a new analytical tool for forex trading1 - ecomod.net apsari, aghnia - ecomod 1017.pdfa new...

TRANSCRIPT

1

ANewAnalyticalToolforForexTrading1

ImanGunadi,ApsariDharmesti,AghniaYurizkanti2

PreliminaryDraftJune2017

AbstractPredictingcurrencymovementisveryimportantforinvestorswhofaceexchangeraterisksintheirinvestments.Unfortunately,themostofexistingtoolsthatareusedasaguidancedonotcontainanyinformationaboutthefuture.Mostexistingtoolsusepastperformanceinpredicting thresholdsor supportand resistance levels.Theydonot take intoaccountinvestors’ reviewson economic forecasts ormarket dealers’ sense in predictingmarketevents.Tofillthisgap,thisstudytrytobuildanalternativeanalyticaltooltosetsupportand resistance levels that is more consistent with economic and market forecasts oroutlooks.Thisstudyusesomesimulationanalysesandcomparativestudiesusingseveralcountries(Brazil,India,Indonesia,Malaysia,Philippine,Russia,ThailandandTurkey)dataandthencombine those data with some market analyst reviews related to those countries toproduceanewanalyticaltool.Usingdatafrom2014until2016,thestudyfoundthatthenewanalyticaltoolperformsbetterthanexistingtools.Therefore,itcanbeusedasamoreappropriateguidanceforinvestorsforreducingcurrencyriskintheirinvestments.

JELClassificationNumbers:E44,E47,F31,F37,G11

Keywords:forextrading,bollingerband

1TheviewsexpressedinthisWorkingPaperarethoseoftheauthor(s)anddonotnecessarilyrepresentthoseofBankIndonesiaorBankIndonesia’spolicy.WorkingPapersdescriberesearchinprogressbytheauthor(s)andarepublishedtoelicitcommentsandtofurtherdebate.2TheauthorsareDeputyDirector,ManagerandAssistantManager,respectively,intheMonetaryManagementDepartmentofBankIndonesia.TheauthorswouldliketothankreviewersinseveraldepartmentsofBankIndonesiaforextensivecomments.Allremainingerrorsareours.

2

I. Introduction

Nowadays,investorsaremuchmoresmarterthantheywereinthepast.Ininvestingtheir

capital,theywillinvestinseveralportfoliosinseveralfinancialmarketsinseveralcountriesto

gain an optimum return. As they can involve in severalmarkets, investors have an ability to

arbritageamongthosemarkets.Capitalcantransformfromoneportfoliotootherportfoliosand

fromone currency to other currencies. As a consequence, capitalmoves very fast from one

financialmarkettoanotherintheformofanycurrencies.Inoneday,ahugeamountofmoney

andmillion transactionsare involved in financialmarkets.Alongwithhigherpotential return,

investingtheirmoneyinmanymarketsinmanycountries,investorswillalsofacesomerisksthat

leadtoalowerreturn.Evenmore,theirmoneywillshrinkiftheyinvestcarelessly.

Therearemanyrisksinfinancialmarkets,suchascreditrisk,marketrisk,interestraterisk,

liquidityrisk,policyrisk,operationalrisk,currencyriskandsoon.Oneofthemostcommonrisks

in investment is currency risk. Fluctuation in currency rates can causeprofitor losswhenan

investorhasexposureto foreigncurrencyor in foreign-currency-traded investmentsalthough

thecurrencyvalueinwhichtheunderlyinginstrumentisregistereddoesnotchanges.Currency

riskitselfdefinedasthepotentialriskoflossfromexchangeratefluctuation.Inordertolower

currencyrisk,investorscandohedgingorothertechniquedesigntooffsetanycurrencyrelated

gains or loses (Kuepper, 2017).Normally, a combination of forex forwards and options let on

investors to fixcurrency riskwithin tolerable levelsas longaspremiumsare reasonable.This

hedging techniques are not continually powerful, though diversification into many major

currenciescanhelplimitthisrisk.

3

Toavoidlosstheirmoney,investorswillcollectallrelevantinformationtoenhancereturn

for their investments. Information is very important to decide howmuchmoney should be

investedinoneportfoliooranother.Informationalsowilltellinvestorswhichmarketsaregoing

to be bullish or bearish. In general, information can be devided into two factors, namely

sentiment factor (rumours) and fundamental factor. These two factors influence markets

frequentlyandgivesignificantimpactonreturnofinvestments.However,investorscouldalso

bedefinedintotwotypes,namelylongterminvestorsandshortterminvestors.Usually,longor

mediuminvestorswillconcernaboutfundamentalfactorsofmarketsandcountrieswherethey

invest.Theydoesnotreallyconcernaboutsentimentfactorsbecausetheyinvestinalongperiod.

