a historical perspective o n the variaties of institutions

TRANSCRIPT

A Historical Perspective on the Variaties of institutions, Finance and Entrepreneurship

Selin Dilli and Gerarda Westerhuis

Document Identifier D2.2 The institutional evolution of finance in Europe and entrepreneurship Version 1.0

Date Due M36

Submission date 15/05/18

WorkPackage 2

Lead Beneficiary UU

1

ManuscriptSubmissionReport

SelinDilliandGerardaWesterhuis

DocumentIdentifier

Annex3toTheInstitutionalevolutionoffinanceinEuropeandentrepreneurship

Version

1.0

DateDue

24May2018

Submissiondate

18May2018

WorkPackage

2

LeadBeneficiary

UU

2

Journal,DateandTimeFinancialHistoryReview,26-04-2016,14.16

Title

A Historical Perspective on the Varieties of institutions, Finance andEntrepreneurship

Abstract

ArecentgrowingbodyofevidenceusingtheVarietiesofCapitalismapproachshows

thatinstitutionsarecomplementaryanddifferentinstitutionalconstellations

supportdifferentformsofentrepreneurialactivity.Thislineofresearchhighlights

thenecessityoftailoredreformstrategiestakingintoaccountthiscomplementarity.

Inthispaper,afteridentifyingthedifferenttypesofconstellationsinthefinancial

institutionsofEuropeandtheirchallengesforentrepreneurialactivity,wefocuson

thehistoricalevolutionofthebanksandfamilylendingastwoalternativefinancing

optionsthatcanhelptoovercomethelackoffinanceoptionsforentrepreneurs.We

arguethatpoliciestargetedatstimulatingfamilylendingcanbeausefulstrategy

particularlyintheMediterraneanandtheEasternEuropeancountriesgiventhat

familytiesarehistoricallystrongandformalfinancialinstitutionsremainlimitedto

stimulateentrepreneurialactivity.Werelyontheevidenceprovidedinthe

secondaryliteraturetosupportourarguments,ashistoricaldataonfinancing

optionsforentrepreneursremainlimitedtomakeacomparisonbetweendifferent

institutionalcontexts.Therefore,futureresearchshouldprioritizehistoricaldataon

financetoallowforamoresystematictestofthehistoricaloriginsofthedivergent

developmentpatternsoffinancialinstitutionstoday.

KeywordsandJEL-classificationKeywords:Entrepreneurship,bank,financialinstitutions,familyJelclassification:G21, D14, L26

CurrentStatusSubmitted.

From: STEFANO BATTILOSSI . [email protected]: Re: submission to the FHR New Scholar Fast-Track

Date: 26 Apr 2018 15:29To: Dilli, S.D. (Selin) [email protected]: [email protected], Westerhuis, G.K. (Gerarda) [email protected]

Dear Dr. Dilli,

many thanks for submitting your paper. We will let you know soon after the deadline for submissions.

Best wishes,

Stefano Battilossi (Carlos III Madrid)Rui Esteves (Oxford)EditorsFinancial History Review

2018-04-26 14:16 GMT+02:00 Dilli, S.D. (Selin) <[email protected]>:

Dear editors of the Financial History Review,I would like to submit my co-authored piece together with Gerarda Westerhuis, "A Historical Perspective on the Variaties of institutions,Finance and Entrepreneurship” to the New Scholars Fast-Track Workshop in Turin. As requested, I attach our manuscript as well asour complete CVs as I was not sure how short the CVs should be. I am happy to provide a briefer version of the CVs upon request.

Thank you in advance for your time and consideration and please do not hesitate to contact me for any further inquiries.

Kind Regards,Selin Dilli

Dear editors of the Financial History Review,I would like to submit my co-authored piece together with Gerarda Westerhuis, "A Historical Perspective on the Variaties of institutions,Finance and Entrepreneurship” to the New Scholars Fast-Track Workshop in Turin. As requested, I attach our manuscript as well asour complete CVs as I was not sure how short the CVs should be. I am happy to provide a briefer version of the CVs upon request.

Thank you in advance for your time and consideration and please do not hesitate to contact me for any further inquiries.

Kind Regards,Selin Dilli

-- STEFANO BATTILOSSI .Universidad Carlos III de Madrid

See More

3

Manuscript

1.Introduction

The availability of financing options is crucial in all stages and types ofentrepreneurial activity: in seeinganopportunity to start a firm, growingbusinessand engagement in innovation (Dilli et al. 2018). While both policy makers andacademics identify the importance of increasing access to finance as a reformstrategy to stimulate entrepreneurial activity in Europe (Sanders et al. 2018), thequestion on how to achieve this goal still remains debated. One of the majorobstaclesinachievingthisgoalisthattheeffectivenessoffinancialintermediariesinthe allocationof resources to firms is limitedby the informational opacity of newfirms,which have uncertain returns and are costly tomonitor. Inmany Europeancountries large financial conglomerates have emerged that seem less suited tofinancing entrepreneurship. Bank credit and collective pension funds may beoptimum for financing fixed, physical capital thatmay serve as collateral fordebt,butmorefinanceintheformofequityorprivatewealthmaybeneededtoenableentrepreneurship(Sandersetal.2015).

Furthermore,the importanceandeaseofaccesstofinanceforentrepreneursbothvary substantially across the European countries (European Commission 2018).AccordingtoarecentreportbytheEuropeanCommission(2018),whichcomparesthe28EUcountries, limitedaccesstofinanceandthe lackoffinancial institutionalarrangements are obstacles particularly in many of the Mediterranean countries(e.g., Italy, Greece, Cyprus) and the Eastern European countries (e.g., Romania,Hungary). In this paper, our aim is to help in identifying strategies to stimulateentrepreneur’s access to finance by considering the complementarity betweenfinancial institutions. In particular, we will aim to answer to what extent twofinancial agencies, banks and family, can provide financial support forentrepreneurial activity in Europe given the diversity of institutional constellationand history of the region. To answer this question, we rely on the secondaryliteratureduetothelackoftheavailablehistoricaldataonfinancingentrepreneursthatiscomparableacrossthewiderangeofEuropeancountries.Before identifying the relevant financingoptions for entrepreneurs in Europe, it isimportanttoclarifywhatwemeanwithentrepreneurshipasthedefinitionsandtheformsofentrepreneurialactivitydifferwidelyintheliterature(Acsetal.2014;Dilli2016).Inabroadeconomicsense,entrepreneurshipmeansowningandmanagingabusiness, or otherwise working on one’s own account (Van Stel 2008). Here,entrepreneurshipisdefinedinthebroadeconomicsense,thusintermsofowninga

4

business.1

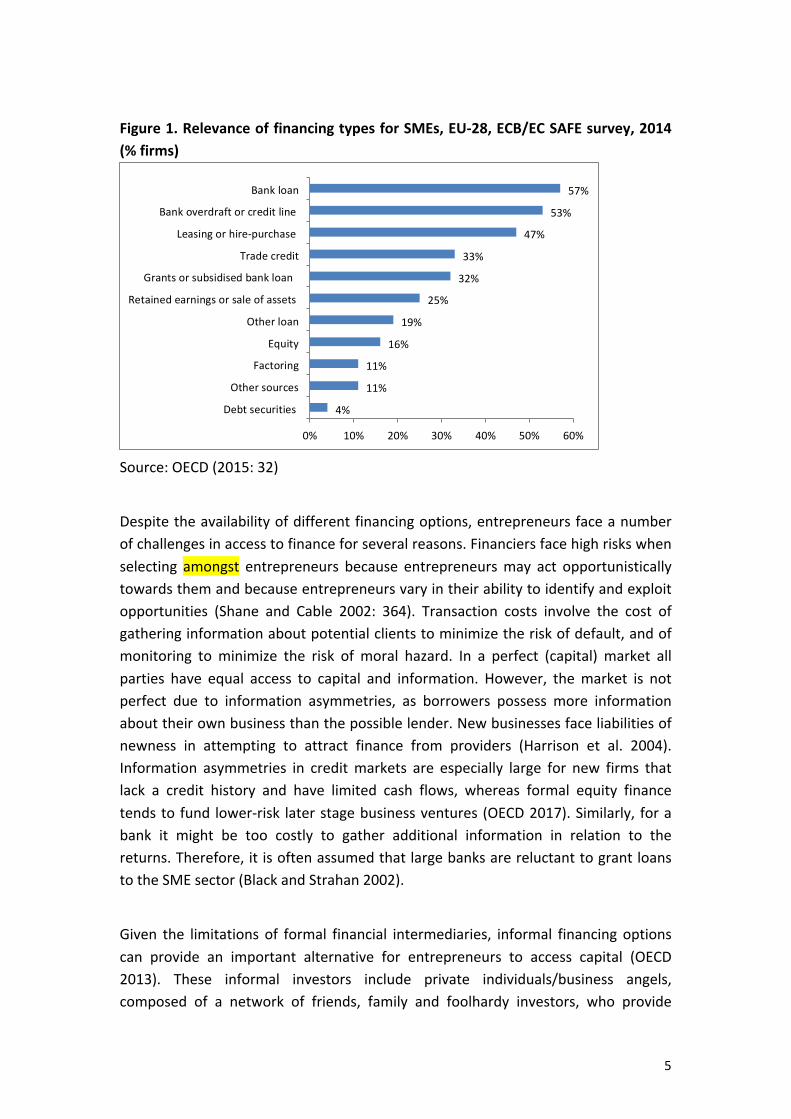

Accordingtoentrepreneurshipliterature,whilebanksarecrucialsourcesoffinance,alternativefinancialinstrumentssuchasventurecapital,businessangelinvestment,family,friendsandfoes(FFFs),asset-basedfinanceinstrumentssuchasleasingandfactoring,mezzanine finance, and crowd funding exist too (OECD 2015; EuropeanCommission 2018). Historicallymany alternatives to banks andmarkets have alsobeen available in the form of retained earnings, family capital, investment fromwealthy entrepreneurs, and short-term loans (Westerhuis 2016). Despite thedifferent alternatives, however, Figure 1 shows the importance of bank loans andoverdrafts for small andmedium enterprises (SMEs) in the European Union (EU).Despite the different alternatives, banks remain as the largest financialintermediaries in all EU countries, although their relative importance variessignificantlyfromonecountrytoanother.Figure1alsoshowsthattheshareofthenon-bankinstrumentsinfinancingentrepreneurialactivityremainsrelativelysmallinEurope,whichisvisiblewiththerelativelylowshareoffactoring,privateequityandother sources.Moreover,whilenotvisible fromFigure1,venturecapital,a crucialsourceoffinancingnewventuresintheUS(OECD2015:18),alsoremainsalimitedsource of funding in Europe. For instance, between 1995 and 2010, Europeanventurecapital investmenthasbeen,onaverage,approximatelyonlyone-thirdthesizeof investment in theUS (OECD2013)andoffered finance solutionsmostly forhigh-techfirmsandinlaterstagesofthebusinessventures.

