a guide for improved business performance - experian · approval rates booking or activation rates...

TRANSCRIPT

Enhance your decision-making capabilities

A guide for improved business performance

TABLE OF CONTENTS

© Experian Information Solutions, Inc. 2011. All rights reserved

Introduction .............................................................................................................. 1

Section I – Identify ................................................................................................... 3

Which types of decisions to improve? ............................................................................. 3 Business improvement opportunities .............................................................................. 4 Decision type objectives ................................................................................................. 5

Section II – Prioritize ................................................................................................ 8

Quantify expected business value .................................................................................. 8 Assess level of effort ....................................................................................................... 9 Create implementation roadmap ................................................................................... 11

Section III – Implement .......................................................................................... 13

Components of an optimized decision-making system ................................................. 13 Define your client-specific requirements ....................................................................... 17 Define recommended solution architecture .................................................................. 19 Implement solution and measure results ...................................................................... 20

Conclusion ............................................................................................................. 23

Appendix A: Products and services glossary ..................................................... 24

Core Decisioning Software ........................................................................................... 24 Software Solutions ........................................................................................................ 24 Analytics/Models ........................................................................................................... 27 Data/Trigger Solutions .................................................................................................. 29 Services/Reports .......................................................................................................... 31

Appendix B: About Experian ................................................................................ 33

TABLE OF CONTENTS

© Experian Information Solutions, Inc. 2011. All rights reserved

This document contains information that is the exclusive property of Experian. In consideration of the receipt of this document, you agree to make this information available only to your employees, directors, representatives, and agents who need access to such information for the purpose of evaluating its contents. You recognize and acknowledge the competitive value, confidential and proprietary nature of the information contained herein or which may hereafter be furnished to you or obtained by you from Experian relating to the subject matter hereof or the services to be performed, as well as the damage which may result to Experian if this information is disclosed to any third party. Except as set forth above, in no event shall this information be disclosed to any third party for any purpose without the prior written consent of an authorized representative of Experian. Further, your review and use of this information is an affirmative acknowledgment by you that you understand, acknowledge, and agree to abide by the foregoing. Experian and the marks used herein are service marks or registered trademarks of Experian. Version: General v2.2

INTRODUCTION

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 1

INTRODUCTION Experian’s expertise in information and data analytics provides companies with the unparalleled insight to make better decisions and fulfill their missions. For financial institutions, telecommunications carriers, energy companies, health-care providers and other companies that need advanced decision-management functionality, improved access to third-party data sources, and better model deployment and scoring capabilities, Experian® provides predictive scoring and decisioning capabilities in both hosted and end-user-installed environments.

Purpose of this guide

The purpose of this guide is to help you identify, prioritize and implement enhanced decision-making capabilities for improved business performance. It is organized in three sections:

Section I – Identify Identify opportunities for improvement by exploring decisioning improvement initiatives across all lines of business and all areas of the Customer Life Cycle.

Section II – Prioritize Prioritize the various opportunities based on potential business value and implementation complexity, and create an implementation roadmap.

Section III – Implement Implement the highest-priority initiatives, and generate positive business results.

INTRODUCTION

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 2

Intended audience

This guide is intended for the following types of companies and organizations:

• Banks, credit unions and other financial institutions of all sizes

• Finance and credit companies

• Retailers

• Telecommunications, energy and utilities companies

• Healthcare providers

• Collections agencies

• Companies that provide products or services to companies listed above

It is intended for individuals in any of the following disciplines:

• Senior management

• Risk and portfolio management professionals

• Information technology personnel

• Credit and collections individuals

• Fraud prevention professionals

• Call center and customer care personnel

• Senior financial or lending executives

• Business and statistical analysts

• Marketing and business development professionals

SECTION I – IDENTIFY

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 3

SECTION I – IDENTIFY This section helps you identify the various types of decisions that are relevant to your company that can be improved or optimized through the use of data, analytics and decision management software.

Which types of decisions to improve? The table below summarizes the types of decisions that are relevant for various companies and lines of business. You can use this information to begin identifying which types of decisions warrant attention for potential improvement.

Relevant types of decisionsApplicable companies Applicable lines of business

Bank

s, c

redi

t uni

ons,

oth

er F

Is

Fina

nce

and

cred

it co

mpa

nies

Ret

aile

rs

Tele

com

, ene

rgy

and

utilit

ies

Hea

lth-c

are

prov

ider

s

Gov

ernm

ent a

genc

ies

Col

lect

ions

age

ncie

s

Pro

cess

ors

and

rese

llers

Stud

ent l

oans

Dep

osits

Pers

onal

/uns

ecur

ed

Cre

dit c

ard/

debi

t car

d

Vehi

cle

finan

ce

Hom

e eq

uity

Mor

tgag

e

Sm

all b

usin

ess

Com

mer

cial

Cross-sell determination ● ● ● ● ● ● ● ● ● ● ● ● ● ●Prospect determination ● ● ● ● ● ● ● ● ● ● ● ● ● ●Pre-screen decision ● ● ● ● ● ● ● ● ● ● ● ● ● ●Offer / treatment determination ● ● ● ● ● ● ● ● ● ● ● ● ● ●Fraud determination ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●Approve/decline decision ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●Initial credit line/limit/usage amount ● ● ● ● ● ● ● ● ● ● ● ● ● ●Initial pricing determination ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●Risk-based pricing ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●NSF pay/no-pay decision ● ● ●Overlimit/shadow limit authorization ● ● ● ● ●Credit line/limit/usage management ● ● ● ● ● ● ● ● ●Retention decisions ● ● ● ● ● ● ● ● ● ● ● ● ● ●Loan/payment modification ● ● ● ● ● ● ● ● ● ● ●Repricing determination ● ● ● ● ● ● ● ● ● ● ● ● ● ●Predelinquency treatment ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●Early/late-stage delinq treatment ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●Collections agency placement ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●Collection/recovery treatment ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●

SECTION I – IDENTIFY

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 4

Business improvement opportunities The table below summarizes those metrics that can be positively impacted by improvements for each type of decision. You can use this table to help identify the decision areas to focus on based on the metrics that are most important to your company.

▲= Increase; ▼ = Decrease

Metrics that can be positively impacted by better decisions

Appr

oval

rate

s

Book

ing

or a

ctiv

atio

n ra

tes

Rev

enue

Cus

tom

er n

et p

rese

nt v

alue

30/6

0/90

-day

del

inqu

enci

es

Aver

age

char

ge-o

ff am

ount

Aver

age

reco

very

am

ount

Man

ual r

evie

w ra

tes

Annu

al a

pplic

atio

n vo

lum

e

Cha

rge-

offs

(bad

deb

t & fr

aud)

Avg.

cos

t per

dol

lar c

olle

cted

Aver

age

amou

nt c

olle

cted

Annu

al re

cove

ries

Reg

ulat

ory

com

plia

nce

Chu

rn o

r attr

ition

Cross-sell determination ▲ ▲ ▲ ▼ ▲ ▼Prospect determination ▲ ▲ ▲ ▲ ▼ ▲ ▼Prescreen decision ▲ ▲ ▲Offer/treatment determination ▲ ▲ ▲ ▼ ▲ ▼Fraud determination ▲ ▲ ▲ ▼ ▼ ▲ ▼ ▼Approve/decline decision ▲ ▲ ▲ ▲ ▼ ▼ ▼ ▲ ▼Initial credit line/limit/usage amount ▲ ▲ ▲ ▲ ▼ ▼ ▼ ▲ ▼Initial pricing determination ▲ ▲ ▲ ▲ ▼ ▼ ▼ ▼ ▲ ▼Risk-based pricing ▲ ▲ ▲ ▲ ▼ ▼ ▼ ▼ ▲ ▼NSF pay/no-pay decision ▲ ▲ ▼ ▼ ▼ ▼ ▼Overlimit/shadow limit authorization ▲ ▲ ▼ ▼ ▼ ▼ ▼Credit line/limit/usage management ▲ ▲ ▼ ▼ ▼ ▼ ▲ ▼Retention decisions ▲ ▲ ▼ ▼Loan/payment modification ▲ ▼ ▼ ▼ ▼ ▲ ▼Repricing determination ▲ ▼ ▼ ▼ ▼ ▲ ▼Predelinquency treatment ▲ ▼ ▼ ▼ ▼Early/late-stage delinq treatment ▲ ▼ ▼ ▲ ▼ ▼ ▲ ▲ ▼Collections agency placement ▲ ▼ ▲ ▼ ▼ ▼ ▲ ▲Collection/recovery treatment ▲ ▼ ▲ ▼ ▼ ▼ ▲ ▲

SECTION I – IDENTIFY

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 5

Decision type objectives The objective of each type of decision is described in the chart below, along with brief explanations on how improved decision-making capabilities could yield incremental business value.

