a value proposition for ltci

TRANSCRIPT

ACTUARIAL

A VALUE PROPOSITIONfor LTCI

Session 33: February 28, 2006Session Producer:

Steve Schoonveld, FSA, MAAAActuarial Advisor, Ernst & Young

2

ACTUARIAL

PANELISTS

• Claude Thau, FSA, MAAA, President, Thau, Inc.

• William Dreher, FSA, MAAA, Managing Director, Compensation Strategies, Inc.

• Steve Schoonveld, FSA, MAAA, Actuarial Advisor, Ernst & Young LLP

ACTUARIAL

“A Value Proposition for LTC Insurance”

Session 33Tuesday, February 28, 2006

Steve Schoonveld

Ernst & Young, LLP

4

ACTUARIAL

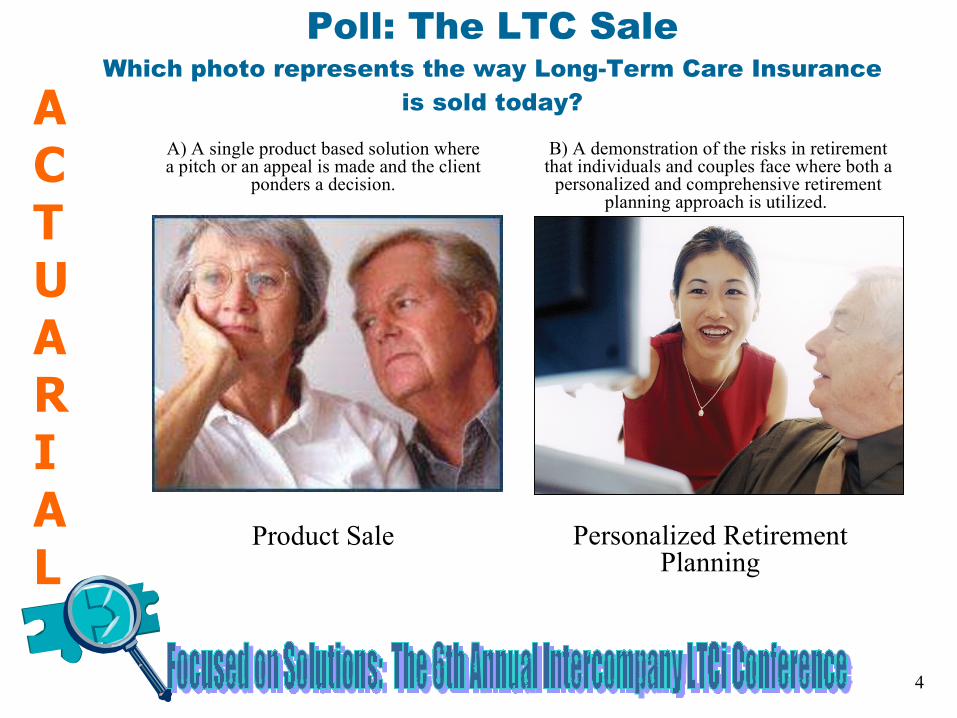

Poll: The LTC SaleWhich photo represents the way Long-Term Care Insurance

is sold today?

A) A single product based solution where a pitch or an appeal is made and the client

ponders a decision.

B) A demonstration of the risks in retirement that individuals and couples face where both a

personalized and comprehensive retirement planning approach is utilized.

