abb - credit suisse

TRANSCRIPT

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/researchdisclosures or call +1 (877) 291-2683 US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

20 February 2013

Europe/Switzerland

Equity Research

Electrical Equipment (Capital goods - Engineering (Europe))

ABB (ABBN.VX) INITIATION FOCUS LIST STOCK

A transforming business

We initiate on ABB with an Outperform rating and add it to Credit Suisse’s European Focus List (TP of SFr26, 24% potential upside): We forecast 15% avg. EPS growth in FY13-15E versus 7% for ABB’s peers, while our blue-sky scenario indicates 25% growth. Our estimates are 7% ahead of consensus.

■ Consensus underestimating Automation growth potential: Driven by

cyclical recovery (China) and strong structural growth drivers in EM, we think

ABB’s Automation business will grow 6% organically in FY13/14 (cons. 3%).

In addition, a strong market position, acquisition capacity, barriers to entry

and a concentrated market should allow further market share gains.

■ Margin recovery in PP: We expect a stronger EBIT margin recovery than

consensus (13.8% vs. 12.9% in FY14) due to improved new order pricing

and cost savings. We see solid medium-term growth potential in the US due

to the age of the installed base, new energy sources, equipment monitoring,

stricter regulation and the housing recovery driving T&D investment.

Stimulus in China’s rail and wind markets could boost growth further.

■ Strong acquisition capacity: ABB’s target range of 1.5-2x ND/EBITDA

could provide $12-18bn of excess cash in FY13E (17-25% potential EPS

accretion). Re-levering up to 0.5x (FY12: 0.0x) could lift earnings by 8%.

■ Underappreciated returns profile: ABB generates the highest CFROI® in

our Electricals coverage yet is priced for CFROI to fade to 10% with margins

falling to 9% over the next 10 years. This compares with the HOLT® DCF

(using the mid-range of ABB’s targets) deriving a CFROI of c16% over the

next 5 years and CS estimates of 16.9% operating margins in FY15E.

■ Valuation: After a 15% underperformance vs. peers (12 months), ABB

trades on FY14E 12.4x / 8.5x PE / EV/EBITA (9% / 8% sector discount).

■ Catalysts: Automation and Power World, Orlando (FL), 25 March.

Share price performance

15

20

Feb-11 Jun-11 Oct-11 Feb-12 Jun-12 Oct-12

Price Price relative

The price relative chart measures performance against the SMI

PRICE which closed at 7530.69 on 15/02/13

On 15/02/13 the spot exchange rate was SFr1.23/Eu 1. -

Eu .75/US$1

Performance Over 1M 3M 12M Absolute (%) 6.6 25.6 9.2 Relative (%) 3.9 10.3 -11.4

Financial and valuation metrics

Year 12/12A 12/13E 12/14E 12/15E Revenue (US$ m) 39,336.0 42,827.4 45,663.8 48,486.1 EBITDA (US$ m) 5,240.20 6,727.32 7,536.29 8,092.52 Adjusted Net Income (US$ m) 2,987.8 3,731.0 4,212.1 4,568.4 CS adj. EPS (US$) 1.30 1.62 1.83 1.99 ROIC (%) 14.25 18.86 21.04 21.95 P/E (adj., x) 17.49 14.02 12.42 11.45 P/E rel. (%) 111.8 97.8 96.1 99.1 EV/EBITDA 10.7 8.1 7.0 6.3

Dividend (12/13E, US$) 0.81 IC (12/13E, US$ m) 21,033.54 Dividend yield (%) 3.6 EV/IC 2.6 Net debt (12/13E, US$ m) 1,783.8 Current WACC 9.0 Net debt/equity (12/13E, %) 9.3 Free float (%) 100.0 BV/share (12/13E, US$) 8.1 Number of shares (m) 2,314.74

Source: FTI, Company data, Thomson Reuters, Credit Suisse Securities (EUROPE) LTD. Estimates.

Rating OUTPERFORM* Price (15 Feb 13, SFr) 20.97 Target price (SFr) 26.00¹ Market cap. (SFr m) 48,540.17 Enterprise value (US$ m) 54,487.5

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

Research Analysts

Simon Toennessen

44 20 7883 6893

Andre Kukhnin CFA

44 20 7888 0350

Max Yates

44 20 7883 8501

Jonathan Hurn, CFA

44 20 7883 4532

Specialist Sales: David Arnold

44 20 7883 3549

Credit Suisse HOLT®: Ian Gray

44 20 7883 6116

20 February 2013

ABB (ABBN.VX) 2

Picturing the story Figure 1: Consensus is underestimating the growth potential in Automation in FY13/14E…

Figure 2: …despite a pick-up in IP growth historically resulting in even stronger Automation growth globally

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2008 2009 2010 2011 2012 2013E 2014E

Org

an

ic g

row

th (

%)

ABB Automation - Organic growth (incl. CSe)

Org. growth forecasts (Cons)

Industrial production Process Factory

Year EM Developed Global Global Global

2003 8.4% 1.0% 3.7% -0.3% 11.3%

2004 10.6% 2.4% 5.4% 5.1% 13.0%

2005 8.3% 2.1% 4.4% 8.4% 9.1%

2006 9.5% 2.9% 5.5% 11.4% 11.4%

2007 10.0% 2.8% 5.7% 8.8% 11.5%

2008 5.0% -2.7% 0.5% 10.6% 2.4%

2009 0.8% -13.4% -7.2% -5.1% -19.5%

2010 12.6% 7.1% 9.6% -3.3% 20.6%

2011 7.6% 2.8% 5.0% 9.7% 13.8%

2012E 5.1% 0.7% 2.8% 3.1% 4.2%

2013E 6.8% 1.3% 4.0% 4.4% 6.0%

2014E 7.3% 2.4% 4.8% 5.2% 7.1%

Historic avg 8.1% 0.6% 3.6% 5.0% 8.2%

vs Global IP * 1.5x 2.0x Source: Company data, SME, Credit Suisse estimates Source: Thomson Reuters, Credit Suisse estimates

Figure 3: Market seems to be solely focussing on the margin development of the Power Products business…

Figure 4: …while ignoring that 68% of ABB’s profits are derived from its more attractive Automation business

12

14

16

18

20

22

24

10%

11%

12%

13%

14%

15%

16%

Q1

11

Q2

11

Q3

11

Q4

11

Q1

12

Q2

12

Q3

12

Q4

12

Sh

are

pri

ce (

SF

r)

EB

IT m

arg

in (

%)

Power Product - EBIT margin ABB share price

Power32%

Automation68%

Source: SME, Credit Suisse estimates Source: Company data

Figure 5: Compared to consensus we forecast a stronger margin improvement in PP…

Figure 6: …at times when the top-line could be supported by higher transmission investment in the US

12%

13%

14%

15%

16%

17%

18%

19%

2007 2008 2009 2010 2011 2012 2013E 2014E

Marg

in (

%)

EBIT margin - Power Products (CSe) Consensus estimates

8.6 8.9 9.5 10.3 10.211.1

13.5

16.0

0

5

10

15

20

2006 2008 2010 2012E 2011-16E

Inv

estm

en

t (U

SD

bn

) avg. annual expected spend

Source: Company data, SME, Credit Suisse estimates Source: EEI, Business Information Group, Quanta Services

Figure 7: Due to the focus on PP margins we think ABB has underperformed its peers by 15% over the last 12m

Figure 8: We highlight that ABB generates the second highest CFROI®s within the wider Electrical Eng. universe

-25%

-20%

-15%

-10%

-5%

0%

5%

Fe

b-1

2

Mar-1

2

Ap

r-12

May-1

2

Jun

-12

Jul-1

2

Au

g-1

2

Se

p-1

2

Oct-1

2

No

v-1

2

De

c-1

2

Jan

-13

Fe

b-1

3

Rela

tive p

erf

orm

an

ce (

%)

ABB share performance spread vs. Electricals (ex ABB)

-5%

0%

5%

10%

15%

20%

So

mfy

AB

B

Le

gra

nd

Schne

ider

Va

con

Als

tom

Sa

ft

Ph

oen

ix M

eca

no

PK

C G

rou

p

Mers

en

Pysm

ian

Hu

ber &

Suhn

er

Gam

esa

SG

L C

arb

on

Zu

mto

bel

Ve

sta

s

Vo

n R

oll

Ne

xan

s

CF

RO

I (%

)

