a global / country study and report on brazil

TRANSCRIPT

A

GLOBAL / COUNTRY STUDY AND REPORT

ON

BRAZIL

Submitted to

Gujarat Technological University

IN PARTIAL FULFILLMENT OF THE

REQUIREMENT OF THE AWARD FOR THE DEGREE OF

MASTERS OF BUSINESS ADMINISTRATION

UNDER THE GUIANCE OF

Faculty Guide

Prof. Kruti Desai

Submitted by

MBA SEMESTER III/IV

Batch: 2011 - 13

Parul Institute of Management

MBA PROGRAMME

Affiliated to Gujarat Technological University

August, 2012-2013

TABLE OF CONTENT

Sr. No. Particulars Page No.

1. Agriculture Industry 1

2. Telecommunication Industry 14

3. Airlines Industry 26

4. Automobile Industry 38

5. Coffee Industry 49

6. Media & Entertainment Industry 59

7. Mining Industry 70

8. Textile Industry 83

9. Oil and Gas Industry 96

10. Cement Industry 106

Annexure 123

1

1. AGRICULTURE INDUSTRY OF BRAZIL

Brazil’s potential to become a major agricultural player in the international trade market is

seen by their untapped fertile land and advanced farming techniques. Brazil’s historic

economic decisions have shown it to be aggressive in pushing economic reform to boost

output. Through its biotechnology research and untapped resources, Brazil is looking to

continue its agricultural output with particular emphasis on the soybean, as it is currently

only second to the United States as the leading producers and exporters of soybean. This

paper explores the history agriculture in Brazil, its use of genetically modified crops and

the untapped potential that exists within Brazil to continue growth as a large soybean

producer.

Brazil’s historical agricultural policies have placed an emphasis on agribusinesses. These

farming operations are large-scale business operations embracing the production,

processing, and distribution of agricultural products and the manufacture of farm

machinery, equipment, and supplies. This enabled the agriculture output to increase

dramatically with the advent of new technologies to allow for increased efficiencies.

Brazil’s position in international agricultural trade and its position in biotechnology places

it an interesting crossroads with regards to genetically modified crops. As one of the last

GM-free producers of soybean, it provides an alternative to other producers using GM

seeds. But on the other hand its strong biotechnology research into genetically modified

crops gives it an edge for GM crop usage. Furthermore the pull toward the use of

genetically modified soybean seeds by farmers and the lobbying by private firms investing

in research.

The future of Brazil’s agricultural role is dependent on utilizing their untapped resources.

Transportation infrastructure is particularly important to Brazil because of the large amount

of under-utilized land in central savannah. These lands are poised to be converted into

fertile plots through the use of different farming techniques and irrigation. Further accent

on increased efficiency and mechanization could continue to bolster the agricultural output.

2

History of Agriculture of Brazil

Brazil began as an agricultural player post World War II. And in two time periods, Brazil

has managed to grow from simply a player to that of an agricultural force to be reckoned

with. There was first the horizontal expansion from 1949 to 1969 and then the conservative

modernization from 1970 to today. Right after World War II, Brazil’s president was

overthrown and democratic rule was established. But “the overvalued foreign-exchange

rate, established in 1945, remained fixed until 1953. This, combined with persistent

inflation and a repressed demand, meant sharp increases in imports and a sluggish

performance of exports.” (Country Studies – “Brazil”) The new government became

worried about the future of their exports and this would potentially have a negative impact

on inflation. So as a result, the new government adopted an import-substitution

industrialization strategy to increase economic growth. Heavy export taxes were levied on

export commodities, and as a result, Brazil’s economy began growing at a tremendous

pace.

This required that the agricultural sector generate most of the economy’s foreign exchange

and as a result, agricultural GDP increased 4.2 percent each year between 1949 and 1969.

This was seen as a direct consequence of “horizontal expansion,” which was the

incorporation of new land, especially along the agricultural frontier, with the advent of

aggressive road construction. Moreover, the disincentives of the import-substitution

industrialization policies were avoided by providing access to land at concessionary terms

for the landowning elite and for commercial farmers.

In the late 1960s, it was seen that the horizontal agricultural growth was reaching its limits.

The government implemented a “conservative modernization strategy” which provided

incentives for the formation of agribusiness complexes. At this point the government began

investing in the adaptation and development of green-revolution technologies. This had an

important side-effect for mechanization and chemical inputs. The government provided

strong incentives for the creation and expansion of processing industries and for the

development and modernization of agricultural input industries. These agribusiness

complexes received subsidized credit, guaranteed prices, and tax exemptions and subsidies

when exported. Traditional, unprocessed, agricultural products, however, were subjected to

3

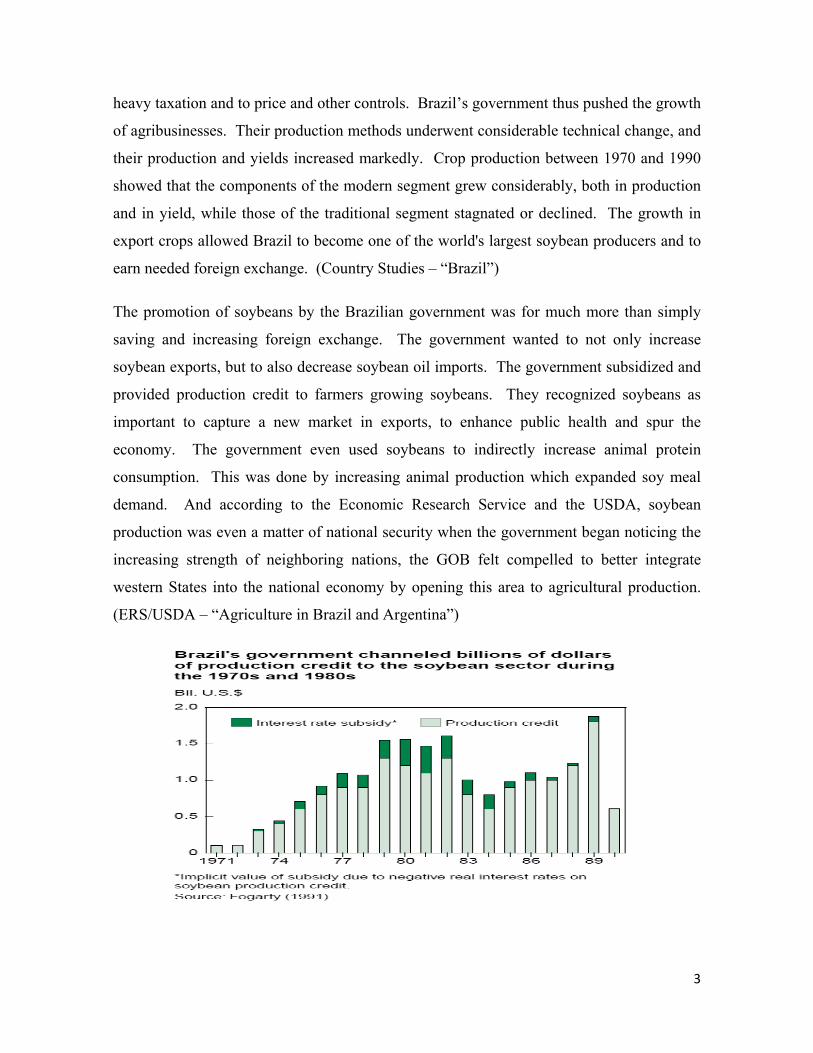

heavy taxation and to price and other controls. Brazil’s government thus pushed the growth

of agribusinesses. Their production methods underwent considerable technical change, and

their production and yields increased markedly. Crop production between 1970 and 1990

showed that the components of the modern segment grew considerably, both in production

and in yield, while those of the traditional segment stagnated or declined. The growth in

export crops allowed Brazil to become one of the world's largest soybean producers and to

earn needed foreign exchange. (Country Studies – “Brazil”)

The promotion of soybeans by the Brazilian government was for much more than simply

saving and increasing foreign exchange. The government wanted to not only increase

soybean exports, but to also decrease soybean oil imports. The government subsidized and

provided production credit to farmers growing soybeans. They recognized soybeans as

important to capture a new market in exports, to enhance public health and spur the

economy. The government even used soybeans to indirectly increase animal protein

consumption. This was done by increasing animal production which expanded soy meal

demand. And according to the Economic Research Service and the USDA, soybean

production was even a matter of national security when the government began noticing the

increasing strength of neighboring nations, the GOB felt compelled to better integrate

western States into the national economy by opening this area to agricultural production.

(ERS/USDA – “Agriculture in Brazil and Argentina”)

4

The Role of agriculture in Brazilian economy

After two decades of stagnation, the Brazilian economy recovered and experienced

relatively high rates of economic growth over the period 2000‐2010. According to Fraga

(2004) the Latin America countries, including Brazil, adopted economic reforms based on

fiscal and monetary tightness, economic openness, privatization and deregulation that were

mostly implemented by 1995. However, the relatively high rates of growth in real GDP

exceeding 3.0% per annum in the early 1990s declined near the end of this decade and

returned to rates of growth averaging about 3.7% per annum over the period 2000‐

10. Despite the recovery of higher rates of growth, growth performance lies below that of

the average rate of the BRICs. This relatively poor performance may be linked to

fundamental features and institutional impediments of the economy. One fundamental

feature is that Brazil, being a natural resource‐rich country, is experiencing a phenomenon

known as the “natural resource curse.” As shown by Gaitan & Roe (2011), countries with

abundant natural resources can grow less rapidly than those countries without when the

abundant resource sector faces an inelastic demand for a primary resource (in this case,

primary agricultural goods).