Product Sale Personalized Retirement Planning

5

ACTUARIAL

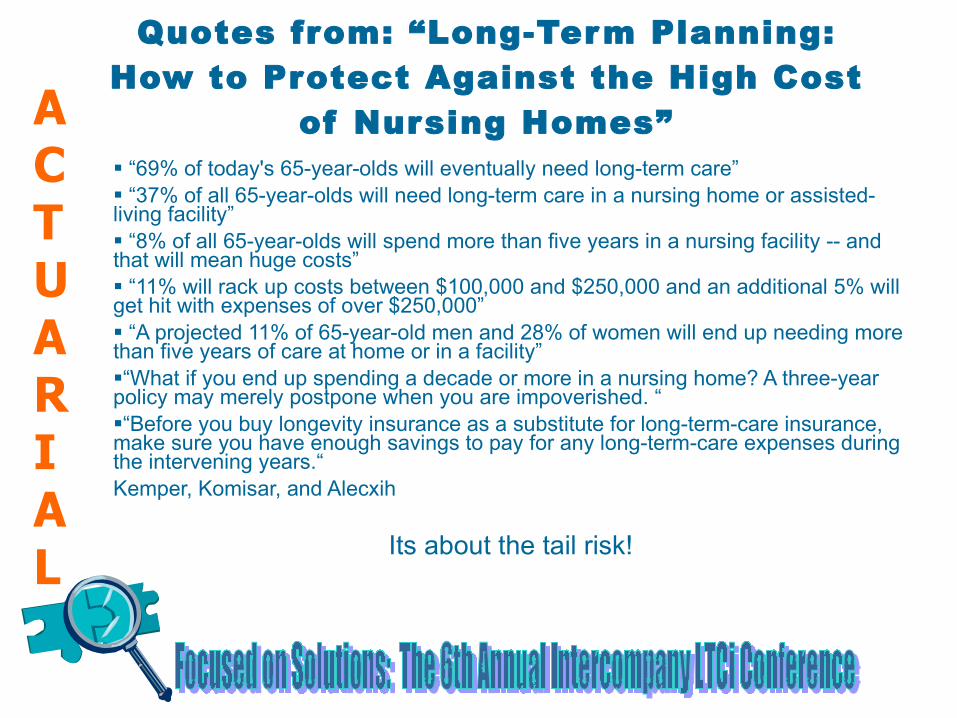

Long-Term Planning: How to Protect Against the High Cost of Nursing Homes

By Jonathan Clements

02/22/2006The Wall Street Journal(Copyright (c) 2006, Dow Jones & Company, Inc.)

ACTUARIAL

Quotes from: “Long-Term Planning: How to Protect Against the High Cost

of Nursing Homes” “69% of today's 65-year-olds will eventually need long-term care” “37% of all 65-year-olds will need long-term care in a nursing home or assisted-living facility” “8% of all 65-year-olds will spend more than five years in a nursing facility -- and that will mean huge costs” “11% will rack up costs between $100,000 and $250,000 and an additional 5% will get hit with expenses of over $250,000” “A projected 11% of 65-year-old men and 28% of women will end up needing more than five years of care at home or in a facility”“What if you end up spending a decade or more in a nursing home? A three-year policy may merely postpone when you are impoverished. “ “Before you buy longevity insurance as a substitute for long-term-care insurance, make sure you have enough savings to pay for any long-term-care expenses during the intervening years.“Kemper, Komisar, and Alecxih

Its about the tail risk!

7

ACTUARIAL

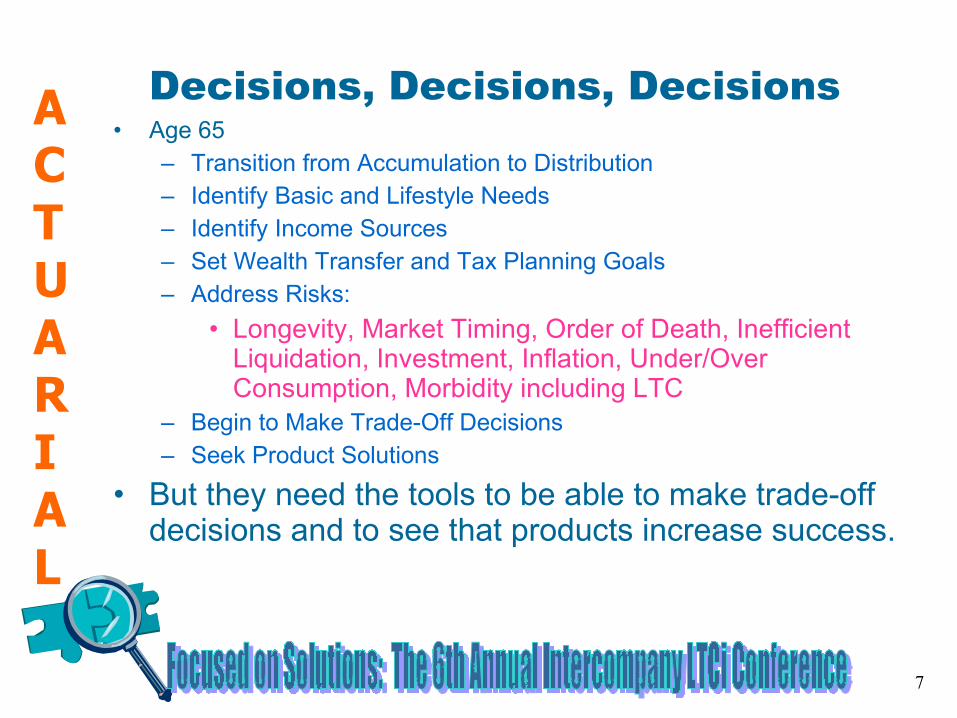

• Age 65– Transition from Accumulation to Distribution– Identify Basic and Lifestyle Needs– Identify Income Sources– Set Wealth Transfer and Tax Planning Goals– Address Risks:

• Longevity, Market Timing, Order of Death, Inefficient Liquidation, Investment, Inflation, Under/Over Consumption, Morbidity including LTC

– Begin to Make Trade-Off Decisions– Seek Product Solutions

• But they need the tools to be able to make trade-off decisions and to see that products increase success.