1Moreover,it isimportanttoacknowledgethatthedifferencesbetweencountries’

performances in terms of entrepreneurial activity are generated by the type(replicative vs. high−impact) and motivation (necessity vs. opportunity) ofentrepreneurialactivity(Stenholmetal.2013).Firms,whichprovidethelargestpotential for new jobs, and enhance economic growth, are defined ashigh−impact firms (Acs 2008; Henrekson et al. 2010). Opportunity−basedentrepreneurshipreferstocasesinwhichpeoplemainlystartanewbusinesstoexploit a perceived business opportunity. In the case of necessity−basedentrepreneurship,individualsdecidetostartupabusinessoutofnecessitysuchas unemployment (Hechavarria and Reynolds 2009; Dilli 2016, p. 5). However,the historical evidence in the literature is too limited to provide a systematicstudyofthedifferentformsofentrepreneurialactivityhistorically.

5

Figure1.RelevanceoffinancingtypesforSMEs,EU-28,ECB/ECSAFEsurvey,2014(%firms)

Source:OECD(2015:32)

Despitetheavailabilityofdifferentfinancingoptions,entrepreneursfaceanumberofchallengesinaccesstofinanceforseveralreasons.Financiersfacehighriskswhenselecting amongst entrepreneurs because entrepreneursmay act opportunisticallytowardsthemandbecauseentrepreneursvaryintheirabilitytoidentifyandexploitopportunities (Shane and Cable 2002: 364). Transaction costs involve the cost ofgatheringinformationaboutpotentialclientstominimizetheriskofdefault,andofmonitoring to minimize the risk of moral hazard. In a perfect (capital) market allparties have equal access to capital and information. However, themarket is notperfect due to information asymmetries, as borrowers possess more informationabouttheirownbusinessthanthepossiblelender.Newbusinessesfaceliabilitiesofnewness in attempting to attract finance from providers (Harrison et al. 2004).Information asymmetries in creditmarkets are especially large for new firms thatlack a credit history and have limited cash flows, whereas formal equity financetendsto fund lower-risk laterstagebusinessventures (OECD2017).Similarly, forabank it might be too costly to gather additional information in relation to thereturns.Therefore,itisoftenassumedthatlargebanksarereluctanttograntloanstotheSMEsector(BlackandStrahan2002).

Given the limitations of formal financial intermediaries, informal financing optionscan provide an important alternative for entrepreneurs to access capital (OECD2013). These informal investors include private individuals/business angels,composed of a network of friends, family and foolhardy investors, who provide

4%

%11

11%

16%

19%

25%

%32

33%

%47

53%

57%

0% 10% %20 30% 40% 50% 60%

Debtsecurities

Othersources

Factoring

Equity

Otherloan

Retainedearningsorsaleofassets

Grantsorsubsidisedbankloan

Tradecredit

Leasingorhire-purchase

Bankoverdraftorcreditline

Bankloan

6

financingdirectly tounquotedcompanies inwhichtheyhavenofamilyconnection(Szerb et al. 2007). Economic explanations generally hold that allocation ofcontractual rights, the staging of capital, and risk shifting lead entrepreneurs todisclose information inways thatovercome this informationasymmetry (Gompersand Lerner 2000). Organization scholars, on the other hand, have proposed thatseed-stageinformalinvestorsrelyonsocialrelationshipstoselectwhichventurestofund and argued two different mechanisms—information transfer through socialtiesandsocialobligation-influenceinvestors’decisions(ShaneandCable2002:364).While information transfers throughsocial ties isacrucialdeterminantof informalinvestmentbynon-relatives,socialobligation isacrucialexplanationofwhyfamilymembers invest in new ventures. In this paper, we focus on the cross-nationalvariations in family ties to identify the context(s)where stimulating family lendingcanprovideanalternativestrategytobanklending.

This paper proceeds as follows: we first discuss the diversity in the financialinstitutions relevant for entrepreneurial activity today. In order to assess thefinancingoptionsofentrepreneurs,itiscrucialtoknowtheregulationswithregardsto finance as a whole since these institutional arrangements determine thewillingnessofthefinancerstoinvest inbusinesses.Second,wefocusonbanksandtheir historical evolution to evaluate the variation in the importance of banks infinancing entrepreneursover timeand across countries. Third,we focuson familylending as an alternative form of financing and then link it with the historicaldifferencesinfamilyorganization.Inthelastsection,wedraftourpolicyimplicationsbasedon thehistorical evolutionof these two financial intermediaries consideringthe complementarity of financial institutions and the diversity of the historicalpatternsintheinformalinstitutionsofEurope.

2.TheDiversityoftheFinancialInstitutionsinEurope

Inthissection,basedonthetypologyprovidedbyDillietal. (2018),weprovideanoverviewofthediversityoffinancialinstitutionsrelevantforentrepreneurialactivityin Europe for two main reasons. First, it provides a holistic perspective on thediversityofthefinancialinstitutionalstructureinEuropethatdistinguishesbetweencontexts where access to finance is a larger obstacle for entrepreneurship thanothers.Institutionalarrangementsarecrucialindeterminingtheleveloftransactioncosts and risks attached to information asymmetries. As a result, institutionsdetermine the availability of financial sources and the decision of formal andinformalfinancial intermediariesinlendingmoney(LaPortaetal.1997).Second,ithelps in distinguishing between contexts where financial institutions reducetransaction costs and risks attached with information asymmetries and thus

7

stimulate formal financing lending such as through banks versus where informalfinancingoptions through familycanbeaviable strategy to limited formal lendingoptions.UsingtheVarietiesofCapitalism(VoC)frameworkandentrepreneurship literature,Dilli et al. (2018: 4-5) identify the ‘entrepreneurship relevant’ financial institutionsand their diversity in Europe by considering their complementarity. They identifyfour types of financial institutions to be particularly relevant for entrepreneurialactivity:thecorporategovernancesystemthatgrantsshareholderstherighttoelecttheirrepresentativesontoasupervisoryboard,theprotectionofshareholderrightsin case of venture failure, minimum capital requirements that founders need toplaceintotheirventureatitsinception,andtheavailabilityofventurecapital.First,shareholdersneedtobeassuredthattheirinvestmentisusedinthemostefficientwayby thecorporatemanagement. In coordinatedmarketeconomies (henceforthCMEs), for instance, shareholders have a say and insight into how their funds areusedandconsequently, theyoftenpreferprojects thatguarantee lower,butmorestable and predictable returns over a longer period of time. Second, in case offailure, shareholders’ possibilities to disinvest importantly dependon the rights ofcreditors to recover their investments that in turn, are determined by nationalinstitutions. The more easily creditors can recover the funds provided toentrepreneurial ventures, the more likely they would invest in entrepreneurialactivity.Third, the lower theamountof capital required, theeasier itwouldbe toopen a venture. Last, venture capital (VC) is one of the most crucial sources ofentrepreneurial activity especially in theUS, depicted as themost entrepreneurialsociety in the world (Dilli et al. 2018: 4-5). While venture capital is a source offinance rather than an institutional arrangement, this dimension is relevant toinclude,astothebestofourknowledge,thereisnodirectinstitutionalmeasureonthisformoffinancing.

8

Figure2.FinancialConstellationsinEuropeandtheUS

Source:Dillietal.(2018)Using these four aspects of financial institutions, Dilli et al. (2018) identify fourdistinct institutional constellations in Europe and the US, which also correspondswellwiththeVarietiesofCapitalismliterature(Figure2).Thefirstoneiscomposedof the liberal market economies (henceforth LME) (UK, Ireland, and the US),characterized by permissive finance-related institutions. In this constellation,corporategovernancerightsmakemanagersaccountabletoshareholders,therearelow minimum capital requirements, there is availability of venture capital, andinstitutions privilege shareholders in case of corporate failure. The secondinstitutional group consists of Nordic CMEs and Belgium, and offers somewhatpermissivefinance-relatedinstitutions.ThisgroupmainlydiffersfromLMEsintermsof a lower protection of minority investors and a higher minimum capitalrequirement,whereastheirfacilitationofventurecapitalandtherecoveryratearesimilar to LMEs. A third cluster includesmostlyMediterraneanmarket economies(henceforth MMEs) (Italy, France, Spain, Portugal) and some of the ‘traditional’Continental CMEs (Germany, the Netherlands, Austria, as well as Slovenia). Thisclusterperformsworseonall four finance-related institutions compared toNordicCMEsintheirextentofstimulatingentrepreneurialactivity,wherebythisdifferenceis least pronounced in terms of their minimum capital requirements. Finally, thefourthclusterincludesmostlyEasternmarketeconomies(henceforthEMEs)(Poland,

