a new chapter: taking a leap of faith -...

TRANSCRIPT

Page | 1 | PHILLIP SECURITIES RESEARCH (SINGAPORE) MCI (P) 022/11/2014 Ref. No.: SG2014_0199

Asia ex-Japan

A NEW CHAPTER: TAKING A LEAP OF FAITH

MACRO | ECONOMY | Equity Market

29 December 2014

Global Macro, Equities, Phillip Securities Research OW = Overweight ; NW = Neutralweight ; UW = Underweight

Present Prior

G3 US LT OW

ST NW

LT OW

ST NW

Fidelity - America

Legg Mason - Clearbridge US Aggressive Grow th

Legg Mason - Royce US Small Cap Opportunity

SPDR S&P500 (SGX) - S27

Lyxor NASDAQ (SGX) - H1Q

iShares Russell 2000 (NYSE Arca) - IWM

Europe NW NW Templeton - European

Schroder - European Equity Alpha

Schroder - ISF European Smaller Companies

DBX Tracker MSCI Europe - IH3

VGK Vanguard European Stock Index

Japan OW OW Aberdeen Japan Equity Fund

Lion Global Japan Grow th Fund

Nikko AM Shenton Japan Fund

DB X-trackers MSCI Japan ETF – LF2 (SGX)

iShares MSCI Japan – EWJ (NYSE/Amex)

WisdomTree Japan Hedged Equity – DXJ

Asia ex-Japan China/HK OW OW Fidelity Greater China

First State Regional China

Schroder Greater China

db x-trackers MSCI China TRN Index 1C

(LG9.SGX)

db x-trackers CSI300 Index ETF 1D (KT4.SGX)

ChinaAMC CSI 300 ETF (3188.HK/83188.HK)

iShares FTSE A50 China (2823.HK)

CSOP FTSE China A50 ETF (2822.HK/82822.HK)

India OW OW Aberdeen - India Opportunities SGD

Fidelity - India Focus A SGD

Lion Global - India Acc SGD

MSCI India (I98.SGX)

DBX India (LG8.SGX)

Indonesia OW OW Aberdeen Indonesia Equity

Fidelity Indonesia A USD

Lyxor Indonesia10US$x@ (P2Q.SGX)

DBXT MSINDO 10US$x@ (KJ7.SGX)

Ishares MSCI Indonesia ETF (EIDO.NYSEARCA)

Market Vectors Indonesia Index ETF

(IDX.NYSEARCA)

Thailand NW NW Fidelity Thailand Fund

Aberdeen Thailand Equity Fund

Lyxor ThaiSET 10US$x@ (P2P.SGX)

Ishares MSCI Thailand Capped ETF

(THD.NYSEARCA)

X DBMSCITHAI (3092.HK)

Malaysia NW NW Lion Global Malaysia Fund

Aberdeen Malaysian Equity Fund

db x-trackers MSCI Malaysia TRN Index 1C

(LG6.SGX)

XIE Shares Malaysia (FTSE BM KLCI) ETF

(3029.HK)

Singapore NW NW DWS Singapore Small/Mid Cap Fund

Nikko AM Singapore Dividend Equity

Amundi Singapore Dividend Grow th Fund

SPDR STI ETF (ES3.SGX)

Nikko AM STI ETF (G3B.SGX)

Source: PSR (as at 16 Dec 2014)

Rating

CountryRegion Unit Trust ETF

Executive Summary Asia ex-Japan (AxJ) markets tumbled across the board in tandem with falls in oil prices,

while Chinese shares fell on profit taking after recent gains. Uncertainties arising from US interest rates normalisation, stalling Europe economy, flagging Japanese economy, geo-political events and the slowdown in the region added fuel to volatility.

The interest rate normalisation is likely to have a negative repercussion on countries with twin deficits, heavily-indebted and high inflation. They may again experience an inevitable painful correction and see their currencies slide as the greenback appreciates gradually, which will in turn increase risks of financial instability.

Nonetheless, markets could benefit from falling energy prices, domestic policy support, the still abundant global liquidity and structural reform agendas.

The plummeting crude oil prices helped to offset inflationary pressures somewhat, as countries embarks on massive deleveraging process to rein in fiscal and/or current account deficit(s) – providing room for central banks to maintain a supportive monetary policy to bolster growth.

Valuation metrics remain supportive, compared with the US and European markets and own history.

In this context, we remain broadly positive on AxJ. However, domestic reform and restructuring agendas will remain the main trigger to the equity market performances.

We maintain OWs on China, India and Indonesia, as reforms are already underway for these economies.

We are NW on Singapore (restructuring bites), Thailand (political uncertainties) and Malaysia (inflationary risks and fluctuations following freefall of oil prices).

