aberdeen breakfast briefing – cost efficiency - oil & gas...

TRANSCRIPT

Aberdeen Breakfast Briefing – Cost Efficiency

Aberdeen Breakfast Briefing - Cost Efficiency

Oonagh Werngren MBE Operations Directorate

Oil & Gas UK

Scale of issues

• Over 4,400 UK jobs lost – 30 Companies • 40,000 global jobs lost – Operators and Tier 1 Contractors

- (100,000 global jobs estimated by Douglas-Westwood)

• £1.9bn reduction in spend by UK Operators • £20.5bn cuts globally by Majors will impact UK • Offshore rotas – move to 3:3 by 6 UK Operators • UK Contractor Rate cuts 10 - 20% • UK staff salary cut -5% • 10 rigs stacked in the UK • 34 rigs to be scrapped globally • UK projects being stalled • Company mergers

Aberdeen Breakfast Briefing - Cost Efficiency

Chaired by Oonagh Werngren, Oil & Gas UK

This morning’s speakers are …

Dan Cole, Mckinsey & Company

Gordon Ballard, Schlumberger UK

Paul Warwick, Talisman Energy Inc.

The scale of the challenge

Dan Cole Mckinsey & Company

Cost efficiency: the scale of the challenge Oil & Gas UK – breakfast briefing

Aberdeen 6 May 2015

CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of McKinsey & Company is strictly prohibited

McKinsey & Company | McKinsey & Company 7 7 | McKinsey & Company

The cost challenge in the UKCS

21

18

12

2.5

Percent Annual inflation rates, 2000–14

Big Mac

North Sea platform lifting costs1

UK lifting cost per barrel of oil equivalent (2004–14)2

UK development cost per barrel of oil equivalent (2004–13)2

SOURCE: McKinsey’s Energy Insight Offshore Operations Benchmarking Database; Oil & Gas UK Activity Surveys

1 Unweighted average of total lifting cost for 17 UKCS North Sea platforms (total cost, not cost per barrel) 2 Weighted average

McKinsey & Company | McKinsey & Company 8 8 | McKinsey & Company

The increase was largely unforeseen

SOURCE: Oil & Gas UK 2012 Economic Reports and 2015 Activity Survey

Growth in operating cost forecast from UKCS operators GBP billions

9.0

8.0

7.0

6.0

5.0

4.0

3.0

2.0

1.0

0.0

2013 actual (8.9) 2014 actual (9.6)

01 2003 2005 2007 2009 2011 2013 2015 2017 2019

McKinsey & Company | McKinsey & Company 9 9 | McKinsey & Company

The fall in oil price has made the North Sea a lot less profitable

USD 99 bbl 88

54 USD 55 bbl

SOURCE: WoodMac GEM (2015); McKinsey analysis

1 Price below which NPV of the remaining reserves of the field will be zero based on end 2014 cost and production forecast.

