acc422 wiley cpa excel chapters 21 answers

DESCRIPTION

ACC422 Wiley CPA Excel Chapters 21 AnswersTRANSCRIPT

Question 1:PVE-0037Need a hint?See Reference...The lessee’s balance sheet liability for a capital lease would be periodically reduced by the totalMinimum lease payment plus the amortization of the related asset.Minimum lease payment less the amortization of the related asset.Minimum lease payment less the portion of the minimum lease payment allocable to interest.Minimum lease payment.This answer is correct. During the lease term, each minimum lease payment consists of both interest and reduction of the lease obligation. Lease amortization produces a constant periodic rate of interest on the remaining balance of the obligation, known as the "effective interest" method.

Question 2:PVE-0007Need a hint?See Reference...The Morn Company leased equipment to the Lizard Company on May 1, year 1. At that time the collectibility of the minimum lease payments was not reasonably predictable. The lease expires on May 1, year 3. Lizard could have bought the equipment from Morn for $900,000 instead of leasing it. Morn’s accounting records showed a book value for the equipment on May 1, year 1, of $800,000. Morn’s depreciation on the equipment in year 1 was $200,000. During year 1 Lizard paid $240,000 in rentals to Morn. Morn incurred maintenance and other related costs under the terms of the lease of $18,000 in year 1. After the lease with Lizard expires, Morn will lease the equipment to the Cold Company for another 2 years. The income before income taxes derived by Morn from this lease for the year ended December 31, year 1, should be$ 22,000$100,000$122,000$240,000

This answer is correct. The lease shall be accounted for as an operating lease because none of the four requirements applicable to both lessees and lessors is met. Even if one or more was met, the lease would still be classified as an operating lease as the payments are not reasonably predictable (ASC Topic 840). The calculation for lease income for year 1 would be as follows:

Rental income $ 240,000

Less: year 1 depreciation

(200,000)

Maintenance costs (18,000)

Income from lease for $

year 1 22,000

Question 3:PVE-0029Need a hint?See Reference...What is the cost basis of an asset acquired by a lease which is accounted for as a capital lease?The net realizable value of the asset determined at the date of the lease agreement plus the sum of the future minimum lease payments under the lease.The sum of the future minimum lease payments under the lease.The present value of the minimum lease payments under the lease (exclusive of executory costs and any profit thereon) discounted at an appropriate rate.The present value of the market price of the asset discounted at an appropriate rate as an amount to be received at the end of the lease.This answer is correct. When a lease is accounted for as a capital lease, lessees record the lease by debiting the asset and crediting a liability for the present value of the future minimum lease payments (ASC Topic 840).

Question 4:PVE-0051Need a hint?See Reference...Conn Company purchased a new machine for $480,000 on January 1, year 1, and leased it to East the same day. The machine has an estimated 12-year life, and will be depreciated $40,000 per year. The lease is for a 3-year period expiring January 1, year 4, at an annual rental of $85,000. Additionally, East paid $30,000 to Conn as a lease bonus to obtain the 3-year lease. For year 1 Conn incurred insurance expense of $8,000 for the leased machine. What is Conn’s year 1 operating profit on this leased asset?$67,000$55,000$47,000$37,000This answer is correct. This lease is an operating lease because it does not meet any of the four criteria to be a capital lease as described in ASC Topic 840. The lessor (Conn) should recognize as revenue the year 1 rental payment ($85,000) plus a proportionate fraction of the lease bonus ($30,000/ 3-year lease term = $10,000 per year). Therefore, total revenue for year 1 is $95,000 ($85,000 + $10,000). Year 1 expenses total $48,000 (depreciation of $40,000 and insurance of $8,000). Thus, operating profit on the leased asset is $47,000 ($95,000 revenues less $48,000 expenses).

Question 5:PVE-0034Need a hint?See Reference...

The lessee should amortize the capitalizable cost of the leased asset in a manner consistent with the lessee’s normal depreciation policy for owned assets for leases that

Contain a bargainpurchase option

Transfer ownership of theproperty to the lessee bythe end of the lease term

No NoNo YesYes YesYes NoThis answer is correct. A lease that transfers ownership of the property to the lessee by the end of the lease term and a lease that contains a bargain purchase option are properly classified as capital leases. Per ASC Topic 840, if the lease meets either of the above criteria, the asset should be amortized in a manner consistent with the lessee’s normal depreciation policy for owned assets because the asset will be used by the lessee for its entire life.

Question 6:PVE-0048Need a hint?See Reference...In a sale-leaseback transaction, the seller-lessee retains the right to substantially all of the remaining use of the equipment sold. The profit on the sale should be deferred and subsequently amortized by the lessee when the lease is classified as a(n)

Capital lease

Operating lease

No YesNo NoYes NoYes YesThis answer is correct. Per ASC Topic 840, any profit related to a sale-leaseback transaction in which the seller-lessee retains the right to substantially all of the remaining use of the equipment sold shall be deferred and amortized in proportion to the amortization of the leased asset if the transaction is classified as a capital lease. If the transaction is classified as an operating lease (e.g., if the lease begins in the last 25% of the asset’s economic life), the profit shall be deferred and amortized in proportion to the related gross rental charged to expense over the lease term. It is important to note that losses are recognized immediately for either a capital or operating lease.

Question 7:PVE-0008Need a hint?See Reference...Rent received in advance by the lessor for an operating lease should be recognized as revenue

When received.At the lease’s inception.In the period specified by the lease.At the lease’s expiration.This answer is correct. Under an operating lease rental revenue is to be recognized in each accounting period on a straight-line basis unless another systematic and rational basis is more representative of the decline in the asset’s service potential.

Question 8:PVE-0001Need a hint?See Reference...The present value of the minimum lease payments should be used by the lessee in the determination of a (n)

Capital lease liability

Operating lease liability

Yes NoYes YesNo YesNo NoThis answer is correct. Per ASC Topic 840, the present value of the minimum lease payments should be used to determine the liability under a capital lease. Under an operating lease, a liability arises when rent expense is recorded but has not been paid. Furthermore, it is recorded at the actual amount of cash to be paid, not its present value.

Question 9:PVE-0057Need a hint?See Reference...Koby Co. entered into a capital lease with a vendor for equipment on January 2 for seven years. The equipment has no guaranteed residual value. The lease required Koby to pay $500,000 annually on January 2, beginning with the current year. The present value of an annuity due for seven years was 5.35 at the inception of the lease. What amount should Koby capitalize as leased equipment?$ 500,000$ 825,000$2,675,000$3,500,000This answer is correct. The requirement is to determine the amount of the capitalized value of the leased equipment. The equipment should be capitalized as the present value of the minimum lease payments. The present value of the

minimum lease payments at January 2 is calculated as the present value of the annuity due factor times the payment, or $2,675,000 (5.35 x $500,000).