In contrary, short term investorswill concernboth fundamental and sentiment factors.

Thesetypesofinvestorsmovestheirinvestmentsfromonemarkettoothermarketquiterapidly.

Theywillcometoinvestinportfoliousuallyinashortperiodwhichdependmostlyongoodnews

in themarket. This condition could lead currencymovement toone sidebecauseof herding

behaviourof investors.Also inashortterm,theycouldmovetotheoppositedirectionifbad

newssuddenlyappearorthepreviousgoodnewsdonotmeettheirexpectations.Thissituation

makescurrencyswingandalsocalledahighcurrencyvolatility.

Inordertoanalysecurrencymovement, investorshaveanumberoftoolsforpredicting

currencymovement. Ingeneral,asanadditiontoglobalmarketview, investorsmostlyadopt

severaltechniqueswhicharewidelyavailableinfinancialmarketfortechnicalmethodsuchas

Bollingerband,MACD3andmanyothers.However,inpredictingdailycurrencymovement,most

3MACD=movingaverageconvergenceanddivergence

4

ofexistingtoolsdonothaveacapabilitytodothejob.Inaddition,itisverydifficulttobuilda

sophisticatedmodeltosupportforextrading.Thus,usingcharts,paterns,simplecalculationsand

othersimpletoolsthatareabletobeproducedquicklyarethemostpreferable.

Almostall analytical tools areable tobea risk guideline for investorswho investusing

particularcurrency.Forexample,wheninvestorsinvesttheirmoneyinonecountry,theycanuse

Bollingerbandtomeasurecurrencyriskoftheinvestment.Theyalsocanseehowclosecurrent

currencyleveltoitssupportingorresistancelevel.Thisinformationisusedtodecidewhether

they have to make portfolio adjustment or not. However, most available tools using past

performanceinpredictingsupportandresistancelevel.Thoseexistingtoolsdoesnottakeinto

accountinformationneededfor investorsthathavebeenmentionabove.Furthermore,those

existing tools alsoneglect current condition, fundamental economy,peer countries’ currency

movement and so on. Most available tools do not cover analyst review or dealer sense in

predictingmarket event. Hence, it needs some adjustment to get themore suitable tools in

predictingfutureevent.

Therefore,thispaperfocusonhowtocombinehistoricaldatawithmarketforecastand

informationincludingfundamentalandsentimentfactorsinordertobuildanewanalyticaltool.

Therefore, thisnewanalytical tool isexpected togivea forecastof currencymovement.This

alternative tool couldbesimilarordifferentwith theexisting tools suchasBollingerbandor

others.Itdependsonhowamarketanalyst’sviewabouttheoutlookofmarkets.Ifthemarketis

abouttoconsolidatethenthisnewtoolcouldbesimilarwithBollingerbandorothers.Hence,

thisnewanalytical toolneedstobetestedwithempiricalstudiesusingdataset fromseveral

countries.Inthisstudy,datafromsomeemergingcountriesareusedforseveralreasons.Apart

5

fromthetechnicalissuessuchasaccessibilityofthedata,thoseobservedcountriesshowedquite

similarreactiontomarketsentimentsincurrencymovement.

Thisstudywillevaluatewhethertherealcurrencymovementfromobservedcountriesare

movinginsidethenewtool.Inevaluatingthosemovement,thisstudywilluseasetofdatafrom

January2014toDecember2016.Thus,thisstudywillaccommodatemarketviewfromanalystin

believingtheircurrencymovementagainstUSDinoneprobabilitywhichcoveredtheirviewfrom

globalanddomesticfactors.

Thisstudywillbedividedintoseveralparts.Afterintroductionatthefirstpart,thisstudy

willexploresomeliteratureswhichpresentedsomeexistingtoolsforforextradingbandatthe

secondpart.Thirdpartwillexplainedthemethodologyusedinthisempiricalstudy.Fourthpart

willtalkaboutthedatathatusedinthisstudy.Inthispartalsowilldiscussabouttheresultofthe

exerciseddata.Then,fifthpartisaconclusion.

