“a-day” – a pensions bonanza? more choice and a fundamental change pensions – not products,...

TRANSCRIPT

“A-Day” – a pensions bonanza?

• More choice and a fundamental change

• Pensions – NOT products, investments

• “Long-term tax-relieved like ISAs or PEPs”*

• To fund 30 years of changing lifestyle

• “A period of work, education and leisure”**

* William Kay, Sunday Times, July 2005

** HSBC Survey, May 2005.

Retirement Distribution Planning

As You Approach Retirement

“How do I accumulate more funds?”

“Will my funds last throughout my retirement years?”

Investment Philosophies

Consider Retirement Phases

• Trips in segments — Retirement in Phases • Phases defined by activity levels• Retirement expenses vary with activity

Retirement Expenses by Phases

70% Basic Needs – 20% Extra Wants

70% Basic Needs – 10% Extra Wants

70% Basic Needs

60% of Prior Income

“How much do we need to maintain our lifestyle and to have the retirement we’ve dreamed?”

Retirement Planning

• Family Tree• Better Health Care• Medical Advances

“How long should we plan for?

We don’t want to outlive our assets!”

Investments During Retirement

• Predictable income for current phase • Predictable income from very

conservative investments• More risk and return for assets used for

later phases• Longer time horizon prior to phase, the

more aggressive the investments• Shift assets as retirement phases

change

Steps for Retirement Journey

Determine the likely times of retirement phases

Requirements– Basic Needs

– Additional Wants

Known Income–State Benefits

–Pension

–Retirement Plans

–Annuities & Other

Analysis Desired Income

less Known Income

equals Remaining Requirements

Six Questions

1. When do you want to retire?

2. How much monthly income do you need?

3. Current value of retirement plans? (Co. Schemes, Pers Pens, Stakeholder,SIPPs, SASSs etc.)

4. Current value of retirement assets?

5. Illustrate State Benefits ?

6. Any other retirement income?

Retirement Destination

Monthly Needs in Today’s Money(Typical Needs in Today’s Pounds if Current Income Is £5,000 Monthly)

Begins at Robert’s Age

Basic Needs

Additional Wants

Total Desired

65 £3,500 £1,500 £5,000

75 £3,000 £1,000 £4,000

85 £2,700 £0 £2,700

92 £2,500 £0 £2,500

Comparing Income & Sources

• Show monthly needs and additional wants• Adjust for estimated inflation

Comparing Income & Sources

• Apply Social Security estimates

Comparing Income & Sources

• Add qualified retirement plan distributions

Comparing Income & Sources

• Add income from other known sources• Determine the remaining amount required

Required for Remaining IncomeAssets Required in Today’s Money

Basic Needs

Additional Wants

Total Desired

£18,654 £235,619 £254,273

£54,039 £135,578 £189,617

£84,590 £0 £84,590

£151,776 £0 £151,776

Total £309,059 £371,197 £680,256

Funding Each Phase

• If income is being received, very conservative – predictable

• If next phase, conservative so little fluctuation when time to convert to income

• For phases years away, seek maximum yields – moderate and aggressive

• Funding changes as you move to next phase

Timing Determines Investments

Very Conservative

Conservative

Moderate

Aggressive

Capital PreservationVery secured, predictable

Income AssetsSecured, minimum fluctuation

Income and GrowthFluctuates with market conditions

Growth AssetsLong-term growth but fluctuations

Yields and Risks

• Low Yields / Low Risks• High Yields / High Risks

Money Required for Each Phase

• Funding early retirement phase• £254,273 invested conservatively until retirement• At retirement, it could be invested very

conservatively—predictably• It could provide the additional income for this phase

Money Required for Each Phase

• Funding seasoned retirement phase• £189,617 invested moderately until retirement• At retirement, invested conservatively• When seasoned retirement starts, invest predictably• Income during the seasoned retirement years very

secured

Money Required for Each Phase

• Funding matured retirement phase• £84,590 invested aggressively until retirement• At retirement, invested moderately• When seasoned retirement starts, invest conservatively• When matured retirement starts, invest very conservatively• Income during the matured retirement years very secured

Money Required for Each Phase

• Funding survivorship phase• £151,776 invested aggressively until seasoned phase• When seasoned retirement starts, invest moderately• When matured retirement starts, invest conservatively• At spouse’s death, invest very conservatively• Income during the survivorship years very secured

Combination of Funding for All Phrases

A year-by-year allocation of investments for the remaining monthly needs

Asset Mix for Remaining Amounts Required

“Can I use this as a guide to adjust my investments at the start of each phase?"

Applying Retirement Assets

Assets designated for retirement can provide a portion of the remaining income desired.

“Will our retirement assets solve our needs?”

Annuity for Guarantee IncomeLife InsuranceRe-Investment of AssetsAre Goals Unrealistic?Best Use of Qualified PlansEstate Planning Comprehensive Planning Delay Retirement Unexpected ExpensesAnnuity as the Conservative Investment Allocation of Assets

What Should You Recommend?

