accounting financial instruments pp t

DESCRIPTION

AccountingTRANSCRIPT

Business Unit

Accounting for Financial InstrumentsInstrumentsIAS 39 current issues and IFRS 9 update9 update

Strictly Private and Confidential

29 October 2013

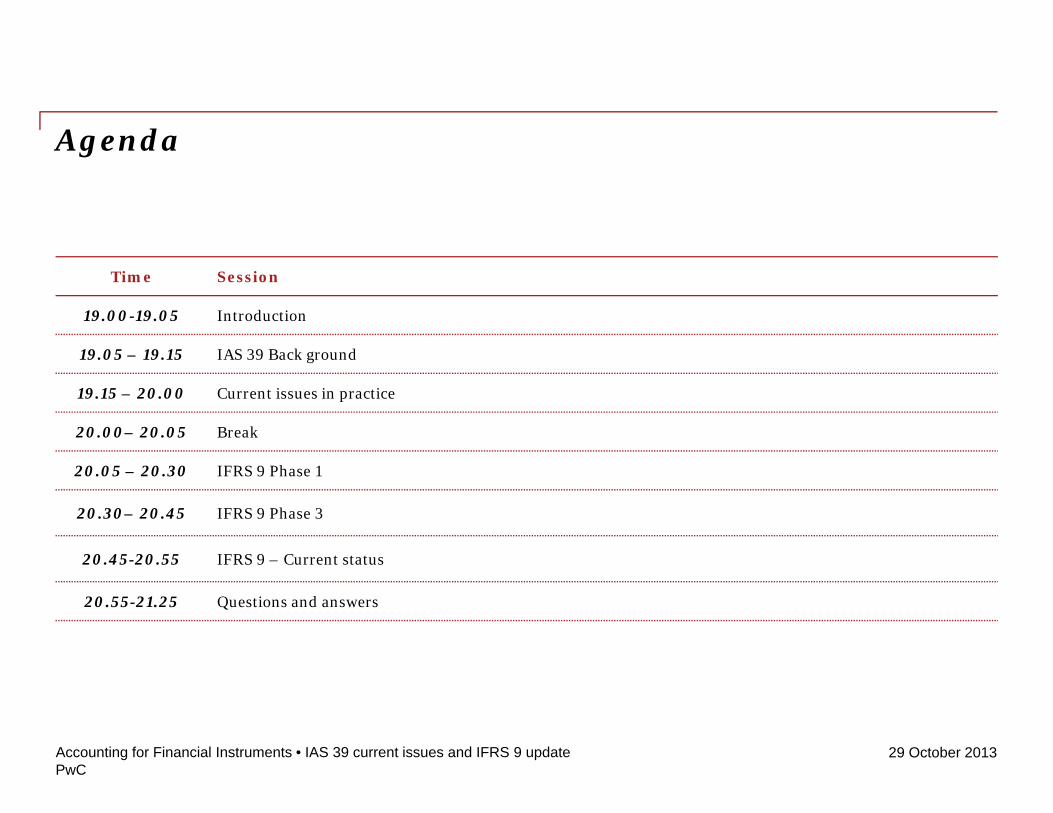

Agenda

Time Session

19.00-19.05 Introduction

19.05 – 19.15 IAS 39 Back ground

19.15 – 20.00 Current issues in practice

20.00– 20.05 Break

20.05 – 20.30 IFRS 9 Phase 1

IFRS Ph20.30– 20.45 IFRS 9 Phase 3

20.45-20.55 IFRS 9 – Current status

20.55-21.25 Questions and answers

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

Your speaker todaySection 1Your speaker today

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

1

Section 1 – Your speaker today

Zulfiqar UnarSection 1 Your speaker today

Zulfiqar Unar is a Senior Manager in PWC Dubai’s Capital Markets Accounting Advisory Services (CMAAS)responsible for provision of accounting advisory services focusing on complex financial instruments and ontreasury financial instrument. Zulfiqar has over thirteen years of experience in providing assurance and advisory

i t fi i l i t i i j i di ti i A i Af i E d th Middl E tservices to financial services sector in various jurisdictions in Asia, Africa, Europe and the Middle East.

Zulfiqar trained as an accountant with PWC Karachi specialising in the financial services sector. After more thanfour years with PWC he joined Deloitte in London in its Banking and Capital Markets group where he specialisedand lead the provision of assurance and advisory services to treasury departments of tier 1 banks and investmentb k i L d Z lfi h i i f i i i f i d hbanks in London. Zulfiqar has extensive experience of reviewing various types of treasury instruments and howthey are used for risk management and capital management purposes.

After leaving Deloitte, Zulfiqar accepted an accounting policy role with the banking regulator in London, theFinancial Services Authority (FSA), where he spent the next three years in a role aimed at identifying risks tofi i l i fi d b h f fi i l i d d l i ff i i li ifinancial services firms posed by the use of financial instruments and developing effective accounting policies tomitigate identified risks. Zulfiqar also played a key part in negotiating in the EU the FSA’s policy positions on BaselIII regulatory capital requirements for banks. As part of this role Zulfiqar advised the regulatory capital policyteam on the effects of the use of complex debt and equity instruments on regulatory capital held by banks.

In his last role, at BDO in London, Zulfiqar led the firm’s financial services accounting advisory team and was thetechnical accounting lead for the financial services group.

Zulfiqar is a fellow member of the Association of Chartered Certified Accountants, United Kingdom.

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

2

IAS 39 BackgroundSection 2IAS 39 Background

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

3

Section 2 – IAS 39 Background

IAS 39 BackgroundSection 2 IAS 39 Background

Initially issued in I999 IAS 39 h b i d

In the wake of the financial crises in 2007/08 came under criticism for:

has been revised several times since its issuance and

• A very complex framework of accounting leading to inconsistent application.Complex

framework

issuance and remains one of the most complex

• Various options under IAS 39 mean that comparability between companies is not easy.

Too much optionality

complex standards in the IFRS literature to apply in

• In the case of loan loss provisioning does not provide the right solution.Too little too

late

pp ypractice. • Accounting outcomes can seem to be

disconnected with the business activities.Not reflective of

business activities

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

4

Accounting for Financial Section 3Accounting for Financial Instruments under IAS 39

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

5

Section 3 – Accounting for Financial Instruments under IAS 39

IAS 39- Current issues in practiceSection 3 Accounting for Financial Instruments under IAS 39

• As the IASB develops the new frameworkfor financial instruments accounting,companies across the middle east continuet f h ll i th li ti f IAS

Delays in IFRS 9 project mean

to face challenges in the application of IAS39.

• Delays and uncertainties in the IFRS 9

that IAS 39 will continue to dominate

d f th project mean that IAS 39 will continue todominate financial reporting agenda for thenext 3-4 years.

agenda for the next few years.

• Next few slides will discuss some of thecomplex areas of accounting under IAS 39which a number of companies in themarket have faced and are likely to arise inthe future.

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

6

Section 3 – Accounting for Financial Instruments under IAS 39

Current issues in practiceSection 3 Accounting for Financial Instruments under IAS 39

In recent time we have seen a consistent theme in the type of issues that clients are facing in the application of IAS 39. The ones that most recur include:

A P i l id iArea Potential considerationsRefinancing of existing arrangements

Companies are looking to refinance existing expensive sources of financing which leads to consideration of de-recognition and hedge accounting related issues.

Hedge accounting Hedge continues to present challenges in the application of its requirements. A number of companies are keen to explore new opportunities under IFRS 9.

Available for sale instruments

Differences in impairment (and its reversal) and test and for debt and equity i t t f i i ti A b f li t ki b d instruments instruments cause confusion in practice. A number of clients making border line decisions on AFS impairment.

Embedded derivatives Not always very clearly identified in contractual arrangements.

Fair value under IFRS 13 Companies are now required to calculate CVA/DVA under IFRS 13.

Debt/equity classification Although quite a rule based area of IAS 32, we can seen a recurring theme in preparers misunderstandingthe requirements of IAS 32.

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

7

p p g q

Section 3 – Accounting for Financial Instruments under IAS 39

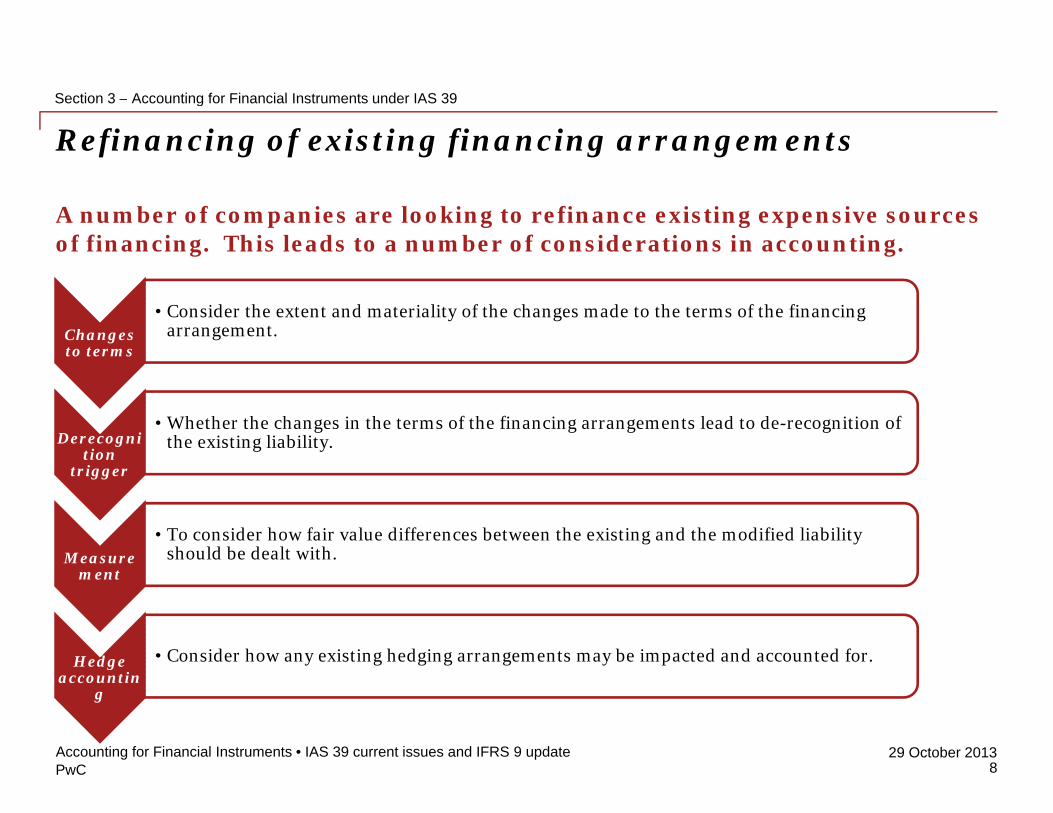

Refinancing of existing financing arrangementsSection 3 Accounting for Financial Instruments under IAS 39

A number of companies are looking to refinance existing expensive sources of financing. This leads to a number of considerations in accounting.

C id h d i li f h h d h f h fi i Changes to terms

• Consider the extent and materiality of the changes made to the terms of the financing arrangement.

Derecognition

trigger

• Whether the changes in the terms of the financing arrangements lead to de-recognition of the existing liability.

Measurement

• To consider how fair value differences between the existing and the modified liability should be dealt with.

Hedge accountin

g

• Consider how any existing hedging arrangements may be impacted and accounted for.

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

8

Section 3 – Accounting for Financial Instruments under IAS 39

Refinancing of existing financing arrangementsSection 3 Accounting for Financial Instruments under IAS 39

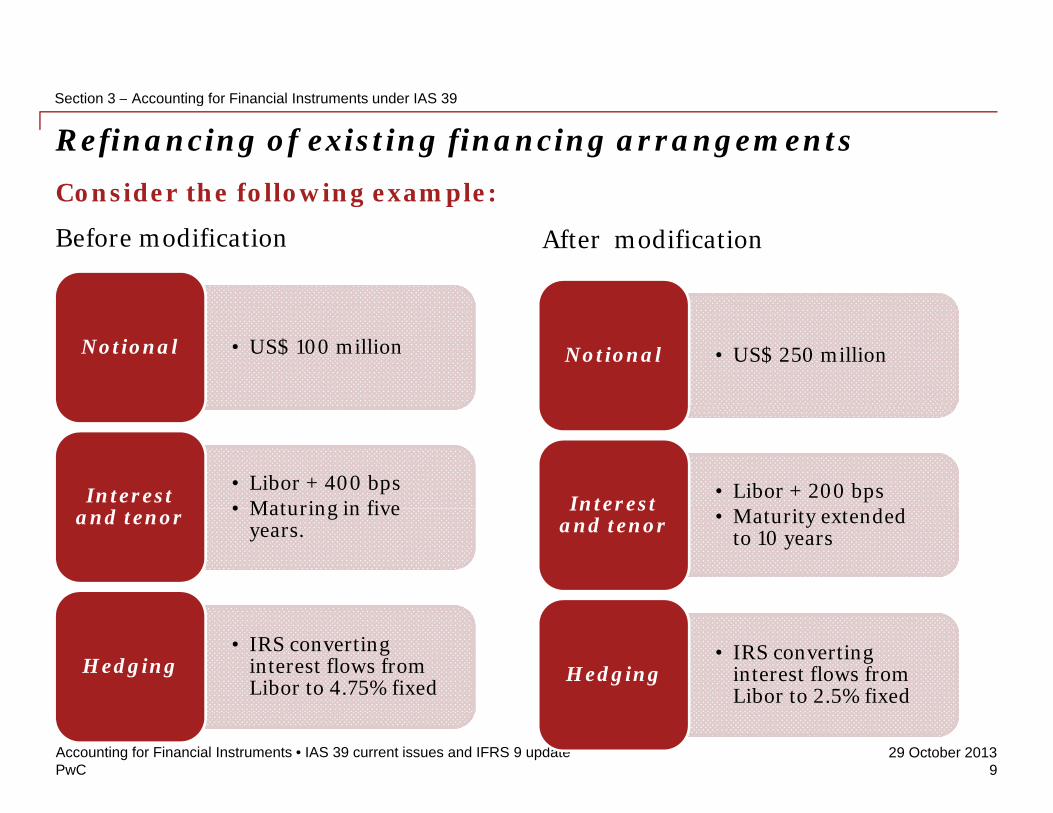

Consider the following example:g p

Before modification After modification

• US$ 100 million Notional • US$ 250 million Notional

• Libor + 400 bps• Maturing in five Interest

d• Libor + 200 bps

M i d d Interest • Maturing in five years.and tenor • Maturity extended

to 10 years

Interest and tenor

• IRS converting interest flows from Libor to 4.75% fixed

Hedging • IRS converting interest flows from Libor to 2.5% fixed

Hedging

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

9

Section 3 – Accounting for Financial Instruments under IAS 39

Refinancing of existing financing arrangementsSection 3 Accounting for Financial Instruments under IAS 39

Questions that arise?

• What is the nature of changes to the terms. Are they reflective of a modification in the

Changes to terms

What is the nature of changes to the terms. Are they reflective of a modification in the terms of an exchange?

• Has the liability been legally released?

• Do the changes result in the liability becoming derecognised and a new one being

Derecognition

trigger

Do the changes result in the liability becoming derecognised and a new one being recognised.

• Typically a 10% differences in the carrying value of the existing liability and the fair value of the new liability would indicate that old liability should be derecognised.

Measurement

• At what amount should the liability should be recorded whether the 10% test is met or not.

Hedge accountin

g

• Whether the existing hedging arrangements can continue or not depend on the nature of the changes and also on how the hedge was designated.

• If the hedged item is derecognised generally difficult to avoid P&L impact.

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

10

Section 3 – Accounting for Financial Instruments under IAS 39

Hedge AccountingSection 3 Accounting for Financial Instruments under IAS 39

Hedge accounting continues to be a very challenging area of accounting. The main issues we have seen in the hedge accounting space relate to:

H d ff iHedge effectiveness• Tendency not to treat this as very important.

Documentary requirements• Lack of understanding of the importance of having the right documentation (hedge designation/

hedge accounting policy)

New innovative products• A number of institutions are coming up with innovative products that may not always achieve

hedge accounting or may not be good risk management tools.

Complex macro hedging strategiesL k f id i thi k h d ti h ll i t l • Lack of guidance in this area makes hedge accounting very challenging to apply.

Quality of advice• We have seen a number of companies receive not very good quality advice relating to hedge

accounting providing short term short cuts but storing long term problems

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

11

accounting providing short term short cuts but storing long term problems.

Section 3 – Accounting for Financial Instruments under IAS 39

Available for Sale instrumentsSection 3 Accounting for Financial Instruments under IAS 39

Accounting for AFS instruments has always presented challenges for preparers.

• To recap- AFS is a residual classification category under IAS 39 and items falling into this category are recorded at fair value with fair value movements falling into this category are recorded at fair value with fair value movements being recorded in other comprehensive income.

• Accumulated fair value movements will only be recorded in profit and loss when there is impairment or security is sold leading to cliff edge effects on when there is impairment or security is sold leading to cliff edge effects on profitability.

• AFS classification is available for both debt and equity instruments however h b f diff i h h i i di d hthere are a number of differences in the their accounting, as discussed on the

next slides, that can lead to inconsistent answers.

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

12

Section 3 – Accounting for Financial Instruments under IAS 39

Difference in AFS Debt and EquitySection 3 Accounting for Financial Instruments under IAS 39

AFS- Debt AFS Equity

• Objective evidence of impairment required

Impairment• Significant OR

prolonged decline in fair value

Impairment

• Subjective assessment based

il blBasis of

impairment

• Significant OR prolonged decline is

t t hi h h Basis of

i i on available evidence

impairment test a test, which when

met, impairment should recorded.

impairment test

• Can reverse through profit and loss.

Reversal of impairment • Can only reverse

through OCI.Reversal of impairment

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

13

Section 3 – Accounting for Financial Instruments under IAS 39

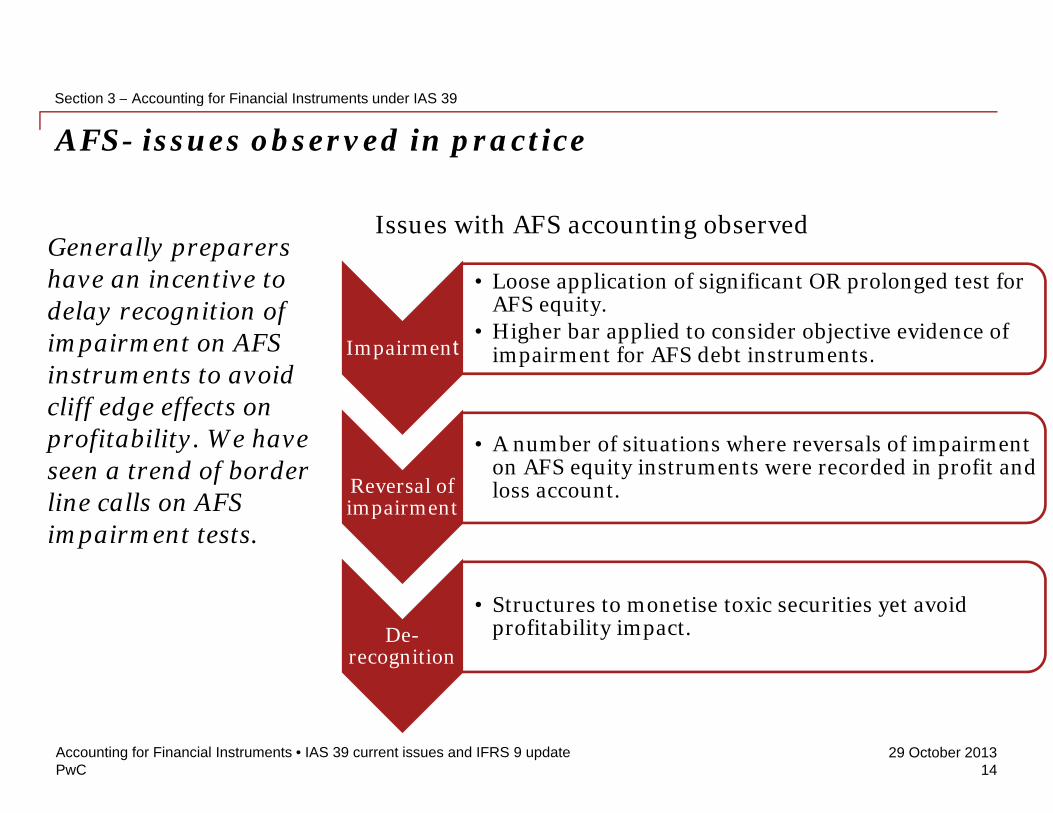

AFS- issues observed in practiceSection 3 Accounting for Financial Instruments under IAS 39

Generally preparers have an incentive to d l iti f

Issues with AFS accounting observed

• Loose application of significant OR prolonged test for AFS equitydelay recognition of

impairment on AFS instruments to avoid cliff edge effects on

Impairment

AFS equity.• Higher bar applied to consider objective evidence of

impairment for AFS debt instruments.

cliff edge effects on profitability. We have seen a trend of border line calls on AFS

Reversal of impairment

• A number of situations where reversals of impairment on AFS equity instruments were recorded in profit and loss account.line calls on AFS

impairment tests. impairment

• Structures to monetise toxic securities yet avoid De-

recognition

Structures to monetise toxic securities yet avoid profitability impact.

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

14

Section 3 – Accounting for Financial Instruments under IAS 39

Is FVOCI different from AFS?

A hi h l l i f d bt i t t ( i il iti )

Section 3 Accounting for Financial Instruments under IAS 39

A high-level comparison for debt instruments (similarities)

Available for sale (IAS 39) FV-OCI (IFRS 9)

Balance sheet

• Fair value + transaction costs • Fair value + transaction costs

Profit or loss

• Effective interest• Impairment losses• FX gains and losses

• Effective interest• Impairment losses• FX gains and lossesFX gains and losses

• Recycle amount from OCI upon derecognition

FX gains and losses• Recycle amount from OCI upon de-

recognition (except for FVOCI for Equity securities)

OCI • All other fair value changes • All other fair value changes

PwC29 October 2013

17

Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update15

Section 3 – Accounting for Financial Instruments under IAS 39

Is FVOCI different from AFS? (continued)Section 3 Accounting for Financial Instruments under IAS 39

Available for sale (IAS 39) FV-OCI (IFRS 9)

A high-level comparison for debt instruments (differences)

Impairment • Acquisition cost less- Current fair value less

Previous impairment losses

• Same as amortised cost- Based on expected credit losses

- Previous impairment losses

Residual category

Yes No- Business model test- SPPI test

PwC29 October 2013

18

Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update16

Section 3 – Accounting for Financial Instruments under IAS 39

If t id tifi d ti l b i b dd d d i ti h

Embedded DerivativesSection 3 Accounting for Financial Instruments under IAS 39

If not identified on a timely basis embedded derivatives can have a material impact on the cash flows of a contract. • Under IAS 39, derivatives embedded in host contracts are required to be separated

d d f d l d i i l h l l l d and accounted for as standalone derivatives so long as they are not closely related to the host contract.

• Based on the anecdotal evidence seen by us we have noticed two major trends in l ti t ti f b dd d d i ti relation to accounting for embedded derivatives:

ion

of

ativ

es We have seen a number of examples where entities were not able to identify ti

on o

f at

ives Lack of understanding of

when an embedded derivative requires

Iden

tific

atdd

ed d

eriv

a were not able to identify derivatives in seemingly simple debt contracts.

A detailed assessment of

Sepa

rat

dded

der

iva derivative requires

separation.

Lack of detailed guidance around “close relation” to I

embe

d A detailed assessment of terms of the contract not carried out.

embe

d around close relation to the host contract also a contributor.

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

17

Section 3 – Accounting for Financial Instruments under IAS 39

Embedded DerivativesSection 3 Accounting for Financial Instruments under IAS 39

A detailed review of the terms of key contracts

th t

• Although the concept of closely related has not historically been a difficult one to apply in

ti h d t l id th can ensure that any hidden embedded derivatives are identified on a timely basis

practice however, per anecdotal evidence, the ever increasing complexity in financial instruments can make application of such a test a challenge This is particularly relevant since on a timely basis. challenge. This is particularly relevant since complex financial instruments may expose entities to more than one risk.

We recommend that entities should seek independent accounting advice inrelation to the identification, separation and accounting for embeddedderivatives.

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

18

Section 3 – Accounting for Financial Instruments under IAS 39

Fair value under IFRS 13Section 3 Accounting for Financial Instruments under IAS 39

Calculation of Credit Valuation Adjustment (CVA)/ Debit Valuation Adjustment (DVA) is required under IFRS 13 effective 1 Jan 2013.

• IAS 39 did not require the calculation of CVA/DVA beyond requiring that the fair value of an instrument should reflect the credit quality of the instrumentfair value of an instrument should reflect the credit quality of the instrument.

• Due to this a number of companies are in the process of developing methodologies and tools to calculate CVA and DVA.

F B l II li f th i ti d l b l d t i • For Basel II compliers some of the existing models can be leveraged to arrive at a CVA calculation method, however companies will need to develop new accounting policies and procedures , for example, where to get data from etc.

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

19

Section 3 – Accounting for Financial Instruments under IAS 39

Debt vs. Equity classificationSection 3 Accounting for Financial Instruments under IAS 39

We have seen a trend whereby the terms of shares have been changedleading to re-consideration of the classification as debt/equity

• The Debt/Equity classification rules are contained within IAS 32 which is generally arule based standard and one where not a lot of issues in practice have been reported.

• Recently however we have seen some transactions where the terms attaching to theordinary shares were modified triggering a different classification than the one usedordinary shares were modified triggering a different classification than the one usedprior to the modification.

The ke consideration hen assessing hether an instrument is a equit instrument is• The key consideration when assessing whether an instrument is a equity instrument isto assess whether the issuer has the unconditional ability to avoid making paymentsunder the terms.

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

20

Section 3 – Accounting for Financial Instruments under IAS 39

Key take away messageSection 3 Accounting for Financial Instruments under IAS 39

• A lot of these issues represent topical issues and ones which we see recur at a number of our clients.

• As the reporting season nears companies should assess whether they are exposed to these or other financial instruments related risk exposed to these or other financial instruments related risk.

• If issues are material we recommend getting independent financial advice.

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

21

IFRS 9 Phase 1 refresherSection 4IFRS 9 Phase 1 refresher

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

22

Section 4 – IFRS 9 Phase 1 refresher

Objectives of IFRS9 Phase 1Section 4 IFRS 9 Phase 1 refresher

With the role of accounting under the

tli ht ft th

• Intention was to design a simpler model that reflected the objectives of the business

Simpler framework

spotlight after the global financial crises the IASB commenced work to develop a

business

• Reclassification between categories allowed only under restricted Limitation on

l ifi iwork to develop a new financial instrument accounting standard

ycircumstancesreclassification

• Fewer and simpler options based on the b i f h ldi th t R d d accounting standard

to replace IAS39.business purpose of holding the assets as opposed to the intention of holding the individual asset.

Reduced optionality

• Convergence with FASB was initially an • Convergence with FASB was initially an objective behind the development of the new standard

Convergence with FASB

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

23

Section 4 – IFRS 9 Phase 1 refresher

Timeline for codification of IFRS9 Phase 1Section 4 IFRS 9 Phase 1 refresher

Financial Assets

• IFRS 9 Classification and Measurement requirements for financial assets published in November 2009. O

riAssets

Financial • IFRS9 Classification and Measurement requirements for financial liabilities published in

October 2010.

igin

al p

ubl

Liabilities

Early

• Available for early adoption on publication.• November 2011 IASB extended the mandatory adoption date to 2015 and with it the early

d l

lication

Early Adoption adoption timeline.

• In November 2011 IASB decided to make limited amendments to IFRS9 phase 1 and bli h d ED i D b

Mod

ifi

Amend-ments

published an ED in December 2012.

fication

s

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

24

Key changesSection 4.1Key changes

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

25

Section 4 1 – Key changes

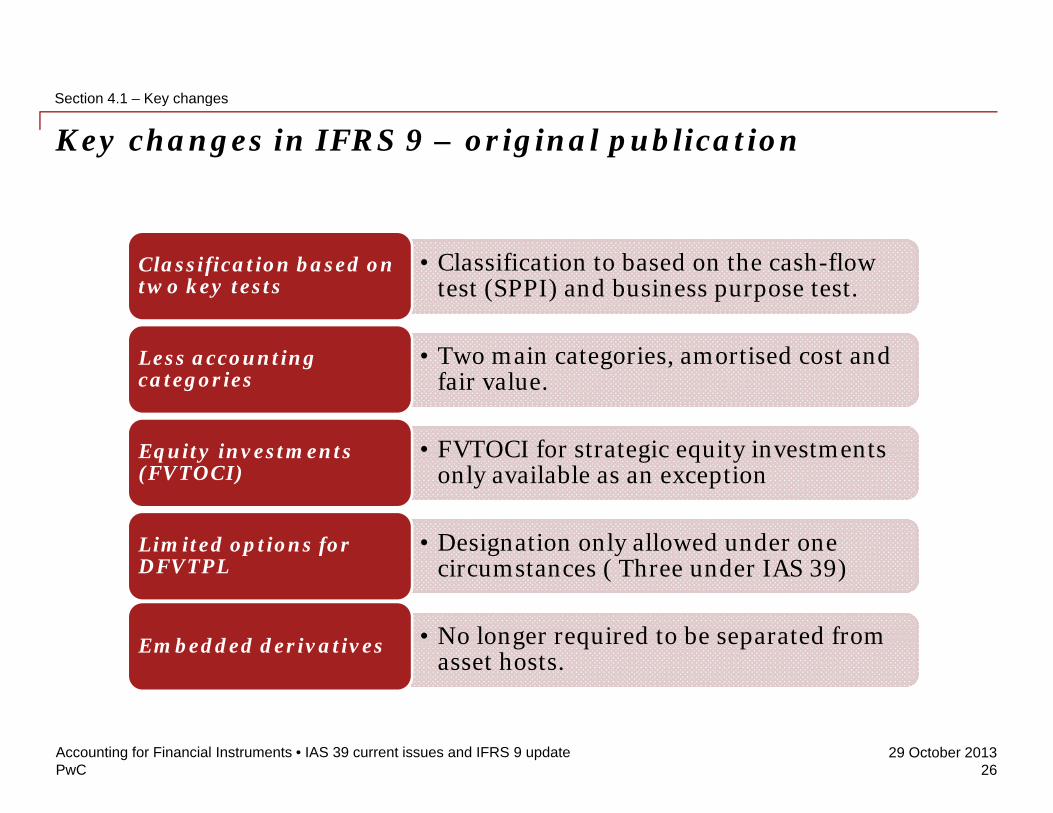

Key changes in IFRS 9 – original publicationSection 4.1 Key changes

• Classification to based on the cash-flow test (SPPI) and business purpose test.

Classification based on two key tests

• Two main categories, amortised cost and fair value.

Less accounting categories

• FVTOCI for strategic equity investments only available as an exception

Equity investments (FVTOCI)

• Designation only allowed under one circumstances ( Three under IAS 39)

Limited options for DFVTPL

• No longer required to be separated from asset hosts.

Embedded derivatives

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

26

Section 4 1 – Key changes

Contractual Cash Flow CharacteristicsSection 4.1 Key changes

Assess the characteristics of the contractual cash flows

h h h flWhat can the cash flows represent?

OK NOT OKOK

Principal Leverage / multiples

Interest on principal outstanding Non-financial variables

Time value of money Conversion features

Credit risk Prepayment option

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

27

Section 4 1 – Key changes

Business purpose test for classification under IFRS9Section 4.1 Key changes

Amortised costBusiness model

Contractual cash flow h i i

Business modelFVO for

accounting mismatch

FVOCI

Reclassification required if business model changes

characteristics FVOCI

Fair Value ( i i )

All other instruments:• Equities

Equities: OCI

presentation (No impairment)Equities

• Derivatives• Some hybrid contracts

presentation available

(exception)

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

28

Limited ammendmentsSection 4.2Limited ammendments

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

29

Section 4 2 – Limited ammendments

Limited amendments Section 4.2 Limited ammendments

In November 2011 IASB decided to make limited amendments to the existing IFRS 9 classification and measurement model and in December 2012 issued an exposure draft introducing amendments that address:introducing amendments that address:

• Issues related mainly to classification of instrument resulting from th li ti f th h fl d b i bj ti t tSpecific

issuesthe application of the cash flow and business objective test

• This was principally an insurance industry specific issue but also P&L

volatility

• This was principally an insurance industry specific issue, but also echoed with banks and financial institutions

Convergence with

FASB

• To reduce differences between the IASB and FASB classification and measurement model

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

30

Section 4 2 – Limited ammendments

Key proposal in the Limited Amendments to Phase ISection 4.2 Limited ammendments

New Clarification of Own credit Revised

Limited amendments include the following key proposals:

classification category

• FVTOCI for qualifying debt i t t

business model and cash flow test

• IASB provided further guidance on

h t ki d f h

Own credit provisions

• Recording of own credit gain in OCI

ll d t b

transition guidelines

• Revised transition guidance to require

ll h IFRS 9 instruments introduced

• Recycling is allowed, as opposed

what kinds of cash flows would meet the cash flow test

• Clarified further the

was allowed to be early adopted at any point, without early adopting the entire standard

all phases IFRS 9 adopted together once final standard is issued

, ppto FVTOCI for equity instruments

business model test

The comment period for this ED expired at the end of March 2013, with the final standard expected in Q2 2014

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

31

Section 4 2 – Limited ammendments

Business model test after the limited amendmentsSection 4.2 Limited ammendments

Is objective of the entity’s business model to hold the

Is objective of the entity’s business model to collect

NoNo

Proposed category in EDClarified guidance

financial assets to collect contractual cash flows?

contractual cash flows and for sale?

Yes Yes

Do contractual cash flows represent solely payments of principal and interest?

Yes

No

YesFair

value through

Does the company apply the fair value option to eliminate an accounting mismatch?

No No

Yes

through P&L

No No

Amortised costFair value through other comprehensive income

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

32

IFRS9 Phase 1 - comparison with Section 4.3IFRS9 Phase 1 - comparison with IAS39

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

33

Section 4 3 – IFRS9 Phase 1 - comparison with IAS39

Classification categoriesSection 4.3 IFRS9 Phase 1 comparison with IAS39

IAS 39 Accounting categories IFRS 9 Accounting categories

l h• Held to maturity• Loans and

receivable

Amortised cost

• Contractual cash flows SPPI and business model hold to collect

Amortised cost

• Held for tradingFair value ( )

• Residual category, if i d

Fair value ( )• Fair value option(PL) not amortised cost(PL)

• Limited option for • Available for sale -

Debt• Available for sale-

Equity

Fair value (OCI)

• Limited option for strategic equity investments

• OCI for debt instrument [Limited

Fair value (OCI)

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

34

amendment]

Section 4 3 – IFRS9 Phase 1 - comparison with IAS39

Other things to considerSection 4.3 IFRS9 Phase 1 comparison with IAS39

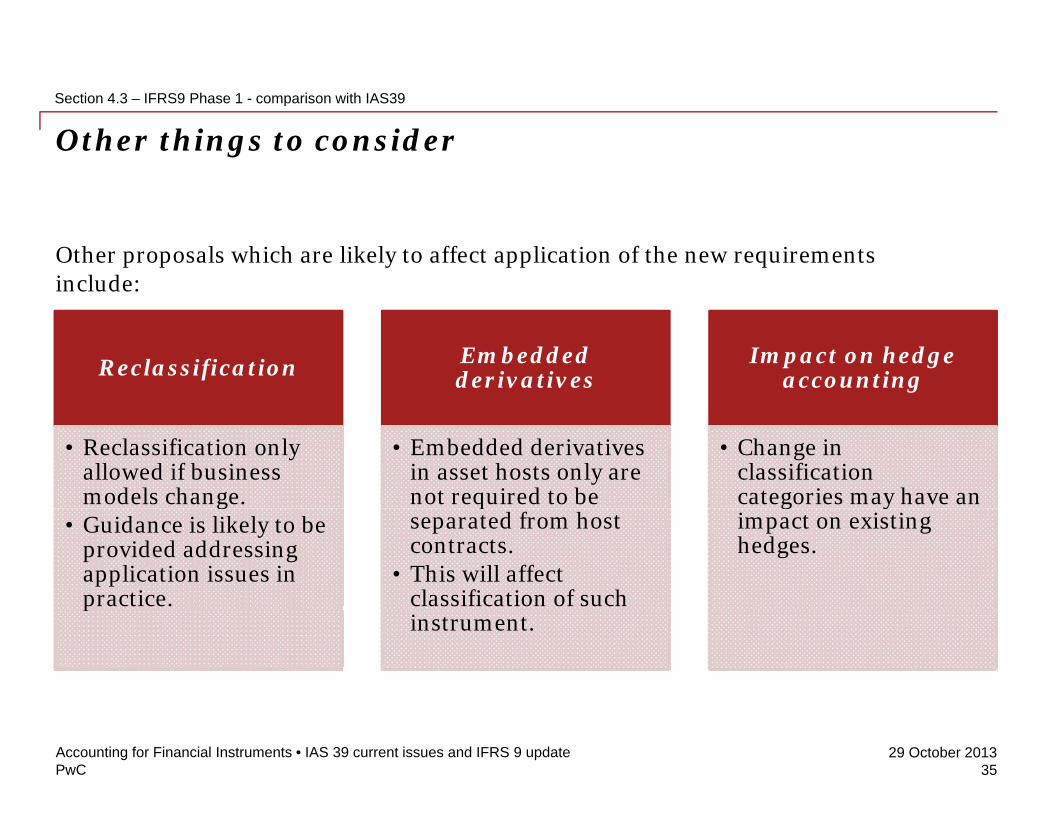

Other proposals which are likely to affect application of the new requirements include:

Reclassification Embedded derivatives

Impact on hedge accounting

• Reclassification only allowed if business models change.

• Embedded derivatives in asset hosts only are not required to be

• Change in classification categories may have an g

• Guidance is likely to be provided addressing application issues in practice.

qseparated from host contracts.

• This will affect classification of such

g yimpact on existing hedges.

pinstrument.

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

35

Financial liabilities under IFRS9Section 4.4Financial liabilities under IFRS9

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

36

Section 4 4 – Financial liabilities under IFRS9

Financial liabilitiesSection 4.4 Financial liabilities under IFRS9

Based on feedback received from constituents, IASB considered that the IAS 39 classification and measurement model for financial liabilities worked well in

tipractice.

• Therefore the rules on classification and measurement of financial liabilities • Therefore the rules on classification and measurement of financial liabilities have been carried forward from IAS 39 almost unchanged, with one exception.

• That exception relates to the recording of own credit gain in OCI, as opposed to the profit and loss account, as required in IAS 39.

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

37

IFRS 9 Phase 3 refresherSection 4.5IFRS 9 Phase 3 refresher

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

38

Section 4 5 – IFRS 9 Phase 3 refresher

Background to IFRS 9 Phase 3 – Hedge AccountingSection 4.5 IFRS 9 Phase 3 refresher

The existing accounting standard dealing with accounting for financialinstruments, International Accounting Standard 39, was criticised for beinginstruments, International Accounting Standard 39, was criticised for beingtoo complex and lacking transparency.

1 After the crises in 2007/08 role of accounting for financial instrumentscame under the spotlightcame under the spotlight.

2 As a result G20 asked FASB and IASB to redevelop financial instrumentaccounting standards.

IFRS i IASB’ j t t l IAS It lit i t th h3

IFRS 9 is IASB’s project to replace IAS 39. It was split into three phases.Recognition and Measurement (Phase 1), Impairment (Phase 2) andHedge Accounting (Phase 3).

4 Mandatory adoption timeline of IFRS 9, initially driven by G20, was/ /4 1/1/2013.

5 However due to delays in the project, it has been pushed further out to1/1/2015.

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

39

Background to IFRS9 Phase 3Section 4.6Background to IFRS9 Phase 3

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

40

Section 4 6 – Background to IFRS9 Phase 3

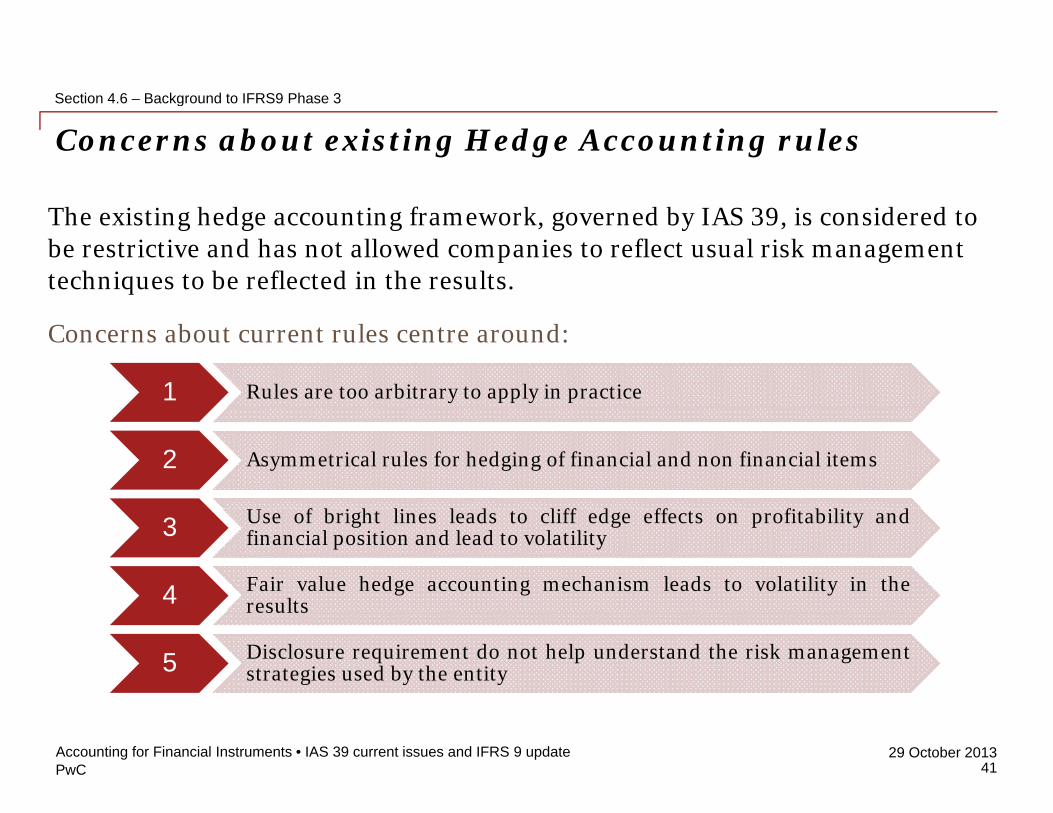

Concerns about existing Hedge Accounting rulesSection 4.6 Background to IFRS9 Phase 3

The existing hedge accounting framework, governed by IAS 39, is considered to be restrictive and has not allowed companies to reflect usual risk management techniques to be reflected in the results.

Concerns about current rules centre around:

1 Rules are too arbitrary to apply in practice

2 Asymmetrical rules for hedging of financial and non financial items

U f b i h li l d liff d ff fi bili d3 Use of bright lines leads to cliff edge effects on profitability andfinancial position and lead to volatility

4 Fair value hedge accounting mechanism leads to volatility in theresultsresults

5 Disclosure requirement do not help understand the risk managementstrategies used by the entity

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

41

Section 4 6 – Background to IFRS9 Phase 3

The IASB’s response Section 4.6 Background to IFRS9 Phase 3

In response to the concerns IASB has undertaken a significant project to develop a Hedge Accounting Framework as part of IFRS 9.

The areas to be addressed include:

1 Overall approach

2 Eligibility of hedged items and hedging instruments

3 Hedge effectiveness testing and discontinuation of hedgingrelationshiprelationship

4 Fair value hedge accounting mechanism

The project is being progressed in two stages. The current stage concerns micro hedging with macro hedging to be addressed next

5 Presentation and disclosure

PwC29 October 2013

hedging, with macro hedging to be addressed next.Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

42

IFRS 9 Phase 3 - Key proposalsSection 4.7IFRS 9 Phase 3 - Key proposals

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

43

Section 4 7 – IFRS 9 Phase 3 - Key proposals

The IFRS 9 macro hedging proposalsSection 4.7 IFRS 9 Phase 3 Key proposals

Hedged items

Risk Components Aggregate Exposures

Groups / Net Positions

• Can isolate more types of risk to be

hedged. e.g. commodities’ price

• Can combine derivatives + non-

derivatives as h d d it

•Fewer restrictions on hedging on a group basisp

risk hedged items •Can hedge layers

These proposals aim to ensure that exposures economically hedged i i l hi h d iin practice can also achieve hedge accounting

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

44

Section 4 7 – IFRS 9 Phase 3 - Key proposals

The IFRS 9 macro hedging proposalsSection 4.7 IFRS 9 Phase 3 Key proposals

Hedging InstrumentsHedging Instruments

Non-Derivatives Options & Forwards

• Eligible if at FVTPL also for hedging of interest rate risk

• Can defer changes in time value / forward points in OCI and amortise over hedgeamortise over hedge

These proposals aim to ensure that instruments used for risk management can also achieve effective hedge accounting

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

45

Section 4 7 – IFRS 9 Phase 3 - Key proposals

Hedge EffectivenessSection 4.7 IFRS 9 Phase 3 Key proposals

Rules on hedge effectiveness are likely to be relaxed ensuring hedge relationships can continue even if the level of offset is not perfect. This is likely to help entities avoid recording severe consequences of failing hedge

Eligible Relationships

likely to help entities avoid recording severe consequences of failing hedge effectiveness hedge effectiveness testing

Economic Relationship

“Less arbitrary –Not a looser or

- Much less prescriptive; no 80-125% test; - Criteria are qualitative not quantitative; Not a looser or

higher hurdle”q q ;

- Must be “balanced”;- Must still measure + report ineffectiveness

Hedge effectiveness testing will only be prospective and driven by risk management strategy

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

46

Section 4 7 – IFRS 9 Phase 3 - Key proposals

Other itemsSection 4.7 IFRS 9 Phase 3 Key proposals

• Link established between risk management objectives and hedge accounting

Link between hedge accounting and risk

management

IAS t i ti b t h d i b i lik l t b • IAS 39 restriction about hedging on group basis are likely to be relaxed, aiming to ensure hat more groups of items can qualify for hedge accounting.

Hedging of groups of items

• Hedging of net positions is now allowed, helping to reduce costs and represent more accurately the commonly applies risk Hedging of net positionsmanagement strategy

• De-designation only allowed in case of a change in risk management objectives.

Voluntary de-designation not allowed

• Fair value mechanism is likely to change such that the “noise” recorded in the profit and loss will be reduced.

Mechanism for fair value hedging

• Equity instruments at FVTOCI will not achieve fair value hedgingHedging of equity instruments at FVTOCI

• Enhanced disclosures to help provide more meaningful information to the users of the financial statements about the hedging applied by entities.

Disclosures

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

47

Reaction to the Phase 3 proposalsSection 4.8Reaction to the Phase 3 proposals

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

48

Section 4 8 – Reaction to the Phase 3 proposals

Reaction to the IASB proposalsSection 4.8 Reaction to the Phase 3 proposals

The reaction has been:

Generally positive

Agreement that the New rules providesignificant opportunities for:

More flexible framework

Key issues likely to be addressed

More hedging on group and

net basisHedging of

layers means

However there is a view more couldhave been done to address: No mandatory

de-designationHedging of risk

components

Complexity in application

Voluntary de designation

de-designation components

Voluntary de-designation

Guidance on areas of judgment

Potential for imperfect hedging

Derivatives can be hedged items

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

49

Section 4 8 – Reaction to the Phase 3 proposals

Timetable to implement and future note on hedge accounting

Section 4.8 Reaction to the Phase 3 proposals

Implementation timeline: What else to expect:

Q • Expect a fair value option for

hedging of credit risk This is Fair value

ti f Q4 2012 Final draft

issuedMandatory application

hedging of credit risk. This is aimed at addressing concerns raised mainly by banks.

option for hedging of credit risk

Q4 2013 Standard expected

• Macro hedging rules will be issued as a separate standard. Currently the detailed rules are being deliberated with the

Macro hedge

accounting p gaim to issue a discussion paper in Q2 2014.

grules

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

50

Key take awaySection 4.9Key take away

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

51

Section 4 9 – Key take away

What you need to think aboutSection 4.9 Key take away

The expected new rules are likely to present a unique opportunity for entities to hedge more risks and align risk management and accounting.

Existing hedges

• What can be improved

New opportunities

• New risks to be hedged

IFRS 9 adoption

• Adoption impact assessmentimproved

• Documentation• Impact on

hedging of liquidity/

hedged• New hedging

instruments to use

• Hedging credit

assessment• Changes in IFRS

9 Phase impact• Development of

policiesliquidity/ investment portfolio

• Changes in processes and

• Hedging credit risk

• Cost savings for group hedges

• Risk

policies• Dry run leading

up to mandatory adoption

pcontrols

Risk management policies to develop

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

52

IFRS 9 current statusSection 4.10IFRS 9 current status

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

53

Section 4 10 – IFRS 9 current status

IFRS 9 statusSection 4.10 IFRS 9 current status

IFRS 9 Phase IFRS 9 Phase Macro hedge IFRS 9 – Phase I

• Since July IASB has discussed

IFRS 9 – Phase II

• Deliberations on the feedback

IFRS 9 – Phase III

• Drafting of the final text of the

Macro hedge accounting

• IASB is developing its has discussed

feedback to the ED.

• Number of concepts

on the feedback received on the ED are on-going.

• IASB and FASB

final text of the IFRS is underway.

• Target IFRS Q4 2013

developing its approach to address macro hedging

• A discussion concepts clarified.

• Own credit proposal to be included in

• IASB and FASB holding joint sessions on this.

• Some concepts further

2013 • A discussion paper to be issued in Q2 2014

included in IFRS 9 for early adoption

• Target IFRS: Q2 2014

further clarified.

• Target IFRS Q2 2014

Q2 2014

Mandatory adoption date is up for consultation but no decisions have yetb d

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

54

been made.

Section 4 10 – IFRS 9 current status

Questions?Section 4.10 IFRS 9 current status

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

55

Contact

Zulfiqar Unaru qa U aPwCDirect: +971 (0) 4 304 3918 Mobile: +971 (0)566 820 643 E il lfi @Email: [email protected]

PwC29 October 2013Accounting for Financial Instruments • IAS 39 current issues and IFRS 9 update

56

pwc.com/middle-east

PwC firms provide industry-focused assurance, tax and advisory services to enhance value for their clients. More than 161,000 people in 154 countries in firms across the PwC network share their thinking, experience and solutions to develop fresh perspectives and practical advice. See pwc.com for more information.

“PwC” is the brand under which member firms of PricewaterhouseCoopers International Limited (PwCIL) operate and provide services Together PwC is the brand under which member firms of PricewaterhouseCoopers International Limited (PwCIL) operate and provide services. Together, these firms form the PwC network. Each firm in the network is a separate legal entity and does not act as agent of PwCIL or any other member firm. PwCIL does not provide any services to clients. PwCIL is not responsible or liable for the acts or omissions of any of its member firms nor can it control the exercise of their professional judgment or bind them in any way.

P C i h Middl EPwC in the Middle East

Established in the region for over 40 years, PwC has offices in 12 countries: Bahrain, Egypt, Iraq, Jordan, Kuwait, Lebanon, Libya, Oman, Palestine, Qatar, Saudi Arabia and the United Arab Emirates, with around 2,500 people.

Complementing our depth of industry expertise and breadth of skills is our sound knowledge of local business environments across the Middle East.

www.pwc.com/middle-east

© 2013 PricewaterhouseCoopers. All rights reserved.