They show that growth in trade revenues can induce the resource‐abundant country to

invest relatively less than the country lacking in exhaustible resources” (Gaitan & Roe,

2011, p.1). Studying constraints to growth, Pinto (2011) fits to Brazilian data a Ramsey

growth model with four sectors. The results suggest that the country´s potential to double

real income per capita from transition growth will require about 79 years (compared to 8 to

15 years for other leading emerging market economies). The key constraints limiting the

country’s growth, following Rodrik (2006)and Hausman et al (2005)are the low rate of

domestic savings (17% of GDP), transportation infrastructure, and the low stock of human

capital. The relatively low savings could result from capital market rigidities, as suggested

by Rodrik, or from disincentives linked to the natural resource course.

Brazil

interna

with t

growth

import

words

dampe

interna

Regard

inputs

Accor

repres

shocks

tend to

evolut

2010 w

and 20

has exper

ational comm

the Brazilian

h. The inter

tant; in the

, the apprec

en the expa

ational price

ding the stru

, farm outpu

rding to CEP

ented aroun

s

o produce r

tion of the B

was 3%, app

009.

rienced an

modities pri

n export exp

rnationalcom

same perio

ciation of th

ansion of B

es have comp

ucture of the

ut, agro‐indu

PEA (Cente

nd 22% of th

elevant imp

Brazilian agr

proximately,

export boo

ice increased

pansion (Fig

mmodities p

od,the effect

he real exch

Brazilian ag

pensated this

Brazilian ec

ustries and di

er for Advan

he Brazilian

acts on the

ribusiness G

and similar

om starting

d 185%, and

gure 2), wit

prices effect

tive exchang

hange rate,

gribusiness

s negative sh

conomy, the

istribution –

nced Studie

n GDP in 20

country’s e

GDP; the ave

r the econom

in 2003.

d this move

th positive e

on Brazilia

ge rate beca

like a Dutc

exports, bu

hock on expo

agribusines

comprises a

es on Applie

010. Conseq

economic gro

erage growth

my´s growth,

From 2003

ement is hig

effects on B

an exports

ame overva

ch disease, c

ut the high

orts.

ss sector – in

a large share

ed Economi

quently, agri

owth. Figur

h rate on the

, despite the

3 to 2010,t

ghly correlat

Brazilian GD

is particular

alued, in oth

could serve

level of t

ncluding farm

of GDP.

ics) the sect

cultural sect

re 3 shows t

e period 200

years of 20

5

the

ted

DP

rly

her

to

the

m

tor

tor

the

01‐

005

6

The macroeconomic data suggests that at least part of the Brazilian economic growth is

sustained by the international market (commodities prices) through the agricultural sector.

Alvares‐Cuadrado & Poschke (2011) suggest that the “labor push” out of agriculture is due

to

improvements in agricultural technology that combined with the Engel´s law release

resources

from agriculture to the rest of the economy as development occurs and per capita incomes

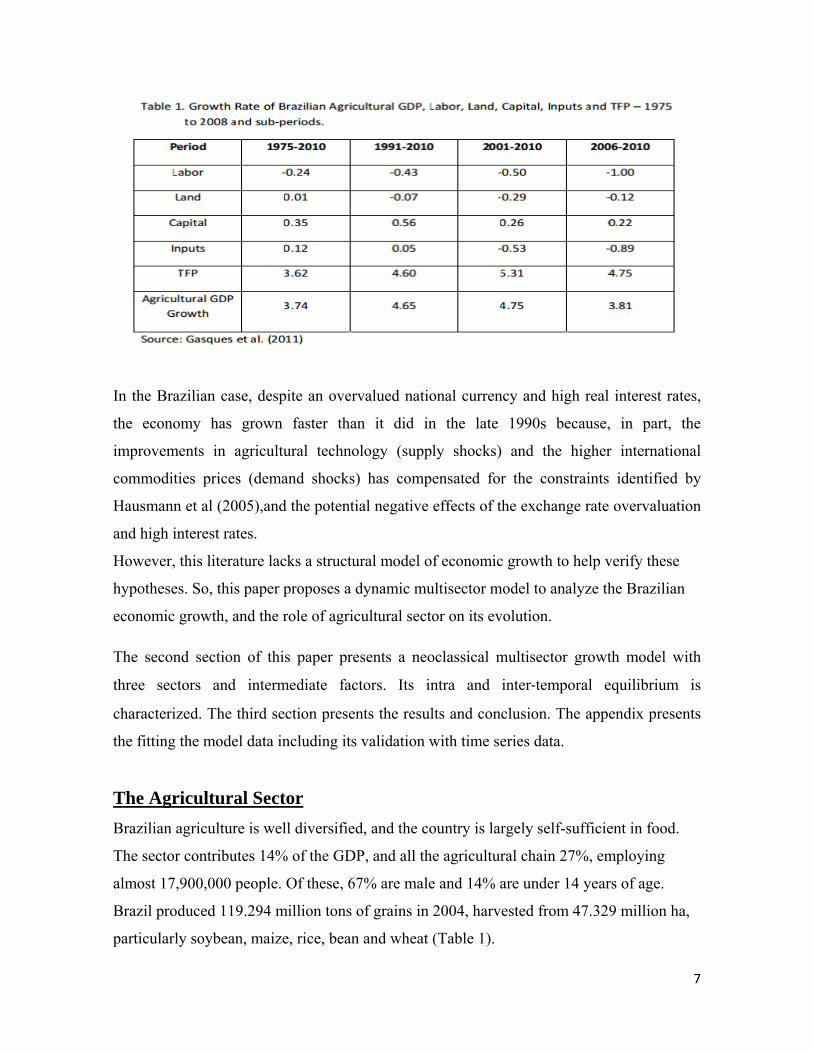

grow. Gasques et al. (2011) estimated the Brazilian agricultural GDP growth, over the

1975‐2010 period. They conclude that growth in agricultural output has been driven by

growth in TFP that was particularly pronounced in the last decade (4.75% aa).

7

In the Brazilian case, despite an overvalued national currency and high real interest rates,

the economy has grown faster than it did in the late 1990s because, in part, the

improvements in agricultural technology (supply shocks) and the higher international

commodities prices (demand shocks) has compensated for the constraints identified by

Hausmann et al (2005),and the potential negative effects of the exchange rate overvaluation

and high interest rates.

However, this literature lacks a structural model of economic growth to help verify these

hypotheses. So, this paper proposes a dynamic multisector model to analyze the Brazilian

economic growth, and the role of agricultural sector on its evolution.

The second section of this paper presents a neoclassical multisector growth model with

three sectors and intermediate factors. Its intra and inter‐temporal equilibrium is

characterized. The third section presents the results and conclusion. The appendix presents

the fitting the model data including its validation with time series data.

The Agricultural Sector

Brazilian agriculture is well diversified, and the country is largely self-sufficient in food.

The sector contributes 14% of the GDP, and all the agricultural chain 27%, employing

almost 17,900,000 people. Of these, 67% are male and 14% are under 14 years of age.

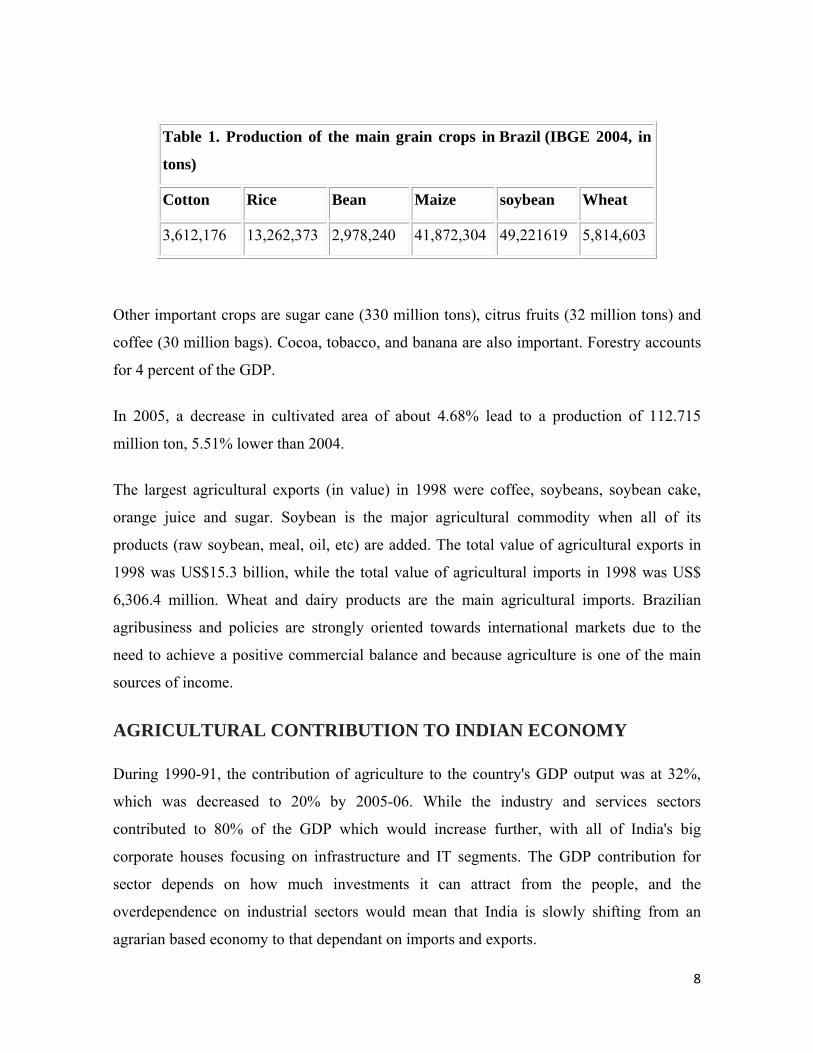

Brazil produced 119.294 million tons of grains in 2004, harvested from 47.329 million ha,

particularly soybean, maize, rice, bean and wheat (Table 1).