Decisions, Decisions, Decisions

8

ACTUARIAL

• Meet basic needs• Maintain a desired lifestyle• Provide inheritance• Minimize risk exposures• Avoid spousal impoverishment• Efficient tax planning• Ability to adjust plans when needed

• In other words, Success, which equals having met goals and at least $1 left at last death

Retirement Goals

9

ACTUARIAL

• Fixed Rate of Return • Systematic Withdrawal Rate• Target Accumulation or Target Savings• Target Age of Death• Simplistic Order of Death• Single Product Solution – if any• Provides a Yes/No Answer• Lacks a Personal Focus and has Limited

Distribution Phase Planning

Characteristics of Common Retirement Decision Tools

10

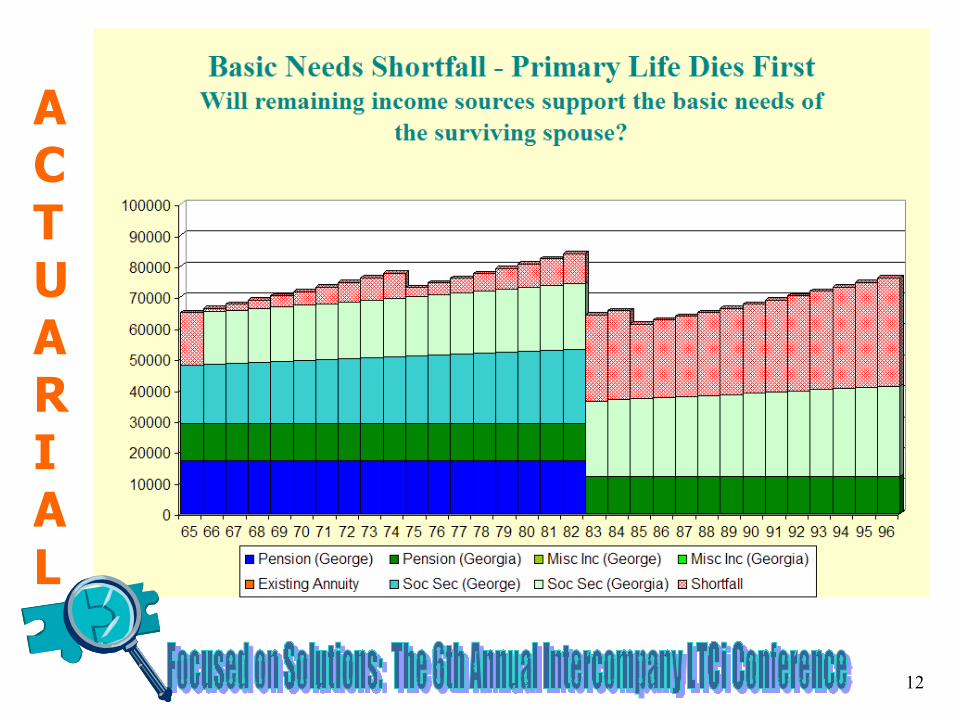

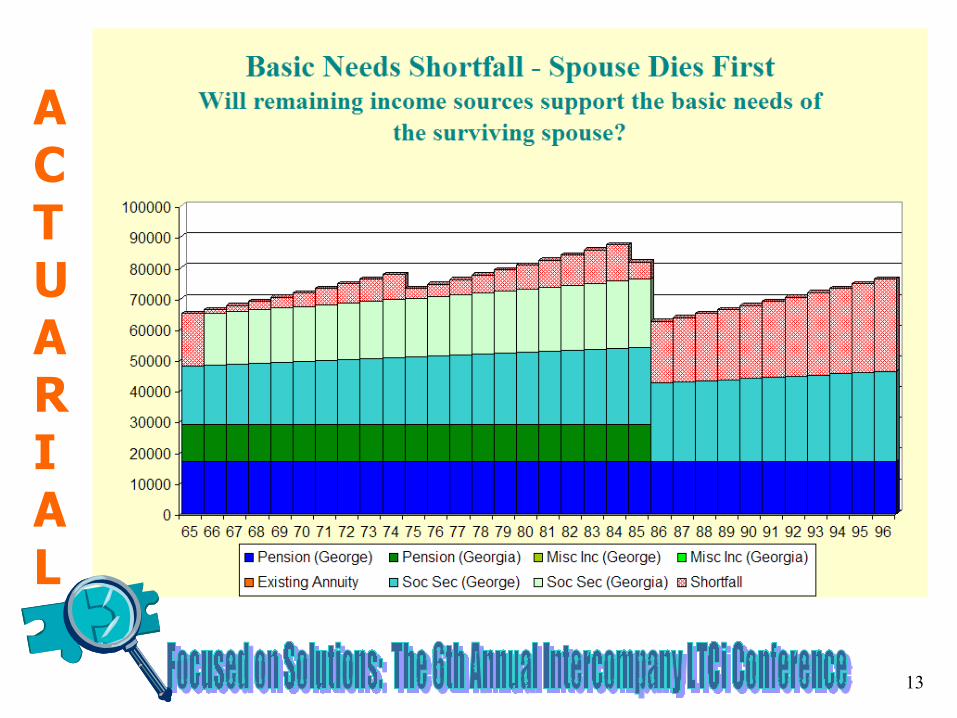

ACTUARIAL

Sample Couple

Spousal Impoverishment,

Outliving Assets

Sound Transition Approach

Concerns/Needs:

Value of HomeWealth Transfer Goal

70K per yearLifestyle Needs

65K per yearBasic Needs

550KValue of Home

George 17K,

Georgia 12K

Pension Income

George 19K,

Georgia 17K

Soc Sec Income

$400K + 50K savingsAssets

65, 64Age

George and Georgia Smith (retired)

11

ACTUARIAL

12

ACTUARIAL

13

ACTUARIAL

14

ACTUARIAL

The average planner approach does not capture the risk nor inform.

15

ACTUARIAL

Randomizing mortality, rate of return and inflation.

16

ACTUARIAL

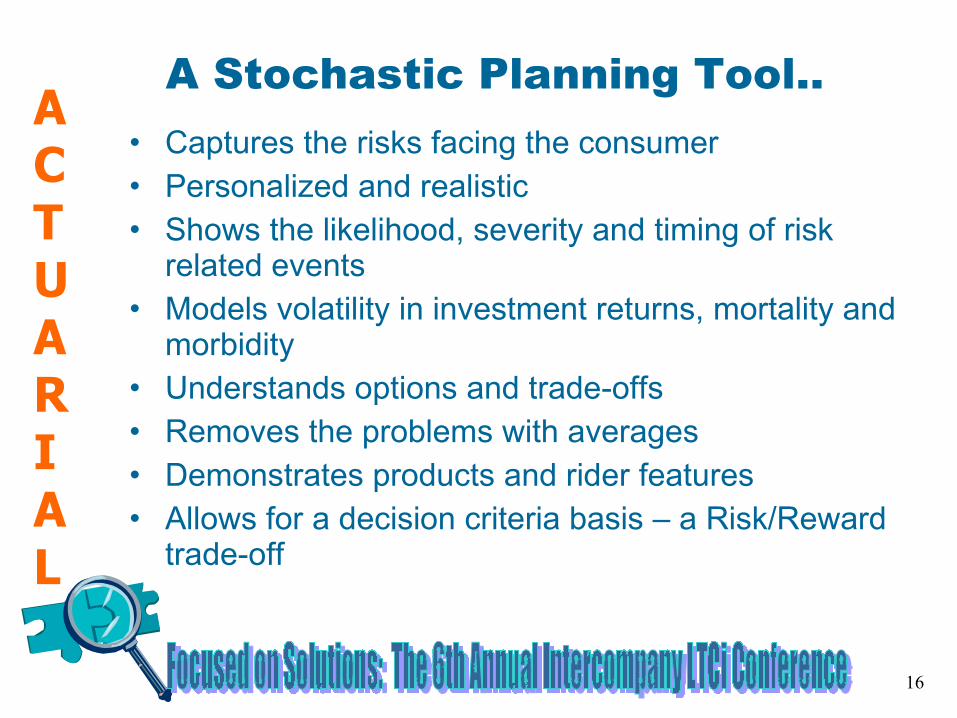

• Captures the risks facing the consumer• Personalized and realistic• Shows the likelihood, severity and timing of risk

related events• Models volatility in investment returns, mortality and

morbidity• Understands options and trade-offs • Removes the problems with averages• Demonstrates products and rider features• Allows for a decision criteria basis – a Risk/Reward

trade-off

A Stochastic Planning Tool..

