a share monthly portfolio€¦ · stocks, one non-ferrous metal stock, one food and beverage stock,...

TRANSCRIPT

1

A-Share Monthly Portfolio

May 16, 2016

Rally pattern continuing; focus on small cap with

growth potential

The rate of return in April 2016 for the portfolio of the 10 golden stocks of Galaxy

Securities was 1.79%, 3.7ppt higher than CSI 300 Index. In January-April 2016, the

cumulative return on the monthly portfolio of Galaxy Securities was -3%, 12.4ppt higher

than CSI 300 Index. From January 2013 to now, the cumulative monthly return has

been 330%, significantly higher than the 305% return of the CSI 300 Index and

significantly higher than the 186% return of the ChiNext Index.

Outlook for May: Expectations of a FED increase in the interest rate are very low, and

the RMB exchange rate is expected to remain relatively stable. The fundamentals of

domestic economic policies will be the dominant factors affecting market trend, and it is

expected that the economy in Q2 will continue to stabilize, and that financial and

monetary policies will remain unchanged in general or see only minor fine-tuning. It is

possible for liquidity to be affected, and special care should be paid to changes in credit

risk. Capital markets place particular importance on the building of major institutions,

and the central government pays close attention to the healthy development of the stock

market. Generally, it is possible for the rally pattern to continue in May.

The prices of consumer goods continue to rise, as do high-quality growth stocks.

Cyclical products with sound fundamentals deserve attention, focusing mainly on

medium and small caps.

Our May portfolio includes one petrochemical stock, two machinery and military industry

stocks, one non-ferrous metal stock, one food and beverage stock, one construction

stock, one electrical equipment and new energy stock, one electronics stock, and one

computer stock.

Our stock portfolio for May (in no particular order) is as follows: Geo-Jade Petroleum

(600759.CH), Longhua Energy-saving (300263.CH), Anhui Zhongding (000887.CH),

Chenming Paper (000488.CH), Hengshun Zhongsheng (300208.CH), Shuanghui

Development (000895.CH), Arts Group (603017.CH), Pinggao Electric (600312.CH),

DMEGC (002056.CH), Conant (300061.CH).

Yang Huachao — Chief Analyst of Small-

and Mid-cap Stocks

(8621) 20252681

yanghuachao @chinastock.com.cn

Practicing Certificate No.: S0130512050003

Sun Jianbo — Doctor, Chief Strategy Ana-

(8610) 83571306

sunjianbo @chinastock.com.cn

Practicing Certificate No.: S0130511040002

Qin Xiaobin — Strategy Analyst Director

(8610)6656 8746

Practicing Certificate No.: S0130511030001

Wong Chi Man—Head of Research

(852) 3698-6317

Sources: China Galaxy Securities Research

Figure 1: Portfolio of May for Galaxy Securities (Note: share prices are the closing prices on May 16, 2016)

Stock

Code

Stock Discription EPS (RMB) PE (X)

2014A 2015A 2016E 2017E 2014A 2015A 2016E 2017E

600759.SH Geo-Jade Petroleum 0.02 0.03 0.06 0.34 393.0 262.0 131.0 23.1

300263.SZ Longhua Energy-saving 0.33 0.40 0.50 0.62 47.6 39.3 31.4 25.3

000887.SZ Anhui Zhongding 0.47 0.76 1.05 1.33 44.1 27.3 19.7 15.6

000488.SZ Chenming Paper 0.26 0.53 1.02 1.37 32.0 15.7 8.2 6.1

000895.SZ Shuanghui Development 1.84 1.29 1.35 1.48 11.6 16.6 15.9 14.5

603017.SH Arts Group 0.75 0.55 1.04 1.31 44.6 60.8 32.2 25.5

600312.SH Pinggao Electric 0.61 0.73 0.86 1.02 23.3 19.5 16.5 13.9

002056.SZ DMEGC 0.93 0.79 1.02 1.29 14.8 17.4 13.5 10.7

300208.SZ Hengshun Zhongsheng 0.15 0.42 0.70 1.26 92.1 32.9 19.7 11.0

300061.SZ Conant 0.24 0.21 0.48 0.66 120.3 137.4 60.1 43.7

2

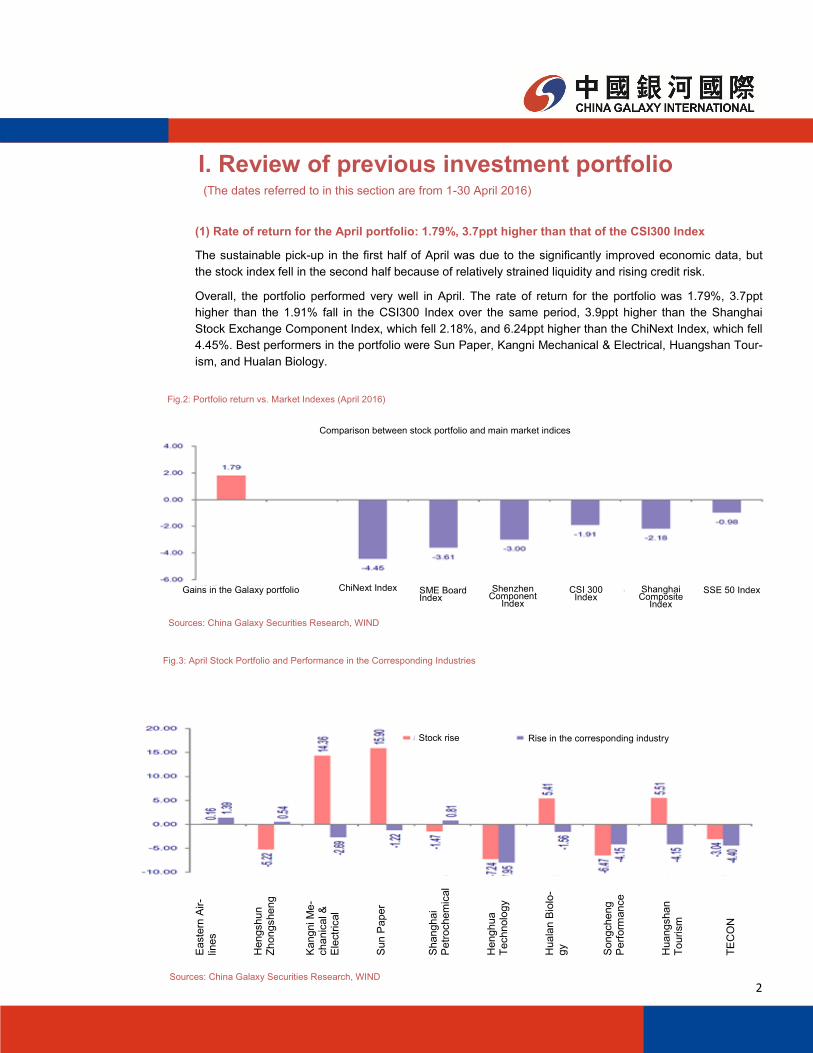

(1) Rate of return for the April portfolio: 1.79%, 3.7ppt higher than that of the CSI300 Index

The sustainable pick-up in the first half of April was due to the significantly improved economic data, but

the stock index fell in the second half because of relatively strained liquidity and rising credit risk.

Overall, the portfolio performed very well in April. The rate of return for the portfolio was 1.79%, 3.7ppt

higher than the 1.91% fall in the CSI300 Index over the same period, 3.9ppt higher than the Shanghai

Stock Exchange Component Index, which fell 2.18%, and 6.24ppt higher than the ChiNext Index, which fell

4.45%. Best performers in the portfolio were Sun Paper, Kangni Mechanical & Electrical, Huangshan Tour-

ism, and Hualan Biology.

I. Review of previous investment portfolio

Fig.2: Portfolio return vs. Market Indexes (April 2016)

Sources: China Galaxy Securities Research, WIND

Gains in the Galaxy portfolio

Stock rise Rise in the corresponding industry

Fig.3: April Stock Portfolio and Performance in the Corresponding Industries

Sources: China Galaxy Securities Research, WIND

Comparison between stock portfolio and main market indices

(The dates referred to in this section are from 1-30 April 2016)

Shenzhen Component

Index

ChiNext Index SME Board Index

CSI 300 Index

SSE 50 Index Shanghai Composite

Index

Easte

rn A

ir-

lines

Hengshun

Zh

ongsheng

Kangni M

e-

chanic

al &

E

lectr

ical

Sun P

aper

Shanghai

Petr

ochem

ical

Henghua

Te

chnolo

gy

Huala

n B

iolo

-gy

Songcheng

Perf

orm

ance

Huangshan

To

urism

TE

CO

N

3

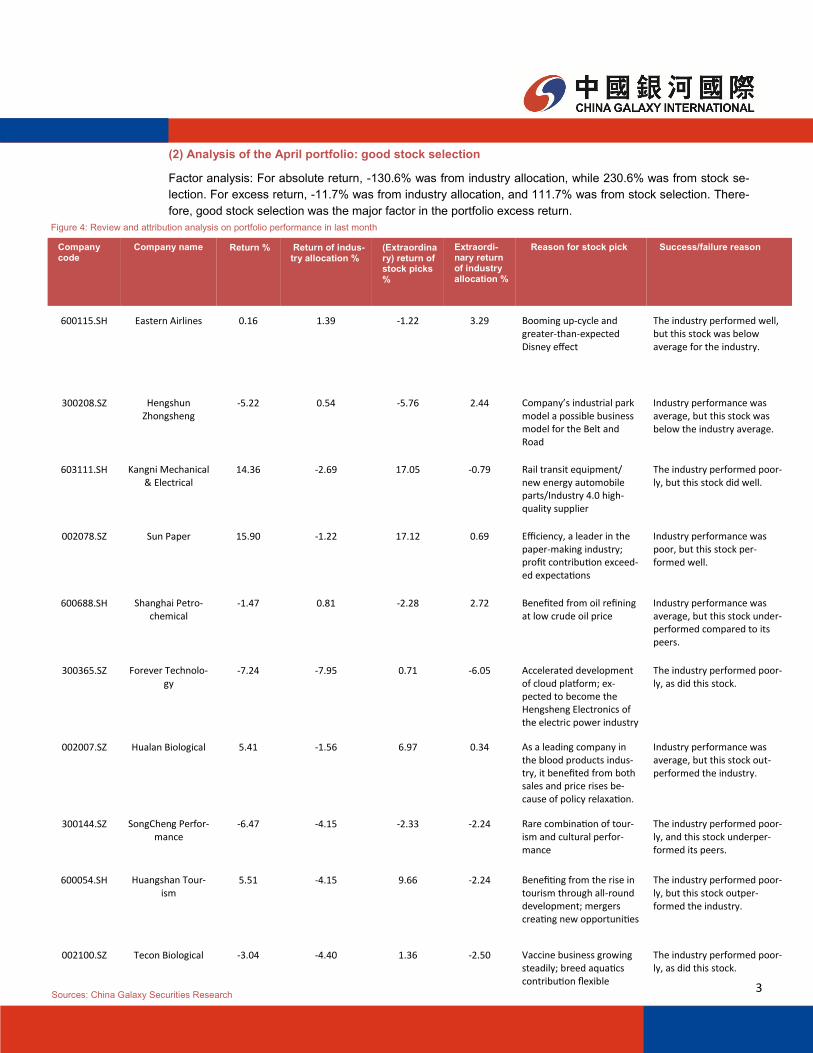

(2) Analysis of the April portfolio: good stock selection

Factor analysis: For absolute return, -130.6% was from industry allocation, while 230.6% was from stock se-

lection. For excess return, -11.7% was from industry allocation, and 111.7% was from stock selection. There-

fore, good stock selection was the major factor in the portfolio excess return.

