a breakfast presentation

TRANSCRIPT

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 1/51

India RisingIndia to 2020 – Tiger, Tiger Burning Bright

Dr Neil J. Bristow

Presentation at Salva’s Sydney BreakfastSydney, 7th June 2011

H & W Worldwide

+61240286268

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 2/51

Some Interesting Facts on India

Until 1896, India was the only source for diamonds to the world.

India was one of the richest countries till the time of British in the early 17thCentury.

India is among the top 5 producers in the world for food grains, pulses, poultryand first for milk.

Over the last 15 years, India has been the second fastest growing country in

the world after China, averaging above 6% growth per year.

The number system was invented by India. Aryabhatta was the scientist whoinvented the digit zero.

Indian railways is the largest employer in the world, employing over 1 million

people.

Had just 3 shopping malls in 2001, India had 100 in 2005, 345 by 2007 and~420 today.

Christopher Columbus was attracted by India's wealth and was looking for

route to India when he discovered America by mistake.

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 3/51

Plan of Presentation

1. Australia and India the Past Relationship

2. India - Drivers for Accelerated Growth

3. The Future from a Coal Perspective

4. Summary and Implications

H & W Worldwide Consulting

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 4/51

Key Takeaways

Australia and India have a strong long term relationship in coal

Australia is well endowed with a suite of met coals ideal for India current

and future needs

Australia is a proven reliable, long term supplier......unlike potential “new”

suppliers

If India’s steel and power growth takes off, Australia must be prepared to

meet strong demand growth for all coals

Emerging India investment in Australia is a sign of things to come and of abeneficial future relationship

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 5/51

Plan of Presentation

1. Australia and India the Past Relationship

2. India - Drivers for Accelerated Growth

3. The Future from a Coal Perspective

4. Summary and Implications

H & W Worldwide Consulting

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 6/51

Background to the Relationship

Why does India need Australian coal?

India has large reserves of its own coking coal₋ Some coking properties OK, but high ash content

Large iron ore reserves why not DR?

₋ Limited natural gas, DR small scale relatively inefficient

Other importers – why Australia?₋ Australia largest exporter and relatively close

But why does India need HCC rather than WCC?

₋ To carry domestic and other cheaper coals

₋ To increase coke quality as industry develops larger scale BF, steel plants

But why does India not buy large volumes of thermal coal?

₋ Major use of Indonesian thermal coal, particularly sub bituminous

₋ Going forward will need significantly more coal - Australian

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 7/51

Australia and India

Import History

Source: Australian Customs

India has become an increasingly important part of Australia’s export market; share

rising from below 6% to 10% in 2010.

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

50

100

150

200

250

300

M i l l i o n t o n n e s

India's share of Australian exports

India

Australia total

%

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 8/51

Australia and India

Import History - Hard Coking Coal

Source: Australian Customs

India’s importance in HCC is more pronounced having doubled from a 1999 low to

around 25%, and still increasing YTD 2011 - over 28% at a growth rate of ~10.5%pa

0%

5%

10%

15%

20%

25%

30%

0

20

40

60

80

100

120

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011an

m i l l i o n t o n n e s

India's share of HCC exports

India

Australia HCC

%

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 9/51

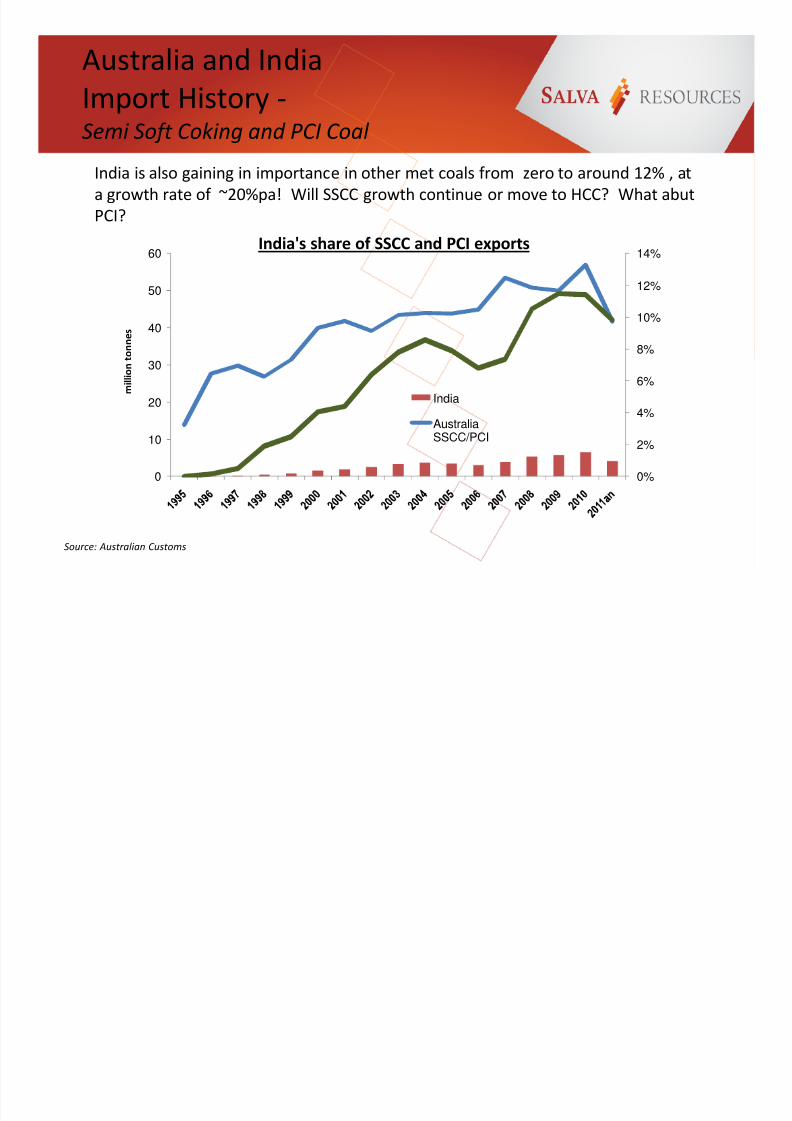

Australia and India

Import History -Semi Soft Coking and PCI Coal

Source: Australian Customs

India is also gaining in importance in other met coals from zero to around 12% , at

a growth rate of ~20%pa! Will SSCC growth continue or move to HCC? What abut

PCI?

