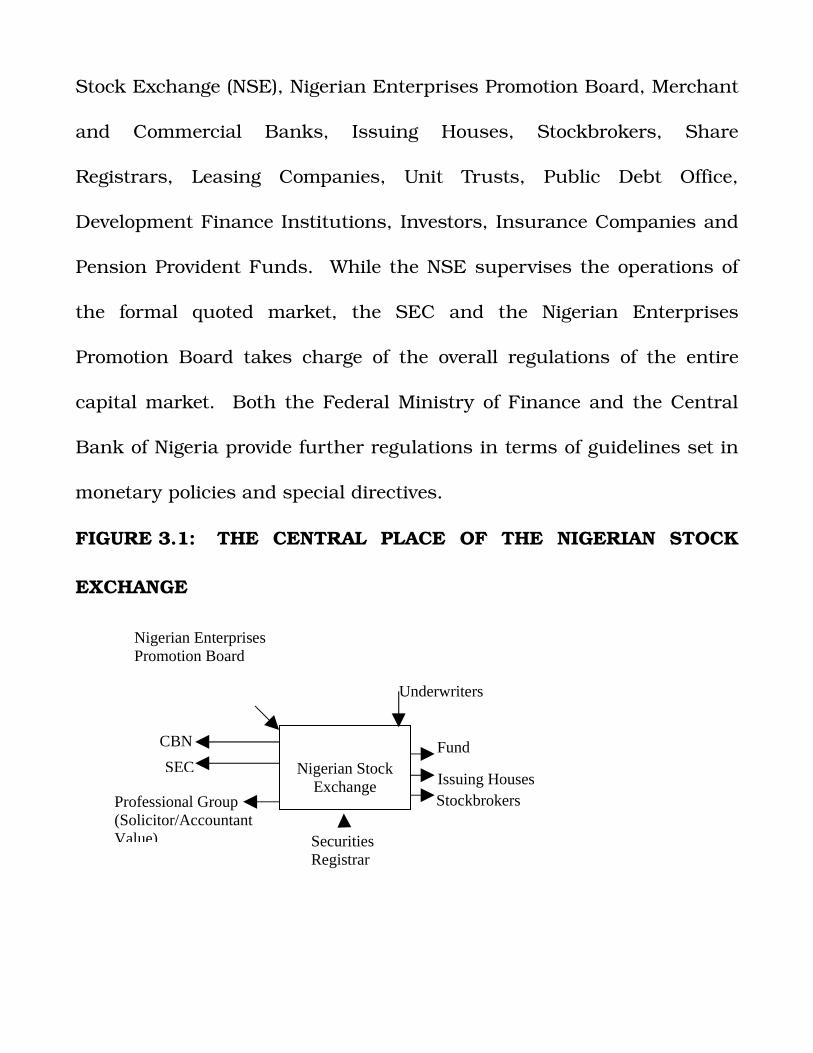

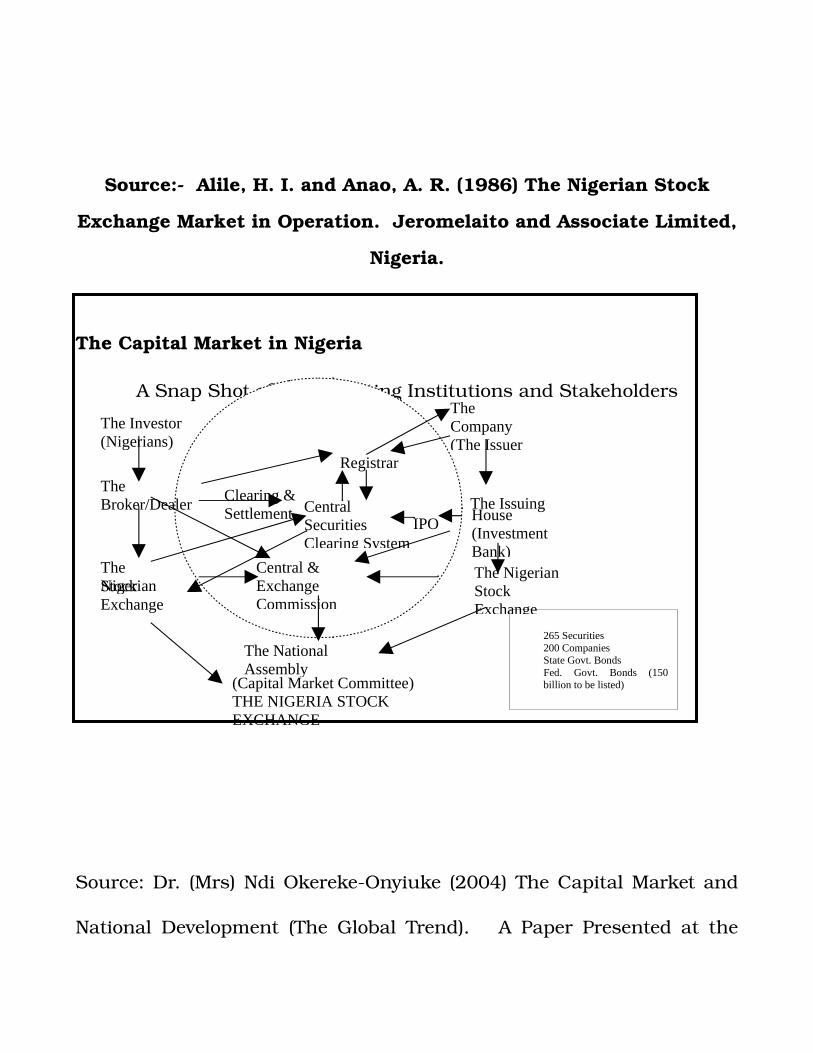

a critical study of the relationship between capital market development and economic growth in...

DESCRIPTION

FREE Download Permission: www.research.sanddatas.com, [email protected] OR Call/SMS Now +234-8030433711. Unlimited Research Works. This paper is a research study undertaken in Nigeria. The study is Presented in Theses format from chapter 1-5 and references. A comprehensive research , studying in details theThis study is a research work is presented in a thesis format for school academic research work. you may request for permission to download. [email protected] or www.sanddatas.com call 08030433711 A STUDY OF STUDENTS ATTRIBUTIONS OF CAUSALITY FOR ACADEMIC ACHIEVEMENT A CASE STUDY OF SCHOOL RELATED FACTORS AFFECTING NIGERIAN SECONDARY SCHOOL PUPILS ACADEMIC PERFORMANCE A COMPARATIVE ANALYSIS OF JOB A COMPARATIVE STUDY OF JOB A COMPARATIVE STUDY OF THE A COMPARISON OF STUDENTS AND TEACHERS PERCEPTIONS OF STUDENT PROBLEMS A CONCEPTUAL FRAMEWORK FOR THE ESTABLISHMENT OF AN OPEN UNIVERSITY IN NIGERIA A CORRELATIONAL STUDY OF STUDENTS SCORES IN BASIC SCIENCE THEORY AND PRACTICAL SUBJECTS IN KWARA STATE COLLEGE OF EDUCATION A CRITICAL ANALYSIS OF THE PRIMARY SCHOOL MATHEMATICS TEACHER EDUCATIONAL OBJECTIVES IN NIGERIA A CRITICAL APPRAISAL OF PROCEDURES FOR LANGUAGE AND LITERATURE TEACHING A DESCRIPTION OF THE DEVELOPMENT A LONGITUDINAL STUDY OF THE SCHOOL SUBJECT PREFERENCES OF A GROUP OF NIGERIAN ADOLESCENTS A MODEL FOR DEVELOPING POST A MODEL FOR THE OPTIMAL ALLOCATION OF TEACHERS TO SECONDARY SCHOOLS IN NIGERIA A NEW APPROACH TO THE TEACHING A NOTE ON THE MANAGEMENT OF HIGHER EDUCATIONAL INSTITUTIONS IN THE 80s A REAPPRAISAL OF FIELDWORK AS A TEACHING METHOD IN GEOGRAPHY A REVIEW OF CORRELATE OF CLIENTS A STUDY OF FACTORS INFLUENCING CHOICE OF HISTORY IN KWARA STATE SECONDARY SCHOOLS A STUDY OF LOCATION DIFFERENCES IN A STUDY OF PUBLIC PARTICIPATION IN THE MANAGEMENT OF HIGHER INSTITUTIONS IN OGUN STATE, NIGERIA. A STUDY OF TEACHER TURNOVER IN SELECTED SECONDARY SCHOOLS A STUDY OF THE MATHEMATICS COMPONENT OF THE MATHEMATICS TEACHERS PROGRAMME IN NIGERIAN UNIVERSITIES A STUDY OF THE PERFORMANCE OF UNDERGRADUATE EDUCATION STUDENTS IN EDUCATION A STUDY OF THE PIAGETIAN LEVELS OF A SURVEY OF HANDICAPPED CHILDREN IN THE PRIMARY SCHOOLS IN ILORIN METROPOLIS A SYNCHRONIC CONTRASTIVE STUDY OF ACADEMIC PERFORMANCE OF SECONDARY ACADEMICS INVOLVEMENT IN COLLECTION ACCOUNTABILITY IN THE NIGERIAN ACE, RELIGION AND STUDENTS LECTURERS PERCEPTION OF SEXUAL HARASSMENT A CASE STUDY OF UNIVERSITY OF ILORIN Activity Level and Academic Ability of Primary School Children Aged 6-11 Years in Kwara State Adult Literacy as an Agent of Development among Rural Communities in Gwagwalada Area Council of F.C.T. ADULTS AND LEARNING SOME BASIC PRINCIPLES Alleviating Poverty in Nigeria AN APPRAISAL OF THE LEGAL STRUCTURE OF EDUCATION IN NIGERIA AN ASSESSMENT OF ENGLISH ERRORS AMONG SECONDARY AN ASSESSMENT OF THE IMPLEMENTATION OF THE 6-3-3-4 SYSTEM OF EDUCATION IN NIGERIA A CASE STUDY OF ILORIN, KWARA STATE. AN EVALUATION OF THE CONCEPT OF THE GRANT SUMMARIES USED BY THE AGENCY FOR INTERNATIONAL DEVELOPMENT (AID) IN APPRAISING THE QUALITY OF GRANTS IN NIGERIA AN EVALUATION OF THE EFFECT OF A SICKLE CELL EDUCATION PROGRAMME ON KNOWLEDGE AND ATTITUDE OF STUDENTS TOWARDS GENETIC SCREENING AN EVALUATION OF THE NIGERIAN JUNIOR SECONDARY SCHOOL SCIENCE CURRICULUM AN EVALUATION OF THE POSTGRADUATE AN EXAMINATION OF THE ADEQUACY OF THE N EXPERIMENTAL REVIEW OF THREE AN INVESTIGATION INTO THE DIFFERENCES BETWEEN MEN AND WOMEN IN SCIENCE AN INVESTIGATION INTO THE DIFFICULT AREAS OF THE CURRENT JUNIOR SECONDARY SCHOOL MATHEMATICS CURRICULUM AN INVESTIGATION INTO THE ORGANIZATIONAL EFFECTIVENESS OF OGUN STATE MINISTRY OF EDUCATION IN EDUCATIONAL PLANNING AND DEVELOPMENT AN INVESTIGATION INTO THE PRINCTRANSCRIPT

