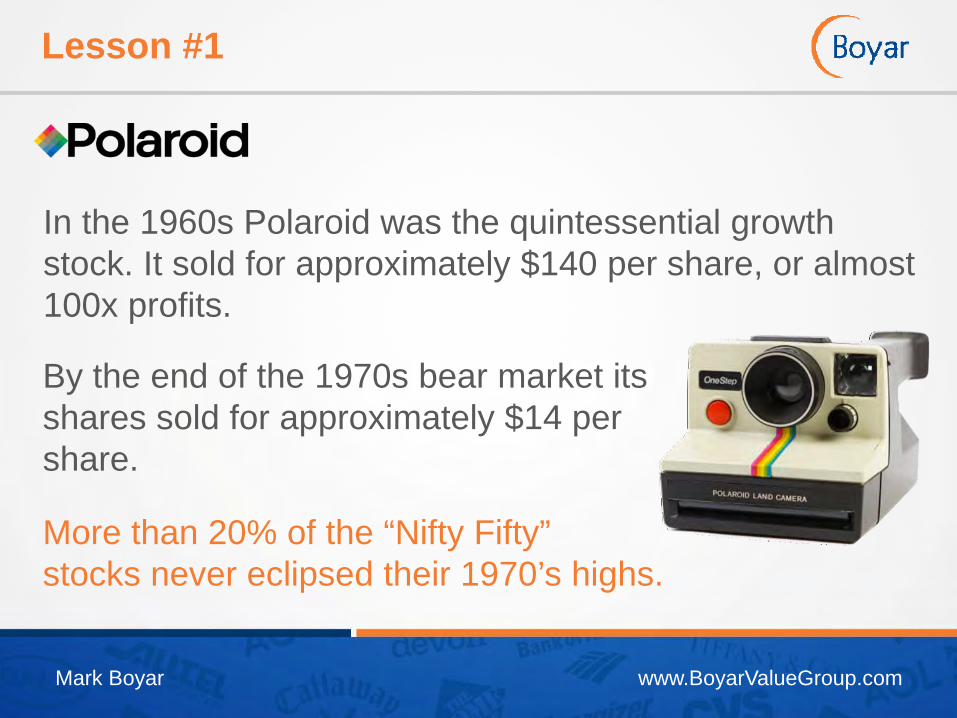

In the 1960s Polaroid was the quintessential growth stock. It sold for approximately $140 per share, or almost 100x profits.

By the end of the 1970s bear market its shares sold for approximately $14 per share.

More than 20% of the “Nifty Fifty”stocks never eclipsed their 1970’s highs.

Mark Boyar www.BoyarValueGroup.com

Lesson #1

By the 1990s large-capitalization stocks were once again commanding outsized multiples.

COMPANY 1990’S PEAK

Ticker Company Name Date Peak Price Trailing P/E Ratio Annual Dividend Yield

GE General Electronic Company Dec. 99’ 45.41 43.39 1.03%

MSFT Microsoft Corporation Dec. 99’ 48.06 58.97 0.00%

JNJ Johnson & Johnson Nov. 99’ 52.13 41.40 1.07%

PFE Pfizer, Inc. Apr. 99’ 46.52 90.60 0.63%

DIS The Walt Disney Company May 99’ 41.33 40.30 0.50%

CSCO Cisco Systems, Inc. Dec. 99’ 47.78 154.10 0.00%

SYY Sysco Corporation Dec. 99’ 19.28 33.53 1.25%

INTC Intel Corporation Sept. 99’ 44.66 40.20 0.13%

Mark Boyar www.BoyarValueGroup.com

Lesson #1

Today the majority of those companies are currently commanding significantly lower multiples and have a higher dividend yield!

COMPANY CURRENT

Ticker Company Name Date Current Price Trailing P/E Ratio Annual Dividend Yield

GE General Electronic Company 9/4/13 23.10 17.1 3.3%

MSFT Microsoft Corporation 9/4/13 31.21 12.1 2.8%

JNJ Johnson & Johnson 9/4/13 86.86 19.3 3.1%

PFE Pfizer, Inc. 9/4/13 28.44 7.9 3.4%

DIS The Walt Disney Company 9/4/13 61.17 18.5 1.2%

CSCO Cisco Systems, Inc. 9/4/13 23.89 12.8 2.9%

SYY Sysco Corporation 9/4/13 32.20 19.3 3.5%

INTC Intel Corporation 9/4/13 22.76 12.2 4.1%

Mark Boyar www.BoyarValueGroup.com

Is there a multiple expansion on the horizon?

Mark Boyar www.BoyarValueGroup.com

LESSON #2:Load up the truck

Mark Boyar www.BoyarValueGroup.com

Lesson #2

Usually after bear markets or unforeseen geopolitical events common stocks go on sale.

Major Examples:

1970’s – Oil Embargo, Vietnam War, Watergate1987 – Stock Market Crash2001 – September 11, 20012008 - 2009 – Lehman Brothers, Bear Stearns, Financial Crisis

Mark Boyar www.BoyarValueGroup.com

LESSON #3:

NEVER EVERlisten to the Chairmanof the Board of a company

Mark Boyar www.BoyarValueGroup.com

Lesson #3

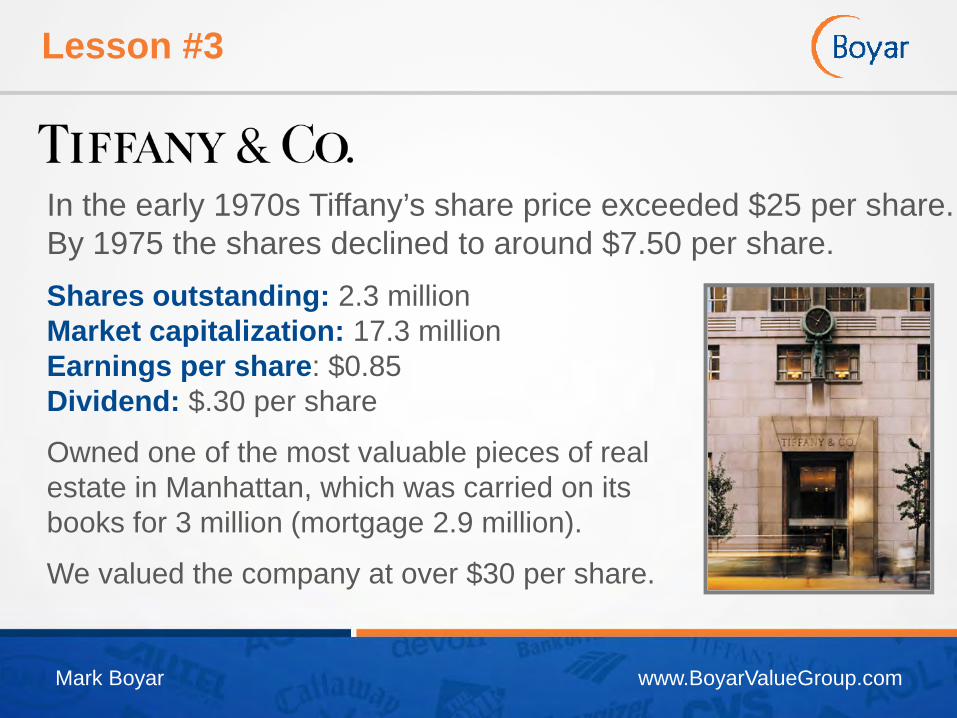

In the early 1970s Tiffany’s share price exceeded $25 per share. By 1975 the shares declined to around $7.50 per share.Shares outstanding: 2.3 millionMarket capitalization: 17.3 millionEarnings per share: $0.85Dividend: $.30 per share

Owned one of the most valuable pieces of real estate in Manhattan, which was carried on its books for 3 million (mortgage 2.9 million).

We valued the company at over $30 per share.

Mark Boyar www.BoyarValueGroup.com

Lesson #3

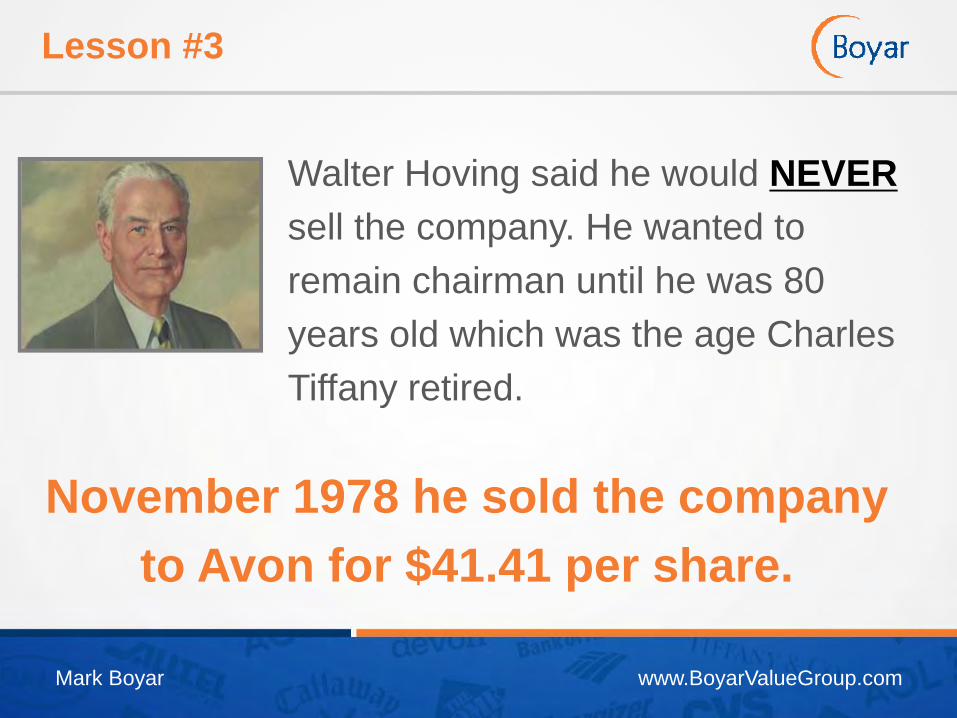

Walter Hoving said he would NEVERsell the company. He wanted to remain chairman until he was 80 years old which was the age Charles Tiffany retired.

