accounting & auditing update - ncacpa | professional ... · pdf fileaccounting &...

TRANSCRIPT

North Carolina Association of CPAs Employee Benefit Plans Conference

Accounting & Auditing Update

Tricia A. Van Vliet, CPA Elliott Group CPAs, PLLC

What We Have Lined Up for You

• Current developments from our standard setters

– FASB

– AICPA

– PCAOB

• Changes impacting your audits in 2014 and looking forward

• Important reminders…before you “check the box”

– Revisiting your risk assessment & audit plans that respond to risks identified

2

Current developments from our standard setters - FASB

Very narrow scope…however, some confusion caused by title

Intended to address issues associated with private company ESOPs

Relief for sponsors of private

company ESOPs; quantitative information

regarding significant unobservable inputs used in

determining fair value of sponsor’s nonpublic equity

securities categorized within Level 3 of the hierarchy

Disclosures required by

ASC 820-10-50-2(bbb)(2)

Deferred Indefinitely

FASB ASU No. 2013-09 – Fair Value Measurement (Topic

820): Deferral of the Effective Date of Certain Disclosures

for Nonpublic Employee Benefit Plans in Update

2011-04

3

Current developments from our standard setters - FASB

Intended to improve comparability between entities reporting under GAAP and IFRS; enhance disclosure and provide converged disclosures for certain financial and derivative instruments

Effective date: Fiscal years beginning on or after

January 1, 2013, and related interim periods within that fiscal year; retrospective

implementation for all comparative periods presented

Expectation that many defined Benefit and health & welfare plans or master trusts, as well as certain defined contribution plans with more diverse & complex portfolios hold contracts that include master netting arrangements within the scope of this ASU

Terms of contracts can be very complex and may require legal

interpretation to determine enforceability of netting provisions…expect information

gathering, coordination of expertise & conclusions take time…plan ahead!

FASB ASU No. 2011-11 as amended by ASU No. 2013-

01 – Disclosures About Offsetting Assets & Liabilities

4

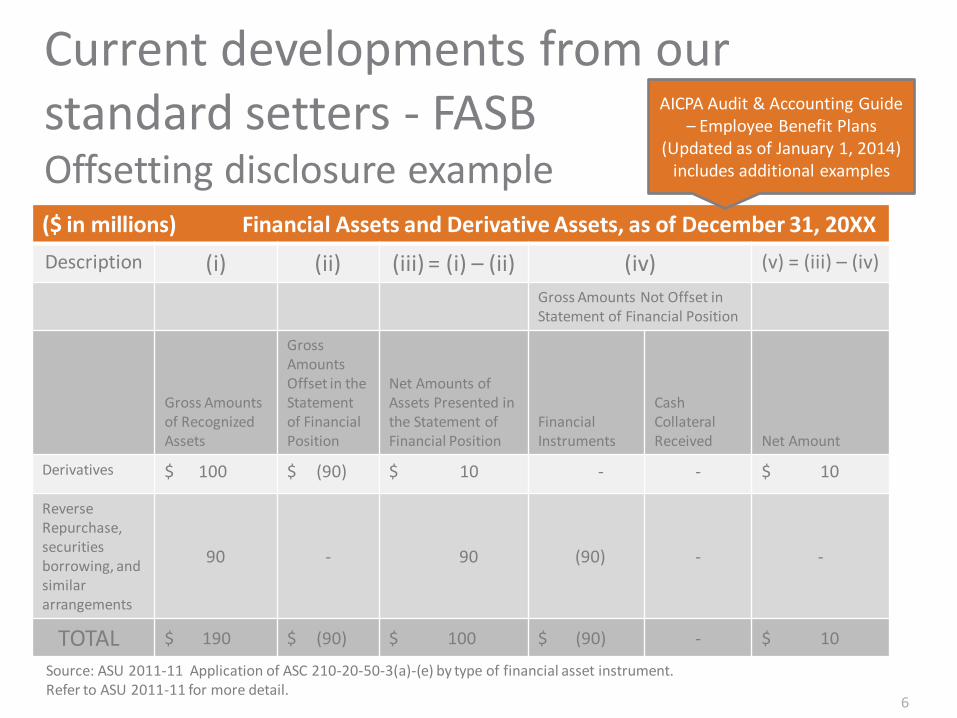

Current developments from our standard setters - FASB

The following quantitative information for assets & liabilities (within the scope of the ASU), disclosed in a table at the end of the reporting period:

(a) Gross amounts of recognized assets & recognized liabilities

(b) Amounts offset in the statement of net assets available for benefits

(c) Net amount presenting in the statement of net assets available for benefits

(d) Amounts subject to master netting arrangement or similar agreement: amounts related to recognized financial or other derivative instruments; amounts related to financial collateral

(e) Net amount after deducting amounts in items (d) & (c)

5

A Closer Look at the Offsetting Asset & Liability Disclosure

Requirements

Current developments from our standard setters - FASB Offsetting disclosure example

($ in millions) Financial Assets and Derivative Assets, as of December 31, 20XX

Description (i) (ii) (iii) = (i) – (ii) (iv) (v) = (iii) – (iv)

Gross Amounts Not Offset in Statement of Financial Position

Gross Amounts of Recognized Assets

Gross Amounts Offset in the Statement of Financial Position

Net Amounts of Assets Presented in the Statement of Financial Position

Financial Instruments

Cash Collateral Received Net Amount

Derivatives $ 100 $ (90) $ 10 - - $ 10

Reverse Repurchase, securities borrowing, and similar arrangements

90 - 90 (90) - -

TOTAL $ 190 $ (90) $ 100 $ (90) - $ 10

Source: ASU 2011-11 Application of ASC 210-20-50-3(a)-(e) by type of financial asset instrument. Refer to ASU 2011-11 for more detail.

6

AICPA Audit & Accounting Guide – Employee Benefit Plans

(Updated as of January 1, 2014) includes additional examples

Current developments from our standard setters - FASB

Prepare financial statements using liquidation basis of accounting when liquidation is imminent; plan for liquidation is approved or is being enforced by other forces (e.g., involuntary plan termination)

Effective date: For entities that determine liquidation is imminent

during annual reporting periods beginning after December 15, 2013 and interim reporting periods

therein; applied prospectively from day that liquidation becomes imminent; early adoption

permitted

Present relevant information about plan’s expected resources in liquidation; generally measuring & presenting assets at amount of expected cash proceeds; recognize & measure liabilities in accordance with applicable GAAP; accrue & separately present costs expected to be incurred & income expected to be earned during liquidation

If a plan is already on the liquidation basis of accounting at effective date of ASU, plan would

continue to apply current guidance in ASC 960-40, 962-40 and 965-40 until liquidation is complete

FASB ASU No. 2013-07, Presentation of Financial Statements (Topic 205):

Liquidation Basis of Accounting

7

Current developments from our standard setters - FASB • Special considerations for defined benefit