Share of UKCS production that breaks even1 Oil price

McKinsey & Company | McKinsey & Company 10 10 | McKinsey & Company

- 4.0%

Cost increase not due to increased activity …

Helicopter hours Hours

Wells drilled Number

+1.5%

SOURCE: McKinsey Energy Insights

Deck cargo shipped Tonnes

+2.0%

McKinsey & Company | McKinsey & Company 11 11 | McKinsey & Company

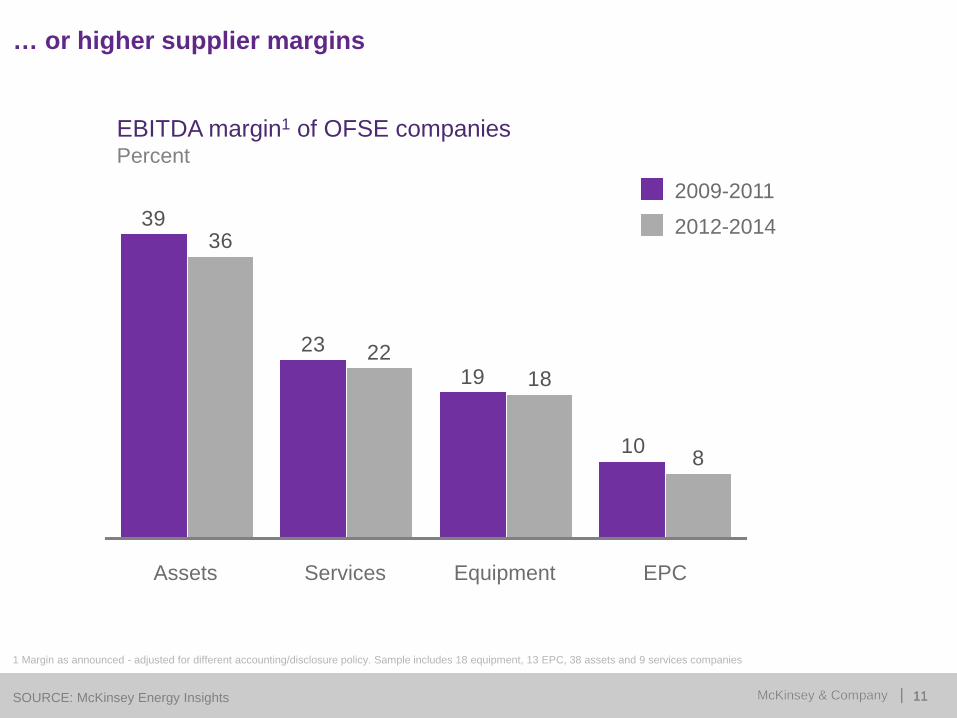

… or higher supplier margins

1 Margin as announced - adjusted for different accounting/disclosure policy. Sample includes 18 equipment, 13 EPC, 38 assets and 9 services companies

SOURCE: McKinsey Energy Insights

EBITDA margin1 of OFSE companies Percent

10

1923

39

8

1822

36

Assets EPC Services Equipment

2012-2014

2009-2011

McKinsey & Company | McKinsey & Company 12 12 | McKinsey & Company

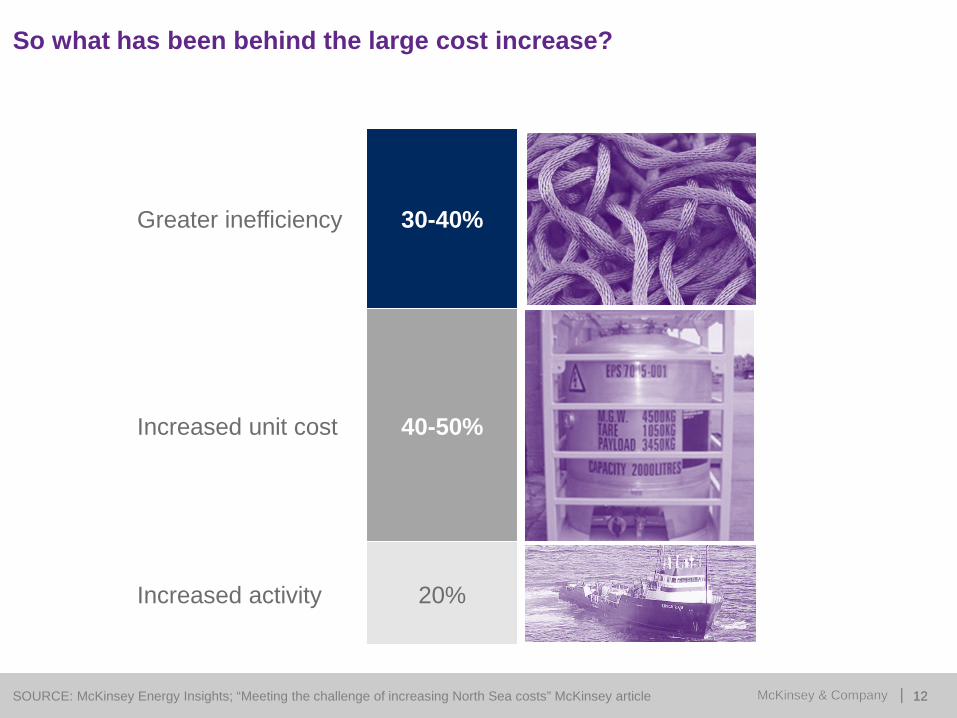

So what has been behind the large cost increase?