9

Czech Republic, Slovak Republic, and Hungary, as well as Switzerland) and ischaracterized by little protection of minority investors, high minimum capitalrequirements, little facilitation of venture capital, and a recovery rate favoringcreditorsovershareholders(Dillietal.2018:22).Dilli et al. (2018) conclude that the financial institutions are least favorable in theMMEs and EMEs for entrepreneurial activity. This implies that financialintermediarieswouldbelesslikelytolendmoneyintheMMEsandEMEsastherisksassociatedwith lendingmoneywouldbehigher in these contexts. Below,we firstlookatwhether thesedifferences in the institutional structureare reflected in thecross-national differences in bank lending and the extent to which these crossnationaldifferencesarehistoricallyrooted.Wethenarguefor family lendingasanalternativestrategytostimulateentrepreneurs’accesstofinanceintheMMEsandEMEs given their historical difference from theCMEs and LMEs in termsof familyorganization.3.Increasingdominanceoflargefinancialconglomerates:Banks

Inmany European countries large financial conglomerates have emerged that areperceived as less willing to finance entrepreneurship. Bank credit and collectivepensionfundshavebeenarguedtobelessfavorableforenablingentrepreneurshipdue to transactions costs and information asymmetries. After the recent financialcrisis, there isabroadconcernabout thecredit constraints for theSMEsector,asbankfinancingcontinuestobecrucialfortheSMEsector(OECD2015).Thisisnotarecentconcern.Forexample,aftertheoilcrisesinthe1970sandeconomicrecessionintheearly1980s,thereweresimilarworries.However,giventhatbankscontinuetobe thebiggest lenderofSMEs today (Figure1above),we first lookat thecrossnationaldifferencesinthebankingsectortounderstandwhetherthisplaysaroleinentrepreneurs’ access to finance and then study to what extent banks werehistorically important for entrepreneurial activity tounderstand the importanceofbanksforentrepreneurialactivityfromalongtermperspective.The size of the banks has been linked with the availability of bank credit forentrepreneurship. Small banks have traditionally been important lenders to smallfirmsbecausesmallfirmshavetheircomparativeadvantageinrelationshiplending.According to this view, small banks are better than large banks at relationshiplending that depends on "soft" information. Large banks, in contrast, specialize intransaction lending tomoremature firmswhere less discretion is involved. (BlackandStrahan2002:2808).ThevaryingimportanceandthesizeofthebankingsectoracrossEuropeancountriesaswellasovertime(asillustratedinFigures3and4)maybearelevantexplanationforthedifferencesintheimportanceofbanksinfunding

10

entrepreneurialactivity(OECD2015).Figure3.BankingassetstoGDP

Source:WorldBank(2013)thelargecross-nationalvariationinbanksandtheirincreasingimportanceovertimeisillustratedinFigure3.BankingassetstoGDPisameasureoftherelativeeconomicimportanceofcountries’bankingindustries.Abouthalf(seven)ofthecountriesforwhichthereisdatainbothtimeperiodsshowroughlythesameassets-to-GDPsizeinboth time periods, an indication that banking industry growthwas roughly in linewiththegrowthoftheeconomy.Sixcountries(Greece,Italy,Netherlands,Portugal,Spain andUK) showabout a doubling in the banking assets- to-GDP ratio in 2011compared to 1993. Two countries, Switzerland and Ireland, even show a ratio in2011multipletimesthatin1993.

0.050.0100.0150.0200.0250.0300.0

UnitedStates

Switzerlan

d

Japa

n

Cana

da

Austria

Belgium

Den

mark

Finlan

d

Fran

ce

German

y

Greece

Irelan

d

Italy

Luxembo

urg

Nethe

rlan

ds

Portugal

Spain

Swed

en

United

BANKINGASSETSTOGDP(%)

1993

2011

11

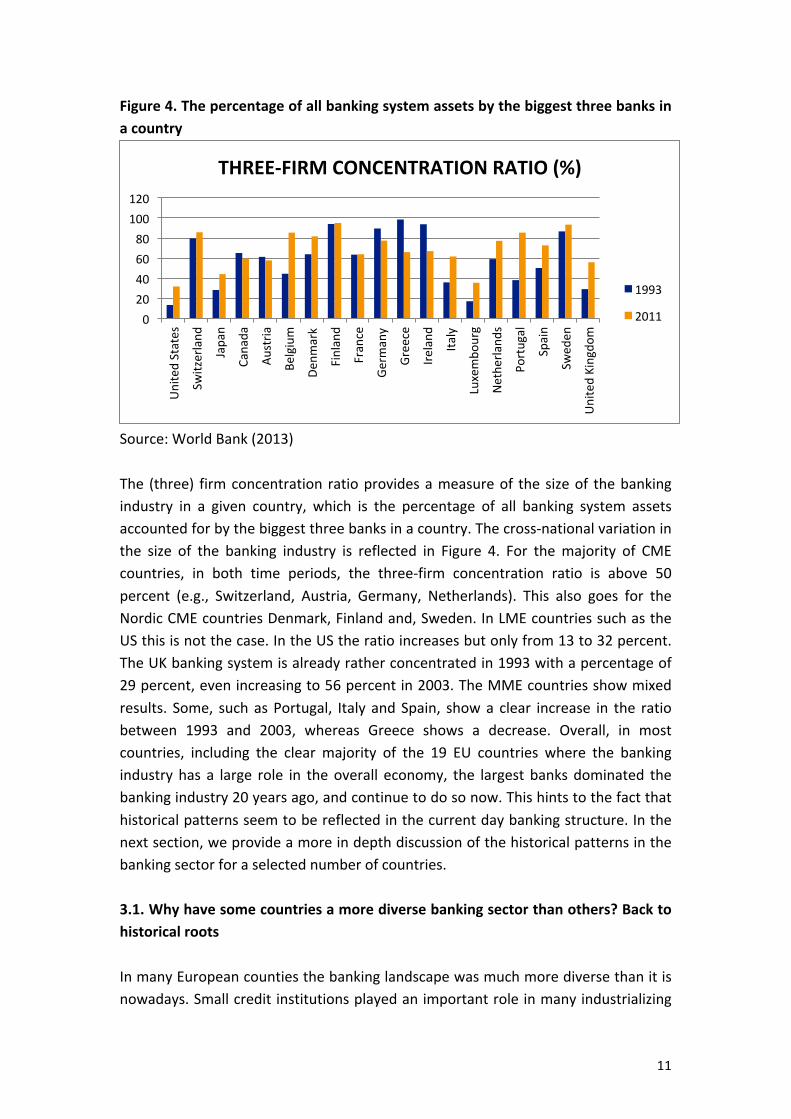

Figure4.Thepercentageofallbankingsystemassetsbythebiggestthreebanksinacountry

Source:WorldBank(2013)The (three) firmconcentration ratioprovidesameasureof thesizeof thebankingindustry in a given country, which is the percentage of all banking system assetsaccountedforbythebiggestthreebanksinacountry.Thecross-nationalvariationinthe size of the banking industry is reflected in Figure 4. For themajority of CMEcountries, in both time periods, the three-firm concentration ratio is above 50percent (e.g., Switzerland, Austria, Germany, Netherlands). This also goes for theNordicCMEcountriesDenmark,Finlandand,Sweden.InLMEcountriessuchastheUSthisisnotthecase.IntheUStheratioincreasesbutonlyfrom13to32percent.TheUKbankingsystemisalreadyratherconcentratedin1993withapercentageof29percent,evenincreasingto56percentin2003.TheMMEcountriesshowmixedresults. Some, suchasPortugal, Italy andSpain, showa clear increase in the ratiobetween 1993 and 2003, whereas Greece shows a decrease. Overall, in mostcountries, including the clear majority of the 19 EU countries where the bankingindustry has a large role in theoverall economy, the largest banksdominated thebankingindustry20yearsago,andcontinuetodosonow.Thishintstothefactthathistoricalpatternsseemtobereflectedinthecurrentdaybankingstructure.Inthenextsection,weprovideamoreindepthdiscussionofthehistoricalpatternsinthebankingsectorforaselectednumberofcountries.3.1.Whyhavesomecountriesamorediversebankingsectorthanothers?Backtohistoricalroots

InmanyEuropeancountiesthebankinglandscapewasmuchmorediversethanitisnowadays.Smallcreditinstitutionsplayedanimportantroleinmanyindustrializing

0

20

40

60

80

100

120

UnitedStates

Switzerland

Japan

Canada

Austria

Belgium

Den

mark

Finland

France

Germany

Greece

Ireland

Italy

Luxembo

urg

Nethe

rland

s

Portugal

Spain

Swed

en

UnitedKingdo

m

THREE-FIRMCONCENTRATIONRATIO(%)

1993

2011

12

countries by extending financial services to the general public, introducinginnovationsandprovidingfinancingtofirmsandsectorsthatwereoverlookedbythelarger financial institutions (Wadhwani 2016: 192). In some countries (e.g.Netherlands, UK) they have almost vanished by now, whereas in others (e.g.Germany)theystillplayanimportantroleinthefinancialsystem.Attheendofthe19thcenturydifferencesbetweenbankingsystemsacrossEuropeancountriesstartedtoemerge.Inparticular,withtheSecondIndustrialRevolutionandthe emergence of large-scale firms the increased demand for capital led to thecreationoflargecommercialbanks(Westerhuis2016).Inmanycountries,bigbanksemergedreplacingrelationshipbankingwithimpersonaltransactionbanking.IntheUKmanylocalbanksdisappearedasaresult.DuringtheinterwarperiodUKbankingbecame more concentrated and less competitive. The emerged banking cartelbecame evenmore risk averse. Reasons for this process of concentration in 1919include the almost complete absence of opposition. The British central bank evenencouraged the concentration process, because it could exercise influence over asmaller number of larger banks. Stability of the banking sector occurred at theexpenseofthesmallfirms.ProvincialbanksweretakenoverbylargeLondonbasedbanks,whichpreferredhigher liquidity ratios.This reducedthesupplyof funds forthe industrial clients, in particular smaller provincial ones. There were no otherfinancial institutions to replace them. However, recent research has shown thatothersourcesofexternalfinancehavebeenimportant intheUKtoo.For instance,specialist markets and institutions such as stockbrokers, private investors, anddealers, were relatively well developed and historically have been an importantsourceoffinanceintheUK(seee.g.,Ross1996).Thispatterncorrespondswellwiththe LME’s institutional structure, which stimulatesmarket-oriented solutions (HallandSoskice2001).Incontrast,inGermany,ItalyandFrance,thebankingsystemremainedfragmentedand the state intervened by creating public and semipublic lending institutions.Thesepublic,semi-publicandregionalbanksspecializedinsegmentsofthemarket,reducing information asymmetries, because lending to the same type of clientlowered the risk assessment costs. It also led to the development of long-termrelationshipswiththeirclients,inparticularforbanksthatweredeeplyembeddedinlocal economies (Carnavali 2005). This type of banking structure thus loweredassessment andmonitoring costs due to long term relations between lenders andborrowers. The banking structure based on the long term relationship and thegovernmental interventionalsocorrespondswiththetypeof institutionalstructureof the CMEs identified in theVoC literature that stimulates coordination betweendifferentagentsoftheeconomy.Thedisadvantagewasthatthesebankswere less

