a review of the federal government 2015 budget of nigeria

TRANSCRIPT

A REVIEW OF THE FEDERAL GOVERNMENT 2015 BUDGET

PROPOSAL

A REVIEW OF THE FEDERAL GOVERNMENT 2015 BUDGET

PROPOSAL

By Donald Ikenna OFOEGBU

Economist, Researcher & Program Officer PFM,Centre for Social Justice, Abuja.

[email protected], 08126156014

@Donaldikenna1

Outline:Outline:1. The Rules of the Game

2. Compliance to the Basic Rules: Reviewing 2014 Budget & its Implementation

3. WHERE IS THE 2015 BUDGET ANCHORED?

4. THE 2015 BUDGET: A Transition Budget & Hope

5. THE FISCAL ITEMS

6. THE ALLOCATIONS AND PRIORITIES

7. HUMAN CAPITAL DEVELOPMENT

8. THE ALLOCATIONS AND THE TRANSFORMATION AGENDA (TA)

9. ON THE REVENUE SIDE

10. FRIVOLITIES AND WASTEFUL LINE ITEMS IN THE 2015 PROPOSED BUDGET

11. CONCLUSIONS

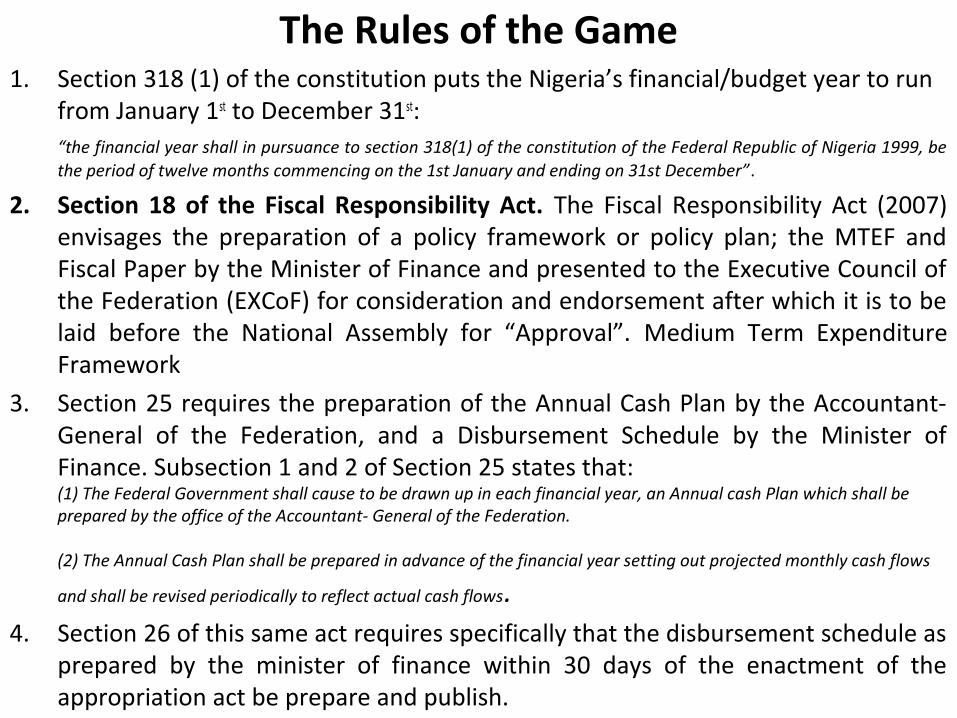

The Rules of the Game1. Section 318 (1) of the constitution puts the Nigeria’s financial/budget year to run

from January 1st to December 31st: “the financial year shall in pursuance to section 318(1) of the constitution of the Federal Republic of Nigeria 1999, be the period of twelve months commencing on the 1st January and ending on 31st December”.

2. Section 18 of the Fiscal Responsibility Act. The Fiscal Responsibility Act (2007) envisages the preparation of a policy framework or policy plan; the MTEF and Fiscal Paper by the Minister of Finance and presented to the Executive Council of the Federation (EXCoF) for consideration and endorsement after which it is to be laid before the National Assembly for “Approval”. Medium Term Expenditure Framework

3. Section 25 requires the preparation of the Annual Cash Plan by the Accountant-General of the Federation, and a Disbursement Schedule by the Minister of Finance. Subsection 1 and 2 of Section 25 states that:(1) The Federal Government shall cause to be drawn up in each financial year, an Annual cash Plan which shall be prepared by the office of the Accountant- General of the Federation.

(2) The Annual Cash Plan shall be prepared in advance of the financial year setting out projected monthly cash flows

and shall be revised periodically to reflect actual cash flows. 4. Section 26 of this same act requires specifically that the disbursement schedule as

prepared by the minister of finance within 30 days of the enactment of the appropriation act be prepare and publish.