November 1978 he sold the company to Avon for $41.41 per share.

Mark Boyar www.BoyarValueGroup.com

LESSON #4:Industry specific analysts know a lot about companies within their given industry, but can they make you money?

Mark Boyar www.BoyarValueGroup.com

Lesson #4

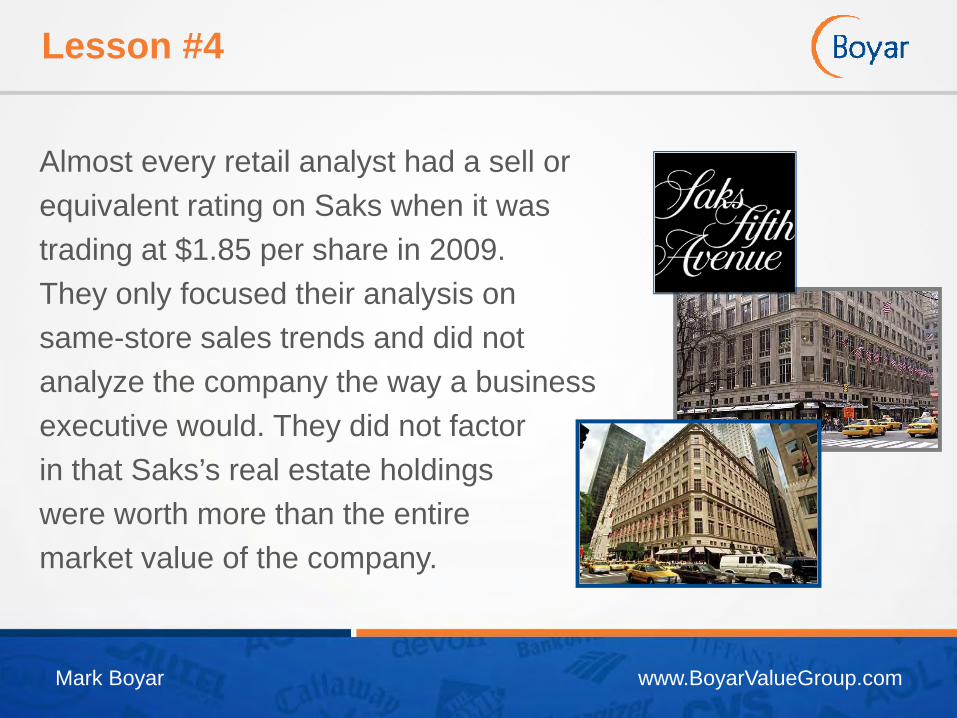

Almost every retail analyst had a sell or equivalent rating on Saks when it was trading at $1.85 per share in 2009. They only focused their analysis on same-store sales trends and did not analyze the company the way a business executive would. They did not factor in that Saks’s real estate holdings were worth more than the entire market value of the company.

Mark Boyar www.BoyarValueGroup.com

So Where Do We Go From Here?

Mark Boyar www.BoyarValueGroup.com

So Where Do We Go From Here?

Months Months

Current Bull Market

Average Bull Market Since 1921

Vs.

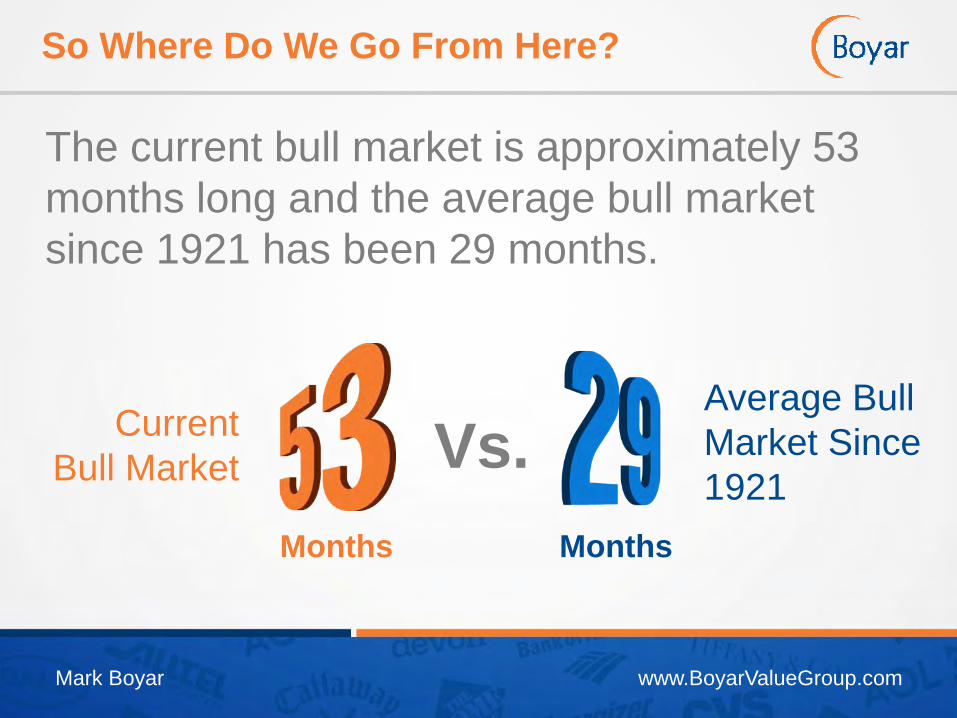

The current bull market is approximately 53 months long and the average bull market since 1921 has been 29 months.

Mark Boyar www.BoyarValueGroup.com

So Where Do We Go From Here?

The average price increase

Jump in the S&P 500

Vs.

The average price increase from the bottom during the past 17 bull markets has been 153% vs. a 150% jump in the S&P 500 from 3/9/2009.

Mark Boyar www.BoyarValueGroup.com

So Where Do We Go From Here?

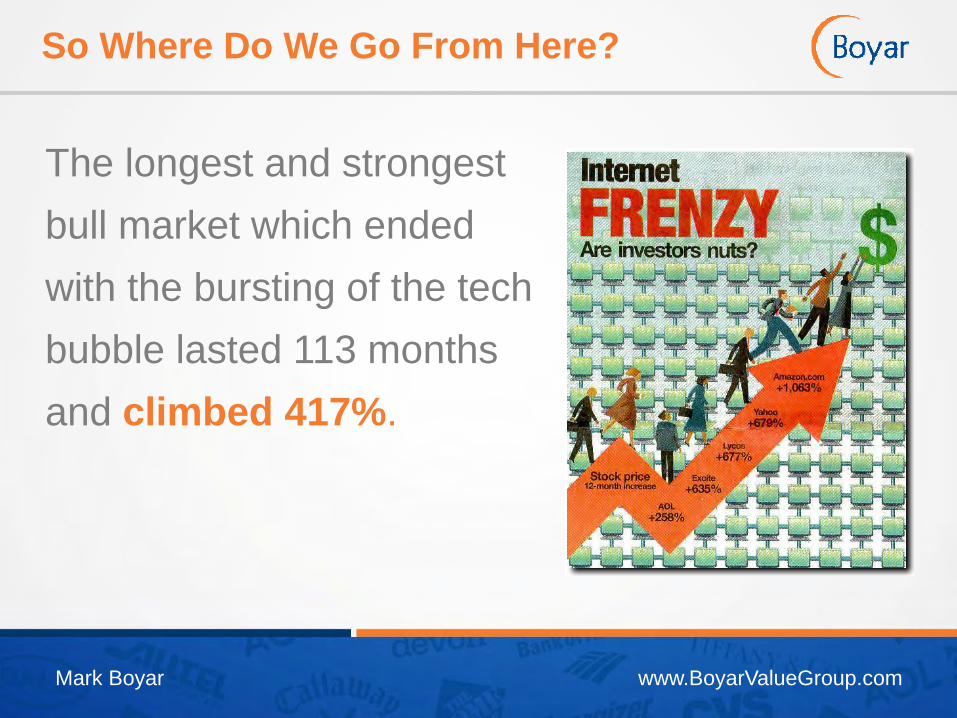

The longest and strongest bull market which ended with the bursting of the tech bubble lasted 113 monthsand climbed 417%.

