a discussion of fatca and selected changes in the tax …€¢imposes new reporting and withholding...

TRANSCRIPT

#14219051v1

International Tax Issues A Discussion of FATCA and Selected Changes in the Tax Laws of South Korea, Australia, China and India

PEI Fund Compliance Forum | May 3, 2011

William D. LaFayette Managing Director and CFO

Steven D. Bortnick

2

Part I

FATCA

3

Current Rules – UBS Abuse

Acct. Holder FPC

SH

UBS

interest & capital gains invests in U.S. securities

4

Current Rules – UBS Abuse

• UBS provides U.S. payor with certificate that interest and capital gains allocable to FPC − No U.S. tax on interest (portfolio interest) or capital gains

• SH is U.S. person − Evades U.S. tax

5

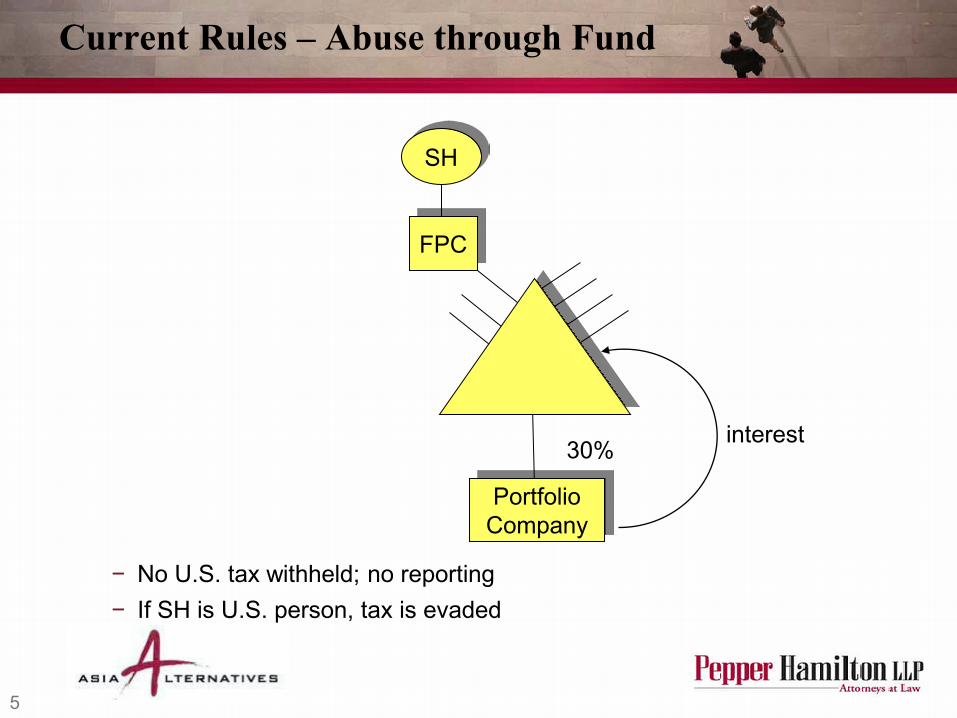

Current Rules – Abuse through Fund

interest 30%

FPC

Portfolio Company

SH

− No U.S. tax withheld; no reporting − If SH is U.S. person, tax is evaded

6

Enter FATCA

• Imposes new reporting and withholding tax regime on payments of U.S. source “withholdable payments” to foreign entities

• The world is divided into − Foreign financial institutions (“FFI”) − Non financial foreign entities (“NFFE”)

• Effective date − Generally for payments made after 12/31/2012 − No FATCA withholding on “obligations” that are outstanding on or

before March 18, 2012

7

FATCA

• New Regime − Payments of “withholdable payments” to foreign entities subject to

30% withholding tax unless recipient agrees to comply with new disclosure rules

• Withholdable payment − U.S. Source Interest (including portfolio interest), dividends, and

other fixed determinable annual or periodic income AND − Gross proceeds from the disposition of property (stocks or bonds)

that can produce U.S. source interest or dividends

8

Payments to FFI

• Withholdable payment subject to 30% withholding unless − FFI enters into agreement with IRS to disclose information about

certain U.S. account holders, including name, address, account balance, gross receipts, OR

− FFI agrees to be treated as a U.S. financial institution and treat each holder of a U.S. account that is a specified holder as a U.S. person, and thus being subject to 1099 reporting, etc. Eliminates need to report account balance

− Known as 1471(b) agreements

9

What is an FFI?