Soh Lin Sin (+65 6531 1516)

Page | 2 | PHILLIP SECURITIES RESEARCH (SINGAPORE)

ASIA EX-JAPAN

Overview

Concerns on moderating growth, mounting disinflationary pressures, liquidity crunch Lingering concerns about lull recoveries from G3 and weaker-than-expected high

frequency economic indicators from the two Asian giants: Europe’s renewed downward pressure on inflation, Japan’s surprise recession, China’s cooling property markets continue to weigh on growth, as well as decelerated economic growth in India, cloud the region’s outlook somewhat.

Flagging economic prospects pose challenge to US. However, fall in energy prices coupled with concerted stimulus boost by central banks stoke business and consumer confidence.

Stimulus package from ECB and BOJ, and later joined by China, to counter stagnation and deter disinflation, would continue to provide a globally low-interest-rate environment. However, markets would still be vulnerable to any news on the impending interest rate hike by US.

Strengthening dollar will no doubt have a profound impact on the global economy, and particularly on emerging markets, by raising debt burdens. Countries and companies highly indebted with US dollar denominated loans will face a major setback. Nonetheless, macroprudential policies would lend support to the currencies - “taper tantrum” seen last year would be unlikely to repeat - but likely to remain vulnerable to interest rate hike as US tighten its monetary policy.

Housing market in China remains a drag to the region – but tentative signs of bottoming out. China still trying to iron out the excess capacity.

Exports will benefit from the recovery in the advanced economies and from regional demand, the trend is likely to moderate, reflecting both the high base effect from 2013 and lower commodity prices.

Domestic demand, particularly from public spending would continue to underpin the economy growth of the region, as huge household debt which dampened consumer spending. Impact from government stepped up in public spending are likely to be seen in the final quarter or next year. With holiday seasons around the corner, may see retails sales to improve.

Inflation steadied on the back of low commodity prices and overcapacity despite subsidies rationalization and interest rate hike. But the inflation spike triggered by subsidy rationalization and GST are likely to shave off consumer’s purchasing power and compress corporates margin somewhat.

Falling oil prices: Good or bad?

Despite that stocks markets pulled back in tandem with the oil prices freefall, weighed by energy sector, falling oil prices are beneficial for the region, in two ways: a) Most are net oil importers, except for Malaysia – falling oil prices will improve

trade and current accounts; and b) Fuel prices are highly subsidized in India, Indonesia and Malaysia – falling oil

prices would provide room for the countries to scrap their fuel subsidies system while providing room for fiscal spending and redistribution of wealth.

As softer oil prices lift some pressures off countries with twin deficits and considerably reduce its external vulnerability, we do not expect the same “taper tantrum” to repeat itself when US increases its interest rates.

More intra-trades, partnerships, FDIs within the region

The “noodle-bowl” effect getting more and more complex – Aftermath of the Asia-Pacific Economic Cooperation (APEC) CEO Summit, Association of Southeast Asian Nations (ASEAN) Summit, and G20 Summit, where new free trade agreements and trade initiatives emerged. While the US is promoting the Trans-Pacific Partnership (TPP), a massive free trade agreement including 12 nations but excluding China, Beijing is in a move to garner support for the Free Trade Area of the Asia-Pacific (FTAAP). On the other hand, China and the 10-member ASEAN have dubbed the next 10 years a

Page | 3 | PHILLIP SECURITIES RESEARCH (SINGAPORE)

ASIA EX-JAPAN

“Diamond Decade”, which both sides hope will feature more practical cooperation and regional economic integration. Strategic partnership within the region should deepen market-driven economic integration as well as to consolidate regional integration. These initiatives also indicated China’s determination to further open up and implying more business and investment opportunities are on the way.

New funding channels for infrastructure projects – The Asian Infrastructure Investment Bank (“AIIB”), spearheaded by China, will start with $50 billion in capital to fill the massive infrastructure funding gap in Asia. The AIIB can not only channel more resources (by lending money to build roads, mobile phone towers and other forms of infrastructure) toward developing countries; it can do so in a way that is better suited to their needs, with fewer bureaucratic barriers and more flexibility than its more established counterparts. The "Marine Silk Road Bank" will fund development of the "New Silk Road" to revive intercontinental land routes and maritime links through central Asia. The New Silk Road would drive more fund inflows into infrastructure investments, speed up industrial and financial cooperation and "break the connectivity bottleneck" within the region. It would also open up the region for new exports markets.

Singapore planting its flag in the heart of India – International Enterprise (IE) Singapore will partner the Andhra Pradesh state government in India to build the southern state a brand new capital which bodes well for bilateral ties. The project will pool land for the building of its new capital, hoping that the 8 sq km core district, which will include government offices, residential complexes and schools, would be developed before 2019 with Singapore's help.