5. On the practice of implementation, reporting is expected:• Section 30. (1) The Minister of Finance, through the Budget

Office of the Federation, shall monitor and evaluate the implementation of the Annual Budget, assess the attainment of fiscal targets and report thereon on a quarterly basis to the Fiscal Responsibility Council and the Joint Finance Committee of the National Assembly

• (2) The Minister of Finance shall cause the report prepared pursuant to subsection (1) of this section to be published in the mass and electronic media and on Ministry of Finance website not later than 30 days after the end of each quarter. – FRA (2007)

Compliance to the Basic Rules: Reviewing 2014 Budget & its Implementation

• the Fiscal Responsibility Act 2007 requires the 2014 Budget to be presented before the National Assembly by October ending 2013. Contrary to the FRA 2007 and best practice, the 2014 Budget was presented to the joint section of NASS in December 19, 2013.

• No annual cash plan or disbursement schedule was made available to this effect.

• The proposed 2014 budget was subject to the traditional delays generated from the debate on the oil price benchmark between NASS and the Executive.

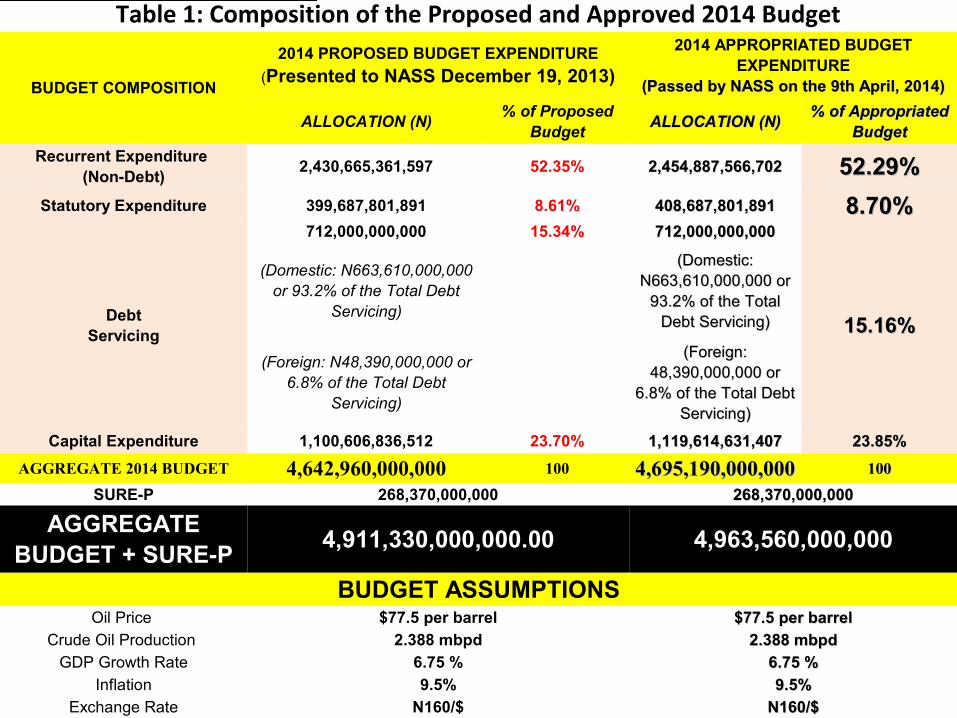

Table 1: Composition of the Proposed and Approved 2014 Budget

BUDGET COMPOSITION

2014 PROPOSED BUDGET EXPENDITURE

(Presented to NASS December 19, 2013)

2014 APPROPRIATED BUDGET EXPENDITURE

(Passed by NASS on the 9th April, 2014)(Passed by NASS on the 9th April, 2014)

ALLOCATION (N)% of Proposed

BudgetALLOCATION (N)ALLOCATION (N)

% of Appropriated % of Appropriated BudgetBudget

Recurrent Expenditure (Non-Debt)

2,430,665,361,597 52.35% 2,454,887,566,7022,454,887,566,702 52.29%52.29%

Statutory Expenditure 399,687,801,891 8.61% 408,687,801,891408,687,801,891 8.70%8.70%

DebtServicing

712,000,000,000 15.34% 712,000,000,000712,000,000,000

15.16%15.16%

(Domestic: N663,610,000,000 or 93.2% of the Total Debt

Servicing)

(Domestic: (Domestic: N663,610,000,000 or N663,610,000,000 or

93.2% of the Total 93.2% of the Total Debt Servicing)Debt Servicing)

(Foreign: N48,390,000,000 or 6.8% of the Total Debt

Servicing)

(Foreign: (Foreign: 48,390,000,000 or 48,390,000,000 or

6.8% of the Total Debt 6.8% of the Total Debt Servicing)Servicing)

Capital Expenditure 1,100,606,836,512 23.70% 1,119,614,631,4071,119,614,631,407 23.85%23.85%