Mark Boyar www.BoyarValueGroup.com

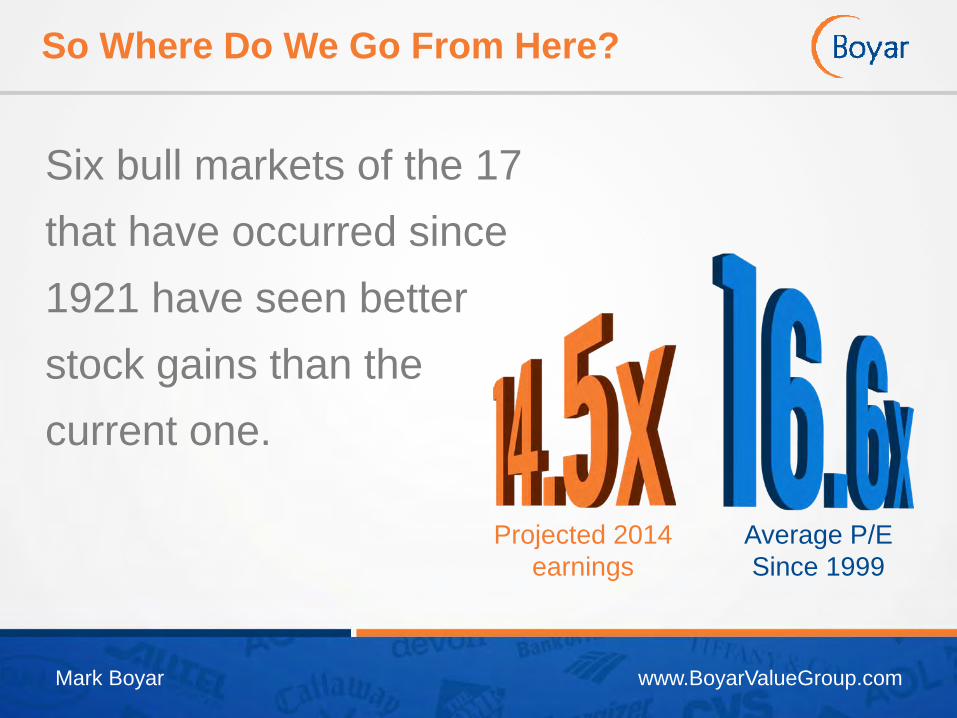

So Where Do We Go From Here?

Projected 2014earnings

Average P/ESince 1999

Six bull markets of the 17 that have occurred since 1921 have seen better stock gains than the current one.

Mark Boyar www.BoyarValueGroup.com

So Where Do We Go From Here?

NASDAQ

Typically bull markets come to an end following a period of extraordinary performance.

Mark Boyar www.BoyarValueGroup.com

So Where Do We Go From Here?

Growth Value

The months leading to market tops share striking similarities:• Growth stocks outperform

value stocks

• Small capitalization stocks outperform large capitalization stocks

Mark Boyar www.BoyarValueGroup.com

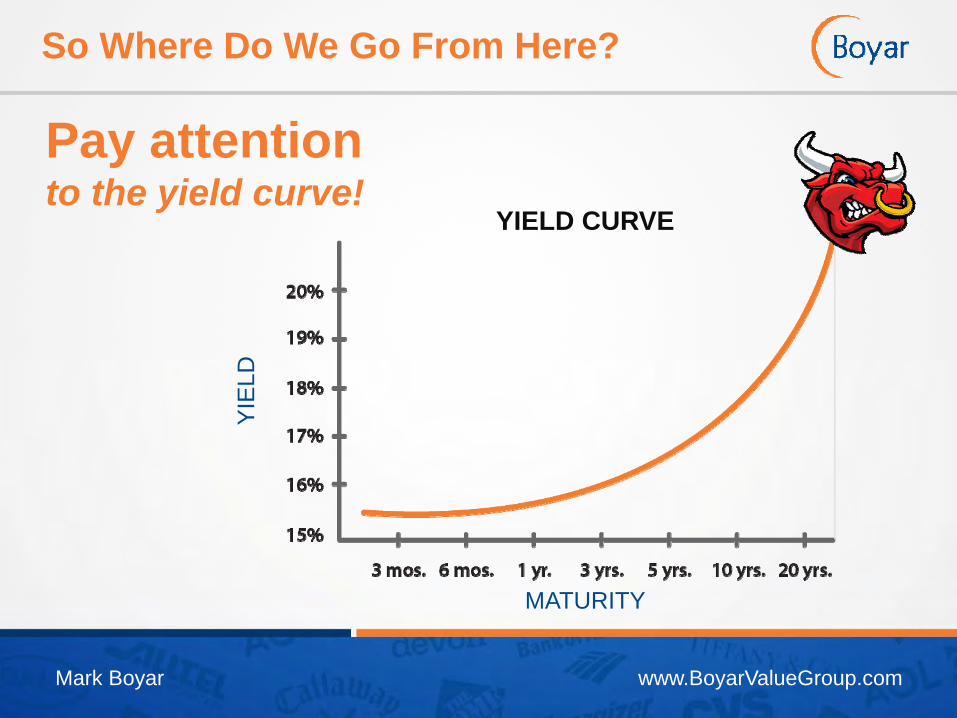

Pay attention to the yield curve!

YIELD CURVE

MATURITY

YIE

LD

So Where Do We Go From Here?

Mark Boyar www.BoyarValueGroup.com

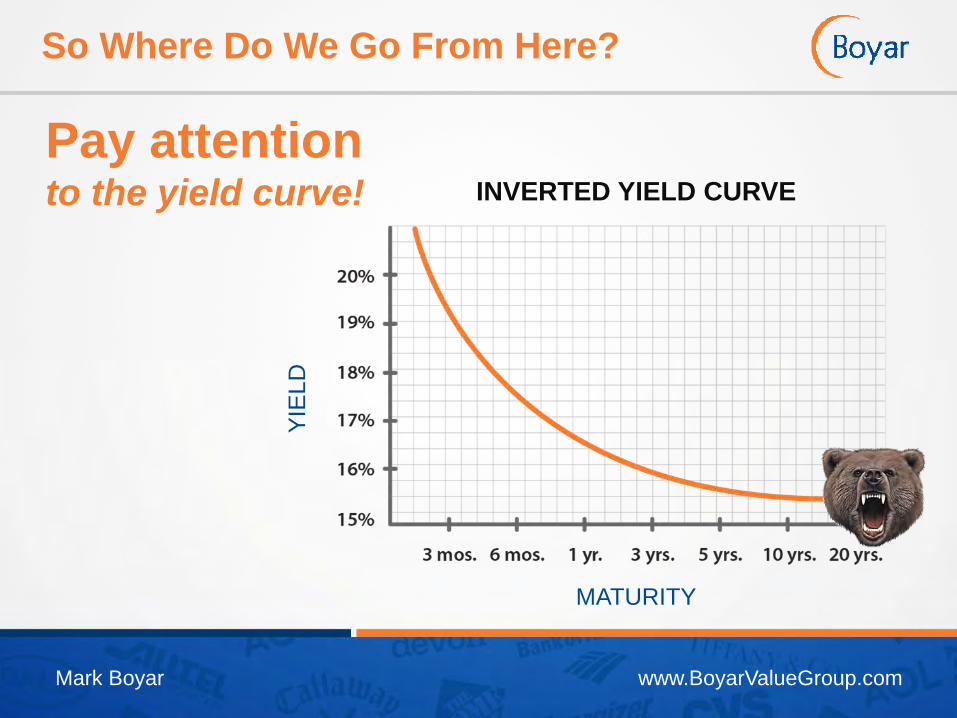

INVERTED YIELD CURVE

MATURITY

YIE

LD

Pay attention to the yield curve!

So Where Do We Go From Here?

Mark Boyar www.BoyarValueGroup.com

So Where Do We Go From Here?

A look back at the granddaddy of all bull markets.

Mark Boyar www.BoyarValueGroup.com

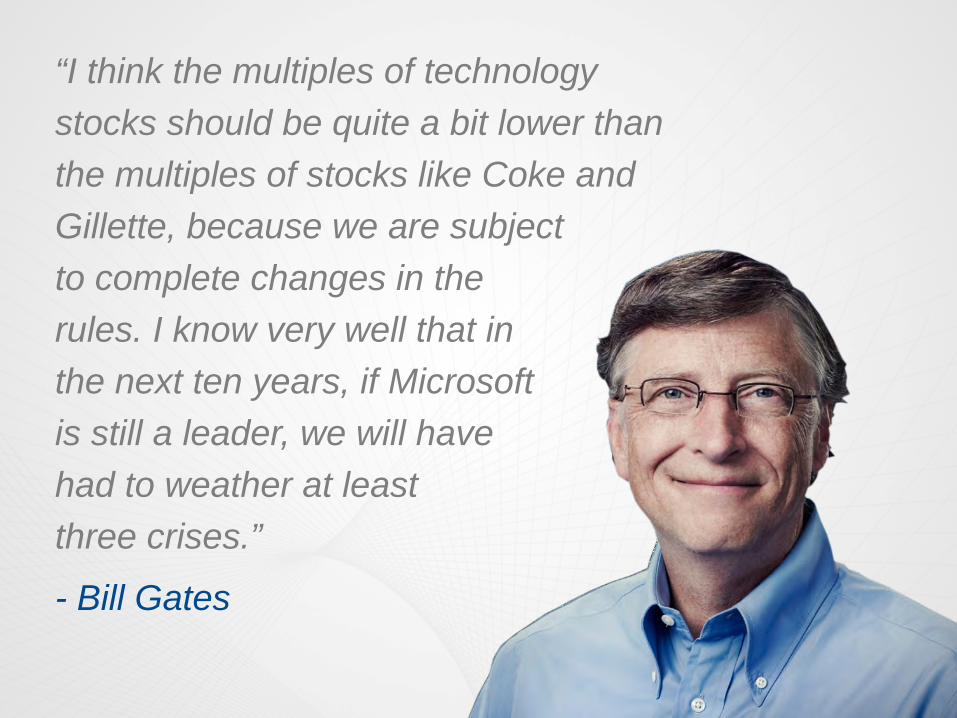

“I think the multiples of technology stocks should be quite a bit lower than the multiples of stocks like Coke and Gillette, because we are subject to complete changes in the rules. I know very well that in the next ten years, if Microsoft is still a leader, we will have had to weather at least three crises.”