Company code

Company name Return % Return of indus-try allocation %

(Extraordinary) return of stock picks %

Extraordi-nary return of industry allocation %

Reason for stock pick Success/failure reason

600115.SH Eastern Airlines 0.16 1.39 -1.22 3.29 Booming up-cycle and greater-than-expected Disney effect

The industry performed well, but this stock was below average for the industry.

300208.SZ Hengshun Zhongsheng

-5.22 0.54 -5.76 2.44 Company’s industrial park model a possible business model for the Belt and Road

Industry performance was average, but this stock was below the industry average.

603111.SH Kangni Mechanical & Electrical

14.36 -2.69 17.05 -0.79 Rail transit equipment/new energy automobile parts/Industry 4.0 high-quality supplier

The industry performed poor-ly, but this stock did well.

002078.SZ Sun Paper 15.90 -1.22 17.12 0.69 Efficiency, a leader in the paper-making industry; profit contribution exceed-ed expectations

Industry performance was poor, but this stock per-formed well.

600688.SH Shanghai Petro-chemical

-1.47 0.81 -2.28 2.72 Benefited from oil refining at low crude oil price

Industry performance was average, but this stock under-performed compared to its peers.

300365.SZ Forever Technolo-gy

-7.24 -7.95 0.71 -6.05 Accelerated development of cloud platform; ex-pected to become the Hengsheng Electronics of the electric power industry

The industry performed poor-ly, as did this stock.

002007.SZ Hualan Biological 5.41 -1.56 6.97 0.34 As a leading company in the blood products indus-try, it benefited from both sales and price rises be-cause of policy relaxation.

Industry performance was average, but this stock out-performed the industry.

300144.SZ SongCheng Perfor-mance

-6.47 -4.15 -2.33 -2.24 Rare combination of tour-ism and cultural perfor-mance

The industry performed poor-ly, and this stock underper-formed its peers.

600054.SH Huangshan Tour-ism

5.51 -4.15 9.66 -2.24 Benefiting from the rise in tourism through all-round development; mergers creating new opportunities

The industry performed poor-ly, but this stock outper-formed the industry.

002100.SZ Tecon Biological -3.04 -4.40 1.36 -2.50 Vaccine business growing steadily; breed aquatics contribution flexible

The industry performed poor-ly, as did this stock.

Sources: China Galaxy Securities Research

Figure 4: Review and attribution analysis on portfolio performance in last month

4

Composition of total return

1.79 -2.34 4.13

Contribution to total return

100% -130.6% 230.6%

Composition of excess earnings

3.70 4.13 -0.43

Contribution to

excess earnings 100% 111.7% -11.7%

Consumption, growth and cycle relatively balanced

Industry selection was poor; good stock selection produced excess earnings.

Company code

Company name Return % Return of indus-try allocation %

(Extraordinary) return of stock picks %

Extraordi-nary return of industry allocation %

Reason for stock pick Success/failure reason

Sources: China Galaxy Securities Research

Industries topping the list in terms of return were coal, food and beverage, banking, steel, petrochemicals

and nonferrous metals. Falling behind were media, computer, military, shipping and agriculture. Cyclical

stocks performed well; growth industries performed relatively poorly.

As for hot themes, the best performers were sub-new stocks. Relatively good performers included hydro-

power construction, military-civilian integration, rare earth permanent magnets and new energy vehicles.

Relatively poorly performing industries were mobile payment, network security, smart TV, Internet celebri-

ties and aircraft.

With respect to individual stocks, only 42 stocks achieved over 30% growth in April, most of which were sub

-new stocks. This significantly reduced the potential for investors to profit, and individual stocks were not

very active.

5

Name Change Name Change

Sub-new stock 60.17 Mobile payments -7.59

Water conservan-cy and hydro-power construc-tion

10.05 Network security -7.32

Military-civilian integration

9.10 Smart TV -7.00

New energy auto-mobiles

7.99 Internet celebrities -6.88

Rare-earth perma-nent magnets

7.33 Aircraft carriers -6.74

Lithium batteries 6.62 Credit investigation -6.67

Beautiful China 5.89 Satellite navigation -6.41

Placards 5.03 Cold chain logistics -6.28

Beijing-Tianjin-Hebei integration

4.59 Smart city -5.92

Beibu Bay Free Trade Zone

4.04 Third-party payment -5.91

Sources: WIND, China Galaxy Securities Research

Figure 6: The Best and the Worst 10 Concept Stocks in March

Figure 5: April 2016 Performance of All Industry Indexes (%)

Sources: WIND, China Galaxy Securities Research

Co

al

Foo

d a

nd

bev

erag

e

Ban

kin

g

Stee

l

Pet

role

um

an

d p

etro

chem

ical

s

No

nfe

rro

us

met

als

Ap

plia

nce

s

Au

tom

ob

iles

Co

ngl

om

erat

es

Co

mm

un

icati

on

Bas

ic c

hem

ical

s

Bu

ildin

g m

ater

ials

Ligh

t m

anu

fact

uri

ng

Rea

l est

ate

Elec

tric

al e

qu

ipm

ent

Med

icin

e

CSI

300

Ind

ex

Texti

les

and

gar

men

ts

Elec

tro

nic

co

mp

on

ents

Elec

tric

an

d u

tiliti

es

Co

mm

erci

al r

etai

ling

Mac

hin

ery

Arc

hit

ectu

re

No

n-b

ank

fin

anci

als

Cat

erin

g an

d t

ou

rism

Agr

icu

ltu

re a

nd

far

min

g

Tran

spo

rtati

on

Def

ence

Med

ia

Co

mp

ute

r

6

Code Name Change Industry Code Name Change Industry

300474.SZ Jingjia Micro 530.0916 Defence industry 002018.SZ CEFC Anhui Interna-tional Holding

-45.8154 Basic chemicals

603028.SH Jiangsu Safety Wire Rope

371.1256 Steel 000034.SZ Digital China -29.3023 Agriculture and farming

603701.SH Zhejiang Dehong Automotive Electron-

ic & Electrical

245.2160 300028.SZ Geeya Technology -28.4436 Electronic compo-nents

300484.SZ Shenzhen V&T Tech-nologies

227.0291 Electrical equipment 300336.SZ Shanghai New Cul-ture Media Group

-26.4550 Media

603798.SH Qingdao Copton Technology

177.2771 002546.SZ Nanjing Xinlian Electronics

-26.0471 Computers

002793.SZ Zhejiang Doyin Pump Industry

159.5708 600116.SH Three Gorges Capital Holdings

-25.5492 Electric and utilities

603868.SH Shanghai Flyco Elec-trical Appliance

135.8629 300401.SZ Zhejiang Garden Bio-Chemical High-Tech

-25.3803 Medicine

300506.SZ Shenzhen Minkave Technology

119.1265 Architecture 002536.SZ Henan Province Xixia Automobile Water

-24.9319 Automobiles

300508.SZ Shanghai Weihong Electronic Technolo-

114.3499 002768.SZ Qingdao Gon Tech-nology

-24.7315 Basic chemicals

002792.SZ Tongyu Communica-tion

82.7116 Communication 300437.SZ Henan Qing Shui Yuan Technology

-24.2577 Basic chemicals

603726.SH Zhejiang Langdi Group

77.1462 002631.SZ Der Future Science & Technology Holding

Group

-24.2518 Agriculture and farming

002427.SZ Zhejiang Unifull Industrial Fiber

67.1252 Basic chemicals 600538.SH Beihai Gofar Marine Biological Industry

-23.8223 Basic chemicals

002168.SZ Shenzhen Hifuture Electric

67.0416 Electrical equipment 002346.SZ Shanghai Zhezhong Group

-23.7445 Building materials

000980.SZ Huangshan Jinma 62.7155 Automobiles 300431.SZ Beijing Baofeng Technology

-23.6087 Media

002786.SZ Shenzhen Silver Basis Technology

61.5255 Machinery 000676.SZ Genimous Invest-ment

-23.1874 Electrical equipment

002610.SZ Jiangsu Akcome Science & Technolo-

55.9921 Electrical equipment 002751.SZ Shenzhen ESUN Display

-22.9320 Light manufacturing

600890.SH Cred Holding 55.0459 Real estate 000626.SZ Lianyungang Ideal Group

-22.6548 Commercial retailing

002643.SZ Valiant 52.3793 Basic chemicals 300023.SZ Bode Energy Equip-ment

-22.4623 Non-banking finance

300509.SZ Jiangsu Newamstar Packaging Machinery

46.3235 002280.SZ Hangzhou Liaison Interactive Infor-

mation Technology

-22.0949 Computers

300141.SZ Heshun Electric 44.1030 Electrical equipment 002776.SZ Guangdong Bobaolon -21.7810 Textiles and gar-ments

Sources: WIND, China Galaxy Securities Research

Figure 7: The Best and Worst 20 Stocks in April and Related Industries

The best 20 stocks The worst 20 stocks

7

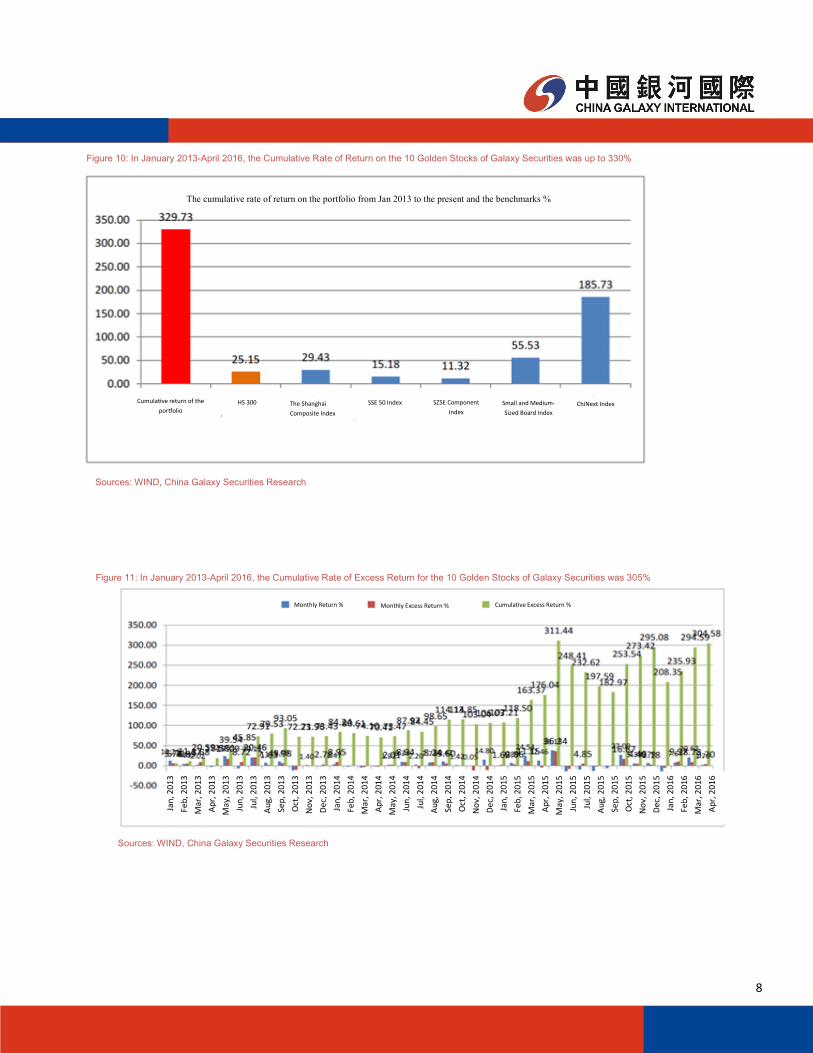

(3) 4M2016 cumulative rate of return on portfolio: -3%, with excess return 12.4ppt

In January-April 2016, the cumulative rate of return for the monthly portfolio of Galaxy Securities was -3%,

12.4ppt higher than CSI 300 Index.