AGGREGATE 2014 BUDGET 4,642,960,000,000 100 4,695,190,000,0004,695,190,000,000 100100

SURE-P 268,370,000,000 268,370,000,000268,370,000,000

AGGREGATE BUDGET + SURE-P

4,911,330,000,000.00 4,963,560,000,000

BUDGET ASSUMPTIONSOil Price $77.5 per barrel $77.5 per barrel$77.5 per barrel

Crude Oil Production 2.388 mbpd 2.388 mbpd2.388 mbpd

GDP Growth Rate 6.75 % 6.75 %6.75 %

Inflation 9.5% 9.5%9.5%

Exchange Rate N160/$ N160/$N160/$

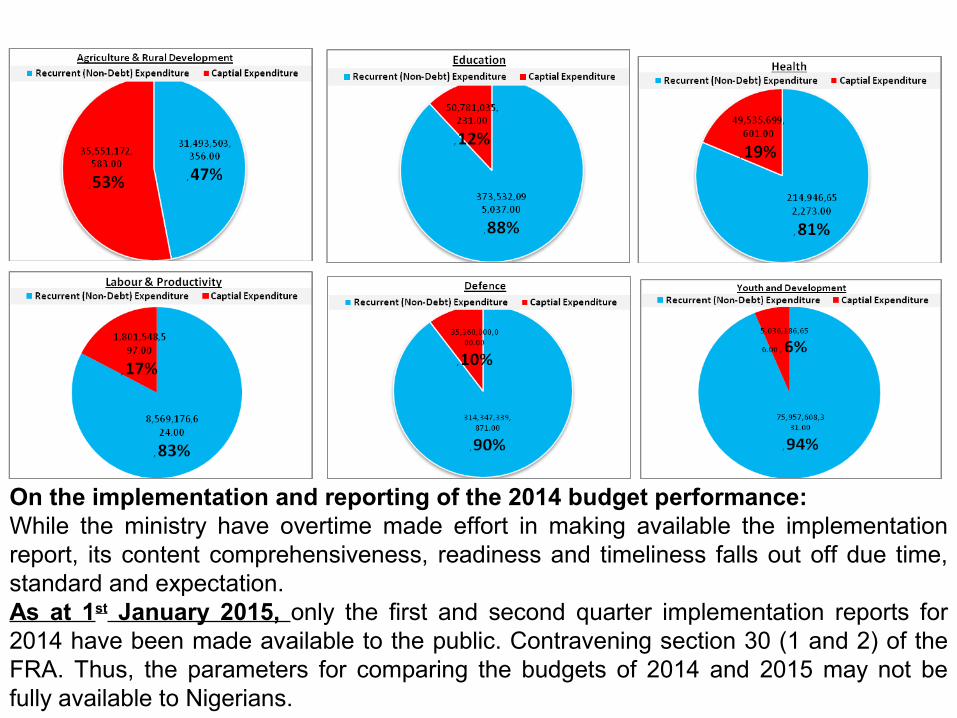

• Appropriating for the Human Development & key Ministries/Sector in the 2014 budget act:

Education -N424.3billion - 9% of the Agg. Budget.

Health - N264.5billion - 5.6%

Agric & Rural Devpt - N67.04billion - 1.4% Defence - N347.7billion - 7.4%

Works - N133.73billion - 2.8%

Labour & Productivity - N10.4billion - 0.2%

On the implementation and reporting of the 2014 budget performance:While the ministry have overtime made effort in making available the implementation report, its content comprehensiveness, readiness and timeliness falls out off due time, standard and expectation.As at 1st January 2015, only the first and second quarter implementation reports for 2014 have been made available to the public. Contravening section 30 (1 and 2) of the FRA. Thus, the parameters for comparing the budgets of 2014 and 2015 may not be fully available to Nigerians.

Implementation in 2014 was challenging for two major reasons (BIR Q1&Q2 2014)

1) Annual appropriation proposal did not get the passage of the National Assembly until the beginning of the second quarter.

2) The revenue receipts from resources were significantly below their projected estimates. These shortfalls in revenue were serious impediments to the effective implementation of the budget in the quarter.

These were where drive by oil pipeline vandalism and “shut-ins”. Quantity of oil produced averaged at about 2.2 million bpd in the first 3 quarters of 2014; falling short of the 2.38million bpd projected in the Budget.

Oil Price fall in the international oil price was another. Prices crashed from a peak of about $114pb earlier in June 2014, to around $58pb by December 2014. This is below the Budget benchmark price of $77.5 pb for 2014. As a result, revenues falls short of the Budget targets of N3.73 trillion. As at the end of October 2014, total revenues were about N2.72 trillion.