In short, AxJ markets continue to be dominated by the 3 “R”s: Reform, Restructuring and Rebalance, where we will continue to see growth moderates in near-medium term. Global liquidity remains abundant and will continue to be so in 2015, given the collective action to support growth and to ward off deflation.

Page | 4 | PHILLIP SECURITIES RESEARCH (SINGAPORE)

ASIA EX-JAPAN

Equity Markets

MSCI AxJ (OW) MSCI Asia ex-Japan Still in an uptrend, albeit volatile. Most emerging market countries have taken actions to reduce their domestic and external imbalances – fundamentals improved to ride through the global interest rate hike. However, the normalization of US monetary policy is still likely to increase volatility in the short-term. Market could benefit from falling energy prices, domestic policy support, the still abundant global liquidity and structural reform agendas.

AxJ Bond Yields (10Yr-2Yr Yield Spread) Chinese bonds yield spread surged as investors demand a higher premium arising from higher default risk in bonds, trust products and other wealth management investments. Authorities’ recent move to ban local bonds rated lower than AAA to be used as collateral for short-term loans adds on to investor concerns on such fallouts.

Asia Dollar Index With MYR being the worst performing currency year-to-date within the region as oil prices dropped.

Page | 5 | PHILLIP SECURITIES RESEARCH (SINGAPORE)

ASIA EX-JAPAN

PMI (Private) Heat Map Name Nov-2014 Oct-2014 Sep-2014 Aug-2014 Jul-2014 Jun-2014 May-2014 Apr-2014 Mar-2014 Feb-2014 Jan-2014 Dec-2013 Nov-2013

JPMorgan Global Composite PMI SA 53.2 53.5 54.8 55.1 55.5 55.4 54.2 52.8 53.5 53.1 54.0 53.8 54.0

JPMorgan Global Manufacturing PMI SA 51.8 52.2 52.2 52.5 52.4 52.6 52.1 51.9 52.4 53.2 53.0 52.9 52.9

JPMorgan Global Services PMI SA 53.5 53.6 55.2 55.6 56.1 55.8 54.5 52.7 53.5 52.7 53.8 53.5 53.8

Markit Developed Markets Composite PMI SA 53.9 54.2 55.6 56.0 56.7 56.4 55.3 53.5 54.4 53.8 54.8 54.5 54.6

Markit Developed Markets Manufacturing PMI SA 52.6 53.3 53.4 53.8 53.2 54.0 53.5 53.4 54.2 55.3 54.4 54.2 54.0

Markit Developed Markets Services PMI Business Activity SA 54.0 54.2 55.8 56.2 57.1 56.5 55.3 53.2 54.1 53.0 54.5 54.0 54.2

HSBC Emerging Markets Composite PMI SA 51.2 51.5 52.5 52.4 51.7 52.3 50.7 50.4 50.3 51.1 51.4 51.6 52.1

HSBC Emerging Markets Manufacturing PMI SA 50.9 50.9 50.7 51.0 51.4 50.8 50.4 49.8 49.8 50.3 50.9 51.1 51.3

HSBC Emerging Markets Services PMI SA 51.2 51.5 53.2 52.6 51.2 52.9 50.6 50.7 50.7 51.2 50.9 51.2 51.9

HSBC China Composite PMI Output SA 51.1 51.7 52.3 52.8 51.6 52.4 50.2 49.5 49.3 49.8 50.8 51.2 52.3

HSBC China Manufacturing PMI SA 50.0 50.4 50.2 50.2 51.7 50.7 49.4 48.1 48.0 48.5 49.5 50.5 50.8

HSBC China Services PMI Business Activity SA 53.0 52.9 53.5 54.1 50.0 53.1 50.7 51.4 51.9 51.0 50.7 50.9 52.5

HSBC Hong Kong PMI SA 48.8 47.7 49.8 49.6 50.4 50.1 49.1 49.7 49.9 53.3 52.7 51.2 52.1

HSBC India Composite PMI SA 53.6 51.0 51.8 51.6 53.0 53.8 50.7 49.5 48.9 50.3 49.6 48.1 48.5

HSBC India Manufacturing PMI SA 53.3 51.6 51.0 52.4 53.0 51.5 51.4 51.3 51.3 52.5 51.4 50.7 51.3

HSBC India Services PMI SA 52.6 50.0 51.6 50.6 52.2 54.4 50.2 48.5 47.5 48.8 48.3 46.7 47.2

HSBC Indonesia Manufacturing PMI SA 48.0 49.2 50.7 49.5 52.7 52.7 52.4 51.1 50.1 50.5 51.0 50.9 50.3