Increased unit cost

Increased activity

Greater inefficiency

20%

40-50%

30-40%

SOURCE: McKinsey Energy Insights; “Meeting the challenge of increasing North Sea costs” McKinsey article

McKinsey & Company | McKinsey & Company 13 13 | McKinsey & Company

Opex example: integrity inspections cost

SOURCE: Sanitised client example

Comparison of topsides integrity inspection costs per asset GBP thousands per installation, gross

McKinsey & Company | McKinsey & Company 14 14 | McKinsey & Company

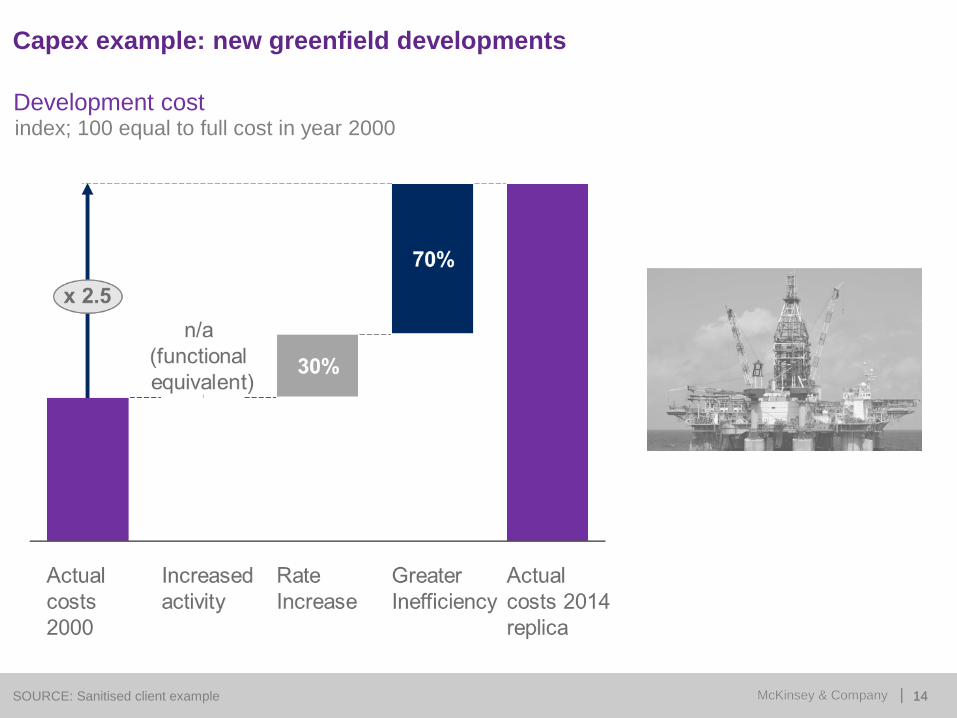

Capex example: new greenfield developments

SOURCE: Sanitised client example

Development cost index; 100 equal to full cost in year 2000

McKinsey & Company | McKinsey & Company 15 15 | McKinsey & Company

This is something other highly technical industries appear to have avoided

Nominal price inflation for a new commercial airliner

Nominal price inflation for a new 5-door hatchback in Western Europe

+ 0.2 – 1.5% + 1.0%

SOURCE: A2Mac1; manufacturer’s public data; Airline Monitor: McKinsey analysis

McKinsey & Company | McKinsey & Company 16 16 | McKinsey & Company

Recap

Industry Efficiency

Gordon Ballard Chairman

Schlumberger UK

Industry Efficiency Gordon Ballard Schlumberger 6 May 2015

This industry is a national asset

20

It’s worth fighting for!

