abn-amro - mobile networks - w

DESCRIPTION

mobile networks studyTRANSCRIPT

Industry250 Bishopsgate

London EC2M 4AA, UK

Tel: + 44 20 7678 8000

Fax: + 44 20 7678 7353

A S I A P A C I F I C

Hong Kong

ABN AMRO Asia Ltd

38th Floor, Cheung Kong Center

2 Queen’s Road Central, Hong Kong

Tel: +852 2700 3000

Tlx: HX 74111

Fax: +852 2700 5000

Auckland

ABN AMRO Equities (NZ) Ltd

+64 9 358 7500

Bangkok

ABN AMRO Asia Securities Public

Company Limited

+66 2 679 5790

Bombay

ABN AMRO Asia Equities (India) Ltd

+91 22 285 4363

Jakarta

PT ABN AMRO Asia Securities (Indonesia)

+62 21 515 1880

Kuala Lumpur

ABN AMRO Asia Equity Research

(Malaysia) Sdn Bhd

+60 3 2166 8213

Makati City

ABN AMRO Asia Securities (Philippines) Inc.

+63 2 867 7800

Port Louis

SBM ABN AMRO Asia Securities Ltd

+230 202 1473

Seoul

ABN AMRO Asia Limited

+82 2 2131 6400

Shanghai

ABN AMRO Asia Ltd

+86 21 5049 6333

Singapore

ABN AMRO Asia Securities

(Singapore) Pte Limited

+65 536 7688

Sydney

ABN AMRO Equities Australia Ltd

+61 2 8259 5000

Taipei

ABN AMRO Bank NV

+886 2 25037888

E U R O P E A N D A F R I C A

United Kingdom

ABN AMRO Equities (UK) Ltd

250 Bishopsgate

London EC2M 4AA, UK

Tel: +44 20 7678 8000

Fax: +44 20 7678 7353

Netherlands

ABN AMRO Bank N.V.

Gustav Mahlerlaan 10

1082 PP Amsterdam

The Netherlands

Tel: +31 20 628 9393

Fax: +31 20 628 7740

Brussels

ABN AMRO Bank N.V.

+32 2 546 0460

Bucharest

ABN AMRO Bank (Romania) S.A.

+40 1 2 020 400

Cairo

ABN AMRO Delta Securities (Egypt)

+20 2 3317480

Copenhagen

Alfred Berg Bank A/S

+45 33 961000

Dublin

ABN AMRO Stockbrokers (Ireland) Ltd

+353 1 609 3700

Frankfurt

ABN AMRO Bank (Deutschland) AG

+49 69 2690 00

Helsinki

Alfred Berg Finland Oy Ab

+358 9 228 321

Istanbul

ABN AMRO Bank NV

+90 212 2938802

Johannesburg

ABN AMRO Bank NV

+27 11 685 2000

Madrid

ABN AMRO Equities (Spain) S.A. SVB

+34 91 423 6900/82

Milan

ABN AMRO Bank N.V.

+39 02 722671

Oslo

Alfred Berg Norge A/S

+47 22 005000

Paris

ABN AMRO Securities (France) S.A.

+33 1 56 21 5000

Stockholm

Alfred Berg Fondkommission AB

+46 8 7235800

Warsaw

ABN AMRO Securities (Polska) S.A.

+48 22 573 0500

T H E A M E R I C A S

New York

ABN AMRO Inc.

Park Avenue Plaza

55 East 52nd Street,

6th Floor

New York, New York 10055

Tel: +1 212 409 1000

Fax: +1 212 409 5224

Boston

ABN AMRO Inc.

+1 617 753 6900

Chicago

ABN AMRO Inc.

+1 877 711 1781

Houston

ABN AMRO Inc.

+1 832 681 7100

Mexico

ABN AMRO Securities (Mexico) SA

+52555 2577800

San Francisco

ABN AMRO Inc.

+1 415 659 3086

Sao Paulo

Banco ABN AMRO Real

+55 11 31742600

Jamie Mariani

+44 20 7678 0243

Rodney Sherrington

+44 20 7678 1610

Marketing Analyst

Simon Carrington

+44 20 7678 0395

October 2002Pan-European Telecoms

3G Tsunami: the revolution begins

� The 3G growth opportunity

exists - in voice, not data,

services

� Network capacity could grow

five-fold

� 58% price cuts may deliver

30% ARPU growth by 2006

� Wireless stocks to rerate,

after initial period of

readjustment

� mmO2 and Orange offer

greatest long-term upside

potential

Pan

-Eu

ro

pean

Tele

co

ms

3G

Tsu

nam

i: the r

evo

lutio

n b

eg

ins

Octo

ber 2

00

2

3G-tsnunami-cov 15/10/02, 12:03 pm1

Please refer to terms relating to the provision of this research at the end of the document.

http://www.abnamroresearch.com

ABN AMRO UK250 BishopsgateLondonEC2M 4AAUnited Kingdom

IndustryMobile Networks - W. Europe

3G Tsunami: The revolution beginsLonger-term flat rate access plans and pre-to-post-paid migration

will drive structurally higher ARPUs and increased cash flow per sub.

In the interim price reductions will put pressure on margins. We

maintain a neutral stance and highlight mmo2 (Buy from Add) and

Orange (Buy) as preferred plays.

Summary of recommendations

New Recomm. Old Recomm. Price Target

Mmo2 Buy Add 60p

Orange Buy Buy €7.0

TIM Hold Hold €4.1

TEM Hold Hold €6.0

Vodafone Add Add 105pSource: ABN AMRO

The European cellular equity story has changed. While stale bulls

continue to cling to the 'blue sky' mobile data service vision, mobile voice

communication is the killer application. We believe wireless networks will

account for 30%-40% of originated traffic (from 10%-15% today),

structurally shifting ARPU by up to 30% by end 2006.

New entrant competition: We anticipate that H3G will adopt bucket

pricing plans throughout its operations in Europe (similar to VoiceStream in

the US). Aggressively priced bundles charged at a flat rate fee could result

in a structural shift in European cellular's share of GDP.

In Europe, 3G capacity enables voice substitution. We believe 3G

will increase available capacity by up to 5x in some markets. As wireless

voice prices decline towards a 50% premium to underlying fixed line prices,

we expect a material displacement of volume from fixed to mobile.

Ahead of rising ARPU, lower prices will hit profitablity, due to

declining gross telephony margins. Ironically, operators with

disproportionate exposure to the corporate market could suffer most, as

they cannabalise higher-value customers.

Prior to CYQ3 results we continue to prefer Orange (Buy) and mm02

(Buy from Add). We have reduced our price targets for TIM (€4.1 from €4.4)

and TEM (€6 from €6.7).

16 October 2002

Jamie Mariani

[email protected]+44 207 678 0243

Rodney Sherrington

[email protected]+44 207 678 1610

Telecom Networks

W. Europe

Europe-Ds Telecom Services

605.74

Sector Performance

435

935

1435

1935

2435

Aug-99 Aug-00 Aug-01

I N D US TR Y D E V E LO P M E N TS > CO R P O R A T E S TR A TEG Y

(1M) (3M) (12M)

Absolute -4.9% -6.6% -21.0%

Source: Datastream

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 2

In Brief…

What's ChangedPerformance. European wireless stocks have outperformed strongly since we last

looked in detail at the subsector (European Cellular Bear Trap dated 9 July 2002).

Industry restructuring, strong Q202 results and scope for even better numbers at the

Q3s have underpinned this achievement. Our preference for beta has been partially

validated with strong relative performance from Orange (Buy), Vodafone (Add) and

mmo2 (Buy from Add). To the end of the Q302 results season, we expect continued

strong share price movements. Beyond November the key management challenge will

be to turn volume into value.

Chart 1 : Relative share price performance (09/07/02 to date)

-20%-15%

4% 6% 7%10%

19%

-6%

-25%

-15%

-5%

5%

15%

25%

35%

FTSE EURO100

DJ Stoxx 50 FTSE GlobalTelco Services

TEM TIM mmo2 Vodafone Orange

Percentage change

Top picks

Source: ABN AMRO

Capacity and competition. The deployment of 3G networks throughout Europe will

increase capacity by up to 5x (with Italy most affected). Contrary to consensus

expectations (which focus on the long-promised data wave), we suspect that H3G

could introduce “bucket” pricing plans. It is our core belief that as cellular prices move

to a 50% premium to underlying fixed line prices, mass substitution could occur. We

believe that wireless networks will account for 30%-40% of originated traffic (from

10%-15% today), structurally shifting ARPUs by up to 30% by end 2006.

Unfortunately changing business model is unlikely to frictionless. We expect a

minimum 300-500bp contraction in margin.

Recommendations. We have upgraded mmo2 to Buy (from Add) and increased our

fair value estimate to 60p, reflecting recent consolidation in the German market and

the prosect of further restructuring. The Buy recommendation on Orange is

maintained, with a price target of €7. Price targets for the southern European

operators have been lowered to €4.1 and €6.0 for TIM and TEM respectively. We areleaving our view on Vodafone unchanged (Add, 105p price target).

E X E C U T I V E S U M M A R Y

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 3

A C T I O N P O I N T S

■ Ahead of CYQ302 results we prefer Orange and mmo2. This is framed

with reference to our core belief that in the event of (1) industry

restructuring, (2) strong Q3 (over Q2) ARPU expansion higher-risk stocks

will outperform.

■ During the medium term (into 2003), we would consider a change in

stance, reflecting our core belief that a change in business model (to

bucket pricing from tariff plans) could dramatically contract margins

(300-500bp). Operators with corporate exposure (eg Vodafone) look

particularly exposed. Longer term we continue to prefer the higher-beta

plays, recognising the potential of F2M substitution.

Issues to Consider

The mobile data services vision is increasingly bankrupt. The core problem

facing Europe’s wireless operators is simple, identifying opportunities large enough to

drive top-line growth today’s absolute level. In our view, data services should be

viewed as an incremental bonus. Disciplined capital investment should require focuson revenue streams, where sufficient demand exists to validate investment.

Fixed to mobile substitution offers a compelling second leg of growth. In the

short term, pre-to-post-paid migration is the most important driver of the top line.

Our forecasts imply 4%-8% blended ARPU growth from this dynamic over the next

four years. During the medium term we expect wireless networks to grab 30%-40%

share of outgoing total traffic by year-end 2006, driven by price cuts of about 50%-

60%. This could structurally shift ARPU upwards by around 30% by year-end 2006.

Bucket pricing plans facilitate displacement and are superior. US operators

have maintained high ARPUs by not targeting lower value prepaid subs, and through

the introduction of bucket plans. The US model generates higher EBITDA per

subscriber. Similar to the impact VoiceStream had on the US, H3G could be thecatalyst in Europe for driving voice substitution through flat rate access.

3G provides capacity to drive wireline volume displacement. European 2G

capacity constraints have prohibited the introduction of bucket pricing plans. We do

not buy into the “3G is data” proposition (3G is capacity). We estimate that W-CDMA,

using a conservative 20% increase in spectral efficiency, results in a 1.7x-2.8xincrease in capacity. In densely populated areas, capacity could increase by up to 5x.

Switching between business models will cause friction. In our view (should

bucket pricing plans emerge), a margin contraction is inevitable. Dramatically falling

prices will drive structurally lower gross telephony margins. Ironically, operators with

exposure to the corporate market could be the worst affected. Notwithstanding this

uncertainty, longer-term investors should view fixed to mobile substitution as a

potentially unique opportunity. We cannot think of any other sector in the wider

economy that offers such easily identifiable growth.

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 4

Contents

I N D U S T R Y D Y N A M I C S

Data services dream 7

The mobile data services vision appears increasingly bankrupt. Global SMSrevenue amounted to about US$13bn (approximately £8.7bn) in 2001,contributing a mere 4% to total global mobile revenue of nearly US$300bn(approx...

Introduction 7

M A C R O D Y N A M I C S

Fixed to mobile substitution 21

In the short term, pre-to-post-paid migration is the most important driver ofrevenue growth. We believe high prepaid call charges have stunted usage. Ourforecasts imply about 4% annual growth in blended ARPU over the n...

