a purchasing intention audit of the audience of powder/bulk solids portrait of respondents

TRANSCRIPT

A Purchasing Intention Auditof the Audience of Powder/Bulk Solids

Portrait of Respondents

• Prepared by third party research firm, Martin Akel & Associates, Chester, NJ

• Survey sent to combined audience of Powder/Bulk Solids magazine, recipients of PBS newsletters, and visitors of powderbulksolids.com

• 1,240 returns for a 95% confidence level

Methodology

Survey Methodology/Responses

Portrait of Respondents by End Market

Chemicals32%

Food/Beverage23%

Other45%

Portrait of Respondents

PBS represents the key markets

Portrait of Respondents by Job Title

Portrait of Respondents

Engineers compose the largest job segment

39.7%

20.7%

16.2%

9.7%

3.5%

10.2%

% Engineering

% Production, Plant Operations, Maintenance

% R&D/Quality Control

% Administration

% Purchasing

% Other

Portrait of Respondents

• Over 90% indicated involvement in product adoption decisions

• Decisions/recommendations are extensive– More than half (55%) impact purchasing enterprise wide– 91% make decisions affecting entire department, division,

or wider• Enterprise wide (multiple sites) 55.2%

• Division or department 90.8%

• PBS audience members influence an average of 5.3 plants; among engineering titles, 6.6 plants

Portrait of Respondents

Readers are highly involved in purchasing decisions

Conclusion

• PBS audience represents professionals who are heavily involved in technology decisions

• PBS readers represent key decision makers for suppliers of products, equipment, and systems

Portrait of Respondents

Technology Investment Trends

Technology Investment

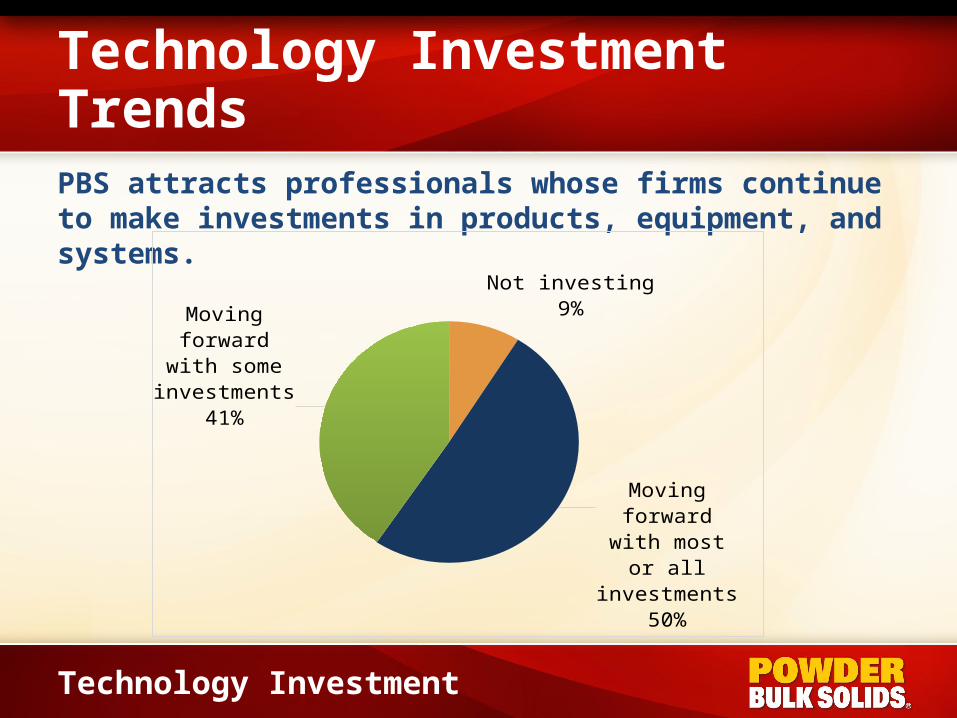

PBS attracts professionals whose firms continue to make investments in products, equipment, and systems.

Not investing9%

Moving forward with most or all

investments50%

Moving forward with some in-

vestments41%

Attitudes: Technological Investments

• “Aggressive. 15% increase in business for the next 5 years.”

