a new cummins investor presentation - iis windows...

TRANSCRIPT

A New Cummins

Investor Presentation

November 2006

2

Disclosure Regarding Forward-Looking Statements & non-GAAP Financial Measures

This presentation contains certain forward-looking information. Any forward-looking statement involves risk and uncertainty. The Company’s future results may be affected by changes in general economic conditions and by the actions of customers and competitors. Actual outcomes may differ materially from what is expressed in any forward-looking statement. A more complete disclosure about forward-looking statements begins on page 60 of our 2005 Form 10-K, and it applies to this presentation.

This presentation contains certain non-GAAP financial measures such as earnings before interest and taxes (EBIT). Please refer to our website (www.cummins.com) for the reconciliation of EBIT to GAAP financial measures.

3

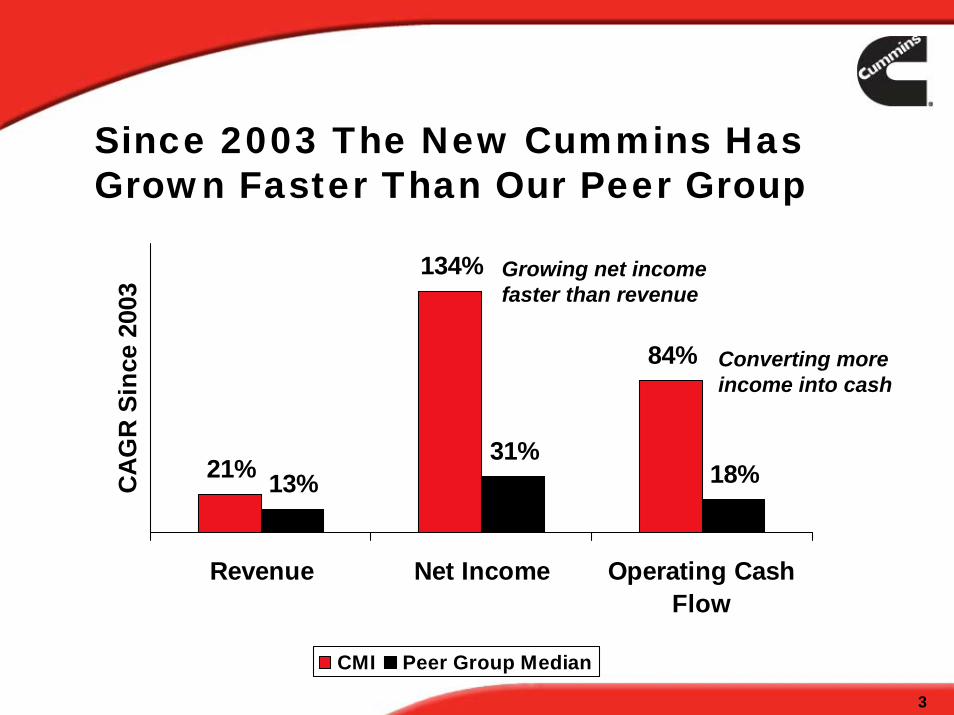

Since 2003 The New Cummins Has Grown Faster Than Our Peer Group

21%

134%

84%

13%31%

18%

Revenue Net Income Operating CashFlow

CA

GR

Sin

ce 2

003

CMI Peer Group Median

Growing net income faster than revenue

Converting more income into cash

4

Excess Return (ROIC- WACC)

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

1999 2000 2001 2002 2003 2004 2005 Q306LTM

The New Cummins is Creating Greater Value Than Ever Before

Creating Shareholder

Value

5

2007 Creates Investment Opportunity

We have fundamentally changed our business2007 emission downturn is a known, predictable, finite eventWe are confident in our ability to perform in 2007 and beyond