0%

2%

4%

6%

8%

10%

12%

14%

0

10

20

30

40

50

60

m i l l i o n t o n n e s

India's share of SSCC and PCI exports

India

AustraliaSSCC/PCI

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 10/51

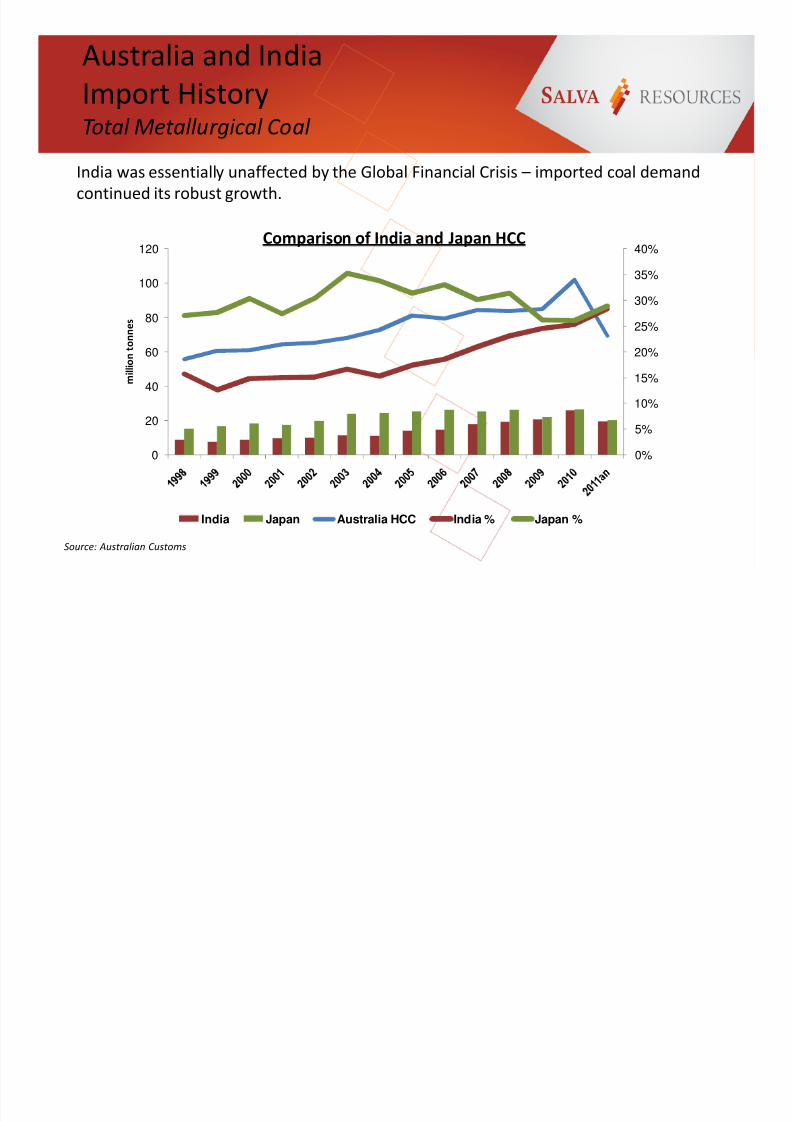

Australia and India Import

History –Total Metallurgical Coal

Source: Australian Customs

India’s importance in Australian met coal exports has grown significantly and accounts

for >20% of the total, and no 2 position. Potentially surpassing Japan in HCC imports in

2011.

0%

5%

10%

15%

20%

25%

0

20

40

60

80

100

120

140

160

180

m i l l i o n t o n n e s

India's Share of Total Met Coal Exports

India

Australia Met

%

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 11/51

Australia and India

Import HistoryTotal Metallurgical Coal

Source: Australian Customs

India was essentially unaffected by the Global Financial Crisis – imported coal demand

continued its robust growth.

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

20

40

60

80

100

120

m i l l i o n t o n n e s

Comparison of India and Japan HCC

India Japan Australia HCC India % Japan %

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 12/51

Australia and India

Import History – A Perspective

Source: Interocean, Salva

Australia is the dominant supplier of coking coal to India, with over 83% of the market;

will it be in the future?

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

T h o u s a n d s

T o n n e s

Indian Coking Coal Imports by Month

Australia China Indonesia New Zealand Russia South Africa

NA USA Vietnam Singapore Canada

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 13/51

Summary – The Past

India has gained in importance to Australia

Major HCC importer – strong rise to no 2

Growth rates suggest India soon to overtake Japan in HCC imports

No effect of the GFC - Growth continued throughout the economic

downturn

Thermal coal buying = Indonesian

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 14/51

Plan of Presentation

1. Australia and India the Past Relationship

2. India - Drivers for Accelerated Growth

3. The Future from a Coal Perspective

4. Summary and Implications

H & W Worldwide Consulting

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 15/51

Global Population Changes

Population is a major driver for increased power demand; India will surpass China by 2030 to be

the most populous country, sustaining strong growth over the next 3 decades.

IndiaIndia

Source : UN Population Prospects, 2008 revisionH & W Worldwide Consulting

0

200

400

600

800

1000

1200

1400

1600

1800

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

P o p u l a t i o n ( M i l l i o n )

Total Population Trend to 2050

ChinaChina

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 16/51

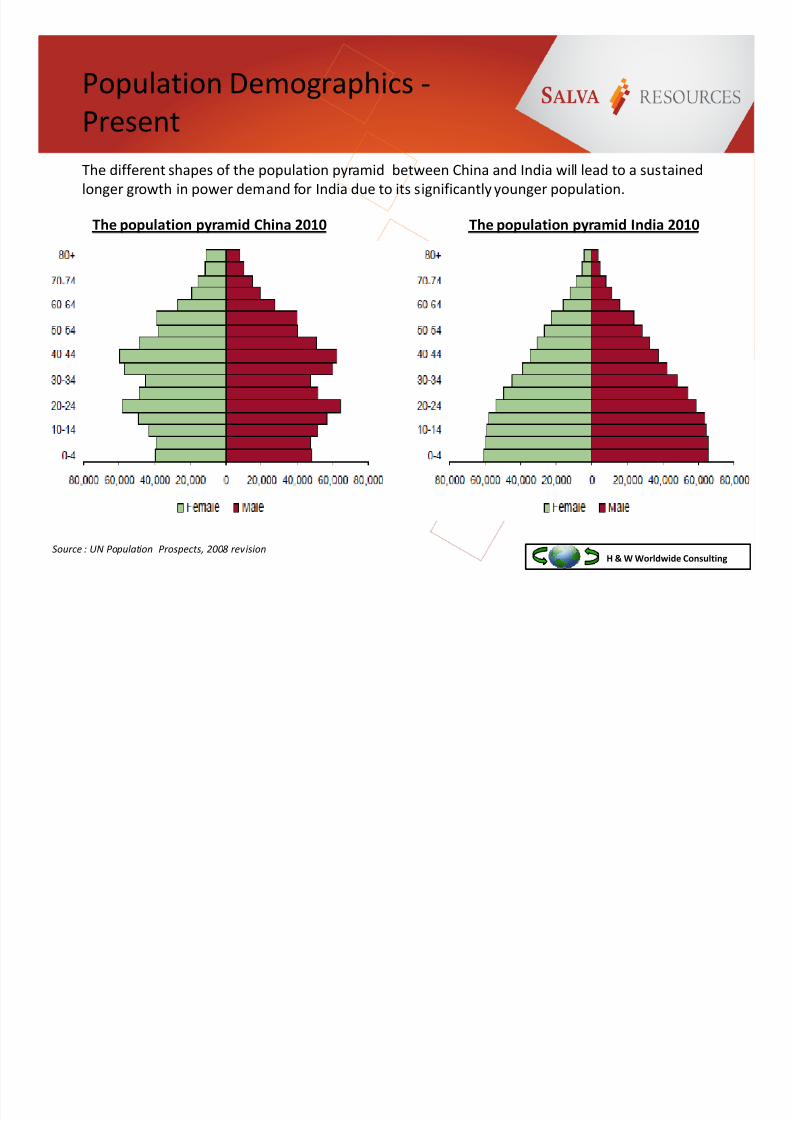

Population Demographics -

Present

The different shapes of the population pyramid between China and India will lead to a sustained

longer growth in power demand for India due to its significantly younger population.