• “My firm is actively investing in new capital projects to go after business avenues created by government regs”

• “Our company is taking aggressive steps in investing in production equipment”

• “Now is the time to invest in the future – the strong will prosper.”

• “If a strong business case is presented, then the investment is approved.”

Technology Investment

Comments from respondents about future growth plans.

Age & Technological Capabilities

of Major Systems

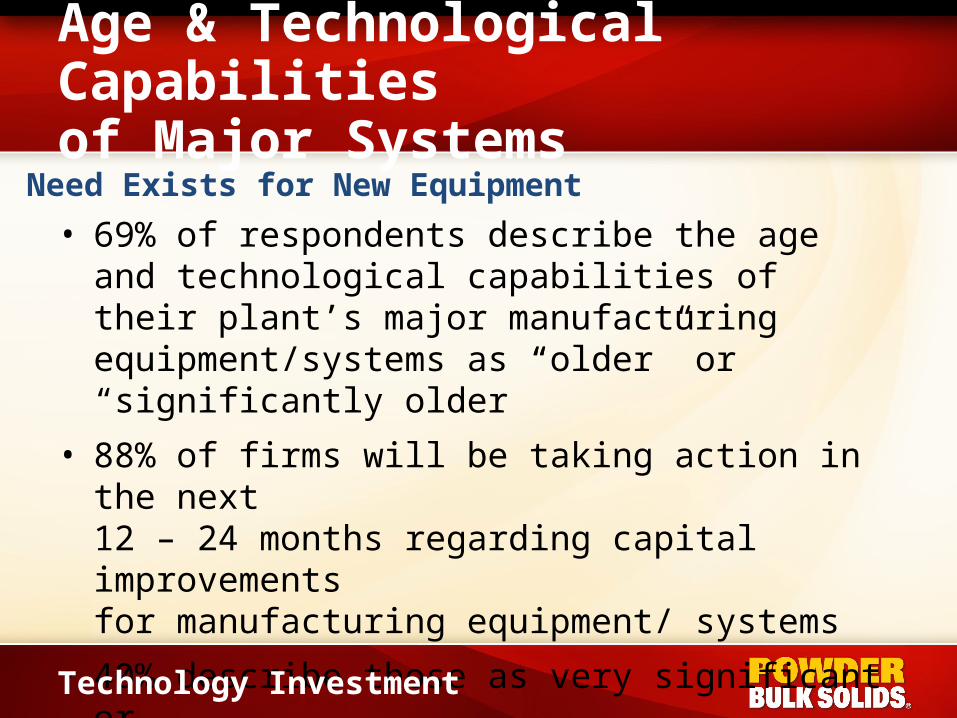

• 69% of respondents describe the age and technological capabilities of their plant’s major manufacturing equipment/systems as “older” or “significantly older”

• 88% of firms will be taking action in the next 12 – 24 months regarding capital improvements for manufacturing equipment/ systems

• 40% describe those as very significant or significant improvements

Technology Investment

Need Exists for New Equipment

Plant Construction /Modernization

With

in 6

mos.

With

in 1

2 mos.

With

in 2

4 mos.

Beyond 2

4 ...

Start

within

24...

No curre

nt p...

