a b a c a s u b s e c t o r - institute for social

TRANSCRIPT

Model Building for Scaling Up

Biodiversity-Friendly Enterprise Initiatives (MBS-BDFEI)

A B A C A S U B S E C T O R

ACTION RESEARCH REPORT

This report was prepared by the Institute for Social Entrepreneurship in Asia (ISEA) with support from the GEF Small Grants Programme in the Philippines (SGP-5), a programme of the Global Environment Facility (GEF), United Nations Development Programme (UNDP) and the Biodiversity Management Bureau (BMB) of the Department of Environment and Natural Resources (DENR). December 2018

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 1

T A B L E O F C O N T E N T S

TABLE OF CONTENTS 1

ACRONYMS 4

EXECUTIVE SUMMARY 8

INTRODUCTION 12

A. Background of the Subsector Action Research 12

B. Strategic/ Focus Subsector Selection Process 12

C. Rationale on the Choice of Abaca Industry as Focus for this Subsector Action Research 14

D. Subsector Action Research Scope, Methodology, and Constraints 16

Scope of the Subsector Action Research 16

Subsector Action Research Process and Methods/Tools Used 17

Research Limitations and Constraints 18

PART 1. RESULTS OF THE SUBSECTOR ACTION RESEARCH 19

A. SUBSECTOR HISTORY AND RELEVANCE 20

The Philippine Abaca Industry 20

Pre-Spanish & Spanish Colonial Period 20

American Regime 20

Post-World War II / Philippine Independence from the Americans-Present 21

The Abaca Industry of Eastern Visayas 25

The Abaca Industry of Northern Samar 27

The Abaca Industry of Mondragon, Northern Samar 29

B. SUBSECTOR DESCRIPTION AND SCOPE 32

C. Market Analysis: Market and Market Channels 37

Global Abaca Production and Market 37

National Abaca Production and Market 39

Regional Abaca Production and Market 41

Provincial (Northern Samar) & Municipal (Mondragon) Abaca Production and Market 44

CEFA as Local Abaca Fiber Trader 46

Perceived Demand & Demand Gap 47

D. Subsector Stakeholders/Participants, Functions and Technologies 49

Description of Participants in the Value Chain/Subsector 49

Cost-Benefit Analysis 54

Primary Stakeholders Analysis 57

Profile of Abaca Farmer Producers in Mondragon 57

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 2

Women Participation in the Abaca Subsector 57

E. Abaca Subsector Structure 64

F. Policy and Regulatory Environment 66

National Level 66

Local Level 69

G. Institutional Mapping of Potential Subsector Intervention Partners 71

H. State of the Natural Resource Base and Climate Change-Related Risks 79

I. Dynamics and Prospects of the Social Enterprises and Subsector Development and Growth 81

Analysis of Market Dynamics 81

Analysis of Opportunities for Social Enterprises and Identified Primary Stakeholders 83

Use of High-Yielding and Virus-Resistant (HYVR) Planting Materials 83

Better Management of Abaca Farms and Adoption of Sustainability Standards 83

Shifting from Manual/Hand Stripping to Spindled Stripping or

Decorticating Machines 85

Shifting of Channel from a Traditional Consolidator/Trader to a Developmental

Market Channel (CEFA) 86

Taking Over of Functions in the Value Chain 88

Application for Sustainability Certification 89

Opportunities for Leveraged Interventions 91

Strategic Cluster of Barangays and Municipalities 91

Development of a Multisectoral Platform for Subsector Development 93

Social Enterprise Development Focused on System Nodes 97

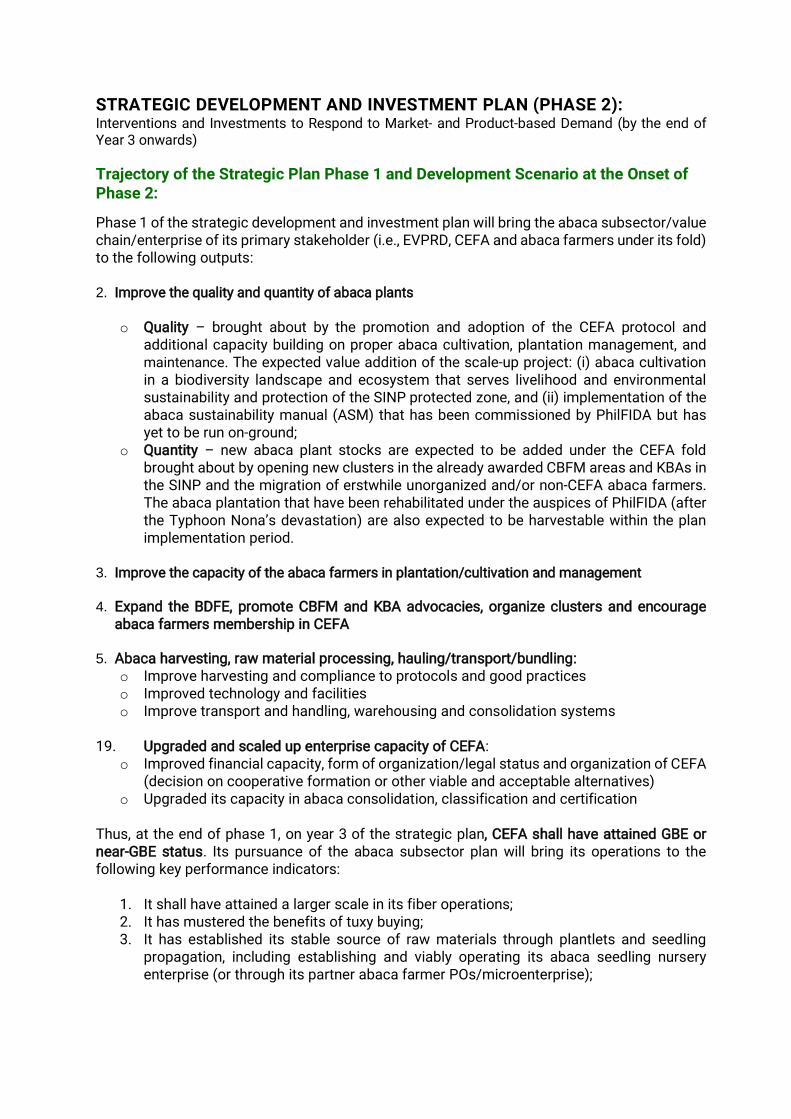

PART 2. STRATEGIC DEVELOPMENT AND INVESTMENT PLAN FOR SCALING UP ABACA BIODIVERSITY-FRIENDLY SOCIAL ENTERPRISE OF EVPRD-CEFA 113

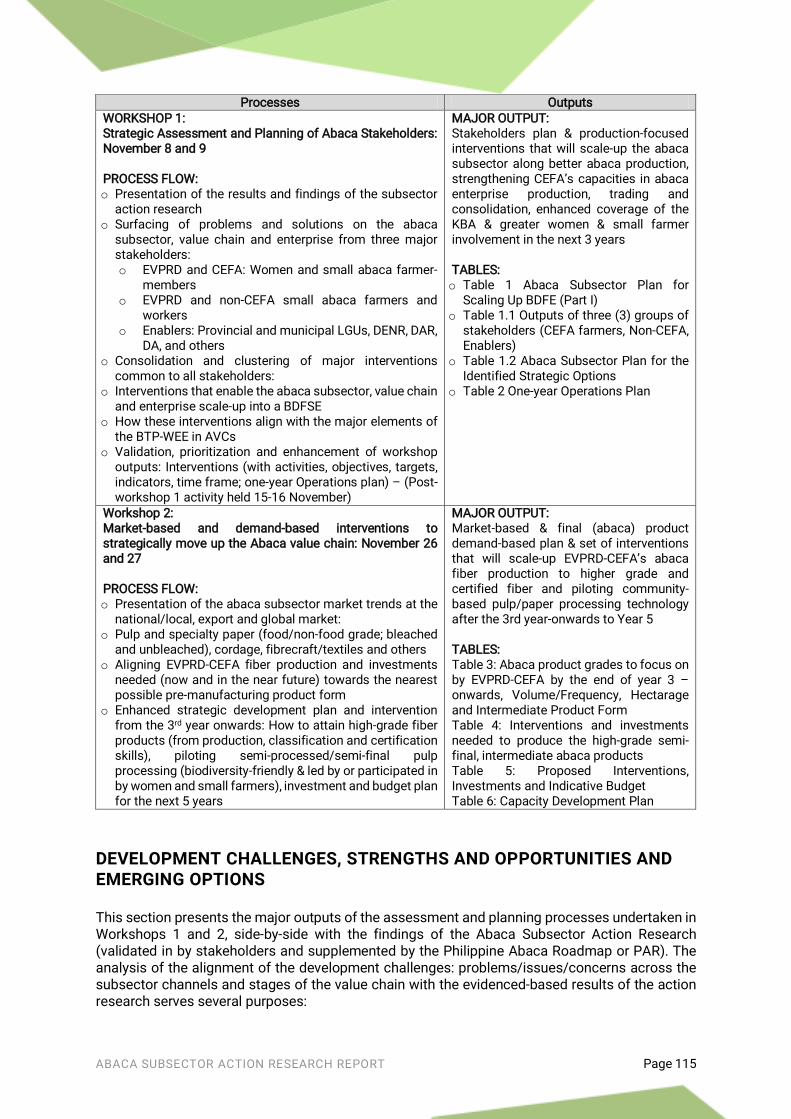

Background 114

Objectives and Scope of Discussion 114

Strategic Assessment and Planning Process 114

Development Challenges, Strengths and Opportunities and Emerging Options 115

Strategic Development and Investment Plan (Phase 1):

Stakeholders and Abaca Subsector Plan (Year 1 to 3) 121

Stakeholder-Based Interventions:

EVPRD-CEFA, EVPRD and Non-CEFA Abaca Stakeholders

and Abaca Industry Enablers 121

Production-Based Interventions:

Abaca Subsector Plan of CEFA (in partnership with EVPRD) 122

Strategic Development and Investment Plan (Phase 2): 139

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 3

Trajectory of the Strategic Plan Phase 1 and Development Scenario

at the Onset of Phase 2: 139

Location in the Value Chain 140

Abaca Market and Final Product Demand 140

Imperatives to Move Up the Value Chain, Produce Intermediate Abaca Products

and Attain Major Player Status at the Community Level 141

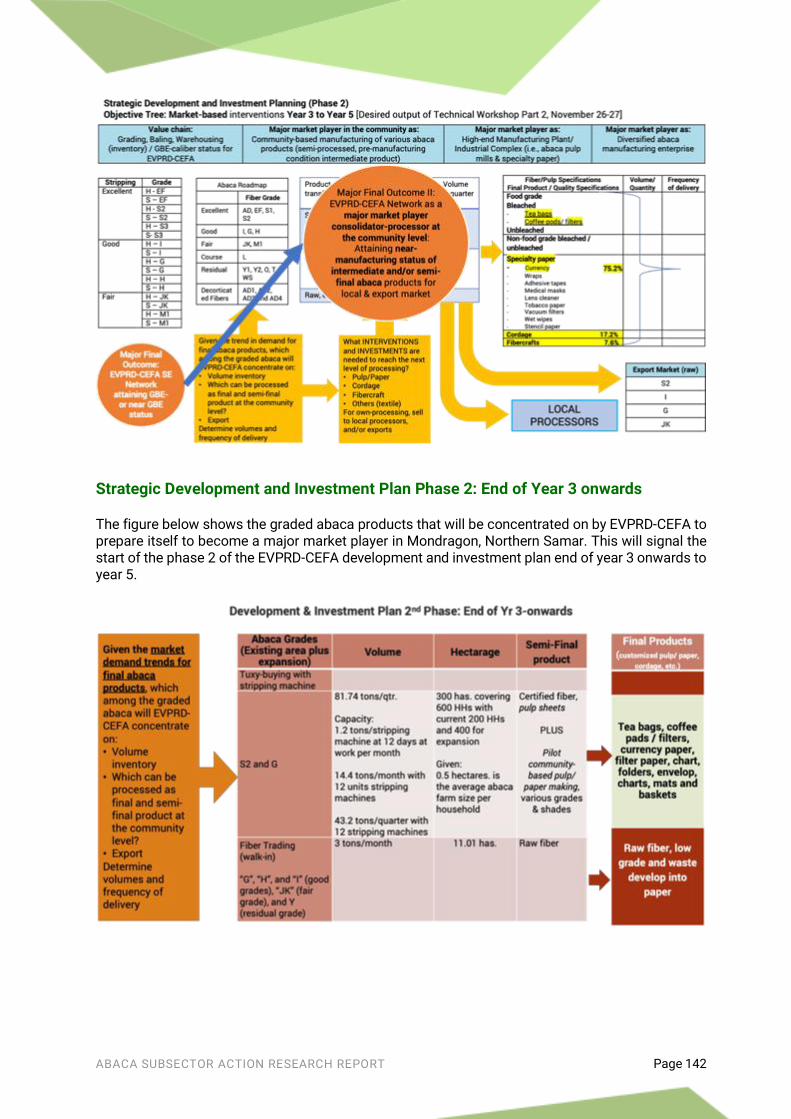

Strategic Development and Investment Plan Phase 2: End of Year 3 onwards 142

Phase II Investments and Interventions Pre-positioned at Year 1 143

Investment and Budget for Year 1-2 (Utilization of the UNDP-GEF SGP5 Grant) 144

Strategic Development and Investment Plan: 145

PART 3. STRATEGIC DEVELOPMENT AND INVESTMENT PLAN FOR SCALING UP ABACA

BDFSE OF EVPRD-CEFA 147

Strategic Plan for Scaling Up the Abaca BDFSE of EVPRD-CEFA 148

Program Description 148

Desired Abaca Subsector Map in the Two Plan Phases (Year 1 to Year 5) 159

Investment Plan 164

REFERENCES 169

ANNEXES 175

Annex 1. Results of Validation of Candidate BDFE Initiatives 176

Annex 2. KII Respondents 186

Annex 3. List of FGDs Conducted 188

Annex 4. Gendered Market Supply Chain and Production Flow Maps 189

Annex 5. Gendered Production Process Flow 192

THE PROJECT TEAM 195

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 4 A C R O N Y M S

4Ps Pamilyang Pilipino Pantawid Program

ABTV Abaca Bunchy-Top Virus

ACPC Agricultural Credit Policy Council

ACT Adaptive Community Transformation

ADMP Abaca Disease Management Project

AFAES Access Facilities and Enhancement Services

AFG Abaca Focal Group

AMCFP Agro-Industry Modernization Credit and Financing Program

AMSC Abaca Multi-sectoral Coalition

APCP Agrarian Production Credit Project

ARB Agrarian Reform Beneficiaries

ARBO Agrarian Reform Beneficiary Organization

ARMM Autonomous Region of Muslim Mindanao

ASL Accessible and Sustainable Lending

ASM Abaca Sustainability Manual

ATDF Abaca Techno-Demonstration Farm

BAFS Bureau of Agriculture and Fisheries Standards

BBrMV Banana Bract Mosaic Virus

BDFE Biodiversity Friendly Enterprise

BDFSE Biodiversity Friendly Social Enterprise

BMB Biodiversity Management Bureau

BPI Bureau of Plant Industries

BSP Bangko Sentral ng Pilipinas

BTP-WEE-AVCs Benchmarks for Transformational Partnerships and Women’s Economic Empowerment in Agricultural Value Chains

CALP Cooperative Agricultural Lending Program Facility

CAR Cordillera Administrative Region

CARD Center for Agriculture and Rural Development, Inc.

CARP Comprehensive Agrarian Reform Program

CBFM Community Based Forest Management

CBFMA Community Based Forest Management Agreement

CBP Currency Bank Paper

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 5

CDA Cooperative Development Authority

CEFA Centralized Farmers Association

CLOA Certificate of Land Ownership Award

CODA Cotton Development Administration

CPH Census of Population and Housing

CPMU Country Programme Management Unit

CRS Catholic Relief Services

CSO Civil Society Organization

CY Calendar Year

DA Department of Agriculture

DAR Department of Agrarian Reform

DBP Development Bank of the Philippines

DENR Department of Environment and Natural Resources

DOLE Department of Labor and Employment

DOST Department of Science and Technology

DOT Department of Tourism

DPWH Department of Public Works and Highways

DSWD Department of Social Welfare and Development

DTI Department of Trade and Industry

EO Executive Order

EVPRD Eastern Visayas Partnership for Rural Development Inc.

FAO Food and Agriculture Organization

FGD Focus Group Discussion

FIDA Fiber Industry Development Authority

FPE Foundation for the Philippine Environment

FPRDI Forest Products Research and Development Institute

GBE Grading and Baling Establishment

GEF-SGP5 Global Environment Facility - Small Grants Programme Phase 5

GFI Government Financial Institution

GMA Genetically Modified Abaca

GOCC Government-Owned and Controlled Corporation

HYVRV High Yielding and Virus Resistant Variety

ICTS Information & Communications Technology

IEC Information and Education Campaign

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 6

IPB Institute of Plant Breeding

ISEA Institute for Social Entrepreneurship in Asia

ISP Industry Strategic S&T Plan

Kalahi-CIDDS Kapit-Bisig Laban sa Kahirapan-Comprehensive and Integrated Delivery of Social Services

KII Key Informant Interview

KRA Key Result Area

LBP Land Bank of the Philippines

LCA Local Conservation Area

LGC Local Government Code

LGU Local Government Unit

MCIT Minimum Corporate Income Tax

MFI Microfinance Institution

MIT Massachusetts Institute of Technology

MOA Memorandum of Agreement

MPDC Municipal Planning and Development Coordinator

MRI Mutually Reinforcing Institution

MSMEs Micro, Small, and Medium Enterprises

MT Metric Ton

NARC National Abaca Research Center

NCR National Capital Region

NGA National Government Agency

NGO Non-Government Organization

NGP National Greening Program

NIA National Irrigation Administration

NICCEP National Industry Cluster Capacity Enhancement Program

NSIC National Seed Industry Council

P3 Pondo sa Pagbabago at Pag-Asenso

PAO Provincial Agriculture Office

PAR Philippine Abaca Roadmap

PCA Philippine Coconut Authority

PCAARRD Philippine Council for Agriculture, Aquatic, and Natural Resources

PCCAO Provincial Cooperative and Community Affairs Office

PCIP Provincial Commodity Investment Plan

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 7

PDC Provincial Development Council

PDP Philippine Development Program

PEC Personal Entrepreneurial Competency

PGENRO Provincial Government Environment and Natural Resources Office

PhilFIDA Philippine Fiber Industry Development Authority

PNS Philippine National Standards

PO People's Organization

PPDO Provincial Planning and Development Office

PPMA Philippine Paper Manufacturers Association, Inc.

PPP Public Private Partnership

PRDP Philippine Rural Development Program

PSA Philippine Statistics Authority

PSPI Pulp Specialties Phil., Inc.

PUNLA Program for Unified Lending in Agriculture

PVC Polyvinyl Chloride

RCIT Regular Corporate Income Tax

RDC Regional Development Council

S&T Science and Technology

SAN Sustainable Agriculture Network

SARED Sustainable Agribusiness and Rural Enterprise Development

SCFMF Special Credit Facility for Marginal Farmers and Fisherfolks

SEC Securities and Exchange Commission

SEI Social Enterprise Institution

SILCAB Social Infrastructure and Local Capacity Building

SINP Samar Island Natural Park

SPMI Specialty Pulp Manufacturing, Inc.

SPPI Sentro ha Pagpauswag ha Panginabuhi, Inc.