- Bill Gates

Mark Boyar www.BoyarValueGroup.com

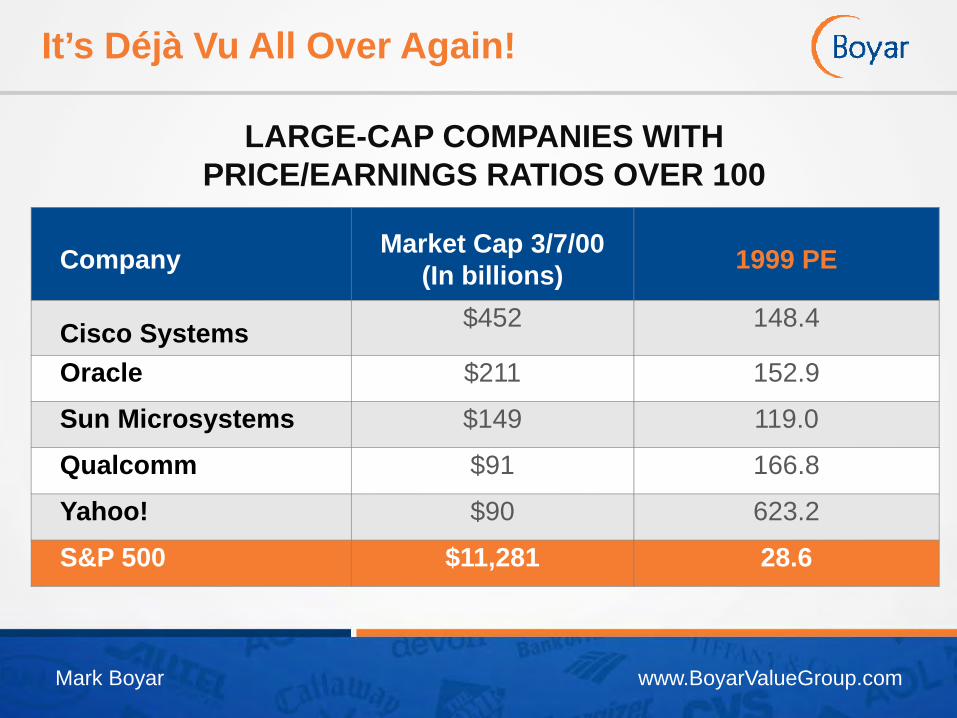

It’s Déjà Vu All Over Again!

Company Market Cap 3/7/00(In billions) 1999 PE

Cisco Systems $452 148.4

Oracle $211 152.9

Sun Microsystems $149 119.0

Qualcomm $91 166.8

Yahoo! $90 623.2

S&P 500 $11,281 28.6

LARGE-CAP COMPANIES WITH PRICE/EARNINGS RATIOS OVER 100

Mark Boyar www.BoyarValueGroup.com

It’s Déjà Vu All Over Again!

Company Market Cap(in billions) PE Ratio

Netflix$17 195x 2013

Amazon $134 382x 2013

Tesla $20 293x 2013

Zillow $3.6 189x 2014

Linkedin $27 155x 2013

TODAY’S HIGH FLYERS

Mark Boyar www.BoyarValueGroup.com

Did Yahoo Make The Same Mistake Again?

• In 1999 Yahoo purchased Broadcast.com from Mark Cuban for $5.7 billion

• This year Yahoo purchased blogging site Tumblr ($14 million in revenue) for $1.1 billion

Mark Boyar www.BoyarValueGroup.com

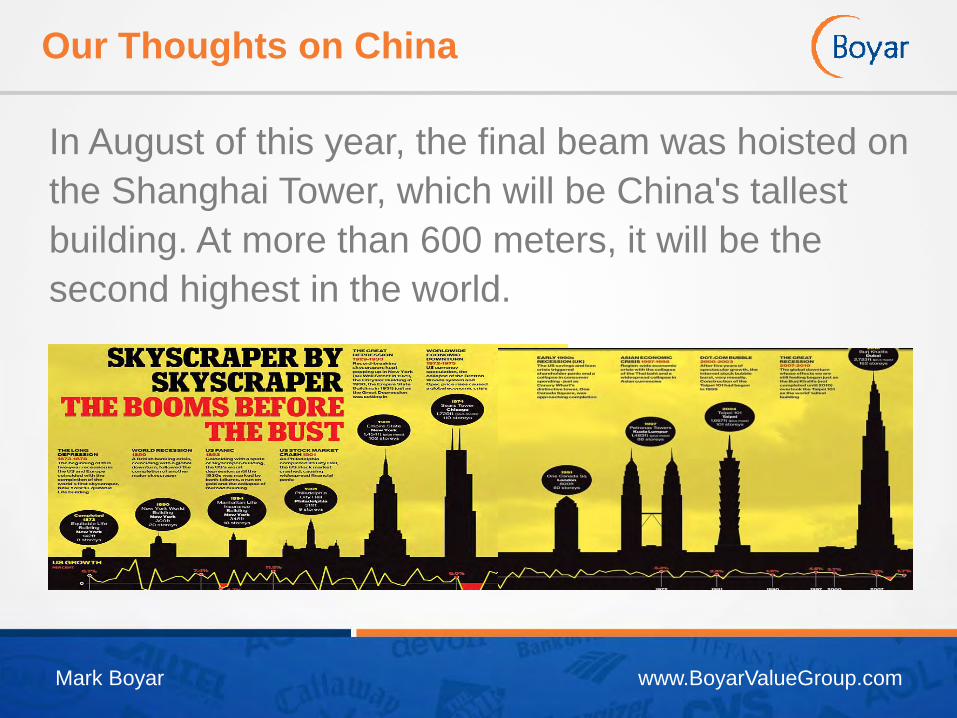

Our Thoughts on China

One of our BIGGEST concerns is China.

Mark Boyar www.BoyarValueGroup.com

Our Thoughts on China

In August of this year, the final beam was hoisted on the Shanghai Tower, which will be China's tallest building. At more than 600 meters, it will be the second highest in the world.

Mark Boyar www.BoyarValueGroup.com

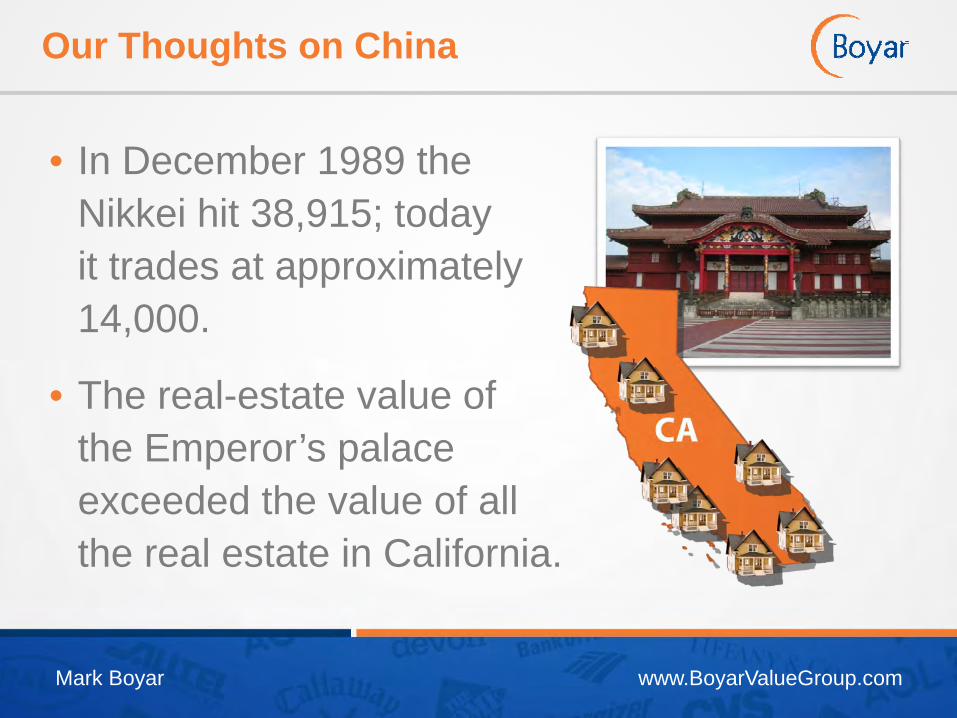

Our Thoughts on China

• In December 1989 the Nikkei hit 38,915; today it trades at approximately 14,000.

• The real-estate value of the Emperor’s palace exceeded the value of all the real estate in California.

Mark Boyar www.BoyarValueGroup.com

Our Thoughts on China

Japan was expected to surpass the U.S. as the leading economic power in the world. A number of leading business periodicals had cover stories entitled The Rising Sun.

