a day in the life of an auditor at the division of state internal audit the state employee fraud,...

TRANSCRIPT

A Day in the Life of an A Day in the Life of an Auditor at the Division of Auditor at the Division of

State Internal AuditState Internal Audit

The State Employee Fraud, The State Employee Fraud, Waste, and Abuse HotlineWaste, and Abuse Hotline

How many calls do we answer in a How many calls do we answer in a typical day?typical day?

There are some days that we There are some days that we respond to 10 callsrespond to 10 calls

There are some days that we There are some days that we respond to four callsrespond to four calls

And there are some days that we do And there are some days that we do not get any calls for the Hotlinenot get any calls for the Hotline

Calls to the HotlineCalls to the Hotline

Are all calls to report allegations of fraud, Are all calls to report allegations of fraud, waste, and abuse?waste, and abuse?• No, some calls are just to find out how the No, some calls are just to find out how the

Hotline worksHotline works• Some are to check on the status of an Some are to check on the status of an

investigationinvestigation• Some are to provide additional information to Some are to provide additional information to

an original callan original call• And some are to check to see if the And some are to check to see if the

investigator has any questions for the callerinvestigator has any questions for the caller

The DSIA AuditorsThe DSIA Auditors We are auditors, too!We are auditors, too! We have the same experience, skills, We have the same experience, skills,

and certifications as agency auditorsand certifications as agency auditors When investigations involve agency When investigations involve agency

heads or other auditors we will heads or other auditors we will perform the investigationperform the investigation

We will write and issue the We will write and issue the investigative reportinvestigative report

The Call to the HotlineThe Call to the Hotline

Thank you for calling the State Thank you for calling the State Employee Fraud, Waste, and Abuse Employee Fraud, Waste, and Abuse Hotline, please do not disclose your Hotline, please do not disclose your identity, are you calling back about a identity, are you calling back about a case that you have previously case that you have previously reported?reported?

The Screen Out ProcessThe Screen Out Process

The DSIA uses two screening processes to The DSIA uses two screening processes to determines if the call falls within the scope determines if the call falls within the scope of the Hotline Policyof the Hotline Policy

The first screen out process determines if The first screen out process determines if the allegation is for an executive branch the allegation is for an executive branch agency, or if the caller should be directed agency, or if the caller should be directed to another agency for assistanceto another agency for assistance

Each Hotline call that is assigned a case Each Hotline call that is assigned a case number goes through a second screening number goes through a second screening processprocess

The Second Screen Out ProcessThe Second Screen Out Process

How material are the allegations?How material are the allegations? How timely are the allegations?How timely are the allegations? Did the caller provide enough detail Did the caller provide enough detail

to perform an investigation?to perform an investigation?

Gathering the InformationGathering the Information

Its our job to obtain as much detailed Its our job to obtain as much detailed information as possible from the information as possible from the caller about the allegationcaller about the allegation

This can, at times, be very difficultThis can, at times, be very difficult We try to put the caller at ease We try to put the caller at ease

The CallerThe Caller

Many of the callers are fearful about Many of the callers are fearful about calling the Hotlinecalling the Hotline

Many callers are fearful that they will Many callers are fearful that they will not remain anonymousnot remain anonymous

Many callers are fearful of retaliation Many callers are fearful of retaliation from their agencyfrom their agency

The identity of the caller is The identity of the caller is anonymous and the information they anonymous and the information they provide is kept confidentialprovide is kept confidential

The Caller (continued)The Caller (continued)

Some callers are reporting the allegation Some callers are reporting the allegation to us as second hand informationto us as second hand information

Some callers don’t have all the facts about Some callers don’t have all the facts about the allegation when they callthe allegation when they call

We have to ask open-ended questions to We have to ask open-ended questions to get the callers to give us information get the callers to give us information about the allegationabout the allegation

Some callers report more than one Some callers report more than one allegationallegation

The Caller (continued)The Caller (continued)

Some callers will send us their Some callers will send us their allegations by mail, email, or faxallegations by mail, email, or fax

Many callers will broadly state that Many callers will broadly state that everyone knows what is going oneveryone knows what is going on

Unfortunately, often when employees Unfortunately, often when employees are interviewed, the information are interviewed, the information provided is of little helpprovided is of little help

The Caller (continued)The Caller (continued)