In January-April 2016, the monthly cumulative rate of return for the Galaxy Securities portfolio was 330%,

higher than ChiNext Index by 186ppt, and much higher than other indexes – 305ppt higher than the CSI 300

Index.

Fig.4: In January-April 2016, the Monthly Cumulative Rate of Return for the 10 Super Stocks of Galaxy Secu-

rities was -3% Index by 295.08pct.

Cumulative return

of the portfolio

Sources: WIND, China Galaxy Securities Research

Figure 8: In January-April 2016, the Monthly Cumulative Rate of Return for the 10 Super Stocks of Galaxy Securities was -3%

Sources: WIND, China Galaxy Securities Research

Figure 9: In January-April 2016, the Monthly Cumulative Rate of Excess Return for the 10 Golden Stocks of Galaxy Securities was 12.4ppt

HS 300 The Shanghai

Composite Index SSE 50 Index SZSE Component Index ChiNext Index

The portfolio’s cumulative rate of return in 2016 and the benchmarks %

SME Index

Monthly Return % Monthly Excess Return % Cumulative Excess Return %

Jan, 2016 Feb, 2016 Mar, 2016 Apr, 2016

8

Sources: WIND, China Galaxy Securities Research

Figure 11: In January 2013-April 2016, the Cumulative Rate of Excess Return for the 10 Golden Stocks of Galaxy Securities was 305%

Jan

, 20

13

Feb

, 20

13

Mar

, 20

13

Ap

r, 2

013

May

, 20

13

Jun

, 201

3

Jul,

20

13

Au

g, 2

01

3

Sep

, 20

13

Oct

, 201

3

No

v, 2

01

3

Dec

, 20

13

Jan

, 20

14

Feb

, 20

14

Mar

, 20

14

Ap

r, 2

014

May

, 20

14

Jun

, 201

4

Jul,

20

14

Au

g, 2

01

4

Sep

, 20

14

Oct

, 201

4

No

v, 2

01

4

Dec

, 20

14

Jan

, 20

15

Feb

, 20

15

Mar

, 20

15

Ap

r, 2

015

May

, 20

15

Jun

, 201

5

Jul,

20

15

Au

g, 2

01

5

Sep

, 20

15

Oct

, 201

5

No

v, 2

01

5

Dec

, 20

15

Jan

, 20

16

Feb

, 20

16

Mar

, 20

16

Ap

r, 2

016

Monthly Return % Monthly Excess Return % Cumulative Excess Return %

Sources: WIND, China Galaxy Securities Research

Figure 10: In January 2013-April 2016, the Cumulative Rate of Return on the 10 Golden Stocks of Galaxy Securities was up to 330%

Cumulative return of the

portfolio HS 300 The Shanghai

Composite Index

SSE 50 Index SZSE Component

Index ChiNext Index

The cumulative rate of return on the portfolio from Jan 2013 to the present and the benchmarks %

Small and Medium-

Sized Board Index

9

(1) May trend prediction: Rally to continue

Outlook for May: The fundamentals of domestic economic policies are still the dominant focus. The

economy may improve, but increasing inflation may impact monetary policy, with concerns about

liquidity and credit risk. The capital markets will focus on institutional developments and whether A-

shares will be included into MSCI index.

Generally, the rally should continue in May, but close attention should be paid to inflation and chang-

es in liquidity.

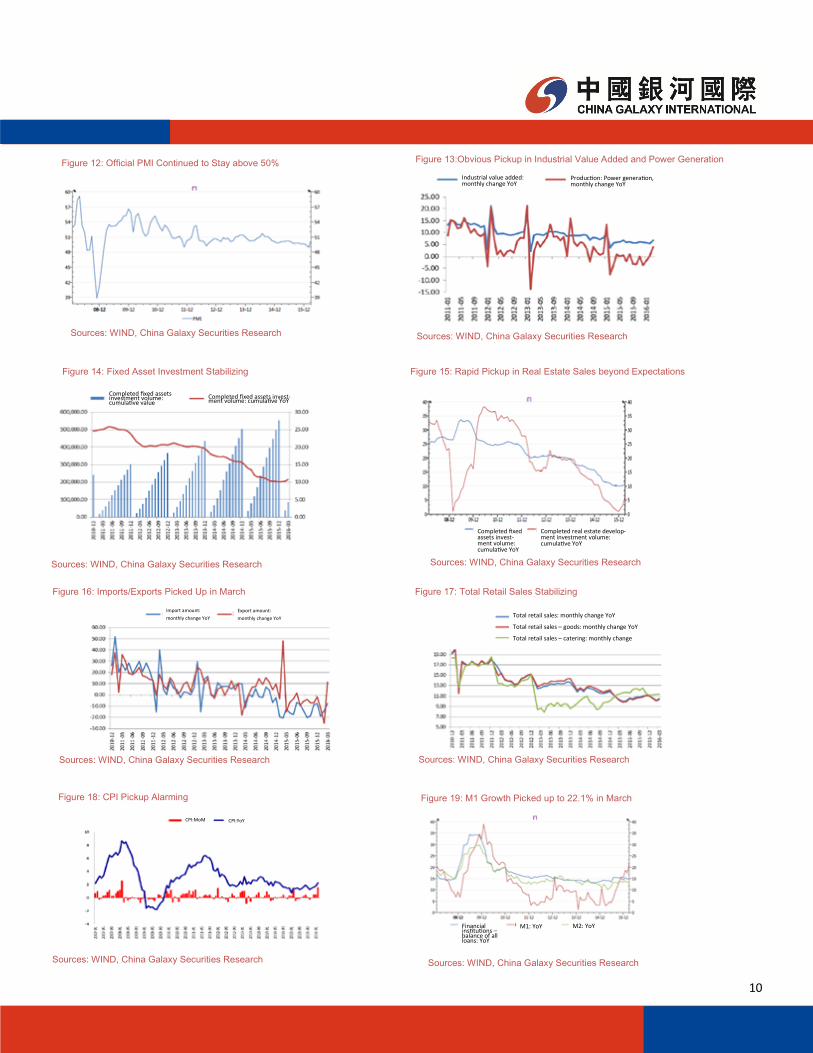

1. Fundamentals: The economy shows signs of stabilizing

The GDP growth rate has fallen slightly. The GDP in Q1 2016 grew 6.7% YoY, a decrease of 0.1ppt

compared with Q4 2015, which basically met recent market expectations, indicating improvement

compared with the pessimistic expectations at the beginning of 2016. However, Q1 growth was only

1.1% QoQ, so there is still considerable downward pressure on the economy. The tertiary industry

contribution rate to GDP increased to 62.8%, an increase of 5.1ppt, with real estate’s contribution

reached up 8.6%, an increase of 5.3ppt, becoming the main driver of economic growth in Q1. The

March PMI was 50.2%, up 1.2ppt from that of February, and the April PMI remained above 50%.

Industry growth picked up and industry profits rebounded. Industrial production saw YoY growth of

6.8% in March, an increase of 1.4ppt compared with 2M2016, and the highest in 12 months. Electric

power generation in March was 477.9 bn kWh, for YoY growth of 4%, a significant increase of 3.7ppt

over that of 2M2016. The pick-up in purchase orders for the manufacturing industry reflected im-

provement in demand from both domestic and overseas markets, which may be maintained for a

while. However, from a long-term perspective, the industry as a whole is facing overcapacity, and

thus downward pressure in the future, with the combination of stabilized growth and structural re-

form. A hard fall is unlikely, given government support. Industry profit in April saw YoY growth of

11.1%, representing continuous improvement over 2M2016.

Infrastructure construction and real estate development stimulated a pick-up in investment. Fixed

asset investment in Q1 was RMB8.58trn, up 10.7% YoY, and rose 0.5ppt compared with 2M2016.

QoQ investment growth reached 0.86% in March. Non-governmental fixed asset investment in Q1

amounted to RMB5.32trn, up 5.7% YoY, but down 1.2ppt compared with 2M2016. Non-

governmental investment growth fell further than overall investment growth, indicating non-

governmental investment is still weak. The upward increase in investment still relied mainly on infra-

structure construction and real estate investment. Infrastructure construction in Q1 was up 19.3%

and real estate growth was up 6.2%. Regarding their contribution to fixed asset investment, infra-

structure construction rose to17.9%, while real estate investment experienced a slight drop to

20.6%.

There was a steady increase in consumption, with both imports and exports picking up. Total retail

sales in March amounted to RMB2511.4bn, for a YoY nominal increase of 10.5%, up 0.3ppt com-

pared with that of 2M2016. Consumption was stable, but it is still difficult to stimulate the economy

before there is any income distribution reform or new consumption drivers. Imports and exports in

March improved significantly because of a low base for comparison and genuine improvement.

Generally speaking, the data of March showed significant indications of stability and even a rally,

and further growth is expected in Q2.