The “Setting Sun” would have been more accurate.

Mark Boyar www.BoyarValueGroup.com

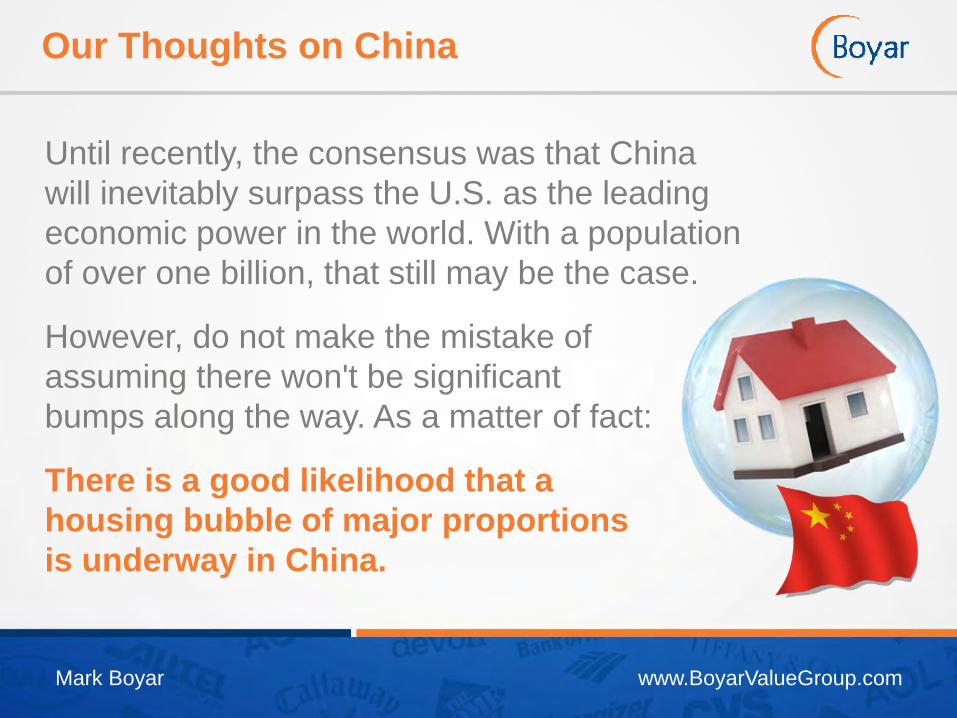

Our Thoughts on China

Until recently, the consensus was that China will inevitably surpass the U.S. as the leading economic power in the world. With a population of over one billion, that still may be the case.

However, do not make the mistake of assuming there won't be significant bumps along the way. As a matter of fact:

There is a good likelihood that a housing bubble of major proportions is underway in China.

Mark Boyar www.BoyarValueGroup.com

A Chinese Housing Bubble?

• In 2007, we advocated to our research clients shortingthe merchant builders.

• We believed “it was different this time.” We realize howdangerous those words can be.

• Our thesis was it was not an interest rate problem, it wasan affordability problem.

• Homes were too expensive. There had been 4 or 5 yearsof double-digit price increases.

• Historical returns are 2%-3%. We believed there wouldbe a reversion to the mean.

Mark Boyar www.BoyarValueGroup.com

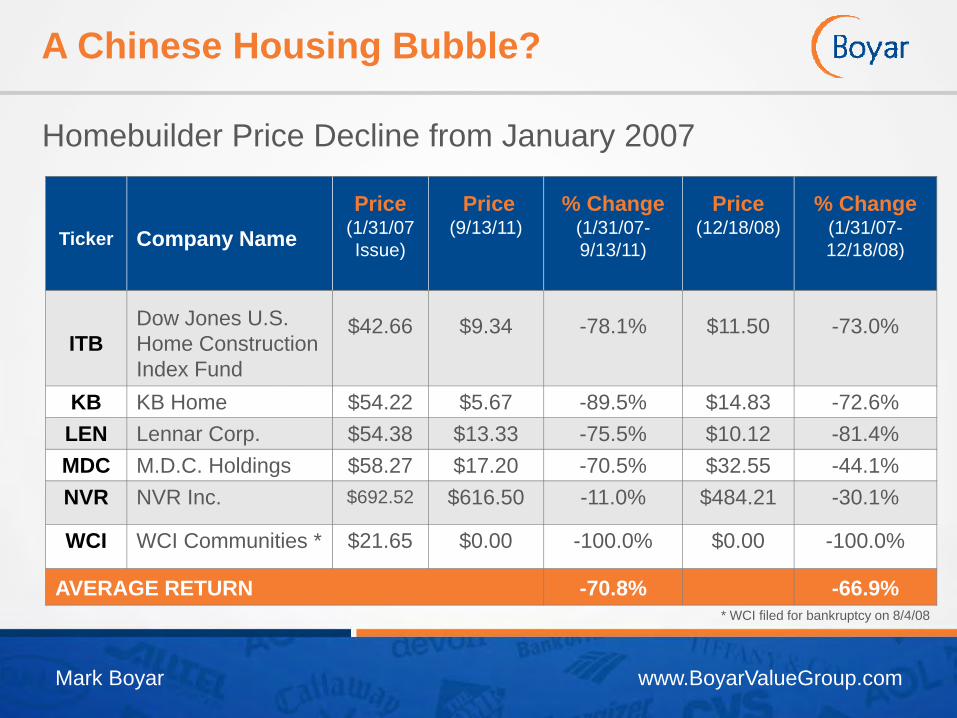

* WCI filed for bankruptcy on 8/4/08

A Chinese Housing Bubble?

Homebuilder Price Decline from January 2007

Ticker Company NamePrice

(1/31/07 Issue)

Price(9/13/11)

% Change(1/31/07-9/13/11)

Price(12/18/08)

% Change(1/31/07-12/18/08)

ITBDow Jones U.S. Home Construction Index Fund

$42.66 $9.34 -78.1% $11.50 -73.0%

KB KB Home $54.22 $5.67 -89.5% $14.83 -72.6%LEN Lennar Corp. $54.38 $13.33 -75.5% $10.12 -81.4%MDC M.D.C. Holdings $58.27 $17.20 -70.5% $32.55 -44.1%NVR NVR Inc. $692.52 $616.50 -11.0% $484.21 -30.1%

WCI WCI Communities * $21.65 $0.00 -100.0% $0.00 -100.0%

AVERAGE RETURN -70.8% -66.9%

Mark Boyar www.BoyarValueGroup.com

A Chinese Housing Bubble?

China is now facing a problem similar to what the U.S. experienced. In our opinion there has been massive overbuilding coupled with huge price increases.

Mark Boyar www.BoyarValueGroup.com

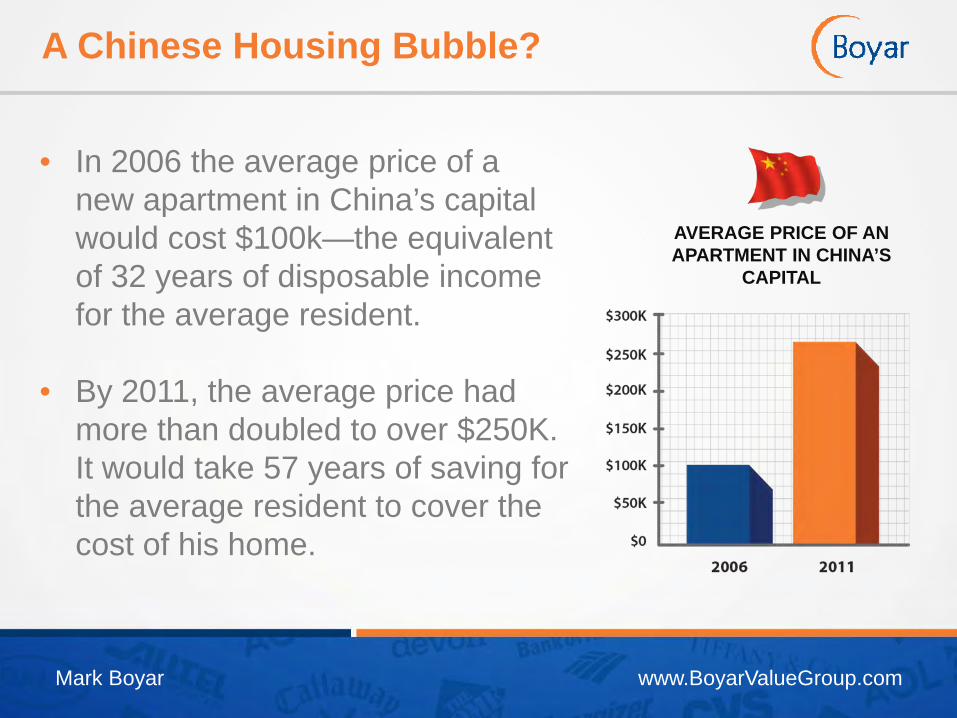

A Chinese Housing Bubble?

AVERAGE PRICE OF ANAPARTMENT IN CHINA’S

CAPITAL

• In 2006 the average price of a new apartment in China’s capital would cost $100k—the equivalent of 32 years of disposable incomefor the average resident.

• By 2011, the average price had more than doubled to over $250K. It would take 57 years of saving for the average resident to cover the cost of his home.