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0% 30.9%

26.2%

11.1%

6.7%

20.3%

15.0%

Technology Investment

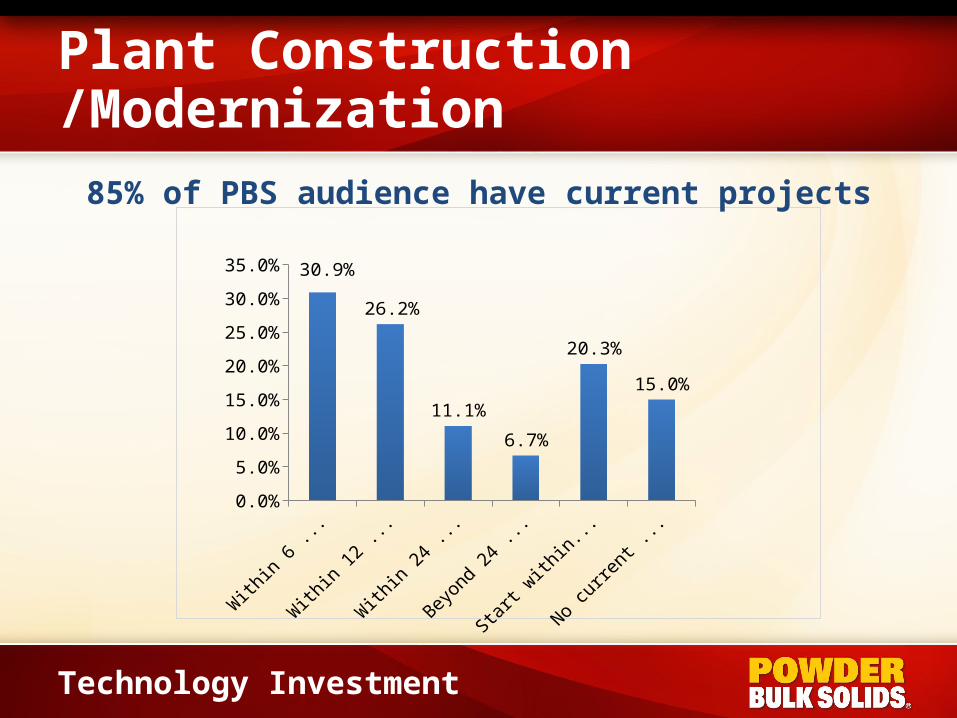

85% of PBS audience have current projects

Conclusion

• PBS attracts professionals at organizations that continue to invest in new products, equipment, and systems

• Their organizations recognize the importance of making necessary investments such as additional product lines, capital investments, and new plants and plant modernization

• Suppliers seeking to identify where potential new sales will come from will find a substantial number of buyers across the PBS audience

Technology Investment

Early Phase Middle Phase Final Phase

52.7%45.6%

22.3%

Purchasing

Purchasing

76% of audience is currently involved in the purchasing process. Projects range from being in early, middle or late phases.