II. Investment ideas for May 2016

10

Figure 12: Official PMI Continued to Stay above 50% Figure 13:Obvious Pickup in Industrial Value Added and Power Generation

Figure 14: Fixed Asset Investment Stabilizing

Sources: WIND, China Galaxy Securities Research

Figure 15: Rapid Pickup in Real Estate Sales beyond Expectations

Figure 16: Imports/Exports Picked Up in March

Sources: WIND, China Galaxy Securities Research

Figure 17: Total Retail Sales Stabilizing

Sources: WIND, China Galaxy Securities Research

Completed fixed assets investment volume: cumulative value

Sources: WIND, China Galaxy Securities Research

Comparison with the previous month

Completed fixed assets invest-ment volume: cumulative YoY

Sources: WIND, China Galaxy Securities Research Sources: WIND, China Galaxy Securities Research

Completed fixed assets invest-ment volume: cumulative YoY

Completed real estate develop-ment investment volume: cumulative YoY

Import amount:

monthly change YoY Total retail sales: monthly change YoY

Total retail sales – goods: monthly change YoY

Total retail sales – catering: monthly change

CPI:MoM

Export amount:

monthly change YoY

CPI:YoY

Financial institutions – balance of all loans: YoY

M1: YoY M2: YoY

Figure 18: CPI Pickup Alarming Figure 19: M1 Growth Picked up to 22.1% in March

Sources: WIND, China Galaxy Securities Research

Industrial value added: monthly change YoY

Production: Power generation, monthly change YoY

Sources: WIND, China Galaxy Securities Research

11

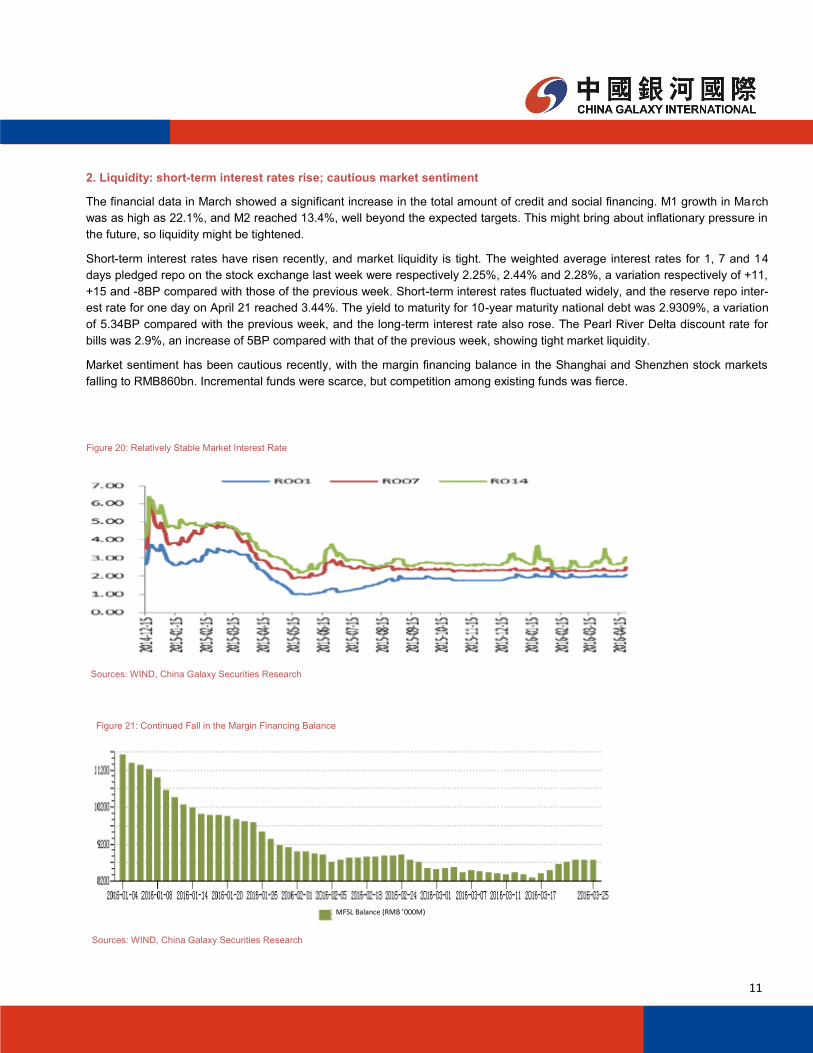

2. Liquidity: short-term interest rates rise; cautious market sentiment

The financial data in March showed a significant increase in the total amount of credit and social financing. M1 growth in March

was as high as 22.1%, and M2 reached 13.4%, well beyond the expected targets. This might bring about inflationary pressure in

the future, so liquidity might be tightened.

Short-term interest rates have risen recently, and market liquidity is tight. The weighted average interest rates for 1, 7 and 14

days pledged repo on the stock exchange last week were respectively 2.25%, 2.44% and 2.28%, a variation respectively of +11,

+15 and -8BP compared with those of the previous week. Short-term interest rates fluctuated widely, and the reserve repo inter-

est rate for one day on April 21 reached 3.44%. The yield to maturity for 10-year maturity national debt was 2.9309%, a variation

of 5.34BP compared with the previous week, and the long-term interest rate also rose. The Pearl River Delta discount rate for

bills was 2.9%, an increase of 5BP compared with that of the previous week, showing tight market liquidity.

Market sentiment has been cautious recently, with the margin financing balance in the Shanghai and Shenzhen stock markets

falling to RMB860bn. Incremental funds were scarce, but competition among existing funds was fierce.

Figure 20: Relatively Stable Market Interest Rate

Sources: WIND, China Galaxy Securities Research

Figure 21: Continued Fall in the Margin Financing Balance

Sources: WIND, China Galaxy Securities Research

MFSL Balance (RMB ’000M)

12

3. Policy: Stable, with fine adjustments to ensure healthy stock market development

Overseas markets. Close attention is paid to expectations of an interest rate increase by the Fed, along with a series of recent data

releases in the US. The market is not convinced the Fed will raise the interest rate, so there should not be a significant shrinkage of

global liquidity. This is quite different from the situation last year.

National policy. The Political Bureau of the CCP Central Committee convened a meeting at the end of April to analyze the current eco-

nomic situation and plan future economic measures, which set the main policy tone for next period. The following main issues were

covered in the meeting:

(a) Firstly, there was a summary of the economic work completed in Q1, and the conclusion was positive. GDP growth, new urban

jobs, urban and rural income growth, and other major economic indicators were in line with expectations. The economy was operating

within an appropriate range. Agricultural production maintained good momentum, industrial enterprises improved efficiency, the ser-

vice sector continued to account for a high portion of the economy, restructuring was advancing, and social undertakings were devel-

oping well. Some industries with high degree of market orientation and emphasis on innovation had seen increases in growth in terms

of quality and benefits. Supply-side structural reform was better understood by the various regions and departments. As a result, they

were carrying out their work actively and there was already gradual evidence of initial success.

(b) Secondly, there was an analysis of the future economic situation. Economic downturn pressure was still high, and some enterpris-

es still had difficulty in production and operations, increasing market risks. It was agreed that close attention must be paid to existing

conflicts and problems, that they must be analyzed calmly, that specific corresponding measures must be taken, and that we must get

ready for a protracted uphill battle.

(c) The third point had to do with the general tone of future policy: (i) adhering to the moderate expansion of aggregate demand, (ii)

implementing a proactive fiscal policy and prudent monetary policy, (iii) taking the promotion of supply-side structural reforms firmly as

the main line, (iv) accelerating new development momentum, (v) transforming and upgrading traditional comparative advantages, (vi)

fully implementing the five key tasks of "cutting overcapacity and excess inventory, de-leveraging, reducing costs, and strengthening

points of weakness", and (vii) ensuring that there is no deviation from, or deformation of, the policies determined by the Central Com-

mittee of the Communist Party of China (CPC) and ensuring the full and rigid implementation of these policies. At the end of last year,

the Central Economic Work Conference defined the macro policy goals for 2016 as "stronger proactive fiscal policy" and "monetary

policy that is neither too tight nor too loose". The overall tone regarding monetary and fiscal policies during this conference remained

unchanged. The goals are still defined as proactive fiscal policy and stable monetary policy, but the emphasis on "stronger" and

"neither too tight nor too loose" was not mentioned again. This may have been due to the stable economic growth in Q1, high mone-

tary growth, and positive results in other indexes, so only fine adjustment measures were needed.

(d) The fourth issue involved strengthening macroeconomic policy in relation to the stock market, exchange rates, real estate, employ-

ment, prices, state-owned enterprise (SOE) reform, etc.

(i) It is necessary to maintain healthy stock market development, giving full play to the role of market mechanisms, strengthening basic

system construction and market supervision, and protecting the interests of investors. It is rare to see the Central Government address

the healthy development of the stock market, so this shows the great importance of the Central Government gives to the stock market.

Capital markets pay a lot of attention to building a solid foundation for the sytem. Other focus include the introduction of long-term

funds such as regional social security funds and whether or not A-shares will be included in the MSCI index.

(ii) The RMB exchange rate should be kept basically stable, and a market-based, two-way floating exchange rate and flexible opera-

tion mechanism should gradually be formed. In the context of a weakened expectation on US rate hike, the RMB exchange rate has a

stable foundation.

(iii) Efforts will be stepped up to increase the number of Chinese people registered as permanent urban residents and to deepen the

reform of housing system requirements to help stimulate an orderly cut in real estate inventory. There will also be a greater focus on

regional and structural problems, and on implementing appropriate regulatory policies for specific circumstances.

(iv) The objective is to maintain stable employment, properly handle the issue of employment in the process of economic restructuring,

help employees adapt to new economic circumstances, and improve their re-employability.

13

Sector Name PE ratio (TTM)

3.25 PE 2015.6.12 PE 2015.8.25 PE 2012.12.4

CSI 300 Index 11.77 10.68 11.20 9.49

A-share in Shanghai Stock Exchange 14.03 12.50 13.32 10.21

All A-shares 19.51 17.08 17.87 11.94

SME market 52.97 45.02 48.49 24.02

ChiBext 69.34 67.04 75.90 28.53

SP500 Composition 22.88 19.81 19.12 15.50

Nasdaq Composite 19.46 17.94 17.54 16.82

Russell 2000 index 289.36 89.92 50.57 29.64

Figure 22: A Share Valuation Structure and International Comparison

Sources: WIND, China Galaxy Securities Research

4. Structural undervaluation

At present, blue chips are under-valued, performance of growth stocks are differentiated, with some high-quality stocks offering long-

term investment value. With the strengthening of regulations and a stronger execution of delisting, companies with poor performance

and a weak restructuring potential face risks.

(v) Attention must be paid to price changes, guaranteeing effective supply, and actively and steadily pushing forward price reforms.

There was not too much concern on pressure on the CPI from rising food prices because of the cyclical nature of agricultural prices.

(vi) Market confidence is expected to be enhanced by adhering to the basic economic system, deepening the reform of SOEs, promot-

ing the healthy development of the non-public economy, expanding the opening-up process to attract foreign capital to invest in China,

and ensuring stable development.

The official report of the central meeting did not directly mention recent market concerns about credit risk, indicating that credit risk is

not considered to be a big issue impacting the overall situation and that it can be addressed through the general adjustment mecha-

nisms in the systematic and regional financial risk-control policies.

Viewed as a whole, the policy environment in May will be favourable to A-shares.

14

5. Market trend and investment views

(a) Investment views: upward but turbulent market trend will continue

Outlook for May: The fundamentals of domestic economic policies will be the dominant factors affecting market

trends. Though economic improvement will continue in Q2, consumer prices may influence monetary policy. As

for liquidity, the emphasis will be on “stability” and concern about credit risk. Capital markets will focus on build-

ing a solid foundation for the system and whether A-shares will be included in the MSCI index.

Generally, the markets in May should see a continuation of the rally with attention to inflation and liquidity

changes.

(b) Investment strategy and sector allocation: neutral to optimistic; choose stocks carefully with atten-

tion to small cap growth stocks

For May, the market is neutral to optimistic, and stocks should be carefully chosen, paying attention to small cap

growth stocks.

(i) Prices should rise in general, with emphasis on the cyclical and consumer sectors: chemical engineering,

agriculture, food, medicine, textile and garment, light industry, etc.

(ii) Examine opportunities related to the consumption peak season: e.g. tourism.

(iii) Carefully choose high-quality growth stocks with reasonable valuation: technology, media and telecommuni-

cations (TMT), machinery and military equipment.

