accounting aspects for mergers and acquisitions (2)

DESCRIPTION

this is all about mergers and acquisitionsTRANSCRIPT

MODULE 4

ACCOUNTING ASPECTS OF

MERGERS AND

ACQUISITION

Dr. Rajesh P Ganatra

Introduction

When a company just acquires another company but does not amalgamate that company within itself, the shares purchased from the promoters and other shareholders are shown as ‘investment’ in the acquirer company’s books and are accounted at the cost at which they were acquired.

In the target company’s books no adjustment is required at all.

Accounting Fundamentals

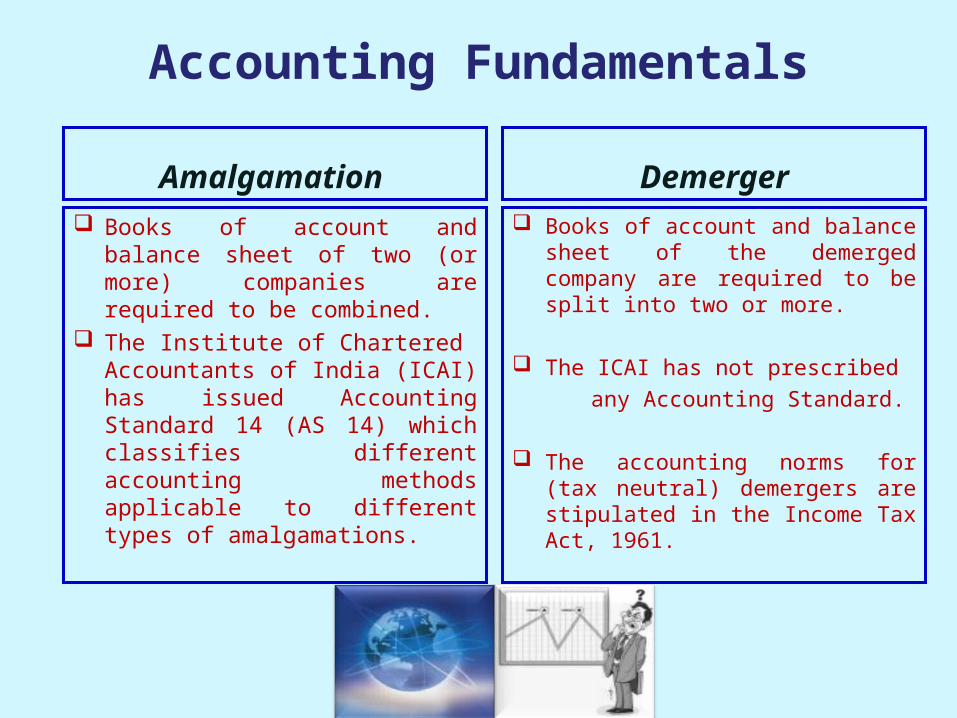

Amalgamation

Books of account and balance sheet of two (or more) companies are required to be combined.

The Institute of Chartered Accountants of India (ICAI) has issued Accounting Standard 14 (AS 14) which classifies different accounting methods applicable to different types of amalgamations.

Demerger Books of account and balance

sheet of the demerged company are required to be split into two or more.

The ICAI has not prescribed

any Accounting Standard.

The accounting norms for (tax neutral) demergers are stipulated in the Income Tax Act, 1961.

Accounting for Amalgamation

Accounting for Amalgamation

ACCOUNTING STANDARD 14

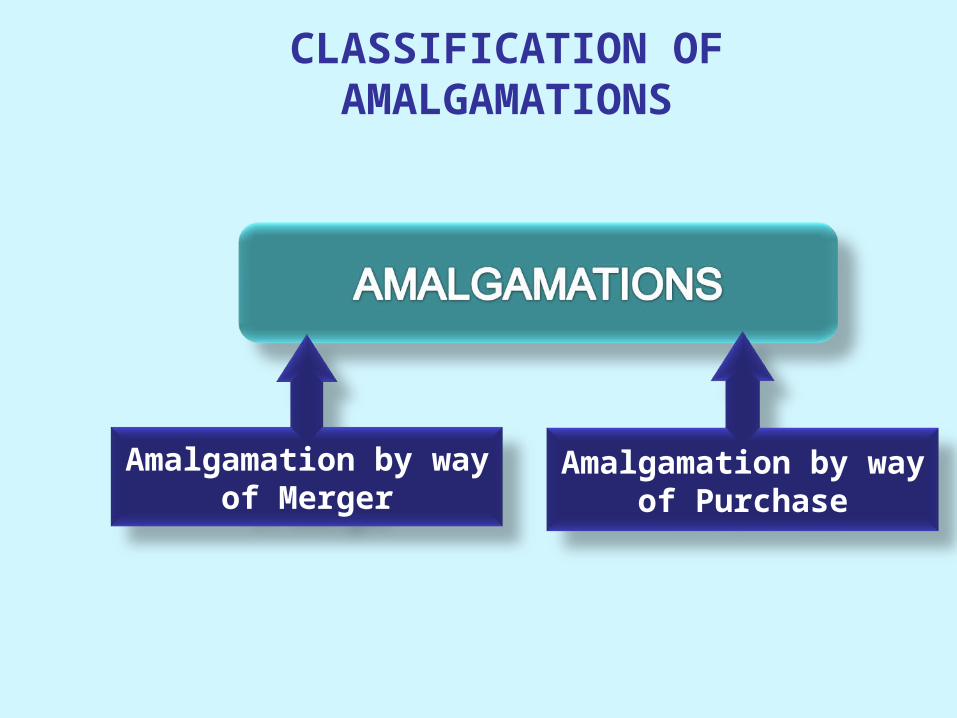

CLASSIFICATION OF AMALGAMATIONS

METHODS OF ACCOUNTING

(AS 14) Accounting for Amalgamations

The Standard deals with accounting for amalgamations and the treatment of any resultant goodwill or reserves.

The Standard does not deal with cases of acquisition which arise when there is purchase by one company (referred to as the acquiring company) of the whole or part of the shares, or the whole or part of the assets of another company (referred to as the acquired company) in consideration for payment in cash or by issue of shares or other securities in the acquiring company or partly in one form and partly in the other.

CLASSIFICATION OF AMALGAMATIONS

Amalgamation by way of Merger

Amalgamation by way of Purchase

Amalgamation by way of Merger

• Five Preconditions for Merger:All assets and liabilities of the transferor company become, after amalgamation, the assets and liabilities of the transferee company.

Shareholders holding not less than 90 percent of the face value of the equity shares of the transferor company (other than the equity shares already held by the transferee company or its subsidiaries or nominees) become the equity shareholders of the transferee company by virtue of the amalgamation.

The consideration for amalgamation received by those equity shareholders of the transferor company who agree to become the shareholders of the transferee company is discharged by the transferee company wholly by the issue of equity shares in the transferee company, except that cash may be paid in respect of any fractional shares.

Amalgamation by way of Merger

The transferee company intends to carry on the business of the transferor company after the amalgamation.

No adjustment is intended to be made in the book value of the assets and liabilities of the transferor company when they are incorporated in the financial statements of the transferee company except to ensure the uniformity of accounting policies.

An amalgamation in which any one or more of the five conditions mentioned earlier are not satisfied, then it is considered as amalgamation by way of purchase.

Amalgamation by Way ofPurchase

METHODS OF ACCOUNTING

Pooling of Interest Method Purchase Method

Pooling of Interest Method

• In case of an amalgamation by way of merger, the method prescribed is known as ‘pooling of interests method’.

• Under this method following norms are required to be adhered to:

In preparing the transferee company’s financial statements, the assets, liabilities and reserves of the transferor company should be recorded at their existing carrying amounts and in the same form as at the time of amalgamation.

Even the reserves under various heads in the transferor company’s books have to be accounted under the same heads in the transferee company’s books. Thus, ‘revaluation reserves’ of the transferor company will become or get added to the ‘revaluation reserves’ of the transferee company and so on.

The difference between the amount recorded as the share capital issued (plus any additional consideration in the form of cash or other assets) and the amount of share capital of the transferor company should be adjusted in reserves.

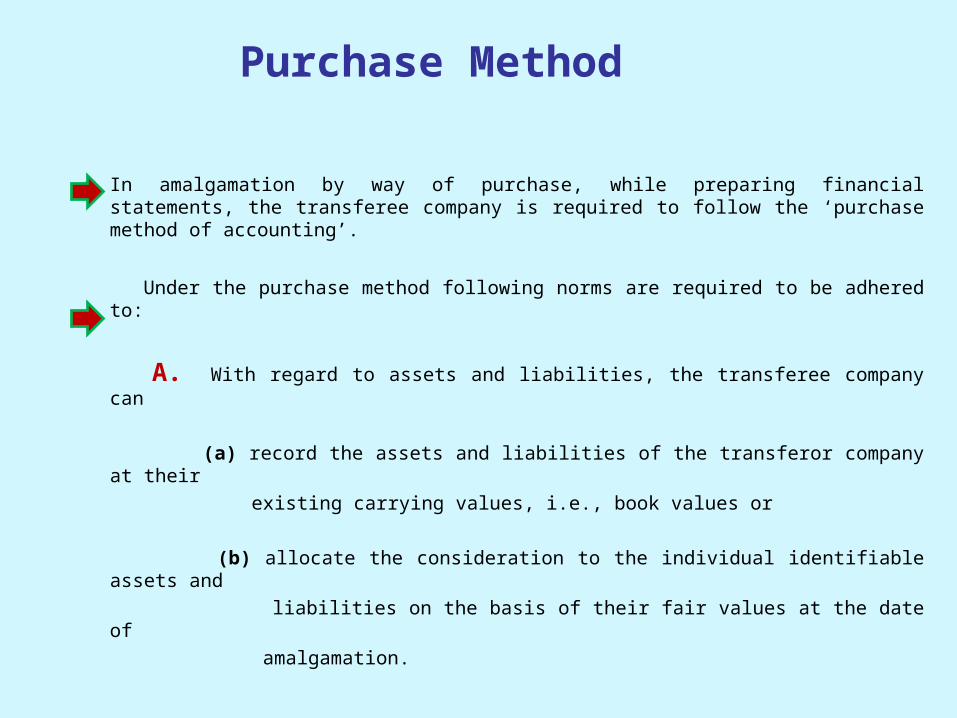

Purchase Method

• In amalgamation by way of purchase, while preparing financial statements, the transferee company is required to follow the ‘purchase method of accounting’.

Under the purchase method following norms are required to be adhered to:

A. With regard to assets and liabilities, the transferee company can

(a) record the assets and liabilities of the transferor company at their

existing carrying values, i.e., book values or

(b) allocate the consideration to the individual identifiable assets and

liabilities on the basis of their fair values at the date of

amalgamation.

Purchase Method

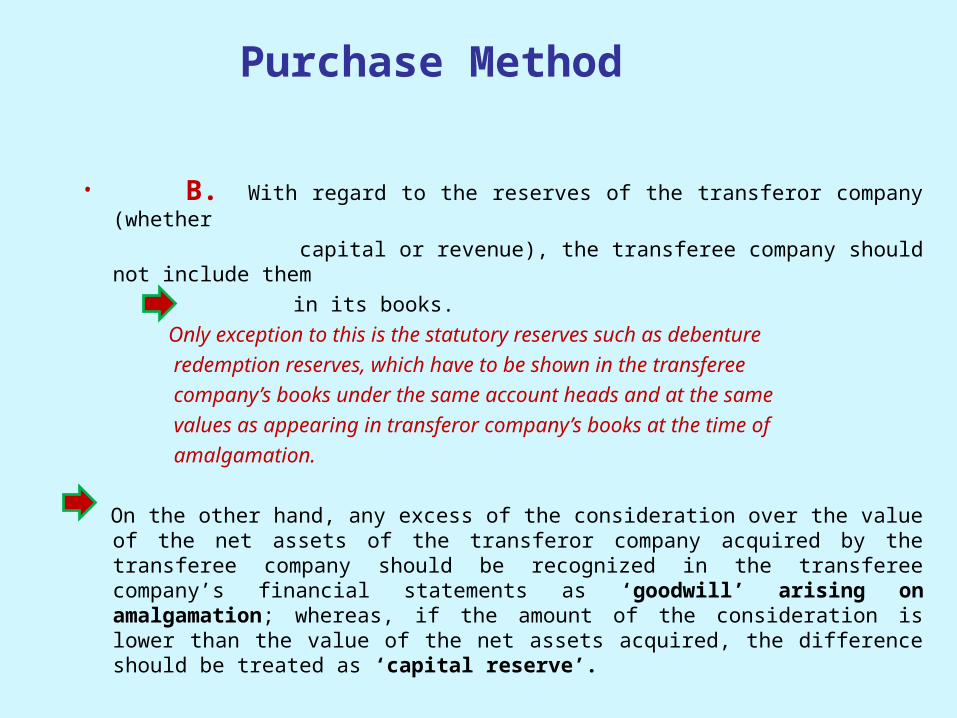

• B. With regard to the reserves of the transferor company (whether

capital or revenue), the transferee company should not include them

in its books.

Only exception to this is the statutory reserves such as debenture

redemption reserves, which have to be shown in the transferee

company’s books under the same account heads and at the same

values as appearing in transferor company’s books at the time of

amalgamation.

On the other hand, any excess of the consideration over the value of the net assets of the transferor company acquired by the transferee company should be recognized in the transferee company’s financial statements as ‘goodwill’ arising on amalgamation; whereas, if the amount of the consideration is lower than the value of the net assets acquired, the difference should be treated as ‘capital reserve’.

C. With regard to the norm of crediting the difference between the consideration paid and net value of assets to ‘capital reserve’ (where consideration is less than net value of assets), there is a loophole provided in the AS 14 itself.

D. With regard to the goodwill, if any, as created above, AS 14 requires the said goodwill to be amortized over its useful life but

not exceeding five years.

E. AS 14 also provides that where the statutory reserves of the transferor company have been recorded in the financial statements of the transferee company under the same accounting heads as in the books of the transferor company, a corresponding debit should be given to the ‘amalgamation adjustment account’, which should be disclosed under the ‘miscellaneous expenditure’.

Purchase Method

Accounting for Demerger

Accounting for Demerger

The ICAI has, as yet, not prescribed any accounting standard for demerger. However, ironically, the Income Tax Act, 1961, has defined the accounting norms for demerger.

The Act stipulates that all the assets and liabilities of the undertaking being demerged must be transferred to the resulting company and must be transferred at book values only.

If any asset of the undertaking being demerged has been revalued, such revaluation needs to be ignored.

This means that while transferring to the resulting company the assets of the undertaking being demerged, which were earlier revalued, have to be restated at cost (less accumulated depreciation in case of fixed assets).

A peculiar situation would, however, arise if the company has already capitalized these reserves by the issue of bonus shares. In such a case, the transferor company would end up adjusting the diminution in the value of assets against its general reserves.

Accounting for Demerger

Transfer of Liabilities and Loans

Specific liabilities of the undertaking being demerged have to be transferred to the resulting company.

Specific loans or borrowings including debentures raised, incurred and utilized solely for the activities and operations of the undertaking being demerged have to be transferred to the resulting company.

Common loans and borrowing have to be apportioned to the resulting company in the same ratio as the book value of the assets transferred to the resulting company bears to the total book value of the assets of the demerged company prior to demerger.

Accounting for Demerger