accounting and excel notes for small business owners by enactus lse

TRANSCRIPT

3 . I N T R O D U C T I O N T O A C C O U N T I N G A N D E X C E L

C R E A T I V E C Y C L E O N L I N E E N T R E P R E N E U R S H I P P R O J E C T

“I didn’t get there by wishing for it, or hoping for it,

but by working for it.” !

- Estee Lauder, of Estee Lauder Companies.

R E T R I E V E D F R O M New York World-Telegram and the Sun staff photographer: Sauro, Bill, photographer. - Library of Congress Prints and Photographs Division. New York World-Telegram and the Sun Newspaper Photograph Collection

A. LEARN BASIC EXCEL SKILLS

B. UNDERSTAND HOW ACCOUNTING WORKS

C. LEARN KEYWORDS USED IN EXCEL SPREADSHEETS

D. MAKE MORE INFORMED BUSINESS DECISIONS USING WHAT IS TAUGHT

T O D A Y ’ S A G E N D A

"Apple, the Apple logo and iPhone are trademarks of Apple Inc., registered in the U.S. and other countries."

4

• A computer program used to organise and manipulate data.

!• We will learn to use it for accounting purposes! !

W H A T I S E X C E L ?

W H A T I S E X C E L ?

5

• You can enter data in (such as revenue from necklace sales, PayPal fees), or enter in mathematical formulas.

• It is very useful to check what happens when there are changes in the data.

H O W D O I U S E E X C E L ?

6

• Entering data:

• For example, if you want to change PayPal fees, click on the corresponding cell (E25 in this case), and enter the new number.

H O W D O I U S E E X C E L ?

7

• Entering a formula:

The cell G27, corresponding to total expenses. It has the formula: =E22+E23+E24+E25+E26+E27 (don’t forget the equal sign at the start!) That way if any of the expenses changes, total expenses changes automatically.

W H A T I S A C C O U N T I N G ?

8

• Accounting is the process of keeping financial accounts.

"Apple, the Apple logo and iPhone are trademarks of Apple Inc., registered in the U.S. and other countries."

A C C O U N T I N G I S A L S O V A L U A B L E T O …

9

Keep financial records, analyse them and then make business decisions.

Build a good financial reputation. Important if you want to obtain funds and loans!

Prevent and discover fraud.

A P A R T F O R B E I N G U S E D T O C A L C U L A T E Y O U R T A X E S …

A C C O U N T I N G A N D T A X E S

10

• Refer to HMRC’s website: http://www.hmrc.gov.uk/guidance/selling/income.htm

!

• If you are trading, you may have to pay Income Tax, National Insurance Contributions and VAT. HM Revenue and Customers (HMRC) will treat you as self-employed in that trade.

A M I T R A D I N G ?

11

As an entrepreneur, you probably are! !

!Generally, you are considered to be trading if you are: • Selling goods you bought for resale • Making goods and selling them with the intention of gaining profit • Selling or buying goods on behalf of others for financial gain (e.g.

commission) • Providing a service and receiving payments for it.

B E F O R E Y O U R A C C O U N T I N G …

12

• In addition to using Excel, you also have to keep track of your purchases, expenses and sales!

• This is known as Book-Keeping.

"Apple, the Apple logo and iPhone are trademarks of Apple Inc., registered in the U.S. and other countries."

B O O K - K E E P I N G

13

• Book-keeping is simply keeping track of your expenses and revenues.

!

• Keep them tidily in a folder so you can track your flow of money.

B O O K - K E E P I N G

14

Expenses Revenue from online shop

Purchases

B O O K - K E E P I N G - K E E P I N G A J O U R N A L

15

• The journal, also known as the ledger, is where you list all relevant transactions for your business: Sales, Purchases and Expenses.

!

• You can keep the journal entries recorded in the spreadsheet we have provided for you.