CFROI LFY CFROI - 12mth fwd

Source: the BLOOMBERG PROFESSIONAL™ service Source: Credit Suisse HOLT®

20 February 2013

ABB (ABBN.VX) 3

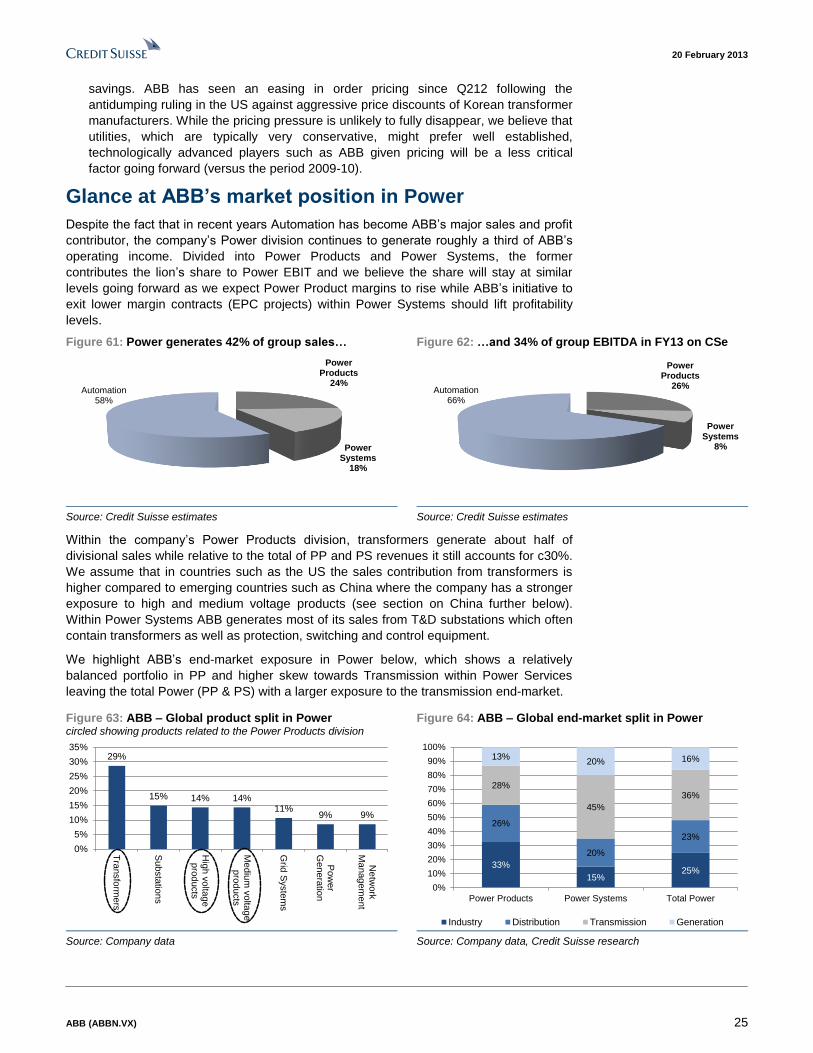

Table of contents Picturing the story 2 Investment summary 4 ABB ABBN.VX 7 Automation 8

Glance at ABB’s market position in Automation 9 Solid sales growth potential in Automation in 2013/14 11 ABB should benefit from Robotics and Oil & Gas / Petrochemicals 16 Consensus underestimates ABB’s growth potential in Automation 20 Higher Service sales could trigger higher valuation 21

Power 24 Glance at ABB’s market position in Power 25 Drivers for higher US T&D spend going forward 26 Benefits from Chinese government stimulus 29 Stronger margin upside potential in Power Products 32

Scope for acquisitions 36 Inorganic sales growth target could imply $8-12bn acquisition spend (FY13-15E) 37 Acquisition focus should continue to be on faster growing Automation markets 38 Potential large Automation deals that might make strategic sense 40

Valuation 44 Sum of the parts 44 Discounted cash-flow 45 ABB through the Credit Suisse HOLT lens 46 ABB’s share price has lagged the sector 50 Credit Suisse versus consensus estimates 51 Multiple comparisons 52

Divisional analysis 53 Discrete Automation & Motion 54 Low Voltage Products 56 Process Automation 57 Power Products 60 Power Systems 62

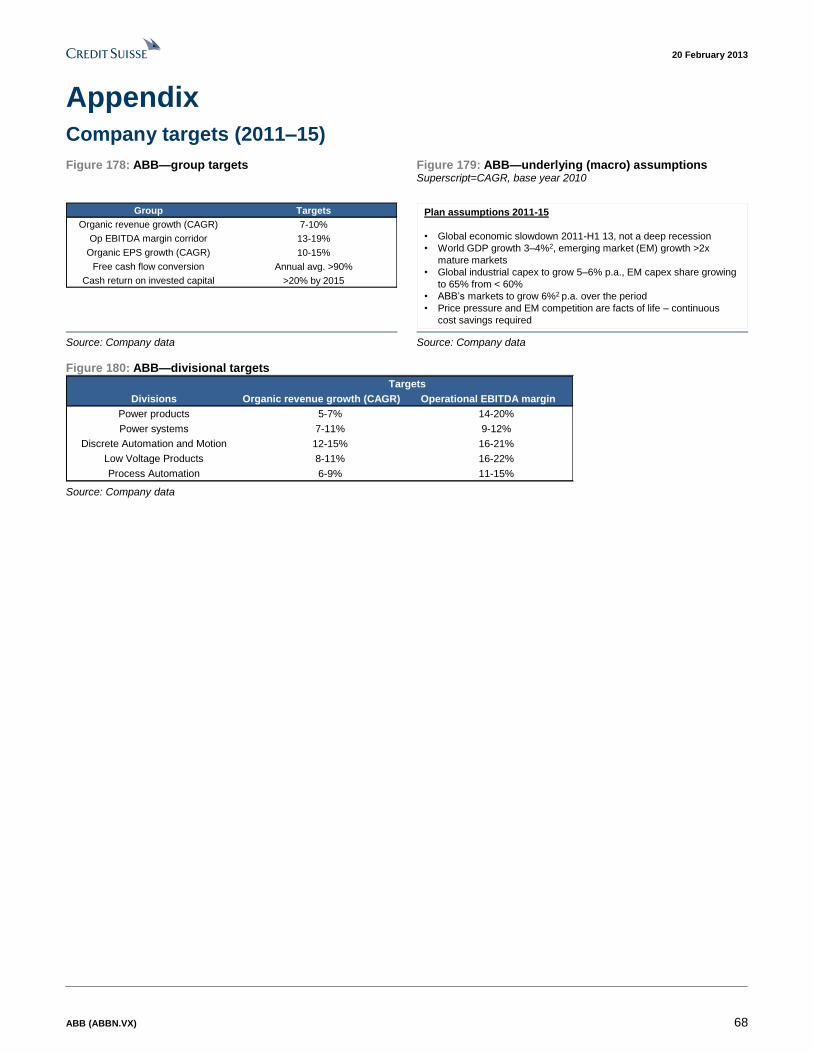

Financial statements 64 Appendix 68

Company targets (2011–15) 68 Acquisition history 69 ABB’s cost savings programme in detail 70 Description of companies used in SOTP 71 Vendor data—Automation & Power 73 PEERs map 75

20 February 2013

ABB (ABBN.VX) 4

Investment summary We initiate on ABB with an Outperform rating and a TP of SFr26 (24% potential

upside). We add ABB to the Credit Suisse European Focus List.

In our view ABB shares offer an attractive investment opportunity owing to a combination

of strong medium term growth potential within the company’s Automation division (68% of

group profits), margin recovery within ABB’s Power Products business, sizable acquisition

potential and strong return generation. We derive EPS growth of 15% over the next three

years compared to 7% for its Electrical peers while our blue-sky scenario offers 25%

earnings growth. We focus on the following:

■ Consensus underestimating the growth potential in Automation

■ Margin recovery and medium term growth potential in Power Products

■ Acquisition capacity of $12-18bn could lead to 17-25% EPS accretion

■ Market materially underestimating ABB’s strong returns profile

Consensus underestimating the growth potential in Automation

■ ABB’s strong market position in Automation – We view Industrial Automation as

one of the most attractive end-markets within Capital Goods in the medium to long

term due to its potential for cyclical recovery (correlation to industrial production) yet

more importantly, in our view, strong structural growth drivers particularly in emerging

markets. Given ABB generates 68% of its group profits from products and services

exposed to Automation end-markets, we believe the company is well positioned to

benefit from this trend.

■ Attractive structural growth drivers – We are forecasting ABB’s Automation

business to grow revenues on average by 6% organically over the next two years

compared to consensus forecasts of 3%. In our view, consensus is underestimating

structural growth drivers such as high wage inflation in emerging markets based on a

strongly growing middle-class and government efforts to push up wages (c.10% in

China) as well as low penetration rates (see Figure 10), which should trigger higher

Automation investment in the medium term. In addition, we believe that ABB’s leading

market position in several product areas, its acquisition capacity, geographical

diversity, limited threat from new entrants, a high degree of market consolidation and

limited capacity additions by incumbents should allow the company to gain market

share. Near-term, we think that leading indicators improving in China, strong

Automation potential in the US and Europe possibly stabilising should boost organic

growth to higher levels seen last fiscal year.

Figure 9: Automation markets have structurally outgrown industrial production in the past in x, unless otherwise stated

Figure 10: One key structural growth driver is a low penetration rate in emerging markets Robot density=Number of robots per 10k manufacturing employees

Industrial production Process Factory

Year EM Developed Global Global Global

2003 8.4% 1.0% 3.7% -0.3% 11.3%

2004 10.6% 2.4% 5.4% 5.1% 13.0%

2005 8.3% 2.1% 4.4% 8.4% 9.1%

2006 9.5% 2.9% 5.5% 11.4% 11.4%

2007 10.0% 2.8% 5.7% 8.8% 11.5%

2008 5.0% -2.7% 0.5% 10.6% 2.4%

2009 0.8% -13.4% -7.2% -5.1% -19.5%

2010 12.6% 7.1% 9.6% -3.3% 20.6%

2011 7.6% 2.8% 5.0% 9.7% 13.8%

2012E 5.1% 0.7% 2.8% 3.1% 4.2%

2013E 6.8% 1.3% 4.0% 4.4% 6.0%

2014E 7.3% 2.4% 4.8% 5.2% 7.1%

Historic avg 8.1% 0.6% 3.6% 5.0% 8.2%

vs Global IP * 1.5x 2.0x

0

50

100

150

200

250

300

350

Japan

Kore

a

Germ

any

Italy

US

Spain

Taiw

an

Fra

nce

Sw

itzerl…

Austra

lia

UK

Chin

a

Bra

zil

Russia

India

Ro

bo

t d

en

sit

y (

x)

Robot density Global average

Source: Thomson Reuters, Credit Suisse estimates Source: World Bank, IFR, United Nations, BLS

20 February 2013

ABB (ABBN.VX) 5

Margin recovery and medium term growth potential in Power Products

■ Improved pricing to benefit margins – ABB’s margin erosion within its Power

Products division had been a key area of market concern for a prolonged period of

time. Fuelled by material price discounts of up to 30% by Korean transformer

manufacturers in the US, ABB’s profitability in this business declined sharply (see

Figure 11). Yet, following the US antidumping ruling in mid 2012 pricing pressure has

abated and ABB’s operating margins have stabilised for five quarters in a row.