• Foreign bank, foreign custodian and foreign entities “primarily engaged in the business of investing, re-investing or trading in securities, partnership interests or commodities or any interest in such items − Includes foreign hedge funds, foreign private equity funds, − “Foreign Entity” means any entity that is not a U.S. person

• Place of organization key for corporations and partnerships

10

Fund Structures

• U.S. Fund pays U.S. source interest or capital gains − Cayco and Cayco LLC must enter into agreement with IRS to provide

information on all U.S. account holders (LPs), including looking through FPC

Cayco Cayco LLC

U.S. Fund

FPC FPC USTE

Foreign Individuals USTP

11

Fund of Fund Structure

• Payment to Foreign Hedge Fund is subject to 30% unless FHF is compliant with reporting

• For FHF to be compliant Cayco Fund must advise FHF of the specified U.S. persons in Cayco Fund and comply with information reporting

Cayco Fund

Foreign Hedge Fund

U.S. source interest capital gains from investment

12

Certification Approach – Notice 2010-60

• Notice sets out detailed rules on diligence that must undertake. • Notice indicates that Treasury/IRS considering allowing MNCs to rely on

certifications from entity payees as to their FATCA treatment (i.e., good or bad FFIs or NFFEs).

− Substantially less burdensome than documentation and due diligence requirements expected of financial institutions paying holders of “financial accounts.”

− Just following this approach still requires identification of substantial U.S. owners of entity payees.

− Would these certifications be an official IRS form or could each taxpayer create its own?

− What information would be needed on such a certification?

− Would there be any associated due diligence required? (Presumably at odds with “reliance” concept.)

− Would the certifications need to be renewed periodically?

− How about monitoring any changed circumstances in FATCA treatment of entity (e.g., “good” FFI goes “bad”; entry of new substantial U.S. owners, etc.)?

13

Notice 2010-60 - Holding Companies

• Foreign entity formed to be holding company for subsidiary or group primarily engaged in trade or business other than FI excluded as FFI. − No help to fund, but

helps portfolio cos. • Is FC still exempt

holding company? • PE funds will sell FC, so

FC should not be an “investment vehicle.”

FC

dividend

FC1 USC FC2

dividend

PE Funds

14

Part II

Selected Changes in the Tax Laws of South Korea, Australia,

China and India

15

General Tax Considerations in Cross-Border Investing

• Minimize taxes in foreign jurisdiction • Avoid taxation before cash receipts (“phantom income”) • Maintain capital gain on exit/partial exit and qualified dividend

income on distributions • Avoid/minimize tax on leveraged recap • Avoid/minimize foreign withholding taxes • Avoid UBTI for tax-exempt investors • Maintain VCOC status of the fund • Will a buyer like the structure or be able to restructure on a tax

efficient basis? • What does it take/cost to implement and maintain structure?

16

PE Investment in PRC – Circular 698

• Released December 10, 2009, effective January 1, 2008. • Permits taxation of gain on sale of non PRC holding companies

of PRC companies. • Initial impetus on withholding agent to withhold tax. • If no withholding, seller must file return and pay tax within 7 days

of transfer. • Provides rules for determining purchase price if in non-PRC

currency. • If tax rate on seller is <12.5%, subject to

information/documentation request. • Tax authorities allowed to ignore holding company under

substance over form doctrine. • Ability to adjust purchase price if not arms’ length.

17

PE Investment in China – Jiangsu Case

• PRC taxed sale of Hong Kong under GAAR

• Hong Kong lacked substance − No employees − No assets/liabilities other

than Jiangsu − No operational activities

Hong Kong

Offshore Intermediate

Co.

Jiangsu

US Group

49%

18

Investment in India – Vodafone

• India proceeded against Vodafone for failure to withhold

• Transaction was indirect transfer of controlling interest in Indian operating co.

• Government – transaction involved transfer of control premium, right to use Hutch brand in India and non-compete and certain intra-group being and option rights – all Indian

• Bombay High Court – diverse rights and entitlements gave had sufficient nexus with India

• Scheduled for hearing before Supreme Court in July

Vodafone Int’l Holdings

BV

Hutchinson Essex Ltd.