SSF Shared Service Facilities

TESDA Technical Education and Skills Development Authority

UEP University of Eastern Philippines

UNDP United Nation Development Programme

UPLB University of the Philippines Los Baños

VCA Value Chain Analysis

VSU Visayas State University

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 8

E X E C U T I V E S U M M A R Y This subsector action research (SAR) documents the study on the abaca subsector where CEFA (assisted by EVPRD) operates its biodiversity-friendly enterprise (BDFE) located within the Samar Island Natural Park (SINP) in Mondragon, Northern Samar. The results of the abaca SAR served as basis for guiding the strategic development and investment planning process to scale up the BDFE of EVPRD-CEFA along a social entrepreneurship framing. This was participated in by all the subsector and project stakeholders identified under the ISEA project “Model Building for Scaling Up BDFE Initiatives” funded by UNDP GEF-SGP5. The SAR used both primary and secondary data gathering methodologies. This covers the macro (global and national) and industry-level abaca historical past and present situation, as well as micro and local conditions at the ground level. Data and information were gathered and analyzed around the following major components: (a) socio-economic profile of the primary stakeholders (abaca farmers, women and farm workers), (b) condition of the natural resource base and state of biodiversity in area and its impact on the abaca subsector, (c) market and enterprise situation of the abaca value chain, and (d) level of support of enablers in the locality both from the public and private sector and how all these affect the development and growth of the abaca subsector and industry. The Abaca Subsector The Philippine abaca industry is centuries old. Abaca cultivation and utilization dates back to the pre- and Spanish colonial period. The Spaniards used abaca fiber to manufacture ropes for their ships that sailed between Manila and Acapulco, Mexico for the Galleon trade. The American colonial period -- the years 1900s to 1940s -- is considered to be the peak period of the Philippine abaca industry. During this period other uses of abaca fiber aside from textile and cordage were discovered. Bicol region, Samar Island, Leyte and later, Davao and the rest of Mindanao, are the main producers of abaca. Industry decline started in the mid-1940s until 1980s. Abaca fiber trading in the Philippines involved a lot of middlemen with the farmers ending up receiving only 25 to 50 percent of the buying price. Commercial use of plastic, nylon, and other synthetics for cordage has greatly reduced the market for abaca fiber and contributed to the unstable prices in the local and international market. The industry almost collapsed in the 1960s to 1980s due to low production. The development of local businesses that process abaca raw materials saved the industry from collapsing. Abaca products have diversified into pulp and specialty papers, cordage, handwoven fabrics, and fiber crafts. Abaca is also being introduced in the automobile and construction industry. Germany and other European countries, Japan, and the US are the biggest export market of Philippine abaca, particularly pulp (the product used in making paper). The bulk of abaca exports are pulp products. The Philippines still currently dominates the world market for abaca. It supplies 87.5% of the total global demand even with stiff competition from Ecuador, the growing demand of local industries, and limited abaca fiber production. Eastern Visayas was the top abaca producing region from 1993 to 2010. The province of Northern Samar is the current largest abaca producer in Eastern Visayas and the 2nd major abaca producing province in the Philippines behind Catanduanes. Abaca fiber production in Northern Samar was stable from 1990 to 1998 until it became unstable in 2006. From then it slowly increased until 2015. The peak productivity of abaca fiber production was attained in 2014 at 7,579 MT. The most recent typhoon that severely damaged abaca farms in Northern Samar was typhoon Nona in December 2015. Market The abaca industry presents several strategic advantages for the Philippines in local and international trade since it is basically a monopoly of the country for two centuries. The Philippines dominates global production, accounting for 63.23% of the total world production at 67,403 MT (FAO, 2016). The

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 9

Philippines’ closest competitor is Ecuador posting a 34.82% share. It has taken advantage of the fact that it is the leading producer of abaca in the world by dominating the export market. Presently, the country exports 87.50% of the total world abaca requirements. Abaca export trend has been unpredictable from 2010-2016. Market reports from PhilFIDA and FAO attributed the decline in overall export volume in 2012-2013 to the global weakening in demand due to the economic slowdown in major importing countries. In 2014, it increased due to the recovery of the importing countries’ economy. The export market for the abaca industry has greatly recovered after having some rough periods in 2012-2013. This trend is expected to continuously rise in the coming years. Majority of abaca fiber being produced in the Philippines is being processed locally into pulp, cordage, and various fibrecraft. The pulp sector consistently remains as the growth area of the industry. It utilized an average of 36,137 MT or 79% of the annual average local consumption from 2012-2016. The pulp millers’ utilization level is highly dependent on the demand for pulp by the specialty paper manufacturers abroad. The cordage sector consumed an average of 5,722 MT of abaca fiber or about 12% of the average fiber consumption of domestic manufacturers in 2012 -2016. Eastern Visayas is the second largest abaca producing region in the Philippines. In 2017, Northern Samar dominated the production with 57% average share of the total regional production. Twenty (20) out of the 24 municipalities of Northern Samar are producing abaca. The top producing municipalities are Las Navas, Silvino Lobos, and Mondragon, respectively. These top abaca producing municipalities are covered by the buffer zone of the SINP. CEFA members account for 4.33% of total abaca fiber production and 5.77% of total abaca planted area in Mondragon, Northern Samar. Out of the 67.50 MT average annual production of its members, CEFA can only buy 30 MT yearly with its current capitalization. Other produced not sold to CEFA are absorbed by other local traders. CEFA members represent 15% of the estimated total abaca farmers in Mondragon. It should be noted that CEFA only started trading abaca fiber in 2017. The forecast for abaca fiber demand in the next five years in the municipality will be 50 MT weekly or around 2,600 MT per year. In Eastern Visayas, the combined demand for abaca fiber by Leyte-based processors is 43,200 MT per year. There is also a 59,000 MT yearly demand deficit for abaca fiber in the Philippines according to PhilFIDA. The biggest pulp mill in the region with an estimated capacity of 36,000 MT of fiber or 12,000 MT pulp/year is only able to obtain 1,938 MT or 5.38% of its capacity. Due to extreme shortage of fiber supply, pulp mills obtain fiber from Catanduanes, Mindanao, and Ecuador to maximize operating costs. Subsector Stakeholders, Participants, Functions and Technologies There are five major stakeholders/participants that are involved in the abaca industry in Mondragon, Northern Samar:

1. Abaca Farmers which includes: (a) Women and men members of CEFA who are involved in the organized production and marketing of abaca fiber initiated by EVPRD and CEFA (200 active abaca farming household members), and (b) Other Abaca Farmers of Mondragon who are non-CEFA members (estimated at 1,106 active producers);

2. Abaca farm workers within Mondragon who are also abaca farmers that offer their services in exchange for immediate cash income. Usually, abaca farmers within a community/barangay work together among themselves;

3. Consolidators are local residents/abaca farmers who are involved in consolidating abaca fibers from farmers within a barangay or cluster of barangays;

4. Local Traders - There are six licensed abaca local traders in Mondragon. CEFA is included in this list. The primary functions of these local traders are: (a) buying and consolidating abaca fibers from farmers and consolidators from different barangays and even from other municipalities, and (b) selling these fibers to GBEs, trader-exporter, and processors;

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 10

5. Buyers (GBEs, Trader-Exporter, Processors) - The abaca fiber buyers in Northern Samar are S.C. Tan Export Corporation (Catarman-based GBE), Ching Bee Trading Corporation (a trader-exporter), SPMI (a GBE and processor which is a sister company of Ching Bee), and PSPI (a processor).

Women participate in all aspects of abaca fiber production except bundling of dried abaca fibers. Overall, women are involved in 84% of abaca production activities and 32.5% of marketing activities. Factors affecting economic benefits of abaca farmers are: (a) constraints in production (risk of typhoon damage, pests and diseases, poor cultivation practices, etc.), (b) constraints in marketing (market and pricing information, fiber classification and grading, etc.), and (c) constraints in value adding and processing (access to technology and equipment). Abaca Subsector Structure (Policy Environment, Mapping of Interventions and State of the Environment and other Risks) Market Channels. There are three existing market channels of abaca fiber in Mondragon, Northern Samar. Channels 1 (Farmer – Local Consolidators – Traditional Local traders – Buyers) & 2 (Farmer – Traditional Local Traders – Buyers) are the most dominant channels both in the past and in the present. Channel 3 is exclusive for CEFA abaca farmer members. Members of the association, at present, still go through channels 1 & 2 because CEFA cannot buy all their abaca fibers. Policy and Regulatory Environment. PhilFIDA is an attached agency of the DA which is mandated to promote the growth and development of the natural fiber industry through research and development, production support, fiber processing and utilization, standards implementation, and trade regulation. It is tasked with abaca trade regulatory services such as: (a) Licensing services to abaca fiber industry, (b) Fiber inspection and enforcement of grading standards, (c) Certification of abaca farms and farmers in terms of sustainability and good agricultural practices for the enhancement of cultural practices. It is undeniable that PhilFIDA plays a significant role in the development of the abaca industry in Northern Samar. However, the agency faces numerous constraints. Other agencies that are considered enablers of the industry are: DTI, DOST, DENR, DAR and local agencies such as: Abaca Multi-Sectoral Coalition, DENR-Provincial, Provincial LGU (PGENRO, PAO), CEFA, EVPRD, UEP, TESDA, DSWD, DPWH, NIA, GFIs (LBP and DBP), NGOs and the Private Sector. Natural Resource Base. The present BDFE site is being covered by a CBFMA that is awarded to the CEFA. The area is around 1,050 hectares of forestland nestled within Mondragon and is within the buffer zone of the bigger key biodiversity area—the SINP. EVPRD and CEFA believes that effective management of these areas would serve as a strong “biodiversity fence” that will shield the SINP protected areas from further encroachment and degradation. Dynamics and Prospects of SE Development and Growth Abaca farmers can get higher benefits from abaca production and trading if they can improve their farming practices, increase recovery of abaca fiber through better stripping technologies, join an organized marketing group such as CEFA and improve the quality of their abaca fiber to get higher price. The primary stakeholders have several opportunities to explore to improve and scale up their position or the benefits derived from the subsector. These are: (a) Use of high-yielding and virus-resistant planting materials compatible with the biodiversity parameters, (b) Better management of abaca farms and adoption of sustainability standards (CEFA protocol), (c) Shifting from manual/hand stripping to spindled stripping or decorticating machines, (d) Shifting of channel from a traditional consolidator/trader to a developmental market channel (CEFA), (e) Taking over of functions in the value chain, and (f) Application for sustainability certification.

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 11

Opportunities for Leveraged Interventions and Desired Subsector Map Building on the strengths of the primary stakeholders and their enablers, the following are the identified leveraged interventions:

a) Strategic cluster of barangays and municipalities radiating around the CEFA-influenced areas and abaca farmers;

b) Development of a multisectoral platform for subsector development – basically reviving the initiative of the PLGU on the abaca multisectoral and inter-agency oversight body;

c) Social enterprise development - strengthening CEFA, explore possibility of forming a cooperative structure of CEFA, and establishing abaca-related SEs and new product lines (tuxy, nursery, other value adding products, fabrication/trading of women-friendly stripping device);

d) TESDA accreditation as a skills training center, and e) Accreditation as agro-ecotourism site.

Through the several scaling up interventions already presented, CEFA shall be transformed, from being a mere fair trade and BDFE initiative, into a GBE or Class A trader social enterprise that is taking over several functions from planting stocks production to marketing. The abaca farmer producers shall have ample time to concentrate in farm establishment and maintenance, and in taking part in CEFA’s value adding activities such as fiber craft production as result of the association’s expanded functions.