Contrary to consensus estimates, we believe that ABB’s PP division will see a

stronger margin recovery towards the end of FY13 and in FY14 from improved pricing

momentum on new orders last fiscal year (average lead time 12-18 months in PP).

While the pricing pressure is unlikely to fully disappear, we believe that utilities, which

are typically very conservative, might prefer well established, technologically advanced

players such as ABB given pricing will be a less critical factor going forward (versus

the period 2009-10). In addition, we think ABB will continue to focus strictly on its cost

savings programme (3-5% of cost of sales annually) biased towards the Power

division (60% of total savings in Power in FY12).

Figure 11: Improved new order pricing last year should lead to a stronger recovery in PP margins…

Figure 12: …while ABB continues to focus on cost savings, particularly within its Power division

12%

13%

14%

15%

16%

17%

18%

19%

2007 2008 2009 2010 2011 2012 2013E 2014E

Ma

rgin

(%

)

EBIT margin - Power Products (CSe) Consensus estimates

-50

0

50

100

150

200

250

300

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

Ne

t s

av

ing

s (

US

Dm

)

Sa

vin

gs

/ P

ric

e e

ros

ion

(%

)

Productivity savings Product price erosion (negative)

Net savings (Savings - Price erosion)

Source: Company data, SME, Credit Suisse estimates Source: Company data

■ Medium-term growth potential from higher US and Chinese Transmission and

Distribution spend – Our channel checks have highlighted the potential for improved

pricing in the US based on a pick-up in transmission and distribution (T&D) investment

spend. Driven by rising reliability issues due to the age of the installed base (>30

years or more for transformers), on-going economic growth, new energy sources such

as renewables, increased equipment monitoring, harsher regulation and a continuous

recovery of the housing market (3-year lag to distribution investment), US utilities

appear likely increase their investment spend in the transmission and distribution

market. Following improved power order momentum in China (+13% in Q412), we

think ABB will increasingly benefit from higher government stimulus particularly related

to offshore wind and infrastructure investments such as rail.

Acquisition capacity of $12-18bn could lead to 17-25% EPS accretion

Due to an explicit target of 3-4% inorganic sales CAGR, we expect ABB to continue to use

its balance sheet mainly for acquisition purposes rather than share buybacks or special

dividends. Following 75% of acquisition spend in Automation (FY08-H112), we believe that

strong structural growth opportunities mean most of the spending will continue to be in

Automation. More precisely, we believe that ABB will expand its market position further in

PLC’s and attractive end-markets such as Oil & Gas as well as growing its Service

business via strategically sensible deals. While management recently flagged that ABB

does not target large deals in the short term, we believe that size will be a less critical

issue if a potential deal makes strategic sense. We highlight potential larger acquisition

targets in this report and estimate that based on ABB’s leverage target range of 1.5-2x net

debt / EBITDA management has $12-18bn of acquisition capacity in FY13.

20 February 2013

ABB (ABBN.VX) 6

Market materially underestimating ABB’s strong returns profile

■ Limited volatility in cash return despite competitive and cyclical pressure – ABB

has maintained its CFROI within a range of 14-16% over the last five years. Achieving

this level of returns is impressive and puts ABB firmly within the top decile of Global

Capital Goods companies and at the top end of the Electrical Equipment industry in

Europe. The company’s ability to maintain high and stable cash returns has resulted in

qualifying for a HOLT eCap (extended fade window of 10 years instead of 5 years) – a

distinction which only 7% of companies in the HOLT database qualify for.

■ ABB priced for CFROI to fade to 10% and margins to 9% – The market is currently

pricing ABB’s CFROI to fade to 10% over the next 10 years which, should this happen,

will represent an 8 year low (see Figure 13). If we use the HOLT DCF model using the

mid-range of ABB’s group targets on sales and margins we derive a CFROI of c16%

over the next five years translating into a share price of SFr27.50 (30% potential

upside). If we use the 10 year fade window, ABB’s EBITDA margins are priced to

deteriorate down to 9% by 2021 (CSe 16.9% in FY15), which represents nearly a

600bps decline from the 14.8% margins ABB generated in FY12. In addition to rising

PP margins, group margins should benefit from stronger Power Systems margins due

to management’s decision to exit EPC contracts as well as targeting a higher share of

group Service sales (20-25% target by FY15 from 17% in FY12).

■ Shares underperformed by 15% over last 12 months / 2014 valuation attractive –

We derive a TP of SFr26 by using an average of our SOTP, DCF and Credit Suisse

HOLT analysis. Following an underperformance of 15% (12 months), ABB trades on

FY14E 12.4x / 8.5x PE / EV/EBITA, implying a 9% and 8% peer discount, respectively.

Figure 13: ABB is currently priced for CFROI to fade to 10%

Figure 14: ABB has significantly underperformed its Electrical peers over the last 12 months

-25%

-20%

-15%

-10%

-5%

0%

Feb-1

2

Ma

r-12

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug-1

2

Sep-1

2

Oct-1

2

Nov-1

2

Dec-1

2

Jan-1

3

Feb-1

3

Rela

tive p

erf

orm

an

ce (

%)

ABB share performance spread vs. Electricals (ex ABB) Source: Credit Suisse HOLT Source: the BLOOMBERG PROFESSIONAL™ service

Blue-sky scenario suggesting 25% annual earnings growth potential in FY13-15E

Figure 15: Blue-sky scenario – Impact on earnings forecasts Blue sky scenarios FY13E FY14E FY15E Avg. Description

CS EPS forecasts (base) 1.62 1.83 1.99

Growth 25% 13% 8% 15%

EPS accretion

Stronger Automation sales growth 2% 6% 11%

Faster top-line growth assumption particularly in China/Europe

leading to double digit organic sales growth in FY14/15E with

margins closer to the top end of ABB's guidance range in FY15

Faster margin re-acceleration in Power

Products1% 3% 4%

Our current forecasts reflect a margin re-acceleration in PP from

14.8% in FY12 to 15.5%/15.9% in FY13/14 (cons 15.1%/15.4%).

In our blue-sky scenario we estimate margins of 16.5% in FY14

(still >200bps off FY09) mainly due to improved pricing.

Use of excess cash 5% 8% 11%

Based on financial headroom targets (1.5-2x) ABB has

acquisition firepower of $12-18bn in FY13. We use a leverage of

0.5x in our blue-sky scenario as we find this more realistic.

CS EPS forecasts (blue-sky) 1.75 2.16 2.53

Growth 35% 23% 17% 25% median multiple (2009-2012)

PE multiple 15.3x discounted back, FX adjusted to SFr

Potential target price (blue-sky) 30 Source: Company data, the BLOOMBERG PROFESSIONAL™ service, Credit Suisse estimates

20 February 2013

ABB (ABBN.VX) 7

ABB ABBN.VX Price (15 Feb 13): SFr20.97, Rating: OUTPERFORM, Target Price: SFr26.00

Income statement (US$ m) 12/12A 12/13E 12/14E 12/15E

Sales revenue 39,336 42,827 45,664 48,486 EBITDA 5,240 6,727 7,536 8,093 Depr. & amort. (1,486) (1,444) (1,489) (1,574) EBIT (CS) 4,058 5,435 6,158 6,629 Net interest exp. (220) (244) (261) (236) Associates — — — — Other adj, 435 76 36 36 PBT (CS) 4,274 5,266 5,933 6,429 Income taxes (1,030) (1,401) (1,592) (1,726) Profit after tax 3,244 3,865 4,341 4,703 Minorities (108) (113) (119) (125) Preferred dividends — — — — Associates & other (148) (21) (10) (10) Net profit (CS) 2,988 3,731 4,212 4,568 Other NPAT adjustments (284) (55) (26) (26) Reported net income 2,704 3,675 4,186 4,542

Cash flow (US$) 12/12A 12/13E 12/14E 12/15E

EBIT 4,058 5,435 6,158 6,629 Net interest (220) (244) (261) (236) Cash taxes paid — — — — Change in working capital (411) (233) (366) (726) Other cash & non-cash items 352 (109) (214) (263) Cash flow from operations 3,779 4,849 5,317 5,405 CAPEX (1,230) (1,293) (1,430) (1,502) Free cash flow to the firm 2,549 3,556 3,887 3,902 Acquisitions (3,694) — — — Divestments — — — — Other investment/(outflows) (588) — — — Cash flow from investments (5,575) (1,257) (1,340) (1,422) Net share issue/(repurchase) 90 — — — Dividends paid (1,747) (1,985) (2,122) (2,267) Issuance (retirement) of debt 5,452 — — — Other (6,250) — — — Cash flow from financing activities

