a multi-phase, flexible, and accurate lattice for pricing complex derivatives with multiple market...

TRANSCRIPT

A Multi-Phase, Flexible, and Accurate Lattice for Pricing

Complex Derivatives with Multiple Market Variables

BTT(Bino-trinomial Tree)

• A method can reduce nonlinearity error.• The nonlinearity occurs at certain critical

locations such as a certain point, a price level, or a time point.

• Pricing results converge smoothly and quickly.• A BTT is combined a more bBTT(basic BTT)

bBTT(Basic Bino-trinomial Tree)

• The bBTT is essentially a binomial tree except for a trinomial structure at the first time step.

• There is a truncated CRR tree at the second time step to maturity.

• Which provides the needed flexibility to deal with critical locations.

Basic Terms

• The stock price follow a lognormal diffusion process:

=> • The mean and variance of the lognormal

return of :

• The CRR(Cox, Ross, & Rubinstein) lattice adopts: ,

,

t t

r t r t

u d

u e d e

e d u eP P

u d u d

( )S t

( )S t

Log-distance

• Define the log-distance between stock price and as .• The log-distance between any two adjacent

stock price at any time step in the CRR lattice is .

1S 2S 1 2| ln ln |S S

2 t

ln ln ln ln

ln ln

( )

2

t t

Su Sd u d

e e

t t

t

CRR tree

bBTT

bBTT

• Coincide the lattices and the barriers.• Let • Adjust s.t to be an integer.• The first time interval

2

h l

t

t

' 1 ( ' > )T

t T t t tt

ln( ) ln( ) s s

H Lh and l

S S

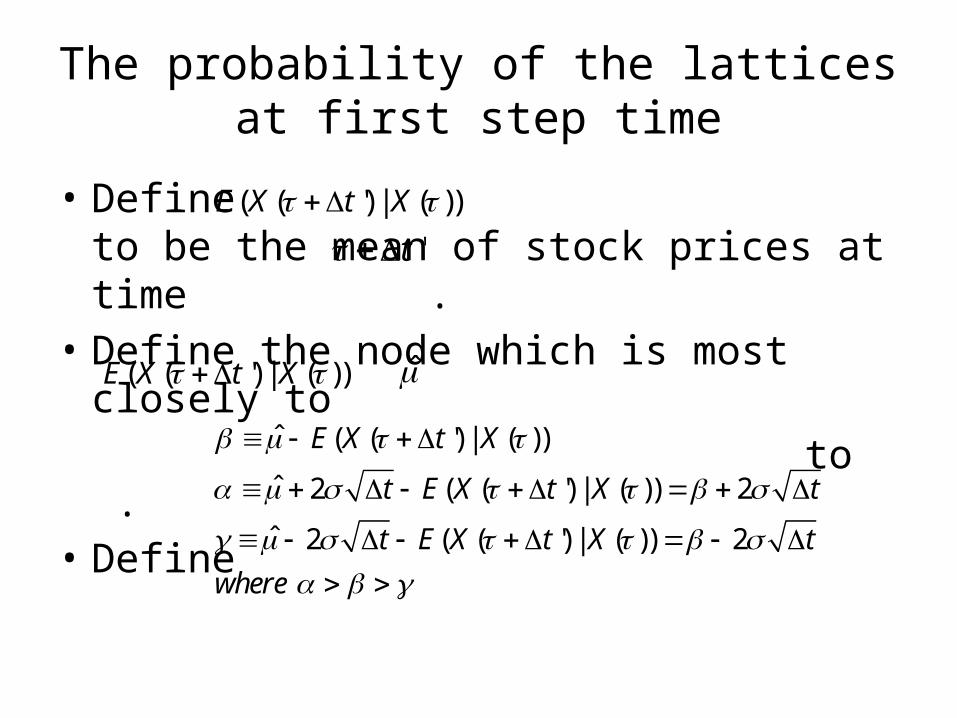

The probability of the latticesat first step time

The probability of the latticesat first step time

• Define to be the mean of stock prices at time .