Source : UN Population Prospects, 2008 revision

The population pyramid China 2010 The population pyramid India 2010

H & W Worldwide Consulting

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 17/51

Population demographics -

Future

The shapes of the population pyramid will remain very different as China becomes an old country

and India remains “young” with ~60% below 30 years of age.

Source : UN Population Prospects, 2008 revision

The population pyramid China 2030 The population pyramid India 2030

H & W Worldwide Consulting

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 18/51

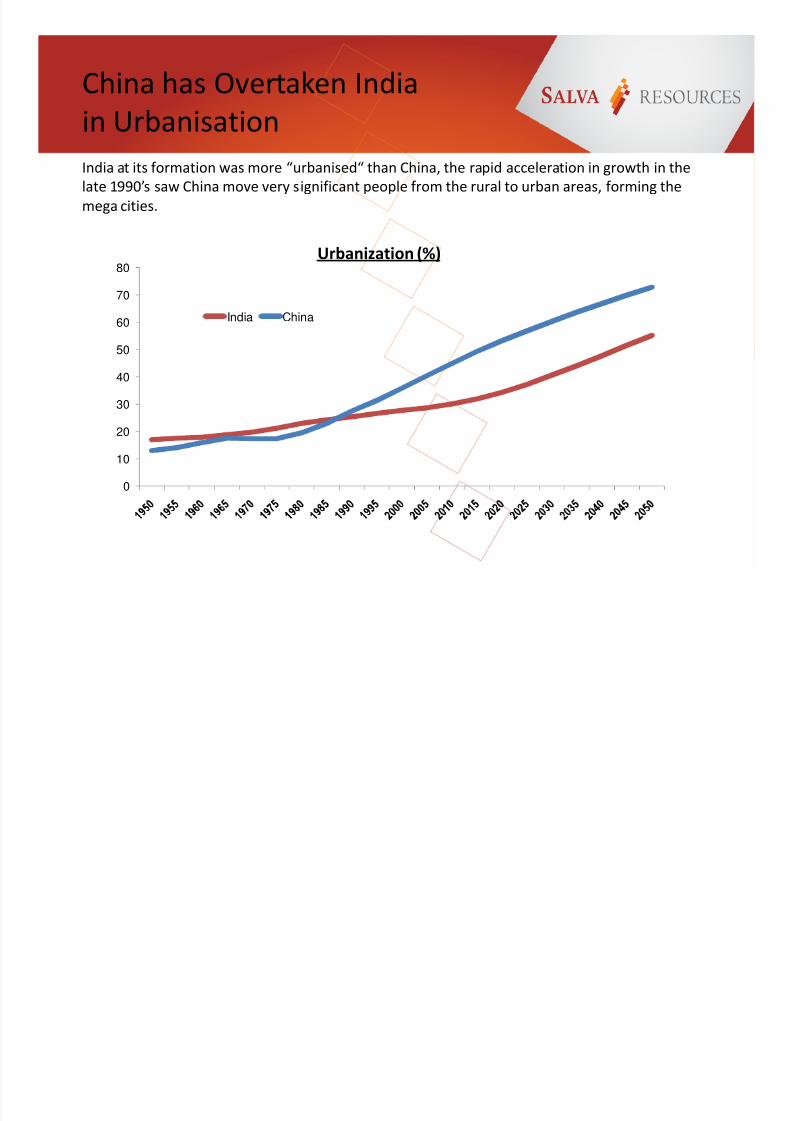

China has Overtaken India

in Urbanisation

0

10

20

30

40

50

60

70

80Urbanization (%)

India China

India at its formation was more “urbanised“ than China, the rapid acceleration in growth in the

late 1990’s saw China move very significant people from the rural to urban areas, forming the

mega cities.

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 19/51

India will Continue Strong

Urbanisation

India will urbanise a further 215 million people by 2025. Although China will exceed this total the

effect will see India adopting some of the key Chinese concepts i.e. Constructing taller buildings

which will boost steel demand.

Source : McKinsey, BHPBilliton presentation

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 20/51

India will grow at a faster

rate than China

0

2

4

6

8

10

12

14

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2005 2008 2011 2014 2017 2020

G D P g r o w t h r a t e %

G D P U S $ t r i l l i o

n s

China GDP % India GDP % China GDP (US$b) India GDP (US$b)

Forecasts

In the next 10 years Chinese economic growth will moderate and slow, as India is forecast to pick

up growth and over take China in the next couple of years.

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 21/51

GDP - Comparisons

and Differences

The GDP structures of India and China are very different: India is far more focused on services while

China is focused on manufacturing. Agriculture trends are similar although the importance to India

of the agriculture sector is far higher

Source : World Bank

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 22/51

GDP - The Importance

of Services

India has a vibrant active service sector highly competitive in the global market place, it is yet to

develop a strong manufacturing sector – recent signs show that this is underway.

Source : World Bank

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 9 6 1

1 9 6 4

1 9 6 7

1 9 7 0

1 9 7 3

1 9 7 6

1 9 7 9

1 9 8 2

1 9 8 5

1 9 8 8

1 9 9 1

1 9 9 4

1 9 9 7

2 0 0 0

2 0 0 3

2 0 0 6

2 0 0 9

Composition of GDP in India (%)

Agriculture Industry Services

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 9 6 1

1 9 6 3

1 9 6 5

1 9 6 7

1 9 6 9

1 9 7 1

1 9 7 3

1 9 7 5

1 9 7 7

1 9 7 9

1 9 8 1

1 9 8 3

1 9 8 5

1 9 8 7

1 9 8 9

1 9 9 1

1 9 9 3

1 9 9 5

1 9 9 7

1 9 9 9

2 0 0 1

2 0 0 3

2 0 0 5

2 0 0 7

2 0 0 9

Composition of GDP in China (%)

Agriculture Industry Services

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 23/51

Drivers of India’s Economy

High savings rates

Availability of low cost, skilled and semi skilled labour Technology – supporting the Service sector

Favourable demographics

Trade opening Manufacturing

– Growth in parts manufacture

– Emerging centre for small car development and manufacture

– Plans for intelligent engineering products

– Major opportunities for food processing and manufacturing

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 24/51

Is India Following China

with a lag of ~15 years?

-

20,000

40,000

60,000

80,000

100,000

120,000 FDI Flows (US$M)

China India

India has seen a pick up in FDI. Could India become the major centre replacing China by 2020?

Major boost to steel and power demand and presenting major growth in coal requirements.

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 25/51

India is showing strong signs of following the conventional development route

Exports trends to GDP continue to climb

Exports from special economic zones are following China model

Signs India is set for manufacturing and industrial take off in next 10 years

Is India that different?

No, not really.