(2,455) (1,985) (2,122) (2,267) Effect of exchange rates 90 — — — Changes in Net Cash/Debt (4,161) 1,606 1,855 1,715 . Net debt at start (771) 3,390 1,784 (71) Change in net debt 4,161 (1,606) (1,855) (1,715) Net debt at end 3,390 1,784 (71) (1,786)

Balance sheet (US$ m) 12/12A 12/13E 12/14E 12/15E

Assets Cash and cash equivalents 6,875 8,481 10,336 12,051 Accounts receivable 11,575 11,778 12,558 13,576 Inventory 6,182 6,731 7,176 7,620 Other current assets 3,370 3,370 3,370 3,370 Total current assets 28,002 30,359 33,440 36,617 Total fixed assets 5,947 6,419 6,921 7,455 Intangible assets and goodwill 13,727 13,220 12,680 12,105 Investment securities — — — — Other assets 1,394 1,394 1,394 1,394 Total assets 49,070 51,392 54,435 57,571 Liabilities Accounts payable 6,441 6,802 7,385 7,752 Short-term debt 2,537 2,537 2,537 2,537 Other short term liabilities 9,996 10,153 10,430 10,799 Total current liabilities 18,974 19,492 20,352 21,088 Long-term debt 7,534 7,534 7,534 7,534 Other liabilities 5,116 5,116 5,116 5,116 Total liabilities 31,624 32,142 33,002 33,738 Shareholders' equity 16,906 18,723 20,921 23,336 Minority interest 540 526 512 497 Total equity & liabilities 49,070 51,392 54,435 57,571 Net debt (US$ m) 3,390 1,784 (71) (1,786)

Per share data 12/12A 12/13E 12/14E 12/15E

No. of shares (wtd avg) 2,295 2,298 2,297 2,297 CS adj. EPS (US$) 1.30 1.62 1.83 1.99 Dividend (US$) 0.73 0.81 0.87 0.93 Dividend payout ratio 55.81 49.80 47.20 46.56 Free cash flow per share (US$)

1.11 1.55 1.69 1.70

Key ratios and valuation

12/12A 12/13E 12/14E 12/15E

Growth(%) Sales 3.5 8.9 6.6 6.2 EBIT (13.0) 33.9 13.3 7.7 Net profit (13.1) 24.9 12.9 8.5 EPS (9.9) 17.8 11.4 8.2 Margins (%) EBITDA margin 13.3 15.7 16.5 16.7 EBIT margin 10.3 12.7 13.5 13.7 Pretax margin 10.9 12.3 13.0 13.3 Net margin 7.6 8.7 9.2 9.4 Valuation metrics (x) EV/sales 1.4 1.3 1.1 1.0 EV/EBITDA 10.7 8.1 7.0 6.3 EV/EBIT 13.8 10.0 8.5 7.6 P/E 17.4 14.0 12.4 11.4 P/B 3.1 2.8 2.5 2.2 Asset turnover 0.80 0.83 0.84 0.84 ROE analysis (%) ROE stated-return on equity

16.5 20.6 21.1 20.5 ROIC 14.3 18.9 21.0 22.0 Interest burden 1.1 1.0 1.0 1.0 Tax rate 26.8 27.0 27.0 27.0 Financial leverage 0.60 0.54 0.48 0.43 Credit ratios (%) Net debt/equity 19.4 9.3 (0.3) (7.5) Net debt/EBITDA 0.65 0.27 (0.01) (0.22) Interest coverage ratio 18.4 22.2 23.6 28.1

Source: FTI, Company data, Thomson Reuters, Credit Suisse Securities

(EUROPE) LTD. Estimates.

15

20

Feb-11 Jun-11 Oct-11 Feb-12 Jun-12 Oct-12

Price Price relative

The price relative chart measures performance against the SMI PRICE which

closed at 7487.13 on 15/02/13

On 15/02/13 the spot exchange rate was SFr1.23/Eu 1. - Eu .75/US$1

20 February 2013

ABB (ABBN.VX) 8

Automation ABB’s Automation division generates more than two thirds of group profits – a share which

has risen from c50% in 2008. We believe the market is underestimating the expansion

potential in Automation supported by two sizable, well integrated acquisitions in the US

and the scope for further deals going forward. Driven by strong structural growth drivers

particularly in emerging markets, we think Automation is one of the most attractive end-

markets within Capital Goods in the medium term. Although most industrial end-markets in

EM (such as China) are likely to grow at a slower pace going forward, we think Automation

will be an exception. ABB has a strong market position to benefit from these trends.

Within this section, we focus on the following topics:

■ Glance at ABB’s market position in Automation – ABB’s breadth of automation

products and services offerings, its diversity and market leading position in several

areas within Automation (e.g. Distributed Control Systems (DCS)) puts ABB into a

sweet spot to benefit from the growth potential within an attractive end-market, in our

view. We believe ABB offers the opportunity to invest into above average growth

markets such as Oil & Gas, Petrochemicals, Transport, Power Generation and

Automotive equipment (particularly in emerging countries) and to benefit from strong

underlying growth and in addition structurally driven Automation expansion within

those markets.

■ Solid sales growth potential in Automation in 2013/14E – The global Automation

market should grow at around 6% in the medium term, hence its historic trend of IP+

(industrial production) growth should continue. Driven by structural growth drivers in

emerging markets such as demographic shifts (growing middle class) and government

efforts to push up wages we expect the global industrial automation market to grow at

~1.5x global IP over the next cycle versus ~1.3x during the last cycle. ABB’s strong

market position, the limited threat from new entrants, a high degree of market

consolidation and limited capacity additions by incumbents should allow ABB to gain

market share. We forecast average organic growth for ABB over the next two years of

6%.

■ Consensus underestimates ABB’s potential in Automation – We think consensus

growth estimates (organically) over the next two years are too conservative,

particularly in FY13 (consensus 0% vs. CS 5%). With Chinese leading indicators

improving, Europe potentially stabilising throughout the year and a more positive

development in the US (note that other automation players such as Rockwell surprised

positively in the US last quarter), we believe ABB’s organic growth in Automation has

seen its trough last year. We believe consensus estimates are too bearish, particularly

for Discrete Automation & Motion (DA&M), where our sales forecasts are 7-10%

ahead of the Street in FY13/14. Our analysis indicates that at times of elevated

economic activity consensus estimates have often been too bearish over the past five

years (see Figure 56).

■ Higher Service sales could trigger higher valuation – ABB aims to increase the

revenues portion from Services from 17% in FY12 to 20-25% by 2015. Given the

significantly higher levels of profitability from Service contracts we believe this will be

margin supportive medium term. Following the company’s successful acquisitions of

Baldor and Thomas & Betts, ABB has considerably improved its installed base

particularly in North America, which in our view should lead to higher Service business

over time. We note that ABB’s target will put the company on a similar Service level to

its peers (on average; ex Legrand). Due to the fact that in our view higher Service

contribution has been a driver for higher valuation in the past we believe the market

might also acknowledge this improvement with a higher valuation for ABB. Currently

ABB’s peers trade at an 8% premium on FY14 EV/EBITA estimates.

20 February 2013

ABB (ABBN.VX) 9

Glance at ABB’s market position in Automation

Compared to its peers, ABB has one of the broadest product offerings in Automation,

ranging from a variety of plant level controls to a raft of plant instrumentation products

such as sensors, drives or motion control products such as motors. ABB represents one of

the few Automation companies that generates a sizable revenue portion from both discrete

and process automation. As we highlight further below in this report, this is relatively rare

in the industry given limited synergy potential between products used: for example, in an

oil refinery (process) and an automotive production facility (discrete). Yet, ABB has

managed to build strong market positions within respective product areas in both process

and discrete automation markets such as a market leading position in DCS within process

as well as a strong robotics and motors market position in factory automation.

Figure 16: ABB’s position in the Automation value chain

Major players

PLM: Autodesk, Dassault, Siemens

ERP: Oracle, SAP

MES: Aspen, CDC Software, Invensys, Siemens

SCADA: ABB, Invensys, Siemens

DCS: ABB, Honeywell, Siemens, Yokogawa

PLC: ABB, Omron, Mitsubishi, Rockwell,

Schneider, Siemens

V ^ V ^

Computerized Numerical

Control (CNC)CNC: Fanuc, Siemens

V ^ V ^ V

V ^ V ^ Human Machine Interface (HMI)

Drives Sensors

Robots

MotorsMachine

Vision

HMI: ABB, Invensys, Mitsubishi, Siemens,

Schneider

Plant

InstrumentationValves Sensors Machine Tools

Sensors: ABB, Eaton, Honeywell, Omron

Machine Vision: Cognex, Teledyne

Drives: ABB, Danaher Mitsubishi

Robots: ABB, Fanuc, Kuka

Machine Tools: Gildemeister, Mori Seiki

Motors: ABB, Emerson, GE, Regal Beloit,

Rockwell, Schneider, Siemens, Weg,

Yaskawa

Plant Level

Controls

Supervisory Control and Data Analysis (SCADA)

Process Factory

Distributed Control

System (DCS)

Programmable Logic

Controller (PLC)

Enterprise Level

Controls

Product Lifecycle Management (PLM)

Enterprise Resource Planning (ERP)

Manufacturing Execution System (MES)

Source: Credit Suisse research

While ABB’s Automation business generated around half of group sales in FY09, stronger

organic growth and falling profitability in the company’s Power division has meant that

Automation became an even more important contributor to the company’s group

performance over time. Today, Automation generates the majority of group sales and due

to a stronger margin profile more than two-thirds of group profits. We note that the

business shift towards a higher Automation exposure has been even more pronounced in

emerging countries such as China. In FY08 ABB’s Automation business generated 45% of

sales in China while in H112 this division already contributed 58% to total Chinese sales.