• Define the node which is most closely to to .• Define

( ( ') | ( ))E X t X

't

( ( ') | ( ))E X t X ̂

ˆ ( ( ') | ( ))

ˆ 2 ( ( ') | ( )) 2

ˆ 2 ( ( ') | ( )) 2

E X t X

t E X t X t

t E X t X t

where

The probability of the latticesat first step time

• The branching probabilities of node A can be derived by solving the equalities:

( . ., , , )u m di e P P P

The probability of the latticesat first step time

• By Cramer’s rule, we solve it as

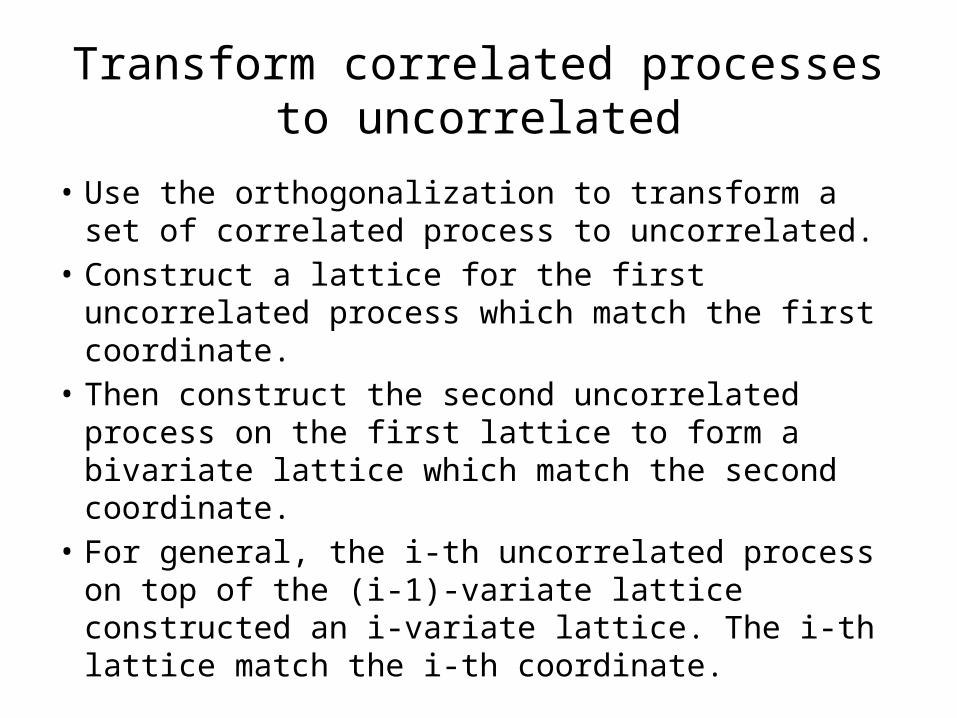

Transform correlated processes to uncorrelated

• Use the orthogonalization to transform a set of correlated process to uncorrelated.

• Construct a lattice for the first uncorrelated process which match the first coordinate.

• Then construct the second uncorrelated process on the first lattice to form a bivariate lattice which match the second coordinate.

• For general, the i-th uncorrelated process on top of the (i-1)-variate lattice constructed an i-variate lattice. The i-th lattice match the i-th coordinate.

Transform correlated processes to uncorrelated

• Demonstrate for 2 correlated processes.• Let and follow:

• can be decomposed into a linear combination of and another independent Brownian motion :

1S 2S

2dz

1dz

dz

Transform correlated processes to uncorrelated

• The matrix form:

• Define =>

1

22 2

0

1A

11

2 21 2

1 0

1

1 1

A

Transform correlated processes to uncorrelated

• Transform and into two uncorrelated processes and .