II. LiteratureStudies

Inthefinancialmarket,eitherstockmarketorcurrencymarket,peoplecommonlymixed

a chartistwith technical analyst.A chartist analyzesprice chartsonly,while technical analyst

studiestechnicalindicatorsderivedfrompricechangesinadditiontothepricechart.4According

tothatdefinition,technicalanalystscrutinizesthepriceactionofthefinancialmarketsinsteadof

thefundamentalfactorsthatseemtoaffectmarketprices.Itisbecausethereisbelievethatall

4CreditSuisse,TechnicalAnalysis–Explained,GlobalTechnicalResearchandBehavioralFinance.Zurich:(https://www.credit-suisse.com/pwp/pb/pb_research/technical_tutorial_de.pdf)

6

the relevant market information is reflected (or discounted) in the price. There are several

technical analysis thatare commonlyusedby investors. These technical analyses showsome

resistanceandsupportlevelsforhistoricaldata.Someofthemusepattern(triangles,flagsand

doublebottoms)todetermineresistanceandsupportlevels(seefigure1).Therestofthemusing

econometricsorsimplymathematicapproach,suchasmovingaverageincludingBollingerBand

andMACD,stochastic,index5andothers.

Figure1.ExampleofPatterninTechnicalAnalysis

Source:http://www.mrao.cam.ac.uk/~mph/Technical_Analysis.pdf

OneofthemostpopulartechnicalanalysisinforeignexchangemarketisBollingerband.

BasicallyBollingerBandprovidestradingbandforinvestorandanswerswhetherpricesaretoo

highortoolowonarelativebasis.Bollinger(1992)explainedthatBollingerbandareplottedtwo

standarddeviationsaboveandbelowasimplemovingaverage.Bollingerbandshows foreign

5RelativeStrengthIndex.

7

exchange move within corridor on daily basis. Usually, Bollinger band is used to look at a

momentum of currency’s movement at one period. Therefore we can predict whether the

observedcurrencyhasatendencytocontinueatcurrentmoveorithasreachedasupportor

resistancelevel.Inthiscase,theobserversdonothaveanycapabilitytobreakthelevel.

Figure2.BollingerBandinTechnicalAnalysis

(source:Bloomberg2017)

Bollinger(2001)statedthatstandardBollingerBandformulasasfollows:

𝑈𝑝𝑝𝑒𝑟𝑏𝑎𝑛𝑑 = 𝑀𝑖𝑑𝑑𝑙𝑒𝑏𝑎𝑛𝑑 + 2 ∗ 𝑠𝑡𝑎𝑛𝑑𝑎𝑟𝑑𝑑𝑒𝑣𝑖𝑎𝑡𝑖𝑜𝑛

𝑀𝑖𝑑𝑑𝑙𝑒𝑏𝑎𝑛𝑑 = 20𝑝𝑒𝑟𝑖𝑜𝑑𝑚𝑜𝑣𝑖𝑛𝑔𝑎𝑣𝑒𝑟𝑎𝑔𝑒

𝐿𝑜𝑤𝑒𝑟𝑏𝑎𝑛𝑑 = 𝑀𝑖𝑑𝑑𝑙𝑒𝑏𝑎𝑛𝑑 − 2 ∗ 𝑠𝑡𝑎𝑛𝑑𝑎𝑟𝑑𝑑𝑒𝑣𝑖𝑎𝑡𝑖𝑜𝑛

8

Accordingtoitscalculationbase,BollingerBandsometimesisusedtoidentifyperiodwherehigh

volatilityor lowvolatilityhappened.Thewidthof thebandsgetnarrowerduring lessvolatile

periodandviceversa.Hence,itcanidentifiedperiodwhenpricesareatextremeandpossibly

unstablelevels.

Other popular technical analysis in foreign exchange market is Moving Average

ConvergenceDivergence(MACD).Thismethodwasdevelopedin1970sbyGeraldAppelasan

indicatorofthechangeinasecurity’sunderlyingpricetrend(Grimes,2012).MACDcommonly

calculatedbytheformulaasfollows;

𝑀𝐴𝐶𝐷𝐿𝑖𝑛𝑒 = 12𝑑𝑎𝑦𝐸𝑀𝐴 − 26𝑑𝑎𝑦𝐸𝑀𝐴

𝑆𝑖𝑔𝑛𝑎𝑙𝐿𝑖𝑛𝑒 = 9𝑑𝑎𝑦𝐸𝑀𝐴𝑜𝑓𝑀𝐴𝐶𝐷𝐿𝑖𝑛𝑒

𝑀𝐴𝐶𝐷𝐻𝑖𝑠𝑡𝑜𝑔𝑟𝑎𝑚 = 𝑀𝐴𝐶𝐷𝐿𝑖𝑛𝑒 − 𝑆𝑖𝑔𝑛𝑎𝑙𝐿𝑖𝑛𝑒

EMAstandsforexponentialmovingaveragewhicharesimilartomovingaverage,exceptthat

moreweightaregiventothelatestdata.Consequently,thistypeofmovingaveragetakesfaster

torecentpricechangesthatsimplemovingaverage.Thus,theinteraction,whethercrossoveror

divergence,betweenMACDlineandsignallinethattechnicalanalystlookfor.Assuggestedby

its name, MACD is distressed with the convergence and divergence of the two exponential

movingaverages.Hence,themainpurposesoftheanalysisistoidentifyturningpointsinatrend

byfocusingonitsdivergenceandconvergence.

