“a study of loans and advances and their ...bdbacollegeaundh.edu.in/pdf/nimbalkar_sir.pdf“a...

TRANSCRIPT

“A STUDY OF LOANS AND ADVANCES AND THEIR

MANAGEMENT BY THE URBAN CO-OPERATIVE

BANKS (UCBs) IN THE PUNE DISTRICT.”

A REPORT SUBMITTED TO UNIVERSITY

GRANTS COMMISSION

AS A

MINOR RESEARCH PROJECT IN

THE SUBJECT OF COMMERCE

BY

DR. NIMBALKAR SUHAS ABASAHEB

BHARATRATNA DR. BABASAHEB AMBEDKAR

COLLEGE AUNDH, PUNE-411007

MAY-2015

DECLARATION BY THE RESEARCHER

I hereby declare that this Minor Research Project titled “A study of

loans and advances and their management by the urban co-operative banks

(UCBs) in the Pune district” submitted is based on actual work carried out by

me. Any reference to works done by any other person or institution or any

material obtained from other sources have been duly cited and referenced. It

is further to state that, this work is not submitted anywhere else for any

examination.

Dr.Nimbalkar Suhas Abasaheb

ACKNOWLEDGEMENT

It is my duty to thank them all those who have helped me in

completing my Minor Research Project work.

I express my sincere gratitude to Prin. Dr. M. V. Bobade and all the

colleagues of my college for their valuable guidance, continuous support

throughout this minor research project.

I would like to mention a special thank to the Managers of all the

selected banks who had provided essential information regarding this

project work.

It would have been impracticable for me to undertake this work

without the inspiration of my wife Sneha and son Yash.

Last but not the least my gratitude are also to all those who directly

and indirectly supported me for completion of work.