6

The New Cummins

Diversified to mitigate the cyclicality of our end markets

Building greater stability in earnings

Focused cash management strategy

Virtually integrating through OEM partnerships

Global technology leader in constantly changing emissions environment

7

Diversified Global Power Leader

Four Complementary Businesses

Engines PowerGeneration

Components Distribution

8

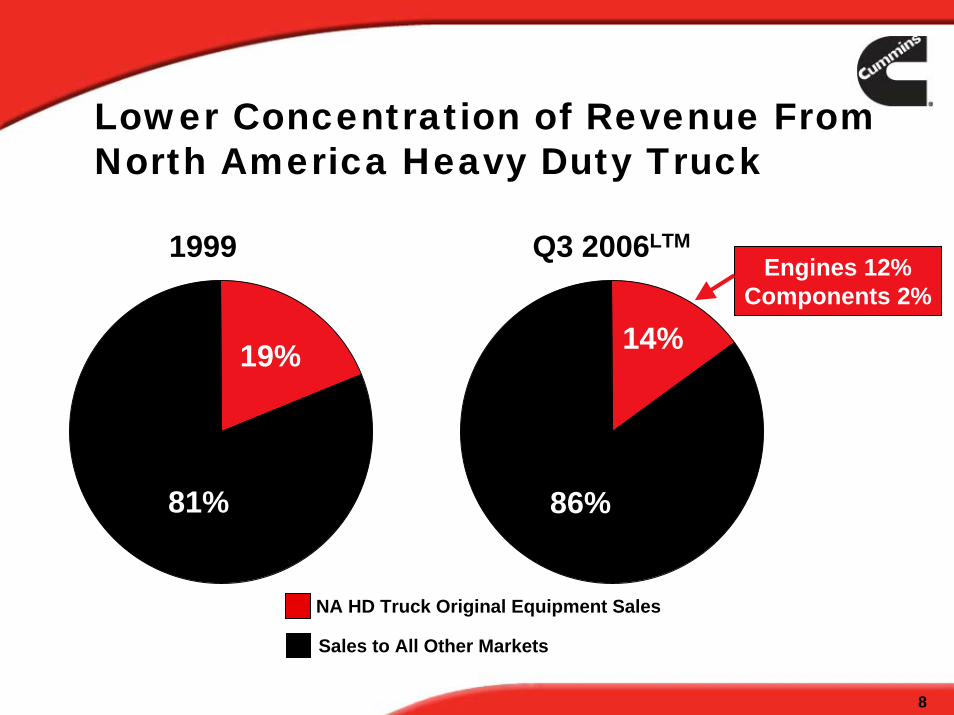

NA HD Truck Original Equipment Sales

Sales to All Other Markets

1999 Q3 2006LTM

86%

14%

Engines 12%Components 2%

19%

81%

Lower Concentration of Revenue From North America Heavy Duty Truck

9

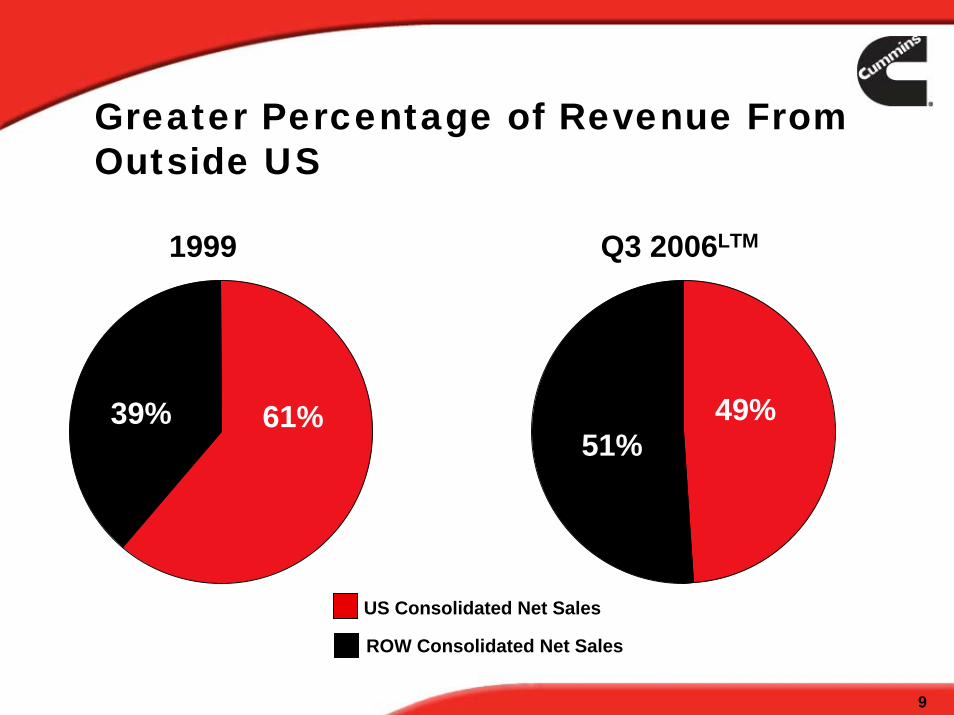

US Consolidated Net Sales

ROW Consolidated Net Sales

1999 Q3 2006LTM

51%49%61%39%

Greater Percentage of Revenue From Outside US

10

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

2000 2001 2002 2003 2004 2005

`

$0

$200

$400

$600

$800

$1,000

$1,200

2000 2001 2002 2003 2004 2005

Consolidated Net Sales

Unconsolidated JV Net Sales

Capitalizing on Established Position in Emerging Markets

China

US$

Mill

ions

18% CAGR

India

27% CAGR

11

Growing Stable Diversified Earnings

EBIT

$0

$250

$500

$750

$1,000

$1,250

1999* Q3 '06

US$

Mill

ions

Stable Cyclical

Larger contributor to total EBITLess cyclicalGrowth demonstrates return on investment