9

Figure3.MovingAverageConvergenceDivergence(MACD)inTechnicalAnalysis

(source:Bloomberg2017)

Relative Strength Index (RSI) is an analysis developed by J.WellesWilder, to identify

overbought and oversold conditions by measuring velocity of security’s price movement

(Hayden,2004).Fortechnicalanalystsortraders,usingRSItorecognizepotentialturningpoints

helpsthemtomakeentryorexitdecision.ThevaluesofRSIarecalculatedfromeitherclosing

pricesoryields.Hayden(2004)describedthereareonlytwoequationinvolvedinRSIcalculation.

Thefirstparttoobtainisthevalueofrelativestrength(RS)whichistheratiooftheaverageup

closestotheaveragedownclosesover“n”periodsasfollows,

𝑅𝑆 =𝐴𝑣𝑒𝑟𝑎𝑔𝑒𝑜𝑓 𝑁H H𝑑𝑎𝑦𝑠𝑐𝑙𝑜𝑠𝑒𝑠𝑈𝑝𝐴𝑣𝑒𝑟𝑎𝑔𝑒𝑜𝑓 𝑁H H𝑑𝑎𝑦𝑠𝑐𝑙𝑜𝑠𝑒𝑠𝐷𝑜𝑤𝑛

10

Hence,theRSIcalculationcanbedescribebytheequationasfollows,

𝑅𝑆𝐼 = 100 −1001 + 𝑅𝑆

Figure4.RelativeStrengthIndex(RSI)inTechnicalAnalysis

(source:Bloomberg2017)

Other technical analysis that can be used is candlestick charting. Candlestick charting

originallyisJapanesetechnicalanalysisforricetraderinthe17thcentury.Manytradersbelief

thatcandlestickchartingtechniqueaccuratelyreflectsshort-termoutlooks.Moreoveritblend

perfectlywithnearlyallthetraders’commontechnicalanalysismethods.

11

Candlestickisformbyputtingtogetheropening,high,lowandclosingpriceofthedayin

oneverticalline.Whentheopeningpriceishigherthanclosingpricethenafilledcandlestickis

drawnwithdark color, usually black.On the contrary,when theopeningprice is lower than

closingpricethenahollowcandlestickisformed.Thelines,whichcanbeshortorlong,aboveor

belowthecandlerepresentsthehighorlowpricerangeandtheselinesareknownasseveral

names(shadows,tails,wicks).Thecandlemayormaynothaveshadows,tailsorwicks.

Figure5.CandlestickGraph

(Source:Bloomberg2017)

Apatterncanbeformedbyoneorseveralcandlesticks,butnotmorethanfive6.Mostof

the time, candle patterns show reversal patterns but they also help in projecting trends. A

6http://www.optionsuniversity.com/CandlestickSecrets/Book/candlesticksecrets.pdf

12

reversalpatternshowsthatthedirectionofastockisgoingtocurtailitsflowandattimesthis

conveysthatanuptrendordowntrendwillreverseitscourse

Incandlestick,Darsonoetal(2017)explainedthatDojiwasformedincandlestickchart

whenopeninglevelandclosinglevelareatthepricelevel.Dojiisthemostfamouscandlestick

amongalldifferentkindsofcandlesticksandDojiStaristhemostfamousDojipatternsinceits

reliabilityistoshowreversalsign.However,sometraderbeliefthatDojicandlesticksignaland

patternsaresometimestricky,thusaddinganothertoolstothechartcanavoidfalsesignal.In

combiningDojicandlestickandBollingerBands,traderlooksforDojicandlestickwhichhitthe

upperbandorlowerbandasaconfirmedreversalsignforthecurrencyorsecuritiesmovement.

Figure6.CombinationofDojiCandlestickandBollingerBandConfirmingReversalTrend

(Source:Investopedia2017)

13

III. Methodology

Theapproachusedinthenewmethodofdeterminingthetradingbandorexchangerate

corridor beginswithusing the exchange rateof thehighest and lowest transaction from the

previousperiodtodeterminetheexchangerateisexpectedtohappen(expectedexchangerate).

Hencetheexpectedexchangeratewouldbeusedasthereferenceforexchangeratecorridor.

Expectedexchangeratecanbedescribedinthefollowingequation.