Dr.Nimbalkar Suhas Abasaheb

Date: / / /20

CONTENTS

Chapter No Particulars Page No

List of Tables I

List of Graphs II

List of Maps III

Abbreviations III

Chapter-I Introduction 1-6

1.1 Introduction 2

1.2 Origin of the research problem 3

1.3 Need of the Study 4

1.4 Significance of the study 4

1.5 Reason for selection of the topic 4

1.6 Scope and limitations 5

1.7 Objectives of the study 5

1.8 Hypothesis 5

1.9 Research Methodology 6

1.10 Sources of the study 6

1.11 Conclusion 6

Chapter-II Pune City and Review of literature 7-15

2.1 Introduction 8

2.2 Study of Pune District 8

2.3 Study of Pune City 9

2.4 The Geographical area of Pune

city

10

2.5 Administrative information of

Pune District and City

10

2.6 Climatic Conditions 10

2.7 Population 11

2.8 Literacy rate 11

2.9 Educational facilities 11

2.10 Medical Facility 12

2.11 Review of literature 12

2.12 Conclusion 15

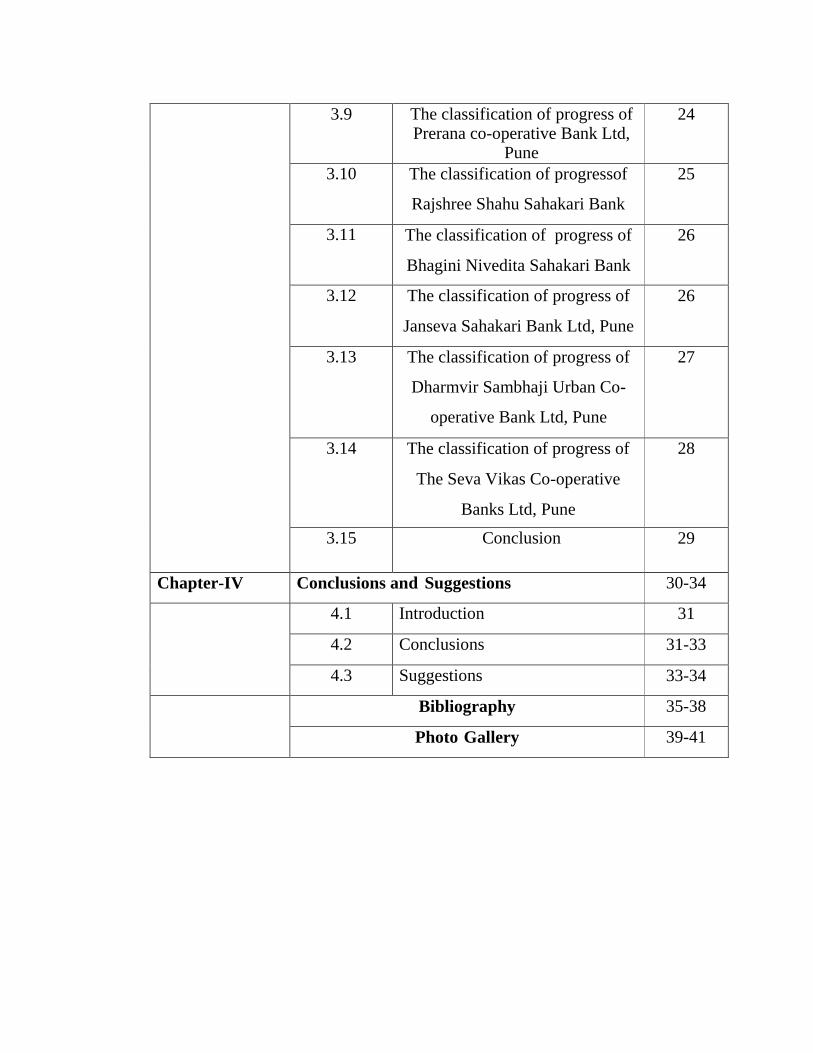

Chapter-III Management of loans and advances of

UCBs

16-29

3.1 Introduction 17

3.2 Concept of Management 17

3.3 Process of Management 17

3.4 Stages of Management 18

3.5 The analysis of the selected nine

urban co-operative banks in Pune

district

19

3.6 The classification of progress of Pimpri Chinchwad Sahakari Bank Ltd, Pimpri

21

3.7 The classification of progress of

Pavana Sahakari Bank Ltd, Pune

22

3.8 The classification of progress of Indrayani Co-operative Bank Ltd, Pune

23

3.9 The classification of progress of Prerana co-operative Bank Ltd,

Pune

24

3.10 The classification of progressof

Rajshree Shahu Sahakari Bank

Ltd, Pune

25

3.11 The classification of progress of

Bhagini Nivedita Sahakari Bank

Ltd, Pune

26

3.12 The classification of progress of

Janseva Sahakari Bank Ltd, Pune

26

3.13 The classification of progress of

Dharmvir Sambhaji Urban Co-

operative Bank Ltd, Pune

27

3.14 The classification of progress of

The Seva Vikas Co-operative

Banks Ltd, Pune

28

3.15 Conclusion 29

Chapter-IV Conclusions and Suggestions 30-34

4.1 Introduction 31

4.2 Conclusions 31-33

4.3 Suggestions 33-34

Bibliography 35-38

Photo Gallery 39-41

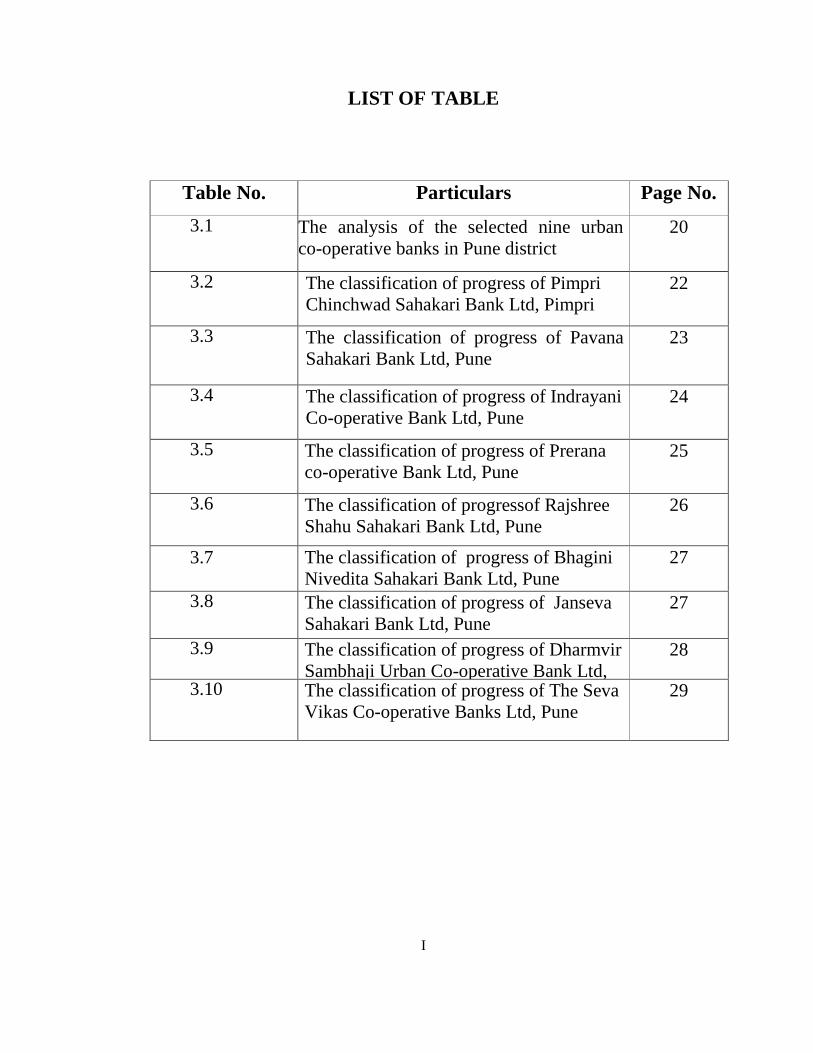

LIST OF TABLE

Table No. Particulars Page No.

3.1 The analysis of the selected nine urban

co-operative banks in Pune district

20

3.2 The classification of progress of Pimpri

Chinchwad Sahakari Bank Ltd, Pimpri

22

3.3 The classification of progress of Pavana

Sahakari Bank Ltd, Pune

23

3.4 The classification of progress of Indrayani

Co-operative Bank Ltd, Pune

24

3.5 The classification of progress of Prerana

co-operative Bank Ltd, Pune

25

3.6 The classification of progressof Rajshree

Shahu Sahakari Bank Ltd, Pune

26

3.7 The classification of progress of Bhagini

Nivedita Sahakari Bank Ltd, Pune

27

3.8 The classification of progress of Janseva

Sahakari Bank Ltd, Pune

27

3.9 The classification of progress of Dharmvir

Sambhaji Urban Co-operative Bank Ltd,

Pune

28

3.10 The classification of progress of The Seva

Vikas Co-operative Banks Ltd, Pune

29

I

LIST OF GRAPHS

Graph No. Particulars Page No.

3.1 The analysis of the selected nine urban

co-operative banks in Pune district

21

3.2 The classification of progress of Pimpri

Chinchwad Sahakari Bank Ltd, Pimpri

22

3.3 The classification of progress of Pavana

Sahakari Bank Ltd, Pune

23

3.4 The classification of progress of Indrayani

Co-operative Bank Ltd, Pune

24

3.5 The classification of progress of Prerana

co-operative Bank Ltd, Pune

25

3.6 The classification of progressof Rajshree

Shahu Sahakari Bank Ltd, Pune

26

3.7 The classification of progress of Janseva

Sahakari Bank Ltd, Pune

28

3.8 The classification of progress of The Seva

Vikas Co-operative Banks Ltd, Pune

29

II

LIST OF MAP

Figure No. Particulars Page No.

Map No.2.1 Pune District 8

Map No.2.2 Pune City 9

ABBREVIATIONS

Per. Percentage

i.e. That is

Govt. Government

NA Not Available

Ltd. Limited

III

1

CHAPTER-I

INTRODUCTION

2

CHAPTER-I

INTRODUCTION

1.1 Introduction

Co-operative banks are a group of financial institutions organized under the provisions

of the cooperative society‟s act of the states. These banks are essentially co-operative

credit societies organized by members to meet their short term and medium term

financial requirements. A co-operative is an autonomous association of persons united

voluntarily to meet their common economic, social and cultural needs and aspirations

through a jointly owned and democratically enterprise. Mutual co-operation leads to

co-operatives. Co-operatives banks are constituted on co-operative principles of

voluntary association, self-help and mutual aid, one share one vote and non-

discrimination and equality of members. Co operative Banks in India are registered

under the Co-operative Societies Act 1904.

Theco-operative bank is also regulated by the RBI. They are governed by the

Banking Regulations Act 1949 and Banking Laws (Co-operative Societies) Act, 1965.

The term Urban Co-operative Banks (UCBs), though not formally defined, refers to

primary cooperative banks located in urban and semi-urban areas. These banks were

traditionally centered on communities, localities work place groups. They essentially

lent to small borrowers and businesses. Today, their scope of operations has widened

considerably.

The co-operative banking along with other types of cooperatives, later on

strengthens the cooperative spirit. Cooperative banking is one of the most important

economic systems, run on self-governing lines to attain economic escalation with

social and economic egalitarianism both agro-rural and industrial-urban sectors and

people in them. In fact, urban people with small means are unable to offer any tangible

security other than their own personal security. They so not satisfy the standards

followed by the commercial banks, thus they do not get adequate credit. Thus urban

people have obtained credit from moneylenders. The circumstances needed an agency,

3

which will provide cheaper and adequate credit to extricate the urban people with a

limited means from the clutches of usurers. From the inception of the palling era in the

country, the thrust of the government policy has been the development of agricultural

and allied activities as, initially the rural areas deserved urgent attention than urban

areas. Nevertheless, ameliorative programmes concerning the urban lower middle and

poor classes cloud not receive the attention up to the First Five Year Plan.

1.2 Origin of the research problem

The need for the provision of credit facilities to town-dwellers was as much

urgent as it was in villages in order to combat usury. Joint stock banks were not

interested in developing the business of small loans, because the cost of advancing and

recovering them was high. Further, as joint stock banks were not likely to have under

ordinary circumstances full and intimate knowledge of the standing and resources of

persons of moderate means, they would not advance loans on personal security.

Ultimately, number of persons with small means, residing in urban and semi- urban

area like small traders, artisans, townsmen, factory workers, self-employed persons ,

petty shopkeepers, retailers, small industrialists, professional, firewalls, cottage

workers etc. require credit for their productive and consumption needs. This has given

a rise to the movement of developing urban cooperative banking for the use of urban

dwellers.

Although the urban co-operative banks operate under the purview of Banking

Regulation Act, they are philosophically quite different from the commercial banks.

They are smaller, their area of operation is limited and they have limited but particular

and committed clientele. The urban co-operative banks have less of „Walk-in‟

customers. The deposit base of them generally does include corporate and large

institutional funds. The urban cooperative banks being the cooperative institutions,

they are bound to follow the cooperative principles and values (i.e. open and voluntary

membership, democratic management, equitable distribution of surplus, limited

interest on capital, cooperative education, cooperation among cooperative and concern

for the community etc.) considering the role, importance and responsibility of urban

cooperative banks, they must be viable, productive and operationally efficient enough

4

in performing their socio-economic responsibility in an effective manner.

Looking at the significance of Urban Cooperative Banks, it has been decided to

focus on the study of loans and advances and their management by the Urban

Cooperative Banks (UCBs) in the Pune City

1.3 Need of theStudy

The urban co-operative credit movements started in India with the chief object

of catering to the banking and credit requirements of the urban middle class, e.g., the

small traders or businessmen, the artisans or factory workers, the salaried people with

a limited fixed income in urban or semi-urban areas. Besides protecting the middle

classes and men of modest means from the clutches of the moneylenders, the

movement is also expected to inculcate the habit of thrifts and savings amongst them.

The movement provides the frugal section of the community an opportunity of

investing then savings and people tide over the period of stress and strain.