20 February 2013

ABB (ABBN.VX) 10

Figure 17: Automation generates 58% of group sales… Figure 18: …and 66% of group EBITDA in FY13 on CSe

Discrete Automation &

Motion22%

Low Voltage17%

Process Automation

19%

Power42%

Discrete Automation &

Motion28%

Low Voltage21%

Process Automation

17%

Power34%

Source: Credit Suisse estimates Source: Credit Suisse estimates

We show ABB’s Automation business split in Figure 19. Across its three subdivisions, ABB

generates the majority of its revenues from motors and generators, supported by the

acquisition of Baldor in the US, followed by low voltage drives and products related to oil,

gas and petrochemical end-markets.

Figure 19: ABB’s total Automation business split Figure 20: ABB has a market leading position in DCS

0%2%4%6%8%

10%12%14%16%18%20%

% o

f A

uto

mati

on

sale

s

ABB

0%

5%

10%

15%

20%

25%

1999 2001 2003 2005 2007 2009 2011

Ma

rket

sh

are

(%

)

Main competitors: Emerson, Honeywell, Invensys, Siemens, Yokogawa (alphabetical order)

Source: Company data, Credit Suisse estimates Source: Company data, ARC DCS Worldwide Outlook

In both figures below we go into more detail as to which end-markets ABB is most

exposed to as well as outlining the company’s main customers. While in Automation ABB

tends to work closer together with industrial-related customers (60% of group customers),

the company’s Power business naturally builds a closer relationship to utility companies

offering products such as transformers, circuit breakers or gas-insulated switchgears. If we

split up ABB’s industrial customers amongst their respective end-markets we note that the

company has the most significant end-market exposure to minerals and metals as well as

to oil, gas and petrochemicals, both accounting for 15% and 10%, respectively.

Figure 21: ABB’s customers split (2011) 3-year rolling average

Figure 22: ABB’s end-market split (2011) in US$ millions, circled = Industrial customers

Industrial customers

(direct / indirect)

60%

Utlity customers

(direct)40%

Power Transmission

20%

Minerals & metals15%

Oil, gas & petrochemicals

10%

Power generation

10%

Power distribution

10%

Marine5%

Pulp & paper5%

Discrete manufacturing, automotive &

transport5%

Buildings5%

Other15%

Source: Company data Source: Company data

20 February 2013

ABB (ABBN.VX) 11

Solid sales growth potential in Automation in 2013/14

We believe that Automation will be one of the most attractive end-markets in Capital

Goods in the medium term backed by solid sales growth potential due to a combination of

strong structural drivers in emerging markets (high wage inflation, low penetration rates)

and the potential for a cyclical rebound in more developed markets such as Europe and

the US if economic data continues to improve (see more details in the note from our

Global Cap Goods team, Global Industrial Automation – The next growth phase, 14th

August 2012)

Underpinned by industry data and the historic correlation with industrial production the

global Automation market looks set to grow at around 6% over the next three years with

growth economies outpacing more mature markets and factory automation outgrowing

process automation (see Figure 28). In both figures below we show the difference in size

between the total automation market and the industrial automation market. Due to ABB’s

customer exposure, the latter should be more relevant.

Figure 23: Total automation market size / growth estimate Figure 24: Industrial automation market split

2010 2015E

$285bn

$380bn

6% CAGR

Discrete manufacturing

25%

Process manufacturing

25%Oil & Gas

20%

Mining & minerals

10%

Utilities10%

Hybrid manufacturing

10%

$180bn market size (2012)

Source: Company data Source: Company data, ARC DCS Worldwide Outlook

We highlight historic Automation sector spend in Figure 25, which shows a pick-up in

growth particularly in emerging markets, which expanded at c.8% on average between

2000 and 2010. We view the growth forecasts for developed markets as too conservative

if the European economy begins to improve and capital restraints in the US resulting from

the ‘fiscal cliff’ do not significantly impact manufacturing growth over the next two years.

Figure 25: Automation sector spend in $tr, spend by oil & gas, mining, iron & steel, electricity, gas & steam, basic industrial chemicals, pulp & paper, infrastructure construction sectors

0

1

2

3

4

5

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

Au

tom

ati

on s

ecto

r sp

end

($tr

)

Developed markets Emerging markets

1990-2000

3.3% pa

2000-2005

7.4% pa

2005-2010

8.8% pa

2010-2015

6.9% pa

1990-2000

0.9% pa

2000-2005

1.0% pa

2005-20103.2% pa

2010-2015

2.1% pa

Source: Company data, Global Insight, Credit Suisse research

20 February 2013

ABB (ABBN.VX) 12

ABB should outgrow Automation markets

Owing to ABB’s strong market position, the limited threat from new entrants, a high degree

of market consolidation and limited capacity additions by incumbents we believe ABB has

the potential to grow at a faster pace than the global automation market (note that we

forecast average organic growth of 7% for ABB between 2013-15E) driven by ABB’s

excellent market position within the Automation value chain (as highlighted above in

Figure 16), which should for example enable the company to win a greater amount of large

integrated automation projects.

We think that market-leading players such as ABB are not under imminent threat from new

market entrants in emerging markets. During our last field trip China in November 2012

Rockwell’s China head emphasised that it would likely take new market participants a

minimum of ten years to replicate the technology of market leading Western players. While

he admitted that it might be quicker for instrumentation products such as drives and

motors, the minimum time of ten years was particularly pertinent for plant level controls

products such as DCS’s where ABB holds a market leading position. Furthermore, we

believe that ABB should continue to gain market share on the back of

1) a significant focus on product quality given controls products are often a very critical

component within the Automation process and 2) ABB’s potential to use its strong cash-

flow generation for selective M&A deals.

According to ABB the key growth drivers in Automation are:

■ Factory Automation

■ User of energy (Oil & Gas)

■ Transportation and mobility

■ Energy efficiency

■ Commodity demand

For obvious reasons order growth in ABB’s Automation tends to follow trends in industrial

production (in developed markets) pretty well. We note that macro forecasts are becoming

increasingly more optimistic for 2013 and beyond (see Figure 27). History suggests that

this should lead to stronger investment particularly in the areas of manufacturing.

Following a year of weaker GDP growth especially in Europe and China we expect more

automation investment to come through and improved growth rates for Automation players

such as ABB (see Figure 26).

Within the divisional section at the back of this report we go into further detail around the

cyclicality of ABB’s specific divisions. While the company’s Power business in particular

Power Systems is clearly more exposed to customers operating in late cyclical end-

markets we note that due to the high Process Automation exposure (customers: e.g. oil &

gas, petrochemical companies) ABB’s total automation business tends to be less short-

cycle than one might assume. ABB’s only pure short-cycle division is Low Voltage

Products, which accounts for roughly 20% of ABB’s group sales. Figure 26 demonstrates

the impact from the later cyclical process business particularly throughout the last

downturn.

20 February 2013

ABB (ABBN.VX) 13

Figure 26: ABB Automation order growth vs industrial production growth

Figure 27: CS macro forecasts – More positive trends in China and Europe

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Q10

9

Q20

9

Q30

9

Q40

9

Q11

0

Q21

0

Q31

0

Q41

0

Q11

1

Q21

1

Q31

1

Q41

1

Q11

2

Q21

2

Q31

2

Q41

2E

Q11

3E

Q21

3E

Q31

3E

Q41

3E

IP g

row

th (

%)

Org

. g

row

th (

%)

ABB Automation - Org. order growth IP - Eurozone

IP - US IP - China

Macro forecasts 2012E 2013E 2014E Trend for 2013/14

Global Real IP 3.1% 3.5% 4.0%

IP 2.8% 4.0%

US Real IP 2.3% 1.9% 2.5%

Euro Area Real IP -0.4% 0.5% 1.5%

NJA Real IP 6.3% 6.8% 7.0%

China Real IP 7.7% 8.0% 8.2%

IP 10.0% 10.9% 11.4%

Source: The BLOOMBERG PROFESSIONAL™ service, Company

data, Credit Suisse estimates

Source: Credit Suisse estimates

We believe industrial automation will continue to outgrow industrial production. Automation

relative to IP could potentially see higher growth this cycle compared with the previous

one, given the emergence of several new growth themes.

■ Much of China’s recent output growth has been driven by construction and

infrastructure build-outs. Industrial vendors supplying these markets will likely see

lower trend growth going forward. Automation however will likely benefit from two

emerging trends in China: (1) wage inflation is accelerating; and (2) the increased

government emphasis on consumption;

■ The global capex outlook for key automation end-markets such as Petrochemicals is

stronger today in our view compared to last cycle;

■ The efficacy of discrete automation is becoming increasingly apparent, yet penetration

remains low in many markets, offering scope for increased penetration to drive growth.

Below, we show bottom-up Process and Factory Automation market growth (generated by

a wide sample of automation vendors that we track), in the context of Industrial Production.