Introduction 21

I N V E S T M E N T V I E W

Bucket pricing plans 45

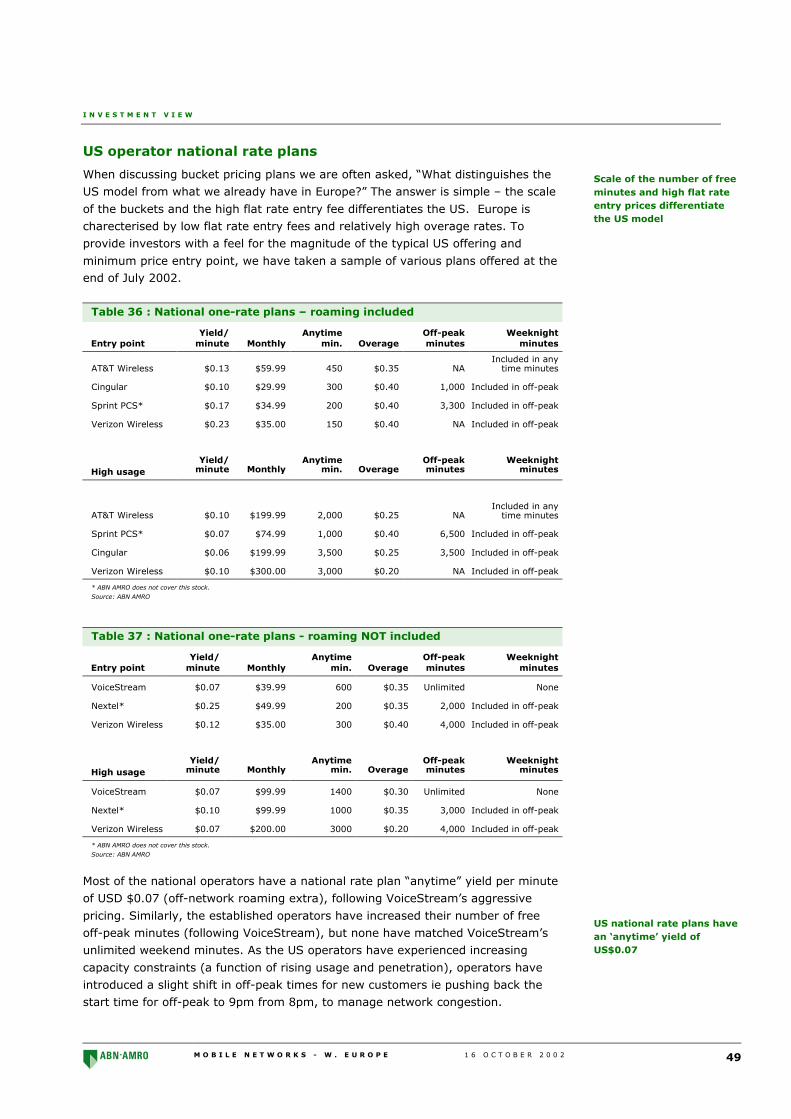

Despite intense competition, US operators have maintained high ARPU levels bynot targeting lower-value prepay subscribers, and through the introduction of“bucket plans.” US operators have increased the number of free m...

Introduction 45

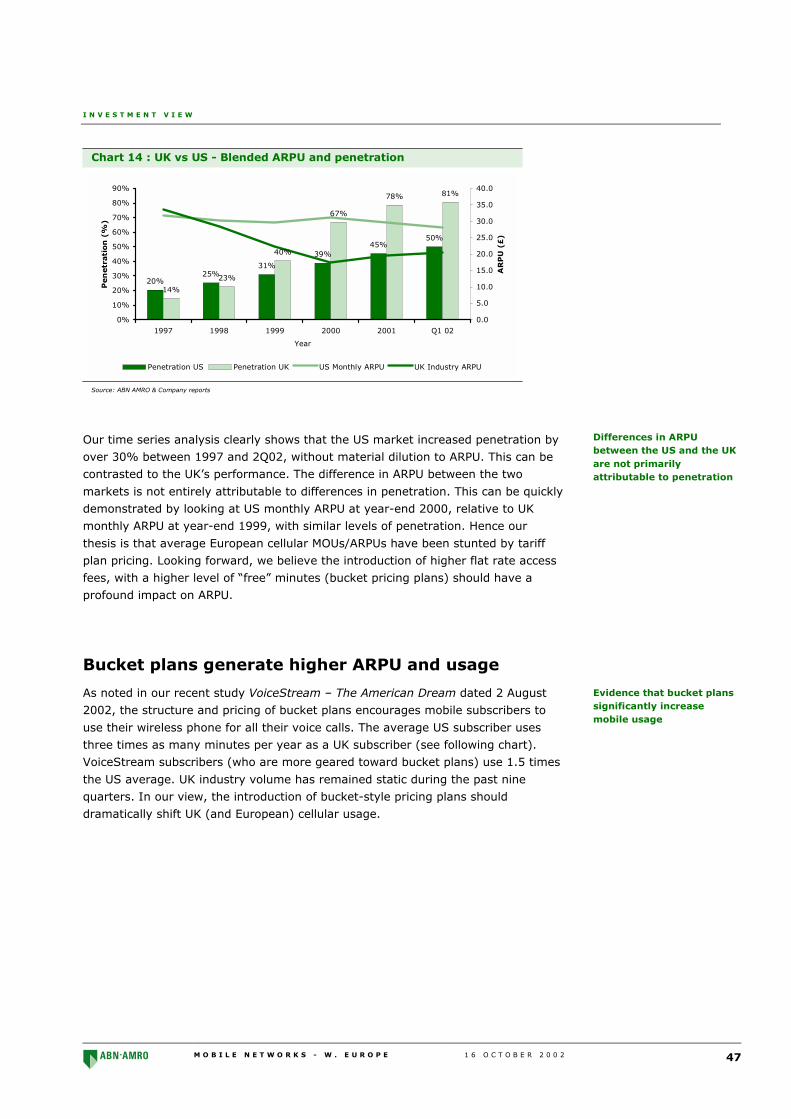

Bucket plans generate higher ARPU and usage 47

Average yield based on actual minutes used 51

S E C T O R D Y N A M I C S

3G as the facilitator 59

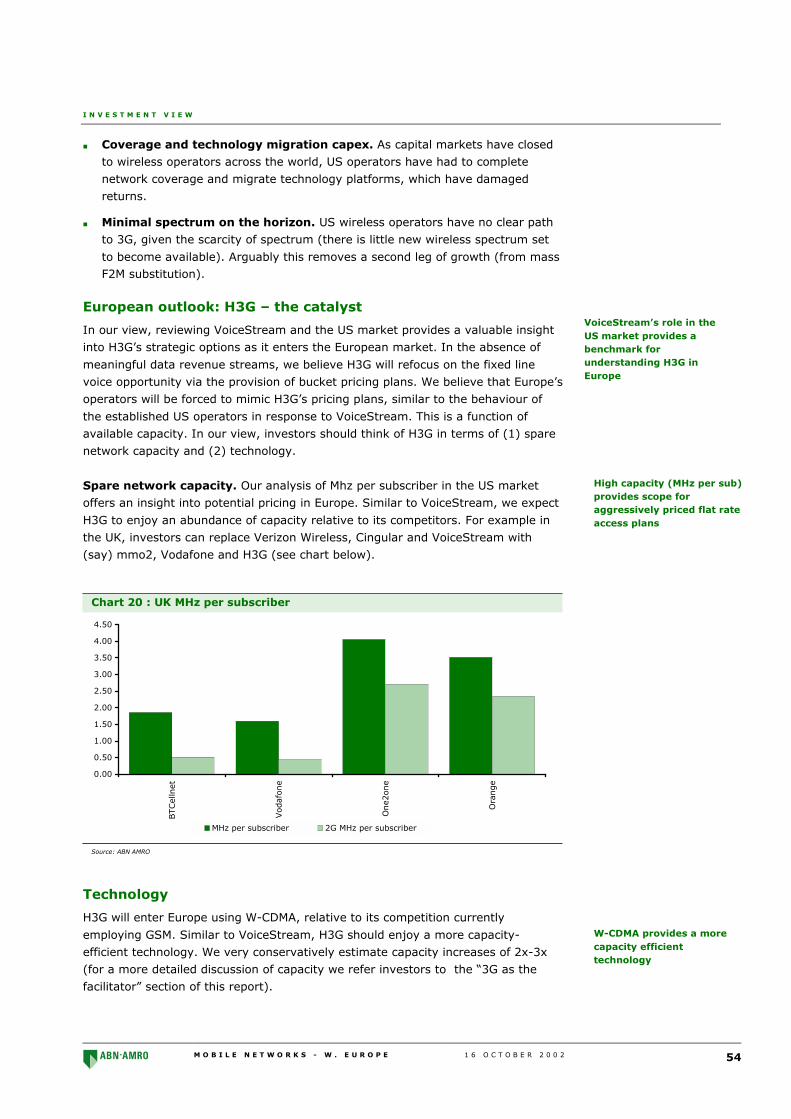

In our view, European 2G capacity constraints have prohibited the introduction ofbucket pricing plans (and by association fixed-to-mobile substitution). While 3Gmay facilitate the use of high-speed applications, the re...

Introduction 59

N E W S H I G H L I G H T

Fixed-line tariff rebalancing 71

Fixed-line tariff rebalancing is a significant topic that merits more space than wehave in this note (hence our intention to revisit it at a later date). However, wemust recognise that fixed line tariff rebalancing pro...

Background 71

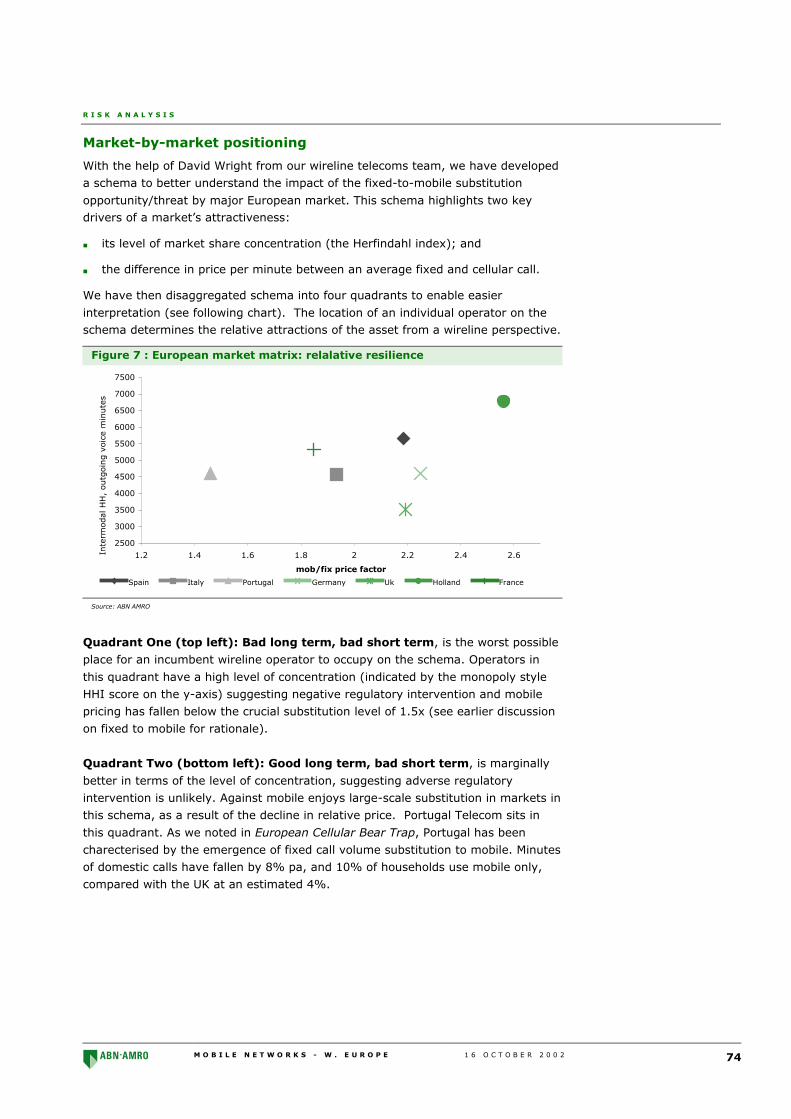

R I S K A N A L Y S I S

Economic impact 73

We see between 10% and 25% upside from our existing fair value estimates forthe European wireless community as a result of (1) our pre-to-post-paidmigration thesis and (2) our central case fixed-to-mobile substitution...