Distribution ChannelEmerging MarketsAftermarket

*

LTM

$306M

$1,145M

* Excludes restructuring charges

12

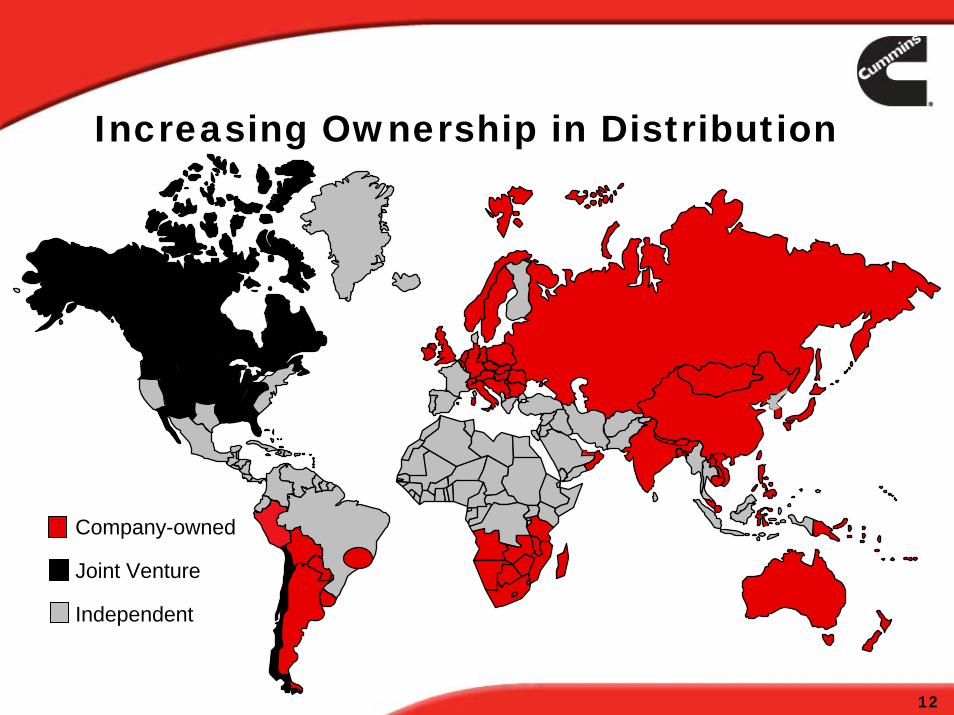

Company-owned

Joint Venture

Independent

Increasing Ownership in Distribution

13

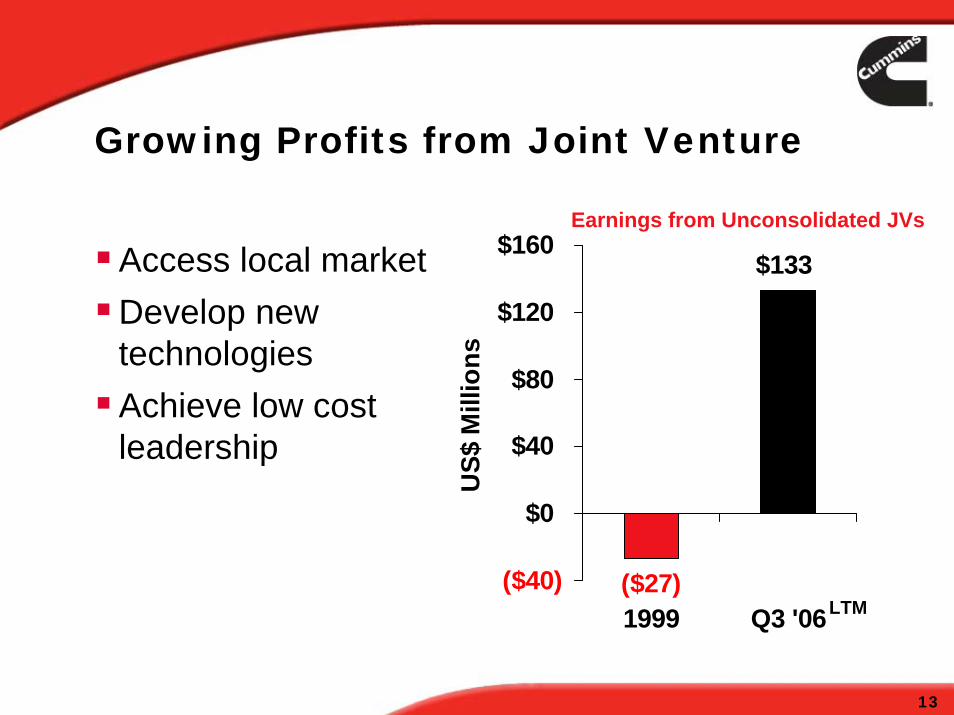

Growing Profits from Joint Venture

Access local marketDevelop new technologiesAchieve low cost leadership

($27)

$133

($40)

$0

$40

$80

$120

$160

1999 Q3 '06

US$

Mill

ions

LTM

Earnings from Unconsolidated JVs

14

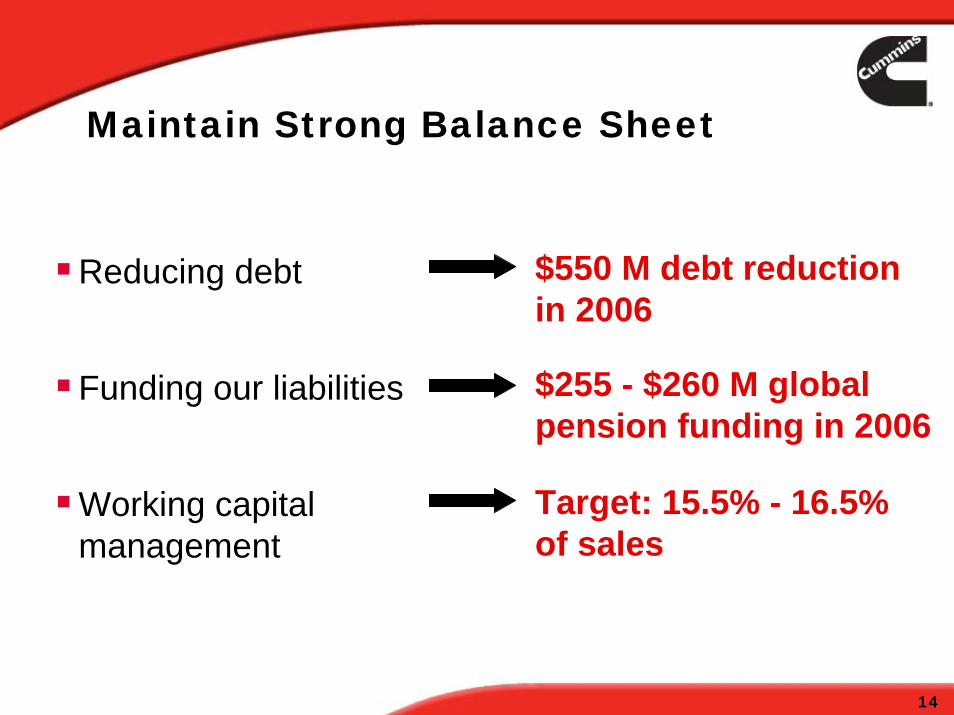

Reducing debt

Funding our liabilities

Working capital management

Maintain Strong Balance Sheet

$550 M debt reductionin 2006

$255 - $260 M global pension funding in 2006

Target: 15.5% - 16.5%of sales

15

Investing in Profitable Growth

New light-duty diesel in North America

New 13-liter engine – Dongfeng

11-liter engine – Shaanxi

New 2.8 to 3.8-liter engine – Foton

New product introductions for Components

Increased capacity

16

Focusing Capital on Returns

0%

1%

2%

3%

4%

5%

6%

7%

8%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Q3'06

Cap

ex/R

even

ue (%

)