13

capableinspreadingrisks.However,nexttobanks,therewerealternativefinancialintermediariespresent(Carnavali2005).Savings banks are an example of these alternative financial intermediaries thatemerged with the development of formal financial systems. The first ones wereestablished inGermany in the late18thcentury inorder toprovidepossibilities forworkingandpoorpeopletosaveforperiodsofneedduetoillness,unemploymentor retirement.Asimilar financial institutionwascreated in theUK in the1810s. Inthe mid-19th century savings banks had been established in many Europeancountries (Mura 1996). At the end of the 19th century divergence of the role andmodelofsavingbankscamein.Incountrieswithastrongstateandlargepublicdebt,the state became a competitor for these local saving banks by establishing postalsavings systems (e.g. UK, Italy, France, the Netherlands). They often crowded outsmaller institutions(Wadhwani2011). IncountriessuchasGermanywithaweakercentral state and a federalist political structure, the introduction of such postalsavings systems met with fierce resistance resulting in delay and provisionsconstraining the ability to competewith existing financial institutions. As a result,theroletheyplaynowadays isverydifferent fromcountrytocountry. InGermanyandItaly,savingsbanksstillplayasignificantroleasfinancial institutionsholdingalargeshareinthetotalassetsheldbyfinancialinstitutions.Inothercountries,suchastheUKandtheNetherlands,theirnumberhasdecreasedsignificantlybymergerand acquisitions and their activities are largely the same as those of the largecommercialbanks(Wadhwani2016).Cooperatives are another form of financial intermediaries that are owned andcontrolledbyitsmembersandgrantsloanstoitsmemberswhomightlackaccesstocreditatthelargefinancial institutions.Assuchcooperativeshaveinformationandmonitoring advantages. Informal cooperatives date back centuries, whereas theformal credit cooperatives emerged like savings banks as an integral part of theemergenceofmodern financial systems. InGermany,cooperativesemerged in the19th century in response to the failure of existing lenders to lend credit to smallretailersandruralpopulations(Wadhwani2016).AroundtheFirstWorldWarcreditcooperativestogetherwithcommercialbanksandsavingsbanksformedthecoreofthe German banking system (Deeg 1999). Like the savings banks the cooperativemodelhasspreadacrossEuropesince thesecondhalfof the19thcentury. In Italy,theybecameaveryimportantpartofthefinancialsystemaswell(Carnevali2005).Incontrast, intheUKandUS,typicalLMEeconomies,thecreditcooperativeswereestablishedrelativelylateandmetwithobstacles.Inthesecontexts,commercialandsaving banks were already providing financial services to the working and ruralpeople.

14

The reasonwhy these smaller credit institutions, such as savings banks and creditcooperatives, emerged is often explained by economic theories of asymmetricinformation. Smaller financial institutions might benefit from information andmonitoring advantages compared to large ones. For example they can useinformation due to social relationships. Apart from local embeddedness theorganizational formmightalsoplayarole.Forexamplesavingsbanks,often inthemutual and trustee form, did not have shareholders and managers were oftenprohibited from taking profits. However, it is not only the economic theories thatexplain the emergence of these smaller financial institutions. As said in somecountriesthebankinglandscaperemaineddiverse,whereasinothersthesesmallerfinancials disappeared in the 20th century. An important explanation for thisdivergence is the socio-political environment and importance of small firms(Carnevali2005).InFrance,ItalyandGermany,smallfirmshavebeenhistoricallyconsideredasbeingveryimportantfortheeconomyandculturalidentityofthesethreecountries.Asaresult,politicianscouldnotexcludethemfromtheirplanassmallfirmswereseenas“preserversofsocialstabilityandasavaluablepoolfvotes”.Ontheotherhand,intheUKthegovernmentstartedtodealwithSMEsonlysincethelate1970sanditdidso by removing or compensating for market imperfections in line with the freemarket regime. For example, minimizing taxation to provide for finance andinformation(Carnevali2005).InGermany, cooperativesandsavingsbankshistoricallydevelopedclose linkswithlocalSMEbusiness.Althoughintheextendedliteraturethefocusisoftenonthebigbanks from Berlin, we know that with the emergence of these banks, in theInterbellummany SMEs still dependedon local and regional banks. The SME, alsoknown as theMittelstand, consisted of among others artisans, shopkeepers, andsmall business owners. Moreover, they were considered a social class (Carnevali2005:46).Theymetwithfierceoppositionfromthecommercialbankanditwasthisconflict that “shaped the state’s response towards competition between differenttypes of banks, ensuring the permanence of segmentation” (Carnevali 2005: 196).Thus,inGermanythestateplayedanimportantroleinmediatingbetweendifferenttypesofbanks. ItwasanactivepoliticalchoicetoprotecttheSMEsandtheir localeconomies. In contrast, savings banks in theUK for examplewere not allowed tolend for commercial purposes as itwas forbiddenby law. In the 1950s and1960slongtermfinanceoftheMittelstandwasmadeavailableviasavingsandcooperativebanks, ensured by strong competition and state regulation. Regulation providedincentivesforthesavingandcooperativebankstograntSMEslong-termcredits.Thebanks operated in a limitedmarket and their success depended on the economicwelfare of the region. In their charters it was stated that pursuing profits was

15

importantbutonlyasameans toothergoals. Savingsbanksweremandatedwiththepromotionofthelocaleconomyandcooperativebankshadtoserveinterestsoftheirmembers(Carnevali2005).Thus, local financial institutionswereable tosupport thecompetitivenessofSMEsand the development of local industrial districts (see also Vitols 1995 and Deeg1999). Zeitlin (2007) for example stresses the importance of understanding localindustries and knowledge about regional economies, which the larger financialinstitutionsfailedtodo.Carnevali (2005)stressescomparativeadvantagesoftheseregionalbanksinItaly,FranceandGermanyaftertheSecondWorldWarcomparedtothemuchmoreconsolidatedbankingsystemintheUK.However,whilethebanksdiffered across these countries, the limited historical evidence shows that thenumberoffirmsthatcouldtakeadvantageofthebanks’combinationofinvestmentcommercialbankingservicesinGermanywasquitesmall(Culletal.2006).Italy,a typicalexampleofaMME in theVoC literature,hada fragmentedpoliticalstructure until the political unification in the mid-19th century. The country alsostartedrelativelylatewiththeindustrializationprocesscomparedtoitsneighboringcountries and there were large differences in terms of wealth, agriculturaldevelopment,andindustrialspecializationbetweenthevariousregionsofItaly.TheItalian case shows that banks were necessary for economic growth but it alsorequiredan“adequatesociopoliticalmatrixoflaw,regulation,andcustominwhichthey operated and appropriate government policies” (5leberger 2006: 151).Governmentseemstohavelackedtherighttoolstoseizeopportunities.Asaresult,“whenbankingandbusinessopportunitiespresentedthemselves,theywereseizedfor themostpartby foreigners”. (Kindleberger2005:146).Bythe interwarperiod,Italy hadmovedmore in the direction of industrialization by the development oflarge scale capital intensive firms. After the Second World War, the economicstructuredidnotchangemuch:itconsistedofSMEsgroupedinsegmentedindustrialsectorscombinedwithagroupofverylargefirmswitheconomicandpoliticalpowerovertheeconomy.Thisgroupof largefirmsexistedmainlyofstate-ownedfirmsinsteel, chemicals and energy. Like in Germany, small firms were seen as essentialpreservers of social stability both in the countryside and cities. Policies for smallfirms included exemptions from income tax, subsidized loans, and regionaldevelopmentpolicies.After the SecondWorldWar, the banking system was restructured by creating adecentralizedsystemtostrengthenlocalbanks.Governmentwantedtocreatelocalfinancialchannels(decentralizedcapitalism)toactasacounterbalancetothepowerof the large private business groups. While decentralization and a segmentedbankingsystemwereseenaselementsthatwouldincreasestability,aconcentrated

