accountancy futures – issue 03

DESCRIPTION

Accountancy Futures – February 2011 – Issue 03 (Published by ACCA)TRANSCRIPT

ACCOUNTANCY FUTURESCRITICAL ISSUES FOR TOMORROW’S PROFESSION I EDITION 03 I 2011

THE AGE OF INTEGRATIONA NEW DAWN FOR CORPORATE REPORTING?

PLUS: CFOs: AFTER THE STORM I GENERATION Y I PEOPLE POWER FOR SMALL PRACTICE I CARBON MARKETS I CAPACITY BUILDING I AUDITORS IN DANGER I AUSSIE TAX RULES I ACCOUNTING FOR CONFIDENCE I KENYA’S CASH REVOLUTION I CONVERGENCE CRUNCH

AC

CO

UN

TAN

CY FU

TURES I E

DITIO

N 03 I 2011

29 Lincoln’s Inn Fields London WC2A 3EE United Kingdom +44 (0)20 7059 5000 www.accaglobal.com

Editor Chris Quick

+44 (0)20 7059 5966

Managing editor Jamie Ambler

Sub editors Dean Gurden, Peter Kernan

Design manager Jackie Dollar

Junior designer Robert Mills

Production manager Anthony Kay

Head of publishing Adam Williams

Pictures Corbis

Printing Polestar Wheatons

Paper Antalis McNaughton Group. This magazine is produced on paper that

contains certified fibres sourced from forestry within 120km of the paper mill.

The mill operates under ISO 14001 certified environmental management system

and has its own biomass energy production.

ACCA

President Mark Gold FCCA

Deputy president Dean Westcott FCCA

Vice-president Barry Cooper FCCA

Chief executive Helen Brand

ACCA Connect

Tel +44 (0)141 582 2000

A list of ACCA offices can be found inside the back cover of this journal.

ACCA (the Association of Chartered Certified Accountants) is the global body for professional accountants. We aim to offer business-relevant, first-choice qualifications to people around the world who seek a rewarding career in accountancy, finance and management. ACCA has 140,000 members and 404,000 students, who it supports throughout their careers, providing services through a network of 83 offices and centres around the world.

Accountancy Futures® is a registered trademark of ACCA.

All views expressed in Accountancy Futures are those of the contributors. The Council of ACCA and the publishers do not guarantee the accuracy of statements by contributors or advertisers, or accept responsibility for any statement that they may express in this publication. Copyright ACCA 2011 Accountancy Futures. No part of this publication may be reproduced, stored or distributed without the express written permission of ACCA. Accountancy Futures is published by Certified Accountants Educational Trust in cooperation with ACCA. ISSN 2042-4566. Accountancy Futures Edition 3 was published in February 2011.

29 Lincoln’s Inn FieldsLondon WC2A 3EEUnited Kingdom+44 (0)20 7059 5000www.accaglobal.com

ACCOUNTANCY FUTURES

PG02 EDITION 03

ACCOUNTANCY FUTURES

PG03 EDITION 03

John Davies head of [email protected]

Aziz Tayyebi financial reporting [email protected]

Dr Afra Sajjad head of education and policy development, ACCA Pakistan

Editorial board

The start of a new era in corporate reporting? The concept of integrated reporting – the integration of financial and non-financial information in a company’s reporting – now has real impetus with the launch of a committee of big-name companies, global accountancy firms, professional bodies and standard-setters to back it and draw up a plan of how it will work. It could range from the maintenance of International Financial Reporting Standards with some environmental and other bolt-ons, right up to a fundamental overhaul of corporate reporting. We will follow what promises to be a lively debate closely in Accountancy Futures, starting in this edition with a series of articles exploring the concept, including an article by Sir Michael Peat, chairman of the new committee. We also tackle many other topics of interest to finance professionals and business leaders keen to explore what the future holds and how they can shape it.

Chris Quick, editor You can find out more about ACCA’s Accountancy Futures programme at www.accaglobal.com/af

ACCOUNTANTS FOR BUSINESSWe explore the vision for integrated reporting and look at the new environment facing CFOs. We also examine the challenges Generation Y gives employers and report from the World Congress of Accountants.

CARBON ACCOUNTINGWe take a look at the development of carbon markets and the accounting and measurement issues they raise. Also under the spotlight are Scope 3 emissions – those that are produced indirectly by businesses. The fact that these are not being counted could hinder the development of a low-carbon economy.

Public sector goes global: Andreas Bergmann, chair of the International Public Sector Accounting Standards Board, reports on progress in creating a global accounting framework. PG66

PG01

CO

VE

RPG

02 C

ON

TAC

T D

ETA

ILS

PG03

WE

LCO

ME

PG04

CO

NTE

NTS

PG05

PG06

LO

OK

ING

AH

EA

D: R

OU

ND

-UP

PG07

PG

08 IN

TEG

RA

TED

RE

POR

TIN

G: S

IR M

ICH

AE

L PE

AT

PG09

PG10

INTE

GR

ATE

D R

EPO

RTI

NG

: A N

EW

DA

WN

?PG

11PG

12PG

13PG

14 IN

TEG

RA

TED

RE

POR

TIN

G: R

OB

ER

T E

CC

LES

PG15

INTE

GR

ATE

D R

EPO

RTI

NG

: PA

UL

DR

UC

KM

AN

PG16

CFO

s: A

FTE

R T

HE

STO

RM

PG

17PG

18PG

19PG

20 G

EN

ER

ATI

ON

Y: T

HE

GR

EA

T TA

LEN

T SH

OW

PG21

PG22

SM

ALL

PR

AC

TIC

E: K

NO

CK

ING

ON

DO

OR

SPG

23PG

24PG

25 S

MA

LL P

RA

CTI

CE

: PE

OPL

E P

OW

ER

PG26

PG27

PG28

WO

RLD

CO

NG

RE

SS O

F A

CC

OU

NTA

NTS

PG29

PG30

PG31

PG32

PG33

PG34

CA

RB

ON

: CR

EA

TIN

G A

MA

RK

ET

PG35

PG36

PG37

PG38

CA

RB

ON

: CA

LIB

RA

TIN

G T

HE

CO

STPG

39PG

40PG

41PG

42 C

AR

BO

N: S

CO

PE 3

PG43

PG44

AU

DIT

: TH

E IN

FORM

ATI

ON

FLO

WPG

45PG

46PG

47PG

48 A

UD

IT: I

N S

EA

RC

H O

F A

WID

ER

RO

LEPG

49PG

50

PG04 EDITION 03

AUDITWith audit in the spotlight after the financial crisis, we ask how it could evolve in the future, reporting on the views of CFOs, auditors, investors and others. We also explore the thorny issue of auditor liability.

NARRATIVE REPORTING We report on an ACCA/Deloitte survey of CFOs’ views and perspectives on narrative reporting.

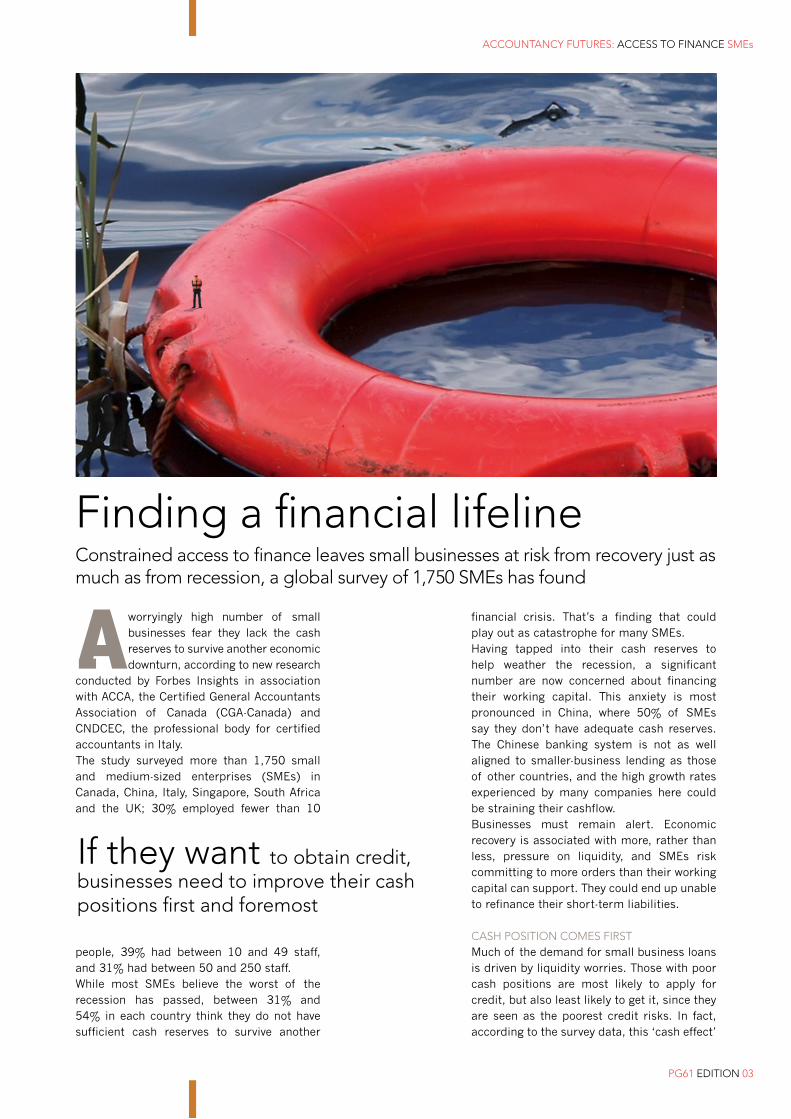

ACCESS TO FINANCEConstrained access to finance leaves small businesses at risk from recovery just as much as from recession, finds a global survey of 1,750 small business by ACCA, CGA-Canada and Italian accountancy body CNDCEC.

PG51

AU

DIT

: LIA

BIL

ITY

AN

D T

HE

DA

NG

ER

ZO

NE

PG52

PG53

PG54

PG55

AU

DIT

: CO

NFI

DE

NC

E A

CC

OU

NTI

NG

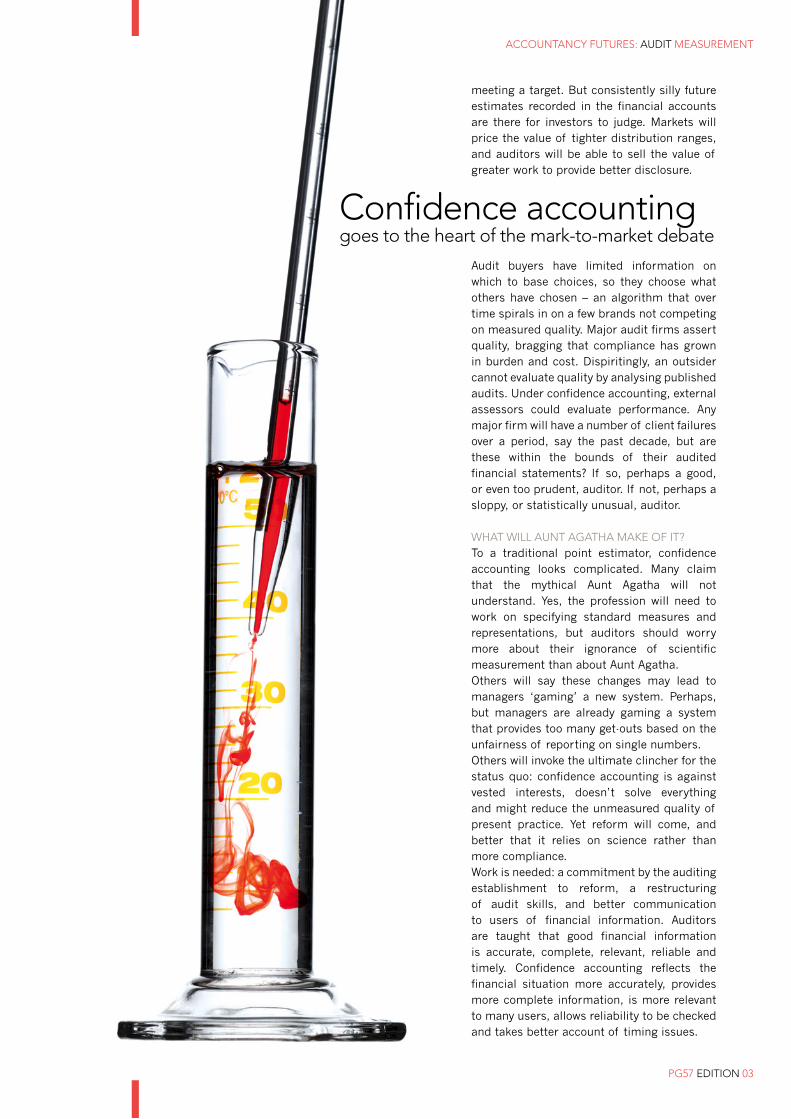

PG56

PG57

PG58

NA

RR

ATI

VE

RE

POR

TIN

G: C

FO P

ER

SPE

CTI

VE

SPG

59PG

60PG

61 A

CC

ESS

TO

FIN

AN

CE

: SM

Es

PG62

PG63

PG64

AC

CE

SS T

O F

INA

NC

E: K

EN

YA’S

CA

SH R

EV

OLU

TIO

NPG

65PG

66 P

UB

LIC

SE

CTO

R: A

ND

RE

AS

BE

RG

MA

NN

PG67

PG68

PG69

PG70

PU

BLI

C S

EC

TOR

: SU

STA

INA

BIL

ITY

SCR

UTI

NY

PG71

PG72

PU

BLI

C S

EC

TOR

: ETH

ICA

L ST

AN

DA

RD

SPG

73PG

74 C

APA

CIT

Y B

UIL

DIN

G: I

NFR

AST

RU

CTU

RE

PG75

PG76

PG77

PG78

CA

PAC

ITY

BU

ILD

ING

: RE

SEA

RC

H S

KIL

LSPG

79PG

80 F

INA

NC

IAL

RE

POR

TIN

G: I

FRS

CO

NV

ER

GE

NC

EPG

81PG

82 F

INA

NC

IAL

RE

POR

TIN

G: P

AU

L C

HE

RRY

PG83

PG84

TA

X: A

USS

IE R

ULE

SPG

85PG

86PG

87 R

ISK

: TH

E T

RU

TH A

BO

UT

LEV

ER

AG

EPG

88PG

89PG

90 D

IVE

RSI

TY: R

ISE

OF

THE

She

FOPG

91PG

92PG

93 D

IVE

RSI

TY: C

RA

CK

ING

TH

E G

LASS

CE

ILIN

GPG

94PG

95PG

96 H

EA

LTH

: TE

CH

NO

LOG

YPG

97PG

98PG

99 A

CC

A N

ETW

OR

KPG

100

BA

CK

CO

VE

R

PG05 EDITION 03

Carve-outs and convergence: Paul Cherry, chair of the IASB’s IFRS Advisory Council, shares his views on the future of International Financial Reporting Standards. PG82

ACCOUNTANCY FUTURES: PREVIEW

PG06 EDITION 03

Looking aheadA round-up of recent and upcoming research and events

01 INVESTING IN WOMENGovernments would benefit from paying more attention to the vital role women play in driving economic growth, new research shows. The Deloitte report, The Gender Dividend: Making the Business Case for Investing in Women, found that the role women play – or don’t play – can affect economic competitiveness. Go to www.accaglobal.com/genderdividend to read the report in full.

02 MAXIMISE YOUR PEOPLE POWERA new report from ACCA and KPMG, Effective Talent Management in Finance, sends some clear messages about the importance of integrated talent management and the key elements required. The research highlights that less than 20% of organisations fully integrate talent identification, development, deployment and retention activity across the finance team. Talent management practices are often informal and sometimes run in isolation. The report looks at how talent management can shape and influence the structure of finance functions, and highlights the practices organisations should adopt to deliver the best possible talent development for finance professionals. Go to www.accaglobal/accountants_business for more.

03 IAAER AND ACCA PROLONG PARTNERSHIPThe International Association of Accounting Education and Research (IAAER) and ACCA announced at the 11th World Congress of Accounting Educators and Researchers in Singapore in November 2010 that they would continue working closely together until 2014 – an extension of three years on the original memorandum of understanding. Donna Street, IAAER president and professor at the University of Dayton, said: ‘IAAER is delighted that the extension of our partnership with ACCA through 2014 will enable our organisations to continue to help focus academic research on issues facing international standard setters by informing the debate on a variety of agenda topics. The three-year extension also ensures continuation of our joint efforts to build accounting research and teaching skills capacity in transitional economies.’ 04 ASSESSING PPP PRACTICESACCA has commissioned research into public-private partnerships (PPPs). Using France and the UK – both mature in their use of PPPs – as benchmarks, the project will assess the PPP maturity of a number of countries in Asia Pacific. It will look at the degree of

Female solidarity: demonstrations in Makati, Philippines last year on International Women’s Day. It is on 8 March this year and is celebrated as a national holiday in China, Russia, Vietnam and Bulgaria.

ACCOUNTANCY FUTURES: PREVIEW

PG07 EDITION 03

establishment of policy frameworks provided by the central government, the sectors of application, and capabilities in relevant sectors. The project will identify the variety of PPP concepts globally with the aim of drawing up guidelines for appropriate local practice in a global context rather than advocating global best practice, and will pay specific attention to accountability issues. 05 RISK APPETITE RESEARCHACCA is examining the role of corporate governance in controlling the risk-taking behaviour of boards. The study is designed to address the gap in research literature and wider understanding about the governance processes that determine the level of risk to which companies choose to be exposed when setting cash-holding and leverage policies. 06 WHAT BUSINESS LEADERS THINKAn ACCA survey of surveys of CFOs and CEOs in 2010 reflects uncertain environments, both macro and micro, and a strengthening push for innovation. Surveys by PwC, Deloitte, IBM and Ernst & Young are among the studies looked at. The uncertain environments range from the world economy to consumer demand, along with increasing regulation, shifts in economic power with increasing competition and price pressures. Accompanying the need to innovate and respond to changing environments, there is evidence of conservatism and control. Accountants’ skills in measuring and monitoring performance as well as controlling costs are being relied upon to provide stability. 07 GLOBAL BUSINESS RISKRegulation and compliance remain the biggest risks to global business in 2011, but cost cutting and lower margins are the fastest-growing risks, according to new research. Ernst & Young’s Global Business Risk Report reveals that cost cutting had risen four places to number two and pricing pressures had moved up 10 places to fifth position compared with 2010. The report is available at www.accaglobal.com/gbrr 08 CONFIDENCE GROWINGCEOs’ confidence in future growth has returned to nearly pre-crisis levels, according to a new survey. PwC’s 14th annual global CEO

Survey found that the positive momentum in CEO confidence was reflected in hiring plans. More than half of CEOs polled worldwide said they expected to recruit in the next 12 months. CEOs in Central Europe, Asia Pacific and Africa were particularly bullish about hiring.More at www.accaglobal.com/ceosurvey 09 CANCUN CONVERSATIONSCompanies are increasingly seeking out and adopting sustainable business practices, according to emerging evidence from a global research project. A Review of Corporate Sustainability in 2010 reveals a clear increase in the numbers of companies with active programmes, the research, commissioned by KPMG International and carried out by the Economist Intelligence Unit, showed. For more visit www.accaglobal.com/kpmg_cop16 10 ISLAMIC FINANCE ROUNDTABLEAs Islamic finance rapidly expands, so divergence in accounting practices is an ever more difficult factor. ACCA and KPMG have therefore embarked on a joint project to direct the International Accounting Standards Board’s (IASB) response to standardise accounting in this area. The first of three high-level roundtables was held in Kuala Lumpur, Malaysia, last October. Subsequent meetings of the IASB, regulators, banks and ratings agencies are due to take place in April 2011 in London and Bahrain. A final report will be issued later this year. 11 THE IMPACT OF ECONOMIC CONDITIONSGlobal economic conditions continue to dominate business life. ACCA is launching a range of projects to research the effect of economic conditions around the world, and ways in which the impact can be managed. The aims of the research include: understanding trends and developments, championing the role of the accountant in business – especially the CFO – and illuminating areas of best practice to help companies add value to business strategy and operations. It will also identify ways in which accountants can add value as advisers, and work at understanding learning points and indicators for moving towards a refreshed global economy. Go to www.accaglobal.com/gec to read the latest insights and results of the most recent global economic conditions survey report.

When I took my first tentative steps as an accountant (they are still fairly tentative!), my grandfather told me that the essence of the

job was to provide trust and confidence, vital prerequisites for commerce and prosperity. He added that accounting information should be clear and comprehensible – meaningful and powerful communication. The test was whether the information could be understood by an intelligent but non-financially literate person. HRH The Prince of Wales has always had a remarkable knack for putting his finger on

issues of long-term importance. Fairly soon after I started to work for him, some eight years ago, he made it clear that he didn’t believe that the accounting profession was providing the information needed to tackle the issues confronting the world economy at the beginning of the 21st century: increasing population, over-consumption of finite natural resources, pollution of land, sea and air and climate change. His Royal Highness felt that the limited information provided to investors, managers, employees, and indeed consumers and members of the public, was a major

The integrated imperativeInternational Integrated Reporting Committee chairman Sir Michael Peat sets out a vision for corporate reporting that brings together the financial and non-financial

HRH The Prince of Wales: accountants must draw out the information needed to tackle pollution, climate change and over-consumption.

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS INTEGRATED REPORTING

PG08 EDITION 03

Integrated reporting is a vital building block to enable the world’s economy to evolve and maintain standards of living for people who already enjoy a good quality of life, and create them for the hundreds of millions who do not

Sir Michael Peat is principal private secretary to HRH The Prince of Wales and The Duchess of Cornwall. He has also served as keeper of the privy purse and been a partner at KPMG. A qualified accountant, he has an MBA from INSEAD and an MA in law from Oxford.

Deep-seated changes to our current economic model are need to tackle the over-consumption of resources and the risk of catastrophic climate change. Every publicly listed company has to file an annual report on its financial performance in compliance with, in most cases, either International Financial Reporting Standards (IFRS) or US GAAP. Increasingly, companies are also producing corporate social responsibility or sustainability reports although these can vary widely in terms of relevance and quality, largely because there is no global standard for measuring and reporting on environmental, social and governance performance.What is required is a concise, comprehensive and comparable reporting framework that integrates material financial and non-financial information. It should be structured around the organisation’s strategic objectives, its governance and business model. The objectives for an integrated reporting framework are to:A support the information needs of long-term

investors, by showing the longer-term

consequences of decision-making

B reflect the interconnections between

environmental, social, governance and

financial factors in decisions that affect

long-term performance, making clear the link

between sustainability and economic value

C provide the framework for environmental and

social factors to be taken systematically into

account in reporting and decision-making

D rebalance performance metrics away from an

undue emphasis on short-term financials

E bring reporting closer to the information

used by management to run the business on

a day-to-day basis.

Source: www.integratedreporting.org

barrier to the development of a more resource-efficient, sustainable economy. He established The Prince’s Accounting for Sustainability Project (A4S) to address this issue. During its first four years A4S created a prototype integrated reporting framework and provided practical guidance for how organisations can embed sustainability into their day-to-day operations. In July last year, integrated reporting developed globally with the formation of the International Integrated Reporting Committee (IIRC). The committee is a joint initiative between A4S, the Global Reporting Initiative and the International Federation of Accountants, together with a powerful cross-section of representatives from the corporate, accounting, securities, regulatory and standard-setting sectors. The role of the IIRC is to help develop a new internationally accepted approach to reporting – an approach which provides more comprehensive information about the full range of an organisation’s impacts and performance, past and future, in a clear, concise, consistent and comparable manner. In other words, to help develop reports that not only provide financial information, but information about an organisation’s governance, social and environmental performance; and not in disconnected sections or silos but in an integrated manner, which reflects the reality that all these elements (financial, governance, social and environmental) are closely related and inter-dependent and flow from the organisation’s overall strategy. This is a significant step forward and a daunting task, but it is a task that cannot be shirked if the information needed so urgently to meet the challenges of the 21st century is to be provided. Put briefly, integrated reporting is a vital building block to enable the world’s economy to evolve and maintain standards of living for people who already enjoy a good quality of life, and create them for the hundreds of millions who do not, without the present unsustainable over-consumption of the world’s finite natural resources. Information of this kind would meet the test articulated by my grandfather all those years ago.

IIRC on integrated reporting

PG09 EDITION 03

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS INTEGRATED REPORTING

New dawn for reportingACCA’s Neil Stevenson looks at who and what is driving the ambitious moves to develop an integrated reporting framework and make it compulsory

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS INTEGRATED REPORTING

PG10 EDITION 03

The global financial crisis has persuaded many of the need for a new economic model that can protect businesses, investors, employees

and society from a cycle of successive and increasingly debilitating crises. At present, short-term financial gains can take priority over long-term value generation, encouraging a gung-ho approach to risk-taking that can lead to a level of market instability, which has the potential to devastate individual businesses and whole economies. The current model of corporate reporting, it is felt, does not do enough to discourage such behaviour because it doesn’t pay enough attention to factors such as risk, strategy, governance and the sustainability of business models.These concerns, which have grown as business leaders and governments have agonised over the causes of the financial crisis, have given impetus to existing demands for a change in emphasis in corporate reporting on the grounds that it does not currently adequately reflect material environmental, social and governance (ESG) factors. These include resource usage, social impacts, human rights and how a business might contribute to or be affected by climate change. Many believe that over-consumption of finite natural resources and the risk of catastrophic climate change present one of the world’s greatest challenges – and is its biggest business risk. Supporters of integrated reporting argue that the inclusion of all these non-financial but nevertheless crucial risk factors into corporate reporting would help steer business decision-making in a more sustainable direction – in both financial and environmental terms. They argue that the quality of reporting would improve because businesses would provide a more strategic picture of the issues that are critical to their long-term sustainability and success. In addition, those managing companies would be able to make better resource decisions by including issues relating to natural and social capital as well as financial capital. The result would be a more holistic picture of the reporting entity that covers both risks and opportunities, and reflects the interconnections between ESG and financial factors.

INTEGRATED REPORTINGWhile there have been significant advances in sustainability reporting over recent years, no single body has so far had the authority or oversight to bring all the different reporting pillars together in a single, mandatory, fully integrated and globally endorsed framework. This is the ambition of the International Integrated Reporting Committee (IIRC),

Neil Stevenson is ACCA’s executive director – brand, and a member of the International Integrated Reporting Committee (IIRC) Engagement and Communications taskforce. His remit at ACCA covers marketing, communications, policy, technical issues and publishing. This includes promoting a global agenda of research and insights, complementing his interest in issues involving change and innovation in the global professions.

formed last year by a progressive section of the business, financial and accounting community, bringing together many leading accountancy firms, big-name companies, business groups and professional accountancy bodies, including ACCA. The two key bodies involved are the Prince of Wales Accounting for Sustainability Project (A4S) and the Global Reporting Initiative. A series of profile-raising events are planned for 2011, kicking off with a roundtable discussion in Mumbai, India, chaired by International Organization of Securities Commissions chairman Jane Diplock, as Accountancy Futures went to press.The release of a discussion paper looking at an integrated reporting framework is planned for June 2011. Interested stakeholders are invited to comment before it is formalised and presented to the G20 in Cannes in November 2011. G20 approval will add credibility and inject vigour into the move towards global standardisation. The IIRC’s aim is that the framework will be constructed in a way that allows companies to report in a clear, concise, consistent and comparable way.

SUSTAINABILITY CHALLENGEThe accounting element of the massive change required was highlighted by the creation of A4S in 2004, which reiterated the need for new approaches to accounting and reporting to reflect the broader and longer-term consequences of corporate decisions. Without more complete and comprehensive information, management, investors and others cannot make the fully informed decisions needed to prosper in the face of sustainability challenges.A4S felt that the profession’s best contribution to sustainability would be to establish a

Man

agem

ent c

omm

enta

ry

Financial

Gov

erna

nce

and

rem

uner

atio

n Environm

ent and social

Integrated reporting

framework

INTEGRATED REPORTING: FOCUSING ON THE TOP SLICEIntegrated reporting provides the top level structure for the whole reporting pyramid

Source: IIRC

PG11 EDITION 03

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS INTEGRATED REPORTING

global framework of mandatory ‘connected reporting’ requirements for listed companies and for a global committee of key stakeholder groups to push for global adoption. The GRI, along with other bodies such as the Carbon Disclosure Project, have made significant steps forward in formalising reporting guidelines for companies’ material environmental, social and economic impacts. Yet despite the corporate uptake and integration of more-than-financial impact assessments, there is still little evidence that collective corporate efforts have significantly halted activities that pollute, deplete resources and destroy non-financial value. The voluntary nature of such reporting initiatives means that take-up can be fragmented, allowing companies with large impacts on the environment and society to avoid full and transparent disclosure.

WHAT WILL IT LOOK LIKE?Considering that integrated reporting is still in an embryonic phase, it should come as no surprise that a clear formulation of what exactly it constitutes is still being debated. Definitions range from the maintenance of current financial reporting and accounting practices based on International Financial Reporting Standards (IFRS) with an ESG section bolted on, right up to a complete change in the fundamentals of accounting and reporting formats. There is, however, agreement on the need for a concise and comprehensive integrated reporting framework which is structured around an organisation’s strategic objectives, its governance and business model, and integrating material financial and non-financial information.The key consideration is the strategic ingraining and disclosure of all ESG factors affecting the future financial performance

The result would be a more holistic picture of the reporting entity that covers both risks and opportunities, and reflects the interconnections between ESG and financial factors

and associated risk rating of a company’s activities. The central tenet of integrated reporting has been part of the sustainability and CSR reporting space for a number of years, but it is IIRC’s ambition to bring together financial and non-financial risk disclosure in a global, mandatory framework which sets it apart from past initiatives, and which engages and relates to investors.Sceptics of the integrated reporting initiative point towards a raft of issues. The first is the sheer ambition of the change that is being put forward, involving the huge challenge of gaining global consensus to a mandatory change, especially given that it has so far taken more than 30 years to agree the global application of IFRS. Other criticisms include fears that it will lead to increased complexity in reporting and greater resourcing requirements, and a tick-box approach. But given the powerful backers and the fundamental financial and environmental issues involved, the launch of the IIRC may well turn out to be a turning point in the development of corporate reporting.However, alongside this development, it is clear that we will also need to encourage a greater proportion of shareholders to become more interested in the governance and sustainability of the organisations they invest in. This will be the best way of ensuring integrated reporting is embedded in business in practice. Much attention has been paid, rightly, to the models around auditing and assurance and corporate reporting. Perhaps we need to develop more urgency around this third dimension: governance and stewardship. This could lead to the fulfilment of the ambitions of those who advocate the ‘triple bottom line’: a sustainable approach to sustainability.

For new ACCA/Deloitte research into narrative reporting, see page 58.

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS INTEGRATED REPORTING

PG12 EDITION 03

Blurry greys: Clarification on what it means is needed, but ACCA’s Rachel Jackson says integrated reporting can sharpen the focus of corporate activities

The idea of integrated reporting has been increasingly under discussion by stakeholders in the world of business accounting and sustainability reporting. The definition of what integrated reporting actually covers is currently a range of blurry greys rather than a crisp and clear black and white. However, looked at in broad terms, integrated reporting is simply the end result (the reporting) of a complex but inclusive process that integrates the business strategy with material sustainability issues.Some optimistic observers see an integrated strategy as boosting transparency and offering a clearer explanation of the relationship between companies’ financial and non‑financial performance. Other, more cautious professionals highlight possible challenges such as greater reporting complexity, comparability and assurance across sectors and countries, and discord in timescales between compilation of the integrated reporting framework and continuing physical impacts of climate change.There is no doubt that a well‑developed integrated reporting methodology could focus corporate efforts to integrate material sustainability issues and impacts arising from business activities more deeply in strategic decision‑making processes. Deploying an integrated strategy as a risk screen to assess operations for their medium to long‑term sustainability and financial implications could strengthen governance protocols, create less disparate businesses and change financial market investment behaviour.Few companies currently take an integrated reporting approach. This blank canvas offers the relevant professions an opportunity to shape the framework. ACCA is pleased to be part of the IIRC, which has ambitious plans to do just this. We shall continue to participate actively, taking part in the debates that arise, addressing questions around the relevance of integrated reporting, finding ways to stimulate investor and regulator demand for integrated reporting, and developing useful reporting metrics.

Join the dots: Filling in the gaps left by the key guidance for integrated reporting is essential to drive widespread take-up, says ACCA’s Roger Adams

One of the main proposals made by the International Integrated Reporting Committee (IIRC) is the need for new approaches to accounting and reporting to reflect the broader long‑term consequences of corporate activities. By providing robust and comparable reporting guidance on how to link corporate strategy to financial and non‑financial performance, the IIRC can convince businesses and investors that financial value can be derived from integrated reporting.Integrated reports should clearly identify and explain the link between an organisation’s strategic goals and the resulting impact on parameters such as the wider business context, key relationships, resource dependencies and governance structures, and help establish a more holistic corporate risk profile.To ensure widespread business acceptance, the IIRC must connect the dots between itself and other key reporting guidance. ACCA continues to support the GRI and its sustainability reporting framework, and the Climate Disclosure Standards Board (CDSB) and its climate change reporting framework. As well as identifying the information needs of investors, the IIRC needs to provide solutions to any perceived barriers to the take‑up of integrated reporting. The to‑do list includes addressing the requirements of multiple stakeholders, determining the materiality of issues, giving an option of different reporting levels, assessing knock‑on impacts to auditing standards and internal control checks, and overcoming corporate confidentiality issues.Opportunities and benefits arising from a move towards integrated reporting will have to be clearly demonstrated within an urgent context requiring the momentum towards a sustainable, low‑carbon global economy to gather pace. Ultimately the establishment of an international framework that not only merges financial and sustainability outcomes but also supports the achievement of a sustainable economy will require support from governments, the finance and accounting community and wider stakeholder groups.

Rachel Jackson is ACCA’s head of sustainability. She champions ACCA’s global sustainability agenda on reporting and disclosure with specific reference to environmental, economic and social issues. Rachel represents ACCA on various technical committees and working groups including FEE and the EPC Climate Change Adaptation Task Force.

Roger Adams FCCA is ACCA’s director – special assignments. He previously managed ACCA’s global policy positions on professional issues, such as sustainability and corporate responsibility.

PG13 EDITION 03

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS INTEGRATED REPORTING

Q: How would you define integrated reporting?A: It is reporting in a single document the material measures of financial and non-financial (ie environmental, social and governance) performance and their relationships to each other. It is also about an integrated website that makes it easy for users to find and analyse in one place financial and non-financial information, including more detailed information of particular interest to specific stakeholders. Finally, integrated reporting is as much about listening as talking. A company should use its website for dialogue and engagement with shareholders and all other stakeholders to create a collective conversation. Q: What makes it different from existing concepts and models in this area?A: Two things come to mind. The first is corporate social responsibility or sustainability reporting, typically in a report separate from the company’s financial report; it was originally referred to as the triple bottom line of economic, environmental and social metrics. The second is the balanced scorecard, which includes financial and non-financial metrics.

Q: Why do we need it?A: A sustainable society requires all its companies to have sustainable strategies. A sustainable strategy is one that creates value over the long term. This is in contrast to a focus on short-term financial performance

that imposes negative externalities on society. Integrated reporting establishes the discipline for integrated internal management of financial and non-financial performance. It is also the best way to report on a sustainable strategy. Q: What are the main challenges to adoption?A: First, a company must truly have a sustainable business rather than just say it has. Second, a collaborative and multifunctional process is required for producing the integrated report; no one group has all the information necessary for doing so. Third, internal control and measurement systems for non-financial information are typically not as sophisticated and robust as those for financial information. Fourth, internal sceptics have to be brought on board. Fifth, a great deal of education will be required of the users of the integrated report, both shareholders and other stakeholders.

Q: Will it make annual reports even longer?A: Not necessarily. An integrated report doesn’t have to be the annual report. Southwest Airlines morphed its Southwest Cares report into its integrated report. The key thing to note is that the integrated report is the material financial and non-financial information, so it doesn’t have to be long. Length often comes from detailed disclosures required by regulation.

Q: What role do you see accountants playing in integrated reporting?A: Accountants have a major role to play, if they are willing to do so. They are experts in the measurement and reporting of financial information. They need to broaden their content knowledge to include non-financial information, often working with others who are expert in a particular aspect of it so they can help the organisations they work for to implement integrated reporting both internally and externally.

Q: How can integrated reports be audited?A: Integrated reporting requires integrated auditing. There are a number of barriers to overcome here. Better standards are needed for non-financial measurement and reporting, auditors need to develop the capability to audit non-financial information, and there are also liability concerns.

Professor Robert Eccles is a senior lecturer at Harvard Business School. He undertakes research on corporate reporting, and has written three books on the subject, including One Report: Integrated Reporting for a Sustainable Strategy (with Michael Krzus). He is also a steering committee member of the International Integrated Reporting Committee.

Perspective: the academicWe put the same set of key questions about integrated reporting to two experts in the field. First up, Professor Robert Eccles of Harvard Business School

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS INTEGRATED REPORTING

PG14 EDITION 03

Q: Will it make annual reports even longer?A: This question misses the point. We are certainly not talking about combined reporting but integrated reporting. Combined reporting adds to the annual report but integrated reporting changes some of the fundamentals.

Q: What role do you see accountants playing in integrated reporting?A: At present the ‘natural’ role for the accountancy profession has been seen to be in financial reporting. However, the training of an accountant is not in numbers but in information, the data that underpins an organisation. Thus integrated reporting is the domain of the accountant more than other professions. It may need broader thinking and the use of multidisciplinary teams with specific skills and experience, but the judgment and analytical skills inherent in the accountancy profession are the key.

Q: How can integrated reports be audited?A: The information reported (and withheld) should be capable of being verified at some point in the future. Possible assurance may be in the form of an audit confirmation that the management has embraced integrated reporting framework principles. It is also worth considering whether management and auditors should confirm that the information reported is a fair reflection of the information used by management to run the business.

Q: How would you define integrated reporting?A: Integrated reporting brings together financial and non-financial information in a clear, concise, consistent and relevant format. The goal of an integrated reporting framework is to improve the quality of corporate reporting so companies can provide a more strategic picture of the issues critical to long-term sustainability and success. Integrated reporting includes information about natural and social capital as well as financial capital. This information provides important insights for those interested in the way a company thinks and acts. The framework should help to create a more cohesive reporting model by highlighting areas where convergence is needed in standards and national regulations.

Q: What makes it different from existing concepts and models in this area?A: The strategic long-term perspective across the entire company differentiates it. Other models also address this concept and are generating good ideas, but the International Integrated Reporting Committee (IIRC) uniquely brings together for the first time financial standard setters, securities regulators and sustainability standard setters with representatives from companies, investors and civil society.

Q: Why do we need it?A: The financial crisis has demonstrated the need for reporting that gives better information about how a business is performing against its long-term strategy. At present various standard setters and regulators are responsible for individual elements of reporting. There is thus a risk that multiple standards will emerge.

Q: What are the main challenges to adoption?A: These troubled economic times may lead businesses to see priorities differently, plus there is an expectation from many quarters of deeper and more rigorous standards for financial and non-financial reporting. The convergence to integrated reporting appears to have a momentum that will mean success but there will also be the devil in the detail when it comes to implementing the design of the integrated reporting framework however flexible a framework is conceived.

Paul Druckman is chair of the executive board of The Prince of Wales’s Accounting for Sustainability Project, and co-chair of the working group of the International Integrated Reporting Committee. After a highly successful business career as a technology entrepreneur, he is a non-executive chairman and director for a number of businesses.

Perspective: the entrepreneurOur second expert, Paul Druckman, allies business acumen to his work in driving sustainability issues in the accountancy profession

PG15 EDITION 03

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS INTEGRATED REPORTING

As we move into 2011 there is a general feeling that the worst of the financial crisis is behind us and a conviction that growth, albeit

slow, is returning to the major economies. But there is also much less certainty about prospects than there used to be, and the post-crisis environment is one that is placing new demands on CFOs.As Krzysztof Rybi ski, former deputy governor of the Polish National Bank, said, after a crisis that has put an end to 20 years of moderation it is now difficult to make forecasts. How will the currency wars end? How will financial

markets react when central banks tighten monetary policy, as eventually they must? What will follow the cessation of EU purchases of southern European government bonds? Will the looming pension funding problem be solved, and how? Will growing government debt eventually be reduced by resorting to higher inflation? These are just some of the unknowns around us. And so Rybi ski declined to make growth forecasts when as guest speaker he addressed ACCA’s CFO European Summit in Warsaw in October. In what, borrowing a phrase from former US Federal Reserve chairman Alan Greenspan, the Polish banker termed ‘the age of turbulence’, any forecasts based on models using data from the last 20 years will give utterly wrong predictions. CFOs now have to think less about hard forecasts and more about scenario analysis, and making sure that their companies are equipped to react to any eventuality. The crisis has refocused CFOs’ work on their core responsibilities and, as Lukasz Topolnicki FCCA, finance director at retailer Castorama Polska, noted, many of the less interesting things in finance – internal controls, audit committees and the like – are returning to prominence. There is also much greater

After the stormThe global financial crisis may be receding, but it has ushered in an age of turbulence for businesses and is posing unaccustomed challenges for CFOs

The shocks of the past few years have delivered salutary lessons to over-ambitious CEOs and given CFOs a more prominent role in decision-making

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS CFO STRATEGY

PG16 EDITION 03

emphasis than there used to be on the importance of trust and integrity. Ethical behaviour is an essential part of the ACCA Qualification, and the need for trust and integrity (and their close relatives – reliability and transparency) was frequently mentioned in Warsaw. These qualities are not technical

skills that can be taught, but have to develop from the culture of the organisation. And that, as Karen Burgess, until recently CFO of TVN, Central Europe’s largest media group, emphasised, depends very much on senior management’s approach, and on the long-term experience of working together. These values are important because the CFO can’t

always be checking what finance people are doing and must be able to rely on them and what they report. Transparency is needed both inside and outside the company. Crucial business information needs to be disseminated widely in a comprehensible form so as to build trust within the company. Delivering clear and reliable information to decision-makers depends on having reliable sources and so HR becomes of importance for the CFO too: people management and team building is a crucial part of the CFO’s role. Outside the company, the education of stakeholders, and particularly of shareholders, is important for retaining their support in turbulent times. Informing shareholders in detail of business plans and expectations should help protect the company even if the market deteriorates, suggested Ewa Bozek, CFO at Canon subsidiary Octopol Technology. Short-termism remains a vexing problem for CFOs, particularly for those of listed companies, with hedge funds and others trading in and out of their shares. In a volatile economic environment, the pursuit of short-term targets is bound to be particularly disruptive. The balance needed is one between medium-term and long-term objectives. And with targets today less nakedly profit-related than they were, a balance also needs to be struck between profit and risk. Risk management is more important than before and stakeholders increasingly want to see businesses set targets that are appropriate to the risk assumed.The pain inflicted by the volatility of commodity, foreign exchange and other markets in the past few years has refocused CFOs’ attention on the financials. The destruction of the assumption that credit will always be available at a price to companies – and to their customers – is also forcing CFOs to give more consideration not just to prospective returns, but also to the risks associated with them. Those risks can be mitigated and managed, but they can’t be eliminated. It is therefore important to think though the possible eventualities so as to be ready to react to them. It is also important to convey to stakeholders in a transparent, effective and trustworthy manner how risks are managed, stressed Pawel Cygan ACCA, VP of Polish power distributor Enion.While the changing business environment has been pressuring companies to return to fundamentals and pay more attention to risks as well as potential rewards, thus changing the objectives that CFOs find themselves bound to pursue, there have also been changes in the roles played by CFOs within organisations.

Krzysztof Rybi ski: any forecasts based on models using data from the last 20 years will be utterly wrong.

PG17 EDITION 03

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS CFO STRATEGY

Traditionally, the finance function has been seen by many as being primarily one of keeping the assets safe and the books in order, but the shocks of the past few years have delivered salutary lessons to over-ambitious CEOs and given CFOs a more prominent role to play in corporate decision-making. Their being able

to do so has been facilitated by the progress of IT, which is giving CFOs greater freedom to think strategically and innovatively.Management of information, so that it is accurate and delivered at the right time, is crucial if companies are to make the best decisions, and IT’s development is making it technically easier for CFOs to provide CEOs with the information needed. There is no simple technical fix, though. Developing financial management capacity also means increasing understanding of the organisation and the processes that take place within it, what information they can provide and how that can be translated usefully into numbers and narratives and delivered to decision-makers, said Waldemar Wojtkowiak FCCA, CFO at credit insurer Euler Hermes’ Polish unit. If they are to raise the finance function’s credibility across the organisation, CFOs need to develop their soft skills. They can turn finance staff into an effective team by recruiting to achieve diversity, delegating responsibilities, teaching by analysing errors that have been made, and using rewards. Meanwhile, there is a need to engage in continuous dialogue with other managers, and finance for non-finance staff programmes can spread financial literacy through the company, enabling more effective communication with other departments. CFOs’ enhanced corporate role looks set to continue, for the lessons of the financial crisis will not be forgotten swiftly and the uncertain conditions that companies face in coming years are going to keep demand high for their special skills. But with resources limited, taking advantage of the opportunity to contribute more to strategic thinking is going to depend on using technology to build systems that can ensure the efficient performance of CFOs’ more mundane tasks.

John Presland, journalist

CHRISTOS KASSAPANTONIOU FCCA, CFO, HOUSE MARKET (IKEA), GREECE, CYPRUS, BULGARIA

‘The finance function has to contribute by adding value, by being a business navigator, directing resources to achieve the company’s financial and business objectives.‘It’s important to get out from behind the desk and away from your Excel spreadsheets, and to work on getting the trust of others in the firm. At Ikea, controllers have to spend time working in the sales and logistics areas; if they understand what drives stocks, staff costs and gross margins, they can contribute more to adding value. There are lots of KPIs, but we need to be able to communicate with business partners, with truck drivers or stock controllers, for example, in their own language so that they understand how they drive value. ‘Resources are limited and we must now do more with less. We have to build competence by developing systems and procedures, and delegating authority to finance people who understand the need for accuracy and checkable numbers. When both systems and reporting work reliably, then we can go to the sexier role of being the navigator and playing a more value-adding role.’

The pain inflicted by the volatility of commodity, foreign exchange and other markets in the past few years has refocused CFOs’ attention on the financials

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS CFO STRATEGY

PG18 EDITION 03

RAFAL WICINSKI FCCA, CFO, COCA-COLA HBC POLSKA

‘CFOs need new skills. The world is increasingly complex and turbulent and we need to spend more time trying to understand what’s happening, to understand our business and our market. Equally crucial are people and people management. In finance we have a tendency to concentrate on numbers, but people play a more important part in business than is often assumed. ‘We need to build the capability of the finance function and that needs leadership and vision. We need to know how to stand up in front of a finance team and make sure everyone follows what we say. That’s not easy, but it’s an increasingly important skill in these uneasy times. Once you’ve set up a vision, you can define roles and the direction you’re going in.‘We must look at simpler ways of doing things. Many things are now done very differently from even 10 years ago. I have a vision of e-finance, of doing everything without signing pieces of paper. That will help us eliminate time-consuming back-office work and put more time into strategic thinking, which we all love but for which we’ve too little time.’

PETER WHISKERD-W GORZEWSKI, FD, CENTRAL AND EASTERN EUROPE, PROLOGIS

‘My first job as CFO was with Mars in 1990. I was immediately told that the role was to be a custodian, which is obviously the essence of the job. There were also three other Cs – all of them behavioural – to be a catalyst, to be constructive and to be challenging. ‘Googling the role of the CFO today yields a model that’s very similar to what Mars said 20 years ago. Deloitte says the CFO has “four faces”: steward – protecting and preserving the assets of the organisation; operator – balancing capabilities, costs and service levels; catalyst – stimulating behaviours to achieve strategic and financial objectives; and strategist – providing financial leadership in determining strategic direction and aligning financial strategies. Catalyst and strategist are what we’re really about when we’re trying to make a value-added contribution.‘I’m trying to implement this model throughout my organisation, because even an accounts payable clerk can proactively go out and influence people to process invoices faster, pay better and develop better relationships with our strategic suppliers.’

PG19 EDITION 03

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS CFO STRATEGY

Although the past few years have been turbulent, many organisations see promising signs on the horizon. But one area that remains as elusive as

ever is the competition for star talent, which will only intensify and test even the most proactive talent management programmes. Companies are aware that they need to attract, retain and manage key accounting talent. Accountants underpin oversight and supervision in an increasingly global regulatory environment, and help organisations manage risk effectively. However, talent shortages in the profession are already apparent, the result of shrinking numbers of new entrants, the failure of educational systems, and universal competition for the star performers. Young professionals are a vital source of talent. Currently, the people coming through are those born between 1980 and 1993, who have been dubbed ‘Generation Y’. Research by ACCA and consulting, outsourcing and investment services provider Mercer has uncovered the fascinating traits and motivations of

this group of tomorrow’s financial leaders, and the dramatic implications for business. Employers who fail to understand what drives Generation Y professionals will also fail to recruit and retain them.Most Generation Y professionals have grown up with the internet, mobile phones, laptops and social media. They are an extremely confident generation; they value security but will walk away if their employer can’t or won’t deliver their career path. The research, Generation Y: Realising the Potential, surveyed 3,200 individuals across 122 countries. It reveals a generation seeking dynamic career paths, both inside and outside traditional mainstream finance careers.

MONEY AND MOREMake no mistake: money matters to this age group. But while they seek out competitive packages they also want a total package. As well as money, they are looking for work-life balance and a career at an attractive brand that reflects their own values.

Generation Y professionals are different, and unless you meet their aspirations they will be taking their skills to your rivals, warns Mercer’s Jason Jeffay

The great talent show

Ace face place: Facebook, created by Mark Zuckerberg, is one of the most popular social networking sites with Generation Y.

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS GENERATION Y

PG20 EDITION 03

Recruiting and retaining Gen Y professionals

TOP FIVE ATTRACTION FACTORS95% Career development and learning opportunities 87% Remuneration package (base salary) 83% Nature of role81% Job security81% Work-life balance

TOP FIVE RETENTION FACTORS64% Career development and learning opportunities56% Challenging work48% Remuneration package (base salary)47% Relationship with line manager45% Team morale

Organisations have a range of tools to help here. They can showcase the career paths available. Career maps, which offer employees knowledge and control over their own career paths, are also worth considering. A career map shows how the organisation wants people to progress, and is designed by working backward from a destination job to identify the feeder jobs that will let staff get there. Another type of career map is built on data about how and how quickly people move through roles to reveal the pathways that employees actually take to that destination job. This type of career mapping often reveals pathways the organisation wasn’t aware of and provides information about how long it takes to follow a particular career path. Employers can create career opportunities by restructuring work and moving people out if they reach a plateau or are underperforming, or through proactive churn. It’s also worth considering expanding secondment programmes and stepping up rotational activities to provide face-to-face courses and experiential learning.

THE HEADLINESThe lessons employers must learn from the research are clear. Lifestyle factors are more important than contractual elements in attracting Generation Y through the front door. The organisation’s brand, and the values it represents, are equally important. Remuneration must be pitched competitively as part of a wider attraction proposition. Career development is key to attracting, developing and retaining this generation of finance professionals. Employers must ensure they understand what career paths are available in the organisation and communicate these clearly to prospective employees. They also need to deliver a range of learning interventions to leverage the skills of Generation Y. Successful retention translates into a better return on training investment and lower recruitment costs.The biggest challenge facing organisations over the next few years will be the creation of value. Today we live in a knowledge economy, where information is key to value creation. Value will be created by people, ideas and the brand, and Generation Y finance professionals will be leading the way.

Generation Y: Realising the Potential is available at www.accaglobal.com/gen_yMercer is a leading global provider of consulting, outsourcing and investment services, with more than 25,000 clients. www.mercer.com

Experiential learning is crucial. Employers and Generation Y professionals themselves both see it as key to developing the essential financial skills. It’s a tech-savvy generation, but face-to-face learning still resonates. Career development is front and centre for Generation Y, and employers need to put development at the heart of their career proposition. This is a generation that values job security but will leave the company if career promises are not fulfilled. Exciting careers are in heavy demand. Generation Y professionals want interesting and exciting careers, either inside finance or, increasingly, outside, using their valuable finance skills in a different capacity in the wider business environment. In the wake of the global economic crisis, organisations of all sizes and in all sectors have turned to their finance departments to help chart a pathway to recovery and to influence and shape business strategy. They accordingly face an uphill battle in attracting and retaining these valuable workers. According to the study, most Generation Y finance professionals are satisfied with their current role but are concerned about the future. Half believe their organisation is not able to offer them sufficient career development opportunities, and one in three wants to change employer – now. Unless employers effectively manage career expectations and development, they face a significant retention risk, particularly when global economic conditions improve.An effective career management process will combine three factors: transparency, control and velocity. Generation Y professionals want the transparency of knowing their options and alternatives inside and outside finance. They want the ability to exercise some control over their roles and experiences. And they want velocity to move quickly through those roles and experiences to gain a sense of progression and self-defined success.

Jason Jeffay manages Mercer’s consulting strategies in talent alignment and strategy, workforce architecture, leadership development and succession planning, performance management and employee value proposition and culture. He has more than 20 years of consulting experience, and is an author and speaker. He has sponsored and participated in leading-edge HR research, and has an MBA from the University of Chicago.

PG21 EDITION 03

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS GENERATION Y

To evolve with the changing nature of owner-managed businesses and the regulatory environment, accountants will have to market their services more

effectively to prospective clients instead of passively relying on referrals, new research from ACCA has found. The research also underlines how for some accountants the idea of becoming a salesperson is anathema, with some arguing that a greater marketing effort would erode their

credibility, integrity and ethics. One accountant interviewed during the course of the research said: ‘I’m not a particularly gregarious character who goes out and woos my clients with charisma. More work comes my way due to my work ethic.’ Another said: ‘I don’t knock on doors! It does not have the same credibility as a referral. It’s not a hard sell of the services, but a hard sell of you as someone with ability, credibility, integrity and ethics.’

I don’t knock on doors!It might be anathema to some, but small practices need to step up their marketing efforts to retain their strong position in the SME market

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS SMALL PRACTICE

PG22 EDITION 03

The clear reluctance of accountants in small practices to become more proactive in marketing their services raises the question of whether or not the accountancy profession should, and could, increase its level of service marketing, the research found. More marketing may be counter-productive, requiring the accountant to play a role ‘out of type’ – a change of character that may breach the very foundations of trust and empathy that small businesses require from their accountant as a trusted adviser. The report, Business Advice to SMEs: Professional Competence, Trust and Ethics, by Kingston University’s Robert Blackburn and Monash University’s Peter Carey and George Tanewski, presents the results of ACCA’s study of small and medium-sized enterprises (SMEs) and their behaviours in seeking business advice.

MEASURING MOTIVATIONAlthough accountants are traditionally viewed as trusted business advisers by small business owners, the main reasons why SMEs seek advice from accountants are for compliance and tax reporting purposes. Based on this assumption, the ACCA research wanted to present a detailed understanding of the nature of the services that accountants provide their SME clients in Australia and the UK. Specifically, this sought to examine the role of professional competence, trust and ethics, to uncover the factors influencing SMEs’ purchase of business advice and to look at the implications of the results for the accountancy profession.

FIRM EVOLUTIONBusiness practices don’t stand still. Over the past few decades, accountants have developed their firms into multidisciplinary practices offering a more diverse range of skills and services to reflect the modern needs of their clients. These go beyond the traditional compliance and tax work typically associated with accountants.Also, regulation has changed. The requirement for a statutory audit has declined as exemptions have risen, for example. Whereas the ability of large accountancy firms to provide non-audit services to audit clients has been restricted, no legislative restriction has been placed on accountants providing statutory and non-statutory advice to their SME clients. Despite these developments, SMEs do not always seek helpful external business advisers, even though there is clear potential for accountants to expand the management accounting services they provide to smaller companies.Moreover, the kind of work accountants provide to their SME clients – typically compliance and tax – is seen by owner-managers as adding no value to their business. It is simply something that SMEs have to do in order to comply with regulations. Indeed, accountants themselves consider this a burden of sorts to their clients.To be able to offer value added services, such as advice on succession planning or international trade, could help change the view that SME owners have of their accountants.One possibility is for accountancy firms dealing in the SME market to restructure and align their services more closely with the needs of their clients. However, respondents pointed to the fact that most small accountancy practices have a diverse range of clients operating in very different industry sectors, making it difficult for accountants to be specialists in all those different sectors.

FACTORS INFLUENCING THE PURCHASE OF BUSINESS ADVICE

Size: The larger the business, the more likely it is to take advice from its external accountant. This finding counters the assumption that SMEs have a greater need for advice because they may lack such important skills as knowledge of financial controls.

Age: The age of an owner-managed business influences its demand for advice. Previous research shows the relationship with external advisers is more important during the earlier stages of the business, as the owner navigates unfamiliar regulatory and operational challenges.

Finances: SMEs facing heightened risk are more likely to seek external advice to help minimise the risk, particularly when a ‘crisis point’ is reached. Lenders may exert pressure on SMEs to seek advice from their accountants before providing additional funding.

PG23 EDITION 03

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS SMALL PRACTICE

‘To understand [a client’s] industry is really hard when you have 40 to 50 clients, basically across every industry, and it’s hard to be an expert in them all; probably of all the things clients say they want it’s the hardest [demand to meet],’ responded one accountant.Other options recommended that could accommodate the evolving needs of SMEs would be for accountants to employ a business development manager or develop strategic alliances with other professional services firms with specialist expertise. What was clear from the responses and analysis is that further research is needed on these complex issues of marketing to SMEs.Yet there remains a solid platform on which to develop the relationship between accountants and owner-managed businesses. The notion of trust provides a firm basis that accountants can build upon.

RELATIONSHIP MATTERSThe study found that trust was crucial to the relationship between the two parties. But, perhaps contrary to belief, the research found no link between the length of an SME’s relationship with its accountant and the level of trust, which suggests that such factors as service quality and delivery are more important than longevity for the establishment of trust.One reason why accountants are not seen as a normal source of management advice to small businesses was that they lack the requisite knowledge and business expertise. This finding again feeds into the issue of the unwillingness of many accountants to market themselves and their services effectively.The research findings show that SMEs seek business advice from a variety of sources. Instead of extending their relationship with their accountant, owner-managers prefer to use other sources. For example, one SME respondent used an external accountant for compliance advice, a financial planner for wealth management advice, and an independent business adviser for business advisory services. This analysis highlights an ‘expectation gap’ between what the SME owner believes accountants can offer and the services today’s accountants actually provide.

‘The market for business advice is highly competitive and while external accountants are well placed to gain this work, they need to convince clients that they have the necessary business expertise to deal competently with the owner-manager’s issues,’ the report states.Importantly, the study discovered that during so-called crisis points, SMEs did tend to seek external business help. If ever there was a time when SMEs were facing turbulence on many levels it is now. The economic upheaval shows no signs of abating in the immediate future, while regulators and legislators around the world are hard at work scrutinising financial frameworks to uncover the failings that led to the global financial crisis. This has led to a variety of regulatory and legislative changes – with more to come. Research has shown that such an environment gives rise to a demand for business services, particularly for businesses starting up.One accountant who was interviewed for the study said: ‘Problematic economic times can drive demand, or one-off events such as divorce, a more competitive industry or a highly geared business.’The report comments: ‘Such events could be termed “milestone” events and may prompt the SME owner to seek out the services of the external accountant, having already built a continuing relationship of trust. Most small firms do not have sufficient in-house resources, certainly to deal with “one-off” events such as a rapid growth spurt or, on the other hand, business exit, and this means that they tend to look to their external accountant to fill the gap in their experience and knowledge base. In such situations, accountants could be regarded as an external resource.’Currently, opportunities for accountancy firms to expand their services are ripe. Whether practices can take advantage of that moment, in helping their clients grow, exit their businesses or simply survive these tough economic times depend on their willingness to adapt. And that is something that lies in their hands.

Michelle Perry, journalist

Business Advice to SMEs: Professional Competence, Trust and Ethics can be found at www.accaglobal.com/SME_advice

‘The market for business advice is highly competitive and while external accountants are well placed to gain this work, they need to convince clients that they have the necessary business expertise to deal competently with the owner-manager’s issues’

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS SMALL PRACTICE

PG24 EDITION 03

People power for SMPsIs there more scope for smaller practices to provide SMEs with advice on HR and employment law issues? Yes, say Mike Rigby and Professor Robin Jarvis

PG25 EDITION 03

ACCOUNTANCY FUTURES: ACCOUNTANTS FOR BUSINESS SMALL PRACTICE

In the last issue of Accountancy Futures IFAC past president Bob Bunting highlighted the important changes in the role of small and medium-sized

practices (SMPs) providing support to small and medium-sized enterprises (SMEs), citing evidence from a recent IFAC research paper.The evidence from the paper, entitled The Role of Small and Medium Practices in Providing Business Support to Small and Medium-sized Enterprises, indicates that globally SMPs are the preferred provider of business support to SMEs, providing an array of services including advice on HR and employment law issues. Indeed, from a UK perspective, research has found that SMPs are the main providers of advice on HR and employment law to SMEs.However, little is known about the nature of the involvement of SMPs in this relationship, and ACCA has commissioned research to find out. This article summarises the research and highlights some of the issues.To obtain a meaningful insight into the relationship between accounting practices and SMEs, the study carried out 20 in-depth interviews with accounting practices. The practices were mainly chosen at random although the study took account of the varying sizes of practices.The type of advice varied and was dependent to some extent on the size of the practice,

reflecting its knowledge and experience of dealing with HR and employment law issues. Typically, the services provided by the practices in the study were employment-related. They included contracts, dismissals, redundancy, benefits and leave, resourcing (searching and interviewing), remuneration (setting up bonus schemes and grading structures) and succession planning. There were several reasons why SMEs chose accountants to give this advice. Trust was a significant one and was derived from the close relationship SMEs developed with their accountants while receiving traditional accounting compliance services, such as tax returns and auditing financial reports. Additionally, the trust relationship benefited from the institutionalised trust generated by the accountant being a member of a professional organisation underpinned by an ethical code.

Another reason given for the choice of an accountant for advice was that SMEs recognised that SMPs’ needs and experiences are similar to their own and that they talk the same language.Practices fell into three categories in their approach to providing HR and employment law advice: the qualified HR model, the payroll model and the minimalist model.

QUALIFIED HR MODEL In the case of the qualified HR model, qualified HR personnel were employed in the practice. These practices saw their involvement in HR and employment law more strategically than those in the other two categories and positioned themselves as part of a one-stop-shop approach to their clients’ needs. The development of HR/employment law services was part of a decision to seek to provide a full range of support services to SMPs. As one of the respondents mentioned: ‘We want to become a broader-based advisory practice.’These qualified HR practices initially moved in this direction because their clients were seeking HR/employment law support. The respondents pointed out that they were aware of their competitive advantage over HR consultancies that were not accounting practices: ‘Our clients can shop around for any HR package… but we are in a unique position.

They are already in-house, they already like our service, we know their business.’ Respondents recognised that by expanding the services they were offering it was possible to attract new clients.While these practices saw the development of HR/employment law support as strategically significant, their mode of entry into it was sometimes opportunistic. For example, one practice had appointed an HR specialist to deal with the practice’s own HR and employment law issues and only subsequently realised it represented an opportunity to develop an HR service for clients. Another practice had a long-standing referral relationship with an HR consultant. Recognising the growing demand for this type of service, it established a joint venture with the HR consultant.The level of business activity generated owed a great deal to a practice’s active promotion

Professor Robin Jarvis is ACCA’s head of small business and professor of Accounting at Brunel University. He is a member of the European Commission’s Expert Group –Financial Services Users Group and is a member of the International Accounting Standards Board’s (IASB) SME Implementation Group.