Question 10:PVE-0044Need a hint?See Reference...On January 1, year 1, Vick Company as lessee signed a 10-year noncancelable lease for a machine stipulating annual payments of $20,000. The first payment was made on January 1, year 1. Vick appropriately treated this transaction as a capital lease. The 10 lease payments have a present value of $135,000 at January 1, year 1, based on implicit interest of 10%. For the year ended December 31, year 1, Vick should record interest expense of$0$ 6,500$11,500$13,500This answer is correct. At the inception of the lease on 1/1/Y1, the capitalized lease liability was $135,000. The first payment, also on 1/1/Y1, consisted entirely of principal and reduced the liability to $115,000 ($135,000 – $20,000). Therefore, year 1 interest expense is $11,500 ($115,000 x 10%).

Question 11:PVE-0013Need a hint?See Reference...When should a lessor recognize in income a nonrefundable lease bonus paid by a lessee on signing an operating lease?When received.At the inception of the lease.At the expiration of the lease.Over the life of the lease.This answer is correct. ASC Topic 840 specifies that, in an operating lease, the lesser should recognize rental revenues on a straight-line basis. This means that a lease bonus should be recorded as unearned revenue and recognized as rental revenue over the life of the lease.

Question 12:PVE-0032Need a hint?See Reference...For a capital lease, the amount recorded initially by the lessee as a liability shouldExceed the present value at the beginning of the lease term of minimum lease payments during the lease term.

Exceed the total of the minimum lease payments during the lease term.Not exceed the fair value of the leased property at the inception of the lease.Equal the total of the minimum lease payments during the lease term.This answer is correct. Per ASC Topic 840, the lessee shall record a capital lease as a debit to an asset account and a credit to a liability account for an amount equal to the present value of the total of the minimum lease payments as of the beginning of the lease term. However, if the amount so determined exceeds the fair value of the leased property at the inception of the lease, the amount recorded as the asset and obligation shall be the fair value of the leased property.

Question 13:PVE-0010Need a hint?See Reference...Howard Company sublet a portion of its warehouse for 5 years at an annual rental of $18,000, beginning on May 1, year 1. The tenant paid 1 year’s rent in advance, which Howard recorded as a credit to unearned rental income. Howard reports on a calendar-year basis. The adjustment on December 31, year 1, should be

Dr. Cr. No entry Unearned rental income Rental income

$ 6,000

$ 6,000

Rental income Unearned rental income

$ 6,000

$ 6,000

Unearned rental income Rental income

$ 12,000

$ 12,000

This answer is correct. The solutions approach is to determine how much of the annual rental payment is earned income and how much should be deferred to the next period. The amount earned this period is calculated by multiplying the annual payments by that portion of the year that has expired since May 1, year 1 ($18,000 x 8/12 = $12,000). The adjusting entry is

Unearned rental income

12,000

Rental income 12,000

Question 14:PVE-0045Need a hint?See Reference...On January 1, year 1, Flip Corporation signed a 10-year noncancelable lease for certain machinery. The terms of the lease called for Flip to make annual payments of $30,000 for 10 years with title to pass to Flip at the end of this period. Accordingly, Flip accounted for this lease transaction as a capital lease of the machinery. The machinery has an estimated useful life of 15 years and no salvage value. Flip uses

the straight-line method of depreciation for all of its fixed assets. The lease payments were determined to have a present value of $201,302 with an effective interest rate of 10%. With respect to this capitalized lease, Flip should record for year 1Lease expense of $30,000.Interest expense of $16,580 and depreciation expense of $13,420.Interest expense of $20,130 and depreciation expense of $13,420.Interest expense of $13,420 and depreciation expense of $16,580.This answer is correct. Per ASC Topic 840, a lessee’s capital lease will incur interest expense. Interest expense, $20,130, is the carrying value of the lease obligation multiplied by the effective interest rate ($201,302 x 10%). Additionally, the cost of the equipment is depreciated over the life of the asset rather than the life of the lease since title automatically passes to the lessee at the end of 10 years and the lessee will own the asset. Depreciation expense, $13,420, is the cost of the equipment depreciated over 15 years ($201,302/15 years). One difficulty with this question is whether there was a $30,000 payment on January 1, year 1. If so the interest expense would have been $17,130 [($201,302 – $30,000 x 10%)]. There is no interest expense given in that amount. Therefore we must assume an ordinary annuity.

Question 15:PVE-0049Need a hint?See Reference...On December 31, year 1, Bain Corp. sold a machine to Ryan and simultaneously leased it back for 1 year. Pertinent information at this date follows:

Sales price $360,000

Carrying amount 330,000

Present value of reasonable rentals ($3,000 for 12 months @ 12%)

34,100

Estimated remaining useful life 12 years

In Bain’s December 31, year 1 balance sheet, the deferred revenue from the sale of this machine should be$34,100$30,000$ 4,100$0This answer is correct. ASC Topic 840 generally treats a sale-leaseback as a single financing transaction in which any profit on the sale is deferred and amortized by

the seller. However, ASC Topic 840 amends this general rule when either only a minor part of the remaining use of the leased asset is retained (case 1), or when more than a minor part but less than substantially all of the remaining use of the leased asset is retained (case 2). Case 1 occurs when the PV of the lease payments is 10% or less of the FV of the sale-leaseback property. Case 2 occurs when the leaseback is more than minor but does not meet the criteria of a capital lease. This is an example of case 1, because the PV of the lease payments ($34,100) is equal to or less than 10% of the FV of the asset ($360,000). ASC Topic 840 specifies that under these circumstances, the full gain ($360,000 – $330,000 = $30,000) is recognized, and none is deferred.

Question 16:PVE-0035Need a hint?See Reference...On January 1 of the current year, Tell Co. leased equipment from Swill Co. under a nine-year sales-type lease. The equipment had a cost of $400,000, and an estimated useful life of fifteen years. Semiannual lease payments of $44,000 are due every January 1 and July 1. The present value of lease payments at 12% was $505,000, which equals the sales price of the equipment. Using the straight-line method, what amount should Tell recognize as depreciation expense on the equipment in the current year?$26,667$33,667$44,444$56,111This answer is correct. The leased asset should be recorded at the present value of the future lease payments because it is less than or equal to the fair value of the leased asset. Since the facts do not indicate that title is transferred to the lessee or a bargain purchase or lease option exists, the leased asset should be depreciated over the lesser of the lease term or the asset’s useful life; $56,111 (= $505,000 ÷ 9 years).

Question 17:PVE-0005Need a hint?See Reference...Bain Co. entered into a 10-year lease agreement for a new piece of equipment worth $500,000. At the end of the lease, Bain will have the option to purchase the equipment. Which of the following would require the lease to be accounted for as a capital lease?The lease includes an option to purchase stock in the company.The estimated useful life of the leased asset is 12 years.The present value of the minimum lease payments is $400,000.The purchase option at the end of the lease is at fair

market value.This answer is correct because the ten-year lease term is greater than or equal to 75% of the life of the leased asset (10/12 = 83%).