16

banking system was perceived as a factor that would hinder economic growth(Carnevali 2005: 177; see also Spadavecchia 2005). The role of the state thus hasbeen very important in the Italian case. Alsowhen the Bank Lawwas updated in1946, the central bank believed that growth could only be accomplished if firmscould access the creditmarket. The diverse financial landscape of the 1930swithvarioustypesandsizeoffinancialintermediarieshadtobedefendedasaguaranteeforthediffusionofcredit.Asaresult,regulationswerereshapedinordertorestrainbankingcompetitionandprotectthesmallandmediumsizedbanksfromthelargernational ones (Carnevali 2005: 178). Thus, the banking system after the SecondWorldWarwashighlyregulatedbasedontheBankingLawof1936.Theawarenessof policy makers that SMEs had disadvantages in access to market finance,contributed to the introduction of financial subsidies as part of national industrialpolicy(Spadavecchia2005).Fromthemid-1970showever,thedecentralizedbankingsystemwas increasinglybeingquestioned.As a result,many territorial restrictionswereabolishedaswellascontrolsoverinterestrates,evenleadingtothemergersofbanksinthe1990s.However,thebankingsystemof Italyhasbeencriticizedheavilybecauseithasnotdeveloped into an efficient banking system. Italy has not been able to reform thepublicadministration,whichhadledtocorruptionandrentseeking(Carnevali2005).Moreover, the historical divide between the North and the South of Italy still, inparticularwiththesloweconomicgrowthinthesouth,continuedtoremainanissue.Of the various countries discussed here, the Italian banking system has been themost regulatedandsubsidizedwith theaim topromote thedevelopmentof smallfirms.However,inItalywhiletheoverallnumberofbusinessownershipislargebothhistoricallyandtoday,alargemajorityiscomposedofnecessityentrepreneurs(vanStel2005).IncontrasttoGermany,industrializationinFranceoccurredinapoliticalcontextofaunified nation state, with strong central government. Although large French firmsestablished themselvesbetween1918-1930,SMEs remainedavery importantpartof theeconomy. Lescure (1999) shows that in the1920s, theSMEsectorplayedacentralroleintheprocessofeconomicgrowth.Healsomentionscreditavailabilityproblems inthisperiod,becausecommercialbanks limitedcredit tothissector.AsillustratedintheVoCliterature,andbeingaCME,France’sinstitutionalenvironmentwasverydifferent fromtheUK,because thestatehadamuchmoreactive role inFrance resulting in amore diverse banking sector. The state pursued policies thatwere aimed at avoiding overproduction. Small firms were seen as better for theeconomy than big ones. Due to agreements to fix prices and quotas there werehardlyincentivesforfirmstomergeintobiggerconglomerates(Carnevali2005).

17

During the Great Depression of the 1930s many local and regional banks had toclose, and after the SecondWorldWar a process of concentration dominated thebankingsectorinwhichtheregionalandlocalbanksmergedwiththenationalones.Four large deposit banks were nationalized after 1945; they had national branchnetworks.Twootherlargedepositbankswerenotnationalizedbutalsohadbranchnetworksacross thecountry. In1957,22 regionalbanksand158 localbankswereleft. The local banks had a strong hold over the local market. They had specialknowledgeofthelocalityandwerewillingtograntcreditstolocalbusiness.Forthisreason, one of the two non-nationalized banks, the CIC, worked closely togetherwiththesebanks insteadofacquiringthem.Thegreaterroleof thestateafter theSecondWorldWarwasalsoreflectedintheroleofpublicandsemi-publicbanksinstimulating investments. The popular banks became important in that sense andgrantedcredittothemiddleclassesandtoSMEs(Carnevali2005)A process of liberalization and increased supervision leading eventually to themonetary union in 1992 led to increased concentration, also in the continentalcountries. In the 1990s, theGermanbanks for example startedmerging, involvingprivate banks but also saving and cooperative banks. However, even today thenumberofsavingandcooperativebanksisstillrelativelyhighandstillembeddedinlocalmarkets(seeforthisconsolidationprocessalsoWesterhuis2016).Despitetheconsolidationprocess,thebankingsectorsinGermany,FranceandItalystillremaindiversereflectedintheirsize,geographicalspreadandspecialization.However,theextenttowhichthesedifferencesinthebankingstructurearerelevantforexplainingentrepreneurialactivityisnotclear.BothbasedonourcomparisonofthehistoricalcasesandaccordingtothestudyofCulletal.(2006),whohasstudiedthe resources available to SMEs during the 19th and early 20th centuries,we canconclude that historical differences in banking structure were present. However,thesedifferencesinbankswereofmarginalsignificancetoSMEsinthepast.InsteadSMEsmostly relied on local intermediaries, which ranged from notaries in FrancewhowerearrangingtheloanstothecooperativemovementinGermany.AccordingtoCulletal. (2006),SMEssolvedtheir financeproblemsthroughprivate initiativesandsettingup institutions,whichweredemanddriven.Culletal (2006:3028), forexample,showthatinnineteenthcenturyFrance,textilemanufacturersindifferentparts of the country raised funds in strikingly differentways. In Alsace and in theSeineRiverValleybetweenParisandRouen,theyraisedcapitalbysellingequity,andrelying on family and business connections to reduce the information problemsinvolved in securing outside infusions of funds. Around Lille, on the other hand,familyborrowingmadeupanimportantsourceoffinancing.Inthenextsection,weevaluatetheroleprivateinitiatives,inparticularfamilylending,canplayinprovidinganalternativeformoffinancingforentrepreneursintheinstitutionalcontextswhere

18

the transaction costs and risks associated with lending due to the informationproblemsremainhigh.

4.InformalFundersandFamilyasanAlternativeSourceofFinance

Sections2and3 illustrate that theavailabilityof formal financingoptions throughbanks and the financial institutions that support formal finance options remainslimitedespecially in theEasternand theMediterraneanMarketEconomies. In thissection,weevaluatewhetherinformalfundingoptionscanprovideanalternativetothechallengesrelatedtotheformalfinanceintermediariesandformalinstitutionsintheseeconomies.AccordingtoSteletal.(2011),acountry’slevelofentrepreneurialactivity increasedwith the supply of informal investors.Here,weput forward theidea that family lending can provide an alternative in the Eastern and theMediterraneanMarketEconomieswherefamilytieshavebeenhistoricallystrongerthanintheNorthWesternEurope.Thisisbecausefamilymembersmaybewillingtoinvest in thebusinessoutof ‘love’or socialobligationsevenwhen the risk ishighduetolackofsupportivefinancialinstitutions.Familyhasbeenhistoricallyacrucialsource of finance for businesses and remains important today (Cull et al. 2006).Moreover,studiesthat lookedattheroleof informal institutions inshapingformalinstitutions highlight that norms and values define what is preferable in socialrelations, and as a result, they decrease the costs for developing, justifying andsustainingtheformalinstitutionsunderpinningaregime(Lichtetal.2007;Nee2005;Dilli 2016). Moreover, institutional reforms can prove counterproductive if theydestroytheexistingbenefitsofsuchinformalinstitutions(Ebner2009).

Toevaluatethefeasibilityofthisidea,wefirstlookatboththesupplyanddemandside of family lending by discussing the current day cross-national differences inbusinessangels’choiceininvestingfamilymembers(supply)andindividual’schoiceof borrowing from family members (demand). We then evaluate whether thesecross-national patterns in family lending correspond with historically embeddednormsandvalueswithregardsto familyorganization.Weconcludethissectionbypresenting suggestions on in which contexts and how family lending inentrepreneurialactivitycanbestimulatedinEurope.

A recent growing body of evidence in economics and economic history literatureshowsthatthedifferencesininformalinstitutionsshapedbyhistoricalsettinghaveset inmotiondivergentevolutionarypaths, leading to the long termcross-countrydifferences in development outcomes today (Nunn 2009; Dilli 2017). Recently,historicallyrootedfamilytieshavebeenshowntomatterforeconomic,institutional,socialandpoliticaloutcomesof societies. For instance,Durantonetal. (2011) find

19

that regions with weak family ties perform better in terms of economic growth,adopt better to sectoral shift andhave a higher educational attainment. Similarly,Alesina et al. (2013), comparing the different migrant populations in the UnitedStates, showthat individualswho inherit stronger family tiesare lessmobile,havelower wages, are less often employed and support more stringent labor marketregulations.Whileevidenceintheliteraturehintstothefactthatregionswithweakfamily ties are performing better in economic outcomes, strong family ties canprovideadvantagesespeciallywhenitcomestoinformallending.Inentrepreneurshipliterature,familytieshavereceivedsomeattention(AldrichandCliff2003;seeArregleetal.2015forareview).Familymembersareoftenassumedtobeimportantprovidersoffinancialresources(socalled‘‘lovemoney’’)(Bygraveetal. 2003). This is because financial capital from family members has importantadvantagessuchas lowertransactioncosts(AuandKwan2009), favorable interestand payback requirements (Steier and Greenwood 2000), and availability whenothersourcesarenotavailable(Steier2003).Especiallywhenthefirmrequiresmoretime to provide returns, family may provide a better lending possibility to theentrepreneurthanformalfinancingoptions(Arregleetal.2015).Consequently,theliteraturetendstoassumeimplicitlythatthemoremoneythefamilyhasavailable,themorelikelytherearetobeentrepreneurialintentions(SiegerandMinola2017).Despite their advantages, however, findings in the literature show thatentrepreneursoftenprefer toaccessbusiness resources fromnon-familypartners,suchasventurecapitalistsorbusinessassociates (AuandKwan2009).Thesenon-familypartnerscanbringnotonlyfinancialresourcestonewventuresbutalsobroadexperience in new venture development (e.g., De Clercq and Sapienza, 2001). Inaddition, out of loyalty to the family and considering the high failure rate of newventures,manyentrepreneursmayprefertoavoidplacingfamilyassetsatriskinanewventurebecause if that ventureperformsbadly or fails, the familywill suffer(Arregleetal.2015:333).Moreover, the share of family financing in new business ventures differs widelyacrosscountries,regionsandovertime(Szerbetal.2007;BygraveandHunt2008;Chuaetal.2011).Studieswhichpaidattention to thecross-nationaldifferences ininformal venture capital show that individual explanations (e.g. know anentrepreneur,seegoodopportunities,haveentrepreneurialskills,fearoffailure)aregenerally farmore important determinants of informal investment than country’seconomic development, pro-enterprise government programmes, new businesscosts,orhighlevelsofentrepreneurshipeducation(Szerbetal.2007).However,lessattentionhasbeenpaidtotheroleofhistoricallyrootedinformalinstitutionsasanexplanatory factor. As mentioned earlier, organizational studies highlight the

