a low cost alternative - sig

TRANSCRIPT

DE

NV

ER FALL

SU MMIT

2014

Vietnam, the New Offshore

Location

A Low Cost Alternative:

Viet HoChief Procurement Officer

Russell Investments

www.sig.org/eval

DE

NV

ER FALL

SU MMIT

2014

Evaluation How-to:

Your feedback drives

SIG Event content

By signing and

submitting your

evaluation, you are

automatically entered

into a prize drawing

Why?

Option 1: App

1. Select Schedule2. Select Schedule by Day3. Select Day4. Select Session5. Scroll to Description 6. Click on the Evaluation link

Option 2: Browser

1. Go to www.sig.org/eval2. Select Session (#WS06)

How?

Viet Ho, Chief Procurement Officer

A low-cost alternative.

Vietnam - the new offshore location.

OCTOBER 2014

About Russell Investments*

p.4

What we’ve done

Who we are

Every step matters. Russell is a global asset manager that provides multi-asset

solutions, including strategic advice, implementation services, and global

performance benchmarks.

Outcomes that matter. As of June 30, 2014, Russell has approximately

$280 billion in assets under management and works with institutional clients,

independent distribution partners and individual investors globally. Assets

benchmarked to the Russell Index family surpass $5.2 trillion — more than all

other U.S. equity indexes combined.

What we do

Headquartered in Seattle, Russell has approximately 1800 associates in 21

offices around the world. Russell’s Global Sourcing & Procurement (“GSP”)

team is currently comprised of 30 FTEs responsible for approximately $1

billion in spend.

*Source: http://www.russell.com/us/about-russell/default.page

Today’s key objectives & takeaways

p.5

Part Two: Review

• Overview of the offshore market

and its challenges

• Offshore opportunities in Vietnam

• Case study by Russell

• Next steps to take

Part One: Discussion

Offshore Market and Its Challenges - Discussion

Offshore outsourcing – A brief history*

p.7

20

years

ago

Today

10

years

ago

15

years

ago

5

years

ago

The beginning of the

Offshore/Outsourcing

phenomenon

The improvement in

telecommunication and

the Y2K challenges

created opportunities to

shift technology work to

low-cost countries

India, with its large pool

of English speaking and

technically proficient

manpower, was at the

center of the offshore

story

Other outsourcing

countries such as China,

Philippines, Mexico,

Poland, Ireland, Costa

Rica, and Argentina came

into the mix

The ITO/BPO global outsourcing market is estimated at

$180B annually, with India capturing 50% of the market

* Source: Nasscom - Association for the Indian software industry

Emerging challenges in offshoring (focusing on ITO)

p.8

Profile* Volume Challenges

Large Offshorer > 1000 FTEs

• Supplier fragmentation with at least 4-5 suppliers

• Offshore rates are comparable across most suppliers

• Onshore/niche consulting spend is significant

• Business units have their preferred suppliers which

lead to a lack of competition

Medium Offshorer 300-1000 FTEs

• In addition to the above ...

• Cost pressure as contracts are renewed

• Service quality deteriorating (less focus from major

suppliers as they chase new business)

• High turnover and visa issues are cropping up and

are impacting operations

Small Offshorer < 300 FTEs

• In addition to the above ...

• Too small for major suppliers, end up with Tier 2 or 3

providers

* Russell segmentation - for discussion purposes only

Some key considerations* for potential and/or existing offshorers

Risk Management

• Security and data privacy

• Intellectual property

• Resource risk

Service Levels

• Knowledge transfer

• Quality control

• Account management

• Capability

Financial Considerations

• Total cost

• Inflation differential

• FOREX

Long-term viability

• Capacity

• Innovation

• Regulation

• Political stability

p.9

Outside of procurement process, four areas are worthy of additional review:

* Russell framework - for discussion purpose only

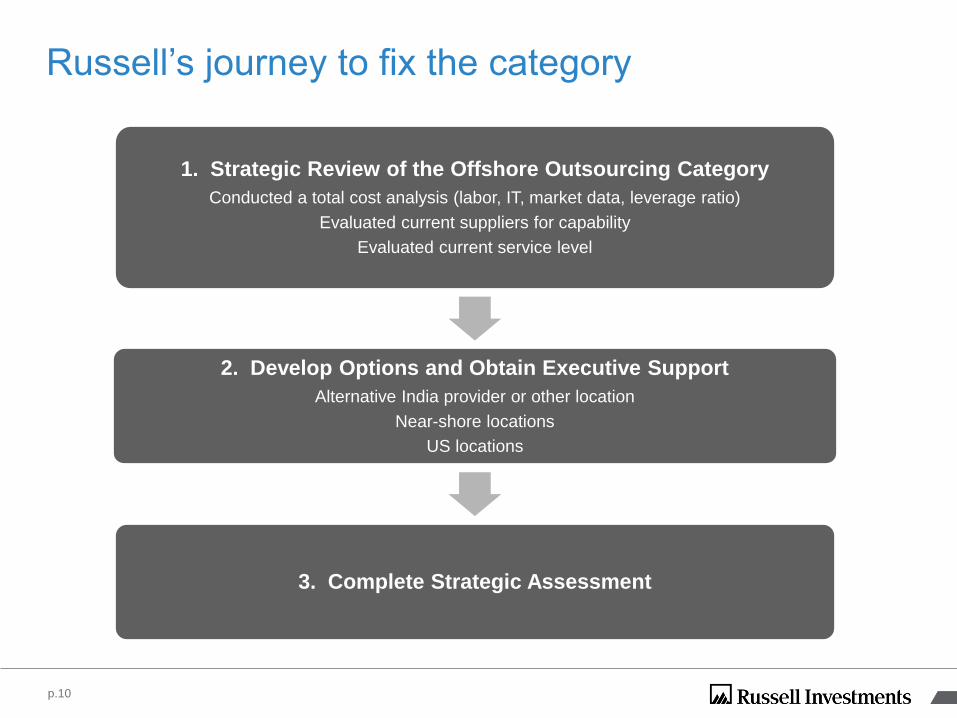

Russell’s journey to fix the category

p.10

1. Strategic Review of the Offshore Outsourcing Category

Conducted a total cost analysis (labor, IT, market data, leverage ratio)

Evaluated current suppliers for capability

Evaluated current service level

2. Develop Options and Obtain Executive Support

Alternative India provider or other location

Near-shore locations

US locations

3. Complete Strategic Assessment

Russell’s search for another low-cost supplier

• Talk with industry analysts (Gartner, Forrester)

• Internet and peer research

• Conduct RFI

Step One

Conducted market and supplier search

• Eastern Europe

• Latin America

• Asia (incl. India, China)

Step Two

Evaluated different geographic locations

• Philippines

• Malaysia

• Vietnam

Step Three

Detailed look at the following three

short-listed locations

p.11

Conclusion from assessment for Russell

p.12

› Bring some of the scope with higher costs and low service levels

back in-house

› Compliance

› Reporting

› Identify another low cost location for some of our needs

› Explore Vietnam for ITO services

› Introduce more competition to current supplier base using a new

supplier

Why Russell prefers Vietnam

› Financial attractiveness of Vietnam is significant – 30% to 50%

lower cost than India (it helps to reset the clock back 10 years)

› Political, social and economic stability are attractive

› For ITO, Vietnam is a comparable alternative to India across

multiple areas

› Availability of high-quality skilled resources is attractive

› ‘Strategic partnership’ focus from Vietnam companies is better

aligned to meet both short and long-term needs of companies

like Russell

p.13

Opportunities in Vietnam – Discussion

Vietnam – A new destination for outsourcing

p.15

“Vietnam remains one of the most competitive options in the

world for software outsourcing due to its competitive labor

costs and other business costs.” (2010)

“Vietnam is one of the 10 most attractive global

services locations in the world.” (2011)

“Low labor cost in Vietnam is attracting many Japanese

companies in outsourcing their software development

services.” (2014)

“Ho Chi Minh City to watch as a location for the next

outsourcing boom.”