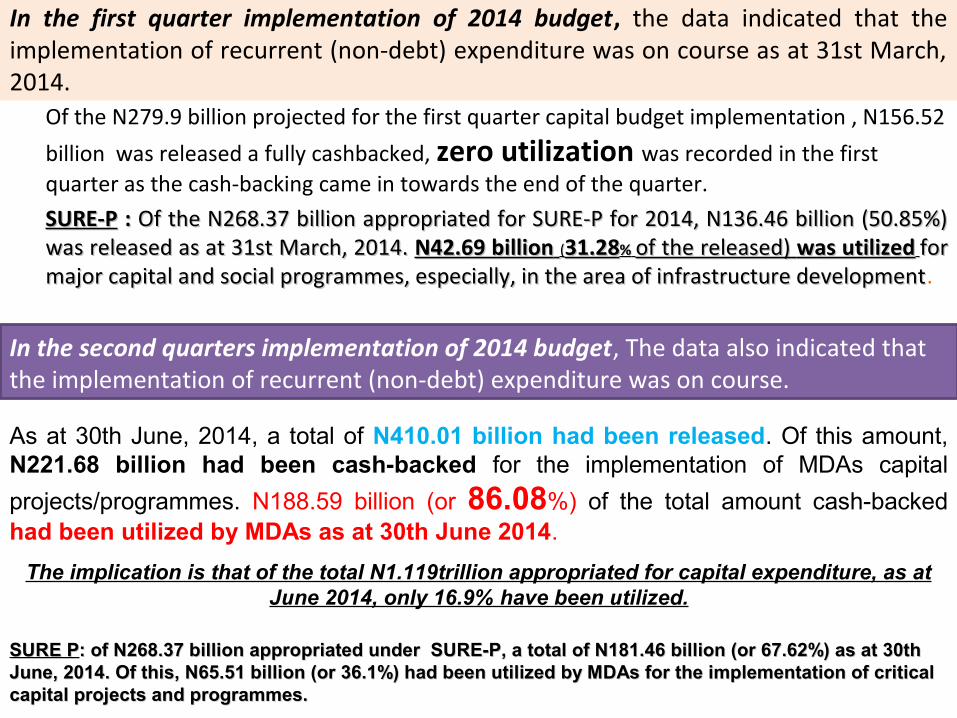

In the first quarter implementation of 2014 budget, the data indicated that the implementation of recurrent (non-debt) expenditure was on course as at 31st March, 2014.

Of the N279.9 billion projected for the first quarter capital budget implementation , N156.52

billion was released a fully cashbacked, zero utilization was recorded in the first quarter as the cash-backing came in towards the end of the quarter.

SURE-PSURE-P : : Of the N268.37 billion appropriated for SURE-P for 2014, N136.46 billion (50.85%) Of the N268.37 billion appropriated for SURE-P for 2014, N136.46 billion (50.85%) was released as at 31st March, 2014. was released as at 31st March, 2014. N42.69 billionN42.69 billion ((31.2831.28%% of the released) of the released) was utilizedwas utilized for for major capital and social programmes, especially, in the area of infrastructure developmentmajor capital and social programmes, especially, in the area of infrastructure development.

In the second quarters implementation of 2014 budget, The data also indicated that the implementation of recurrent (non-debt) expenditure was on course.

As at 30th June, 2014, a total of N410.01 billion had been released. Of this amount, N221.68 billion had been cash-backed for the implementation of MDAs capital

projects/programmes. N188.59 billion (or 86.08%) of the total amount cash-backed had been utilized by MDAs as at 30th June 2014.

The implication is that of the total N1.119trillion appropriated for capital expenditure, as at June 2014, only 16.9% have been utilized.

SURE PSURE P: of N268.37 billion appropriated under SURE-P, a total of N181.46 billion (or 67.62%) as at 30th : of N268.37 billion appropriated under SURE-P, a total of N181.46 billion (or 67.62%) as at 30th June, 2014. Of this, N65.51 billion (or 36.1%) had been utilized by MDAs for the implementation of critical June, 2014. Of this, N65.51 billion (or 36.1%) had been utilized by MDAs for the implementation of critical capital projects and programmes.capital projects and programmes.

On the 3rd Quarter: While presenting the 2015 budget proposal to the public, on 17th December 2014, the Minister of Finance verbally announced the performance of the 2014 budget in the third quarter. In her words:

“...we have managed to keep the country running. Recurrent Expenditure is being paid and government is running. We are aware of some MDAs, e.g. Education, where salary payments are delayed due to glitches in IPPIS. This is being rectified and all will be paid this December. Capital expenditure however has suffered. We could not cashback N100 billion of 3rd quarter capital and have not been able to release 4th quarter capital.- COE/MOF (17th Dec, 2014)The implication is that as at end third quarter; September (final quarter of 2014) no other utilization has been done from the regular budget. Hence the total implementation of the capital project as at that date was still the 16.85%.

SURE P: The minister however noted that existing capital implementation was ongoing using the SURE-P sums, as well as releases for the last quarter of 2014. Quoting the minister:

“....Nevertheless, we have managed to keep most of our priority projects going with the support of SURE-P resources. Of the N1.12 trillion in the Budget, the sum of N610 billion has been released (as at the end of October) with N465 billion of this amount only fully cash-backed. About 83.5 percent of the amount cash-backed had been utilized by MDAs as at the end of October”.