-5%

0%

5%

10%

15%

20%

25%

30%

35%

RO

AN

A (%

)

ROANA Capex/Revenue

Reducing capex as % of revenue

Increasing ROANA

17

Returning Value to Our Shareholders

Dividends

Share repurchase

Total shareholder return

$158

$614

$760

$988

$0

$200

$400

$600

$800

$1,000

$1,200

2003 2004 2005 Q3 '06LTM

US$

Mill

ions

Operating Cash Flow

18

Virtually Integrating Through OEM Partnerships

Cost

Brand

Global presence

Technology

Strong partnerships

19

Fuel Systems

Electronic Controls

Air Handling Systems

Filtration and Aftertreatment

Combustion Technologies

Unique Technology Integration

20

Technology Leadership Creates Advantage in 2007

Building on current product architectureComparable fuel economyField tests with end-users receiving very positive feedbackEPA certification in process for MR and HD platformsWell positioned to grow on-highway market share significantly in 2007

21

Improved Power-Generation

Business

Improved Power-Generation

Business Global

Engine BusinessGlobal

Engine Business

Strong GlobalDistribution

Network

Strong GlobalDistribution

Network

This is the New Cummins

Growing KeyTechnologies in

Components

Growing KeyTechnologies in

Components

Appendix

23

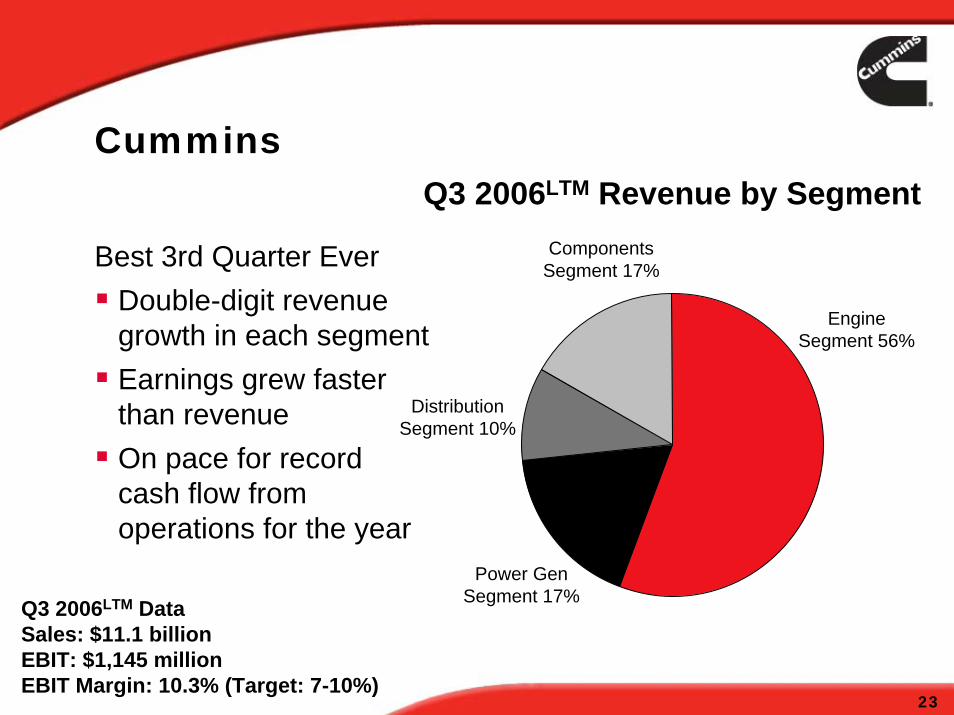

Cummins

Best 3rd Quarter EverDouble-digit revenue growth in each segmentEarnings grew faster than revenueOn pace for record cash flow from operations for the year

