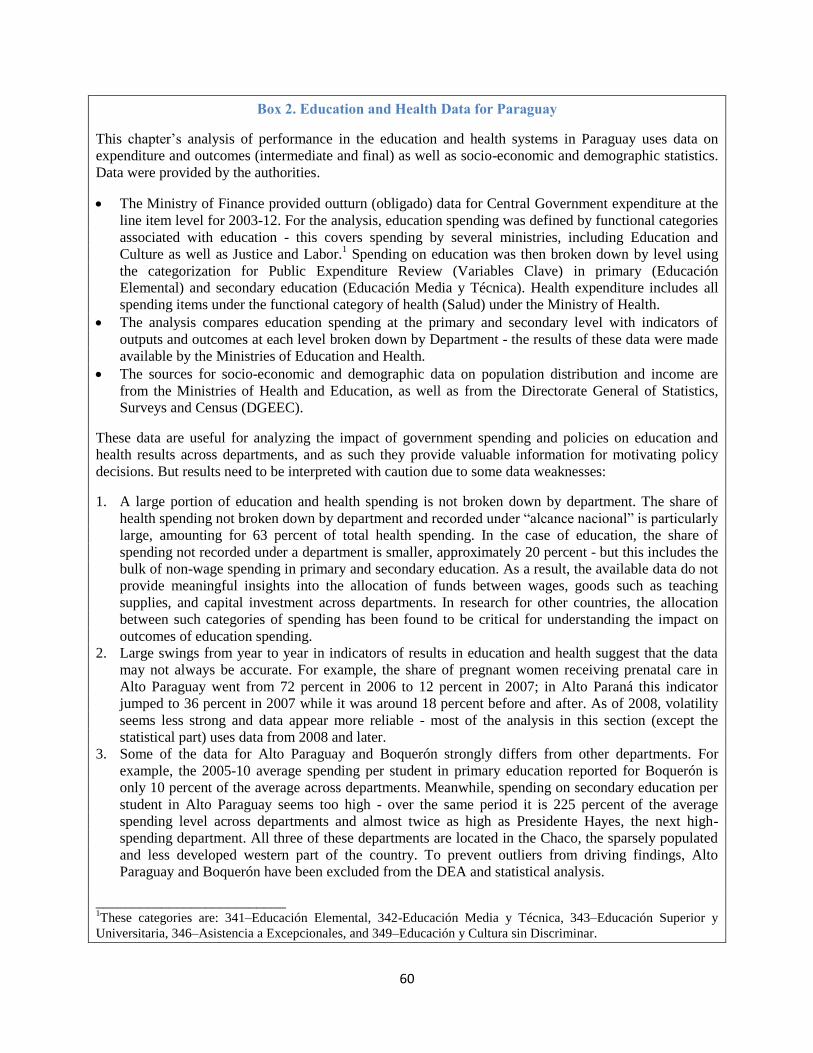

a public expenditure review for paraguay - world...

TRANSCRIPT

RESTRICTED

Report No. 78194-PY

A Public Expenditure Review for Paraguay

The quest for optimal tax and expenditure policies for

shared prosperity

November 25, 2013

Argentina, Paraguay and Uruguay Country Management Unit

Poverty Reduction and Economic Management

Latin America and the Caribbean Region

Document of the World Bank

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY AND EXCHANGE RATE

(As of November 25, 2013)

CURRENCY UNIT = GUARANIES

US$1.00 = Gs.4,423

FISCAL YEAR

January 1 – December 31

ABBREVIATIONS AND ACRONYMS

BCP Central Bank of Paraguay

(Banco Central de Paraguay)

LAC Latin America and the

Caribbean

BOOST Public Expenditure Database MDG Millenium Development Goal

CCT Conditional cash transfer MERCOSUR Southern Common Market

(Mercado Común del Sur)

CEPAL National Commission for Latin

America (Comisión Nacional

para América Latina

MICs Middle Income Countries

CGE Computable General

Equilibrium

PER Public Expenditure Review

CIT Corporate Income Tax PISA Program for International

Student Assessment

DEA Data Envelopment Analysis PPP Purchasing Power Parity

DGEEC National Institute of Statistics

(Dirección Nacional de

Encuestas Estadísticas y

Censos)

SET Department of Tax Revenue

Collection (Secretaria de

Estado de Tributación)

DINAC National Directorate of Civil

Aeronautics (Dirección

Nacional de Aeronáutica civil)

SITUFIN Public Financial Report

(Informe de la Situación

Financiera del país)

DPT Diphteria, Pertusis and Tetanus SNEPE National Evaluation System

of Educational Process

(Sistema Nacional de

Evaluación del Proceso

Educativo)

EPH National Household Survey

(Encuesta Permanente de

Hogares)

SOE State Owned Enterprise

FDI

Foreign Direct Investment TB Tuberculosis

GDP Gross Domestic Product UNESCO United Nations Educational,

Scientific and Cultural

Organization

GFS Goverment Finance Statistics USAID United State Agency for

International Development

HOI Human Opportunity Index VAT Value Added Tax

IMAGRO Agricultural Income Tax

(Impuesto a las Actividades

Agropecuarias)

WDI World Development

Indicators

IMF International Monetary Fund WHO World Health Organization

IRACIS Corporate Income Tax on

Commerce, Industry and

Services (Impuesto a la Renta

Comercial, Industrial o de

Servicios)

Vice President: Hasan A. Tuluy

Country Director: Penelope J. Brook

Sector Director: Rodrigo A. Chaves

Sector Manager: Auguste Tano Kouame

Sector Manager: Zafer Mustafaoglu

Task Team Leaders: Friederike (Fritzi) Koehler-Geib /

Jasmin Chakeri

iv

Table of Contents Acknowledgements ...................................................................................................................................... ix

Executive Summary ...................................................................................................................................... x

Chapter 1: Introduction: challenges and context .................................................................................... 1

1.1. The economic turnaround ................................................................................................................ 1

1.2. The economic stabilization program ................................................................................................ 4

1.3. The development dividend of stabilization ...................................................................................... 6

1.4. Challenge 1: Volatile macroeconomic environment ........................................................................ 7

1.5. Challenge 2: Limited fiscal resources that constrain spending on human development and growth-

enhancing policies ..................................................................................................................................... 8

1.6. Challenge 3: High levels of poverty and inequality remain ............................................................. 9

1.7. Transparency and data availability .................................................................................................. 9

1.8. Objective, methodology, and the value added of this PER ............................................................ 10

Chapter 2: Public Finances in a commodity driven economy .............................................................. 12

2.1 Fiscal consolidation with limited fiscal resources—the genesis of the current revenue structure . 12

2.2 The link between fiscal policy and macroeconomic volatility ....................................................... 21

2.3 Expenditures .................................................................................................................................. 26

2.4 Policy options ................................................................................................................................ 31

Chapter 3: Fiscal policy, poverty reduction and shared prosperity....................................................... 34

3.1 Fiscal policy and income redistribution ......................................................................................... 34

3.2 Fiscal policy and equity of opportunity ......................................................................................... 41

3.3 How progressive is Paraguay’s fiscal system with regard to the distribution of income and

opportunities? .......................................................................................................................................... 45

3.4 Policy options ................................................................................................................................ 49

Chapter 4: Efficiency of Public Spending and Service Delivery .......................................................... 51

4.1 The efficiency of public spending in Paraguay in international comparison ................................. 51

4.2 Within-country differences in the efficiency of public spending ................................................... 55

4.3 Case study: expenditure efficiency in State-Owned Enterprises (SOEs) ....................................... 61

4.4 Policy options ................................................................................................................................. 62

List of references ......................................................................................................................................... 63

v

Annexes ...................................................................................................................................................... 67

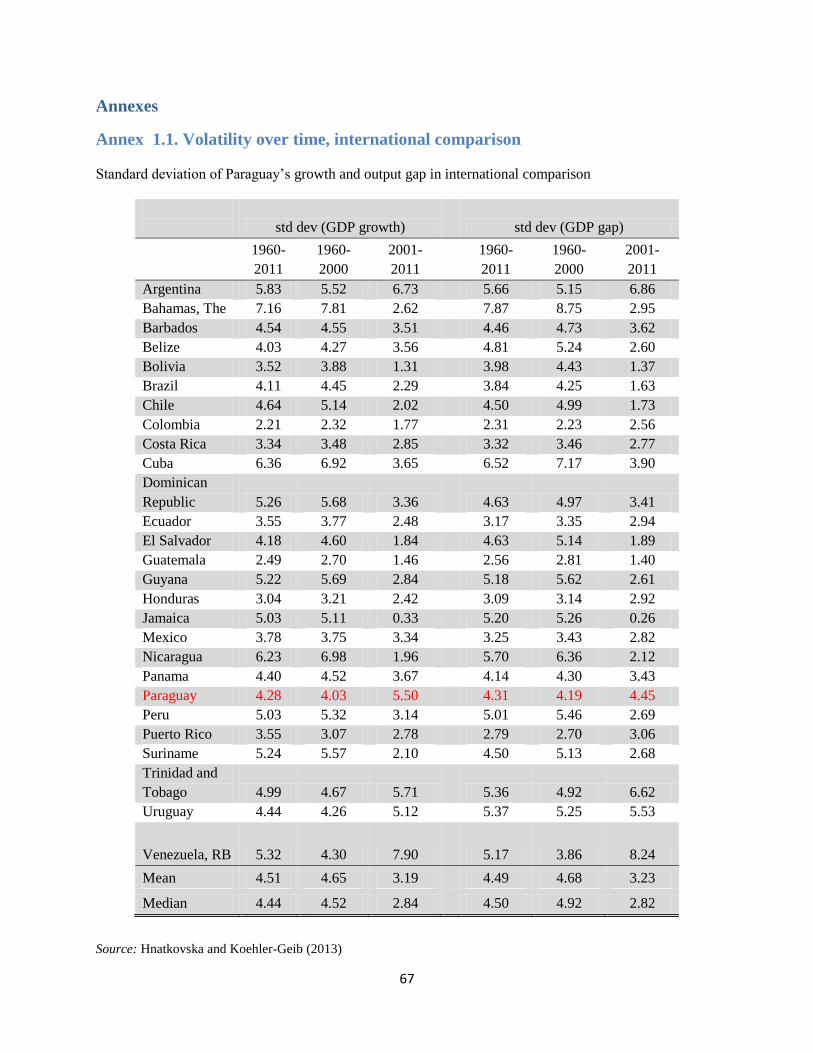

Annex 1.1. Volatility over time, international comparison ................................................................. 67

Annex 1.2. Volatility breaks of macro-economic variables in Paraguay ............................................. 68

Annex 1.3. Social development indicators ........................................................................................... 69

Annex 1.4. Poverty, Extreme Poverty, Inequality in Latin America and the Caribbean ...................... 70

Annex 4.1: Data envelopment analysis (DEA) .................................................................................... 71

Map ....................................................................................................................................................... 73

vi

List of Figures-Chapter 1

Figure 1.1: Real GDP and real GDP per capita .............................................................................. 2

Figure 1.2: Aggregate demand decomposition of growth (percent annual contribution) ............... 3

Figure 1.3: Sectoral decomposition of growth (percent annual contribution) ................................ 3

Figure 1.4: Revenues and expenditures .......................................................................................... 5

Figure 1.5: Fiscal balance ............................................................................................................... 5

Figure 1.6: Public debt .................................................................................................................... 6

Figure 1.7: Inflation ........................................................................................................................ 6

Figure 1.8: Public and private investment ...................................................................................... 6

Figure 1.9: Net capital inflows........................................................................................................ 6

Figure 1.10: Tax-to-GDP ratio 2011 ............................................................................................... 8

Figure 1.11: Social Expenditure ..................................................................................................... 8

List of Figures-Chapter 2

Figure 2.1: Revenues and expenditures (percent of GDP) .......................................................................... 13

Figure 2.2: Government revenues, average 2007- 2011 (percent of GDP) ................................................. 13