1.4 Significance of thestudy

Socio-economic development of the people is impacted by the industrial

development of the area. Availability of financial and banking services are essential

for boosting industrial development. Such financial and banking services are not

available in sufficient number in rural, urban and semi-urban area hence remain

undeveloped. In 1931 the central banking enquiry committee recommended that

limited liability of co-operative societies generally known as Urban banks should be

established wherever necessary for the benefit of middle class people. How for Urban

Co-operative Banks in Pune district helped to the people is essential to study. In this

minor research project the performance of Urban Cooperative banks working in the

district has been studied

1.5 Reason for selection of thetopic

Theresearcherbeing the member of a UCBknows theproblemsof Urban

Cooperative Banks. The term Urban Cooperative Banks (UCBs) till 1996 were

allowed to lend money only for agricultural purpose but now their scope

5

has widened considerably to small industries, housing finance etc. In the

era of globalization there is a rapid change in the lives of the people

residing in the city area. In order to fulfill the different financial needs,

large numbers of people rely on the Urban Co-operative Banks. This has

resulted in providing loans and advances to the large number of people and

it required the management of the loans and advances, hence the researcher

has selected this topic with the view of getting information about nature of

loans and advances provided by UCBs in Pune city.

1.6 Scope andlimitation

The study deals with the work done by Urban Co-operative Banks in their areas

of operation i.e. Pune city. The detailed study covers only from the year 2010-11

to 2012-13. The functioning of Urban Co-operative Banks thus becomes the

universe of the present study. The complete study on the functioning of UCBs and

sample respondents (Bank Managers) would certainly disclose and highlight the

factors affecting the performances of the UCBs.

1.7 Objectives of thestudy

1) Tostudy the progress of Co-operative banks of Pune city.

2) Toanalyze the growth and composition of loans and advances of Urban

Co-operative Banks.

3) To make suggestions about the problems faced by Urban Co-operative

Banks of Pune city.

1.8 Hypothesis

1) The urban co-operative banks in Pune city have made remarkable progress

during the study period.

2) The organization and management of Urban Co-operative Banks is active.

3) There are some difficulties faced by banks officials in granting loans and

advances to its customers in Pune city.

6

1.9 ResearchMethodology

The research topic is based upon exploratory research. Secondary data such as

annual reports with schedule and loans and advances of selected nine Urban Co-

operative Banks have been collected for the period 2010-11 to 2012-2013. Some of the

data were collected from National Institute of Banking Management (NIBM) - Pune,

RBI statistical department publication and Indian banks association publications,

Published journals, news papers and Books.

It is important to make a plan in order to study and to understand the

problems.Theaimofthestudydoesnotgetfulfilled,iftheproperplanisnotdone.Hencet

hetopic “A study of loans and advances and their management by the urban co-

operative banks (UCBs) in the Pune

district”wascarriedonaftermakingaproperandauthenticplan.

1.10 Sources of thestudy

Secondarysources:

The study has been undertaken through reading of various annual

reports, books,magazines,researcharticlesandstatisticsgiveninthe various

sources.

1.11 Conclusion

The present research is based on the management of the loans and advances

of the nine urban co-operative banks of Pune city. In the present research topic

the origin of the research problem, the need of the study, significance of the

study, the reasons behind selecting the topic, scope of the topic, the various

objectives of the research and hypothesis, research methodology and source of

the study have been analyzed by the researcher.

7

Chapter-II

PuneCityandReview

ofliterature

8

Chapter-II

Pune City and Review

ofliterature

2.1 Introduction

2.2 Study of PuneDistrict

Puneis one of

thedevelopeddistrictsofMaharashtra,adevelopedstateofIndia.Punedistrictcomesi

ntothewesternMaharashtradivisionandhasgreathistory.Puneisknownasthecultura

lcapital of Maharashtra. It includes 14 blocks (Taluka) Pune, Haweli,

Indapur,Baramati,Daund,Bhor,Purandar,Velhe,Khed,Shirur,Junnar,Ambegaon,

Maval and

Map No2.1

PuneDistrict

9

Mulashi.Punecityislocatedatthesouthernpartofthedistrict.Thegeographicalare

aandextentofPunedistricthasnaturallybeenwellstructured.ThePunedistrictislo

cated 17.54 to 19.24 north latitude and 73.19 to 75.10 east longitude. It

borderswithAhamadhnagar from north and east, it has Satara and Raigad

districts from south andwestrespectively. It is bound with Solapur and Thane

districts. It covers the 5% of total areaofMaharashtra.

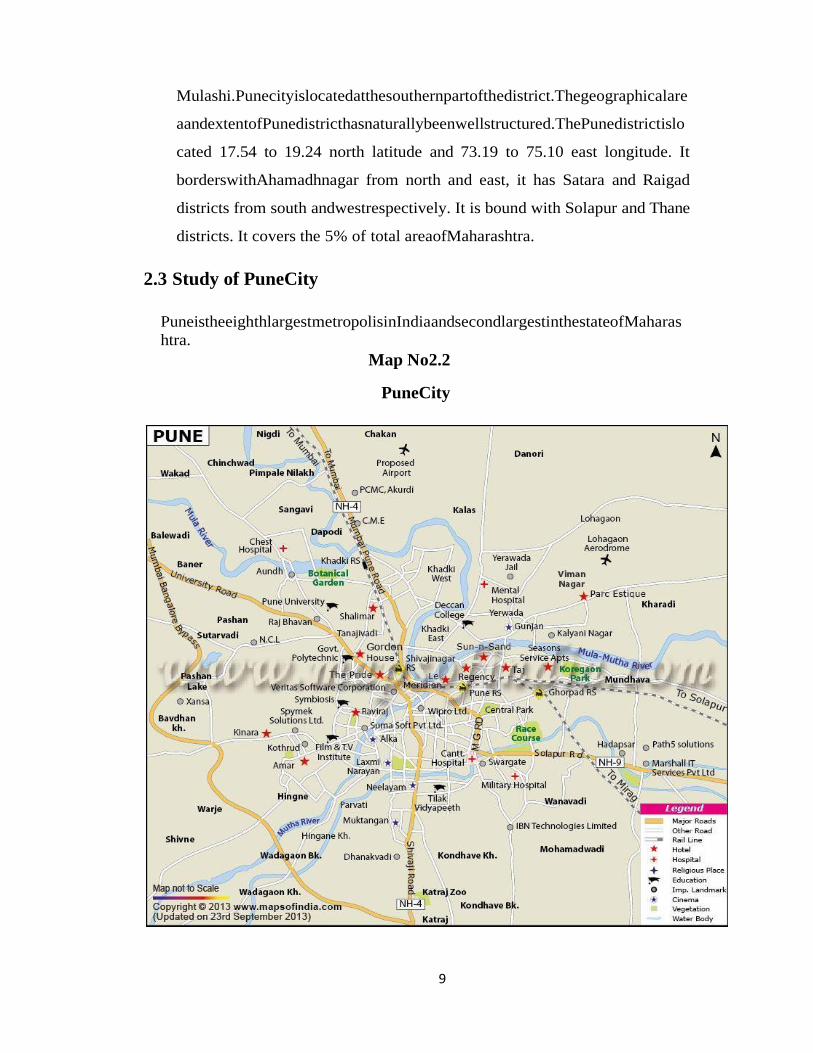

2.3 Study of PuneCity

PuneistheeighthlargestmetropolisinIndiaandsecondlargestinthestateofMaharas

htra.

Map No2.2

PuneCity

10

Itissituated560meters(1837feet)abovesealevelontheDeccanplateauattheri

ghtblankoftheMuthariver.PunecityistheadministrativeheadquarterofPunedistrict

andwasoncethecentreofpoweroftheMarathaEmpire.Puneisknowntohaveexisteda

satownsince1847.ChhatrapathiShivajiRajeBhosalemadeitastheCapitalofMarath

aEmpire.LaterPunewasruledbyPeshwas,whowerethePrimeministersofMarathaE

mpire.

2.4The Geographical area of Punecity

The total area of Pune city is 450.69 sq. Km. Out of total area,38.6 %

isresidentialarea,1.8%iscommercialarea,9.5%isdefensearea,11%isindustrialarea

and9.7%isrecreationalarea.

2.5 Administrative information of Pune District andCity

Thereare14Talukasand13PanchayatSamitisinPunedistrict.IthasTwomuni

cipalcorporations. Pune Municipal Corporation (PMC) and Pimpri –

ChinchwadMunicipalCorporation(PCMC).Therearearound1,866villagesinthePu

nedistrict.

In the modern age, the city has received unique importance because of

beingfamousinthefieldofmanufacturing,automobileindustries,Governmentandpr

ivatesectorresearchinstitutes, information technology, and educational,

management, training institutes.Thecity of Pune is referred as the Oxford of

East proudly. Many research instituteslikeUniversity of Pune, National

Chemical Laboratory, and C-DAC do their research

invarioussubjects.ThelargesttelescopeofAsiahasbeensetupnearPune-

Nashikhighwayinkhodad.The students from India as well as the various

countries come here to have thequalityeducation.