Projected Expenditures

0

Less than $25K

$25K - 49K

$50K - 99K

$100K - $249K

$250K - 499K

$500K - 999K

$1 mil - 2.9 mil

$3 mil - 4.9 mil

$5 mil - 9.9 mil

$10 mil - 19.9 mil

$20 mil - 29.9 mil

$30 mil - 39.9 mil

$40 mil - 49.9 mil

$50 mil or more

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

8.0%11.5%

6.5%

8.8%

13.4%

8.4%

16.1%

10.7%

4.6%

2.3%

6.5%

0.4%

0.8%

0.0%

1.9%

Purchasing

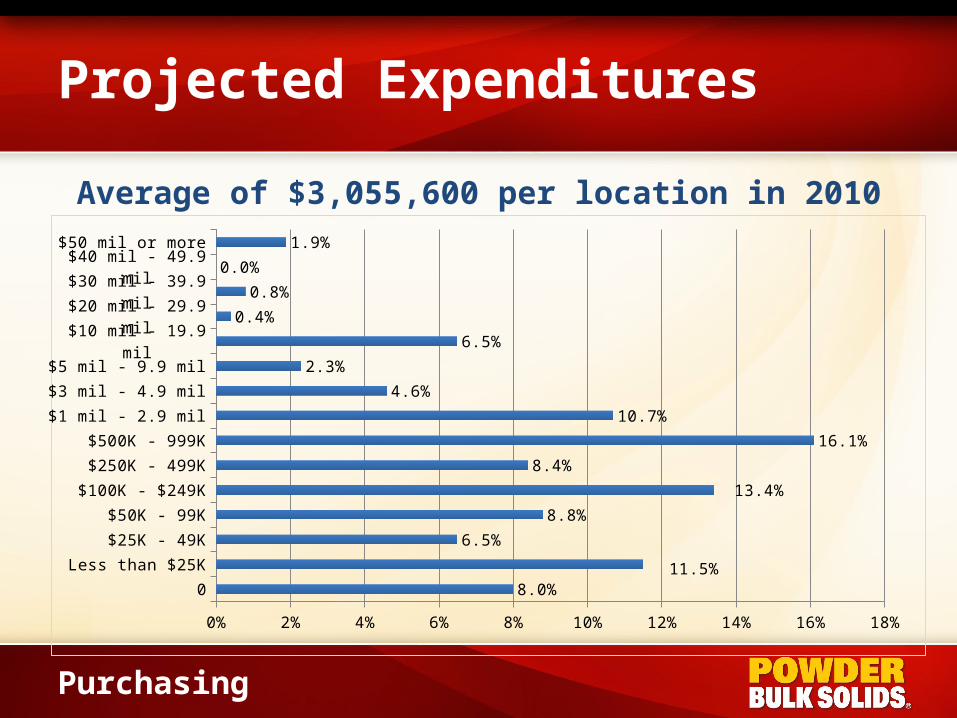

Average of $3,055,600 per location in 2010

Projected Expenditures

• 44% foresee expenditure increases for ALL dry processing-related technology and services

• 50% foresee expenditures to stay the same

• Only 8% forecast declines

• Net change will be +17.5%

Purchasing

Expenditure increases anticipated

Audience Usage by Product CategoryProduct % Using This Category % with Purchasing Plans in 24 mos.

Drying & thermal solids processors 54.2 46.4

Dust collection & air pollution control equipment 85.4 57.6

Feeders 76.7 57.0

Instrumentation & control equipment 93.0 74.9

Material handling & transportation 88.2 56.9

Mechanical conveying equipment 81.8 59.7

Mixers & blenders 80.2 45.4

Packaging & bagging products/equipment 73.8 55.8

Particle enlargers & formers 27.2 30.6

Pneumatic conveying equipment 69.3 48.1

Screening & separation equipment 67.8 46.4

Size reduction equipment 58.0 39.7

Storage equipment 80.5 39.7

Valves, gates, & airlocks 85.3 70.2

Weighing systems & scales 91.4 41.7

Purchasing

2010 Expenditures by Product CategoryProduct % with 2010 Expenditures Avg. Expenditure per Subscriber

Drying & thermal solids processors 28.9 $476,900

Dust collection & air pollution control equipment 57.0 $252,380

Feeders 44.4 $117,950

Instrumentation & control equipment 74.8 $309,890

Material handling & transportation 58.7 $243,970

Mechanical conveying equipment 49.4 $261,330

Mixers & blenders 42.9 $194,420

Packaging & bagging products/equipment 44.0 $308,170

Particle enlargers & formers 10.7 $191,780

Pneumatic conveying equipment 39.9 $327.660

Screening & separation equipment 34.0 $143,640

Size reduction equipment 23.2 $216,970

Storage equipment 39.9 $337,000

Valves, gates, & airlocks 61.9 $133,160

Weighing systems & scales 58.6 $180,340

Purchasing

Expenditure Projections

Product Projected Average Total 2010 Expenditures

Drying & thermal solids processors $2,133,000,000

Dust collection & air pollution control equipment $2,266,000,000

Feeders $784,000,000

Instrumentation & control equipment $3,728,000,000

Material handling & transportation $2,286,000,000

Mechanical conveying equipment $2,094,000,000

Mixers & blenders $1,337,000,000

Packaging & bagging products/equipment $2,133,000,000

Particle enlargers & formers $143,000,000

Pneumatic conveying equipment $2,150,000,000

Screening & separation equipment $719,000,000

Size reduction equipment $834,000,000

Storage equipment $1,928,000,000

Valves, gates, & airlocks $1,323,000,000

Weighing systems & scales $1,379,000,000

Purchasing

Conclusions

• Through PBS, you reach professionals who have serious purchasing intentions for 2010 and 2011

• PBS’s technology-focused editorial is proven to attract those who represent primary purchasing targets for suppliers

Purchasing

Public

atio

ns

Directo

ries

E-new

slette

rs

Newsle

tters

Whi

te p

aper

s

Web

sites

Other

dig

ital m

edia

Trade

show

s

Other

med

ia d

evice

s0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%98.2%

54.0%49.3%

25.9%

40.2%

97.1%

70.2%

80.9%

52.0%

Use of Media

Use of Media

How do professionals stay current? Publications are still the top choice.