(iv) Consider thematic opportunities: e.g. SOE reform, Disney.

(c) Risk factors

Risk factors include (a) credit risk and liquidity pressure exceeding expectations, and (b) downward pressure on

the economy exceeding expectations.

II. May portfolio

Portfolio of May: 1 petrochemical stock, 2 machinery and military industry stocks, 1 non-ferrous metal stock, 1

light manufacturing stock, 1 food & beverage stock, 1 construction stock, 1 electrical equipment & new energy

stock, 1 electronics stock, and 1 computer stock.

Stock portfolio in current month (pari passu):

Geo-Jade Petroleum (600759.CH)

Longhua Energy-saving (300263.CH)

Anhui Zhongding (000887.CH)

Chenming Paper (000488.CH)

Hengshun Zhongsheng (300208.CH)

Shuanghui Development (000895.CH)

Arts Group (603017.CH)

Pinggao Electric (600312.CH)

DMEGC (002056.CH)

Conant (300061.CH)

15

Sources: China Galaxy Securities Research

Figure 23: Portfolio of May for Galaxy Securities (Note: share prices are the closing prices on May 16, 2016)

Stock

Code

Stock Discription EPS (RMB) PE (X)

2014A 2015A 2016E 2017E 2014A 2015A 2016E 2017E

600759.SH Geo-Jade Petroleum 0.02 0.03 0.06 0.34 393.0 262.0 131.0 23.1

300263.SZ Longhua Energy-saving 0.33 0.40 0.50 0.62 47.6 39.3 31.4 25.3

000887.SZ Anhui Zhongding 0.47 0.76 1.05 1.33 44.1 27.3 19.7 15.6

000488.SZ Chenming Paper 0.26 0.53 1.02 1.37 32.0 15.7 8.2 6.1

000895.SZ Shuanghui Development 1.84 1.29 1.35 1.48 11.6 16.6 15.9 14.5

603017.SH Arts Group 0.75 0.55 1.04 1.31 44.6 60.8 32.2 25.5

600312.SH Pinggao Electric 0.61 0.73 0.86 1.02 23.3 19.5 16.5 13.9

002056.SZ DMEGC 0.93 0.79 1.02 1.29 14.8 17.4 13.5 10.7

300208.SZ Hengshun Zhongsheng 0.15 0.42 0.70 1.26 92.1 32.9 19.7 11.0

300061.SZ Conant 0.24 0.21 0.48 0.66 120.3 137.4 60.1 43.7

16

Content

Geo-Jade Petroleum (600759.CH): Belt and road play, overseas oil and gas acquisitions ........................................................ 17

Conant (300061.CH): Traditional business upgraded, M&A advancing soundly to build a leading consumer finance stock ....... 19

Longhua Heat Transfer & Energy Conservation (300263.CH): Management expected to introduce major changes .............. 21

Lnhui Zhongding (000887.CH): Good potential development from environmental protection engines for UAVs, charging piles,

and after-market components for vehicles.................................................................................................................................... 23

Henan Shuanghui Investment & Development Co., Ltd. (000895.CH): Positive development trend for new products, slaughter

capacity expected to rise .............................................................................................................................................................. 25

Shandong Chenming Paper Holdings Limited (000488.CH): Excellent leading enterprise expected to benefit from supply-side

reform, two main businesses with satisfactory performance ........................................................................................................ 27

Qingdao Hengshun Zhongsheng Group Co., Ltd. (300208.CH): China replicating its model to the world at top speed.......... 29

Henan Pinggao Electric Co., Ltd. (600312.CH): Expedited delivery of ultra-high voltage products, good potential for charging

pile sales ...................................................................................................................................................................................... 31

Arts Group Co., Ltd. (603017.CH): Industrial park development service provider, domestic and international growth potential

..................................................................................................................................................................................................... 33

DMEGC (002056.CH): Driven by growth and cyclical factors, concurrent development of magnetic materials and new energy

..................................................................................................................................................................................................... 35

17

Geo-Jade Petroleum (600759.CH): Belt and Road potential, overseas oil and gas ac-

quisitions

Driving factors, key assumptions and main predictions:

The Company intends to increase its capital through an RMB8.2bn equity offering and another RMB7bn supporting loan, for a total of

RMB15.2bn, to purchase three overseas high-quality oil and gas assets through Shanghai Longzhou Xinke, which is a major project

involving bargain-hunting for overseas oil and gas assets arising as a result of low oil prices.

With the completion of this acquisition, the residual recoverable reserves of the Company will more than double, from 218m barrels to

553m barrels, and annual output will increase over five-fold, from 0.65m tons to 3.64m tons. Residual recoverable reserves for each

10,000 shares will rise from 963 tons to 1,349 tons; crude output for each 10,000 shares will increase from 2.9 tons to 8.9 tons. Earn-

ingsare based on oil prices, with each US$10/barrel rise resulting in another approximately RMB1bn in net profit.

The supply-over-demand pattern is expected to improve in 2016, but it may be seen only in 2H, which means the oil price may be low

in 1H, but higher in 2H. The previous oil price below US$30 was below the full cost of production for most global oil companies, with

the exception of those in the Middle East, which has increased the risk of political unrest in many of the main oil-producing countries.

In our opinion, before the expectation that OPEC would reduce output fell through, it was unlikely that oil prices would face major

risks. We should note that the failure of the output-reduction plan, combined with inventory accumulation, may cause the oil price to

fall, but it is unlikely to give rise to another new low. The price is expected to rebound to US$40–50 by the end of this year.

Main financial indicators 2014 2015 2016E 2017E 2018E

Operating income (RMB m) 1,387 1,261 6,978 9,230 13,845

Operating income growth rate -9.13% 468% 32% 50%

Net profit (RMB m) 85 65 249 1,385 3,231

Net profit growth rate / -24% 8208% 317% 133%

EPS (RMB) (DILUTED) 0.02 0.03 0.06 0.34 0.79

P/E 393.0 262.0 131.0 23.1 10 Sources: Company data,China Galaxy Securities Research

Investment Rating:

Recommend

Wang Qiang: (8621)20252621 [email protected] No. of certificate to practice: S0130511080002

Qiu Xiaofeng: (8621) 20252676 [email protected] No. of certificate to practice: S0130511050001

How our views differ from the market’s

Originally, oversupply and weak demand were considered to

have been the two key reasons for the falling oil price. The

agreement among major oil-producing countries to freeze

production caused a rise in the oil price in this round. For a

considerable period in the future, the key factors affecting

the oil price will be transferred to the supply end: i.e. wheth-

er OPEC is able to continue the “freeze production” policy.

In the long run, the current international oil price of US$30-

40 per barrel is in the bottom range. Future downslide poten-

tial is considered unlikely, which means this is the best time

to purchase high-quality overseas oil and gas resources.

The One-Belt, One Road strategy introduced by China and

development strategies related to oil and gas will proceed

simultaneously, “driven by two wheels”. Therefore, the Com-

pany is expected to become a middle-to-large international

oil company.

Company valuation and investment recommendation

Provided that the average oil price of Brent Crude in

2016–2018 is US$42, 50 or 60 a barrel, and provided

that the purchase is settled in October this year, crude

output in 2016, 2017 and 2018 is expected to reach

1.15m, 4m, and 5m tons, respectively. We estimate

that the net profit of the Company in 2016, 2017 and

2018 will be RMB80m, 1.38bn, and 3.231bn, respec-

tively, provided all RMB4.1bn of additional equity is

fully diluted, and that the EPS will be RMB0.02, 0.34,

and 0.79, respectively. We give it a “Recommend”

rating.

18

Catalyst for share price performance

International crude oil price stabilizing or rebounding.

Continued success in overseas assets acquisition.

Main risk factors

Another oil price decline and continued lack of stability.

Slower than expected progress in share placement and acquisition.

19

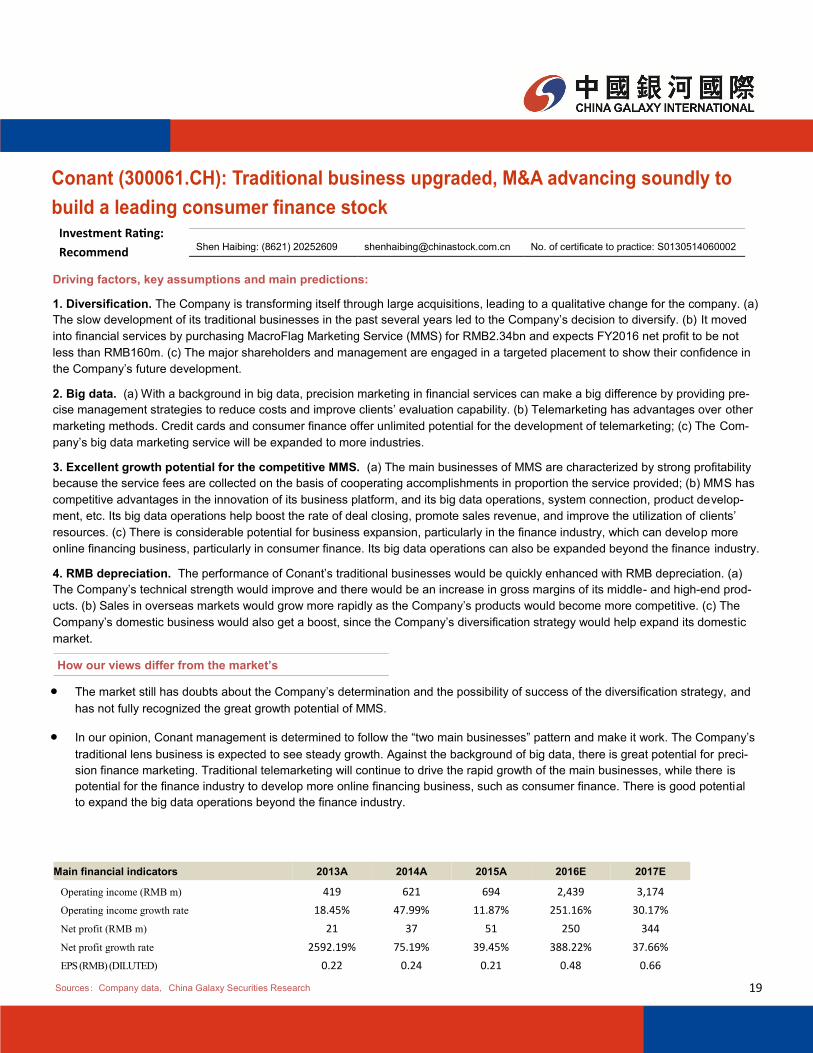

Conant (300061.CH): Traditional business upgraded, M&A advancing soundly to

build a leading consumer finance stock

Driving factors, key assumptions and main predictions:

1. Diversification. The Company is transforming itself through large acquisitions, leading to a qualitative change for the company. (a)

The slow development of its traditional businesses in the past several years led to the Company’s decision to diversify. (b) It moved

into financial services by purchasing MacroFlag Marketing Service (MMS) for RMB2.34bn and expects FY2016 net profit to be not

less than RMB160m. (c) The major shareholders and management are engaged in a targeted placement to show their confidence in

the Company’s future development.