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 12

I N T R O D U C T I O N

A. BACKGROUND OF THE SUBSECTOR ACTION RESEARCH The Institute for Social Entrepreneurship in Asia (ISEA) partnered with the United Nations Development Programme (UNDP) and the Biodiversity Management Bureau (BMB) of the Philippines’ Department of Environment and Natural Resources (DENR) to implement a project entitled: “Model Building for Scaling Up BDFE Initiatives” from July 1, 2018-December 15, 2018 under the UNDP’s Global Environment Facility-Small Grants Programme 5th Operational Phase (GEF-SGP5). BDFE stands for Biodiversity Friendly Enterprise. SGP5 has supported 35 projects with BDFE components in Palawan, Samar Island, and the Sierra Madre Mountain Range. Most of these BDFEs are being implemented by Non-Government Organizations (NGOs) and Peoples’ Organizations (POs). The project’s goal is to establish a model to scale up the outreach and depth of impact of these BDFE initiatives. The project fully supported a selected SGP5 grantee with a BDFE endeavor in scaling up its initiative by engaging its stakeholders in a strategic and investment planning process. It included the development of a one-year implementation plan that qualified the relevant BDFE stakeholders to receive a start-up grant from SGP5 in support to scaling up their enterprise. All of these were done through this subsector action research. The subsector action research approach was selected as a tool for this project because it is a systems approach to the study of economic activity which helps analysts better understand the dynamics of the subsector. Its objective is to analyze all of the participants, their linkages, and influential factors in the agribusiness system in order to identify constraints and opportunities for growth. Thus, subsector action research is a powerful tool for project designers and decision makers because it clearly illustrates where change can have the most significant impact on the subsector. Aside from supporting the scaling up of a selected BDFE initiative, this subsector study also greatly contributed to the realization of other project outputs which include:

A handbook on scaling up BDFE initiatives; and A framework paper for scaling up BDFE initiatives through a social entrepreneurship framed

subsector approach which also contains an adaptation of the benchmarks for transformational partnerships and women’s economic empowerment within the context of biodiversity conservation.

B. STRATEGIC/ FOCUS SUBSECTOR SELECTION PROCESS The process of selecting a BDFE initiative to be engaged for this subsector action research was tedious. The steps undertaken are as follows: 1. ISEA together with the SGP5 Country Programme Management Unit (CPMU), the Foundation for the

Philippine Environment (FPE)-the SGP5 implementing partner, and the DENR-BMB shortlisted 10 BDFE initiatives from among the 35 SGP5 supported projects with BDFE components. The following criteria were used in shortlisting these BDFEs:

Market potential for scaling up; Significance in terms of number/critical mass of poor/marginalized households to be

potentially engaged; Start-up capacity of leadership and team; Presence of support institutions and enabling organizations; and

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 13

Strategic value of the site for model building. 2. The holders of the shortlisted BDFEs participated in a learning event on social entrepreneurship as

pathways for scaling up BDFE initiatives (another output of the project). This was held on August 14-16, 2018 at Microtel, Diliman, Quezon City, Philippines. The subsector approach as a tool for scaling up BDFEs was emphasized in this training. During the event, the BDFE holder participants assessed their readiness for scaling up through self-assessment rating using the above-mentioned criteria and other Personal Entrepreneurial Competency (PEC) assessment tools.

In photos: BDFE leaders participate in sub-sector analysis workshops

3. ISEA, SGP5-CMPU, FPE and DENR-BMB used the self-assessment ratings of the BDFE holder

participants generated during the learning event to decide which BDFE initiative to engage for this subsector action research. However, the panel was not able to unanimously select a BDFE due to the emergence of two top contending candidates-the abaca production and marketing enterprise of Eastern Visayas Partnerships for Rural Development (EVPRD) and its PO partner-the Centralized Farmers Association (CEFA), and the seaweeds production and marketing initiative of Sentro ha Pagpauswag ha Panginabuhi, Inc. (SPPI). Both of these BDFE initiatives are located in Northern Samar. These two BDFEs present unique advantages and perceived weaknesses which needed further validation (i.e. market potential for abaca, organizational capacity of SPPI).

4. ISEA’s Field Research Team conducted site validation of the top two contending BDFEs to shed light on the issues surrounding each initiative. The five criteria used during the shortlisting of BDFEs were adopted. A sixth criterion was added which is the tenure security of the BDFE resource base. The abaca production and marketing of EVPRD and CEFA was chosen as the strategic BDFE to be engaged for this subsector action research based on the findings of the Field Research Team. The summary of findings during the validation is attached as Annex 1.

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 14

Top: (L) Bryan de Guia, a seaweed farmer and barangay consolidator of dried seaweeds in San Pedro, Biri, shows a row of harvestable seaweeds. (R) Merlinda P. Calubaquib (wearing black pants), ISEA’s Field Research Team Leader, visits SPPI’s office in Catarman to meet with the BOT and staff. Bottom: (L) ISEA Field Team interviews EVPRD Management Staff & Trustees, and CEFA Chairman at EVPRD’s Office in Catarman, Northern Samar. (R) CEFA’s Spindle Machine provided by buyer Ching Bee Trading.

C. RATIONALE ON THE CHOICE OF ABACA INDUSTRY AS FOCUS

FOR THIS SUBSECTOR ACTION RESEARCH The abaca industry was chosen as the focus of this subsector action research mainly because the selected BDFE to be supported for scaling up, which is the abaca fiber production and marketing of EVPRD and CEFA, is covered within its scope. Furthermore, the following local factors and conditions identified by the Field Research Team during the validation process greatly influenced the choice of abaca industry as focus of this subsector study.

MARKET POTENTIAL FOR SCALING UP: Abaca products have high and increasing market demand, both locally and internationally. Price of abaca fiber is stable and continuously increasing. CEFA officers and members, through Focus Group Discussion (FGD), revealed that volume of production of current producers is continuously increasing which enables the organization to complement the increasing market demand of abaca fibers. EVPRD and CEFA also expressed that they already have the capability to satisfy the volume requirement of their market/buyer. The abaca subsector has high potential for value adding with the finished products having ready market (i.e. abaca fiber to abaca twine/rope). The Philippine Fiber Industry Authority (PhilFIDA) also predicts that abaca products consumption worldwide will continue to increase due to recent developments on new industrial uses of abaca fiber.

SIGNIFICANCE IN TERMS OF NUMBER/CRITICAL MASS OF POOR/MARGINALIZED HOUSEHOLDS

TO BE POTENTIALLY ENGAGED: There are around 1,500 abaca producers in the municipality of Mondragon alone where CEFA operates as a developmental abaca fiber trader. Two hundred (200) of these farmers are members of CEFA. They are mostly located in three barangays of the

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 15

municipality, namely: Cablangan, Flormina, and Nenita. These are among the five barangays covered by the Community-Based Forest Management Agreement (CBFMA) that is awarded to CEFA. Mondragon has 24 barangays, 14 of which are abaca producing areas. CEFA estimates that at least 200 additional households spread in seven nearby barangays within and along the boundaries of its CBFM site can be actively engaged as captured producers. Moreover, approximately 1,025 farming households in other CBFM areas in Northern Samar with secured land tenure (CBFMA) can also be potentially engaged. Abaca farmers are considered poorest of the poor earning an average monthly income of Php 3,000 to 4000 pesos.

START-UP CAPACITY OF LEADERSHIP AND TEAM: EVPRD and CEFA have strong partnership

especially in their BDFE initiative which is centered on organized production and marketing of abaca fiber. This collaboration is made possible through the EVPRD’s SGP5 supported project entitled “Creating a Model on Social Fencing for SINP through Establishment of Organized Production and Marketing System for Abaca and other CBFM Produce” that was implemented from 2015 to 2017. SINP refers to the Samar Island Natural Park. The project covered the 1,050 hectares CBFM area that is managed by the CEFA. This CBFM area spans five barangays of Mondragon, Northern Samar, namely: Cablangan, Cahicsan, Flormina, Hinabangan, and Nenita. CEFA is based in Barangay Cablangan. An Abaca Techno-Demonstration Farm (ATDF) was established in this CBFM area and now serves as a platform for learning abaca production using conservation-compatible and socially acceptable farming systems, and technologies.

EVPRD and CEFA have competent/trained and adequate manpower support to sustain their social enterprise. They have management and finance unit which are necessary structures for a transparent and sustainable business operations. Moreover, EVPRD has substantial track record in project implementation since 2004. It has implemented 11 major projects (mostly in the field of agriculture and forestry) in partnership with 11 donor agencies, mostly foreign institutions. CEFA also has outstanding track record in implementing projects in partnership with various Civil Society Organizations (CSOs), Local Government Units (LGUs), and National Government Agencies (NGAs). In 2017, CEFA was recognized by the DENR of Northern Samar as ‘Best PO’ for their outstanding performance in implementing their project under the government’s National Greening Program (NGP).

EVPRD was organized in early 2003 by a group of local development workers and professionals seeking to contribute to the reduction of poverty in Northern Samar and in conserving its remaining biodiversity resources. EVPRD was formally registered with the Securities and Exchange Commission (SEC) in July 23, 2003. CEFA was formed in 2008 through the initiative of the Provincial Government Environment and Natural Resources Office (PGENRO) of Northern Samar. It was registered with the Department of Labor and Employment (DOLE). From its formation until today, the organization is involved in copra trading. It also engaged in palay trading but the venture was not sustained. In 2017, CEFA entered the abaca trade in order to contribute to increased income and improved quality of life of its farmer members. EVPRD supported the initiative through provision of technical support in terms of improving CEFA’s organizational and social enterprise management capacities and enhancing its current production and marketing practices.

PRESENCE OF SUPPORT INSTITUTIONS AND ENABLING ORGANIZATIONS: EVPRD and CEFA have

built strong linkages with various support institutions such as PhilFIDA, University of Eastern Philippines (UEP), Department of Agrarian Reform (DAR), and LGUs. Both have strong ability to mobilize external assistance and support such as technical, material inputs, policy, and equipment. For instance, CEFA has availed a truck from DAR and spindle stripping machines from Ching Bee Trading Corporation. These support institutions play critical roles in the BDFE scaling up process.

STRATEGIC VALUE OF THE SITE FOR MODEL BUILDING: The BDFE site has high potential to

influence the abaca industry in Northern Samar and the whole Samar Island. Furthermore, the BDFE site and influence areas rank high in terms of biodiversity conservation as they are located at the buffer zone of the SINP. Since the market demand of abaca is high and continuously increasing, both

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 16

locally and internationally, the BDFE has high potential for demonstrating sustainable value chain involving the primary stakeholders and the key industry players. Moreover, the BDFE has high potential for replication in other areas since abaca farming requires low capital input and simple technology. The local people also have inherent knowledge on the agronomic characteristics of abaca, its cultivation methods, as well as its soil and climatic requirements.