Top 100 Outsourcing Destinations - The de facto ranking of

outsourcing cities around the world (2014)

-Ho Chi Minh City is ranked at 17th above Kuala Lumpur

-Hanoi is ranked at 22nd

Why Vietnam?*

› Population of 92M people with 65% younger than 35

› One of the fastest growing economies in South East Asia

› Politically stable with strong government support for the IT industry

› 290 universities/colleges offering IT and communication training

› English is the second language

› Highly skilled and motivated labor force

› Rates are 30% to 50% lower than India or China

› Quickly becoming the major manufacturing alternative to China

(“China +1” strategy)

› Has the potential to be the ITO/BPO alternative to India (“India +1”

strategy)

p.16

*Sources: General Statistics Office of Vietnam; www.fpt.com; http://www.vietnamoutsource.org/vno-outsource-foundation.html;

http://www.tmasolutions.com/whyvn.aspx

The TRANS-PACIFIC PARTNERSHIP (TPP) will

change the game for Vietnam*

Objectives Timeline Countries Involved

• The TPP intends to enhance trade and

investment among the TPP partner countries,

promote innovation, economic growth and

development, and support the creation and

retention of jobs.

• All signatory countries will be required to

conform their domestic laws and policies to

the provisions of the Agreement, which will

follow international standard in areas such as

cross-border service supply, financial service,

E-commerce, investment, intellectual

property, government procurement,

employment, environment, state-owned

enterprises.

• Started in 2005 and is

slated to wrap up

negotiations by end

2014.

• It is one of the key

foreign policy objective

of President Obama.

• United States

• Vietnam

• Australia

• Brunei

• Canada

• Chile

• Japan

• Malaysia

• Mexico

• New Zealand

• Peru

• Singapore

* For discussion purposes only

p.17

Some areas of outsourcing in Vietnam

ITO

› Product engineering

› Application development

› QA & testing

› Maintenance & supporting

› Porting & migration

› IT managed services

› R&D

p.18

BPO/KPO – Non-voice BPO

› Data entry & conversion

› Digitization

› Document processing

› Online catalog/image processing

› Loans & mortgage processing

› Title insurance processing

› Procurement, accounting, and finance

Sources: http://www.fpt.com.vn/en/products_and_services/software/; http://www.tmasolutions.com/services.aspx; Gartner

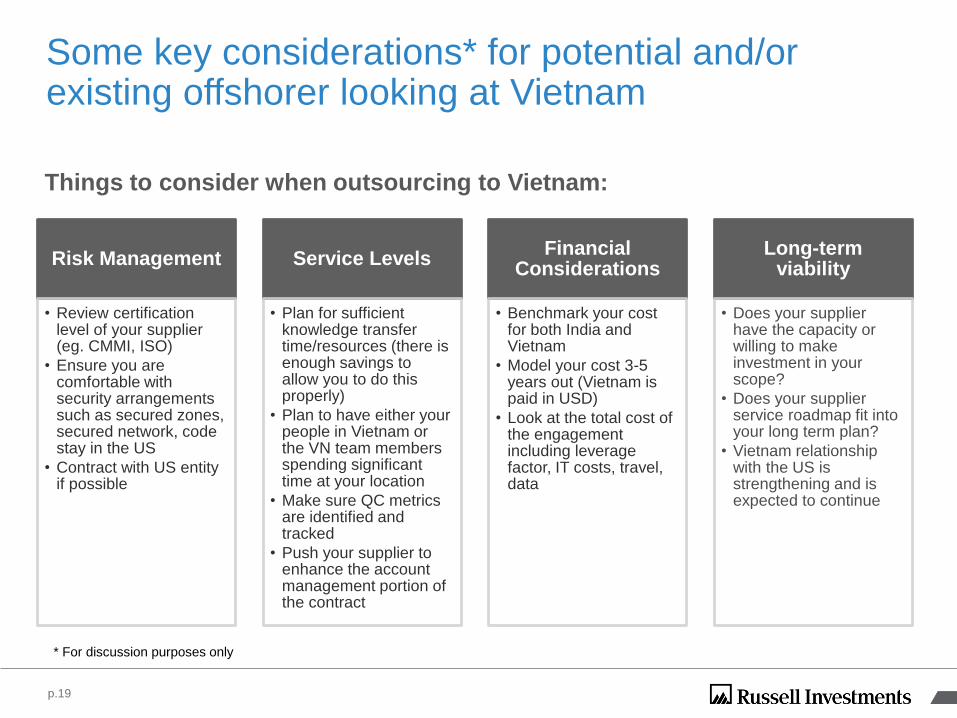

Some key considerations* for potential and/or existing offshorer looking at Vietnam