Mark Boyar www.BoyarValueGroup.com

Possible Ramifications of a Chinese Housing Crisis

A real-estate collapse in China could cause a banking crisis that would dwarf our subprime problem.

Mark Boyar www.BoyarValueGroup.com

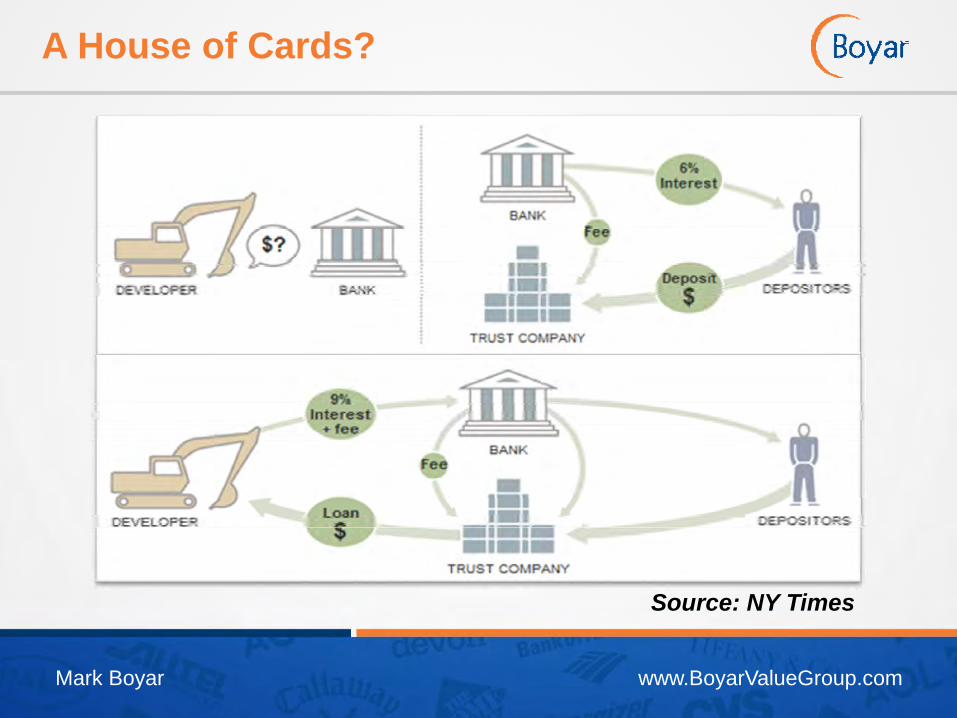

A House of Cards?

Source: NY Times

Mark Boyar www.BoyarValueGroup.com

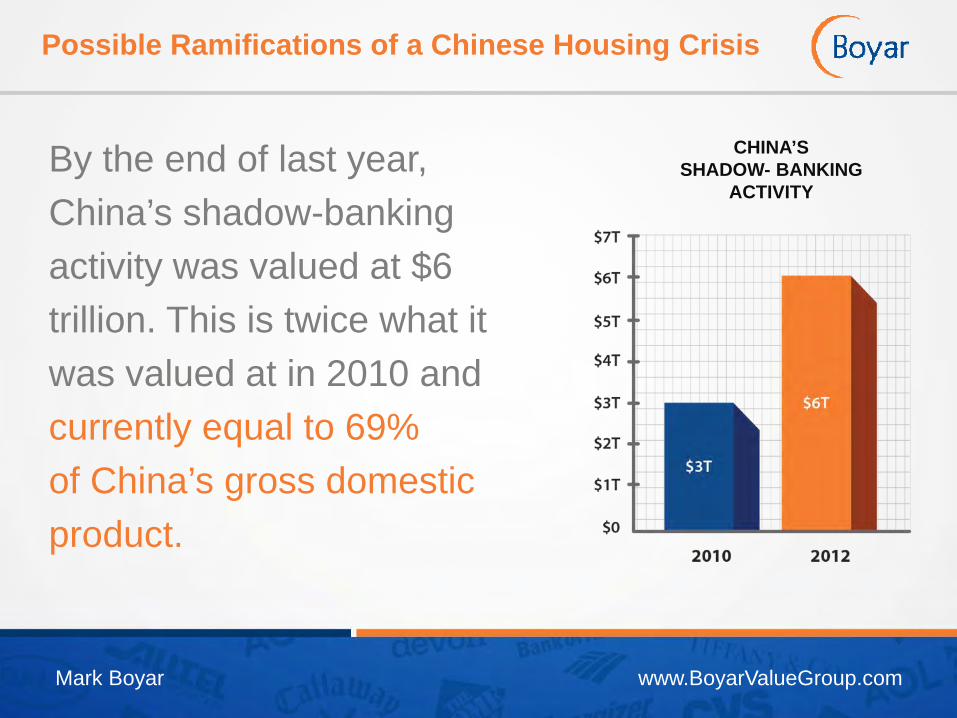

CHINA’S SHADOW- BANKING

ACTIVITYBy the end of last year, China’s shadow-banking activity was valued at $6 trillion. This is twice what it was valued at in 2010 and currently equal to 69% of China’s gross domestic product.

Possible Ramifications of a Chinese Housing Crisis

Mark Boyar www.BoyarValueGroup.com

A House of Cards?

Ultimately who is responsible for the loan is not always clear, and that’s where everyone starts getting nervous.

If a wealth-management product ultimately fails causing bank customers to suffer losses, it could create a house of cards.

Think subprime on steroids.

Mark Boyar www.BoyarValueGroup.com

Madison Square Garden Inc.(Show us the Money)

Mark Boyar www.BoyarValueGroup.com

Madison Square Garden Inc.

Madison Square Garden was initially probed in the March 2010 issue of Asset Analysis Focus.

The stock price at the time of publication was $21.91 which represented/offered 112% upside to our estimate of intrinsic or private market value.

Mark Boyar www.BoyarValueGroup.com

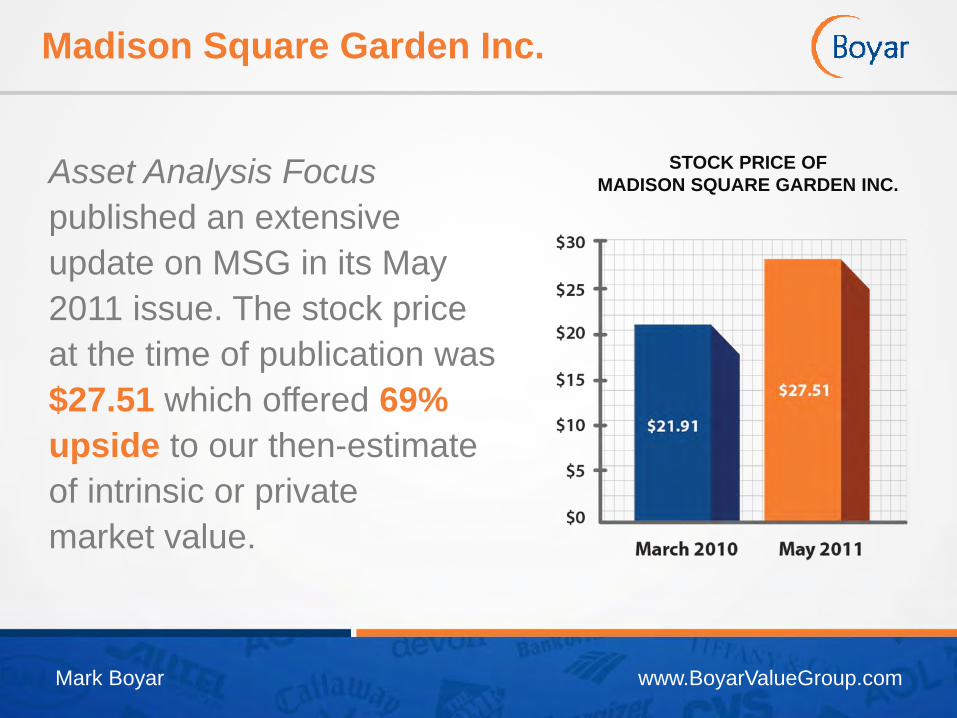

Madison Square Garden Inc.

Asset Analysis Focus published an extensive update on MSG in its May 2011 issue. The stock price at the time of publication was $27.51 which offered 69% upside to our then-estimate of intrinsic or private market value.

STOCK PRICE OF MADISON SQUARE GARDEN INC.

Mark Boyar www.BoyarValueGroup.com

Investment Rationale for MSG

MSG boasts a number of trophy properties in the sports and entertainment industry including the legendary Garden arena, the NY Knicks and NY Rangers sports franchises, the MSG cable networks and Radio City Music Hall. In addition to its marquee assets, the Company owns significant air/development rights associated with the Garden arena.