Decision type Decision objective

Cross-sell determination

To increase revenue and retention by 1) identifying cross-sell opportunities for existing customers (and for new customers at the time of account origination), by 2) identifying the ideal package of products and services for each customer, and by 3) taking action when behavioral customer actions warrant immediate cross-sell activity.

Prospect determination To increase application volume, approval rates, activation rates and overall revenue by identifying those prospects most likely to respond and accept your offer and become profitable customers.

Prescreen decision To increase application volume, approval rates, activation rates and revenue, while reducing marketing costs by “pre-screening” potential customers to ensure they meet your pre-defined criteria before you extend an offer.

Offer/treatment determination

To increase approval rates, activation rates, retention rates and overall profitability by ensuring the right offer is made, at the right time, for the right product, through the right channel at the right price.

Fraud determination To reduce losses to fraud, to reduce manual review rates, to increase approval rates and improve the customer experience (through fewer false positives), and to ensure regulatory compliance by identifying fraudulent behavior quickly.

Approve/decline decision To increase approval rates, activation/booking rates and customer NPV, while reducing credit risk, fraud risk and manual reviews and ensuring regulatory compliance by making effective and automated approve/decline decisions for new applicants.

Initial credit line/limit/usage amount

To increase approval rates, activation/booking rates and customer NPV, while reducing delinquencies and attrition by assigning the optimal initial credit lines, loan amounts or usage limits at the time of origination.

Initial pricing determination

To increase approval rates, activation/booking rates and customer NPV, while reducing delinquencies and attrition and ensuring regulatory compliance by assigning the optimal interest rate, fees, service plans or payment terms at the time of origination.

SECTION I – IDENTIFY

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 6

Decision type Decision objective

Risk-based pricing

To increase approval and activation rates, to promote higher revenue from good customers, to reduce risk from high-risk segments, to ensure regulatory compliance and to reduce attrition by creating and assigning pricing and service plans that are tied to customer risk.

NSF pay/no-pay decision To increase fee-income, to improve customer NPV, to reduce manual review rates and to reduce attrition by automatically determining when to pay or not pay a check that has been written against an account with insufficient funds.

Over-limit/shadow limit authorization

To increase interest income by authorizing a “shadow limit” to qualified credit card holders that allows them to spend over or above their credit limit.

Credit line/limit/usage/ management

To increase revenue, while reducing delinquencies and attrition by modifying or managing credit lines, line amounts, usage limits or service plans for existing customers. For example, increase credit limits of low-risk revolvers (for credit card accounts), reduce limits or control/cancel usage on high-risk segments, promote balance growth (for revolving accounts) by allowing low-risk clients to “skip a payment” without falling delinquent.

Retention decisions To reduce attrition by proactively assigning and offering the most effective retention treatment strategies and by taking immediate action when behavioral customer actions warrant retention activity.

Loan/payment modification To reduce delinquencies, charge-offs and losses to bad debt, and to ensure regulatory compliance, by modifying loan or payment terms to high-risk clients in an optimized manner to maximize overall profitability.

Repricing determination To increase revenue; to reduce losses and attrition; and to ensure regulatory compliance by modifying interest rates, fees, service plans or payment terms for existing customers.

Predelinquency treatment To reduce delinquencies and charge-offs by identifying non-delinquent customers with a high probability of payment difficulties in the near future. Proactively contact these customers and resolve financial problems before delinquency.

Early/late-stage delinquency treatment

To reduce later-stage delinquencies and charge-offs and to reduce manual review expenses by assigning the appropriate delinquency treatment by level of risk. For example, allow low-risk accounts to self-cure while focusing on high-risk segments.

SECTION I – IDENTIFY

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 7

Decision type Decision objective

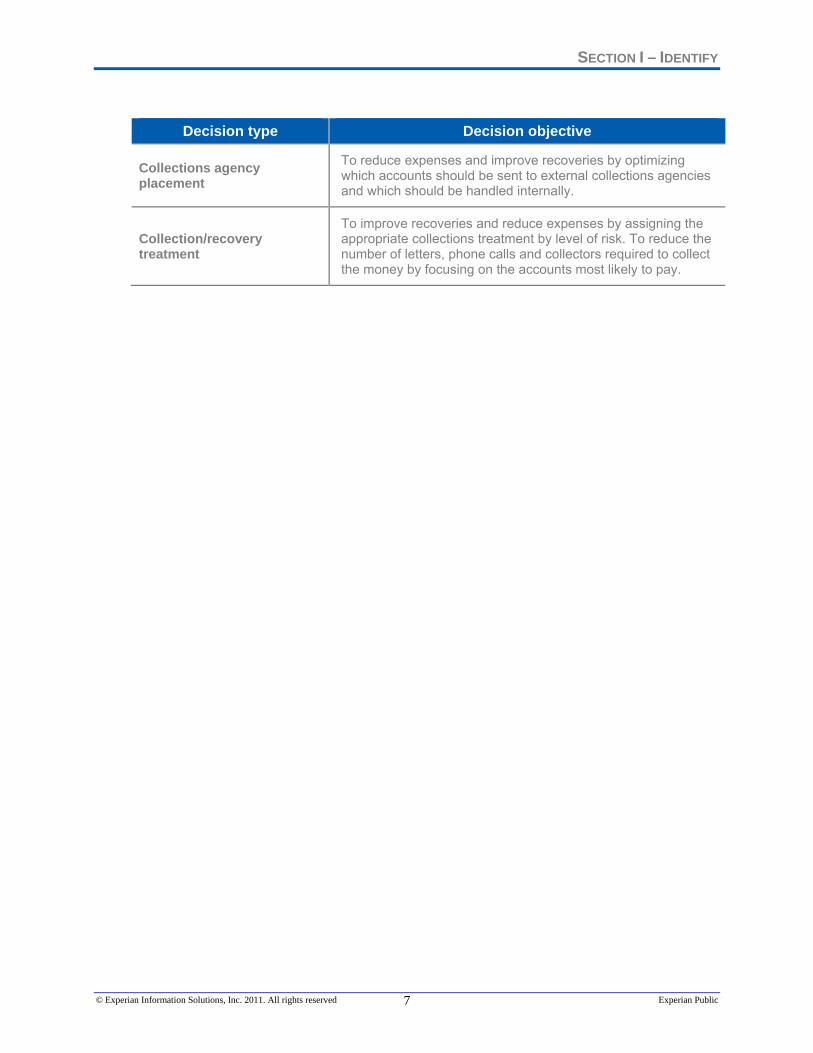

Collections agency placement

To reduce expenses and improve recoveries by optimizing which accounts should be sent to external collections agencies and which should be handled internally.

Collection/recovery treatment

To improve recoveries and reduce expenses by assigning the appropriate collections treatment by level of risk. To reduce the number of letters, phone calls and collectors required to collect the money by focusing on the accounts most likely to pay.

SECTION II – PRIORITIZE

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 8

SECTION II – PRIORITIZE Once you have identified all of the potential areas for improvement, the next step is to prioritize decision-making improvement efforts based on potential business value and the level of effort and cost required to achieve the expected business benefits.

Quantify expected business value The value from improved decision-making capabilities is typically generated by improvements in one or more of the following areas:

Efficiency Reduce costs through the automation of manual checks; improve the consistency of data to enhance the quality of decisions; minimize manual processes; reduce errors and associated rework

Speed Meet or exceed customer expectations with instant decisions; improve take-up rates by minimizing delays; instantly identify cross-sell/up-sell opportunities

Agility Remove dependence on IT or vendor support; quickly adapt to changing market conditions or competitor activity; implement new product propositions without delay

Accuracy Validate all data to minimize errors; make thousands of decisions instantly and accurately; create granular / complex segmentation models to better target customers

Consistency Centralize control over all decision points; use validated and automated data; minimize manual intervention in the decisioning process

As a general rule of thumb for creating an initial high-level business case, you can typically assume between 5 percent and 15 percent business improvement by enhancing the quality of your decision making capability.