RESOURCE BASE SECURITY OF TENURE (PUBLIC LAND, STEWARDSHIP, ETC.): The current and

potential BDFE sites are within the buffer zone of the bigger key biodiversity area-the SINP. The BDFE holders believe that effective management of these areas (mostly covered by CBFMA) as multiple use zones would serve as a strong “biodiversity fence” that will shield the SINP protected areas from human encroachment and degradation. The EVPRD and CEFA abaca production and marketing enterprise requires farmers to comply with relevant production protocols such as:

Adoption of organized production pattern (the farmers need to pass the farm inspection being

required by EVPRD, and they should have an approved farm lay-out and production plan); Planting stocks must only be sourced within the municipality of Mondragon to prevent possible

pest and disease outbreak (e.g. bunchy top, mosaic); Producers are not allowed to open forest areas/kaingin for planting abaca; Abaca farms should only be established within the multiple use zones; Integrated farming must be practiced/adopted (i.e. intercropping of abaca with coconut,

endemic forest trees, root crops, and vegetables); and Planting of hedgerows for soil and water conservation is a must for sloping farms.

In addition to the above reasons, there are also various opportunities, prospects, and developments in the abaca industry that the Field Research Team has considered in selecting the abaca subsector as focus for the field research and BDFE model building. Foremost is that the abaca industry is expected to continue making a stronghold in both the domestic and international markets. The following information which were taken from Entrepinoy published articles strongly support this trend:

• Strong demand for abaca as a result of the expanding market for specialty papers for food packaging such as tea bags and meat casings, filter papers, non-wovens, and disposables;

• Growing demand to conserve forest resources and to protect the environment from problems posed by non-biodegradable materials, particularly plastics, contributed to the growing demand for natural fibers such as abaca;

• Due to environmental degradation, Japan, which is one of the major abaca consumers, is now replacing polyvinyl chloride (PVC) with natural fibers or materials free from chlorine;

• Development of new uses for abaca such as textile materials for the production of pinukpok or as blending material with silk, piňa or polyester in the production of high-end fabrics; and

• Growing demand for handmade paper for art media, photo frames, albums, stationery, flowers, all-purpose cards, and decorative.

D. SUBSECTOR ACTION RESEARCH SCOPE, METHODOLOGY, AND

CONSTRAINTS

SCOPE OF THE SUBSECTOR ACTION RESEARCH The scope of this subsector study is the abaca industry in Northern Samar in the Eastern Visayas Region (Region VIII) since it is where the EVPRD and CEFA operates their abaca-based BDFE initiative.

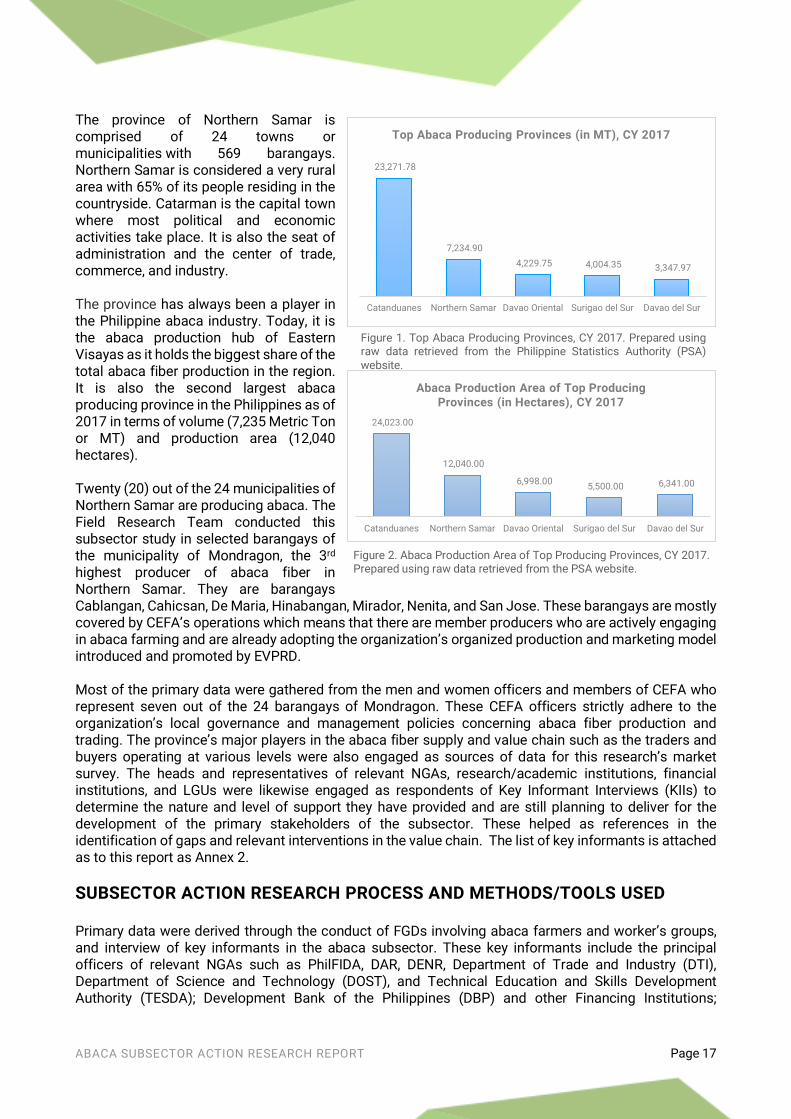

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 17

The province of Northern Samar is comprised of 24 towns or municipalities with 569 barangays. Northern Samar is considered a very rural area with 65% of its people residing in the countryside. Catarman is the capital town where most political and economic activities take place. It is also the seat of administration and the center of trade, commerce, and industry. The province has always been a player in the Philippine abaca industry. Today, it is the abaca production hub of Eastern Visayas as it holds the biggest share of the total abaca fiber production in the region. It is also the second largest abaca producing province in the Philippines as of 2017 in terms of volume (7,235 Metric Ton or MT) and production area (12,040 hectares). Twenty (20) out of the 24 municipalities of Northern Samar are producing abaca. The Field Research Team conducted this subsector study in selected barangays of the municipality of Mondragon, the 3rd highest producer of abaca fiber in Northern Samar. They are barangays Cablangan, Cahicsan, De Maria, Hinabangan, Mirador, Nenita, and San Jose. These barangays are mostly covered by CEFA’s operations which means that there are member producers who are actively engaging in abaca farming and are already adopting the organization’s organized production and marketing model introduced and promoted by EVPRD. Most of the primary data were gathered from the men and women officers and members of CEFA who represent seven out of the 24 barangays of Mondragon. These CEFA officers strictly adhere to the organization’s local governance and management policies concerning abaca fiber production and trading. The province’s major players in the abaca fiber supply and value chain such as the traders and buyers operating at various levels were also engaged as sources of data for this research’s market survey. The heads and representatives of relevant NGAs, research/academic institutions, financial institutions, and LGUs were likewise engaged as respondents of Key Informant Interviews (KIIs) to determine the nature and level of support they have provided and are still planning to deliver for the development of the primary stakeholders of the subsector. These helped as references in the identification of gaps and relevant interventions in the value chain. The list of key informants is attached as to this report as Annex 2.

SUBSECTOR ACTION RESEARCH PROCESS AND METHODS/TOOLS USED Primary data were derived through the conduct of FGDs involving abaca farmers and worker’s groups, and interview of key informants in the abaca subsector. These key informants include the principal officers of relevant NGAs such as PhilFIDA, DAR, DENR, Department of Trade and Industry (DTI), Department of Science and Technology (DOST), and Technical Education and Skills Development Authority (TESDA); Development Bank of the Philippines (DBP) and other Financing Institutions;

Figure 1. Top Abaca Producing Provinces, CY 2017. Prepared using raw data retrieved from the Philippine Statistics Authority (PSA).

23,271.78

7,234.90

4,229.75 4,004.35 3,347.97

Catanduanes Northern Samar Davao Oriental Surigao del Sur Davao del Sur

Top Abaca Producing Provinces (in MT), CY 2017

Figure 1. Top Abaca Producing Provinces, CY 2017. Prepared using raw data retrieved from the Philippine Statistics Authority (PSA) website.

Figure 2. Abaca Production Area of Top Producing Provinces, CY 2017. Prepared using raw data retrieved from the PSA website.

24,023.00

12,040.00

6,998.00 5,500.00 6,341.00

Catanduanes Northern Samar Davao Oriental Surigao del Sur Davao del Sur

Abaca Production Area of Top Producing Provinces (in Hectares), CY 2017

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 18

provincial and municipal LGU offices; and academic institutions such as the UEP that are involved in the development of the subsector. Key actors of the subsector’s market supply chain such as local traders and barangay middlemen were also interviewed. The Field Research Team also secured secondary data from official reports and publications of concerned NGAs, LGUs, academic and research institutions, and some NGOs with development programs related to the subsector to enrich the primary data gathered. Internet research was also performed to supplement the gathered primary and secondary data. Research tools especially for gendered mapping, market surveys, and guide questions for the various FGD topics and KIIs were developed. These tools ensured substantial data acquisition and orderly conduct of this subsector action research.

RESEARCH LIMITATIONS AND CONSTRAINTS This subsector action research is principally aimed on establishing a model to scale up the outreach and depth of impact of BDFEs so that the primary stakeholders are able to optimize their economic benefits. The abaca subsector in Northern Samar was selected as sample for this model building. This study focused on the following specific objectives:

• Establishing data that reflects the production or supply of abaca fiber for the last five years and in the next five years within the study area;

• Determining the market demand for abaca fiber for the last five years and in the next five years; • Defining the current abaca fiber market characteristics by plotting out the current market/value

chain, establishing gendered-market map, and delineating the enabling and disabling factors; • Establishing the viability of abaca subsector by determining what other products, processed or

semi-processed, that rural communities can develop aside from abaca fiber; • Determining the current producers and potential producers/adopters of abaca production in the

municipality of Mondragon and in the province of Northern Samar that can be engaged as primary stakeholders for the BDFE scaling up initiatives;

• Identifying the development constraints that impede the primary stakeholders from obtaining the optimum benefits from the subsector;

• Drawing out issues/constraints, opportunities, strategies/intervention, and potential recommendations to facilitate scaling up of the subsector and the benefits derived by the relevant primary stakeholders from the subsector;

• Identifying investment opportunities to facilitate the growth of the subsector as basis for a subsector development investment plan; and

• Developing a one-year plan of operations as initial step for the scaling up process. The Field Research Team encountered the following constraints in the conduct of this subsector action research:

• Absence of established social enterprises or institutions in Northern Samar that process or do value-adding works on abaca fiber despite the wealth of abaca production in the province. This constrained the team from gathering primary data on this aspect of the subsector.