Singapore Purchasing Manager Index Manufacturing 51.8 51.9 50.5 49.7 51.5 50.5 50.8 51.1 50.8 50.9 50.5 49.7 50.8* HSBC/Markit Survey and Singapore Insti tute of Purchas ing & Materia ls Management (SIPMM), as of 16 Dec 2014

Source: Bloomberg Source: Bloomberg, CEIC, Phillip Securities Research (Singapore) Estimates

China (OW)

While property markets cool down, deleveraging and reforms raised risks to growth in the short-term, it also sparked speculation on more stimulus measures to bolster growth. Alongside stimulus hope, the positive sentiment on reforms (Shanghai Hong-Kong Stock Connect, interest rates and currency liberalization, fiscal reforms) and low valuation metrics would continue to support Chinese stocks. Key Market and Macro Data

FY11 FY12 FY13 FY14F Avg

EPS %y-y (SHCOMP) 22.00 0.10 4.40 15.43 18.70

P/E , year avg (SHCOMP) 14.44 12.00 11.35 13.44 19.84

USD:Local Currency, year avg 6.46 6.31 6.15 6.12 7.50

Real GDP %y-y 9.35 7.71 7.68 7.40 9.44

Inflation %y-y 5.41 2.62 2.64 2.10 5.78

Pol icy Rate, year avg 6.35 6.26 6.00 5.60 7.46

Budget % GDP -1.80 -1.54 -1.86 -2.10 -2.58

C % GDP 35.75 36.00 36.17 - 39.73

G % GDP 13.36 13.49 13.63 - 14.17

GFCF % GDP 48.31 47.75 47.79 - 42.10

X % GDP 25.89 24.87 23.86 - 26.05

M % GDP -23.74 -22.05 -21.04 - -22.67

CA % GDP 1.86 2.61 1.97 2.30 5.18

Total Govt. Debt % GDP 36.50 38.11 40.60 - 34.01

External Debt % GDP 9.49 8.96 9.34 - 11.60

Total Debt % GDP - - - - -

Remarks :

(1) PSR estimates are ca lculated based on ca lendar year, not fi sca l year of respective country

Source: Bloomberg, CEIC, PSR est.

* “-“ impl ies no information avai lable

Page | 6 | PHILLIP SECURITIES RESEARCH (SINGAPORE)