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 26/51

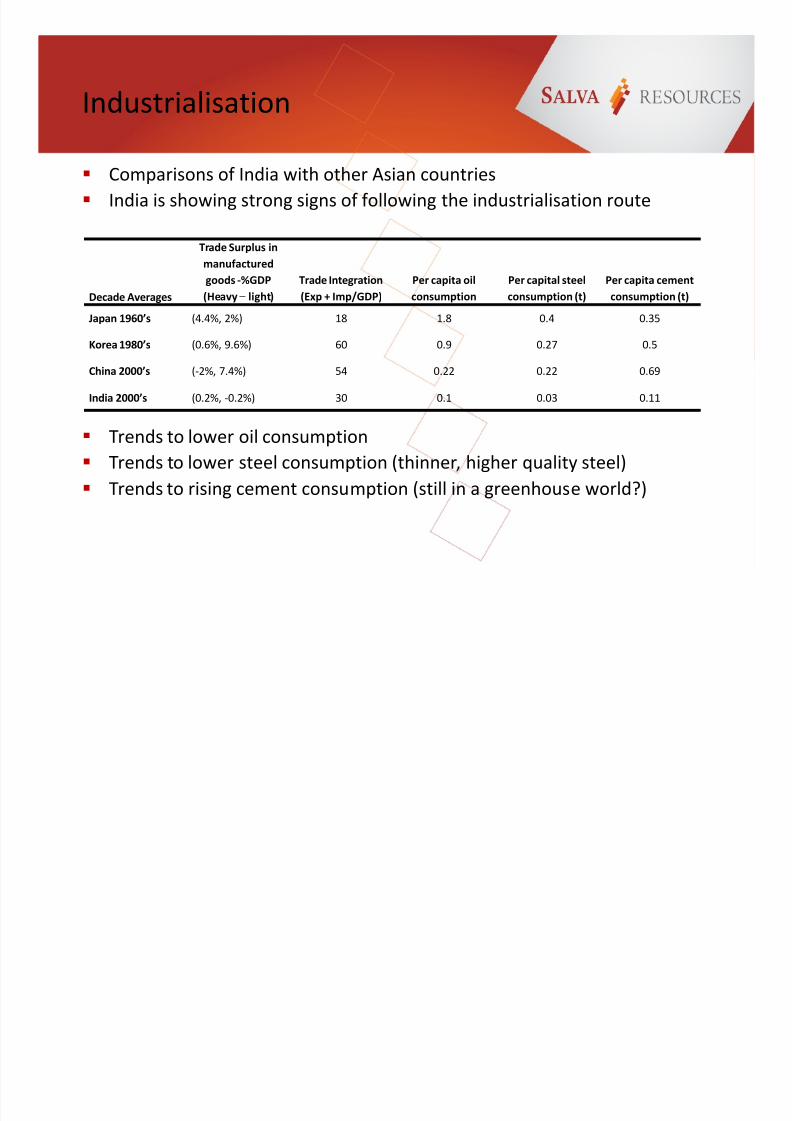

Industrialisation

Comparisons of India with other Asian countries

India is showing strong signs of following the industrialisation route

Trends to lower oil consumption Trends to lower steel consumption (thinner, higher quality steel)

Trends to rising cement consumption (still in a greenhouse world?)

Decade Averages

Trade Surplus in

manufactured

goods -%GDP

(Heavy – light)

Trade Integration

(Exp + Imp/GDP)

Per capita oil

consumption

Per capital steel

consumption (t)

Per capita cement

consumption (t)