20

importance of social relations in acquiring finance through informal channels.However, while the importance of social relationships in lending behavior ofbusiness angels is acknowledged, less attention has been paid to the historicaloriginsof thesecrossnationaldifferences in the strengthof the social relations.Abetterunderstandingofthesehistoricalconditionsiscrucialasinformalinstitutionschange very slowly over time and through their impact on shaping informal andformal institutions,historical family institutionsare likely to influence lender’s andborrower’schoicetoday.Previous studies have argued that the level of social obligations individuals feeltowardstheirfamilymembersshapethewillingnessoftheborrowertolendmoneytothefamilymember(supplyside)andthewillingnessofthelendertoborrowfroma familymember (demand side). For instance, Bygrave andReynolds (2005) arguethattheratioofaltruismtotheself-interestdecreasesastherelationshipbetweenaninvestorandanentrepreneurincreases.Thealtruisticwayofinvestmentismostcommonly seen in investment in family members. Therefore, in contexts wherefamily tiesarestronger,businessangelscanbemore likely to lendmoneyto theirfamilymembers out of social obligation/out of love. Therefore, we formulate thehypothesisthattheshareoffamilyfinancingisexpectedtobehigherinareaswheretraditionallythefamilyhaspriorityovertheindividual(strongfamilyties).AbulkofliteraturehasillustratedthatthereisalargevariationinEuropeintermsofthestrengthofthefamilyties.DemographersReher(1998)andTodd(1985),usingcensus data, have shown that strong family ties characterize the Mediterraneancountries whereas weak family ties (the individual have priority over family)characterizetheNorthWesternEuropeancountries(Reher1998;Todd1985).Morerecently, Alesina and Giuliano (2010), using the World Values Survey data,constructed a more direct measure of family ties based on three items, namelyindividual’sresponsibilitytowardstoparentsandchildren,respecttowardsparents,andimportanceofthefamily.TheyshowthatwhileonaveragetheMediterraneancountries have the strongest family ties, the Eastern European countries havemoderatelystrongfamilytiesandtheNorthWesternEuropeancountrieshaveweakfamilyties.Similarly,RijpmaandCarmichael(2013),usingethnographicdata,reachtosimilarconclusionsonthedifferencebetweentheNorthWesternEurope,EasternEuropeandtheMediterraneancountriesintermsoffamilystructure.Based on the Global Entrepreneurship Monitor (GEM) (2011) database, Figure 5illustrates the cross-national differences in terms of the investment of businessangelsinclosefamilyandrelativestoseewhetherbusinessangelsaremorelikelytoinvest in family members in regions with strong family ties. Figure 5 shows thatInvestmentofbusinessangels infamilymembers ishighparticularly intheEastern

21

Europeancountries,whichhasmoderatelystrongfamilytiesinAlesinaandGiuliano(2010)’s typology. While the share of the business angels who invest in familymembers is also relativelyhigh in theMediterranean countries, Portugal seems tohavea lowshareofbusinessangelswhosupportfamilymembers intheirbusinessventures.ThisiscontrarytoourexpectationgiventhatPortugalischaracterizedwithrelatively strong family ties. Moreover, contrary to our expectation, Sweden andBelgium, depicted as having weak family ties, are outperforming the rest of theEuropean countries in terms of their share of business angel investment in familybusinesses.Anexplanation for thesecontradictorycasescanbedue to theoverallsupply of business angels due to the favorable institutional context (Au and Ding2011). According to the GEM data (2011), while Belgium and Sweden have thehighestshareofbusinessangelsamongtheEuropeancountrieswithrespectively15%and8%oftherespondentsreportedbeingabusinessangel,inPortugalthissharewasonly2%.Anotherfactorcanbethelevelofentrepreneurialactivity,whichcaninfluence theavailabilityof financingoptions.Thus, thedirectionof causality is anissuehere,whichrequiresfurtherinvestigation;however,thisisbeyondthescopeofthecurrentstudy.Figure5.BusinessAngelsinvestmentinCloseFamilyMembersandRelatives.

Source:GlobalEntrepreneurshipMonitor(2011)Furthermore,familytiescanberelevantnotonlyforthesupplysidebutalsoforthedemandsideoffinancebyshapingentrepreneur’sdecisiontoborrowmoneyfroma

(.0253859,.0805621](.0209067,.0253859](0,.0209067][0,0]

Business Angel Investment in Relatives

22

familymember.Whilewelackdataonentrepreneur’slendingbehaviorfromfamilymembers,basedontheWorldBank(2011)FindexDatabase,Figure6illustratestheunweightedaverageofborrowingbehaviorofindividualsinthelast12monthsfrombanks or any other financial institution (Figure 6.1) and from family, relatives, orfriends (Figure 6.2). A divide between the Southern/Eastern and the continentalEuropean countries in terms of the individuals’ borrowing behavior is clear fromFigure 6. According to Figure 6.2, borrowing money from a family member is acommonlyusedsourceoffinance intheSouthernEuropeancountries, followedbytheEasternEuropeancountries,bothofwhicharecharacterizedwithstrongfamilyties.Ontheotherhand,theformalfinancialinstitutionsandparticularlybanksseemtobeacommonsourceoffinanceintheScandinavianandthecontinentalEuropeancountries(seeFigure6.1)bothofwhicharecharacterizedwithweakfamilyties.Figure6.BorrowedMoneyfromFinancialversusFamilyInstitutions

Source:WorldBankGlobalFindexDatabase(2014)

Overall, thepatternspresented inFigures5and6showthat family lendingoccursunder two conditions. First, in the Eastern European and the Mediterraneancountries, except Portugal, business angels seem to invest in the familymembersdespitetheunfavorablefinancialinstitutionalenvironmentidentifiedinsection2.IntheNorthernEuropeancountries,ontheotherhand,wheresuchasocialobligationis lowerdue toweak family ties, the investmentofbusinessangelsandborrowingbehaviorfromthefamilyremain limited.Giventhatthesetworegionshavestrongfamily ties and borrowing from family members is commonly done, creatingincentives forbusinessangels to invest in the familymembers in the twocontextscanbeastrategytostimulatefinancingoptionsforentrepreneurs.

23

Alternatively, thecasesofBelgiumandSwedenshowthatbusinessangelscanstillinvestintheirfamilymembersincontextswherefamilytiesarerelativelyweakbutthequalityof financial institutionsarehigh.Dillietal. (2018)showthattheNordicCMEs and Belgium have the second most favorable financial institutionalenvironment for entrepreneurial activity after the LMEs. This favorable formalinstitutionalenvironmentcanbeusefultounderstandwhyfamilyborrowingishighin the UK and Finland. Moreover, policies targeted at stimulating family lendingseem to be reflected in the investment of business angels to family members.Recently,Belgiumintroducedawin-win-scheme,wherebyanyonewholendsaloantoabusinessasafriend,family,oracquaintancereceivesataxreductioninreturn(OECD2015).WearguethatsimilarpoliciestoBelgiumshouldbeprioritizedintheEasternandtheMediterraneancountriestostimulatefamilylendingwhichalsohavethe supportive informal institutional structure. To explain further why this is thecase, in the next section, we discuss the persistence in family ties and divergentpatternsoffamilylendinginEuropefromahistoricalperspective.4.1.TheHistoricalRootsofFamilyTiesandFamilyLending

The previous section focused on the link between family ties as an informalinstitution and family funding. In this section, we discuss the historical familyorganizationasareasonbehindthecross-nationalvariationsinfamilytiestoarguewhy family funding can provide a feasible alternative to formal financing optionsparticularlyintheMediterraneanandtheEasternEuropeancountries.One of the core explanations as to why NorthWestern European countries havemuchweakerfamilytiescomparedtotheEasternandSouthernEuropeancountrieshasbeenattributedtothedifferencesinthelivingarrangementsoffamilymembers.Figure7belowshowsthattheshareofthepopulationresidingwithparentsuntilalaterage ismuchhigher intheMediterraneanandtheEasternEuropeancountriescomparedtotheNorthWesternEurope.Typicallyyoungpopulationscontinuetolivewiththeirparentsuntilfindingajobormarriageandinsomecasesaftermarriageinthe Mediterranean countries whereas in the North Western European countries,they would typically live until around the age of 20 (Reher 1998). Scholars havearguedthatthesedifferences in livingarrangementsresultedinvaryingpatterns insocial obligationswith regards to individual’s duties towards familymembers (seeAlesina and Giuliano 2010 for a review). The argument is that in societies whereindividuals continued living with their parents longer, they developed strongerfeelingofsocialobligationstowardsfamilymembers(strongfamilyties).Insocietieswhereindividualslefttheirparents’homeearlier,ontheotherhand,thisfeelingofsocialobligationislower(weakfamilyties).

24

Figure7.CoresidencePatternsin2013

Source:Eurostat(2013)EconomicanddemographichistoriansarguedthatthesecoresidencepatternshavebeenpresentinEuropeatleastsincethelateMiddleAgesandhardlychangedovertime. According to the historical demographers, the line (known as Hajnal's St.Petersburg-Triesteline),whichseparatesthecentralandnorthernEuropeterritories(Scandinavia, theUK, the LowCountries,much ofGermany andAustria) from theEasternandtheMediterraneanintermsofcoresidencepractices,hasbeenpresentforcenturies(Reher1998).ThestudyofReher(1998)showsthatfromat leastthelateMiddleAgesuntilthesecondhalfofthenineteenthcentury,itwascommoninrural England and in the Low Countries for young adults to leave their parentalhouseholdsatayoungagetoworkasagriculturalservantsinotherhouseholds.Ontheotherhand,intheSouthernEuropeansocietieseventhoughtherewereservantsinbothruralandurbansettings,itaffectedonlyasmallpartoftheyoungpopulationinruralareas(Table1).Recent empirical evidence also supports the view on the persistence of thecoresidence practices and norms and values regarding family life (Duranton et al.2009).Forinstance,onagloballevel,RijpmaandCarmichael(2013)showthatthereisastrongcorrelationbetweenfamilypracticesaroundthe1920s,therecentfamilynorms and values from theWorld Values Survey database (1985-2015) and SocialInstitutions related to Gender Equality (SIGI) (2009). This persistence has been