Where we are……

Production Exploration Wells

OPEX CAPEX

No other basin in the world has seen such rapid cost inflation

22

It’s more than just production at risk – the supply chain is too

Billions in income tax and national insurance

Bold and immediate action is required

• Unless the UKCS adapts rapidly to the prevailing business environment, it will be a much smaller and greatly diminished industry by 2020

• Action now will ensure that the UKCS is as active in 2020 as it has been over the last decade

• The 2020 vision

- Actively exploring and maximising recovery of oil and gas - A supply chain providing a strong engine for growth - Lifting costs contained at around $20 per barrel

Ongoing Actions

Other Industry Initiatives

• Energy Jobs Taskforce - Scottish Enterprise, Highland & Island Enterprise - practical support & advice; promoting & defining good practice - Scottish Manufacturing Advisory Service (SMAS) - Working with Scottish industrial sector to drive efficiency and productivity

• Step Change in Safety - Safety standardisation – challenge the multiplicity of different safety schemes and initiatives

• The Oil & Gas Industry Council - PWC x-Industry Study - project to identify pragmatic lessons in

improving operations efficiency from across relevant industry sectors.

Cost Efficiency - Schlumberger

Cost Base Management: Manage Cost vs Operating Activity

Inventory & Asset Management

Facility Rationalisation

Sourcing and Distribution

Workforce Utilisation

41% Improvement

Distribution - Schlumberger

DSC provides a replenishment centre closer to point of use

At a local level • Single point of contacts

• Delivery KPI on E2E performance

• Logistics and Materials consolidation

DSC Functions: • Centralised Stock

• Inventory Control

• Network Optimisation

• Order Tracking and Expediting

• Global Traceability

Inventory & Asset Management - Schlumberger

Inventory Management: Bar Coding full lifespan

Reduction and Centralisation

Planned demand based on historical usage

Significant reduction on lead times

Operation confidence with on time delivery

Real Time Asset Tracking Assets bar coded to permit tracking

Determine actual usage by asset

Cycle element of asset

Reduce tool count based on

availability

18% improvement

33% improvement

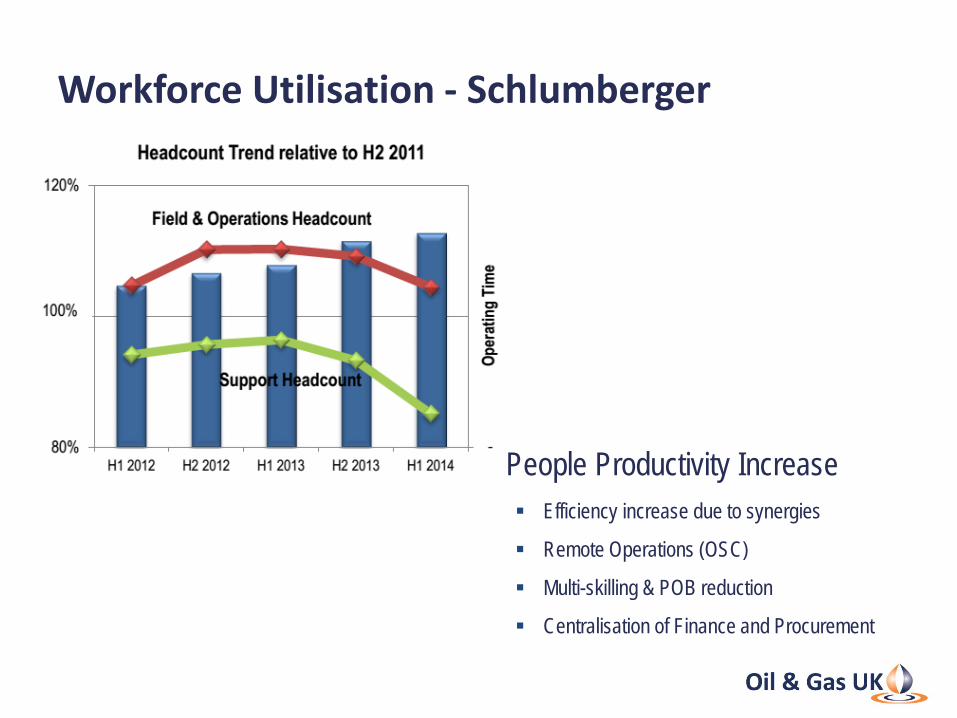

Workforce Utilisation - Schlumberger

People Productivity Increase Efficiency increase due to synergies

Remote Operations (OSC)

Multi-skilling & POB reduction

Centralisation of Finance and Procurement

Everyone has a part to play.