WHERE IS THE 2015 BUDGET ANCHORED? No Approved 2015-2017MTEF

Section 11 of the Fiscal Responsibility Act (FRA) 2007 mandates the Minister of Finance to prepare the MTEF and FSP and lay them before the Federal Executive Council (FEC) and the National Assembly for consideration and approval. Going by Section 18 of the Act, the MTEF is the basis for the preparation of the annual budget.

The 2015-2017 statutory documents were submitted late in October 19th 2014. The 2015-2017MTEF proposed a 2015 budget of N4.817trillion, Recurrent Expenditure of N2.622trillion, and Capital Expenditure of N1.436trillion. The oil price was marked at $78pb and exchange rate of N160/$.

Given the continuous fall in the international oil prices, and the overshot MTEF of the ministry, a revised 2015-2017 Medium Term Expenditure Framework (MTEF) and Fiscal Strategy Paper (FSP) of N4.661 trillion budget estimates for 2015 fiscal year was on the 19th November 2014 submitted to the Senate by the Federal Government. The new MTEF and FSP showed a reduction in capital expenditure from the earlier proposed N1.436 trillion to N1.208trillion, the Federal Government retained the recurrent expenditure of N2.622 trillion proposal in the first MTEF. The N4.661 trillion budget estimates for 2015, according to the document, was predicated on $73 per barrel oil benchmark and a foreign exchange of N162 to a dollar.

The 2015-2017MTEFs having been recalled and resubmitted is yet to be approved by NASS. Before The 2015-2017MTEFs having been recalled and resubmitted is yet to be approved by NASS. Before the approval of the reviewed 2015-2017MTEF by NASS, the 2015 Budget proposal have been drafted the approval of the reviewed 2015-2017MTEF by NASS, the 2015 Budget proposal have been drafted and submitted to NASS for approval. This is a fat breach of the Fiscal Responsibility Act, it makes and submitted to NASS for approval. This is a fat breach of the Fiscal Responsibility Act, it makes rubbish its wise recommendation of the MTEF being the basis upon which the 2015 budget should be rubbish its wise recommendation of the MTEF being the basis upon which the 2015 budget should be drawn.drawn.

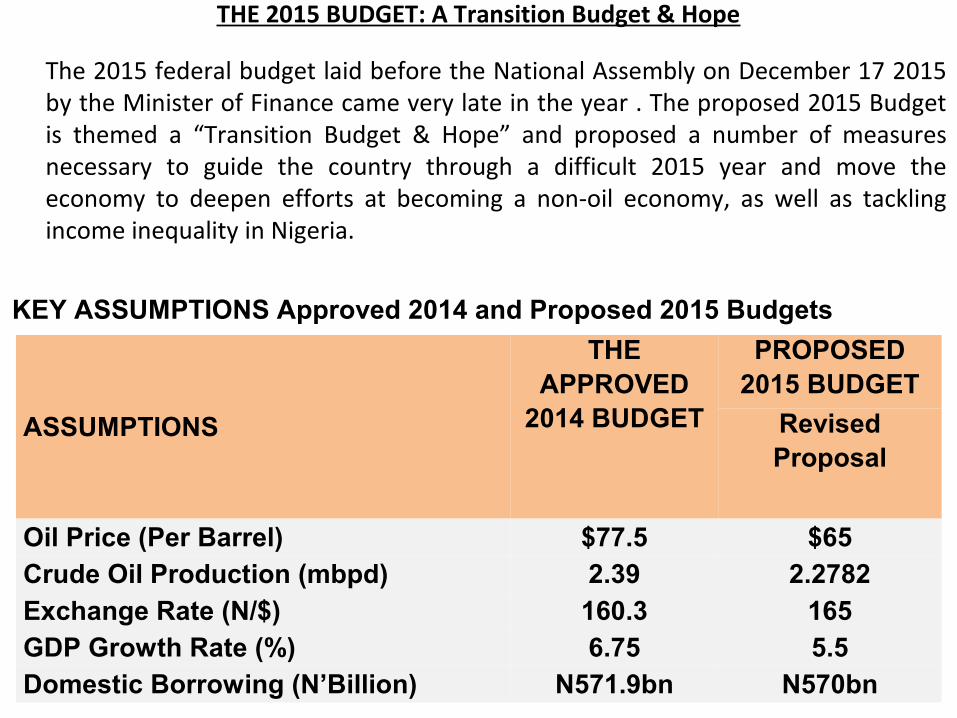

THE 2015 BUDGET: A Transition Budget & Hope

The 2015 federal budget laid before the National Assembly on December 17 2015 by the Minister of Finance came very late in the year . The proposed 2015 Budget is themed a “Transition Budget & Hope” and proposed a number of measures necessary to guide the country through a difficult 2015 year and move the economy to deepen efforts at becoming a non-oil economy, as well as tackling income inequality in Nigeria.