Risk Management

• Review certification level of your supplier (eg. CMMI, ISO)

• Ensure you are comfortable with security arrangements such as secured zones, secured network, code stay in the US

• Contract with US entity if possible

Service Levels

• Plan for sufficient knowledge transfer time/resources (there is enough savings to allow you to do this properly)

• Plan to have either your people in Vietnam or the VN team members spending significant time at your location

• Make sure QC metrics are identified and tracked

• Push your supplier to enhance the account management portion of the contract

Financial Considerations

• Benchmark your cost for both India and Vietnam

• Model your cost 3-5 years out (Vietnam is paid in USD)

• Look at the total cost of the engagement including leverage factor, IT costs, travel, data

Long-term viability

• Does your supplier have the capacity or willing to make investment in your scope?

• Does your supplier service roadmap fit into your long term plan?

• Vietnam relationship with the US is strengthening and is expected to continue

p.19

Things to consider when outsourcing to Vietnam:

* For discussion purposes only

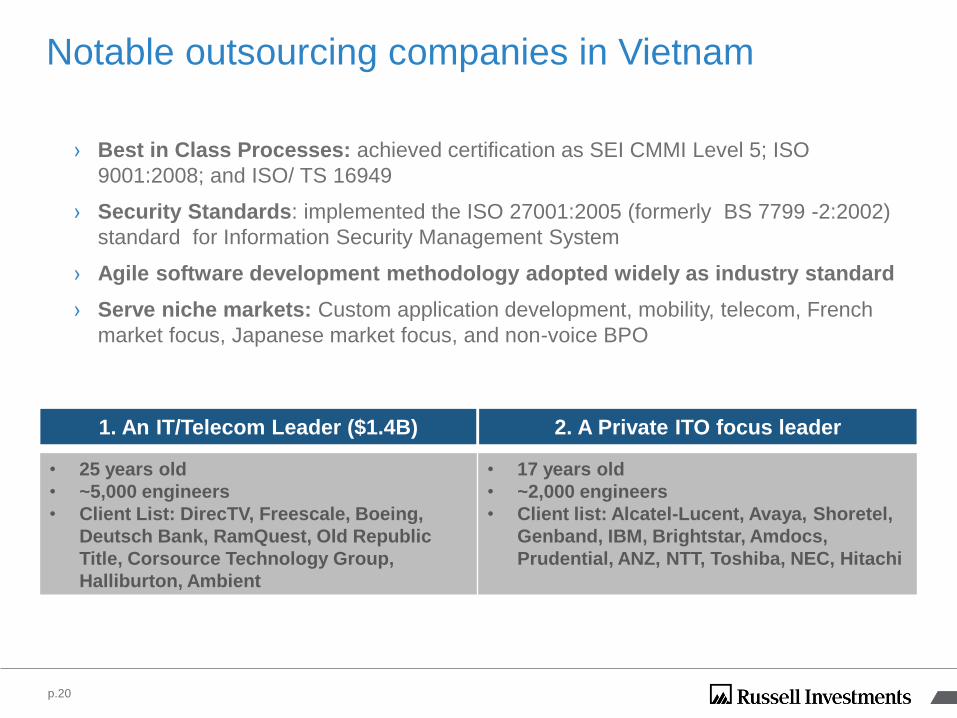

Notable outsourcing companies in Vietnam

• 25 years old

• ~5,000 engineers

• Client List: DirecTV, Freescale, Boeing,

Deutsch Bank, RamQuest, Old Republic

Title, Corsource Technology Group,

Halliburton, Ambient

• 17 years old

• ~2,000 engineers

• Client list: Alcatel-Lucent, Avaya, Shoretel,

Genband, IBM, Brightstar, Amdocs,

Prudential, ANZ, NTT, Toshiba, NEC, Hitachi

p.20

› Best in Class Processes: achieved certification as SEI CMMI Level 5; ISO

9001:2008; and ISO/ TS 16949

› Security Standards: implemented the ISO 27001:2005 (formerly BS 7799 -2:2002)