We ask for the names of witnessesWe ask for the names of witnesses Some callers will provide the names Some callers will provide the names

of witnessesof witnesses Sometimes the witnesses have some Sometimes the witnesses have some

information which is helpfulinformation which is helpful Sometimes the witnesses do not Sometimes the witnesses do not

have any useful informationhave any useful information

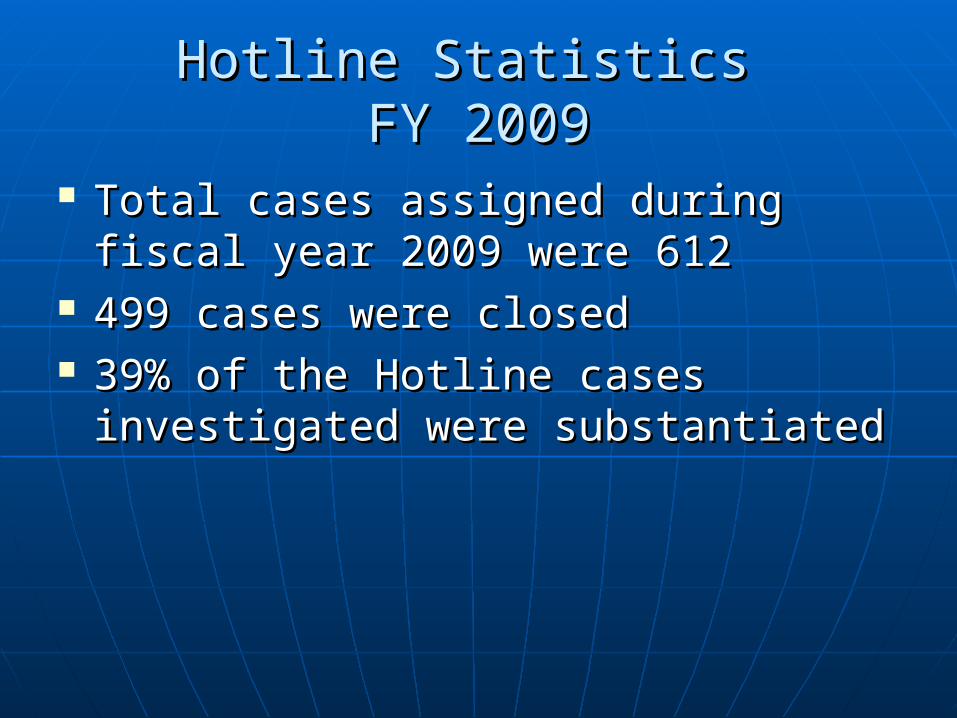

Hotline Statistics Hotline Statistics FY 2009FY 2009

Total cases assigned during fiscal Total cases assigned during fiscal year 2009 were 612year 2009 were 612

499 cases were closed499 cases were closed 39% of the Hotline cases 39% of the Hotline cases

investigated were substantiatedinvestigated were substantiated

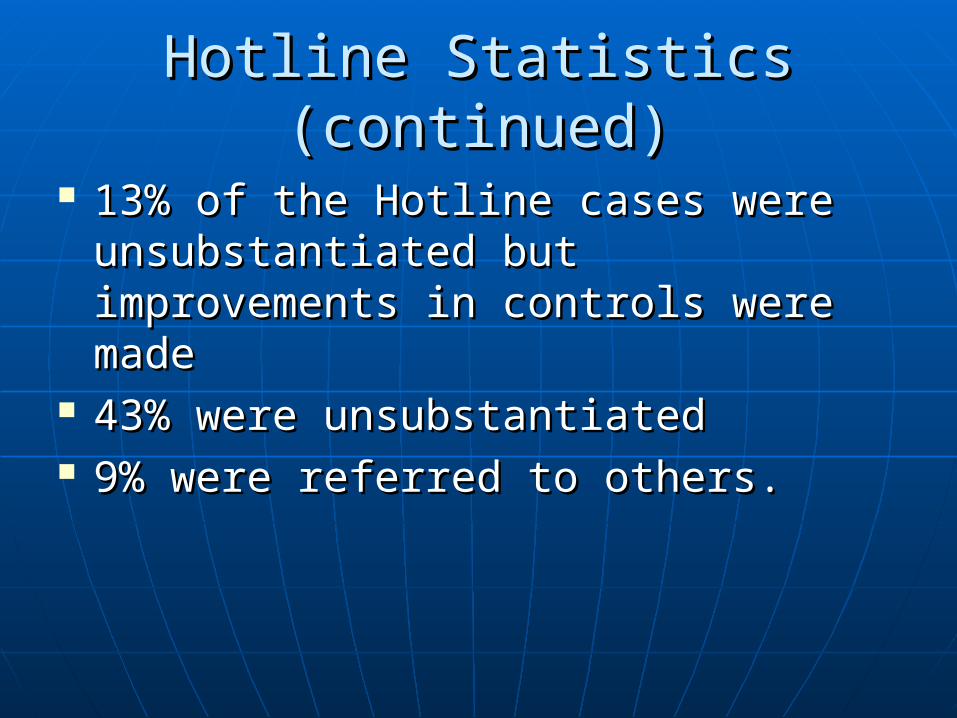

Hotline Statistics (continued)Hotline Statistics (continued)

13% of the Hotline cases were 13% of the Hotline cases were unsubstantiated but improvements in unsubstantiated but improvements in controls were madecontrols were made

43% were unsubstantiated43% were unsubstantiated 9% were referred to others. 9% were referred to others.