The table on the following page provides a simple example that calculates the approximate annual benefit of making a 15 percent and 10 percent improvement to attrition rate and customer NPV, respectively.

SECTION II – PRIORITIZE

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 9

As you develop high-level business benefit calculations, each major assumption should be identified so that you can use them as key performance indicators as you measure future progress.

Target objective

Example benefit calculation

Annual benefit

Reduce attrition by 15%

250,000 (New accounts per year – assumption) $180 (Net present value of each new account) $45,000,000 (Value of new accounts: 250,000 x $180) $16,200,000 (Loss in value due to attrition: $45,000,000 x 36% attrition) $2.4 million (Value of reducing attrition by 15%: $16.2 million x 15%)

$2.4 million per year

Increase customer NPV by 10%

250,000 (New accounts per year – assumption) $180 (Net present value of each new account) $45,000,000 (Value of new accounts: 250,000 x $180) $198 (10% improvement in NPV: $180 x 1.10) $18 (Incremental dollar improvement in NPV $198 - $180) $4,500,000 (Incremental value from improved NPV: 250,000 x $18)

$4.5 million per year

Total expected annual business benefit: $6.9 million per year

Assess level of effort As you assess the level of effort to make an improvement, you should examine and understand the challenges of your current environment and identify those things that are holding you back today from making better decisions. As you understand your current constraints, you can begin to assess the level of effort needed to make the necessary improvements.

The table on the following page identifies some of the typical problems and challenges that must be addressed as companies strive for improved decision-making effectiveness. The better you understand your true obstacles to success, the better you’ll be able to determine the appropriate solution to achieve your business expectations.

SECTION II – PRIORITIZE

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 10

As you review the issues and challenges identified below, you should identify those that are most relevant to your organization.

Typical issues and/or challenges

We are unable to leverage more than a few variables (four or five), and are therefore limited in our ability to manage credit risk effectively. This situation causes significant credit losses.

Given limitations in the current environment, deployment of new predictive risk models is problematic and time-consuming, resulting in significant delays to receiving the expected business benefits of the new models.

We are unable to take advantage of test-and-learn capabilities in a Champion/Challenger environment, making it infeasible to easily test new strategies in a risk-controlled manner. This issue results in significant lost opportunity due to slow time-to-market with strategy changes.

It takes too long and it’s technically infeasible to access new data sources for use in making more effective decisions, resulting in higher costs and lower-quality decisions.

We need to reduce costs by outsourcing applications in a hosted model where appropriate.

We have numerous disparate systems for bureau access, model deployment and decision management across our various lines of business and across different areas of the Customer Life Cycle. This issue creates cost inefficiencies, inconsistent decisions and slow time-to-market with strategy changes.

We are unable to effectively create and manage new custom attributes for use in its models and decision strategies.

Our current decisioning environment requires significant support from an IT perspective to make credit policy and other strategy changes, resulting in higher costs and a lack of agility. The lack of agility makes it difficult for us to react quickly to (and take advantage of) changing market conditions and other opportunities.

Our current systems lack “business user” capabilities such as graphical decision trees, easy-to-manage decision matrices and graphical decision flow. They also lack effective testing capabilities such as validation, testing and “what-if” simulation testing. This situation causes slow time-to-market with strategy changes, resulting in lost opportunity, inefficiencies, high costs, and inaccurate decisions.

Our decision turnaround time takes too long due to high levels of manual review and non-automated decisioning. We need to increase booking rates and reduce costs with faster, real- time decisions.

SECTION II – PRIORITIZE

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 11

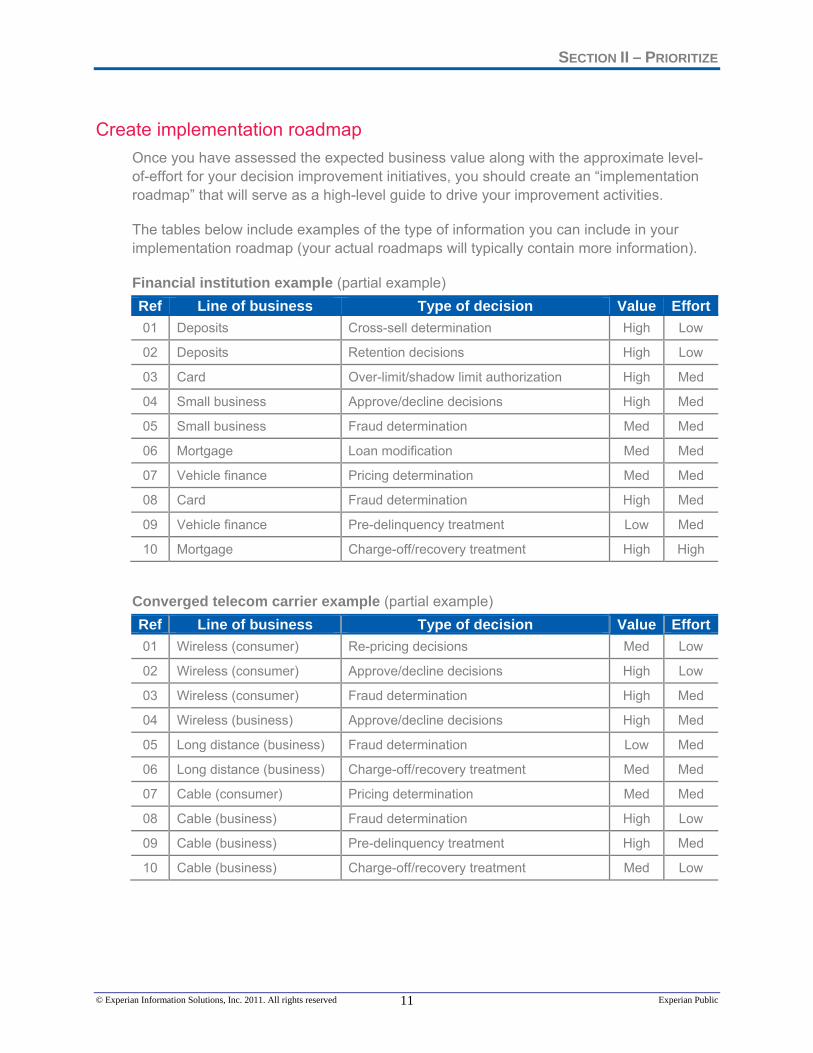

Create implementation roadmap Once you have assessed the expected business value along with the approximate level-of-effort for your decision improvement initiatives, you should create an “implementation roadmap” that will serve as a high-level guide to drive your improvement activities.

The tables below include examples of the type of information you can include in your implementation roadmap (your actual roadmaps will typically contain more information).

Financial institution example (partial example) Ref Line of business Type of decision Value Effort01 Deposits Cross-sell determination High Low

02 Deposits Retention decisions High Low

03 Card Over-limit/shadow limit authorization High Med

04 Small business Approve/decline decisions High Med

05 Small business Fraud determination Med Med

06 Mortgage Loan modification Med Med

07 Vehicle finance Pricing determination Med Med

08 Card Fraud determination High Med

09 Vehicle finance Pre-delinquency treatment Low Med

10 Mortgage Charge-off/recovery treatment High High

Converged telecom carrier example (partial example) Ref Line of business Type of decision Value Effort01 Wireless (consumer) Re-pricing decisions Med Low

02 Wireless (consumer) Approve/decline decisions High Low

03 Wireless (consumer) Fraud determination High Med

04 Wireless (business) Approve/decline decisions High Med

05 Long distance (business) Fraud determination Low Med

06 Long distance (business) Charge-off/recovery treatment Med Med

07 Cable (consumer) Pricing determination Med Med

08 Cable (business) Fraud determination High Low

09 Cable (business) Pre-delinquency treatment High Med

10 Cable (business) Charge-off/recovery treatment Med Low

SECTION II – PRIORITIZE

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 12

After identifying the various decision improvement initiatives, you can use charts such as the ones below to plot the initiatives based on value and effort to implement.