Timing 73

T A B L E O F C O N T E N T S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 5

A P P E N D I X

European 3G licensing conditions 81

In this section we have presented regulatory requirements for rollout by majorEuropean market. License duration ranges between 12 and 20 years, with sharplydivergent coverage requirements by country. In Korea, we note...

Technical glossary 82

Erlang 82

T E A M

Acknowledgements 83

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 6

This page has been left intentionally blank

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 7

I N D U S T R Y D Y N A M I C S

Data services dream

The mobile data services vision appears increasingly bankrupt. Global SMS revenue

amounted to about US$13bn (approximately £8.7bn) in 2001, contributing a mere

4% to total global mobile revenue of nearly US$300bn (approximately £200bn). In

the E5 (France, Germany, Italy, Spain and the UK), we estimate mobile revenue of

€75bn was generated during 2001. The core problem facing Europe’s wireless

operators is simple, identifying opportunities large enough to drive top-line growth

from this absolute level. Contrary to some commentators’ expectations, we do not

believe that MMS will materially affect European operators’ top line during the next

24 months. Disciplined capital investment should require operators to focus on

identifiable revenue streams. In our view data should be viewed as an incremental

“bonus.”

Introduction

In this section of the note we present:

■ the size of the E5 voice and data market (€75bn and €6bn, respectively);

■ the absolute revenue required to generate a material upside surprise (€9bn);

■ the validity of operator-articulated targets for data as a percentage of revenue;

■ our view on the sustainability of the low volume/high prices of SMS;

■ the problem of scale – why MMS will struggle to drive growth;

■ the potential cannibalisation of voice/SMS by MMS; and

■ a preliminary assessment of the margin/capex impact of take-up.

Data services lookincreasingly like the ‘bettermousetrap’ nobody wants

I N D U S T R Y D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 8

European revenue

In the E5, we estimate that mobile revenue of €75bn was generated during 2001,

accounting for about 1.1% of GDP. The problem facing Europe’s major operators is

clear – identifying opportunities large enough to generate material growth from thisabsolute number.

Table 1 : E5 total revenue (€m) calendarised

1999E 2000E 2001E

France 8,863 12,343 15,046

% Change 39% 22%

Germany 10,729 15,057 16,480

% Change 40% 9%

Italy 11,671 13,808 15,534

% Change 18% 12%

Spain 6,523 8,107 9,615

% Change 24% 19%

UK 11,975 16,384 18,582

% Change 37% 13%

Total E5 49,761 65,699 75,257

% Change 32% 15%

Source: ABN AMRO estimate

Data revenue

Relative to the absolute size of the European cellular market, data pales by

comparison. We calculate that data revenue of €6.3bn was posted in 2001,

corresponding to a small 8.3% of the total top line, or nearly 10% of service

revenue.

Major operator revenue outlook

As the absolute size of operators’ revenue line grows further, future growth

becomes more difficult. We calculate that to deliver 5%-10% upside surprise at the

top line, Europe’s major operators would need to generate an additional €4.5bn-

9.0bn to December 2002/March 2003 (see following table), corresponding to thetotal top line of the UK IT Hardware sector.

Table 2 : Revenue by major operator

Unit Revenue2002/03F

5% Upside 10% upside

mmo2 £m 4,815 241 481

Orange €m 16,877 844 1,688

TIM €m 10,648 532 1,065

TEM €m 9,096 455 910

Vodafone £m 29,480 1,474 2,948

Total Revenue €m 88,063 4,403 8,806

Source: ABN AMRO

Wireless revenue of €75bnwas generated during 2001in the E5

Scale creates growthdifficulties

Revenue upside would needto register scale in line withthe top line of the UK IThardware sector

I N D U S T R Y D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 9

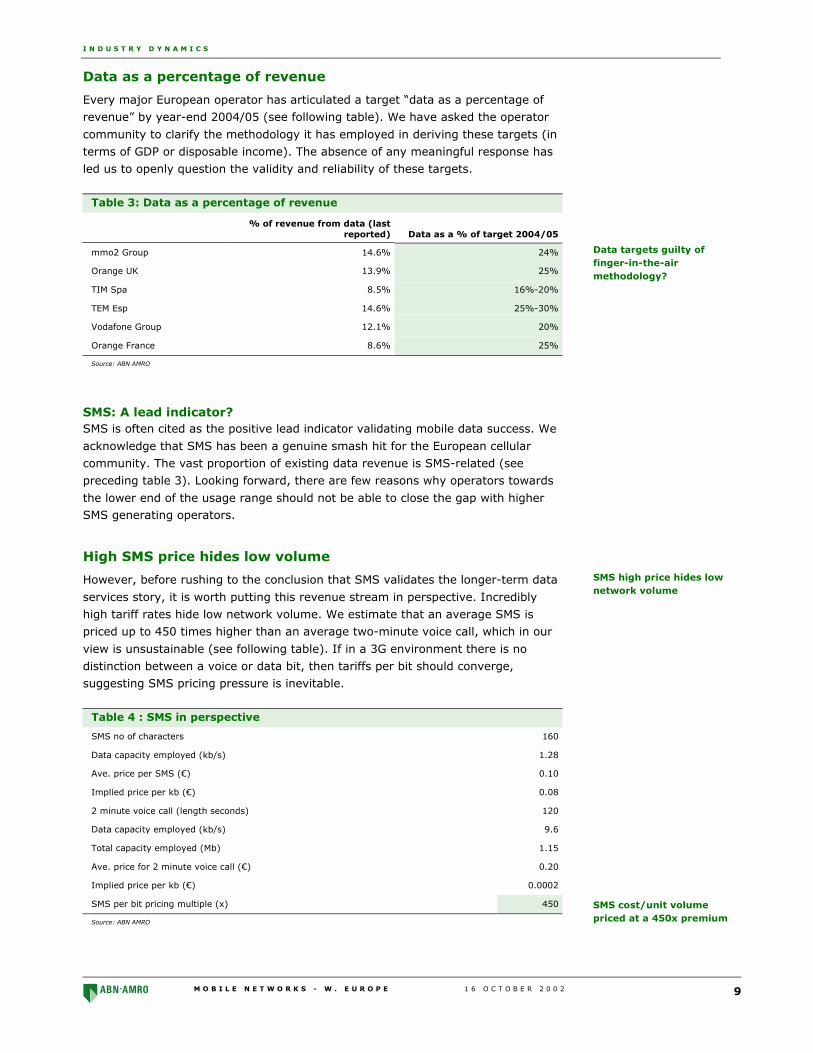

Data as a percentage of revenue

Every major European operator has articulated a target “data as a percentage of

revenue” by year-end 2004/05 (see following table). We have asked the operator

community to clarify the methodology it has employed in deriving these targets (in

terms of GDP or disposable income). The absence of any meaningful response has

led us to openly question the validity and reliability of these targets.

Table 3: Data as a percentage of revenue

% of revenue from data (lastreported) Data as a % of target 2004/05

mmo2 Group 14.6% 24%

Orange UK 13.9% 25%

TIM Spa 8.5% 16%-20%

TEM Esp 14.6% 25%-30%

Vodafone Group 12.1% 20%

Orange France 8.6% 25%

Source: ABN AMRO

SMS: A lead indicator?SMS is often cited as the positive lead indicator validating mobile data success. We

acknowledge that SMS has been a genuine smash hit for the European cellular

community. The vast proportion of existing data revenue is SMS-related (see

preceding table 3). Looking forward, there are few reasons why operators towards

the lower end of the usage range should not be able to close the gap with higherSMS generating operators.

High SMS price hides low volume

However, before rushing to the conclusion that SMS validates the longer-term data

services story, it is worth putting this revenue stream in perspective. Incredibly

high tariff rates hide low network volume. We estimate that an average SMS is

priced up to 450 times higher than an average two-minute voice call, which in our

view is unsustainable (see following table). If in a 3G environment there is no

distinction between a voice or data bit, then tariffs per bit should converge,

suggesting SMS pricing pressure is inevitable.

Table 4 : SMS in perspective

SMS no of characters 160

Data capacity employed (kb/s) 1.28

Ave. price per SMS (€) 0.10

Implied price per kb (€) 0.08

2 minute voice call (length seconds) 120

Data capacity employed (kb/s) 9.6

Total capacity employed (Mb) 1.15

Ave. price for 2 minute voice call (€) 0.20

Implied price per kb (€) 0.0002

SMS per bit pricing multiple (x) 450

Source: ABN AMRO

Data targets guilty offinger-in-the-airmethodology?

SMS high price hides lownetwork volume

SMS cost/unit volumepriced at a 450x premium

I N D U S T R Y D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 10

Actual capacity used close to 0%

We estimate that SMS traffic is close to 0% of total traffic carried. Even in the

youth segment (the keenest users of SMS), we understand that SMS traffic

represents less than 0.5% of total traffic. We can demonstrate this with reference

to TIM, the leading Italian operator. To June 2002, TIM generated 17.8bn voice

minutes and 3.8bn messages (see following table).

Table 5 : SMS capacity in perspective

Jun-02

Voice minutes (m) 17,842

Average length (seconds) 60

Capacity employed per second (kb/s) 9.6

Capacity employed per minute (kb/s) 576.0

Total capacity employed (Mb) 10,277

SMS volume (m) 3,826

Ave. no of characters per SMS 160

Capacity employed per SMS (kb/s) 1.28

Capacity employed (Mb) 4.9

SMS as a % of total traffic 0.05%

Source: ABN AMRO

We calculate that SMS as a percentage of total traffic accounts for about 0.05% of

usage. While Italy does not “lead the curve” in terms of SMS usage, our example

underlines an important point, namely, the tiny volume contribution of SMS.

Regulator interest in SMS

We also note that OFTEL, the UK regulator, is examining UK SMS termination rates,

following a complaint by an unnamed operator. At present, SMS termination rates

are unregulated, leaving operators free to set rates. The four UK operators

currently charge a termination rate of 3p per message. This is approximately 3x the

rate of fixed-line termination charges in the UK, and 30% of voice cellular

termination fees. A risk to forecasts is that the “cost price” of SMS becomes an

important determinant of retail prices as a result of regulatory intervention. We

also highlight the role OFTEL plays as an opinion leader in European regulation.

MMS: The silver bullet?Multimedia Messaging Service (MMS) allows users to send and receive messages

with colour photos, voice, sound and text. Data bulls have suggested that the MMS

has immense potential (see following chart). According to Mobile Streams by 2008,MMS volume globally is expected to be double that of SMS.

SMS capacity used minimal

TIM SMS less than 1% oftotal traffic

SMS termination rates maycome under increasingscrutiny

Data bulls continue tobelieve in the ‘power’ ofMMS

I N D U S T R Y D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 11

Chart 2 : Monthly mobile messaging volume at year-end, 2002-2008

0

10,00

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,00

Monthly total global Monthly total global

Monthly total global

Source: Mobile streams

Our discussions with investors suggest to us that MMS is still perceived as the silver

bullet for European cellular. Following the somewhat unexpected success of SMS,

the market appears to believe that MMS provides the next step on the long path to

build a credible mobile data equity story.

2002/03: An important year for messaging?MMS was widely launched across Europe during 1H02. Historically, we (incorrectly)

viewed the potential of MMS as the largest potential upside risk to our short-term

forecasts. Today we do not expect a material impact on group revenue for any ofEurope’s major cellular operators this year (or next year) from MMS.