Common AllegationsCommon Allegations

State vehicle abuse: 62 casesState vehicle abuse: 62 cases Abuse of the State’s leave policy:68 Abuse of the State’s leave policy:68

casescases Unnecessary purchases: 40 casesUnnecessary purchases: 40 cases

Cases Assigned by CategoryCases Assigned by Category

CategoryCategory FY 2009FY 2009 FY 2008FY 2008 FY 2007FY 2007

AbuseAbuse 381381 391391 229229

WasteWaste 139139 115115 104104

FraudFraud 7070 6161 4343

PersonnelPersonnel 00 1919 2020

OtherOther 00 1313 4747

TotalTotal 612612 599599 443443

Cases Assigned by TypeCases Assigned by TypeTypeType FY 2009FY 2009 FY2008FY2008 FY 2007FY 2007

Misuse of State Misuse of State VehicleVehicle

6262 6161 2626

Leave AbuseLeave Abuse 6868 6767 3737

Improper HiringImproper Hiring -- 3939 --

Non-compliance Non-compliance with agency with agency internal policyinternal policy

3939 3838 2727

Employee Employee MisconductMisconduct

5757 3737 2626

Poor ManagementPoor Management -- -- 4444

Misuse of State Misuse of State Equip.Equip.

-- -- 3535

All Other TypesAll Other Types 346346 357357 248248

TotalTotal 612612 599599 443443

Cases Substantiated by CategoryCases Substantiated by Category

CategoryCategory FY 2009FY 2009 FY 2008FY 2008 FY 2007FY 2007

AbuseAbuse 126126 127127 8484

WasteWaste 3232 3434 3232

FraudFraud 1414 2222 1010

PersonnelPersonnel 66 44 1818

OtherOther 11 44 1414

TotalTotal 179179 191191 158158

Documenting the AllegationDocumenting the Allegation

We write up the allegation in a clear We write up the allegation in a clear and concise format for the Agency and concise format for the Agency auditor to investigateauditor to investigate

Sometimes, depending on the Sometimes, depending on the allegation and or the Agency, we allegation and or the Agency, we may do some preliminary research to may do some preliminary research to assist the agency auditorassist the agency auditor

Documenting the Allegation Documenting the Allegation (continued)(continued)

We make and mail a copy of the We make and mail a copy of the allegation write-up to the Agency allegation write-up to the Agency Internal Audit DirectorInternal Audit Director

We keep the original write-up in the We keep the original write-up in the DSIA Hotline filesDSIA Hotline files

We enter the Hotline case We enter the Hotline case information into the DSIA databaseinformation into the DSIA database

Documenting the Allegation Documenting the Allegation (continued)(continued)

The agency is given 60 days to complete The agency is given 60 days to complete its investigationits investigation

The agency provides a written report to The agency provides a written report to the DSIAthe DSIA

We review the Agency Internal Auditor’s We review the Agency Internal Auditor’s investigative report to ensure that it investigative report to ensure that it adequately addresses the allegationsadequately addresses the allegations