8

Table 1. Production of the main grain crops in Brazil (IBGE 2004, in

tons)

Cotton Rice Bean Maize soybean Wheat

3,612,176 13,262,373 2,978,240 41,872,304 49,221619 5,814,603

Other important crops are sugar cane (330 million tons), citrus fruits (32 million tons) and

coffee (30 million bags). Cocoa, tobacco, and banana are also important. Forestry accounts

for 4 percent of the GDP.

In 2005, a decrease in cultivated area of about 4.68% lead to a production of 112.715

million ton, 5.51% lower than 2004.

The largest agricultural exports (in value) in 1998 were coffee, soybeans, soybean cake,

orange juice and sugar. Soybean is the major agricultural commodity when all of its

products (raw soybean, meal, oil, etc) are added. The total value of agricultural exports in

1998 was US$15.3 billion, while the total value of agricultural imports in 1998 was US$

6,306.4 million. Wheat and dairy products are the main agricultural imports. Brazilian

agribusiness and policies are strongly oriented towards international markets due to the

need to achieve a positive commercial balance and because agriculture is one of the main

sources of income.

AGRICULTURAL CONTRIBUTION TO INDIAN ECONOMY

During 1990-91, the contribution of agriculture to the country's GDP output was at 32%,

which was decreased to 20% by 2005-06. While the industry and services sectors

contributed to 80% of the GDP which would increase further, with all of India's big

corporate houses focusing on infrastructure and IT segments. The GDP contribution for

sector depends on how much investments it can attract from the people, and the

overdependence on industrial sectors would mean that India is slowly shifting from an

agrarian based economy to that dependant on imports and exports.

9

Indian Agricultural industry also assumes significance owing to India's sizable agrarian

economy, which contributes over 35% of GDP and employs around 65 % of the population.

The consumer food segment goods have top priority both in terms of foreign investment

and number of joint- ventures / foreign collaborations. Indian agricultural industry that have

the capacity to lure foreigners with promising benefits are the deep sea fishing, aqua

culture, milk and milk products, meat and poultry segments.

PRESENT TREND IN THE AGRICULTURAL SECTOR

Organic farming is the latest trend in agricultural bisiness.both the countries focused on

organic farming to cope with problems pertaining with traditional farming. Such as soil

pollution due to excessive usage of fertilizers ,wastage of water, technological changes,

lack of skilled workers etc.

Organic agriculture has grown out of the conscious efforts by inspired people to create the

best possible relationship between the earth and men. Since its beginning the sphere

surrounding organic agriculture has become considerably more complex. A major

challenge today is certainly its entry into the policy making arena, its entry into anonymous

global market and the transformation of organic products into commodities.

During the last two decades, there has also been a significant sensitization of the global

community towards environmental preservation and assuring of food quality. Ardent

promoters of organic farming consider that it can meet both these demands and become the

mean for complete development of rural areas. After almost a century of development

organic agriculture is now being embraced by the mainstream and shows great promise

commercially, socially and environmentally. While there is continuum of thought from

earlier days to the present, the modern organic movement is radically different from its

original form. It now has environmental sustainability at its core in addition to the founders

concerns for healthy soil, healthy food and healthy people.

Asia - The total organic agricultural area in Asia is nearly 3.3 million hectares.This

constitutes nine percent of the world’s organic agricultural land. 400’000 producers were

reported. The leading countries by area are China (1.9 million hectares) and India (1 million

hectares). Timor Leste has the most organic agricultural area as a proportion of total

10

agricultural land (seven percent). Organic wild collection areas play a major role in India

and China, while Aquaculture is important in China, Bangladesh and Thailand.

TRADE POLICES OF AGRICULTURE SECTOR OF BRAZIL

In the late 1980s, Brazil started to adopt liberal and arketoriented policies, which

significantly impacted the performance of its food and agricultural (henceforth agrifood)

sector. The agrifood sector is now among the most dynamic in the Brazilian economy.

Grain production doubled from 58 to 120 million metric tons (MT) and meat production

surged from 7.5 to 20.7 million MT etween1990 and 2005. The agrifood economy

generated R$534 billion S$183 billion) in 2004, which is equivalent to30% of the country’s

GDP. In addition, it represented35% of total employment and 40% of total exports in 2004.

Concurrent with these significant institutional and policy changes, the Brazilian agrifood

system transitioned from a traditional to an increasingly global and industrial model.

Fostered by rising incomes, urbanization, economic liberalization, and access to

competitive raw materials, multinational food processors and retailers entered or increased

their investments in the Brazilian

Market during the 1990s. Increased foreign direct investment (FDI) by large, private

agribusinesses in Brazil displaced domestic competitors, increased industry concentration,

and eliminated many medium and small companies. As a result, the market share of

multinational corporations in the domestic food market increased. For instance, Brazilian

affiliates of multinational agrifood companies generated 137,000 jobs, almost US$5 billion

in exports, and

TRADE POLICY OF INDIAN AGRICULTURAL SECTOR

Indian agriculture has, since Independence, made rapid strides. In taking the annual

foodgrains production from 51 million tonnes in early fifties to 206 million tonnes at the

turn of the century, it has contributed significantly in achieving self-sufficiency in food and

in avoiding food shortages.

The National Policy on Agriculture seeks to actualise the vast untapped growth potential of

Indian agriculture, strengthen rural infrastructure to support faster agricultural

11

development, promote value addition, accelerate the growth of agro business, create

employment in rural areas, secure a fair standard of living for the farmers and agricultural

workers and their families, discourage migration to urban areas and face the challenges

arising out of economic liberalization and globalisation.

BUSINESS OPPORTUNITIES IN FUTURE

Many countries from South America, Asia and East Europe are able to provide agri-food

products in response to the increasing demand in regions such as East and North Asia, the

Middle East, and African countries. However, few countries are global traders like Brazil,

providing a large range of commodities and processed products to a large range of

countries. The growth of consumption of agri-food is far from stabilizing. The availability

of land, water scarcity, low productivity and protectionist policies signal that developed

and developing countries will necessarily resort to the world market to guarantee food

security for their urban populations by procuring agri-food products at reasonable prices

for the domestic consumer. Brazil is a central variable in that equation.

Two great challenges remain for Brazilian agriculture: trade negotiations and transport

infrastructure. As Brazil is a global player, with its trade flux roughly evenly distributed

among various importers, trade negotiations are a major issue for Brazil, particularly in

view of the fact that trade barriers and distortions in agriculture are much greater than in

manufactured products. Brazil is now engaged in an unprecedented effort of negotiating on

three major fronts: WTO, MERCOSUR-European Union, and the Free Trade Area of the

Americas.

The Brazilian agricultural sector is also paying the price of being market-oriented. The

sector is being affected by an overvalued exchange rate; lack of investments in

infrastructure; reduction of expenditure in research and development; and low priority of

sanitary policies, not only to meet importers’ standards, but also to protect domestic

production against unsafe imported products.

With the development of bio-energy, agriculture is becoming a more complex economic

and social activity. Old mechanisms such as trade-distorting subsidies, intervention prices,

and production quotas, although still in use, tend to lose sense as feed and energy markets

12

converge. Agricultural production will be completely transformed in the future and Brazil

is a major candidate to play a central role on this process. It is, therefore, no coincidence

that Brazil has been playing a very active role in the Doha Development Agenda

negotiations.

As coordinator of the G-20, which consists of developing countries from three continents

as the country with the largest trade surplus in agriculture; and having had to reform its

own agricultural policies, Brazil is particularly well-placed to continue to influence the

pace of the reform of agriculture.

SUGGETIONS

From economic perspective, an export-oriented production system is considered more

important than those that supply domestic demands. The Indian organic produce market is

mainly export oriented.Focusing on export alone involves hidden costs including transport

and risks to local food security. Policies considering domestic demands particularly food

security as equally important are needed for a rationale balance of trade.

Agriculture is the main source of employment for rural people.Specialized and mechanized

practices reduce rural employment. Sustainable agriculture, as witnessed through organic

farming system, being labor-intensive helps overcome such problems.

The growth of Brazilian agriculture has been built with a strong market orientation, rather

than by government intervention. Brazil undertook major reforms of its agricultural policies

during the 1990s, and the productive sector reacted swiftly to become more efficient and

competitive.

The growth of consumption of agrifood is far from stabilizing. The availability of land,

water scarcity, low productivity and protectionist policies signal that developed and

developing countries will necessarily resort to the world market to guarantee food security

for their urban populations by procuring agrifood products at reasonable prices for the

domestic consumer. Brazil is a central variable in that equation.

13

The technological development plays significant role in development of agricultural trade

between two countries. India can import new technology from brazil like irrigation,

warehousing, harvesting, fertilizers etc. to improve production of agriculture.

Some trade barriers should be eliminated for better trade relation between two countries.

Like import duty on coffee, and norms of trade should be kept easy to encourage small

marketer. to enter at international agricultural market.