Question 18:PVE-0042Need a hint?See Reference...Steam Co. acquired equipment under a capital lease for six years. Minimum lease payments were $60,000 payable annually at year-end. The interest rate was 5% with an annuity factor for six years of 5.0757. The present value of the payments was equal to the fair market value of the equipment. What amount should Steam report as interest expense at the end of the first year of the lease?$0$3,000$15,227$18,000This answer is correct. The requirement is to determine the amount of interest expense that should be reported. This problem requires you to calculate the present value of the minimum lease payments, which is the present value of the ordinary annuity of $60,000 at 5% for 6 periods, or $304,542 (5.0757 x $60,000). This is the correct answer because interest expense for Year 1 is calculated as 5% of the carrying value of $304,542, or $15,227.

Question 19:PVE-0043Need a hint?See Reference...On December 30, year 1, Ames Co. leased equipment under a capital lease for 10 years. It contracted to pay $40,000 annual rent on December 31, year 1, and on December 31 of each of the next 9 years. The capital lease liability was recorded at $270,000 on December 30, year 1, before the first payment. The equipment’s useful life is 12 years, and the interest rate implicit in the lease is 10%. Ames uses the straight-line method to depreciate all equipment. In recording the December 31, year 2, payment, by what amount should Ames reduce the capital lease liability?$27,000$23,000$22,500$17,000This answer is correct. The initial lease obligation at 12/31/Y1 was $270,000. The first payment was made the same day, and therefore consisted entirely of principal reduction. After the payment, the lease obligation was $230,000 ($270,000 – $40,000). The next lease payment, on 12/31/Y2, consists of both principal and interest. The interest portion is $23,000 ($230,000 x 10%), so the reduction in the lease liability is $17,000 ($40,000 – $23,000).

Question 20:PVE-0031Need a hint?See Reference...A lease contains a bargain purchase option. In determining the lessee’s capitalizable cost at the beginning of the lease term, the payment called for by the bargain purchase option wouldNot be capitalized.Be subtracted at its present value.Be added at its exercise price.Be added at its present value.This answer is correct. Per ASC Topic 840, minimum lease payments include the rental payments plus the amount of the bargain purchase option if it exists. The amount to be capitalized is the present value of the minimum lease payments. Therefore, the present value of the bargain purchase option would be added to the present value of the rental payments (assumed to be previously calculated) in determining the lessee’s capitalizable cost.

Question 21:PVE-0039Need a hint?See Reference...On December 31, year 1, Neal, Inc. leased machinery with a fair value of $105,000 from Frey Rentals Co. The agreement is a 6-year noncancelable lease requiring annual payments of $20,000 beginning December 31, year 1. The lease is appropriately accounted for by Neal as a capital lease. Neal’s incremental borrowing rate is 11%. Neal knows the interest rate implicit in the lease payments is 10%.

The present value of an annuity due of 1 for 6 years at 10% is 4.7908.The present value of an annuity due of 1 for 6 years at 11% is 4.6959.

In its December 31, year 1 balance sheet, Neal should report a lease liability of$75,816$85,000$93,918$95,816This answer is correct. The initial lease liability at 12/31/Y1, before the 12/31/Y1 payment, is $95,816 ($20,000 x 4.7908). The liability is recorded at the lower of the FV of the leased asset ($105,000) or the PV of the minimum lease payments ($95,816). The 10% rate is used to compute PV, rather than the 11% rate, because ASC Topic 840 states that the discount rate is to be the lessee’s incremental borrowing rate, unless the lessor’s implicit rate is known and is less than the

lessee’s incremental borrowing rate. The 12/31/Y1 payment consists entirely of principal, reducing the 12/31/Y1 liability to $75,816 (95,816 – $20,000).

Question 22:PVE-0026Need a hint?See Reference...Benedict Company leased equipment to Mark, Inc. on January 1, year 2. The lease is for an 8-year period expiring December 31, year 9. The first of 8 equal annual payments of $600,000 was made on January 1, year 2. Benedict had purchased the equipment on December 29, year 1, for $3,200,000. The lease is appropriately accounted for as a sales-type lease by Benedict. Assume that the present value at January 1, year 2, of all rent payments over the lease term discounted at a 10% interest rate was $3,520,000. What amount of interest income should Benedict record in year 3 (the second year of the lease period) as a result of the lease?$261,200$296,000$320,000$327,200

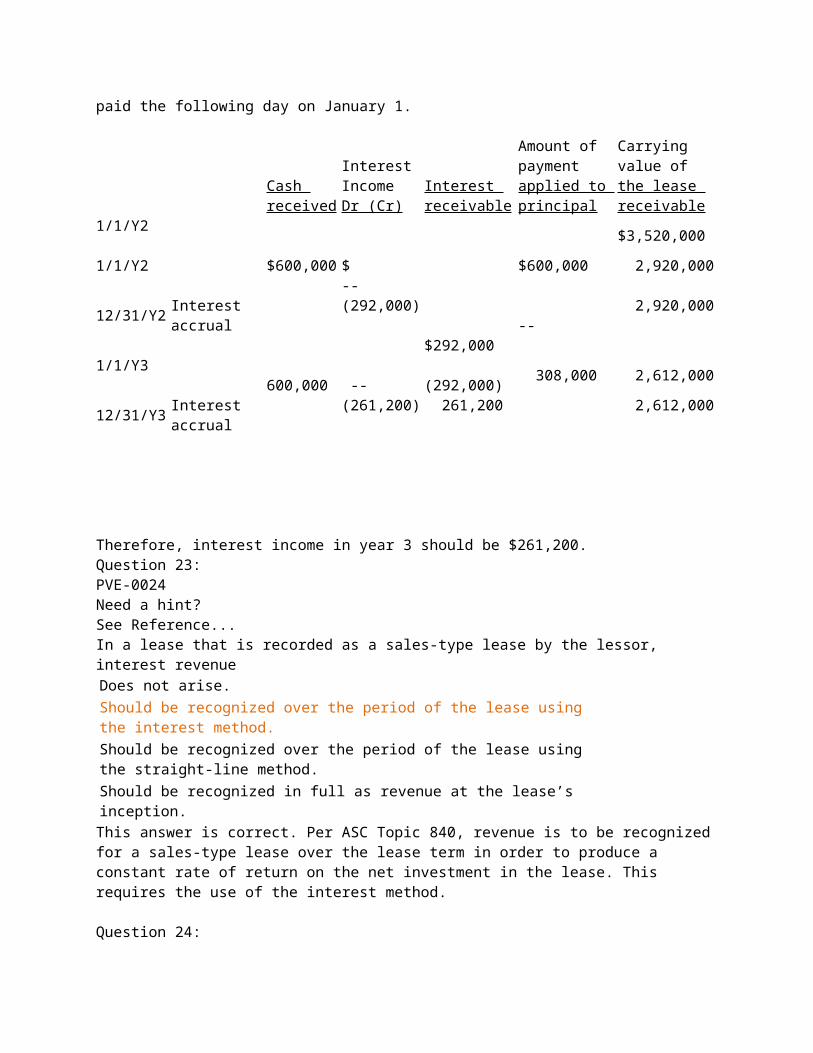

This answer is correct. The income recorded would be 10% of the present value of the lease receivable balance outstanding in year 2 (year 3). The interest can be computed using an amortization table. Notice that interest is accrued on December 31 of each year, and is paid the following day on January 1.