Figure 28: Automation market growth forecasts in x, unless otherwise stated; * excluding outliners

Figure 29: ABB – CS org. sales forecasts by subdivision in US$ millions, unless otherwise stated

Industrial production Process FactoryYear EM Developed Global Global Global2003 8.4% 1.0% 3.7% -0.3% 11.3%2004 10.6% 2.4% 5.4% 5.1% 13.0%2005 8.3% 2.1% 4.4% 8.4% 9.1%2006 9.5% 2.9% 5.5% 11.4% 11.4%2007 10.0% 2.8% 5.7% 8.8% 11.5%2008 5.0% -2.7% 0.5% 10.6% 2.4%2009 0.8% -13.4% -7.2% -5.1% -19.5%2010 12.6% 7.1% 9.6% -3.3% 20.6%2011 7.6% 2.8% 5.0% 9.7% 13.8%2012E 5.1% 0.7% 2.8% 3.1% 4.2%2013E 6.8% 1.3% 4.0% 4.4% 6.0%2014E 7.3% 2.4% 4.8% 5.2% 7.1%Historic avg 8.1% 0.6% 3.6% 5.0% 8.2%vs Global IP * 1.5x 2.0x

-15%

-10%

-5%

0%

5%

10%

15%

20%

2008 2009 2010 2011 2012 2013E 2014E

Org

an

ic g

row

th (

%)

Organic growth - DA&M Organic growth - Process

Organic growth - LV

Source: Thomson Reuters, Credit Suisse estimates Source: Thomson Reuters, Credit Suisse estimates

In order to derive a clearer picture of how ABB’s respective Automation markets are

expected to grow, we have created Figure 30, in which we specifically list growth

expectations for a variety of Automation markets in which ABB operates. Our conclusion

from Figure 30 is that ABB’s markets should grow close to 6% on average over the next

three years. As mentioned above, we believe that ABB has the potential to outgrow its

respective markets due to a strong competitive position in a raft of its marketplaces.

20 February 2013

ABB (ABBN.VX) 14

Figure 30: Growth estimates in ABB’s Automation markets and regions in millions, unless otherwise stated

Growth estimates ABB's Automation markets 2011 2012E 2013E 2014E 2015E

Industrial Control Systems (ICS) 7.3% 6.6% 5.0% 6.4% 6.2%

SCADA 7.2% 4.3% 4.5% 5.3% 6.0%

DCS 7.3% 8.3% 5.0% 6.7% 6.2%

PLC 7.6% 6.2% 6.5% 8.1% 6.9%

Field Devices 5.9% 4.1% 5.3% 5.3% 5.5%

Robotics 6.6% 7.5% 8.5% 7.5% 7.5%

Sensors 5.6% 3.6% 3.6% 4.2% 4.2%

Motion & Drives 4.9% 1.5% 3.7% 4.3% 4.4%

Others 6.5% 6.0% 6.0% 6.0% 6.0%

Total 6.9% 5.9% 5.0% 6.1% 6.0%

ABB's Automation market growth by region 2011 2012E 2013E 2014E 2015E

Americas 6.6% 7.5% 6.1% 6.3% 5.5%

Europe 6.5% 3.3% 2.0% 3.8% 3.9%

APAC 7.4% 7.0% 7.2% 8.5% 8.8%

ROW 8.7% 7.8% 7.0% 6.9% 6.9%

Total 6.9% 5.9% 5.0% 6.1% 6.0% Source: Markets and Markets, Credit Suisse estimates

Structural growth drivers such as high wage inflation and rising penetration rates in

emerging markets will force Automation investment

We believe on-going high wage inflation (c.10%) in emerging markets such as in China will

continue to pressurise corporate profitability levels, putting China’s cost competitive

manufacturing at risk. In order for China to remain a manufacturing powerhouse it is vital

in our view to significantly invest into Automation. For us to exactly pinpoint the time of

higher investment coming through is difficult yet we believe that turning economic

momentum can certainly be one important trigger point.

Although Chinese companies are likely to have little choice in upgrading their automation

investment / manufacturing technology, one could argue that multi-national companies

could simply move their production to countries with cheaper labour costs. We note though

that many other emerging markets are also seeing a substantial increase in wages, and

their base level today is not substantially lower than China’s.

Figure 31: Wage growth CAGR (2007-2011) in US$, unless otherwise stated

Figure 32: Hourly manufacturing costs (2011) in US$, unless otherwise stated

3%2%

8%

10%

9%

4%

Developed Developed(Ex Japan)

EmergingMkts Total

NJAEmerging

LatAmEmerging

EMEAEmerging

$39 $39

$10 $8

$10 $12

Developed Developed(ex Japan)

Emergingmarkets

NJAemerging

LatAmemerging

EMEAemerging

Source: BLS Source: BLS

We think Non-Japan Asia has the largest growth opportunity for investments as this region

accounts for 35% of the world’s manufacturing output, but has a robot density of only 11

per 10,000 manufacturing employees (Figure 33) compared with developed markets which

produce 50% of manufacturing output and yet have a significantly higher robot density of

149. In Figure 33 we show the robot density, which we use a proxy to quantify the level of

20 February 2013

ABB (ABBN.VX) 15

automation, by country, clearly demonstrating that countries such as China or India

currently have considerably lower penetration levels compared to more developed markets

such as Japan, the US or Germany.

Figure 33: % of global output and robots per employee in x, unless otherwise stated

Figure 34: Robot density for select countries (2011) Robots per 10,000 manufacturing employees, unless otherwise stated

50%41%

50%

7%

35%

8%

149

88

11 711

6

Developed Developed(ex Japan)

EmergingMarkets Total

EMEAEmerging

NJAEmerging

LatAmEmerging

% of Global Manufacturing Output

Number of Robots per 10,000 Manufacturing Employees

0

50

100

150

200

250

300

350

Japan

Kore

a

Germ

any

Italy

US

Spain

Taiw

an

Fra

nce

Sw

itzerla

nd

Austra

lia

UK

Chin

a

Bra

zil

Russia

India

Ro

bo

t d

en

sit

y (

x)

Robot density Global average

Source: World Bank, IFR, United Nations Source: World Bank, IFR, United Nations, BLS

Potential pick-up in China could boost organic growth for Automation players

Recent momentum in Chinese indicators (manufacturing PMIs, consumer confidence) and

the new leadership appear likely to spur increased economic activity. If this holds true then

we believe this should bode well for stronger Automation investment going forward.

We show recent corporate momentum in Figure 35 below. Despite a more stable trend

compared to H112, we continue to see earnings volatility as seen in Rockwell’s operating

performance over the last two quarters. Following strong organic sales growth of 11%

during the company’s Q4 (Jul-Sep12) management stated that growth rates in China fell

by more than 9% (seen in the total Asian region) during Q113 (Sep-Dec12). On the

earnings call management continued to cite tight credit availability (similar reason heard

for H112) and delayed order momentum as key explanations why growth in China has not

yet consistently picked up. On a more positive note Rockwell cited better order than sales

performance which might indicate a turning point in momentum starting to kick-in.

We believe there is upside risk to our organic growth forecasts in Automation if there is a

more pronounced pick-up in Chinese Automation investment than we currently assume.

Figure 35: Growth momentum in China/Asia Growth rate specification for included companies: ABB=Asia; Emerson=China; GE=China; GEA=China; Hollysys=China; Omron=China; Rockwell=China; Schneider=Asia; Siemens=China; Yokogawa=Asia

-20%

-10%

0%

10%

20%

30%

40%

50%

Ma

r-09

Jun

-09

Se

p-0

9

De

c-0

9

Ma

r-10

Jun

-10

Se

p-1

0

De

c-1

0

Ma

r-11

Jun

-11

Se

p-1

1

De

c-1

1

Ma

r-12

Jun

-12

Se

p-1

2

De

c-1

2

Sa

les

gro

wth

(%

)

ABB Emerson Rockwell Automation Average (all companies)

Source: Company data, Credit Suisse estimates

20 February 2013

ABB (ABBN.VX) 16

ABB should benefit from Robotics and Oil & Gas /

Petrochemicals

As we highlighted further above ABB has quite a diverse end-market exposure, yet oil &

gas and petrochemical companies represent one of the most important end-markets

accounting for roughly 10% of ABB’s customer base. In addition, we believe that product

areas in factory automation such as Robotics or Motors should continue to generate solid

growth rates in the medium term. We focus on the following:

■ Oil & Gas / Petrochemicals (see points 1 and 2 below) – Strong underlying growth

in Oil & Gas, refining capacity growth in emerging markets and a better outlook for

developed markets, particularly the US

■ Robotics – Above average growth potential within Automation Instrumentation

Oil & Gas / Petrochemicals (1) – Strong underlying growth in Oil & Gas and refining

capacity growth in emerging markets

Oil & Gas represents an important end-market within global industrial automation

(accounting for 20% of the total market; see Figure 24) and strong growth drivers explain

why Automation players such as ABB aim to further expand in this market. ABB operates

mainly in the upstream market (exploration and production) and sells control systems,

drives, cables or electrical solutions to its customers.

Figure 36: ABB’s end-market split in Process Automation Figure 37: ABB’s end-market split in DA&M

Chemical, Oil & Gas35%

Metals & Mining25%

Marine15%

Pulp & Paper10%

Power Generation

5%

Other10%

Discrete

Manufact.20%

Power Generation

10%

Buildings5%

Oil & Gas, Petrochemical

10%

Minerals & Metals25%

Transport10%

Water5%

Other15%

Source: BP Stats, OGJ, Credit Suisse estimates Source: OGJ, Credit Suisse estimates

In order to provide an indication of the growth potential in this market we have highlighted

expectations for offshore rig counts and tubulars in the figures below.