14

2.TELECOMMUNICATION INDUSTRY

Thirteen years after the Brazilian telecoms industry was privatized, its revenues for 2010

were US$114bn, which represented 5% of the gross domestic product. The political and

economic stability in Brazil over the last few years has been critical in the growth of the

telecom market. The increased purchasing power of the poorer classes of the population has

significantly changed Brazilian consumption standards—both qualitatively and

quantitatively—and has positively affected the industry. The National Broadband Plan,

regulation of mobile virtual network operators and new laws for cable TV provision are

some of the recent changes that will bring even more opportunity to this exciting market.

The Brazilian telecommunications industry, as it is today, results from a process of

deregulation and the opening of trade that began in the second half of the 1990s. At that

time, a series of laws were approved that redefined the principles of competition and

universalization for the telecoms industry, as well as allowed foreign companies to invest in

Brazil.

Reorganizing Telebrás into three companies to provide local landline service accompanied the

division of Brazil into three large regions. Each one of these regions was to be served by one of the

new incumbent companies. When the companies were sold to private investors in 2001, the

regulatory body began the process of approving new authorizations so that competitors also could

provide local landline services.

When the sector was privatized, one present operator, Embratel, was certified to provide

national and international long distance service. Different from the local landline service,

this segment reached such a high level of competition that the regulatory body began

discussing, in early 2011, deregulating the pricing system for international calls as of 2016.

Initially, eight privatized companies operating in eight regions of the country formed the

mobile segment. Four major companies now dominate the segment, and they offer service

nationally to 97.2% of the Brazilian municipalities.

The growth of broadband in Brazil has accelerated, due mainly to mobile broadband. The

1.7m subscribers to mobile broadband in 2008 grew to 20.6m at the end of 2010, reflecting

the increasing demand for content through mobile devices.

15

Brazilian cable TV reached 9.8m subscribers in 2010, representing a density of 5

subscribers per 100 inhabitants. That number is low compared to the potential market of

57.5m homes occupied, according to data from the 2010 census published by the Brazilian

Institute of Geography and Statistics.1

Introduction to Telefonica

Telefónica is one of the world leaders’ integrated operators in the telecommunication

sector, providing communication, information and entertainment solutions, with presence in

Europe and Latin America.

Telefónica has one of the most international profiles in the sector with 76% of its business

outside its home market and a reference point in the Spanish and Portuguese speaking

market.

In Latin America, Telefónica gives service to more than 211.9 million customers as of the

end of December 2012 becoming the leader operator in Brazil, Argentina, Chile and Peru

and has substantial operations in Colombia, Costa Rica, Ecuador, El Salvador, Guatemala,

Mexico, Nicaragua, Panama, Puerto Rico, Uruguay and Venezuela. In Europe, on top of the

Spanish operations, the Company has operating companies in the United Kingdom, Ireland,

Germany, Czech Republic and Slovakia, providing services to more than 103.1 million

customers as of the end of December 2012.

Introduction of Bharti Airtel

Bharti Airtel Limited is a leading global telecommunications company with operations in

20 countries across Asia and Africa. Headquarters in New Delhi, India, the company ranks

amongst the top 4 mobile service providers globally in terms of subscribers. In India, the

company's product offerings include 2G, 3G and 4G wireless services, mobile commerce,

fixed line services, high speed DSL broadband, IPTV, DTH, enterprise services including

national & international long distance services to carriers. In the rest of the geographies, it

offers 2G, 3G wireless services and mobile commerce. Bharti Airtel had over 267 million

customers across its operations at the end of February 2013 airtel was born free, a force

unleashed into the market with a relentless and unwavering determination to succeed. A

1 www.telefonica.com

16

spirit charged with energy, creativity and a team driven “to seize the day” with an ambition

to become the most admired telecom service provider globally. airtel, in just ten years of

operations, rose to the pinnacle of achievement and continues to lead.2

Social Impact of Telefonica

At the close of 2011, we employed a total of 291,027 professionals, 2.1% more than

in 2010, and we had invested 66.4 million Euros in their training.

Telefonica was chosen as one of 25 best global companies to work at by the Great

place to work.

We developed nearly 50 initiatives for social innovation by means of ICT ideas and

solutions to meet the social needs of the elderly, the disabled and those at the foot of

the pyramid.

Swot Analysis of Telephonica

Strength

Significant Market Position

Focus on Research and Development

Strong Growth in Mobile and Broadband Segment

Weakness

Lack of presence in Asia Pasific

Opportunities

Agreement with Deutsche pst world Net

Business Expansion

Growth of broadband and pay TV services in Latin America

New Collaboration

Threats

Exchange rate Fluctuations

Declining ARPU

Regulatory Environment

SWOT Analysis of Airtel

Strengths 2 www.airtel.in

17

BhartiAirtel has added more than 65 million customers. It is the leading cellular

provider in India, and also has provisions of broadband and telephone services - as

well as many other telecommunications services to both domestic and corporate

customers.

Other stakeholders in BhartiAirtel include Sony-Ericsson, Nokia - and Sing Tel,

with whom they seize a strategic alliance. This means that the business has

admittance to knowledge and technology from other parts of the

telecommunications world.

The company has covered the entire Indian nation with its network. This has

underpinned its huge and increasing customer base.

Weaknesses

A frequently cited original weak spot is that when the business was started by Sunil

Bharti Mittal over 15 years ago, the business has small knowledge and experience

of how a cellular telephone system actually worked. So the start-up business had to

outsource to industry experts in the field.

Until justAirtel did not its own towers, which have a particular strong point of

several of its competitors such as Hutchison Essar. Towers are important if your

company wishes to provide wide coverage nationally.

The fact that the Airtel has not pulled off a deal with South Africa's MTN could

signal the lack of any real emerging market investment opportunity for the business

once the Indian market has become mature.

Opportunities

The company possesses a modified version of the Google search engine which will

enhance broadband services to customers. The tie-up with Google can only enhance

the Airtel brand, and also provides advertising opportunities in Indian for Google.

Global telecommunications and new technology brands see Airtel as a key strategic

player in the Indian market. The new iPhone will be launched in India via an Airtel

distributorship. Another strategic partnership is held with BlackBerry Wireless

Solutions.

in spite of being forced to outsource much of its technical operations in the early

days, this allowed Airtel to work from its own blank sheet of paper, and to question

industry approaches and practices - for example replacing the Revenue-Per-

18

Customer model with a Revenue-Per-Minute model which is better suited to India,

as the company moved into small and remote villages and towns.

The company is investing in its operation in 120,000 to 160,000 small villages

every year. It sees that less well-off consumers may only be able to afford a few

tens of Rupees per call, and also so that the business benefits are scalable - using its

'Matchbox' strategy.

BhartiAirtel is embarking on another joint venture with Vodafone Essar and Idea

Cellular to create a new independent tower company called Indus Towers. This new

business will control more than 60% of India's network towers. IPTV is another

potential new service that could underpin the company's long-term strategy.

Threats

Airtel and Vodafone seem to be having an on/off relationship. Vodafone which

owned a 5.6% stake in the Airtel business sold it back to Airtel, and instead invested

in its rival Hutchison Essar. Knowledge and technology previously available to

Airtel now moves into the hands of one of its competitors.

The quickly changing pace of the global telecommunications industry could tempt

Airtel to go along the acquisition trail which may make it vulnerable if the world

goes into recession. Perhaps this was an impact upon the decision not to proceed

with talks about the potential purchase of South Africa's MTN in May 2008. This

opened the door for talks between Reliance Communication's Anil Ambani and

MTN, allowing a competing Inidan industrialist to invest in the new emerging

African telecommunications market.

BhartiAirtel could also be the target for the takeover vision of other global

telecommunications players that wish to move into the Indian market.3

Licensing of Telefornica

Peru’s unit of Telefónica has accepted the requirements imposed that the Peruvian

government for renewing its operating licenses. Telefónica classified the conditions and

terms required by the Ministry of Transport and Communications (MTC) as harsh and said

that they are unprecedented.

3 www.slideshare.net

19

Telefónica said that to comply with the MTC’s terms and conditions, it will have to do

extraordinary investments and also do management efforts. The telecom operator also

highlighted that it has fulfill its previous obligations, contributing significantly to the

“dramatic growth of mobile telephony in Peru with more coverage and increasingly

competitive rates.”

“The amount Telefonica had to commit to invest in rural coverage areas in exchange of the

renewal of license, around U.S.$1.2 billion, is very high,” Marceli Passoni, senior analyst

for Latin America at Informa Telecoms & Media told RCR Wireless News. “For instance,

in Brazil, the regulator raised U.S.$1.3 billion in its LTE auction, when six companies

acquired spectrum. However, the Peruvian government was want to impose some

conditions for the license renewal.”

Among the agreement’s positive aspects, Menutti said that mobile services will reach 409

district capitals and 1,848 locations where there was no Telefónica coverage, achieving

100% mobile coverage of the district capitals. “In addition, up to 1 million people will have

a reduced rate for mobile services, which will be reflected in increased service adoption.

These obligations are in line with the objectives of the National Plan for the Development

of Broadband in Peru asked to minimize the digital divide, ensuring that 100% of the

country’s districts have broadband,” he said.