pension plans

– Looking ahead to implementation

8

Liq

uid

atio

n Im

min

ent

Board vs. PBGC approvals

Imp

lem

enta

tio

n

Beginning vs. end of year presentation

Act

uar

ial E

stim

ates

Settlement liability & required contributions

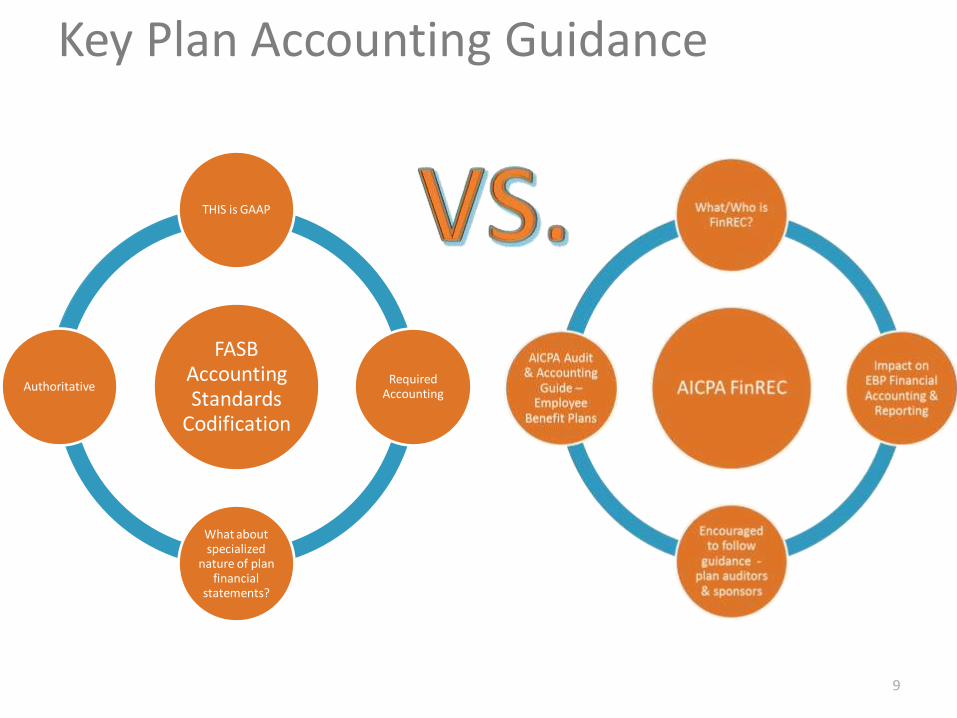

Key Plan Accounting Guidance

FASB Accounting Standards

Codification

THIS is GAAP

Required Accounting

What about specialized

nature of plan financial

statements?

Authoritative

9

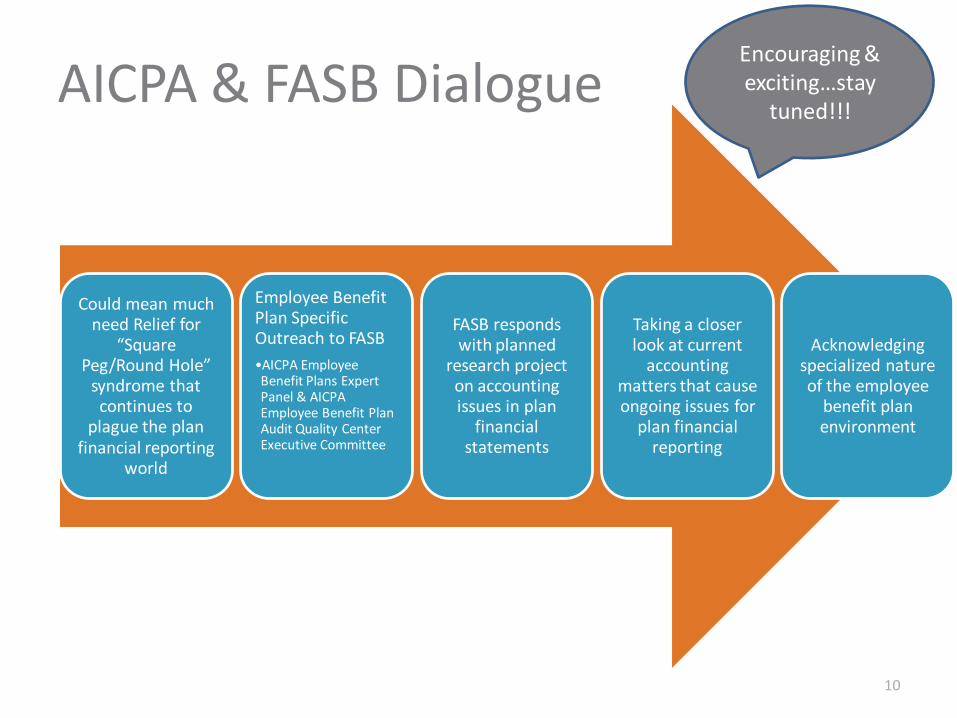

AICPA & FASB Dialogue

10

Could mean much need Relief for

“Square Peg/Round Hole”

syndrome that continues to

plague the plan financial reporting

world

Employee Benefit Plan Specific Outreach to FASB

•AICPA Employee Benefit Plans Expert Panel & AICPA Employee Benefit Plan Audit Quality Center Executive Committee

FASB responds with planned

research project on accounting issues in plan

financial statements

Taking a closer look at current

accounting matters that cause ongoing issues for

plan financial reporting

Acknowledging specialized nature of the employee

benefit plan environment

Encouraging & exciting…stay

tuned!!!

