a strategy for materials - matuk.co.uk · a strategy for materials materials innovation and ......

TRANSCRIPT

A STRATEGY FOR MATERIALS

Materials Innovation and Growth Team

Printed in the UK on recycled paper with a minimum HMSO score of 75.First published March 2006. Department of Trade and Industry.

www.dti.gov.uk URN 06/651

Forewords 2

Chairman’s introduction 3

Executive summary 5

Action matrix 6

The way forward 7

The Innovation and Growth Team 10

Materials and their importance 11

How the UK measures up 13

Drivers of change 16

Challenges for the future 19Energy 19Raw materials 20Sustainable development 22Health 23Security and defence 24Construction and the built environment 25Transport 25Information and communication 25Sensors and diagnostics 26Further opportunities 27

The environment for research and innovation 28

Priorities for the UK 30Knowledge transfer 31Raising awareness 33Accelerating innovation 35Improving skills and knowledge 37Better business environment 39

Annex 1 Representive body: Materials UK 41

Annex 2 Materials UK:Key Performance Indicators 44

Annex 3: IGT’s methodology 48

1

Contents

Supporting this report of the MaterialsIGT’s findings, we have reproduced onthe attached CD the record of variousworkshops held to inform the work and aseries of working papers written by theTask Groups covering:

• Science & Technology.

• Policy & Impact.

• Assets & Infrastructure.

• Best Practice.

• People & Skills.

• Economic Analysis.

• International comparisons.

Foreword by the Prime Minister

I must congratulate the materialsindustry for coming together to formthis Innovation and Growth Team andproviding this excellent report.

I am delighted the whole materialscommunity, industry, academiacustomers and other stakeholders, aredetermined to continue to driveforward together to deliver a strategythat will enable Britain to continue tobenefit from being one of the foremostadvanced technological societies inwhich world class materials expertiseunderpins sustainable growth.

I wish them and the body they are forming, Materials UK, everysuccess as they strive to deliver thechallenging but very necessary agendathey are proposing.

The Rt. Hon.Tony Blair Prime Minister

Foreword by theSecretary of State

Materials are important to everydaylife. It seems eminently sensible thatBritain seeks to ensure it optimisesthe wealth creation opportunitiesmaterials production, processing, use,recycling and re-use provide. However,tough challenges lie ahead, the globaleconomy is highly competitive. Whilewe still retain some excellence intraditional materials, it is essential wecontinue to evolve this and develop ourexpertise in the newer emergingmaterials such as composites andsmart materials utilising ouracknowledged world class academicexpertise in materials and othertechnology such as nano and bio-technology. The strategy produced byWyn and his team should help us dothis. I wish them well as they moveinto the implementation phase andhope that Materials UK does indeedbecome the driving force forcontinuing success in Materials.

The Rt. Hon. Alan Johnson MP

32

Forewords

The UK has a long establishedreputation for excellence in materialsscience, research and development.Companies in the UK excel in thedevelopment and use of materials in engineering and constructionalsteels, float glass, aerospace andautomotive. They also excel in bio-pharmaceutical manufacturing.

The consumption of materials, directly orin manufactured products, is growing inthe UK as it is globally. In emergingeconomies people aspire to thefundamentals of modern life includinggood health and nutrition. In advancedcountries people show little sign ofabating their desire for improved lifestyles and this is politically difficult tochange. New technologies, such ascommunications, create new demandsfor materials and developments inmaterials. This growth in the use ofmaterials - and acceptance of thechallenges posed by health, climatechange, energy supply and the quest forsustainability - place pressures to usematerials differently and more wisely.Innovation has to bridge the conflictbetween satisfying the global demandsof societies and what is sustainable.

Sophisticated societies employregulation to bridge any gaps betweenthe desirable and undesired effect ofhuman endeavour. Not all countries havethe same regulatory framework, forexample on environment and energy

Chairmans introduction by Wyn Jones, OBE, Chairman Materials IGT

matters. Regulatory interfaces tend to belarger for materials than for otherindustries and can be more complex. Itis therefore important that regulation isintelligent and focused on the intendedoutcomes rather than prescriptive on themethods of achieving them. Thematerials community believes the focuson sustainability is rightly growing butthe recycling infrastructure in the UK andits regulatory regime needs to change topromote the avoidance of, collection,segregation, and reuse, of waste.

The “Materials Industry” has largelybeen defined intuitively. Metrics are notreadily available and the community,although containing significant skills, isfragmented and disparate. Because ofthis my team deployed a wide focus onsupply chain issues rather thanselecting a group of materials. Bylooking at the supply chains andinfrastructure, we have identified waysin which the UK can continue toprosper from materials manufacturingby improving knowledge transfer andinnovation. There is significant scopefor sharing information and addressingcommon barriers.

Decisions on manufacturing, design andengineering are often taken outside theUK. By improving the UK infrastructureand networks, in the widest sense,sound decision making will beaccelerated making the UK a betterchoice for multinationals to continue toinvest. Also, public procurement willbenefit from improved coordination inpromoting and delivering sustainablesupply chains.

From the viewpoint of skills,“materials” has an undeservedly dullimage in the UK that pays little regardto the highly innovative worlds ofnanotechnology and miniaturisation, or

5

to the huge progress in “traditional”materials. The absence of a goodimage hinders recruitment and this inturn leads to insufficient skills at boththe technical and research levels.

Many issues, such as better regulationand the need to improve sustainability,affect all materials. Skills and educationare also common issues, as is image.Many of the challenges facing societywill rely on multi-material solutions. Thereis a need for a clear interface betweenthe major forces driving industry and thesupply chains affecting materials.

By working in an industry-ledcooperation across supply chains thematerials community can address thecommon themes uncovered in our yearlong investigation. We are formingMaterials UK, an industry-led body witha clear purpose and well definedmeasures of success. The new bodywill build on what has gone before. Inbroad terms it will improve theefficiency of communication, accelerateinnovation and the transfer ofknowledge, and help to reduce

4

Secretariat Team

DTI: Gerry Miles, RobertQuarshie, Julian Thompson, Nick Morgan/Jan Weston,Sagitta Fernando/Narinder Kaur

IoM3: Jackie Butterfield

The secretariat would like toacknowledge the help given by Michael Kenward to writethis report.

Chair:Wyn Jones, Alcan

Vice Chair:Steve Garwood, Rolls Royce*

Task Group Chairs:David Pulling, GKNDuncan Pell, CorusJack Brettle, PilkingtonBob John, TWIEbby Shahidi, ACGBernie Bulkin, SD CommissionBernie Rickinson, IoM3Graham Davies, Birmingham UniversityDavid Bott, Consultant*Jason Wiggins, SEEDAJohn Wood, CCLRC

Advisory Group:Martin Temple, EEFJohn Wand, EPSRCDerek Allen, AlstomUlf Linder, SiemensMichael Walsh, Community

Peter Arnold, Smith & NephewAlan Begg, Automotive AcademyJohn Alty/Simon Edmonds, DTIAnne Glover, AmadeusCameron Harvie, HeathcoateJon Heffernan, Sharp Electronics*Chris Leach, MODTerence Ilot, DEFRACaroline Barr, TreasuryKamal Hossain, NPLMindy Wilson, CBI* Served on another IGT

There were also valuablecontributions from: -Richard Jones, MODScott MacDonald, CorusDavid Farrar, Smith & NephewIan Rodgers, EEFBernie Walsh, DEFRAGordon McColvin, SiemensGraham Sims, NPLMichael Ankers, CPA

The Materials Innovation & Growth Team

regulatory and financial risk. Its aim isto resolve the multinational dilemma bymaking the UK the best place in whichto do business involving materials.

We have welcomed the involvement ofcustomers and specifiers in our taskgroups, as well as representation frommanufacturers, academics andrepresentative organisations. We arealso grateful for the significant interestfrom Government Departments.

I thank my colleagues from industry,academia and many government bodiesfor their support of this IGT. It has beena major enterprise and the enthusiasmand tremendous commitment shownconvinces me that the materialsindustry in the UK has found a way toaddress itself to a challenging world. Ialso pay tribute to the foundations ofinstitutions and analysis on which wehave built and thank those who tookpart in creating them. They will all beimportant players in the new body.

Society cannot exist without materials.They underpin everything we do andaffect most areas of economic activity.Manufacturing and construction areentirely dependent on materials inmany different forms.

Material businesses in the UK,companies that produce and processmaterials, have an annual turnover ofaround £200 billion. They make amajor direct contribution to theeconomy at 15% of the country’s GDP,while also underpinning all areas ofeconomic activity. The diversity of thematerials community has previouslymade it difficult to achieve a collectivevision and to respond with a coherentstrategy to the major challenges of theday, globalisation, sustainability and theenvironment. To address these issues,the Materials Innovation and GrowthTeam (Materials IGT) has looked forwardto define the challenges facing thosewho develop, make and use materials.

