a study on cash flow statement of - …docshare04.docshare.tips/files/31110/311107559.pdf · a...

TRANSCRIPT

A STUDY ON CASH FLOW STATEMENT

OF

TCS- ION Company

A project report submitted to the Punjab Technical University in partial fulfillment of therequirements for the award of the degree

of

Bachelor of Commerce (Professional)

(2013-2016)

Under the Guidance of Submitted By

Prof. (Department of Management Studies) B.com (P)

1328956

DAV College, BATHINDA

(Affiliated to PunjabI University, PATIALA)

Page | 1

TABLE OF CONTENTS

S.NO NAME OF TOPIC PAGE NO.

CERTIFICATE

DECLARATION

ACKNOWLEDGEMENT

EXECUTIVE SUMMARY

CHAPTER-1 COMPANY PROFILE

CHAPTER-2 INTRODUCTION TO TOPIC

CHAPTER-3 REVIEW OF LITERATURE

CHAPTER-4 RESEARCH METHODOLOGY

-RESEARCH OBJECTIVES

-SCOPE OF STUDY

-IMPORTANCE OF STUDY

-LIMITATIONS OF STUDY

CHAPTER-5 DATA ANALYSIS & INTERPRETATION

CHAPTER-6 FINDINGS & CONCLUSION

CHAPTER-7 RECOMMENDATION/

SUGGESTION

CHAPTER-8 BIBLIOGRAPHY

Page | 2

DECLARATION

I hereby declare that the project entitled “A STUDY ON CASH FLOW STATEMENT OF TCS-

iON ” Submitted in partial fulfillment of the requirements for award of the degree of B.B.A. at

DAV College Bathinda, Affiliated to Punjabi University, Patiala is an authentic work and has not

been submitted to any other University/Institute for award of any degree/diploma.

Name-

Page | 3

ACKNOWLEDGEMENT

Firstly I would like to express our immense gratitude towards our institution DAV College

Bathinda, which created a great platform to attain profound technical skills in the field of

B.com(P) thereby fulfilling our most cherished goal.

I would thank all the finance department of “TCS- iON“ specially Mr. Aman Kumar, and the

employees in the finance department for guiding me and helping me in successful completion of

the project.

I will also specifically thank to Prof., Department, Head, Dav college Bathinda for the (Internal

Guide) for extending his cooperation in doing this project.

I shall be failing in my duty if I do not acknowledge the affection, assistance, blessings an

moral support given to me by my family, specially my father who encouraged me and instilled

me the self belief and never to say die attitude.

Last but not the least, I will like to thank God for blessing me and giving me such a wonderful

opportunity.

Page | 4

CHAPTER-1

COMPANY PROFILE

Page | 5

TATA Consultancy Service

Type Public

Traded as BSE: 532540

NSE: TCS

BSE SENSEX Constituent

CNX Nifty Constituent

Industry IT services, IT consulting

Founded 1968

Founder J.R.D Tata

Headquarters Mumbai, Maharashtra, India

Area served Worldwide

Key people N Chandrasekaran

(CEO & MD)

Services IT, business consulting and outsourcing services

Revenue US$ 15.5 billion (2015)

Operating income US$ 3.7 billion (2015)

Profit US$ 3.5 billion (2015)

Total assets US$ 54.58 billion (2015)

Total equity US$ 84.35 billion (2015

Number of 335,620 (August 2015)

Page | 6

employees

Parent Tata Group

Subsidiaries iON Limited, TCS China, TRDDC, Computational Research

Laboratories

Slogan Experience certainty

Website www.tcs.com

Tata Consultancy Services Limited (TCS)is an Indian multinational information technology (IT)

service, consulting and business solutions company head quartered in Mumbai, Maharashtra. It is a

subsidiary of the Tata Group and operates in 46 countries.TCS is one of the largest Indian companies

by market capitalization ($80 billion). TCS is now placed among the ‘Big 4’ most valuable IT

services brands worldwide. In 2015, TCS is ranked 64th overall in the Forbes World's Most

Page | 7

Innovative Companies ranking, making it both the highest-ranked IT services company and the first

Indian company. It is the world's 10th largest IT services provider, measured by the revenues.

History:

2000 to present

On 25 August 2004, TCS became a publicly listed company.

In 2005, TCS became the first India-based IT services company to enter the bioinformatics market.

In 2006, TCS designed an ERP system for the Indian Railway Catering and Tourism Corporation.

In 2008, TCS's e-business activities were generating over US$500 million in annual revenues.

In 2008, TCS undertook an internal restructuring exercise which aimed to increase the company's

ability.

TCS entered the small and medium enterprises market for the first time in 2011, with cloud-based

offerings. On the last trading day of 2001 TCS overtook RIL to achieve the highest market

capitalization of any India-based company.

In the 2011/12 fiscal year, TCS achieved annual revenues of over US$10 billion for the first time.

In May 2013, TCS was awarded a six-year contract worth over ₹ 1100 crores to provide services to

the Indian Department of Posts.

In 2013, TCS moved from the 13th position to 10th position in the League of top 10 global IT

services companies

In July 2014, TCS became the first Indian company to cross the Rs 5 lakh crores mark in market

capitalization.

In Jan 2015, TCS ends RIL's 23-year run as most profitable firm.

Products and services:

TCS and its 67 subsidiaries provide a wide range of information technology-related products and

services including application development, business process outsourcing, capacity planning,

consulting, enterprise software, hardware sizing, payment processing, software management and

Page | 8

technology education services. Its established software products are TCS Banks and TCS

Master Craft.

Service lines:

TCS' services are currently organized into the following service lines (percentage of total TCS

revenues in the 2012-13 fiscal year generated by each respective service line is shown in

parentheses):

Application development and maintenance (43.80%) value;

Asset leverage solutions (2.70%);

Assurance services (7.70%);

Business process outsourcing (12.50%);

Consulting (2.00%);

Engineering and Industrial services (4.60%);

Enterprise solutions (15.20%); and

IT infrastructure services (11.50%).

Operations:

TCS have 230 offices across 46 countries and 147 delivery centers in 21 countries.At the same date

TCS had a total of 58 subsidiary companies.

Locations:

TCS has operations in the following locations:

India: Ahmedabad, Bangalore, Baroda, Bhubaneswar, Chennai, Coimbatore, Patna, Delhi, Gandhina

gar, Goa, Gurgaon,Guwahati, Hyderabad, Bhopal , Indore, Jamshedpur, Kochi, Kolkata, Lucknow ,

Kalyanpur, Mumbai, Nagpur, Noida, Puneand siliguri, Trivandrum

Africa: South Africa, Morocco

Asia

Page | 9

(excludingIndia): Bahrain, China, Israel, UAE, Hon

g kong, Indonesia, Japan, Malaysia, Philippines, Saudi Arabia, Singapore, South

Korea, Taiwan, Thailand, Qatar

Australia: Australia

Europe: Belgium, Denmark, Finland, France, Germany, Hungary, Iceland, Republic of

Ireland, Italy, Luxembourg,Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and United

Kingdom.

North America: Canada, Mexico and United States.

South America: Argentina, Brazil, Chile, Colombia, Ecuador, Peru and Uruguay.

Tata Research Development and Design Centre:

TCS established the first software research centre in India, the Tata Research Development and

Design Centre, in Pune, India in 1981. TRDDC undertakes research in Software

engineering, Process engineering and systems research. Research at TRDDC has also resulted in the

development of Sujal, a low-cost water purifier that can be manufactured using locally available

resources. TCS deployed thousands of these filters in the Indian Ocean Tsunami disaster of 2004 as

part of its relief activities. This product has been marketed in India as Tata swach, a low cost water

purifier.

Innovation Labs:

In 2007, TCS launched its co-innovation network, a network of innovation labs, start up alliances,

university research departments, and venture capitalists. In addition, TCS has 19 innovation labs

based in three countries.TCS' partners include Collabnet, Cassatt, academic institutions such

as IITs, Stanford, MIT, Carnegie Mellon and venture capitalists like Sequoia and Kleiner Perkins.

Employees:

TCS is one of the largest private sector employers in India, and the second-largest employer among

listed Indian companies (after Coal India Limited).

