a founders and vc perspective

TRANSCRIPT

Financing your start-up..A Founder’s and VC’s

perspective

Commercial in ConfidenceThis document is subject to commercial in confidence and must not be distributed, reproduced or published in whole or in part without the prior written consent of AirTree Ventures Pty Ltd (ACN169 127 020). Attribution under creative commons (Mekeltan on flickr). For more information contact AirTree Ventures ([email protected]).

Craig Blair, AirTree Ventures

@craigRblair

Four seasoned entrepreneurs and investment professionals

Daniel PetreCo-founder, Partner

Craig BlairCo-founder, Partner

Paul Bennetts Investment Director

Cath Rogers Investment Manager

• Founded 2 of Australia’s most successful technology investment firms

• Senior leadership roles at Microsoft in Seattle/Asia Pac

• 2 portfolio board positions

• Principal at netus – a top decile VC firm

• Founder/CEO/Director of Travelselect, Beamly (Aus), PetCircle Expedia

• 3 portfolio board positions

• Entrepreneur, investments, operations, PE and investment banking

• 2 portfolio board positions

• Entrepreneur, operations, PE and investment banking

• 2 portfolio board positions

2

We have built and invested in >20 businesses over the last 15 years

Key skills we bring to invest-ments

Deep insights into business model evolution and technology trends causing business disruption

Large, extensive network of local entrepreneurs, product peo-ple at larger tech companies, an-gel investors, exit stakeholders and ecosystem at large

Wide operational expertise at all of levels of organisation.

What have we done before?

Netus 2005 - 2012

Ecorp 1997 - 2003

15 years experience

3rd Venture Fund

4.1X cash on cash returns

($1 invested returned $4.10 to investors at the end of fund life)