Financial institution example

Converged telecom carrier example

Legend

Pote

ntia

l val

ue

Highvalue

Lowvalue

Low effort High effortImplementation effort

Wireless (business)Long distance (business)Cable (consumer)Cable (business)

05

Wireless (consumer)03

09

01

02

07

08

04

06

10

Legend

Pote

ntia

l val

ue

Highvalue

Lowvalue

Low effort High effortImplementation effort

10

MortgageVehicle financeCredit cardSmall business

07

DDA

03

05

0102 0804

06

09

SECTION III – IMPLEMENT

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 13

SECTION III – IMPLEMENT This section describes the components of an optimized decision-making system and provides a recommended approach to ensure success when implementing your improved decision-making capabilities.

Components of an optimized decision-making system The diagram below illustrates the components of an optimized decision-making system and how these decision-making capabilities typically interact with applications and processing systems within your current environment.

Once you determine the types of decisions that are of high priority for your organization, you need to determine where and how the decisions are made today. For example, “approve/decline” decisions are typically made within your account origination system, collection treatment decisions within your collections system, and cross-sell decisions within your call center or customer relationship management systems. You also need to determine whether you plan to make decisions at the individual “account” level or at a broader customer and relationship level.

As illustrated in the diagram above, an optimized decision-making capability is “called” by your existing systems to request and receive a decision on either a batch or real-time basis. An optimized decision-making capability can also “push” decisions (without being called) when certain trigger events occur. For example, if new delinquent trade lines

Optimized Decision-Making Capability

Retrievedata

Calculate model

score(s)

2 Execute optimizedalgorithms

Apply policyrules

Determinedecision

Calculateattributes

3 4 5 6 7

“Calling” systems(Examples include: prospect databases; loan origination systems; credit & collection systems; core

processing systems; CRM applications; call center applications; etc.)

Types of decisions(Examples include: cross-sell decisions; prospect determination; pre-approval; approve/decline;

fraud determination; pricing; initial credit line; collection treatment; etc.)

Receive decision request Return decision

Y o u r c u r r e n t e n v I r o n m e n t

1 8

SECTION III – IMPLEMENT

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 14

appear for a customer, the decision-making system can “push” a predelinquency treatment decision to your account management system.

The table below describes each of the components that make up a typical decision making system. Once in production, these decision-making components are either installed on-site at your premises, or they are hosted by Experian and connected to your systems in a secure environment.

Decisioning component Description

1. Receive decision request

The first step in the optimized decision-making process is to receive a decision request from the calling system. The request can be either on a batch or real-time basis. For example, on a weekly “batch” basis, you may want the decision-making system to identify the ideal cross-sell products and treatments for all existing customers and prospects for your prospect database and CRM systems. On a monthly “batch” basis, you may want to determine which accounts should be offered changes to their pricing plans, loan terms or credit lines.

Alternatively, on a “real-time” basis, you may need your decision-making system to instantly approve or decline an applicant for a new product or service, or instantly prescreen the applicant for an additional product or service. These types of decisions are returned immediately to the calling system.

Finally, there are some decisions that are “pushed” when certain events occur. These events are typically referred to as “triggers,” and they fall in to the following categories: prospecting, risk, retention, cross-sell and collection triggers. Experian can monitor the credit activity of your customers and prospects and proactively push a decision when pre-defined trigger events occur.

2. Retrieve data

Once the decision request has been received, the first step is to retrieve all necessary data from the credit bureaus (as well as other internal and external data sources). Depending on the type of decision requested, this data is captured either on a real-time basis for a single decision at a time, or on a periodic basis for batch decisions.

The Experian product that supports this process is called Attribute ToolboxTM. (Additional descriptions of products and services referenced in this guide can be found in the Appendix).

SECTION III – IMPLEMENT

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 15

Decisioning component Description

3. Calculate attributes

As the raw data is received from the credit bureaus and other sources, the next step is to convert this raw data into “information” by calculating predictive variables or “attributes.” Examples of attributes include “number of times past due last 30 days,” “average utilization last 6 months” and “% utilization.”

Experian’s Attribute Toolbox™ product is used to create and calculate your attributes. In addition, Experian’s Premier AttributesSM offers more than 800 predefined attributes that have been leveled across all three bureaus. Industry-specific attributes are available for bankcard, auto, mortgage, installment, telecom and student lending.

4. Calculate model scores

The attributes are used as inputs to your predictive models, which convert these attributes into a predictive score. You use different predictive models based on the type of decision. For example, “application credit risk scores” are used to support approve/decline decisions, and a “recovery score” is used to support a collection-treatment decision.

Predictive models can be implemented in Experian’s Strategy ManagementSM product. In an operational scenario, Strategy Management accepts the attributes and other data, executes the model and generates the score. Custom-built models can be used as well as predeveloped models such as Experian’s Vantage Score®, BustOut ScoreSM, Recovery ScoreSM, Never PaySM, and many others.

5. Execute optimized algorithms

Once all the data has been collected, attributes calculated and scores generated, it’s time to make a decision based on all of this information. There are two types of decisions; judgmental decisions and empirically-derived optimized decisions.

Judgmental decisions are based on your expertise and your domain knowledge. For example, a judgmental risk-based pricing decision might be “If the applicant is full-time employed and has a credit score above 650, offer $10,000 at 7.8%.” This judgmental decision is based on your knowledge and experience.

An empirically-derived optimized process arrives at the same type of decision, but rather than being judgmentally determined, it’s based on an empirical analysis of historical information. Therefore, in the case of risk-based pricing, rather than determining the risk-based price yourself, you give the optimization software your constraints, and the optimization software determines the appropriate risk-based price for every potential scenario. For example, you might give the system the

SECTION III – IMPLEMENT

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 16

Decisioning component Description

5. Execute optimized algorithms (continued)

following constraints: “What should my risk-based pricing be if I want to increase interest income by 10%, reduce losses by 5% and keep approval rates constant at 55%?” Optimization software determines the appropriate risk-based pricing using a constraint-based empirical analysis of historical data.

Experian offers a product called Marketswitch OptimizationSM which is used to develop empirically-derived optimized algorithms. Both types of decisions, judgmental and empirically derived, are encoded and executed within Strategy Management.

6. Apply policy rules During the operational process, all of your various policy rules, scores and decision algorithms that have been encoded in Strategy Management are applied on either a real-time or batch basis, depending on the type of decision requested.

7. Determine decision

Strategy Management utilizes a decision tree approach to determine the final decision. The response will vary based on the type of decision requested. For a cross-sell decision, the response will be the next best product to cross-sell; for a pre-screen decision, it would be whether or not to extend an offer; for a retention decision it might be which price plan to offer the customer.

8. Return decision

The final step is to return the decision to the calling system in an automated manner. As mentioned above, this can be either on a real-time instantaeous basis, or on a batch basis. Your existing processing and operational systems are then used to take action accordingly based on the decision.

SECTION III – IMPLEMENT

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 17

Define your client-specific requirements Now that we’ve examined the various components of an optimized decision-making capability, the next step is to define your client-specific requirements. No two companies will need exactly the same thing, so it’s important to examine your environment closely – and your high-priority needs and initiatives – and then define and document exactly what you need in an improved decision-making system.

The table below includes a representative example of the types of requirements related to an improved decision-making capability. Again, these are just examples that you can use as a guide as you create your own client-specific requirements.

As you identify your requirements, you should also assign a priority level to each requirement since it’s common to implement solutions in a phased and incremental manner. Therefore, it’s important to understand those requirements that must be met in phase 1, versus other requirements that can perhaps be deferred to a later phase.

Ref High level business requirements

HLR_01

The system shall support decision types including, but not limited to: - Cross-sell determination - Prospect determination - Prescreen decision - Offer/treatment determination - Fraud determination - Approve/decline decision - Initial credit line/limit/usage amount - Initial pricing determination - Risk-based pricing - NSF pay/no-pay decision - Over-limit /shadow limit authorization - Credit line/limit/usage/management - Retention decisions - Loan/payment modification - Repricing determination - Predelinquency treatment - Early/late-stage delinquency treatment - Collections agency placement - Collection/recovery treatment

HLR_02 The system shall enable the client to directly and measurably achieve its business expectations to increase revenue, to reduce operational costs, to improve recoveries, and to minimize losses to bad debt and fraud.

HLR_03 The system shall produce at least a 5-to-1 “benefit-to-cost” ratio. (For example, if the system costs $100,000 per year, it should generate at least $500,000 in annual benefits.)