The vision of the Materials IGT is thatthe UK will continue to be one of theforemost advanced technologicalsocieties in which world-class materialsexpertise underpins sustainable growth.

We have identified the key issues torealise this vision as:

• Resources - uncertainties in theavailability of energy and rawmaterials due to the depletion of,and growing competition for, globalreserves, limitation of supplies andavailability of strategic materials.

• Globalisation - threat from low-costmanufacturing in emerging countriesand opportunities in emerging markets

• Sustainability - energy efficiency,the low-carbon economy, recyclingreuse and ‘ecodesign’.

• Innovation - making best use of theR&D base, bringing more valueadded products to the market, fasterthan the competition, enhancingexisting materials through design.

To meet these challenges, we propose specific actions under fivebroad headings:

• Knowledge transfer - through, forexample, signposting services, accessto materials education and databasesof job vacancies, best practice tools,technology roadmaps and thetechniques of life-cycle analysis.

• Raise awareness - alert youngpeople and the public to theimportance of materials throughpromotion in schools, workexperience and collaboration withRegional Development Agencies.

• Accelerate innovation - better useof assets, implementation of R&Dpriorities and effective supportmechanisms throughout theinnovation cycle, and through betterinteraction of materials with design.

• Improve skills and knowledge -promote best practice, thedevelopment of specialist coursesand international partnerships.

• Build a better business environment

- improve materials innovation in theUK through better regulation, enhancedsupply chains and public procurement.

To take forward these actions, and to unite the materials communityunder a common vision, we areestablishing Materials UK, a body thatwill act as an umbrella for the existingorganisations within the broadermaterials sector. Building on thesuccess of Materials KnowledgeTransfer Network (KTN), Materials UKwould provide the leadership requiredto meet the challenges.

Executive summary

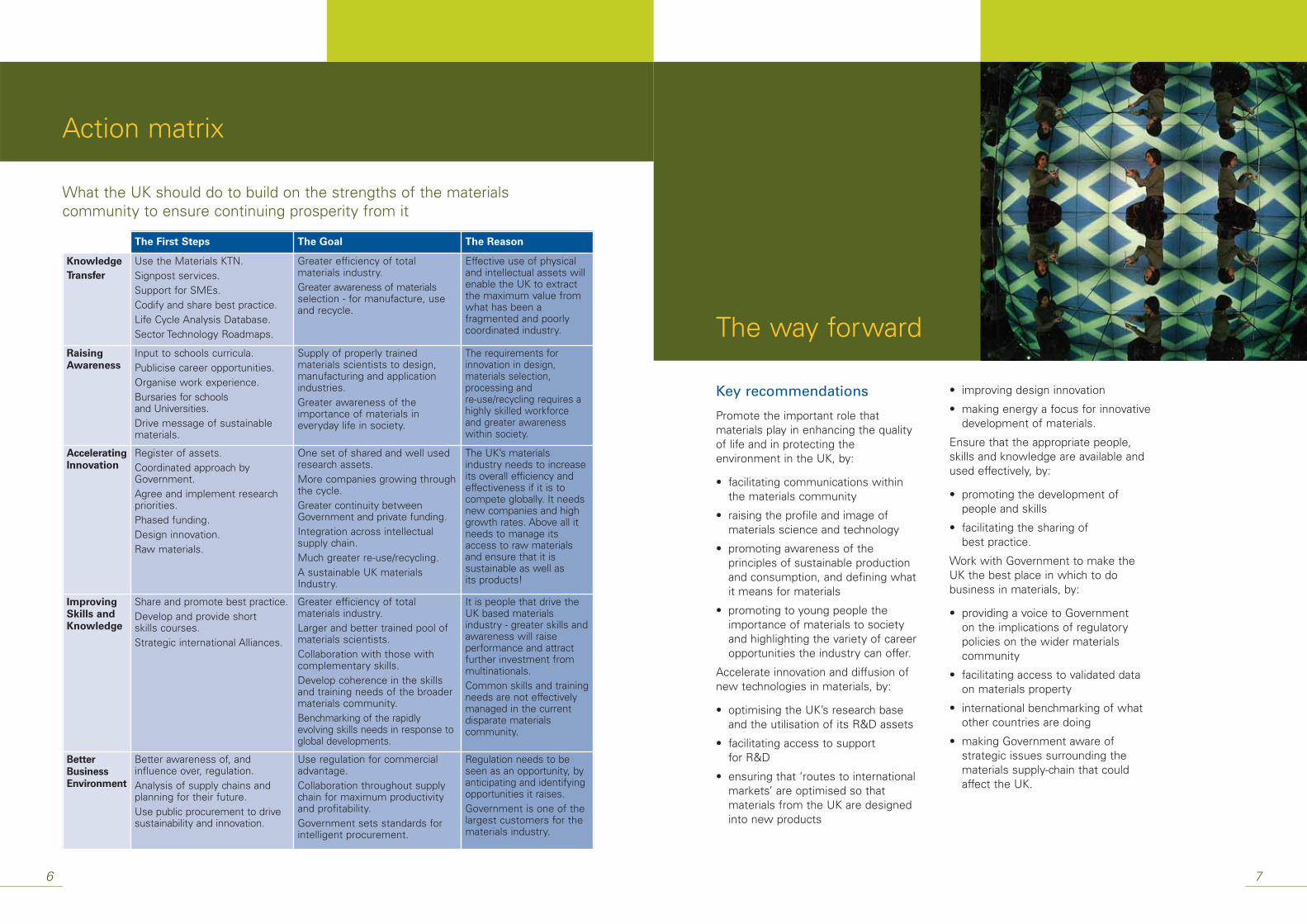

What the UK should do to build on the strengths of the materialscommunity to ensure continuing prosperity from it

76

The First Steps The Goal The Reason

Knowledge

Transfer

Use the Materials KTN.Signpost services.Support for SMEs.Codify and share best practice.Life Cycle Analysis Database.Sector Technology Roadmaps.

Greater efficiency of totalmaterials industry.Greater awareness of materialsselection - for manufacture, useand recycle.

Effective use of physicaland intellectual assets willenable the UK to extractthe maximum value fromwhat has been afragmented and poorlycoordinated industry.

Raising

Awareness

Input to schools curricula.Publicise career opportunities.Organise work experience.Bursaries for schools and Universities.Drive message of sustainablematerials.

Supply of properly trainedmaterials scientists to design,manufacturing and applicationindustries.Greater awareness of theimportance of materials ineveryday life in society.

The requirements forinnovation in design,materials selection,processing and re-use/recycling requires ahighly skilled workforce and greater awarenesswithin society.

Accelerating

Innovation

Register of assets.Coordinated approach byGovernment.Agree and implement researchpriorities.Phased funding.Design innovation.Raw materials.

One set of shared and well usedresearch assets.More companies growing throughthe cycle.Greater continuity betweenGovernment and private funding.Integration across intellectualsupply chain.Much greater re-use/recycling.A sustainable UK materialsIndustry.

The UK’s materialsindustry needs to increaseits overall efficiency andeffectiveness if it is tocompete globally. It needsnew companies and highgrowth rates. Above all itneeds to manage itsaccess to raw materialsand ensure that it issustainable as well as its products!

Improving

Skills and

Knowledge

Share and promote best practice.Develop and provide short skills courses.Strategic international Alliances.

Greater efficiency of totalmaterials industry.Larger and better trained pool ofmaterials scientists.Collaboration with those withcomplementary skills.Develop coherence in the skillsand training needs of the broadermaterials community. Benchmarking of the rapidlyevolving skills needs in response toglobal developments.

It is people that drive theUK based materialsindustry - greater skills andawareness will raiseperformance and attractfurther investment frommultinationals.Common skills and trainingneeds are not effectivelymanaged in the currentdisparate materialscommunity.

Better

Business

Environment

Better awareness of, andinfluence over, regulation.Analysis of supply chains andplanning for their future.Use public procurement to drivesustainability and innovation.

Use regulation for commercialadvantage.Collaboration throughout supplychain for maximum productivityand profitability.Government sets standards forintelligent procurement.

Regulation needs to beseen as an opportunity, byanticipating and identifyingopportunities it raises.Government is one of thelargest customers for thematerials industry.

Action matrix

The way forward

Key recommendations

Promote the important role thatmaterials play in enhancing the qualityof life and in protecting theenvironment in the UK, by:

• facilitating communications withinthe materials community

• raising the profile and image ofmaterials science and technology

• promoting awareness of theprinciples of sustainable productionand consumption, and defining whatit means for materials

• promoting to young people theimportance of materials to societyand highlighting the variety of careeropportunities the industry can offer.

Accelerate innovation and diffusion ofnew technologies in materials, by:

• optimising the UK’s research baseand the utilisation of its R&D assets

• facilitating access to support for R&D

• ensuring that ‘routes to internationalmarkets’ are optimised so thatmaterials from the UK are designedinto new products

• improving design innovation

• making energy a focus for innovativedevelopment of materials.