(1) 𝑋 = 𝐻. ℎ + 𝐿 1 − ℎ

Where𝐻isthehighesttransactionrateofthepreviousperiod,𝐿isthelowesttransactionrate

ofthepreviousperiod,ℎrepresentstheprobabilityofcurrencydepreciationagainsttheUSDand

𝑋representstheexpectedexchangerate.Sinceℎrepresentsprobability,thenumberofℎcanbe

variedfrom0to1.

Furthermore,thisstudyusingthenumberofexpectedexchangeratetocalculatethe

widthofhalftradingband.Halfthewidthofthetradingbandwhichisdenotedby𝑌is

representedfromthefurthestdistancebetweentheexpectedexchangerate(𝑋)withthevalue

ofthehighesttransactionrate(𝐻)orlowesttransactionrate(𝐿).Thehalfwidthofthecorridor

canberepresentedbythefollowingequation.

(2) 𝑌 = max{𝐻 − 𝑋, 𝑋 − 𝐿}

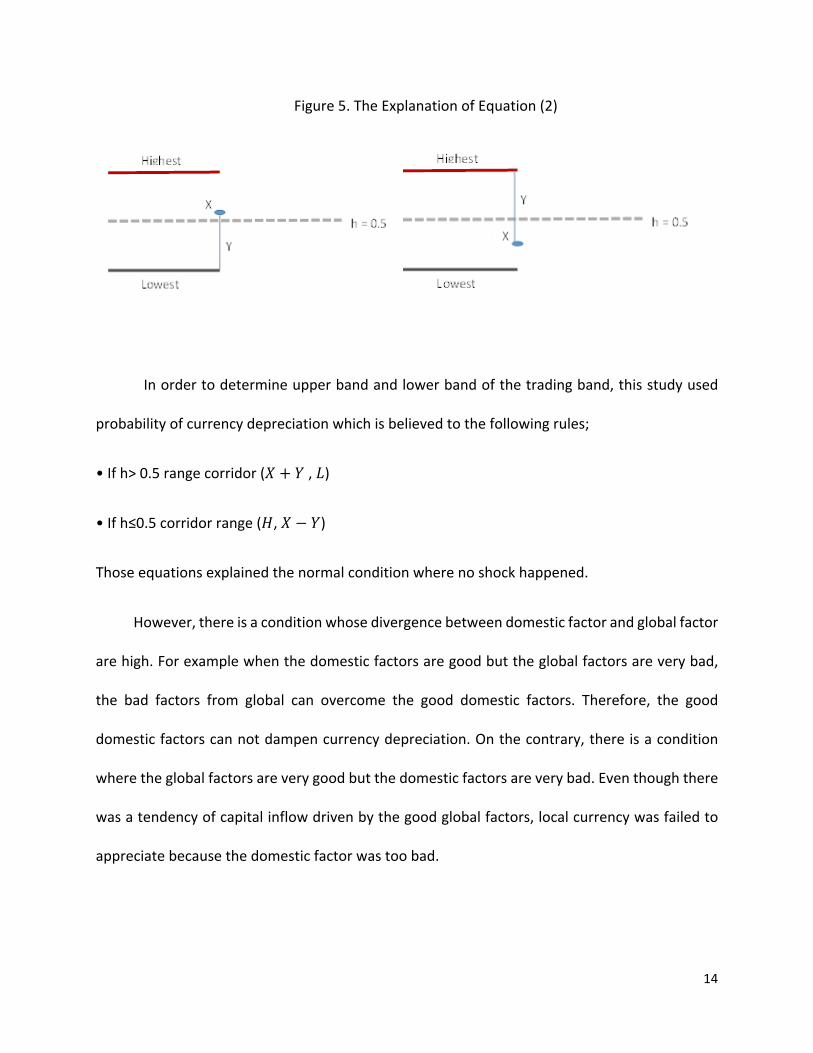

Thefollowingfiguregavetheideaofequation(2).

14

Figure5.TheExplanationofEquation(2)

Inordertodetermineupperbandandlowerbandofthetradingband,thisstudyused

probabilityofcurrencydepreciationwhichisbelievedtothefollowingrules;

•Ifh>0.5rangecorridor(𝑋 + 𝑌,𝐿)

•Ifh≤0.5corridorrange(𝐻,𝑋 − 𝑌)

Thoseequationsexplainedthenormalconditionwherenoshockhappened.

However,thereisaconditionwhosedivergencebetweendomesticfactorandglobalfactor

arehigh.Forexamplewhenthedomesticfactorsaregoodbuttheglobalfactorsareverybad,

the bad factors from global can overcome the good domestic factors. Therefore, the good

domesticfactorscannotdampencurrencydepreciation.Onthecontrary,thereisacondition

wheretheglobalfactorsareverygoodbutthedomesticfactorsareverybad.Eventhoughthere

wasatendencyofcapitalinflowdrivenbythegoodglobalfactors,localcurrencywasfailedto

appreciatebecausethedomesticfactorwastoobad.