SAND DATASCOM

Academic Research Materials

A CRITICALLY STUDY OF THE RELATIONSHIP BETWEEN

CAPITAL MARKET DEVELOPMENT AND

ECONOMIC GROWTH IN NIGERIA

A THESIS FORMAT

www.research.sanddatas.com

THIS RESEARCH MATERIAL IS DOWNLOADABLE ON REQUEST

EACH DOWNLOAD IS CHARGED WITH A FEE PAYABLE IN NAIRA

SIMPLY REQUEST PERMISSION FOR DOWNLOAD

+234 803 043 3711

ABSTRACT

BLANK

CHAPTER ONE

INTRODUCTION

1.1 BACKGROUND TO THE STUDY

No business can exist and grow without capital (money), which can be

much likened to a lubricant or fuel without which a mechanical

object such as a motor vehicle cannot function. At every stage and

development of a business enterprise, capital is needed, be it to

startup, for expansion or for its daily operations. In order to

capture the essence of capital formation, one must first understand

the various forms of capital. In broad terms, capital refers to any

form of wealth or resources useful in the creation of more wealth or

resources. However, capital can be defined in terms of its natural

characteristics such that it is possible to distinguish human capital

from physical capital or capital stock.

Thus, capital formation embodies a broad and holistic mechanism

through which investible funds and other tangible and intangible

resources are mobilized from surplus sector within the economy for the

creation of financial assets such as loans, leases, etc to be subsequently

utilized for productive investment by deficit economic units. In any

economy, the issue of savings, investment and capital formation is

critical. Capital formation involves the production and setting aside of

real capital goods for use in subsequent production. It involves making

some sacrifices in consumption now with the aim of increasing our

production base.

The subject of financing economic growth and development relates

to the provision of real resources to raise the level of real output

(national income) and living standards (income per head) in developing

countries like ours. The growth of output is not, of course, the only goal

of economic policy in developing countries, but policies to raise the rate

of output growth and this forms the major part of most countries’

development plans, because: (i) growth is seen as a necessary condition

for an improvement in the general welfare and because (ii) growth is

seen as the precondition for the achievement of other development

objectives such as the provision of greater employment opportunity, the

redistribution of income and wealth, and the provision of social capital

in the form of housing, communication and facilities for the

development of human resources. Although it has become fashionable

for the international middle class to renounce growth, it remains, in the

absence of a massive redistribution of world income, the only means of

eradicating primary poverty, which still afflicts at least twothirds of

humanity.

Economic growth requires real resources devoted to the production

of capital goods, where capital goods are defined broadly to include

industrial plant, machinery, social overhead capital, and educational

facilities indeed the production of anything, which is not immediately

consumable but yields a flow of income in the future. The economic

growth of a nation and the ability to gain the most from its accumulated

resources, (men, materials, money and machines) of necessity requires a

well developed capital market(s) that continuously oil them. The demand

for funds – economic capital comes mainly from three sources namely:

business, government and individuals and exist because their income

does not equal their need for current expenses plus expenditure for fixed

assets. Funds raised through debt and equity instruments by business;

government and individuals are normally invested in fixed assets and

inventories, public facilities and housing respectively.

Modern economies rely to a very large extent on the existence of

efficient and reliable credit system for their growth and development. As

financial intermediaries, financial institutions facilitate the operation of

the requisite credit system by mobilizing funds for on lending to

companies and governments. This allocating function is crucial in

determining the overall growth of an economy for if capital resources are

not provided to those economic areas where demand is growing and

which are capable of increasing productivity and production, and then

the rate of expansion of the economy will be constrained.

History of direct government involvement in economic management

is both long and substantial. Government therefore designs activities to

stimulate and assist private enterprises, regulate and control business

practices so that operations within the private sector are consistent with

the public interest. Government and companies mobilize funds for

economic activity designed to increase, improve and/or maintain the

productive quality of the existing stock of capital. The Nigerian capital

market enables government and companies to mobilize and allocate

funds for new project development, expansion, modernization and

refurbishment of plants for both government and industrial/commercial

projects. Since the introduction of Structural Adjustment Programmes

(SAP) in 1986, privatization/commercialization and debt conversation

programmes emphasis has shifted from reliance on external funding to

using domestic resources in order to accelerate economic growth. For

sustainable growth and development, funds must be effectively

mobilized and allocated to enable the economy and business harness

their human, material and management resources for optional output.

The centrality of savings and investment to economic growth has been

given considerable attention in the literature (Soyode, 1990, Aigbokan,

1995, Samuel, 1996, DemirgueKunt and Levine, 1996., Onyuike, 2000).

According to Ahmad (1986) and Oronsaye (2003), the capital

market and its institutions are so much talked about and yet least

understood by the general public. So much is said and written about the

capital market yet, so few people understood and still fewer people utilize

the services of the capital market. Even amongst the educated class; the

capital market is often regarded as an elitist affair and the exclusive

preserve of the top – echelons of the capitalist enterprise system. It is

even regarded by some as another neocolonialist ploy to perpetuate the

interest of the upper and middle classes in the ownership and control of

the enterprise system. As posited by Oronsaye (2003), the Nigerian

capital market is still underdeveloped when compared when with other

countries of the world. Studies show that less than 3 percent of

120million Nigerians invest in the capital market unlike 77percent in the

United States, 63 percent in the European Union, and more than 26

percent in South Africa. This ignorance was further supported by the

various road shows organized by the Nigerian Stock Exchange to boost

the needed awareness of the importance of the capital market in order to

promote investment culture among Nigerians at home and in diaspora.

Understanding the role of capital market by the generality of Nigerians

will facilitate the ultimate goal of restructuring the Nigerian economy.

The misconception is compounded by the fact that the capital market

per se, and its actors and wares are not people and goods as commonly

seen in everyday market place. In the capital market, the actors are

corporate institutions comprising the apex regulatory bodies (including

the Nigerian Stock Exchange, the Securities and Exchange Commission,

etc) and a host of intermediation agents called operators, while the

goods traded are actually bonds, stocks and shares. By their special role

in creating money and liquidity, capital market institutions are

indispensable to the nation’s economic system and have a catalytic

impact on the growth of the market oriented economy.

1.2 STATEMENT OF THE PROBLEM

The Nigerian economy has been bugged by a lot of socioeconomic

and political malaise, antithetical to economic growth and development.

Capital markets the world over; serve as veritable channels to mobilize

both domestic and foreign savings for developmental purposes. But

despite the feat achieved by the Nigerian capital market in the area of

capital formation over the years, individuals, corporate bodies and

governments were yet to take full advantage of the opportunities

available in the market. The capital market remains underdeveloped

when compared to other countries of the world such as Hong Kong,

Australia, Switzerland, USA, UK, South Africa, Egypt, and Malaysia in

relation to market capitalization, number of listed companies, trading

activities in both volume and value of securities etc. This study has also

tried to identify the factors inhibiting the development of capital market

to include: low level of financial intermediation, dismal domestic savings

mobilization, investor apathy, lack of market depth, infrastructural

inadequacies, low public awareness, insufficient knowledge and

information about the capital market and transactions being conducted

on archaic trading platform, buyandhold attitude of shares certificates

by investors which suppressed liquidity and stunting overall market

activity, lack of trust, transparency and poor corporate governance, few

financial instruments, institutions and markets, inadequate legal and

regulatory frameworks, low liquidity, infrequent trading and fewer

listing of 276 in 2004 than those of Sri Lanka established in 1984 with

1778, South Africa – 1000 while India can boast of 6500 quoted

companies. The limited listing of private companies in Nigeria limits the

attractiveness of the capital market for domestic and foreign investors.

The lack of absorption capacity and low demand for equity securities

and the absence of government securities for the past 17years have

worsened the attraction of new companies and investors to the market.

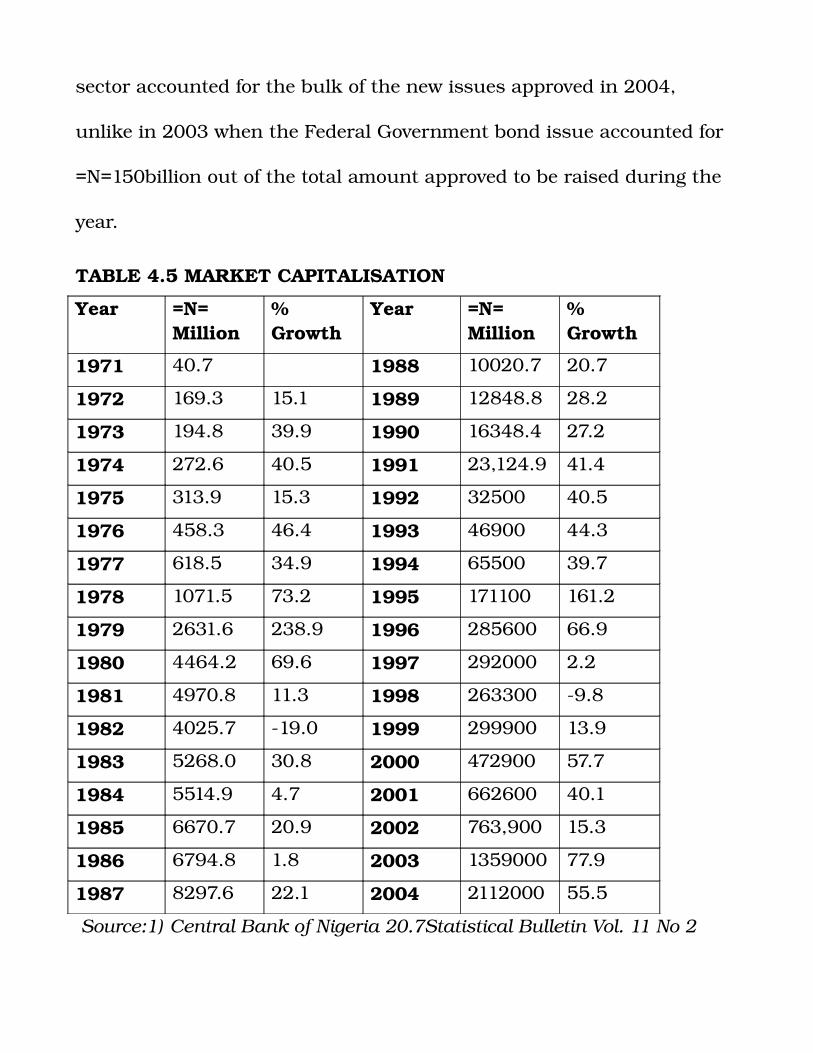

Since inception in 1961, the Nigerian capital market has had a

mixed history of growth. It has gone from an inactive market to one of

the potentially buoyant centerpieces of a new emerging market. It is

considered the fourth largest market in the continent and one of the

best performing world wide, according to recent survey published by

United Nations Development Program (UNDP). Market capitalization has

growth from N40.7million in 1970 to N2.112 trillion in 2004 just as the

number of listed companies has dramatically increase from 19 in 1961

to 276 in 2004. Critics argued that given its long history of existence the

Nigerian Capital market should have done better. One line of research

argues that capital market development is not important to economic

growth. Another line stresses the importance of capital market in

mobilizing savings, allocating capital, exerting corporate control, and

easing risk management. Moreover, some theories provide a conceptual

basis for the belief that larger, more efficient capital market boost

economic growth.