On the negative side, the analyst pointed out that the negotiation delay for the contract

renewals resulted in the new district infrastructure deployments beginning at least one year

later than they should have, since Telefónica’s licenses expired between May 2011 and

February 2012.4

Commercialization Conditions in Telefónica:

The present commercialization conditions (hereinafter “Commercialization Conditions”)

are based on clause 5.3 of Blue Via General Conditions (hereinafter “General Conditions”)

previously accepted by the Developer, under which the Developer agrees that after

selecting the Application Stores in which it wishes to commercialize its Application the

4 http://www.rcrwireless.com/americas/20130123/carriers/telefonica-peru-finds-harsh-accepts-governments-conditions-renewal-licenses/

20

Developer must accept additional Commercialization Conditions in order to commercialize

the Application through such Application Stores.

APPLICATION GUIDELINES:

Applications using Wi-Fi or data traffic as a base for voice or data P2P communications are

not allowed.

Games, Video streaming, Ringtones, SMS/MMS Alerts and Music related Applications

need to be authorized by The Operator previously to the Commercialization of the

Application trough The Application Stores. Developer must send an email to the Bluevia

Community [email protected] with a short description of the Application. The

Application will be supposed accepted by the Operator unless within 5 days following the

initial delivery of proposal, The Operator notifies Developer its non-acceptance, and then

such Application will not be uploaded to The Application Stores.

Import:

We use public shipping records to provide insights into the trading activities of importers

and exporters around the world.

Import Genius empowers your business with actionable data about your overseas suppliers

and domestic competitors. By tapping into genuine shipping records from U.S. Customs as

well as nine governments in Latin America, we can show you what goods your competitors,

suppliers and competitors' suppliers have been shipping.

Terms and conditions of Airtel:

1. Airtel Dhamaka Offers the service (hereinafter referred to as “Services”) bring to you by

Bharti Airtel Limited having its register office at Bharti Crescent, 1, Nelson Mandela Road,

Vasant Kunj, Phase II, New Delhi – 110 070 (herein after referred to as “Airtel”).

2. Services are valid only for customers who acquire a fresh postpaid relation (excluding

the customers who have company paid connection) for the period of the sponsorship time

i.e. 1st June’11 to 31st Aug’11

21

3. Customer should describe the elected no. i.e. 55255 after 48 hrs from the instance of

activation of the SIM.

4. Customer can get benefit from the offer within 10 days from the activation of the SIM,

after which the offer will get failed.5

Policies:

This policy aims to:

Ø Provide an independent forum by means of the Office of the Ombudsperson, for

employees and external stakeholders of the company to raise concerns and complaints

about improper practices which are in breach of the Bharti Code of Conduct.

Ø Put in place a fair and equitable inquiry process and redressed mechanism.

Ø Reassure employees and other stakeholders raising the concerns, that each one will be

fully protected against possible reprisals, intimidation, coercive action, dismissal, demotion

or victimization when a serious and genuine concern of apparent unprofessional conduct

has been made in good faith.

Communication and implementation of the embeds person policy

The implementation of this policy will be the responsibility of the Ombudsperson.

A copy of the policy is available to all employees on the various company intranets. The

policy will be explained to new joinees at the time of induction and continuous

communication will ensure that awareness of the Code of Conduct and Ombudsperson

Policy is cascaded to all in the organization.

Export:

“India's Industrial Production (IIP)” approximately shrank in February due to a contraction

in infrastructure industry output and flagging demand, after a surprisingly strong increase in

January.

5 http://www.importgenius.com/venezuela/importers/informacion-telefonica-infortel-c

22

A consensus forecast by a poll of 26 economists showed factory production likely fell by

0.7 percent in February on a year earlier, following a 2.4 percent surge in January.

Before that surprise rise in January, industrial output had contracted in seven of the

previous 10 months.

Another fall does not bode well for Asia\'s third-largest economy, as it struggles to recover

after a decade low annual growth rate in the fiscal year that ended in March.

"Core infrastructure has dropped very sharply... it wouldn’t\'t be a big surprise at all if IP

came off quite sharply," said Aninda Mitra, an economist at Capital Economics in

Singapore, who forecasts a 3 percent contraction.

"It overall reflects a generalized slowdown in demand and production is just responding to

that," Mitra added.

Output in the country's eight key infrastructure industries, which make up almost 40

percent of factory production, contracted by an annual 2.5 percent in February and after

January, 3.9 percent rise.6

BUSINESS OPPORTUNITIES IN FUTURE

Since the beginning of internationalization, the company has practiced a significant growth.

Telefónica is a reference in the Latin American Telco market and has attained a relevant

scale in Europe.

They strengthened with global partnerships and collaboration agreements. As an engine for

economic sustainable development and innovation and to help overcome social divides.

Broadband increases productivity 5% in industrial sector and 10% in service sector due to

process improvement.

6http://www.airtel.in/wps/wcm/connect/airtel.in/airtel.in/home/whats+new/festival_terms_conditions

23

With a clear commitment with innovation and entrepreneurship into the following

ways:-

WAYRA, accelerator program created to find and nurture the best technology ideas and

talent.

Wayra provides technological resources, financing and support in order to simplify new

emerging startups across Europe and Latin America.

Telefónica also promotes social unity through the development of social programs.

•523,416 children at risk of social exclusion have been attended in Latin America to fight

against child labor.21, 687teachers have been trained. More than 26,000 volunteers have

taken part in harmony initiatives.8, 911young people have been trained to support the

development of 3,410 projects.” Total beneficiaries of Telefónica Foundation 1,510,449”

Telefónica boasts one of the industry’s most international profiles, generating 76% of its

business outside its home market. And is the foremost operator in the Spanish and

Portuguese speaking market.

In 2011 decisiveadvancesweremadetofosterTelefónica’stransformationprocess, making the

Company better placed to meet current and future challenges and to leverage the

opportunities gave by the growth of the digital world beyond communication needs;

evolving towards a smart, hyper-connected world.

The new digital world offers a unique opportunity to consolidate Telefónica’s leadership

and enhance its relationships with its customers. To take full advantage of these

opportunities, Telefónica has undertaken a wide-ranging alteration of the Company’s

organizational structure, creating two horizontal units (Telefónica Digital and Telefónica

Global Resources) in order to leverage the efficiency and opportunities offered by its global

scale and two business units for the two major regions in which we operate - Europe and

Latin America.

A listed company - Telefónica is a 100% listed company, with more than 1.5 million direct

shareholders. Its share capital currently comprises 4.551.024.586 ordinary shares traded on

the Spanish Stock Market and on those in London, New York, Lima, and Buenos Aires.

24

Revenues in the first nine months of 2012 totaled 46,519 million euros thanks to the

persistent growth in main revenue drivers, Latin America and mobile data. Telefónica’s

Latino-America’s revenues grew by 5.9% year-on-year, while mobile data revenues

continued showing strong growth rising 14.2% year-on-year to account for more than 34%

of combined mobile service revenues. Telefónica Digital is a global business division of

Telefónica. Its mission is to seize the opportunities within the digital world and deliver new

growth for Telefónica.

And if the GDP is growing, we do think that the telecommunication sector is going to grow

accordingly. And in fact, we think that the telecommunication sector should fuel that

growth. And according to most of the surveys, the growth of the telecommunication sector

is going to be in the neighborhood of 7.7%, which is almost double the growth of the GDP.

And we think this is going to be a stable growth. From controlling point of view, there is no

major turmoil in the horizon.

And we have been able to reach new channels of communications to expand our services,

to enlarge our revenues and at the same time to lower our cost. In fact, since we use Twitter

as way of communicating with them, the cost of our call centers have been going down

20%.

Bharti Airtel should do well to endure this challenge as it has on its discarding the

incumbent operator advantage. The company is well positioned to expand its network in the

remote areas of the country. Also the fact that while new entrants will only have start-up

spectrum of 4.4MHz for use, Bharti will benefit from having more spectrum in most of the

circles.

Bharti through its association with SingTel is also on the positive side as far as experience

in offering 3G services goes. IT is expected to bid for pan-India 3G license and particularly

for metro circles where it is faced with the challenge of keeping a check on deteriorating

ARPUs.

25

Bharti is aggressively eying acquisitions in the overseas market with a special focus on

emerging markets.7

7 http://www.telefonica.com/en/mwc/telefonica_mwc/ponentes_presentaciones.shtml

26

3.AIRLINES INDUSTRY

Introduction of Airlines

An airline is a company that provides air transport services for traveling passengers and

freight. Airlines lease or own their aircraft with which to supply these services and may

form partnerships or alliances with other airlines for mutual benefit. Airlines vary from

those with a single aircraft carrying mail or cargo, through full-service international airlines

operating hundreds of aircraft. Airline services can be categorized as being intercontinental,

intra-continental, domestic, regional, or international, and may be operated as scheduled

services or charters.

Introduction of Brazil Airlines

The Brazilian airport sector has been growing 10% a year, According to IATA (2010),

requiring appropriate terminals, adequate numbers of routes for the volume of passengers

and airlines companies for the long-term demands. However, this data is not a new

phenomenon once it has been widely analyzed by logistics airport experts for some years

with widespread concern about the capacity of the management sector and associated

innovations. Soon, through long-term growth, it is essential to understand competition,

prices charged by airlines and the necessary conditions to achieve profits according to

market behavior.

Introduction of Indian Airlines

Indian, formerly Indian Airlines (Indian Airlines Limited from 1993 and Indian Airlines

Corporation from 1953 to 1993) was a major Indian airline based in Delhi and focused

primarily on domestic routes, Along with several international services to neighboring

countries in Asia. It was state-owned, and was administered by the Ministry of Civil

Aviation. It was one of the two flag carriers of India, the other being Air India. The airline

officially merged into Air India on 27 February 2011. The airline operated closely with Air

India, India's national carrier. Alliance Air, a fully owned subsidiary of Indian, was

renamed Air India Regional.