Figure 2.3: Share of agricultural tax revenue in internal tax revenues versus sectoral share in GDP ........ 14

Figure 2.4: Total internal tax revenue: Number of contributors versus average contribution by taxpayer 17

Figure 2.5: VAT: Number of contributors versus average contribution by taxpayer ................................. 17

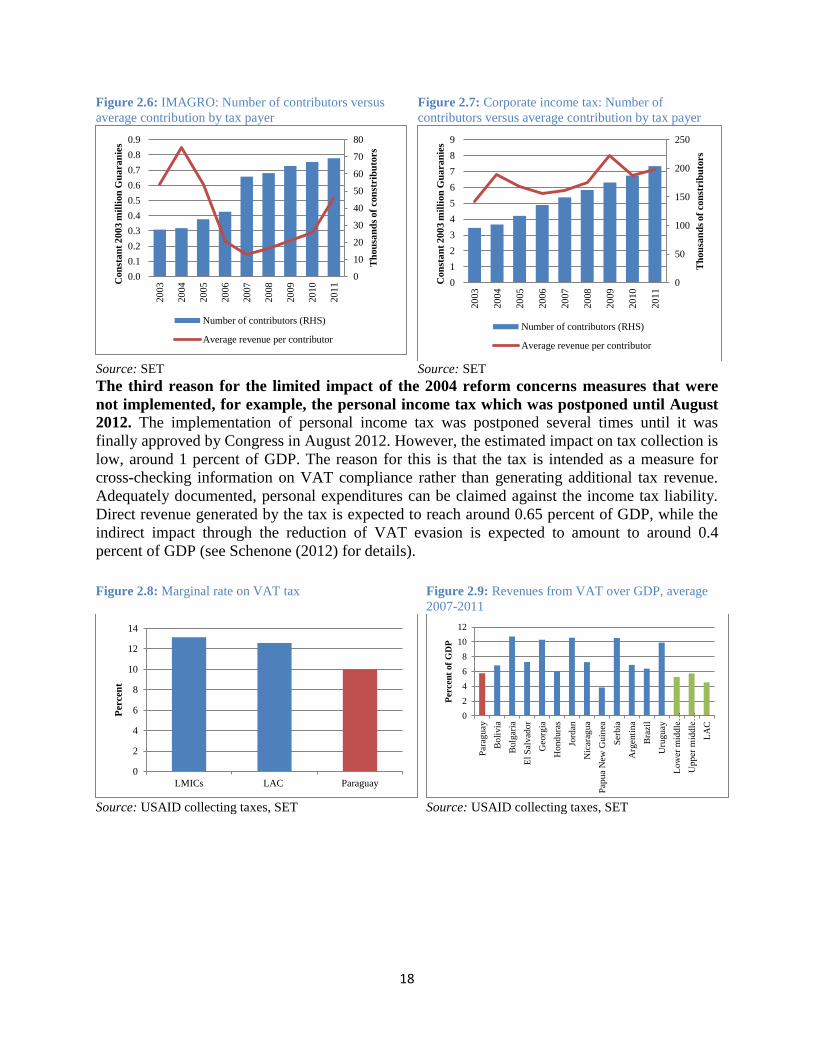

Figure 2.6: IMAGRO: Number of contributors versus average contribution by tax payer ........................ 18

Figure 2.7: Corporate income tax: Number of contributors versus average contribution by tax payer ...... 18

Figure 2.8: Marginal rate on VAT tax ........................................................................................................ 18

Figure 2.9: Revenues from VAT over GDP, average 2007-2011 ............................................................... 18

Figure 2.10: Marginal rate on corporate income tax ................................................................................... 19

Figure 2.11: Revenues from corporate income tax over GDP, average 2007-2011 ................................... 19

Figure 2.12: Marginal tax on personal income tax ..................................................................................... 19

Figure 2.13: Revenues from personal income tax over GDP, average 2007-2011 ..................................... 19

Figure 2.14: VAT productivity, average 2007-2011 ................................................................................... 20

Figure 2.15: Corporate income tax productivity, average 2007-2011 ........................................................ 20

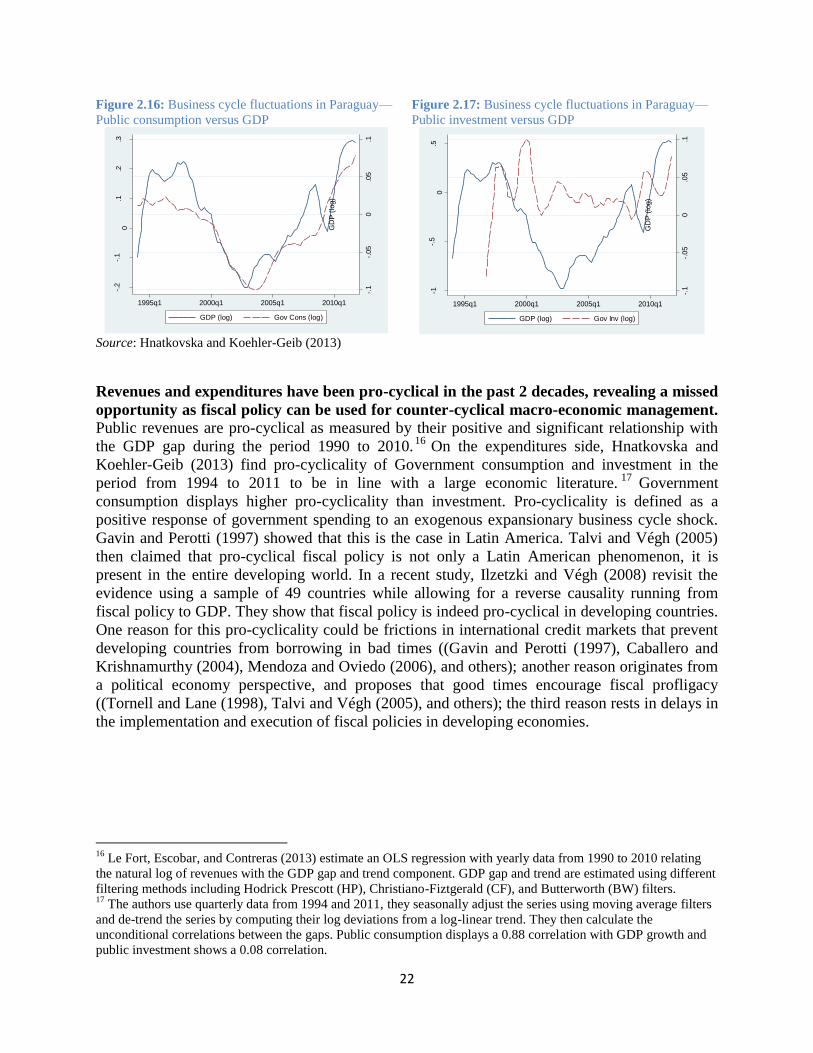

Figure 2.17: Business cycle fluctuations in Paraguay—Public consumption versus GDP ......................... 22

Figure 2.18: Business cycle fluctuations in Paraguay—Public investment versus GDP ............................ 22

Figure 2.19: Contribution of public and private demand components to real GDP growth ...................... 23

Figure 2.20: Public consumption and investment (quarterly y-o-y growth) ............................................... 24

Figure 2.21: Exports by product ................................................................................................................. 24

Figure 2.22: Fiscal Space ........................................................................................................................... 27

Figure 2.23: Public Expenditure in international comparison (average 2007-2011) .................................. 27

Figure 2.24: Paraguay’s public debt over time ........................................................................................... 27

Figure 2.25: Interest expenditure in Latin America .................................................................................... 27

Figure 2.26: Functional classification ......................................................................................................... 29

Figure 2.27: Education expenditure in international comparison (average 2007-2011) ............................. 29

Figure 2.28: Health expenditure in international comparison ..................................................................... 29

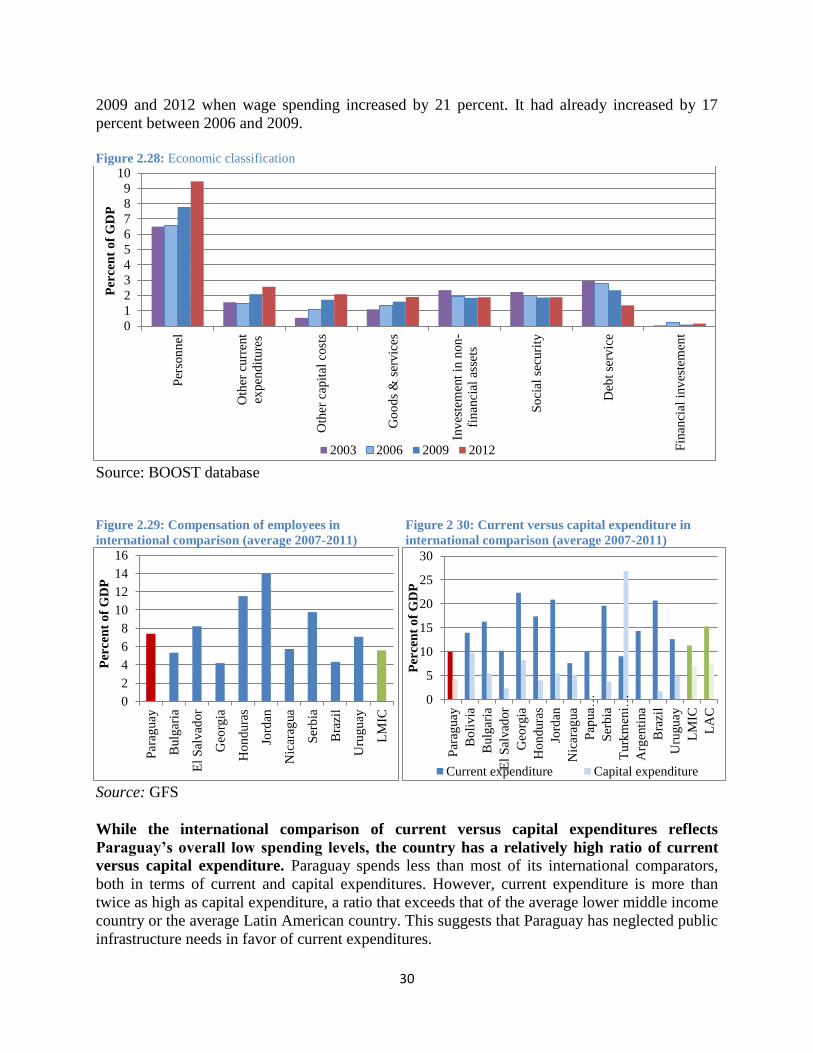

Figure 2.29: Economic classification .......................................................................................................... 30

Figure 2.30: Compensation of employees in international comparison (average 2007-2011) ................... 30

vii

Figure 2 31: Current versus capital expenditure in international comparison (average 2007-2011) .......... 30

List of Figures-Chapter 3

Figure 3.1: Public expenditure on health and education (% of total public expenditure) ............ 35

Figure 3.2: Public social spending in Paraguay and comparator countries (2009-11; % of GDP)35

Figure 3.3: Gini coefficient for each income concept in Argentina, Bolivia, Brazil, Guatemala,

Mexico, Paraguay, Peru and Uruguay .......................................................................................... 36

Figure 3.4: Inequality in Paraguay (2010) – benchmark vs. sensitivity analysis ......................... 37

Figure 3.5: Percent of direct transfer beneficiaries who are poor in Argentina, Bolivia, Brazil,

Guatemala, Mexico, Paraguay, Peru and Uruguay ....................................................................... 39

Figure 3.6: Percent of poor receiving at least one direct transfer ................................................. 39

Figure 3.7: HOI for Latin American Countries (proj. 2010) ........................................................ 42

Figure 3.8: Change in the HOI and coverage ............................................................................... 43

Figure 3.9: Coverage and HOI in Paraguay (2010) ...................................................................... 44