In assessing these allegations levied against and for capital market

development, it might be expedient to address some questions such as:

1. Why has it become so important to develop capital market?

2. Do capital market affect overall economic growth and if so, how?

3. What is the relationship between capital markets in fostering

economic growth? And how can Nigeria benefit from capital

market development?

4. What are the problems of the capital market in Nigeria?

It is on the basis of the foregoing that this research work draws

interest by attempting to empirically analyse the relationship between

capital market development and longrun economic growth in Nigeria.

1.3 SIGNIFICANCE OF THE STUDY

The Nigerian capital market as a network of facilities for mobilising

and dealing in longterm funds has grown substantially from 19

securities listed on the Nigerian Stock Exchange in 1961 to 276 in 2004

which is made up of 69 federal government development stock and

industrial loans/bonds/preference stocks and 207 equities. The market

capitalization of securities has also grown appreciatively from

N4.5billion in 1980 to N2.112 trillion in 2004. Transaction value was

N1.49million in 1961, and in 2004 it has grown to N225.82billion. All

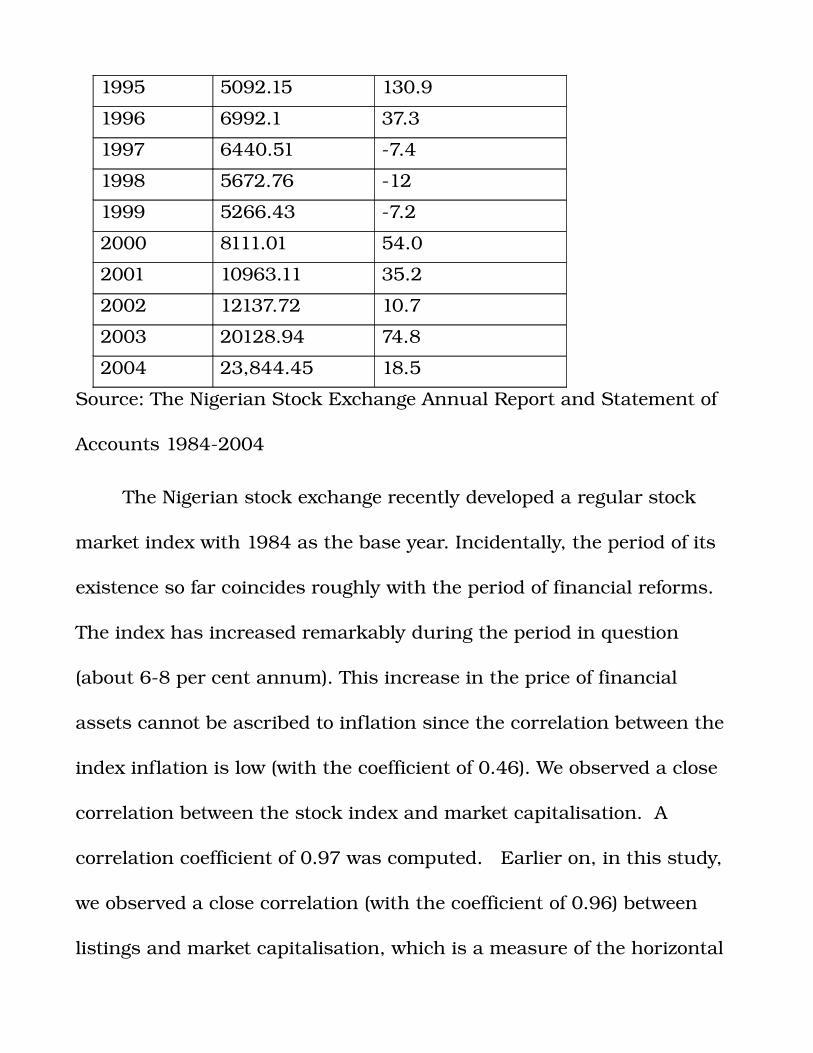

Share Indexes increases from 513.8 in 1990 to 23844.45 in 2004.

It is expected that the result obtained from this study will be of

immense benefits to researchers, business organisations, government,

investors as well as people in general. The study of the capital market is

of paramount importance to the longrun growth and prosperity of

business and government organisations since they provide the funds

needed to acquire fixed assets and implement programmes aimed at

ensuring the continued existence of organisations. The attainment of

efficiency in the utilisation of financial resources towards sustainable

economic growth and development remains a cardinal challenge for any

wellmeaning nation. Furthermore, the significance of this research lies

in the fact that the financial system is important in bridging the

savings/investment gap. Kolb (1983) noted the importance of financial

markets when he said, “these markets provide fluidity of capital by

making possible the transfer or allocation of savings in the economy to

the demanders. Without the financial markets, the ability of each

economic unit to acquire real assets would be limited to the savings of

that unit. Economic growth and development by the society would be

stifled, resulting in much lower productivity and wealth accumulation”.

The unique benefit of the stock market to corporate bodies

and government is the provision of longterm, nondebt financial capital.

Through the issuance of equity securities, companies acquire perpetual

capital for development and this also invariably enables companies to

avoid overreliance on debt financing, thus improving corporate debtto

equity ratio. The study on capital market development and economic

growth will help the government to restructure the Nigerian economy

through improved financial intermediation, which leads to higher

savings, and capital accumulation, which are channeled to high

productive projects. Thus, in these period of serious economic

difficulties when most economies are inward looking for effective

mobilisation and efficient allocation of scare financial resources, this

study will provide needed awareness among Nigerians for greater

patronage of the Nigerian capital market. Finally, like many other

studies before it, this study will stimulate further research into capital

market development and its relationship with capital formation and

sustainable economic growth.

1.4 THE RESEARCH OBJECTIVES

The main objective of this study is to critically examine the

relationship between capital market development and economic growth

in Nigeria (1961 – 2004). To achieve this main objective, the following

specific objectives are pursued:

i) To describe the nature and patterns of the capital market in

Nigeria.,

ii) To discuss the important role played by the capital market in the

economic health of Nigeria.

iii) To ascertain the reasons why and how government intervenes in

capital market in Nigeria.

iv) To examine the various constraints that impede the development

of efficient capital markets and how these constraints can be

removed.

v) To make recommendations as to how the optimum linkages

between capital development and economic growth can be

realised in Nigeria.

1.5 SCOPE OF THE STUDY

Essentially this research focuses on an examination of the

relationship between capital market development and economic growth

in Nigeria (19712005). This period covers the major historical

developments in the economic history of Nigeria and this is a period

considered long enough for any meaningful study. The research also

concerned itself with the description of four categories of capital market

players, which includes:

1. Provider of funds: Individuals, unit trust, development Banks.

2. User of fund: Companies, Governments.

3. Intermediaries: Stockbroking firms, issuing houses, registrars,

auditing firms.

4. Regulators: Securities and Exchange Commission (SEC), (Apex

regulatory body), The Nigerian Stock Exchange (NSE), (a Self

Regulatory Organisation (SRO)).

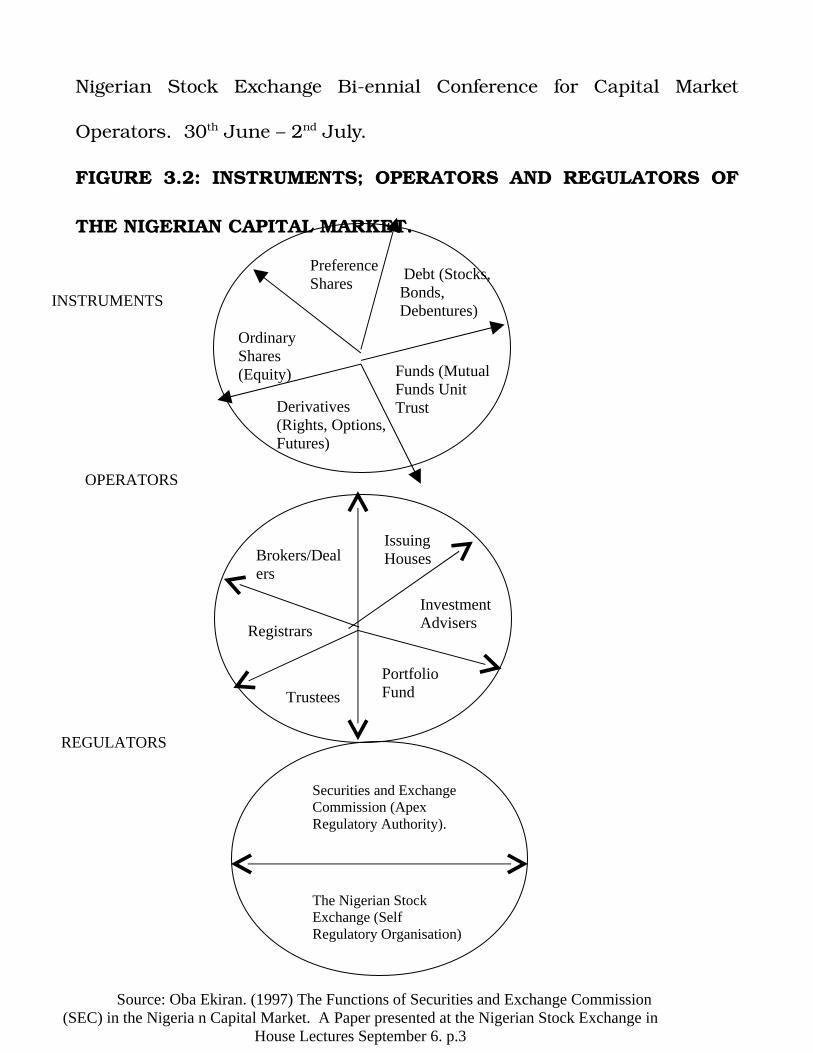

Financial instruments (equity, preference shares, debt instrument,

government bonds (Federal, State and Local Governments), industrial

loans/debenture stock and bonds and derivatives (options, futures,

rights etc) used in the capital market was also discussed.