17

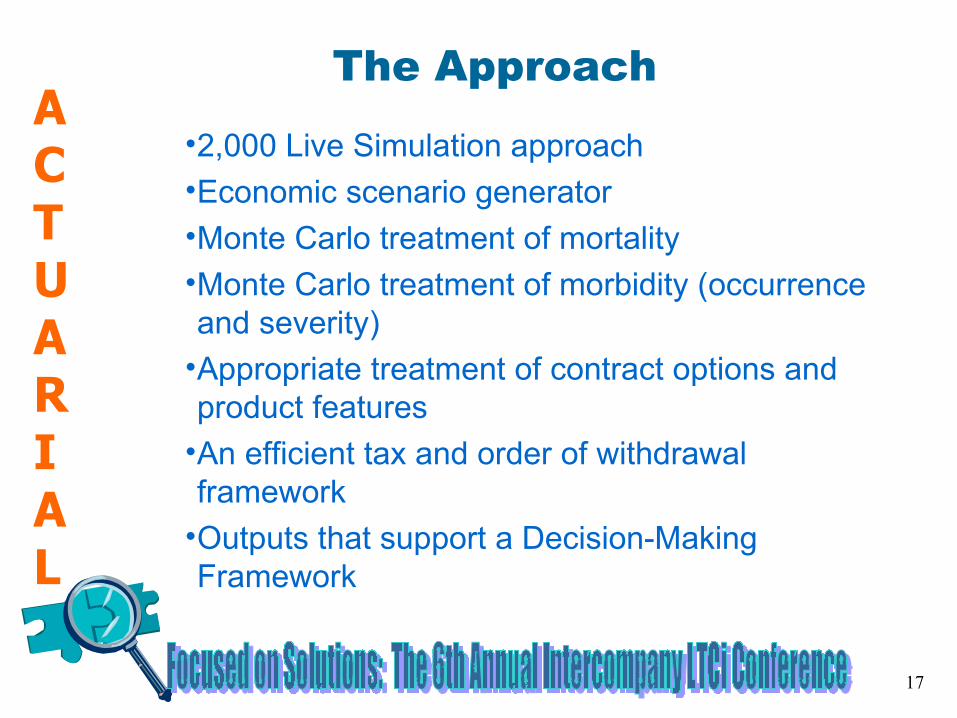

ACTUARIAL

The Approach

•2,000 Live Simulation approach•Economic scenario generator•Monte Carlo treatment of mortality•Monte Carlo treatment of morbidity (occurrence and severity)

•Appropriate treatment of contract options and product features

•An efficient tax and order of withdrawal framework

•Outputs that support a Decision-Making Framework

18

ACTUARIAL

Here are 50 of the 2,000 scenarios.

19

ACTUARIAL

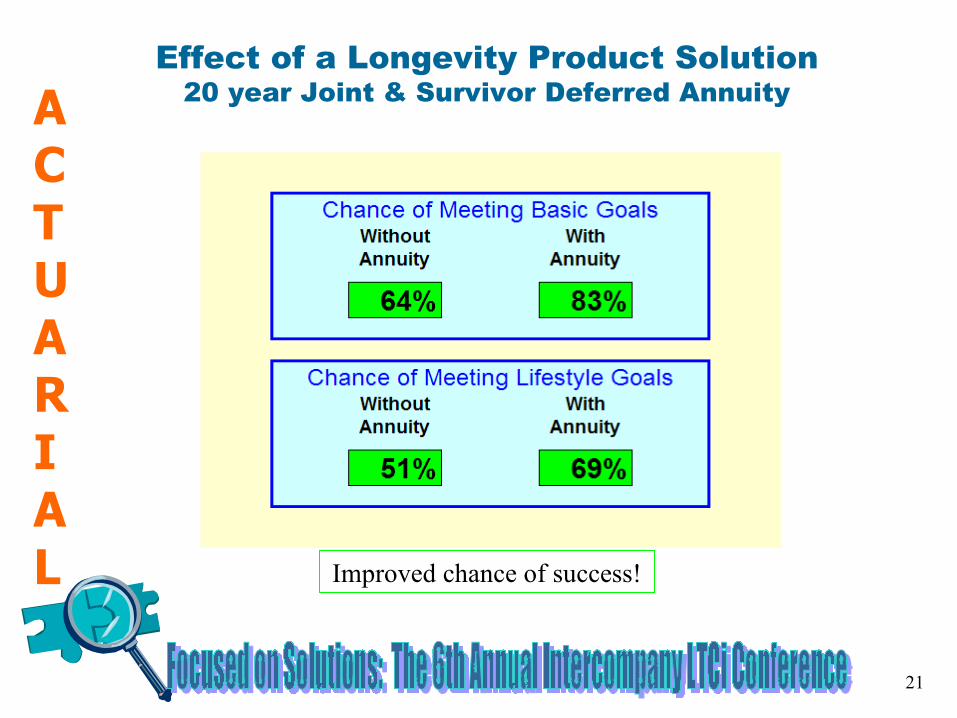

Success Rates No Product Solution

Success = meeting all retirement goals with at least a dollar upon the last death.