Figure 3.10:Concentration shares of taxes in Paraguay (2010) .................................................... 46

Figure 3.11: Concentration coefficients of public expenditure categories in Paraguay (2010) .... 47

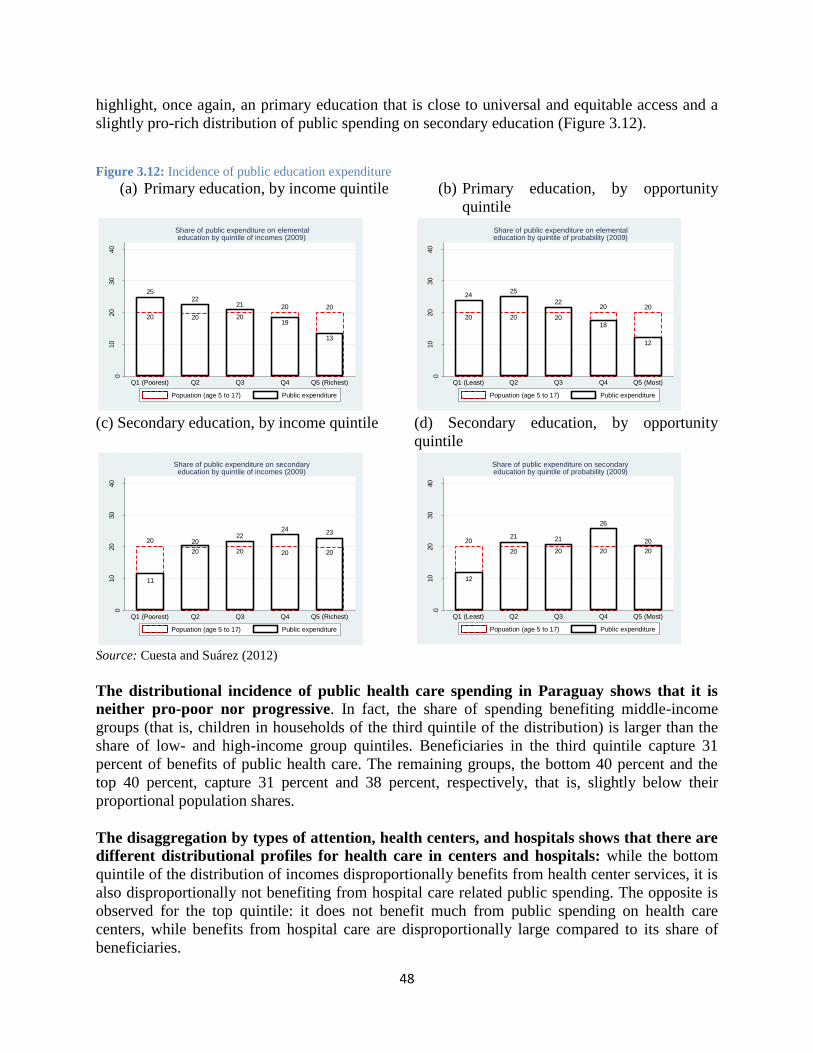

Figure 3.12: Incidence of public education expenditure ............................................................... 48

Figure 3.13: Incidence of public health expenditure .................................................................... 49

List of Figures-Chapter 4

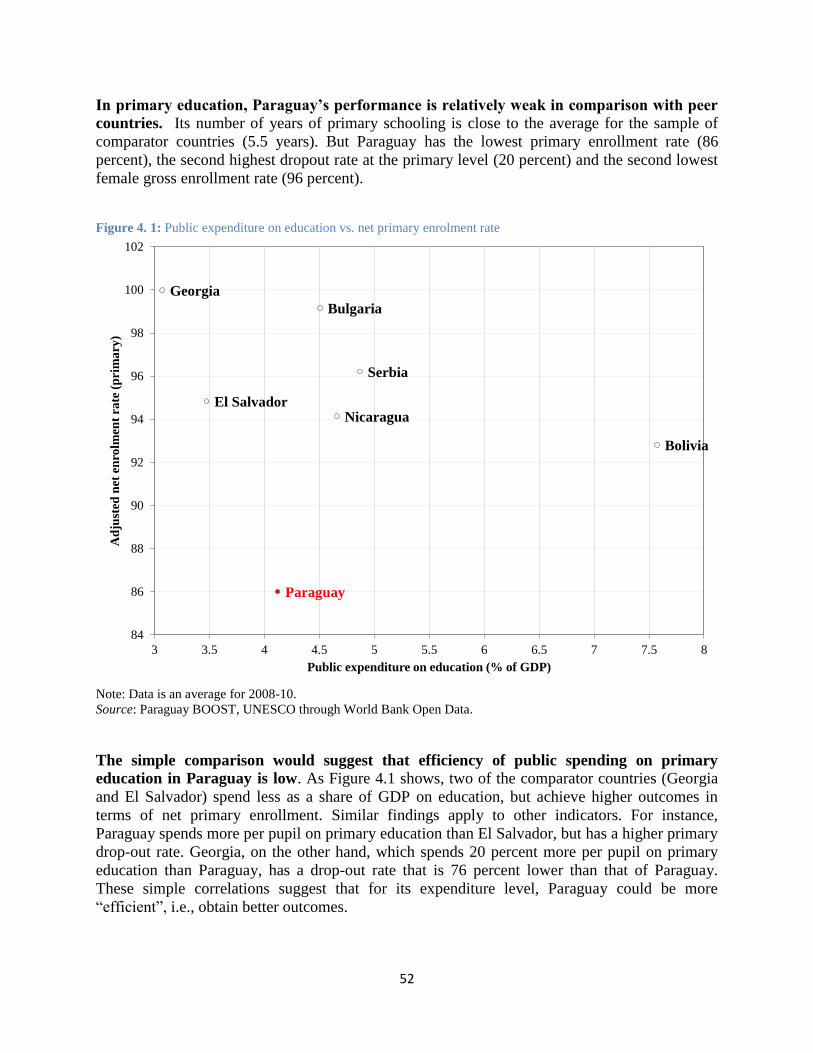

Figure 4. 1: Public expenditure on education vs. net primary enrolment rate .............................. 52

Figure 4.2: Public expenditure on education vs. secondary graduation rate ................................ 53

Figure 4.3: Health expenditure and maternal mortality rate ......................................................... 54

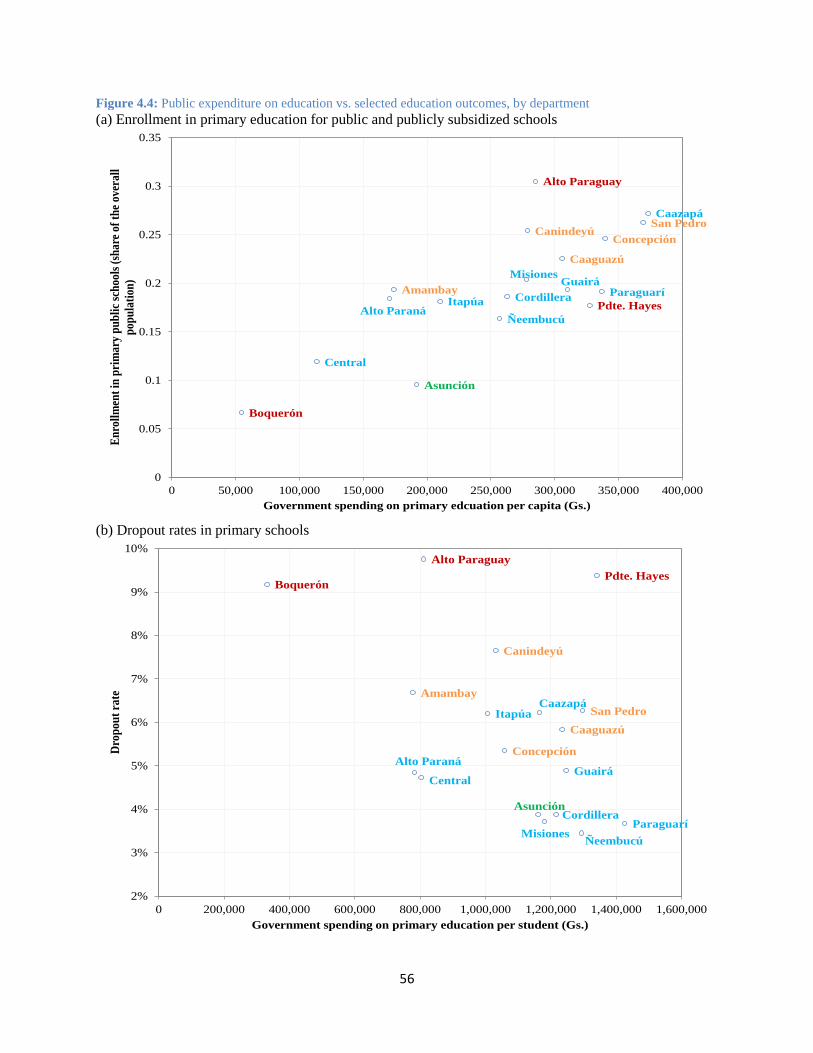

Figure 4.4: Public expenditure on education vs. selected education outcomes, by department ... 56

Figure 4.5: Public expenditure on health vs. selected health outcomes, by department ............... 59

List of Tables-Chapter 1

Table 1.1: Poverty and equity indicators ........................................................................................ 3

List of Tables-Chapter 2

Table 2.1: Government tax versus non-tax revenue (percent of GDP)......................................... 14

Table 2.2: Sectoral weights in gross value added ......................................................................... 14

Table 2.3: Sectoral contribution to total internal tax revenue ....................................................... 15

Table 2.4: Revenue by tax type..................................................................................................... 15

Table 2.5: Government tax revenue by tax type (percent of total unless stated otherwise) ......... 16

Table 2.6: Marginal tax rates over time ........................................................................................ 16

Table 2.7: Volatility of revenues and expenditures ..................................................................... 21

Table 2.8: Export by destination ................................................................................................... 24

Table 2.9: Volatility of different tax types (annual real growth) ................................................. 26

List of Tables-Chapter 3

Table 3.1: Taxes, transfers, inequality and poverty in Paraguay (2010) - benchmark ................. 37

viii

List of Tables-Chapter 4

Table 4.1: Characteristics of the SOE Sector in Paraguay............................................................ 62

ix

Acknowledgements

This report was prepared by a team led by Friederike (Fritzi) Koehler-Geib and Jasmin Chakeri (LCSPE)

under the overall supervision and guidance of Zafer Mustafaoglu (Lead Economist and Sector Leader,

LCSPR), Auguste T. Kouame (Sector Manager, LCSPE), Rodrigo A. Chaves (Sector Director, LCSPR)

and Penelope J. Brook (Country Director, LCC7C). The peer reviewers were David Rosenblatt

(Economic Advisor, DECOS), Dominique Van De Walle (Lead Economist, DECHD), Eduardo Ley

(Lead Economist, PRMED), Gallina Vincelette (Senior Economist, ECSP1), and Jose Molinas (Country

Sector Coordinator, ECSH4).

The core team included Carolina Diaz-Bonilla (LCSPP), Rossana Polastri (previous Country Manager,

LCCPY), Dante Mossi (Country Manager, LCCPY), (Eduardo Andres Estrada, Renato Busquets

(WBIOG), Elida Caballero Cabrera, Guillermo Cabral, Jorge Araujo, Miriam Beatriz Villarroel, Patricia

Chacon Holt, Patrick Rittenauer, Peter Siegenthaler, and Silvia Gulino (all LCSPE), Gloria Dure, Rosa

Arestivo de Cuentas Zavala, Telma Alvarenga Capurro (all LCCPY). Inputs and background papers were

also received from Edgardo Favaro, Julio Ramirez, Lisa Stewart, Martin Cicowiez, Nora Lustig, Osvaldo

Schenone, Sean Higgins, William Swanson (all consultants), Jose Antonio Cuesta and Pablo Suarez

Becerra (PRMPR), Eriko Togo (PRMED), Antonio Velandia-Rubiano (FABDM), Ana Mie Horigoshi

Rei, Fanny Weiner (all LCSPS), Luis Orlando Perez (LCSHH), Rafael de Hoyos (LCSHE), Juan Martin

Moreno (LCSHS), Agustin Indaco, Andres Lajer Baron, Carolina Saizar, Hannah Nielsen, Nathalie

Picarelli, Pia Maria Zanetti, Sona Varma (all LCSPE), Marijn Verhoeven (PRMPS), and Massimo

Mastruzzi (WBIOG).