• Inconsistencies and conflicting data base of PSA and PhilFIDA on important research data such as annual production area and the annual production volume of abaca fiber, among others, that made data presentation and analysis difficult.

• Hectic schedules of appropriate key informants especially the heads or point persons of NGAs and LGU offices which necessitated persistent follow ups and return visits by the research team members.

PART 1. RESULTS OF THE SUBSECTOR

ACTION RESEARCH

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 20

A. SUBSECTOR HISTORY AND RELEVANCE

THE PHILIPPINE ABACA INDUSTRY

Pre-Spanish & Spanish Colonial Period The Philippine abaca industry exists because of abaca-a Philippine native plant that is similar to banana. Abaca fiber, the raw material for abaca products, is extracted from the abaca plant. It is categorized as hard fiber because of its rough and hard external appearance. The Philippine abaca industry is centuries old. Abaca has been widely cultivated and utilized by the inhabitants of our islands for textiles before the Spanish occupation. Antonio Pigafetta, the Italian chronicler of Ferdinand Magellan’s voyage, recorded in 1521 that the natives of our archipelago were wearing clothing made from abaca. The Spanish colonizers used abaca fiber to manufacture ropes for their ships that sailed between Manila and Acapulco, Mexico for the Galleon trade (1565-1815). Abaca fiber became an exclusive Philippine export commodity in 1825 after the American Navy discovered that it is an excellent material for marine cordage. This was made possible because in 1820, John White, an American Lieutenant of the US Navy, brought abaca fibers to the United States. In 1831, export of abaca fiber amounted to 346 MT. It became the most important cordage fiber in the world market by 1850 especially in the shipping industry because of its strength, lightness, and resistance to salt water corrosion. By 1858, abaca fiber export reached 27,500 MT, of which 67% went to the United States. Abaca fiber comprised 20% to 30% of the total value of exports from the Philippines in the latter part of the 1800s. Within the said period, the cultivation of abaca land in the Philippines increased tenfold.

American Regime Abaca fiber was the most important export item from the Philippines during the American regime. It made up 72% of the total export value in 1904. The US, UK, and Japan were the biggest importers of the commodity until World War II. In the early 1900s, progress in Philippine abaca fiber production was challenged by several issues caused primarily by defects in organization and lack of control of the industry. Dissatisfaction abounds on all sides. Abaca plantations were neglected which resulted to low product quality. Large number of export firms imposed varied fiber grading and inspection. Sellers were suspicious that they were being cheated. Manufacturers and consumers complained about poor product quality. To solve these conditions, the Philippine Legislature in 1914 passed a law known as Act No. 2380-"An Act Providing for the Inspection, Grading, and Baling of Abaca (Manila Hemp), Maguey (Cantala), Sisal, and Other Fibers." The grading of abaca was based on color, tensile strength, and cleaning. Four classes were created, namely: excellent, good, fair, and coarse. Each of these classes was subdivided into a total of 21 grades of definite description. Bicol region, Samar Island, and Leyte were the main producers of abaca fiber prior to World War I. After the war, Davao region in Mindanao became the new abaca production center after the introduction of modern plantation management by the Japanese. Abaca cultivation in Davao region was started by retired US soldiers and was later taken over by Japanese immigrants who first came to work as farm laborers in the abaca plantations starting in 1903. By 1930 the Japanese came to own 75,070 hectares of abaca land. After 1938, the abaca fiber production in Davao region, most of which were produced by the Japanese, accounted for more than half of all abaca fiber production in the Philippines.

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 21

High market demand for abaca fiber led to the introduction of the abaca plant in Sumatra by the Dutch (1925); in Panama, Costa Rica, Honduras, and Guatemala by the US Department of Agriculture (1929); in North Borneo (now Sabah) by the British (1930); and in Ecuador by the Japanese (1930). During World War II, abaca production in South America greatly increased because Philippine abaca has fallen to the hands of the Japanese. The years 1900s to 1940s is considered to be the peak years of the Philippine abaca industry. It was during this period that other uses of abaca fiber aside from textile and cordage were discovered. In 1935, Fay H. Osborne, an MIT graduate and paper chemist at the Dexter Corporation in the US, produced long fiber paper out of discarded abaca ropes. This served as the precursor to the development of teabags and coffee filters after World War II. In Japan, abaca fiber found its way into the paper manufacturing and sanada weaving industry, aside from rope making. Of all the uses of imported abaca fiber, sanada weaving had the biggest impact on Japanese modern industry and local societies although its utilization share of all the Japan exported abaca fiber is only four to five percent. Sanada weaving was an industry that followed the fashion trends of the time such as hat making. The weavers tried to anticipate the fashion of the importer countries and made efforts to develop new products. Initially, a sharp competition existed between abaca fiber and Mexican sisal hemp (henequen). When sisal production started in Africa and Indonesia, it surpassed abaca in terms of production. In the 1930s, sisal production was more than double the amount of abaca fiber production. However, sisal lacked durability because it absorbed water and decayed easily. While this presented no problem for machinery rope, it was not suited for rope intended for ships, oil wells, and agriculture. Because of its light color, sisal hemp packaging twine was needed widely in places such as department stores. Sisal grew in barren tropical land and did not require much labor even on a large-scale tract of land. It was cost effective since it produced twice as much volume as abaca per hectare and it was easy to extract fiber from the sisal using machinery. The usage of sisal expanded due to improvements made in terms of breeding, cultivation technology, and water resistance (accomplished by treating it with preservatives). As result, it encroached on the demand for abaca fiber. Sisal eventually surpassed abaca except for making rope for ships and for sanada weaving, which required the best quality fiber.

Post-World War II / Philippine Independence from the Americans-Present

Industry Decline After World War II, abaca fiber trading in the Philippines involves a series of middlemen. Because of the numerous middlemen involved, the farmers end up receiving only 25 percent to 50 percent of the buying price. Commercial use of plastic, nylon, and other synthetics for cordage in the Philippines after the war has greatly reduced the market for abaca fiber and contributed to the unstable prices of the commodity in the local and international market. The Philippine abaca industry almost collapsed in the 1960s to 1980s due to low production (i.e. average of 0.60 MT per hectare in 1982), low and unstable prices of abaca fiber, poor farming practices (i.e. farmers used unidentified and low-yielding varieties which resulted in decline in production by 8,000 MT in 1982), lack of farmers’ capital, incidence of pest and diseases, occurrence of natural calamities (i.e. typhoons), and lack of production inputs and drying facilities. The major diseases of abaca were first observed as early as 1901 but it was still manageable by that time. Their rampant spread is believed to have occurred during World War II when most abaca plantations were neglected.

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 22

In the 1980s, the country's abaca product exports consisted of unmanufactured or raw fiber, cordage, cables, ropes and twines, pulp, and fiber crafts. Among these five export items, raw fiber is most valued followed by cordage, and pulp. Abaca fiber export generally declined from the 1980s to the present. The Fiber Industry Development Authority (FIDA) was created on July 27, 1981 through Executive Order (EO) 709 to promote the growth and development of the Philippine natural fibers (except cotton). On May 29, 2013, FIDA merged with the Cotton Development Administration (CODA) and became the PhilFIDA. Its mandate is to promote the growth and development of the natural fiber industry through research and development, production support, fiber processing and utilization, standards implementation, and trade regulation. The National Abaca Research Center (NARC) at the Visayas State University (VSU) in Leyte, which is mandated to help uplift the abaca industry, started its operation in 1987 with the launching of an integrated and multidisciplinary research and development program on abaca. Up to this day, NARC is one of the agencies that is actively involved in research and extension work in the industry.

Industry Resurgence The development of local businesses that process abaca raw materials in the Philippines saved the industry from collapsing. Currently, a whole range of abaca products are being produced such as specialty papers, cordage products, handwoven fabrics, and fiber crafts. Abaca is also being introduced in the automobile and construction industry. Manufactured abaca products complement Philippine abaca fiber exports, thus, keeping the industry afloat and making it one of the major contributors of foreign exchange earnings to the country's economy. The biggest exporters of Philippine abaca products, especially pulp, the product used in making paper which consists the bulk of abaca exports, are Germany and other European countries, Japan, and the US. Philippines generates an average of US$100 million from exports of abaca fiber and manufactures. In 2016, the abaca industry generated 130.3 million US dollars in foreign exchange earnings. The majority of this revenue comes from outbound shipments of abaca pulp which averaged US$63.1 million, equivalent to a 65% share of the average export earnings per year. The country’s abaca pulp exports averaged 20,382 MT from 2006 to 2015. On the average, about 49,260 MT or 76.51% of the country’s average yearly production of abaca fiber in the last ten years is consumed by domestic processors of pulp, cordage, and fibercraft. The remaining 23.49% (15,124 MT) is exported. Pulp processors account for 75% (36,945 MT) of the domestic utilization. Cordage and fibercraft manufacturers comprise 17% (8,374 MT), and 8% (3,941 MT) of the consumption, respectively.

Figure 3. Philippine Abaca Fiber Export, 1983-2013. Adapted from "Determinants of the Export Demand for Philippine Abaca Fiber", by Quilatan, Julie Ann, M., 2017, December 21, Journal of Academic Research, [S.l.], v. 2, n. 2, p. 38-51. Retrieved on October 8, 2018 from http://ojs.ssu.edu.ph/index.php/JAR/article/view/179.