SECTION III – IMPLEMENT

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 18

Ref High level business requirements

HLR_04

The system shall support lines of business including, but not limited to: - Commercial lines, loans and leases - Credit card/debit card - Debit card (prepaid/reloadable) - Deposit /DDA - Home equity loans/lines of credit - Installment loans - Mortgage loans - Small-business lines, loans and leases - Vehicle finance loans and leases - Cable service - Utility service - Wireless service (consumer and small business) - Wireline service (consumer and small business)

HLR_05

The system shall be capable of receiving bureau triggers on a batch or real-time basis and shall be capable of incorporating the trigger information into decisioning criteria. The system shall accommodate the following types of triggers: - Prospect triggers - Risk triggers - Retention triggers - Cross-sell triggers - Collection triggers

HLR_06

The system shall include a business-user-friendly “configuration environment” to define and manage attributes, define credit policies, perform what-if simulation in a test environment, set Champion/Challenger strategies and generate standard performance reports.

HLR_07 The configuration environment shall support graphical business metaphors such as business object flows, decision trees and decision matrices.

HLR_08 The system shall support rapid deployment of predictive credit risk, bankruptcy, recovery and/or cross-sell models in a real-time or batch environment with little IT involvement and with minimal system integration requirements.

HLR_09 The system shall be available in either a hosted manner by Experian or shall be installable on an end-user basis at the client’s premises.

HLR_10 The system shall consolidate disparate systems for bureau access, scoring and decision-management in to a single centralized scoring and decisioning system environment.

HLR_11 As appropriate, the system shall support all of the client’s lines of business and all areas of the Customer Life Cycle with no limit to the number of “calling applications.”

HLR_12 The system shall support the re-scoring of previously scored applicants on a batch basis with new decision strategies and/or new models to analyze and compare the impact of the changes.

SECTION III – IMPLEMENT

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 19

Ref High level business requirements

HLR_13

The system shall provide the following reports and analyses to help drive improved performance: - Accept versus decline distribution - Actual versus expected characteristic distribution (custom scores only) - Bad versus good score distribution - CSR analysis (override, delinquency) - Deposit analysis - Manual review analysis - Performance by score range

Define recommended solution architecture Once your requirements are determined, the next step is to define the most appropriate solution architecture to meet your requirements and exceed your business expectations. Given that the requirements for each client are unique, the solution architecture will be unique as well and should be tailored specifically to your requirements.

As you define the solution architecture, a “requirements traceability matrix” should be used that describes how each requirement is met by the solution architecture. By using this process, you can ensure your requirements will be met, and, by meeting your requirements, you maximize your business success.

The following table can be used to help define an effective solution architecture. It includes a list of numerous Experian products and services along with the types of decisions each product or service supports. You will note that some products such as Strategy Management and Attribute Toolbox help support all types of decisions, while others like Recovery Score support specific types of decisions such as collection/recovery treatment. Appendix A provides further descriptions of each product and service to help provide additional guidance for appropriate use.

With so many potential solutions available to help you address your requirements, the process of identifying and implementing the best combinations of products and services can be daunting. Experian works closely with clients to help you define your requirements, and to select and implement those products and services that will deliver the maximum possible return on investment.

[Insert table below]

SECTION III – IMPLEMENT

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 20

Experian products and services that support specific types of decisionsType of decision

Ref. Product Name Cro

ss-s

ell d

eter

min

atio

n

Pro

spec

t det

erm

inat

ion

Pre

scre

en d

ecis

ion

Offe

r/tre

atm

ent d

eter

min

atio

n

Frau

d de

term

inat

ion

App

rove

/dec

line

deci

sion

Initi

al c

redi

t lin

e/us

age

amt

Initi

al p

ricin

g de

term

inat

ion

Ris

k-ba

sed

pric

ing

NS

F pa

y/no

-pay

dec

isio

n

Ove

r-lim

it/sh

adow

lim

it au

th

Cre

dit l

ine/

limit/

usag

e/m

gmt

Ret

entio

n de

cisi

ons

Loan

/pay

men

t mod

ifica

tion

Rep

ricin

g de

term

inat

ion

Pre

delin

quen

cy tr

eatm

ent

Ear

ly/la

te-s

tage

del

inq

treat

men

t

Col

lect

ions

age

ncy

plac

emen

t

Col

lect

ion/

reco

very

trea

tmen

t

Core Decisioning Software (supporting all types of decisions)01 Attribute Toolbox™ ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●02 Marketswitch OptimizationSM ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●03 Strategy ManagementSM ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●

Software Solutions04 BakerHill® Bank2Business® ● ● ● ● ● ● ● ● ● ● ●05 BakerHill® Bank2Consumer® ● ● ● ● ● ● ● ● ● ● ●06 BakerHill® Client Advisor® ● ● ● ● ● ● ● ● ●07 BakerHill® Portfolio Risk Advisor® ● ● ● ● ● ● ● ● ●08 BakerHill® Statement AnalyzerSM ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●09 Commercial Fraud InsightSM ●10 Credit Card Verification ●11 Instant Prescreen ● ● ● ● ● ●12 Knowledge IQSM ●13 Portfolio Management Package ● ● ● ●14 Precise IDSM for Account Opening ● ●15 Precise IDSM for Compliance ●16 Precise IDSM for ID Screening ●17 Probe SMSM ● ● ● ● ● ● ● ● ● ● ● ●18 Prospect NavigatorSM ● ● ● ●19 Tallyman™ ● ● ● ●20 Transact SMSM ● ● ● ● ● ●21 Universal ID ●

Analytics/Models22 Bankruptcy PLUSSM ● ● ● ● ● ● ● ● ● ● ●23 BustOut ScoreSM ● ● ● ● ● ● ●24 Custom Scoring Models ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●25 Custom Credit Acquisition Modeling ● ●26 Emerging Credit ScoreSM ● ● ● ● ● ● ●27 Vantage Score® ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●28 Fast StartSM ● ● ● ● ●29 Financial Personalities ● ● ● ●30 Fraud ShieldSM ● ●31 In the Market ModelsSM ● ● ● ●32 Intelliscore PlusSM ● ● ● ● ● ● ● ● ● ● ● ● ● ●33 Never PaySM ● ● ● ● ●34 Premier AttributesSM ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●35 PriorityScore for CollectionsSM ● ●36 Recovery ScoreSM ● ●37 Trend ViewSM ● ● ● ●

SECTION III – IMPLEMENT

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 21

Experian products and services that support specific types of decisionsType of decision

Ref. Product Name Cro

ss-s

ell d

eter

min

atio

n

Pro

spec

t det

erm

inat

ion

Pre

scre

en d

ecis

ion

Offe

r/tre

atm

ent d

eter

min

atio

n

Frau

d de

term

inat

ion

App

rove

/dec

line

deci

sion

Initi

al c

redi

t lin

e/us

age

amt

Initi

al p

ricin

g de

term

inat

ion

Ris

k-ba

sed

pric

ing

NS

F pa

y/no

-pay

dec

isio

n

Ove

r-lim

it/sh

adow

lim

it au

th

Cre

dit l

ine/

limit/

usag

e/m

gmt

Ret

entio

n de

cisi

ons

Loan

/pay

men

t mod

ifica

tion

Rep

ricin

g de

term

inat

ion

Pre

delin

quen

cy tr

eatm

ent

Ear

ly/la

te-s

tage

del

inq

treat

men

t

Col

lect

ions

age

ncy

plac

emen

t

Col

lect

ion/

reco

very

trea

tmen

t

Data/Trigger Solutions38 Auto Share of Garage ● ● ●39 AutoCheck® for Lenders ● ● ● ● ● ● ● ● ●40 AutoCount Market ReportSM ● ● ● ● ● ● ● ● ●41 Business Profile Report ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●42 Collection AdvantageSM ● ● ●43 Credit Profile ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●44 MetroNet® ● ● ●45 National Fraud DatabaseSM ● ●46 PINpoint ServicesSM ● ● ● ● ● ● ● ●47 Prescreen ●48 QAS® - Quick Address Software ● ●49 QuestSM ● ● ● ● ● ● ● ● ● ●50 Triggers (Prospect TriggersSM) ●51 Triggers (Cross-sell TriggersSM) ●52 Triggers (Risk TriggersSM) ● ● ● ● ● ● ●53 Triggers (Retention TriggersSM) ● ●54 Triggers (Collection TriggersSM) ● ● ●

Services/Reports55 Business Intelligence ● ● ● ● ● ● ● ● ● ● ●56 Business Review Service ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●57 Data IntelligenceSM ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●58 Market Intelligence Reports ● ● ● ● ● ● ● ● ● ● ●59 Model Validation ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●60 Performance InsightSM ● ● ●61 Risk-based Pricing ●62 Strategy Review Service ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●VantageScore® (ow ned by and licensed to Experian by VantageScore Solutons, LLC).VantageScore® is ow ned by VantageScore Solutions, LLC.