Comments and inputs were also received from many colleagues working in the Paraguay country team,

including Alexandre Arrobbio, Raul Junquera (all LCSPS), Andrew Follmer, Carla Cutolo, Elena Feeney,

Mariela Alvarez, Tatiana Proskuryakova, Sabine Hader (all LCC7C), Richard Ferreira Candia, Ruth

Gonzalez Llamas (LCREA), and Graciela Sanchez Martinez (LCSSO).

The team is thankful for the excellent collaboration with the Ministry of Finance, in particular with the

Vice Ministry of the Economy including the Departments of Economic Studies, Macro Fiscal Policies,

Debt Policy, and Financial-Economic Information Systems, and the Ministries of Health, Education, and

Public Works.

x

Executive Summary

Paraguay has achieved significant progress in terms of fiscal policy over the past decade.

Fiscal consolidation was at the core of the economic stabilization program that contributed to the

economic turnaround beginning in 2003. It included an increase in tax revenues through the

implementation—albeit partial—of a tax reform package, as well as significant rationalization of

expenditures. Tax revenues increased from 8.7 percent of GDP in 2003 to 12.3 percent in 2012.

The overall fiscal surplus averaged 1 percent of GDP between 2004 and 2011, and public debt

fell from 41 percent of GDP in 2002 to 12 percent in 2012.

Despite this progress on fiscal reform, three major challenges remain: (i) a volatile

macroeconomic environment; (ii) still insufficient fiscal resources; and (iii) high levels of

poverty and inequality. First, while Paraguay’s growth in the past decade has exceeded its

average for the past three decades, it has also become more volatile in recent years. In the period

from 1960 to 2000 the standard deviation of GDP growth in Paraguay undershot the regional

mean and median, and in contrast in the past decade has exceeded them. Moreover, Paraguay is

one of the few Latin American countries that show an increasing trend comparing the standard

deviations of GDP growth for these two periods. The increased volatility renders fiscal policy,

especially planning and forecasting, more difficult. The second major challenge is the still

limited fiscal resources that constrain spending on human development and growth-enhancing

policies. Paraguay’s tax to GDP ratio is lower than that of any relevant peer group including the

average Latin American or lower middle income country. At the same time, the share of social

expenditure in GDP is also lower than that of the relevant peer countries and overall outcomes of

social services are improving at a slower pace than in other countries. Third, despite significant

poverty reduction since 2003, the incidence of poverty and inequality remains high in

international comparison and calls for further improvements in the future.

In light of these three challenges, the objective of this report is to examine the extent to

which fiscal policy in Paraguay has contributed to the social progress of the past decade,

and can serve the purpose of further reducing poverty and enhancing shared prosperity in

the years to come. Overall, fiscal policy can contribute to containing poverty and inequality by

buffering the negative impact of financial and economic crises on vulnerable parts of the

population. Moreover, tax and expenditure policies that redistribute from high- to low-income

households in a well-targeted manner can also contribute to these goals. In Paraguay,

Government intervention helped containing the negative impact of the 2009 crisis on poverty and

inequality, thereby contrasting earlier crisis that had large negative effects. In terms of

redistribution, the role of fiscal policy in Paraguay has been limited in the past partly due to the

low tax to GDP ratios as well as low expenditures in social sectors including social protection.

There is scope to increase the role of fiscal policy in reducing poverty and sharing prosperity in

Paraguay in the future due to the possibility of raising additional tax revenues, expanding the

coverage of social protection programs, and reducing remaining inefficiencies.

Fiscal policy in Paraguay remains constrained by limited tax revenues. Still today, Paraguay

is characterized by a low tax-to-GDP ratio by international standards. The tax reform in 2004

could not generate significant additional revenues for the following three main reasons: (ii) it

failed to introduce taxation in the agricultural sector to rise the sector’s fiscal contribution to a

xi

level that is proportional to its share of GDP; (ii) significant tax exemptions weakened some

reform measures and still do, as in the case of the reformed corporate income tax of the

agricultural sector (IMAGRO); and (iii) some measures, for example the personal income tax,

were not implemented for a long time. In addition, the reform did not change the actual structure

of the tax system, especially with regard to reliance on indirect taxes. In fact, reliance on indirect

taxes increased over time, rendering the system even more regressive.

The current structure of the tax system appears suboptimal in light of the identified

challenges. Even though the reliance on indirect taxes insulates public revenues from economic

volatility to a certain extent, it imposes high costs associated with sufficiency and equity of the

system. Other policy tools such as a fiscal rule or a stabilization fund could be used to manage

volatility more effectively. Furthermore, the regressivity of the tax system, as a result of a high

degree of indirect taxation, is particularly harmful in an economy with high poverty rates.

Adequate taxation of the agricultural sector is needed to level the playing field for business

development in all sectors and to address the insufficiency of taxes. While the full

implementation of the 2004 tax reform could still raise tax revenues, eliminating significant tax

exemptions could provide an additional source of fiscal revenue. Some elimination would have

to be accompanied by targeted spending increases to offset the potential negative effect on

poverty. This could help Paraguay generate the fiscal resources necessary to increase spending

on infrastructure and the social sectors and to implement countercyclical fiscal policies. In

addition, the low taxation of agriculture provides an incentive to be active in this economic

sector, which already has a heavy weight in the economy. Removing this distortion would foster

the diversification of the economy.

While fiscal policy contributes less to poverty reduction and shared prosperity in Paraguay

than in the other countries analyzed for this study, direct transfers are well targeted. The

nature of Paraguay’s fiscal system – low tax revenues and, consequently, relatively low

expenditure – represents important limitations for the scope of fiscal redistribution and basic

service delivery. As a result, fiscal policy in Paraguay reduces inequality only slightly, and fiscal

policy measures such as taxes and transfers have a net negative impact on the poverty headcount.

This is partly because the poor pay a large share of their income on taxes. In addition, transfers

do not increase the income of the poor by as much as they do in other countries: the extremely

poor receive, on average, just US$0.38 PPP per day in household per capita terms from direct

transfers. And while direct transfers (especially the conditional cash transfer program) are well

targeted, they reach only a quarter of the extreme poor. As a result, all income deciles, including

the poorest, are net contributors to the fiscal system.

Income inequality is partly a result of the inequity of opportunities, which has improved in

recent years. The Human Opportunity Index (HOI) measures how far a society is from universal

provision of basic services and goods, such as sanitation, clean water and education, and the

extent to which those goods and services are unevenly distributed. Paraguay performs below the

LAC average on the HOI, but has improved faster than other countries since 2003. This is

because the coverage of basic social services, the overall wellbeing of the population and the

distribution of disparities among population groups have all improved, and have improved in line

with increased spending. However, the inequity of opportunity remains particularly high in

services where coverage remains low, such as access to safe sanitation, completion of 9th

grade

and enrollment in pre-school.

xii

Overall, Paraguay’s fiscal system is less progressive than in other Latin American

countries analyzed. Paraguay’s reliance on indirect taxes makes its overall tax system

regressive. Furthermore, social expenditures are less progressive than in other countries: while

the CCT program is highly progressive (by design), education and health spending is much less

progressive than in other countries. Public spending on primary education is pro-poor with the

bottom 40 percent capturing 47 percent of total public resources. Conversely, public spending on

secondary education is pro-rich, with the bottom 40 percent capturing only 31 percent of total

public resources while the top 40 percent captures close to half of total public resources.

Similarly, the poorest benefit disproportionally from public expenditures on health centers, while

the richest benefit disproportionally from public expenditures on hospitals.

Even though some social programs are very effective, the expenditure efficiency in

education and health is relatively low. This partly explains why public spending does not

contribute much to the reduction of poverty and inequality. Given Paraguay’s limited fiscal

resources, getting the most value out of public spending is an important priority. However, not

only does Paraguay spend less on the social sectors than many other countries, it also achieves

relatively weak outcomes in education and health. Preliminary analysis based on international

comparisons suggests that Paraguay could improve the efficiency of public spending in these two

sectors. An area with scope for improvements is the oversight of state-owned enterprises which

provide a large share of public basic services. Services such as water and sanitation are relevant

for health sector outcomes, and existing inefficiencies in the sector of state-owned enterprises

thereby generate follow-on effects. There also appears to be significant variation in expenditure

efficiency among departments within Paraguay, which may be related to a number of factors.

More and better data is needed at the departmental level in order to better assess what drives

social outcomes in different parts of the country.

The sufficiency and efficiency of social expenditures have to be considered within the

context of fiscal prudence, which is a continuous task. This is especially important in light of

the recent expansionary fiscal stance. Only if the Government is able to sustain fiscal prudence in

the future, will it be able to maintain macroeconomic stability and performance. The

Government needs to revert quickly to tighter fiscal policies after the 2012 fiscal stimulus to

buffer the effect of a bad harvest and the run-up to the April 2013 Presidential elections. In

addition, further improvements in debt management and addressing weaknesses in the budget

process would be important to sustain past gains in the future.

Policy options

A number of policy options emerge from the analysis carried out in the PER:

Related to the volatile macroeconomic environment, policy options to address the pro-

cyclicality of fiscal policy include the introduction of a fiscal responsibility law or the

introduction of a stabilization fund. Other options include strengthening automatic stabilizers

such as unemployment insurance and other social protection measures.

Direct taxation could be increased through the elimination of exemptions and further

reforms of personal income and property taxes. The main exemptions currently apply to the

xiii

agricultural income tax (IMAGRO); corporate income tax (IRACIS); personal income tax and

property tax. The most important gains in terms of revenue would stem from changes to value

added tax, including the elimination of the suspension of VAT application to petrol imports;

replacement of the reduced VAT rate of 5 percent with a uniform rate of 10 percent as envisaged

during the 2004 reform; and elimination of the exemption of sales of the agricultural sector and

of paid interests. A reform of property taxes could base taxation of property on market valuation

as opposed to fiscal valuation in order to render property tax a more effective tax. This could

promote better land use, it could also increase municipal revenue, which in turn could increase

accountability and reduce dependency on central government transfers.

Such reforms would also help address the regressivity of the tax system. The regressivity of

Paraguay’s tax system is in large part due to its reliance on indirect taxes. Reforming key direct

taxes and increasing their share in tax collections will help make Paraguay’s fiscal system more

progressive.

Eliminating tax exemptions and reforming direct taxes would help generate additional

revenue, which could be used to strengthen the progressivity of public spending.

Simulations using a CGE model prepared for this report suggest that the reduction in exemptions

(especially VAT exemptions) and the use of these resources for social expenditure could be

beneficial for human development outcomes. The simulations look specifically at increases in

spending on education, health and water and sanitation, and on the effect of this increased

spending on MDGs. Such spending could be better targeted to improve access to basic services

used by particularly vulnerable groups, including those identified as households whose head

speaks only Guaranï and went to school for less than 6 years. Similarly, any additional resources

freed up could be used for the CCT program, which would have beneficial impacts on poverty

and inequality given that it is already well targeted.

In order to assess and enhance the efficiency of public expenditure, it is important to

continue to improve disaggregated data at the departmental level. In addition to improving

the accuracy of available data, breaking down data on total expenditure by department, including

at the program or even facility level (such as schools and health centers) would push progress

even further by allowing for better targeting of resources. More and better data on outcomes in

key sectors, as well as on socio-economic and demographic indicators at the departmental or

municipal level, would also be beneficial for policy making.