15

Therefore,therewasaneedtoadjustthevalueofℎfromequation(1).Inthiscase,ℎwas

determinebytwofactors,globalanddomestic.Hence,ℎmightlessthanzeroorevenhigherthan

1.Symbolℎ∗willrepresentsthenewℎoradjusteddepreciationfactor.

Inordertocapturecurrencydepreciationfactorfrombothdomesticsideandglobalside,the

depreciationfactoristhesumofdomesticandglobalfactor.Hence,thedepreciationfactorcan

berepresentedbythefollowingequation.

(3) ℎ∗ = ℎU + ℎV

Whereℎ∗standsforadjusteddepreciationfactor,ℎU standsfordomesticdepreciationfactor

andℎVstandsforglobaldepreciationfactor.Thus,equation(1)becameadjustedasfollows

(4) 𝑋 = 𝐻. ℎ∗ + 𝐿 1 − ℎ∗

IV. DataandAnalysis

Data

ThisstudyusingseveralsetofdailydatafromemergingcountriessuchasBrazil,Malaysia,

Mexico,India,Indonesia,Philippine,ThailandandTurkeyfromJanuary2014toDecember2016.

Apartfromthetechnicalissuessuchasaccessibilityofthedata,thoseobservedcountriesshowed

quitesimilarreactiontomarketsentimentsincurrencymovement.

Next,equation(1)needsthevalueofprobabilityofcurrencydepreciationwhichrepresents

by ℎ. Instead of using continuous variables, this study used discrete variables to facilitate

classification market condition following investor’s pattern. This study classified ℎ to five

16

numbers (0.2; 0.4; 0.6; 0.8; 1.0) based on investor’s belief to depreciation of local currency.

Wheremarketisexpectedinconsolidationcondition,ℎissetto0.6.Meanwhile,ifexchangerate

is expected to appreciate, ℎis set to 0.2 (highly appreciation) or 0.4 (appreciation). And if

exchangerateisexpectedtodepreciate,ℎissetto0.8(depreciation)or1.0(highlydepreciation).

Prediction ℎHighlyappreciation 0.2

Appreciation 0.4Consolidation 0.6Depreciation 0.8

Highlydepreciation 1.0Table1.ℎbasedoninvestor’sbelief

Then,sinceℎ∗mightbeinnegativeterritoryorhigherthan1,itrequiredtransformation

probability of currency depreciation for global and domestic sentiments. Instead of using

continuous variables, this study used discrete variables to facilitate classification market

conditionfollowinginvestor’spattern.Thisstudyclassifiedglobalsentiments,ℎV,tofivenumbers

(0.2;0.4;0.6;0.8;1.0)basedoninvestor’sbelieftodepreciationoflocalcurrency.Wheremarket

isexpectedinconsolidationcondition,ℎVissetto0.6.Meanwhile,ifexchangerateisexpected

toappreciate,ℎVissetto0.2(highlyappreciation)or0.4(appreciation).Andifexchangerateis

expectedtodepreciate,ℎVissetto0.8(depreciation)or1.0(highlydepreciation).

Prediction ℎVHighlyappreciation 0.2

Appreciation 0.4Consolidation 0.6Depreciation 0.8

Highlydepreciation 1.0Table2.ℎVbasedoninvestor’sbelief

17

Domestic sentiments are influenced by economic factors, politic factors, and other

domesticfactors.Inthisempiricalstudy,weusedGDP,CPI,andTradeBalancethatareavailable

and obtained easily from data provider, such as Bloomberg. Political factors were not used

becauserelativelydifficulttoobtain.Then,thesethreeeconomicdataareprocessedtogetℎU.

First,thisstudycalculatedaverageandstandarddeviationforGDP,CPI,andTradebalance.This

studyused1and½standarddeviation.Second,thisstudyclassifiedeachdatatosixcategories

(1,2,3,4,5,6)basedondeviationbetweenvalueofdataandtheiraverage.