standard for Information Security Management System

› Agile software development methodology adopted widely as industry standard

› Serve niche markets: Custom application development, mobility, telecom, French

market focus, Japanese market focus, and non-voice BPO

1. An IT/Telecom Leader ($1.4B) 2. A Private ITO focus leader

Russell Case Study:

A Review (For Discussion Purposes Only)

Russell case study – MS App. Dev. RFP*

p.22

• Application development and support for MS IT projects with $3M in projected spend.

Scope

• Global Sourcing and Procurement engaged IT to discuss options for application development and IT support. IT was concerned about the low service level provided by the current suppliers and was receptive to consolidating the supply base.

• The project executive sponsor is the CIO.

Engagement

• Russell currently uses six providers (4 US and 2 India) and would like to consolidate the supply base to leverage the spend and reduce the complexity of supplier management.

• Control costs. Applications development and support costs have increased 15% annually from 2011 to 2013.

• Identify MS certified providers that have the scale and skills to support Russell’s applications development and support needs for the short and long term.

Goals

• GSP conducted an RFP with active participation from IT to define the scope, requirements, and evaluation criteria.

• The RFP was sent to 14 suppliers and10 responses were received. Based on price and scoring of responses, 6 suppliers were invited to on-site presentations.

Sourcing

Final ResultRussell consolidated the MS

Applications Development

providers to 2 providers. One

located in Vietnam and one

located in the US. The

recommendation was based on

the selected providers having

strong service delivery and lower

costs. Vietnam providers’ costs

are 40% below India and 80%

below US providers.

* For discussion purposes only

Next Steps

Vietnam as a solution to strategic challenges*

p.24

Profile Volume Challenges Solutions

Large> 1000

FTEs

• Supplier fragmentation with at least 4-

5 suppliers

• Offshore rates are comparable across

most suppliers

• Onshore/niche consulting spend is

significant

• Business units have their preferred

suppliers which lead to a lack of

competition

• Strategic: Develop a Vietnam supplier in this

space, start with a pilot in their sweet spot,

then help to position your new partner as a

competitor to your incumbents as the partner

become more knowledgeable (this apply to

both India providers as well as US consulting

suppliers)

Medium300-1000

FTEs

• Cost pressure as contracts are

renewed

• Service quality deteriorating (less

focus from major suppliers)