Ensure that the appropriate people,skills and knowledge are available andused effectively, by:

• promoting the development ofpeople and skills

• facilitating the sharing of best practice.

Work with Government to make theUK the best place in which to dobusiness in materials, by:

• providing a voice to Government on the implications of regulatorypolicies on the wider materialscommunity

• facilitating access to validated dataon materials property

• international benchmarking of whatother countries are doing

• making Government aware ofstrategic issues surrounding thematerials supply-chain that couldaffect the UK.

Materials UK (MatUK)1

Many of our recommendations requireclose and continued collaborationbetween the research community,professional institutions, businessesand Government. This will not happenwithout strong and sustainedleadership. Such is the nature of thematerials community that no singlebody can presently provide thisleadership and bring together all of theinterested parties.

A representative body, Materials UK(MatUK), is being established to takeforward this strategy and to build onthe momentum created by theMaterials IGT.

The intention is not that this body willdisplace existing bodies that representthe numerous sections of thematerials community, many of whichwere involved in the Materials IGT, butthat the new body will bring themtogether in a structure that will enablethem all to continue to function asthey wish in their own key areas.MatUK will build on the best practiceor expertise of each organisation andwill add value to their activities byworking with them to address majorissues of common concern. MatUKwill have a strong focus on supplychain issues and be seeking to identifyclear wins for the UK.

Creating an umbrella organisation forthe wider community of materialsbodies will make it easier for thecommunity to engage at an earlystage in policy development throughresponding to formal consultations.Collectively, the community shouldalso find it easier to gather intelligenceon, and respond to, internationalinitiatives such as the OECD’s work onsustainable materials management orhow to optimise the opportunities forUK firms in delivery of the Olympics in 2012.

MatUK will seek out opportunitieswhere the materials communityworking together can seize global

advantage for the benefit ofcompanies operating in the UK byensuring the recommendations ofthe Materials IGT are taken forward.

A detailed structure for MatUK is setout in Annex 1.

Vision

The vision of the Materials IGT, and forthe future of MatUK, is that the UK willcontinue to be one of the foremostadvanced technological societies inwhich world-class materials expertiseunderpins sustainable growth.

Mission

The mission of MatUK is to enable theUK to pursue and benefit fromopportunities for materials in the globaleconomy, through:

• Leadership

• Strategic guidance and direction

• Engaging stakeholders

• Working with Government to make UK the best place in which todo business

• Recognising the importance ofmaterials to society’s needs.

Aims and objectives

MatUK will enlist broad representationfrom the materials community,working with such bodies as tradeassociations, learned societies (e.g.IoM32), the Foresight Materials Panel,Defence and Aerospace NationalAdvisory Committees, for example.

Working with that broader community, MatUK will continue thework of the Materials IGT to deliverstrategies for essential activities suchas the optimisation of the UK’s R&Dbase, provision of a validated database of materials property fordesigners, producers and users, andknowledge transfer to support thedevelopment of materials,manufacturing and new applications.

981 Information of how to engage with MatUK is available on www.MatUK.co.uk 2 IoM3 is the Institute of Materials, Minerals and Mining

With the support of the new body, the UK’s materials community will bein a position to respond to newopportunities and challenges and tomobilise high-powered teams quicklyto review key issues and identifyopportunities for global leads for the UK.

MatUK will allow the materialscommunity to provide a coherent viewon common policy, regulation andfunding strategies to government. Inthis way the umbrella body will addstrength and persuasiveness to theactivities of the organisations that nowrepresent individual sectors.

The new body will seek to influencethe regional materials strategies of theRDAs, devolved administrations andmajor funding bodies such as ResearchCouncils, Ministry of Defence, Healthand Safety Executive, Department ofHealth, Department for Transport andothers so that UK resources forinnovations in materials are optimised.

MatUK will seek to create a climate inwhich the UK is considered to be agood place to carry out materialsrelated business, including worldleading design, R&D and educationand training.

As delivery mechanisms MatUK shouldtake ownership of the MaterialsKnowledge Transfer Network (KTN) andpromote and sustain the newMaterials Assets Connect andMaterials Property Validation facilities.It will deliver its mandate following thekey performance indicators that wehave developed in consultation withthe community (see Annex 2).

Figure 8

Activities defining the materials community

The IGT’s definition of the Materials Community includes the full cycle of value-adding activities:• Research, design and development.• Raw materials, primary production.• Processing and fabrication.• Standards, testing and end of life management.

Raw materials

Primary production

Processing Fabrication After sales services

R & D design

Materials user

Primary activity

Supporting activity

Education & training

Standards and testing

Logistics Recycling

The Materials IGT began its formalwork in January 2005. The purposewas to propose a strategy to optimisethe benefits that materials technologycan bring to the UK. In particular, theterms of reference were:

• Look ahead at 5, 10 and 20-yearhorizons and define what the keymaterials requirements will be and how these compare withcurrent materials.

• Look at likely future Governmentpolicy approaches – for example, toenvironmental challenges – and howthe industry can respond.

• Consider what constitutes bestpractice in all aspects of thebusiness process, including R&D,knowledge transfer, design, efficientuse of resources, wasteminimisation and recovery/recycling,and investigate how it could bepromulgated in the UK.

11

Recognising the importance of materials against a background of climatechange, energy pressures, resource needs and increasing globalcompetitiveness – and the need to assess the implications of these factorsfor the UK materials sectors – the Secretary of State for Trade and Industryapproved the creation of the Materials Innovation and Growth Team(Materials IGT) in October 2004.

• Consider the policy implications forGovernment, and address theeffects that current and futurenational and European legislation –on emissions, recycling, sustainableproduction, for example – mighthave on the materials sector.

The Materials IGT’s methodology3

involved establishing Task Groups toengage all interested stakeholdersthrough a series of workshops,meetings and interaction electronicallythrough a website4. In addition, therewas specific activity on materials inenergy, construction, sustainableproduction and consumption, thecontribution of minerals and theacademic community as well as someformal stakeholder surveys. In all,some 650 companies, organisations5 orindividuals contributed to the work ofthe Materials IGT and its Task Groups.

10

The Innovation andGrowth Team

3 Methodology used by the Materials IGT outlined in Annex 34 www.amf.uk.com5 see CD and website for complete list

Materials underpin everything we do. Manufacturing and construction areentirely dependent on materials in some form. Materials technology affectsmost economic activities. The quickening revolution in information andcommunications technologies would not be possible without a wealth ofnovel functional materials.

opportunities from materialsproduction, processing, fabrication,use and recycling. Increased activity in processing and fabrication shouldmore than match any decline inprimary production. In this way, theUK can create increasing value for the economy, including significantexport opportunities.

Materials and their importance

As the report of the Economic AnalysisTask Group6 shows, the materialssector is a major contributor to theUK’s economy (Figure 1) and has ahigher productivity than the nationalaverage (Figure 2).

The nature of the materials sector is such that it is difficult to analyse the economic activities of particularareas in any detail, however, we doknow that with activities that rangefrom processing raw materials through to recycling, the sector has a turnover of around £200 billion,contributing at least 15% of the GDPof the UK. It employs some 1.5 millionpeople and supports around 4 millionmore jobs.

The economic goal

The UK will always be a major user ofmaterials, so it is essential that weoptimise the wealth creation

Turnover & GVA of UK materials

300

250

200

150

100

50

0

Valu

e (£

bill

ion

)

Year End

Turnover of UK materials

GVA

1999 2000 2001 2002 2003

Figure 1

6 Report of the Economic Analysis Task Group can be found in attached CD

1312

Labour productivity: Gross Value-added (GVA) per

employee in UK Materials

60

50

40

30

20

10

0

GV

A p

er E

mp

loye

e(£

,000

)

Year End

National average

GVA per employee

1999 2000 2001 2002 2003

Figure 2

CASE STUDY

Minimizinggreenhouse gaseswith monolithicactivated carbons

Based on its advanced monolithic activated Carbons, ‘MAST’ has developed a uniqueenvironmental solvent vapour recovery system from polymer-derived Carbons.

With less than 0.1% of the environmental emissions of conventional thermaloxidation systems, MAST’s system minimizes solvent vapours that are a majorcontributor to greenhouse gases arising from biomedical, catalytic and energystorage applications.

MAST Carbon http://www.mastcarbon.com/

Dimension of diameter is nominal 20mm.

How the UKmeasures up

Any analysis of the challenges facing the materials sector in the UK has to build on an understanding of the strengths and weaknesses of thematerials community.

area, if it wants to match the bestperformance of its competitors andmaintain or increase its contributionto GDP.

The contribution that the materialssector makes to the economy is oneobvious strength Figure 3 showsturnover by value chain, Figure 4 atypical export profile. For 2003 totalexports were £50bn.

The UK is the home of a number ofworld class manufacturing companieswhose success depends on theirdevelopment and use of advancedmaterials. The country also has anactive world-class research community.The business environment is such thatthe UK is a favoured nation for inwardinvestment, and is ahead of somecountries in providing venture capitaland other forms of investment.