Cash received

Interest IncomeDr (Cr)

Interest receivable

Amount of paymentapplied to principal

Carrying value ofthe lease receivable

1/1/Y2 $3,520,0001/1/Y2 $600,000 $ -- $600,000 2,920,00012/31/Y2

Interest accrual

(292,000)

$292,000 -- 2,920,000

1/1/Y3 600,000 -- (292,000) 308,000 2,612,00012/31/Y3

Interest accrual

(261,200) 261,200

2,612,000

Therefore, interest income in year 3 should be $261,200.Question 23:PVE-0024Need a hint?See Reference...In a lease that is recorded as a sales-type lease by the lessor, interest revenueDoes not arise.Should be recognized over the period of the lease using the

interest method.Should be recognized over the period of the lease using the straight-line method.Should be recognized in full as revenue at the lease’s inception.This answer is correct. Per ASC Topic 840, revenue is to be recognized for a sales-type lease over the lease term in order to produce a constant rate of return on the net investment in the lease. This requires the use of the interest method.

Question 24:PVE-0036Need a hint?See Reference...The lessee’s net carrying value of an asset arising from the capitalization of a lease would be periodically reduced by theTotal minimum lease payment.Portion of minimum lease payment allocable to interest.Portion of minimum lease payment allocable to reduction of principal.Depreciation/amortization of the asset.

This answer is correct. The solutions approach is to prepare the journal entry for the lease payment

Capital lease obligation (principal)

xxx

Interest expensexxx

Cash

xxx

and the journal entry for the lease amortization.

Amortization of leased asset xxx

Accumulated amortization/depreciation

xxx

Therefore, only the amortization of the leased asset results in a reduction of the carrying value of the asset.

Question 25:PVE-0050Need a hint?See Reference...On January 1, year 1, Hooks Oil Co. sold equipment with a carrying amount of $100,000, and a remaining useful life of 10 years, to Maco Drilling for $150,000. Hooks immediately leased the equipment back under a 10-year capital lease with a present value of $150,000 and will depreciate the equipment using the straight-line method. Hooks made the first annual lease payment of $24,412 in December year 1. In Hooks’ December 31, year 1 balance sheet, the unearned gain on equipment sale should be$50,000

$45,000$25,588$0This answer is correct. According to ASC Topic 840, sale-leaseback transactions are treated as though two transactions were a single financing transaction, if the lease qualifies as a capital lease. Any gain on the sale is deferred and amortized over the lease term (if possession reverts to the lessor) or the economic life (if ownership transfers to the lessee). Since this is a capital lease, the entire gain ($150,000 – $100,000 = $50,000) is deferred at 1/1/Y1. At 12/31/Y1 an adjusting entry must be prepared to amortize 1/10 of the unearned gain (1/10 x $50,000 = $5,000), because the lease covers 10 years. Therefore, the unearned gain at 12/31/Y1 is $45,000 ($50,000 – $5,000).

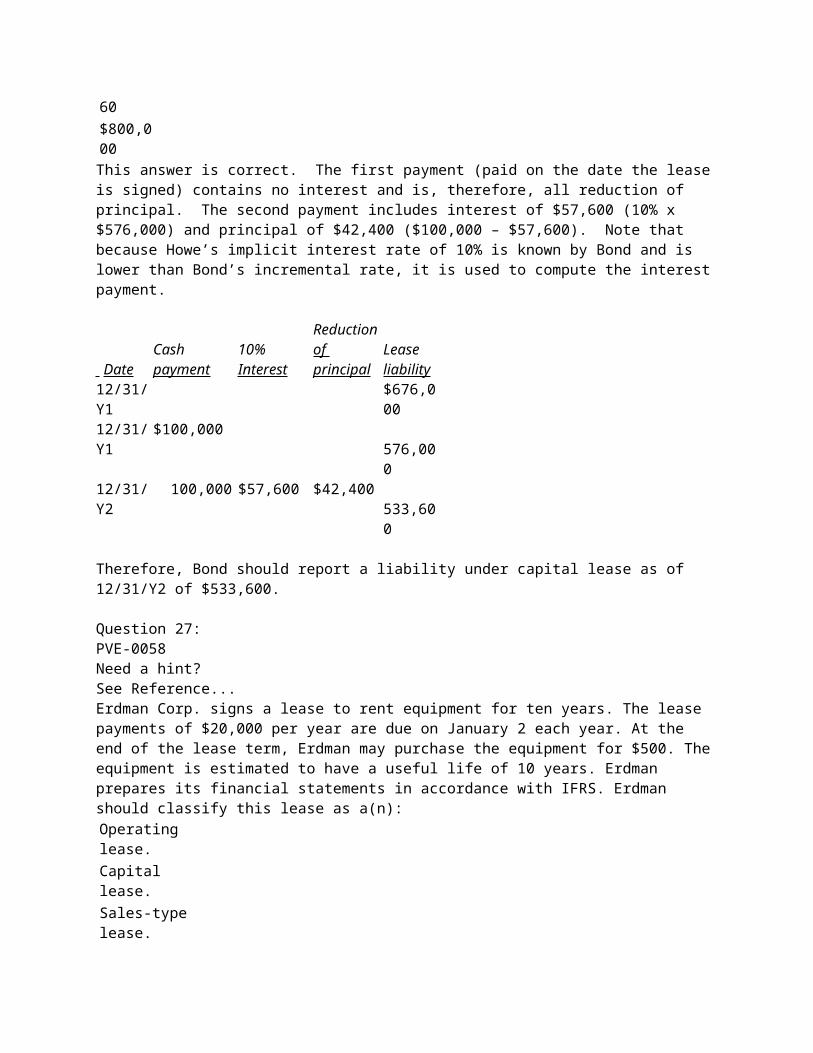

Question 26:PVE-0041Need a hint?See Reference...Bond Company leased equipment from Howe, Inc. on December 31, year 1, for a 10-year period (the useful life of the asset) expiring December 30, year 11. Equal annual payments under the lease are $100,000 and are due on December 31 of each year. The first payment was made on December 31, year 1, and the second payment was made on the due date. The present value at December 31, year 1, of the minimum lease payments over the lease term discounted at 10% (the implicit rate computed by Howe and known by Bond) was $676,000. Bond’s incremental borrowing rate was 12% at December 31, year 1. The lease is appropriately accounted for as a capital lease by Bond. What should be the balance in Bond’s liability under capital lease account at December 31, year 2?$533,600$545,120$607,960$800,000

This answer is correct. The first payment (paid on the date the lease is signed) contains no interest and is, therefore, all reduction of principal. The second payment includes interest of $57,600 (10% x $576,000) and principal of $42,400 ($100,000 – $57,600). Note that because Howe’s implicit interest rate of 10% is known by Bond and is lower than Bond’s incremental rate, it is used to compute the interest payment.