20

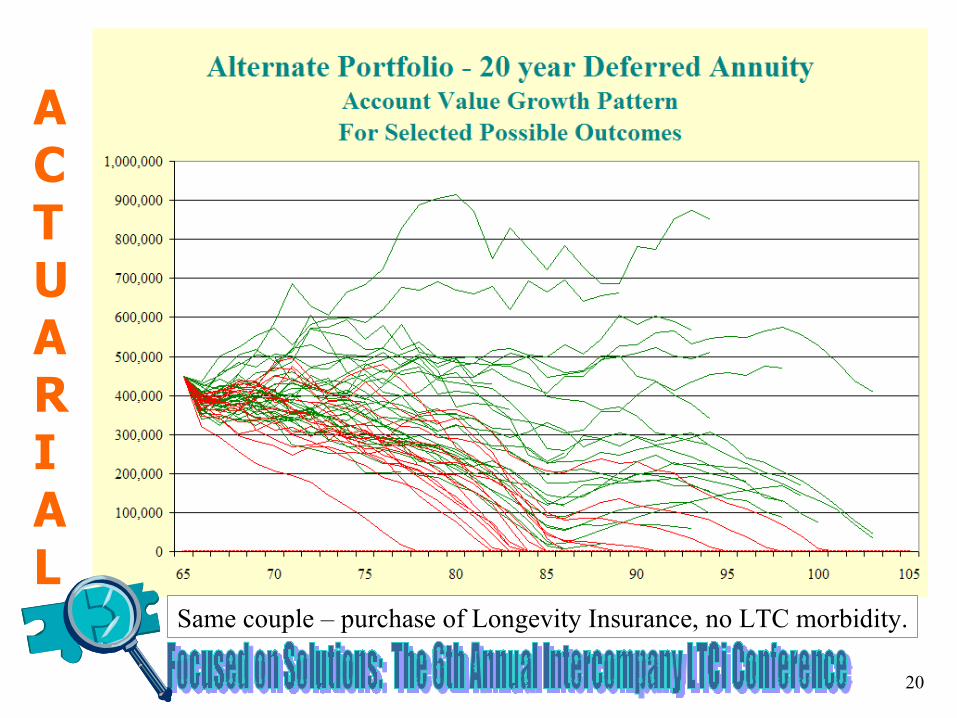

ACTUARIAL

Same couple – purchase of Longevity Insurance, no LTC morbidity.

21

ACTUARIAL

Effect of a Longevity Product Solution20 year Joint & Survivor Deferred Annuity

Improved chance of success!

22

ACTUARIAL

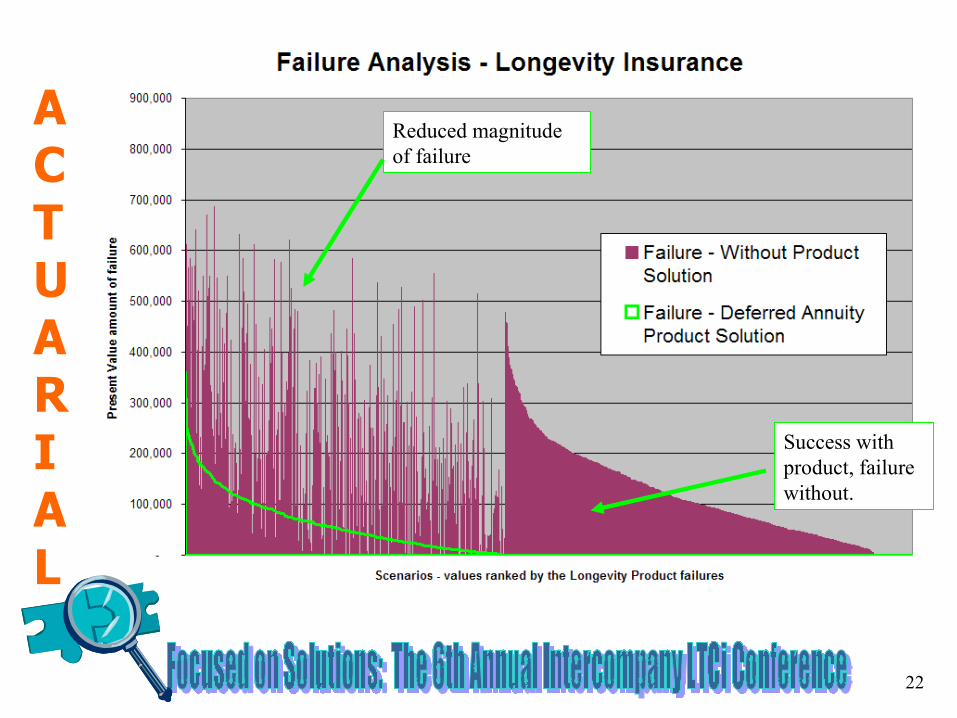

Success with product, failure without.

Reduced magnitude of failure

23

ACTUARIAL

Demonstration Tool Inputs1. Information Gathering

- YOB, gender, state of residence- expected retirement income (Social Security, pension, other)- Assets (Qualified, non-Qualified, Tax deferred, Tax free, and savings)- health characteristics (optional)- goals – needs, wealth transfer

2. Products – pre-installed- modeled plan features

3. Actuarial Assumptions – pre-installed- economic scenario generator- mortality and morbidity – realistic- inflation

4. Results- can be developed to enable multiple product solutions or demonstrate the benefits of an individual product, for example LTC insurance.

24

ACTUARIAL

Each purchase a 5 year benefit period, 50% HHC, 5% inflation, at today’s costs in Arizona.