While we have already highlighted thefact the materials sector in the UKhas higher productivity than someother areas of manufacturing, noindustry can ever call a halt toattempts to improve its productivity.The materials community certainlyneeds to continue to improve on thisfront, particularly in the fabrication

Breakdown of turnover by value chain activity

for UK materials

300000

250000

200000

150000

100000

50000

0

Turn

over

(£m

)

Year End

Recycling

Fabrication

Processing

Primary Production

Raw Materials: Non-Energy

Raw Materials: Energy

1999 2000 2001 2002 2003

Figure 3

Figure 5

SWOT analysis of UK materials

1514

UK Strengths Weaknesses

UK has a stable economy with low inflation

Long established academic reputation

World class engineering/construction steels, floatglass, aerospace, automotive and biopharmaceuticalmanufacturing

World class and well respected designers

Excellence in low volume, niche production

Attractive location for inward investment

Financial centre facilitating raising of capital

Disparate Community

Decision making is often taken outside UK formanufacturing, design and engineering

Investment levels not high

Recycling infrastructure is far behind establishedcollection segregation and re-use schemes in EU

Productivity and capacity issues

Status (image) of materials and manufacturing

Uncoordinated public procurement

Opportunities Threats

Make greater use of bilateral International joint co-operation agreements

Decisive energy policy: for materials, the re-growth ofnuclear power is also an opportunity

UK to become an international hub for research anddesign in materials

Build upon low volume, high niche manufacturing

Develop or import the right skills

Enhance/address the image of Manufacturing

Low-cost economies getting smarter

Access to raw materials

Transport infrastructure

Strong national strategies for materials research andexploitation by rival countries

Lack of engineering and technician skills

Decision making/influences outside UK

Lack of adequate recycling infrastructure is becominga burden to business

Strong national facilities, e.g. Japan, Singapore, Germany

Exports by UK Material in 2003

Raw Materials: Non-Energy

Primary Production

Processing

Fabrication

Figure 4 The Materials IGT and its Task Groupshave analysed those strengths andweaknesses (Figure 5). We addressthe most important issues that arisefrom this analysis in the followingsections, including Drivers of Changeand Challenges for the Future.

Materials community

A possible weakness of the materialscommunity, in perception at least, isthat it covers the whole landscape,unlike many other sectors ofmanufacturing, which supply a specificmarket or inhabit a particulartechnological niche.

While manufacturers of electronicchips can drive the development ofelectronic materials, and makers ofaircraft engines can push forward thefrontiers for materials for gas turbines,in many areas of materials technologythe connection between the materialmanufacturer and the end user is less clear.

Traditionally, the materials communityhas organised itself along materialgroupings, for example, minerals,

Low emissivity glass looks just the same as ordinary glass but a transparentcoating on its surface “reflects” heat back into a room while allowing heat fromthe external environment into the room.

About half of our total Carbon dioxide emissions in the UK are attributable tobuildings, more than twice that from cars. However we are progressivelyreplacing glazing with low emissivity double glazing: Pilkington ‘K’. That will saveover 9 million tonnes of CO2 emissions annually, which is enough energy to heatsix cities the size of Birmingham.

Cutting carbondioxide emissions

CASE STUDY

steel, non-ferrous metals, polymers,plastics, ceramics, glass, wood,concrete and so on. Yet these sectorsshare many issues. For example, theyare all influenced by globalisation,climate change, trade liberalisation,and the challenge of an everdeveloping world.

This breadth of the materialscommunity has implications both forthe way in which it comes together todiscuss common issues and for theway in which it communicates withother groups.

The diffuse nature of materialsrequires action to bring together thevarious players. It is for this reasonthat we believe that the UK shouldcreate an umbrella organisation thatcan act as a voice for materials.

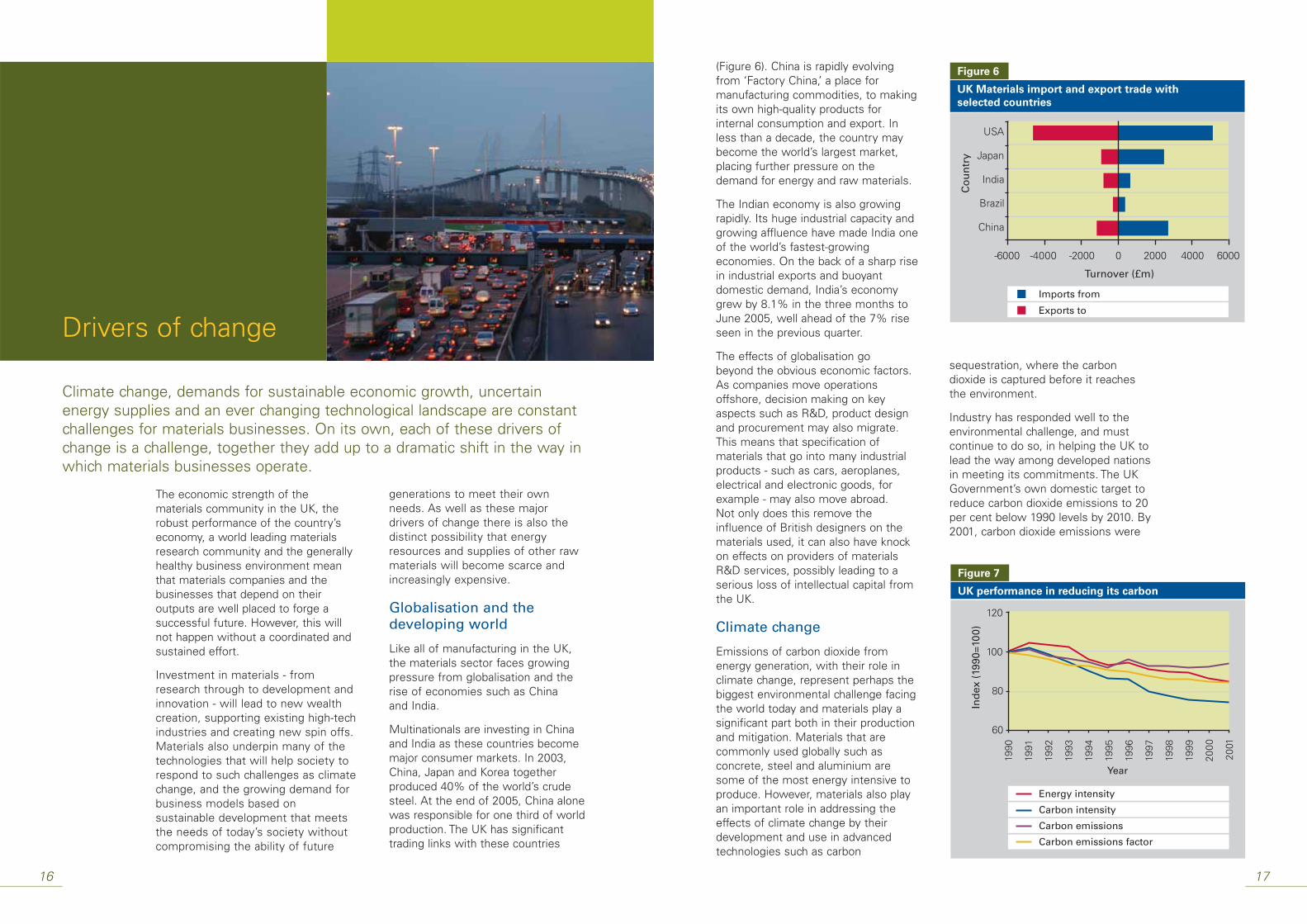

(Figure 6). China is rapidly evolvingfrom ‘Factory China,’ a place formanufacturing commodities, to makingits own high-quality products forinternal consumption and export. Inless than a decade, the country maybecome the world’s largest market,placing further pressure on thedemand for energy and raw materials.

The Indian economy is also growingrapidly. Its huge industrial capacity andgrowing affluence have made India oneof the world’s fastest-growingeconomies. On the back of a sharp risein industrial exports and buoyantdomestic demand, India’s economygrew by 8.1% in the three months toJune 2005, well ahead of the 7% riseseen in the previous quarter.

The effects of globalisation go beyond the obvious economic factors.As companies move operationsoffshore, decision making on keyaspects such as R&D, product designand procurement may also migrate.This means that specification ofmaterials that go into many industrialproducts - such as cars, aeroplanes,electrical and electronic goods, forexample - may also move abroad. Not only does this remove theinfluence of British designers on thematerials used, it can also have knockon effects on providers of materialsR&D services, possibly leading to aserious loss of intellectual capital fromthe UK.

Climate change

Emissions of carbon dioxide from energy generation, with their role inclimate change, represent perhaps thebiggest environmental challenge facingthe world today and materials play asignificant part both in their productionand mitigation. Materials that arecommonly used globally such asconcrete, steel and aluminium aresome of the most energy intensive toproduce. However, materials also playan important role in addressing theeffects of climate change by theirdevelopment and use in advancedtechnologies such as carbon

sequestration, where the carbondioxide is captured before it reachesthe environment.