3

4

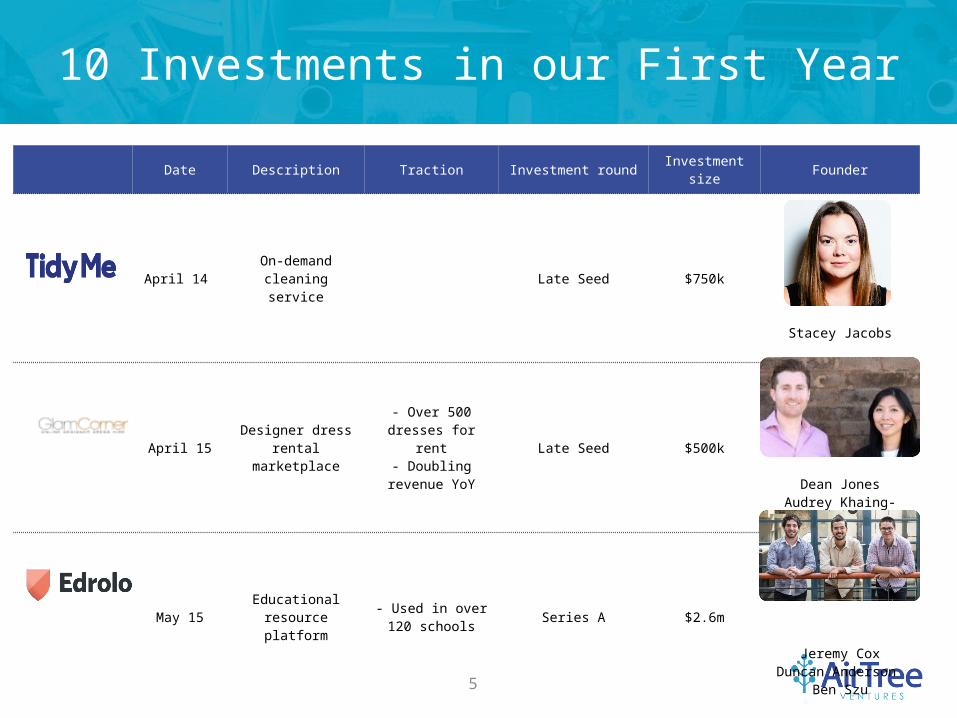

10 Investments in our First Year

Date Description Traction Investment roundInvestment

size Founders

Dec 14 Online pet sitting

Leading marketplace in

11 markets including

Canada, UK and NZ

Convertible Note $1.5m

Tanguy Peters

Feb 15Design

marketplace

- 456k Graphic Designers

- $26m design projects and competitions

Series B $6m

Alec Lynch

March 15Web based

design platform- 3.9m active

members Convertible Note $7.5m USD

Cameron Adams, Cliff Obrecht & Melanie

Perkins

5

Date Description Traction Investment roundInvestment

size Founder

April 14 On-demand cleaning service

Late Seed $750k

Stacey Jacobs

April 15Designer dress

rental marketplace

- Over 500 dresses for rent

- Doubling revenue YoY

Late Seed $500k

Dean JonesAudrey Khaing-Jones

May 15 Educational resource platform

- Used in over 120 schools

Series A $2.6m

Jeremy CoxDuncan Anderson

Ben Szu

10 Investments in our First Year

6

Date Description Traction Investment roundInvestment

size Founder

June 15 Cloud-based rostering

Late Seed $1.2m

Aulay Macaulay

June 15

Vertically integrated

ecommerce furniture business

Series A $2m

Ivan Lim

TBA July 15Marketplace

business

TBA July 15HealthTech business

10 Investments in our First Year

7

Startup Ecosystem

8

The start-up journey1. Often raising seed/angel 3. Series

A/B raised2. Need time and

the right team andinvestors to navigate

Source: Gartner Hype Cycle

9

The cost of a start-up is getting lower

…it’s now possible to build a start-up with a credit card

£5m

$1.5m

$20K

1998

My first start-up

2005-2011

Businesses built in the Netus vintage 201

5

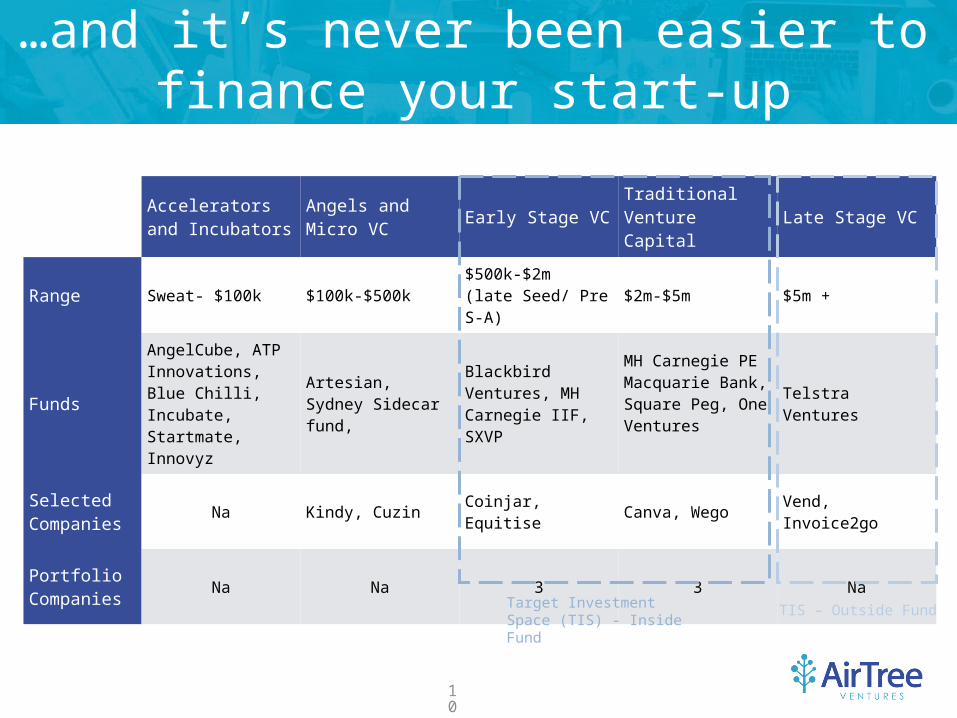

Accelerators and Incubators

Angels and Micro VC Early Stage VC Traditional

Venture Capital Late Stage VC

Range Sweat- $100k $100k-$500k$500k-$2m(late Seed/ Pre S-A)

$2m-$5m $5m +

Funds

AngelCube, ATP Innovations, Blue Chilli, Incubate, Startmate, Innovyz

Artesian, Sydney Sidecar fund,

Blackbird Ventures, MH Carnegie IIF, SXVP

MH Carnegie PEMacquarie Bank, Square Peg, One Ventures

Telstra Ventures

Selected Companies

Na Kindy, Cuzin Coinjar, Equitise Canva, Wego Vend, Invoice2go

Portfolio Companies

Na Na 3 3 Na

Target Investment Space (TIS) - Inside Fund

10

…and it’s never been easier to finance your start-up

TIS – Outside Fund

11

VC Funding Process

VC World Entrepreneur World

We have seen 400 business in 9 months

60 Became Leads 340 didn’t fit our thesis

20 were intensely reviewed

40 didn’t fit our thesis

6 were funded

You make 5 calls

5 responses 5 Responses 0 Responses

Everyone Loves it Too Early(VCs never say No)

VCs Suck!

Who to choose?VC is dead

AUS VCs don’t take risks

12

Approaching a VC

Use contacts to get an

introduction

1 2Do homework

on the VC/Partner

Background Check

3

Use advisor sparingly

- e.g. Support on deal terms not for introductions

4Be clear on the differences of a VC lead round over a ‘book

build’ approach

5

Some Dos and Don’ts

14

What To Do

• Have a detailed understanding of your competitors

• Develop a healthy paranoia for your position in the market

✔

15

What Not To Do

Self Aware

Dumb

Genius

Ignorant

US✖

Competitor 1

Competitor 3

Competitor 2

16

What To Do

✔• Tell a narrative

• Be authentic

• Acknowledge most ideas are derivative

17

What Not To Do

✖• Create a bullshit story!