AICPA & FASB Dialogue (continued)

www.aicpa.org/InterestAreas/EmployeeBenefitPlanAuditQuality/Resources/TestimonyandCmtLtrs/DownloadableDocuments/EBP-Discussion-Memo-Observations-About-Current-EBP-Accounting.pdf

11

Further details can be found by accessing the full discussion

memorandum as follows:

Current Developments –Regulatory Matters to Consider in 2014 Audits

12

Defense of Marriage Act (DOMA)

• Primarily inquiry considerations to evaluate sponsor entity’s attention to and understanding of ongoing regulatory requirements in connection with overall risk assessment

Affordable Care Act (ACA) • Medial loss ratio rebates

• Notice requirements

• Changes that may impact certain healthcare arrangements; consider stand-alone features that may now be require association with a health plan (certain HRAs and FSAs)

• Employer Shared Responsibility Payment

• Delays: 1/1/2015 for employers with >= 100 FTEs; 1/1/2016 for employers with 50-99 FTEs; certain conditions apply

• Transition rules can be complex – communication is key

• Consider responses to inquiries & findings to evaluate sponsor entity’s attention to and understanding of ongoing regulatory requirements in connection with overall risk assessment

Current Developments - AICPA

February 2014 – ASB finalized redrafting of last pre-clarity AU section; completed the Clarity Project relating to SASs

Supersedes SAS No. 65, The Auditor’s Consideration of the Internal Audit Function

in an Audit of Financial Statements; also amends AU-C Sec. 315, among others

Addresses auditor responsibilities when using work of internal auditors: in obtaining audit evidence; using internal auditors to provide direct assistance under direction, supervision & review of the external auditor

Effective Date: audits of financial statements for periods ending on or after

December 15, 2014

SAS No. 128, Using the Work of Internal Auditors

(AU-C Sec. 610)

13

Current Developments - PCAOB

Applicable to plan’s considered to be SEC registrants and subject to SEC filing requirements (Form 11-K)

Intended to enhance relevance & timeliness of communications; facilitate dialogue regarding

significant audit and financial reporting matters

Requirements are similar to those of AICPA Professional Standards AU-C Section 260, The Auditor’s Communication with Those Charged with Governance; differences do exist; auditors of plan’s subject to 11-K filing must comply with requirements of both standards

Effective Date: audits of SEC registrant financial statements of fiscal periods beginning

on or after December 15, 2012

Auditing Standard (AS) No. 16, Communications with

Audit Committees

14

Looking Ahead

PCAOB AS 17 – Auditing Supplemental Information

Accompanying Audited Financial Statements

(effective for financial statements of fiscal years ending on or after

June 1, 2014)

PCAOB and IAASB Reporting Proposals

Clarified Attestation Standards

Interpretation No. 101-18, Application of Independence Rules

to Affiliates

(effective for engagements covering periods beginning on or after

January 1, 2014)

15

Important Reminders…before you “check the box”

• Numerous factors impact your client’s employees and plan operations…and should be considered in your ongoing risk assessment and planned audit response

Stay informed

• FASB, AICPA, PCAOB, DOL, IRS, PBGC, etc.

Standard setting and regulatory bodies

• Economic conditions can significantly influence decisions made by plan sponsor

The economy

16

Important Reminders…before you “check the box” (continued)

• AICPA Employee Benefit Plan Audit Quality Center: www.aicpa.org/InterestAreas/EmployeeBenefitPlanAuditQuality/Pages/EBPAQhomepage.asp

• US Department of Labor Employee Benefits Security Administration: www.dol.gov/ebsa

• Internal Revenue Service Retirement Plans: www.irs.gov/Retirement-Plans

• Pension Benefit Guaranty Corporation Practitioners: www.pbgc.gov/prac/index.html

Resources Available to Assist Are Just a Click Away

17

Questions

18

Tricia A Van Vliet, CPA

Elliott Group CPAs, PLLC

(616) 258-8519

19