accounting for current liabilities chapter 9 copyright © 2016 mcgraw-hill education. all rights...

TRANSCRIPT

Accounting for Current LiabilitiesChapter 9

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Wild, Shaw, and ChiappettaFinancial & Managerial Accounting6th Edition

Wild, Shaw, and ChiappettaFinancial & Managerial Accounting6th Edition

09-C1: Defining Liabilities

2

11 - 3

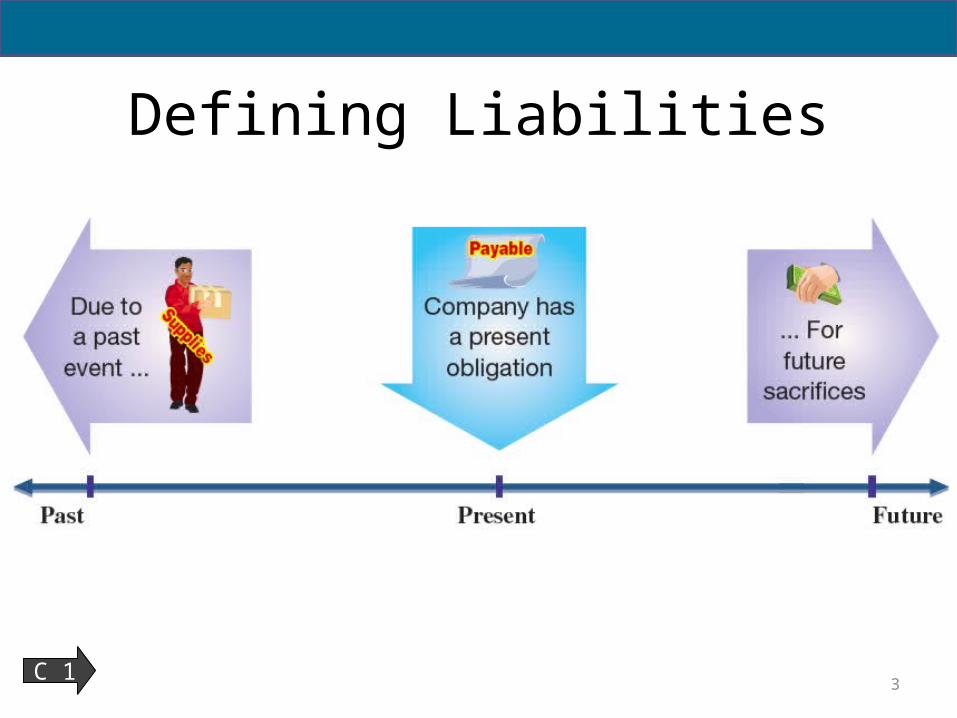

Defining Liabilities

C 13

11 - 4

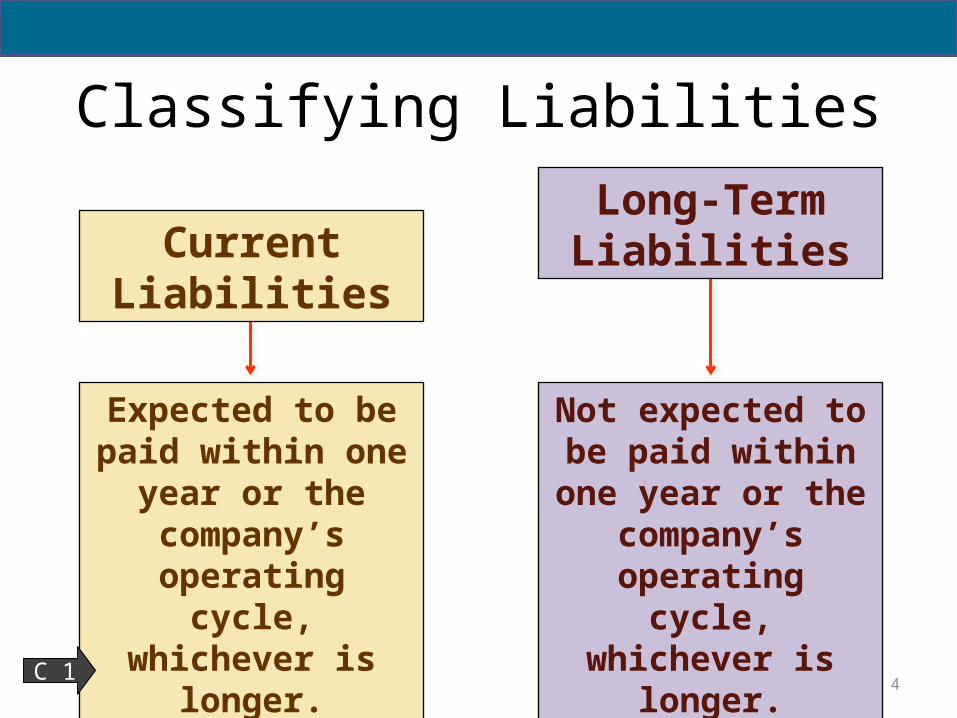

Classifying Liabilities

Expected to be paid within one year or the company’s operating

cycle, whichever is longer.