1.6 ORGANISATION OF THE STUDY

This project is structured into five chapters. Chapter one is the

introduction, which consists of the background, research problems,

significance, research objectives, scope and organisation of the study.

Chapter two focuses on the review of related literature concerning

capital market development and economic growth, economic growth

theories, and efficiency in capital market. Chapter three examines the

historical profile of the Nigerian capital market, research hypotheses,

data specification, method of data collection and method of data

analysis. Chapter four is the data presentation and analysis, which

examined the relationship between capital market development and

economic growth. The summary, conclusion and policy

recommendations are contained in chapter five.

CHAPTER TWO

LITERATURE REVIEW AND THEORETICAL FRAMEWORK

2.1 CAPITAL MARKET AND ECONOMIC GROWTH DEFINED

A capital market is the complex of institutions (regulators,

facilitators, issuers and investors) and mechanisms through which

intermediate and longterm funds of households, firms and government

are pooled and made available to various sectors of the economy for

development purposes (Dougall and Gaumitz, 1975). Alile (1986) defines

the capital market as a network of specialised financial institutions that

in various ways bring together suppliers and users of capital. By their

special role in creating money and liquidity, capital market institutions

are indispensable to the nation’s economic system and have a catalytic

impact on the growth of the market oriented economy. The importance

of the capital market stems from the fact that it enables institutions in

the economy that are in need of medium to longterm funds for the

acquisition of fixed assets and other longterm projects to obtain such

funds. In addition, the capital market provides a mechanism through

which longterm loans and investments can be liquidated. Ahmed

(1993) posited that effective capital markets are crucial for the efficiency

and solvency of the financial system. These markets enhance

competition, reduce intermediation costs and provide borrowers and

lenders with alternative sources of fund or investment outlets (equity

and/or debt) for the period most convenient for them. The level of

development of capital markets also determines the flexibility and pace

with which the financial system can adjust to internal changes and

absorb external shocks. The effectiveness of financial market is

enhanced by sound fiscal and monetary policies, appropriate legal and

regulatory framework and by professionalism on the part of market

operators. Although Nigeria’s capital market have expanded over the

years; the pace of growth of the Nigerian capital market has been a

checkered one because until recently market operators, institutions and

investors have tended to deal at the short end of the market in order to

hedge against inflation and other structural distortions in the system.

With the introduction of the Structural Adjustment Programme (SAP)

and with the emphasis on deregulation of the market, there are

indications that there would be greater efficiency in the market with a

spontaneous lengthening in the maturity of assets demanded by the

public, and expansion in related trading and a wide range of financial

instruments.

In the light of this, an efficient capital market, comprising of the

primary (i.e. new issues of securities) and secondary (trading in old

issues of stock) markets has a catalytic impact on growth in the market

oriented economy. According to Obadan (1998), the Nigerian capital

market, at inception, was intended to accomplish a number of

objectives, which include:

Provision of local opportunities for borrowing and lending for long

term purposes;

To enable governments mobilise longterm capital for the development

of the country;

To provide foreign businesses with the facility to offer their shares and

the Nigerian public an opportunity to invest and participate in the

share ownership of foreign businesses;

To provide facilities for quotation of and ready marketability of shares

and stock and opportunities and facilities to raise fresh capital in the

market;

To provide a healthy and mutually acceptable environment for

participation and cooperation of indigenous and expatriate capital in

the joint effort to develop the Nigerian economy, to the mutual benefit

of both parties; and.

To introduce a code of conduct, check abuses and regulate the

activities of the operators of the market.

The rapid development of capital markets has attracted the

attention of development economists, policy makers, practitioners and

planners. Recent government interests in promoting investments and

attracting foreign capital inflows in developing countries have focused on

creating an enabling environment for the emergence of a virile, active

and dynamic capital market. Not surprisingly many countries in Africa

such as South Africa, Botswana, Cote d’lvoire, Egypt, Ghana, Kenya,

Mauritius, Morocco, Tunisia, Uganda and Nigeria have reformed their

laws and regulations to removed barriers that impede capital market

development with a view to attract foreign portfolio flows (Nyong, 1997).

Brewis (1990) said that the Nigerian capital market exists to

provide risk capital for Nigerian commerce and industry and to provide

investors with a market in which to dispose of their investments when

they wish. Capital markets are of key importance to the long run

growth and prosperity of business, and government organisations since

they provide the funds needed to acquire fixed assets and implement

programmes aimed at ensuring organisations continued existence. The

capital market facilitates the transfer of new savings to new investments

and the exchange of old securities. The backbone of the capital market

is the various Security Exchanges, which provide a market place for debt

and equity transactions. Capital markets the world over serve as

veritable channels to mobilize both domestic and foreign savings for

developmental purposes. The financial sector of any nation is usually

regarded as its ‘lifeline’, mobilizing capital resources and facilitating

their flow into productive activities. The ability to efficiently mobilize

and allocate resources among competing needs in the society is a major

indicator of the level of development of the financial sector. A weak and

inefficient financial system would therefore give rise to low financial

intermediation, which invariably will fail to adequately support the

development process. Thus, efficient money and capital markets are

crucial for the efficiency and solvency of the financial system.

Economic growth means a sustained increase in total national

income. It is an economic condition, which is present when a country’s

capacity to produce goods and services grow from year to year over a

long period of time. Economic growth is the steady process by which

productive capacity of the economy is increased over time to bring about

rising level of national income. Economic growth means more output,

which implies more input and more efficiency – that is, an increase in

output per unit of input (Udu and Agu 1989). Economic growth is the

rate of expansion of the national income or total volume of production of

goods and services of a country. According to Parkin (1990), economic

growth is the persistent expansion of our production possibilities. Two

key activities generate economic growth: capital accumulation and

technological progress. Capital accumulation is the growth of capital

resources. Technological progress is the development of new and better

ways of producing goods and services. Economic growth is either growth

in national output, as measured by Gross National Product (GNP) or

Gross Domestic Product (GDP). The first measures economic power, the

second measures the well being of citizens. In the most fundamental

sense, economic growth is concerned with policy measures aimed at

expanding a nation’s capacity to produce. In general, economic growth

can be seen as an outward shift of an economy’s production possibilities

frontier. That is, economic growth means increase productive capability.

It is a function of labour and capital. This does not happen without

resources being made available for production purposes. On the other

hand, no amount of resources utilised will result in reasonable growth if

they are not used productively. The growth impact of given resources

(savings) will reflect the efficiency with which they are utilised. The

measurement for the rate of growth is the national income. Economic

growth generally refers to an increase in a country’s output measured by

the Gross Domestic Product (GDP) or National income in real terms

between two periods. The physical ability of an economy to produce

more goods and services is dependent on a number of factors amongst

which are capital accumulation, labour force, natural resources,

productivity, technological progress, as well as a favourable socio

political environment, (Ojo, Oladunni, Bamidele 1997).

Demson and Kendrick (1985) said that there are two types of

growth namely extensive growth and intensive growth. Extensive growth

is growth in output resulting from increases in inputs (capital and

labour). If labour grows by X percent the percentage of growth in

national output is roughly calculated by this X percent weighted by

(multiplied by) labour’s relative contribution to production. Extensive

growth contribution might be measured by the share of wage payments

in the value of output. Intensive growth is growth that results from

improvements in factors quality, technology, and efficiency of markets

and institutions. Intensive growth results from the four listed factors:

advances in knowledge (technological break through), a better –

educated labour force, improved resource allocation, and scale

economies. Growth that occurs through technological change and

capital deepening brings social transformation. Economic growth could

be define either as increasing real national output (income) or increasing

per capital real output. The process of economic growth necessarily

involves the structural transformation of the society, along with

concomitant changes in institutions, interrelationships and value.

What policies are available to promote economic growth? According

to basic macroeconomic model, a policy mix that includes a structurally

balanced budget and a monetary policy leading to relatively low interest

rates will promote growth. Economic growth can be promoted by other

policies encouraging saving and investment as well. In addition growth

could be potentially stimulated by tax policies designed to encourage

savings and investment.

According to Udu and Agu (1989) the following are the factors

affecting economic growth: the quality and quantity of capital available;

the skills and efforts of the working population; organisational factors,

such as specialisation, and technological improvements (discovery of

fertilizers); the general economic climate involving trade relationships

with other communities, the extent of monopoly and the impact of

government policy.

2.2 CAPITAL MARKET DEVELOPMENT

What is the conceptual definition of capital market development?

How can capital market be empirically measured? Theory does not

provide a unique concept of capital market development to guide

empirical research. Existing models suggest that capital market

development is a multifaceted concept, involving issues of market size,

market liquidity, and integration with world capital markets. While

capital market development naturally implies greater use of equity and

longterm debt instruments in raising capital. Capital market

development has involved research activities aimed at improving market

efficiency, and competitiveness as well as introducing new instruments

and initiating policies with positive implications for the capital market.

The Securities and Exchange Commission thus in carrying out its

duties ensures that it balances regulation with development. In other

words, the market must not be over regulated as to hinder its

development while regulatory issues are not neglected in pursuit of its

development objectives. According to Oladejo (1996) the incentives to

capital market development in Nigeria are as follows: computerization

and link up with internet; reduction of withholding tax; reduction of

period for raising funds; reduction in settlement date;

internationalization of the market; privatisation of government

parastatals; political stability; and realistic exchange, interest and

inflation rates.