ASIA EX-JAPAN

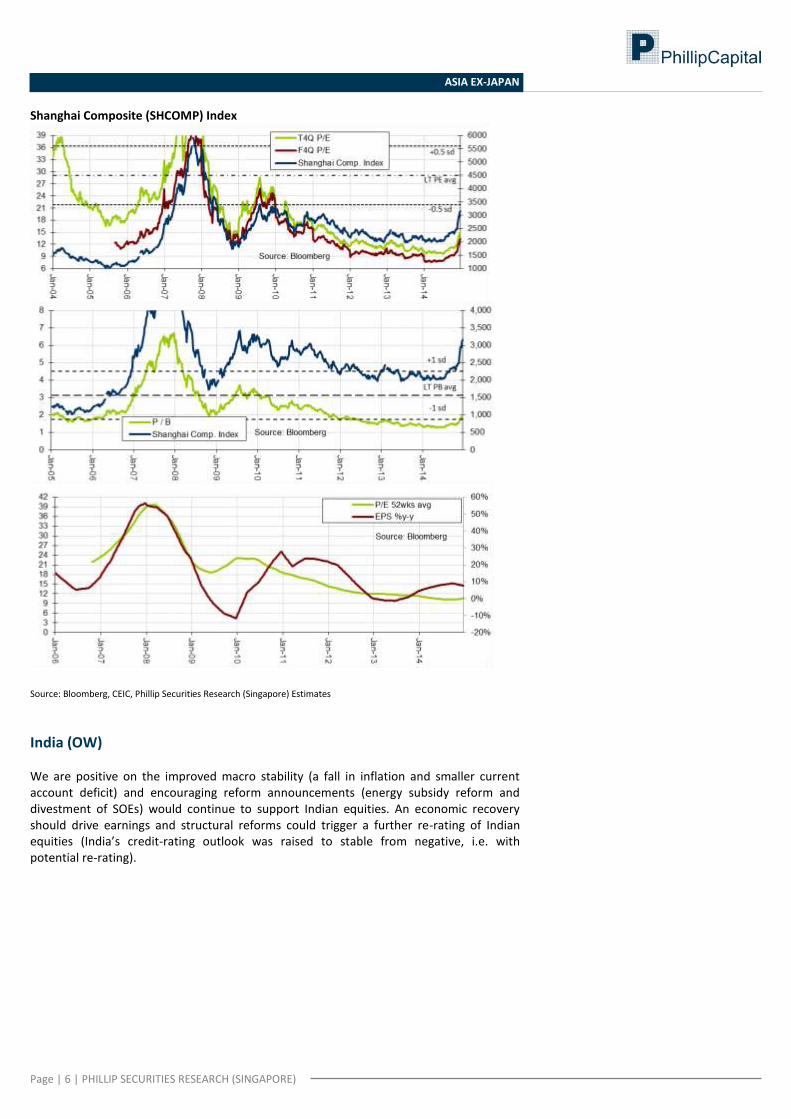

Shanghai Composite (SHCOMP) Index

Source: Bloomberg, CEIC, Phillip Securities Research (Singapore) Estimates

India (OW)

We are positive on the improved macro stability (a fall in inflation and smaller current account deficit) and encouraging reform announcements (energy subsidy reform and divestment of SOEs) would continue to support Indian equities. An economic recovery should drive earnings and structural reforms could trigger a further re-rating of Indian equities (India’s credit-rating outlook was raised to stable from negative, i.e. with potential re-rating).

Page | 7 | PHILLIP SECURITIES RESEARCH (SINGAPORE)

ASIA EX-JAPAN

Key Market and Macro Data

FY11 FY12 FY13 FY14F Avg

EPS %y-y (SENSEX) 24.20 7.90 1.00 23.16 16.20

P/E , year avg (SENSEX) 16.85 15.40 17.06 17.56 17.52

USD:Local Currency, year avg 46.69 53.35 58.59 61.80 47.23

Real GDP %y-y 7.67 4.81 4.70 5.50 7.52

Inflation %y-y - 9.69 10.07 7.00 9.57

Pol icy Rate, year avg 7.58 8.13 7.52 8.00 7.02

Budget % GDP -7.18 -5.92 -5.89 -4.20 -5.08

C % GDP 61.10 61.40 61.36 - 61.85

G % GDP 12.20 12.65 12.94 - 12.09

GFCF % GDP 33.92 32.75 31.26 - 33.34

X % GDP 25.21 26.12 26.50 - 23.71

M % GDP -31.22 -33.31 -31.37 - -28.45

CA % GDP -3.36 -4.97 -2.61 -2.00 -3.28

Total Govt. Debt % GDP 49.23 51.30 51.67 - 53.36

External Debt % GDP 18.45 21.40 22.67 - 19.06

Total Debt % GDP - - - - -

(2) Bloomberg's India Forecasts are based on fi sca l year (2014 = FY14/15, 2015 = FY15/16)

Source: Bloomberg, CEIC, PSR est.

* “-“ impl ies no information avai lable

Remarks :

(1) PSR estimates are ca lculated based on ca lendar year, not fi sca l year of respective country

SENSEX Index

Source: Bloomberg, CEIC, Phillip Securities Research (Singapore) Estimates

Indonesia (OW)

For Indonesia, on hope for structural reform, but President Joko Widodo (a.k.a. “Jokowi”) will face challenges from a parliament controlled by the opposition. The promising first move from the new president – subsidized fuel prices hike – in mid Nov aimed to curb the twin deficits and thus provide room for his reform agendas. However, the positive impact arising from the subsidy cuts would need some time to realise (if the savings are put into good use, e.g. infrastructure projects). Indonesia remains vulnerable with sub-par growth and twin deficits.

Page | 8 | PHILLIP SECURITIES RESEARCH (SINGAPORE)

ASIA EX-JAPAN

Key Market and Macro Data

FY11 FY12 FY13 FY14F Avg

EPS %y-y (JCI) 21.60 6.50 5.50 37.71 10.70

P/E , year avg (JCI) 18.30 18.87 19.99 17.43 19.37

USD:Local Currency, year avg 8,773.25 9,381.00 10,420.00 12,200.00 8,427.00

Real GDP %y-y 6.49 6.26 5.78 5.10 5.47

Inflation %y-y 5.37 3.98 6.40 6.30 6.06

Pol icy Rate, year avg 6.58 5.77 6.48 7.75 7.42

Budget % GDP -1.14 -1.86 -2.33 -2.40 -1.21

C % GDP 55.60 55.10 54.80 - 57.60

G % GDP 8.20 7.80 7.80 - 7.90

GFCF % GDP 24.30 25.10 24.90 - 23.00

X % GDP 49.60 47.60 47.40 - 45.40

M % GDP -38.20 -38.40 -36.70 - -35.50

CA % GDP 0.20 -2.78 -3.34 -3.00 0.38

Total Govt. Debt % GDP 23.58 23.32 22.38 - 25.51

External Debt % GDP 26.65 28.78 30.53 - 35.42

Total Debt % GDP - - - - -

Source: Bloomberg, CEIC, PSR est.