Print magazinesDigital magazines

DirectoriesE-newsletters

Print newslettersWhite papers

Websites from magazines

Websites from associa-tions

Websites from online only providers

Supplier websitesSearch engines

RSS feedsWebinars

Online videosPodcasts

BlogsVirtual trade shows

Work-related social mediaGeneral social media

Trade showsConferences

Mobile devicesDVD/CDs

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%80.3%

55.0%54.0%

49.3%25.9%

40.2%58.9%

44.6%24.4%

76.6%66.7%

15.4%47.6%

31.0%7.4%7.6%

12.1%11.3%

13.8%73.3%

50.5%16.8%

44.8%

Use of Media

Use of Media

The types of media have increased

Trend in Time Spent with Media

Use of Media

75% spend more time with all media than 3-4 yrs ago

Increase; 74.5%

No change; 17.0%

Decrease; 8.5%

Desirability of Print Magazines

• Reliable way to be updated 70.7%

• Portable 67.7%

• Tangible 62.2%

• Convenient 57.7%

• Very visual 57.5%

• Random access 45.4%

• Easy to save 42.9%

• Less time on computer 35.3%

• Write notes, highlights 34.2%

• Personal and relevant 18.5%

• Do not find print pubs desirable 4.6%

Use of Media

95% of professionals studied find print publications desirable for the following reasons

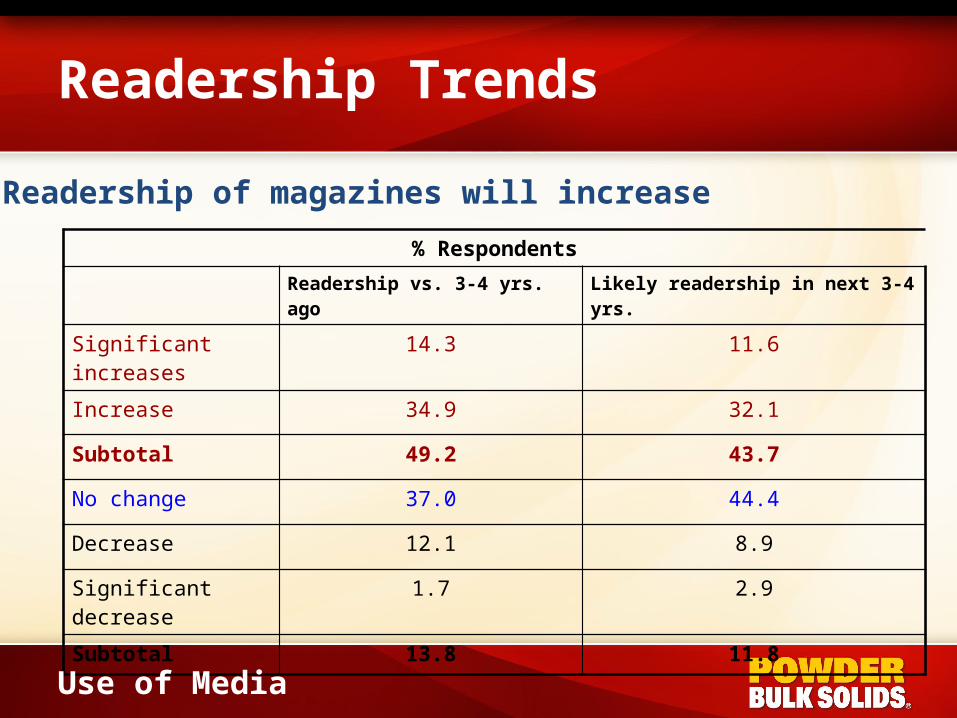

Readership Trends

% Respondents

Readership vs. 3-4 yrs. ago Likely readership in next 3-4 yrs.

Significant increases 14.3 11.6

Increase 34.9 32.1

Subtotal 49.2 43.7

No change 37.0 44.4

Decrease 12.1 8.9

Significant decrease 1.7 2.9

Subtotal 13.8 11.8

Use of Media

Readership of magazines will increase

Why do they read your ads?