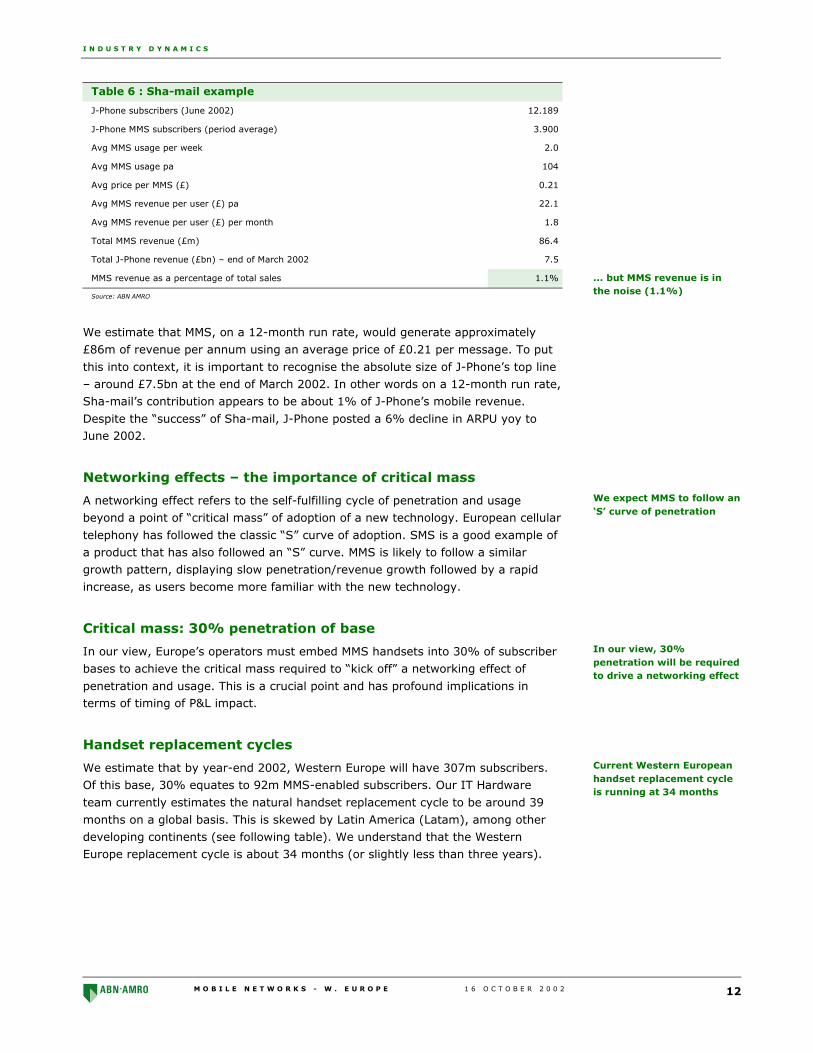

The problem of scale – Sha-mail lead indicator?

The J-Phone service Sha-mail is often cited as an example of the success of MMS,

although Vodafone (J-Phone’s owner) does not disclose the top-line contribution.

We understand the following.

■ Historically, J-Phone has charged between €0.12 and €0.33 per message (about

£0.21, at the top end).

■ At year-end (March 2002), J-Phone had 4 million camera phone customers

(about one-third of the subscriber base).

■ At the end of August 2002, J-Phone had 6m Sha-mail enabled handsets (at theend of August 2001, J-Phone had approximately 1.8m Sha-mail handsets sold).

■ To August, J-Phone had a 12-month period-average number of Sha-mailsubscribers of 3.9m.

■ In early 2002 (at the time of the J-Phone presentation to analysts, 28 February

2002), Vodafone management indicated that the J-Phone picture messagingservice was being used about twice a week.

For simplicity, we have factored in a constant “two messages sent a week” scenarioto calculate the revenue generated from MMS.

MMS silver bullet statusprovides some hope ...

... but ignores theimportance of handsetreplacement and top-lineabsolute scale

Sha-mail is often cited asexample of MMS success

I N D U S T R Y D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 12

Table 6 : Sha-mail example

J-Phone subscribers (June 2002) 12.189

J-Phone MMS subscribers (period average) 3.900

Avg MMS usage per week 2.0

Avg MMS usage pa 104

Avg price per MMS (£) 0.21

Avg MMS revenue per user (£) pa 22.1

Avg MMS revenue per user (£) per month 1.8

Total MMS revenue (£m) 86.4

Total J-Phone revenue (£bn) – end of March 2002 7.5

MMS revenue as a percentage of total sales 1.1%

Source: ABN AMRO

We estimate that MMS, on a 12-month run rate, would generate approximately

£86m of revenue per annum using an average price of £0.21 per message. To put

this into context, it is important to recognise the absolute size of J-Phone’s top line

– around £7.5bn at the end of March 2002. In other words on a 12-month run rate,

Sha-mail’s contribution appears to be about 1% of J-Phone’s mobile revenue.

Despite the “success” of Sha-mail, J-Phone posted a 6% decline in ARPU yoy toJune 2002.

Networking effects – the importance of critical mass

A networking effect refers to the self-fulfilling cycle of penetration and usage

beyond a point of “critical mass” of adoption of a new technology. European cellular

telephony has followed the classic “S” curve of adoption. SMS is a good example of

a product that has also followed an “S” curve. MMS is likely to follow a similar

growth pattern, displaying slow penetration/revenue growth followed by a rapid

increase, as users become more familiar with the new technology.

Critical mass: 30% penetration of base

In our view, Europe’s operators must embed MMS handsets into 30% of subscriber

bases to achieve the critical mass required to “kick off” a networking effect of

penetration and usage. This is a crucial point and has profound implications interms of timing of P&L impact.

Handset replacement cycles

We estimate that by year-end 2002, Western Europe will have 307m subscribers.

Of this base, 30% equates to 92m MMS-enabled subscribers. Our IT Hardware

team currently estimates the natural handset replacement cycle to be around 39

months on a global basis. This is skewed by Latin America (Latam), among other

developing continents (see following table). We understand that the Western

Europe replacement cycle is about 34 months (or slightly less than three years).

... but MMS revenue is inthe noise (1.1%)

We expect MMS to follow an‘S’ curve of penetration

In our view, 30%penetration will be requiredto drive a networking effect

Current Western Europeanhandset replacement cycleis running at 34 months

I N D U S T R Y D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 13

Table 7: Replacement cycle (months)

2000 2001 2002E 2003E

Europe (W & E) 24 31 35 35

- W Europe 24 30 34 34

- E Europe 34 39 48 40

Middle East & Africa 33 32 44 45

Asia/Pacific 34 37 46 47

North America 27 31 33 32

South America 30 37 50 48

Total 28 33 39 39

Source: ABN AMRO IT Hardware equity research team

A three-year handset replacement cycle suggests an annual rate of handset churn

of nearly 33%. Even if 50% of the replacement handsets sold during 2003 were

MMS-enabled this corresponds to only 17% of Western Europe’s existing subscriber

base owning an MMS-enabled handset by calendar year-end 2003, some distance

below the critical mass level we estimate is required to drive usage/revenue.

Using the 34-month handset replacement cycle, Western Europe would need to

wait until year-end 2004 to reach the point of critical mass in terms of MMS

penetration. This suggests that a material revenue boost will not occur until

CY2005. Bulls of MMS beware!

What about guidance of 18 months?

We have heard some operators talking handset replacement cycles of 18 months

today, ie every one and a half years. We can sanity-check the “reasonableness” of

this claim with reference to total global handset sales. Holding “new” European

sales and ROW handset sales constant, we can identify the implied replacement

handsets sold in Europe and the impact this has on total global handset sales. For

example, if we believe that 2002 and 2003 will both have an 18-month

replacement cycle, we can imply global handset sales of 474m and 559m

respectively (see following table), somewhat ahead of our IT Hardware team’s

forecasts.

Table 8 : Scenario analysis: 18-month handset replacement cycle

2002E 2003E

Suggested replacement cycle (months) 18 18

Replacement cycle implied replacement handsetsales 153 187

Add new sales 18 13

Implied total handset WE sales 171 200

ROW handset sales 303 359

Implied total handset sales 474 559

IT Hardware forecast 402 471

Variance 72 88

Source: ABN AMRO

Nevertheless we do not rule out a shortening of the handset replacement cycle in

Western Europe, should operators choose to aggresively subsidise growth.

Even if 50% of all WesternEuropean handsets sold in2003 were MMS, only 17%of Western Europe’s basewould be MMS-enabled

MMS critical mass isreached CY2005

18-month replacementcycle would lead to materialupgrades of global handsetsale forecasts

I N D U S T R Y D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 14

Vodafone – a worked example

Using Vodafone group as a benchmark, we can quickly emphasise the importance

of absolute scale. To the end of March 2003, we forecast Vodafone to generate

£29.3bn of revenue (consolidated – see following table). To deliver a 10% upside

surprise at the top line, Vodafone would need to generate another £2.9bn in

revenue.

MMS pricing structures vary on a case-by-case basis. The average price appears to

be around €0.40-0.60 per message (about 25p-40p; outliers such as Telenor in

Norway have recently dramatically reduced their price from as much as €1.33 permessage to €0.65).

Table 9 : Vodafone – the problem of scale (£)

Mar-03 Mar-04

Vodafone consolidated revenue 29,480 31,922

Vodafone average subscribers 91.7 95.8

Vodafone consolidated ARPU 321.5 333.4

Vodafone consolidated ARPU (Monthly) 26.8 27.8

10% upside surprise (revenue) 2,948 3,192

MMS Enalbed Handsets 11% 26%

MMS Subscribers (period end) 10.4 25.2

MMS Subscribers (beginning period) 4.0 10.4

Ave. MMS Subscribers 7.2 17.8

MMS ARPU (Monthly) 34.2 15.0

Ave. price per MMS 0.25 0.25

Implied MMS volume per subscriber (Monthly) 136.9 59.9

Implied MMS volume per subscriber (Weekly) 31.6 13.8

Implied total MMS volume 11,792 12,769

Source: ABN AMRO

In our example we have factored in 11% and 26% of Vodafone’s subscriber base to

buy MMS-enabled handsets by the end of March 2003 and March 2004,

respectively, and an average price of £0.25 per message. Our basic analysis shows

that to deliver a 10% upside surprise to our existing revenue forecast, Vodafone

would need to encourage its initial MMS-enabled subscribers to pay for 31.6

messages a week to the end of March 2003 (or 13.8 messages per week to the end

of March 2004). We believe this level of volume is too challenging.

Best case: 1.5% impact

To fiscal 2004, we suspect that MMS provides at most 1.5% upside to our existing

forecasts. This view is based on three simple drivers:

■ factoring in a generous 26% of Vodafone’s base will buy (and use) MMS-enabled

handsets (implying 25.6m MMS subscribers at the end of March 2004 from10.4m at the end of March 2003);

■ usage of 2x a week (resulting in 104 messages a year);.and

■ an average price of £0.25,

Vodafone would need togenerate about £3bn ofrevenue to generate a 10%upside revenue surprise.

Using an average price of 25pper message ...

... implied volume appearschallenging: 32 messages aweek could provedemanding

I N D U S T R Y D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 15

Pulling these drivers together suggests potential incremental revenue of nearly £2.2

per month per subscriber, corresponding to £26 per year. In total, this offers

£469m of additional revenue to the end of March 2004 (about 1.5% of consolidated

revenue). This realistic upside is in the noise (see following table).

Table 10 : Vodafone impact of MMS

Mar-04

Avg MMS subs (m) 18.0

Usage pa per sub 104.0

Total usage (m) 1,875.6

Price per MMS 0.25

MMS ARPU pa 26.0

MMS ARPU (monthly) 2.2

MMS revenue (£m) 468.9

Implied % of revenue 1.5%

Source: ABN AMRO

Voice cannibalisation

We also note the potential cannibalisation of existing SMS revenue by MMS, and the

potential of MMS to substitute for voice usage. Arguably MMS can be viewed as the

classic “technology” push innovation, for which little or insufficient demand exists.

Should customers not perceive they have a real "new” need for the technology,

they could either:

■ not buy the innovation; or

■ substitute MMS for existing cellular usage.