2.3 MEASURES OF CAPITAL MARKET DEVELOPMENT

While the development of any nation is measured by criteria such

as its Gross National Income per capital, etc capital market development

however according to Akingbohungbe (195) is assessed by such criteria

as liquidity, choice, efficiency and regulation. The presumption is that

institutional and other infrastructural facilities are in place. All these

criteria and their interplay bear influence on the successful marketing

of new issues. Business opportunities, the size of income, as well as the

growth of household and institutional savings inter alia are factors that

control demand for and supply of new issues regulation of capital

market is essential to orderly conduct of affairs amongst the parties to

capital market transactions, the efficiency of the market by way of

information dissemination aid investor perception. In terms of choice,

the investing public in Nigeria has all along been restricted by the rather

than nature of the Nigeria capital market since inception. This has

tended to encourage buy and hold attitude of Nigeria market. The

indicators of capital market development are market capitalization, new

issues, liquidity (trading value, trading volume, turnover ratio, and total

value traded ratio), number of listed companies, and market index,

1. MARKET CAPITALIZATION

Market capitalization is the market value of a company’s issued

share capital. It is the product of current quoted price of shares and the

number of shares outstanding. The term is also used as performance

indicator of the capital market when all listed companies are considered.

Market capitalization is a common index often used as a measure of the

size of the capital market. Market capitalization equals the total value of

all listed shares. It is a function of the prevailing market price of listed

equities and the size of the issued and paidup capital of the affected

companies and is derived for each quoted company by multiplying the

market price of equity by the outstanding share of the company. The

market capitalization for the entire equity market is thus obtained by

summing up the market capitalization of all quoted companies.

For individual quoted companies, the size of its market

capitalization is an indicator of the market value (i.e. investor’s

assessment) of the company. Thus, market capitalization does fluctuate

with movements in the market price of company’s equity. Similarly, an

increase in the outstanding shares of a company with the market price

either held constant or increased would enhance the market

capitalization of the company. However, an improvement may not

necessarily be witnessed in market capitalization of outstanding share

increase but the market price drops significantly.

Generally, the aggregate market capitalization of a capital market

would witness increasing trend in bullish market while the converse

would happen in a bearish market situation. To notable global investors,

the size of market capitalization is an important motivating factor for

investment presence in a given company or market.

To assess how big a stock market is within the national economy,

the market capitalization is usually compared with the Gross Domestic

Product (GDP).

2. PRIMARY SECURITIES OR (NEW ISSUES)

Primary Securities or new issues are funds generated through the

sales of long term securities in form of stocks and bonds for the first

time after subscription by the general public, or only by existing

shareholders of a company or if placed privately (directly) with

previously identified investors.

The total amount of new issues raised in the capital market could

be indicative of the popularity of the capital market as a source of funds,

which in turn is largely dependent on investors’ confidence, and the

comparative cost of raising capital from the competing sectors’ of the

financial market. Certain government policies could also influence the

level of primary market activities. For instance, where interest rates are

deliberately kept low, the tendency would be for corporate bodies to

source all or a good proportion of their longterm funds through the

money market, as it becomes a cheaper financing source. Tax policies,

which favour money market instruments, could also shift funds away

from the capital market and consequently impact adversely on the

subscription level of new issues and indeed could dampen the desire by

corporate bodies to source funds through the market.

The health of the national economy is another vital factor, which

usually impacts on the level of new issues. In fact, a strong correlation

does exist between the level of new issues and the economic health of a

country. When economic activities are declining therefore, the level of

new issues usually drops while the converse happens in times of

economic expansion.

In most economies where public companies meet their additional

fund requirements through the floatation of subsequent issues, the

frequency of new issues would to some extent be dependent on the

number of public companies operating within each of such economies.

The contributions of the new issues market to the national

economy may be assessed through a comparison of new issues with

some economic indicators such as the Gross Fixed Capital Formation

during a given period. Capital Formation is defined as investment in

fixed assets, which in part are financed with monies raised through the

capital market. Thus, new issues contribute to the stock of capital in an

economy and invariably to economies growth and development. In some

economies; the size of the new issues market is a major source of funds

for the acquisition of fixed assets in the economy.

3. LIQUIDITY

Liquidity is used to refer to the ability of investors to buy and sell

securities. It is an important indicator of capital market development

because it signifies how the market helped in improving the allocation of

capital and thus enhancing the prospects of longterm economic growth.

This is possible through the ability of the investors to quickly and

cheaply alter their portfolio thereby reducing the risk of their investment

and facilitating investment in projects that are profitable though with a

long gestation period. Two main indices are often used in the

performance and rating of the stock market: Trading Value and Trading

Volume.

Trading Value: Trading Value is the amount of all deals transacted on a

Stock Exchange during a given period. The trading value, on each

trading day is calculated by multiplying the number of shares,

bond/stock that changed hands among share/stockholders by the

prevailing market prices of such securities. A rapid increase in the

trading volume of security in the exchange is indicative of interest in the

security or the market. Persistence rise in volume and prices can

sometimes lead to overheating of the market and a consequent crash.

Trading Volume: The trading volume (i.e. the number of shares/stock

traded) and value are also important indicators of the level of liquidity,

the efficiency of the infrastructural facilities (such as the Clearing and

Settlement System) of a capital market and the investment culture of the

populace.

Turnover Ratio: The turnover ratio (i.e. trading value as a percentage of

market capitalization) is another method of assessing how active a

capital market is. Turnover ratio is usually higher in active markets than

markets, which are relatively inactive. Turnover ratio is used as an index

of comparison for market liquidity rating and the level of transaction

costs. The ratio equals the total value of shares traded on the stock

market divided market capitalization. It is also a measure of the value of

securities transactions relative to the size of the securities market. Total

value traded ratio measures the organized trading of equities as a share

of the national output.

4. NUMBER OF LISTED COMPANIES

Number of listed Companies: The total number of quoted companies

on an exchange is another criterion to assess the popularity and size of

a capital market. In countries with high aversion to companies going

public, the number of listings is usually small while in countries where

public quotation is seen as a prestige and its benefits well realized, the

number of equity listing is relatively high. One factor which might also

impact on the number of public quotations is the stringency or

otherwise of the listing requirements. Some countries, in order to

encourage wellrun markets introduce markets with less listing

requirements e.g. the USM in Britain, the Second Marche in France and

the SecondTier Securities Market (SSM) in Nigeria. In markets with

strong aversion to quotation, it has been discovered that government

policies and supplyside incentives are necessary catalysts in

stimulating listings.

5. MARKET AVERAGES AND INDICES

Stock market indices are vital as investment benchmarks. Market

Averages and Indices: A market average or index is an important

yardstick for evaluating the performance of a stock market as a whole or

a given sector of it. It is considered an important analytical tool intended

to depict the behaviour of a stock market and indeed the direction of the

economy among other things.

Aggregating the prices of all equities derives stock averages and

dividing the total sum by the number of constituent securities derives

stock averages. In the alternative a select group of comparable securities

could be chosen, their prices weighted, adjusted, summedup and

divided by the number.

In essence, an average is merely an arithmetic mean of the prices

of the group of selected securities; the Dow Jones Industrial Average in

USA is perhaps the most popular stock average. An index on the other

hand is a weighted average in relation to the base period. The market

values of the various securities are in order words related to a given

base period. Rising averages and indices are evidences of firm prices

while falling indices indicate general drop in prices. The index movement

is very important to analysts and investors.

According to Marsh (2002) indices have many purposes. First, they

are used to monitor and measure market movements, whether in real

time, daily, or over decades. A good index will tell us how much richer or

poorer investors have become. Second, equity and bond indices are

economic barometers, while equity indices are leading indicators.

Monitoring markets and comparing movements with data such as

wages, profits and inflation helps us to understand economic conditions

and prospects. Third, indices provide essential benchmarks in fund

management. A managed fund can communicate its objectives and

target universe by stating which index or indices serve as the standard

against which its performance should be judged.

Forth, indices underpin products such as index funds, exchange

tradedfunds, and options and futures on indices. These indexrelated

products form a several trillionnaira business and are used widely in

investment, hedging and risk management.

Finally, indices support research (for example, as benchmarks for

evaluating trading rules, technical analysis systems and analysts’

forecast); risk measurement and management; and asset allocation and

international diversification decisions.

Indices are all – pervasive, with more than 4000 in operation.

Equity market indices; such as the Dow, Nikkei, Dax FTSE100 and all

share indexes tend to be the best known. But indices are also important

for other assets such as government and corporate bonds. Commodities

currency baskets and retail prices. As well as market indices, there are

numerous sub indices. For equities, these cover sectors, size bands,

investment styles, and even ethical and religious dimensions; for bond

indices they span maturities and credit risk categories. There are

international indices that aggregate country indices into regions (such

as Asia), currency zones (such as the euro), market types (such as

emerging markets) and worldwide indices.

6. PRICE – EARNINGS RATIO

Price – Earnings Ratio: The Price – earnings ratio is a figure

depicting how covered by earnings is an equity investment in any

company. It may be based on actual earnings of a company, or on a

projected figure in which case it is referred to as “projected price –

earnings ratio”. It gives an idea of the period it takes an investor to

recoup his/her investment going by present earnings trends of a

company. It is derived by dividing the prevailing market price of an

equity by the earnings per share derives it. The perceived investment

risk of an equity is usually focused though its priceearning ratio. Thus,

a seasoned company with good and stable financial and dividend

payment track record could have a high priceearnings ratio while a

poorly performing company would likely record a low priceearnings

ratio. The priceearnings ratio is the inverse of the earnings yield or the

returns on equity investment of a company.

7. CONCENTRATION

The factor measures the level of domination of the market by a few

enterprises. The significance of concentration as a measure of

performance of capital market is because of the adverse effect it may

have on the liquidity of the market. The share of market capitalization

accounted for by the 10 largest stocks often measures the degree of

market capitalization of the top ten equities listed on the Nigerian Stock

Exchange.

8. VOLATILITY

Volatility is a twelvemonth rolling standard deviation estimate

based on market returns. Greater volatility is not necessarily a sign of

more or less capital market development. Indeed high volatility could be

an indicator of development, so far as revelation of information implies

volatility in an efficient market (Bekaert and Harvey 1995)

9. ASSET PRICING

It deals with the efficiency of the asset pricing process in the

securities market. The major yardstick for measuring efficiency in terms

of market prices is the information content inherent in such prices. A

market price is touted as reflecting a strongly efficient market if it

adequately and correctly reflects all available information (past, present

and future) and are at the disposal of all market participants

simultaneously contained in the historical prices and all publicly

available information. Where the current prices reflect only the

historical information with little predictive value, the market is regarded

as weak (Inanga and Emenuga 1997).