We close the case in the DSIA databaseWe close the case in the DSIA database

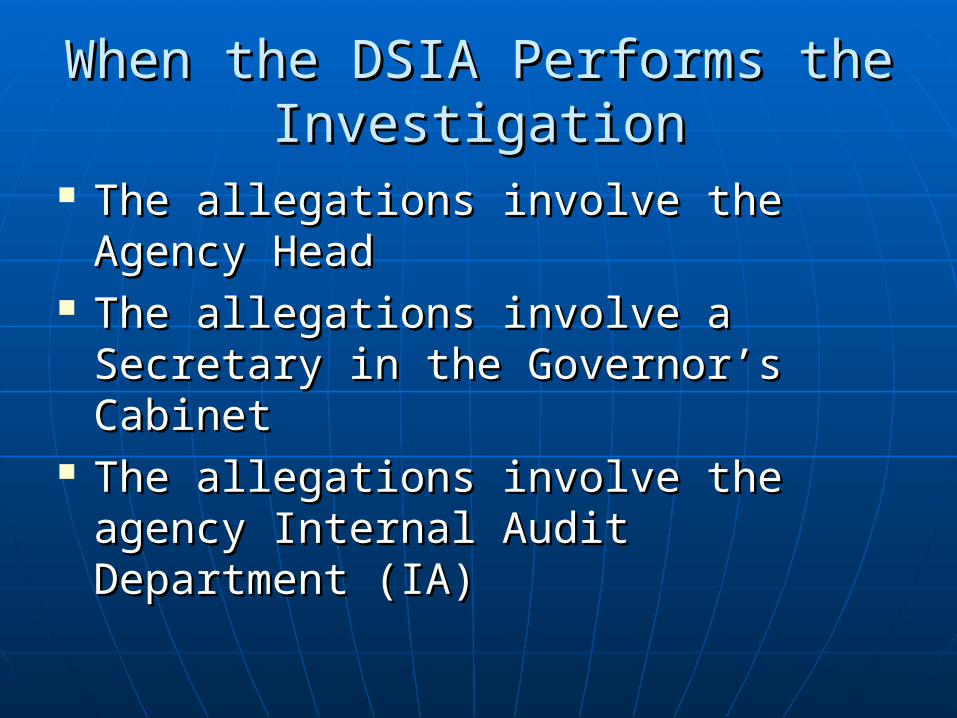

When the DSIA Performs the When the DSIA Performs the InvestigationInvestigation

The allegations involve the Agency The allegations involve the Agency HeadHead

The allegations involve a Secretary in The allegations involve a Secretary in the Governor’s Cabinetthe Governor’s Cabinet

The allegations involve the agency The allegations involve the agency Internal Audit Department (IA)Internal Audit Department (IA)

When the DSIA Performs the When the DSIA Performs the Investigation (continued)Investigation (continued)

There may be an appearance of a There may be an appearance of a conflict of interest if the agency IA conflict of interest if the agency IA Department performs the Department performs the investigationinvestigation

The agency does not have an IA The agency does not have an IA Department or Hotline CoordinatorDepartment or Hotline Coordinator

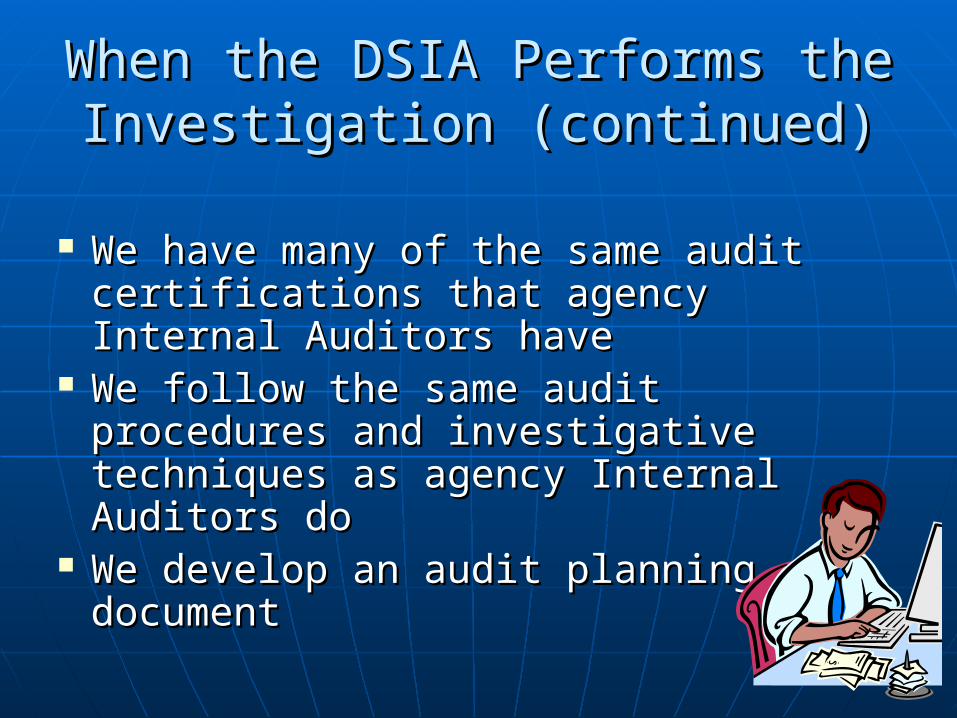

When the DSIA Performs the When the DSIA Performs the Investigation (continued)Investigation (continued)