2.6 ClimaticConditions

Thetemperatureofcityrangesbetween12c

to37c.Theaveragerainfallrecordedis600to700mm.Maximumrainfallisabsorbedfr

11

omJunetoSeptembereveryyear.

Owingtoitsgeographicallocation,theclimateofthecityiscoolandpleasantthrougho

utthe year. ThenaturalbeautyofthecityhasgivenitthetitleofDeccanQueen.

2.7 Population

Apopulationisasummationofalltheorganismsofthesamegrouporspecies,w

hichlive in the same geographical area, and have the capability of

interbreedingwisdom,imaginationdecisionmakingandambitiousaretheimportant.

2.8 Literacyrate

PuneisknownastheeducationalcityofMaharashtra.Thequalityeducationpro

videdherebroughtaboutasignificationincreaseinliteracyrateofPune.Accordingtot

he2011census,thetotalliteracyrateofPunecityis

86.15%outofwhichfemaleliteraryrateis 81.05 and male literacy rate was 90.84

respectively. Pune is 7th

largest literary rate districts of Maharashtra.

2.9 Educationalfacilities

Punehasmorethanhundrededucationinstitutesandnineuniversities.Student

sfromall over the world studying at the colleges of the University of Pune.

Most colleges inPuneare affiliated to the University of Pune established in

1948. Seven others Universitieshavealsobeenestablishedinthecity.

Many research institutions of central Government as well as State

Governmentarelocated in city. There are well-known coaching classes for

UPSC and

MPSCExaminationsbecauseofthiscivilserviceaspiringcandidatesalsopreferPune

City.

12

2.10 MedicalFacility

Puneisthefastestgrowingmetropolitancity

inIndia.Thepopulationofthecityisincreasing day by day. In the city life there is

always a question of health relatedproblems.The Pune city is surrounded with the

number of Hospitals and Medical Institutions

suchasSasoonHospital,PunedistrictHospital.Thecityhasmanyprivatehospitalsalso,S

uchasRubyHall,BirlaHospital,DinanathMangeshkarHospital,andPoonaHospitaletc.

Therearesomemedicalinstitutionswherethemedicalstudentscandotheirpracticeafterc

omplacenceof theirstudy.

2.11 Review ofliterature

A number of studies related to performance of co-operative banking sector in

India have been conducted. Here, an attempt is being made to provide an overview of

various aspects and issues of this study through the review of existing literature. Some of

the main studies selected for review have been discussed below.

Kalyankar (1983)

In his study titled, “Willful Default in Loans of Co-operatives” examined the

trends in deposits, share capital, working capital, loans outstanding, advances, over dues

and recoveries at the district level financing institutes. Socio-economic factors

responsible in projecting and promoting future development in the operations and

approaches of the co-operative credit organizations were also considered to examine the

specific progress made by Central Co-operative Bank of Parbhani District. The study

revealed that the cropping intensity, irrigation facility and working capital of the societies

were the major factors for explaining over dues at primary agricultural credit societies‟

level. The socio-economic factors were notresponsible for increasing over dues at the

borrowers‟ level, but over dues were mainly mounted due to the non-economic factors in

case of willful defaulters.

13

Devadas (1987)

In his book titled, “Co-operative Banking and Economic Development” studied

the role of Assam Co-operative Apex Bank Ltd. in economy of the State. He found that

apart from working as a commercial bank it had to discharge three other functions, i.e., to

finance primary credit societies, to act as banking centre for primary societies, and to

undertake supervision of primary societies. He found that bank had not been able to

achieve much in these three fields due to lack of adequate support from government of

the state.

Prasad (2005)

In his research paper titled, “Co-operative Banking in a Competitive Business

Environment” stated that the technology had made tremendous impact on entire banking

sector, which had thrown new challenges, due to which co-operative banks were

constantly exposed to competition and risk management. Therefore, they needed a

combination of new technologies and better processes of credit and risk appraisal,

treasury management, product diversification, internal control and external regulation

along with infusion of professionalism. In the present business environment, the co-

operative banks should be backed by democratization, decentralization so as to make

them competitive. He felt an urgent need for transformation in the mindset, identity,

business operations, governance and systems & procedures, which will definitely boost

the morale of co-operative banks to face environmental challenges.

Singh and Singh (2006)

In their study titled, “Funds Management in Central Cooperative Banks−Analysis

of Financial Margin” attempted to estimate the impact of identified variables on the

financial margin of the central co-operative banks in Punjab with the help of correlation

and multiple step-wise regression approach. The ratio of own funds to working funds and

the ratio of recovery to demand were observed to be having positive significant influence

on financial margin, whereas over dues to total loans were found to be negatively

associated with the concerned parameter. A high percentage of own funds and timely

14

recovery of previous loansoutstanding, as a source of funding new loans by the bank,

increased the financial margin in these banks.

Dhanappa (2009)

In his study titled, “Performance Evaluation of UCBs: A Case Study of

Kallappanna Awade Ichalkaranji Janata Sahakari Bank Ltd. Ichalkaranji” made an

attempt to examine the working and financial performance of UCBs. The objective of the

study was to examine and analyze the trend, progress and problems of this bank and to

offer some important suggestions for improving the competency and efficiency of the

bank. The related data had been collected for the period from 1995-96 to 2007-08. He

used various statistical tools such as ratios, percentages, averages, and chi-square test to

analyze the data, to know the performance of the UCBs in respect of share capital,

deposits, reserve funds, loans and advances, investment, profit, and NPAs. He observed

that the bank had maintained NPAs under control at the best stipulated level of RBI

norms. There was immense instability in net profit.The bank should focus on non-

interest income sources (commission based services) to increase the profit level and

reduce the NPAs. CD ratio of the bank was declining continuously which was not a good

signal. The economic health of the bank was sound and the Bank was able to compete

with other banks. He further suggested that loans should be provided (at least to regular

borrowers) on competitive rates of interest.

Heiko and Martin (2007)

IMF conducted a study on co-operative banks and their financial stability. The

study was based on individual bank data drawn from the Bank Scope Database for 29

major advanced economies and emerging markets that were members of the Organization

for Economic Co-operation and Development (OCED). They found that co-operative

banks in advanced economies and emerging markets had higher scores than commercial

banks, suggesting that co-operative banks were more stable. These findings, perhaps

somewhat surprising at first, were due to much 40 lower volatility of co-operative banks‟

returns, which offsets their relatively lower profitability and cap.

15

2.12 Conclusion

Ithasbeenobservedthroughthereviewofliteraturethattheresearchershavestudi

edthenature of loans and advances of Urban Cooperative Banks of Pune

cityfromdifferent point of view. It is concluded through the above review of

literature that the

urban cooperative banks have unique role to play in 21st century

16

Chapter –III

Management of loans

& Advances in UCBs

17

Chapter –III

Management of loans & Advances in UCBs

3.1 Introduction

This chapter contains ten Urban Cooperative Banks from Pune city. The functions of

these UCBs have deeply been studied in this chapter. A detailed study of various

types of loans and advances provided by UCBs in Pune district has been carried on.

The formal interviews of some selected banks managers have also been taken to

present the statistics based on the annual reports of Urban Cooperative Banks of Pune

district.

3.2 Concepts of Management

As there is no universally accepted definition for management, it is difficult to

define it. A simple traditional definition, defines it as the „art of getting things done by

others‟. This definition brings in two elements namely accomplishment of objective

towards the goal. The weakness of this definition is that firstly it uses the word „art‟

whereas management is not merely an art‟ but it is both art and science. Secondly, the

definition does not state the various functions of a manager clearly. There are various

definitions by eminent experts in the field of management.

A) Fredmund Malik defines it as ‘the transformation of resources into utility’

B) Peter Drunker (1909-2005)

He has the basic task of management as twofold: marketing and Innovation

nevertheless, innovation is also linked to marketing (product innovation is a central

strategic marketing issue).

Andreas Kaplan specifically defines, European Management as a cross

cultural, social management approach based on interdisciplinary principle

3.3 Process of Management

Process management is the ensemble of activities of planning and monitoring

the performance of a process. The term usually refers to the management of business

processes and manufacturing processes. Process of management is the application of

knowledge; skills and toolsvisualize measure, control and report and improve

18

processes with the goal to meet customer requirements profitably.