25

ACTUARIAL

Use of scenario examples to show how the product works

26

ACTUARIAL

27

ACTUARIAL

Effect of Long-Term Care Morbidity on Retirement Success

In this example, the product didn’t improve success, but you should not stop here. Demonstrations that show the value of a product that deals with tail risk can be developed so that a decision enabling approach that highlights your solution can be used.

28

ACTUARIAL

Additional Sample AnalyticsCauses of Success / Failure

29%

14%

8%

27%

23%

LTC event - failanyway

LTC event -success

LTC event - faildue to LTC

failure no LTC

success no LTC

Distribution of Long-Term Care Episode Total Claim Costs

-

50

100

150

200

250

< 100k 100k to

150k

150k to

200k

200k to

300k

300k to

400k

400k to

500k

500k to

750k

750k to

1M

1M to

2M

2M +

Primary

Spouse

Probability of having at least one LTC event and continuing to meet retirement goals without an LTC

policy.

0%

10%

20%

30%

40%

50%

60%

1 6 11 16 21 26 31 36

Cumulative Probability of LTC event Proportion of claims self-funded

LTC Needs Gap

Probability of the having at least one LTC event in the next X years

0%

5%

10%

15%

20%

25%

30%

35%

40%

1 6 11 16 21 26 31 36

Male Cumulative Probability of LTC event

Female Cumulative Probability of LTC event

Examples that demonstrate the Long-Term Care risk and present ways of showing the product features and educating the potential purchaser.

29

ACTUARIAL

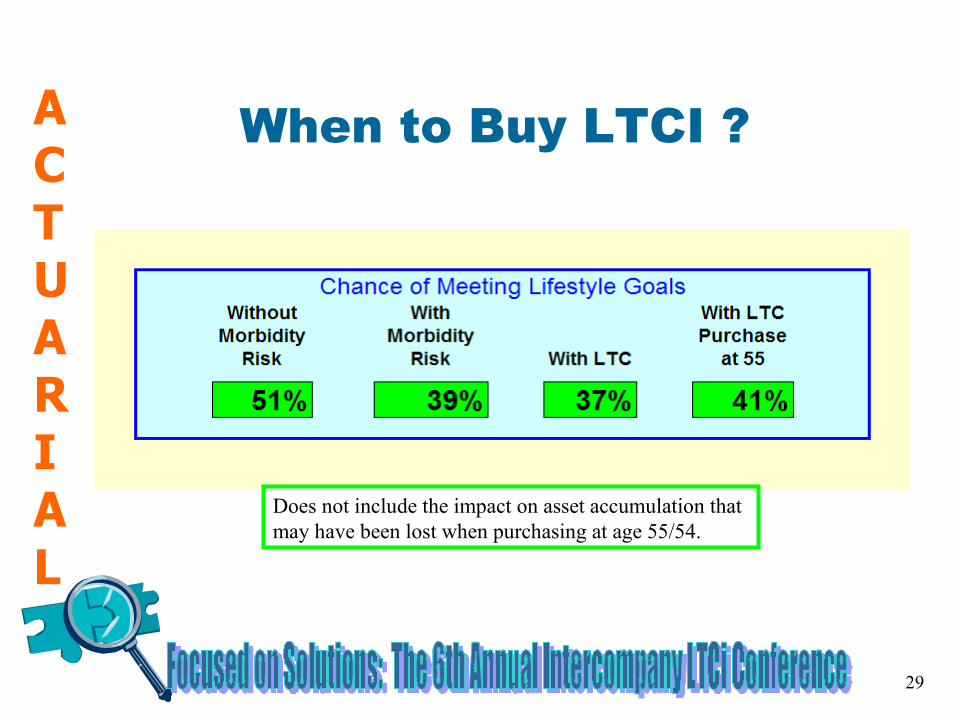

When to Buy LTCI ?

Does not include the impact on asset accumulation that may have been lost when purchasing at age 55/54.