Arguably evidence to date suggests that data has been generated at the expense of

existing voice revenue streams. In the charts that follow we show that NTT

DoCoMo,1 the widely accepted leader in data service deployment, has not yet

registered an increase in ARPU, and data ARPU appear to have been generated

largely at the expense of voice ARPU. Similarly, Vodafone’s voice ARPU in its key

European territories has continued to decline at a faster rate than blended ARPU

(assuming constant spending patterns across time), suggesting data service

cannibalisation.

1Our analysis of NTT DoCoMo ignores the impact of marginal investment costs for 2G. In Japan, a

high number of subscribers for available spectrum has led to higher capital costs (increased cost ofcell splitting), hence discouraging aggressive volume expansion. Nevertheless, data’s initial failure to

drive expanding ARPUs for DoCoMo provides a negative benchmark for European investors.

Realistic upside in the noise

Evidence to date suggeststhat messaging hascannibalised existing voicerevenue streams

I N D U S T R Y D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 16

Chart 3 : NTT DoCoMo ARPU trend (yen) Chart 4 : Voice/Data ARPU trends CY Q2 02/Q2 01

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1997

1998

1999

2000

2001

Q1 0

2

Q2 0

2

Q3 0

2

Q4 0

2

Q1 0

3

Q2 0

3F

Q3 0

3F

Q4 0

3F

ARPU (12m, contract) VARPU DARPU

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

VOD - UK VOD -Germany

VOD - Italy DoCoMo

ARPU VARPU

CY Q2 02/Q2 01

Source: Company reports Source: Company reports

Notwithstanding this axiom, we do acknowledge that the higher pricing of MMS

relative to existing voice and SMS usage could reduce the risk of cannibalisation.

Table 11 : Relative price, voice, SMS and MMS (€)

Price Premium/Discount to voice

Avg price 2 minute voice call 0.20 0%

Avg price per SMS 0.10 -50%

Avg price per MMS 0.40 100%

Source: ABN AMRO

Margin impact of MMS

So far we have considered the revenue impact of MMS. It is also important to

consider the margin implications. As we have noted historically (see Floating at the

edge, dated 14 January 2002) the process of embedding MMS-enabled handsets

into an operator’s subscriber base requires a substantial investment in opex

(handset subsidies, dealer commissions and marketing expenses).

Subscriber acquisition costs/subscriber retention costs (SAC/SRC) historically have

represented 7.0%-45% of an operator’s top line. The top end of this range has

been provided by the least mature new entrants throughout Europe. Typically, for a

more mature operator, we see SAC/SRC running at 7.0%-20.0% of sales. A major

risk to margins is the cost of (1) acceleration in the handset replacement cycle (ie

volume) and/or (2) increasing handset subsidies (ie unit cost).

(1) Volume

Our views on the prospect of acceleration in the European handset replacement

cycle are well known. We have long argued that an increase in churn is inevitable,

if the European operator community is to achieve material data-related revenue

growth in the medium term. Our margin thesis has revolved around the concept of

technology migration (stimulating the migration of exiting 2G subscriber to next-

generation terminals).

DoCoMo has failed to drivean ARPU upgrade from data

In our view, embeddinghandsets requires amaterial investment in opex

SAC/SRC could increasebetween 100-300bp as apercentage of sales

We suspect an increase inchurn is inevitable

I N D U S T R Y D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 17

We recognise that the speed of migration will vary on a country-by-country basis,reflecting:

■ the level of market share concentration;

■ the balance sheet strength of the smaller players; and

■ the arrival (or absence) of new entrants.

We continue to believe that Spain and France will be the most benign markets in

terms of competition, with the UK confirming its reputation as the most competitive

market in Europe. Italy, currently a benign market, is a wild card that could seemuch fiercer price-based competition looking forward.

In our view, the key metric on which investors should focus to assess our volume

thesis is gross additions. For the purpose of simplicity, our modelling of costs

includes “internal migrations” as external churn. While this is technically incorrect,

it does enable us to capture the volume driver of costs. Should the number of the

gross adds accelerate (all other factors held equal), operating costs will increase as

a percentage of sales. We highlight the structural shift in growth that Europe has

(and will) continue to undergo away from “new” growth, to the size and share ofthe disconnection pool, driven by churn and SOGA (see following chart).

Chart 5 : German gross adds example

2.0 2.5 5.79.3

34.4

7.33.7 4.7 4.0

1.4 1.4

2.1

3.5

5.9

12.014.2

15.2 15.7

29%

14% 15%

19%

16%

23%25% 25% 24%

0

5

10

15

20

25

30

35

40

45

1996 1997 1998 1999 2000 2001 2002 2003 2004

0%

5%

10%

15%

20%

25%

30%

35%

Net Adds (m) Disconnections (m) Churn %

Source: RegTP/Group3G

Our modelling incorporates full detail on the trend in gross adds across Europe. A

copy of this model is available upon request. Investors requiring further detail of

our views on technology migration should refer to Vodafone – The cost of capitalchallenge, dated 8 April 2002.

(2) Unit cost

We note recent comment from the Carphone Warehouse that by late January 2003,

MMS-enabled handsets will be priced for the mass market. The Nokia 7650 is

currently priced at €450-500. In 2003, Carphone is seeking to sell camera-enabled

handsets for €72-80 to contract customers. Similarly, first estimates of the unit

cost of the dual-mode 3G Nokia handset were €700-800 (about £500).

Speed of migration will varyon a country-by-countrybasis

Churn becomes a key driverof margin

Tracking gross adds crucial

Handset retailers havesuggested that handsetswill need to be retailedbelow €100

I N D U S T R Y D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 18

Our IT Hardware team has suggested an initial unit cost range of €600-700 per 3G

handset. To put this in some context, existing unit costs for 2G handsets in Europe

range between €250 and €300. (Globally, costs range between €100 and €110,

reflecting the low-end 2G handsets sold into markets such as China). While we

would expect this cost to fall as scale production commences, it could result in a

sharp short-term spike to subsidies.

Average subsidies at the last reported date have been running €24-350 per

addition. At the (all-important) post-paid level, SACs have been €156-350

(excluding the Italian experience; see following table). Post-paid subsidies over the

past year have diverged between (1) falling subsidisation of lower-end handsets

and (2) accelerating subsidisation of higher-end handsets (eg the Ericsson T68i).

Table 12 : Major operator SAC trends FY2002/1H02

Vodafone mmO2 Orange

(€) ContractSAC

PrepaidSAC

BlendedSAC

SAC as% ofSales

ContractSAC

PrepaidSAC

BlendedSAC

SAC as% ofSales

ContractSAC

PrepaidSAC

BlendedSAC

SAC as% ofSales

UK 184 41 110 7.5% 286 84 156 13.1% 350 32 158 9.0%

Germany 156 24 81 6.6% 254 70 157 17.1% na na na na

Italy 35 35 35 3.0% na na na na na na na na

France na na na na na na na na 206 83 140 10.2%

Source: ABN AMRO

Using a unit cost of (say) €650 would result in a material spike in subsidies if the

operator’s objective is to retail the product below €300 (about £200). This could

have a profound impact on margin. The implied subsidy would grow to about €350

per handset. This is significantly ahead of existing average post-paid handset

subsidies, although we note that it is more in line with existing high-end handset

subsidies. The actual margin impact would be driven by the number of gross adds

(volume) connecting to 3G. Our central case is for a 100-300bp reduction in

profitability (purely from an increase in SG&A as a percentage of sales).

A key risk to a positive outlook is that aggressive subsidisation does not result in

significant increases in ARPU (ie value destruction occurs). This risk is most

pronounced in markets such as the UK and Germany (in Europe) given the lower

level of industry concentration and the scope for the present equilibrium to be

destabilised by aggressive new entrants.

Capex impact of MMS

Investors should also be aware of the capex implications of successful MMS

deployment. GSM networks operate with eight time slots. A typical MMS can take

up to three time slots, cannibalising existing time slots allocated to voice

communication.

While the operator community claim this “success-driven” capex is already built

into its models, we are sceptical given the lack of visibility on (1) MMS subscriber

targets and (2) existing network capacity utilisation in major urban areas. Hence

the successful deployment of MMS could lead to upward momentum in capex

guidance from the major operators, although we note that this spend would besuccess-driven.

Our IT Hardware teamsuggests that 3G handsetswill cost €600-700

Post-paid subsidiescurrently sit at €156-300

Average subsidies couldmaterially increase to make3G handset prices attractiveto the end user

Successful deployment ofMMS could shift capexexpectations upwards ...

... although capex would besuccess-driven …

I N D U S T R Y D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 19

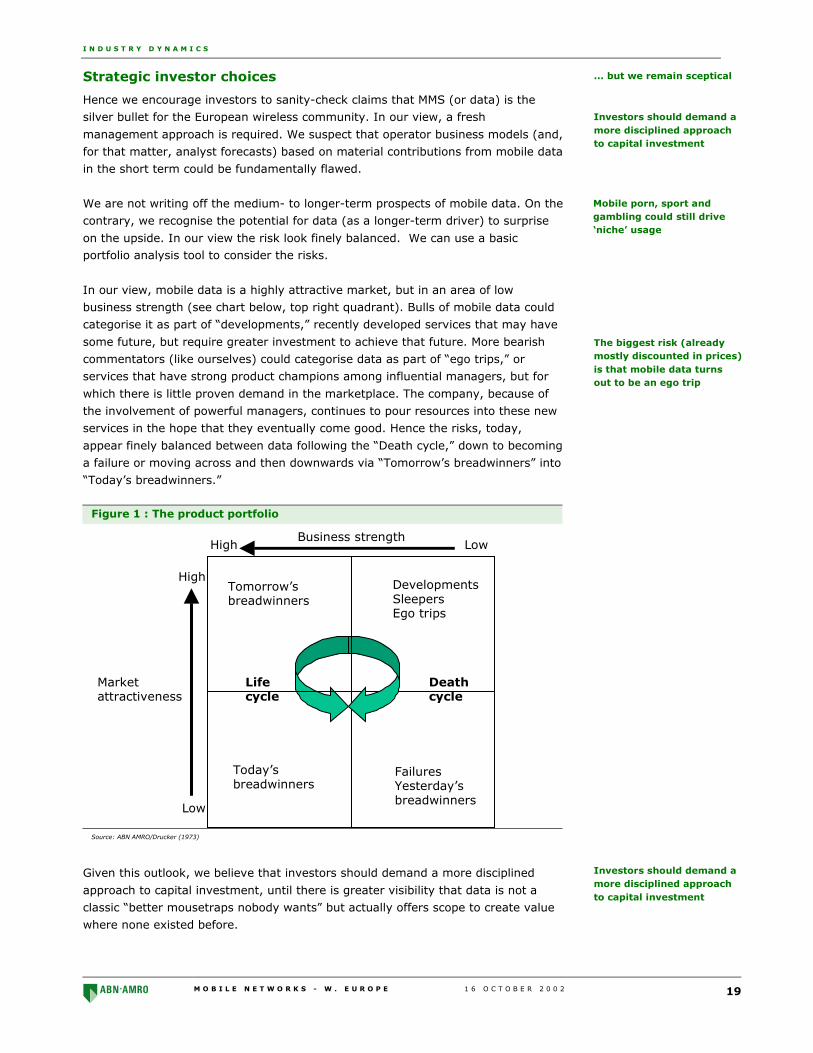

Strategic investor choices

Hence we encourage investors to sanity-check claims that MMS (or data) is the

silver bullet for the European wireless community. In our view, a fresh

management approach is required. We suspect that operator business models (and,

for that matter, analyst forecasts) based on material contributions from mobile data

in the short term could be fundamentally flawed.

We are not writing off the medium- to longer-term prospects of mobile data. On the

contrary, we recognise the potential for data (as a longer-term driver) to surprise

on the upside. In our view the risk look finely balanced. We can use a basicportfolio analysis tool to consider the risks.