3.4 Stages of Management

The management process is more than just a set of rules to follow. It is a

philosophical approach to business. The management process is best implemented

when everyone within the business understands the strategy. The five stages of

management are as follows

1) Goal setting

The purpose of goal setting is to clarify the vision of the business. The

stage consists of identifying the various key facets.

2) Analysis

Analysis is key stage because the information gained in this stage will

shape the next two stages. In this stage gather as much information and

data relevant to accomplishing the vision. The focus of the analysis should

be on understanding the needs of the business as sustainable entity, its

direction and identifying initiatives that will help the business grow.

3) Strategy Formulation

The first step in forming a strategy is to review the information gleaned

from completing the analysis. Determine what resources the business

currently has that can help reach the defined goals and objectives.

4) Strategy Implementation

Successful strategy implementation is critical to the success of the

business venture. This is the action stage of the strategy management

process.

5) Evaluation and Control

Strategy evolution and control actions include performance

19

measurements, consistent review of internal and external issues and

making corrective actions when necessary

3.5 The analysis of the selected nine co-operative banks from Pune

City

The researcher has selected nine urbancooperative banks from Pune district

for the present research. The researcher has studied the loans and advances provided

by these nine co-operative banks from 2010 to 2013.

Table No- 3.1

Comparative position of growth of loans and advances duringthe

year(2010-11 to 2012-13)

(Rs. in Lakhs)

Sr.

No

Particulars Year Increase

(+)

2010-11 2011-12 2012-13

1 Pimpri-Chinchwad Sahakari Bank

Ltd, Pimpri.

7177.36 7821.49 8996.09 1818.73

2 Pavana Sahakari Bank Ltd, Pune 10189.41 14292.18 20255.56 10066.15

3 Indrayani Co-operative Bank Ltd,

Pune

3320.25 3850.38 4595.54 1275.29

4 Prerana Co-operative Bank Ltd,

Pune

7056.79 9448.72 10430.19 3373.4

5 Rajshree Shahu Sahakari Bank Ltd,

Pune

11429.86 17690.86 20253.01 8823.15

6 Bhagini Nivedita Sahakari Bank

Ltd, Pune

25348.57 28202.93 33047.09 7698.52

7 Janseva Sahakari Bank Ltd, Pune. 56478.96 72173.90 87560.47 31081.51

8 Dharmvir Sambhaji Urban Co-

operative Bank Ltd, Pimpri-

Chinchwad

3304.82 4181.74 4959.44 1654.62

9 The Seva Vikas Co-operative Bank

Ltd, Pune.

30058.61 38163.48 49362.37 19303.76

Source- Annual Reports (2011 to 2013) “All Selected Banks”

20

Graph No 3.1

The table& Graph no 3.1 explains that there is increase in the loans and

advances provided by Pimpri-Chinchwad Sahakari Bank with 1818.73 lakhs. The

Pavana Sahakari Bank has 10066.15 lakhs, Indrayani Co-operative Bank Ltd, Pune

has 1275.29 lakhs, Prerana Co-operative Bank Ltd, Pune has 3373.4 lakhs, Rajshree

Shahu Sahakari Bank Ltd, Pune has 8823.15 lakhs, Bhagini Nivedita Sahakari Bank

Ltd, Pune has 7698.52 lakhs, Janseva Sahakari Bank Ltd, Pune has 31081.51 lakhs,

Dharmvir Sambhaji Urban Co-operative Bank Ltd, Pimpri-Chinchwad has 1654.62

lakhs, and The Seva Vikas Co-operative Bank Ltd, Pune has 19303.76 lakhs increase

in their loans and advances. It is concluded that Janseva Sahakari Bank has highest

increase and Indrayani Co-operative Bank Ltd, Pune has lowest increase in loans and

advances.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Increase (+)

Year

Year

Year

21

3.6 The classification of progress of Pimpri-Chinchwad Sahakari

Bank Ltd, Pimpri.

Table& Graph No 3.2

(Rs. in Lakhs)

Particular 2010-11 2011-12 2012-13 Increase

(+)

No.of Branches 4 4 4 0

No. of Members 6090 6467 6843 753

Share Capital 863.01 895.68 932.37 69.36

Reserve & Other

fund 664.88 811.98 933.56 268.68

Deposit 11585.50 12300.79 13830.29 2244.79

Working capital 12899.37 13837.48 15131.55 2232.18

Profit 101.53 146.11 181.41 79.88

Audit Class A A A A

It has been observed through the above table that there is increase in the

number of members of banks from 2010 to 2013 i.e. 753. The share capital increased

0

2000

4000

6000

8000

10000

12000

14000

16000

No .ofBranches

No. ofMembers

ShareCapital

Reserve& Other

fund

Deposit Workingcapital

Profit

2010-11

2011-12

2012-13

Increase (+)

22

till 69.36 lakhs, the reserve and other fund raised till 268.68 lakhs. There is remarkable

increase in the bank‟s deposit of 2244.79 lakhs and working capital went up to

2232.18 lakhs. The profit of the bank was 79.88 lakhs. „A‟ class has been allotted to

the bank during auditing.

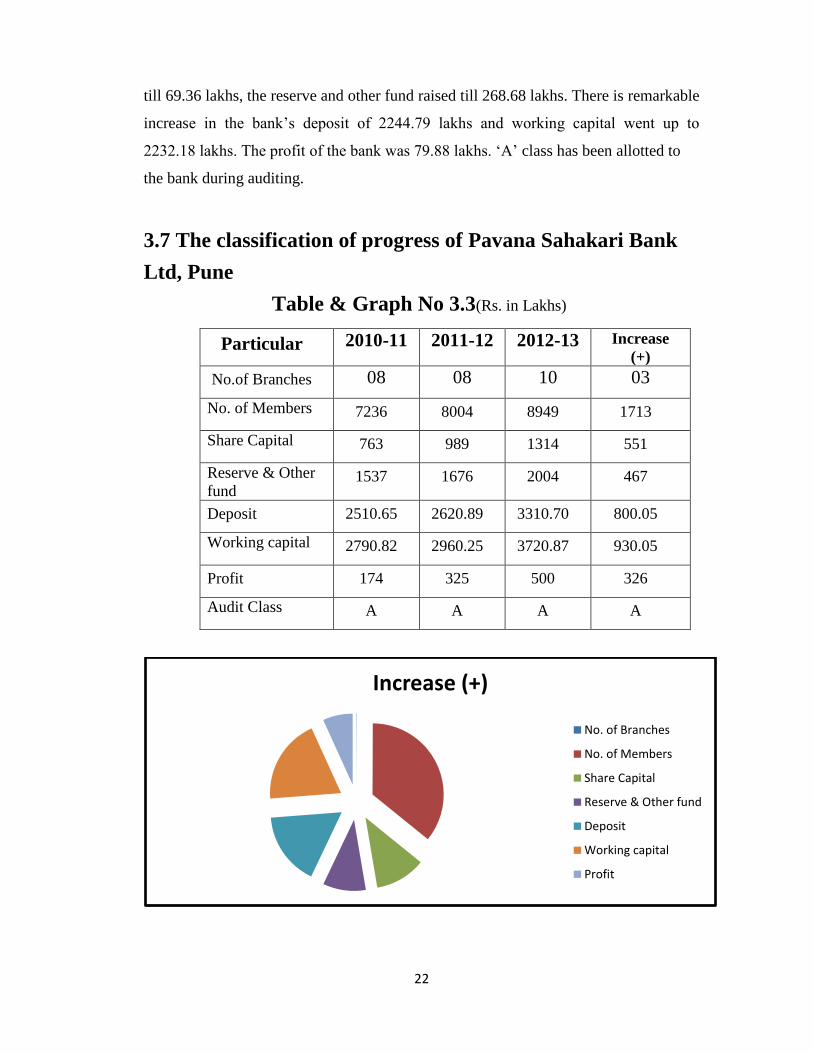

3.7 The classification of progress of Pavana Sahakari Bank

Ltd, Pune

Table & Graph No 3.3(Rs. in Lakhs)

Particular 2010-11 2011-12 2012-13 Increase

(+)

No.of Branches 08 08 10 03

No. of Members 7236 8004 8949 1713

Share Capital 763 989 1314 551

Reserve & Other

fund 1537 1676 2004 467

Deposit 2510.65 2620.89 3310.70 800.05

Working capital 2790.82 2960.25 3720.87 930.05

Profit 174 325 500 326

Audit Class A A A A

Increase (+)

No. of Branches

No. of Members

Share Capital

Reserve & Other fund

Deposit

Working capital

Profit

23

The table 3.3 shows that Pavana Sahakari Bank Ltd, Pune has increase in the

number of members i.e. 1713. The share capital went up to 551 lakhs and reserve and

other fund were 467 lakhs. The deposit rose up to 800.05 lakhs and working capital

was 930.05 lakhs. The profit that the bank received was 326 lakhs with maintaining

the class „A‟ of the audit.