Mark Boyar www.BoyarValueGroup.com

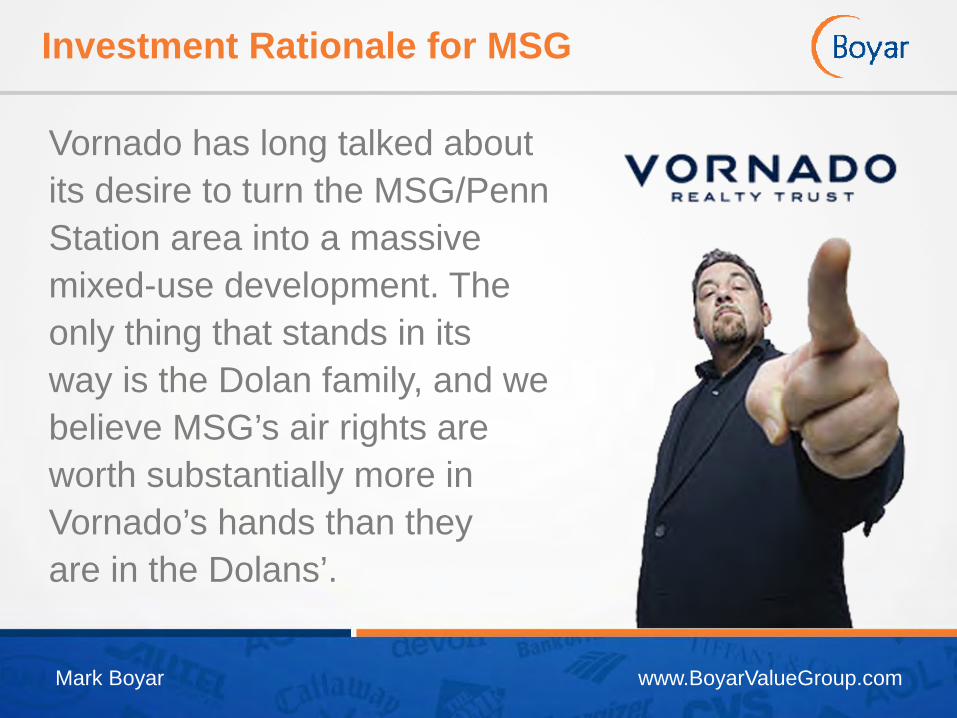

Investment Rationale for MSG

Vornado has long talked about its desire to turn the MSG/Penn Station area into a massivemixed-use development. Theonly thing that stands in itsway is the Dolan family, and webelieve MSG’s air rights areworth substantially more inVornado’s hands than they are in the Dolans’.

Mark Boyar www.BoyarValueGroup.com

Prime Real-Estate Location

Madison Square Garden (depicted as point “A” on the following map) is situated right in the middle of a collection of Vornado-owned properties. We believe this to be extremely important given that Vornadohas long held ambitious plans for development in the area.

Map Source: Mapquest.comData Source: NY Observer

330 W. 34th StreetMoynihan Station (Potential Development)One Penn PlazaTwo Penn Plaza

Hotel PennsylvaniaManhattan Mall11 Penn Plaza7 W. 34th Street

Mark Boyar www.BoyarValueGroup.com

Prime Real-Estate Location

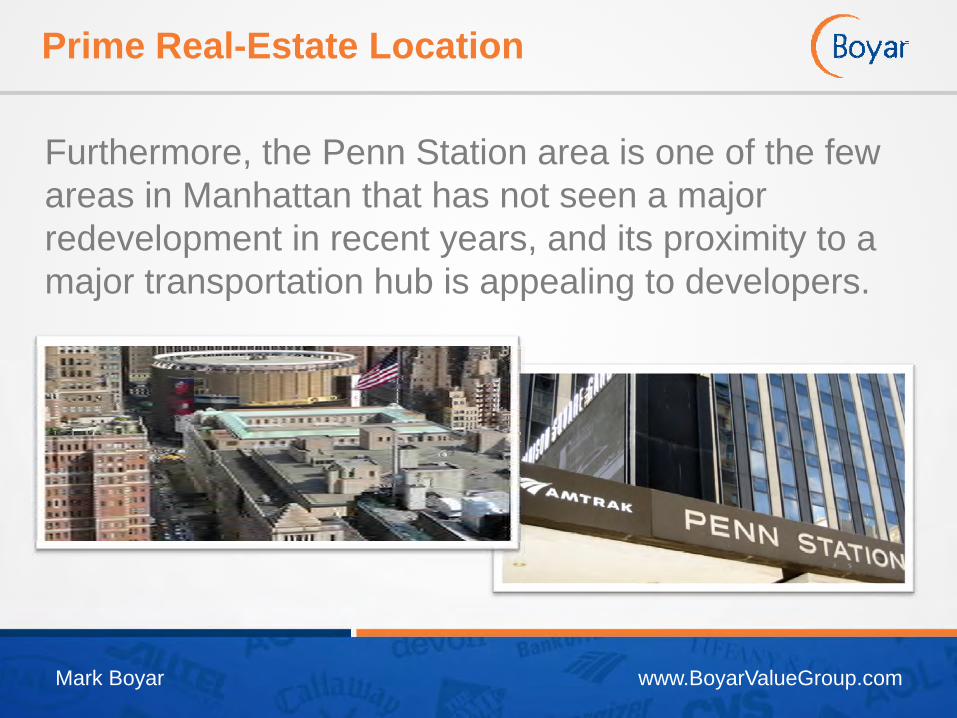

Furthermore, the Penn Station area is one of the few areas in Manhattan that has not seen a major redevelopment in recent years, and its proximity to a major transportation hub is appealing to developers.

Mark Boyar www.BoyarValueGroup.com

Prime Real-Estate Location

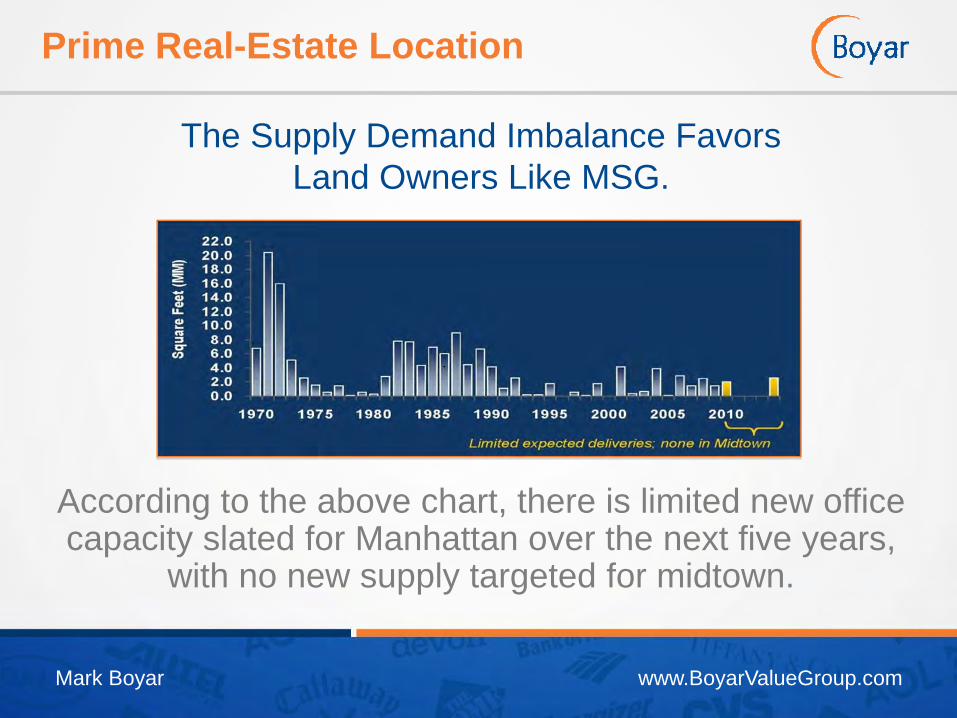

According to the above chart, there is limited new office capacity slated for Manhattan over the next five years,

with no new supply targeted for midtown.

The Supply Demand Imbalance Favors Land Owners Like MSG.

Mark Boyar www.BoyarValueGroup.com

Prime Real-Estate Location

We believe that despite the current supply/demand real estate imbalance in Manhattan, the current environment may present an opportunity for a long-term oriented (and patient) investor such as Vornado.

Mark Boyar www.BoyarValueGroup.com

Fears That MSG Will Be Forced to Move Are Unfounded

City councilwoman and former mayoral candidate Christine Quinn would like to force MSG to relocate in ten years in order to rebuild Penn Station. They are attempting to do this by refusing to issue MSG an operating permit in perpetuity.

Mark Boyar www.BoyarValueGroup.com

An actual move is highly unlikely to occur due to the tremendous tax payer cost that would be involved in transforming Penn Station, as well as the enormous compensation the government would have to pay MSG if they forced them to move.

Remember MSG does not lease the land it uses from the city, it owns it outright.

Fears That MSG Will Be Forced to Move Are Unfounded

Mark Boyar www.BoyarValueGroup.com

In early September, Madison Square Garden Co. announced it will set up an artist-management venture with former Live Nation Entertainment Inc. Chairman Irving Azoff, agreeing to pay $125 million (in addition to providing a $50 million credit line) for half of the new company. Azoff, 65, will contribute his company and be chairman and chief executive officer of Azoff MSG Entertainment LLC.

MSG is Sending Wall Street Mixed Messages

Mark Boyar www.BoyarValueGroup.com

As John Malone, whom we believe to be one of the most astute investors around, once said of Live Nation:

“You’re talking about rock musicians. This is not my kind of thing. I don’t like a business where the assets go up and down on elevators. I like them to be fixed, hung on poles or up in space going around.”

MSG is Sending Wall Street Mixed Messages

Mark Boyar www.BoyarValueGroup.com

MSG is Sending Wall Street Mixed Messages

In our opinion, MSG should not consider itself to be a growth company, and should divert the massive amount of FCF it generates back to shareholders.