Industry has responded well to theenvironmental challenge, and mustcontinue to do so, in helping the UK tolead the way among developed nationsin meeting its commitments. The UKGovernment’s own domestic target toreduce carbon dioxide emissions to 20per cent below 1990 levels by 2010. By2001, carbon dioxide emissions were

Climate change, demands for sustainable economic growth, uncertainenergy supplies and an ever changing technological landscape are constantchallenges for materials businesses. On its own, each of these drivers ofchange is a challenge, together they add up to a dramatic shift in the way inwhich materials businesses operate.

generations to meet their own needs. As well as these major drivers of change there is also thedistinct possibility that energyresources and supplies of other rawmaterials will become scarce andincreasingly expensive.

Globalisation and thedeveloping world

Like all of manufacturing in the UK,the materials sector faces growingpressure from globalisation and therise of economies such as China and India.

Multinationals are investing in Chinaand India as these countries becomemajor consumer markets. In 2003,China, Japan and Korea togetherproduced 40% of the world’s crudesteel. At the end of 2005, China alonewas responsible for one third of worldproduction. The UK has significanttrading links with these countries

1716

Drivers of change

The economic strength of thematerials community in the UK, therobust performance of the country’seconomy, a world leading materialsresearch community and the generallyhealthy business environment meanthat materials companies and thebusinesses that depend on theiroutputs are well placed to forge asuccessful future. However, this willnot happen without a coordinated andsustained effort.

Investment in materials - fromresearch through to development andinnovation - will lead to new wealthcreation, supporting existing high-techindustries and creating new spin offs.Materials also underpin many of thetechnologies that will help society torespond to such challenges as climatechange, and the growing demand forbusiness models based onsustainable development that meetsthe needs of today’s society withoutcompromising the ability of future

UK Materials import and export trade with

selected countries

USA

Japan

India

Brazil

China

Turnover (£m)

Co

un

try

Imports from

Exports to

-6000 -4000 -2000 0 2000 4000 6000

Figure 6

UK performance in reducing its carbon

Year

Energy intensity

Carbon intensity

Carbon emissions

Carbon emissions factor

Figure 7

Ind

ex (

1990

=100

)

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

120

100

80

60

estimated to be 6 per cent below 1990levels (Figure 7). This places significantchallenges on the materials sector interms of energy production,conservation and usage.

Energy

The world has experienced fuel crisesin the past, along with forecasts ofdeclining production, only to see thesedisappear. However, risingconsumption and the rapid increase indemand in industrialising nations,combined with political instability incertain parts of the world, add to theconcern over the future availability andsecurity of energy supply.

To tackle this, the UK will require abalanced energy portfolio to minimiseboth the environmental impact and therisks to security of supply. As such,materials technology will play a keyrole in the development of advancedgeneration technologies, which willlikely comprise a mix of fossil, nuclearand renewable energy sources.

Equally, materials have an importantpart to play in the more efficient use ofenergy. Improved insulating materialsand lightweight alloys and compositescan lead to big reductions in theenergy that is used by the buildings,products and services that we all needto sustain our way of life.

Raw materials

Energy is but one of many ‘rawmaterials’ that we depend on forcontinued economic growth. Indeed,the sources of that energy, such as oil,are also sources of feedstock for manymaterials e.g. plastics or manychemicals. In parallel with uncertaintiesabout energy supplies, there are alsouncertainties in the supply of somestrategic metals for example titanium,tantalum, hafnium especially as theyare found in only a few countries.Closer to home, while the UK haslarge reserves of minerals, in reality,those readily accessible are limited ordeclining due to environmental and

land use policies. These need to beplaced in the strategic context ofmaterials availability.

Sustainable development

Sustainable consumption andproduction forms a key part of the UK’sand EU’s drive to sustainabledevelopment. It is also increasinglybeing taken up by the emergingeconomies - notably China. It is aboutdoing more with less and aboutbreaking the link between economicgrowth and environmental degradationand the unsustainable use ofresources. The aim is to reduce boththe amount of materials input andwaste outputs and to make fullest useof materials in the economy

This is increasingly being reflected withthe introduction of mutually reinforcingpolicy instruments designed totransform markets and behaviours.Such producer responsibility legislation(e.g. End of Life Vehicles, WasteElectrical and Electronic Equipment)taxation (e.g. Climate Change Levy,Aggregates and Landfill taxes) fiscalincentives (e.g. Enhanced CapitalAllowances for energy and water savingequipment), permit trading, publicprocurement, negotiated and voluntaryagreements, and business supportprogrammes, all form part of the drivetowards greater resource efficiency.

The regulation and taxation hasincreased public awareness of theseissues. Younger generations arecertainly aligned towards sustainabledevelopment. However, consumptionof products is increasing as is thedemand for new applications. Thereare opportunities for the materialscommunity through innovation and useof materials. Also sophisticatedapplications of materials technologysuch as composites bring heir owntechnological demands for end of lifedeconstruction and recycling or reuse.This presents further opportunities forinnovation and growth.

1918

Challenges for the future

Materials technologies will play a central part in addressing many of thechallenges of the 21st century.

Materials are central to all areas oftechnology and economic activity. Forexample, it will be difficult, if notimpossible, to improve energyefficiency or to create new energytechnologies, without materialstechnology. Thus materials R&D will beessential in any efforts to reduceemissions of carbon dioxide and toachieve sustainability. To meet thosechallenges, the UK’s materialscommunity needs to address anumber of important issues. TheMaterials IGT Task Group on scienceand technology has conducted adetailed assessment of materials R&Din the UK7. This analysis, along withrecommendations for specific areas,appear in a separate report. In thefollowing section, we look at thecontributions that materialstechnologies can make to a number of essential sectors.

Energy

Energy is an area where materialstechnology will play a particularlyimportant role in meeting the needs ofthe future.

The global energy industry is morethan £600 billion. Energy generation ishighest in North America followed byFar East and Oceania, and thenWestern Europe.

The growing importance ofenvironmental issues is such thatenergy generation, conservation,storage and security of supply willcontinue to be major drivers formaterials technology. We needsustainable energy production and usewhile at the same time meeting socioeconomic and environmental targets.

Energy production through toconservation encompass a broad rangeof technologies and materials (seetable in Figure 9).

The high priority of energy makes itimportant to sustain research,development and modelling ofmaterials for energy applications.

Skills are also an issue of continuingconcern. Changes in the energymarkets in the UK over the past 30years, particularly the lack ofinvestment in cleaner coal and new

7 The Science & Technology Task Group report is on the enclosed CD. This report will be published along with the reports from the Task Group’s subgroups in June 2006

nuclear plant, mean that the countryhas lost much of its technical expertisein materials relevant to important areasof energy technology.

The UK should set out to recover, capture and develop theknowledge-base of high integritystructural materials for future power generation.

The UK needs design skills andmanufacturing capability to enable it tobe an intelligent customer for futureprocurement of energy technologies.For example, the UK needs to quantifythe contribution that materialstechnologies can make to nucleardecommissioning and possible newcivil nuclear generation. In addition, thedevelopment of nuclear fusiontechnologies, in particular, will not bepossible without a complete strategyfor associated materials. Figure 8shows how materials companiessupply the UK energy generationindustry at present.

The UK should examine transferable material solutions andmethods across the completeenergy portfolio to attain maximumcompetitive advantage.

It is equally important to investigatethe materials needs of other sourcesof energy generation, such as fossilfuel, fuel cells, renewables, and energyconservation and storage.

The global focus on energy is anopportunity to develop world-classknowledge and capability in the UK inmaterials for energy generation, lowenergy processing and energyconservation, and to attract investment(including inward investment).

Raw materials

Production and consumption ofmaterials continues to increaseworldwide. While there is noimmediate threat to the global supplyof the raw materials required to make

2120

Overview of the material supply market

Note: List of companies is not exhaustive. It covers the main names provided during interviews with generators, contractors and OEMs.