Role of Indian Airlines in Economy

27

The Ailines have contributed in a significant way to India's economic growth in the last few

years:

Airlines have enhanced the efficiency and reduce the costs for productive business

activities. The spped with small and large businesses are able to interact and

conclude business transactions and deals have increased.

Airlines have significantly eased the transport bottlenecks for tourists, business and

trade travelers as well as other travelers including doctors. Patients, engineers,

doctors, patients, etc. between and among far flung smaller cities and towns and the

metropolitan cities as well as foreign cities of business and tourist importance,

thereby reducing unnecessary delays and prompt response. This has enabled the

efficiency and productivity of the Indian economy to grow.

Brazil Airlince

GOL TRANSPORTES AÉREOS

INTRODUCTION

• Gol Transportes Aéreos ("Gol Air Transport," BM&F Bovespa: GOLL3, GOLL4,

/ NYSE:GOL) is a Brazilian low-cost airline based in ComandanteLineu Gomes

Square, Sao Paulo, Brazil. It also owns the brand Varig, although now that name

refers to the informally known "new" Varig, founded in 2006 and not to the "old"

Varig, founded in 1927. Gol operates a growing domestic and international

scheduled network. Its main hubs are São Paulo's Rio de Janeiro's Galeao

International Airport Congonhas.

HISTORY

• The airline was established in 2000 and started operations on January 15, 2001 with

a flight from Brasília to São Paulo. It is a subsidiary of the Brazilian conglomerate

GrupoÁurea based at Minas Gerais state, which has other transport interests

including Brazil's largest long-distance bus company. GrupoÁurea in turn is owned

28

by the Constantino family. As of 2004, Gol had carried 11,600,000 passengers, and

constituted 20% of the Brazilian air travel market.

PROFILE

• Innovation, pioneering spirit and low prices

• Structure, systems and controls

• Aircraft and market expansion

Mission

Bring people closer safely and intelligently.

Vision

To be the best airline for travel, work and investment.

Data Statistics

Guidance 2012 versus 2012 Actual

29

2012 Guidance Min. Max. 2012

Brazilian GDP Growth * 1.5% 2.5% 0.9%

Domestic Demand Growth (%RPK) 6.0% 9.0% 6.8%

Domestic Load Factor 71% 75% 71%

Passengers Transported (in million) 41 42 39

GOL Domestic Capacity (ASK billion) 48 49 48

RPK, System (in billion) 37 39 36

Departures (000) 354 364 349

CASK ex-fuel (R$ cents) 9.0 9.6 10.2

Fuel Liters Consumed (billion) 1.60 1.75 1.66

Average Exchange Rate (R$/US$) 1.95 2.00 1.95

Operating Margin (EBIT) Negative -11.2%

Terms and Condition of GOL Transportes Aéreos

• Fares are round trip. Fares incl. all fuel surcharges, our service fees and taxes.

• Tickets are non refundable, non transferable, non-assignable.

• Name changes are not permitted.

• Fares are subject to change without notice.

• Fares subject to availability.

• There is a higher probability of seats being available at this fare on Tuesday,

Wednesday and Thursday and may require a Saturday night stay at your destination.

TAM AIRLINES

INTRODUCTION

• TAM Airlines (Portuguese: TAM Linhas Aéreas is the Brazilian brand of LATAM

Airlines Group. The merger of TAM with LAN Airlines was completed on June 22,

2012. The company is currently the largest Brazilian airline. Before the takeover,

30

TAM was Brazil's and Latin America's largest airline. Its headquarters are in Sao

Paulo, operating scheduled services to destinations within Brazil, as well as

international flights to Europe and other parts of North and South America. The

airline announced that it will withdraw from the Star Alliance during the second

quarter of 2014 and will join One world immediately afterwards. A date is expected

to be announced late 2013.

HISTORY

TAM – Taxi Aereo Marília

• TAM – Taxi Aereo Marília and TAM – Transportes Aéreos Regionais were two

different entities, although both belonged to the TAM Group. TAM – Marília, an air

taxi company founded in 1961, provided the start-up infrastructure for TAM –

Regionais.

• TAM – Transportes Aéreos Regionais (KK)

• On November 11, 1975, the Government of Brazil created the Brazilian Integrated

System of Regional Air Transportation and divided the country in five different

regions, for which five newly-created regional airlines received a concession to

operate air services. Founded by Rolim Adolfo AmaroTAM

• TAM (KK) joint operations with TAM (JJ)

• In August 1986, the company, under financial stress, went public and began floating

stock in the market. The same year, TAM – TransportesAéreosRegionais (KK)

acquired another regional airline, VOTEC, which operated in areas of northern and

central Brazil. VOTEC was then renamed Brasil Central LinhasAereas. The

different color schemes of the aircraft, and their designated areas of operation. In

1988, TAM flew its 3 millionth passenger. On May 15, 1990, the Brazilian

Government lifted restrictions on operational areas of regional airlines allowing

them to fly anywhere in Brazil. As a consequence, Brasil Central was renamed

TAM – Transportes Aéreos Meridionais, acquired the same color scheme of TAM

(KK) but maintained the IATA code JJ.

31

• Agreement with LAN to create LATAM

• On August 13, 2010, TAM signed a non-binding agreement with Chilean airline

LAN Airlines to merge and create LATAM Airlines Group. This was changed into

a binding agreement on January 19, 2011. Latam agreement was approved with 11

restrictions by Chilean authorities on September 21, 2011 On December 14, 2011,

Brazilian authorities approved the agreement imposing similar restrictions as

Chilean authorities. Presently TAM has two pairs of slots while LAN has four. LAN

will have to cede two pairs to competitors interested in using them.

• DESTINATIONS AND FLIGHTS

1. Around 150 destinations in 22 countries.

2. Domestic operations in 6 countries (Argentina, Brasil, Chile, Colombia, Ecuador

and Peru).

3. International flights to/from Latin America,United States, Europe and Oceania.

4. Daily flights: average of 897 (TAM) + 575 (LAN) daily departures in 2011.

EMPLOYEES:

• Total =51600

• LAN=21800

• TAM=29800

• 13.5 Billion Gross Income [2011]

• 5.7 billion LAN

• 7.8 billion TAM• Total fleet: 310 aircraft (149 LAN + 161 TAM)

• Average fleet age: 6,9 years.

• Passengers Aircraft : 135 LAN + 161 TAM

• Cargo aircraft: 14 LAN

32

• Orders: 240 (137 LAN + 103 TAM)

POLICY AND NORMS OF TAM AIRLINES

• Conclusions in the TAM Flight 3054 crash investigation report by São Paulo's

Instituto de Criminalística were released to the press today, after 16 months of

work. According to OESP, the report concludes that the plane crash was caused by a

series of errors at different decision levels. Although it confirms that the left thrust

lever was in full reverse while the right thrust lever was in "climb", the final report,

signed by Antonio de Carvalho Nogueira Neto, affirms pilots were not properly

trained by TAM, were not adequately informed about runway conditions, and

lacked an alarm, not installed in the Airbus, which could have warned them of

improper throttle handling.

INDIAN AIRLINES

AIR INDIA

Introduction

• Air India is the flag carrier airline of India. It is part of the government owned Air

India Limited (AIL). The airline operates a fleet of Airbus and Boeing aircraft

serving Asia, the United States, and Europe Its corporate office is located at the

Indian Airlines House, in the parliament street of New Delhi.

HISTORY

Early years

Tata Sons, a division of Tata Sons Ltd. (now Tata Group) was founded by J. R. D. Tata in

1932. The aviator NevillVintcent had an idea to run mail flights from Bombay and

Colombo that connected with the Imperial Airways flights from the United Kingdom. He

found a supporter for his plans from J. R. D. Tata of the Tata Iron and Steel Company.

After three years of negotiations Vintcent and Tata won a contract to carry the mail in April

1932 and in July 1932 the Aviation Department of Tata Sons was formed. On 15 October

33

1932, J.R.D. Tata flew a single-engined De Havilland Puss Moth carrying air mail (postal

mail of Imperial Airways) from Karachi's Drigh Road Aerodrome to Bombay's Juhu

Airstrip via Ahmedabad. profit of 60,000 rupees its first year, and by 1937, that profit had

risen to 600,000 rupees.