(58.62222,71.23333](44.59444,58.62222](36.44444,44.59444][18.68889,36.44444]

Coresidence in Europe, 2008-2015

25

attributed to the intergenerational transmission of these values from parents tochildren (Kok 2009; Alesina and Giuliano, 2010) and the formation of formalinstitutions, which in return perpetuate the dominant family traits over time(GalassoandProfeta2010).Table1.TheHistoricalCo-residencePatterns

NorthernandCentralEuropeancountries SouthernEuropeancountries

Country year %servant region/place Country year %servantregion/sample

Denmark

1787/1801 17.6

Threeperishes Italy 1610-1839 0.7-1.5

Kingdom ofNaples

Iceland 1729 17.1Threecounties

1654 4.0-6.0 Parma

Norway 1801 8.9 Threeareas

1656-1740 9.5 Pisa

Belgium 1814 14.2

NineFlemmishvillages 1853 5.0-7.0 Bologna

Austria17th-19thcen. 13 19listings Portugal 1740-1900 3.6 Minho

Holland 1622-1795 11.7Fourlocalities

1796 4.6

Tras-os-Montes

Germany 1795 10.7 Grossenmeer

1788,1789 6 Santarem

France 1778 12.6Longuennesse

1801 2.5 Colmbra

France 1644-97 6.4

Twosouthernvillages Spain 1753,1788 3.8 Valencia

1786 7.3 Navarre

1752 3.0-4.0 Santander

1752 2.6-3.5 Galicia

1766,1877 5.3

BasqueCountry

1750-1850 3.6-5.0 Cuenca

1719-1829 1.3

Murcia-Alicante

1787 2.4 Andalusia

26

Source:Reher(1998)The historical differences in the family structure have been shown to matter forsocieties’long-term(institutional)development.AccordingtoReher(1998:209),forinstance,traditionallyinMediterraneansocietiesmuchoftheaidgiventovulnerablemembers of the society came from the family, while in northern societies charitywas largely organized through the public (e.g., English Poor Laws) and privateinstitutions.HemakesasimilarargumenttoexplainwhypublicelderlycareisbetterdevelopedinNorthWesternEuropeasopposedtotheSouth.AccordingtoGreifandTabellini (2010), while the nuclear family type in Western Europe has led to theemergenceofinstitutionssuchasguildsanduniversitiesinlateMedievalEurope,theextended family structure of China, where children continue residing with theparents during their adulthood, resulted in the emergence of social institutionsbased on kinship relations (also in Greif 2006). More recently, Dilli (2016) showscountries characterized by a nuclear household structure in the past also tend tohavemoresustainableandhigherlevelsofdemocracyinthelongrun.

These historical family arrangements are possibly linked with the long-termdevelopment of financing options. The scarce historical evidence from the lateMiddleAgesandEarlyModernEuropeshowsthatinthisperiod,privatelendingwasalreadyformalizedintheLowCountries.VanZandenetal.(2012)demonstratethatinthefifteenthandsixteenthcenturies,propertieswereusedascollateralonalargescaleandthatinterestratesonbothsmallandlargeloanswererelativelylow(about6percent).Asaresult,manyhouseholdsownedfinancialassetsand/ordebts,andthedegreeoffinancialsophisticationwasrelativelyhigh.Similarly,GelderblomandJonker(2004)showthatdepositsandbondswerecommonamongbusinessmenandentrepreneurs to borrow from family members in the 16th century Netherlands.Thus, formal institutions stimulated lending both from family and non- familymembers in this period. On the other hand, while financial historians show thatItalian city-states were crucial financial centers in the fifteenth and sixteenthcenturies too, it was mainly concentrated in the hands of a small group ofmerchants. The presence ofweak family tiesmight have created the necessity toregulatethelendingbehaviormoreformallyintheNorth,whichresultedinaccesstocreditbyalargershareofthepopulationcomparedtotheSouth.However,thelackofhistoricaldatadoesnotallowustoprovideaformaltestofthishypothesis.

5.DiscussionandPolicyImplications

This paper provided an overview of the diversity in the financial institutionscharacterizingEuropetoidentifythecontextswhereaccesstofinanceremainsasachallengeforentrepreneurs.Inparticular,thefinancerelatedinstitutionalstructure

27

remainsleastfavorabletosupportentrepreneurialactivityintheMediterraneanandtheEasternEuropeaneconomiestoday.Wethenstudiedthehistoricalevolutionoftwofinancial intermediaries,banksandfamilyandthefinancial institutionsrelatedtothesetwointermediariestoidentifypossiblesolutions.AhistoricalperspectiveonthebankingstructureinEuropeshowsthatbanksweremorediversifiedinthepastthantodayandprovideddifferentpossibilities forentrepreneurs tohaveaccess tomoney.Moreover,ratherthanlargebanks,thechallengesinaccessingfinanceweresolvedinmanycasesthroughlocalandprivateinitiatives.Therefore, instead of focusing on solutions related to the formal financialinstitutions,weevaluatedwhether family lendingcanprovideanalternative intheMediterraneanandtheEasternEuropeaneconomies.Wearguedthatthewayfamilyhas been organized in the past forms further implications for the organization ofsocietytoday.Wearguedthatinsocietieswherethefamilyismorecentralthantheindividual (strong family ties), family would be an attractive financial source forbusinessventures.While strong family tieshavebeenargued toplaya role in thedevelopmentoflesseffectiveformalinstitutions(e.g.,Reher1999),theycanprovideanadvantageinlendingthroughfamily.Therefore,introductionofpolicytoolsthatwouldencouragefamily lendingcanprovideaviablesolutionforfinancingfornewventures in theMediterranean and the Eastern European countries. The Belgiumexample provides an example of how to achieve this. For instance, in Belgium,anyonewho grants a loan to an entrepreneur as a friend, acquaintance or familymember receives an annual tax discount of 2.5% of the value of the loan. If theenterpriseisunabletorepaytheloan,thelendergets30%oftheamountowedbackviaaone-offtaxcreditinthecontextofthe“winwin-lending”scheme(OECD2015).This change in the policy seems to have helpedwith increasing the availability offinancetoentrepreneursinBelgium.Our investigationalso showed that inanumberof countrieswhere family tiesareweak (Sweden and Belgium), the supply of business angels are high which isreflectedinthehighlevelsofinvestmentinthenewventuresincludingfamily.Thisislikelytobetheresultofformalfinancialinstitutionsthatstimulatetheoveralllevelof business angels and entrepreneurial activity. In the continental Europeancountries, where the formal financial institutions are less favorable to stimulateentrepreneurialactivityandarealsocharacterizedwithweakfamilyties,followingasimilar model to the Scandinavian countries and Belgium can help improve thefinancing options. Moreover, family lending can provide advantages over banklendingsuchas fewerrequirementssuchascollateral in lendingprocessandmoreflexiblearrangements inreturningthe loans.However,an important implicationofweak family systems in the continental European countries is that, policies shouldprioritize targeting improvement of the formal financial institutions rather than

28

family lending. This is because policymakers may need to deal with institutionalbarriers that are related to inherited family structures and cultures particularlyresistanttochange(Durantonetal.2009).However,oursuggestionsshouldbetakenwithcautionandfurtherinvestigationisrequired to reach for more conclusive evidence. The lack of long-term historicalfinancial data that is comparable across different institutional contexts of Europemeans that our analysis on the role of historical family structure for financialinstitutions remains descriptive and we cannot eliminate the role alternativeexplanationsthat influencefinancial institutionstoday.Moreover,reversecausalityisan issueasregionswhereentrepreneurialactivity ishigher, investorswouldalsobemorelikelytoinvestinbusinessesanddevelopformalinstitutionsmorefavorableforentrepreneurialactivity.Giventheslowchangingnatureofinstitutionsandtheirhistoricalorigins,thedirectionofcausalityislikelytorunfromfinancialinstitutionsto entrepreneurship.Moreover, the typeof entrepreneurial activity influences thedemand for different forms of financing options. To gain insight on these issues,future research should prioritize collection of systematic data on entrepreneur’saccess to finance brokendownby different forms of entrepreneurial activity bothacrosstimeandacrosscountriestoallowforamoreformaltestoftheseissues.Thisremainsasanambitionforfuturestudiestoinvestigate.

References:Arregle,Jean-Luc,BatBatjargal,MichaelA.Hitt,JustinW.Webb,ToyahMiller,andAnneS.

Tsui.(2015).“FamilyTiesinEntrepreneurs’SocialNetworksandNewVentureGrowth.”EntrepreneurshipTheoryandPractice39(2):313–44.

Alesina,Alberto,andPaolaGiuliano.(2010)“ThePoweroftheFamily.”JournalofEconomic

Growth15(2):93–125.Alesina,Alberto,PaolaGiuliano,andNathanNunn.(2013).“OntheOriginsofGenderRoles:

WomenandthePlough.”TheQuarterlyJournalofEconomics128(2):469-530.Au,K.,andDing,Z.J.(2011).“Institutionalinfluenceonlovemoney:InformalInvestmentto

family,friends,strangersacrosscountries.”FamilyBusinessAssociationAnnualConference,Perth.http://www.fambiz.org.au/wp-content/uploads/Institutional-Influence-on-Love-Money-Informal-Investment-to-Family-Friends-and-Strangers-across-Countries-Professor-Kevin-Au-and-Zhujun-Ding.pdf

Au,K.,andKwan,H.K.(2009).Start-upcapitalandChineseentrepreneurs:theroleoffamily.”EntrepreneurshipTheoryandPractice33:889–908.

Black,SandraE.,andPhilipE.Strahan.(2002)“EntrepreneurshipandBankCreditAvailability.”TheJournalofFinance57(6):2807–33.

Bygrave,William,andStephenHunt.(2008)“ForLoveorMoney?AStudyofFinancialReturnsonInformalInvestmentsinBusinessesOwnedbyRelatives,Friends,andStrangers.”SSRNScholarlyPaper.Rochester,NY:SocialScienceResearchNetwork.https://papers.ssrn.com/abstract=1269442.