Figure 38: Growth expectations for offshore rig count in x, unless otherwise stated

Figure 39: Growth expectations for tubulars in x, unless otherwise stated

Source: IHS Petrodata Source: IHS Petrodata

20 February 2013

ABB (ABBN.VX) 17

We see two distinct drivers for higher automation investment by the Petrochemical

industry in this cycle compared with prior cycles: (1) increased efforts by emerging Asian

countries to develop domestic refinery / chemical processing capacity; (2) low gas prices

stimulating increased petrochemical plant investments in the US.

After declines in global refining capacity in 2011 and 2012, we are likely to see strong

capacity additions growth over the coming years. On a quarterly basis, refining capacity

additions are set to peak around Q314 / Q115.

We note that at the last Capital Markets Day in September 2012 ABB outlined its plans to

increase its relevance particularly in the oil & gas market. ABB aims to become the

preferred partner for the oil & gas industry supported by an expanding product portfolio.

Figure 40: Addition to global refining capacities in mbopd, unless otherwise stated

Figure 41: Quarterly capacity addition forecasts in mbopd, unless otherwise stated

(1.0)

(0.5)

-

0.5

1.0

1.5

2.0

2.5

3.0

199

51996

199

71

99

81

99

92

00

02001

200

22

00

32

00

42

00

52

00

62

00

72

00

82

00

92

01

02

01

12

01

2E

201

3E

201

4E

201

5E

mb

op

d

(400)

(200)

-

200

400

600

800

1,000

1,200

1,400

Q1

12

Q2

12

Q3

12

Q4

12

Q1

13

Q2

13

Q3

13

Q4

13

Q1

14

Q2

14

Q3

14

Q4

14

Q1

15

Q2

15

mb

op

d

Source: BP Stats, OGJ, Credit Suisse estimates Source: OGJ, Credit Suisse estimates

A large portion of the capacity growth is due to new refineries in China (27% / 49% of

global additions in 2012 / 2013 respectively – Figure 42 and Figure 43) and India (33% /

12% of additions in 2012 / 2013 respectively). In China, our Asia O&G team believes that

key drivers of growth are domestic demand and the desire to reduce the dependence on

imports.

In India, public sector companies are building more capacity – this is potentially because

they are looking to reduce the country’s dependence on private sector refiners.

Figure 42: Refining capacity additions (2012E) Figure 43: Refining capacity additions (2013E)

China

India

Rest of Asia

Middle East

North America

South America

Others

(0.8) (0.6) (0.4) (0.2) - 0.2 0.4 0.6mbopd

China60%

India12%

Middle East12%

North America11%

Rest of Asia3%

South America

1%

Others1%

Source: OGJ, Credit Suisse estimates Source: OGJ, Credit Suisse estimates

20 February 2013

ABB (ABBN.VX) 18

Petrochemicals/Oil & Gas (2) – Better outlook for developed markets, particularly

the US

The recent history of downstream petrochemical investment in the US and Western

Europe has been fairly poor. However, this is changing in the US, given technology

changes in extraction, in particular around hydraulic fracturing technology, which is leading

to substantial production increases in natural gas. The effect on natural gas prices has

been particularly evident over the past 12 months; our Energy Team expects this to persist.

Figure 44: US natural gas reserve/production change Figure 45: US natural gas price

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Gro

wth

yo

y (

%)

US Dry Natural Gas Production US Dry Natural Gas Reserves

0

2

4

6

8

10

12

14

Feb-0

8

May-0

8

Aug-0

8

Nov-0

8

Feb-0

9

May-0

9

Aug-0

9

Nov-0

9

Feb-1

0

May-1

0

Aug-1

0

Nov-1

0

Feb-1

1

May-1

1

Aug-1

1

Nov-1

1

Feb-1

2

May-1

2

Aug-1

2

Nov-1

2

Feb-1

3

Pri

ce (

US

D p

er

MM

Btu

)

US Natural Gas Price Source: The BLOOMBERG PROFESSIONAL™ service Source: The BLOOMBERG PROFESSIONAL™ service

Low gas prices are positive for process automation investment because the cheap

feedstock is resulting in improved economics for companies to invest in US petrochemical

capacity, potentially with a view to increasing exports. According to ICIS, for instance,

currently planned US ethylene capacity additions total 32% of existing capacity.

Figure 46: Announced ethylene capacity expansions in US$bn, unless otherwise stated

Company Project Capacity (tonnes) Location Cost ($bn) Start-up

ExxonMobil Chemical New cracker 1.5mn Baytow n, Texas NA 2016

Chevron Phillips Chemical New cracker 1.5mn Cedar Bayou, Texas NA Q1 2017

Dow Chemical New cracker w orld-scale US Gulf Coast NA 2016-17

Shell New cracker w orld-scale US Northeast NA 2016-17

Formosa Plastics New cracker 800000 Point Comfort, Texas 1.7 2016

Dow Chemical Restart 390000 St. Charles, Louisiana NA end 2012

Westlake Chemical Expansion 108863 Lake Charles, Louisiana NA H2 2012

Williams Expansion 272158 Geismar, Louisiana .35-.40 Q3 2013

INEOS Debottleneck 115000 Chocolate Bayou, Texas NA end 2013

Westlake Chemical Expansion 113399 Lake Charles, Louisiana NA 2014

LyondellBasell Expansion 386000 La Porte, Texas NA 2014

Considered expansions

Sasol New cracker 1.0-1.4m Lake Charles, Louisiana 3.5-4.5 NA

Indorama Ventures New cracker 1.3m NA NA 2018

LyondellBasell Expansion NA Channelview , Texas NA NA

SABIC New cracker w orld-scale US NA NA

Braskem New cracker NA US NA NA

Occidental Chemical New cracker NA Ingleside, Texas NA NA

Aither Chemicals New cracker NA US Northeast 0.75 2016

PTT Global Chemical New cracker NA NA NA NA Source: ICIS

Robotics – Above-average growth potential within Automation Instrumentation

We believe the global robotics market will grow at c.8% on average over the next three

years compared to the total automation instrumentation sector expanding at c.5%. Given

ABB’s top 5 market share position (see Figure 47), we think the company should be a

major beneficiary from this trend. Robotics accounts for 15% of DA&M revenues yet due to

a stronger growth profile we believe that the sales contribution from Robots will surge

20 February 2013

ABB (ABBN.VX) 19

closer to 20% over the next few years. In the most recent quarter management noted a

very strong performance of the company’s Robotics division.

Figure 47: Industrial robot market share Figure 48: Automation Instrumentation market split by revenues

Yaskawa23%

Fanuc22%

Kuka15%

ABB13%

Fujikoshi8%

Kawasaki8%

Other11%

Sensors

30%

Machine Vision20%

Robotics17%

Relays & Switches

16%

Motion Drives12%

Others5%

Source: Credit Suisse research Source: Credit Suisse research

In Figure 49 we have shown growth expectations for the robotics market by region. While

the Americas was forecasted to grow very strongly in 2012, current expectations imply that

growth will level out around 6% by 2015E. In 2013 the APAC region should continue

outgrowing other regions and account for more than 60% of generated Robotics revenues.

Figure 49: Robotics market growth forecasts by region Figure 50: Robotics sales generation by region (2013E)

-1.0%

1.0%

3.0%

5.0%

7.0%

9.0%

11.0%

13.0%

2011 2012E 2013E 2014E 2015E

Gro

wth

(%

)

Americas Europe APAC ROW Total

Americas15%

Europe17%

APAC61%

ROW7%

Source: Markets and Markets, Credit Suisse estimates Source: Markets and Markets, Credit Suisse estimates

The example of Japan from the 1970s and 1980s, and the growth trend in China in recent

years, suggest that China is now entering its inflection point, with discrete automation

investment set to accelerate (see Figure 51). As highlighted further above in this report,

the robot density in emerging markets still falls significantly behind that in developed

regions, particularly relative to hourly wage costs.

Figure 51: Robot stock (base year = 1974 for Japan, 1999 for China) Robot stock in units, unless otherwise stated

Figure 52: Robot density relative to hourly wage cost in different regions in US$, robot density per 10,000 manufacturing employees

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

T+0 T+5 T+10 T+15 T+20 T+25 T+30

Japan

China

$39 $39

$10 $8 $10 $12

149

88

11 7 116

Developed Developed(Ex Japan)

EmergingMkts Total

NJAEmerging

LatAmEmerging

EMEAEmerging

Hourly Cost (USD) Robot Density

Source: IFR, Credit Suisse estimates Source: IFR, Credit Suisse estimates

20 February 2013

ABB (ABBN.VX) 20

We note that Robotics peer company Kuka reported preliminary FY12 results at the

beginning of February highlighting a strong order backlog in Robotics, which has grown

35% in the last fiscal year driven by “considerable demand in China”. The company

expects strong demand in the coming years and consequently is building a new plant for

robot assembly in China.

Consensus underestimates ABB’s growth potential

in Automation

We believe consensus estimates for ABB’s Automation business are too bearish. The

Street currently forecasts flat organic growth in this division in 2013 compared to our

forecasts of 5% organic growth.

Figure 53: Consensus expects org. growth in Automation to be lower than in 2012 despite signs of Chinese leading indicators improving, Europe returning to GDP growth and positive Automation momentum in the US

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2008 2009 2010 2011 2012 2013E 2014E

Org

an

ic g

row

th (

%)

ABB Automation - Organic growth (incl. CSe) Org. growth forecasts (Cons)

Source: SME, Credit Suisse estimates

In our view consensus expectations, particularly for ABB’s DA&M business, are too

conservative. As described in our top down section on growth drivers above we think that

due to a potential pick-up in shorter-cycle end-markets mainly in emerging markets (and

the US) factory automation will outgrow Process over the next two years. We forecast ABB

to grow DA&M revenues at around 6% (medium term market growth expectations) in

FY13, accelerating to 8% thereafter. Our reported EBIT forecasts in Automation are 8-10%

ahead of consensus over the next two years (see Figure 54).