% Respondents

Alert me to potential solutions 76.7%

Alert me to new suppliers 60.2%

Help position individual suppliers in my mind 59.0%

Continuing education on current technologies 51.0%

Information to request/access more details 52.5%

Alert me to changes at suppliers 50.4%

Ads are a quick way to stay current 30.6%

Keep me up-to-date on new models/upgrades 18.3%

Do not find ads worthwhile 3%

Use of Media

97% find advertising to be desirable

Conclusion

• All professionals continue reading publications; readership remains strong

• Professionals value publication advertising because it alerts them to potential solutions

• Despite some opinions, magazines and magazine advertising continue to be highly effective media for contacting primary customers and prospects

Use of Media

Mag

azin

es

Searc

h en

gine

s

Suppl

ier w

ebsit

es

Print d

irecto

ries

Mag

azin

e web

sites

E-new

slette

rs

Sales

reps

Trade

show

s

Unaffil

iate

d web

sites

Direct

mai

l

Other

dig

ital m

edia

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Mention #1

Mention #1 or 2

How different media are used

Use of Media

Media via which professionals first learn about new products/services—Magazines are the top choice

Media by which professionals first learn about new products/suppliers (version 2)

Average score (ranked 1 as highest)

Articles & ads in magazines 2.7

Search engines 3.8

Websites from suppliers 4.2

Trade shows 4.3

Sales reps 4.5

Websites from magazines 4.8

Printed directories/buyer’s guides 4.9

E-newsletters 5.3

Direct mail from suppliers 5.3

Unaffiliated websites 5.5

Other digital media (blogs, videos, etc.) 5.9

Use of Media

43.1%

7.8%6.7%

31.3%

5.3%

2.9% 2.9%

Magazine articles/adsE-newslettersMagazine websitesSearch enginesTrade showsOther websitesDirect mail

Professionals first learn about supplier websites

Use of Media

58% chose either publications, their newsletters, or websites

Which suppliers are investigated?

• 74% are likely to investigate companies they’ve become familiar with via communications programs

• 46% are likely to seek more information from suppliers they’ve heard of but are not familiar with

• Only 33% are likely to do so with suppliers they’ve never heard of

• Branding of companies and products prior to use of search engine marketing is essential

Use of Media

Suppliers with communications programs

Multiple media helps brand adoption

• 75% believe multiple media make them more likely to remain aware of the supplier

• 76% are more likely to contact suppliers that use multiple media when beginning to evaluate that class of product

Use of Media

Multiple media improves branding

% Respondents that believe multimedia assists them during the brand adoption process

Much more likely

More likely

SubtotalNo

differenceLess likely

Much less likely

Subtotal

Remain aware of the supplier

16.8 58.5 75.3 23.3 1.0 0.4 1.4

Form lasting impressions

11.2 50.4 61.6 33.5 4.4 0.4 4.8

Position their products vs. competitor

11.3 50.6 61.9 35.7 1.9 0.4 2.3

Contact that supplier

22.6 53.7 76.3 21.4 1.5 0.8 2.3

Use of Media

Conclusions

• Magazines continue to be a major medium to initiate relationships. Publications are where inititial branding takes place

• Different media contribute different strengths and perform different roles in the adoption process

• A mix of media throughout the buying process will enable suppliers to achieve marketing objectives more effectively.

Use of Media

26.0%

46.1%

13.2%

6.1%

6.6% 2.0%

All issuesMost issuesHalf the issuesLess than halfA few

Why PBS?

Why PBS?

72% of subscribers look into/read all or most issues

Time Spent with PBS Will Increase

% Respondents

Likely spend much more time 1.8

More time 11.8

Same amount of time 78.3

Subtotal, same amount or more 91.9

Less time 6.8

Much less time 1.2

Subtotal, less time 8.0

Why PBS?

Time Spent with PBS Will Increase

Same or more time Less time0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%92%

8%

Why PBS?