Ultra big forging:Japan Steel Works (JSW)

Big forging:Sheffield Forgemasters, JSW

Pulveriser castings:Firth Rixson Castings, Bradken

Boiler tubes:Sandvik, DMV stainless

Turbine rotors:Sheffield Forgemasters, Saar Schmiede

Turbine blade ingot:Corus Engineering Steel, öhler Edelstahl B

Turbine blade finishing:Alstom (at Rugby), Siemens (at Newcastle), C Blade SpA

Super alloys & turbine blade castings (hot end):Howmet (UK), AETC, Doncasters SM

High temperature coatings:Chromoalloy, Howme (USA)

High temperature welding materials:SM, Sprint Arcelor

Turbine rotors:Sheffield Forgemasters

Turbine blades:General Electric (GE), Siemens

Insulation material:Tufnol Composites, Attwater, Von Rollsola, Mekufa

Rotor wedges:Pechiney

Generator rotor:Sheffield Forgemasters, Saar Schiede

Generator nacelle (housing):GE, Siemens

Figure 8

Nuclear

Coal

Gas

Hydro

Wind

EnergyPlant/components

Structuralmaterials

Functionalmaterials

Multifunctionalmaterials Biomaterials

GenerationConventionaland advancedfossil

e.g. Steamturbines Boilers Gas turbinesGasifiersFuel cells Hydrogen from coalCoal liquefaction

SteelsAlloy steelsSuperalloysCeramicsCompositesCoatings

Activatedcarbons FiltersInterconnectorsMembranesSorbents Chemical loopingmaterials

Structural healthmonitoringsystemsDiagnostic SmartmaterialsCatalytic filtermaterials

Anti-corrosionbiofilms

GenerationNuclear

e.g. Boilers &turbinesDecommissioning/ storage Reactor vessels Fission/fusionmaterials

SteelsAlloy steelsSuperalloysCeramicsCompositesCoatings

Filters, Active carbons

Structural healthmonitoringMaterials forremote robotsSelf-repairmaterials SMART materials

GenerationRenewable

e.g. Windturbines Tidal power Hydro turbinesBiomass plant Heat exchangersFuel cells

CompositesPolymersSteelsSuperalloysCeramicsCoatings

PhotovoltaicThermalmaterials(Geo and Solar)Fuel-cellsmaterialsAnti-foulingcoatings

PhotovoltaicmaterialsPiezoelectricsFuel-cellmaterialsCatalytic FiltersConductingmembranesSolid ElectrolytesThermoelectricsPower harvestingStructural healthmonitoringSMART actuationmaterials

BiofuelsBiomimeticstructuresBiohybridmaterialsAnti-corrosionbiofilms

Transmission e.g. HighconductivityapplicationsInsulators High Strength

CeramicsPolymersComposites

PiezoelectricmaterialsSuperconductors

StorageElectrical

e.g. Batteries CeramicsNon-ferrousalloys

Electrodematerials

ElectrolytesMaterials forintegrated powersystems

StorageHydrogen

e.g. PipelinesCompressors Pressure Vessels

SteelsAlloy steels

CarbonNanostructuresActivated carbonmembranes

Highcapacity/integrity

Conservation e.g. LightweightstructuresThermalinsulation

CompositesCeramics

PhotochromicsElectrochromicsThermochromics

Smart packagingInsulationEnergyharvesting

Biodegradation

This table maps the requirements for future applications of materials against key energy areas.

Figure 9

Table of materials required for energy generation, transmission, storage, conservation etc.

primary materials, reserves are notlimitless. Thus the principles ofsustainable production andconsumption are essential forcontinuing future development.

Materials supply depends on ‘rawmaterials’ other than those needed forprimary manufacturing. For example,there is a growing demand forcomposite materials. These too cansuffer from supply problems. Forexample, in the UK there are relativelylimited supplies of materials such ascarbon fibre.

The demand for composites in theaerospace market could grow by morethan 10% in the next five years withthe introduction of several new aircraftcontaining high percentages ofcomposites. Airbus has increased thecomposite content of its airliners fromless than 5% in the A300-600 20 yearsago, to 15% in the A320 in the 1990s.Its next generation aircraft, the A380,will have nearer 25% compositematerial. Boeing too has usedcomposites since the 1960s. Its 787‘Dreamliner’ is due to be the firstcommercial jet aircraft in whichcomposite materials will make upmost of the primary structure.

While market forces appear to haveaddressed immediate problems - anew carbon fibre plant is being built inSpain for example - supply issues arelikely to continue to occur. To deal withthe possibility of future threats, theMaterials IGT identified severaloptions, such as a major re-useinitiative, and an audit of where the UKnow depends on relatively scarcematerials, to enable targeted recycling.

To ensure the best use of rawmaterials, the UK should compile aninventory of the materials that arealready in use. It should also define arecycling policy for strategic materials.This should covering collection,segregation and processing.

The UK should embark upon a majorrecycling initiative and work harder tooptimise its use of materials resourcesincluding a major re-use initiative.

With its high dependence on importedraw materials, the UK should monitorthe implications for the materialscommunity of its dependence on finiteraw materials and investment in R&Dshould focus on the search foralternative raw materials and sourcesor process technologies.

Sustainable development

Materials are crucial to sustainabilityand the quest for manufacturingprocesses that reduce our impact onthe environment. Innovativetechnologies that set out to meetthese environmental objectives canbring new business opportunities,open up developing markets andenhance competitiveness.

Discussions of sustainability focusedon three key areas:

• energy efficiency, production, useand low-carbon emission

• minimising waste generation, andmaximising recycling and re-use

• product design for sustainability(Eco-design).

Business that can meet growingexpectations of higher environmental andethical standards that develop ‘materiallight’ goods and services will be bestplaced to enhance their competitiveness.Corporate responsibility, includingproduct stewardship, must extendthroughout supply chains, from tacklingthe issues arising in the extraction of rawmaterials, to engagement withconsumers about the products andservices they buy and eventually discard.

There is a need for betterunderstanding of the impact ofmaterials and products throughouttheir life cycle through dialogue toenable joined up thinking betweenmaterials producers and users. Thematerials design and user communityshould make greater use of life-cycleand design-for-life concepts,supported by access to data formaterials within a sustainableproduction and consumption agenda.This should be backed up withspecific training where it is needed.

2322

Computer modelling is increasinglyimportant in the development ofmaterials and processes, in predictingthe properties of new materials, forexample. While the UK has significantstrengths in materials modelling, thereis a need for a more holistic approach tothe mathematical modelling ofmaterials, both in terms of scale andlifecycle. Modelling the continuum,from the atomic level up to bulkmaterials, can bring enormous benefits,for example in improving ourunderstanding of adhesion and welding.

Whole lifetime predictive modelling,cradle to grave, is important for thedevelopment of new materials as wellas to sustainability, recycling and re-use.

The generation of generic models inthis area would be particularly valuable.

Innovative solutions, includingdevelopments in technology, to reducethe materials component ofmanufactured goods would not onlysupport the quest for sustainability butwould also minimise the risks of lossof supply to manufacturing in the UK.

Health

Medicine and healthcare have agrowing need for biomaterials,materials that can reside in closecontact with the body. Biomaterials

have seen exceptional growth anddevelopment over the past decade,creating a worldwide market of over$36 billion. This is projected to grow byup to 10% per annum, for someclinical applications.

Biomaterials are important in thedelivery of radical surgicalinterventions. They often provide theonly viable option for repairing majortissue and organ structures. Thoughoriginally developed for life-threateningand serious debilitating conditions,biomaterials are now increasingly usedto correct minor structural andfunctional defects.

Current generations of biomaterials areinadequate for the management ofserious clinical conditions, particularlyover the longer term. There are majoropportunities to develop newbiomaterials, but if the risk of failure ofclinical devices is to be avoided, thenresearch on biomaterials in a fullymultidisciplinary context,encompassing material/physical andbiological sciences will be required.

Surgical procedures already make use ofbio-resorbable polymeric materials that,for example, dissolve in the body andrelease drugs. Fundamental materialsdesign and concepts are already inplace, so in the next five years newmaterials with controlled interfacial

Integration of biomaterials with inorganic functional materials for diagnosticcapability and sensors. Also self-diagnostic systems and self-healing materials.

Website www.iom3.org/foresight/Biomaterials

Future challenges for Biomaterials

CASE STUDY

properties and predictable degradationare likely to enter the market. This willinitially be for conventional surgical use,but subsequently as scaffolds to providestructural integrity for the body’s ownregeneration processes to replace losttissue. As part of this development, newbiodegradable systems will enablecontrolled release of bioactivecomponents to enhance tissue repairand regeneration. While such materials do exist they are not availablein the desired purity and form.Commercialisation will depend upon refined manufacturing andproduction techniques.

Novel manufacturing will furtherextend the functional, structural andmultifunctional repertoire of existing,clinically acceptable biomaterials, withadaptation of processing technologiesfrom other materials sectors. Newbiomaterials products will emergewithin five years, many incorporatingbioactive components, with retainedstability because of more biologicallycompatibles process development.

Continued support for Biomaterials is essential particularly for thedevelopment and refinement of bio-resorbable and bioactive materials.

There is also scope for materials toimprove the quality of life for anaging population. For example,lifestyle aids that provide mobility andfacilitate self care.

Security and defence

National and personal security willcontinue to be a concern. Technologycan play a significant part here. Forexample, materials offer new ways of preventing counterfeiting ofproducts. There could also beapplications of materials in ‘bio-tags’and biometric products.

There are opportunities to developmaterials for sensors and systems that rapidly scan luggage and travellersand for sensors in clothing andbaggage that facilitate detection ofdangerous substances.