ComponentsSegment 17%

EngineSegment 56%

Power GenSegment 17%

DistributionSegment 10%

Q3 2006LTM DataSales: $11.1 billionEBIT: $1,145 millionEBIT Margin: 10.3% (Target: 7-10%)

Q3 2006LTM Revenue by Segment

24

Cummins

Mexico/Latin America

9%

Africa/Middle East5%Canada

7%

United States49%

Asia/Australia16%

Europe/CIS14%

Q3 2006LTM Revenue by Marketing Territory

International revenue continues to be above 50%Pre-emission demand has accelerated US growth rateMost international areas growing at double digit rateSofter demand in China and SE Asia

25

Cummins – Historical Performance

$139$181

$543

$907

$1,145

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

2002 2003 2004 2005 Q3 '06

$ M$5,853

$6,296

$8,438

$9,918

$11,082

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

2002 2003 2004 2005 Q3 '06

$ M

EBITSales

LTM LTM

26

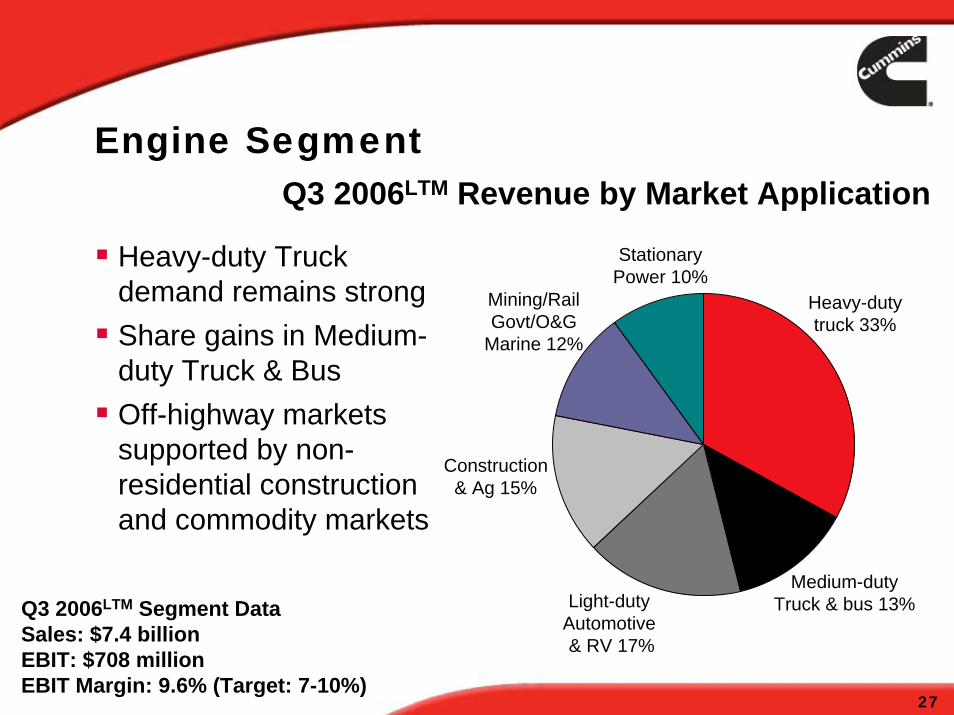

Engine Segment

Emission regulations create opportunitiesAftermarket revenue creates stable earningsEmerging marketsStrategic OEM partnerships High

Horsepower(19-91L) 14%

Midrange(3-9L) 37%

Heavy-Duty(10-15L) 29%

Parts andService 20%

Q3 2006LTM Segment DataSales: $7.4 billionEBIT: $708 millionEBIT Margin: 9.6% (Target: 7-10%)

Q3 2006LTM Revenue by Product

27

Engine Segment

Heavy-duty Truck demand remains strongShare gains in Medium-duty Truck & BusOff-highway markets supported by non-residential construction and commodity markets

Light-duty Automotive & RV 17%

Heavy-dutytruck 33%

Medium-dutyTruck & bus 13%

StationaryPower 10%

Construction& Ag 15%

Mining/RailGovt/O&G

Marine 12%

Q3 2006LTM Segment DataSales: $7.4 billionEBIT: $708 millionEBIT Margin: 9.6% (Target: 7-10%)