ASSUMPTIONS

THE APPROVED

2014 BUDGET

PROPOSED 2015 BUDGET

Revised Proposal

Oil Price (Per Barrel) $77.5 $65Crude Oil Production (mbpd) 2.39 2.2782Exchange Rate (N/$) 160.3 165GDP Growth Rate (%) 6.75 5.5Domestic Borrowing (N’Billion) N571.9bn N570bn

KEY ASSUMPTIONS Approved 2014 and Proposed 2015 Budgets

Table 2: KEY ASSUMPTIONS Approved 2014 and Proposed 2015 Budgets

THE FISCAL ITEMS: Table 3: Composition of the 2015 Budget ProposalFiscal items Approved

2014budget% of Total

2014 Approved

Budget

2015 Proposed

Budget

% of Total Proposed

2015 Budget

N’bn N’bn

FGN Retained Revenue 3,731.00 3,602.96Statutory Transfers 408.69 8.70 411.84 9.45

Debt Service 712 15.16 943 21.64

Recurrent Expenditure 2,454.89 52.29 2,616.01 60.03

Personnel Costs (MDAs) 1,727.61 36.80 1,836.73 42.15Overheads 251.93 5.37 199.18 4.57CRF Pensions 187.45 3.99 231.41 5.31Other Service Wide votes 301.84 6.43 348.69 8.00Capital Expenditure 1,119.62 23.85 387.11 8.88

TOTAL FGN EXPENDITURE 4,695.2 100 4,357.96 100

SUBIDY REINVESTMENT PROGRAM (SURE-P)

268.37 102.5

SURE-P Board (Running Cost)

1.2 0.5

SURE-P (Capital Expenditure)

267.17 102

AGG. FGN EXPENDITURE (INCLUSIVE OF SURE-P) 4,963.57 4,460.46

Fiscal Deficit (Based on Regular Budget) (993.68) (755.00)

Fiscal Deficit/GDP (%) -1.24% -0.79%

• To cut down the recurrent expenditure, instituting measures aimed at improving spending, the cut down exercise is expected to save a total of N82.5 billion covering the following: Overhead expenditures: propose cuts to International Travels and Training by 50% for all MDAs saving about N14billion, while other provisions for Overhead expenditure are to be dropped completely saving about N4 billion. Administrative Expenditures for Buildings, Equipment, Supplies, etc: MDAs’ provisions for the procurement of administrative supplies and equipment will be cut, saving about N5 billion; procurement and upgrade of buildings were similarly curtailed saving about N44 billion. While another N76 billion is proposed for reallocation to more impactful programmes of Government in the security, health, and education sectors.

• The demand for funds to service debts is increasing. It rose from N712bn in 2014 being 14.26% of the budget to N943bn in 2015 being 21.16% of budget. The national Debt Management Office attributed the high debt profile to six factors:

– Inefficient trade and exchange rate policies,

– unfavourable exchange rate movements,

– unfavourable interest rate movements,

– poor lending and inefficient loan utilisation,

– poor debt management practices, and

– accumulation of arrears and penalties.

Given the significant decline in capital expenditure, it appears that funds are being borrowed to finance recurrent expenditure rather than developmental projects.

• The government propose spending N943bn: N555.89billion more on debt service than capital expenditure. The capital expenditure is not only less than the debt servicing, but less than half the debt provision at only 41.05% of the debt service provision! At the same time, debt service amounts to 26.17% of the retained revenue, implying that almost one third of the retained revenue are lost to paying debts that cannot be traced to any capital projects or human developments.

Debt servicing as a percentage of GDP 2010-2015Based on expected

drawdown on existing Loans and

new borrowingsin 2015, the Federal

Government plans to utilize US$6,084.78

millionfrom external sources based on the rolling pipeline projects of

2014.The Government also plans to borrow N570 billion from domestic

sources.

Borrowing program for the 2015 Fiscal YearA. EXTERNAL SOURCES

Source Amount (in US$' million)

a. Drawdown on Existing LoansADF 61.79Eximbank of China 206.43Eximbank of India 16.67French Development Agency 74.93IDA 394.35IDB 1.53IFAD 8.75SUB TOTAL 784.45b. New Borrowings*ADF 563.2Eximbank of China 500French Development Agency 216.67IDA 1091IDB 204.13IFAD 110JICA 123.33KFW (Germany) 72Special National Project 2140Diaspora Bond 300SUB TOTAL 5,320.33Grand Total 6084.78B. Domestic Sources***

Source Amount (US $'million)