TCS had a total of over 335,620 employees as of October 2015, of which 31% were women. The

number of non-Indian nationals was 21,282 as at March 31, 2013 (7.7%).The employee costs for the

FY 2012-13 were US$4.38 billion, which was approx. 38% of the total revenue of the company for

Page | 10

that period. In the fiscal year 2012-13, TCS recruited a total of 69,728 new staff, of whom 59,276

were based in India and 10,452 were based in the rest of the world. In the same period, the rate of

attrition was 10.6%. The average age of a TCS employee is 28 years. The employee utilisation rate,

excluding trainees, for the FY 2012-13 was 82%. TCS was the fifth-largest United States visa

recipient in 2008 (after Infosys, CTS, Wipro and Mahindra Satyam).In 2012, the Tata group

companies, including TCS, were the second largest recipient of H-1B visas.

Subramaniam Ramadorai, former CEO of TCS, has written an autobiographical book about his

experiences in the company called The TCS Story...and beyond.

As of June 2014, TCS has over 300,000 employees. It is world's third largest IT employer behind

IBM and HP..

Class action lawsuit:

On 14 February 2006, U.S. law firm LieffCabraserHeimann& Bernstein, LLP filed a nationwide

class action lawsuit against Tata. In July 2013, judge Claudia Wilken of the U.S. District Court,

Northern District of California in Oakland, California, granted final approval to the settlement of the

lawsuit on behalf of all non-U.S. citizens employed by TCS within the state of California from 14

February 2002 to 30 June 2005. The workers claimed that they were forced to sign over their federal

and state tax refunds to their employer, as well as stating their Indian salaries were wrongfully

deducted from their U.S. pay. On February 22, 2013, the Company entered into an agreement to

settle for a sum of INR 16,163 lakhs ($29.75 million), this class action suit filed in a United States

Court relating to payment to employees on deputation.

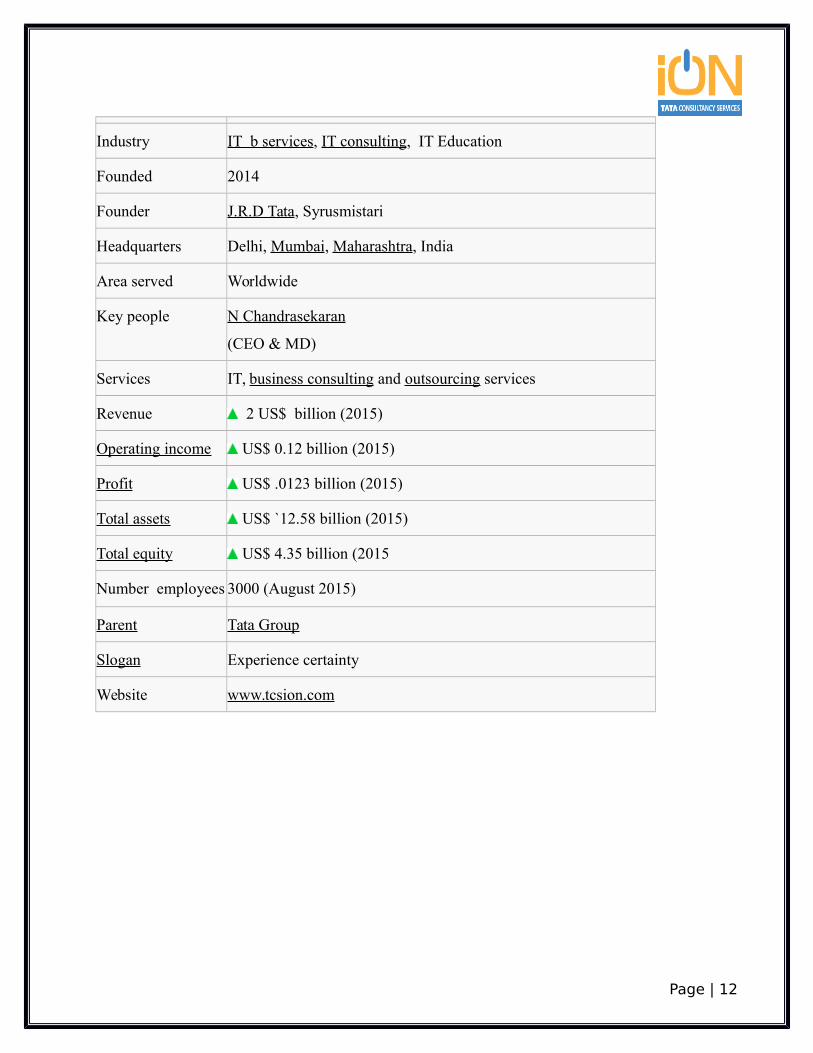

TATA Consultancy Service- iON

Type Public

Traded as NSE: TCS-iON

Page | 11

Industry IT b services, IT consulting, IT Education

Founded 2014

Founder J.R.D Tata, Syrusmistari

Headquarters Delhi, Mumbai, Maharashtra, India

Area served Worldwide

Key people N Chandrasekaran

(CEO & MD)

Services IT, business consulting and outsourcing services

Revenue 2 US$ billion (2015)

Operating income US$ 0.12 billion (2015)

Profit US$ .0123 billion (2015)

Total assets US$ `12.58 billion (2015)

Total equity US$ 4.35 billion (2015

Number employees 3000 (August 2015)

Parent Tata Group

Slogan Experience certainty

Website www.tcsion.com

Page | 12

TCS- iON

Now TCS is dealing in education and web development under the name of iON. TCS-iON

is at present, the most rapidly growing online web solutions company in India, providing IT

enabled services, consultation and outsourcing to companies spread in more than 165

countries across 7 continents. Their advanced delivery model blends technology practices

with functional expertise to help us improve our business processes and boost performance.

Their professional website design, Website development, logo design, Flash design, and

SEO services, among others, can go a long way in determining the success of your business.

Custom creation also includes, but is not limited to, incorporating images, video and other

interactive content into our site, apart from the usual text element

They offer their clients a repertoire of services like ecommerce website creation and portal

development, brand marketing on leading ad networks, digital marketing, web analytics and

much more. Their talented and experienced team of professionals comprise Web 2.0

development executives who offer advanced solutions for publishers and advertisers. They

Page | 13

create professional and dynamic pages for us using intelligent and smart practices.

They also double up as a digital marketing agency that serves leading brands, corporate

clients, as well as other players. Their cost-effective and customized web development, and

online media solutions are tailor-made to suit our specific needs and requirements. TCS-iON

offers us cutting edge services for website designing, development and internet marketing.

Their aim is to convert our “Creating Global Profeesionate’’.

Get Quality and Economic Web Services

TCS-iON is a web design and development company based in India .A fully integrated ITEsfirm, we provide world-class web design services to their global clientele spread across 7continents and major countries including USA, UK, Australia, and several throughout Asiaand Europe .

TCS-iON provides a wide range of highly cost-effective and customized web services tocompanies in varied industries such as entertainment, fashion, music, finance, environment,business, commerce, IT and telecommunications, travel and tourism, hospitality, education,etc. Their affordable web services are ideal for small, medium and large scaled private andcorporate organizations and also start-up businesses and aspiring entrepreneurs

TCS-iON is One-stop Shop for Comprehensive Web Services!

Page | 14

Their comprehensive list of web design and development services includes graphics design,corporate identity design and custom logo design services, custom web programming, blogcustomization and e-commerce solutions, Flash designs, search engine optimization servicesand much more.

.

Website Design Services:

At TCS iON India, creative talent meets technical expertise to produce smart and effective designs

with high appeal and usability value. They understand your need to be different from regular selling

or informative sites, increase visitor inflow and decrease bounce rates. Their professional web

Page | 15

designers employ fresh innovative ideas and advanced designing tools to produce optimized and

profit generative websites for you.

Their website design services are focused on producing uniquely appealing and result-oriented

websites for our specialized business. Leverage our quality web design services for dynamic

and flexible websites and enjoy maximum benefit.

IT - as - a Service:

The IT-as-a Service business model of iON a cloud based ERP solution was conceptualized by TCS

through close interactions with Small and Medium Businesses (SMB) across relevant stakeholders,

developing a deep understanding of their ICT consumption pattern and business challenges. An

innovative service model, iON uses emerging technologies like cloud computing and virtualization

to create a holistic, fit-for-purpose solution stack for SMBs integrating hardware, network, software

and services. And all of this is backed by business, technical and consulting services by iON. The

iON Cloud ERP Solution is highly modular, scalable and configurable giving SMBs the benefits of

increased efficiencies; faster go to market, predictability of technology as well as spend, IT talent on

call and better business results.