Date Cash payment

10% Interest

Reductionof principal

Leaseliability

12/31/Y1

$676,000

12/31/Y1

$100,000 576,00

012/31/Y2

100,000 $57,600 $42,400 533,600

Therefore, Bond should report a liability under capital lease as of 12/31/Y2 of $533,600.

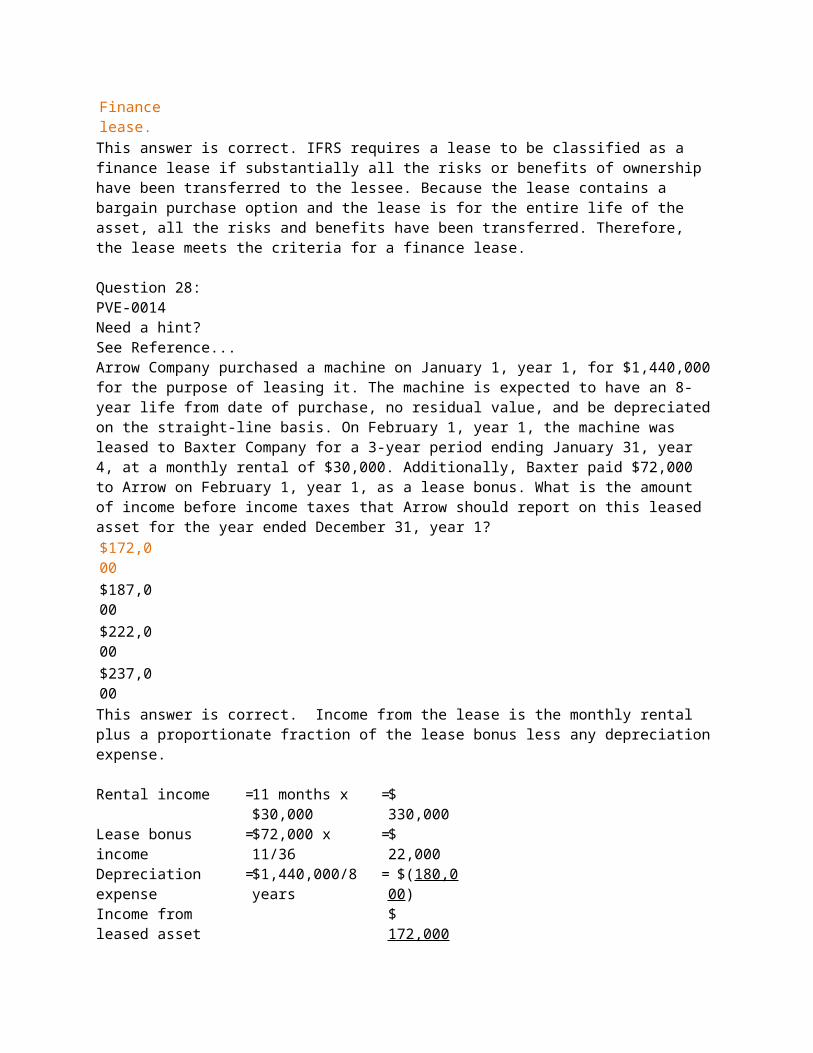

Question 27:PVE-0058Need a hint?See Reference...Erdman Corp. signs a lease to rent equipment for ten years. The lease payments of $20,000 per year are due on January 2 each year. At the end of the lease term, Erdman may purchase the equipment for $500. The equipment is estimated to have a useful life of 10 years. Erdman prepares its financial statements in accordance with IFRS. Erdman should classify this lease as a(n):Operating lease.Capital lease.Sales-type lease.Finance lease.This answer is correct. IFRS requires a lease to be classified as a finance lease if substantially all the risks or benefits of ownership have been transferred to the lessee. Because the lease contains a bargain purchase option and the lease is for the entire life of the asset, all the risks and benefits have been transferred. Therefore, the lease meets the criteria for a finance lease.

Question 28:PVE-0014Need a hint?See Reference...Arrow Company purchased a machine on January 1, year 1, for $1,440,000 for the purpose of leasing it. The machine is expected to have an 8-year life from date of purchase, no residual value, and be depreciated on the straight-line basis. On February 1, year 1, the machine was leased to Baxter Company for a 3-year period ending January 31, year 4, at a monthly rental of $30,000. Additionally, Baxter paid $72,000 to Arrow on February 1, year 1, as a lease bonus. What is the amount of income before income taxes that Arrow should report on this leased asset for the year ended December 31, year 1?$172,000$187,000$222,000$237,000

This answer is correct. Income from the lease is the monthly rental plus a proportionate fraction of the lease bonus less any depreciation expense.

Rental income =11 months x $30,000

=$ 330,000

Lease bonus income

=$72,000 x 11/36 =$ 22,000

Depreciation expense

=$1,440,000/8 years

= $(180,000)

Income from leased asset

$ 172,000

Note that the lease bonus is recognized as income proportionately over the 36-month lease period. The leased asset is depreciated for a full year since it has an 8-year life from the date of purchase (January 1).