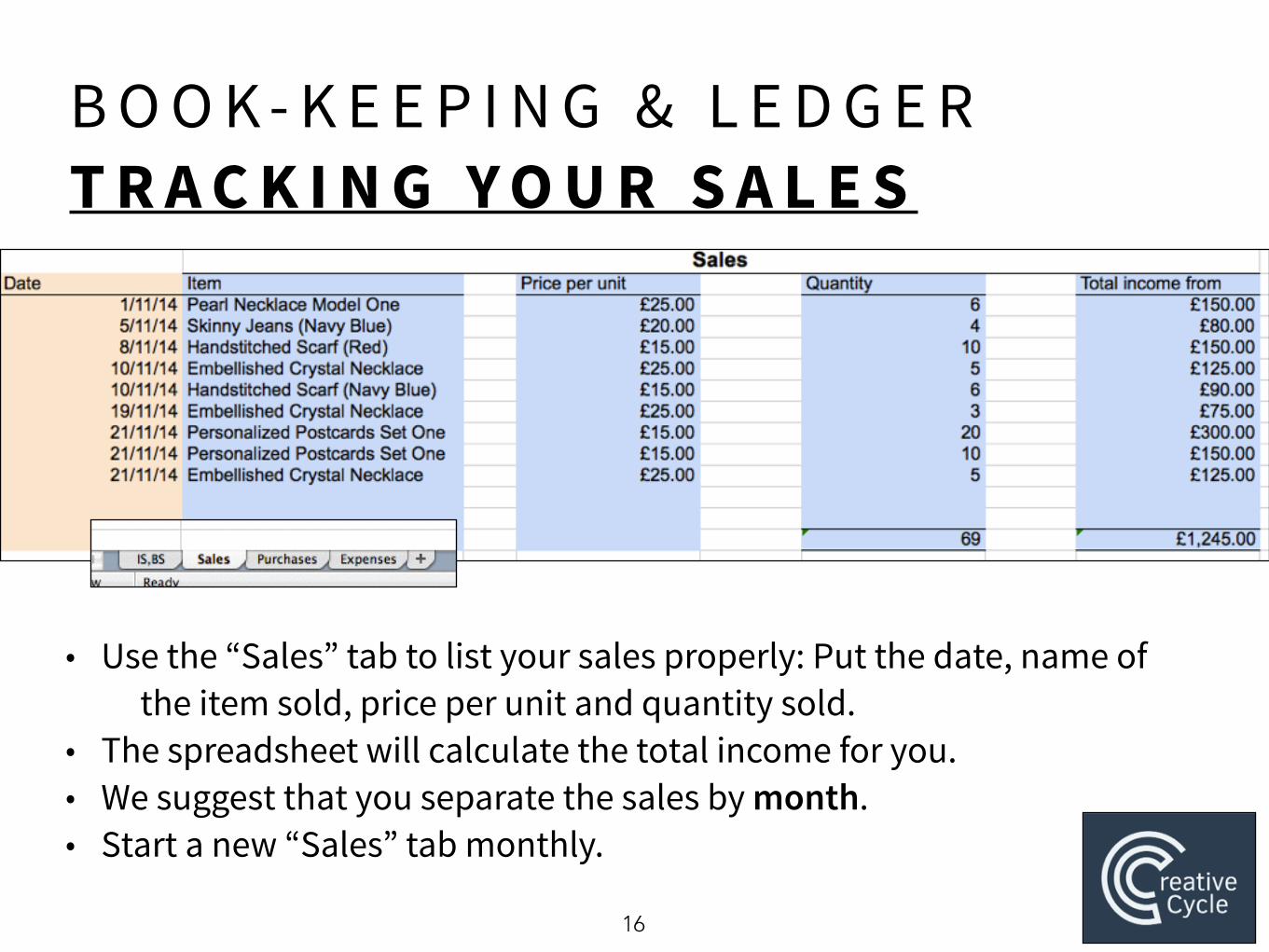

B O O K - K E E P I N G & L E D G E R T R A C K I N G Y O U R S A L E S

16

• Use the “Sales” tab to list your sales properly: Put the date, name of the item sold, price per unit and quantity sold.

• The spreadsheet will calculate the total income for you. • We suggest that you separate the sales by month. • Start a new “Sales” tab monthly.

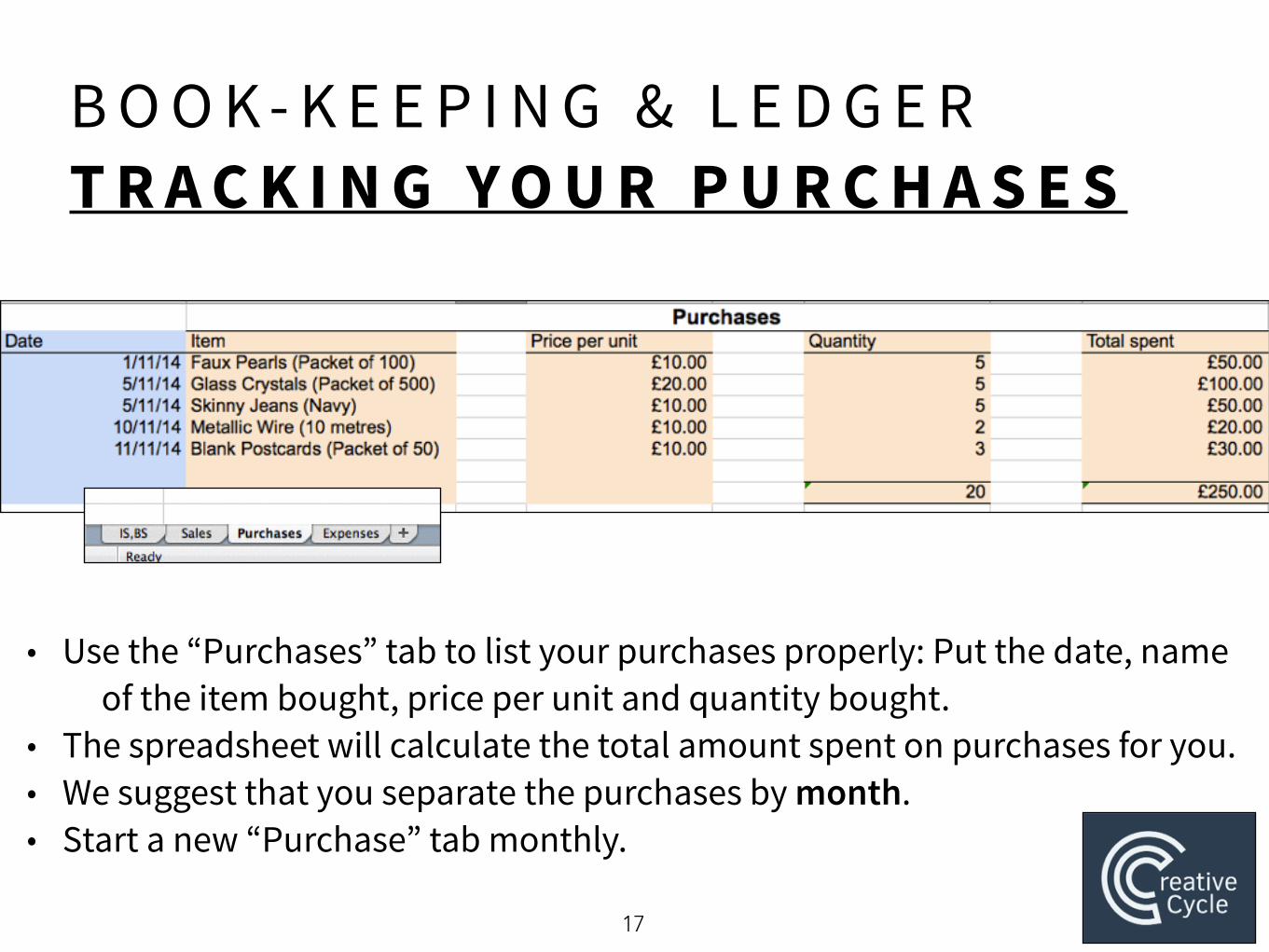

B O O K - K E E P I N G & L E D G E R T R A C K I N G Y O U R P U R C H A S E S

17

• Use the “Purchases” tab to list your purchases properly: Put the date, name of the item bought, price per unit and quantity bought.

• The spreadsheet will calculate the total amount spent on purchases for you. • We suggest that you separate the purchases by month. • Start a new “Purchase” tab monthly.

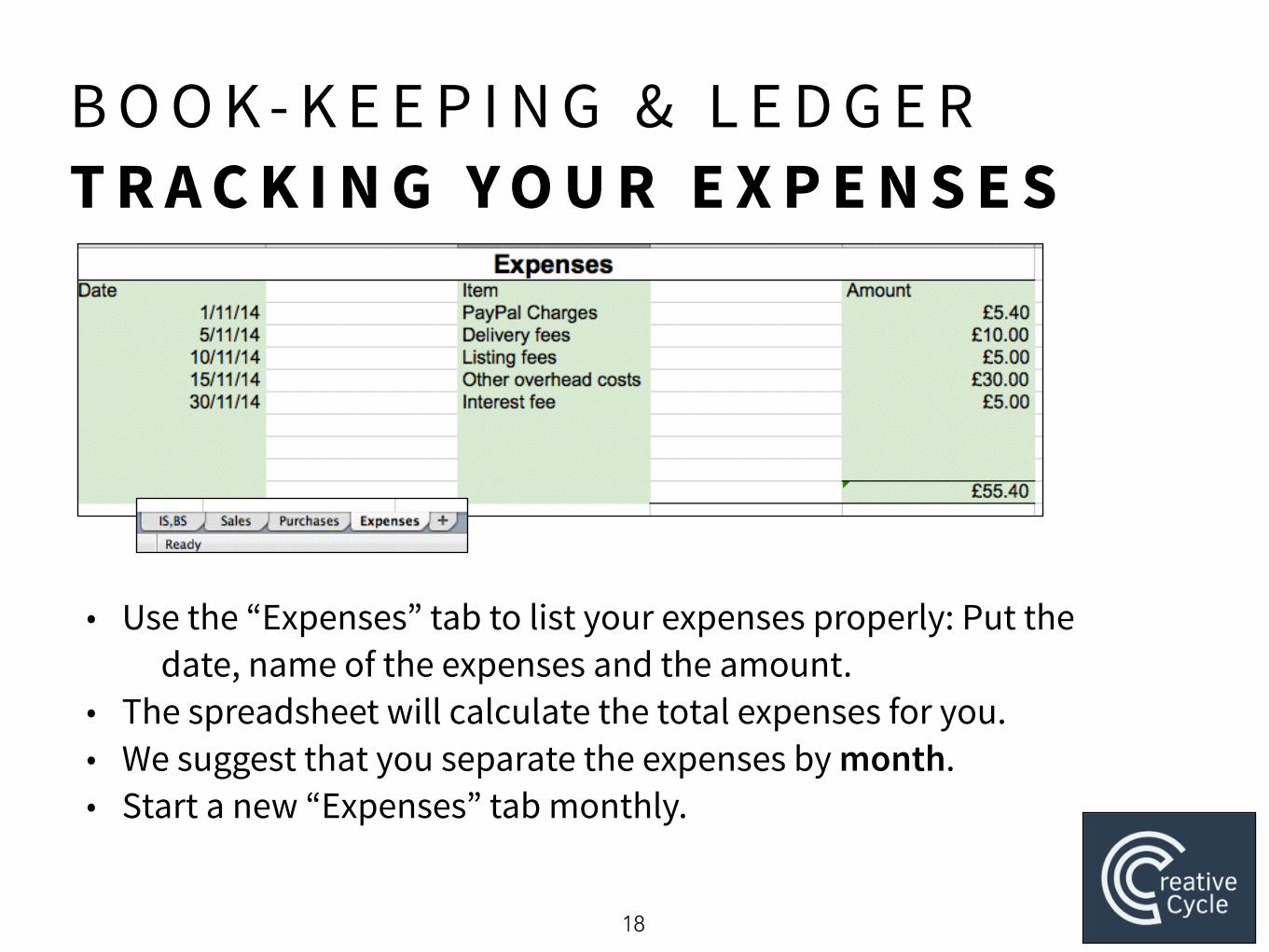

B O O K - K E E P I N G & L E D G E R T R A C K I N G Y O U R E X P E N S E S

18

• Use the “Expenses” tab to list your expenses properly: Put the date, name of the expenses and the amount.

• The spreadsheet will calculate the total expenses for you. • We suggest that you separate the expenses by month. • Start a new “Expenses” tab monthly.

19

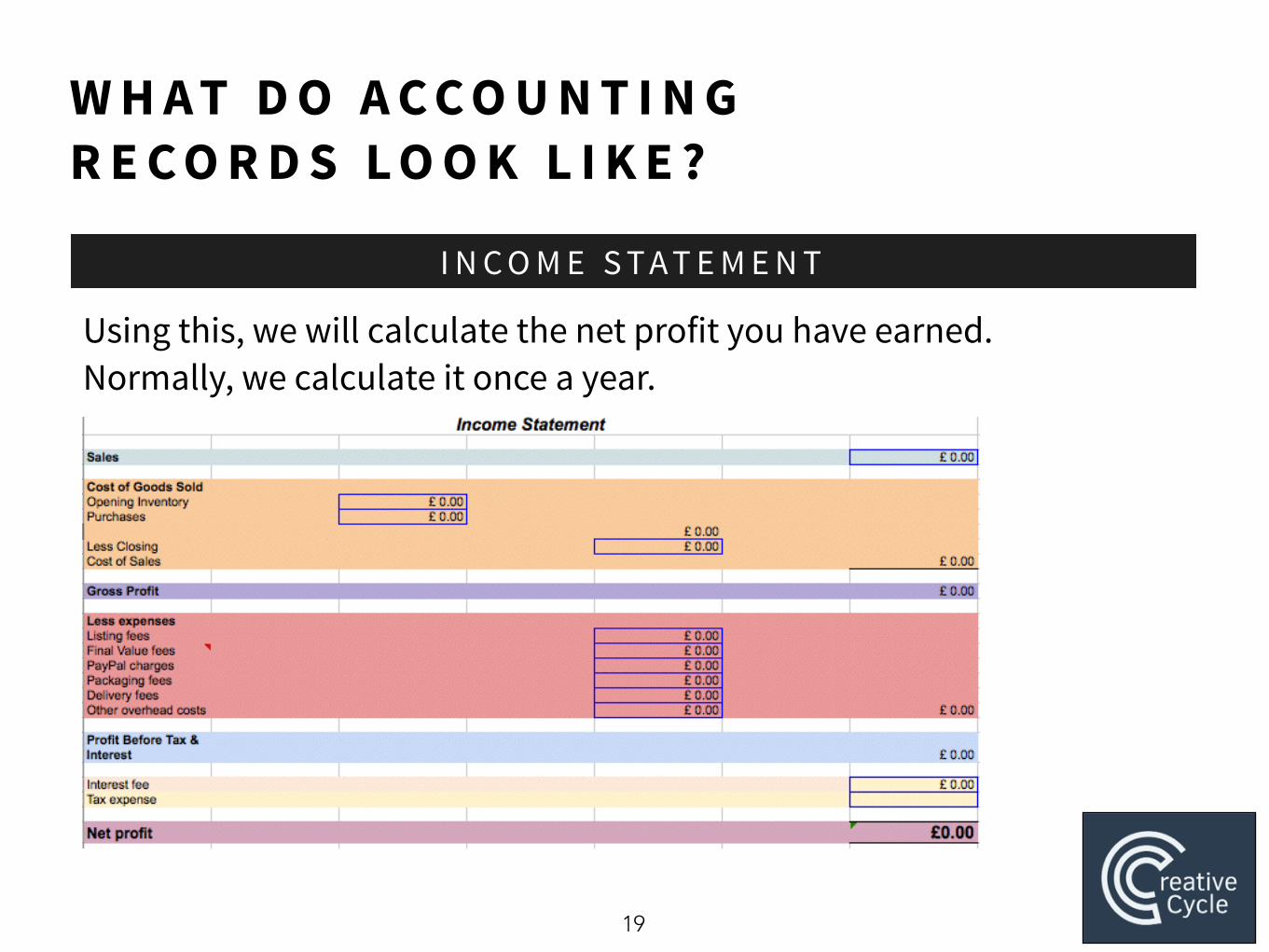

I N C O M E S T A T E M E N T

Using this, we will calculate the net profit you have earned. Normally, we calculate it once a year.

W H A T D O A C C O U N T I N G R E C O R D S L O O K L I K E ?

W H A T D O A C C O U N T I N G R E C O R D S L O O K L I K E ?

20

C O M P O N E N T S O F T H E I N C O M E S T A T E M E N T

SALES. This is where you record the revenue you earned from sales

of your goods.

This is where we enter expenses incurred in purchasing materials or making our goods.

COST OF GOODS SOLD.

Other expenses incurred in selling your product. This includes fees paid to PayPal, mailing fees,

packaging and even rent, electricity and wages!

EXPENSES.

W H A T D O A C C O U N T I N G R E C O R D S L O O K L I K E ?

21

S T A T E M E N T O F F I N A N C I A L P O S I T I O N

Provides you with a snapshot of the state of your business - what assets you have, how much do you owe people and where your revenues are at.

W H A T D O A C C O U N T I N G R E C O R D S L O O K L I K E ?

22

C O M P O N E N T S O F S T A T E M E N T O F F I N A N C I A L P O S I T I O N

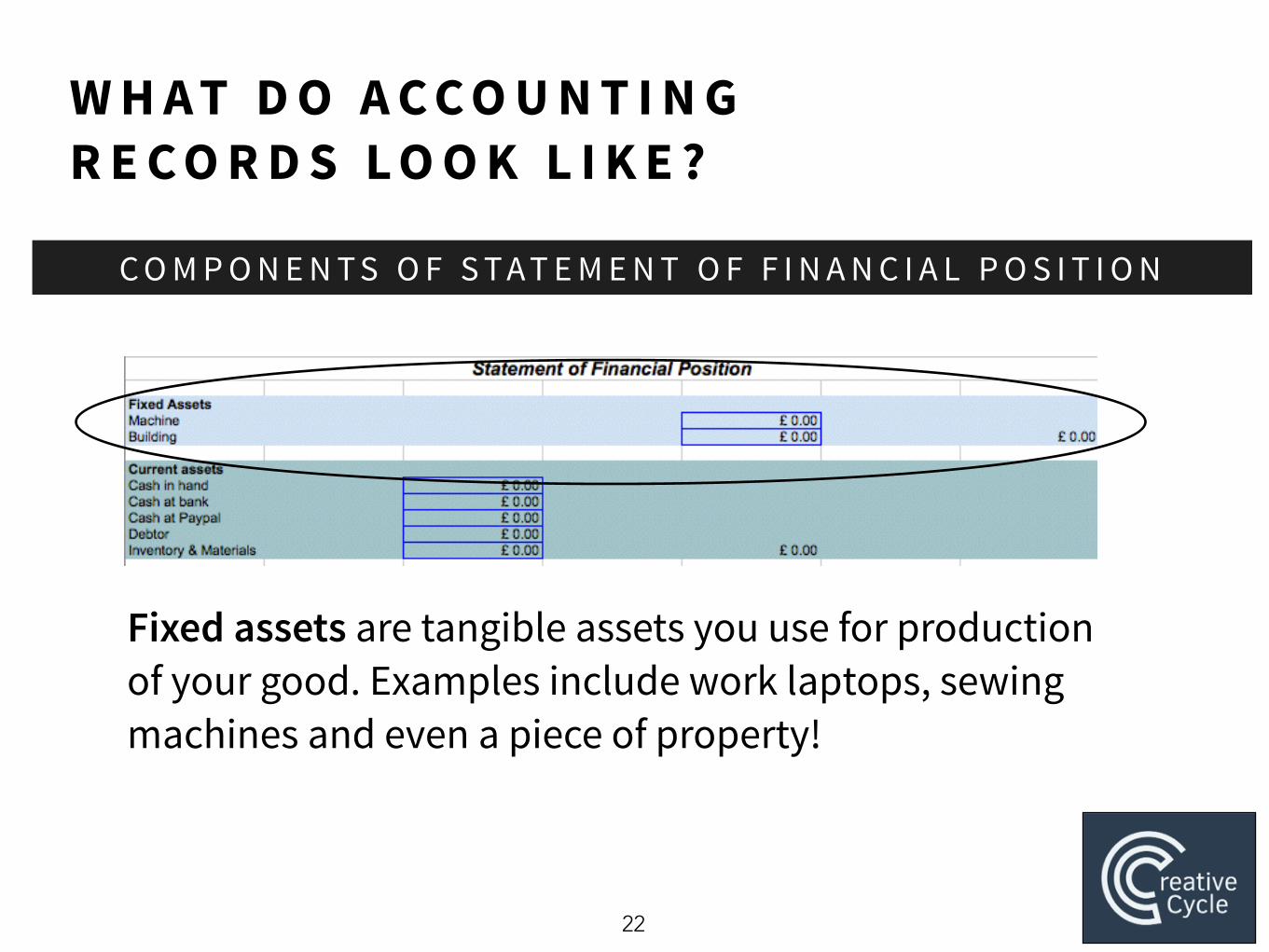

Fixed assets are tangible assets you use for production of your good. Examples include work laptops, sewing machines and even a piece of property!

W H A T D O A C C O U N T I N G R E C O R D S L O O K L I K E ?

23

C O M P O N E N T S O F S T A T E M E N T O F F I N A N C I A L P O S I T I O N

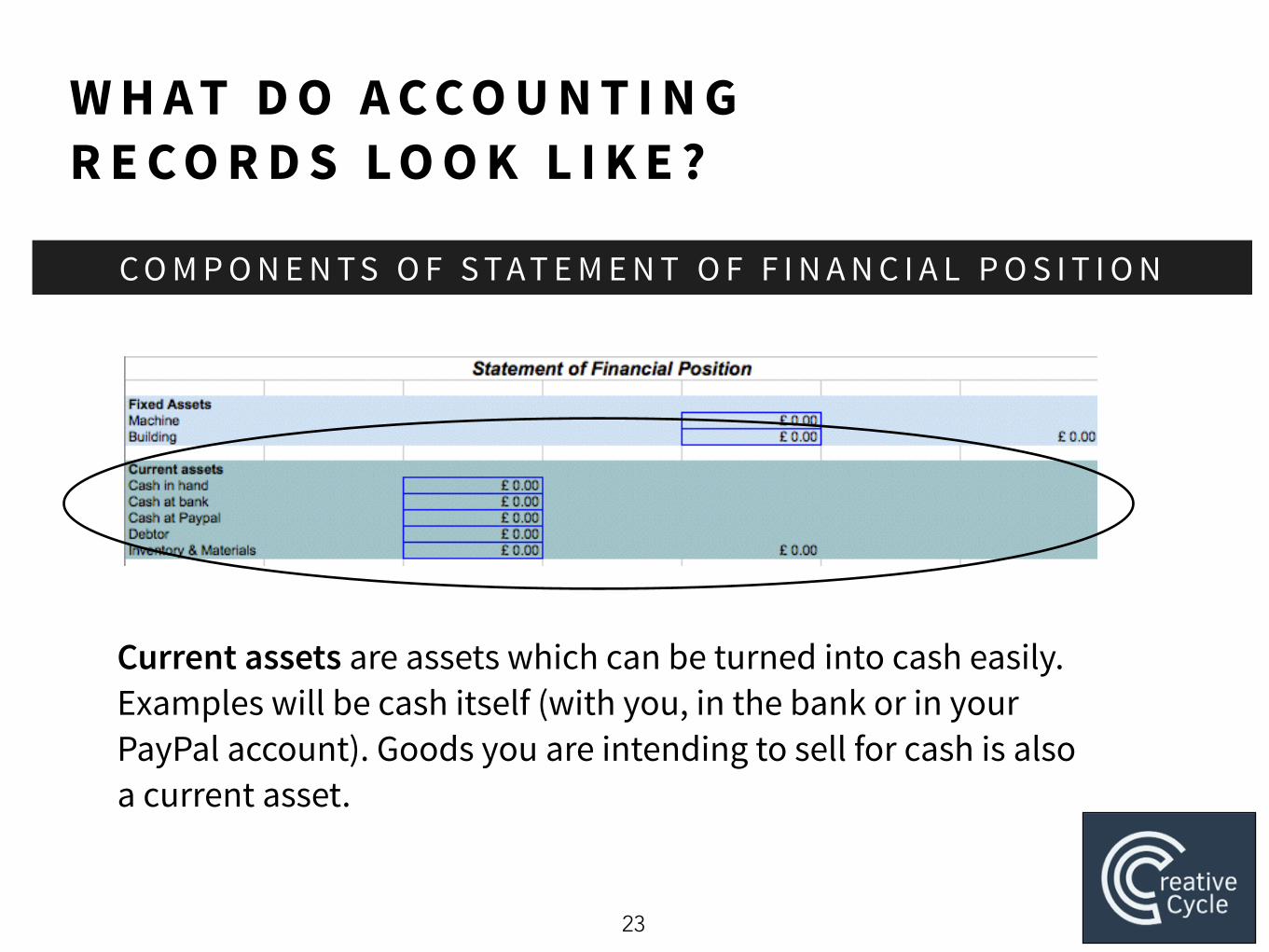

Current assets are assets which can be turned into cash easily. Examples will be cash itself (with you, in the bank or in your PayPal account). Goods you are intending to sell for cash is also a current asset.

W H A T D O A C C O U N T I N G R E C O R D S L O O K L I K E ?

24

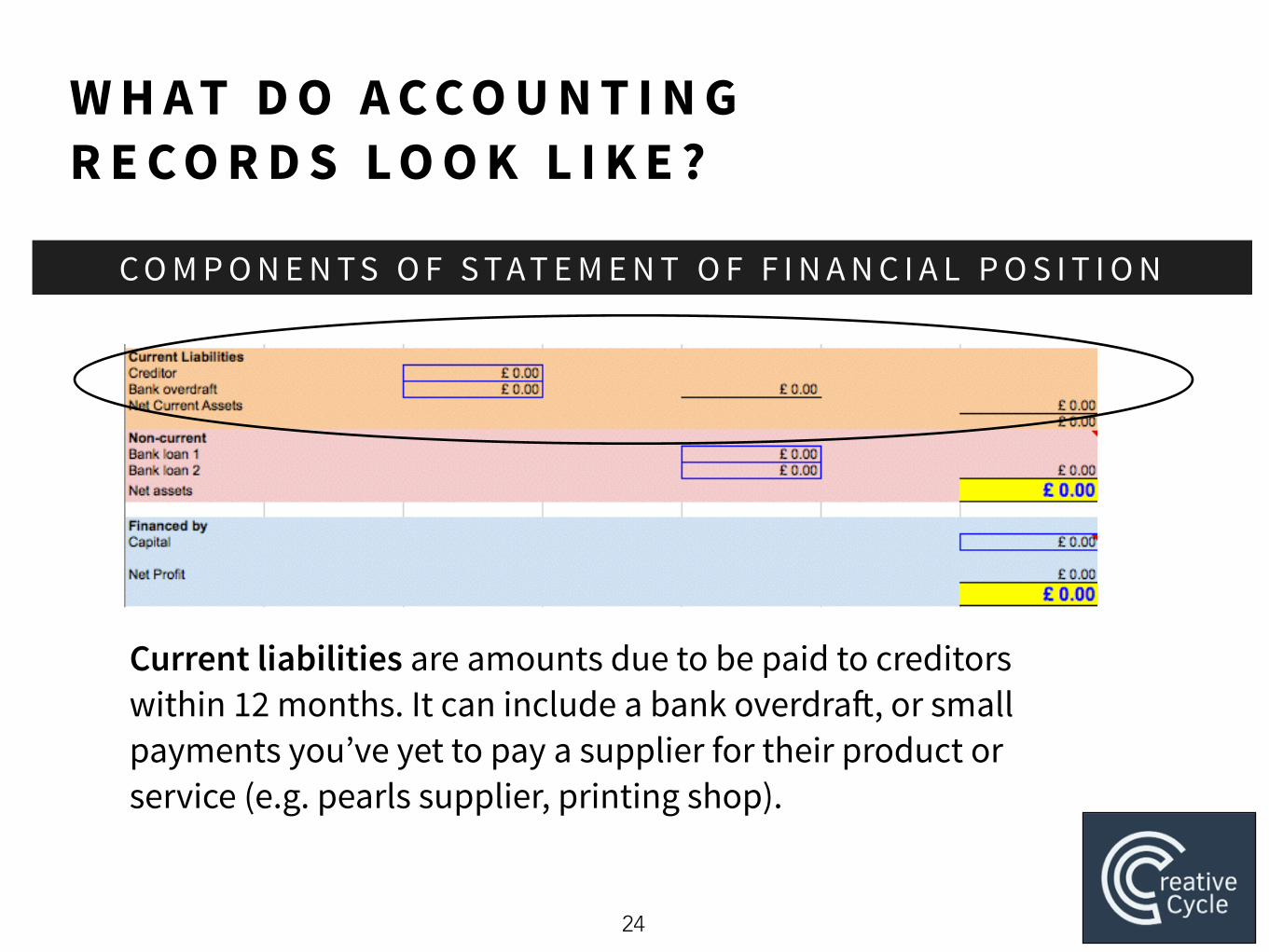

C O M P O N E N T S O F S T A T E M E N T O F F I N A N C I A L P O S I T I O N

Current liabilities are amounts due to be paid to creditors within 12 months. It can include a bank overdraft, or small payments you’ve yet to pay a supplier for their product or service (e.g. pearls supplier, printing shop).

W H A T D O A C C O U N T I N G R E C O R D S L O O K L I K E ?

25

C O M P O N E N T S O F S T A T E M E N T O F F I N A N C I A L P O S I T I O N

Non-current liabilities are amounts due to be paid to creditors after a longer period of time (above 12 months). It can be a 5-year bank loan, or long-term lease obligations for your shop.

W H A T D O A C C O U N T I N G R E C O R D S L O O K L I K E ?

26

C O M P O N E N T S O F S T A T E M E N T O F F I N A N C I A L P O S I T I O N

Capital is what you initially invested in the company.

L E T ’ S L E A R N …

27

!In the next few slides we will take a step-by-step approach to gradually teach you the basics of accounting. !You will go through an example similar to real life conditions!

A C C O U N T I N G & E X C E L

28

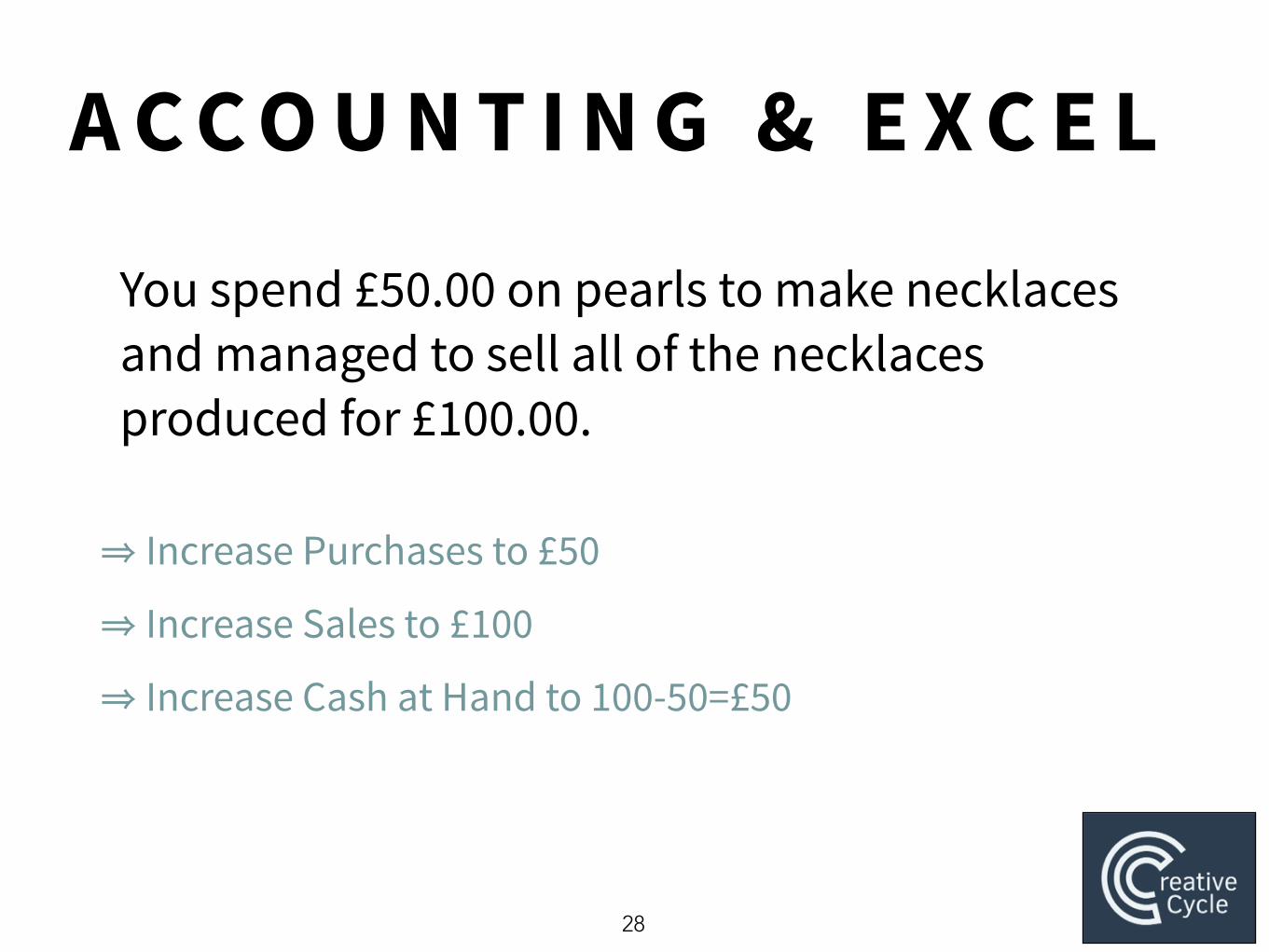

You spend £50.00 on pearls to make necklaces and managed to sell all of the necklaces produced for £100.00.

!⇒ Increase Purchases to £50

⇒ Increase Sales to £100

⇒ Increase Cash at Hand to 100-50=£50

29

However, instead of buying the pearls with cash earlier, you bought them on credit. !

You also haven’t yet received the money for a quarter of the necklaces.!⇒ Increase Creditors to £50

⇒ Increase Debtor to 100*(¼)= £25

⇒ Increase Cash at hand to 50+50-25=£75

A C C O U N T I N G & E X C E L

30

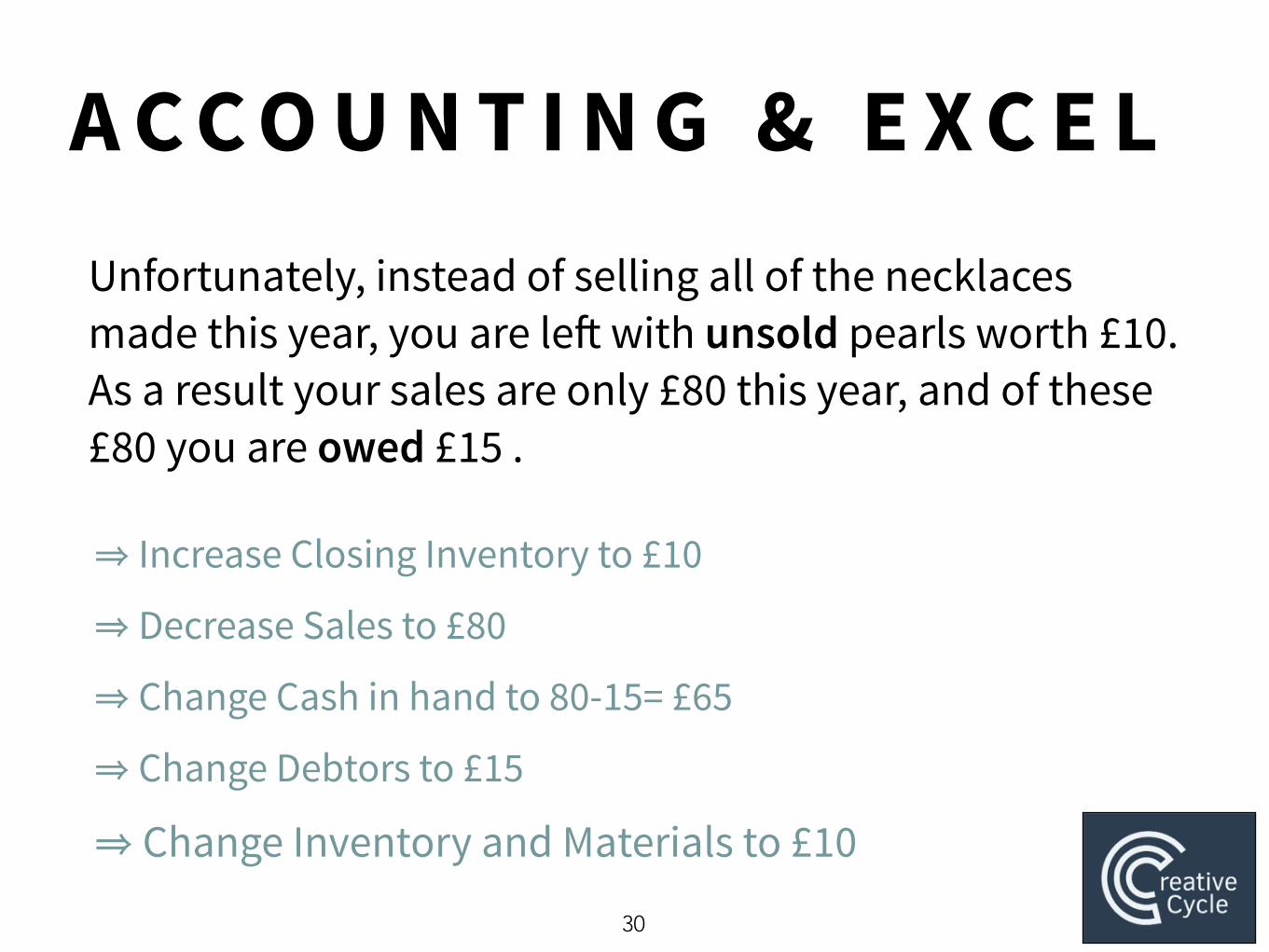

Unfortunately, instead of selling all of the necklaces made this year, you are left with unsold pearls worth £10. As a result your sales are only £80 this year, and of these £80 you are owed £15 .

⇒ Increase Closing Inventory to £10

⇒ Decrease Sales to £80

⇒ Change Cash in hand to 80-15= £65

⇒ Change Debtors to £15

⇒ Change Inventory and Materials to £10

A C C O U N T I N G & E X C E L

31

You realise that you forgot to account for pendants that you bought last year for £20 but didn’t manage to sell. Fortunately you managed to get rid of them at their face value (£20).

⇒ Sales increase by £20 to £100.

⇒ Opening inventory increases by £20.

A C C O U N T I N G & E X C E L

32

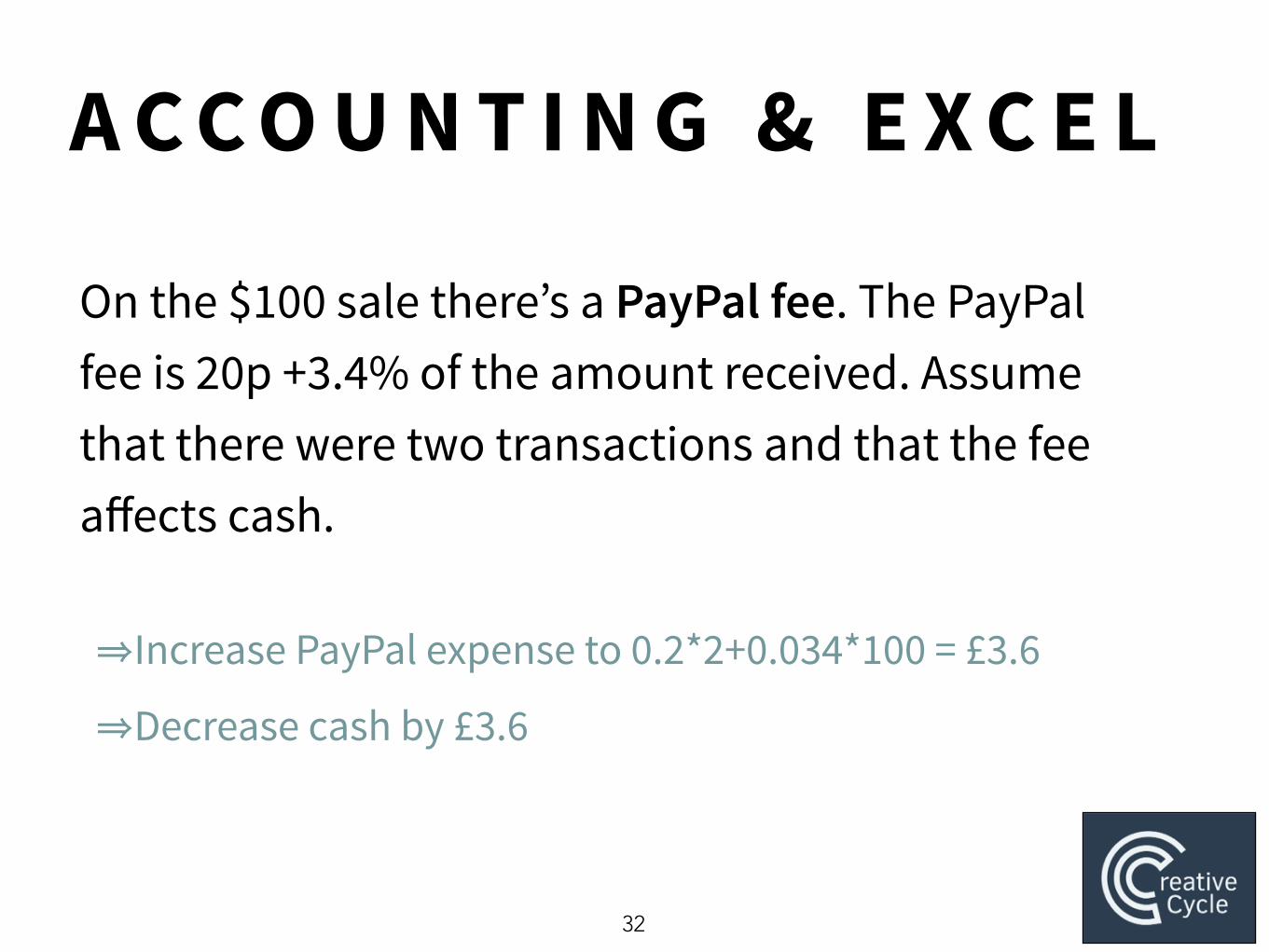

On the $100 sale there’s a PayPal fee. The PayPal fee is 20p +3.4% of the amount received. Assume that there were two transactions and that the fee affects cash.

⇒Increase PayPal expense to 0.2*2+0.034*100 = £3.6

⇒Decrease cash by £3.6

A C C O U N T I N G & E X C E L

33

Last year you made the acquisition of a machine that allows the making of necklaces faster. It cost £500 which you paid for entirely by borrowing for 10 years.

⇒ Increase machine to £500

⇒ Increase loans to £500

A C C O U N T I N G & E X C E L

34

You have to pay interest on your loan. The rate is 4% per year, which is £20. You pay it using the bank as an intermediary. You also decide to transfer £30 of your cash at hand to your bank account.

⇒Increase Interest Expense by 0.04*500=£20

⇒Cash at hand: 61.4-30= £31.40

⇒Cash at bank: 30-20= £10

A C C O U N T I N G & E X C E L

A P P E N D I X - D E F I N I T I O N S

35

Assets: Anything of value that you own. Bank overdraft: when the cash at bank is negative. Capital: amount invested in the business. Cost of transport IN: Cost of transporting the purchases. Closing inventory: Value of goods, supplies and materials held at end of year. Creditor: Purchases that we have not paid for yet. Current assets: Assets that can be converted easily into cash. Current liabilities: Liabilities that have to be paid back in the near future. Debtor: Money owed by customers. Expenses: Costs not directly related to the production of goods. Final Value Fees: Fees paid to Etsy and eBay for a sale (commission), as well as PayPal.

A P P E N D I X - D E F I N I T I O N S

36

Fixed assets: Assets that cannot easily be sold for cash. Gross profit: Sales minus cost of goods sold. Interest fee: Cost of having a loan. Liabilities: Anything that you owe to someone else. Net profit: Gross profit add income minus expenses minus taxes minus interest fees. Non-current liabilities: Liabilities that do not need to be settled in the near future. Purchases: Amount paid for supplies and materials this year. Opening inventory: Value of goods, supplies and materials held at beginning of year. Overhead costs: Grouped expenses (rent, gas, electricity) necessary for the business but not immediately linked to the good sold. Sales: Income received from sale of goods.

A D D I T I O N A L R E S O U R C E S

37

Accounting Coach: http://www.accountingcoach.com !

An online website with extensive resources. They have a search function on their website which allows you to search for answers to any queries you might have.

O N L I N E A C C O U N T I N G R E S O U R C E S

A D D I T I O N A L R E S O U R C E S

38

!

Entrepreneur Education - Accounting 101: https://www.youtube.com/watch?v=hRCdKlJnNkI !

An optional video. While it relates to US laws, it provides a good starting point with relevant examples to help you better understand how you can incorporate accounting for your own business.

A C C O U N T I N G F O R E N T R E P R E N E U R S

A D D I T I O N A L R E S O U R C E S

39

YouTube videos with tax information for UK businesses: https://www.youtube.com/user/HMRCgovuk !

Guidelines on how to pay your taxes when starting your business: http://www.hmrc.gov.uk/startingup/index.htm

T A X I N F O R M A T I O N - H M R C G U I D E L I N E S