Japan 1960’s (4.4%, 2%) 18 1.8 0.4 0.35

Korea 1980’s (0.6%, 9.6%) 60 0.9 0.27 0.5

China 2000’s (-2%, 7.4%) 54 0.22 0.22 0.69

India 2000’s (0.2%, -0.2%) 30 0.1 0.03 0.11

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 27/51

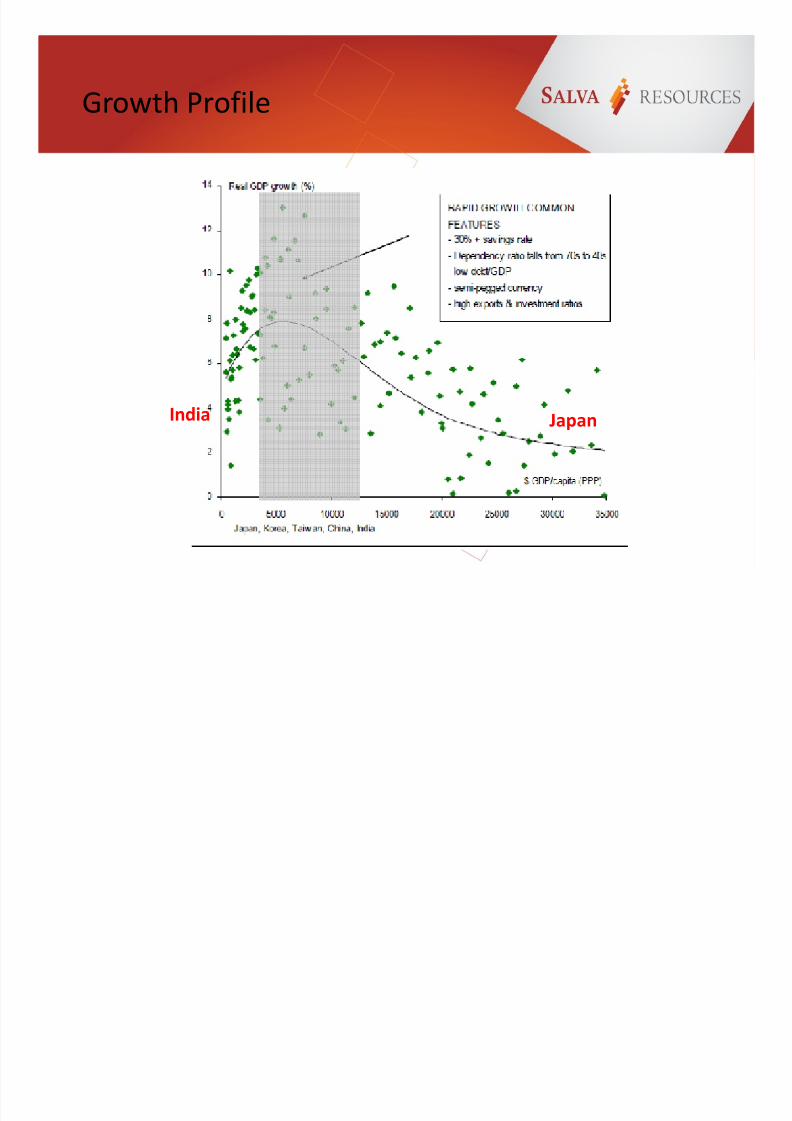

Growth Profile

JapanIndia

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 28/51

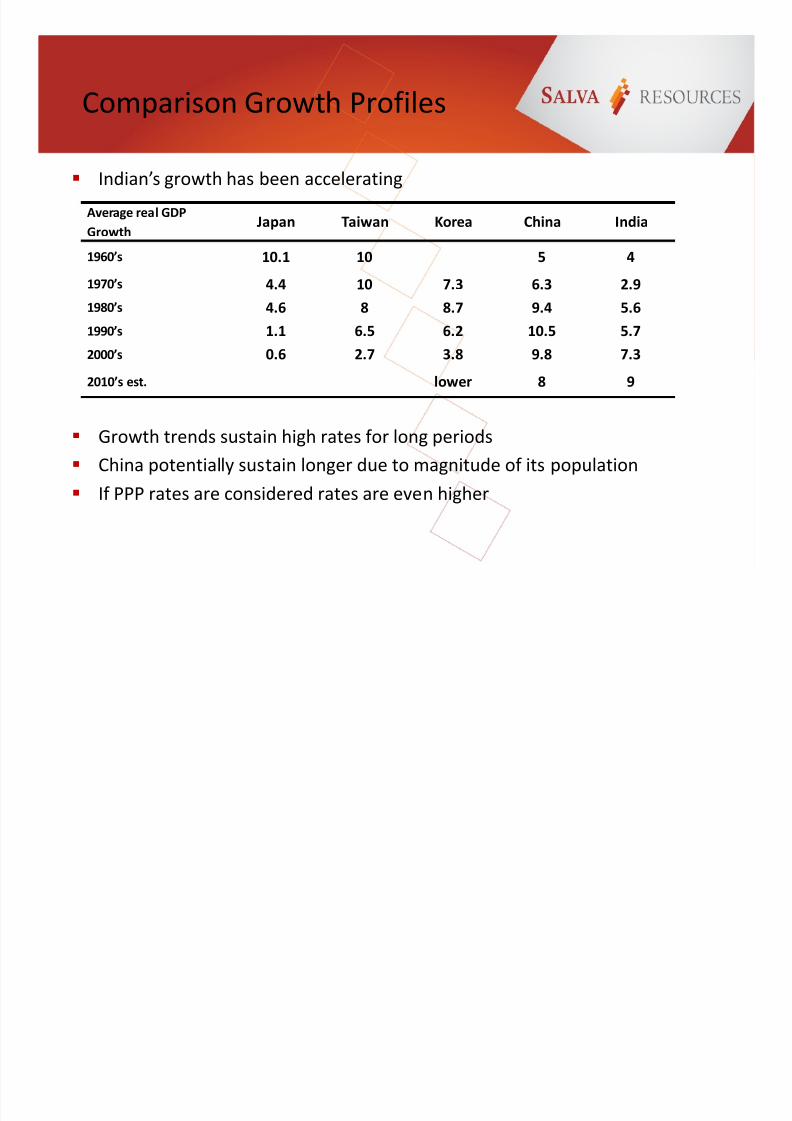

Comparison Growth Profiles

Average real GDP

Growth Japan Taiwan Korea China India

1960’s 10.1 10 5 4

1970’s 4.4 10 7.3 6.3 2.9

1980’s 4.6 8 8.7 9.4 5.6

1990’s 1.1 6.5 6.2 10.5 5.7

2000’s 0.6 2.7 3.8 9.8 7.3

2010’s est. lower 8 9

Indian’s growth has been accelerating

Growth trends sustain high rates for long periods China potentially sustain longer due to magnitude of its population

If PPP rates are considered rates are even higher

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 29/51

Consider Automotive Sector

India is already moving in 4 wheels Leading development of small “people’s car” e.g. Nano

Led acquisition to build competitive position ahead of China

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 30/51

Per capita consumption of steel in selected countries

0

100

200

300

400

500

600

700

800

900

1 9 0 0

1 9 0 5

1 9 1 0

1 9 1 5

1 9 2 0

1 9 2 5

1 9 3 0

1 9 3 5

1 9 4 0

1 9 4 5

1 9 5 0

1 9 5 5

1 9 6 0

1 9 6 5

1 9 7 0

1 9 7 5

1 9 8 0

1 9 8 5

1 9 9 0

1 9 9 5

2 0 0 0

2 0 0 5

2 0 1 0

k g / p e r s o n

USA Japan France Germany China India Brazil

Per Capita Consumption-

Where is the Potential?

Source: MySteel, Arcelor Mittal, Macquarie Research

History suggests >700kg per capita consumption for many years. This would equate to

production of >1bt from ~70Mt currently.

India

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 31/51

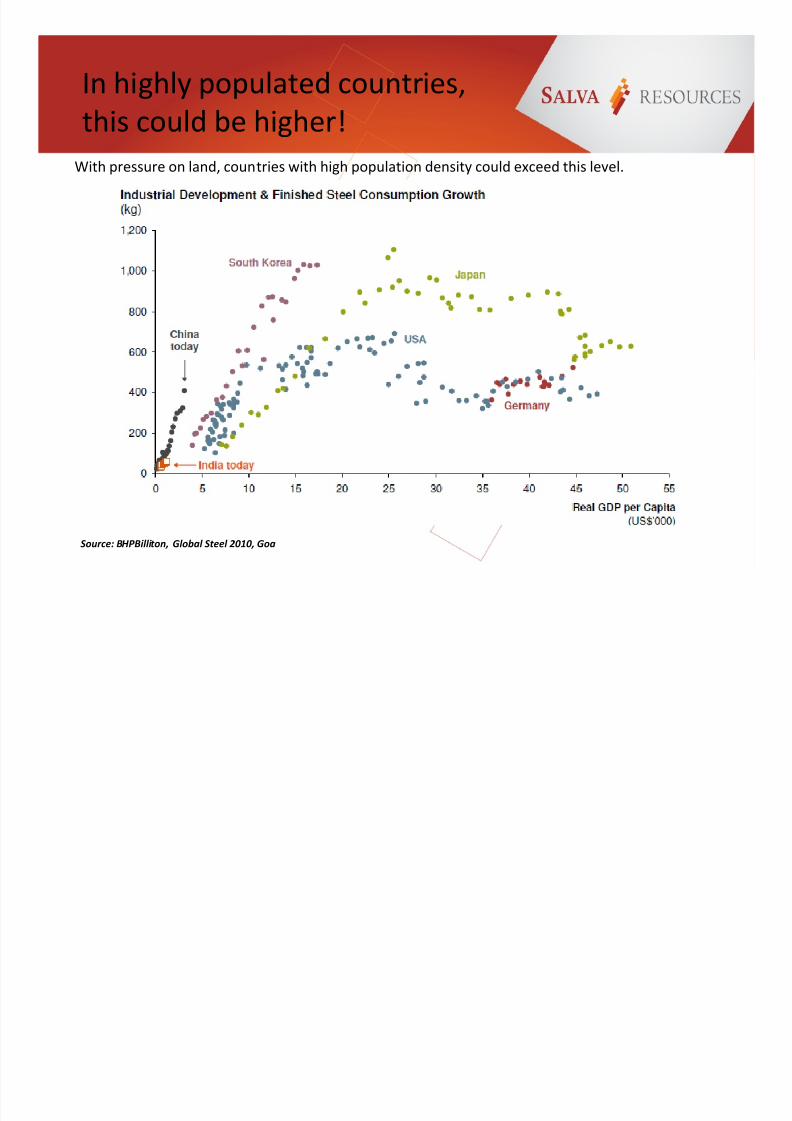

In highly populated countries,

this could be higher!

Source: BHPBilliton, Global Steel 2010, Goa

With pressure on land, countries with high population density could exceed this level.