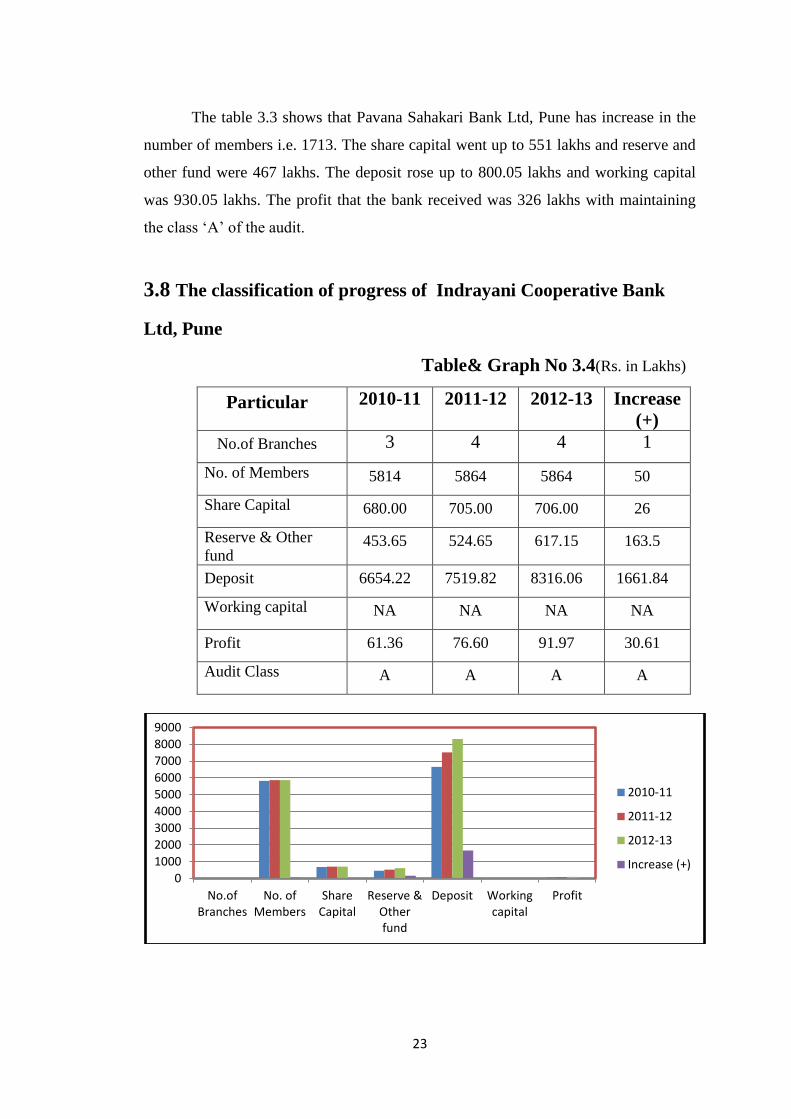

3.8 The classification of progress of Indrayani Cooperative Bank

Ltd, Pune

Table& Graph No 3.4(Rs. in Lakhs)

Particular 2010-11 2011-12 2012-13 Increase

(+)

No.of Branches 3 4 4 1

No. of Members 5814 5864 5864 50

Share Capital 680.00 705.00 706.00 26

Reserve & Other

fund 453.65 524.65 617.15 163.5

Deposit 6654.22 7519.82 8316.06 1661.84

Working capital NA NA NA NA

Profit 61.36 76.60 91.97 30.61

Audit Class A A A A

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

No.ofBranches

No. ofMembers

ShareCapital

Reserve &Otherfund

Deposit Workingcapital

Profit

2010-11

2011-12

2012-13

Increase (+)

24

Tableno 3.4 explains the progress of Indrayani Cooperative Bank Ltd, Pune.

There is little increase in the members of the banks during the years. The share capital

increased up to 26 lakhs and reserve and other funds went up to 163.5 lakhs. The

deposit that the bank received was 1661.84 lakhs. The profit of the bank was 30.61

with audit class „A‟.

3.9 The classification of progress of Prerana Co-operative Bank

Ltd, Pune

Table& Graph No 3.5(Rs. in Lakhs)

Particular 2010-11 2011-12 2012-13 Increase

(+)

No. of Branches 4 4 4 0

No. of Members 5326 5642 5900 574

Share Capital 388.31 463.17 525.86 137.55

Reserve & Other

fund 834.55 1112.36 1372.66 538.11

Deposit 14396.40 17280.89 19258.69 4862.29

Working capital 15985.45 19335.28 22028.25 6042.8

Profit 151.38 203.51 323.28 171.9

Audit Class A A A A

. There is increase in the number of members of the bank i.e. 574. There share

capital and reserve funds raised up to 137.55 and 538.11 lakhs respectively. The

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

No.ofBranches

No. ofMembers

ShareCapital

Reserve &Other fund

Deposit Workingcapital

Profit

2010-11

2011-12

2012-13

Increase (+)

25

deposit that the banks received was 4862.29 lakhs. The working capital of the bank

went up to 6042.8 lakhs with the profit of 171.9 lakhs. The bank maintained its

audit class of „A‟.

3.10 The classification of progress of Rajshree Shahu Sahakari

Bank Ltd, Pune

Table & Graph No 3.6(Rs. in Lakhs)

Particular 2010-11 2011-12 2012-13 Increase

(+)

No. of Branches 7 7 7 0

No. of Members 9753 10713 11509 1756

Share Capital 686.40 867.34 1020 333.6

Reserve & Other

fund 3905.14 4294.23 4583.80 678.66

Deposit 19309.44 23444.18 31349.14 12039.7

Working capital 25155.58 29731.40 38501.00 13345.42

Profit 261.04 345.58 526.49 265.45

Audit Class A A A A

Table No 3.5 shows that Rajshree Shahu Sahakari Bank has made remarkable

progress in its various sections. The number of the members went up to 1756 in the

0

10000

20000

30000

40000

50000

60000

70000

No. ofBranches

No. ofMembers

ShareCapital

Reserve &Otherfund

Deposit Workingcapital

Profit

Increase (+)

2012-13

2011-12

2010-11

26

given period. The share capital and reserve funds increased 333.6 and 678.66 lakhs

respectively. The deposit the bank received was 12039.7 lakhs and working capital

increased with 13345.42 respectively. The profit made by bank was 265.45 with „A‟

audit class.

3.11 The classification of progress of Bhagini Nivedita Sahakari

Bank Ltd, Pune

Table No 3.7(Rs. in Lakhs)

Particular 2010-11 2011-12 2012-13 Increase

(+)

No.of Branches 12 12 13 01 No. of Members 32041 34976 39125 7084

Share Capital 543.00 562.00 585.00 42

Reserve & Other fund 265.00 233.00 307.00 42

Deposit 42369 45193 52899 10530

Working capital NA NA NA NA

Profit 854.73 1027.77 1088.00 233.27

Audit Class A A A A

Table no 3.6 mentions the progress of Bhagini Nivedita Sahakari Bank Ltd,

Pune. There is increase in members of the bank with 7084. The share capital and

reserve funds were same i.e.42 and 42 lakhs respectively. The bank received the

deposit of 10530 lakhs and the profit was 233.27 lakhs with audit class „A‟.

3.12Janseva Sahakari Bank Ltd, Pune.