-

5,000.00

10,000.00

15,000.00

20,000.00

25,000.00

30,000.00

35,000.00

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

VO

LU

ME

(M

T)

Philippine Abaca Fiber Export (1983-2013)

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 23

Trends, Opportunities, and Challenges Today, Philippines still dominates the abaca world market. It supplies 87.5% of the total world demand despite stiff competition from Ecuador, growing demand of local industries, and limited abaca fiber production. PhilFIDA reports that the current demand deficit for abaca fiber in the country is 59,000 MT yearly because of increasing local and international demand for abaca products, and low abaca fiber production. As result, local pulp mills have been importing abaca fiber and sisal from Ecuador since 1991 to plug the shortfall in local production. PhilFIDA shares that the country’s low yields was the foremost problem of the abaca industry due to use of mixed varieties, lack of disease-resistant planting materials and postharvest facilities, and fragmented research and development. The Philippine Council for Agriculture, Forestry and Natural Resources Research and Development (PCAARRD) also mentioned the use of outdated planting techniques instead of the new technologies, farmers’ lack of financial and educational capabilities, peace and order situation in some areas, and stronger typhoons as the factors hindering the development of the abaca industry. Most of these were the long-standing problems of the abaca industry five or six decades ago. In 2012, the Philippine government allotted Php 4.1 million to rehabilitate and expand abaca plantation in some provinces. The rehabilitation was led by the NARC. It included the mass production of laylay and inosa varieties as well as providing disease-resistant breeds and capability building for farmers to further establish and manage nurseries for tissue-cultured plantlets. From 2016-2017, PhilFIDA formulated the Philippine Abaca Roadmap (PAR) for 2018-2022. The roadmap sets the direction for the Philippine abaca industry for the next five years and is targeted to be implemented to meet the volume of abaca fibers needed by the domestic and international markets. Under the PAR, PhilFIDA targets to triple the average annual abaca production volume and double the current production area by 2022. Rehabilitation of existing abaca farms will also be carried out. PhilFIDA targets to concentrate the expansion of production areas in Bicol and Eastern Visayas under the PAR. Moreover, existing abaca farms in Bicol (89,558 hectares) and Eastern Visayas (19,214 hectares) are also set for rehabilitation. PhilFIDA developed an Abaca Sustainability Manual (ASM) to guide the implementation of the roadmap. An upward trajectory in prices of abaca fiber of all classification is observed in the last 27 years. This is expected to continue due to existing and renewed demand for natural fibers in the local and international market. This was buoyed by the United Nations (UN) when it declared 2009 as the UN International Year of Natural Fibres which promoted natural fiber as an environmentally friendly product. With the whole world “going green”, the art and fashion industry is recently embracing the use of abaca fiber.

72734.71

221238

180302

239666

Current Target

Philippine Abaca Roadmap Targets2018 - 2022

Yearly Production Volume (MT) Production Area (Hectares)

Figure 4. PAR Targets, 2018-2022. Prepared using raw data retrieved from PhilFIDA website.

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 24

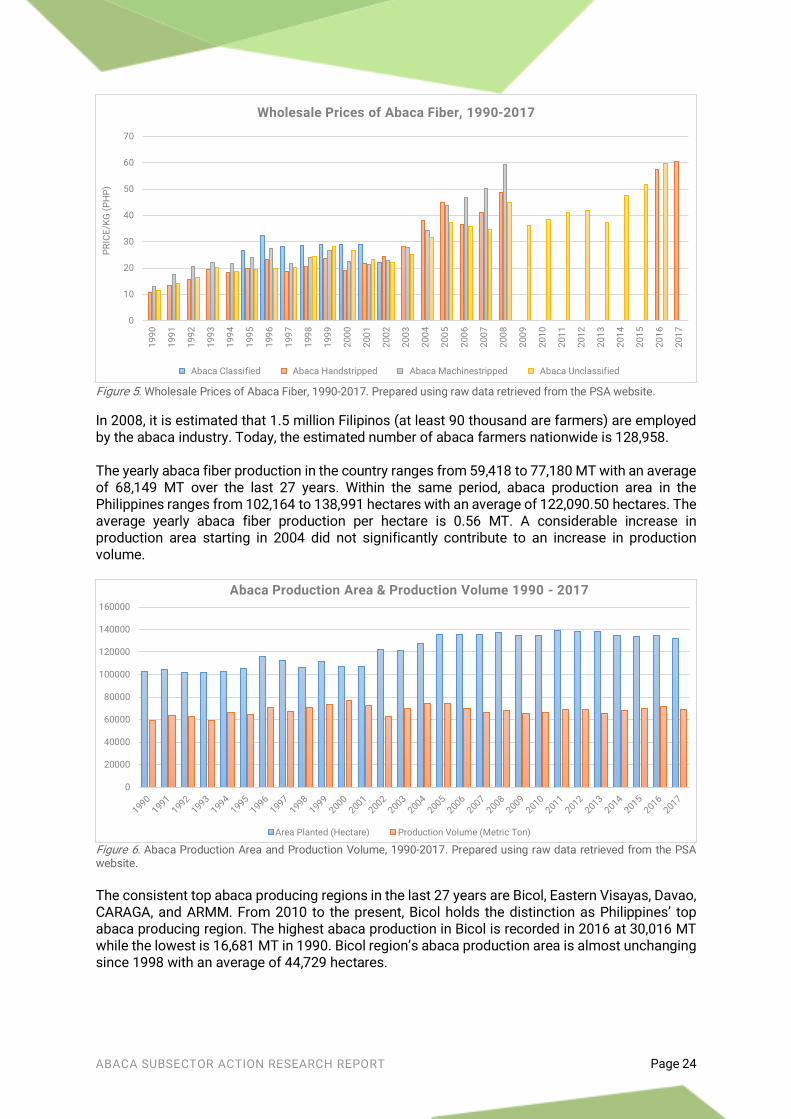

Figure 5. Wholesale Prices of Abaca Fiber, 1990-2017. Prepared using raw data retrieved from the PSA website.

In 2008, it is estimated that 1.5 million Filipinos (at least 90 thousand are farmers) are employed by the abaca industry. Today, the estimated number of abaca farmers nationwide is 128,958. The yearly abaca fiber production in the country ranges from 59,418 to 77,180 MT with an average of 68,149 MT over the last 27 years. Within the same period, abaca production area in the Philippines ranges from 102,164 to 138,991 hectares with an average of 122,090.50 hectares. The average yearly abaca fiber production per hectare is 0.56 MT. A considerable increase in production area starting in 2004 did not significantly contribute to an increase in production volume.

Figure 6. Abaca Production Area and Production Volume, 1990-2017. Prepared using raw data retrieved from the PSA website.

The consistent top abaca producing regions in the last 27 years are Bicol, Eastern Visayas, Davao, CARAGA, and ARMM. From 2010 to the present, Bicol holds the distinction as Philippines’ top abaca producing region. The highest abaca production in Bicol is recorded in 2016 at 30,016 MT while the lowest is 16,681 MT in 1990. Bicol region’s abaca production area is almost unchanging since 1998 with an average of 44,729 hectares.

0

10

20

30

40

50

60

70

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

PR

ICE

/KG

(P

HP

)Wholesale Prices of Abaca Fiber, 1990-2017

Abaca Classified Abaca Handstripped Abaca Machinestripped Abaca Unclassified

0

20000

40000

60000

80000

100000

120000

140000

160000

Abaca Production Area & Production Volume 1990 - 2017

Area Planted (Hectare) Production Volume (Metric Ton)

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 25

The Abaca Industry of Eastern Visayas Eastern Visayas was the top abaca producing region from 1993 to 2010. Abaca production in Eastern Visayas peaked at 30,174 MT in 2000 while the lowest was recorded in 2016 at 12,493 MT. Abaca production in the region started to decrease in 2005 due to disease infestation. This decline was further worsened by super typhoon Yolanda in 2013 which ravaged the area. The region exhibits considerable instability in terms of abaca production land area in the last 27 years. It recorded the largest production area in the Philippines from 2005 to 2008 before it gradually decreased until today. A steep drop-off in production area occurred in 2013 to 2014 due to damages sustained from super typhoon Yolanda. Abaca fiber production in Eastern Visayas was previously dominated by Leyte and Southern Leyte, followed by Northern Samar. However, Abaca Bunchy-Top Virus (ABTV) gravely affected abaca farms in Leyte and Southern Leyte starting in 2002. As result, 80% of abaca fiber production in said provinces was diminished. Northern Samar led the region in terms of share in abaca fiber production starting in 2011. In 2017, Eastern Visayas produced 12,671 MT of abaca fiber. Northern Samar has the highest share of the regional production at 57% followed by Southern Leyte (19%), Leyte (13%), and Western Samar (11%). Biliran and Eastern Samar accounted for 1% of the total regional abaca fiber production.

-

5,000.00

10,000.00

15,000.00

20,000.00

25,000.00

30,000.00

35,000.00

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

PR

OD

UC

TIO

N (

MT

)

Abaca Production Volume and Trend in Top Producing Regions 1990 - 2017

..BICOL REGION ..EASTERN VISAYAS ..DAVAO REGION ..CARAGA ..ARMM

Figure 7. Abaca Production Volume and Trend in Top Abaca Producing Regions, 1990-2017. Prepared using raw data retrieved from PSA website.

-

10,000.00

20,000.00

30,000.00

40,000.00

50,000.00

60,000.00

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

PR

OD

UC

TIO

N A

RE

A (

HA

)

Abaca Production Area and Trend in Top Producing Regions 1990 - 2017

..BICOL REGION ..EASTERN VISAYAS ..DAVAO REGION ..CARAGA ..ARMM

Figure 7. Abaca Production Volume and Trend in Top Abaca Producing Regions, 1990-2017. Prepared using raw data retrieved from PSA website.

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 26

Figure 9. Abaca Production Volume and Trend in Eastern Visayas, 1990-2017. Prepared using raw data retrieved from PSA website.

In 2017, Eastern Visayas had a total of 30,698 hectares of abaca-planted areas. Northern Samar had the largest share of planted areas at 39%, followed by Leyte (27%), Southern Leyte (20%), Western Samar (6%), Biliran (5%), and Eastern Samar (3%).

Figure 10. Abaca Production Area in Eastern Visayas, 1990-2017. Prepared using raw data retrieved from PSA website.

The PhilFIDA has been busy in rehabilitating calamity affected and disease infested abaca areas in the region. The agency is working closely with LGUs, CSOs, NARC, and other stakeholders in the implementation of its different programs and projects. Through its Abaca Disease Management Project (ADMP), several municipalities in the region were declared disease free. However, replanting of these disease eradicated areas can only be done after two years. A total of 3,879 hectares planted with abaca, mostly in Leyte and Southern Leyte, were covered by the ADMP from 2014 to 2016.

-

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

12,000.00

14,000.00

16,000.00

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

PR

OD

UC

TIO

N V

OL

UM

E (

MT

)Abaca Production Volume & Trend in Eastern Visayas 1990 - 2017

....Biliran ....Eastern Samar ....Leyte

....Northern Samar ....Samar (Western Samar) ....Southern Leyte

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

HE

CT

AR

ES

Abaca Production Area in Eastern Visayas 1990 - 2017

....Biliran ....Eastern Samar ....Leyte

....Northern Samar ....Samar (Western Samar) ....Southern Leyte

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 27

In 2016, only 60% or 27,816 hectares of the 46,360 hectares total abaca production area in the region were productive while 40% were rehabilitated.