You gain from:

Integrated solutions:

We as a Cloud ERP Solution for SMBs offer single- window IT with a pre-integrated suite of

hardware, network, software and services. We ensure that your functions are digitized, automated

and connected. For example, if you are using a CRM solution along with a core ERP (e.g a

Manufacturing ERP) and have a document management system to organize supporting files and an

HRMS, we ensure that these solutions are connected and work as one. So for you, it is simply one IT

and not multiple applications. Integrated applications thus provide a comprehensive view of business

enabling better decisions.

Page | 16

Increased agility:

We bring in the agility to keep pace with changing processes or a new line of business. We help you

configure the processes to work as you currently do or the software recommends and allows you to

choose industry best practices based on your business parameters. iON gives you increased

convenience allowing you to perform various tasks from your mobile device, no matter where you

are. Being automatically compliant with statutory requirements, the solution ensures your company

is always audit ready and legally compliant.

A pay-as-you-use model:

Our model eliminates capital investment up front as we facilitate procurement of the IT

infrastructure and software on rent for the duration of the contract. Additionally, you only pay for the

number of users who actually use the software. Thus, you pay as you use on a monthly basis which

includes maintenance and training. Typically, with the iON Cloud ERP the ROI exceeds rental

within three months, when best practices are well followed.

Personalized solution:

Although iON is a cloud service for small and medium businesses, the software is configurable to

each business. You will always get the flavor of your business by picking and choosing what

processes you would need. Furthermore, the multilingual capability of the software allows you to

customize the solution label names to read in vernacular languages (like Hindi, Marathi, Tamil etc)

enabling users to learn and operate the solution with ease.

Automatic upgrades:

We continuously invest in our cloud based ERP solutions to incorporate best practices. The software

is constantly enriched based on user feedback and industry and statutory changes. You will get the

upgrades without disrupting your business operations or any additional cost. Being in perpetual beta

ensures that there is no technology obsolescence.

Enhanced Business Continuity

Page | 17

Our solution offers optimal performance in normal broadband connectivity along with a stringent

security mechanism to ensure your data privacy is maintained. The capacity of the iON Cloud ERP

solution grows with your increasing computing needs and reduces the need for IT staff. The solution

is resilient to failures as the service works from back-up data centers in the event of a disaster,

ensuring continuity of business operations.

PARTNER:

iON Partners play a key role in helping organisations of all sizes transform their businesses. We help

customers buy and implement solution that best fit their unique needs. iON Partners also provide

continuous support to customers after the implementation of the solution.

iON Sales and Implementation Partners

iON Sales and Implementation Partners (SIPs) are specially trained to help customers choose and

implement the best solution from a range of iON Education solution. SIPs have years of expertise in

the educational technology domain, and are well acquainted with the delivery model of our

solutions.

iON Channel Sales Partners

iON Channel Sales Partners have in-depth understanding of the education segment. The Channel

Sales Partners help customers across different education segments implement the most appropriate

iON solution.

A Manufacturing nervous system

Recording orders, sales and purchases would have little meaning unless they were connected. At the

heart of our manufacturing solution lies a production system that ensures that these are in sync. You

procure as much as you produce; and produce as much as you are able to sell. The goal is as simple

as keeping the lowest inventory.

At iON, we tend to make the complex manufacturing process look simple by connecting the

different parts of the operations. The software is organized into planning and execution. Production

plan for instance, would tell your operations to expect the right amount of sales, and then initiate the

right quantity of procurement. But what happens when the execution slips from what is planned?

Vigilant reports and dashboards would alert you in time.

Page | 18

Solution Stack:

Power your workforce performance:

Across industries, organizations are looking at new ways to manage their workforce and measure

performance through HR analytics, performance management systems, and social media.

The iON Human Capital Management (HCM) Solution is an integrated solution that helps you

effectively manage your employees and increase productivity across your workforce. You can align

employee goals with business objectives, cultivate employee skills, measure and reward

Page | 19

performance. iON HCM is a complete Enterprise Resource Planning (ERP) solution that automates

your human resource management and payroll processes with on-demand Business Intelligence (BI)

reporting capabilities and dashboards to help make quick decisions while maintaining statutory

complianc iON Human Resources Management Solution (HRMS) manages your recruitment and

performance evaluation processes, while also managing employee records and validating their

financial detailsiON Payroll Solution manages every stage of the payroll process, ensuring effective,

accurate payroll cycles and helps in faster decision making with on-demand business intelligence

(BI) reporting capabilities In addition, iON HCM has additional solution and services to further

enhance the productivity and learning environment in your organization iON Human Capital

Management (HCM) is delivered as a:

Managed Service: Manages the process end-to-end with the service delivered as an output.

Implementation Service: Delivers a completely configured system ready for end users to transact

and extract output on a day-to-day basis.

Page | 20

TCS in education:

Campus System:

iON Campus Management System comprises a suite of offerings, catering to seasonal academic

events, mapped to specific departments of an institution. Our solution facilitates the entire student

lifecycle management from enquiry to alumni. Offerings are integrated, yet modular in nature, which

can help automate certain functions within the institution depending on preference and suitability.

With Pre-built business processes and easy-to-configure solution capabilities, institutions can start

using the system with minimal implementation time and effort. To make the delivery process smooth

and effective for the end users, some of the modules are available in a Managed Services model as

well.

Page | 21

Assessment Management:

iON Assessment Management solution provides end-to-end services to configure and schedule

examinations starting from creating online and offline assessments to configuring attendance, hall

tickets, creating drives, as well as assigning a test center and exam shift to candidates. The solution

also manages the distribution of question papers, the Evaluation process, in addition to Results

Management and providing Support Service.

Digital evaluation:

iON Digital Evaluation solution enables evaluation of physical answer scripts made available in

electronic form. All the pages of the answer script and respective tabulated reports can be accessed

by the Evaluator, Supervisor and select members of the Institution. The solution combines ease of

manual evaluation coupled with flexibility, accuracy and efficacy of a computer.

The manual evaluation method is transformed into a digital process starting with electronic scanning

of answer scripts, where student details are masked with fictitious code, questions and relevant

marking scheme is uploaded into the solution, evaluators assigned with individual ID and password,

supervisor reviews or re-assigns evaluated scripts in case of discrepancies and finally the overall

status of answer scripts evaluated, reviewed and pending are known through the detailed Reports

functionality. Thus, iON Digital Evaluation solution from TCS addresses the major issues of the

current evaluation process like missing answer scripts in transit, human error in evaluation,

tabulation and award lists and most importantly struggling to announce results on time.

Demat Service:

iONDemat Services helps universities in leveraging IT to manage the entire lifecycle of issuing

certificates; starting from student record collection up to printing of certificates, along with digital

verification in a secured, organized, and cost-effective manner.

For student records that were maintained in physical registers before digitization, the services

include scanning and digitizing of the records along with secured storage and retrieval on-demand.

The solution makes use of digital encryption technologies for providing the highest degree of Data

Security and Integrity along with increased speed of certificate issuance and digital verification.

Page | 22

Communicator:

iON Communicator is the ultimate communication tool for Schools. Enabling the school

administration and teachers to connect with parents and students in real-time, from anywhere, iON

Communicator lets you communicate almost anything - news, alerts, calendar events, photographs,

activities or homework, from one, easy-to-use system. Giving you the flexibility to communicate the

way you want, it also includes a user-friendly smartphone app to access all the communications. Be

assured, that parents will never miss a communication, anymore.

Exam management:

TCS iON Exam Management Solution digitizes and automates University and Boards Examination

processes end-to-end, providing uncompromised 'Secrecy' in Examination Question Paper creation

and its distribution to various examination centers with significant reduction in administrative and

logistical overheads and costs. Increasing automation at every step like enrolling students for each

examination, scheduling of exams, exam centre management, allocating students to exam centers,

assigning subjects to faculties for question paper creation, alerts and notifications to various

stakeholders significantly reduces manual effort, schedule compliance failures and unforeseen errors.

Course management:

iON In-Course Assessment is designed to enable Institutions delivering Professional higher

education an opportunity to leverage Computer Based Testing to empower their teaching staff and

enhance the value delivered to students. iON In-Course Assessment allows for secure and

collaborative content development and vetting by faculty, seamless delivery of tests and capturing of

student responses and generation of multiple meaningful stakeholder specific reports on student

performance data.

Leading Exchange:

iON Learning Exchange is a collaborative Learning Platform designed to provide an incremental and

interactive learning environment to enable an Institute increase participant learning outcomes.

Powered by best-in-class Learning Management System (LMS), the learning spaces are enriched

with a suite of collaboration tools helping learners to learn from one another in a community

structure.