• The matrix form:1X 2X

1S 2S

1

11 11

1 22 22 2

1 2

1

1 1

1 2

2 21 2

1 1

1 0

0 1

1 1

dS

dX dSA

dS dSdX dS

dzdt

dz

Transform correlated processes to uncorrelated

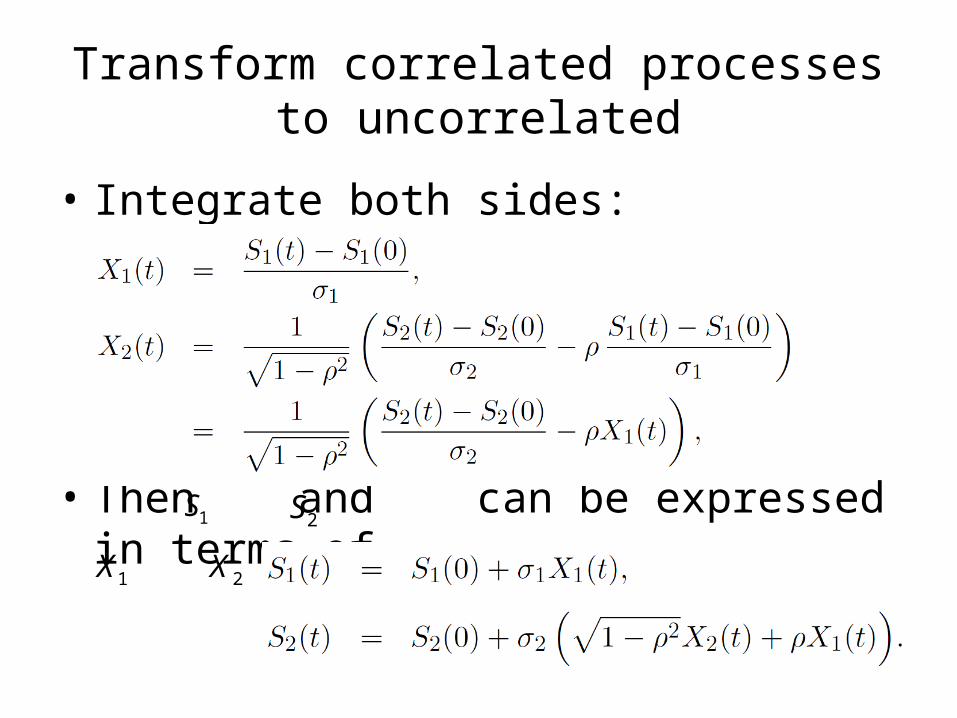

• Integrate both sides:

• Then and can be expressed in terms of and :

1S 2S

1X 2X

Multi-phase branch construction

A bivariate lattice: two correlated market variables

• Define is the stock price, is the firm’s asset value.

• The bivariate lattice is built to price vulnerable barrier options with the strike price and the barrier .

• The default boundary for the firm's asset value where

( )S t ( )V t

K( )( ) T tB t Be

* ( )( ( ), ) ( ( ), )r T tD S t t De c S t t

A bivariate lattice: two correlated market variables

• Assume and follow the processes:

• By Ito’s lemma:

( )S t ( )V t

A bivariate lattice: two correlated market variables

• Use the orthogonalization:

=>

ln

ln

ln ln

2 2ln ln

1 0

0 1

1 1

S

S S

S V

S V

dzdXdt

dY dz

Transform to( )B t ( )XB t

1 11

1

( ) (0)( )

ln ( ) ln (0)( ) ( )X

S

S t SX t

B t SB t

Transform to*( )D t * ( )YD t

2 22 12

2

**

2

( ) (0)1( ) ( )

1

1 ln ( ) ln (0)( ) ( )

1Y

V

S t SX t X t

D t VD t X t

The branches

An example lattice

• Assumption:

0

0

30

3

40

20%

100

20%

S

V

K

T

S

V

0

5%

75%

35

0.01

90

r

B

D

An example lattice

• Set the option for 2 periods ( ).• Compute the lattices in X coordinate first.• For example, • • • The log-distance between 2 vertically

adjacent nodes is•

1.5t

( )ln ( ) ln (0)( ) , ( ) sX t

s

S t SX t S t e

0.2 ( 0.743)(1.5) 34.479S e

2 2.45t

1.5t

21 0.2(1.5) 0.05 1.5 0.225

0.2 2

(1.5)

X

XXB

An example lattice

• • Similar,• • •

(1.5) 1.707, (1.5) 3.192, (1.5) 56.275, (1.5) 21.125u d u dX X S S 0.01 (3 3)ln(35 ) ln(40)