92% will spend the same or more time reading PBS in the future

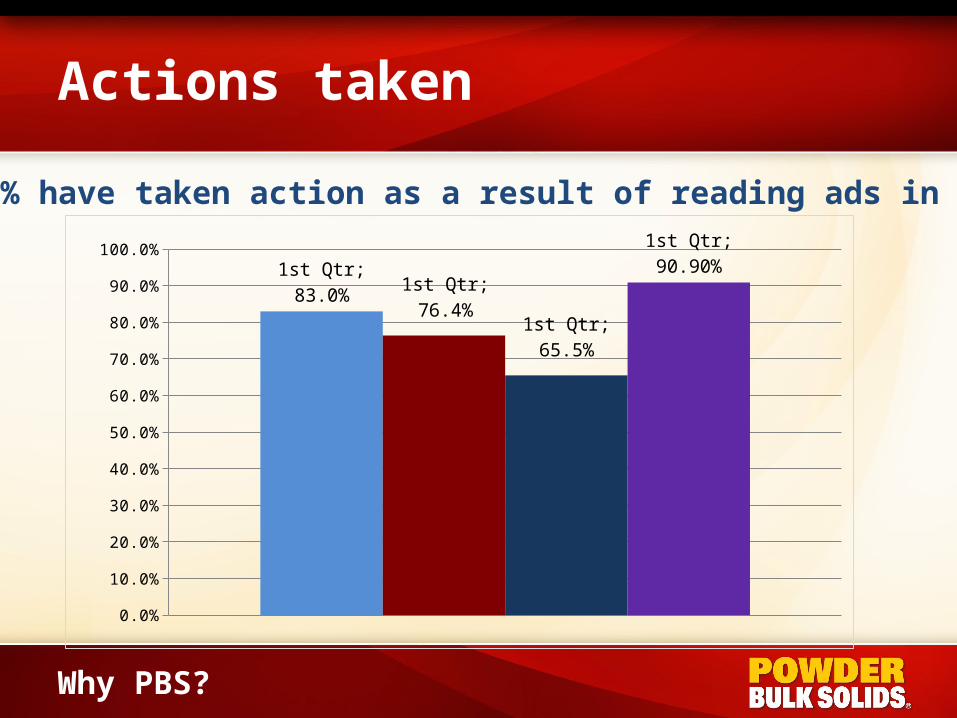

Actions taken

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

1st Qtr; 83.0%1st Qtr; 76.4%

1st Qtr; 65.5%

1st Qtr; 90.90%

Why PBS?

91% have taken action as a result of reading ads in PBS

Detailed actions taken

Phone

d su

pplie

r

Visite

d su

pplie

r web

site

Sent e

to s

uppli

er

Stopp

ed a

t sup

plier

trad

e sh

ow b

...

Asked

sta

ff m

embe

r to

follo

w up

Sugge

sted

pro

duct

s be

use

dPas

sed

ad o

n

0% 10% 20% 30% 40% 50% 60% 70% 80%

43.8%18.7%

69.9%31.7%

29.2%3.4%

18.8%27.2%

17.3%

32.1%23.3%

32.1%

32.1%9.1%

Why PBS?