Paraguay would also benefit from participation in additional international assessments in

order to better gauge its performance vis-à-vis peer countries. For instance, taking part in the

PISA study could make education outcomes in Paraguay comparable to other countries, thus

providing important information that could guide policy making in that sector.

Finally, improved management and oversight of SOEs could contribute to better social

service provision. Specific measures include: (i) approval and implementation of the draft law

institutionalizing an independent SOE supervisory body; (ii) further reforms to strengthen the

SOE governance and oversight framework; (iii) assurance of sufficient supply and quality of

basic public services; (iv) preparation of a long- and medium-term investment plan to efficiently

address infrastructure gaps; (v) the set-up of an investment system for SOEs; (vi) a set of rules

xiv

for managing debt and fiscal risk of SOEs; and (vii) schemes on transfers, subsidies and

outstanding payments.

1

Chapter 1: Introduction: challenges and context

Paraguay’s economic turnaround started in 2003, driven by an economic stabilization program

and favorable external demand. Since then, the Government has achieved significant progress in

the areas of development and reform, yet three major challenges remain for fiscal policy. First,

although Paraguay’s growth in the decade has exceeded its historical average since 1980, it has

become more volatile in recent years. This increased volatility renders planning and forecasting

more difficult. The second major challenge is the limited fiscal resources that constrain spending

on human development and growth-enhancing policies. Third, despite significant poverty

reduction since 2003, levels of poverty remain high, and achievements appear more modest if the

period prior to the deep crisis of 2002 and 2003 is taken into account. In the same vein, in terms

of reducing inequality and sharing prosperity the country has achieved less than its regional

peers, remaining one of the most unequal economies in Latin America - the most unequal region

in the world.

The purpose of the current study is to answer the following question: given the structure and the

challenges of the Paraguayan economy, has fiscal policy served the purpose of reducing poverty

and sharing prosperity? Based on the findings related to this question, the study seeks to trigger

a public debate about on optimality of tax and expenditure policies for Paraguay.

The current study seeks to answer this question in four chapters. This first, introductory chapter

presents the background in economic developments over the last decade and spells out

remaining challenges. Following this review it will also provide the objective, methodology, and

the value added of this PER. The second chapter addresses fiscal policy in a volatile

macroeconomic environment; the third chapter covers the role of fiscal policy in reducing

poverty, inequality and sharing prosperity; and the fourth chapter deals with the efficiency of

public spending.

1.1. The economic turnaround

After a quarter century of chronic stagnation and crisis, an economic stabilization program

and favorable external demand have led a recovery in growth since 2003. Paraguay

experienced a period of fast economic growth and prosperity throughout the 1960s and 1970s

with real per capita income more than doubling and real GDP growth averaging 7 percent per

year. The construction of the Itaipu dam provided significant economic impulse during that

period but this faded with the dam’s completion in the fall of 1982. Subsequently, Paraguay

could not maintain the high growth rates and slipped into a period of recurring and costly

financial distress in the late 1990s. This translated into slow advances in per capita GDP, which

grew on average 1 percent per year between 1982 and 1996 and then declined by 14 percent

between 1997 and 2002. In terms of real GDP, an average annual growth of 3.8 percent

contrasted with a subsequent drop of 4.4 percent between 1997 and 2002. The crisis in the late

1990s was a result of rapid financial liberalization, which was allowed to take place in the

2

absence of prudential regulations and safeguards.1 Shortly thereafter, Paraguay was affected by

contagion from the regional crisis in 2002, which exacerbated inherent weaknesses in the

financial system. This undermined confidence and precipitated large deposit runs as well as a

deep financial crisis that depressed the economy further. In response to this crisis, the new

Duarte-Frutos administration adopted an ambitious stabilization program in 2003. Strong

external demand helped stabilization and recovery. It triggered fast export growth which in turn

translated into strong recovery of private consumption and investment, the main drivers behind

growth recovery in that period.

As a result, average annual real GDP growth reached 3.9 percent between 2003 and 2012

and was broadly shared for the most part. By 2008, real per capita GDP had recovered from

the crisis and had regained the pre-crisis levels of 1997. With strong real export growth of 5.4

percent per year on average between 2003 and 2012, private consumption and investment also

expanded rapidly, contributing on average 3.5 and 0.7 percentage points respectively to annual

growth in this period (Figure 1.2). The services sector contributed most to growth, accounting for

2.2 percentage points on average between 2003 and 2012, of which wholesale and retail trade,

followed by transport and communications, were the most important subsectors. Agriculture was

the second most important sector explaining on average 0.6 percentage points of growth,

followed by the electricity and water sector with 0.5 percentage points. As a consequence of

solid growth, unemployment fell from 8.1 percent in 2003 to 5.6 in 2011 and poverty was

reduced from 44 percent to 32 percent over the same period.

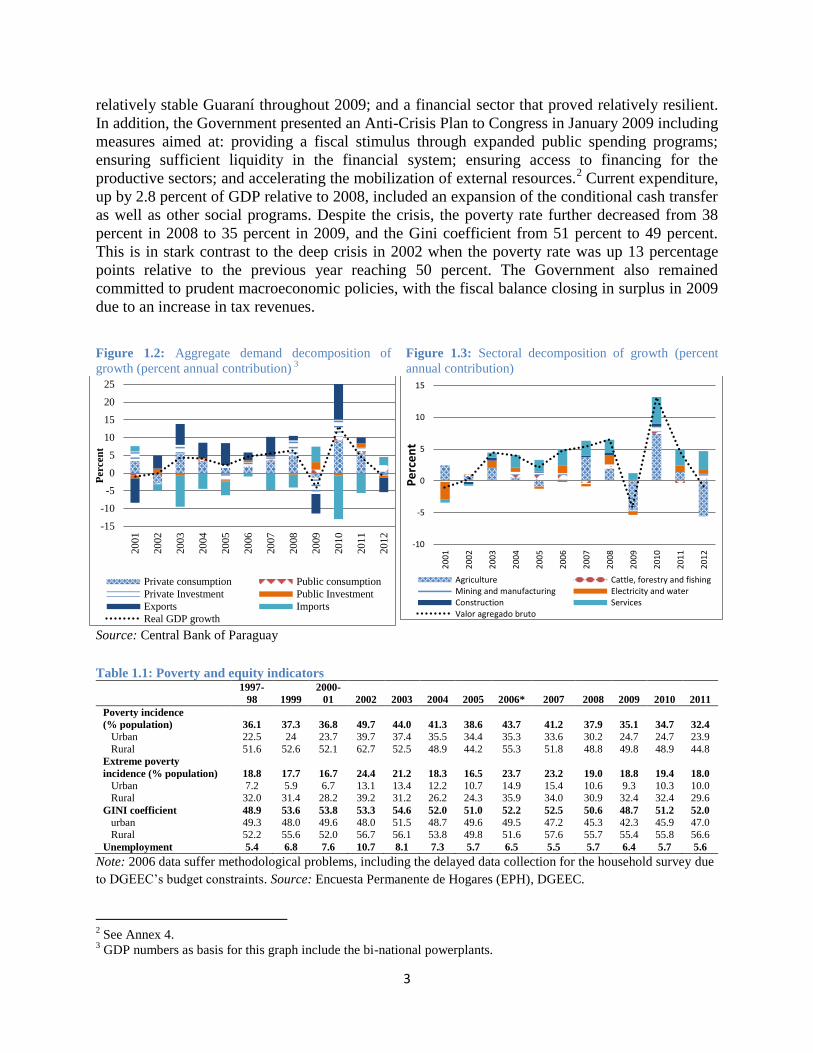

While the 2009 crisis temporarily interrupted Paraguay’s economic turnaround, the

impact on poverty was contained and fiscal policy remained prudent in contrast to earlier

crises. A severe drought exacerbated the impact of the international economic crisis in Paraguay,

triggering a 4 percent real contraction of the economy and a 25 percent drop in agricultural

production. Yet, record growth of 13.1 percent in 2010 illustrates how short-lived the impact

was. Paraguay’s external position remained stable throughout 2009, because the significant drop

in exports was balanced out by: the drop in imports; a lower than expected drop in remittances; a

1 IMF (2009) provides a detailed description.

Figure 1.1: Real GDP and real GDP per capita

Source: World Bank, WDI

-10

-5

0

5

10

15

20

40

60

80

100

120

140

196

0

196

2

196

4

196

6

196

8

197

0

197

2

197

4

197

6

197

8

198

0

198

2

198

4

198

6

198

8

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

Per

cen

t

Ind

ex (

20

05

=1

00

)

Real GDP per capita index Real GDP growth

3

relatively stable Guaraní throughout 2009; and a financial sector that proved relatively resilient.

In addition, the Government presented an Anti-Crisis Plan to Congress in January 2009 including

measures aimed at: providing a fiscal stimulus through expanded public spending programs;

ensuring sufficient liquidity in the financial system; ensuring access to financing for the

productive sectors; and accelerating the mobilization of external resources.2 Current expenditure,

up by 2.8 percent of GDP relative to 2008, included an expansion of the conditional cash transfer

as well as other social programs. Despite the crisis, the poverty rate further decreased from 38

percent in 2008 to 35 percent in 2009, and the Gini coefficient from 51 percent to 49 percent.

This is in stark contrast to the deep crisis in 2002 when the poverty rate was up 13 percentage

points relative to the previous year reaching 50 percent. The Government also remained

committed to prudent macroeconomic policies, with the fiscal balance closing in surplus in 2009

due to an increase in tax revenues.

Figure 1.2: Aggregate demand decomposition of

growth (percent annual contribution) 3

Figure 1.3: Sectoral decomposition of growth (percent

annual contribution)

Source: Central Bank of Paraguay

Table 1.1: Poverty and equity indicators

1997-

98 1999

2000-

01 2002 2003 2004 2005 2006* 2007 2008 2009 2010 2011

Poverty incidence

(% population) 36.1 37.3 36.8 49.7 44.0 41.3 38.6 43.7 41.2 37.9 35.1 34.7 32.4

Urban 22.5 24 23.7 39.7 37.4 35.5 34.4 35.3 33.6 30.2 24.7 24.7 23.9

Rural 51.6 52.6 52.1 62.7 52.5 48.9 44.2 55.3 51.8 48.8 49.8 48.9 44.8

Extreme poverty

incidence (% population) 18.8 17.7 16.7 24.4 21.2 18.3 16.5 23.7 23.2 19.0 18.8 19.4 18.0

Urban 7.2 5.9 6.7 13.1 13.4 12.2 10.7 14.9 15.4 10.6 9.3 10.3 10.0 Rural 32.0 31.4 28.2 39.2 31.2 26.2 24.3 35.9 34.0 30.9 32.4 32.4 29.6

GINI coefficient 48.9 53.6 53.8 53.3 54.6 52.0 51.0 52.2 52.5 50.6 48.7 51.2 52.0

urban 49.3 48.0 49.6 48.0 51.5 48.7 49.6 49.5 47.2 45.3 42.3 45.9 47.0 Rural 52.2 55.6 52.0 56.7 56.1 53.8 49.8 51.6 57.6 55.7 55.4 55.8 56.6

Unemployment 5.4 6.8 7.6 10.7 8.1 7.3 5.7 6.5 5.5 5.7 6.4 5.7 5.6

Note: 2006 data suffer methodological problems, including the delayed data collection for the household survey due

to DGEEC’s budget constraints. Source: Encuesta Permanente de Hogares (EPH), DGEEC.