Deviation GDP CPI TradeBalanceAbove1Std.Dev 6 1 6+½–1Std.Dev 5 2 50–+½Std.Dev 4 3 40–-½Std.Dev 3 4 3-½–-1Std.Dev 2 5 2Below-1Std.Dev 1 6 1

Table3.ValueofDeviation

Intable3,weseethatthereisadifferenceindeterminethevalueofdeviationbetween

CPIandotherdata(GDPandTradeBalance).IthappenedbecausewhenvalueofGDPandTrade

balance are above average (positive deviation), then itwill contributes positive sentiment to

exchangerate.Incontrary,forCPI,whenvalueofCPIareaboveaverage(positivedeviation),then

it will contributes negative sentiment to exchange rate. Third step, value of deviation are

summedbasedonweightofeachdata.Specifically,thisstudyweight50:30:20forGDP:CPI:Trade

Balance.Thoseweightingisusedbasedoninvestor’sviewwhichseeGDPgivemoreimpactto

exchange rate than CPI and Trade Balance. Then the value that has been weighted are

transformedtoℎU whichisdividedasfollows:

18

Table4.ℎU value

ℎU is a correction factor of ℎV, as example, if investor predicts exchange rate will

depreciate,sothevalueofℎVis0.8whiledomesticdataisimproved,sothevalueofℎU is-0.2.

Then,ℎ∗,usingequation(3),is0.6.

ProposedBand

1stSimulation

In order to get proposed band, this study conducting two calculation in all observed

countries,using theequation (1)and (2)andusingequation (4)and (2).Themaindifference

between these two groups is the type of probability of currency depreciation using in the

equation.Group1whichconductingcalculationusingequation(1)and(2),usingtheprobability

ofcurrencydepreciationbasedoninvestor’sbeliefwhichwasrepresentedbyℎ.Ontheother

hand,group2conductingcalculationusingequation(4)and(2)usingequation(3)asmodified

currency depreciation factor or ℎ∗. Since, this study would compare the result with simple

BollingerBand,Group1andGroup2usedhighest-lowestexchangerateinpreviousmoving20

WeightedValueofdeviation

ℎU

6 -0,35 -0,24 -0,13 02 0,11 0,2

19

days.Thus,asacontrolgroupthestudycalculatedupperbandandlowerbandusingBollinger

Bandmethodwith20daysmovingaverageinallobservedcountries.

Byplottingtheupperandlowerbandoftheexchangeratetogetherwiththeexchangerate

happened in the observed period, this study found the number of exchange rate happened

outsidetheproposedband.Hence,accordingtotheresults,theproposedbandusingstandard

probabilityofcurrencydepreciationgave thebesteventoferrorsamongotherobservations.

Only Malaysia and Russia gave best result in proposed band using modified probability of

currencydepreciation.

Table5.Resultfrom1stSimulation

2ndSimulation

Second simulation in this study is conducted by the samemethodwith 1st simulation.

However,thissimulationexercisingthreedifferentlengthformovingaverageforBollingerBand

and moving highest-lowest exchange rate for proposed band. There are three groups of

20

observationthatweusedinthisstudy.GroupAusinghighestandlowestexchangerateinthe

last30daysinexercisingproposedband.GroupBusinghighestandlowestexchangerateinthe

previous60daysinexercisingproposedband.Lastly,groupCusinghighestandlowestexchange

rate in theprevious90days inexercisingproposedband.Thus, asa control group the study

calculatedupperbandand lowerbandusingBollingerBandmethodwith30,60and90days

movingaverageinallobservedcountries

Byplottingtheupperandlowerbandoftheexchangeratetogetherwiththeexchangerate

happened in the observed period, this study found the number of exchange rate happened

outsidetheproposedband.Hence,accordingtotheresults,theproposedbandusingstandard

probabilityofcurrencydepreciationgavethebesteventoferrorsamongotherobservations.

Table6.ExchangeRateHappenedOutsideTradingBandin30daysMovingHighestandLowest

ExchangeRate

21

Table7.ExchangeRateHappenedOutsideTradingBandin60daysMovingHighestandLowestExchangeRate

Table8.ExchangeRateHappenedOutsideTradingBandin90daysMovingHighestandLowestExchangeRate

Althoughproposedbandwithunadjustedℎgivebestresult ineventoferror ingeneral,

therearesomecountrieswhichgivedifferent result.MalaysiaandRussiagotworse result in

22

eventoferrorbyusing30daysmovinghighestlowestexchangerate,IndonesiaandRussiagot

worse result in event of error by using 60 days moving highest lowest exchange rate, and

Indonesiagotworseresultineventoferrorbyusing90daysmovinghighestlowestexchange

rate. Moreover, the longer moving highest lowest exchange rate, the better event of error

producedbyproposedband.

However,thereareseveralpointstobeconsideredinthisstudy.Firstly,inimplementing

thisstudy,intensediscussionamongexpertsandcomprehensiveanalysisareneededinorderto

determineconfidencelevelofcurrencymovement(ℎ).Secondly,sinceeverycurrencyhasitsown

sensitivitytorespondeventinthemarket,determinationofℎneedtobeimprovedtomakeitin

linewiththecountriesconditionsinsteadofarbitrarydetermination.Thirdly,intheeventoflow

andstagnantvolatilityinthepastnormalobservationperiod,longerobservationperiodcanbe

appliedinordertodetermineforextradingband.