How do you decide what to recommend?

Proceed with Recommendations

• “Intelligent” recommendations at end of PlanFacts (quick fact finder)

• Only recommend if appropriate• Provides calculations needed to decide• Re-calculates with each recommendation• Complete all recommendations in one pass!• Prints “Brochure,” “Analysis,” and

“Recommendations” at one time

How to Take Qualified Retirement Plan Distributions

Propose an Annuity for Guaranteed Income

Life Insurance Eliminates Assets for Survivorship Phase

Protect Against the Unexpected

Other Available Recommendations

How Should You Take Your Retirement?

• As Needed—defers needs• Level—spreads over retirement years• Required Minimum Distributions—less early income

What is an annuity?

• When Payments Begin– Immediate– Deferred

• How Values Are Determined– Fixed – a stated interest rate– Variable – fluctuates based on equities

• Ways Annuities Pay Lifetime Income– Lifetime income– Guaranteed payment periods– Based on two lives

“What are the different types of annuities?”

An Alternative – Using an Annuity

A lump sum could be added to an annuity and an income could be received throughout retirement, reducing the amount required for the remaining monthly income needs.

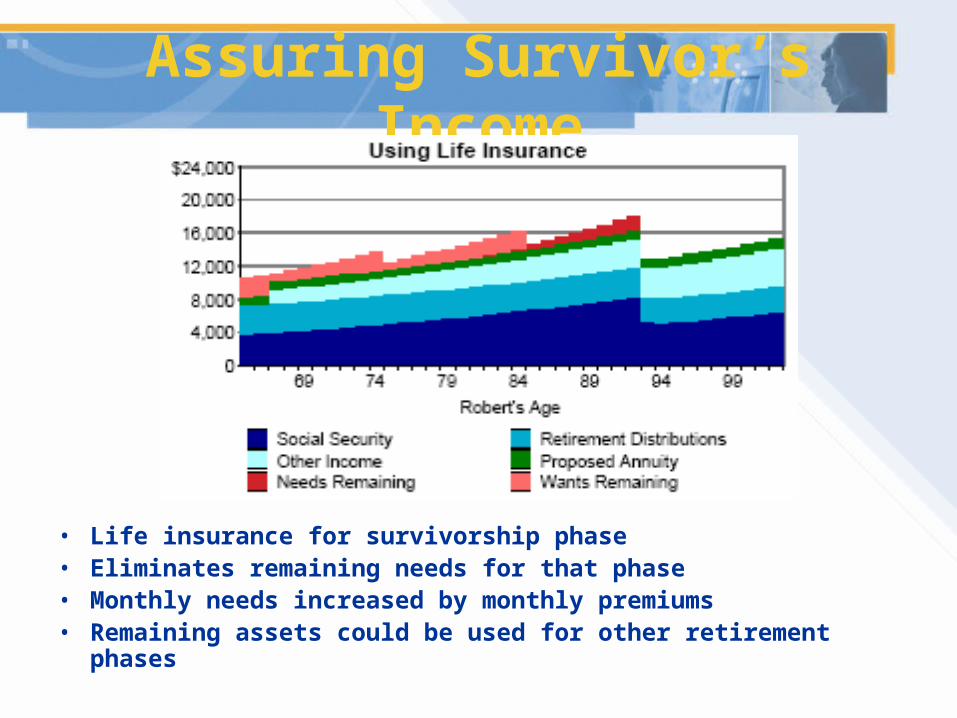

Assuring Survivor’s Income

• Life insurance for survivorship phase• Eliminates remaining needs for that phase• Monthly needs increased by monthly premiums• Remaining assets could be used for other retirement phases

Survivorship Questions

• Permanent, cash value life insurance is the key• If death occurs earlier than assumed, we’ll probably

have extra• If death is later, the cash value (via withdrawals or

policy loans) may be used• You must examine all policy provisions well before

purchasing any life insurance

“But wouldn’t the amount of life insurance be determined by when one of us dies? It’ll probably be different than what we are assuming?”

Recommendations Applied

• Qualified retirement plan distribution applied• Includes annuity income• Illustrates life insurance • Assets applied to remaining objectives

The Unexpected—”What if…?”

• Illustrate affects of an unexpected retirement need • Long-Term Care, Critical Illness, Cancer, Accident• Show how insurance protects against the

unexpected

Personalized Recommendations

• All recommendations are detailed as part of presentation

• Company specific products recommended

• Other planning can be recommended:– Estate Planning– Comprehensive Planning– Qualified Plan Distribution– Asset Allocation

• Annual reviews

A new name for pensions?

• S

• M

• I

• L

• E

* William Kay, Sunday Times, July 2005

A new name for pensions?

• Save• Money and

• Invest for

• Life’s

• Enjoyment

* William Kay, Sunday Times, July 2005

Peace-of-mind for your retirement journey