We need to: Re-create a competitive basin and industry

Learn from other Industries

Initiate structural and sustainable change Challenge behaviours

Cost Efficiency in a complex basin - An Operator in action

Paul Warwick

Executive Vice President Europe-Atlantic Talisman Energy Inc.

Cost Efficiency in a complex basin

April 2015

34 NYSE : TLM | TSX : TLM www.talisman-energy.com

Complex late life assets

▪ The case for change is very strong

▪ Aim high: wholesale transformation

▪ Intensively manage the changes

▪ Make change sustainable

35 NYSE : TLM | TSX : TLM www.talisman-energy.com

HSE- our primary focus - The Talisman Values

SAFETY

PASSION

RESULTS

RESPECT

EXCELLENCE

TEAMWORK

HONEST COMMUNICATION

36 NYSE : TLM | TSX : TLM www.talisman-energy.com

Gyda Process Systems & Surrounding Infrastructure

M

M

M M

GYDA GAS PIPELINE (TALISMAN)

EKOFISK PLATFORM

(CONOCO PHILLIPS)

GYDA RESERVOIR

(TALISMAN)

GYDA WELLS

ULA PLATFORM (BP) UGIP PIPELINE (BP)

GYDA OIL PIPELINE

(BP)

TAMBAR PLATFORM

(BP)

BLANE FIELD

(TALISMAN)

OSELVAR FIELD (DONG)

ULA OIL PIPELINE (BP)

HP SEPARATOR

LP SEPARATOR

GYDA PROCESS FACILITIES

(TALISMAN)

M

M

FUEL GAS

TEST SEPARATOR

GAS DEHYDRATION & COMPRESSION

GAS LIFT COMPRESSORS

PRODUCED WATER TREATMENT &

DISPOSAL

SEAWATER LIFT, FILTRATION & DEAERATION

WATER INJECTION PUMPS

MOL PUMPS & METERING

GAS EXPORT METERING

TO COOLING MEDIUM & UTILITIES

37 NYSE : TLM | TSX : TLM www.talisman-energy.com

The Talisman approach to improvements made Strong Leadership and Focus

Engage and enable the organisation

Ensure sustainability: HSE – Cost – Regularity

Continual challenge:

Reward Achievements

Contractor improvements must be addressed

Break down barriers and be flexible on use of resources

Fix the Basics

Establish standards

Regenerate critical infrastructure

38 NYSE : TLM | TSX : TLM www.talisman-energy.com

0

5

10

15

20

25

30

35

2008 2010 2011 (Q1) 2011 2012

21

Gyda offshore manning levels

32

19

24 22

Asset OPEX Budget [mm$]

Gyda 70

Brage 1.484

Veslefrikk 141.6

39 NYSE : TLM | TSX : TLM www.talisman-energy.com

Gyda – “The Best Place To Be” For our Employees

For our Suppliers

For a future Tie-In customer

The Gyda Experience

Sustainable, Safe and Efficient Operations

Prudent Hub, focused on delivering results and driving change

Co-operative and proficient approach in daily follow-through of activities

Strong HSE focus

High Facility uptime

Cost conscious approach

40 NYSE : TLM | TSX : TLM www.talisman-energy.com

-Minimum manning spec -New criticality assessment

-New maintenance strategy

-Reduced Manning -PM reduction -Cost reduction

-Total mhr reduction -Improved backlog

-Legislated Classification -Steady low mhr consumption -Zero safety critical backlog

Implementation and Opex reduction

29

33

30

32

20

26

31 29

15

17

19

21

23

25

27

29

31

33

35

2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

$

41 NYSE : TLM | TSX : TLM www.talisman-energy.com

AE country averages by year % estimated production potential

Average estimated inflation rate % 2003-2013

Brent, WTI prices and futures US$

Asset Efficiency is dropping Costs have soared Oil price looks set to remain low

70

75

80

85

90

95

0 5 10 15 20 25

NCS (Year 0 = 2003)

UKCS (Year 0 = 1993)