Bygrave,W.D.,andReynolds,P.D.(2005).“Whofinancesstart-upsintheUSA?Acomprehensivestudyofinformalinvestors,1999-2003.”FrontiersofEntrepreneurshipResearch.

Bygrave,W.D.,Hay,M.,Ng,E.andReynolds,P.(2003).“Executiveforum:astudyofinformalinvestingin29nationscomposingtheGlobalEntrepreneurshipMonitor.”VentureCapital5(2):101-116.

Carnevali,Francesca.(2005).Europe’sAdvantage:BanksandSmallFirmsinBritain,France,

Germany,andItalysince1918.Oxford,NewYork:OxfordUniversityPress.Chua,JessH.,JamesJ.Chrisman,FranzKellermanns,andZhenyuWu.(2011).“Family

InvolvementandNewVentureDebtFinancing.”JournalofBusinessVenturing26(4):472–88.

Cull,Robert,LanceE.Davis,NaomiR.Lamoreaux,andJean-LaurentRosenthal.(2006).“HistoricalFinancingofSmall-andMedium-SizeEnterprises.”JournalofBanking&Finance30(11):3017–42.

DeClercq,D.andSapienza,H.J.(2001).“Thecreationofrelationalrentsinventurecapitalist-entrepreneurdyads.”VentureCapital3:107–127.

Deeg,Richard.(1999).FinanceCapitalismUnveiled:BanksandtheGermanPoliticalEconomy.UniversityofMichiganPress.

30/32

Dilli,Selin,NiklasElert,andAndreaM.Herrmann.(2018)“VarietiesofEntrepreneurship:ExploringtheInstitutionalFoundationsofDifferentEntrepreneurshipTypesthrough‘Varieties-of-Capitalism’Arguments.”SmallBusinessEconomics:1–28.

Dilli,Selin.(2016).“FamilySystemsandtheHistoricalRootsofGlobalGapsinDemocracy.”EconomicHistoryofDevelopingRegions31:82–135.

Duranton,G,Rodríguez-Pose,A,andSandall,R.(2009).“FamilyTypesandthePersistenceofRegionalDisparitiesinEurope.”EconomicGeography85(1):23–47.

EuropeanCommission(2018).“Smallandmediumsizedenterprisesaccesstofinance”.https://ec.europa.eu/info/sites/info/files/file_import/european-semester_thematic-factsheet_small-medium-enterprises-access-finance_en.pdf

Ebner,Alexander.(2009).“EntrepreneurialState:TheSchumpeterianTheoryofIndustrialPolicyandtheEastAsian‘Miracle’.”InUweCantner,Jean-LucGaffard,andLionelNesta(eds.),SchumpeterianPerspectivesonInnovation,Competition,andGrowth.Berlin:Springer.

Gelderblom,Oscar,andJoostJonker.(2004).“CompletingaFinancialRevolution:TheFinanceoftheDutchEastIndiaTradeandtheRiseoftheAmsterdamCapitalMarket,1595-1612.”TheJournalofEconomicHistory64(3):641–72.

Galasso,Vincenzo,andPaolaProfeta.(2010).“WhentheStateMirrorstheFamily:TheDesignofPensionSystems.”WorkingPaper.IGIER(InnocenzoGaspariniInstituteforEconomicResearch),BocconiUniversity.http://ideas.repec.org/p/igi/igierp/392.html.

Gompers,Paul,andJoshLerner.(2000).“MoneyChasingDeals?TheImpactofFundInflowsonPrivateEquityValuation.”JournalofFinancialEconomics55(2):281–325.

Hall,P.A.,andSoskice,D.W.(2001).“Anintroductiontovarietiesofcapitalism.”InP.A.Hall&D.W.Soskice(Eds.),Varietiesofcapitalism-theinstitutionalfoundationsofcomparativeadvantage(pp.1–68).Oxford:OxfordUniversityPress.

Harrison,R.T.,Mason,C.M.andGirling,P.(2004).“Financialbootstrappingandventuredevelopmentinthesoftwareindustry.”EntrepreneurshipandRegionalDevelopment16(4):307–346.

Greif,A,2006.“FamilyStructure,Institutions,andGrowth:TheOriginsandImplicationsofWesternCorporations.”AmericanEconomicReview96(2):308–312.

Greif,A,andTabellini,G,2010.“CulturalandInstitutionalBifurcation:ChinaandEuropeCompared.”AmericanEconomicReview:Papers&Proceedings100(2):1–10.

Kindleberger,CharlesP.(2005)AFinancialHistoryofWesternEurope.Taylor&Francis.Kok,Jan.(2009).“FamilySystemsasFrameworksforUnderstandingVariationinExtramarital

Births,Europe1900–2000”.RomanianJournalofPopulationStudies.Supplement2009:13–38.http://virtualknowledgestudio.nl/staff/jan–kok/familysystems–kok2009.pdf.

LaPorta,Rafael,FlorencioLopez-de-Silanes,AndreiShleifer,andRobertW.Vishny(1997).“LegalDeterminantsofExternalFinance.”JournalofFinance52(3):1131–50.

31/32

Lescure,M.(1999).Small-andmedium-sizeindustrialenterprisesinFrance,1900–1975.InK.Odaka,&M.Sawai(Eds.),Smallfirms,largeconcerns:Thedevelopmentofsmallbusinessincomparativeperspective(pp.140–167).Oxford:OxfordUniversityPress

Licht,AN,Goldschmidt,C,andSchwartz,SH.(2007).“CultureRules:TheFoundationsoftheRuleofLawandOtherNormsofGovernance.”JournalofComparativeEconomics35(4):659–688.

Nee,V.(2005).“TheNewInstitutionalisminEconomicsandSociology.”InTheHandbookofEconomicSociology,editedbySmelser,N,andSwedberg,R.Princeton:PrincetonUniversityPress.

Nunn,N.(2009).“TheImportanceofHistoryforEconomicDevelopment.”AnnualReviewofEconomics1(1):65–92.

OECD(2015).FinancingSMEsandEntrepreneurs2015AnOECDScoreboard:AnOECD

Scoreboard.OECDPublishing.OECD(2013).AlternativeFinancingInstrumentsforSMEsandentrepreneurs:Thecaseof

MezzanineFinance.OECDPublishing.Reher,DavidSven.(1998).“FamilyTiesinWesternEurope:PersistentContrasts.”Population

andDevelopmentReview24(2):203–34.Sanders,Marketal.(2018).“PolicyBriefontheFIRES-ReformStrategyforItaly.”

http://www.projectfires.eu/wp-content/uploads/2018/03/d5.12-policy-brief-italy-final.pdf

Sanders,Marketal.(2015).“FinancialandInstitutionalReformsforEntrepreneurialSociety”.http://www.projectfires.eu/work-packages/

Rijpma,A,andCarmichael,S.(2013).“TestingTodd:GlobalDataonFamilyCharacteristics.”AccessedMay30,2013.http://vkc.library.uu.nl/vkc/seh/Lists/Events/Attachments/33/carmichaelrijpma_testing.pdf.

Shane,Scott,andDanielCable.(2002).“NetworkTies,Reputation,andtheFinancingofNewVentures.”ManagementScience,Jg.48(3),S.364-381.

Sieger,Philipp,andTommasoMinola.(2017).“TheFamily’sFinancialSupportasa‘PoisonedGift’:AFamilyEmbeddednessPerspectiveonEntrepreneurialIntentions.”JournalofSmallBusinessManagement55:179–204.

Stel,Andrévan,AndrewBurke,ChantalHartog,andAbdelfatahIchou.(2011).“WhatDeterminestheVolumeofInformalVentureFinanceInvestmentandDoesItVarybyGender?”ScalesResearchReports.EIMBusinessandPolicyResearch.https://ideas.repec.org/p/eim/papers/h201021.html.

Steier,Lloyd.(2003)“VariantsofAgencyContractsinFamily-FinancedVenturesasaContinuumofFamilialAltruisticandMarketRationalities.”JournalofBusinessVenturing18(5):597–618.

Steier,Lloyd,andRoystonGreenwood.(2000).“EntrepreneurshipandtheEvolutionofAngelFinancialNetworks.”OrganizationStudies21(1):163–92.

32/32

Szerb,László,SiriTerjesen,andGáborRappai.(2007).“SeedingNewVentures–GreenThumbsandFertileFields:IndividualandEnvironmentalDriversofInformalInvestment.”VentureCapital9(4):257–84.

Todd,E,(1985).TheExplanationofIdeology:FamilyStructuresandSocialSystem.Oxford:BasilBlackwell.

VanZanden,JanLuiten,JacoZuijderduijn,andTineDeMoor.(2012).“SmallIsBeautiful:TheEfficiencyofCreditMarketsintheLateMedievalHolland.”EuropeanReviewofEconomicHistory16:3–22.

Vitols,Sigurt.“GermanBanksandtheModernizationoftheSmallFirmSector:Long-TermFinanceinComparativePerspective.”DiscussionPapers,ResearchUnit:EconomicChangeandEmployment.SocialScienceResearchCenterBerlin(WZB),1995.https://econpapers.repec.org/paper/zbwwzbece/fsi95309.htm.

Wadhwani,R.Daniel.(2016).“Small-ScaleCreditInstitutions.”InYoussefCassis,RichardS.Grossman&CatherineR.Schenk(Eds.),TheOxfordHandbookofBankingandFinancialHistory(191–216).OxfordUniversityPress.

WorldBank(2013).GlobalFinancialDevelopmentDatabase.Availableat:http://www.worldbank.org/en/publication/gfdr/data/global-financial-development-database.

Westerhuis,Gerarda(2016).“CommercialBanking:ChangingInteractionsBetweenBanks,Markets,IndustryandState.”InYoussefCassis,RichardS.Grossman&CatherineR.Schenk(Eds.),TheOxfordHandbookofBankingandFinancialHistory(pp.110-163).OxfordUniversityPress.