2.4 THEORETICAL SIGNIFICANCE OF CAPITAL MARKET

Theoretically, there is a closeif imperfectrelationship between the

effectiveness of an economy’s capital market and its level of real

development (McKinnon 1993 and Shaw 1973). Financial market

provides liquidity (Bencivenga and Smith 1991, Levine 1991), promote

the acquisition and dissemination of information (Diamond 1981, Boyd

and Prescott 1986, Williamson 1986, Greenwood and Jovanovic 1990),

and permit agents to increase specialization (Cooley and Smith 1992).

Companies require finance according to their different

circumstances and needs. An analysis of corporate capital raisings by

the nature of the financial need identifies three broad categories of

capital requirements:

i) Capital required to startup new business – “Start up Capital,”

ii) Capital required to develop/expand or preserve existing

business – “Development Capital”, and

iii) Capital for new technology and high – risk ventures “Ventures

Capital”

The paramount role of the state in providing effective regulations of

its capital market is also underscored by the accelerator effect of the

capital market on principal objectives of governance – revenue

generation, inflation control and strong balance of payments position.

The capital market business in recent times has become so globalised

that regulation of each national market has begun to focus attention

towards standards that are generally acceptable and considered to be

necessary for safe cross border investments. The level and intensity of

productive activities as measured by such vital economic indicators as

the gross domestic product, per capita income, foreign exchange rate,

balance of payments, inflation and interest rate are vivid reflections of

economic performance of any nation. The financing and expansion of

crucial productive activities therefore, have direct relevance to economic

growth and development and political stability.

The nature and economic significance of the relationship between

capital market development and economic growth vary according a

country’s level of economicdevelopment with a larger impact in less

developed economies (Filler, Hamousek and Campes 1990). The

proponents of positive relationships between capital market development

and economic growth hinged their argument on the fact that the capital

market aids economic growth and development through the mobilization

and allocation of savings, risk diversification, liquidity creating ability

and corporate governance improvement among others.

Edo (1995) asserts that securities investment is a veritable medium

of transforming savings into economic growth and development and that

a notable feature of economic development in Nigeria since

independence is the expansion of the stock market thereby facilitating

the trading in stock and shares. In 1990, Soyode posited that a self

sustained growth process requires substantial investible resources,

which are readily available at the capital market. The development of

the capital market, and apparently economic growth, provides

opportunities for greater funds mobilisation, improved efficiency in

resource allocation and provision of relevant information of appraisal

(Inanga and Emenuga 1997).

Capital market contributes to economic growth through the

specific services it performs either directly or indirectly. According to

Okereke Onyiuke (2003), primarily capital markets exist to reconcile the

conflicting needs of savers/investors and publicly traded securities. The

intermediation between the needs of firms and investors represents the

core function of capital markets, which, by extension, enables

functioning capital markets to facilitate:

Risk diversification – provides a means for sharing investment

risk.

Information acquisition about companies – provides

incentives to seek information about companies.

Corporate control – provides the means for improving

corporate governance.

Also, capital markets function to facilitate the dispersion of

business ownership, thus contributing to asset formation at the

household level. Finally, capital markets, where they exist, facilitate the

transmission and implementation of macroeconomic policies, and is why

public authorities responsible for economic policy as well as private

sector agents who are active in the capital markets have a vested interest

in capital markets that are both efficient and stable. By offering

financial intermediation for debt and equity instruments, capital

markets work to ensure greater competition among financing sources

and thereby promote efficiency in the mobilisation and allocation of

financial resources.

2.5 THE CONCEPT OF THE COST OF CAPITAL

Cost of capital is the cost incurred in securing funds, or capital for

productive purposes. The costs include interest, legal, administrative

and information search charges. This means that cost of capital is likely

to be greater or equal to interest rates on loans.

The issue of cost of capital for firms is a most crucial factor in

finance decisionmaking. Every mode or avenues of obtaining capital to

finance the firm’s assets attracts a cost, either in the absolute or

opportunity form. The more marginal an investment decision is, the

more important it is for the firm to have the required prerequisites for

the measurement of the relevant cost of capital, at least in providing the

firm’s management with a meaningful capital cost assessment. The

firm’s cost of capital can be defined as the rate of return that a company

earn on an investment that will be just sufficient to maintain the value

of business.

Indeed an important part of financial management involved raising

capital in the proportion that will minimize overall cost. There are

alternative ways of arriving at weights but in reality the cost of capital is

merely the weighted arithmetic mean of the cost of each component of

firm’s capital. This need not concern us unduly as far as debt is

concerned; it is the calculation of the equity cost that is central to this

argument. For, while the cost of the debt is represented by the actual

outofpocket payments needed for servicing, the cost of equity is purely

conceptual and bears little relation to payments to equity holders.

The firm’s cost of capital can be defined as the rate of return that a

company must earn on an investment that will be just sufficient to

maintain the value of the business. In capital budgeting decisions, the

discount rate was a significant factor in assessing the profitability of

projects. This rate is often referred to as the cost of capital and it

represents a cutoff rate for the allocation of capital to investment

projects. It is the required rate of return needed to justify the use of

capital and this, in theory, should be the rate of return on a project that

will leave unchanged the market price of the shares.

In evaluating capital projects the appropriate discount rate applied

could be viewed as (a) the explicit cost of funds used in financing the

project(s) or (b) the opportunity cost of foregone investment i.e. the yield

on the best alternative to the project in question. Most of our discussion

later will focus on the explicit cost of capital but in discussing cost of

retained earnings and cost of depreciation, regard will be had to the

opportunity cost concept. With regard to the explicit cost concept, the

appropriate discount rate to be used in evaluating a project is the firm’s

overall or composite cost of funds and not the cost of a particular

component fund to be raised in financing the project. Furthermore this

composite or overall cost of funds should be the marginal cost of funds

to be raised in future for financing the projects and should not be the

historical cost of the funds that have been raised in the past as these

have bearing on this decision. For a proper understanding of the

computation of a firm’s composite or overall cost of capital one needs to

discuss the explicit cost of each of the component source of fund. It is

the discount rate (or what was previously referred to in the valuation

models as the capitalization rate) that equates the present value of the

funds received by the firm, net of underwriting and other costs, with

the present value of expected outflow. Depending on whether the source

of fund is a bond, preference share or ordinary share, the outflows could

be interest payment, repayment of principal or dividends. Therefore the

explicit cost of a particular component source of fund can be determined

by solving for k in the equation below:

Po + Q1 + Q2 + Qn(1+k) (1+k)2 (1+k)n

Where Po is the net amount of funds received by the firm at time

O, Q is the outflow in period t, and n is the duration over which the

funds are provided.

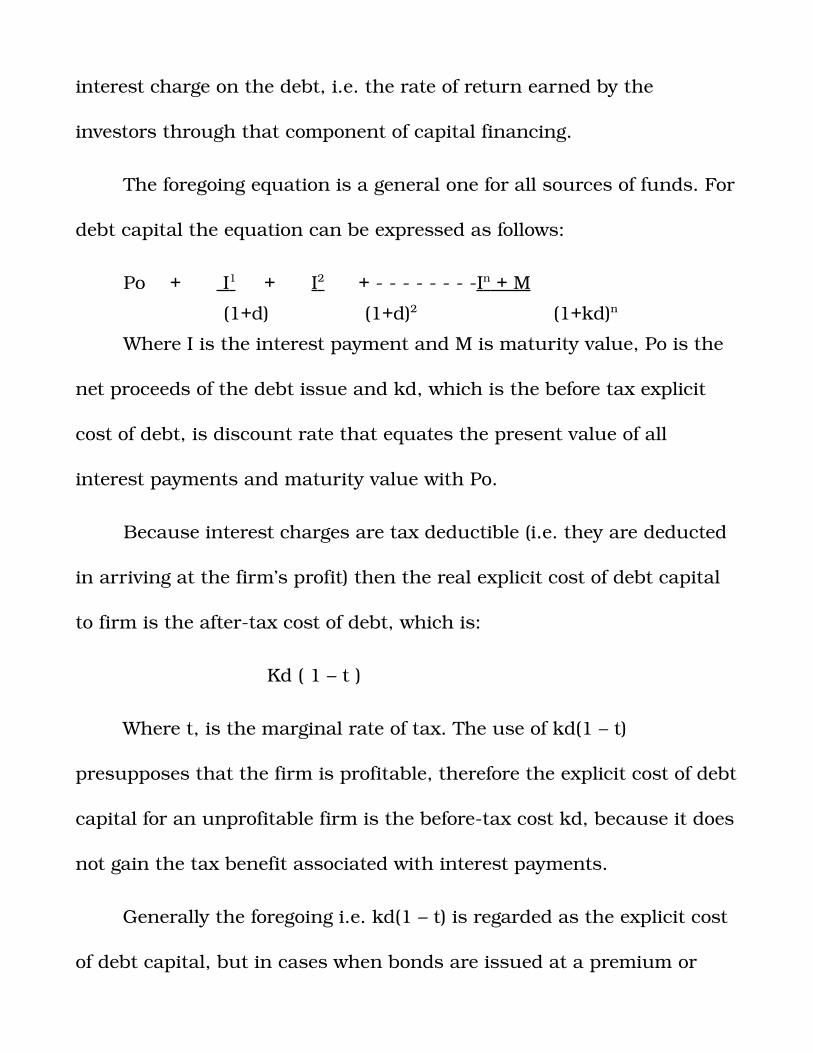

COST OF DEBT CAPITAL

A firm’s debt will often comprise of longterm loans, debentures,

and bonds. As a first appropriation, the firm’s cost of debt capital is the

interest charge on the debt, i.e. the rate of return earned by the

investors through that component of capital financing.

The foregoing equation is a general one for all sources of funds. For

debt capital the equation can be expressed as follows:

Po + I 1 + I 2 + I n + M (1+d) (1+d)2 (1+kd)n

Where I is the interest payment and M is maturity value, Po is the

net proceeds of the debt issue and kd, which is the before tax explicit

cost of debt, is discount rate that equates the present value of all

interest payments and maturity value with Po.

Because interest charges are tax deductible (i.e. they are deducted

in arriving at the firm’s profit) then the real explicit cost of debt capital

to firm is the aftertax cost of debt, which is:

Kd ( 1 – t )

Where t, is the marginal rate of tax. The use of kd(1 – t)

presupposes that the firm is profitable, therefore the explicit cost of debt

capital for an unprofitable firm is the beforetax cost kd, because it does

not gain the tax benefit associated with interest payments.