* “-“ impl ies no information avai lable

Remarks :

(1) PSR estimates are ca lculated based on ca lendar year, not fi sca l year of respective country Jakarta Composite Index (JCI)

Source: Bloomberg, CEIC, Phillip Securities Research (Singapore) Estimates

Thailand (NW)

Sentiments improved as Thailand avoided a technical recession. Despite a lackluster rebound in 3Q14, recovery set to gain momentum in the coming quarters, as fiscal stimulus and other economic measures kick in while the dust settles following the political crisis that ended with a military coup in late May. Infrastructure spending would be the main driver of the economy as low prices of rubber and rice (Thailand’s main agricultural export products) and high levels of household debt hurt Thai’s purchasing power. Political risks lingers as there is no conclusion yet on political reforms.

Page | 9 | PHILLIP SECURITIES RESEARCH (SINGAPORE)

ASIA EX-JAPAN

Key Market and Macro Data

FY11 FY12 FY13 FY14F Avg

EPS %y-y (SET) 30.00 -9.80 18.30 5.05 14.13

P/E , year avg (SET) 12.62 16.49 16.80 15.71 14.17

USD:Local Currency, year avg 30.50 31.05 30.74 32.80 35.33

Real GDP %y-y 0.08 6.49 2.89 0.80 3.92

Inflation %y-y 3.81 3.01 2.19 2.00 2.73

Pol icy Rate, year avg 2.98 2.94 2.54 1.85 2.54

Budget % GDP -1.83 -3.66 -3.16 -2.80 -1.83

C % GDP 54.49 55.33 54.42 - 55.43

G % GDP 13.26 13.58 13.81 - 12.45

GFCF % GDP 26.27 28.53 26.73 - 26.32

X % GDP 76.94 74.98 73.57 - 72.36

M % GDP -72.41 -73.85 -70.28 - -67.52

CA % GDP 2.63 -0.40 -0.54 2.50 2.37

Total Govt. Debt % GDP 40.78 43.61 45.80 - 43.94

External Debt % GDP 30.78 36.35 36.62 - 35.66

Total Debt % GDP - - - - -

Remarks :

(1) PSR estimates are ca lculated based on ca lendar year, not fi sca l year of respective country

Source: Bloomberg, CEIC, PSR est.

* “-“ impl ies no information avai lable

Stocks Exchange of Thailand (SET) Index

Source: Bloomberg, CEIC, Phillip Securities Research (Singapore) Estimates

Malaysia (NW)

Concerns following the plummeting oil prices and a decline in palm oil weakened the currency, as well as pose downside risks on trades, government revenue, and GDP. Inflationary risk mounting as the authorities raised gasoline prices twice within 13 months and scrapped the fuel subsidy regimes since Dec. 1, notwithstanding the impending GST which will start in Apr’15. However, investment activity will remain robust, domestic demand will remain the key driver of growth, while abolishing the subsidy regimes will improve fiscal balance. Fundamentals remain strong to weather the storm.

Page | 10 | PHILLIP SECURITIES RESEARCH (SINGAPORE)

ASIA EX-JAPAN

Key Market and Macro Data

FY11 FY12 FY13 FY14F Avg

EPS %y-y (KLCI) 17.20 12.30 3.70 0.23 11.20

P/E , year avg (KLCI) 16.38 15.54 16.29 16.60 15.69

USD:Local Currency, year avg 3.06 3.09 3.15 3.31 3.40

Real GDP %y-y 5.19 5.64 4.74 5.80 4.77

Inflation %y-y 3.17 1.66 2.11 3.20 2.51

Pol icy Rate, year avg 2.92 3.00 3.00 3.25 2.95

Budget % GDP -4.80 -4.45 -3.91 -3.50 -4.49

C % GDP 49.64 50.85 52.03 - 48.66

G % GDP 13.29 13.20 13.40 - 12.36

GFCF % GDP 24.10 27.45 27.48 - 24.31

X % GDP 100.30 93.20 89.54 - 101.89

M % GDP -87.33 -84.70 -82.45 - -87.22

CA % GDP 11.57 5.78 4.04 5.20 11.87

Total Govt. Debt % GDP 51.52 53.25 54.71 - 47.83

External Debt % GDP 29.07 26.83 32.24 - 30.71

Total Debt % GDP - - - - -

Source: Bloomberg, CEIC, PSR est.