In our view, mobile data is a highly attractive market, but in an area of low

business strength (see chart below, top right quadrant). Bulls of mobile data could

categorise it as part of “developments,” recently developed services that may have

some future, but require greater investment to achieve that future. More bearish

commentators (like ourselves) could categorise data as part of “ego trips,” or

services that have strong product champions among influential managers, but for

which there is little proven demand in the marketplace. The company, because of

the involvement of powerful managers, continues to pour resources into these new

services in the hope that they eventually come good. Hence the risks, today,

appear finely balanced between data following the “Death cycle,” down to becoming

a failure or moving across and then downwards via “Tomorrow’s breadwinners” into

“Today’s breadwinners.”

Figure 1 : The product portfolio

Business strengthLowHigh

Tomorrow’s breadwinners

Developments SleepersEgo trips

Today’s breadwinners

Failures Yesterday’sbreadwinners

Marketattractiveness

Low

High

Lifecycle

Deathcycle

Source: ABN AMRO/Drucker (1973)

Given this outlook, we believe that investors should demand a more disciplined

approach to capital investment, until there is greater visibility that data is not a

classic “better mousetraps nobody wants” but actually offers scope to create value

where none existed before.

... but we remain sceptical

Investors should demand amore disciplined approachto capital investment

Mobile porn, sport andgambling could still drive‘niche’ usage

The biggest risk (alreadymostly discounted in prices)is that mobile data turnsout to be an ego trip

Investors should demand amore disciplined approachto capital investment

I N D U S T R Y D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 20

This page has been left intentionally blank

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 21

M A C R O D Y N A M I C S

Fixed to mobile substitution

In the short term, pre-to-post-paid migration is the most important driver of

revenue growth. We believe high prepaid call charges have stunted usage. Our

forecasts imply about 4% annual growth in blended ARPU over the next five years

from this dynamic. During the medium term, we suspect that consensus models of

revenue growth are fundamentally flawed, assuming 2G economics (lower volume,

low ARPU, low EBITDA per subscriber) will underpin European 3G. It is our core

belief that at a 50% premium to underlying fixed-line prices, mass displacement of

voice minutes and revenue will occur from fixed to mobile networks. In our view,

3G will be characterised by higher-volume, higher-ARPU, higher-EBITDA per

subscriber voice services, similar to the model that prevails in the US. Our central

case assumes mobile grabbing 30%-40% share of outgoing total traffic by year-end

2006, from 10%-15% today, driven by price cuts of about 50%-60%. This view has

a profound implication for European ARPU growth, which could structurally shift

upwards by about 30% by year-end 2006. The key is flawless execution to turn

volume into value.

Introduction

In this section of the note we present:

■ the ARPU impact of pre-to-post-paid migration;

■ US volume as a lead indicator for Europe;

■ the defining characteristics of 3G over 2G economics;

■ the relative price of mobile vs fixed;

■ the cross-elasticity of demand of mobile to fixed-line;

■ a sensitivity analysis on the scope for voice substitution by call type and the

impact on ARPU; and finally

■ the risk/opportunity presented by declining termination rates.

Fixed to mobile substitutionoffers a compelling secondleg of growth

M A C R O D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 22

Background

The average European wireless subscribers still only use their handset for about 3.0

outgoing minutes a day, or 4.5 minutes including incoming minutes of use (MOU).

Across Europe, mobile calls represent 10%-15% of total outgoing call volume. In

the UK there are seven times as many minutes carried on fixed-line networks than

on the UK’s wireless networks (see following chart).

Chart 6 : UK call volume by type (bn minutes)

0

50

100

150

200

250

300

1999 2000 2001

Fixed local calls Fixed Internet calls Fixed long distance calls

Mobile outgoing calls Fixed international calls Fixed to mobile calls

Source: ABN AMRO/OFTEL

At the top line, we believe that Europe’s wireless landscape will be characterised bythree major phases during the next four years, namely:

■ Phase one: prepaid to post-paid subscriber migration (2002-2006);

■ Phase two: material fixed-to-mobile call volume substitution (2004-2006); and

■ Phase three: dramatically declining termination rates (2002-2006).

Phase One: Pre-to-post-paid migration

It is our core belief that European cellular usage has been stunted by high prepaid

call charges. Including the handset subsidy offered on post-paid products, we

estimate prepaid prices are 40%-110% higher than “equivalent usage” post-paid

offers across Europe. In our view, lower call charges have played a key role indriving materially higher volume in the US market.

Prepaid subscribers as a percentage of the total European base appear to have

already peaked. Looking forward, we expect four key drivers to cajole Europe’s pre-

paid subscribers into migrating: (1) handset subsidies, (2) dealer incentives, (3)

product exclusivity and (4) bucket pricing plans (value for money).

Phase One drives higher usage/blended ARPUs

We retain a firm belief that increasing pre-to-post-paid migration offers a

compelling macro driver of volume and blended ARPU. The impact of migration can

be identified with reference to a “generic” model.

European wireless usersstill only use 3 minutes aday

At the top line, the wirelesslandscape will becharacterised by threemajor phases

Prepaid usage has beenstunted by high call charges

In Europe, prepaidsubscribers have peaked asa percentage of totalsubscribers

Prepaid subscribermigration offers a strongmacro driver of blendedARPU

M A C R O D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 23

Our generic model is built on Country X. In Country X we have considered OperatorY.

■ To capture the impact of pre-to-post-paid migration, we have moved operator

Y’s post-paid share of overall gross adds from 38% at x+0 (today), to 60% inx+1 (today + one year).

■ Each new year’s post-paid subscriber connections are assumed to connect to a

lower-priced post-paid plan, reflecting incremental subscriber dilution (we have

factored in a 20% decline pa).

■ In terms of current period (x+0) post-and prepaid ARPU, we have used £40 and£9, respectively.

In the following chart we show the evolution of subscribers by post-paid plan type

(post-paid subscribers joining high-value, Phase One, Phase Two and Phase Three

plans).

Figure 2 : Generic subscriber evolution by plan type

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

X+0 X+1 X+2 X+3 X+4 X+5 X+6 X+7 X+8 X+9 X+10 X+11

Time (Yrs)

Subsc

riber

s (m

)

High Value Contract Phase 1 Contract Phase 2 Contract Phase 3 Contract

Source: ABN AMRO

The chart shows the highest value post-paid subscribers (the bottom area) falling in

absolute numbers over time. Each year’s connections are assumed to connect to a

new type of plan (Phase One in x+1, Phase Two in x+2 and Phase Three in x+3).

In aggregate, total post-paid subscribers grow to nearly 60% of the total base from

31%. We have then factored in the different (declining) incremental post-paidARPUs for new connections (see following chart).

We have built a genericmodel to show theimportance of planmigration

We have grouped eachyears connections by a plantype, to model migration

Incrementally we expectpost-paid ARPU to fall

M A C R O D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 24

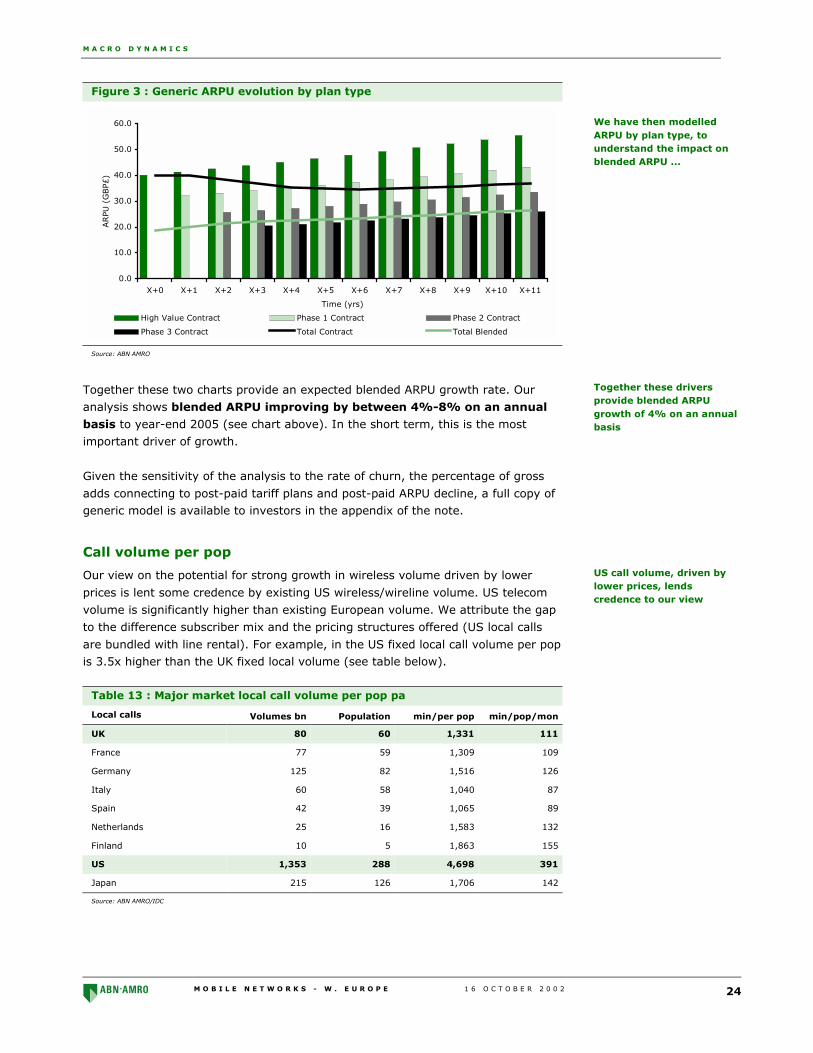

Figure 3 : Generic ARPU evolution by plan type

0.0

10.0

20.0

30.0

40.0

50.0

60.0

X+0 X+1 X+2 X+3 X+4 X+5 X+6 X+7 X+8 X+9 X+10 X+11

Time (yrs)

ARPU

(G

BP£)

High Value Contract Phase 1 Contract Phase 2 Contract

Phase 3 Contract Total Contract Total Blended

Source: ABN AMRO

Together these two charts provide an expected blended ARPU growth rate. Our

analysis shows blended ARPU improving by between 4%-8% on an annual

basis to year-end 2005 (see chart above). In the short term, this is the most

important driver of growth.

Given the sensitivity of the analysis to the rate of churn, the percentage of gross

adds connecting to post-paid tariff plans and post-paid ARPU decline, a full copy ofgeneric model is available to investors in the appendix of the note.

Call volume per pop

Our view on the potential for strong growth in wireless volume driven by lower

prices is lent some credence by existing US wireless/wireline volume. US telecom

volume is significantly higher than existing European volume. We attribute the gap

to the difference subscriber mix and the pricing structures offered (US local calls

are bundled with line rental). For example, in the US fixed local call volume per popis 3.5x higher than the UK fixed local volume (see table below).

Table 13 : Major market local call volume per pop pa

Local calls Volumes bn Population min/per pop min/pop/mon

UK 80 60 1,331 111

France 77 59 1,309 109

Germany 125 82 1,516 126

Italy 60 58 1,040 87

Spain 42 39 1,065 89

Netherlands 25 16 1,583 132

Finland 10 5 1,863 155

US 1,353 288 4,698 391

Japan 215 126 1,706 142

Source: ABN AMRO/IDC

We have then modelledARPU by plan type, tounderstand the impact onblended ARPU ...

Together these driversprovide blended ARPUgrowth of 4% on an annualbasis

US call volume, driven bylower prices, lendscredence to our view

M A C R O D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 25

Call volume per line

If we re-run our analysis using a per line metric, we can remove the distortion of

differences in penetration (see following table). On average we estimate US telco

volume is about 6x higher per line than the European average. For example, in the

US, fixed local call volume is 6.5x higher than the UK fixed local volumes per line,

or 6.9x the European average. Mobile traffic per line is about 3x European average

volume.

Table 14 : Major market wireline local call volume per line

Volume bnNo of Lines

(m) Minutes/Line Min/Line/Mon

UK 80 84 951 79

France 77 73 1060 88

Germany 125 157 794 66

Italy 60 52 1,157 96

Spain 42 33 1,267 106

Netherlands 25 27 950 79

Finland 10 11 849 71

US 1,345 219 6,133 511

Source: ABN AMRO/Country regulators

In the following table we have summarised the multiple of US minutes per line by

call type relative to the European average by call type per line. The evidence makes

stark reading. For the wireless industry we do not believe that the difference in

usage is primarily attributable to differences in penetration.