(India)

CGP Investments

(Cayman)

Marketing Holding

Cos.

Vodafone UK

Essex Group

19

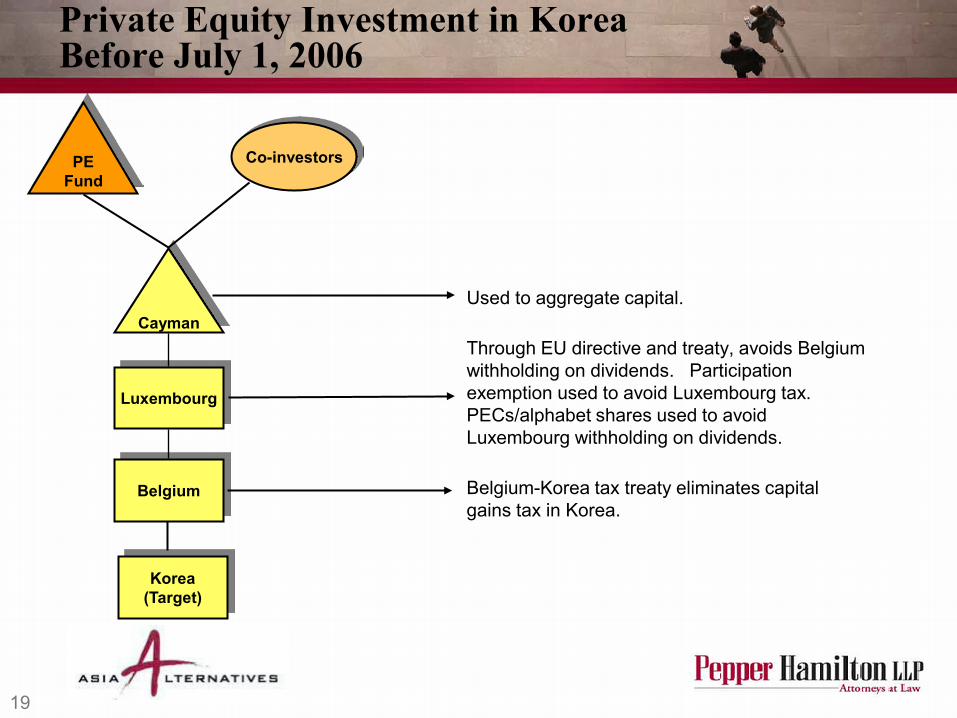

Private Equity Investment in Korea Before July 1, 2006

Used to aggregate capital. Through EU directive and treaty, avoids Belgium withholding on dividends. Participation exemption used to avoid Luxembourg tax. PECs/alphabet shares used to avoid Luxembourg withholding on dividends. Belgium-Korea tax treaty eliminates capital gains tax in Korea.

Belgium

Cayman

Luxembourg

PE Fund

Co-investors

Korea (Target)

20

Korean Attack on Structure

• First attempt 2005 − Substance over form doctrine − Treaty resident not beneficial owner of Korean target

• Treaty resident just formal owner, not true beneficial owner − Difficult to prove

21

Korean Attack on Structure (cont’d)

• July 1, 2006 – Amendments to Corporate Income Tax Act and Investment Tax Adjustment Act effective − Substance over form applied to treaty − Must withhold on dividends, interest, royalties and

capital gains paid to residents of tax havens even if treaty

− What is a tax haven? − Possibility for prior approval not to withhold – substantial

disclosure

22

Private Equity Investment in Australia – Myer/TPG

Used to aggregate funds of investors. Treaty and EU directive used to avoid Dutch withholding on distributions. Participation exemption avoids Luxembourg tax. Methods available to avoid Luxembourg tax on distributions to Cayman Islands. Treaty resident to reduce/diminish taxes on interest, dividends, capital gains.

Cayman Islands

Dutch BV

TPG investors

Australia (Target)

Luxembourg

23

Australian Attack on Structure

• Gain on sale was ordinary income, not capital gain • Source of income was Australia • Dutch treaty did not apply because of treaty shopping • Australian Taxation Office released 4 tax

determinations at the end of December 2010 that impact PE investment in Australia