SECTION III – IMPLEMENT

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 22

Implement solution and measure results Once the expected business value has been determined, your requirements defined and the solution architecture created, the final step is to implement the solution(s) and begin measuring results.

Experian offers the following suggestions to consider as you implement your solution(s):

1) Ensure each improvement initiative is linked to company goals

Use the approaches outlined in this guide to ensure that your improvement initiatives — and related solutions — are directly linked to company goals. Be sure that you can tie a successful implementation to improved business performance.

2) Define key implementation milestones and owners Define the most important high-level key implementation milestones for the initiative, and assign an owner to each milestone. Define them in such a manner that achievement of each milestone represents meaningful progress on the project. The first milestone is typically “Project kickoff,” and the final milestone should be “Success criteria achieved.”

3) Develop (and manage to) a project plan Develop a project plan that includes all of the tactical activities (along with the associated owners and duration) needed to achieve each milestone. Manage to the project plan, and quickly escalate issues if they are encountered during the project.

4) Identify metrics that you will measure (and manage to) on a monthly basis As the project is implemented, identify the key metrics upon which you built the original business case, and measure them on a monthly basis (or other appropriate time frequency). For example, if you built the business case on increasing approval rates and booking rates, while decreasing 30-day delinquencies, then these metrics should be tracked on an ongoing basis.

5) Define success criteria

Define the criteria by which you would consider the project a “success,” and include this as part of your monthly measurement criteria. If your key metrics are approval rates, booking rates and 30-day delinquencies, then specifically define by what amount approval rates and booking rates would need to increase (and 30-day delinquencies to decrease) in order to consider the project a success.

6) Implement improved capabilities iteratively and incrementally

Implement your improvement initiatives in a phased manner such that you can realize at least some degree of measurable business benefit within a six-month time frame. You should leverage the benefits to ensure incremental business value with each subsequent phase.

CONCLUSION

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 23

CONCLUSION By leveraging the information contained in this guide, you will be able to realize substantial improvements in business performance. The guide outlines a process and approach for identifying decisioning-related improvement initiatives across all areas of your business and all areas of the Customer Life Cycle.

It includes a methodology you can use to prioritize the various improvement opportunities based on potential business value and implementation complexity. An example business case is included that quantifies the expected business benefits, assuming a typical implementation scenario. Example implementation roadmaps are provided that you can adapt to your own business environment.

The final section describes all of the components of a typical decision-making system and includes a recommended approach to help you define your client-specific requirements that you would need addressed to ensure maximum business success. Numerous Experian products and services are identified that you can consider as you develop your solution architecture. Finally, several recommendations are provided to help ensure a successful implementation.

We hope you find the information in this guide useful. Experian is eager to collaborate with you as you pursue business improvement opportunities, so please don’t hesitate to contact us at anytime at 1-888-414-1120 or visit us at www.experian.com.

APPENDIX A: PRODUCTS AND SERVICES GLOSSARY

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 24

APPENDIX A: PRODUCTS AND SERVICES GLOSSARY Core Decisioning Software

Product Description 01 Attribute ToolboxTM Attribute ToolboxTM is business-user software that enables data

access to the credit bureaus and other data sources, supports custom attribute creation, and provides attribute management capabilities.

02 Marketswitch OptimizationSM

Marketswitch OptimizationSM is software that uses mathematically-based algorithms to optimize the decisions made on a portfolio or any other general dataset. Marketswitch Optimization can be used to optimize numerous decision scenarios including: cross-sell optimization, initial credit line strategy optimization, product offer optimization, credit line strategy optimization, risk-based pricing optimization, retention optimization, collection-treatment optimization, prospect marketing optimization, and indirect auto lending price optimization, among others.

03 Strategy ManagementSM

Strategy ManagementSM is business rule, scoring and decision strategy software for configuring and executing credit risk-based strategies on a portfolio or customer base. The software includes a strategy design component that is used to create, build, change and deploy business rules and strategies from the desktop. The software also has an executable engine that is installed on the server to integrate with your internal systems such as CRM, application processing or collections systems.

Software Solutions

Product Description 04 Baker Hill®

Bank2Business® Bank2Business® is a browser-based solution that automates the small business and commercial loan origination process from application to booking. It supports multiple decision strategies including blended business and guarantor scores as well as credit policy based decision strategy.

05 Baker Hill® Bank2Consumer®

Bank2Consumer® is a browser-based solution that automates the consumer loan origination process. It supports pooled model scores as well as bureau scores.

06 Baker Hill® Client Advisor®

Client Advisor® is a browser-based solution designed to provide a complete view of client, prospect and centers-of-influence relationships across lines of business. It progresses leads generated from marketing campaigns through the relationship cycle from sales to credit to exception management and risk monitoring.

APPENDIX A: PRODUCTS AND SERVICES GLOSSARY

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 25

Product Description 07 Baker Hill®

Portfolio Risk Advisor®

Portfolio Risk Advisor® is a browser-based solution that continuously monitors internal and external origination, behavioral, scoring and performance data across the enterprise to deliver a point-in-time view of an entire portfolio. Individual accounts are flagged for review, renewal or watch and high-potential accounts can be pushed to sales as cross-sell opportunities.

08 Baker Hill® Statement AnalyzerSM

Statement Analyzer is a browser-based financial analysis solution used to spread and analyze business financial statements with global cash-flow calculations and reports as well as specialized spreading and analysis for commercial real estate loans.

09 Commercial Fraud InsightSM

Commercial FraudSM Insight is a fraud and authentication tool that analyzes information on a business and its business owner to verify accuracy and truthfulness of application data

10 Credit Card Verification

Credit Card Verification is an authentication tool that verifies that a credit card number belongs to a consumer's name and address. Credit Card Verification uses File OneSM to verify the consumer exists and the consumer belongs to the credit card.

11 Instant Prescreen Instant Prescreen is an online, real time prescreen program that allows you to automatically pre-approve your customer for credit products at the point-of-contact (POC).

12 Knowledge IQSM Experian’s Knowledge IQSM powered by Precise IDSM is a revolutionary risk-based tool for identity authentication and fraud prevention. Precise ID scoring models and Knowledge IQ interactive questions provide innovative and integrated authentication and fraud detection on a single platform.

13 Portfolio Management Package

Portfolio Management Package is a hosted strategy management solution for early- to late-stage collections. Portfolio Management Package enables clients to evaluate and manage collection priorities within their portfolios while reducing costs and improving customer service and profitability.

14 Precise IDSM for Account Opening

Precise IDSM authenticates a consumer’s information against Experian databases using client-specific analytics. Clients choose specific product features within the Precise ID suite and receive a single Precise ID response returned alone or as an integrated product within their existing product delivery channels. Precise ID also returns a fraud classification type that indicates the likely type of fraud. This feature is unique in the industry and can be used for referral and underwriting purposes.

Precise ID for Account Opening validates data provided against known sources to determine the identity of the consumer and is available only to users with “permissible purpose” for obtaining account information.

APPENDIX A: PRODUCTS AND SERVICES GLOSSARY

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 26

Product Description 15 Precise IDSM for

Compliance Precise ID for Compliance is for clients focused solely on basic compliance oriented consumer authentication capabilities, such as: name, address, phone number, Social Security number, date of birth, and driver’s license verification. Precise ID for Compliance offers basic identity verification, additional Fraud Shield indicators associated with a consumer' profile, and flexible decisioning to return one or more compliance oriented accept or refer decisions.

16 Precise IDSM for Identity Screening

Precise ID for Identity Screening offers a broader depth of non-credit data tools for ID screening and account opening. This product option validates data provided against known sources to determine the identity of the consumer. This option returns a non-FCRA identity risk score comprised of a verification score and a validation score.

17 Probe SMSM Probe SMSM is a customer strategy management system that allows an organization to mange the entire customer relationship with comprehensive data management, sophisticated segmentation, and predictive behavioral scoring to provide true insight into the behavior of customers across all of their accounts to drive customer value throughout the organization.