2. Big data. (a) With a background in big data, precision marketing in financial services can make a big difference by providing pre-

cise management strategies to reduce costs and improve clients’ evaluation capability. (b) Telemarketing has advantages over other

marketing methods. Credit cards and consumer finance offer unlimited potential for the development of telemarketing; (c) The Com-

pany’s big data marketing service will be expanded to more industries.

3. Excellent growth potential for the competitive MMS. (a) The main businesses of MMS are characterized by strong profitability

because the service fees are collected on the basis of cooperating accomplishments in proportion the service provided; (b) MMS has

competitive advantages in the innovation of its business platform, and its big data operations, system connection, product develop-

ment, etc. Its big data operations help boost the rate of deal closing, promote sales revenue, and improve the utilization of clients’

resources. (c) There is considerable potential for business expansion, particularly in the finance industry, which can develop more

online financing business, particularly in consumer finance. Its big data operations can also be expanded beyond the finance industry.

4. RMB depreciation. The performance of Conant’s traditional businesses would be quickly enhanced with RMB depreciation. (a)

The Company’s technical strength would improve and there would be an increase in gross margins of its middle- and high-end prod-

ucts. (b) Sales in overseas markets would grow more rapidly as the Company’s products would become more competitive. (c) The

Company’s domestic business would also get a boost, since the Company’s diversification strategy would help expand its domestic

market.

Shen Haibing: (8621) 20252609 [email protected] No. of certificate to practice: S0130514060002

Sources: Company data, China Galaxy Securities Research

Investment Rating:

Recommend

Main financial indicators 2013A 2014A 2015A 2016E 2017E

Operating income (RMB m) 419 621 694 2,439 3,174

Operating income growth rate 18.45% 47.99% 11.87% 251.16% 30.17%

Net profit (RMB m) 21 37 51 250 344

Net profit growth rate 2592.19% 75.19% 39.45% 388.22% 37.66%

EPS (RMB) (DILUTED) 0.22 0.24 0.21 0.48 0.66

How our views differ from the market’s

The market still has doubts about the Company’s determination and the possibility of success of the diversification strategy, and

has not fully recognized the great growth potential of MMS.

In our opinion, Conant management is determined to follow the “two main businesses” pattern and make it work. The Company’s

traditional lens business is expected to see steady growth. Against the background of big data, there is great potential for preci-

sion finance marketing. Traditional telemarketing will continue to drive the rapid growth of the main businesses, while there is

potential for the finance industry to develop more online financing business, such as consumer finance. There is good potential

to expand the big data operations beyond the finance industry.

20

Catalyst for share price performance

Consumer finance has support from national policy.

Completion of extended M&A.

Main risk factors

The Company’s performance does not meet expectations

after diversification.

Fierce market competition.

Company valuation and investment recommendations

With its purchase of MMS, the Company now has diversified its business, with two main businesses advancing simultane-

ously. The traditional lens business is on a steady upward trend. With the strong development of MMS, bank precision mar-

keting has the potential to expand to more industries against the big data background. The telemarketing industry also has

good prospects.

We expect the net profit of the Company in 2016–2017 to be RMB250m and 344m, and the EPS to be RMB0.48 and 0.66,

respectively. Therefore, we maintain our "Recommend" rating.

21

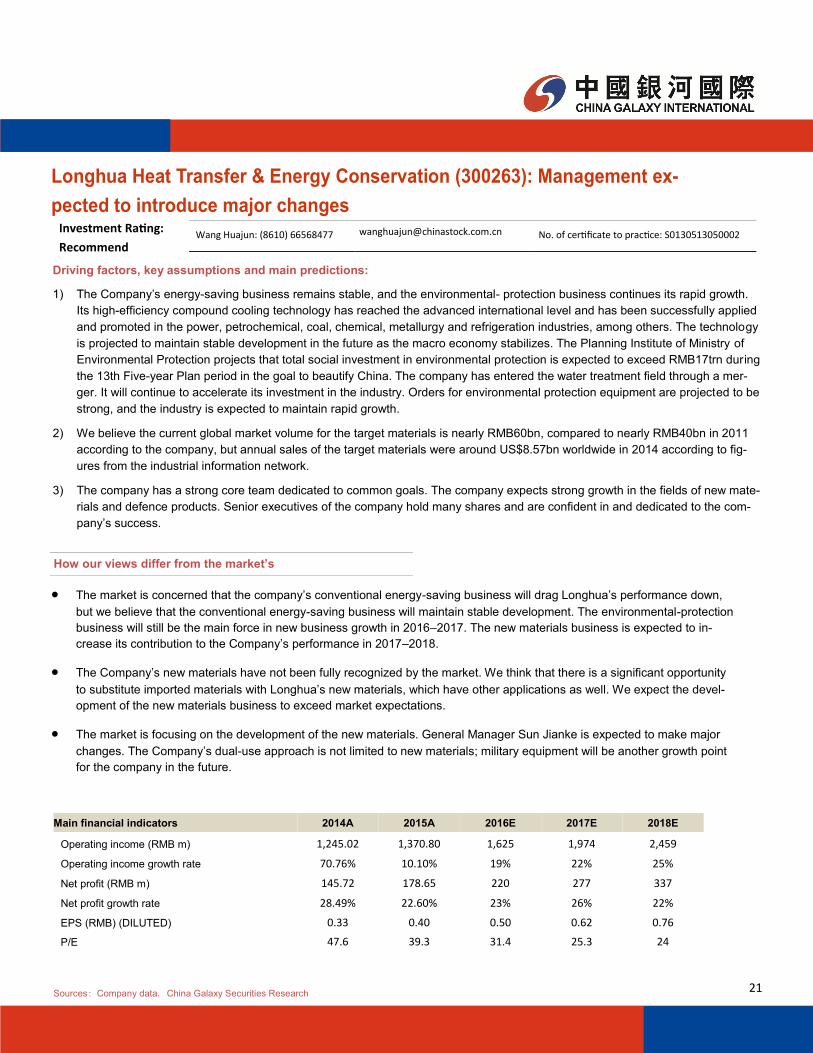

Longhua Heat Transfer & Energy Conservation (300263): Management ex-

pected to introduce major changes

Driving factors, key assumptions and main predictions:

1) The Company’s energy-saving business remains stable, and the environmental- protection business continues its rapid growth.

Its high-efficiency compound cooling technology has reached the advanced international level and has been successfully applied

and promoted in the power, petrochemical, coal, chemical, metallurgy and refrigeration industries, among others. The technology

is projected to maintain stable development in the future as the macro economy stabilizes. The Planning Institute of Ministry of

Environmental Protection projects that total social investment in environmental protection is expected to exceed RMB17trn during

the 13th Five-year Plan period in the goal to beautify China. The company has entered the water treatment field through a mer-

ger. It will continue to accelerate its investment in the industry. Orders for environmental protection equipment are projected to be

strong, and the industry is expected to maintain rapid growth.

2) We believe the current global market volume for the target materials is nearly RMB60bn, compared to nearly RMB40bn in 2011

according to the company, but annual sales of the target materials were around US$8.57bn worldwide in 2014 according to fig-

ures from the industrial information network.

3) The company has a strong core team dedicated to common goals. The company expects strong growth in the fields of new mate-

rials and defence products. Senior executives of the company hold many shares and are confident in and dedicated to the com-

pany’s success.

Wang Huajun: (8610) 66568477 [email protected] No. of certificate to practice: S0130513050002

Main financial indicators 2014A 2015A 2016E 2017E 2018E

Operating income (RMB m) 1,245.02 1,370.80 1,625 1,974 2,459

Operating income growth rate 70.76% 10.10% 19% 22% 25%

Net profit (RMB m) 145.72 178.65 220 277 337

Net profit growth rate 28.49% 22.60% 23% 26% 22%

EPS (RMB) (DILUTED) 0.33 0.40 0.50 0.62 0.76

P/E 47.6 39.3 31.4 25.3 24

Sources: Company data, China Galaxy Securities Research

How our views differ from the market’s

Investment Rating:

Recommend

The market is concerned that the company’s conventional energy-saving business will drag Longhua’s performance down,

but we believe that the conventional energy-saving business will maintain stable development. The environmental-protection

business will still be the main force in new business growth in 2016–2017. The new materials business is expected to in-

crease its contribution to the Company’s performance in 2017–2018.

The Company’s new materials have not been fully recognized by the market. We think that there is a significant opportunity

to substitute imported materials with Longhua’s new materials, which have other applications as well. We expect the devel-

opment of the new materials business to exceed market expectations.

The market is focusing on the development of the new materials. General Manager Sun Jianke is expected to make major

changes. The Company’s dual-use approach is not limited to new materials; military equipment will be another growth point

for the company in the future.

22

Catalyst for share price performance

The company obtains major orders.

The Company has a breakthrough in the development of new

materials.

The company successfully implements M&A

Main risk factors

The Company’s conventional business weakens.

The development of new materials is slower than expec-

tations.

The progress of its M&A expansion is below expectations.

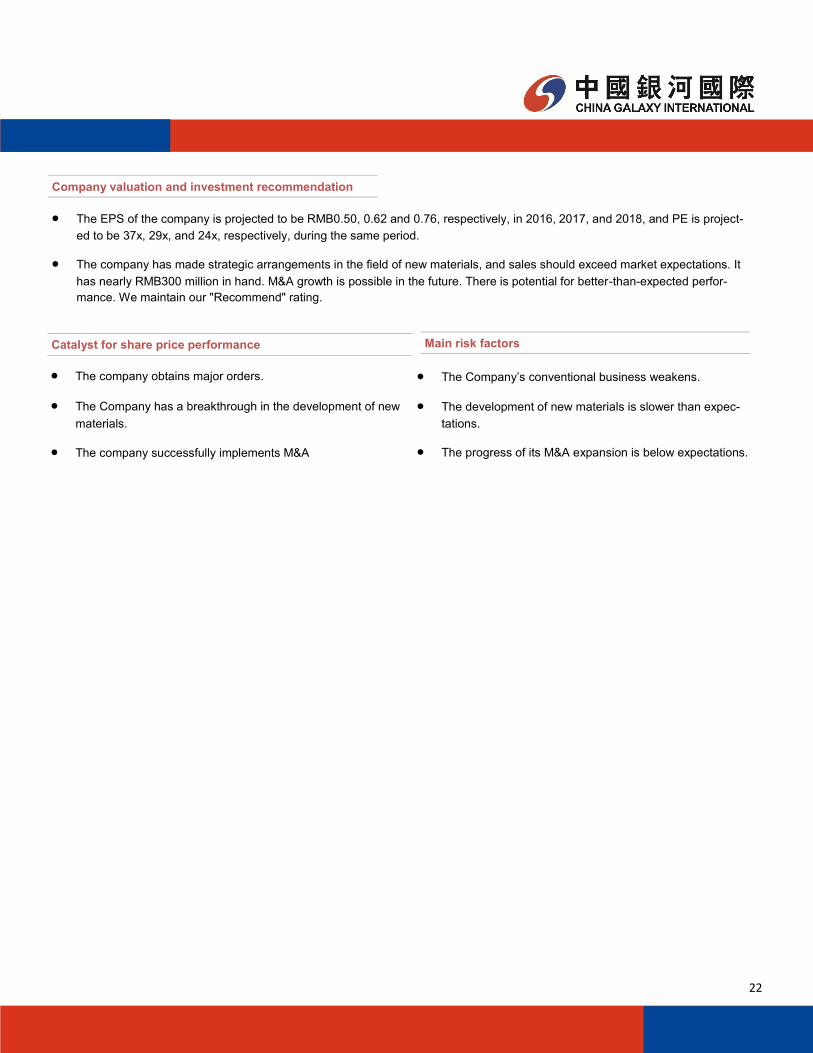

Company valuation and investment recommendation

The EPS of the company is projected to be RMB0.50, 0.62 and 0.76, respectively, in 2016, 2017, and 2018, and PE is project-

ed to be 37x, 29x, and 24x, respectively, during the same period.