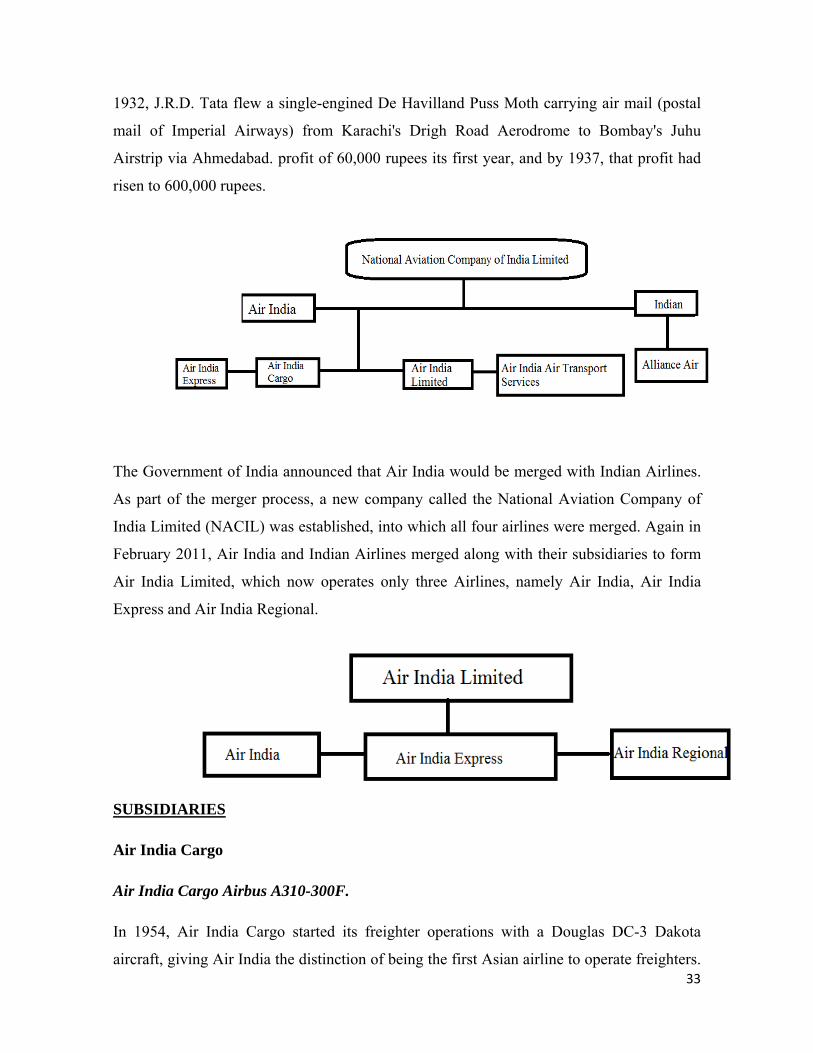

The Government of India announced that Air India would be merged with Indian Airlines.

As part of the merger process, a new company called the National Aviation Company of

India Limited (NACIL) was established, into which all four airlines were merged. Again in

February 2011, Air India and Indian Airlines merged along with their subsidiaries to form

Air India Limited, which now operates only three Airlines, namely Air India, Air India

Express and Air India Regional.

SUBSIDIARIES

Air India Cargo

Air India Cargo Airbus A310-300F.

In 1954, Air India Cargo started its freighter operations with a Douglas DC-3 Dakota

aircraft, giving Air India the distinction of being the first Asian airline to operate freighters.

34

The airline operates cargo flights to many destinations. The airline also has ground truck-

transportation arrangements on select destinations. A member of IATA, Air India carries all

types of cargo including dangerous goods (hazardous materials) and live animals, provided

such shipments are tendered according to IATA Dangerous Goods Regulations and IATA

Live Animals Regulations.

AIR INDIA REGIONAL

Air India Regional was started as a low-cost arm of Indian as Alliance Air As part of

Indian's merger with Air India

AIR INDIA EXPRESS:

Air India Express is the airline's low-cost subsidiary headquartered in Mumbai, operating

mainly from Indian state of Kerala. It operates services mainly to the Middle East and

Southeast Asia.

SERVICES:

• IN-FLIGHTENTERTAINMENT

• FREQUENT FLYER PROGRAMME

• PREMIUM LOUNGE

Jet Airways

INTRODUCTION

Jet Airways is the second largest Indian airline based in Mumbai, Maharashtra, both, in

terms of market share and passengers carried. It is owned by NareshGoyal. It operates over

400 flights daily to 76 destinations worldwide. Its main hub is Mumbai, with secondary

hubs at Delhi, Kolkata, Chennai, Bengaluru and Pune. It has an international hub at

Brussels Airport, Belgium.

History

1992-2009: Inception and growth

35

Jet Airways was incorporated as an air taxi operator on 1 April 1992. It started commercial

operations on 5 May 1993 with a fleet of four leased Boeing 737-300 aircraft. In January

1994 a change in the law enabled Jet Airways to apply for scheduled airline status, which

was granted on 4 January 1995. NareshGoyal – who already owned Jetair (Private)

Limited,

SERVICES

• Cabin

• First Class

• Economy Class

• In-flight entertainment

Terms and Condition of Jet Airway

General Information

While compiling this information, Jet Airways has endeavored to ensure that all

information is correct. However, no guarantee or representation is made to the accuracy or

completeness of the information contained here. This information is subject to changes by

Jet Airways without notice.

• Non-Smoking

• Reservation

Reservation Requirements

• Ticketing / Fares and Time Limit

Jet Airways

Founded April 1, 1992

Commenced operations May 5, 1993

Hubs ChhatrapatiShivaji International Airport (Mumbai) (Primary Hub

& Maintenance Base)

Secon

Focus

Frequ

Airpo

Subsid

Fleet s

Destin

Comp

Paren

Headq

Key p

Reven

Profit

Emplo

Websi

COM

Brazil

Name

ndary hubs

s cities

uent-flyer pr

ort lounge

diaries

size

nations

pany slogan

nt company

quarters

people

nue

t

oyees

ite

PARISON

l Airlines In

rogram J

J

J

1

7

T

T

M

1

w

OF BRAZI

ndustry

Gol t

Beng Bruss Chen Indira Netaj

Airpo Pune Sarda

Airpo Coch Rajiv

JetPrivilege

Jet Lounge

JetKonnect

122

73

The Joy of F

Tailwinds Li

Mumbai, Ind

Nares Nikos Ali G

172.84 bi

-14.20 bi

13,945 (2012

www.jetairw

L AIRLINE

transport esa

galuru Internsels Airport

nnai Internatia Gandhi IntjiSubhash ort(Kolkata)Internationa

arVallabhbhaort(Ahmedabhin Internatiov Gandhi Inte

Flying

imited

dia

shGoyal, Fos Kardassis,

Ghandour, Diillion (US$3

llion (US$−2

2)

ways.com, ww

ES AND IN

aereos

national Airp(Brussels) ional Airporternational A

Chandra

al Airport(Puai bad) onal Airport(ernational A

ounder &ChaCEO

irector 3.2 billion) (2

260 million)

ww.jetkonne

NDIAN AIRL

Indian A

Jet airway

port (Bangalo

rt (Chennai) Airport (Delha Bose

une) Patel

(Kochi) Airport (Hyde

airman

2012)

) (2012)

ect.com

LINES

Airlines Indu

ys

ore)

hi) Interna

Interna

erabad)

ustry

36

ational

ational

37

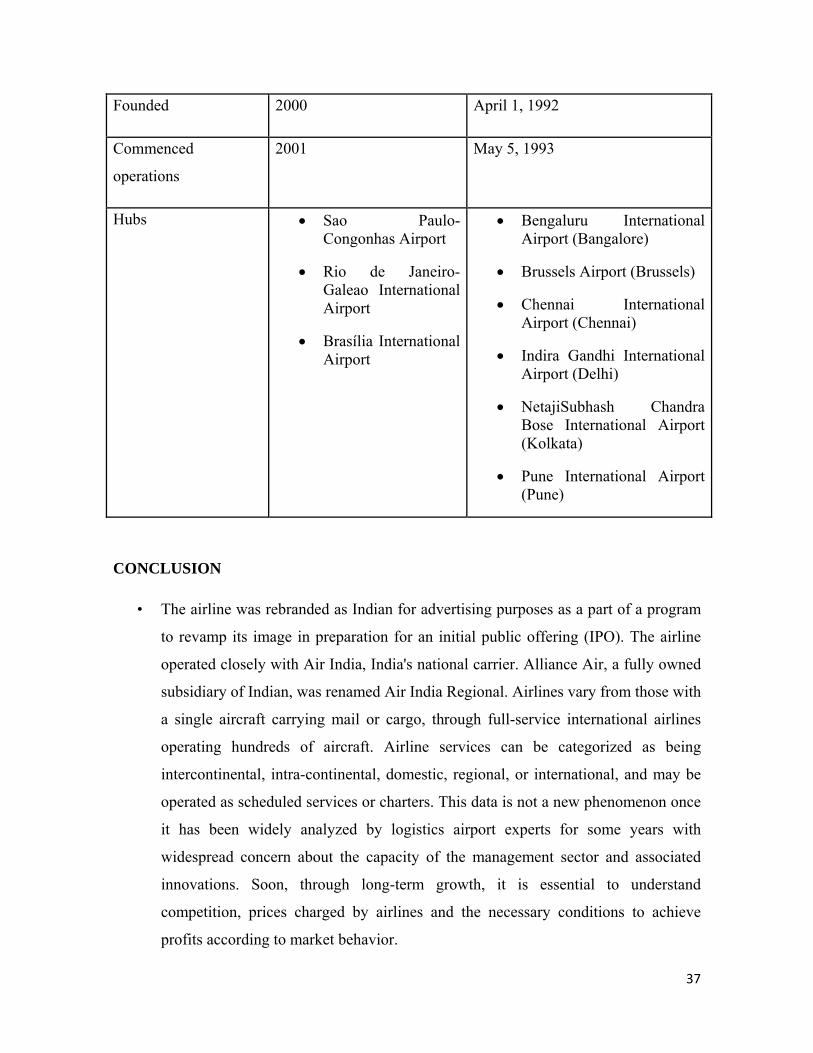

Founded 2000 April 1, 1992

Commenced

operations

2001 May 5, 1993

Hubs Sao Paulo-Congonhas Airport

Rio de Janeiro-Galeao International Airport

Brasília International Airport

Bengaluru International Airport (Bangalore)

Brussels Airport (Brussels)

Chennai International Airport (Chennai)

Indira Gandhi International Airport (Delhi)

NetajiSubhash Chandra Bose International Airport (Kolkata)

Pune International Airport (Pune)

CONCLUSION

• The airline was rebranded as Indian for advertising purposes as a part of a program

to revamp its image in preparation for an initial public offering (IPO). The airline

operated closely with Air India, India's national carrier. Alliance Air, a fully owned

subsidiary of Indian, was renamed Air India Regional. Airlines vary from those with

a single aircraft carrying mail or cargo, through full-service international airlines

operating hundreds of aircraft. Airline services can be categorized as being

intercontinental, intra-continental, domestic, regional, or international, and may be

operated as scheduled services or charters. This data is not a new phenomenon once

it has been widely analyzed by logistics airport experts for some years with

widespread concern about the capacity of the management sector and associated

innovations. Soon, through long-term growth, it is essential to understand

competition, prices charged by airlines and the necessary conditions to achieve

profits according to market behavior.