FGN Bonds & Nigeria Treasury Bills 570,000.00Total 570,000.00

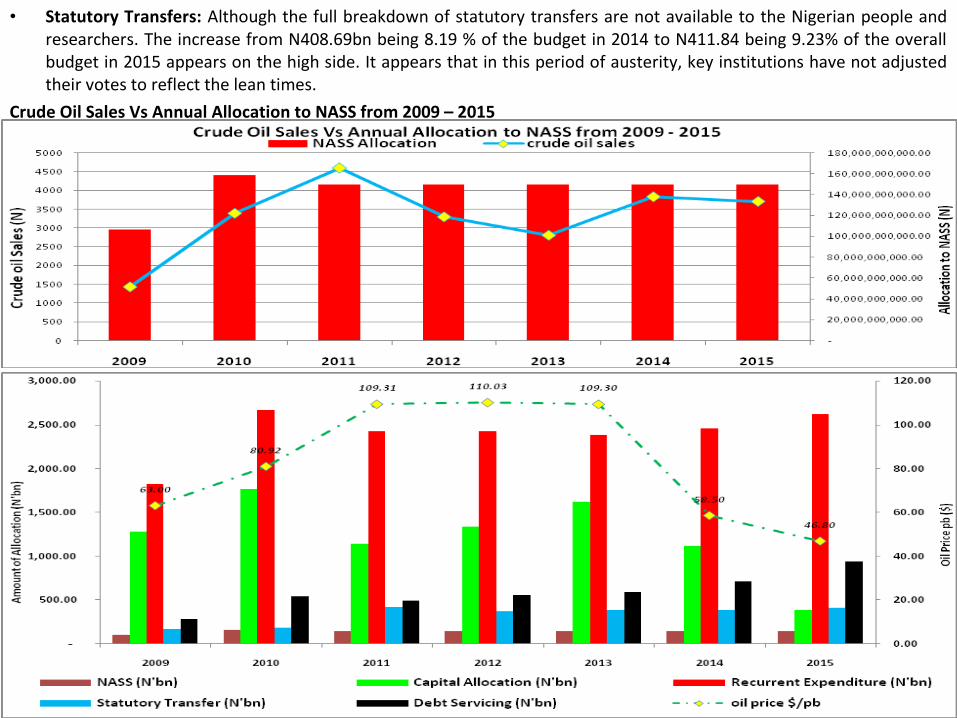

• Statutory Transfers: Although the full breakdown of statutory transfers are not available to the Nigerian people and researchers. The increase from N408.69bn being 8.19 % of the budget in 2014 to N411.84 being 9.23% of the overall budget in 2015 appears on the high side. It appears that in this period of austerity, key institutions have not adjusted their votes to reflect the lean times.

Crude Oil Sales Vs Annual Allocation to NASS from 2009 – 2015

THE ALLOCATIONS AND PRIORITIES

On the average the MDAs have a 87% recurrent expenses and only 13% capital expenses. While a few On the average the MDAs have a 87% recurrent expenses and only 13% capital expenses. While a few MDA have no capital expenses, some others like the FCT have no recurrent expenditure.MDA have no capital expenses, some others like the FCT have no recurrent expenditure.

Budget Summary COMPUTED FIGURE % of Agg Budget1 MDAs PERSONNEL COST 1,836,729,121,525 42.152 MDAs OVERHEAD 199,182,792,624 4.573 MDAs CAPITAL SPENDINGS 194,020,573,767 4.454 CAPITAL SUPPLEMENTATION 193,092,000,000 4.435 PENSIONS AND GRATUITIES 231,408,494,338 5.316 SERVICE WIDE VOTES 348,687,017,746 8.007 STATUTORY TRANSFERS 411,840,000,000 9.458 DEBT SERVICE 943,000,000,000 21.64

AGGREGATE EXPENDITURE 4,357,960,000,000 100.00

HUMAN CAPITAL DEVELOPMENT• Human capital development in this analysis comprises education, health, women and social

development, youth development and labour and productivity. All the sub-sectors with the exception of the women and social development have their recurrent budget higher than the capital budget which may not be faulty owing to the fact that the entire sectors are human dependent in service delivery.

Ministry of Education (+ UBEC) was appropriated only

11.29% of the total 2015 proposed budget. In the 2014 budget (approved), this was 11.36%.

Of the total 2015 budget - 89.7% was for the recurrent expenditure, 10.35% for capital infrastructure provision.A vote of 11.29% of the overall budget to education including UBEC in 2015 will not meet the demands of the sector. It falls short of the 26% demanded by international standards. Note. Nigeria has the highest number of global out of school children. Nigeria is reported to spend about N1.5trillion abroad every year in education.

HEALTH : The allocation for the health sector in 2015 as proposed

was 5.91% of the total budget, slightly above the 2014 budget composition of 5.66% of the overall budget. This also misses the international standard of 15% of the budget. The health sector has seen one strikes too many at the detriment of the sick Nigerians and nursing mothers. It is reported that Nigerians spend over N78b annually for foreign medical services

Agriculture: Nigeria is reported to spend about N1.5trillion abroad every year in education. Against expectation, the composition of agriculture as a percentage of the

aggregate budget fell to only 0.9% from the 1.47% of the approved 2014 budget.