2 See Annex 4. 3 GDP numbers as basis for this graph include the bi-national powerplants.

-15

-10

-5

0

5

10

15

20

25

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Percen

t

Private consumption Public consumption

Private Investment Public Investment

Exports Imports

Real GDP growth

-10

-5

0

5

10

15

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

Pe

rce

nt

Agriculture Cattle, forestry and fishingMining and manufacturing Electricity and waterConstruction ServicesValor agregado bruto

4

1.2. The economic stabilization program

At the core of the Government’s economic stabilization program was fiscal consolidation

that allowed for the reduction of the debt-to-GDP ratio and also kept inflation in check. After high public spending in the late 1990s and early 2000s, the Government’s consolidation

resulted in overall fiscal surpluses for the eight consecutive years between 2004 and 2011. These

surpluses averaged 1 percent of GDP. The combination of continuous surpluses and solid

economic growth also reduced the debt-to-GDP ratio from 41 percent in 2002 to 12 percent in

2012. Additionally, sound fiscal policies together with the Central Bank’s focus on price stability

resulted in single-digit inflation for most years.

Table 1.2: Paraguay’s fiscal accounts (percent of GDP)

Source: Ministerio de Hacienda

2005 2006 2007 2008 2009 2010 2011 2012

Total revenues 15.7 16.0 15.6 15.8 17.5 16.9 17.4 18.4

Current revenues 15.6 15.9 15.6 15.8 17.2 16.7 16.8 17.9

Tax revenues 10.1 10.5 10.1 10.7 11.6 12.0 12.1 12.3

Non-tax revenues 5.0 4.9 4.8 4.1 4.8 4.0 4.0 4.9

o/w contributions to pension fund 1.0 0.9 1.1 1.1 1.3 1.2 1.2 1.5

o/w royalties 3.1 3.1 2.9 2.3 2.9 2.1 2.1 2.7

Grants 0.1 0.1 0.3 0.3 0.1 0.0 0.0 0.0

Transfers 0.3 0.4 0.3 0.5 0.6 0.7 0.7 0.7

Capital revenues 0.1 0.1 0.0 0.0 0.3 0.2 0.6 0.4

Total expenditures and net lending 15.0 15.5 14.8 13.5 17.5 15.9 16.7 20.1

Total expenditures 15.0 15.6 14.8 13.6 17.5 15.9 16.7 20.1

Current expenditures 11.5 11.9 11.5 11.1 13.4 12.5 12.8 15.5

o/w personal services 6.2 6.5 6.4 6.5 7.7 7.3 7.4 9.3

o/w goods and services 1.0 1.1 1.0 0.9 1.3 1.4 1.5 1.6

o/w interest 1.0 0.9 0.7 0.6 0.5 0.4 0.3 0.2

o/w current transfers 3.3 3.3 3.3 3.1 3.7 3.4 3.6 4.3

Capital expenditures 3.5 3.7 3.3 2.5 4.1 3.4 3.9 4.7

o/w physical investment 2.7 2.6 2.2 1.5 2.6 2.4 2.2 2.5

Net lending -0.1 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Overall balance 0.7 0.4 0.9 2.3 0.1 1.0 0.7 -1.7

Primary balance 1.7 1.3 1.6 2.8 0.6 1.4 1.0 -1.5

5

Figure 1.4: Revenues and expenditures Figure 1.5: Fiscal balance

Source: Ministerio de Hacienda Source: Ministerio de Hacienda

The Government’s stabilization program focused first on immediate macro-economic

imbalances and since 2006 has shifted towards medium-term growth and institutional

issues.4

Immediately after the crisis, the Government addressed fiscal consolidation on the

revenue and expenditure sides. Major reforms from 2003 to 2005 included the reform of the

public pension scheme in late 2003 together with restrictions on employment and wage increases

within selected sectors; a tax policy reform and a new legal framework for revenue

administration were implemented in 2004 as was a new customs code. Financial sector reform

started in 2003 with the adaption of the bank resolution law and the adoption of regulations by

the BCP Board of Directors on asset classification, provisioning requirements, and imputation of

accrued interest, followed by the adaption of the public banking law in 2005. As it became clear

in 2005 that the economy had been stabilized, the Government shifted focus towards structural

reforms with the objective of fostering economic growth while continuing with reforms aimed at

sustaining stability. Reforms in this second phase included: the oversight mandate of state-owned

enterprises; internal control mechanisms in the public sector; and the introduction of the

conditional cash transfer program: Tekopora in 2005; and its subsequent expansion.

4 For a comprehensive description please refer to IMF (2009).

0

5

10

15

20

25

198

0

198

2

198

4

198

6

198

8

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

Per

cen

t o

f G

DP

Revenues/GDP Expenditures/GDP

-6

-4

-2

0

2

4

6

198

01

98

21

98

41

98

61

98

81

99

01

99

21

99

41

99

61

99

82

00

02

00

22

00

42

00

62

00

82

01

02

01

2

Per

cem

t o

f G

DP

Fiscal balance/GDP Primary balance/GDP

6

Figure 1.6: Public debt Figure 1.7: Inflation (CPI, period average)

Source: BCP Source: BCP

1.3. The development dividend of stabilization

The stabilization generated the environment for the private sector to invest with greater

confidence and grow. In the period from 2003 to 2008, investment ratios as a percentage of

GDP increased from 15 percent to 18 percent respectively. This development was partly reversed

as a result of the 2009 crisis when private investment dropped to 17 percent of GDP, but it has

been recovering since then. FDI inflows have also stabilized over the same period and

unemployment dropped from 8.1 percent in 2003 to 5.6 percent in 2011.

Figure 1.8: Public and private investment Figure 1.9: Net capital inflows

Source: BCP Source: BCP

The development dividend of this stabilization was mainly a reduction in poverty;

prosperity that was broadly shared for the most part; and a modest improvement in

inequality. Real per capita GDP increased by 22 percent between 2003 and 2011. Compared to

the crisis years of 2002 and 2003, poverty fell significantly from 49.7 percent and 44 percent

respectively, to 32.4 percent in 2011. Progress in terms of extreme poverty is similarly

significant with rates dropping from 24.4 percent in 2002 to 18 percent in 2011 (Table 1.1).

0

10

20

30

40

50

199

11

99

21

99

31

99

41

99

51

99

61

99

71

99

81

99

92

00

02

00

12

00

22

00

32

00

42

00

52

00

62

00

72

00

82

00

92

01

02

01

12

01

2

Per

cen

t

External Debt/GDP Domestic Debt/GDP

0

5

10

15

20

25

30

35

40

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

Per

cen

t

0

5

10

15

20

25

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Pe

rce

nt

of

GD

P

Public investment Private investment

-5

0

5

10

15

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Pe

rce

nt

of

GD

P

Foreign direct investment Portfolio investmentDerivatives Other investmentTotal

7

Between 2004 and 2011 the bottom 40 percent of the population5 also shared in this economic

growth. Their household income grew by 4.6 percent on average compared to the 3.3 percent

average for the overall population. Yet, three caveats apply to this overall positive development:

(i) income growth of the bottom 40 percent was lower than the regional average, and particularly

than that of neighboring countries; (ii) inequality among this bottom 40 percent has increased;

and (iii) recovery after the 2009 crisis was not as strong for the bottom 40 percent as it was for

the rest of the population and thus, overall inequality has risen since then. Compared to 2003,

Paraguay also witnessed a moderate reduction in inequality with the Gini coefficient falling from

0.55 in 2003 to 0.52 in 2011. It had actually dropped to 0.487 by 2009, but the crisis that year

reversed the positive benefits of this reduction and it rose to 0.52 by 2011.

Despite these critical advances, stabilization and structural reforms could not dispel a

number of major challenges so that the continuation and deepening of the reform effort

will be essential to fully unlock Paraguay’s productivity. In contrast to other Latin American

countries, as for example Peru, stabilization and structural reforms could not reduce the volatility

of the macro-economic environment in Paraguay, where volatility had in fact increased in recent

years In addition, fiscal resources remain limited and are constraining spending on human

development and growth-enhancing policies. Poverty and inequality in Paraguay remain among

the highest in the region. The next three sections describe these three major challenges.

1.4. Challenge 1: Volatile macroeconomic environment

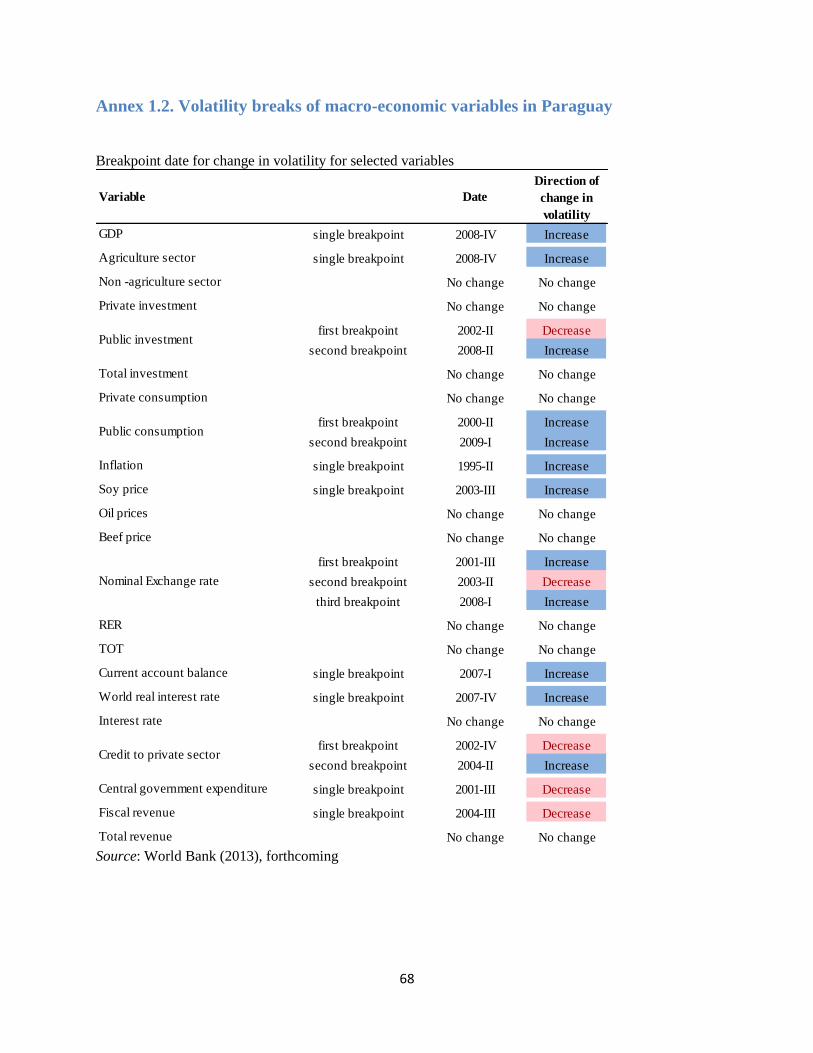

A first key challenge for public financial management in Paraguay is the increase in

volatility of GDP growth, rendering it one of the most volatile economies in the region. In

contrast, many other countries in the region have managed to reduce volatility. In the period

from 1960 to 2000 Paraguay’s volatility was significantly below the regional mean and median,

yet in the last decade it has been above (see Table Annex 1.1). In addition, it is not only

economic growth that has become more volatile: most macroeconomic variables in Paraguay

currently share this pattern, and this poses a challenge to fiscal policy by rendering revenue and

expenditure forecasting more difficult. It also increases the risks of pro-cyclicality of fiscal

policies (see Table Annex 1.2).

The increase in volatility is concerning and needs to be understood thoroughly given its

significant costs in terms of welfare, economic growth, and equality.6 World Bank (2013)

provides an in depth analysis of the sources, effects, and options for managing volatility.

Designing policies that help mitigate the impact of shocks to the economy and that help increase

a country’s resilience is particularly relevant in the light of increased volatility. They are also

5 The time period is dictated by the availability of comparable data. For more details on the topic please refer to

Lopez-Calva, Lugo, and Barriga Cabanillas (2013) forthcoming. 6 A comprehensive economic literature has documented these impacts; for example Loayza, Ranciere, Serven, and

Ventura (2007), Athanasoulis and van Wincoop (2000), World Bank (2000) on the impact of volatility on welfare,

Hnatkovska and Loayza (2005) and Calderon and Schmitt-Hebbel (2003) and Berument, Dincer, and Mustafaoglu

(2011) on the growth impact, and Breen and Garcia Penalosa (2004), Garcia-Penalosa and Turnovsky (2004), or

Huang, Fang and Miller (2012) for the impact on equality.