• Back solve for a passion to fit the story

18

What To Do

✔ • Succinct Elevator Pitch Problem/Solution- Who is the customer?- Differentiator/competitor set- Team- Traction

• Crisp/insightful investor presentation (10-20 Slides)

• Simple model- Clear understanding of business

drivers- Sense check with

competitors/overseas players- Unit economics understood- Cash requirements

19

What Not To Do

✖• Make an 80 page investment

memo!• Detail/data is super important (but

long docs are not data)

20

What To Do

✔• Create relationships with VCs early! • Build the story and understand how they

work

21

What Not To Do

✖• Over invest in PR so that profile

outpaces performance

High Traction

Low Public Profile

High Public Profile

Low Traction

VCs know this space Great place

to be

Good place to be

22

Incubator

$100k of value

10%

$1m*

Funding your businessBeware of the pre-money trap

* Implied

Continuing to raise at higher valuations is difficult. Company forced to live off drip fed angel funding rounds

Starts with artificial valuation before there are real metrics

Angel rounds from HNWs may meanraise is at a high valuation and/or…… not enough raised to grow into valuation

Need to show up rounds – “grew 100% since last round so valuation is 2x previous round”Without a big enough raise to allow the business metrics to catch up to the valuation

Pre-money Valuation

Raise

% Dilution

Post-money valuation

Angel

$3.5m

$.5m

12.5%

$4m

Late seed

$8m

$1m

11%

$9m

23

Funding your business

Beware of the post-money trap

Incubator Angel

Pre-money Valuation

$100k (of value) for 10%

$3.5m

Raise $.5m

Post-money valuation

$1m (implied)

$4m

- Decision option set moves from “what can we afford to do?” to “what is the optimal use of capital and resources?”

- Deploying capital sensibly is more difficult than most teams appreciate

- Company unable to create 3-5x value for every dollar invested….

Pre money valuation is fair, but size of raise inflates post money valuation and makes a subsequent up round more challenging

$5m

$15m

Late seed/Series A

$10m

Raise a lot of capital given opportunities for sensible growth investment

24

Key Focus Points for Series A

Know your metrics• Unit economics are critical

– Consider the “unit” that makes sense for your business– Understand exactly how much your make or lose for each

transaction over time and when a customer becomes profitable– Don’t forget all the direct costs of a transaction (customer service

etc) and make sure the contribution is measured after marketing costs

• CAC or LTV– Bottom line: investors don’t want you to use their funds to “buy”

unprofitable business– The earlier you are in a business the more you can focus on LTV,

it’s OK if customers are expensive to acquire if they are valuable over time

– Be realistic in estimating repeats and retention, very few businesses can confidently assume a customer “lifetime” is more than 5 years

25

People are key• People

– Building a successful start-up to an exit is an extraordinary business outcome

– Requires a few extraordinary people……. not everyone can hit this benchmark

– The best companies are able to hire and develop people....... and they recognise quickly when there is not a fit

– Use networks over recruiters where possible– Prioritise product and customer facing over marketing in the

early days– Consider office manager in the first 4-5 hires……. great utility

and leverage for the rest of the team

• Other– Use equity/ESS to create ownership and alignment……. but

only where this is valued – Founder vesting is good for the company and all shareholders

26

Take Aways

• Long term value of your business > minimizing dilution in a round

• Build the right team including some extraordinary people

• Surround yourself with investors who can help build value

• Consider capped convertible notes when metrics are not clear or raising from Angels or Accelerators

• Too much capital can kill a business

– Raise 12 months in angel/seed

– Raise 18-24 months with Series A

• Allow room for market to value on real metrics

• Know your metrics

27

How to choose your funding partner?

• Can they add value over capital?• Reference check, reference check. High profile does not

always = value add• Are you aligned on how to scale the business?• How you solve problems together in the early discussions

are a good indicator of how you will work together in the future

• Can they support the business through future rounds or in a slow down?

VCs and investors are the employees you can’t fire.. make sure you are doing 4-5 references on the firm and partner

Thank you

Craig Blair, AirTree Ventures

@craigRblair

28

29

Some Common Terms Explained

Term Explanation Rationale Avoid

1. PreferenceIn case of liquidation preferred stock is paid out before common stock

Avoids misalignment at exits around entry price.

1x OK. Avoid 2-3x in early rounds

2.ParticipationThe degree to which preferred holders share in the proceeds after liquidation preference

Demonstrates adequate return for an investors risk

< 1x >

3. Anti-dilutionIn the future, the company can't issue shares to new investors at a lower price than the previous investors

Company has mispriced the round and investors should average out their investment

Full Ratchet

4. Tag-along Rights

Gives the minority shareholders the right to be tagged on the same terms as the majority in case of a sale to a 3rd party

“All in all out”Protection for minority

5. Drag-along Rights

Gives the majority shareholders the right to drag along the minority. if the 3rd party wants a 100% stake in the company.

Enables the majority of the investors to make decisions in the best interests of the company.