Table & Graph No 3.8(Rs. in Lakhs)

Particular 2010-11 2011-12 2012-13 Increase

(+)

No.of Branches 22 25 30 08 No. of Members 24257 28123 39923 15666

Share Capital 2277.11 2741.48 3300.91 1023.8

Reserve & Other

funds 8863.25 10147.32 10981.38 2118.13

Deposit 93172.76 110338.64 136957.37 43784.61

Working capital 108098.22 128988.08 157858.25 49760.03

Profit 1044.03 1212.89 2077.67 1033.64

Audit Class A A A A

27

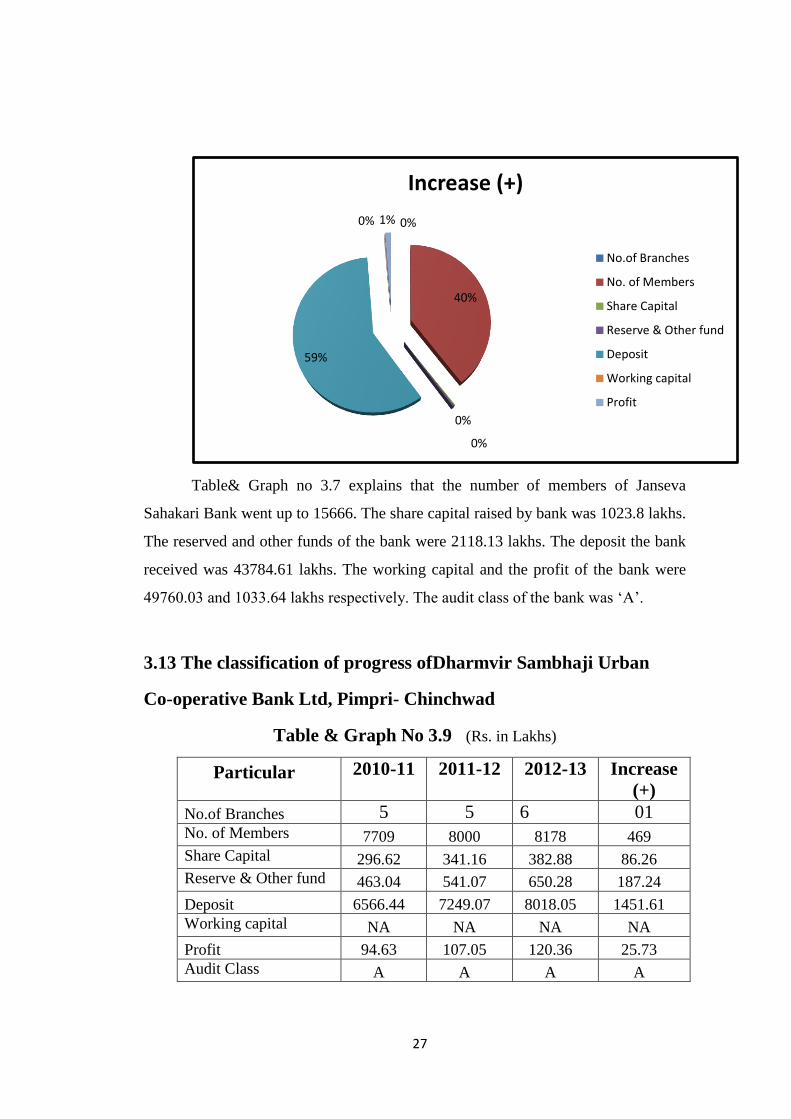

Table& Graph no 3.7 explains that the number of members of Janseva

Sahakari Bank went up to 15666. The share capital raised by bank was 1023.8 lakhs.

The reserved and other funds of the bank were 2118.13 lakhs. The deposit the bank

received was 43784.61 lakhs. The working capital and the profit of the bank were

49760.03 and 1033.64 lakhs respectively. The audit class of the bank was „A‟.

3.13 The classification of progress ofDharmvir Sambhaji Urban

Co-operative Bank Ltd, Pimpri- Chinchwad

Table & Graph No 3.9 (Rs. in Lakhs)

Particular 2010-11 2011-12 2012-13 Increase

(+)

No.of Branches 5 5 6 01 No. of Members 7709 8000 8178 469

Share Capital 296.62 341.16 382.88 86.26

Reserve & Other fund 463.04 541.07 650.28 187.24

Deposit 6566.44 7249.07 8018.05 1451.61

Working capital NA NA NA NA

Profit 94.63 107.05 120.36 25.73

Audit Class A A A A

0%

40%

0%

0%

59%

0% 1%

Increase (+)

No.of Branches

No. of Members

Share Capital

Reserve & Other fund

Deposit

Working capital

Profit

28

Table no 3.9 shows that Dharmvir Sambhaji Urban Co-operative Bank

Ltd, Pune has increase in the number of members i .e. 469. The share

capital and reserve and other funds were 86.26 and 187.26 lakhs

respectively. The banks had deposit of 1451.61 lakhs and profit of the

bank was 25.73 lakhs with audit class of „A‟ grade.

3.14The classification of progress of The Seva Vikas Co-operative

Bank Ltd, Pune.

Table & Graph No 3.10(Rs. in Lakhs)

Particular 2010-11 2011-12 2012-13 Increase

(+)

No.of Branches 13 15 24 11

No. of Members 9938 9938 10270 332

Share Capital 282.46 351.74 600.00 317.54

Reserve & Other fund 5276.60 6497.99 8420.80 3144.2

Deposit 41948.32 51951.97 66664.36 24716.04

Working capital 52450.17 64968.31 82404.94 29954.77

Profit 1263.91 1518.46 1805.29 541.38

Audit Class A A A A

0

50000

100000

150000

200000

250000

Increase (+)

2012-13

2011-12

2010-11

29

Table 3.10 shows that Seva Vikas Bank increased the members

with 332 in the given period. The share capital of the bank was 317.54

lakhs. Reserve and other fund were 3144.2 lakhs. The bank had

deposit of 24716.04 lakhs. The working capi tal and profit of the bank

rose up to 29954.77 and 541.38 lakhs respectively. The „A‟ audit class

has been allotted to the bank.

3.15 Conclusion

It can be concluded through the above information given in the tables that the

urban cooperative banks in Pune district have played an important role in fulfilling the

various financial needs of people living in urban areas. The large numbers of people

rely on these banks. These banks have a vision of national responsibility through co-

operative sector.

30

Chapter - IV

Conclusions and

Suggestions

31

Chapter-IV

Conclusions andSuggestions

4.1 Introduction

Co-operative banking system occupies an important position in the Indian financial

system. Co-operative banks were the first formal institutionsto be conceived and

developed to purvey credit to urban India. Thus far co-operatives banks have been a

key instrument offinancial inclusion in reaching out to the last mile in urban areas. The

researcher has made the following conclusions and suggestions based on the topic.

4.2 Conclusions

1) The percentage of priority sector advances and that of weaker sections of the

society are much higher than that stipulated by the RBI.

2) It is an endeavor of cooperative banks to grant loans on priority to low

income groups.

3) It has been observed during the study that the loans were granted against the

security of term deposits and life insurance policies in accordance with RBI

directives.

4) In accordance with guidelines issued by RBI, advances have been classified

by UCBs as standard, sub-standard, doubtful and loss assets.

5) The selected banks are located in urban area of Pune district, application for

loan and other formalities concerning to borrowing are very easy to

understand without complete help to the others.

6) It has been realized that most of the customers have little information about

the various schemes for loans and advances provided by UCBs

7) UCBs structure is exemplified by its pronounced focus on needs of small and

micro credit. It underwent phenomenal transformation since 1966.

Heterogeneity in size and space is the hallmark of UCBs. Unlike other

cooperative credit institutions, it is not dependent on external assistance.

32

8) The banks have not extended any finance to the members of the Directors

and their relatives, nor renewed and granted extensions to such loans.

9) Lack corporate governance, dual control, political interference, incidence of

financial weakness, lack of professionalism, etc. are said to be major

drawbacks of the sector. Sustained growth of this sector depends on speed

atwhich those weaknesses are corrected, efficient management and

efficacy of regulation.

10) Due to professional management, dynamic leadership the some Urban Co-

op. Banks made the financial inclusion in last a decade. This shows that the

urban cooperative banks were marching towards the national goals. Of

course, there are a number of deficiencies in the working of the banks such

as members' passive participation and the over dues of loans, and hence the

usefulness of the women's banks is to be provided in future than at present.

11) The urban cooperative banks have unique importance among the people

because they have fulfilled their needs in time.