There will also be a continuing needfor materials to support defence.Indeed, defence applications have longbeen a driving force for new civiltechnology in the UK. But for this tohappen, there has to be greaterawareness of the opportunities. It isalso important for businesses torealise the potential for ‘dual use’ ofdefence-related products forcommercial applications. Like its civilcounterparts, the defence sector alsoneeds to call on deep scientific andtechnology understanding, particularlyin materials characterisation andmodelling. Designers and users needa fully validated capability to predictthe performance, safety and reliabilityof materials and systems throughouttheir life.

Effective modelling spans the materialscontinuum from atomic, micro, mesoand macro scales right through toengineering models. Additionally, fordefence applications there is an evengreater need to understand howmaterials behave under extremeconditions of temperature, pressure,high strain rate and shock.

Multifunctional materials are a priority in future applications fordefence and aerospace, particularlywhere they enable the design of smartstructures. There is also a movetowards lighter and smaller systemsfor certain applications. Here advancedmaterials, including composites, canoffer potential robust, weight efficient solutions.

A priority must be research,development and modelling ofmaterials and technologies forsensing and diagnostic applications.This has been highlighted as a keytheme for all aspects of our lives,with applications in security, bothpersonal and ‘homeland,’ energy,transportation, healthcare, the builtenvironment and communicationsand IT.

2524

Construction and the built environment

Construction uses large amounts ofstructural materials, an area in whichthe UK has considerable expertise.Building materials are also used inlarge volume so a small reduction incost or improvement in properties hasa large economic effect.

There is a range of activities going onwith the construction sector in the UKmany of which relate to materials andwhich could derive useful lessons formaterials applications in other areas.MatUK is proposing to establish aworking group for materials inconstruction to build on the verysuccessful events the Materials IGTran with the Construction ProductsAssociation (CPA). The latter will leadthis group for MatUK.

Major drivers for the future inconstruction include affordablehousing, renewal of infrastructure, andbuildings that can be easily adapted forchange of use or style of living orworking or deconstructed optimisingre-use and recycling of the constituentmaterials. The impact of surroundingson worker productivity is now anacknowledged fact. Modular off siteconstruction is growing and needs tobe exploited by UK firms.

Construction materials will also beimportant in any attempts to improvesustainability and to make better useof energy. Buildings are a major userof energy - cutting heat loss frombuildings can make a large contributionto reducing climate change.

Transport

Transport is a also major user of energyand materials. Pressure to reducecongestion and the demand for cheaperand better public transport all presentchallenges for materials technology.

The UK has large automotive andaerospace industries which other IGTshave already reviewed. These reviewshighlighted the need for lighter, safer

road and rail vehicles, with a smallerenvironmental footprint. Transport willbe a large and growing market forcomposite materials, with theirpotential to reduce the weight ofaircraft, motor vehicles and trains.

With its success in the aerospacesector, for example, the UK has donemuch to advance materialstechnologies. As the Aerospace IGThas already pointed out, light alloysand high-temperature nickel-basedmaterials and coatings are importantfor the continuing competitiveness ofthe UK’s aerospace sector.

Building on the recommendations ofthe previous IGTs, specific materialsrequirements in these sectors are:

• Transport is already a major marketfor composite materials, with theirpotential to reduce the weight ofaircraft, motor vehicles and trains.

• Light alloys and high-temperaturenickel-based materials and coatingsare important for the continuingcompetitiveness of the UK’saerospace sector.

• At the same time, there is acontinuing need for continuedimprovements in more ‘traditional’materials (steel, aluminium, glass,plastics etc.) and processingtechniques (casting, forging,powder metallurgy etc.).Continuing development in theseareas must remain a priority.

Information andcommunication

The rapid rise of information andcommunications services over the pasthalf century raises particular issues formaterials. The many technologies ofthe past 50 years, broad bandrevolution - optical fibre, lasers,electronic devices, mobiles, displaysand so on - all depended on thecontinued development of novelfunctional materials. The R&Dcommunity in the UK has been at theforefront in the science behind manyof these materials technologies.

Figure 11

Materials for sensors

The global market for electronicmaterials is estimated as beingbetween five and ten percent ofsemiconductor sales (www.sia-online.org). Forecasts to 2010 shows asignificant increase, with consequentopportunities for materials (Figure 10).

Photonic materials and such conceptsas plasmonics, the merger ofphotonics and electronics at nanoscaledimensions, are critical to the future ofInformation and CommunicationTechnologies (ICT) from the continuingincreases in density and speed ofelectronic circuits to the futuredevelopment of display and solid statelaser technology and the integration ofphotonics and electronics.

As a related technologicaldevelopment in a separate market,there is a rapidly growing globalindustry in solid-state lighting, such assemiconductor light emitting devicesand laser-based lighting. This will havea significant impact on energyefficiency, consuming much lessenergy for lighting. There areopportunities as this technologyaffects the general lighting field.

The semiconductor industry is capitaland technology intensive and facesintense competition and bouts of

2726

over-capacity. Historically, new inputmaterials and production processeshave resulted in both sustaining anddisruptive innovation. Consequently,entrenched firms and new entrantswith innovative technologies have bothbeen successful.

Magnetic materials are also important in electronics, in datastorage for example. Through thecommercialisation of such ideas asspintronics, they will also contribute tofuture sensor technologies andquantum computing.

The challenges for electronicsmaterials arise both at the productionend, with the demand for ever moresophisticated functional materials, andat the end of life of equipment. Theproliferation of electronic devicescreates a growing demand forrecycling and/or re-use.

Sensors and diagnostics

Many of the opportunities that wehave described in this section willneed sensors that can monitor anddiagnose systems, artificial and natural.For example, research, developmentand modelling of materials andtechnologies for sensing anddiagnostic applications are important inthe development of applications insecurity, both personal and ‘homeland,’energy, transportation, healthcare, thebuilt environment and communicationsand IT.

Materials are the essential ingredientof sensing and diagnostics (Figure 11).This area is ripe for invention,innovation and exploitation.Interdisciplinary work will be essentialto model and develop materials andtechnologies for sensors.

Those sensor applications that havethe greatest promise should beprioritised for further research funding.

Global market for electronic materials

Source: www.sia-online.org (using $1.50 to £1 as nominal exchange rate)

Year

Materials (if 10% of Semiconductor sales)

Materials (if 5% of Semiconductor sales)

Figure 10

Sal

es (

£bn

)

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

20

15

10

5

0

Further opportunities

So far we have highlighted areas ofindustry and materials technologywhere there are major challenges andopportunities. There are many otherareas where materials technology willplay a major role, and where there are significant opportunities forresearch to influence the direction ofparticular applications.

Materials technologies will also play apart in many other aspects ofmanufacturing. For example, materialsfor packaging must also respond to themajor challenges of energy andsustainability. They must also addresssuch issues as the growth of internettrading, the need to recycle, thepresence of in-built sensors that monitorand indicate integrity of content.

Packaging raises a number of materialsissues. For example, we should seek

ways to minimise packaging to support‘material light’ goods whilst enhancingproduct presentation. The quest forsustainable development is also a spurto consider reusability and recyclabilityof packaging materials and the use ofalternative materials with lowerenvironmental impacts across the lifecycle. The use of regulation in this areais widespread and will benefit from aco-ordinated industry perspectiveacross materials.

In addition to construction applications,structural materials also represent anarea where the UK can achievesignificant benefits through continuing‘incremental’ developments ofmaterials, where the country hasconsiderable expertise in advancedsteels and light alloys. Composites areincreasingly important in applicationssuch as aerospace and transport.

Sector Structural materialsFunctionalmaterials

Multifunctionalmaterials Biomaterials

Healthcare Implant wear /prosthetics

Telemedicine/ robot surgeryBody signs

Health monitoring‘wearables’Remote sensingBiocompatiblematerialsCompatibility

AssaysDrug deliverysystemsIntelligent Implants

Energy Fuel cells Fuel cells Fuel cells Waste management

Construction Lifetimemeasurement

Concrete ageing Structural healthmonitoring/diagnostics

Microbial hazards

Transport Compositemonitoring

Heat, pressure, wearAsset managementProximity alarms

Integrated sensors/actuatorsSelf-diagnostics

Driver alertnessEnvironment quality

Retail Produce lifetimeStock management

Smart packagingSports equipmentProduct TaggingPrintable power

AntifoulingBiosensing

Communications Asset management -proactive faultreporting

MagneticOpticalNetwork security

Biomimetic networks

Security Structural/buildingmanagement -earthquake sensors

Smoke detectionGas detectionIdentification

Anti-counterfeitingOffender taggingBiometrics

BiometricsBiohazard detection

Optimising the research base

We believe that there should bestronger links between the UK’sresearch funding bodies - the DTI,Research Councils, MOD and others -to ensure support for basic and appliedresearch aligns with the materialstechnology roadmaps validated byMatUK. This activity will includeadvising the Government’s TechnologyStrategy Board on the research andtechnology requirements for materialssuccess in the UK.

