a developer’s view - rushlightevents.com · • manchester – 12 mwe advanced thermal treatment...

TRANSCRIPT

A Developer’s View

Myles Kitcher Rushlight Events: Waste to Energy; 5th June 2013

Peel Environmental

Market Overview

The Challenge

Mitigating Project Risk

Looking Forward

Introduction

Peel Environmental

Peel Environmental Limited owns, manages and develops property in the waste, mineral and environmental technology sector

Key Business Areas: Energy from Waste • Large / medium scale conventional technology • Advanced Thermal Treatment

Anaerobic Digestion Construction, Demolition & Excavation Waste • Inert • Hazardous • Remediation Resource Recovery Parks • Environmental technology business park (e.g. Ince Park)

Unconventional Gas • Facilitating exploration activity • Downstream opportunities Landholding • Maximise value in existing assets (circa 3,000 acre landholding)

• Ince Park, Cheshire – 95MWe energy from waste providing heat and electricity to existing industry and

anchor for new investment

• South Clyde Energy Centre, Glasgow – 20MW energy from waste, heat off-taker, focussed on PPP

contract

• North Selby, York – 2.75 MWe anaerobic digestion with heat to horticultural grower

• Southmoor Energy Centre, Knottingley - 26 MWe EfW providing electricity to adjacent colliery and

heat to wider industry

• Manchester – 12 MWe advanced thermal treatment with heat for cooling adjacent occupier

• Nottinghamshire – 12 MWe advanced thermal treatment with heat to industry

Peel Environmental

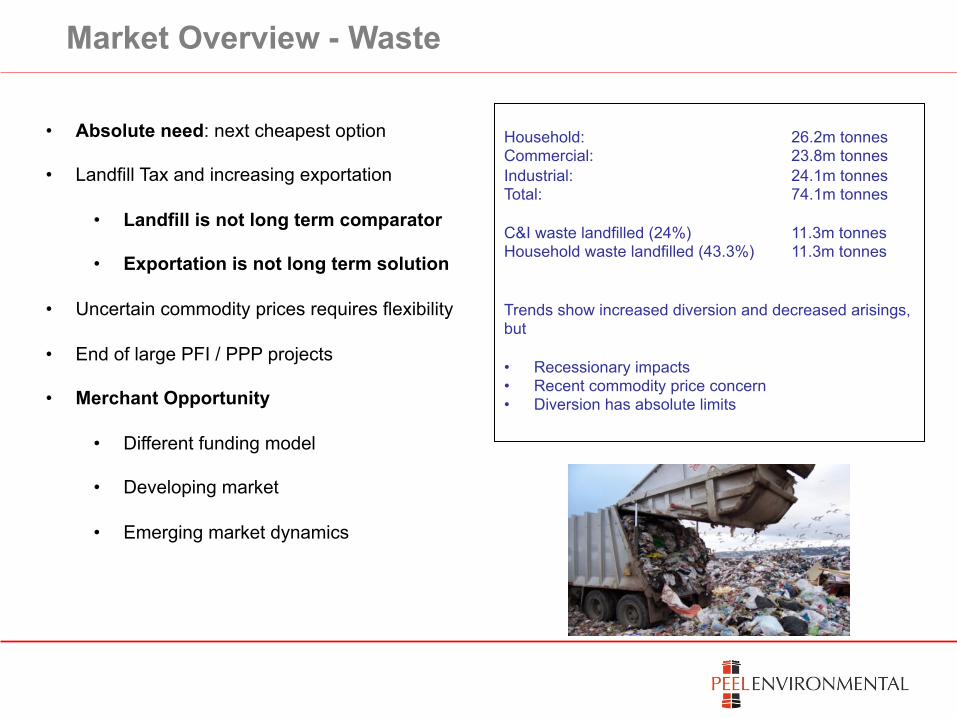

• Absolute need: next cheapest option

• Landfill Tax and increasing exportation

• Landfill is not long term comparator

• Exportation is not long term solution

• Uncertain commodity prices requires flexibility

• End of large PFI / PPP projects

• Merchant Opportunity

• Different funding model

• Developing market

• Emerging market dynamics

Market Overview - Waste

Household: 26.2m tonnes Commercial: 23.8m tonnes Industrial: 24.1m tonnes Total: 74.1m tonnes C&I waste landfilled (24%) 11.3m tonnes Household waste landfilled (43.3%) 11.3m tonnes Trends show increased diversion and decreased arisings, but • Recessionary impacts • Recent commodity price concern • Diversion has absolute limits

• Energy costs will rise in the short, medium and, probably, long term

• Brown electricity predicted to increase by circa 40% in 10 years

• Demand for low carbon and CSR implications

• Market support mechanisms distort market – gate fee driven

• Waste is not the answer to the UK’s energy gap but part of the mix, however;

• Potential for major local impact

• Embedded, low carbon energy solution providing stimulus for inward investment

• “Energy Intensive Industries” - in the UK employ around 620,000 people and contribute over £49 billion

in goods and services to the economy (2008) – pressure to reduce greenhouse gas emissions (CCL etc.)

Market Overview - Energy

• Property and Planning

• traditional barrier, remains an issue but capacity is being consented

• de-risk at early stage

• Funding

• merchant risk in current economic climate requires different funding model

• Construction phase and re-finance

• Or available balance sheet

• Regulatory

• market support and control mechanisms – lack of stability

• Technology

• deliverability and competiveness

• Contractual

• In-take and off-take

• security, longevity, composition

The Challenge

• Technology agnostic

• Efficiency – increasing energy component

• Economically advantageous:

• Reduced cost to consumer and better for the economy

• Competitive advantage – future gate fee competition

• Investor confidence and mitigating contract risk

• Managing fuel supply – calorific value and biogenic content

• Market support mechanisms – distorts market

Mitigating Risk - Technology

• Market analysis

• Technology solution

• Fuel supply contract

• Market capacity – waste & competition

• Energy offer - two approaches:

• Opportunistic – co-locate adjacent existing heat user

• Planned - embedded energy centre

• supports the deployment of smaller scale plant

• Enhanced utility solution – Energy / Multi-Utility Service Company (ESCO / MUSCO) arrangements

• Private wire electricity

• Improved margins = long term competiveness

• Enhanced efficiency is a function of technology and location

Mitigating Risk - Location, Location, Location

Gate fee competition

Technological innovation and disruptive technology:

Gas turbine to electricity

Liquefied gas to transport fuel (road and aviation)

Gas to Grid

Hydrogen fuel cell

“Black swan” technology

Disruptive funding

Driven by market economics – stranded assets

Supported by regulation and market support mechanisms but – stability would be helpful

currently ROC till 2017 and thereafter EMR, expansion of RHI and extension of RO to 2020 would help….

But… market fundamentals are good

Looking forward….

For further informa.on: Myles Kitcher Director Peel Environmental Limited Peel Dome The Trafford Centre Manchester M17 8PL mailto: [email protected] Website: www.peel.co.uk/environmental Telephone: 0161 6298200