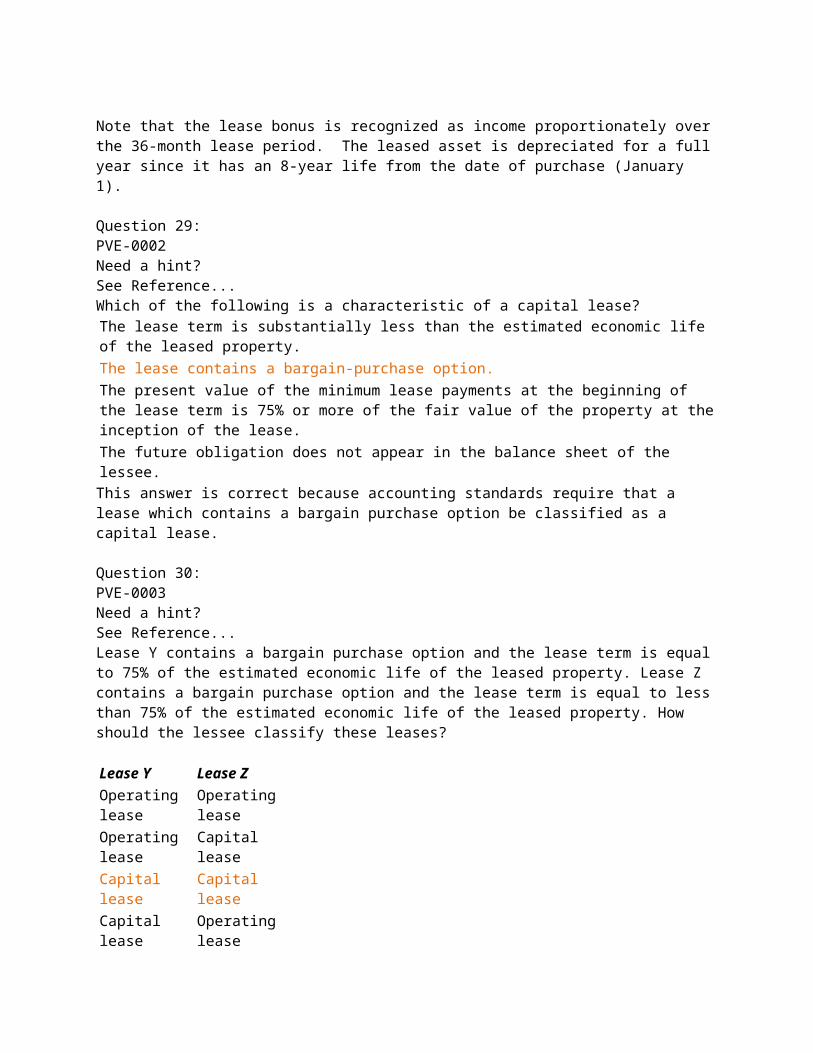

Question 29:PVE-0002Need a hint?See Reference...Which of the following is a characteristic of a capital lease?The lease term is substantially less than the estimated economic life of the leased property.The lease contains a bargain-purchase option.The present value of the minimum lease payments at the beginning of the lease term is 75% or more of the fair value of the property at the inception of the lease.The future obligation does not appear in the balance sheet of the lessee.This answer is correct because accounting standards require that a lease which contains a bargain purchase option be classified as a capital lease.

Question 30:PVE-0003Need a hint?See Reference...Lease Y contains a bargain purchase option and the lease term is equal to 75% of the estimated economic life of the leased property. Lease Z contains a bargain purchase option and the lease term is equal to less than 75% of the estimated economic life of the leased property. How should the lessee classify these leases?

Lease Y Lease Z Operating lease

Operating lease

Operating lease

Capital lease

Capital lease Capital lease

Capital leaseOperating lease

This answer is correct. ASC Topic 840 states that a lease shall be classified as a capital lease by the lessee if one or more of the four criteria are met. The four criteria are as follows:

1.

Lease transfers ownership to the lessee during lease term

2.

Lease contains a bargain purchase option

3.

Lease term is 75% or more of the economic useful life of the property

4.

Present value of the minimum lease payment equals 90% or more of FV of the leased property

Since both Lease Y and Lease Z meet at least one of the criteria, both are considered capital leases.

Question 31:PVE-0056Need a hint?See Reference...Which of the following is a criterion for a lease to be classified as a capital lease in the books of a lessee?The lease contains a bargain purchase option.The lease does not transfer ownership of the property to the lessee.The lease term is equal to 65% or more of the estimated useful life of the leased property.The present value of the minimum lease payments is 70% or more of the fair market value of the leased property.This answer is correct. The requirement is to identify the criterion for a lease to be classified as a capital lease. According to ASC Topic 840, this answer is correct because if the lease contains a bargain purchase option, it must be classified as a capital lease.

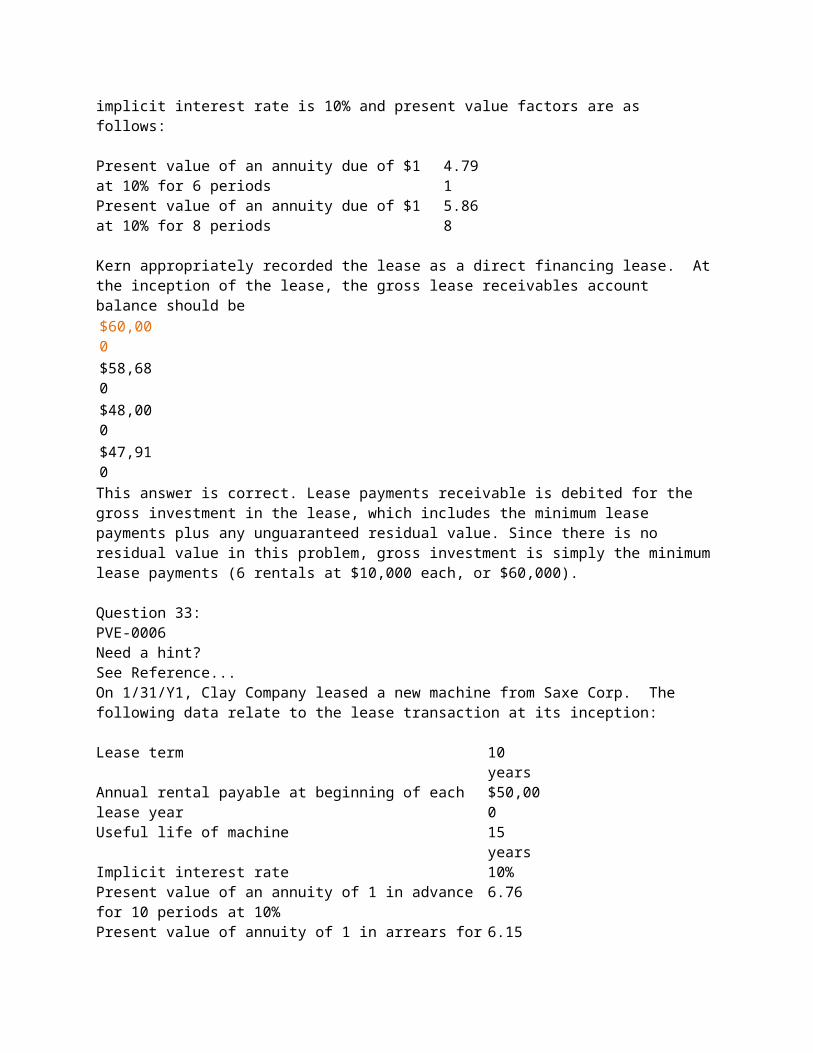

Question 32:PVE-0023Need a hint?See Reference...On August 1, year 1, Kern Company leased a machine to Day Company for a 6-year period requiring payments of $10,000 at the beginning of each year. The machine cost $48,000, which is the fair value at the lease date, and has a useful life of 8 years with no residual value. Kern’s implicit interest rate is 10% and present value factors are as follows: Present value of an annuity due of $1 at 10% for 6 periods

4.791

Present value of an annuity due of $1 at 10% for 8 periods

5.868

Kern appropriately recorded the lease as a direct financing lease. At the inception of the lease, the gross lease receivables account balance should be$60,000$58,680

$48,000$47,910This answer is correct. Lease payments receivable is debited for the gross investment in the lease, which includes the minimum lease payments plus any unguaranteed residual value. Since there is no residual value in this problem, gross investment is simply the minimum lease payments (6 rentals at $10,000 each, or $60,000).

Question 33:PVE-0006Need a hint?See Reference...On 1/31/Y1, Clay Company leased a new machine from Saxe Corp. The following data relate to the lease transaction at its inception:

Lease term 10 years

Annual rental payable at beginning of each lease year

$50,000

Useful life of machine 15 years

Implicit interest rate 10%Present value of an annuity of 1 in advance for 10 periods at 10%

6.76

Present value of annuity of 1 in arrears for 10 periods at 10%

6.15

Fair value of the machine $400,000

The lease has no renewal option, and the possession of the machine reverts to Saxe when the lease terminates. At the inception of the lease, Clay should record a lease liability of$400,000$338,000$307,500$0This answer is correct. At the inception of a lease, the lessee records a lease liability if the lease is considered to be a capital lease. To be considered a capital lease, a lease must satisfy any one of the four criteria specified in ASC Topic 840. This lease does not satisfy any of the four criteria. The lease has no bargain purchase option and does not transfer title. The lease term is not 75% or more of the useful life (10 years out of 15 years is 67%) and the PV of the lease payments is not 90% or more of the FV of the asset [(6.76 x $50,000) / $400,000 = 84.5%]. Therefore, this is an operating lease, not a capital lease, and no liability is recorded at the lease’s inception.

Question 34:PVE-0030Need a hint?See Reference...Beal, Inc. intends to lease a machine from Paul Corp. Beal’s incremental borrowing rate is 14%. The prime rate of interest is 8%. Paul’s implicit rate in the lease is 10%, which is known to Beal. Beal computes the present value of the minimum lease payments using8%10%12%14%This answer is correct. ASC Topic 840 states that the lessee should compute the PV of the minimum lease payments using the lesser of the lessee’s incremental borrowing rate (14% in this case) or the implicit rate used by the lessor if known (10% in this case). The PV of the minimum lease payments should be computed using the implicit rate of 10% because it is known by the lessee and is lower than the incremental rate.

Question 35:PVE-0012Need a hint?See Reference...Initial direct costs areExpensed currently for sales-type leases.Capitalized and amortized to expense over the lease term for all leases.Capitalized only if the related lease qualifies as a capital lease.Presented on the balance sheet as a contra account to capitalized leased assets.This answer is correct. Initial direct costs are costs incurred in connection with the negotiation and consummation of leases, such as legal fees, commissions, etc. For sales-type leases, profit or loss is recognized upon inception of the lease. In keeping with the matching principle, the costs of consummating that lease should be taken into income at the same time as the resulting profit or loss. Therefore, initial direct costs for sales-type leases are expensed currently.

Question 36:PVE-0021Need a hint?See Reference...On January 1, year 1, JCK Co. signed a contract for an 8-year lease of its equipment with a 10-year life. The present value of the 16 equal semiannual payments in advance equaled 85% of the equipment’s fair value. The contract had no provision for JCK, the lessor, to give up legal ownership of the equipment. Should JCK recognize rent or interest revenue in year 2, and should the revenue recognized in year 2 be

the same or smaller than the revenue recognized in year 1?

Year 2 revenues recognized

Year 2 amount recognizedcompared to year 1

Rent The sameRent SmallerInterest The sameInterest Smaller

This answer is correct. This lease qualifies as a direct financing lease; therefore interest revenue will be recognized rather than rent revenue. Had the lease qualified as an operating lease, rent revenue would have been recognized. The lessor’s criteria for direct financing classification is as follows: 1.

The lease transfers ownership to the lessee, at the end of the lease

2.

The lease contains a bargain purchase option

3.

The lease term is > 75% of an asset’s economic life

4.

The present value of the minimum lease payments is > 90% of the fair value of the leased asset.

In addition, collectibility of the minimum lease payments must be predictable and there may be no important uncertainties concerning costs yet to be incurred by the lessee. Since the question is silent in this regard, we will assume that the latter conditions are met. Recall that if one of the first four criteria are met, the lease is treated as a capital lease. In this case, since the lease term is for 80% of the asset’s economic life, test (3) is met, and the lease is properly treated as a capital lease. In addition, the amount of interest revenue will be smaller in year 2 than the revenue in year 1. This result occurs because the present value of the minimum lease payments or carrying value of the obligation decreases each year as lease payments are received. As this occurs, the amount of interest revenue on the outstanding amount of the investment will decrease as well. Over the course of time, the investment reduction portion of each level payment increases and the amount of interest declines.

Question 37:PVE-0004Need a hint?See Reference...On January 1, year 1, Frost Co. entered into a two-year lease agreement with Ananz Co. to lease 10 new computers. The lease term begins on January 1, year 1 and ends on December 31, year 2. The lease agreement requires Frost to pay Ananz two annual lease payments of $8,000. The present value of the minimum lease payments is $13,000. Which of the following circumstances would require Frost to classify and account for the arrangement as a capital lease?The economic life of the computers is three years.The fair value of the computers on January 1, year 1, is $14,000.Frost Co. does not have the option of purchasing the computers at the end of the lease term.

Ownership of the computers remains with Ananz Co. throughout the lease term and after the lease ends.This answer is correct because the present value of the minimum lease payments ($13,000) is greater than 90% of the fair value of the leased asset.

Question 38:PVE-0033Need a hint?See Reference...What are the three types of period costs that a lessee experiences with capital leases?Lease expense, interest expense, amortization expense.Interest expense, amortization expense, executory costs.Amortization expense, executory costs, lease expense.Executory costs, interest expense, lease expense.This answer is correct. The three costs incurred by a lessee with respect to capital leases are interest expense, amortization expense, and executory costs. Each payment consists of principal reduction and interest expense. The amount capitalized must be amortized over the useful life of the asset. Executory costs, such as insurance, maintenance, etc., are borne by the lessee. The basic premise in capital leases is the risks and responsibilities of ownership are transferred from lessor to lessee.

Question 39:PVE-0020Need a hint?See Reference...In a lease that is recorded as a direct financing lease by the lessor, the difference between the gross investment in the lease and the sum of the present values of the components of the gross investment should be recognized as incomeIn full at the lease’s expiration.In full at the lease’s inception.Over the period of the lease using the interest method of amortization.Over the period of the lease using the straight-line method of amortization.This answer is correct. For a direct financing lease, the difference between the gross investment in the lease and the sum of the present values of the components of the gross investment is, by definition, unearned interest income. Per ASC Topic 840, the unearned interest income is recognized as income over the lease term so as to produce a constant rate of return on the net investment using the effective interest method of amortization. Other methods of amortization are allowed by ASC Topic 840 provided the results are not materially different from those obtained by applying the prescribed method. Because no information is given concerning such materiality, this answer is the best answer.

Question 40:PVE-0027Need a hint?See Reference...Melville Company leased equipment from Rice Corporation on July 1, year 1, for an 8-year period expiring June 30, year 9. Equal payments under the lease are $600,000 and are due on July 1 of each year. The first payment was made on July 1, year 1. The rate of interest contemplated by Melville and Rice is 10%. The cash selling price of the equipment is $3,520,000 and the cost of the equipment on Rice’s accounting records is $2,800,000. Assuming that the lease is appropriately recorded as a sales-type lease, what is the amount of profit on the sale and interest income that Rice should record for the year ended December 31, year 1?$0 and $0.$0 and $146,000.$720,000 and $146,000.$720,000 and $160,000.This answer is correct. Melville’s gross profit is the difference between the present value of the lease payments, $3,520,000 (which is also the cash selling price of the equipment), and the cost of goods sold ($2,800,000), or $720,000. Interest income is found by multiplying the book value of the receivable from the lessee (total lease payments receivable minus unearned interest) outstanding during year 1 ($3,520,000 initial balance less $600,000 payment made on 7/1/Y1) times the implicit interest rate (10%) for 1/2 of a year. Therefore, interest income is $146,000 ($2,920,000 x 10% x 1/2).

Question 41:PVE-0025Need a hint?See Reference...Farm Co. leased equipment to Union Co. on July 1, year 1, and properly recorded the sales-type lease at $135,000, the present value of the lease payments discounted at 10%. The first of eight annual lease payments of $20,000 due at the beginning of each year was received and recorded on July 3, year 1. Farm had purchased the equipment for $110,000. What amount of interest revenue from the lease should Farm report in its year 1 income statement?$0$5,500$5,750$6,750This answer is correct. In this sales-type lease, the lessor would recognize a gross profit on the sale on 7/1/Y1 of $25,000 ($135,000 present value less $110,000 cost). In addition, interest revenue is recognized in year 1 for the period 7/1 through 12/31. The initial net lease payments receivable on 7/1/Y1 is $135,000. The first rental payment received on 7/3/Y1 consists entirely of principal, reducing the net receivable to $115,000 ($135,000 - $20,000). Therefore, year 1 interest revenue for the 6-month period is $5,750 ($115,000 x 10% x 6/12).

Question 42:PVE-0046Need a hint?See Reference...Hines Company leased a new machine from Ashwood Company on December 31, year 1, under a lease with the following pertinent information:

Lease term 8 yearsAnnual rental payable at the beginning of each lease year

$ 50,000

Useful life of the machine 10 years

Present value of the 8 lease payments at 12/31/Y1

$258,000

The machine reverts to Ashwood at lease expiration date and has a fair value of $280,000 at the inception of the lease. Hines uses the straight-line method of depreciation. For the year ended December 31, year 2, how much depreciation (amortization) should Hines record for the capitalized leased machine?$35,000$32,250$28,000$25,800This answer is correct. Per ASC Topic 840, the lessee records the asset at the lower of (1) the present value of the minimum lease payments or (2) the fair market value of the leased asset. In this case, the present value ($258,000) is less than the fair market value ($280,000); therefore, $258,000 is capitalized. Since the machine reverts to the lessor at the end of the lease, the lessee should depreciate it over the lease term (8 years) even though it is less than the useful life (10 years). Depreciation expense is $32,250 ($258,000/8 years).

Question 43:PVE-0022Need a hint?See Reference...Beth Co. leased equipment to Wolf, Inc. on April 1, year 1. The lease is appropriately recorded as a direct financing lease by Beth. The lease is for an 8-year period expiring March 31, year 9. The first equal annual payment of $500,000 was made on April 1, year 1. Beth had purchased the equipment on January 1, year 1, for $2,800,000. The equipment has an estimated useful life of 8 years with no residual value expected. Beth uses straight-line depreciation and takes a full year’s depreciation in the year of purchase. The cash selling price of the equipment is $2,934,000. Assuming an interest rate of 10%, what amount of interest income should Beth record in year 1 as a result of the lease?$0

$182,550$243,400$280,000This answer is correct. The present value of the eight $500,000 lease payments is given to be $2,934,000 (cash selling price of the equipment). Since $500,000 is paid at the inception of the lease, the book value of the lease payments receivable (total minimum lease payments minus unearned interest income) outstanding for the last 9 months is $2,434,000. The 10% interest thereon is $243,400, but only 3/4 (9 months/12 months) of this amount, or $182,550, is associated with the period ending December 31, year 1.

Question 44:PVE-0015Need a hint?See Reference...On January 1, year 1, Glen Co. leased a building to Dix Corp. for a 10-year term at an annual rental of $50,000. At inception of the lease, Glen received the first 2 years’ rent of $100,000 and a security deposit of $100,000. This deposit will not be returned to Dix upon expiration of the lease but will be applied to payment of rent for the last 2 years of the lease. What portion of the $200,000 should be shown as a current and long-term liability, respectively, in Glen’s December 31, year 1 balance sheet?

Current Liability

Long-term liability

$ 0 $ 200,000$ 50,000 $ 100,000$ 100,000 $ 100,000$ 100,000 $ 50,000This answer is correct. At 1/1/Y1, Glen would record as a current liability unearned rent of $50,000, and as a long-term liability unearned rent of $150,000. During year 1, the current portion of unearned rent was earned and would be recognized as revenue. At 12/31/Y1, the portion of the long-term liability representing the second year’s rent ($50,000) would be reclassified as current, leaving as a long-term liability, the $100,000 representing the last 2 years’ rent.

Question 45:PVE-0038Need a hint?See Reference...Barker Company leased a new machine from Bell Company on July 1, year 1, under a lease with the following pertinent information:

Lease term 10 years

Annual rental payable at the beginning of each lease year

$30,000

Useful life of the machine 12

yearsImplicit interest rate 14%

Present value of an annuity of $1 in advance for 10 periods at 14%

5.95

Present value of $1 for 10 periods at 14% 0.27

Barker has the option to purchase the machine on July 1, year 11, by paying $40,000, which approximates the expected fair value of the machine on the option exercise date. The cost of the machine on Bell’s accounting records is $150,000. On July 1, year 1, Barker should record a capitalized leased asset of$150,000$178,500$189,300$190,000This answer is correct. In a capital lease, the lessee records as an asset the lower of (1) the present value (PV) of the minimum lease payments, or (2) the FV of the leased asset. Since the FV is not given, we must assume that the asset is to be recorded at the PV of the minimum lease payments. The minimum lease payments must include any bargain purchase options (BPO). However, the $40,000 purchase option in this problem is not a BPO, since $40,000 approximates the expected fair value of the machine on the option exercise date. Therefore, the PV of the minimum lease payments is $178,500 (5.95 x $30,000). Note that the cost of the asset to the lessor ($150,000) is not relevant to the lessee.

Question 46:PVE-0047Need a hint?See Reference...In a sale-leaseback transaction, a gain resulting from the sale should be deferred at the time of the sale-leaseback and subsequently amortized when I. The seller-lessee has transferred substantially all the risks of ownership.II. The seller-lessee retains the right to substantially all of the remaining

use of the property.

I only.

II only.

Both I and II.

Neither I nor II.

This answer is correct. Per ASC Topic 840, in a sale-leaseback where the seller-lessee retains the right to substantially all of the remaining use of the property, a gain resulting from the sale should be deferred and subsequently amortized. On the other hand, when the seller-lessee has transferred substantially all the risks of ownership, any gain or loss on sale is recognized immediately.