Funding for R&D

Materials-related research andapplication driven exploitation is oftenhigh risk. While materials technologyis recognised as a key underpinningtechnology by the Technology StrategyBoard and funded as such,consideration should be given to“phased” funding which would give afixed level of funding during the initialdevelopment phases of a project,continuing on a tapering basis as theproject gains industry support andinnovations come to market. Thiswould facilitate the transfer ofresearch and development fromacademia into industry.

To support the technology opportunities that we have described, the UKneeds to create and sustain the right environment for academic andbusiness research in the UK.

extensive laboratory equipment. Thishardware would be better used if thevarious players had better knowledgeof the location and capabilities ofthese assets.

The UK should establish mechanismsto facilitate access to that equipment,and promote its use, maintaining itwhere appropriate. Such a network willavoid duplication and, wherenecessary, enhance the justification fornew equipment in the UK’s capability.(A business plan for this activity,Materials Assets Connect8, will beprepared for consideration by the DTI,EPSRC and appropriate RDAs9 by theend of September 2006.)

To enhance the use of the country’sR&D assets, the UK should establisha database and network ofequipment available in industry,government and academiclaboratories for materials R&D.

2928

Aligned with this, there should also bemechanisms to fund materialstechnology demonstrators. Togetherwith better predictive modelling,support for demonstrators wouldreduce overall risks of bringingproducts to market. Other supportmodels should be researched to see iflessons can be learned e.g. programmefunded by the US Department ofDefense such as the DefenseAdvanced Research Projects Agency(DARPA) and the Small BusinessInnovation Research (SBIR). The SBIR10

is the largest source of early stagetechnology financing in the US.

Funding for materials R&D as a keyunderpinning technology shouldcontinue but in addition considerationshould be given to more support forthe development phase (and/ordemonstrators) which is often stillhigh risk.

The UK should seek to influence thedirection of EC funding to enhancematerials R&D across the EU andmaximise the opportunities forresearchers and industry in the UK.

The UK should ensure that routes tointernational markets are optimizedso that new products incorporatematerials from the UK.

The environment for research and innovation

Many of the recommendations that wemake elsewhere in the report will alsoinfluence the environment for R&D, onskills and training for example. Indeed,most of our recommendations will alsobring benefits by helping to focus theUK’s materials R&D programmes andsupport mechanisms. For example,‘road mapping,’ which we discuss inthe section on Knowledge Transfer, willbe important in optimising theresearch base.

We have described many of thespecific needs of research andinnovation in the report of theMaterials IGT Task Group on Scienceand Technology. This also describesthe opportunities for particularmaterials in some detail. Here wepresent the key cross cuttingrecommendations from that study.

Better use of R&D assets

Universities, Government laboratories,independent technology organisationsand businesses individually maintain

Neotec™ offers a cost-effective and light-weight alternative to plastic fuel tanks.

Lead-free Steel is easily recycled and emission-free from fuel impregnation, thataffects plastics and raises their recycling costs, therefore future environmentallegislation and end-of-life recycling targets can be met.

www.corusgroup.com

Lead-free metalliccoated steel for fueltanks - Neotec™

CASE STUDY

8 Annex 1 shows where this fits within MatUK9 RDAs are the Regional Development Agencies

10 http://www.acq.osd.mil/sadbu/sbir/overview/index.htm

No matter how good the UK’s scientific knowledge, it will be of little valuewithout effective transfer to the commercial sector.

While there are undeniable pockets ofexcellence in business practices in theUK, there is also room forimprovement. Wider use of ‘bestpractice’ would enhance thecompetitiveness of the materialscommunity, as would wider use of suchtools as road mapping to improve R&Dplanning and product development.

Small and medium-sized enterprisesface particular challenges in knowingwhere to gain access to information onthe choice and use of materials.

The newly created Materials KTNshould continue to be developed tofacilitate communication with thematerials community in the UK and interested stakeholders,particularly SMEs.

The National Composite Networkexists to support the compositessector and links into the MaterialsKTN. Composite materials also providethe platform on which to develop arange of integrated functional,multifunctional and “smart” structuresand system.

The strength of the materials community, and the importance of materialsto every aspect of economic activity, is such that the UK is well placed totake swift and concentrated action to deal with some of the weaknesses,and to exploit the strengths, that are described earlier in this report. Inparticular, it is important to find ways for the various sometimes disparatematerials communities to come together to develop a common vision andto make it happen.

We have identified five key themeswhich the UK need to address toenhance the prospects of thematerials community:

• Knowledge transfer

• Raising awareness

• Accelerating innovation

• Improving skills and knowledge

• Better business environment.

In the following section we describe theissues within each of these themes.

3130

Knowledgetransfer

This and other network nodes for theMaterials KTN should continue to besupported and new ones put in placeprovided the business case is strong.

Best practice

Best Practice concerns the behaviours,processes and procedures whichtogether lead to the best achievableefficiency and effectiveness in industry.

The continued competitiveness ofBritish industry depends on theapplication of best practice andcontinuous improvement. The MaterialsIGT’s Task Group on Best Practiceidentified a number of issues, includinga lack of a common understanding ofjust what constitutes best practice in allaspects of the business process,including shop floor practices,management, optimising innovation inthe selection and use of materials, andthe advantage of benchmarking.Although many large companies havesignificant strength and understanding,this is not so for SMEs.

The Best Practice Task Group foundthat the most common perceived

Priorities for the UK

As we have already stated, our ownvision is that the UK will continue tobe one of the foremost advancedtechnological societies in which world-class materials expertise underpinssustainable growth.

The strengths in research and thepositive business environment areespecially important, putting the UK in a good position to achieve ourvision. By tapping into theopportunities that we have describedin energy, resources and theenvironment, and by using these asareas around which to developcoherent, focussed and well managedresearch, we can tackle the threats ofclimate change, energy uncertaintiesand economic globalisation.

Raising awareness

Support for materials technology - and training and recruitment of skilled workers - depends on greater awareness of the importance ofmaterials to society.

optimise their choices of materialsbased on whole-life considerations. Thematerials community should alsoensure that the ‘materials message’come through in other ‘Image’ raisingprogrammes, such as those intendedto improve the image of manufacturing.

In addition there should be specificmaterials activity to:

• Enhance the appreciation ofmaterials at school level byinfluencing curriculum changes topromote teaching of science asearly as possible, using ‘materials’to illustrate what science can do.Find ways to increase the numberand quality of teachers who candevelop and deliver materialsrelated subjects in schools.

• In collaboration with the RDAs, todevelop a Material s IGT Youthreport as a basis for a betterappreciation of the value ofmaterials and to highlight the careeropportunities in materials

barriers to implementation of bestpractice in materials can besummarised as a general lack ofknowledge of the possibilities andpotential benefits. Without thisknowledge, it is difficult for businessesto justify investment of resources andfunding. Other common barriersinclude lack of sources of materialsdata and a lack of leadership or vision.

The materials community needs to bemade aware of the advantages of usingbest-practice tools and encouraged tomake use of the help available via theManufacturing Advisory Service andvarious industry groups.

There is a need for intelligentsignposting to sources of best-practice tools, covering all aspects ofthe business process, including on-line benchmarking of performance.The Materials KTN should undertakethis role.

With the support of the MaterialsKTN, large companies should assisttheir suppliers in the adoption of bestpractice and in the introduction ofnew materials into the supply chain.

Benchmark

The UK should benchmarkinternationally its performance in allaspects of business delivery ,performance and supply chain issues,and monitor what is happening inother countries so that the UK canreact appropriately.

As well as monitoring key materials,we should also monitor changes inmanufacturing processes and thesupporting infrastructure.

Roadmaps

Technology roadmaps are anincreasingly effective way of tappinginto the collective thinking and expertiseof a business community. Roadmapsoffer a way of thinking about the future,and a framework for supportingcollaboration, decision making. TheForesight Materials Panel has, under the

3332

auspices of the IoM3, acted as a focusfor the creation of a number ofroadmaps for materials technology.

The Materials KTN should maintain adatabase of industry approved andvalidated ‘roadmaps’ of technologyfutures for materials.

Materials services

There is a strong need to co-ordinateand signpost materials services,including R&D, materials propertiesand access to materials manufacturingdatabases. The Materials KTN shouldfacilitate access to these resources. Itshould promote better use of existingfacilities and of the existinginfrastructure supported by theNational Measurement SystemProgrammes on materialsmeasurement testing andstandardisation. For innovative andcompetitive application of new andimproved materials, designers needreliable property data. Such data mustbe obtained by using validated test andmeasurement methods. A MaterialsProperty Validation Network should bebrought into service as quickly aspossible (see annex 1 for its position inMaterials UK) building on the plannedinitiative by the London DevelopmentAgency to provide the hub of a nationalnetwork. This would be well positionedto link in with the current metrologystandardisation work at NPL.

The UK can enhance the attraction ofthe UK as a place to do business byestablishing a centre (or network) tovalidate materials properties.