Table 15 : US vs European telco volume (2000)

Euro ave. MOU perline per line

US ave. MOU perline per month

European averagemultiple

Local - Euro average 84 511 6.1

National - Euro average 35 315 8.9

International - Euro average 5 11 2.1

Mobile - Euro average 107 284 2.7

Source: ABN AMRO

Our thesis is simple – in the event of subscribers moving from pre-to-post-paid

plans (with large bundles), usage should increase. Evidence to date supports a

positive view. We highlight TEM’s Q202 results, which indicated that average usage

from migrated subscribers jumped more than 2x. Applying the US propensity to call

to each of Europe’s major markets results in a significant shift in European wireless

outgoing volume.

US local call volume per line6x higher than in Europe

In aggregate call volume inthe US is between 2x and6x the European average

Should pre-to-post paidmigration occur blendedspend should increase

M A C R O D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 26

Table 16 : Mobile minutes 2001: applying a US multiplier

Annual mobilevolume 2001 (bn)

US multiplier (x) New annual mobilevolume (bn)

UK 69.4 2.7 187.3

France 65.6 2.7 177.1

Germany 74.1 2.7 200.1

Italy 49.1 2.7 132.6

Spain 27.6 2.7 74.6

European major market total 285.8 2.7 771.7

Source: ABN AMRO

Readers should recognise that we have not incorporated this volume increase into

our bottom-up models for each operator. We merely present the data as a further

perspective. This is important from a wireline perspective, given the scope for the

wireless subsector to gain (in terms of volume) from pre-to-post-paid subscribermigration, but not entirely at the revenue expense of the wireline operators.

Phase Two: fixed to mobile substitution

While local access fees may be largely retained by wireline telephony operators, we

expect a large percentage of fixed-line voice calls to migrate to Europe’s cellular

networks. This view has a profound implication for European ARPU growth and

fundamental valuation.

2G vs 3G economics

Increasingly, we suspect that consensus models of revenue growth are

fundamentally flawed, assuming 2G economics will underpin European 3G. We

reject the view that blended ARPU will gently tick along at 3-5% growth pa, coupled

with margin progression and capex/sales falling to sub-10%. In our view, European

cellular models that follow this trend ignore the potential capacity for 3G to enablethe mass substitution of fixed-line voice minutes to the wireless network.

Material wireless growthmay not necessarilyterminally damage wirelinevolume but ...

... As 3G is deployed acrossEurope, we anticipate largeF2M volume displacement

The assumption that 2Gmobile economics willprevail in 3G could befundamentally flawed

M A C R O D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 27

Chart 7 : 2G vs 3G economics

European 2GEconomics

Growth via shift in capacity 3G Economics

Low MOU/low volumegrowth

Low ARPU/declining voiceARPU

Higher MOU/high volumegrowth

Higher ARPU/lower yield

High level of marketconcentration

High margins Lower margins

Lower EBITDA persubscriber

Higher EBITDA persubscriber

Capex: Capacity andmaintenance

Capex: coverage focused

Low NOPAT/IC: goodreturns

Higher NOPAT/Similar IC:higher returns

Lower level of marketconcentration

Shift in Capacity

2 x - 5 x

Source: ABN AMRO

Elasticity of demandHistorically, a great deal of telco equity research has been dedicated to the

discussion of elasticity of demand, the percentage change in quantity demanded for

a percentage change in price. Analysis of elasticity of demand is obscured by

penetration growth. The authors of this study have seen estimates ranging from

negative 0.6 to negative 0.9, suggesting a high degree of elasticity at historical

price levels (implying volume growth somewhat compensates for price declines).

Cross-elasticity of demandFrom a theoretical perspective, the key determinant of elasticity of demand is the

availability of substitutes, which is a key point missed by many industry experts. Adiscussion of elasticity of demand for one good in isolation is flawed.

Elasticity of demand rangesfrom negative 0.6 tonegative 0.9

... but the key is crosselasticity of demand

M A C R O D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 28

In our view, the key factor to focus in on is the cross-elasticity of demand

between European wireless and European wireline (ie At what price will wireless be

preferred to fixed-line communication?). Cross-elasticity of demand refers to the

responsiveness of demand in one product to the change in price of another product.

Substitute goods have positive cross-elasticities. To better understand cross-

elasticity, we have focused our attention on the relative price of cellular to fixed

line.

Fixed vs mobile: A comparative analysis

The average price of a cellular minute of use vs a fixed-line minute of use has fallen

to nearly 3x today from about 6x in 1995 (excluding fixed-line access and

connection fees; see following chart).

Chart 8 : Comparative price of mobile vs fixed

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1996 1997 1998 1999 2000 2001

Euro average

Source: ABN AMRO estimates/IDC

France

In determining revenue, we can either include or exclude access and connection

charges. Choice of methodology has a significant impact on the implied multiple of

cellular prices to fixed line. For example, in the French market, including access

fees, we calculate a multiple of around 2x vs a relative call price of nearer 3x

excluding access fees. In terms of the relative price of fixed voice calls to a mobile

voice calls, the French market offers a decent proxy for Europe in aggregate (seefollowing chart, including fixed-line access).

We estimate wireless as amultiple of wireline hasfallen to about 3x from 6x

In France, the multiple hasfallen to nearly 3x

M A C R O D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 29

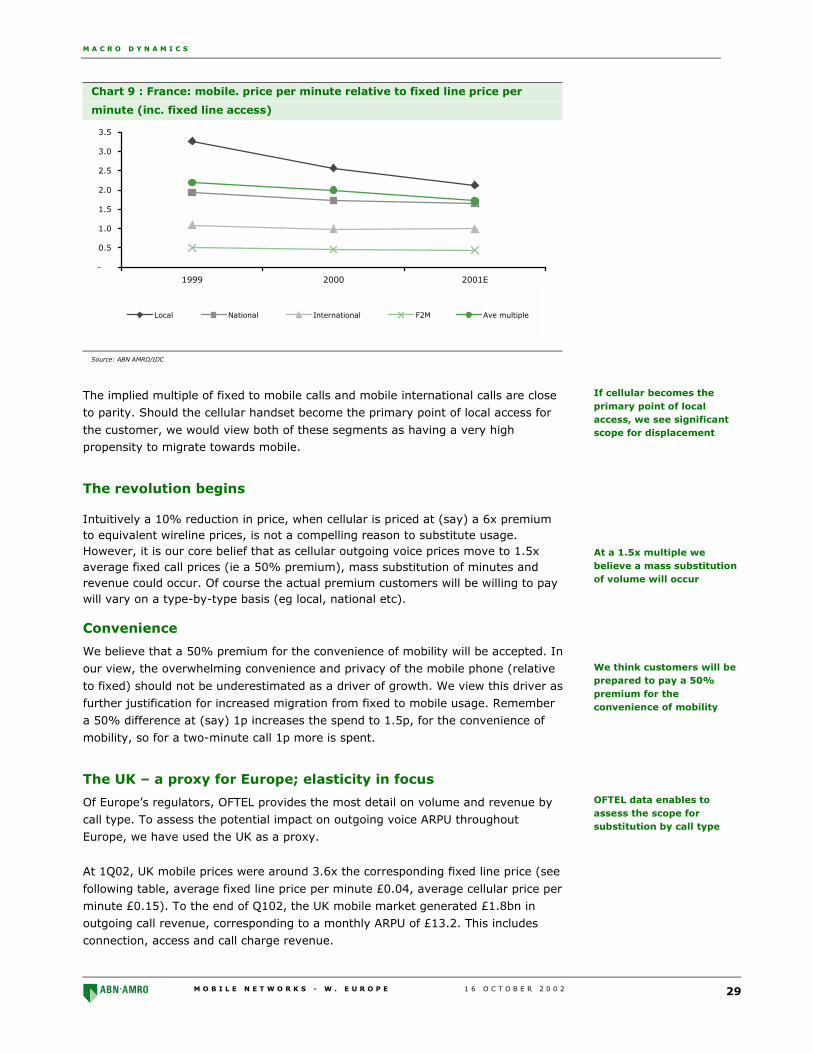

Chart 9 : France: mobile. price per minute relative to fixed line price per

minute (inc. fixed line access)

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1999 2000 2001E

Local National International F2M Ave multiple

Source: ABN AMRO/IDC

The implied multiple of fixed to mobile calls and mobile international calls are close

to parity. Should the cellular handset become the primary point of local access for

the customer, we would view both of these segments as having a very highpropensity to migrate towards mobile.

The revolution begins

Intuitively a 10% reduction in price, when cellular is priced at (say) a 6x premiumto equivalent wireline prices, is not a compelling reason to substitute usage.However, it is our core belief that as cellular outgoing voice prices move to 1.5xaverage fixed call prices (ie a 50% premium), mass substitution of minutes andrevenue could occur. Of course the actual premium customers will be willing to paywill vary on a type-by-type basis (eg local, national etc).

Convenience

We believe that a 50% premium for the convenience of mobility will be accepted. In

our view, the overwhelming convenience and privacy of the mobile phone (relative

to fixed) should not be underestimated as a driver of growth. We view this driver as

further justification for increased migration from fixed to mobile usage. Remember

a 50% difference at (say) 1p increases the spend to 1.5p, for the convenience of

mobility, so for a two-minute call 1p more is spent.

The UK – a proxy for Europe; elasticity in focus

Of Europe’s regulators, OFTEL provides the most detail on volume and revenue by

call type. To assess the potential impact on outgoing voice ARPU throughout

Europe, we have used the UK as a proxy.

At 1Q02, UK mobile prices were around 3.6x the corresponding fixed line price (see

following table, average fixed line price per minute £0.04, average cellular price per

minute £0.15). To the end of Q102, the UK mobile market generated £1.8bn in

outgoing call revenue, corresponding to a monthly ARPU of £13.2. This includes

connection, access and call charge revenue.

If cellular becomes theprimary point of localaccess, we see significantscope for displacement

At a 1.5x multiple webelieve a mass substitutionof volume will occur

We think customers will beprepared to pay a 50%premium for theconvenience of mobility

OFTEL data enables toassess the scope forsubstitution by call type

M A C R O D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 30

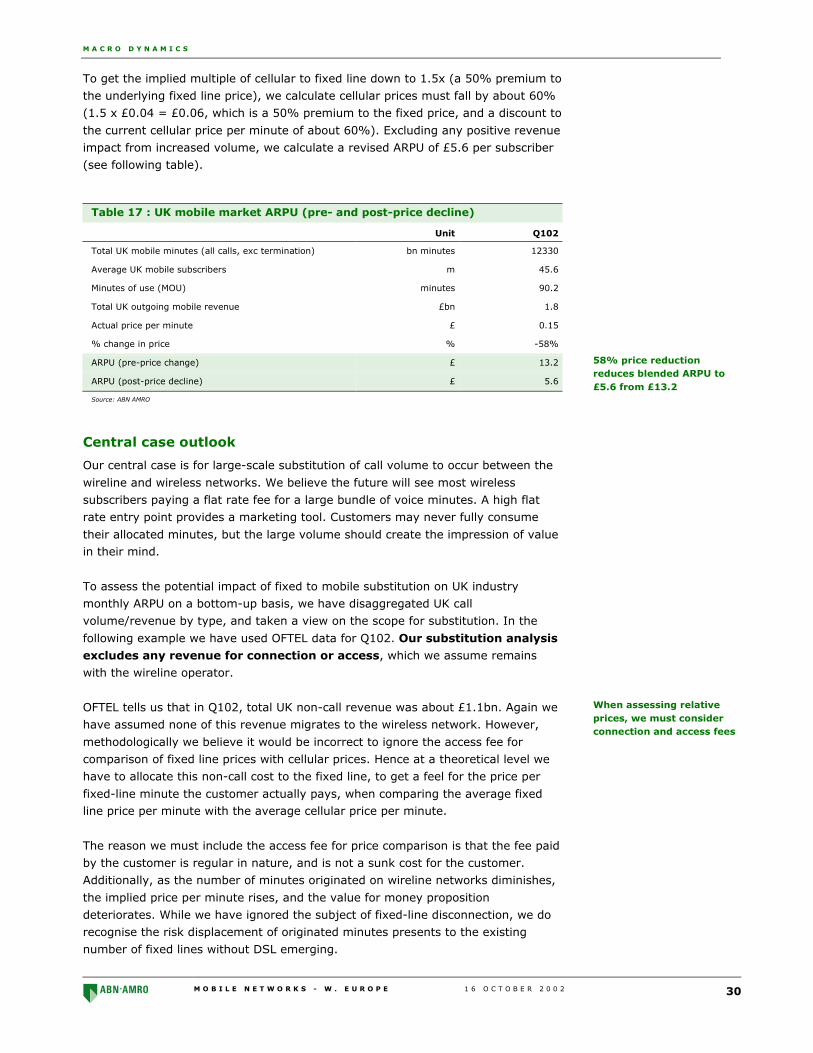

To get the implied multiple of cellular to fixed line down to 1.5x (a 50% premium to

the underlying fixed line price), we calculate cellular prices must fall by about 60%

(1.5 x £0.04 = £0.06, which is a 50% premium to the fixed price, and a discount to

the current cellular price per minute of about 60%). Excluding any positive revenue

impact from increased volume, we calculate a revised ARPU of £5.6 per subscriber

(see following table).