18 Prospect NavigatorSM

Prospect NavigatorSM is a hosted, semi-custom prospect database solution that provides accurate and current consumer data, integrated processes, and powerful tools for end-to-end campaign management from users’ desktops. Leveraging Experian’s relational database platform, financial institutions can increase return on investment and enjoy the benefits of the most robust and up-to-date prospect database solution without the large capital overlay and lengthy time-to-benefit associated with more traditional database solutions.

19 TallymanTM TallymanTM is a software product that manages and enhances collections operations, including resource management, improving bottom line results. It automates and streamlines the collections process enabling clients to maximize performance while minimizing overhead and outsourcing costs, as well as IT reliance.

20 Transact SMSM Transact SMSM is a complete end-to-end application processing system that receives, validates, manages and decisions the flow of data and applications. It automates application processing and customer acquisition lending decisions with a site license or Experian-hosted system that receives, validates, manages and decisions the flow of data and applications.

21 Universal ID Universal ID Check provides consumer authentication across 24 countries via a single solution. Universal ID appeals to global clients that reach out to customers across the covered countries and to local country clients operating within these countries where there is no electronic identity checking available.

APPENDIX A: PRODUCTS AND SERVICES GLOSSARY

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 27

Analytics/Models

Product Description

22 Bankruptcy PLUSSM Bankruptcy PLUSSM is a bankruptcy model that predicts the likelihood of a consumer filling for bankruptcy within 24 months.

23 BustOut ScoreSM BustOut ScoreSM helps decrease bust-out losses by predicting and detecting bust out one to three months in advance. Bust out occurs when a new customer receives credit in the form of credit cards, installment loans, etc. and maintains good history for a period of four to 12 months, then draws down on all available credit and disappears.

24 Custom Scoring Models

Custom-developed modeling solutions can be developed for all phases of the credit life cycle, including marketing analysis, customer acquisition, account management, collections/recovery and fraud. The following specific types of models can be developed: response models; applicant risk models; and behavioral scoring models.

25 Custom Credit Acquisition Modeling

Credit acquisition modeling is used when you are making a pre-approved offer of credit for automotive financing purposes. Both credit and demographic information is used in a predictive model in order to find the individuals and households most likely to purchase and finance a specific vehicle. Deliverables include executive summary reports and a scored list for prospecting purposes.

26 Emerging Credit ScoreSM

Experian’s Emerging Credit ScoreSM is a credit risk score that allows creditors and service providers to expand the creditworthy universe of applicants and prospects creating new revenue opportunities and increased lifetime value of their customers.

27 Vantage Score® Vantage Score® is a risk model built by all three credit reporting companies that predicts the likelihood of a consumer becoming 90 days delinquent or worse on any trade within 24 months.

28 Fast StartSM Experian's Fast StartSM is a suite of empirically derived scorecards that combine account credit bureau data with industry- and product-specific application data to deliver the most highly predictive generic scoring available. Industry-specific versions have been created for: auto finance, bankcard, credit union, direct installment and home equity.

APPENDIX A: PRODUCTS AND SERVICES GLOSSARY

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 28

Product Description

29 Financial PersonalitiesSM

Experian, in conjunction with First Manhattan Consulting Group, developed a new generation of category-specific campaign targeting and tailoring tools for financial services marketers who are seeking to improve the performance of their prescreen and account management programs. Financial PersonalitiesSM categories include credit, mortgage, home equity and personal lines and loans. They are based on the rational and emotional needs and attitudes that drive consumer behavior (e.g., branch choice, product selection, provider loyalty) and help segment along the lines of “self-directed diversifier” versus “conservative branch bankers” versus “demanding advice seekers,” etc.

30 Fraud ShieldSM Fraud ShieldSM uses the power of predictive indicators and scoring to provide specific high-risk characteristic descriptions. It utilizes predictive cross-checking within Experian's File One relational consumer credit database. The optional add-on Fraud Shield score integrates both fraud and credit variables into a single, easy-to-interpret value.

31 In the Market ModelsSM

In the Market ModelsSM identify consumers who are likely to open a specific account type in the next 30–120 days. The suite of In the Market Models predicts purchase behaviors for the following account types: auto, bankcard, home equity, mortgage, personal finance, retail and student loan.

32 Intelliscore PlusSM Intelliscore PlusSM is an all-industry commercial risk model that uses business information and consumer information on the owner/guarantor to predict business risk.

33 Never PaySM Model The Experian Never PaySM model produces the first commercially available score that is designed to predict those applicants who apply for credit, are subsequently booked, and never make a payment. The score is the culmination of 2.5 years of research and development within the fraud space.

34 Premier AttributesSM

Premier AttributesSM is the next generation of Experian’s core STAGG AttributesSM. Experian has dedicated nearly three years to redefining every attribute optimizing all available data elements to enhance lender decisioning power. The new set of attributes is a robust offering with more than 800 attributes providing data at a more granular level than ever before available. The new offering helps lenders compete and maintain profitability in the current economic environment.

35 PriorityScore for CollectionsSM

PriorityScore for CollectionsSM is comprised of a suite of specially blended, industry-specific scoring models. These models enable clients to segment and prioritize accounts based on cost, effort and impact by knowing expected payment amounts, and probability of payment, from consumers with the capacity to pay.

APPENDIX A: PRODUCTS AND SERVICES GLOSSARY

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 29

Product Description

36 Recovery ScoreSM Recovery ScoreSM is a behavioral model that predicts the likelihood a consumer will make a payment on a charged-off account. Score range is 400–800, where the higher the score, the more likely a client will be able to collect on a collection account.

37 Trend ViewSM Trend ViewSM is a powerful value-added tool that contains 24 months of balance history information at the trade line level. Trend View contains specific trade-type information (bankcard, retail, unsecured line of credit, second mortgage, and home equity line of credit) that is able to identify different types of consumer behavior by way of six proprietary algorithms: Rate Surfer, Revolver, Transactor, Consolidator, Seasonality, Non-Activator. These trade line patterns help you determine when to make the most appropriate and profitable offers based on the consumer’s past behavior.

Data/Trigger Solutions

Product Description

38 Auto Share of Garage

Auto Share of Garage provides a snapshot of current vehicle ownership by including what vehicles (up to 10) a household has in its garage. This data helps clients understand vehicle ownership characteristics of their customers or other consumers.

39 AutoCheck® for Lenders

AutoCheck® for Lenders includes vehicle history reports available online or that can be built directly into dealers’ and manufacturers' pre-owned vehicle sales and marketing processes. It offers comprehensive data on pre-owned vehicles.

40 AutoCount Market ReportSM

The AutoCount Market ReportSM provides timely, accurate DMV analysis to automotive lenders that allows them to understand new/used vehicle financing trends and market share by lender.

41 Business Profile Report

Comprehensive credit profile on a business that provides a current, objective picture of how a business handles its financial obligations, including detailed trade, public record, collection and background information critical in assessing a business's creditworthiness.

42 Collection AdvantageSM

Collection AdvantageSM delivers a streamlined solution that combines credit-based scoring, consumer contact data and advanced analytics in one quick, easy-to-use process.

43 Credit Profile The Experian Credit Profile report is a composite history of a consumer's credit and identification information from our File One database of more than 200 million credit-active consumers. It provides accurate, current and complete information to acquire new business, manage customers and maximize collections.