Q3 2006LTM Revenue by Market Application

28

Engines – Historical Performance

$37$62

$328

$582

$708

$0

$100

$200

$300

$400

$500

$600

$700

$800

2002 2003 2004 2005 Q3 '06

$ M

$3,435 $3,582

$5,424

$6,657

$7,397

0

1000

2000

3000

4000

5000

6000

7000

8000

2002 2003 2004 2005 Q3 '06

$ M

Segment EBITSales

LTM LTM

29

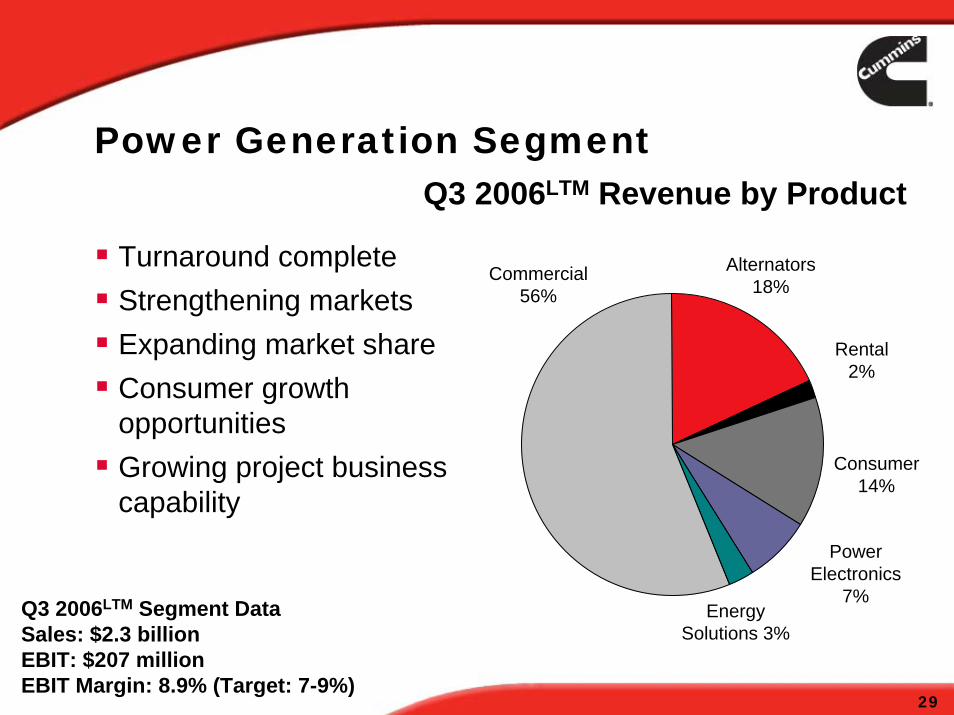

Power Generation Segment

Commercial56%

Alternators18%

Rental2%

Consumer14%

PowerElectronics

7%Energy

Solutions 3%

Q3 2006LTM Revenue by Product

Turnaround completeStrengthening marketsExpanding market shareConsumer growth opportunitiesGrowing project business capability

Q3 2006LTM Segment DataSales: $2.3 billionEBIT: $207 millionEBIT Margin: 8.9% (Target: 7-9%)

30

Power Generation – Historical Performance

($25) ($19)

$60

$145

$207

($50)

$0

$50

$100

$150

$200

$250

2002 2003 2004 2005 Q3 '06

$ M$1,226

$1,329

$1,842$1,999

$2,333

0

500

1000

1500

2000

2500

2002 2003 2004 2005 Q3 '06

$ M

Segment EBITSales

LTM LTM

31

Components Segment

Strategic advantage in emissions complianceSignificant future growth in revenue and earningsMultiple new product introductionsWinning non-CMI business

SpecialtyFiltration

6%Air IntakeSystems

11% Turbocharger26%

FuelSystems

18%Engine

Filtration21%

AcousticExhaust

12%

Q3 2006LTM Revenue by Product

CatalyticExhaust

6%

Q3 2006LTM Segment DataSales: $2.2 billionEBIT: $106 millionEBIT Margin: 4.8% (Target: 7-9%)