Figure 54: We are more optimistic about sales and profits in Automation in 2013/14E in USD millions, unless otherwise stated

CS forecasts 2013E 2014E Consensus 2013E 2014E CS vs. cons 2013E 2014E

Sales Sales Sales

DA&M 10,193 11,009 DA&M 9,559 10,046 DA&M 6.6% 9.6%

Process 8,606 9,209 Process 8,439 8,850 Process 2.0% 4.1%

LP 8,017 8,498 LP 7,714 8,118 LP 3.9% 4.7%

Total 26,816 28,715 Total 25,713 27,013 Total 4.3% 6.3%

Reported EBIT Reported EBIT Reported EBIT

DA&M 1,651 1,816 DA&M 1,503 1,647 DA&M 9.9% 10.2%

Process 1,001 1,104 Process 978 1,053 Process 2.4% 4.8%

LP 1,278 1,467 LP 1,145 1,275 LP 11.7% 15.1%

Total 3,930 4,387 Total 3,625 3,975 Total 8.4% 10.4%

Source: Vara Research consensus, Credit Suisse estimates

20 February 2013

ABB (ABBN.VX) 21

Figure 55: ABB’s current cons. EPS growth forecasts are lagging the correlation to US/EU IP seen historically

Figure 56: At times of elevated economic activity, ABB has beaten consensus earnings estimates

-70%

-45%

-20%

5%

30%

55%

80%

-20%

-15%

-10%

-5%

0%

5%

10%

Ja

n-0

5

Ju

l-05

Ja

n-0

6

Ju

l-06

Ja

n-0

7

Ju

l-07

Jan-0

8

Ju

l-08

Ja

n-0

9

Ju

l-09

Ja

n-1

0

Ju

l-10

Ja

n-1

1

Ju

l-11

Ja

n-1

2

Ju

l-12

EP

S g

row

th, ro

llin

g (

%)

IP g

row

tht

(%)

IP - US IP - EU ABB - Consensus EPS (1yr rolling fw)

-20%

-15%

-10%

-5%

0%

5%

10%

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2007 2008 2009 2010 2011 2012

EP

S (

US

D)

EPS estimates (1 year prior to reporting) EPS reported by ABB IP - US

Source: the BLOOMBERG PROFESSIONAL™ service Source: the BLOOMBERG PROFESSIONAL™ service

Higher Service sales could trigger higher valuation

By 2015 ABB aims to raise its group sales contribution from Services to 20-25% from 17%

last year. As we highlight in Figure 57 ABB has over time gradually improved its revenue

share from its Service business from around 15% five years ago.

Figure 57: ABB targets 20-25% of group sales from Service revenues by 2015E

15% 15% 16% 17% 16% 17%

20-25%

0%

5%

10%

15%

20%

25%

30%

2007 2008 2009 2010 2011 2012 2015E

Reven

ue s

pli

t (%

)

Service Product/Systems

Source: Company data, Credit Suisse research

Although ABB does not split out margins from its Service and Products/Systems business,

we believe that based on disclosures from other Capital Goods companies it is fair to

assume that its aftermarket revenues will generate a significantly higher profitability. Due

to ABB’s increasing contribution from Service revenues over the last few years ABB

should have seen a positive margin effect from a better Service/Product mix.

We note that ABB lagged its peers with respect to its revenue contribution from Services

(see Figure 59) in the past and won’t reach the Service revenue averages of the

Electricals and Mechanicals sector even if we take ABB’s new target of 20-25% into

account. However, this is mainly due to the following reasons:

■ The Mechanicals generally tend to have a stronger contribution from Aftermarket

revenues on the back of a market-leading position in often less penetrated markets.

■ The Services share of the Electricals (31%) is mainly boosted by Legrand (c60% of

group sales from Service). If we exclude Legrand from the Electricals group, we derive

an average of 24% which falls within ABB’s target range of 20-25%, hence does not

put ABB at a disadvantage.

20 February 2013

ABB (ABBN.VX) 22

Acquisitions of Baldor and Thomas and Betts should drive higher Service demand

We highlight in Figure 58 ABB’s split between Service and Product/Systems revenues for

each of the company’s divisions. As the graph demonstrates the company has the most

significant Service offering in its Process Automation business due to:

■ Selling of a service package often in combination with original equipment such as a

control system

■ Solid 10% exposure to turbochargers which have a high service business

■ Stronger software business in Process than in Discrete Automation

Although customers in DA&M often tend to maintain the product themselves, we believe

that both DA&M and Low Voltage have good potential to grow their Service business.

While in DA&M only the Robotics business currently has a strong service business

(c.35%) we think that due to the two sizable acquisitions in Automation (Baldor in DA&M

and Thomas and Betts in LV) ABB has significantly expanded its installed base (+10,000

distributors split between Baldor 4,000 and T&B >6,000) in the North American market,

which over time should lead to an increase in Service demand. While the T&B does not

have a Service business and won’t develop one in our view, we think that Baldor has good

potential to build an aftermarket business from currently using third-party providers.

Figure 58: Split between Service and Products/Systems revenues per division

85%

60%

95% 90% 85%

15%

40%

5% 10% 15%

0%

25%

50%

75%

100%

DA&M PA LV PP PS

Reven

ue s

pli

t (%

)

Products/Systems Service

Source: Company data

20 February 2013

ABB (ABBN.VX) 23

Companies on a higher valuation multiple tend to have a stronger Service offering

We believe that ABB’s target of 20-25% could be conservative given the company’s

installed base in some of its end-markets and a focus on raising the Service share via

acquisitions. While it might seem too optimistic to assume ABB will increase its Service

share to average levels of the Mechanicals, we think that a share beyond 25% could be

achievable. We highlight in Figure 59 that higher margin companies often trade on a

higher valuation multiple and conclude that if ABB successfully raises its share of more

profitable Service revenues the market might reflect this in form of a higher valuation.

Figure 59: A higher Service revenue contribution suggests a higher valuation multiple for Capital Goods companies

% of Group revenues

from Service

EBITA margin

(FY13E)

EBITA margin

(FY14E)

EV/Sales

(FY13E)

EV/Sales

(FY14E)

EV/EBITA

(FY13E)

EV/EBITA

(FY14E)

ELECTRICALS

Alstom 30% 7.0% 7.2% 0.64 0.59 9.1 8.2

Legrand 60% 19.5% 19.6% 2.17 2.06 11.1 10.5

Philips 10% 10.2% 10.3% 0.96 0.89 9.3 8.6

Schneider 37% 14.0% 14.3% 1.48 1.39 10.6 9.7

Siemens 20% 12.4% 12.6% 1.06 0.97 8.5 7.7

MECHANICALS

Alfra Laval 26% 17.3% 18.0% 1.96 1.80 11.3 10.0

Assa Abloy 67% 16.8% 17.0% 2.13 1.95 12.6 11.4

Atlas Copco 41% 21.4% 21.8% 2.34 2.08 10.9 9.6

Electrolux 15% 6.4% 6.5% 0.46 0.42 7.2 6.5

Kone 54% 14.5% 15.0% 2.24 2.06 15.5 13.7

Metso 45% 9.4% 9.7% 0.76 0.71 8.1 7.4

Sandvik 28% 15.0% 15.9% 1.64 1.48 10.9 9.3

Schindler 61% 12.9% 13.6% 1.63 1.49 12.6 11.0

SKF 18% 12.0% 13.6% 1.39 1.28 11.6 9.4

Average Electricals 31% 12.6% 12.8% 1.26x 1.18x 9.8x 8.9x

Average Mechanicals 39% 14.0% 14.6% 1.62x 1.47x 11.2x 9.8x

Average Total 37% 13.5% 13.9% 1.49x 1.37x 10.7x 9.5x

ABB 18% 12.7% 13.5% 1.28x 1.15x 9.9x 8.5x Source: Company data, Credit Suisse estimates

In Figure 60 we provide a sample of ABB’s service offering across its divisions.

Figure 60: ABB’s Service offering across its divisions

ABB's Service portfolio

Service agreements Maintenance Extensions upgrades & retrofits

Installation & commissioning Repairs End of life services

Training Engineering & consulting Replacement

Spares & consumables Advanced services

Source: Company data

20 February 2013

ABB (ABBN.VX) 24

Power ABB’s Power division is the primary reason why ABB’s shares continue to lag the

performance of the wider Capital Goods sector as well as its direct Electrical peers in our

view. It seems as if the market ignores the potential within the company’s Automation

division and despite margin stabilisation in Power Products for several quarters awaits

further evidence that the deterioration in profitability caused by emerging market

competition won’t repeat itself. While we think it would be wrong to rule this out

completely, we would argue that the main transformer costs (raw materials: copper &

steel, labour, shipping) are easily traceable, hence the US Department of Commerce will

likely monitor the development carefully in order to protect local manufacturing going

forward. Contrary to consensus expectations, we believe that ABB’s Power Product

margin has stronger upside potential based on better pricing trends and a strict, on-going

cost savings focus. We have backed up our argument with channel checks, which have

flagged the potential for improved pricing as well as higher US T&D spending in the

medium term benefiting players with a strong market position such as ABB.