The company has made strategic arrangements in the field of new materials, and sales should exceed market expectations. It

has nearly RMB300 million in hand. M&A growth is possible in the future. There is potential for better-than-expected perfor-

mance. We maintain our "Recommend" rating.

23

Anhui Zhongding (000887.CH): Good potential development from environmental pro-

tection engines for UAVs, charging piles, and after-market components for vehicles

Driving factors, key assumptions and main predictions:

1) Four driving forces promote the rapid growth of the company’s main business: (a) restructuring the main business, (b) cost sav-

ings, (c) export development, and (d) industry integration. The size of non-tire rubber market in China is around RMB50bn. The

company accounts for around 10% of this, but the Company’s market share is expected to increase.

2) The company has moved into the energy-saving, environmental protection and new energy vehicles field instead of the conven-

tional vehicle field. A new generation of intelligent charging products is now in mass production. The market demand for charging

piles may exceed RMB10bn in the future, so the market potential is huge. An e-commerce service platform for after-market vehi-

cle components has been created through “Internet Plus”, transforming the Company by opening up new space for growth.

3) The company conducts R&D for UAV heavy oil engines in cooperation with NORINCO GROUP. This is expected to result in an in

-depth integration of military and civilian technology in the future.

Main financial indicators 2013A 2014E 2015E 2016E 2017E

Operating income (RMB m) 4,161.69 5,040.19 6,840 9,045 11,071

Operating income growth rate 23.53% 21.11% 36% 32% 22%

Net profit (RMB m) 388.41 566.59 920 1,270 1,609

Net profit growth rate -24.83% 45.87% 62% 38% 27%

EPS(RMB)(DILUTED) 0.32 0.47 0.76 1.05 1.33

P/E 64.8 44.1 27.3 19.7 17

Sources: Company data, China Galaxy Securities Research

Investment Rating:

Recommend Wang Huajun: (8610) 66568477 wanshuajun@chinastock_com.cn No. of certificate to practice: S0130513050002

How our views differ from the market’s

The market thinks that the company’s main strengths are its large market capitalization and stable growth. We believe that the

company also benefits from its environmental protection engines, UAV engines, charging piles for new energy vehicles, etc. We

expect the Company to maintain high growth and exceed expectations in the future.

The market is concerned that the company’s businesses have a low ceiling, but we believe that it has opened up new growth

space. The Company will benefit from energy saving and environmental protection trends, new energy vehicles, and themed

investment, like the Internet of Vehicles, in the future. We expect its new business development to exceed market expectations.

The market questions the possibility of success of its OPOC engine, but we believe that there is a high probability of success.

The Company’s overseas business accounts for over 60% of its total business. The company has purchased five US companies

and three European companies. It has international vision, and we expect its overseas acquisitions to exceed market expecta-

tions in the future.

24

Catalyst for share price performance

Significant progress in the industrialization of its OPOC

environmental protection engines.

Significant progress in the Company’s M&A .

New energy vehicles and high-end seals business obtain

a major breakthrough.

Main risk factors

Industrialization risks of its OPOC environmental protec-

tion engines.

M&A is slower than expected.

The price of natural rubber and the exchange rate fluc-

tuate.

Company valuation and investment recommendations

If we don’t consider the additional share issue, EPS is projected to be RMB0.80, 1.03, and 1.24 in 2015, 2016, and 2017, re-

spectively, and PER is projected to be 28x, 22x,and 18x, respectively, during the same period.

If we take the additional share issue into account, EPS is projected to be RMB0.76, 1.05, and 1.33 in 2015, 2016, and 2017, and

PER is projected to be 29x, 21x, and 17x, respectively, during the same period. We expect the Company’s performance to im-

prove in the future and maintain our “Recommend” rating.

25

Henan Shuanghui Investment & Development Co., Ltd. (000895.CH): Positive devel-

opment trend for new products, slaughter capacity expected to rise

Driving factors, key assumptions and main predictions:

1. After a dip in Q3 2015, the Company’s business is now picking up. Industry consumption bottomed out in the Q3 2015 and im-

proved in Q4. In Q1 2016, the Company’s slaughter capacity grew 3.02% YoY and 2.05% QoQ.

2. Consumption of meat products increased, and the new American-style products are selling well. With the increase in the consump-

tion of meat products, the Company has enjoyed growth in both high-temperature and low-temperature meat products. The new

American-style products are more popular than the products launched previously, and sales are expected to increase rapidly. These

new products are highly profitable, so they can effectively enhance the Company’s profitability in meat products. In Q1, the Company

sold 341,200 tons of fresh and frozen meat products, for YoY growth of 19.72%. Sales of high-temperature and low-temperature meat

products totalled 373,700 tons, for YoY growth of 7.98%.

3. The Company’s global procurement advantages are helping control costs. As an industry giant, the Company has always had

strong cost controls, even more so with the acquisition of Smithfield Foods. The Company can counter rising domestic costs by utiliz-

ing overseas resources available at lower prices, which was especially important with the increase in the price of domestic pork from

2H 2015 to Q1 2016. In 2015, the Company purchased 160,000 tons of pork abroad, a rapid increase in the import percentage of its

pork purchases. In the future, this is expected to become normalized.

Investment Rating:

Recommend Zhou Ying: (8610) 66568301 [email protected] No. of certificate to practice: S0130511090001

How our views differ from the market’s

Despite some frustration in the promotion of its new prod-

ucts, we believe that the Company, as a major player in the

industry, can afford some losses through trial and error. Its

status will not be challenged. When products succeed, they

will generate considerable profits.

Because meat-consumption patterns change slowly, the

market has given the Company a low valuation, but we be-

lieve that an increase in the percentage of low-temperature

meat products will become an irreversible trend. There is

still huge room for improvement in the Company’s profitabil-

ity structure in the future.

Main financial indicators 2013A 2014A 2015A 2016E 2017E

Operating income (RMB m) 449.50 456.96 446.97 484.07 523.27

Operating income growth rate 13.21% 1.66% -2.19% 8.30% 8.10%

Net profit (RMB m) 38.58 40.40 42.56 44.56 48.85

Net profit growth rate 33.72% 4.71% 5.34% 4.71% 9.6%

EPS (RMB) (DILUTED) 1.75 1.84 1.29 1.35 1.48

P/E 12.2 11.6 16.6 15.9 14.5

Sources: Company data, China Galaxy Securities Research

Company valuation and investment recommendation

We expected EPS to be RMB1.35 and 1.48 and PER

15x and 13.8x in 2016 and 2017, respectively. We

maintain our “Recommend” rating.

The Company’s valuation is still low, presenting a long-

term value opportunity.

26

Catalyst for share price performance (monthly)

According to a grass roots survey, the acceptance of the

Company’s new American-style product is beyond expec-

tations.

Overall market demand is beyond expectations.

Main risk factors

Slow progress in new product acceptance in the con-

sumer market.

A sharp rise in pork prices.

27

Shandong Chenming Paper Holdings Limited (000488): Excellent leading enterprise

expected to benefit from supply-side reform; two main businesses with satisfactory

performance

Driving factors, key assumptions and main predictions:

1. Financing lease business. This business should see rapid growth. At present, the financing lease balance stands at RMB24bn,

and the balance on average throughout the year will reach RMB30bn. The registered capital of Chenming Holdings Hong Kong Lim-

ited increased to RMB11bn benefiting from a private placement and laying a foundation for continued heavy volume in 2017.

2. Paper-making business. Because of a decrease in raw material costs and an increase in product prices, forestry pulp and paper

integration will be followed by a focus on upstream cost control.

3. Supply-side reform. Enterprises failing to meet standards for production capacity and environmental protection will be closed

down, and this will benefit excellent leading enterprises like Shandong. The concentration ratio of the industry is expected to improve.

Main financial indicators 2014A 2015A 2016E 2017E

Operating income (RMB m) 19,101.68 20,241.91 20,241.91 21,678.00

Operating income growth rate -6.31% 5.97% 7.09% 5.48%

Net profit (RMB m) 505.20 1,021.22 1,977.79 2,648.32

Net profit growth rate -28.91% 115.73% 93.67% 33.90%

EPS (RMB) (DILUTED) 0.26 0.53 1.02 1.37

P/E 32.0 15.7 8.2 6.1

Sources: Company data, China Galaxy Securities Research

How our views differ from the market’s

Investment Rating:

Recommend

Profit. The Company’s profit may be better than mar-

ket expectations in 2016. The profit growth rate is

close to 100%.

Financing lease business. This part of the Compa-

ny’s business remains positive, with a rapidly enlarged

scale, enhanced risk management, and adequate sub-

sequent financing projects. By the end of 2016, the

financing lease balance will exceed RMB30bn, and the

balance on average throughout the year should reach

RMB30bn with profit of RMB1.2bn. The private place-

ment program will lay a foundation for an earnings

increase in 2017.

Industry reform. This will result in the paper-making

business of leading enterprises rising steadily, with

lower costs and higher sales prices. This trend is ex-

pected to continue.

Ma Li :(8610)66568489 [email protected] No. of certificate to practice: S0130511020012

Company valuation and investment recommendations

Investment advice. We expect EPS to be RMB1.02 and

1.37 in 2016 and 2017, respectively. The present price is

RMB8.25. The total equity of RMB1.336bn corresponds to a

market value of nearly RMB16bn. The PER is 8x and 6x. We

maintain our “Recommend” rating.

Valuation. The paper-making business has a valuation

ranging from 10x to 15x PER. As the scale of the financing

lease business gets bigger, it should result in a valuation of

12x PER.

28

Catalyst for share price performance

A number of policies for environmental protection have

been introduced, resulting in more small and medium-

sized paper-making enterprises being closed down.

The performance of the Company’s diversified financial

services is better than expectations.

Raw material prices continue to drop.

Main risk factors

Default risk of financing lease business; slower-than-

expected business expansion.

Risk of a rebound in the price of raw materials and a

drop in product prices.

29

Qingdao Hengshun Zhongsheng Group Co., Ltd. (300208.CH): China replicat-

ing its model to the world at top speed

Driving factors, key assumptions and main predictions:

1. Hengshun Zhongsheng is one of the most successful overseas models of One-Belt, One-Road and has gradually gained market

recognition. Since the Company’s successful planning and construction of an Indonesian industrial park, the Company has developed

a complete industrial park model, including investment, development and operations. Using electric power construction as the core

strategy and the acquisition of local mineral resources as the entry point, the Company invests in the construction of local industrial

parks, including infrastructure construction, establishing a platform, attracting tenants, providing logistics support for industry and

commerce, taxation, accommodation, mineral resources development, adding value to products, and forming an industrial ecology

with mutual benefits for upstream and downstream industries.