Generally the foregoing i.e. kd(1 – t) is regarded as the explicit cost

of debt capital, but in cases when bonds are issued at a premium or

discount and not at their face values. Usually the premium or discount

is amortized for tax purposes and where the premium or discount is

material, the aftertax cost of the debt capital can be expressed as

follows:

kd (1 t) = (1 t) (1+1/n (M – P))

½ (M + P)Where I is the period interest payment in naira, M is the par to

maturity value of the bond, P is the bond’s issue price (hence M – P is

the premium or discount), and n is the life of the bond.

In cases where the firm may have a policy of maintaining a given

proportion of debt to its capital structure in such a way that debt

retirements are supplanted by new debt issues, then the debt could be

viewed as having been issued in perpetuity and the beforetax cost of

debt is expressed below:

Kd = I/Po

and aftertax cost of debt, kd (1 –t) = I (1 – t) Po

Where I is the fixed interest cost in all periods, and Po is the net

proceeds of the issue.

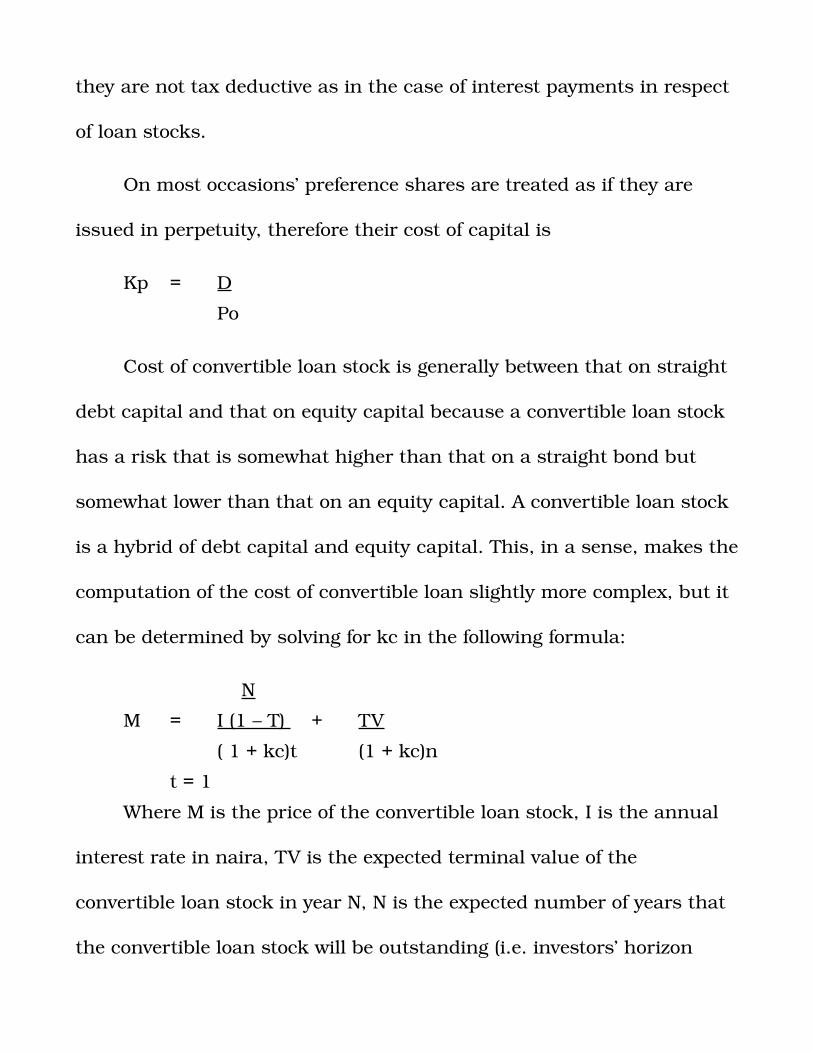

COST OF PREFERENCE SHARE CAPITAL

Preference Share capital differs from debt capital in some respects

though they are both subject to fixed payments. The fixed payments

made in the case of preference share capital are dividends while they are

interest in the case of debt capital. The interest payments on debt

capital take priority over the dividend payments on preference share

capital.

Preference share may be redeemable after certain years or they

may be irredeemable. The cost of redeemable preference share capital

may be determined by solving for kp in the following equation:

Po + D1 + D2 + Dn(1+kp) (1+kp)2 (1+kp)n

For irredeemable preference share capital the cost of capital is

kp = D Po

Where D is the stated annual dividend and Po is the net proceeds

of the preference share issue. Here the aftertax cost of capital has not

been calculated because preference dividends are paid after taxes i.e.

they are not tax deductive as in the case of interest payments in respect

of loan stocks.

On most occasions’ preference shares are treated as if they are

issued in perpetuity, therefore their cost of capital is

Kp = DPo

Cost of convertible loan stock is generally between that on straight

debt capital and that on equity capital because a convertible loan stock

has a risk that is somewhat higher than that on a straight bond but

somewhat lower than that on an equity capital. A convertible loan stock

is a hybrid of debt capital and equity capital. This, in a sense, makes the

computation of the cost of convertible loan slightly more complex, but it

can be determined by solving for kc in the following formula:

NM = I (1 – T) + TV

( 1 + kc)t (1 + kc)nt = 1

Where M is the price of the convertible loan stock, I is the annual

interest rate in naira, TV is the expected terminal value of the

convertible loan stock in year N, N is the expected number of years that

the convertible loan stock will be outstanding (i.e. investors’ horizon

period) and kc is the required rate of return on the convertible loan

stock and it is the discount rate that equates the expected aftertax

interest payments or dividends in the case of convertible preference

share, plus the expected terminal value with the offering price of the

convertible security.

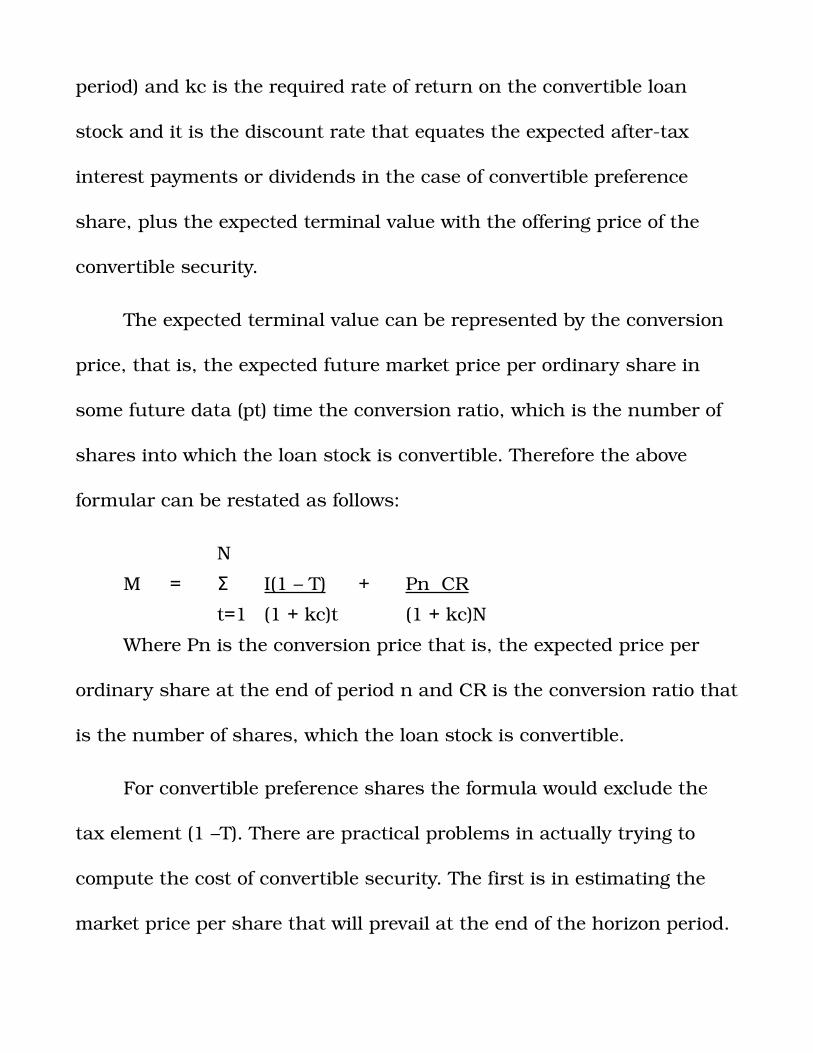

The expected terminal value can be represented by the conversion

price, that is, the expected future market price per ordinary share in

some future data (pt) time the conversion ratio, which is the number of

shares into which the loan stock is convertible. Therefore the above

formular can be restated as follows:

NM = Σ I(1 – T) + Pn CR

t=1 (1 + kc)t (1 + kc)NWhere Pn is the conversion price that is, the expected price per

ordinary share at the end of period n and CR is the conversion ratio that

is the number of shares, which the loan stock is convertible.

For convertible preference shares the formula would exclude the

tax element (1 –T). There are practical problems in actually trying to

compute the cost of convertible security. The first is in estimating the

market price per share that will prevail at the end of the horizon period.

Second, is that different investors have different horizon periods, some

attempt to overcome this problem is in trying to specify a weighted

average horizon period, but a better solution lies in estimating the

length of time the convertible securities are likely to remain outstanding.

Once the horizon period has successfully been determined, the market

price at the end of the period can be estimated. Third, do investors

perceive the estimating the market price?

COST OF EQUITY CAPITAL

The cost of equity capital may be defined as the rate of return

required by investors at the margin on the equity – financed portion of

an investor proposal, holding constant the capital structure, business

risk, and dividend policy of the firm.

The cost of equity capital can be derived from the valuation model:

Po + D1 + D2 + +Dn(1+Ke) (1+Ke)2 (1+Ke)n

ooM = Σ Dt

t=1 (1 + Ke)tWhere Po is the value of an ordinary share at time O, Dt is the

dividend per share expected to be paid in period t, and Ke is the rate of

discount appropriate for the businessrisk complexion of the company. If

the dividend is expected to be constant every year perpetually the above

equation becomes:

Po = DKe

Ke = DPo

The foregoing is a poor measure of cost, as it does not allow for any

growth. If, on the other hand, dividends per share are expected to grow

at a constant rate, g and Ke is greater than g, from the valuation

discussed in previous section we know that

Po = D1Ke g

Where D1 is the dividend per share expected to be paid at the end

of period 1, then the cost of equity capital is expressed as follows:

Ke = D1 + gPo

The foregoing equation assumes that the ordinary shares can be

issued at the appropriate market price without the firm incurring any

flotation expenses and any under pricing or market discount on the

shares. This is not always true as many firms that sell a new issue of

shares to the general public always find out that the issue had to be

priced below the current market price in order to make it attractive and

moreover, placing the issue always involve flotation costs. If the flotation

cost cum the market discount are expressed as a percentage, F, of the

gross price of the ordinary shares, Po, we may then express the cost of

equity capital, given constant growth in dividend; as follows:

Ke = D1 + g Po (1 – F)

The cost of equity capital where flotation and market discount are

taken into account is higher than where these are ignored. Also the

foregoing equations are only suitable where companies pay reasonable

but highly unsuitable for companies that either pay no dividends or pay

a negligible one. In such cases the cost of equity can be expressed as

follows:

Ke = Pn Po Po

Where Pn is the market price at period n,:. Pn – Po is the capital gain

expected due to the growth in the market price of the share in the

future.