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 32/51

Indian Steel Issues

Production growth – Major problems with land and approvals, POSCO

– Inability to grow has seen India move from exporter to importer

– Highly fragmented industry with large DR production and very large numbers

of small induction furnaces

Technology – Higher quality steels are likely to require more efficient BF based steelmaking

– Limited PCI, many BF’s don’t have facilities

– Lack of high quality met coal leading to HRCO

Raw materials – Ports and rail infrastructure required for movement of raw materials

– Will iron ore continue to be exported?

– Who will meet the requirements for met coal?

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 33/51

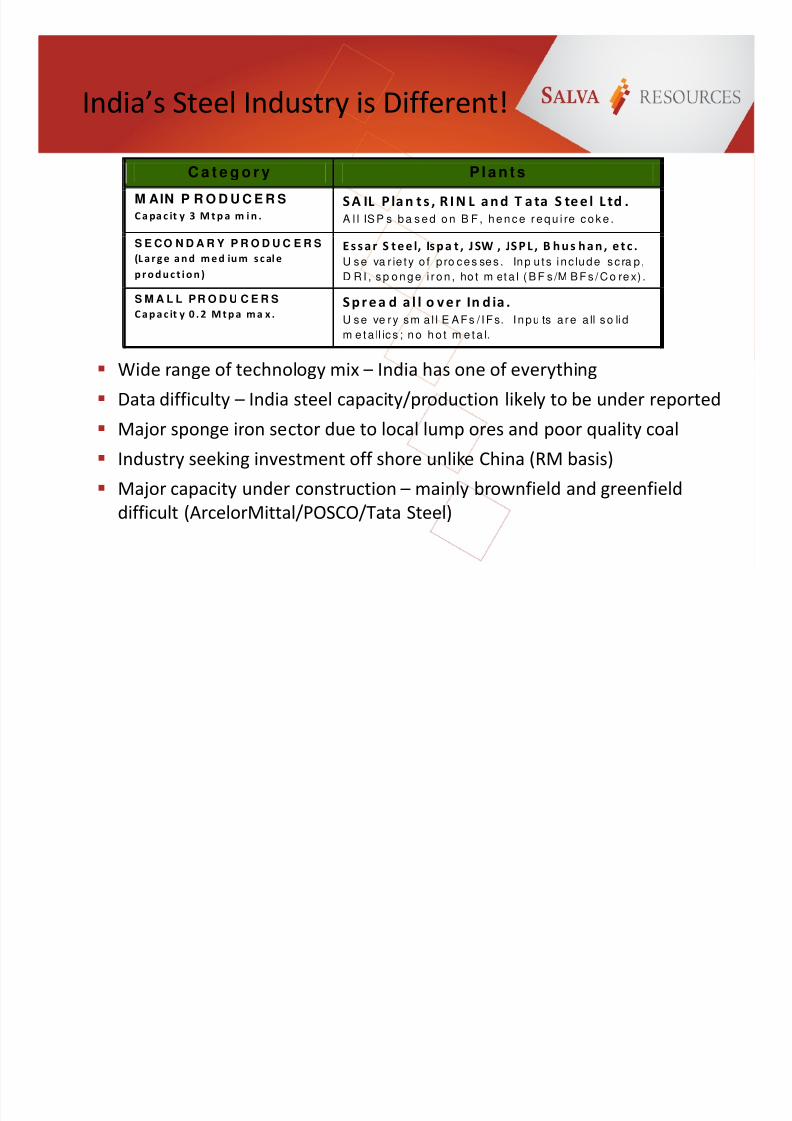

India’s Steel Industry is Different!

Wide range of technology mix – India has one of everything

Data difficulty – India steel capacity/production likely to be under reported

Major sponge iron sector due to local lump ores and poor quality coal Industry seeking investment off shore unlike China (RM basis)

Major capacity under construction – mainly brownfield and greenfield

difficult (ArcelorMittal/POSCO/Tata Steel)

C a t e g o r y P l a n t s

M AIN P R O D U C E R S

C a pa c it y 3 M t p a m i n .

S A IL P la n t s , R I N L a n d T a ta S te e l L td . A l l IS P s b a s e d o n B F , h e n c e r e q u i re c o k e .

S E CO N D A R Y P R O D U C E R S

(L a r g e a n d m e d iu m s c al e

p r o d u c t i o n ) E s s a r S t e e l, Is p a t , J SW , JS P L , B h u s h a n , e t c . U se va r ie t y o f p ro ces ses . Inp u ts inc lude sc ra p ,

D R I , s p o n g e i r o n , ho t m et a l ( B F s /M B F s / C o re x) .

S M A L L PR O D U C E R S

C a p a c it y 0 . 2 M t p a m a x . S p r e a d a l l o v e r In d ia . U se ve ry sm a l l E AFs / IFs. I npu ts a re a ll so li d

m e t a ll ic s ; n o h o t m e t a l.

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 34/51

Indian Steel Outlook to 2025

0

50

100

150

200

250

300

M i l l i o n t o n n e s

Steel and Pig Iron forecasts

Crude Steel

Pig iron

Crude steel 10%Pig Iron 10%

Source: World Steel Association, H&W Worldwide Consulting

Steel production will grow rapidly to 2025 and beyond. Demand growth will most likely see

increased BF/BOF steelmaking to feed emerging manufacturing sector.

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 35/51

Plan of Presentation

1. Australia and India the Past Relationship

2. India - Drivers for Accelerated Growth

3. The Future from a Coal Perspective

4. Summary and Implications

H & W Worldwide Consulting

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 36/51

Total Met Coal Consumption

0

20

40

60

80

100

120

140

160

m i l l i o n t o n n e

s

Met coal consumption

Other

PCI coal

Coking coal

Domestic

Source: Interocean, Salva, H&W Worldwide Consulting

Imports

Based on pig iron forecasts India will overtake Japan as the largest met coal importer around

2015-6, assuming new BF and coke plants come on as forecast.

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 37/51

Power Consumption ForecastsChanging the parameters leads to major growth in industrial use and residential demand, with the

largest percentage change in commercial consumption.

Source : IEA, Macquarie, H&W Worldwide Consulting

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

2005 2010 2015 2020 2025

P o w e r D e m a n d ( G W

)

Base case

Captive Demand lossesOther RailCommercial AgriculturalIndustrial Residential

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

2005 2010 2015 2020 2025

P o w e r d e m a n d ( G W

)