30

ACTUARIAL

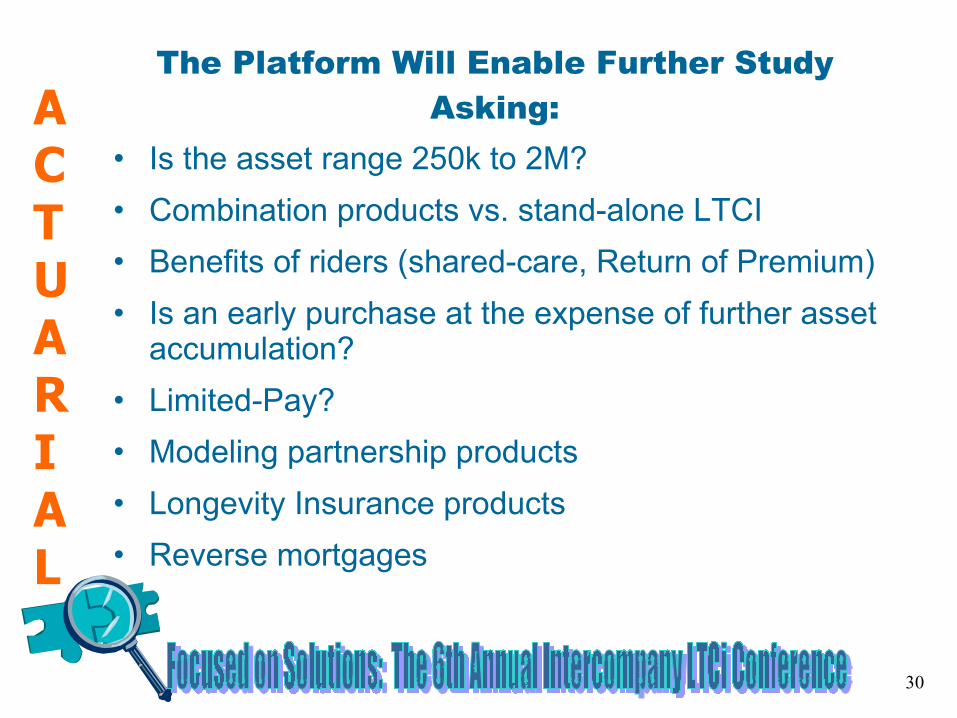

The Platform Will Enable Further Study Asking:

• Is the asset range 250k to 2M?

• Combination products vs. stand-alone LTCI

• Benefits of riders (shared-care, Return of Premium)

• Is an early purchase at the expense of further asset accumulation?

• Limited-Pay?

• Modeling partnership products

• Longevity Insurance products

• Reverse mortgages

31

ACTUARIAL

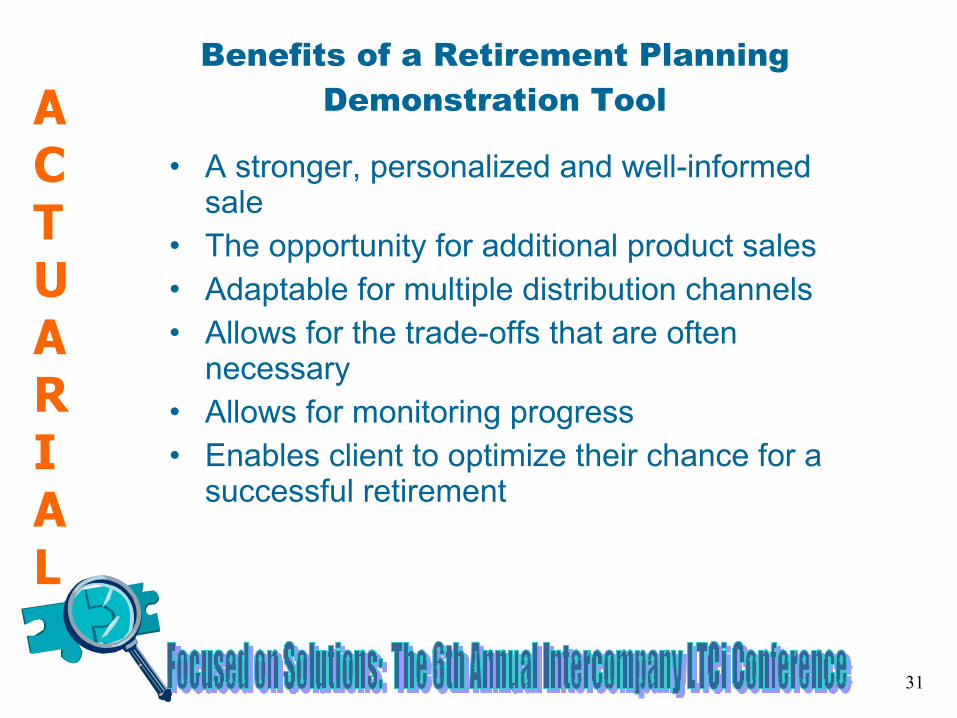

Benefits of a Retirement Planning Demonstration Tool

• A stronger, personalized and well-informed sale

• The opportunity for additional product sales• Adaptable for multiple distribution channels• Allows for the trade-offs that are often

necessary• Allows for monitoring progress• Enables client to optimize their chance for a

successful retirement

32

ACTUARIAL

• Distribution channel education• Product design and development• Market segmentation analysis• Research• Marketing materials• Product suitability studies

Additional UsesBeyond the current use by financial planners, brokerage agencies and carriers.

33

ACTUARIAL

Our value proposition:

Addressing the Long-Term Care risk cannot rely on a one dimensional approach. It requires: - Helping clients plan for giving and receiving care, - Identifying tax advantage opportunities to fund

Long-Term Care costs, and- Providing tools that can demonstrate the risk in a

personal manner and offer comprehensive solutions.

Conclusion