2.71.8

North Sea CAPEX

16-20

North Sea OPEX

10-12

UK CPI

Norway CPI

The case for change is very strong: Our industry in the North Sea faces a real challenge

130

90

120 110 100

80 70 60 0 2012 2020

42 NYSE : TLM | TSX : TLM www.talisman-energy.com

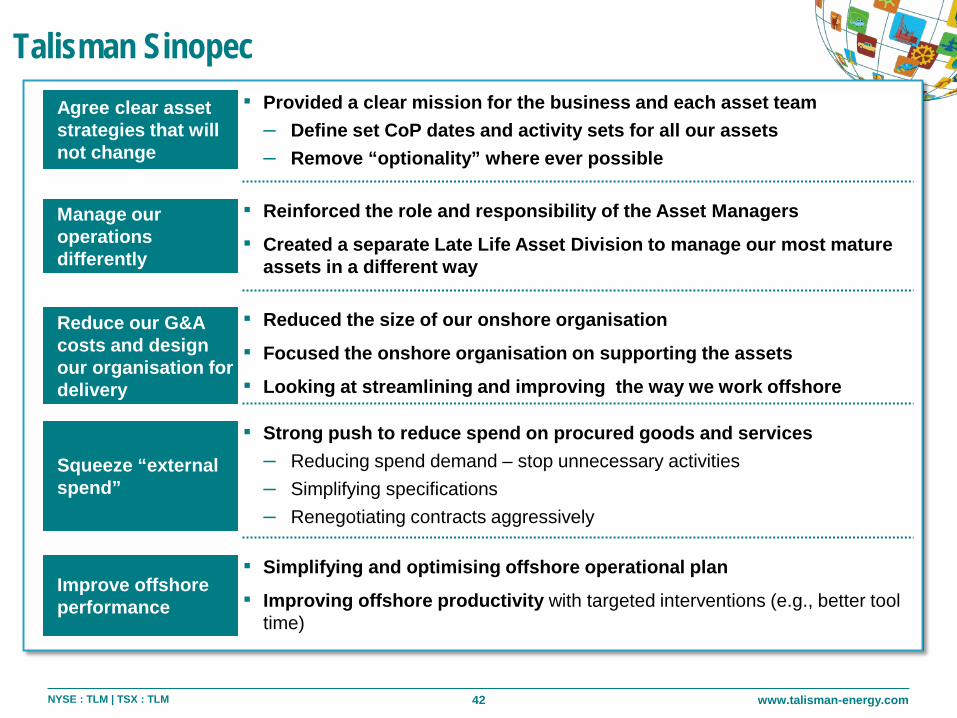

Talisman Sinopec Agree clear asset strategies that will not change

▪ Provided a clear mission for the business and each asset team – Define set CoP dates and activity sets for all our assets – Remove “optionality” where ever possible

Manage our operations differently

▪ Reinforced the role and responsibility of the Asset Managers

▪ Created a separate Late Life Asset Division to manage our most mature assets in a different way

Reduce our G&A costs and design our organisation for delivery

▪ Reduced the size of our onshore organisation

▪ Focused the onshore organisation on supporting the assets

▪ Looking at streamlining and improving the way we work offshore

Squeeze “external spend”

▪ Strong push to reduce spend on procured goods and services – Reducing spend demand – stop unnecessary activities – Simplifying specifications – Renegotiating contracts aggressively

Improve offshore performance

▪ Simplifying and optimising offshore operational plan

▪ Improving offshore productivity with targeted interventions (e.g., better tool time)

43 NYSE : TLM | TSX : TLM www.talisman-energy.com

We are managing the change rigorously

Defined stage gates to collect and work up interventions

L2 L3

L4 L5

L1

Impact accrued

Impact accruing

Initiatives being

planned and

prepared for approval

Initiatives in imple-

mentation

Ideas being

turned into initiatives

Major activities completed

Fully realized

Approved for implementation

Prioritised for plan-ning

Idea sized

Core meetings

Workstream check-in (as needed, multiple times a week)

Cross-cutting check-in (30mins)

TO with Workstreams (90 mins per workstream)

MD catch-up (30 minutes)