We have many of the same audit We have many of the same audit certifications that agency Internal certifications that agency Internal Auditors haveAuditors have

We follow the same audit procedures We follow the same audit procedures and investigative techniques as and investigative techniques as agency Internal Auditors doagency Internal Auditors do

We develop an audit planning We develop an audit planning documentdocument

When the DSIA Performs the When the DSIA Performs the Investigation (continued)Investigation (continued)

We gather data and evidenceWe gather data and evidence We interview witnessesWe interview witnesses We interview the subject(s)We interview the subject(s) We document our findings in our We document our findings in our

work paperswork papers We analyze our findingsWe analyze our findings

When the DSIA Performs the When the DSIA Performs the Investigation (continued)Investigation (continued)

We review our findings with the Audit We review our findings with the Audit ManagerManager

We make recommendations for We make recommendations for corrective action to the agencycorrective action to the agency

Our work papers are confidentialOur work papers are confidential

DSIA ResourcesDSIA Resources

Department of Human Resource Department of Human Resource ManagementManagement

Commonwealth Accounting Policies Commonwealth Accounting Policies and Procedures Manual (CAPP and Procedures Manual (CAPP Manual)Manual)

PaylinePayline Personnel Management Information Personnel Management Information

System (PMIS)System (PMIS) The InternetThe Internet

DSIA Resources (continued)DSIA Resources (continued)

The Commonwealth Accounting and The Commonwealth Accounting and Reporting System (CARS)Reporting System (CARS)

The Small Purchase Charge Card The Small Purchase Charge Card detaildetail

The Reid Interview TechniqueThe Reid Interview Technique

ReportingReporting

We write an audit report that will be We write an audit report that will be issued to an Agency Head, a issued to an Agency Head, a Governor’s Cabinet Secretary, and/or Governor’s Cabinet Secretary, and/or to the Governor’s Chief of Staffto the Governor’s Chief of Staff

We request a response to our audit We request a response to our audit reportreport

We evaluate the appropriateness of We evaluate the appropriateness of the response to our reportthe response to our report

The Audit ReportThe Audit Report

Our audit report contains:Our audit report contains:• The Scope of the InvestigationThe Scope of the Investigation• The Allegation(s)The Allegation(s)• The Finding of FactThe Finding of Fact• The ConclusionThe Conclusion• RecommendationsRecommendations

DSIA Statistical DataDSIA Statistical Data

Information regarding each Hotline Information regarding each Hotline case is entered into our DSIA case is entered into our DSIA databasedatabase

The information in our database can The information in our database can be queried in many waysbe queried in many ways

We issue monthly internal reports of We issue monthly internal reports of Hotline statisticsHotline statistics

DSIA Statistical Data (continued)DSIA Statistical Data (continued)

Quarterly, Hotline status reports are Quarterly, Hotline status reports are requested from Agency Auditors on requested from Agency Auditors on cases older than 60 days cases older than 60 days

Annually, a Hotline statistical report Annually, a Hotline statistical report is issued to the State Comptroller, is issued to the State Comptroller, the Secretary of Finance, and the the Secretary of Finance, and the Governor’s Chief of StaffGovernor’s Chief of Staff

Cases Assigned and Closed by Cases Assigned and Closed by DSIADSIA

Fiscal YearFiscal Year Open Open Cases Cases

Beginning Beginning of Yearof Year

Cases Cases AssignedAssigned

Cases Cases ClosedClosed

Open Open Cases End Cases End

of Yearof Year

FY 2009FY 2009 2222 4848 5252 1818

FY 2008FY 2008 2525 4545 4848 2222

FY 2007FY 2007 1818 4141 3434 2525

TotalTotal 111111 121121

Cases Assigned and Closed by Cases Assigned and Closed by DSIADSIA

Fifty-two cases were closed during 2009, an Fifty-two cases were closed during 2009, an increase of 4 from 2008:increase of 4 from 2008:• Twenty-seven (52% of closed cases) involved Twenty-seven (52% of closed cases) involved

substantiated allegationssubstantiated allegations• Six (11% of closed cases) involved Six (11% of closed cases) involved

unsubstantiated allegations but unsubstantiated allegations but recommendations were maderecommendations were made

• Three (6% of closed cases) involved allegations Three (6% of closed cases) involved allegations that were unsubstantiated that were unsubstantiated

• Sixteen (31% of closed cases) were screened outSixteen (31% of closed cases) were screened out ““Cases assigned” and “cases closed” Cases assigned” and “cases closed”

include screened out cases include screened out cases

QuestionsQuestions