8

important because Paraguay still has a low per capita income compared to its neighbors and

suffers from a persistent high degree of inequality and poverty.

1.5. Challenge 2: Limited fiscal resources that constrain spending on

human development and growth-enhancing policies

The inability to raise tax revenues has resulted in low levels of spending in social sectors

and infrastructure. Despite important improvements on the back of fiscal policy and

administration reforms, Paraguay is characterized by a low tax to GDP ratio by international

standards. It undershoots by a large margin the tax to GDP ratio of its MERCOSUR neighbors;

the ratios in Argentina and Brazil are twice as high as in Paraguay. Compared to all relevant peer

groups, be it lower middle income countries (MICs), Latin American and Caribbean countries, or

countries that have similar characteristics in terms of GDP per capita and population, Paraguay

collects very little in the way of taxes (see Figure 1.9).7 In this environment fiscal surpluses for

eight consecutive years from 2004 to 2011 explain relative caution when it comes to spending.

Despite fast growth in recent years, social expenditure in Paraguay is lower than in comparator

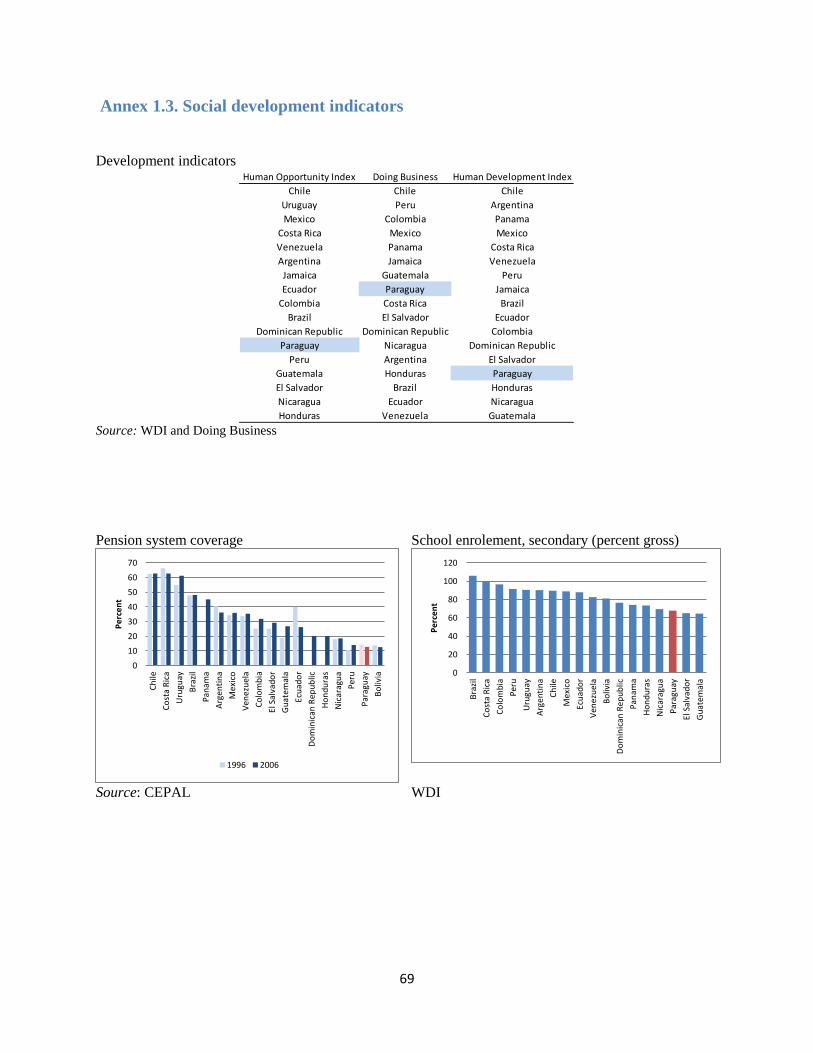

countries (Figure 1.11) and overall outcomes of social services are also improving at a slower

pace than in other countries. This explains Paraguay’s weak performance in terms of the Human

Development Indicator and other social development indicators (see Annex 1.3 for details).

Lack of disaggregated data on social spending and outcomes limits the ability to assess the

efficiency of public spending. Both in health and education, around 80 percent of expenditure is

classified as alcance nacional - spending at the national level. Attribution to specific departments

7 The peer group of countries with similar GDP and population characteristics comprises the ten countries for which

the equally weighted average of Population and GDP per capita is closest to Paraguay. The countries are: Bolivia,

Bulgaria, El Salvador, Georgia, Honduras, Jordan, Nicaragua, Papua New Guinea, Serbia, and Turkmenistan.

Figure 1.10: Tax-to-GDP ratio 2011 Figure 1.11: Social Expenditure

Source: SET and USAID Source: CEPAL (2009-2011)

0

5

10

15

20

25

30

35

Par

aguay

Arg

enti

na

Bra

zil

Uru

gu

ay

Ho

ndu

ras

Ser

bia

Ecu

ado

r

Geo

rgia

Gu

atem

ala

LM

ICs

UM

ICs

Lac

Per

cen

t o

f G

DP

0

5

10

15

20

25

30

35

Arg

enti

na

Boli

via

Bra

zil

Bulg

aria

El

Sal

vad

or

Ho

ndu

ras

Nic

arag

ua

Par

aguay

Ser

bia

Uru

gu

ay

LA

C

Per

cen

t o

f G

DP

9

is only possible for 20 percent of all expenditures. Outcome data is also very limited at the

departmental level, which constrains analysis of the efficiency of public spending at this level.8

In the case of education, the national attainment test SNEPE is only representative at the national

level, so that education outcomes at the departmental level cannot be assessed. This is a serious

limitation as the discourse about performance between different departments offers an excellent

opportunity to understand differences in the administration and processes and the exchange of

best practices. A further limitation to assessing the efficiency of public spending in education in

Paraguay is that the country does not participate in international tests that would allow

comparison with other countries.

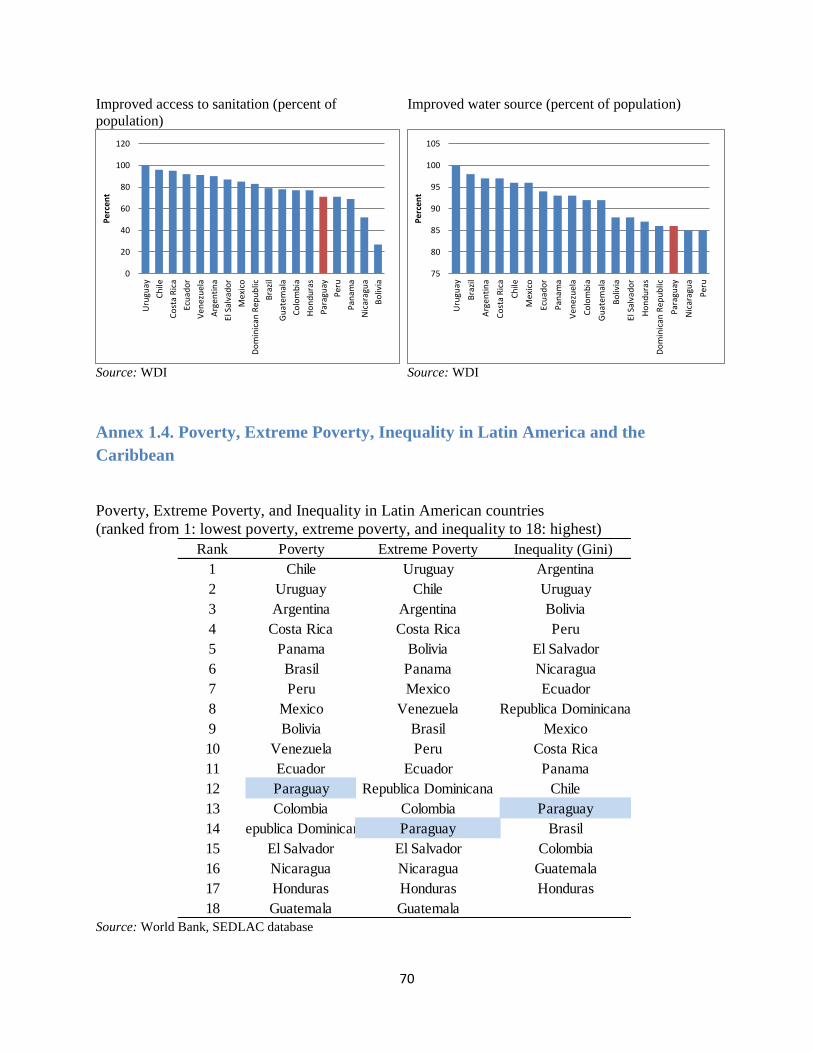

1.6. Challenge 3: High levels of poverty and inequality remain

Despite significant improvements over the past decade, Paraguay’s poverty rates and

inequality remains among the highest in Latin America and the Caribbean—the most

unequal region in the World (Annex 1.4). A major reason behind the still high poverty and

inequality is the negative impact that continuous crises between 1998 and 2002 have had on the

population. Compared to the 2002 crisis, the 2009 crisis had only a minor impact, partly due to

Government intervention that buffered the effects. As a result, overall achievements in Paraguay

appear modest, when comparing current poverty numbers with the pre-crisis year of 1997 when

poverty was at 36.1 percent and extreme poverty at 18.8. In terms of equality, results look less

favorable, with the Gini coefficient at 0.52 in 2011 exceeding that of 0.49 in 1997.

This third challenge is closely linked to the two other challenges, through the negative

impact of volatility on poverty reduction and inequality and the question of redistribution.

As argued in Lopez-Calva, Lugo, and Barriga Cabanilas (2013), the high degree of volatility

may be the weak link between solid average growth performance and employment generation.

The uncertainty resulting from volatile economic growth may reduce the incentive for firms to

employ new staff. Also, persistently high levels of inequality may be linked to high volatility

because citizens at the lower end of the income distribution have reduced access to insurance

mechanisms and therefore suffer more from negative shocks. Together, lagging employment

generation and continued high levels of inequality pose important challenges for Paraguay in the

eradication of extreme poverty. In terms of redistribution, the question is whether tax and

expenditure policies have contributed to income redistribution from high- to low-income

households in a well-targeted manner, and to what extent fiscal policy has contributed to

reducing poverty and inequality.

1.7. Transparency and data availability

The PER supported the government’s efforts to improve the transparency of economic

data through three key tools: (i) the BOOST database of comprehensive treasury data; (ii)

the Social Accountability Matrix; and (iii) the Computable General Equilibrium Model.

Each of these tools was developed as part of the PER and served as the basis for the analysis

presented in the following chapters. But their usefulness reaches beyond this report, as they can

8 For more information on data issues, please see Box 2 in Chapter 4.

10

be used by the government for a number of analytical purposes and contribute to improved

transparency and accountability.

The publication of a BOOST database represents a significant policy change towards

greater transparency of fiscal data. Available through the Ministry of Finance’s website9, the

BOOST platform provides disaggregated budget data for all levels of government in a user-

friendly format for the years 2003 to 2012. Paraguay is the first country in Latin America and the

Caribbean, and the fourth in the world to release budget data to the public using BOOST. The

tool supports government efforts to improve the quality of expenditure analysis, and shows the

government’s commitment towards greater budget transparency. The preparation of the platform

has also contributed to capacity building in the Ministry of Finance as well as to improved

information exchange within the Ministry and with the line ministries.