* “-“ impl ies no information avai lable

Remarks :

(1) PSR estimates are ca lculated based on ca lendar year, not fi sca l year of respective country Kuala Lumpur Composite Index (KLCI)

Source: Bloomberg, CEIC, Phillip Securities Research (Singapore) Estimates

Singapore (NW)

Singapore, a small and open economy, is vulnerable to external shocks, reflecting more the state of global economy and less of that of domestic economy. The economy is expected to grow moderately as the government embarks on restructuring. Eternally-oriented sectors are likely to provide support to growth in tandem with the expected pick-up in external demand although the expansion would likely to be modest in line with a slow and uneven recovery in the global economy. Meanwhile domestically-oriented sectors are expected to remain resilient although labour-intensive ones may see their growth weighed down by labour constraints.

Page | 11 | PHILLIP SECURITIES RESEARCH (SINGAPORE)

ASIA EX-JAPAN

Key Market and Macro Data

FY11 FY12 FY13 FY14F Avg

EPS %y-y (STI) 37.68 -15.83 -13.20 -0.80 16.94

P/E , year avg (STI) 8.99 10.71 13.24 14.61 13.15

USD:Local Currency, year avg 1.26 1.25 1.25 1.29 1.52

Real GDP %y-y 6.06 2.50 3.85 3.00 6.12

Inflation %y-y 5.25 4.58 2.36 1.30 2.74

Pol icy Rate, year avg 0.41 0.38 0.40 - 1.24

Budget % GDP 1.23 2.00 1.30 0.50 1.66

C % GDP 34.92 35.41 34.98 - 38.19

G % GDP 9.50 9.26 9.80 - 10.11

GFCF % GDP 25.69 27.29 25.76 - 25.31

X % GDP 196.45 194.49 194.07 - 198.26

M % GDP -168.13 -169.18 -167.99 - -172.64

CA % GDP 23.29 17.61 18.70 18.30 22.16

Gross Govt. Debt % GDP* 103.55 109.86 107.27 - 95.27

Officia l Reserve Assets % GDP 87.18 91.12 92.29 - 170.07

External Debt % GDP 433.00 424.50 447.10 - 494.10

Total Debt % GDP - - - - -

(2) Singapore's Budget i s based on the primary surplus/defici t, i .e. surplus/defici t before

Specia l Transfers and Net Investment Returns Contribution

Source: Bloomberg, CEIC, PSR est.

* “-“ impl ies no information avai lable

Remarks :

(1) PSR estimates are ca lculated based on ca lendar year, not fi sca l year of respective country

(3) Based on Net Investment Returns Contribution, the Singapore government i s in a net

financia l assets pos i tion. Straits Times Index (STI)

Source: Bloomberg, CEIC, Phillip Securities Research (Singapore) Estimates

Page | 12 | PHILLIP SECURITIES RESEARCH (SINGAPORE)

ASIA EX-JAPAN

Contact Information (Singapore Research Team) Management Chan Wai Chee (CEO, Research - Special Opportunities)

+65 6531 1231 Research Operations Officer Jaelyn Chin +65 6531 1240

Joshua Tan (Head, Research - Equities & Macro)

+65 6531 1249

Macro | Equities Market Analyst | Equities US Equities Soh Lin Sin +65 6531 1516 Kenneth Koh +65 6531 1791 Wong Yong Kai +65 6531 1685 Bakhteyar Osama +65 6531 1793 Finance | Offshore Marine Real Estate Benjamin Ong +65 6531 1535 Caroline Tay +65 6531 1792 Telecoms | Technology Transport & Logistics Colin Tan +65 6531 1221 Richard Leow, CFTe +65 6531 1735

Contact Information (Regional Member Companies) SINGAPORE

Phillip Securities Pte Ltd Raffles City Tower

250, North Bridge Road #06-00 Singapore 179101 Tel +65 6533 6001 Fax +65 6535 6631