Declining Trend Of The Agriculture Vote In Relation To Maputo Declaration:

THE ALLOCATIONS AND THE TRANSFORMATION AGENDA (TA)

• In the absence of an approved medium term frame work, there is the need to see if by coincident the budget as proposed for the 2015 year had the transformation agenda in mind

ON THE REVENUE SIDE

the Federal government 2015 Budget has an Aggregate Budget Revenue of N3.602 trillion made up of: oil revenue of N1.918 trillion and non-oil revenues of N1.684 trillion (implying a ratio of 53% oil revenues to 47% non-oil) to fund an Aggregate Budget Expenditure of N4.46 trillion (inclusive of SURE-P) proposed for 2015 Budget

Tax Revenue: In the short term, the government is determined to improve

tax revenues not by increasing tax rates, but rather as a pro-people

Administration, by first, strengthening the tax administration. The

government via the ministry and supporting agents are aimed at plug leakages, increase the tax base and improve tax collection efficiency. In 2015, the Federal government plans to ramp the FIRS/McKinsey initiative to contribute an extra N160 billion in

tax receipts and an aggregate of about N460 billion over and above the 2014

levels in the 2015-2017 period

Tax Waivers and Exemptions: according to the ministry of finance, analysis shows that about 30% of received tax waivers from government especially under the pioneer status scheme have abuse the waivers and exemption system. As a short-term measure, the government plans to commenced a review of the implementation of pioneer status exemptions to which is expected to unlock up to N36 billion of additional tax revenues in 2015.

Adjustment Measures: Leakages and Under Remittance of IGR by MDA: B. Surcharge on Luxury Goods and Efficiency Gains

Revenue Side: Expected Income/Amount Saved

Surcharges on certain luxury items N23billion10% import surcharge on new private jets N3.7billion39% import surcharge on luxury yatch N1.6billion5% import surcharge on Luxury Cars N2.6billionSurcharge on Business & First Class Tickets on Airlines yet to fix rate3% luxury surcharge on Champagnes, Wines & Spirits N2.3billion1% FCT Mansion Tax on Residential Properties with value of N300million & above N360million

Strengthening Tax Administration and tax policy (N460billion in 3years) that’s an average of

N153.3billion

Expenditure Side:

Freezing purchase of new office equipment & other administrative capital. This will generate some savings:

Purchase of Office Buildings N1.99billionConstruction/Provision of Office Building N24.05billionPurchase of office furniture and fitting N9.50billionInternational travel and training will be limited to only the most crucial for now:

This applies to all public servants so that parastatals can remit more IGR to Treasury N14.02billion

Rationalize expired committees and commissions that lead to leakages N6.49billion

TOTAL N243.36Billion

Frivolities and Wasteful Line Items in the 2015 Proposed Budget• N1.142bn as welfare packages; N295m for purchase of security equipment; N100m for

computer software acquisition – all for the office of the Secretary to the Government of the Federation.

• In the same SGF office, the amount of N1.2bn was requested in the 2014 budget for welfare packages.

• In the Presidency/State House, there is a vote of N826m for the rehabilitation and repairs of buildings and the same subheading got a vote of over N2.6bn in the proposal for last year; purchase of canteen and kitchen equipment for N174m; ; purchase of “crested cockery” for N54m.

• the “Upgrading of Electrical Components at Shehu Shagari Complex (ongoing)” code - SGF16003811. It was allocated N150million by the Secretary to the Government of the Federation (HQTRS). In 2014 this same building attracted N120million for the upgrade of electrical components at Shehu Shagari Complex (ongoing). In 2013 approved budget, the sum of N50million was approved for the same upgrading of electrical components at Shehu Shagari Complex. In 2012 the sum was N60million.

• “Auto fill budgeting practice”; repeating the same figures for almost all the line items. For instance, in the Code of Conduct Tribunal, the sum of N66.7milliion was appropriated for purchase of generator, construction of 3 state offices (in Lagos, Kwara and River) and construction of 5 nos. Zonal court halls in south- south, southwest, south east north east and northwest zones starting with Enugu. The same sum of N1,505,962 was appropriated for water rates, sewage charges, books, newspaper, maintenances, legal services, refreshment and meal, sporting activities, engineering services, etc (N1,505,962 was repeated fifteen times). The sum of N752,981 in different occasion was allocated to engineering services, postages & courier services, and Subscription to professional bodies. This is pure impunity in the budget system, a conspiracy against public resources and reflects pure incompetence in this agency’s budget and planning unit.

CONCLUSIONS• Let the Presidency and National Assembly lead the way in the austerity

measures and adjustments. Nigerians will be too willing to follow.• The executive should empower security agencies to do the simple task of

stopping oil theft and thereby increasing our crude oil production volume to not less than 2.5mbpd.

• The benchmark price of crude oil should be reduced to a realistic estimate, not more than $55pb.

• A moratorium on borrowing unless it is tied to specific capital projects.• Reallocate service wide votes to MDAS.• The Budget provides an opportunity for the presidential candidates to have a

debate around the different perspectives of handling fiscal policy at a time crisis and uncertainty.

• Take steps to recover the N160bn stolen by ghost workers.• Strengthening the Fiscal Responsibility Commission to performs its statutory

duties• Full implementation of the provisions of the Fiscal Responsibility Act.• Eliminate all forms of wastages, frivolities and dubious line items and

appropriation from the budget, while making those responsible for these sharp practices in the budget system to pay.

Thank You