Page | 23

Empower Learning:

iON Learning Exchange empowers teachers with tools to personalize learning for every learner. A

teacher can design & host course catalogues, enlist students into learner communities and deliver

incremental learning material in an immersive way using video, audio, power point presentations

and a variety of SCORM Compliant learning aids. External links to world-class learning material in

the world wide web of learning enables the learner to dip into best resources on a subject or topic.

Teacher can co-share delivery responsibilities with Industry professionals or subject experts to

provide relevancy to curriculum and meet Industry employability expectations.

Personalized Feedback:

The power to conduct assessments after every learning module and provide personalised feedback in

an on-going manner helps learners to be ahead on the learning curve. Personalized mentoring can be

provided to each learner using Taxonomy and LOD tagging of assessments linked to feedback and

"incremental assist publishing". Results and Analytics of learner groups help teachers to undertake

remedial interventions for bringing parity in learning.

Peer learning:

Learning outcomes can be paced faster by enabling room for peer learning. iON Learning Exchange

is designed for community based learning where learners share their expertise and concerns using a

suite of collaboration tools including Forums, Blog, Debate, Surveys, Questions, Wiki and more.

Peer to peer benchmarking and peer speak provide the necessary impetus for pacing each other for

better outcomes.

Content Management System:

Create Courses for various topics and subjects engaging members of the Institution in a collaborative

learning environment. Populate course content in multiple modes (SCORM Compliant) and co-

create content repository, co-deliver curriculum, collaborate with industry and experts across

geographies to bring best of class value delivery to your class rooms.

Testing Engine:

Page | 24

Effectively create, schedule and track Assessments & Assignments, with multiple modes of response

submission (online/offline/both). Create Question Bank with numerous Question types (Multiple

choice multiple answer, Multiple choice single answer, Fill in the blank, True/False, Reading

comprehension) and enrich the tests by tagging them to Syllabus, Difficulty Level and Blooms

Taxonomy parameters. Create Question Papers based on Rule Engine, which fetches Questions

based on Question Types, Syllabus, Difficulty Level and Blooms Taxonomy Parameters.

Analytics Engine:

Analyze the assessment results on various parameters and provide dashboard for providing right

learning interventions to the participants of the Course to improve performance, hence closing the

learning-loop of 'Learn-Assess-Improve'.

Communication tools:

Leverage Communication features (Banner/ Multiple In-Focus & Notice-board items/ Notifications

via Email/SMS) to engage and inform members. All this with the flexibility to communicate with an

individual or with all the members of a Community on general broadcasts.

Page | 25

Page | 26

About Us

Page | 27

WEB PROGRAMMING

Every online business is different from other, even similar niche website. TCS-iON India

understands and respect individual clients needs and provide custom web programming

services to serve unique web requirements. Their team of qualified professionals uses strategic

planning and smart development process with quick operationally efficient and productive

website. Their aim is to provide smart and practical solutions from their website. TCS-iON

India’s custom website programming services cause dramatic and measureable growth in their

website.

FLASH DESIGN

Creative heads at TCS-iON India exploit Flash’s vector technology to produce, beautiful and

eye-catching designs for you. From Flash intros, banners logos and advertisements to full-

blown Flash websites, they give our website the interactive zing it desires. Their creative

Flash design services help transform our website into an effective communication interface.

Page | 28

LOGO DESIGN

TCS-iON India's logos are designed to successfully introduce your company to its

consumers and competitors. Their logos are stylish and aesthetic bearing superb color

scheme and graphical detailing that create long-lasting impressions. Their logo design

services give brand a simple, creative, and appealing quality capable of significant impact

on viewers. They guarantee quality logo design at minimal rates only at TCS-iON India.

LOGO DESIGNS

Branding that delivers your message.

The quickest way to increase the value of the company’s brand is with a well-integrated design

theme that is consistent across the web as well as on paper. A great logo is the keystone of this theme

and will attract the attention you want and deliver the sales that company needs.

Page | 29

Their logos don’t just create an identity; they create a connection with the audience they speak to and

differentiate the product or service being offered. Their logo and branding should allow their

customer to see you as providing a distinct solution to their unique problem. A logo speaks volumes

about what the company does, what its values are and what it can achieve. They make sure the logo

has as much personality as you do.

Logos that are designed by TCS-iON are as follows in march 2016 :-

SERVICES OF COMPANY

HTML5 & CSS3

At ION they offer PSD to CSS3 / JS / HTML5 services for their custom web design needs. We will

help us in getting the best web site design coded in HTML5 which is rich in structural functionality

Page | 30

and in CSS3 to enhance the presentation of your website’s content. Also HTML5/CSS3 expert takes

into account page’s loading time, SEO and web browsers compatibility

CMS

Their Content Management Systems (CMS) service revolutionizes the manner in which we manage

our online information and content – from web copy, published articles, press releases, audio/video

files, marketing brochures and other sales related assets. These applications will help us enterprise

store, maintain version control, publish content on the web and manage documents or digital assets.

Ecommerce Website Development

Ecommerce is a type of business that continues to grow every day. As more people get comfortable

with the Internet, more people are willing to make purchases and do business in this convenient way.

Therefore, ecommerce website design and development is increasingly important for any business

looking to be successful on the Internet. Let SuffesCom be our ecommerce solution provider and

they will be sure to have thousands of satisfied customers.

The focus for an ecommerce business will be a website incorporating product information and the

ability to purchase or make orders online. At Suffes.Com they use the latest database technology to

create ecommerce solutions for our new or existing business.

SEO

Search Engine Optimization (SEO) is a technical cum marketing technique with which SuffesCom

assists its clients to realize their dream of making their websites rank high in web searches. Search

Engine Optimization is a process through which websites are honed in order to make them visible to

Page | 31

online searchers. It’s worth pointing out that SEO is not a “magic bullet” that will necessarily drive

traffic and sales through the roof. SEO makes the website stand out

from the crowd, especially if your industry is highly competitive or if you want to attract a captive

audience for a popular keyword or keywords.

Our process involves the following crucial steps:

Research

Their research team makes a research using various secondary research tools to better understand the

requirements of the client. They prefer to seek assistance from the client by asking them various

questions related to their Business (read website), Target Audience, Strategic Keywords, etc. and

then they formulate the clear and measurable objective for the projects.

Page | 32

Analyze

After research they analyze the market potential and the present competition. They analyze the

market potential to ensure that the website is optimized in compliance with search engine guidelines

and they study the competition to identify the potential gap which needs to be addressed by you.

STRONG RELATIONSHIPS BETWEEN CLIENTS

One of their biggest priorities of all is close collaboration with their clients. Whatever the size of our

company or, indeed, your proposed project, they take steps here at TCS - iON to ensure that your

project is carefully tracked and monitored, from the initial user analysis to the final stage of usability

testing.

This is certainly a thoroughness of approach that has been appreciated by our clients down the years,

who have included business owners, consultants and team leaders alike. It gives you all the more

reason to contact TCS iONwhen your firm next requires a high quality software solution that brings

with it a significant ROI.

Why Choose TCS- iON?

iON is the company which gives the guarantee that we can help your business or organization to be

the best by improving your profitability and efficiency.

They understand that you could be concerned about why you should utilize our services for your

requirements. It is but natural that you logically put these questions to yourself. In an era where there

are many others out there offering similar services claiming similar advantages, it is worth

considering the following points. At SuffesCom we thoroughly undertake the following globally

acknowledged advanced practices.

Page | 33

Latest technologies

They deploy the latest technologies to meet your unmatched IT requirements.

Excellent support

They offer the most excellent support and dedicated service by a full fledged web experts team.

Best talent

They hire only the best talent available in the market and ensure that we utilize the cutting edge top

range methodologies and techniques to develop and execute your projects.

Productive work environment

They share a healthy work environment where our employees continually learn and mature as a

habitual practice.

Strict adherence to quality

Not only do we strictly adhere to the highest international level quality standards, but they regularly

communicate with our clients and keep them aware of the latest developments.

Satisfied Clientele

Needless to say, they have been able to develop a large list of satisfied clients in countries around the

globe. They are really proud to say that all this is due to our honest and equilateral commitment in

understanding the needs of our clients and providing them with precise solutions in accordance with

their individual requirements.

WHAT CLIENTS SAYS

Scott Adams

Remind people that profit is the difference between revenue and expense. This makes you look smart

and also significantly increases your chances.

Page | 34

Tasia

Amrinder worked diligently until he produced something I was happy with. We communicated over

Skype as often as needed and sometimes he’d work afterhours to get the revisions done before he

went home for the day. He’s very patient and that makes life easy when youre trying to produce

something wonderful.