• Turnover/Visa issues are cropping up

and are impacting operations

• Strategic: Leverage a Vietnam supplier in

some sizeable projects, provide competition

to your incumbents

• Tactical: Use Vietnam resources to augment

your weaken areas, shift more as you feel

more comfortable

Small< 300

FTEs

• Too small for major suppliers, end-up

with Tier 2 or 3 providers

• Evaluate Vietnam suppliers as alternative to

your incumbents

• Transition over to the new supplier once you

are comfortable

* For discussion purposes only

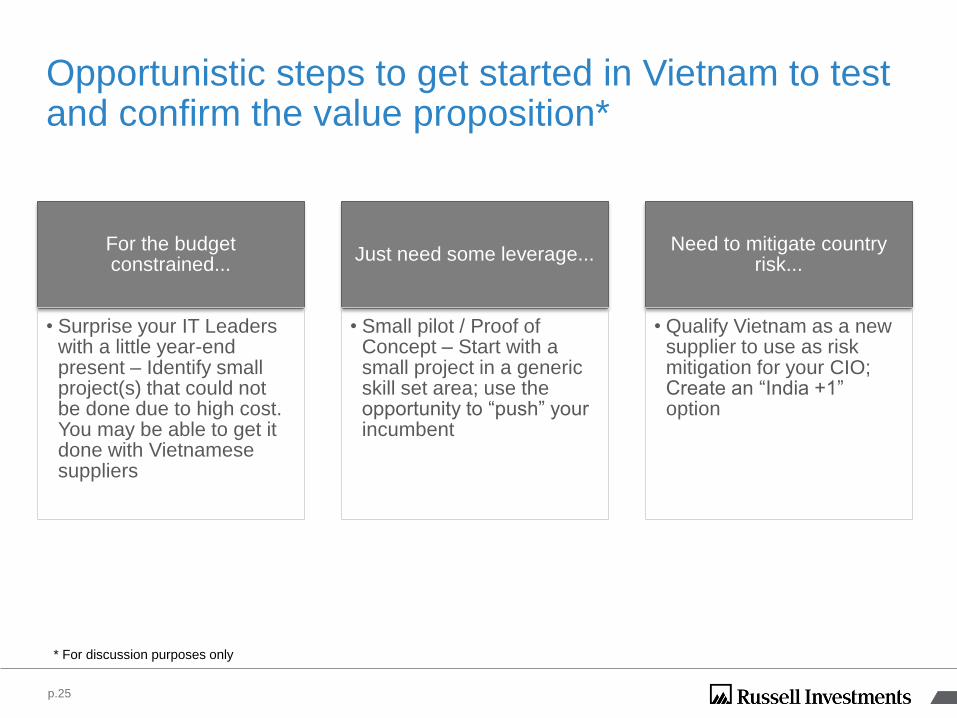

Opportunistic steps to get started in Vietnam to test and confirm the value proposition*

For the budget constrained...

• Surprise your IT Leaders with a little year-end present – Identify small project(s) that could not be done due to high cost. You may be able to get it done with Vietnamese suppliers

Just need some leverage...

• Small pilot / Proof of Concept – Start with a small project in a generic skill set area; use the opportunity to “push” your incumbent

Need to mitigate country risk...

• Qualify Vietnam as a new supplier to use as risk mitigation for your CIO; Create an “India +1” option

p.25

* For discussion purposes only

Rate benchmark* - Complimentary

p.26* For discussion purposes only

Assessment of your Offshore rates:

› The blended offshore rates are high (4th quartile), in particular some of the niche skills rates are

higher than your peers. A job specific analysis will help

› The blended onshore rates for India suppliers are not competitive

› Your India blended offshore rates are 42% higher than Vietnam suppliers, the range is between 34%-

55%. Your onshore rates are 60% higher than Vietnam suppliers

› Your ITO scope can be covered by two Vietnam suppliers (further detail analysis required)

Discuss opportunities:

› Conduct a job specific benchmark analysis to determine rate negotiation strategy – Immediate

› Evaluate Vietnam suppliers for some of the lower risk scope (QA testing, migration support) and

project scope (MobileApp, Microsoft App dev, workflow optimization)

www.russell.com“Russell,” “Russell Investments,” “Russell 1000,” “Russell 2000,” and “Russell 3000”

are registered trademarks of the Frank Russell Company.

Contact information

Viet Ho

Russell Investments

PH: 206.321.5540

DE

NV

ER FALL

SU MMIT

2014

Session #WS06

A Low Cost Alternative: Vietnam, the New Offshore Location

VietHo

Russell Investments206-505-4637

Speaker:

www.russell.com“Russell,” “Russell Investments,” “Russell 1000,” “Russell 2000,” and “Russell 3000”

are registered trademarks of the Frank Russell Company.

Thank you

www.russell.com“Russell,” “Russell Investments,” “Russell 1000,” “Russell 2000,” and “Russell 3000”

are registered trademarks of the Frank Russell Company.

The opinions expressed in this material are not necessarily those held by Russell Investment Group, its affiliates or subsidiaries. While all material is deemed to be reliable, accuracy and completeness cannot be guaranteed. Theinformation, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

Russell Investment Group is a Washington, USA corporation, which operates through subsidiaries worldwide, including Russell Investments, and is a subsidiary of The Northwestern Mutual Life Insurance Company.

DE

NV

ER FALL

SU MMIT

2014

Session #WS06

A Low Cost Alternative: Vietnam, the New Offshore Location

VietHo

Russell Investments206-505-4637

Speaker: