accounting & culture international differences. manifestations of culture symbols symbols

TRANSCRIPT

Accounting & CultureAccounting & Culture

International DifferencesInternational Differences

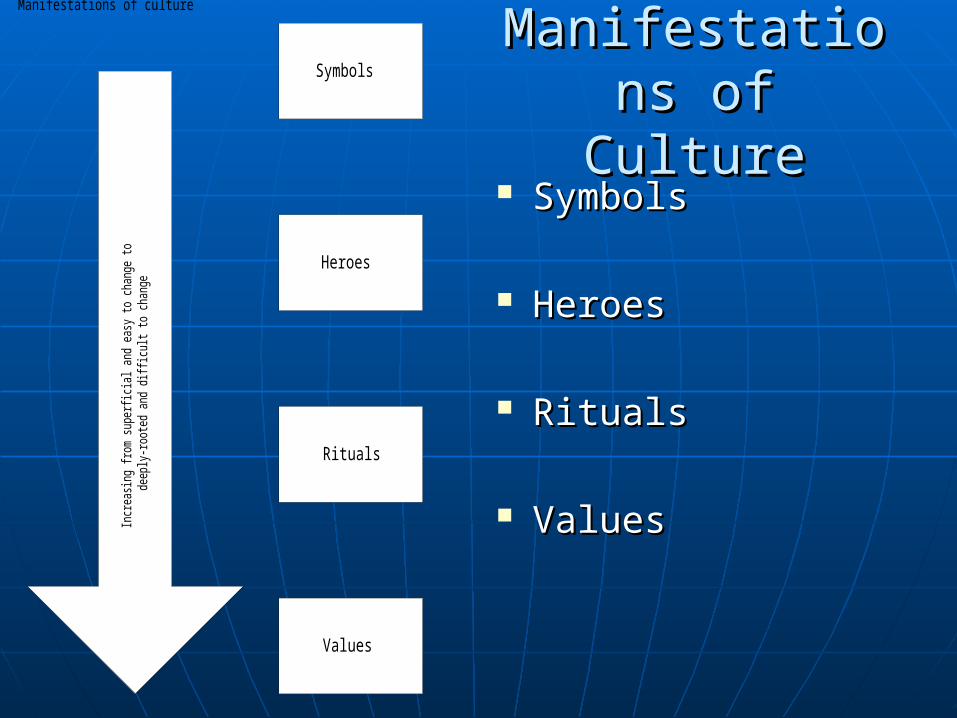

Manifestations of Manifestations of CultureCulture

SymbolsSymbols

Symbols

Heroes

Rituals

Values

Incr

easi

ng fr

om s

uper

ficia

l and

eas

y to

cha

nge

tode

eply

-root

ed a

nd d

iffic

ult t

o ch

ange

Manifestations of culture

Manifestations of Manifestations of CultureCulture

SymbolsSymbols

HeroesHeroes

Symbols

Heroes

Rituals

Values

Incr

easi

ng fr

om s

uper

ficia

l and

eas

y to

cha

nge

tode

eply

-root

ed a

nd d

iffic

ult t

o ch

ange

Manifestations of culture

Manifestations of Manifestations of CultureCulture

SymbolsSymbols

HeroesHeroes

RitualsRituals

Symbols

Heroes

Rituals

Values

Incr

easi

ng fr

om s

uper

ficia

l and

eas

y to

cha

nge

tode

eply

-root

ed a

nd d

iffic

ult t

o ch

ange

Manifestations of culture

Manifestations of Manifestations of CultureCulture

SymbolsSymbols

HeroesHeroes

RitualsRituals

ValuesValues

Symbols

Heroes

Rituals

Values

Incr

easi

ng fr

om s

uper

ficia

l and

eas

y to

cha

nge

tode

eply

-root

ed a

nd d

iffic

ult t

o ch

ange

Manifestations of culture

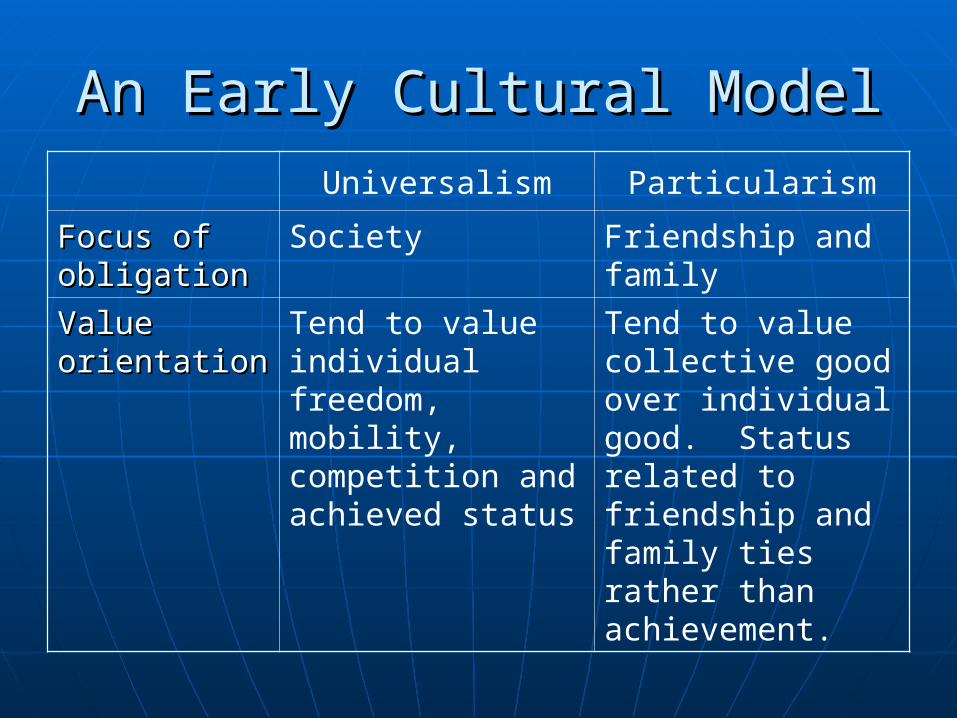

An Early Cultural ModelAn Early Cultural Model

Universalism Particularism

Focus of Focus of obligationobligation

Society Friendship and family

Value Value orientation orientation

Tend to value individual freedom, mobility, competition and achieved status

Tend to value collective good over individual good. Status related to friendship and family ties rather than achievement.

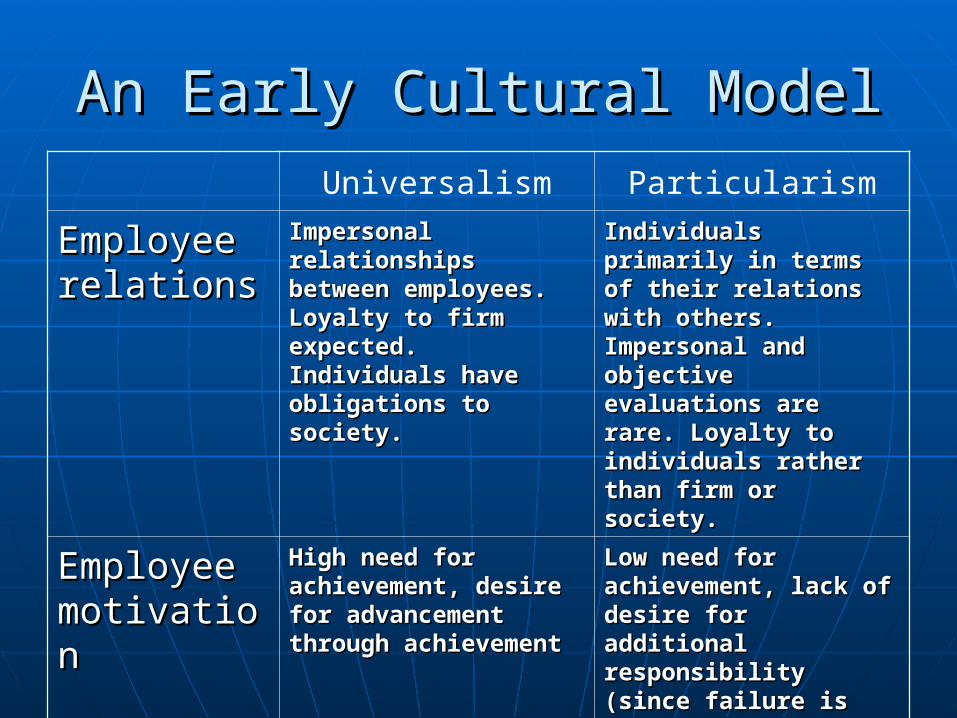

An Early Cultural ModelAn Early Cultural Model

Universalism Particularism

Employee Employee relationsrelations

Impersonal Impersonal relationships relationships between employees. between employees. Loyalty to firm Loyalty to firm expected. Individuals expected. Individuals have obligations to have obligations to society.society.

Individuals primarily Individuals primarily in terms of their in terms of their relations with others. relations with others. Impersonal and Impersonal and objective evaluations objective evaluations are rare. Loyalty to are rare. Loyalty to individuals rather individuals rather than firm or society.than firm or society.

Employee Employee motivationmotivation

High need for High need for achievement, desire achievement, desire for advancement for advancement through achievementthrough achievement

Low need for Low need for achievement, lack of achievement, lack of desire for additional desire for additional responsibility (since responsibility (since failure is possible)failure is possible)

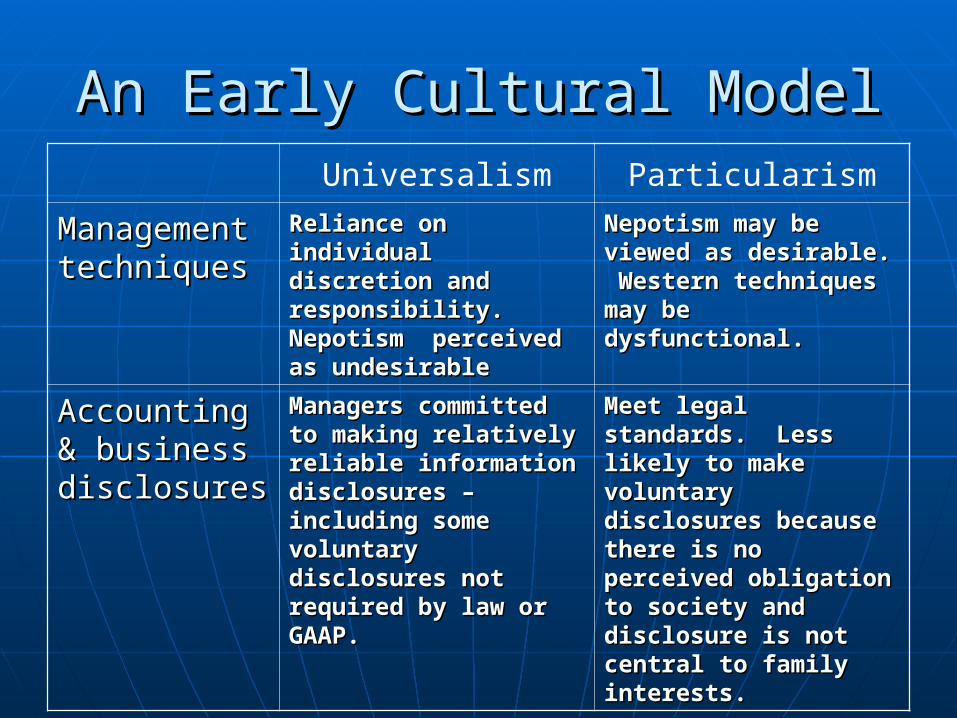

An Early Cultural ModelAn Early Cultural ModelUniversalism Particularism

Management Management techniquestechniques

Reliance on Reliance on individual discretion individual discretion and responsibility. and responsibility. Nepotism perceived Nepotism perceived as undesirableas undesirable

Nepotism may be Nepotism may be viewed as desirable. viewed as desirable. Western techniques Western techniques may be may be dysfunctional.dysfunctional.

Accounting Accounting & business & business disclosuresdisclosures

Managers committed Managers committed to making relatively to making relatively reliable information reliable information disclosures – disclosures – including some including some voluntary disclosures voluntary disclosures not required by law not required by law or GAAP.or GAAP.

Meet legal standards. Meet legal standards. Less likely to make Less likely to make voluntary disclosures voluntary disclosures because there is no because there is no perceived obligation perceived obligation to society and to society and disclosure is not disclosure is not central to family central to family interests.interests.

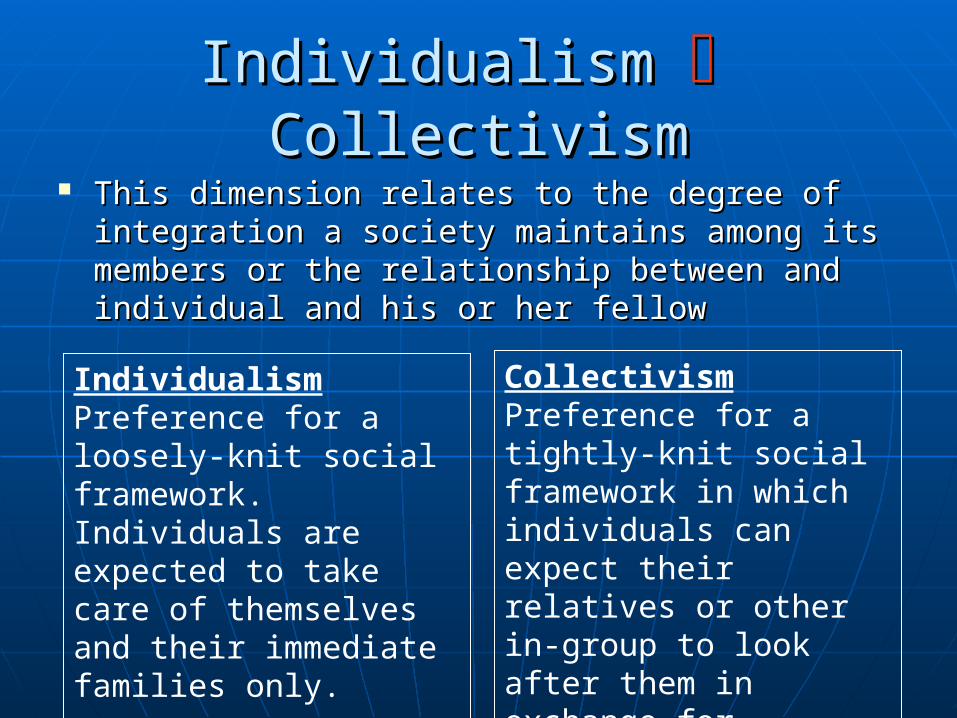

Individualism Individualism CollectivismCollectivism This dimension relates to the degree of This dimension relates to the degree of

integration a society maintains among its integration a society maintains among its members or the relationship between and members or the relationship between and individual and his or her fellowindividual and his or her fellow

Individualism Preference for a loosely-knit social framework. Individuals are expected to take care of themselves and their immediate families only.

Collectivism Preference for a tightly-knit social framework in which individuals can expect their relatives or other in-group to look after them in exchange for unquestioning loyalty.

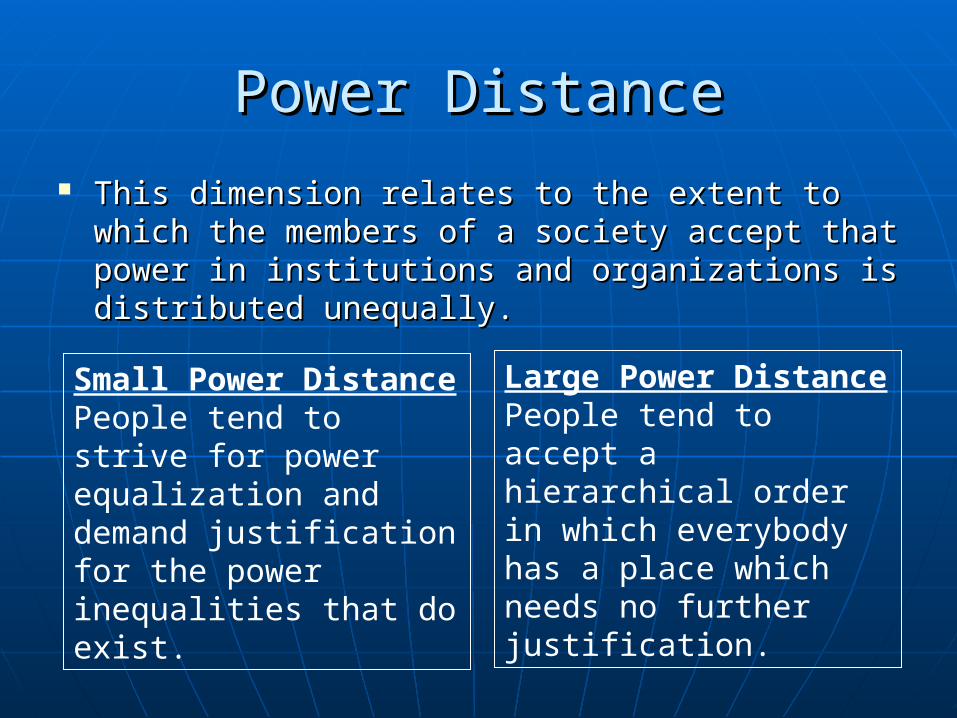

Power DistancePower Distance

This dimension relates to the extent to which the This dimension relates to the extent to which the members of a society accept that power in members of a society accept that power in institutions and organizations is distributed institutions and organizations is distributed unequally.unequally.

Small Power Distance People tend to strive for power equalization and demand justification for the power inequalities that do exist.

Large Power Distance People tend to accept a hierarchical order in which everybody has a place which needs no further justification.

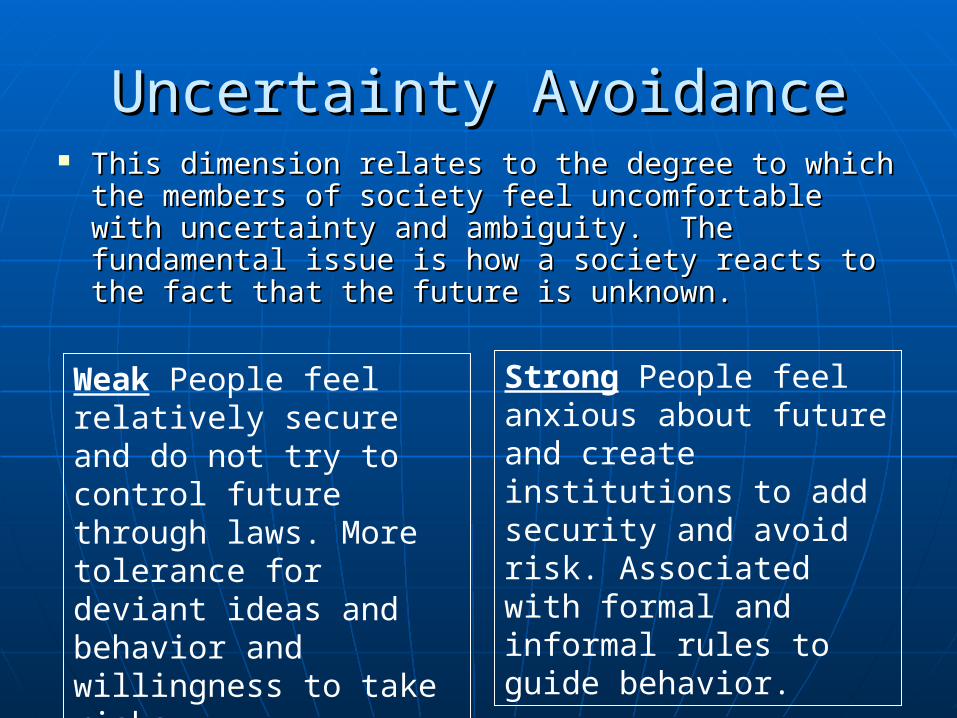

Uncertainty AvoidanceUncertainty Avoidance This dimension relates to the degree to which the This dimension relates to the degree to which the

members of society feel uncomfortable with members of society feel uncomfortable with uncertainty and ambiguity. The fundamental uncertainty and ambiguity. The fundamental issue is how a society reacts to the fact that the issue is how a society reacts to the fact that the future is unknown.future is unknown.

Weak People feel relatively secure and do not try to control future through laws. More tolerance for deviant ideas and behavior and willingness to take risks.

Strong People feel anxious about future and create institutions to add security and avoid risk. Associated with formal and informal rules to guide behavior.

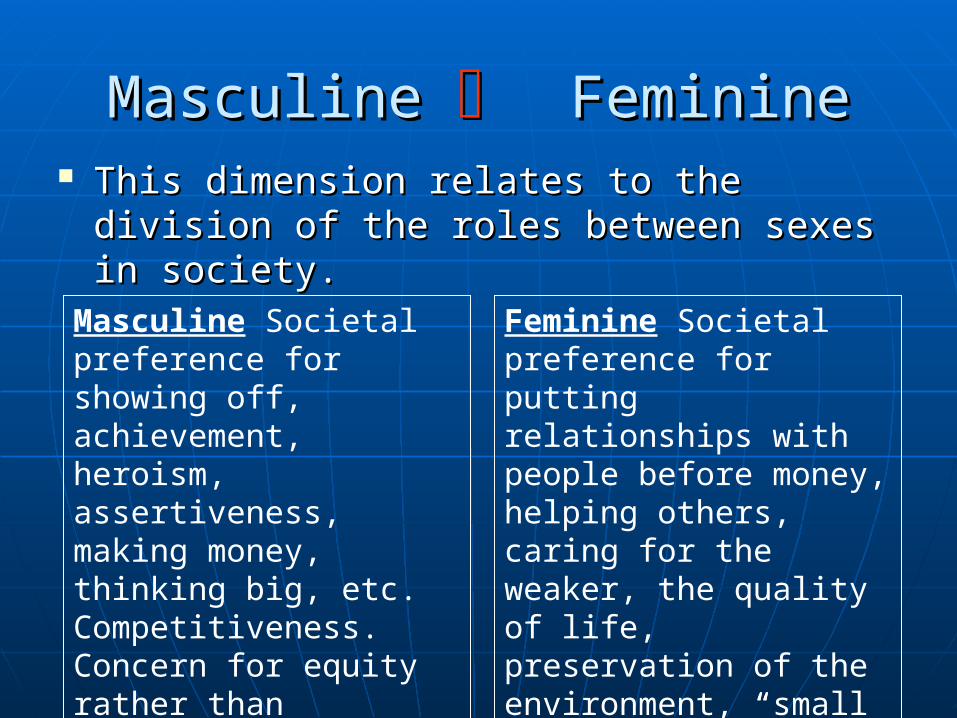

Masculine Masculine FeminineFeminine This dimension relates to the division of This dimension relates to the division of

the roles between sexes in society.the roles between sexes in society.

Masculine Societal preference for showing off, achievement, heroism, assertiveness, making money, thinking big, etc. Competitiveness. Concern for equity rather than equality.

Feminine Societal preference for putting relationships with people before money, helping others, caring for the weaker, the quality of life, preservation of the environment, “small is beautiful” and so on.

Accounting ValuesAccounting Values

ProfessionalismProfessionalism

Uniformity vs. FlexibilityUniformity vs. Flexibility

ConservatismConservatism

Secrecy vs. TransparencySecrecy vs. Transparency

Relationship of Culture to Relationship of Culture to Accounting ValuesAccounting Values

Hypothesis: High individualism, low Hypothesis: High individualism, low uncertainty avoidance, and low uncertainty avoidance, and low power distance is associated with power distance is associated with professionalism.professionalism.

Hypothesis: High uncertainty Hypothesis: High uncertainty avoidance, high power distance, and avoidance, high power distance, and low individualism is associated with low individualism is associated with preference for uniformity.preference for uniformity.

Relationship of Culture to Relationship of Culture to Accounting ValuesAccounting Values

Hypothesis: High uncertainty Hypothesis: High uncertainty avoidance, low individualism, and avoidance, low individualism, and low masculinity is associated with low masculinity is associated with preference for conservatism.preference for conservatism.

Hypothesis: High uncertainty Hypothesis: High uncertainty avoidance, high power distance, low avoidance, high power distance, low individualism, and low masculinity is individualism, and low masculinity is associated with a preference for associated with a preference for secrecy.secrecy.

Standard Setting & CultureStandard Setting & Culture

Hypothesis: The particular standard-Hypothesis: The particular standard-setting process in each country is a setting process in each country is a function of the economic, political, and function of the economic, political, and social environment, i.e., the country’s social environment, i.e., the country’s culture and traditions.culture and traditions.• Bloom, Robert and M. A. Naciri. 1989. “Accounting Bloom, Robert and M. A. Naciri. 1989. “Accounting

Standard Setting and Culture: A Comparative Analysis Standard Setting and Culture: A Comparative Analysis of the United States, Canada, England, Germany, of the United States, Canada, England, Germany, Australia, New Zealand, Sweden, Japan, and Australia, New Zealand, Sweden, Japan, and Switzerland,” Switzerland,” The International Journal of The International Journal of Accounting Education and ResearchAccounting Education and Research 24 (1) 70-97. 24 (1) 70-97.

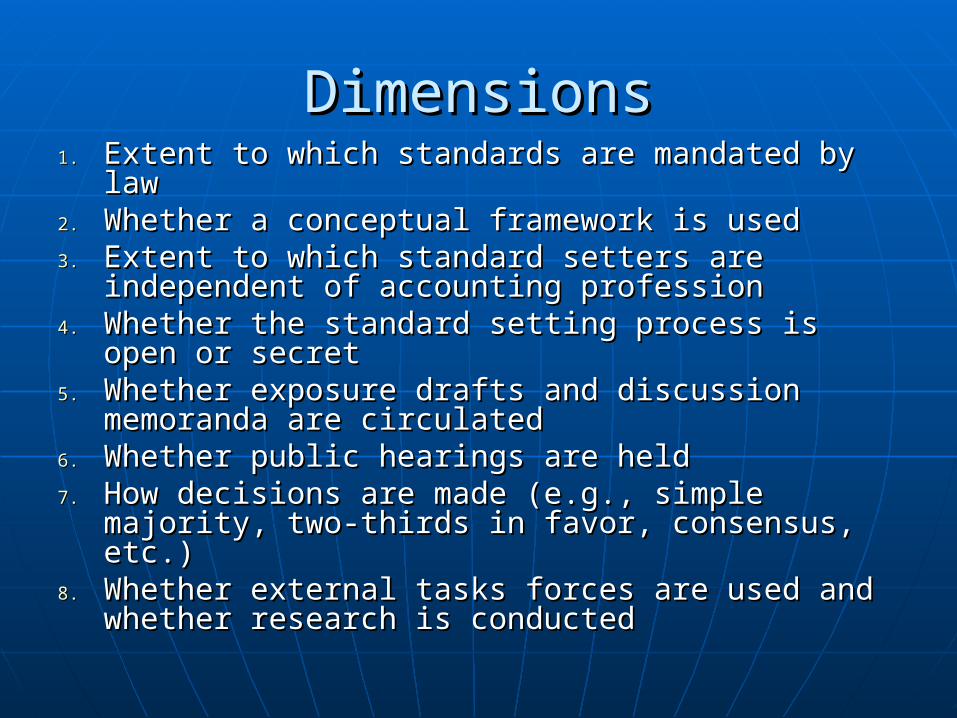

DimensionsDimensions1.1. Extent to which standards are mandated by law Extent to which standards are mandated by law 2.2. Whether a conceptual framework is usedWhether a conceptual framework is used3.3. Extent to which standard setters are Extent to which standard setters are

independent of accounting professionindependent of accounting profession4.4. Whether the standard setting process is open or Whether the standard setting process is open or

secretsecret5.5. Whether exposure drafts and discussion Whether exposure drafts and discussion

memoranda are circulatedmemoranda are circulated6.6. Whether public hearings are heldWhether public hearings are held7.7. How decisions are made (e.g., simple majority, How decisions are made (e.g., simple majority,

two-thirds in favor, consensus, etc.)two-thirds in favor, consensus, etc.)8.8. Whether external tasks forces are used and Whether external tasks forces are used and

whether research is conductedwhether research is conducted

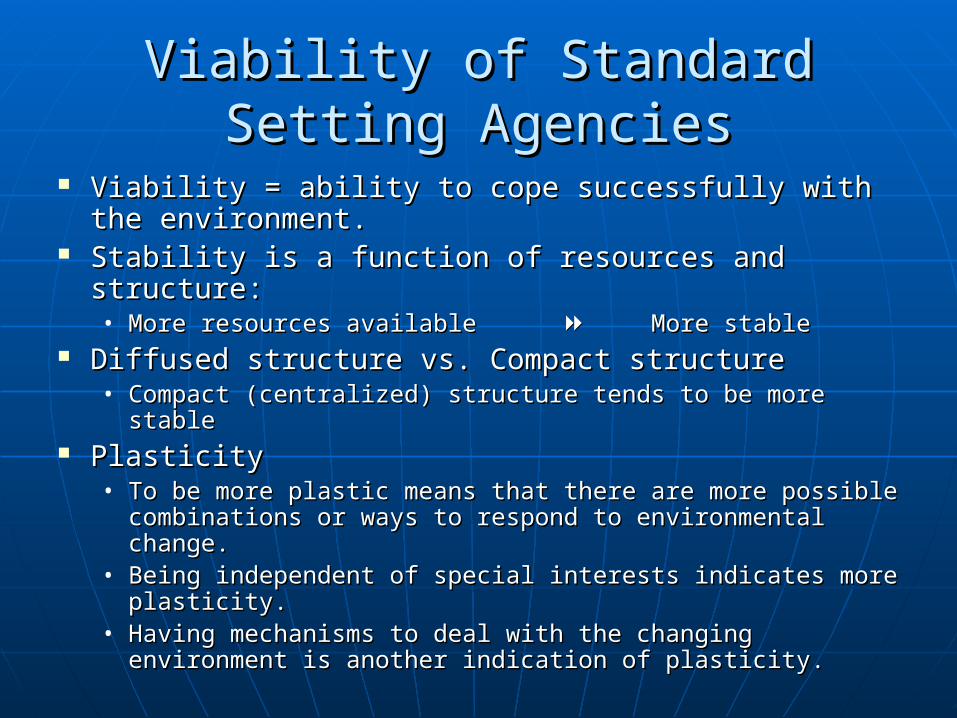

Viability of Standard Setting Viability of Standard Setting AgenciesAgencies

Viability = ability to cope successfully with the Viability = ability to cope successfully with the environment. environment.

Stability is a function of resources and structure:Stability is a function of resources and structure:• More resources available More resources available More stableMore stable

Diffused structure vs. Compact structureDiffused structure vs. Compact structure• Compact (centralized) structure tends to be more stableCompact (centralized) structure tends to be more stable

PlasticityPlasticity• To be more plastic means that there are more possible To be more plastic means that there are more possible

combinations or ways to respond to environmental combinations or ways to respond to environmental change. change.

• Being independent of special interests indicates more Being independent of special interests indicates more plasticity. plasticity.

• Having mechanisms to deal with the changing Having mechanisms to deal with the changing environment is another indication of plasticity.environment is another indication of plasticity.

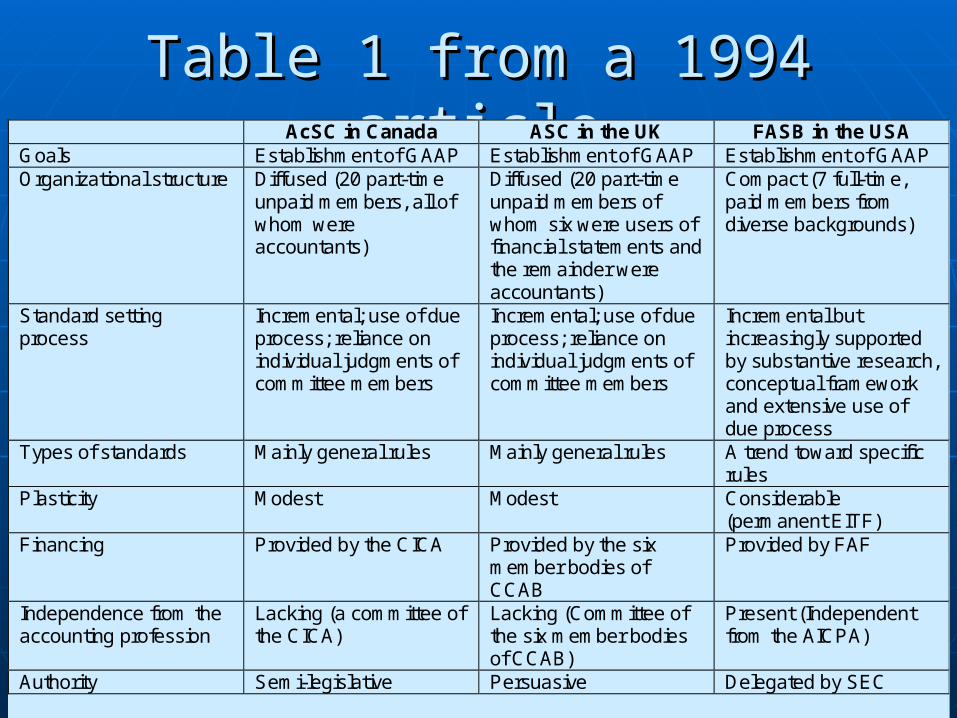

Table 1 from a 1994 articleTable 1 from a 1994 article AcSC in Canada ASC in the UK FASB in the USA

Goals Establishment of GAAP Establishment of GAAP Establishment of GAAP Organizational structure Diffused (20 part-time

unpaid members, all of whom were accountants)

Diffused (20 part-time unpaid members of whom six were users of financial statements and the remainder were accountants)

Compact (7 full-time, paid members from diverse backgrounds)

Standard setting process

Incremental; use of due process; reliance on individual judgments of committee members

Incremental; use of due process; reliance on individual judgments of committee members

Incremental but increasingly supported by substantive research, conceptual framework and extensive use of due process

Types of standards Mainly general rules Mainly general rules A trend toward specific rules

Plasticity Modest Modest Considerable (permanent EITF)

Financing Provided by the CICA Provided by the six member bodies of CCAB

Provided by FAF

Independence from the accounting profession

Lacking (a committee of the CICA)

Lacking (Committee of the six member bodies of CCAB)

Present (Independent from the AICPA)

Authority Semi-legislative Persuasive Delegated by SEC

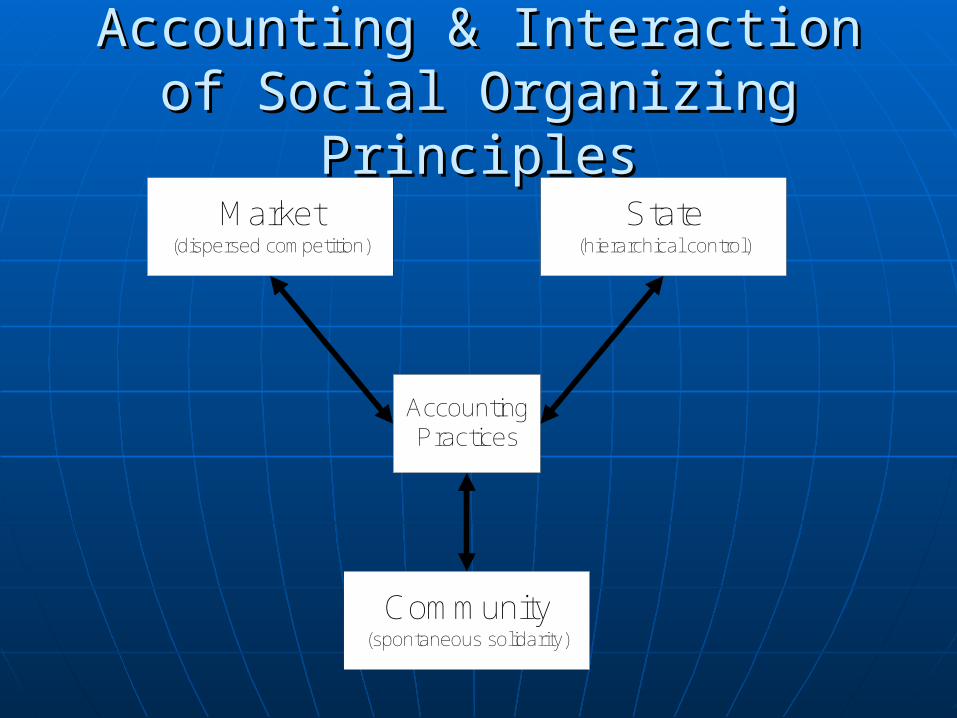

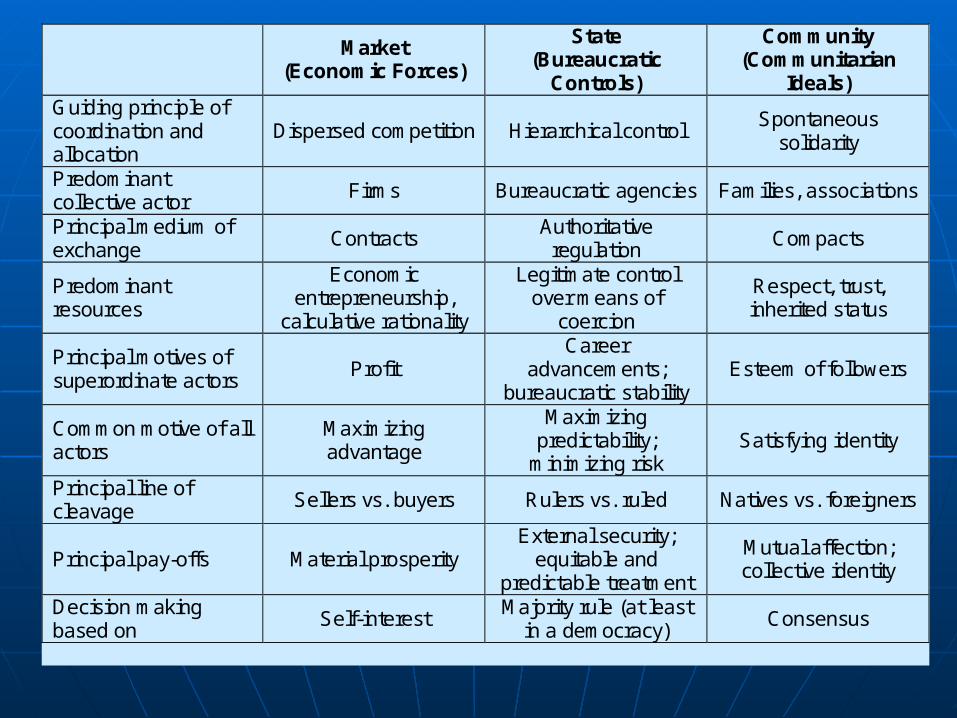

Accounting & Interaction of Social Accounting & Interaction of Social Organizing PrinciplesOrganizing Principles

Market(dispersed competition)

State(hierarchical control)

Accounting Practices

Community(spontaneous solidarity)

Accounting and the interaction of social organizing principles

Market

(Economic Forces)

State (Bureaucratic

Controls)

Community (Communitarian

Ideals) Guiding principle of coordination and allocation

Dispersed competition Hierarchical control Spontaneous

solidarity

Predominant collective actor

Firms Bureaucratic agencies Families, associations

Principal medium of exchange

Contracts Authoritative

regulation Compacts

Predominant resources

Economic entrepreneurship,

calculative rationality

Legitimate control over means of

coercion

Respect, trust, inherited status

Principal motives of superordinate actors

Profit Career

advancements; bureaucratic stability

Esteem of followers

Common motive of all actors

Maximizing advantage

Maximizing predictability;

minimizing risk Satisfying identity

Principal line of cleavage

Sellers vs. buyers Rulers vs. ruled Natives vs. foreigners

Principal pay-offs Material prosperity External security;

equitable and predictable treatment

Mutual affection; collective identity

Decision making based on

Self-interest Majority rule (at least

in a democracy) Consensus

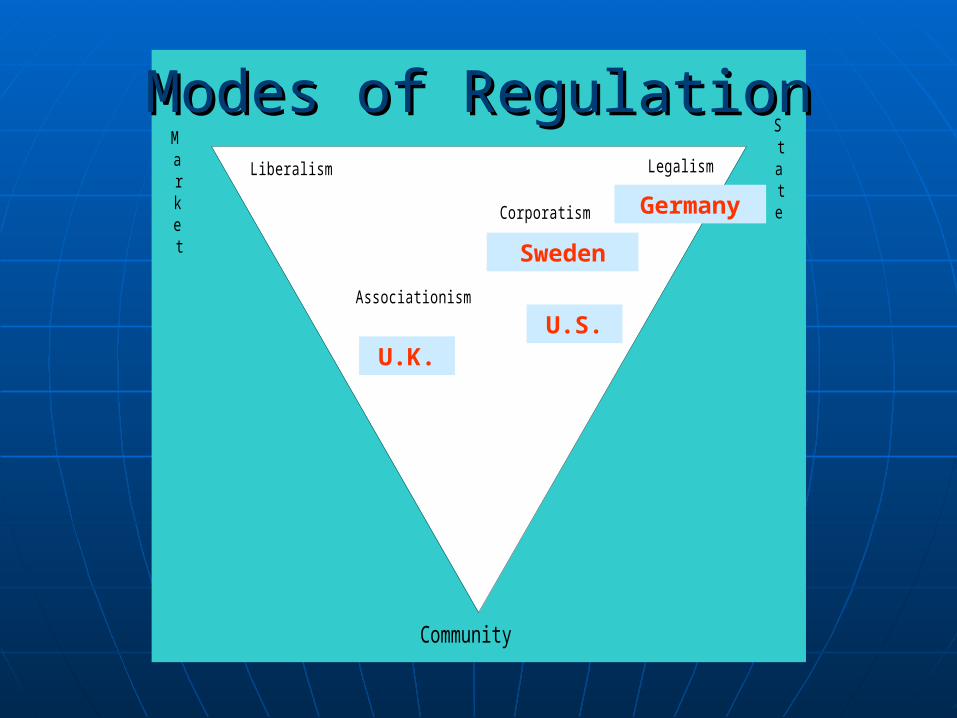

Modes of RegulationModes of Regulation

LiberalismLiberalism

LegalismLegalism

AssociationismAssociationism

CorporatismCorporatism

Community

Market

State

Liberalism Legalism

Corporatism

Associationism

Modes of RegulationModes of Regulation

Germany

Sweden

U.S.U.K.