(3) 0.6680.2X

eB

(3) (1.5) (1.5) 1.707 0.225 1.932X u XX

(3) 0.668 2.45 1.782, (3) 1.782 2.45 4.231m uX X

(3) 93.237, (3) 57.125, (3) 35u m dS S S

An example lattice

• Then compute the lattices in Y coordinate.• For example,• •

0.05(1.5)1 2( (1.5),1.5) (1.5) ( ) 30 ( ) 28.019u uc S S N d e N d

* 0.05 1.5(1.5) 90 28.019 111.516D e

* 1 ln(111.516) ln(100)(1.5) 0 1.707 0.545

0.21 0YD

An example lattice

• Similar, • • • • •

0.05(3-3)1 2( (3),3) (3) ( ) 30 ( ) 63.237u uc S S N d e N d

* 0.05 (3-3)(3) 90 63.237 153.237uD e

0.05(3-3)1 2( (3),3) (3) ( ) 30 ( ) 27.125m mc S S N d e N d

* 0.05 (3-3)(3) 90 27.125 117.125mD e

* 1 ln(153.237) ln(100)(3) 0 4.231 2.134

0.21 0uYD

* 1 ln(117.125) ln(100)(3) 0 1.782 0.790

0.21 0dYD

An example lattice

An example lattice

• Plot the 3D coordinate by X, Y, and t.• Find , , and for the same method, which

• Compute the option value at each node.• Find the initial option value by backward

induction.

iY iV iQ

, , or i u m d

An example lattice

• For node C,

• For node D,• Then the call value at node B:

• By backward induction, the initial value=7.34

1

2

3

( (3) ) 63.237

0.75 ( (3) ) 47.43

93.890.75 ( (3) ) 29.06

153.237

u

u

u

c S K

c S K

c S K

1 2 327.13, 27.13, 20.34d d d

-

An example lattice

The Hull-While interest rate model

• The short rate at time t, r(t) follows

• is a function of time that make the model fit the real-world interest rate market.

• denotes the mean reversion rate for the short rate to revert to .

• denotes the instantaneous volatility of the short rate.

• is the standard Brownian motion.

( ) ( ( ) ( )) r rdr t t ar t dt dz

( )t

a( )r t ( )t

a

r

rdz

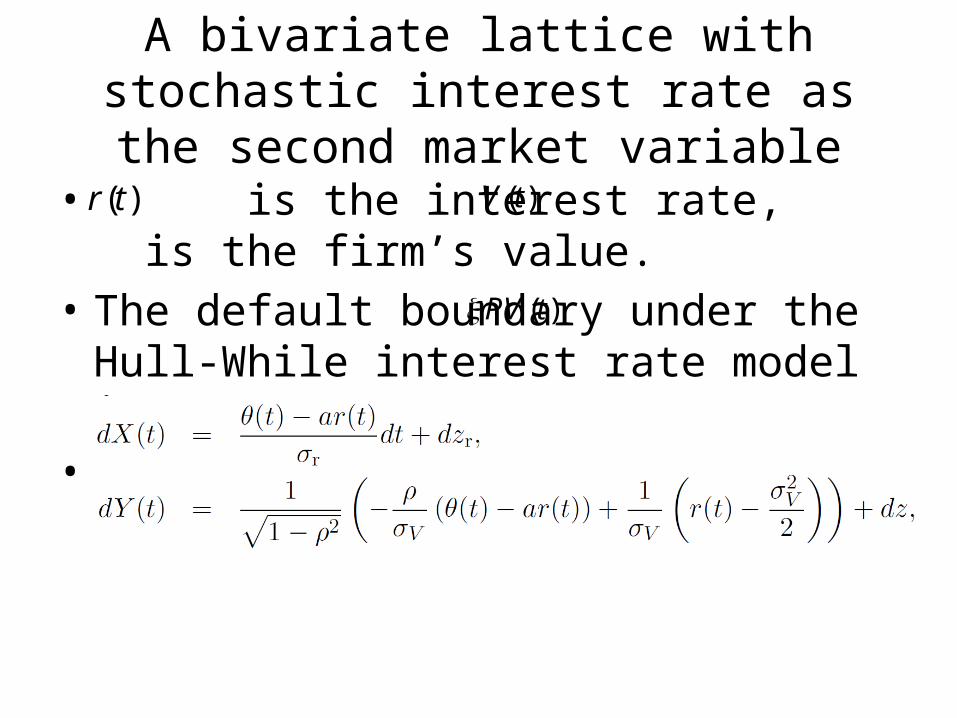

A bivariate lattice with stochastic interest rate as the second market variable

• is the interest rate, is the firm’s value.• The default boundary under the Hull-While

interest rate model is ,• The stochastic process:

( )r t ( )V t

( )PV t