91% have taken action as a result of reading ads in PBS

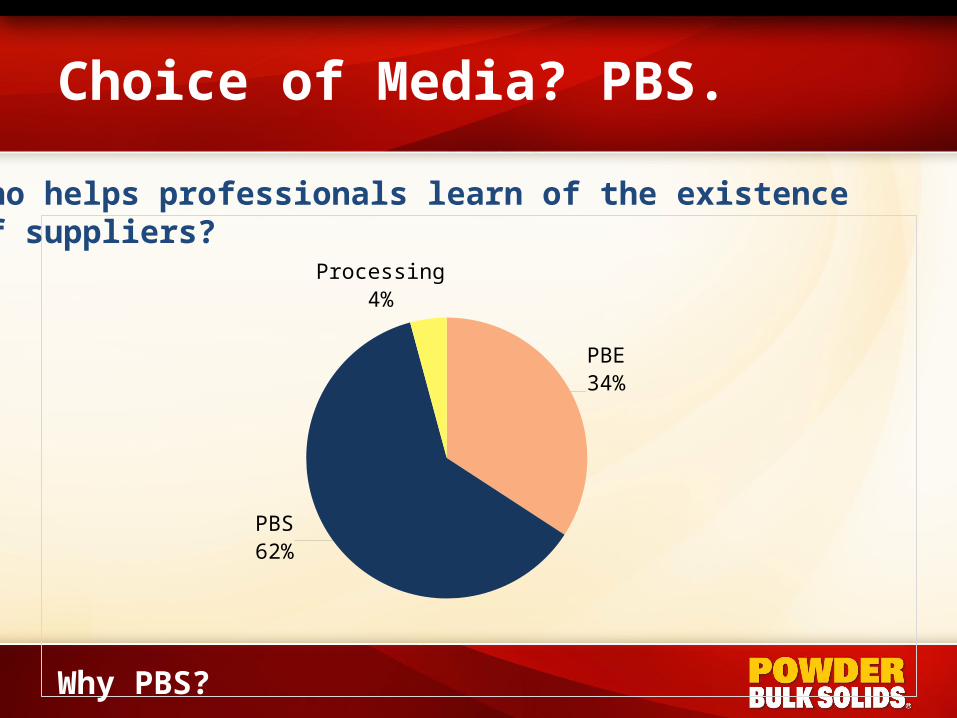

PBE34%

PBS62%

Processing4%

Why PBS?

Who helps professionals learn of the existence of suppliers?

Choice of Media? PBS.

PBE36.2%

PBS56.6%

Processing7.2%

Why PBS?

Who helps form impressions about features/ benefits of a supplier and their equipment? PBS.

Choice of Media? PBS.

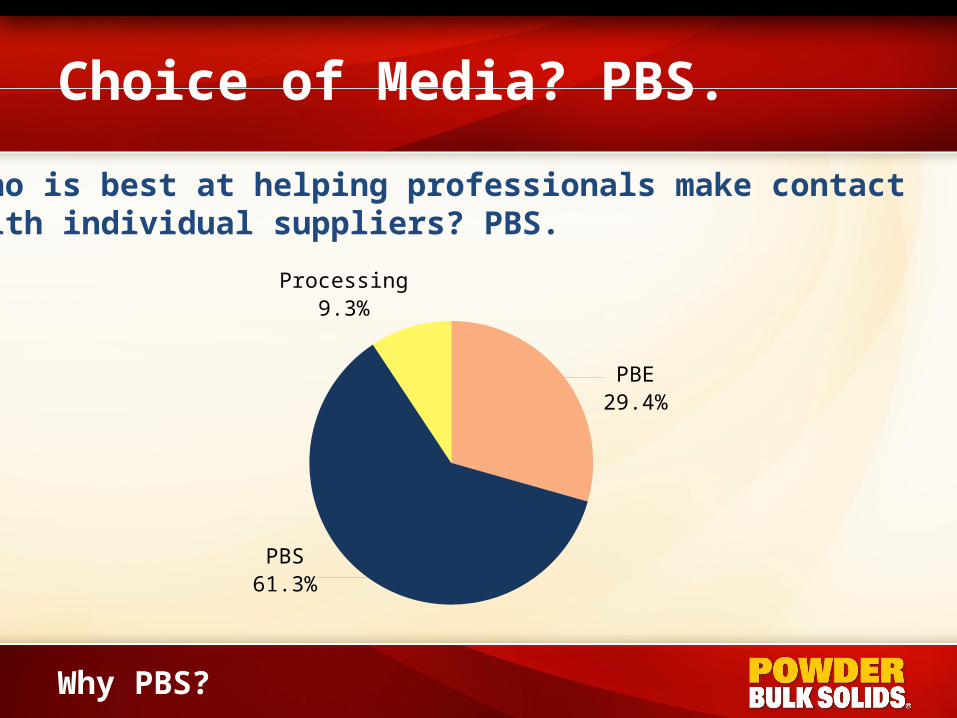

PBE29.4%

PBS61.3%

Processing9.3%

Why PBS?

Who is best at helping professionals make contact with individual suppliers? PBS.

Choice of Media? PBS.

Other Publications NOT being Read Regularly

PBE Processing Neither0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

PBE; 40.2%

Processing; 64.6%

Neither; 28.3%

Why PBS?

These PBS readers CANNOT be reached by PBE and Processing

Conclusion

• Processing professionals rate PBS as superior in helping stimulate solutions and locate products

• PBS is clear leader in helping suppliers brand their products

• PBS is the most likely place for professionals to learn, form impressions, position competitive suppliers, and make contact with suppliers

Why PBS?

Summary

• In the dry particulate industry, there is substantial purchasing activity underway with the readers of Powder/Bulk Solids.

• They are looking for suppliers.

• They are using the various media channels offered by PBS to find them.

• A multi-channel communications program with PBS will plug you into these buyers.

Summary