Core Group1 meeting (~2 hours)

Board update (30 mins)

Mon Tue Wed Thu Fri

An aggressive, weekly schedule to monitor progress

44 NYSE : TLM | TSX : TLM www.talisman-energy.com

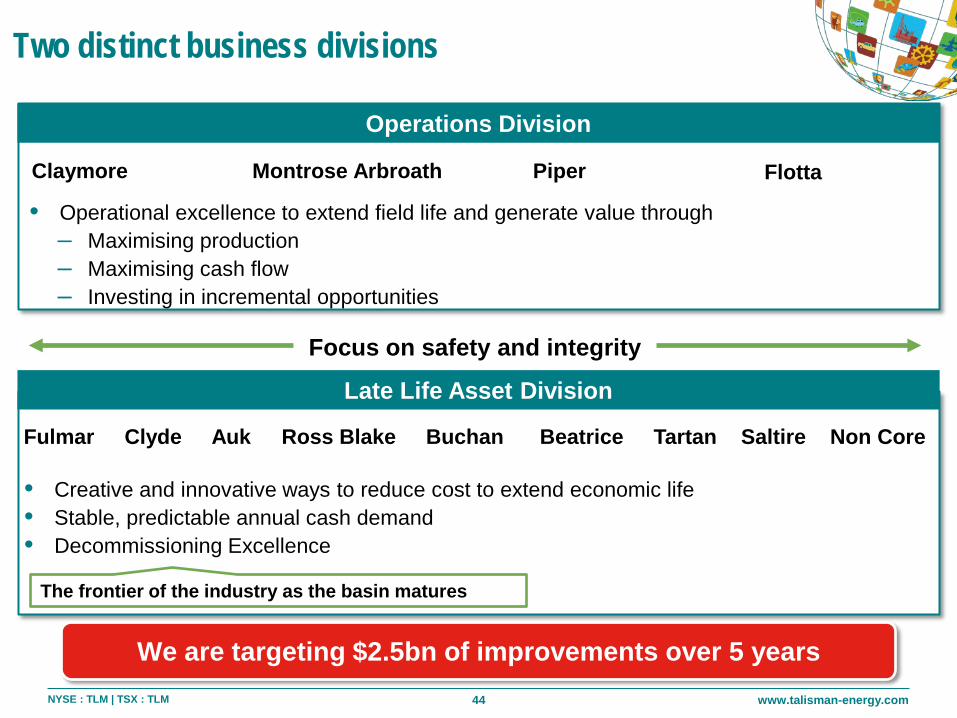

Focus on safety and integrity

Two distinct business divisions

Montrose Arbroath Claymore Piper Flotta

• Creative and innovative ways to reduce cost to extend economic life • Stable, predictable annual cash demand • Decommissioning Excellence

• Operational excellence to extend field life and generate value through – Maximising production – Maximising cash flow – Investing in incremental opportunities

The frontier of the industry as the basin matures

Late Life Asset Division

Fulmar Clyde Auk Ross Blake Buchan Beatrice Tartan Saltire Non Core

Operations Division

We are targeting $2.5bn of improvements over 5 years

45 NYSE : TLM | TSX : TLM www.talisman-energy.com

Aberdeen Breakfast Briefing – Cost Efficiency

Aberdeen Breakfast Briefing - Cost Efficiency

Chaired by Oonagh Werngren, Oil & Gas UK

This morning’s panelists are …

Dan Cole, Mckinsey & Company

Gordon Ballard, Schlumberger UK

Paul Warwick, Talisman Energy Inc.

Colette Cohen, Centrica E&P

Forthcoming Events – 2015 • 19 May Breakfast Briefing - Cost Efficiency (London) • 19 May EU Directive Seminar (Aberdeen)

• 21 May Training Course: Supply Chain Solutions (Aberdeen)

• 02 June Aviation Seminar (Aberdeen)

• 17- 18 June The Oil and Gas Industry Conference (Aberdeen)

• 30 June Oil & Gas UK Members Speed Networking (London)

• 30 June Supply Chain Seminar (Aberdeen)

Visit: www.oilandgasuk.co.uk