V. Conclusion

Hence,theexerciseinthepreviouspartbringsustheconclusion:

a. Accordingtothesampleandmethodologyusingbythisstudy,proposedbandproduceslower

percentageoferrorthanexistingtool.

b. Existing tool using historic data while proposed band also adds investor’s market view

component in its calculation. Therefore, proposed band can be used to enhance tools in

forecastingcurrencymovementsinceinvestor’smarketviewcanbeaccommodatedinthis

method.

23

c. Economicviewoftheinvestorbecomesacrucialdeterminantfactorindeterminingtheupper

andlowerbandinproposedband. It isbecausewiththesamedatatheresultsmaydiffer

dependingonthevalueofℎ.

d. The use of longer period in the calculation produces lower number of error. However,

another consequences of longer period is proposed band become wider. Therefore the

determinationofperiodusedinthecalculationbecomeinvestor’sownpreference.

e. ℎ∗shouldgivebetterresultineventoferrorsinceitscomponentsaremoredetails.However,

accordingtotheexercisehaddoneinthisstudy,theexerciseusingℎ∗doesnotshowbetter

result.Itmightbehappenedbecausethisstudyusingsimplificationandarbitrarilymethodin

determiningℎU bysimplificationindeterminingcomponentsandweight.Thus,therespond

given by each countries should be different.While this study using arbitrarilymethod in

determininghg.However,usingtheproperwayofmethodindeterminingℎ∗mightbetime

consuming.

Basedonthelimitationandconclusionofthestudy,furtherresearchneededtoenhance

thisstudyinsomeaspects:

1. Indeterminingthevalueofℎ,especiallyforℎ,andℎVthisstudyusedarbitrarilymethod

insteadofsophisticatedmethod.Therefore,thereisanopportunityforfurtherresearch

indeterminingthevalueofℎ.

2. In determining the value of ℎU, this study used only three economic data as its

components,CPI,GDPandTradeBalance.Moreover,thisstudyusedarbitrarilymethod

inorder todetermineweight for thosecomponentsofℎU.Thisconditionneeds tobe

elaboratedinfurtherresearch.

24

VI. Referrences

1. Bollinger,John.2001.BollingeronBollingerBand.NewYork:McGrawHill.

2. Bollinger,John.1992.UsingBollingerBands.Stock&CommoditiesV.10:2(47-51)

3. Darsono,SitiAstiyah,R.EkiRahman,TriSubandoro2017.PasarValutaAsing:Teoridan

Praktik.Jakarta:BankIndonesia

4. Grimes,Adam.2012.TheArtandScienceofTechnicalAnalysis:MarketStructure,Proce

Action, and Trading Strategies. Wiley Online Library. Retrieved from

http://onlinelibrary.wiley.com/doi/10.1002/9781119202837.app2/pdf

5. Hayden,John.2004.RSI:TheCompleteGuide.Greenville:TradersPressInc.

6. Kuepper, Justin. 2017.What Is Currency Risk? Currency Risk and How toManage It.

Retrieved from https://www.thebalance.com/g00/what-is-currency-

risk1978927?i10c.referrer=https%3A%2F%2Fwww.google.co.id%2F

7. Mishkin,FredericS.2004.TheEconomicsofMoney,BankingandFinancialMarkets.7th

Edition,PearsonAddisonWesley.

8. Ribnikar,Ivan.2004.ExchangeRateRegimesandMonetaryArrangements.

9. Sarno, Lucio and Mark Taylor. 2002. The Economics of Exchange Rates. Cambridge:

CambridgeUniversityPress.

10. Stone, Mark, Herald Anderson and Romain Veyrune. (2008, March). Exchange Rate

Regimes: Fix or Float? Finance and Development, 45 (1) Retrieved from

http://www.imf.org/external/pubs/ft/fandd/2008/03/basics.htm

25

11. ---. Managed exchange rate system over fixed or floating. 2010. Retrieved from

http://www.discusseconomics.com/foreign-exchange/managed-exchange-rate-system-

over-fixed-or-floating/.

12. ----. TechnicalAnalysis - Explained. Zurich, Switzerland:Global TechnicalResearchand

BehavioralFinance-CreditSuisse.

13. ----. Technical Analysis. 2011. Retrieved from

http://www.mrao.cam.ac.uk/~mph/Technical_Analysis.pdf

14. -----.MovingAverageConvergence–Divergence(MACD),TechnicallySpeaking.Retrieved

from https://www.aaii.com/computerized-investing/article/moving-average-

convergence-divergence-macd.pdf