High case

Captive Demand lossesOther RailCommercial AgriculturalIndustrial Residential

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 38/51

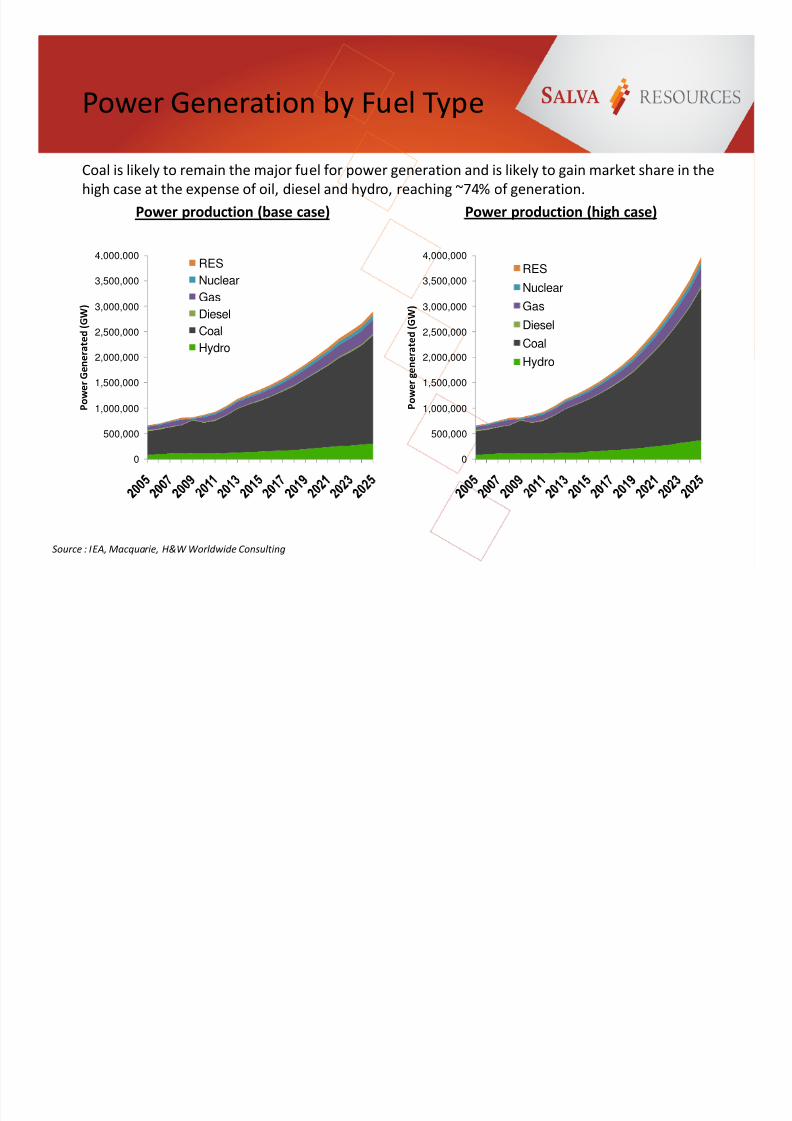

Power Generation by Fuel TypeCoal is likely to remain the major fuel for power generation and is likely to gain market share in the

high case at the expense of oil, diesel and hydro, reaching ~74% of generation.

Source : IEA, Macquarie, H&W Worldwide Consulting

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

P o w e r g e n e r a t e d ( G W )

Power production (high case)

RES

Nuclear

Gas

DieselCoal

Hydro

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

P o w e r G e n e r a t e d ( G W )

Power production (base case)

RES

Nuclear

Gas

Diesel

CoalHydro

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 39/51

India: Big Plans for Coal-fired

Power Generation

Source: NEC, Macquarie Research, July 2011

-

5,000

10,000

15,000

20,000

25,000

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

Hydro Coastal thermal Nuclear Other thermal

MW 11th and 12th plan power projects

Coal is likely to remain the major fuel for power generation, thermal remains the major source of

power generation in future plans.

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 40/51

History of overpromising, but even

conservative estimates are huge

Source: GTIS, Macquarie Research, April 2011

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

51-

56

56-

61

61-

66

69-

74

74-

79

80-

85

85-

90

92-

97

97-

02

`02-

07

Proposed Achieved

MW capacity addition

India 5 year plan - e lectricity expansion

-

20

40

60

80

100

120

140

160

2008 2009 2010F 2011F 2012F 2013F 2014F 2015F

Major Coastal IPPUMPPNon-specific imports

MtIndian Import Demand

However, the track record is not good, unlikely to meet targets as a widening gap between

planned and actually built. This situation is unlikely to improve greatly in the current and next

plans. India will remain very power short!

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 41/51

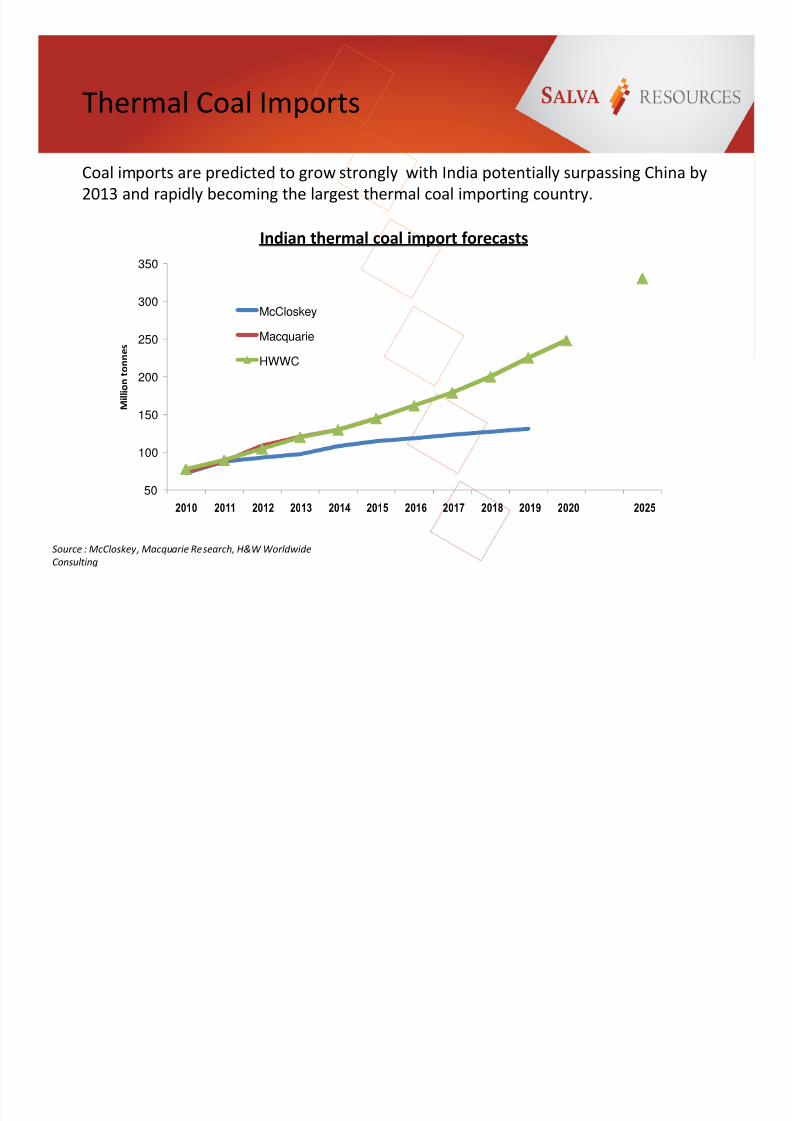

Thermal Coal Imports

50

100

150

200

250

300

350

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2025

M i l l i o n t o n n e s

Indian thermal coal import forecasts

McCloskey

Macquarie

HWWC

Source : McCloskey, Macquarie Research, H&W Worldwide

Consulting

Coal imports are predicted to grow strongly with India potentially surpassing China by

2013 and rapidly becoming the largest thermal coal importing country.

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 42/51

Steel Forecasts - Higher Cases

0

50

100

150

200

250

300

350

400

450

2006 2008 2010 2012 2014 2016 2018 2020

M i l l i o n t o n n e s

Indian steel Growth Forecasts

10%pa 12%pa

15%pa 20%pa

Consider some sample growth rates

Is 20% a fantasy – China exceeded this for a period?