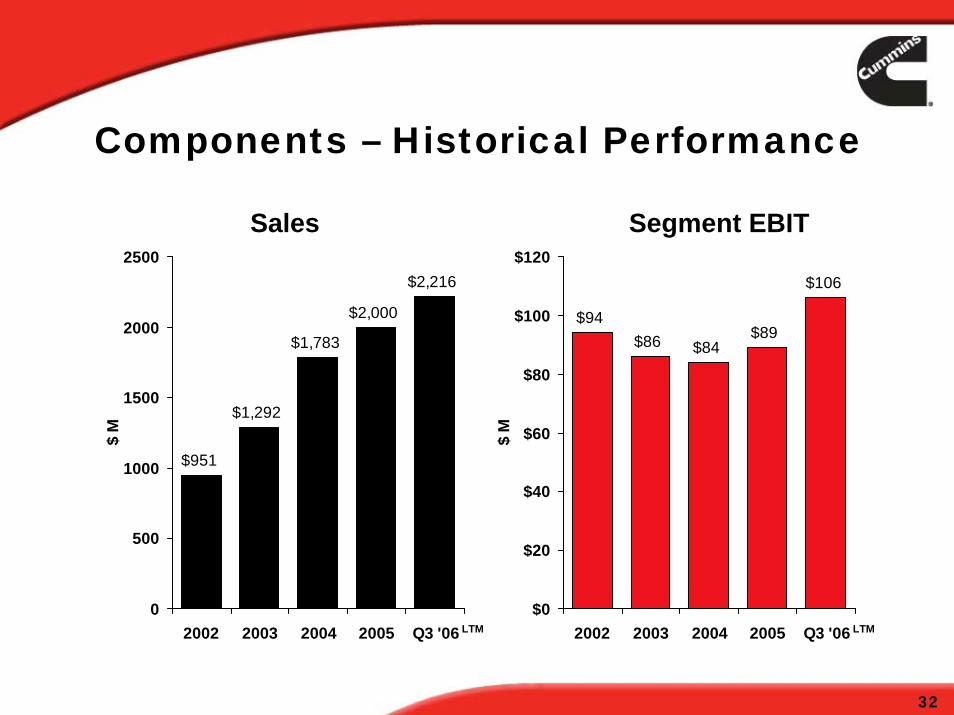

32

Components – Historical Performance

$94$86 $84

$89

$106

$0

$20

$40

$60

$80

$100

$120

2002 2003 2004 2005 Q3 '06

$ M

$951

$1,292

$1,783

$2,000

$2,216

0

500

1000

1500

2000

2500

2002 2003 2004 2005 Q3 '06

$ M

Segment EBITSales

LTM LTM

33

Distribution Segment

Broadening product offeringExpanding global coverageIncreasing equity ownershipExcelling in customer support

Parts,Filters, &

Consumables40%

Service18%

Engines20%

PowerGeneration

22%

Q3 2006LTM Revenue by Product

Q3 2006LTM Segment DataSales: $1.3 billionEBIT: $138 millionEBIT Margin: 10.3% (Target: 8-10%)

34

Distribution – Historical Performance

$33

$51

$79

$107

$138

$0

$20

$40

$60

$80

$100

$120

$140

$160

2002 2003 2004 2005 Q3 '06

$ M

$574$669

$973

$1,191

$1,345

0

200

400

600

800

1000

1200

1400

1600

2002 2003 2004 2005 Q3 '06

$ M

Segment EBITSales

LTM LTM

35

Non-GAAP Reconciliation – EBIT

EBIT = Earnings before interest, taxes, and minority interests.

We use EBIT to assess and measure the performance of our operating segments and also as a component in measuring our variable compensation programs. The table above reconciles EBIT, a non-GAAP financial measure, to our consolidated earnings before income taxes and minority interests, for each of the applicable periods.

Twelve Months Ended

MillionsOctober 1, 2006

Segment EBIT $ 1,145

Interest Expense $ (102)

Earnings before income taxes and minority interests $ 1,043

36

Non-GAAP Reconciliation – Net Assets

Millions September 25, 2005

October 1, 2006

Net assets for operating segments $ 3,312 $ 4,138

Liabilities deducted in computing net assets 3,421 3,541

Minimum pension liability excluded from net assets (826) (837)

Deferred tax assets not allocated to segments 928 712

Debt-related costs not allocated to segments 27 25

Total assets $ 6,862 $ 7,579