Brandon Doe

Engineers like to solve problems. If there are no problems handily available, they will create their

own problems. That is a very known fact there.

THEIR SERVICES

Their e-commerce solutions are the best blend of:

Website Development

There are many variations of passages of LoremIpsum available, but the joy have suffered alteration

in some format, by injected humour.

Website Designing

There are many variations of passages of LoremIpsum available, but the joy have suffered alteration

in some format, by injected humor.

Internet Marketing

There are many variations of passages of LoremIpsum available, but the joy have suffered alteration

in some format, by injected humor.

Website Maintenance:

Let Your Website Speak For You... Manage It Like Your SALESMAN..!!

They offer you fast and efficient website maintenance services. They will update, enhance, backup

Page | 35

and repair our site quickly and efficiently, while you can go on running your business. They will

maintain the quality of our website, keeping it fresh for our return clients. If you need to add more

images, new banners, new calendar events, change the content of the site, backup

any important data, add new plug-in and functionality, let us do it for you .Their website

maintenance services are professional and affordable with quick turnaround and delivery times. They always

have custom solutions to website functionality problems at an affordable cost. They offer professional

help with any bugs or misfortunes which may happen to your site. Their site monitoring is effective

and professional. As soon as they receive maintenance requests, the sites get updated or fixed right

away. All the website development and maintenance is being performed in a secure way, with non-

disclosure of the passwords or any site information.

Some other Services they offer:

a) Phone Business Application Developmentb) iPhone Multimedia Application Developmentc) iPhone Internet Apps Developmentd) iPhone GPS Based Application Developmente) iPhone Entertainment Application Developmentf) iPhone Gaming Application Development.

.

Page | 36

INTRODUCTION TO THE

TOPIC

INTRODUCTION OF CASH FLOW STATEMENTEvery big and small firms performs cash transactions. Cash transaction refers to cash inflows and

outflows. Cash inflows and outflows help to review success, failure of a firm and its ability to meet

maturing debts. Such review and evaluation are possible if the statement of cash flow is prepared. Accounting standard Board (ASB) at international level in 1996 suggested every firm to publish the

statement of cash flow along with the final accounts. Since then the statement of cash flow is getting

more recognition than funds flow statement.

The statement that shows cash inflows and outflows of a firm for a specified period is called the cash

flow statement. Cash flow statement demonstrates where the cash has come during the period and

what the firm has done with the available cash. Therefore, cash flow statement shows a picture of

cash movement occurred in and out from a firm during a year in a summarized form. Cash flow

statement gives a picture of sources and applications of cash of a firm for a year.

Page | 37

DEFINITION:

“Cash Flow is the money that comes in and goes out of a company. It is the generation of

income and the payment of expenses. Cash inflows result from either the generation of revenue

through the selling of goods and services, money borrowed, or money earned through

investments.”

If more cash is coming into the company than leaving the company, you are experiencing positive

cash flow. But if more cash is leaving the company than coming into the company, then you are

experiencing negative cash flow. Keep in mind that just because you are experiencing negative cash

flow for the moment doesn't mean you are going to suffer a loss, because cash flow is dynamic. Cash

flow is reported on the company’s cash flow statement, which is also called a statement of cash

receipts and disbursements.

The cash flow statement was previously known as the flow of Cash statement. The cash flow

statement reflects a firm's liquidity.

The balance sheet is a snapshot of a firm's financial resources and obligations at a single point in

time, and the income statement summarizes a firm's financial transactions over an interval of time.

These two financial statements reflect the accrual basis accounting used by firms to match revenues

with the expenses associated with generating those revenues. The cash flow statement includes only

inflows and outflows of cash and cash equivalents; it excludes transactions that do not directly affect

cash receipts and payments. These non-cash transactions include depreciation or write-offs on bad

debts or credit losses to name a few. The cash flow statement is a cash basis report on three types of

financial activities: operating activities, investing activities, and financing activities. Non-cash

activities are usually reported in footnotes.

Important definitions As per Accounting Standard -3 (revised)

‘Cash’ comprises cash in hand and demand deposits with banks.

Page | 38

‘Cash equivalents’ are short term highly liquid investments that are readily convertible into known

amount of cash and which are subject to an insignificant risk of changes in value. Examples of cash

equivalents are

a) Treasury Bills

b) Commercial papers

c) Investment funds

d) Free Saving Account.

STRUCTURE OF CASH FLOW STATEMENT:

The cash flow statement is distinct from the income statement and balance sheet because it does not

include the amount of future incoming and outgoing cash that has been recorded on credit.

Therefore, cash is not the same as net income which, on the income statement and balance sheet,

includes cash sales and sales made on credit.

Cash flow activities

The cash flow statement is partitioned into three segments, namely:

1. cash flow resulting from operating activities;

2. cash flow resulting from investing activities;

3. cash flow resulting from financing activities.

The money coming into the business is called cash inflow, and money going out from the business is

called cash outflow.

Page | 39

Operating activities

Operating activities include the production, sales and delivery of the company's product as well as

collecting payment from its customers. This could include purchasing raw materials, building

inventory, advertising, and shipping the product.

Under IAS 7, operating cash flows include:

a. Receipts from the sale of goods or services

b. Receipts for the sale of loans, debt or equity instruments in a trading portfolio

c. Interest received on loans

d. Payments to suppliers for goods and services

e. Payments to employees or on behalf of employees

f. Interest payments (alternatively, this can be reported under financing activities in IAS 7)

g. Buying Merchandise

Items which are added back to [or subtracted from, as appropriate] the net income figure (which is

found on the Income Statement) to arrive at cash flows from operations generally include:

a. Depreciation (loss of tangible asset value over time)

b. Deferred tax

c. Amortization (loss of intangible asset value over time)

d. Any gains or losses associated with the sale of a non-current asset, because associated cash

flows do not belong in the operating section (unrealized gains/losses are also added back from

the income statement).

Page | 40

e. Dividends received

f. Revenue received from certain investing activities

Investing activities

These are the acquisition and disposal of long term assets such as land, building, plant machinery etcand other investments not included in cash equivalents. Cash flow from investing activitiesrepresents the extent to which expenditure has been made for resources intended to generate futureincome and cash flows.

Examples of Investing activities are

i. Purchase or Sale of an asset (assets can be land, building, equipment, marketable securities,

etc.)

ii. Loans made to suppliers or received from customers

iii. Payments related to mergers and acquisition.

Financing activities

Financing activities include the inflow of cash from investors such as banks and shareholders, as

well as the outflow of cash to shareholders as dividends as the company generates income. Other

activities which impact the long-term liabilities and equity of the company are also listed in the

financing activities section of the cash flow statement.

Under IAS 7,

a) Payments of dividends

b) Payments for repurchase of company shares

c) For non-profit organizations, receipts of donor-restricted cash that is limited to long-term

purposes

Page | 41

O

pe r

a ti n

g A

c ti vi t i

e s

C

as

h

In

flo

ws

C

as

h

Sa

les

C

as

h p

ur

cha

se

s

C

as

h

ou

tfl

ow

s

C

as

h

Sa

les

C

as

h p

ur

cha

se

s

Items under the financing activities section include:

a. Dividends paid

b. Sale or repurchase of the company's stock

c. Net borrowings

d. Payment of dividend tax

e. Repayment of debt principal, including capital leases.