Is 10% or 12% too conservative if India’s growth accelerates?

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 43/51

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 44/51

Plan of Presentation

1. Australia and India the Past Relationship

2. India - Drivers for Accelerated Growth

3. The Future from a Coal Perspective

4. Summary and Implications

H & W Worldwide Consulting

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 45/51

Implications of Major Steel

Production Growth

What would India’s raw materials outlook be at 2020 on previous scenarios?

Assumptions:

Pig IronAs growth rates increase BF/BOF increasingly preferred at source of production due to economies of scale, larger BF size

and limitations on DR route due to NG and energy costs.

Met Coal

Increase in PCI rates, with faster acceleration in high steel growth case, rates to reach country averages of 100kg/thm

@10%pa to 120kg/thm @20%pa rate. Increased use of SSCC likely at higher demand due to magnitude of volumes and

growth in HRCO.

Iron OreIron ores rats linked to hot metal growth with declining grades likely as growth rates rise due to higher more rapid

demand boosting speed to market and likely increased use of lower grade materials.

2020 Steel increase2020 Pig Iron

Production Increase

Increase in Iron Ore

Demand

Increase in Met Coal

Demand8%pa 77 76 156 50

10%pa 106 99 191 66

12%pa 141 131 239 87

15%pa 203 191 328 12620%pa 347 315 515 208

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 46/51

Implications for Met Coal

8%pa will see ~1.25 times increase in imports

10%pa will see import demand growth similar to total Japanese imports

20%pa increase is equal to current seaborne market for all coking coal

Major increase in all forms of met coal,

₋ PCI = 2.1x today market

₋ HCC = more in demand at higher rates due to rising productivity ~doubling market

Major issue of infrastructure ports and rail at these volumes

Metallurgical coal 8%pa 10%pa 12%pa 15%pa 20%pa

Demand increase (Mtpa) 50 66 87 126 208

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 47/51

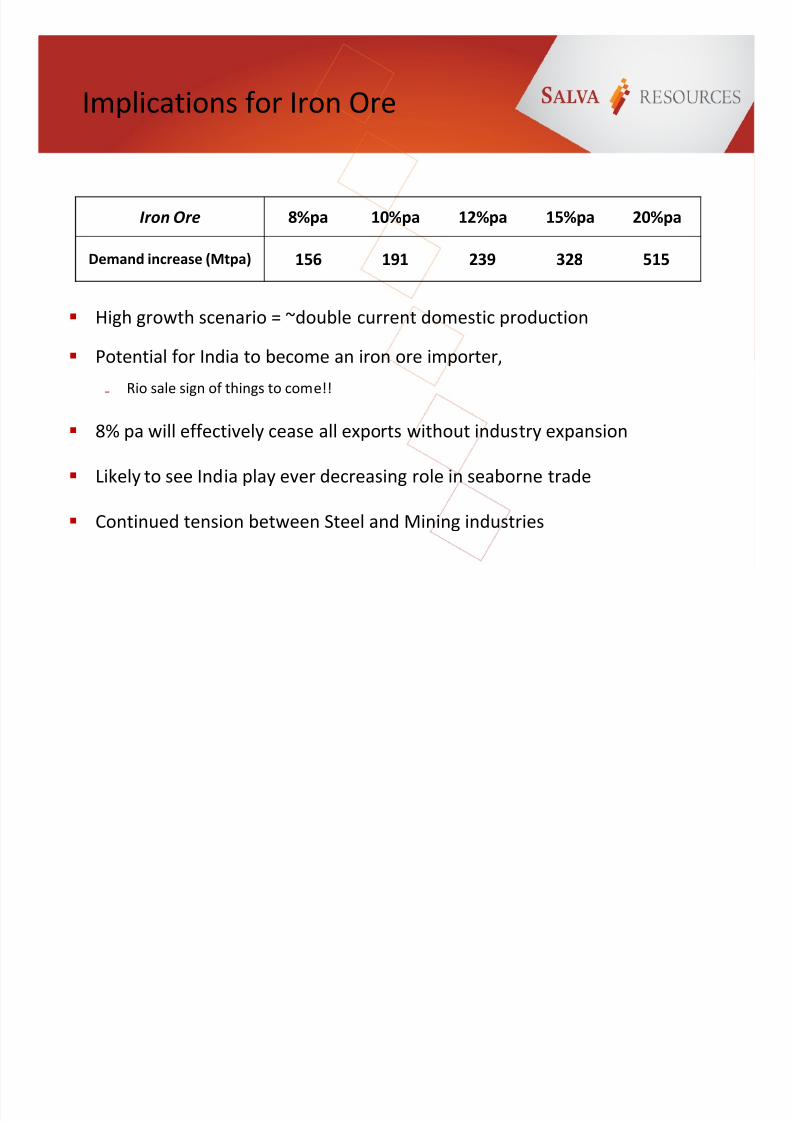

Implications for Iron Ore

High growth scenario = ~double current domestic production

Potential for India to become an iron ore importer,

₋ Rio sale sign of things to come!!

8% pa will effectively cease all exports without industry expansion

Likely to see India play ever decreasing role in seaborne trade

Continued tension between Steel and Mining industries

Iron Ore 8%pa 10%pa 12%pa 15%pa 20%pa

Demand increase (Mtpa) 156 191 239 328 515

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 48/51

Summarising Factors

All assume very significant movement of raw materials

₋ can the infrastructure be built ?

₋ Major rail, port and road building challenge ahead

High growth scenarios look impossible – but we always miss theupside

₋ China boom, pricing, freight etc

Yes, but it’s India.....

₋ India is moving, changing......but is NOT China!!

Major issue, where are raw materials going to come from?

₋ And of course China is still here!! Wanting the same coal and iron ore?

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 49/51

India in 2020

Could be passing Germany for no 4 spot in the world economy

Could have a vibrant manufacturing sector focusing on light cars, motorcycles, smartmanufacturing and light engineering

Could be the no 1 global software and programme developer

Could be the no 1 met coal importer ahead of China

Could be the no 1 thermal coal importer ahead of China

Could be the 2nd most important iron ore importer after China

Could surpass Hollywood in film exports

IPL could become more successful as the English Premier League

Could have turned Cricket into a truly world sport

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 50/51

Salva Report Products

The Salva Report - The world’s leading publication on the Indian steel, power, coal and

infrastructure sectors

India Unlocked - Providing all critical data on Indian coal demand and supply drivers inone location

Outlook Series - Forecasting the Future for India’s Power, Steel and Ports Sectors

Salva Report Products

The Salva ReportOngoing news and analysis

Outlook Series Annual forecast / report

India UnlockedCritical sector data series

Custom

ConsultingBespoke reports / forecasts

8/6/2019 A Breakfast Presentation

http://slidepdf.com/reader/full/a-breakfast-presentation 51/51

Summary and Conclusions

This will be India’s decade

India is following the conventional Asian development growth path

Economic acceleration and “take-off” expected well before end of

decade

Growth rates will surpass China by mid decade

Major growth in steel and power production with corresponding impact

on raw materials

India likely to be no 1 global coal importer

Could be importing iron ore before 2020