38

4.AUTOMOBILE INDUSTRY

Brazil has transcended its condition as the biggest and most resource-rich country in

Latin America to now be counted among the world’s essential powers.

Brazil is not a conservative military power, it does not competitor China or India in

population or economic size, and it cannot counterpart the geopolitical history of

Russia. At rest, how Brazil defines and projects its benefit, a still-evolving process,

is critical to understanding the nature of the new multipolar and random global

order.

Brazil has plentiful natural resources and its economy is quite diversified.

Brazil has in the past, imposed strict pedals over cross border currency business

through a foreign exchange policy that required the register of transactions and

positioned controls mainly on transactions involving outflows of funds from the

country.

Brazil is also a vast industrial country. It benefits from its mineral ore capital and is

the second world exporter of iron and one of the main manufacturers of aluminum.

As an oil producer, the Brazil is aiming to become autonomous in the close to

future. The country is asserting itself more and more in the 1)textile, 2)aeronautics,

3) pharmacy, 4)automobile, 5)steel and 6)chemical industry sectors.

The auto mobile industry is often consideration of as one of the most global of all

the other industries. Its products have spread in the world, and it is under enemy

control by an undersized number of companies with worldwide recognition.

Though, in certain respects the industry is more local than global.

The extend of vehicle manufacture in developing countries inflated markedly in the

thunder years of rapid expansion in the emerging markets in the 1990s.

Global vehicle invention growth almost 7 million units between 1990 and 1997,

although the boost in sales over the same period lagged considerably behind this, at

just under 4 million units.

The automobile industry in country like South Korea, Brazil, China and India is

currently going through impressive growth.

This report discusses industrial development matters for the global auto industry

from the perspective of a global value chain analysis. It places of interest the way in

39

which the blow of globalization processes on the auto industry of developing

countries in the 1990s was partial not only by changes in trade and investment

policies and the globalization strategies of leading companies, but also by changes

within auto industry value chains themselves.

It is related with the following selected countries and regions including 1. China, 2.

India, 3. Mexico, and countries of the Association of Southeast Asian Nations

(ASEAN), Argentina, Brazil, and countries in Central Europe .

These developments in automobile now-a-days suggest that global supply chain

networks are fetching more and more vital. Assemblers and suppliers expand

equivalent networks across the globe. For simplicity, immediately a single product

being supplied to one assembler operating in three different countries: the country

of the assembler’s core operations, and operations in two other locations.

Various developing countries used import substitution industrialization policies to

support the development of their conjugal auto industries. In the beginning of the

year 1990s, there were considerable self-contained vehicle industries in Latin

America, the ASEAN region, India and China with limited exports. Quantitative

limitations were phased out and tariffs concentrated, while Trade-Related

Investment Measures (TRIMs) like local content requirements and foreign exchange

balancing were under increasing hit. At the same time, the global production and

sales strategies of most important international auto companies were also shifting

and developing countries were becoming more essential to their plans. This report

tells that while these changes were most obvious in the assembly sector, even more

major changes were taking place in components production, ambitious as much by

the alterations in the nature of value chain relationships between assemblers and

suppliers as by the company’s globalization.

These changes have had a thoughtful effect on the structure and uniqueness of the

auto industry in developing countries. This report identifies the position of the up-

and-coming markets in the global auto industry. It considers how the industry

changed with time, what effects are for the policy options open to the governments

of developing countries, and what kinds of policies will be sufficient to create

40

feasible auto industries in the new environment of lower levels of protection and

increasingly globalized construction systems.

Markets of BRICS countries now-a-days attracts never seen before in 1.USA,

2.Europe and 3.Japan, and therefore, opening opportunities for the development of

the restricted industry in those countries; Movement of the industry towards cleaner

alternatives, specifically about energy and engine and driving systems at the

vehicles.

There is 500 years of old relations between Brazil and India.

Diplomatic relations between such two companies established in 1948.

From some decades, this relation is extended to Science, Technology,

Pharmaceutical and Space.

Mutual relations between Brazil and India have developed significantly and a

strategic corporation exists between the two countries, said Mr Carlos Duarte,

Brazil’s Ambassador to India, while addressing a seminar on doing business with

Brazil organized by FIEO in connection with the Indo-Brazil Chamber of

Commerce and Industry on November 8, 2012 at New Delhi.

Mr .Duarte informed that in spite of a slowdown, the essentials for Brazil’s constant

inclusive growth remain solid. These include the rising rate of service, expansion of

credit, decreasing real interest rates, inflation under control, optimistic trade balance

and declining fiscal shortfall.

He appreciated that social policies have been winning in tackling dissimilarity, and

are helping to lift up and merge internal purchasing power.

At a time when some of the most important Western economies are slamming their

doors on Indian exports, Brazil is looking at ornamental trade ties with India.

This Latin American country is looking to boost mutual trade with India by

attractive the number of products which could be imported or exported between the

two countries - two of the best ever rising nations in the world.

The Brazilian automobile industry competed with other Latin American ones

(Mexico and Argentina) comparably till the year 1960 but had two jumps then,

making Brazil as regional leader at first and one of the World's leaders moreover.

41

The Brazilian industry is regulated by the company “Associação National dos

Fabricants de Vacuoles Automotives (Anfavea)”,. A fovea is part of

the Organization International des Constructers’ d'Automobiles (OICA), based in

Paris. Most of huge global companies are present in Brazil; such

as 1.Fiat, 2.Volkswagen Group, 3,Ford, 4.GM, NissanMotors, Toyota, etc., and

also the rising nationalized companies such as Troller, Marco polo

S.A., Agrale, Random, Excalibur etc., some of them traditionally produces the

modern equipped replicas of old-timers.

1. On hand laws for components take back (tiers and batteries) but with little

effectiveness;

2. Discussion of laws aiming at regulation of vehicle examination, disassembly

facilities and parts recycle;

3. Design, assembly and supply practices attached to global strategies;

4. Hidden development of a sector of recycling of automotive components;

5. Sturdy players in the steel and extraction industry;

6. Lack of technology in recycling multifaceted components and materials;

7. Role of the producers in defining the ‘rules’ of the game;

Automobile industry has more than 50 years in Brazil. With the stable growing of

local market and the end of development /engineering centers, the country is now

one of the vast players in the international market. There are just about 500 parts

suppliers in the country.

This progress has permissible the Brazilian automobile industry to maintain itself on

the competitive universal market, such as for low-cost compact cars, as well as for

trucks, buses, and agricultural equipment for use in the unkind operating conditions

inbuilt to every country. This qualitative development has been both 1.vertical

2.horizontal.Vertical including the whole production chain from the manufacture of

steel plates, pieces and parts, to concluding details, and horizontal, in having

occurred in all the companies operating throughout Brazil’s vast landmass.

There are 49 industrial flora in the country, in 8 different states. it is an industrial

complex with capacity to produce 4 million vehicles, with a forecasted capacity of 6

million for the year 2013. The introduction of ‘flex’ engines is a major reference in

42

the market for bio fuels; 87% of all the passenger car put on in brazil were ‘flex’

More companies are investing in brazil , including new entrants to the south

American market ,such as Chinese.

Brazil has now the 4th largest global producing industry, this year having moving in

advance of the U.S. and Germany.

Brazilian Market: As symbols of a recovery in Brazil’s economy carry on to

accumulate, the automobile sector appears to be most important the way with good

news, with new assembly plants intended and reports pointing to major potential

development in developed capacity. Government played a major role in the

development of the industry in this country.

The Brazilian government has been annoying to attract foreign car manufacturers to

Brazil by offering tax breaks for those who majority-manufacture locally.

The government has long been hopeful Brazilians to buy more cars in a bid to boost

the economy, by reducing IPI (industrialized product tax) to zero on some models,

as well as ensuring cheaper loans.

Local automotive production has seen a fall of 2% compared to few last years,

which was recognized to a 20% fall in exports. Congestion in many global markets

makes it more tricky to export, but it must be noted that export markets account for

only 13% of restricted production, unlike many other countries that depend mainly

on exports.

Top four Automobile Industries in Brazil:

1. AGRALE :

1.Military vehicles,

2. Motorcycles,

3. Scooters commercial vehicles,

4. Engines and tractors.

43

2. LOBINI: Sports car

3. TAC MOTORS: Four-wheel drive TAC STARK

4. TROLLER: Off-road vehicles , few convention races just about the world

including the Dakar Rally.

Policies: India: The economic needs of the country, efficient use of foreign

exchange and trade as well as consumer necessities are the basic factor which

influences India's import policy. On the import side the policy has three