Page | 42

I n

ve s

t in

g A

c ti vi t i

e s

C

as

h

in

flo

ws

S

a le

o f f

xe

d a ss e

t s

P u r

c ha s

e o f

f xe d

a ss e ts

C

as

h

ou

tfl

ow

s

S

a le

o f f

xe

d a ss e

t s

P u r

c ha s

e o f

f xe d

a ss e ts

F inanc ing Ac ti vi t ie s

Cash inflows

I s su e o f S ha r es f o r c as h

Repayment of loan

Cash outflows

I s su e o f S ha r es f o r c as h

Repayment of loan

Page | 43

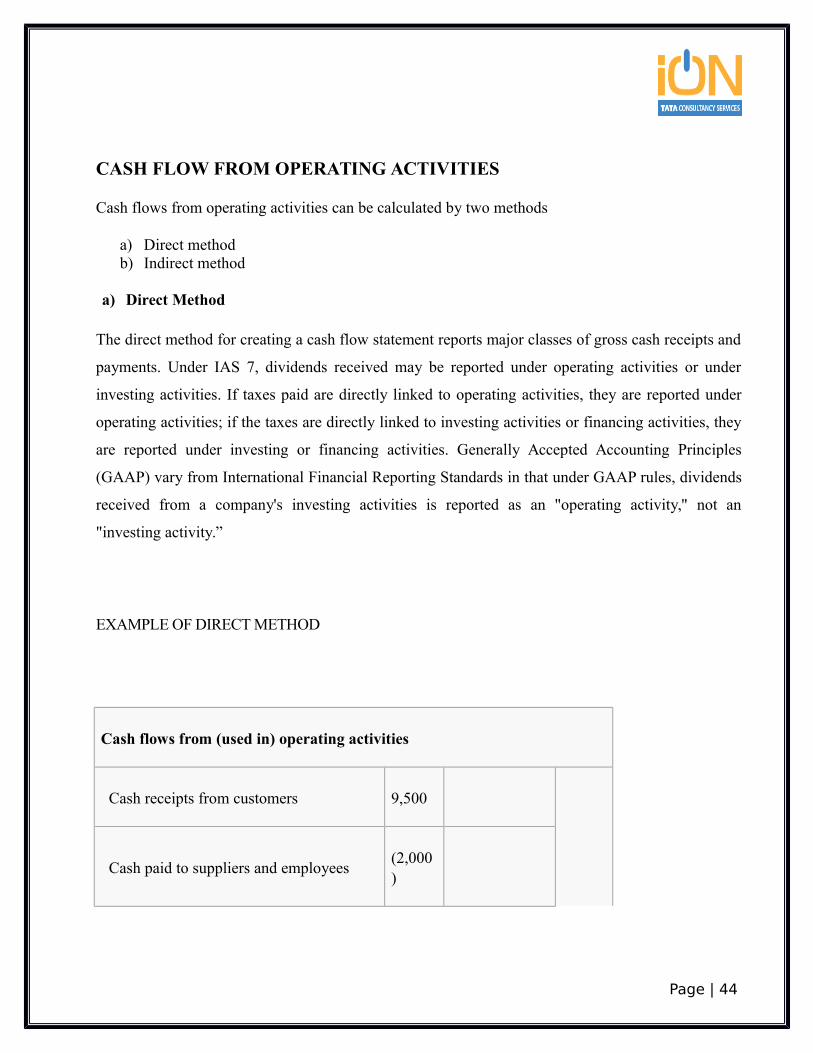

CASH FLOW FROM OPERATING ACTIVITIES

Cash flows from operating activities can be calculated by two methods

a) Direct methodb) Indirect method

a) Direct Method

The direct method for creating a cash flow statement reports major classes of gross cash receipts and

payments. Under IAS 7, dividends received may be reported under operating activities or under

investing activities. If taxes paid are directly linked to operating activities, they are reported under

operating activities; if the taxes are directly linked to investing activities or financing activities, they

are reported under investing or financing activities. Generally Accepted Accounting Principles

(GAAP) vary from International Financial Reporting Standards in that under GAAP rules, dividends

received from a company's investing activities is reported as an "operating activity," not an

"investing activity.”

EXAMPLE OF DIRECT METHOD

Cash flows from (used in) operating activities

Cash receipts from customers 9,500

Cash paid to suppliers and employees(2,000)

Page | 44

Cash generated from operations (sum) 7,500

Interest paid(2,000)

Income taxes paid(3,000)

Net cash flows from operating activities 2,500

Cash flows from (used in) investing activities

Proceeds from the sale of equipment 7,500

Dividends received 3,000

Net cash flows from investing activities 10,500

Cash flows from (used in) financing activities

Dividends paid(2,500)

Net cash flows used in financingactivities

(2,500)

.

Page | 45

Net increase in cash and cash equivalents 10,500

Cash and cash equivalents, beginning ofyear

1,000

Cash and cash equivalents, end of year $11,500

b) Indirect MethodThe indirect method uses net-income as a starting point, makes adjustments for all transactions for

non-cash items, then adjusts from all cash-based transactions. An increase in an asset account is

subtracted from net income, and an increase in a liability account is added back to net income. This

method converts accrual-basis net income (or loss) into cash flow by using a series of additions and

deductions.1. Decrease in non-cash current assets are added to net income2. Increase in non-cash current asset are subtracted from net income3. Increase in current liabilities are added to net income4. Decrease in current liabilities are subtracted from net income5. Expenses with no cash outflows are added back to net income (depreciation and/or amortization

expense are the only operating items that have no effect on cash flows in the period)6. Revenues with no cash inflows are subtracted from net income7. Non operating losses are added back to net income8. Non operating gains are subtracted from net income.

Rules (financing activities)

Finding the Cash Flows from Financing Activities is much more intuitive and needs little

explanation. Generally, the things to account for are financing activities:

a. Include as outflows, reductions of long term notes payable (as would represent the cash

repayment of debt on the balance sheet)

b. Or as inflows, the issuance of new notes payable

Page | 46

c. Include as outflows, all dividends paid by the entity to outside parties

d. Or as inflows, dividend payments received from outside parties

e. Include as outflows, the purchase of notes stocks or bonds

f. Or as inflows, the receipt of payments on such financing vehicles.

In the case of more advanced accounting situations, such as when dealing with subsidiaries, the

accountant must

a. Exclude intra-company dividend payments.

b. Exclude intra-company bond interest.

FORMAT OF CASH FLOW STATEMENTINDIRECT METHOD:

Page | 47

Particulars Amount Amount

Page | 48

Cash Flow from operating activities

Net profit as per profit and loss A/C

Add-Transfer to reserve

Add-proposed Dividend

Add- Interim dividend

Add- Provision for Taxation

Less-Refund of tax

Less- Extraordinary Items

Net profit before taxation and extraordinary items

Adjustments for non-cash and non- operating items

Items to be added:

Depreciation

Goodwill write off

Interest on borrowings

Loss on sale of investment

Loss on issue of shares/ debentures.

Items to be deducted:

Profit on sale of fixed asset

Profit on sale of investments

Rental income

Operating profit before working capital changes

Adjustments for change in current operating assets and liabilities:

Add- Decrease in current assets

Stock-in-trade

Page | 49

Bill receivable

Prepaid expenses

Add- Increase in current liabilities

Creditors

Bills payable

Outstanding expenses

Less- Increase in current assets

Stock-in-trade

Bill Receivable

Prepaid expenses

Less- Decrease in current liabilities

Creditors

Bills Payable

Outstanding Expenses

Cash generate from or used in operations before tax

Less- Income tax paid

Cash flow before extraordinary items

Less- Extraordinary items

Net cash flow from or used in operating activities

2.Cash flow from investing activities

Proceeds from sale of fixed assets

Proceeds from sale of investments

Interest or dividend received

Purchase of fixed assets

Page | 50

Purchase of Intangible asset like Goodwill

Net flow from (used in) investing activities

3.Cash flow from financing activities

Proceeds from issue of shares and debentures

Final dividend paid

Interim Dividend paid

Repayment of loans

Interest on debentures and loan paid

Redemption of debentures/ Preference shares

Net cash flow from (used in) Financing activities.

Net increase/ decrease in cash and cash equivalent(1+2+3)

Add- cash and cash equivalent in the beginning of the year

Cash in hand

Cash at bank(less Overdraft)

Short term deposits or Investments

Marketable Securities

Cash and cash equivalent in the end of the year

Cash in hand

Cash at bank (less Overdraft)

Short term deposits or investments

Marketable Securities

Notes:

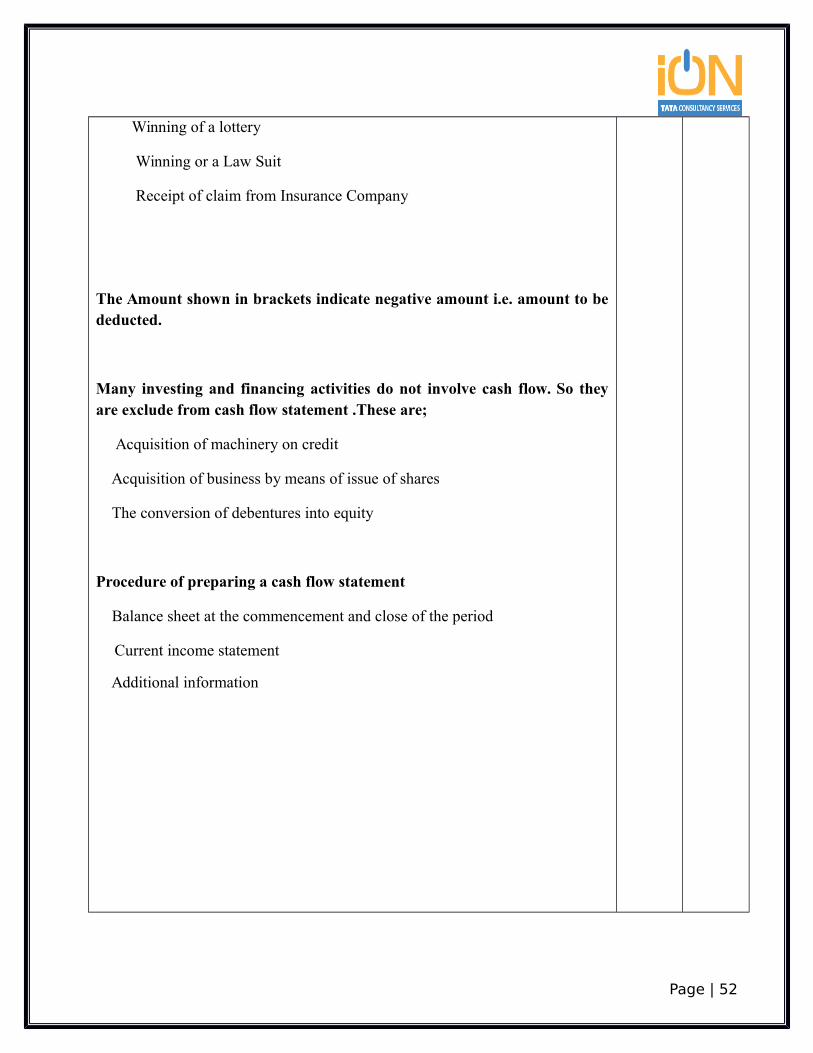

Examples of Extraordinary items are:

Page | 51

Winning of a lottery

Winning or a Law Suit

Receipt of claim from Insurance Company

The Amount shown in brackets indicate negative amount i.e. amount to bededucted.

Many investing and financing activities do not involve cash flow. So theyare exclude from cash flow statement .These are;

Acquisition of machinery on credit

Acquisition of business by means of issue of shares

The conversion of debentures into equity

Procedure of preparing a cash flow statement

Balance sheet at the commencement and close of the period

Current income statement

Additional information

Page | 52

NEED / IMPORTANCE / USES OF CASH FLOW STATEMENT

Therefore cash flow statement is important on the following grounds.

1. Cash flow statement helps to identify the sources from where cash inflows have arisen within a particular period and also shows the various activities where in the cash was utilized.

2. Cash flow statement is significant to management for proper cash planning and maintaining a proper matching between cash inflows and outflows.

3. Cash flow statement shows efficiency of a firm in generating cash inflows from its regular operations.

4. Cash flow statement reports the amount of cash used during the period in various long-term investing activities, such as purchase of fixed assets.

5. Cash flow statement reports the amount of cash received during the period through various financing activities, such as issue of shares, debentures and raising long-term loan.

6. Cash flow statement helps for appraisal of various capital investment programmers to determine their profitability and viability.

There are uses of cash flows on the following grounds.

External uses

1. To assess the ability of the firm to manage cash flows.2. To assess the ability of the firm to generate cash through its operations.3. To assess the ability of the firm its obligations and dividend policy.4. To assess the ability of the firm the effectiveness of firm to convert the revenue its cash.5. Estimating the company’s need for additional financing.

Internal uses

1. To assess liquidity.2. Determine if short term financing is necessary.3. To determine the dividend policy.4. To evaluate the investment and financial decision.

Page | 53

OBJECTIVES OF CASH FLOW STATEMENT

a) To find the liquidity position of the TCS-iON. For the availability cash and utilization of

the cash by the organization.b) It will help find to assess the company's ability to generate positive cash flows in the future

c) To assess its ability to meet its obligations to service loans, pay dividends etc.

d) To assess the effect on its finances of major transactions in the year.

e) To study the firms liquidity.

f) To learn about how company manage its cash & become such well recognized profitable

industry & if there is any problem arise then what steps taken by company.

g) To study the techniques used in organization.

h) To study methods & techniques use for cash flow analysis.

i) Meeting day to day cash requirement of firm.

Page | 54

EXECUTIVE SUMMARY(OVERVIEW)

Page | 55

INFORMATION ABOUT CASH FLOW STATEMENT

Cash flow is the money that comes in and goes out of a company. It is the generation of income and

the payment of expenses. Cash inflows result from either the generation of revenue through the

selling of goods and services, money borrowed, or money earned through investments.

If more cash is coming into the company than leaving the company, you are experiencing positive

cash flow. But if more cash is leaving the company than coming into the company, then you are

experiencing negative cash flow. Keep in mind that just because you are experiencing negative cash

flow for the moment doesn't mean you are going to suffer a loss, because cash flow is dynamic. Cash

flow is reported on the company's cash flow statement, which is also called a statement of cash

receipts and disbursements.

Complementing the balance sheet and income statement, the cash flow statement (CFS), a

mandatory part of a company's financial reports since 1987, records the amounts of cash and cash

equivalents entering and leaving a company. The CFS allows investors to understand how a

company's operations are running, where its money is coming from, and how it is being spent.

Here you will learn how the CFS is structured and how to use it as part of your analysis of a

company.

People and groups interested in cash flow statements include:

a. Accounting personnel, who need to know whether the organization will be able to cover

payroll and other immediate expenses

b. Potential lenders or creditors, who want a clear picture of a company's ability to repay

c. Potential investors, who need to judge whether the company is financially sound

d. Potential employees or contractors, who need to know whether the company will be able to

afford compensation

e. Shareholders of the business.

Page | 56

HISTORY AND VARIATIONS

Cash basis financial statements were very common before accrual basis financial statements. The

"flow of funds" statements of the past were cash flow statements.

In 1863, the Dowlais Iron Company had recovered from a business slump, but had no cash to invest

for a new blast furnace, despite having made a profit. To explain why there were no funds to invest,

the manager made a new financial statement that was called a comparison balance sheet, which

showed that the company was holding too much inventory. This new financial statement was the

genesis of cash flow statement that is used today.[6]

In the United States in 1973, the Financial Accounting Standards Board (FASB) defined rules that

made it mandatory under Generally Accepted Accounting Principles(US GAAP) to report sources

and uses of funds, but the definition of "funds" was not clear. Net working capital might be cash or

might be the difference between current assets and current liabilities. From the late 1970 to the mid-

1980s, the FASB discussed the usefulness of predicting future cash flows.[7] In 1987, FASB

Statement No. 95 (FAS 95) mandated that firms provide cash flow statements.[8] In 1992, the

International Accounting Standards Board issued International Accounting Standard 7 (IAS 7), Cash

Flow Statement, which became effective in 1994, mandating that firms provide cash flow statements

US GAAP and IAS 7 rules for cash flow statements are similar, but some of the differences are:

IAS 7 requires that the cash flow statement include changes in both cash and cash

equivalents. US GAAP permits using cash alone or cash and cash equivalents.

IAS 7 permits bank borrowings (overdraft) in certain countries to be included in cash

equivalents rather than being considered a part of financing activities.

IAS 7 allows interest paid to be included in operating activities or financing activities. US

GAAP requires that interest paid be included in operating activities.

US GAAP (FAS 95) requires that when the direct method is used to present the operating

activities of the cash flow statement, a supplemental schedule must also present a cash flow

Page | 57

statement using the indirect method. The IASC strongly recommends the direct method but

allows either method. The IASC considers the indirect method less clear to users of financial

statements. Cash flow statements are most commonly prepared using the indirect method, which

is not especially useful in projecting future cash flows.

The cash flow statement is partitioned into three segments, namely

1. cash flow resulting from operating activities;

2. cash flow resulting from investing activities;

3. cash flow resulting from financing activities.

The money coming into the business is called cash inflow, and money going out from the business is

called cash outflow.

Cash flow from operating activities can be calculated by two methods:

Direct Method

Indirect Method

TCS-ION uses the Indirect Method for calculating operating activities.

Page | 58

CHAPTER -2

REVIEW OF LITERATUREPage | 59

This chapter looks at the concept of cash flow statement as given by other authors and researchers

with importance to accountability, profit measurement, solvency, ambiguity, and disclosure and their

specific relevance for proper financial management of commercial company .one of the aim and

objectives of this dissertation was to review conceptual though and theoretical framework related to

cash flow analysis. Developing a critical review of cash flow literature and any related issues help

the researcher, manager and any potential reader to better understand the subject and also provide a

framework for data analysis. Governance as stated in the UK charity commission standard for good

governance code is “the systems and processes concerned with ensuring the overall direction,

effectiveness, supervision and accountability of an organization.”