APPENDIX A: PRODUCTS AND SERVICES GLOSSARY

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 30

Product Description

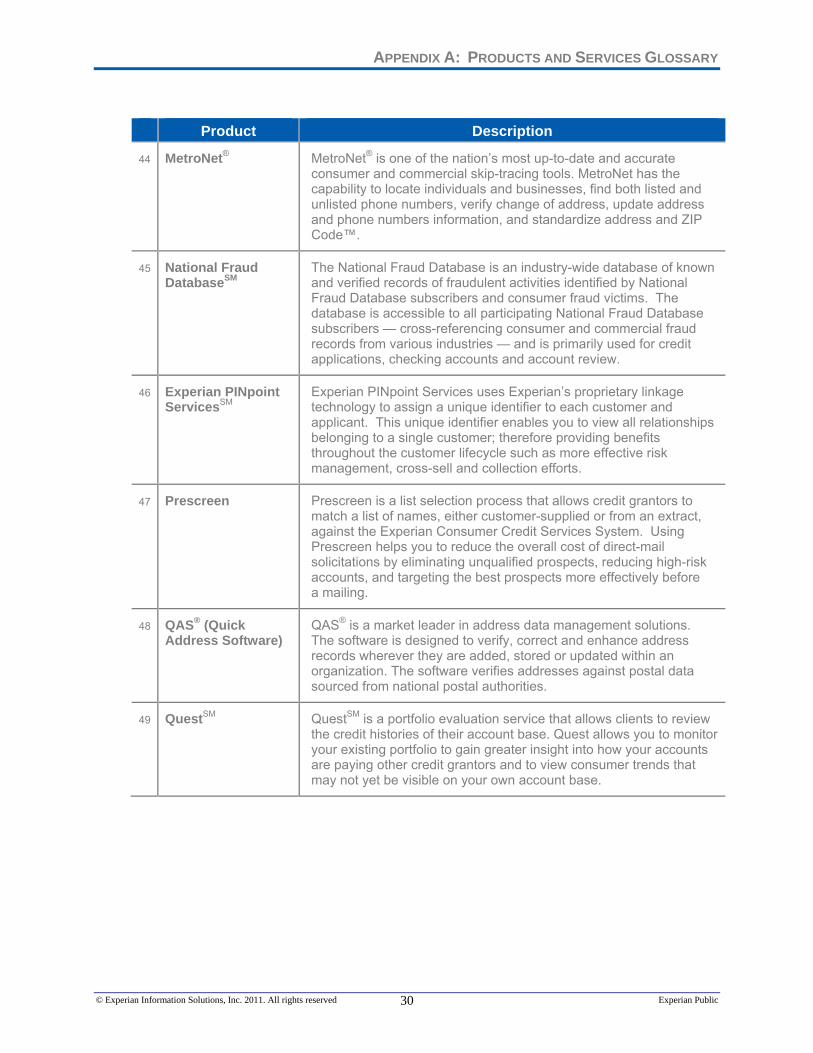

44 MetroNet® MetroNet® is one of the nation’s most up-to-date and accurate consumer and commercial skip-tracing tools. MetroNet has the capability to locate individuals and businesses, find both listed and unlisted phone numbers, verify change of address, update address and phone numbers information, and standardize address and ZIP Code™.

45 National Fraud DatabaseSM

The National Fraud Database is an industry-wide database of known and verified records of fraudulent activities identified by National Fraud Database subscribers and consumer fraud victims. The database is accessible to all participating National Fraud Database subscribers — cross-referencing consumer and commercial fraud records from various industries — and is primarily used for credit applications, checking accounts and account review.

46 Experian PINpoint ServicesSM

Experian PINpoint Services uses Experian’s proprietary linkage technology to assign a unique identifier to each customer and applicant. This unique identifier enables you to view all relationships belonging to a single customer; therefore providing benefits throughout the customer lifecycle such as more effective risk management, cross-sell and collection efforts.

47 Prescreen Prescreen is a list selection process that allows credit grantors to match a list of names, either customer-supplied or from an extract, against the Experian Consumer Credit Services System. Using Prescreen helps you to reduce the overall cost of direct-mail solicitations by eliminating unqualified prospects, reducing high-risk accounts, and targeting the best prospects more effectively before a mailing.

48 QAS® (Quick Address Software)

QAS® is a market leader in address data management solutions. The software is designed to verify, correct and enhance address records wherever they are added, stored or updated within an organization. The software verifies addresses against postal data sourced from national postal authorities.

49 QuestSM QuestSM is a portfolio evaluation service that allows clients to review the credit histories of their account base. Quest allows you to monitor your existing portfolio to gain greater insight into how your accounts are paying other credit grantors and to view consumer trends that may not yet be visible on your own account base.

APPENDIX A: PRODUCTS AND SERVICES GLOSSARY

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 31

Product Description

50 Triggers (Prospect TriggersSM)

Triggers are daily notices based on new inquiry, trade, and public record information to alert you of credit activity. Capturing this data within 24 hours allows you to respond to competitive threats, to capitalize on opportunities to extend additional credit or products to existing customers, and to protect against risk.

Prospect TriggersSM allow you to increase response and conversion rates by targeting in-the-market prospects. Experian can monitor a list of prospects that meet your prescreen criteria and alert you on a daily basis when consumers who meet your pre-approved credit criteria are seeking credit elsewhere.

51 Triggers (Cross-Sell TriggersSM)

Cross-Sell TriggersSM include daily monitoring of new credit inquiries and trades to expand existing customer relationships

52 Triggers (Risk TriggersSM)

Risk TriggersSM offer daily monitoring of new derogatory information to minimize risk.

53 Triggers (Retention TriggersSM)

Retention TriggersSM offer daily monitoring of new credit inquiries and trades to keep your valuable customers.

54 Triggers (Collection TriggersSM)

Collection TriggersSM is a robust, flexible account monitoring tool that quickly and effectively monitors accounts for key changes to credit profile or contact information on unpaid accounts. You choose the information you want Experian to track daily, and, when new information is found, you are immediately notified.

Services/Reports

Product Description

55 Business Intelligence

Business Intelligence is a comprehensive consultative offering that provides access to best practices, industry benchmarks and competitive market intelligence. Leveraging Experian’s rich data sources and analytical expertise, clients gain access to in-depth studies that provide insight for building strategies and solving specific business issues.

56 Business Review Service

Business Review Service includes an assessment of an organization’s current capabilities in key areas such as prospecting, acquisitions, customer management, fraud management and collections. It includes a comparison of the company to industry-standard benchmarks and best practices. It also includes the development of a strategic vision document that identifies tactical and strategic business improvement initiatives and includes a roadmap for successful implementation.

APPENDIX A: PRODUCTS AND SERVICES GLOSSARY

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 32

Product Description

57 Data IntelligenceSM Data Intelligence is a data-driven analytical approach that helps clients utilize data in a more efficient manner. Types of analyses include attribute leveling across multiple bureaus, creation/audit of custom attributes, scorecard audits and system migration.

58 Market Intelligence Reports

Market Intelligence Reports are a suite of industry-leading credit trending subscription services. The service includes data and report deliverables accompanied by editorial and expert commentary. The reports allows organizations to view economic trends, specific industry group and competitor performance.

59 Model Validation The model validation service quantifies performance of a client’s current model(s) and can be used to assess the performance lift of a new “challenger” model.

60 Performance InsightSM

Performance Insight is a consulting and monitoring service for new-applicant scorecards. It provides a thorough periodic checkup of your scorecards and your portfolio, looking at items such as population stability, decision management and scorecard performance.

61 Risk-based Pricing Risk-based Pricing is a consulting service that recommends risk-based acquisition strategies. The purpose of risk-based pricing is to allow financial institutions to price products in a way that accurately reflects the risk and costs associated with each individual applicant. Experian’s consultants work with clients to design strategies in which the interest rates charged to customers are dependent upon the credit risk they represent. We incorporate the client’s specific policies, procedures and lending strategies in order to gain maximum results.

62 Strategy Review Service

Strategy Review Service provides evaluations of current lending and decisioning policies to help drive improved customer decisions in any area of the Customer Life Cycle, including prospecting, customer acquisition, customer management, collections and recovery. The service may incorporate the use of many Experian products and services, such as Risk-based Pricing, Premier Attributes, Triggers and other Experian offerings to develop an effective client solution.

APPENDIX B: ABOUT EXPERIAN

© Experian Information Solutions, Inc. 2011. All rights reserved Experian Public 33

APPENDIX B: ABOUT EXPERIAN Experian® is a global leader in providing information, analytical and marketing services to organizations and consumers to help manage the risk and reward of commercial and financial decisions.

Combining its unique information tools and deep understanding of individuals, markets and economies, Experian partners with organizations around the world to establish and strengthen customer relationships and provide their businesses with competitive advantage.

For consumers, Experian delivers critical information that enables them to make financial and purchasing decisions with greater control and confidence. Clients include organizations from financial services, retail and catalog, telecommunications, utilities, media, insurance, automotive, leisure, e-commerce, manufacturing, property and government sectors.

Experian plc is listed on the London Stock Exchange (EXPN) and is a constituent of the FTSE 100 index. Experian has corporate headquarters in Dublin, Ireland, and operational headquarters in Costa Mesa, Calif., and Nottingham, UK. The Group employs approximately 15,000 people in 40 countries worldwide, supporting clients in more than 65 countries around the world.