Website: www.poems.com.sg

MALAYSIA Phillip Capital Management Sdn Bhd

B-3-6 Block B Level 3 Megan Avenue II, No. 12, Jalan Yap Kwan Seng, 50450

Kuala Lumpur Tel +603 2162 8841 Fax +603 2166 5099

Website: www.poems.com.my

HONG KONG Phillip Securities (HK) Ltd

11/F United Centre 95 Queensway Hong Kong

Tel +852 2277 6600 Fax +852 2868 5307

Websites: www.phillip.com.hk

JAPAN

Phillip Securities Japan, Ltd. 4-2 Nihonbashi Kabuto-cho Chuo-ku,

Tokyo 103-0026 Tel +81-3 3666 2101 Fax +81-3 3666 6090

Website: www.phillip.co.jp

INDONESIA PT Phillip Securities Indonesia

ANZ Tower Level 23B, Jl Jend Sudirman Kav 33A Jakarta 10220 – Indonesia

Tel +62-21 5790 0800 Fax +62-21 5790 0809

Website: www.phillip.co.id

CHINA Phillip Financial Advisory (Shanghai) Co Ltd

No 550 Yan An East Road, Ocean Tower Unit 2318,

Postal code 200001 Tel +86-21 5169 9200 Fax +86-21 6351 2940

Website: www.phillip.com.cn

THAILAND Phillip Securities (Thailand) Public Co. Ltd

15th Floor, Vorawat Building, 849 Silom Road, Silom, Bangrak,

Bangkok 10500 Thailand Tel +66-2 6351700 / 22680999

Fax +66-2 22680921 Website www.phillip.co.th

FRANCE King & Shaxson Capital Limited

3rd Floor, 35 Rue de la Bienfaisance 75008 Paris France

Tel +33-1 45633100 Fax +33-1 45636017

Website: www.kingandshaxson.com

UNITED KINGDOM King & Shaxson Capital Limited

6th Floor, Candlewick House, 120 Cannon Street, London, EC4N 6AS

Tel +44-20 7426 5950 Fax +44-20 7626 1757

Website: www.kingandshaxson.com

UNITED STATES Phillip Futures Inc

141 W Jackson Blvd Ste 3050 The Chicago Board of Trade Building

Chicago, IL 60604 USA Tel +1-312 356 9000 Fax +1-312 356 9005

Website: www.phillipusa.com

AUSTRALIA Phillip Capital Limited

Level 12, 15 William Street, Melbourne, Victoria 3000, Australia

Tel +61-03 9629 8288 Fax +61-03 9629 8882

Website: www.phillipcapital.com.au

SRI LANKA Asha Phillip Securities Limited

No-10 Prince Alfred Tower, Alfred House Gardens, Colombo 03, Sri Lanka Tel: (94) 11 2429 100 Fax: (94) 11 2429 199

Website: www.ashaphillip.net

INDIA PhillipCapital (India) Private Limited

No.1, 18th Floor Urmi Estate

95, Ganpatrao Kadam Marg Lower Parel West, Mumbai 400-013

Maharashtra, India Tel: +91-22-2300 2999 / Fax: +91-22-2300 2969

Website: www.phillipcapital.in

TURKEY PhillipCapital Menkul Degerler

Dr. Cemil Bengü Cad. Hak Is Merkezi No. 2 Kat. 6A Caglayan 34403 Istanbul, Turkey

Tel: 0212 296 84 84 Fax: 0212 233 69 29

Website: www.phillipcapital.com.tr

DUBAI Phillip Futures DMCC

Member of the Dubai Gold and Commodities Exchange (DGCX)

Unit No 601, Plot No 58, White Crown Bldg, Sheikh Zayed Road, P.O.Box 212291

Dubai-UAE Tel: +971-4-3325052 / Fax: + 971-4-3328895

Website: www.phillipcapital.in

Page | 13 | PHILLIP SECURITIES RESEARCH (SINGAPORE)

ASIA EX-JAPAN

Important Information

This publication is prepared by Phillip Securities Research Pte Ltd., 250 North Bridge Road, #06-00, Raffles City Tower, Singapore 179101 (Registration Number: 198803136N), which is regulated by the Monetary Authority of Singapore (“Phillip Securities Research”). By receiving or reading this publication, you agree to be bound by the terms and limitations set out below. This publication has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this document by mistake, please delete or destroy it, and notify the sender immediately. Phillip Securities Research shall not be liable for any direct or consequential loss arising from any use of material contained in this publication.

The information contained in this publication has been obtained from public sources, which Phillip Securities Research has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this publication are based on such information and are expressions of belief of the individual author or the indicated source (as applicable) only. Phillip Securities Research has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete, appropriate or verified or should be relied upon as such. Any such information or Research contained in this publication is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, (i) be liable in any manner whatsoever for any consequences (including but not limited to any special, direct, indirect, incidental or consequential losses, loss of profits and damages) of any reliance or usage of this publication or (ii) accept any legal responsibility from any person who receives this publication, even if it has been advised of the possibility of such damages. You must make the final investment decision and accept all responsibility for your investment decision, including, but not limited to your reliance on the information, data and/or other materials presented in this publication.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this material are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this publication is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This publication should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this publication has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this material is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this publication involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks. Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this research should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this publication, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this publication.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold a interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this publication. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, which is not reflected in this material, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this material.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction. Section 27 of the Financial Advisers Act (Cap. 110) of Singapore and the MAS Notice on Recommendations on Investment Products (FAA-N01) do not apply in respect of this publication.

This material is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this material may not be suitable for all investors and a person receiving or reading this material should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

Please contact Phillip Securities Research at [65 65311240] in respect of any matters arising from, or in connection with, this document. This report is only for the purpose of distribution in Singapore.