The preparation and planned publication of a well-documented and updated social

accountability matrix is also an important milestone. The background work for this PER

contains the preparation of a social accountability matrix as a key ingredient of a computable

general equilibrium model. The social accountability matrix has been prepared in close

collaboration with the Ministry of Finance and the Central Bank. It includes data from

Paraguay’s National Accounts, Fiscal Accounts, Balance of Payments, and Permanent

Household Survey, and builds on an Input-Output Table created by the Central Bank.10

The

publication of the matrix in itself will be another step towards greater transparency in Paraguay

and is expected to facilitate future research.

The dynamic-recursive computable general equilibrium (CGE) model allows the

government to assess the distributional and poverty impact of different policy alternatives.

The CGE model is complemented by a microsimulation model that translates the CGE results

into poverty and inequality outcomes. The model makes it possible to estimate how government

spending and taxation, foreign aid, and exogenous conditions (including world markets) together

influence and are influenced by human development.11

For both the social accountability matrix

and the preparation of the computable general equilibrium model, an important element of

capacity building has taken place and builds the basis for future collaboration. At the same time,

further improvements in data quality and availability would be important for enhanced policy

making (see Box 2 in Chapter 4 for more detail).

1.8. Objective, methodology, and the value added of this PER

Has fiscal policy served the purpose of reducing poverty and sharing prosperity? This is the

overarching question that the current PER seeks to answer in light of the developments of the

past decade and the remaining major challenges. Based on the findings related to this question

9 http://www.openlooksolutions.com/boost_paraguay/.

10 The Input-Output Table is for 1994 and was created by the Central Bank of Paraguay, which is the only official

provider of the data and is in charge of the collection and processing of National Accounts data. 11

For more information on the Social Accountability Matrix and the CGE model, see Chapter 4 of Volume II of this

report.

11

the study aims to trigger a public debate about the optimality of tax and expenditure policies for

Paraguay.

This PER has been prepared at the request of the Paraguayan authorities and in close

collaboration with them, based on a variety of economic and econometric techniques. While

this first volume of the report presents the overall storyline of the challenges to fiscal policy in

Paraguay and discusses policy options to address them. The second volume presents the research

papers that have been prepared as a background to this report in the course of the past two years.

The background papers rely on a variety of economic and econometric techniques, including

VAT estimation, incidence analysis, and the construction of a computable general equilibrium

model. Both the preparation of the BOOST database and of the social accountability matrix are

contributions of this report. The preparation of this report would not have been possible without

the invaluable collaboration with the Ministry of Finance and the Central Bank of Paraguay.

The report provides an overall narrative of remaining challenges for fiscal policy in

Paraguay and a discussion of policy options to address them. To this end, the PER pulls

together existing literature on fiscal policies and economic growth in Paraguay and combines it

with new analysis in the form of background papers presented in volume 2 of the report.

Another contribution is the quantification of characteristics of fiscal policy in Paraguay

that are generally known but have so far eluded discussion due to the lack of concrete

numbers and comparisons. The benefit of providing quantitative analysis for topics that are

widely recognized in Paraguay is that it pulls them into the arena of public discourse. Examples

of such topics in the context of the present PER are: the quantification and international

comparison of the regressivity and progressivity of taxation and expenditures; the quantification

of the dependence of children’s access to public services based on their parents’ socio-economic

background; and the quantification of tax expenditures.

12

Chapter 2: Public Finances in a commodity driven economy

While prudent fiscal policy allowed for macroeconomic stabilization, it also led to low levels of

public spending given limited fiscal resources. Still today, Paraguay is characterized by a low

tax-to-GDP ratio by international standards. A tax reform in 2004 could not generate significant

additional revenues for three main reasons: (i) it failed to introduce taxation in the agricultural

sector proportional to its share of GDP; (ii) significant tax exemptions weakened some reform

measures and still do, as in the case of reformed corporate income tax in the agricultural sector

(IMAGRO); and (iii) some reform measures were not implemented for a long time, for example

the personal income tax. In addition, the reform did not change the actual structure of the tax

system, especially with regard to indirect taxes. In fact, reliance on indirect taxes has increased

over time rendering the system even more regressive than before. While this insulates public

revenues from economic volatility to a certain extent, it imposes high costs associated with

sufficiency and equity of the system. As a result, the current structure of the tax system appears

suboptimal: Other policy tools such as a fiscal rule or a stabilization fund could be used to

manage volatility, and the regressivity is particularly harmful in an economy with high poverty

rates. While the full implementation of the 2004 tax reform could still raise tax revenues,

adequate taxation of the agricultural sector is needed to level the playing field for business

development in all sectors and to address the insufficiency of taxes. An additional source of

fiscal resources would be the elimination of significant tax exemptions. Some of these would

have to be accompanied by targeted spending increases to off-set the potential negative effect on

poverty. This could help Paraguay generate the fiscal resources necessary to increase spending

on infrastructure and on the social sectors and to implement countercyclical fiscal policies. In

terms of expenditures, and in light of the recent expansionary fiscal stance, it appears important

to ensure that fiscal prudence is considered a continuous task. Only if the Government is able to

sustain fiscal prudence in the future, will it be able to maintain macroeconomic stabilization and

performance.

This chapter is structured as follows: section 2.1 provides an overview of the fiscal consolidation

with limited fiscal resources covering the resulting structure of revenues. Section 2.2 describes

the links between fiscal policy and macro-economic volatility. Section 2.3 gives an overview of

the current structure of expenditures, kept brief to avoid overlap with the presentation of social

spending and human development outcomes in sections 1.5 and in Chapters 3 and 4. Section 2.4

concludes with policy recommendations emerging from the findings.

2.1 Fiscal consolidation with limited fiscal resources—the genesis of the

current revenue structure

The Government addressed fiscal consolidation from the perspectives of revenue and

spending, however the main adjustments fell onto spending due to limited revenue

increases. On the revenue side, major changes included the tax policy reform and a new legal

framework for revenue administration. These were implemented in 2004, as was a new customs

code. Yet, the results in terms of additional revenue collection were limited with the tax-to-GDP

13

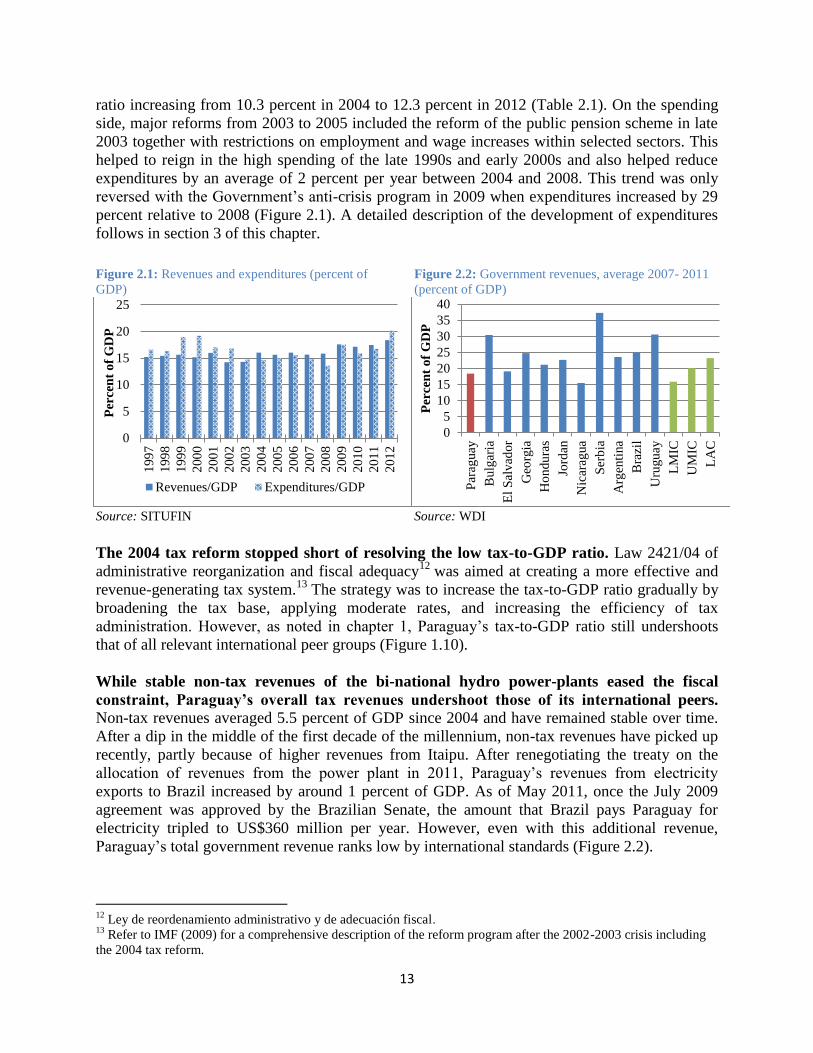

ratio increasing from 10.3 percent in 2004 to 12.3 percent in 2012 (Table 2.1). On the spending

side, major reforms from 2003 to 2005 included the reform of the public pension scheme in late

2003 together with restrictions on employment and wage increases within selected sectors. This

helped to reign in the high spending of the late 1990s and early 2000s and also helped reduce

expenditures by an average of 2 percent per year between 2004 and 2008. This trend was only

reversed with the Government’s anti-crisis program in 2009 when expenditures increased by 29

percent relative to 2008 (Figure 2.1). A detailed description of the development of expenditures

follows in section 3 of this chapter.

The 2004 tax reform stopped short of resolving the low tax-to-GDP ratio. Law 2421/04 of

administrative reorganization and fiscal adequacy12

was aimed at creating a more effective and

revenue-generating tax system.13

The strategy was to increase the tax-to-GDP ratio gradually by

broadening the tax base, applying moderate rates, and increasing the efficiency of tax

administration. However, as noted in chapter 1, Paraguay’s tax-to-GDP ratio still undershoots

that of all relevant international peer groups (Figure 1.10).

While stable non-tax revenues of the bi-national hydro power-plants eased the fiscal

constraint, Paraguay’s overall tax revenues undershoot those of its international peers.

Non-tax revenues averaged 5.5 percent of GDP since 2004 and have remained stable over time.

After a dip in the middle of the first decade of the millennium, non-tax revenues have picked up

recently, partly because of higher revenues from Itaipu. After renegotiating the treaty on the

allocation of revenues from the power plant in 2011, Paraguay’s revenues from electricity

exports to Brazil increased by around 1 percent of GDP. As of May 2011, once the July 2009

agreement was approved by the Brazilian Senate, the amount that Brazil pays Paraguay for

electricity tripled to US$360 million per year. However, even with this additional revenue,

Paraguay’s total government revenue ranks low by international standards (Figure 2.2).

12

Ley de reordenamiento administrativo y de adecuación fiscal. 13

Refer to IMF (2009) for a comprehensive description of the reform program after the 2002-2003 crisis including

the 2004 tax reform.

Figure 2.1: Revenues and expenditures (percent of

GDP)

Figure 2.2: Government revenues, average 2007- 2011

(percent of GDP)

Source: SITUFIN Source: WDI

0

5

10

15

20

25

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

Per

cen

t o

f G

DP

Revenues/GDP Expenditures/GDP

0

5

10

15

20

25

30

35

40

Par

aguay

Bulg

aria

El

Sal

vad

or

Geo

rgia

Ho

ndu

ras

Jord

an

Nic

arag

ua

Ser

bia

Arg

enti

na

Bra

zil

Uru

gu

ay

LM

IC

UM

IC

LA

C

Per

cen

t o

f G

DP

14

Box 1. Royalties from bi-national power plants

Royalties from the bi-national hydropower plants at Itaipu and Yacyreta have accounted for between 2

and 3 percent of GDP between 2005 and 2012, equivalent to between 15 and 20 percent of total revenue.

With the renegotiation of royalties from the bi-national hydroelectric power plant Itaipu, revenues have

increased by around 1 percent of GDP to reach US$ 360 million. In September 2012, the government set

up the Fondo Nacional de Inversion Publica y de Desarollo (FONACIDE) to channel this additional

revenue from the binationals to education, health and infrastructure. Some existing projections vary in a