This chapter begins with a clarified concept of cash flow as stated by the Financial Accounting

Standard Board (FASB) and also develop and update and utility of cash flow when managing

commercial activities. How the better knowledge on that topic helps in business decision making

nowadays.

Expansion of the reporting standard

The Financial Accounting Standards Board (FASB) introduced Statement of Financial Accounting

Standards No. 95 which is the Statement of Cash Flows in November 1987. The requirement of

Page | 60

FASB 95 regarding a full set of financial statements classified cash flow as the fourth required

financial statement (along with a balance sheet, income statement, and statement of retained

earnings). This statement established standards for cash flow reporting, and dated out the Accounting

Principles Board (APB) Opinion No. 19, Reporting Changes in Financial Position. In March 1971,

the APB Opinion No.19 gave chances to enterprises to report cash flow information in a statement of

changes in financial position commonly called a funds statement. During that time, there was no

formal or universally accepted definition to catalogue each statement even though the term “funds”

was not sufficiently defined (Alves et al 2008). Every single industry however had different funds

constitution to others since the statement referred to changes in funds. The term funds referred

sometimes to cash for some company meanwhile some used cash and short term investment and

some used quick asset, some used working capital. The relevance and the valuation of funds

statement has been recognized in most company but the lack of consistency in format and focus from

one firm to another was responsible of the main reason that the FASB obviously took up the matter

and with extensive commentary from accountants and any other interested parties, adopted the

standards espoused in FASB 95.it effectively took place in 1988 had not encouraged use of the world

“funds” because it had been stated with so much (Alves et al 2008).

Cash flow statement

A cash flow statement is an important indicator of financial health because it is possible for a

company to show profits while not having enough cash to sustain operations. It is a financial report

that shows to the user the source of a company's cash and how it was spent over a specific period of

time. A cash flow statement counters the ambiguity regarding a company's solvency that various

accrual accounting measures create. It also categorizes the sources and uses of cash to provide the

reader with an understanding of the amount of cash a company generates and uses in its operations,

as opposed to the amount of cash provided by sources outside the company, such as borrowed funds

or funds from stockholders. The cash flow statement also tells the reader how much money was

spent for items that do not appear on the income statement, such as loan repayments, long-term asset

purchases, and payment of cash dividends (Ryan 2007).

Requirements for cash flow statement

Page | 61

Thornton (2008) indicated that FASB 95 requires a statement of cash flows to classify cash receipts

and cash payments in accordance with the prescribe format whether they start from operating

activities, investing activities, or financing activities. The provisions given by FASB are as follows

on the presentation of cash flow statement are:

a. it provides that the cash flows statement should be prepared under either direct or indirect

method and provides examples of how to use each method when preparing statements.b. It also provides that under the core concept, cash is stated as “cash and cash equivalents”.

while cash is the most liquid assets within the asset portion of a company’s balance sheet

including currency and bank deposit, in the other hand cash equivalents are asset that are

ready to be converted into cash such as money market holding, short term government bond,

bills, marketable securities and commercial paper. Other sources of investments such as

stocks, bonds, futures contracts, and so forth are not considered cash.

Cash and profitability concepts

Cash

Cash is one of the most important aspects of running any large or small business. It is one of the

single most important reasons why many businesses fail regardless of how good the business is. The

physical aspect of cash can be any currency, coins on hand, bank balances, negotiable money and so

forth. Managing cash flow therefore is vitally important in the soft running, survival and success of a

business (Atrill P. 2004).

The use of some examples has illustrated how cash flow can make the difference between success

and failure. The meaning of failure in this case is insolvency that is, the company is unable to pay its

debts. The term bankrupt is sometimes used to describe that situation, even though it is only

individual who can be declared bankrupt. But sometimes both terms can be confusing.

Significance of non-cash transactions

Page | 62

Also known as profitability, non-cash transactions are not included in the statement of cash flows,

but often they need to be disclosed elsewhere in financial statements. Examples of these types of

transactions include:

a) Conversion of bonds to stockb) Acquisition of assets by assuming liabilities.

When there are some few of such transaction, it may be fairly recommended to include them on the

same page as the statement of cash flows but in a separate schedule at the bottom of the statement of

cash flows. Otherwise, the transactions may be reported elsewhere in the financial statements,

clearly referenced to the statement of cash flows. Some other transactions are generally reported in

combination with statement of cash; these include stock dividends, stock splits, and appropriation of

retained earnings.

Classifications/ Presentation of cash flow statement

Nearly all business transactions completed during the fiscal year impact cash flow in one way or

another, and in summary form they are factored into the year's cash flow statement. Exactly where

on the statement depends on the nature of the transaction. As noted, the three essential categories of

cash flow are operating activities, investing activities, and financing activities. The components of

each of these will be addressed separately.

Operating activities

Operating activities are the fundamental transactions that keep the business running. Most notably,

they include incoming revenue (also known as net income) from the sale of goods or services and

most kinds of outgoing payments. Cash flow from operating activities doesn't include principal paid

on or received from loans, and only includes transactions that were completed during the period.

This simply means that an operating transaction is not considered cash flow until the cash is actually

received or paid, as opposed to just being recorded as accounts receivable or payable. In general, if

an activity would appear on the company's income statement, it would be a candidate for the

operating section of the cash flow statement. Net changes in balance sheet categories from period to

period also represent cash flow; thus, a net decrease in accounts receivable from year to year

normally suggests an increase in cash flow for that period. Sometimes goods or services are paid for

Page | 63

prior to the period in which the benefit is matched to revenue (recognized). This results in a deferred

or prepaid expense. Items such as insurance premiums that are paid in advance of the coverage

period are classified as prepaid. Sometimes goods or services are received and used by the company

before they are paid for, such as telephone service or merchandise inventory. These items are called

accrued expenses, or payables, and are recognized on the income statement as an expense before the

cash flow occurs. Operating activities include the production, sales and delivery of the company's

product as well as collecting payment from its customers. This could include purchasing raw

materials, building inventory, advertising, and shipping the product.

Under IAS 7, operating cash flows include:

a) Receipts from the sale of goods or servicesb) Receipts for the sale of loans, debt or equity instruments in a trading portfolioc) Interest received on loansd) Dividends received on equity securitiese) Payments to suppliers for goods and servicesf) Payments to employees or on behalf of employeesg) Interest payments (alternatively, this can be reported under financing activities in IAS 7, and

US GAAP)

Items which are added back to [or subtracted from, as appropriate] the net income figure (which is

found on the Income Statement) to arrive at cash flows from operations generally include:

a. Depreciation (decline in value of assets and, loss of tangible asset value over time)b. Deferred taxc. Amortization (loss of intangible asset value over time)

Any gains or losses associated with the sale of a non-current asset, because associated cash flows do

not belong in the operating section.(unrealized gains/losses are also added back from the income

statement

Investing activities

Investment activities represent the cash flow from the purchase of long term assets ( such as property

and equipment) required to make or sell goods and services. Investment activities also include

purchases of stocks or other securities, loans made to other businesses. A major issue that potential

investors have with the investing activities section is that the money listed here represents activities

Page | 64

paid for in cash. In other words, it includes only the principal or book value of the investment. So, if

an example of company that wanted to purchase $5 million dollars worth of equipment with only $1

million cash and $4 million in financing, only the $1 million will show up under investing activities.

Interest and depreciation are classified as operating cash flow, as are net gains or losses on

investments. Because of these distinctions, cash flow from investment activities is typically more

complex to calculate than that from other categories. Examples of investing activities are

a) Purchase or Sale of an asset (assets can be land, building, equipment, marketable securities,

etc.)b) Loans made to suppliers or received from customers

Financing activities.

Financing activities consist of transactions affecting a company's liabilities and shareholder equity.

Mainly involving how the company obtains capital and enhances the value of its stock, they include

such things as issuing bonds, payments on debt, paying dividends, and issuing and buying back

stock.

Financing activities include the inflow of cash from investors such as banks and shareholders, as

well as the outflow of cash to shareholders as dividends as the company generates income. Other

activities which impact the long-term liabilities and equity of the company are also listed in the

financing activities section of the cash flow statement.

Under IAS 7,

a) Proceeds from issuing short-term or long-term debtb) Payments of dividendsc) Payments for repurchase of company sharesd) Repayment of debt principal, including capital leasese) For non-profit organizations, receipts of donor-restricted cash that is limited to long-term