12) Due to professional management, dynamic leadership the some Urban Co-

op. Banks made the financial inclusion in last a decade. This shows that the

urban cooperative banks were marching towards the national goals. Of

course, there are a number of deficiencies in the working of the banks such

as members' passive participation and the overdues of loans, and hence the

usefulness of the women's banks is to be provided in future than at present.

13) RBI stipulates that 60 per cent of the credit of urban cooperative banks

must flow to priority sector out of which 25 per cent should be for weaker

sections. The urban co-operative banks do not deny their social obligations

but the fact remains that for want of sufficient number of eligible

borrowers to fulfill the target of weaker section advances, these banks find

it difficult to adhere to these stipulations.

14) There seems to be controversy over the principle of 'Open Membership' in

respect of urban banks. Some banks have already become too large in

respect of membership and they feel that any further addition of members

would make them unmanageable.

33

15) Members of urban co-operative banks largely depend on the banks'

finances for acquiring their own houses. The urban banks have been doing

a lot for housing finance in cities and semi -urban places.

16) The democracy among urban banks is mainly found in the state where co-

operative movement is under-developed. The banks which are having high

over dues and are not self-reliant in their resources or mismanaged are

heading towards dormancy and such banks need rehabilitation.

17) It is concluded that Janseva Sahakari Bank has highest increase and

Indrayani Cooperative Bank Ltd, Pune has lowest increase in loans and

advances.

4.3 Suggestions

On the basis of the study made so far it is clear that the growth of urban co-operative

banks on the whole was satisfactory, though therewere imbalances in the various

factors. However, we can suggest some ofthe recommendations which can help to

improve the functioning ofurban co-operative banks.

1) The bank should provide staff with sufficient training. For improving its

performance, it has to concentrate on recovery performance, controlling

expenses, robust risk management practices and diversifying their

operations.

2) The due considerations should be given to the urban areas while opening

the branches.

3) Taking into the consideration the volume of members, deposits and loan

disbursement, the women's banks can divide their work into sub-sections

headed by the sectional head and the member of the board of directors.

The committees such as loan, administration,planning and development,

audit and inspection should beappointed. These sections can help to

speed up the working ofbanks.

4) The experienced and enlightened board of directors will make the

management efficient. Therefore, there is a need for training to board of

directors, as it is said, "It is not the good laws that run the good banking,

34

but it is good people who run the good/sound banks".

5) The refinance facilities of Nations Housing bank should be implemented

through the urban co-operative banks. Generally the loan advanced by

urban banks was for a period of three years. But the loans for

construction purpose require larger amount and longer period, and

therefore, the bank cannot make headway in this respect.

6) It will be wise to take some 'nursing steps' before the bank can go into

rehabilitation. The proper nursing measures can be taken when the

symptoms of financial weakness are seen, so that the bank will not

become weak.

7) There should be uniformity in the presentation of the annual reports of

the banks. The annual reports should give at least 5 years' progress report

in respect of membership, paid-up share capital, deposits, loans, over

dues, profit and loss, audit class, etc.. This will enable the members as

well as the general public to know the working of banks.

8) The 'loan cards' may be issued to the members. Such cards will enable

the member to know the duration, rate of interest and loans outstanding.

9) There should be an Apex bank for the urban co-operative banks to take

care of urban banks.

10) With a view to redressing the complaints of the members and the

customers/deposits the 'Suggestion Box' should be kept in the women's

banks. It was found that none of the banks was having this facility.

35

Bibliography

36

Bibliography

1) Bhole L M (2008) “financial institutions & markets”, tata McGraw-Hill publishing, New

Delhi.

2) Chitab Mukund M (2005) “Urban Cooperative Bank Mergers”, The Chartered

Accountant.

3) Choubey, B.N (1968) “Principals And Practice Of Cooperative Banking In India”, asia

publishing house.

4) Khan M.Y, financial management Tata Mc-graw hill

5) Money & Banking Center for Monitoring Indian Economy, 2004 & 2005

6) Narsimham Committee (NC) 2: Recommendations on Banking Sector Reforms 1998.

7) Ojha, P.D. Cooperative Sector: Some Critical Issue RBI Bulletin Feb ,1989

8) RBI, Report on Trend & Progress of Banking in India, 1989-90, 2004-05, 2005-06

9) Sharma O.P., Brief History Of Urban Cooperative Banks In India RBI monthly bulletin,

June 2008

10) Amit Basak (2009), “Performance Appraisal of Urban Cooperative Banks: A Case Study”,

IUP Journal of Accounting Research and Audit Practices. Year 2009.

11) Bhaskaran R and Praful Josh P (2000), “Non Performing Assets (NPAs) in Co-operative

Rural Financial System: A major challenge to rural development”, BIRD‟s Eye View

Dec.2000.

12) Chander Ramesh and Chandel Jai Kishan (2010), “Financial Viability of an Apex

Cooperative Credit Institution- A Case Study of the HARCO Bank”, Asia-Pacific Business

Review Vol. VI, No.2, April-June 2010, pp 61-70.

13) Gurcharan Singh and Sukhmani (2011) “An Analytical Study Of Productivity And

Profitability Of District Central Cooperative Banks In Punjab“, Journal on Banking Financial

services and Insurance Research, Vol. 1 Issue 3 (June2011), pp. 128-142.

14) Ratna and K.Nimbalkar (2011) “A Study of NPA‟s -Reference To Urban Co-operative

Bank”, Golden Research Thoughts, Vol.1, Issue.VI Dec 2011.

15) Dutta Uttam and Basak Amit (2008), “Appraisal of financial performance of urban co-

operative banks- a case study.” The Management Accountant, March 2008, pp.170-174.

16) Fulbag Singh and Balwinder Singh (2006), "Funds management in the central co-

operative banks of Punjab- an analysis of financial margin", The ICFAI Journal of

Management, Vol. 5, pp.74-80.

17) Kalyankar (1983), “Wilful Default in Loans of Co-operatives”, Indian Co-

operative Review, Volume XX No.2, New Delhi.

37

18) Devadas, Bhorali (1987), Co-operative Banking and Economic Development,

Deep &Deep Publications, Delhi

19) Singh, Fulbag; and Singh, Balwinder (2006), “Funds Management in Central

Cooperative Banks- Analysis of Financial Margin”, ICFAIJournal of

BankManagement, Volume 5, Issue 3, Hyderabad.

20) Dhanappa (2009), “Performance Evaluation of UCBs: A Case Study of

Kallappanna Awade Ichalkaranji Janata Sahakari Bank Ltd., Ichalkaranji”, Indian

Cooperative Review, Vol-XXXXVII, No-2, (Oct.), NCUI – New Delhi.

21) Heiko, Hesse; and Martin,Cihak (2007), “Co-operative Banks and Financial

Stability”, IMF Working Paper (Jan.), Washington, DC

22) Annual Reports (2011 to 2013) Pimpri-Chinchwad Sahakari Bank Ltd, Pimpri.

23) Annual Reports (2011 to 2013) Pavana Sahakari Bank Ltd, Pune

24) Annual Reports (2011 to 2013) Indrayani Cooperative Bank Ltd, Pune

25) Annual Reports (2011 to 2013) Prerana Co-operative Bank Ltd, Pune

26) Annual Reports (2011 to 2013) Rajshree Shahu Sahakari Bank Ltd, Pune

27) Annual Reports (2011 to 2013) Bhagini Nivedita Sahakari Bank Ltd, Pune

28) Annual Reports (2011 to 2013) Janseva Sahakari Bank Ltd, Pune.

29) Annual Reports (2011 to 2013) Dharmvir Sambhaji Urban Co-operative Bank

Ltd, Pimpri- Chinchwad

30) Annual Reports (2011 to 2013) The Seva Vikas Co-operative Bank Ltd, Pune.

.Magazines

1) Economics and Political Weekly. January, March1988.

2) YOJANA

3) SAMPADA

4) LOKRAJYA

5) LOKPRABHA

NewsPaper

1) Lokmat

2) Sakal

38

3) Loksatta

4) The Hindu

5) The IndianExpress

6) MaharashtraTimes

7) Pudhari

8) Times OfIndia

Websites

1) http://www.nibm.com

2) https://www.rbi.org.in

3) http://www.indiastat.com

39

PhotoGallery

40

Photo Gallery

The people are making their transitions in the bank.

The people are making inquiry about loans.

The employees are checking the forms.

41

A woman is submitting her application for account.

The employees are working in the bank.