Keown, Scott, Martins, and Petty (1985) described the

maximization of the firm’s shareholders wealth as the maximization of

the firm’s total value of its common stock. In the valuation of a firm’s

stock, the underlying principle is that of the fundamental theory of

share values which stipulate that the market value of a share is a

function of the future income stream to be earned by such a share,

including the terminal disposal value of the share, all discounted to the

present value, at the investor’s rate of time preference for money, or the

opportunity cost of the investment. (Duran, 1952).

The financial market places an emphatically heavy premium on

current and recent past earnings in forming impressions about future

returns. This notion would invariably and inevitably indicate that a

company that had a high return to its shareholders in the past, would

invariably be faced with penalties in future capital rationing, in that its

calculated cost of capital, and subsequently the cutoff rate for future

investments, would be high, and thereby reducing its profitable

investment opportunities. This seemingly paradoxical concept would

imply two things, viz:

i) The estimate of cost of capital will be based partially on current

yields, so that once the returns the shareholders have been receiving are

known, the share price of the company would rise and therefore bring

down the yield and part of the cost of capital.

ii) The oftendiscredited notion that past growth rates indicate

something about future growth rates cannot be completely ignored; this

is because many investors believe in this notion. A company with high

potentials and expectations for good performance would undoubtedly

disappoint its shareholders with only average returns. Its cost of capital

might consequently shoot up in order to satisfy and retain the

confidence of investors who provide the funds.

TRANSACTION COSTS

Secondary market fees in the Nigerian capital market stand at

about 3.875 percent of an offer proceeds and primary market fees take

about 7.54 percent of the proceeds. A comparative study done by a

London based ban on actual cost of transactions on some African

markets showed that fees payable to regulatory authorities remain

highest in Nigeria than in other stock exchanges while some regulatory

agencies in other parts of the world do not charge any fees at all. For

instance, the regulatory authorities in Botswana do not charge fees for

transactions on it stock exchange. Ghana, Kenya, Mauritius, Tunisia,

Ivory Coast and Zambia charge between 0.5 and 0.25 percent while

Nigeria charges 1.11percent.

Obaseki (2004) said high transaction cost hinder liquidity in the

market because it makes the market less competitive when dealing with

foreign portfolio investors. This serves as a disincentive to stockholders

who do all the work but earn less than the regulators. Moreso, market

making could not thrive under such high costs because high costs stifle

fixed income market.

The significant proportion of these costs go to the government in

form of tax and regulatory fees, while the statutory fees are fixed, fees

due to operators are negotiable. The high cost of transaction in the

market was one of the reasons that delayed the listing of the first

Federal Government N150 billion bonds as well as the low transaction in

it in the secondary market since it was listed. This is because stock

brokers argued that SEC, the capital market’s apex regulatory body,

would get more money than them in terms of fees whereas they were the

people that would engage in marketing of the bond.

The capital market is a source of cheap funds 4 to 9 percent

interest rate when compared to 18 to 21 percent in the money market.

Under the Investments and Securities Act (ISA), the cost of a

primary market issue should not exceed10% of the expected proceed of

the issue. In reality, perhaps to forestall under subscription, costs are

usually in the order of 6% maximum (apart from the marketing and

advertising costs). Of this, about 3% goes to the regulators (SEC and

NSE) as fees. The balance is shared between the coteries of adviser:

issuing house, stockbrokers, registrars, lawyers and accountants.

2.6 EFFICIENCY IN CAPITAL MARKET

Fama (1976) posited that capital market is efficient if prices “fully

reflect” all available information. The concept of efficient market theory

examines relationship between quoted share prices and published

information. There are four schools of thought in relation to these

theories.

I) TECHNICAL ANALYSIS SCHOOL OR CHARTISTS THEORY

Technical analysis, in essence, involves the study of historical price

and volume data either for one stock or a group of stocks and deducing

the future trend from this analysis. That is, the technicians endeavour

to predict future price levels of a stock by examining the past data from

the market itself. The underlying philosophy of technical analysis is

that the price of a stock depends on supply and demand in the market

place and has little relationships to intrinsic value, as the

fundamentalists believe it to be. Supply and demand, in turn, are

influenced by numerous factors both rational and irrational. The result

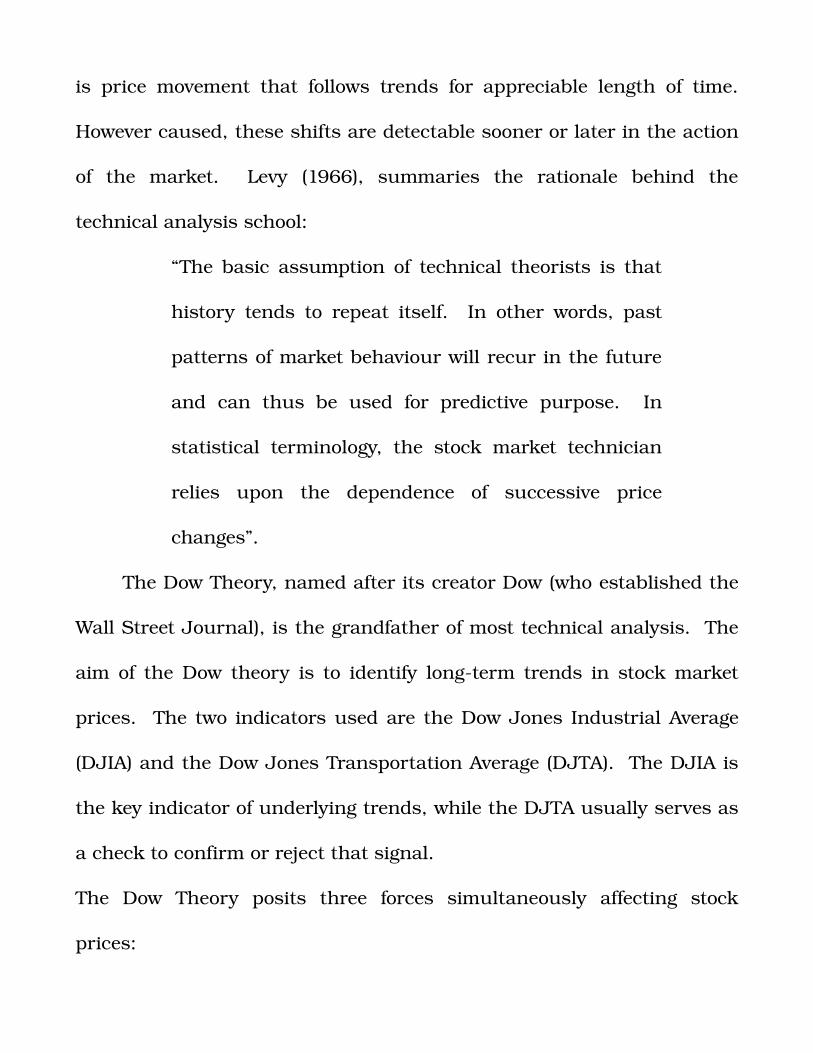

is price movement that follows trends for appreciable length of time.

However caused, these shifts are detectable sooner or later in the action

of the market. Levy (1966), summaries the rationale behind the

technical analysis school:

“The basic assumption of technical theorists is that

history tends to repeat itself. In other words, past

patterns of market behaviour will recur in the future

and can thus be used for predictive purpose. In

statistical terminology, the stock market technician

relies upon the dependence of successive price

changes”.

The Dow Theory, named after its creator Dow (who established the

Wall Street Journal), is the grandfather of most technical analysis. The

aim of the Dow theory is to identify longterm trends in stock market

prices. The two indicators used are the Dow Jones Industrial Average

(DJIA) and the Dow Jones Transportation Average (DJTA). The DJIA is

the key indicator of underlying trends, while the DJTA usually serves as

a check to confirm or reject that signal.

The Dow Theory posits three forces simultaneously affecting stock

prices:

1) The primary trend is longterm movement of prices, lasting from

several months to several years.

2) Secondary or intermediate trends are caused by shortterm

deviation of prices from the underlying trend line. These

deviations are eliminated via corrections, when prices revert

back to trend values.

3) Tertiary or minor trends are daily fluctuations of little

importance.

The Dow Theory is based on a notion of predictably recurring price

patterns. Yet the Efficient Market hypothesis (EMH) holds that if any

pattern were exploitable, many investors would attempt to profit from

such predictability, which would ultimately move stock prices and cause

the trading strategy to selfdestructive. Other chartist techniques involve

moving averages. In one version of this approach average prices over the

past several months are taken as indicators of the “true value” of the

stock. If the stock price is above this value, it may be expected to fall.

In another version the moving average is taken as indicative of longrun

trends. If the trend has been downward and if the current stock price is

below the moving average, then a subsequent increase in the stock price

above the moving average line (a “breakthrough”) might signal a reversal

of the downward trend. Another technique is called the relative strength

approach. The chartist compares stock performance over a recent

period to performance of the market or other stocks in the same

industry. A simple version of relative strength takes the ratio of the

stock price to a market indicator such as the S & P 500 index. If the

ratio increases over time, the stock is said to exhibit relative strength

because its price performance is better than that of the broad market.

Such strength presumably may continue for a long enough period of

time to offer profit opportunities.

Technical analysts also focus as on the volume of trading. The idea

is that a price deficit accompanied by heavy trading volume signals a

more bearish market than if volume we smaller, because the price

decline is taken as representing broaderbased selling pressure. Trading

index (trin statistic) is the ratio of average volume in declining issues to

average volume in advancing issues. Ratios above 1.0 are considered

bearish because the falling stocks would then have higher average

volume than the advancing stocks, indicating net selling pressure. Note,

however, that for every buyer there must be a seller of stock. High

volume in a falling market should not necessarily indicate a larger

imbalance of buyers versus sellers. For example, a trin statistic above

1.0, which is considered bearish, could equally well be interpreted as