Recent comments from CEO Hank Ratner include:

Mark Boyar www.BoyarValueGroup.com

MSG is Sending Wall Street Mixed Messages

“This is an exciting time for our company and, looking ahead, wefeel confident that the successful completion of these significant capital investments, along with our strong balance sheet, will leave us well positioned to pursue opportunities to drive continued growth over the long-term.”

AND…

Mark Boyar www.BoyarValueGroup.com

MSG is Sending Wall Street Mixed Messages

“Well, as we’ve been saying for a while, our priority is growing the company. Again, what we said, that isn’t necessarily mutually exclusive with a capital return, and that we had not made a decision as to whether there would or wouldn’t be any capital return, but emphasize and continue to that the priority is growing the company.”

Mark Boyar www.BoyarValueGroup.com

Ways to Unlock Shareholder Value at MSG

Investors are afraid MSG will use the company’s free cash flow on money losing acquisitions (the history of M&A at Cablevision during the Jimmy Dolan era makes their fears justified).

We believe there are many ways to unlock shareholder value:• Announce a massive share repurchase;• Sell their valuable air rights and use the proceeds to pay a special dividend;• Start paying a significant regular dividend;• Undertake a recapitalization of the company

Mark Boyar www.BoyarValueGroup.com

Cablevision Sale?

Cablevision Sale Could Provide Funding for the Dolan Family to Take MSG Private

Cablevision founder Charles F. Dolan (age 86), unlike his prominent counterpart who heads Viacom/CBS, is under no illusion (at least publicly) that he will live forever. Accordingly, we believe the elder Dolan will soon move to lock in/preserve his strong cable legacy by selling Cablevision in the not too distant future. Such a move would likely help simplify estate planning and address succession issues since we do not believe there is a Dolan heir apparent interested in running the Company’s cable business.

Mark Boyar www.BoyarValueGroup.com

Cablevision Sale?

We believe Charles’ son Jim (President/CEO of Cablevision and Chairman of MSG) is more interested in operating MSG than managing a cable business.

Mark Boyar www.BoyarValueGroup.com

Cablevision Sale?

If JD and the Straight Shot’s gig (the band in which Jim Dolan serves as the lead singer) as the opening act for the Eagles 2013 tour is not enough evidence that the affinity of the next generation of Dolans lies with the MSG entertainment/sports entity, then the July 2010 appointment of Jim Dolan’s son (Charles P. Dolan, age 23) to MSG’s board should remove any doubts.

Mark Boyar www.BoyarValueGroup.com

MSG’s Valuable Air/Development Rights

Excerpts from our March 2010 MSG Initiation Report

Given the Dolans’ history, it does not surprise us that the Company’s most valuable asset received only a cursory mention in MSG’s 248 page Form 10, which was filed with the SEC in connection with the spinoff. The following are the limited details of MSG’s air/development rights, which are buried on page 48 of that filing:

Mark Boyar www.BoyarValueGroup.com

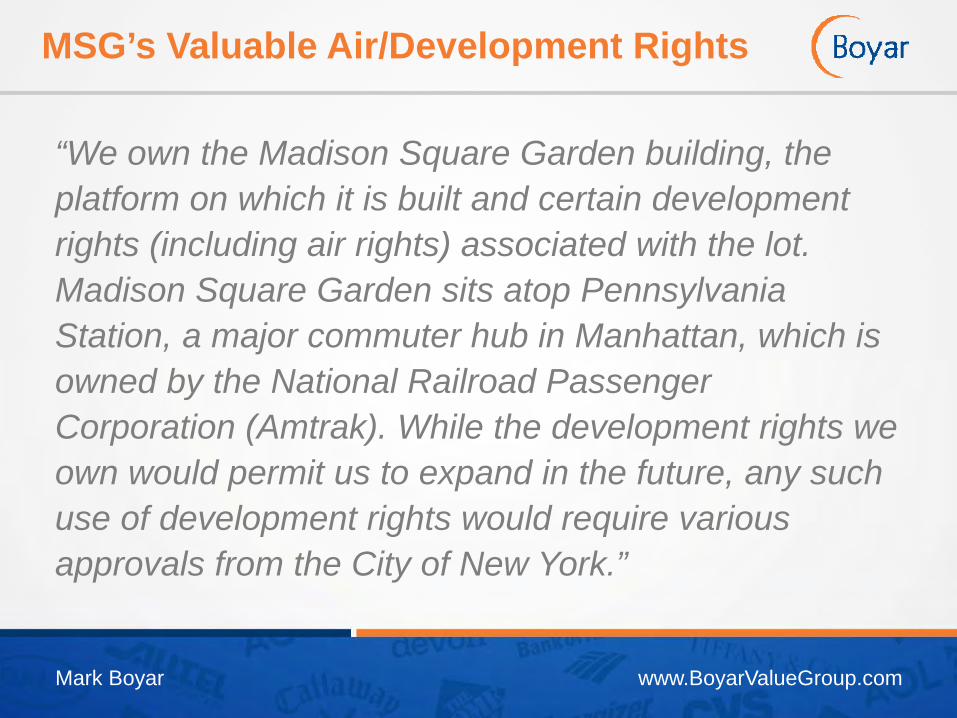

MSG’s Valuable Air/Development Rights

“We own the Madison Square Garden building, the platform on which it is built and certain development rights (including air rights) associated with the lot. Madison Square Garden sits atop Pennsylvania Station, a major commuter hub in Manhattan, which is owned by the National Railroad Passenger Corporation (Amtrak). While the development rights we own would permit us to expand in the future, any such use of development rights would require various approvals from the City of New York.”

Mark Boyar www.BoyarValueGroup.com

Investment Rationale for MSG

Absent a Dolan takeout, we believe that the wide discount (our current MSG intrinsic value estimate is 57% below recent levels) between MSG’s market and intrinsic value will sooner or later catch the attention of a potential acquirer. MSG's real-estate holdings in midtown Manhattan sit right in the middle of a collectionof properties acquired by Vornado, a prominent real estate developer.

Mark Boyar www.BoyarValueGroup.com

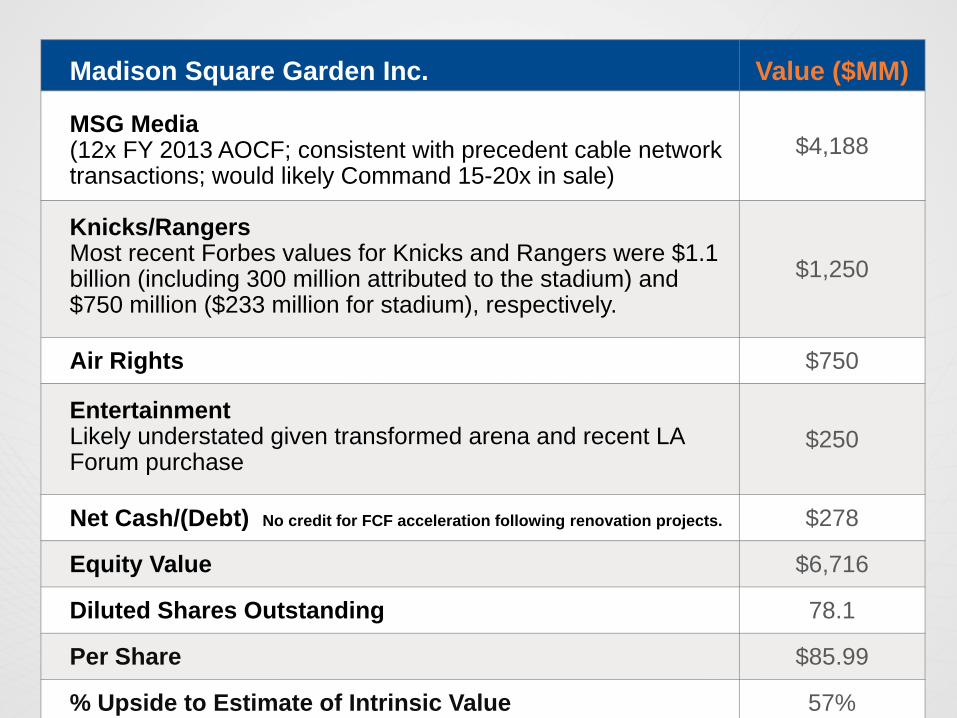

Madison Square Garden Inc. Value ($MM)

MSG Media(12x FY 2013 AOCF; consistent with precedent cable network transactions; would likely Command 15-20x in sale)

$4,188

Knicks/RangersMost recent Forbes values for Knicks and Rangers were $1.1 billion (including 300 million attributed to the stadium) and $750 million ($233 million for stadium), respectively.

$1,250

Air Rights $750

EntertainmentLikely understated given transformed arena and recent LA Forum purchase

$250

Net Cash/(Debt) No credit for FCF acceleration following renovation projects. $278

Equity Value $6,716

Diluted Shares Outstanding 78.1

Per Share $85.99

% Upside to Estimate of Intrinsic Value 57%

Mark Boyar www.BoyarValueGroup.com

Thank You!For more information, please visit:www.BoyarValueGroup.com

Boyar Value Group35 East 21st Street, Suite 8ENew York, NY 10010Telephone: (212) 995-8300Fax: (212) [email protected]

Mark Boyar www.BoyarValueGroup.com