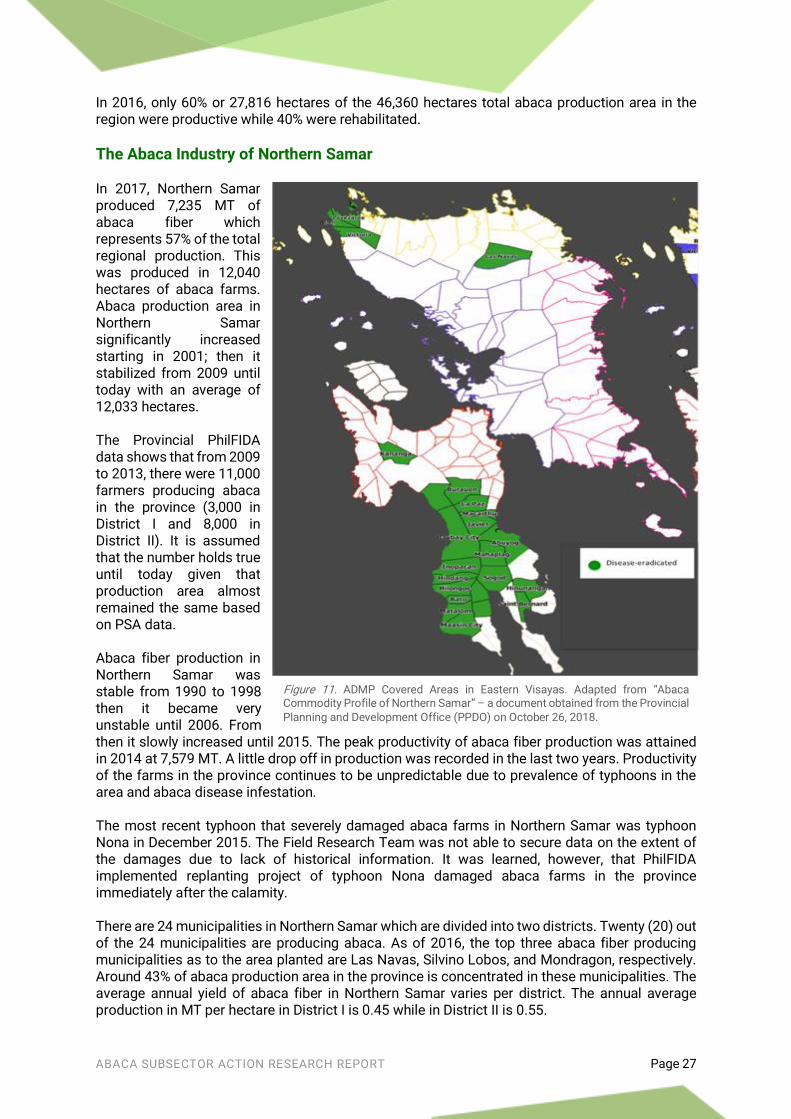

The Abaca Industry of Northern Samar In 2017, Northern Samar produced 7,235 MT of abaca fiber which represents 57% of the total regional production. This was produced in 12,040 hectares of abaca farms. Abaca production area in Northern Samar significantly increased starting in 2001; then it stabilized from 2009 until today with an average of 12,033 hectares. The Provincial PhilFIDA data shows that from 2009 to 2013, there were 11,000 farmers producing abaca in the province (3,000 in District I and 8,000 in District II). It is assumed that the number holds true until today given that production area almost remained the same based on PSA data. Abaca fiber production in Northern Samar was stable from 1990 to 1998 then it became very unstable until 2006. From then it slowly increased until 2015. The peak productivity of abaca fiber production was attained in 2014 at 7,579 MT. A little drop off in production was recorded in the last two years. Productivity of the farms in the province continues to be unpredictable due to prevalence of typhoons in the area and abaca disease infestation. The most recent typhoon that severely damaged abaca farms in Northern Samar was typhoon Nona in December 2015. The Field Research Team was not able to secure data on the extent of the damages due to lack of historical information. It was learned, however, that PhilFIDA implemented replanting project of typhoon Nona damaged abaca farms in the province immediately after the calamity. There are 24 municipalities in Northern Samar which are divided into two districts. Twenty (20) out of the 24 municipalities are producing abaca. As of 2016, the top three abaca fiber producing municipalities as to the area planted are Las Navas, Silvino Lobos, and Mondragon, respectively. Around 43% of abaca production area in the province is concentrated in these municipalities. The average annual yield of abaca fiber in Northern Samar varies per district. The annual average production in MT per hectare in District I is 0.45 while in District II is 0.55.

Figure 11. ADMP Covered Areas in Eastern Visayas. Adapted from “Abaca Commodity Profile of Northern Samar” – a document obtained from the Provincial Planning and Development Office (PPDO) on October 26, 2018.

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 28

Figure 12. Abaca Producing Municipalities in Northern Samar. Primary Data. Most of the abaca production sites in Northern Samar are located within or near watershed areas such as the Catubig Watershed and the Bantayan Watershed. They are also found within the buffer zone of the 333,300 hectares SINP-the largest contiguous tract of old growth forest in the Philippines and the country's largest terrestrial protected area. Its buffer zone is spread north to south over the island's three provinces (Eastern Samar, Northern Samar and Samar Province) and totals 458,700 hectares, about a third of the entire island of Samar. The municipalities of Catubig, Las Navas, Lope de Vega, Mondragon, and Silvino Lobos in Northern Samar are covered by the SINP buffer zone. The abaca industry in Northern Samar, as strategically located and given its continuous expansion as previously presented, can pose critical environmental consequences. Among said concerns is encroachment into key protection areas when not regulated which could spell a bane to the local environment. It could also become an advantage or boon to biodiversity conservation given proper regulation and development interventions.

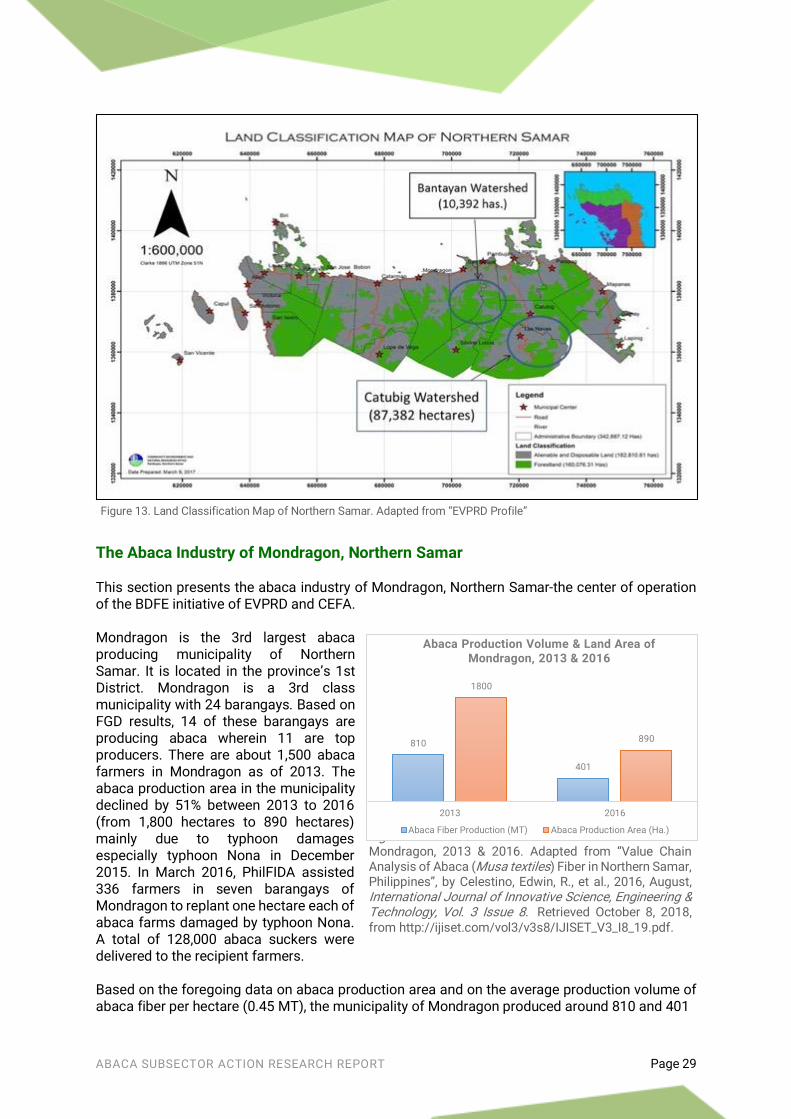

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 29

The Abaca Industry of Mondragon, Northern Samar This section presents the abaca industry of Mondragon, Northern Samar-the center of operation of the BDFE initiative of EVPRD and CEFA. Mondragon is the 3rd largest abaca producing municipality of Northern Samar. It is located in the province’s 1st District. Mondragon is a 3rd class municipality with 24 barangays. Based on FGD results, 14 of these barangays are producing abaca wherein 11 are top producers. There are about 1,500 abaca farmers in Mondragon as of 2013. The abaca production area in the municipality declined by 51% between 2013 to 2016 (from 1,800 hectares to 890 hectares) mainly due to typhoon damages especially typhoon Nona in December 2015. In March 2016, PhilFIDA assisted 336 farmers in seven barangays of Mondragon to replant one hectare each of abaca farms damaged by typhoon Nona. A total of 128,000 abaca suckers were delivered to the recipient farmers. Based on the foregoing data on abaca production area and on the average production volume of abaca fiber per hectare (0.45 MT), the municipality of Mondragon produced around 810 and 401

Figure 14. Abaca Production Volume and Land Area of Mondragon, 2013 & 2016. Adapted from “Value Chain Analysis of Abaca (Musa textiles) Fiber in Northern Samar, Philippines”, by Celestino, Edwin, R., et al., 2016, August, International Journal of Innovative Science, Engineering & Technology, Vol. 3 Issue 8. Retrieved October 8, 2018, from http://ijiset.com/vol3/v3s8/IJISET_V3_I8_19.pdf.

810

401

1800

890

2013 2016

Abaca Production Volume & Land Area of Mondragon, 2013 & 2016

Abaca Fiber Production (MT) Abaca Production Area (Ha.)

Figure 13. Land Classification Map of Northern Samar. Adapted from “EVPRD Profile”

ABACA SUBSECTOR ACTION RESEARCH REPORT Page 30

MT of abaca fiber in 2013 and 2016, respectively. There are not enough historical data on abaca fiber production volume, abaca production area, and number of abaca farmers in the municipality. Thus, trends cannot be established.