2. Constructing the industrial park is driving the rapid growth in new contracts for complete export packages. The Company now has

contracts, including the contracts of intention, worth nearly US$600m. With its continued business expansion, new contracts will be

concluded in 2016. We expect the Company to grow rapidly.

3. The companies in Indonesia Ferro-nickel Industrial Park have started production. The sales revenue from minerals will greatly im-

prove the Company’s resource valuation.

Main financial indicators 2014A 2015A 2016E 2017E

Operating income (RMB m) 670 1,200 1,850 3,100

Operating income growth rate 297% 79% 54% 68%

Net profit (RMB m) 110 315 522 947

Net profit growth rate 188.75% 187.86% 65.69% 81.26%

EPS (RMB) (diluted) 0.15 0.42 0.70 1.26

Sources: Company data, China Galaxy Securities Research

Investment Rating:

Recommend Liu Wenping: (8610) 66568477 liuwenping_yj @chinastock.com.cn No. of certificate to practice

S0130514110003

Company valuation and investment recommendations

We estimate that the net profit attributable to the parent

Company in 2016 and 2017 will be RMB523m and 947m in

2016 and 2017, for a respective growth rate of 54% and

81%. With the Company’s business expansion in South Afri-

ca, Zimbabwe, Thailand, and Laos, it is expected to maintain

rapid growth after 2017. The Company acquired substantial

mineral resources at low prices, including Indonesian nickel,

coal, and manganese, and South African coal, and there

remains huge room to increase its reserves. The Company’s

business model indicates the continued acquisition of high-

quality resources overseas. We maintain our “Recommend”

rating.

How our views differ from the market’s

There is low market recognition of the Company’s

businesses, and there is a considerable difference

in expectations.

The Company’s industrial park model has great po-

tential as a successful business model for the Belt

and Road.

We are confident that the Company’s performance

will improve rapidly.

The value of resources is barely reflected in the

30

Catalyst for share price performance

New purchase orders.

Realization of potential.

Increasing cooperation with Qingdao Urban Construction

Investment Holding (Group) Co., Ltd.

Unlikelihood of the CSRC’s penalizing listed companies.

Main risk factors

What sort of penalty CSRC determines for listed compa-

nies.

Overseas political risks.

31

Henan Pinggao Electric Co., Ltd. (600312.CH): Expedited delivery of ultra -high

voltage products, good potential for charging-pile sales

Driving factors, key assumptions and main predictions:

1. The Company’s UHVAC composite apparatus has maintained a steady leading role, with new orders and deliveries rising sharply.

The Company announced the successful bid for 7 ultra-high voltage GIS intervals for the Ximeng-Shengli Project. At present, the

Company has 45 orders for ultra-high voltage GIS intervals, compared to only 20 confirmed orders in FY2015. Therefore, the 45 or-

ders on hand are already sufficient to guarantee the Company’s rapid profit growth this year. We expect the Company to receive a

large number of orders for the East Junggar-East China DC Line and the Ji’nan-Zaozhuang-Linyi-Weifang AC Line, ensuring growth

for both this year and next.

2. The Company’s base in Tianjin had one production line put into service last year after numerous tests, and the Company has start-

ed its distribution network business and asset integration plan. It is expected that the Tianjin plant will generate revenue of about

RMB1bn this year.

3. The private placement has injected assets in the listed companies. We expect the Company’s profitability to improve in 2016.

4. With the overseas business expansion of Pinggao Group, the Company has received quick, successful international certification of

a large number of products.

5. The Company’s subsidiary Tianjin Pinggao has reported tests on six 30~360kW DC chargers and two 220V and 380V AC charging

piles. It also had successful bids for 89 DC chargers and 106 AC charging piles in Beijing, Xinjiang, etc. Production capacity is in-

creasing. Upon the completion of its automated production line, Tianjin Pinggao will have the capacity to produce 6,000 DC chargers

and 20,000 AC charging piles annually, for potential annual output value of about RMB600m. The Company is listed in the State Grid

system. At present, the five companies (Xuji Group Corporation, Nari Technology Co., Ltd., Beijing Huashang Sanyou New Energy

Technology Co., Ltd., etc.) in the State Grid system enjoy a market share of about 10% each in the State Grid’s annual tenders for

charging piles. We expect the State Grid’s tenders for charging equipment this year to total nearly RMB4bn. If Tianjin Pinggao can get

a 5% market share, it could generate additional revenue of about RMB200m.

Main financial indicators 2014A 2015A 2016E 2017E 2018E

Operating income (RMB m) 4,606 5,831 6,522 7,251 8,342

Operating income growth rate 21 27 12 11 15

Net profit (RMB m) 693 827 978 1,160 1,376

Net profit growth rate 74 19 18 19 19

EPS (RMB) (diluted) 0.61 0.73 0.86 1.02 1.21

P/E 23.3 19.5 16.5 13.9 11.8

Sources: Company data, China Galaxy Securities Research

How our views differ from the market’s

Investment Rating:

Recommend

According to market, the Company benefits mainly from ultra-high voltage AC construction. However, the Company has also

invested and achieved success in DC ultra-high voltage technology, and the Company and its subsidiary Henan Pinggao Toshi-

ba High-Voltage Switchgear Co., Ltd. have successfully bid on tenders for DC field and combined electrical apparatus worth

nearly RMB700m, apart from converter valves and transformers.

Zhang Ling : (8621) 66568643 [email protected] No. of certificate to practice : S013051402000

32

Catalyst for share price performance

The ultra-high voltage project is approved for operation by

the National Energy Administration.

Orders are received for charging piles.

Main risk factors

The number of ultra-high voltage projects approved for

operation is lower than expected.

The Company’s ultra-high voltage products have low

market share and prices drop sharply.

Revenue and profits from the factory in Tianjin are lower

than expected.

Company valuation and investment recommendations

As a leader in the ultra-high voltage GIS industry, the Company benefits from the ultra-high voltage AC and DC construction,

has plenty of orders on hand, and has the capacity to take on more orders. The DC/AC charging piles and low-voltage equip-

ment in its distribution network have created a new growth pole for the Company. We expect the EPS to be RMB0.86, 1.02,

and 1.21 in 2016, 2017 and 2018, respectively, and maintain our “Recommend” rating.

33

ARTS Group Co., Ltd. (603017.CH): Industrial park development service pro-

vider, domestic and international growth potential

Driving factors, key assumptions and main predictions:

1. The Company purchased 100% of ECD’s stock for RMB598m in October 2015. ECD’s original shareholders promised that the after

-tax net profits for 2016 and 2017 would be no less than RMB51m and RMB57m, respectively. The purchase of ECD opens the door

to the market in the southwest. China has finalized the China-Singapore (Chongqing) Strategic Interconnectivity Demonstration Pro-

ject with Singapore. Based on this purchase and the Company’s excellent performance in industrial park design and construction, it is

expected to realize a great leap forward in development.

2. With the Company’s experience in the construction of Suzhou Industrial Park, it has established a unique competitive niche in park

planning and design. It signed a contract valued at RMB358m for the construction of China-Malaysia Qinzhou Industrial Park and a

Strategic Cooperation Agreement on the Jining Economic and Technological Development Zone. The Company’s capability in park

design is fully recognized. In the future, its design is expected to be copied on a national scale, indicating huge potential to receive

more orders for design and planning.

3. The Company has proposed a capital increase of RMB12m in Chongqing Lufugong Image Digital Technology for equity of no more

than 20%. The target company was one of the earliest enterprises in the VR architectural design field. The Company will apply the VR

technology to create innovative designs on the traditional pattern. This will greatly promote the Company’s design business.

4. In July 2015, the Company issued 2.34m restricted shares to 91 directors, middle and senior administrative personnel, and key

staff at RMB18.96/share, totalling RMB44.3664m. The stock ownership incentive will help retain talent and guarantee the Company’s

future development.

Main financial indicators 2014A 2015A 2016E 2017E 2018E

Operating income (RMB m) 540 636 859 1,074 1,288

Operating income growth rate 13.9 17.9 35.0 25.0 20.0

Net profit (RMB m) 91.4 67.7 127.2 160.6 192.2

Net profit growth rate 7.5 -26.0 88.0 26.3 19.6

EPS (RMB) (diluted) 0.75 0.55 1.04 1.31 1.57

P/E 44.6 60.8 32.2 25.5 21.3

Sources: Company data, China Galaxy Securities Research

How our views differ from the market’s

Investment Rating:

Recommend

In 2015, without considering the cost of the stock ownership

incentive plan, the Company had revenue growth of 17.88%

and net profit growth of 5.12%. In view of the effect of acquisi-

tions on consolidated statement, the Company’s performance is

expected to rise sharply.

The purchase of ECD opens the door to the market in the

southwest. China has finalized the China-Singapore

(Chongqing) Strategic Interconnectivity Demonstration Project

with Singapore. The Company is expected to realize a great

leap forward in its development.

The Company is extremely skilful in park design. Its designs are

expected to be copied on a national scale, indicating huge po-

tential to receive more orders for park design.

Zhou Song:(8621) 68956786 zhousong [email protected] No. of certificate to practice : S0130515050001

Company valuation and investment recommendations

We expect EPS of RMB1.04 and 1.31 and PE of 32x

and 25x in 2016 and 2017, respectively, and maintain

our “Recommend” rating.

Valuation: The Company’s valuation is low compared

to that of its peers. Given the Company’s potential

profit upside, we believe that a valuation premium is

reasonable. In 2017, a reasonable valuation range will

be 35x PER, corresponding to a price of RMB45.

34

Catalyst for share price performance

The private placement is completed as expected and the

external-oriented acquisition is implemented step by step.

The framework agreement is signed with Lufugong Image

Digital Technology to develop new VR business.

Main risk factors

Macroeconomic risks.

Asset-restructuring risks.

35

DMEGC (002056.CH): Driven by growth and cyclical factors, concurrent develop-

ment of magnetic materials and new energy

Driving factors, key assumptions and main predictions:

1) In the short run, no other technologies can replace the application of ferrite in shielding materials.

2) In 2014-2015, the solar cell industry underwent a fierce reshuffle, but it began to rebound in 2015. It is expected that the boom

will continue for the coming 1-2 years.

3) DMEGC’s position in the photovoltaic and power battery business has favourable prospects. Meanwhile, its magnetic material

business is increasing steadily. We expect EPS to be RMB1.02, 1.29, and 1.61 in 2016, 2017 and 2018, respectively, corre-

sponding to 25 times the valuation in 2016. We rate it “Recommend”.

Main financial indicators 2015A 2016E 2017E 2018E

Operating income (RMB million) 3,958 5,015 6,246 7,531

Growth rate of operating revenue 7.9% 26.7% 24.5% 20.6%

Net profit (RMB million) 323 418 530 661

Net profit growth rate -15.2% 29.2% 26.8% 24.9%

EPS (RMB) (DILUTED) 0.79 1.02 1.29 1.61

P/E 14.8 17.4 13.5 10.7

Sources: Company data, China Galaxy Securities Research

Investment Rating:

Recommend Wang Li :(8610) 83574039