Table 17 : UK mobile market ARPU (pre- and post-price decline)

Unit Q102

Total UK mobile minutes (all calls, exc termination) bn minutes 12330

Average UK mobile subscribers m 45.6

Minutes of use (MOU) minutes 90.2

Total UK outgoing mobile revenue £bn 1.8

Actual price per minute £ 0.15

% change in price % -58%

ARPU (pre-price change) £ 13.2

ARPU (post-price decline) £ 5.6

Source: ABN AMRO

Central case outlook

Our central case is for large-scale substitution of call volume to occur between the

wireline and wireless networks. We believe the future will see most wireless

subscribers paying a flat rate fee for a large bundle of voice minutes. A high flat

rate entry point provides a marketing tool. Customers may never fully consume

their allocated minutes, but the large volume should create the impression of valuein their mind.

To assess the potential impact of fixed to mobile substitution on UK industry

monthly ARPU on a bottom-up basis, we have disaggregated UK call

volume/revenue by type, and taken a view on the scope for substitution. In the

following example we have used OFTEL data for Q102. Our substitution analysis

excludes any revenue for connection or access, which we assume remains

with the wireline operator.

OFTEL tells us that in Q102, total UK non-call revenue was about £1.1bn. Again we

have assumed none of this revenue migrates to the wireless network. However,

methodologically we believe it would be incorrect to ignore the access fee for

comparison of fixed line prices with cellular prices. Hence at a theoretical level we

have to allocate this non-call cost to the fixed line, to get a feel for the price per

fixed-line minute the customer actually pays, when comparing the average fixedline price per minute with the average cellular price per minute.

The reason we must include the access fee for price comparison is that the fee paid

by the customer is regular in nature, and is not a sunk cost for the customer.

Additionally, as the number of minutes originated on wireline networks diminishes,

the implied price per minute rises, and the value for money proposition

deteriorates. While we have ignored the subject of fixed-line disconnection, we do

recognise the risk displacement of originated minutes presents to the existing

number of fixed lines without DSL emerging.

58% price reductionreduces blended ARPU to£5.6 from £13.2

When assessing relativeprices, we must considerconnection and access fees

M A C R O D Y N A M I C S

M O B I L E N E T W O R K S - W . E U R O P E 1 6 O C T O B E R 2 0 0 2 31

Including access fees, we estimate that the implied multiple (of cellular price per

minute vs fixed price per minute) is about 1.5x (ie cellular at a 50% premium to

the underlying fixed line price). Excluding access fees from the relative price

comparison, the price multiple between the two platform grows from 1.5x to 2.6x.

We can calculate this from total fixed call revenue post-substitution excluding

access of £1.5bn, divided by the number of minutes equals an average price per

minute of £0.02, which is 2.6x less than the implied price per mobile minute of

£0.06 post price decline.

Including access fees, total fixed line quarterly revenue equalled £2.5bn in Q102,

divided by the number of minutes equals an average price per minute of £0.04.

This is 1.5x less than the implied price per mobile minute of £0.06 post pricedecline.

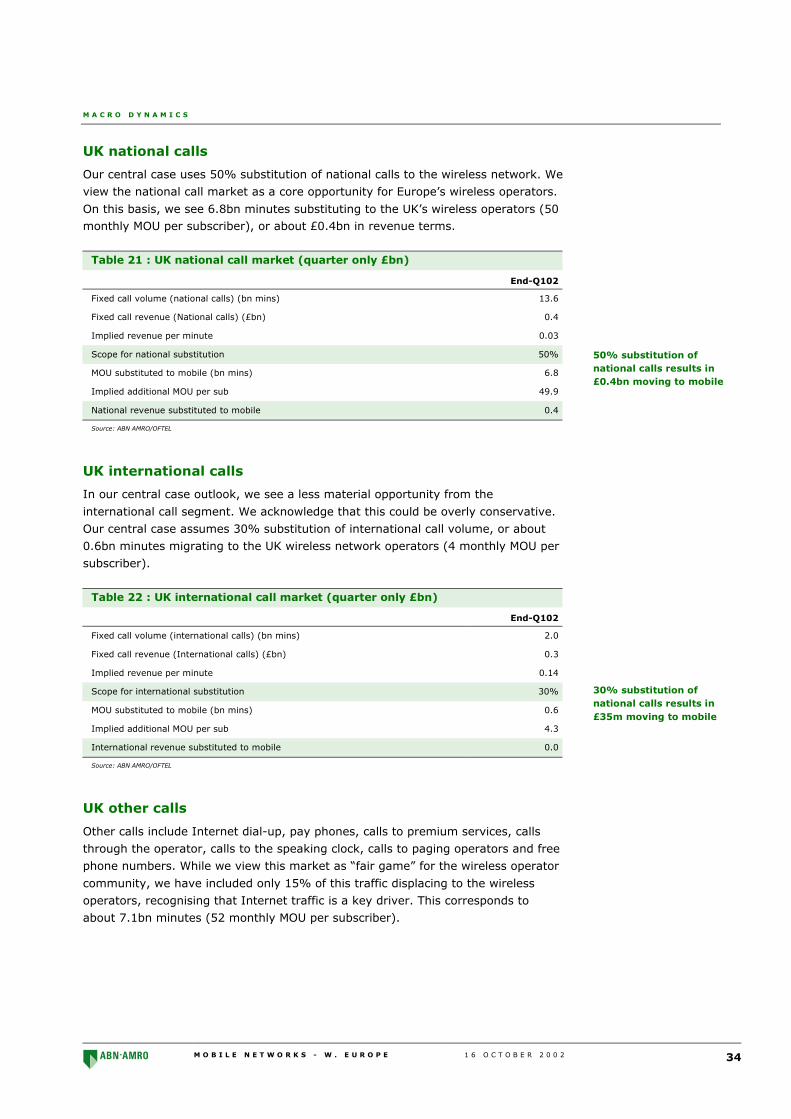

Our central case for volume migration is based on the following assumptions:

■ 30% of all local call volumes substituting to wireless;

■ 60% of all F2M calls substituting to wireless;

■ 50% of all national calls substituting to wireless;

■ 30% of all international calls substituting to wireless; and

■ 15% of “other” calls, including NTS and “free call numbers.”

This equates to 35% of UK call volume orignated by wireless networks from 13%.

Total call volume in Q102 equalled 97.3bn minutes, of which 13% were mobile-

originated. Our central case grabs an additional 22.2bn minutes, giving total

mobile minutes post price decline of 34.5bn minutes, or 35% of the total marketminutes for the quarter.

We are not suggesting that call volume at Q102 offers a good proxy for call volume

in the absence of fixed-to-mobile substitution looking forward. But given the

transparency of Q102 numbers, we have used the data to get a feel for the scope

for an ARPU shift.

Similarly we don’t want to become too bogged down by the question, What’s the

correct percentage for displacement by call type? The future is by definition

unknown, and hence the question is clearly open to debate at a bottom-up level.

In our view it is more important to focus on the bigger picture – What percentage

of total volume will migrate?, and What price reduction is required to drive this

displacement?

Factoring in a willingness to pay a 50% premium to the underlying fixed line price

in aggregate, we estimate conservatively outgoing voice ARPU growth of 18%

(outgoing voice ARPU £5.6 post price decline, from £13.2, adding incremental ARPU

uplift from volume growth of £10.0, resulting in post price decline ARPU of £15.60,

which is 18% ahead of £13.2). Outgoing growth of 18% corresponds to 11%

change in overall ARPU. This would represent a significant upside surprise to

consensus expectations. We note comment from British Telecom that to date about

4% of existing volume pa has been cannibalised by mobile.

Our central case assumesmobile grabbing around35% of total originated callvolume (from 13%)

This corresponds tooutgoing ARPU growth of18% (using a price cut of58%).

MOBILE NETWORKS - W. EUROPE16 OCTOBER 200232

MACRO DYNAMICS

Tab

le 1

8 : U

K M

ark

et O

utg

oin

g D

rivers

Q1

20

02

OFT

EL S

tatistics

Lo

cal ca

lls F

2M

calls

Natio

nal

calls

Inte

rnatio

na

lca

lls O

ther ca

lls T

ota

l Fix

ed

calls

Mo

bile

To

tal A

ll Calls

Sta

rting

Po

int

Call vo

lum

e bn m

ins

18.8

3.5

13.6

2.0

47.1

85.0

12.3

97.3

Call reven

ue (exc. access) £

bn

0.4

0.5

0.4

0.3

0.7

2.3

1.8

4.1

Implied

revenue p

er min

ute

0.0

2 0

.14

0.0

3 0

.14

0.0

1 0

.03

0.1

5 0

.04

Impact o

f Subsitu

tion

Mobile p

rice per m

inute red

uctio

n-5

8%

New

mobile p

rice 0

.06

Sco

pe fo

r local su

bstitu

tion

30%

60%

50%

30%

15%

26%

Averag

e mobile su

bscrib

ers 4

5.6

45.6

45.6

45.6

45.6

45.6

45.6

MO

U su

bstitu

ted to

mobile (b

n m

ins)

5.6

2.1

6.8

0.6

7.1

22.2

22.2

Implied

additio

nal M

OU

per su

b 4

1.3

15.2

49.9

4.3

51.7

162.4

162.4

Reven

ue lo

st to Fixed

Line

0.1

0.3

0.2

0.1

0.1

0.8

Reven

ue su

bstitu

ted to

mobile

0.3

0.1

0.4

0.0

4 0

.4 1

.4 1

.4M

obile R

evenue lo

st due to

price cu

t 1

.0In

cremen

tal ARPU

uplift

2.5

0.9

3.1

0.3

3.2

10.0

10.0

En

d G

am

eCall vo

lum

e bn m

ins

13.2

1.4

6.8

1.4

40.0

62.8

34.5

97.3

Call reven

ue (exc. access) £

bn

0.3

0.2

0.2

0.2

0.6

1.5

2.1

3.6

Implied

revenue p

er min

ute

0.0

2 0

.14

0.0

3 0

.14

0.0

1 0

.02

0.0

6 0

.04

Pre-p

rice declin

e P

ost p

rice declin

eA

RP

U 1

3.2

5.6

Increm

ental A

RPU

uplift (fro

m su

bstitu

tion)

10.0

New

ARPU

(post p

rice declin

e inc. vo

lum

e uplift)

15.6

% C

han

ge

18%

Differen

ce T

otal fixed

line call vo

lum

e 8

5.0

62.8

22.2

Total m

obile call vo

lum

e 1

2.3

34.5

22.2

97.3

97.3

-

Total fixed

line call vo

lum

e87%

65%

Total m

obile call vo

lum

e13%

35%

Differen

ce T

otal fixed

line call rev

enue

2.3

1.5

0.8

Total m

obile call rev

enue

1.8

2.1

0.3

Total telco