Current Liabilities

Not expected to be paid within one year

or the company’s operating cycle,

whichever is longer.

Long-Term Liabilities

C 14

11 - 5

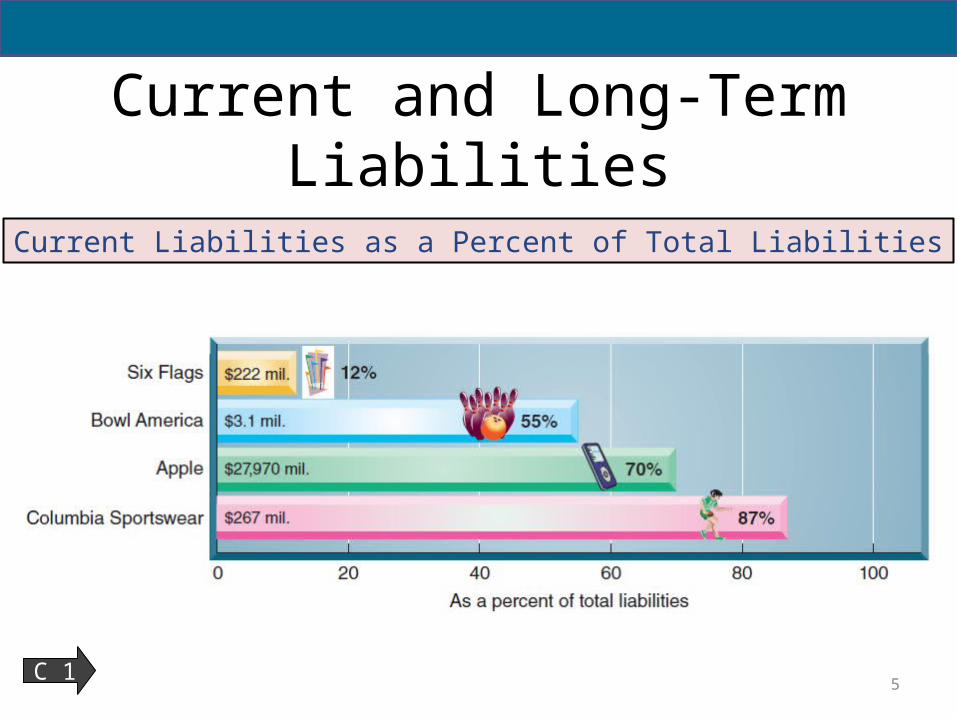

Current and Long-TermLiabilities

Current Liabilities as a Percent of Total Liabilities

C 15

11 - 6

Uncertainty of Liabilities

Uncertainty in When to Pay

C 1

Uncertainty in Whom to Pay

Uncertainty in How Much to Pay

6

09-C2: Known Liabilities

7

11 - 8

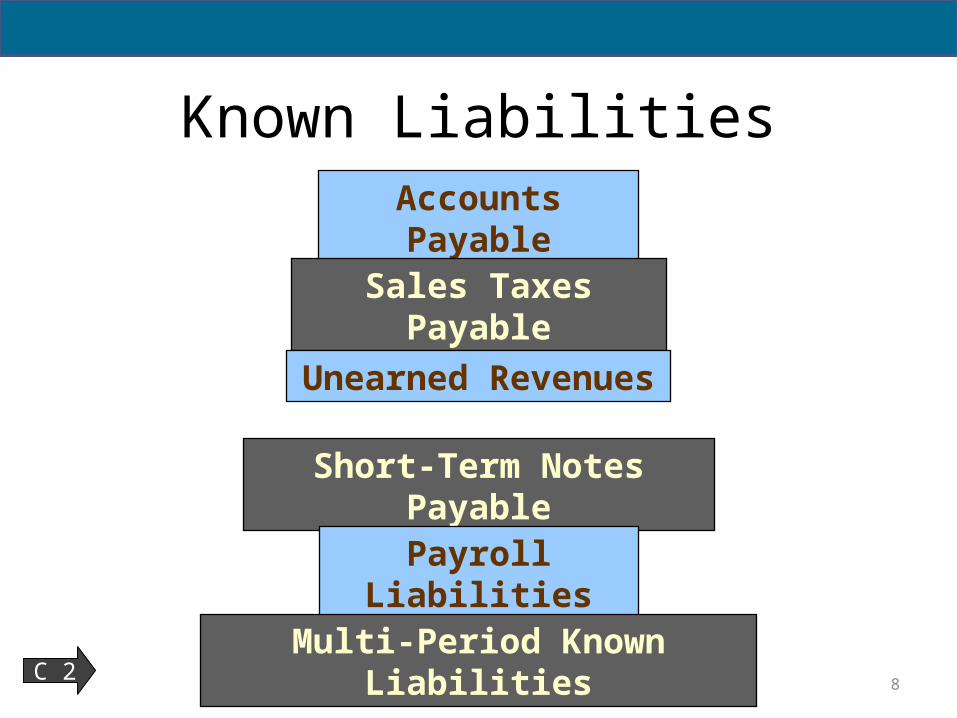

Accounts Payable

Sales Taxes Payable

Unearned Revenues

Short-Term Notes Payable

Known Liabilities

Payroll Liabilities

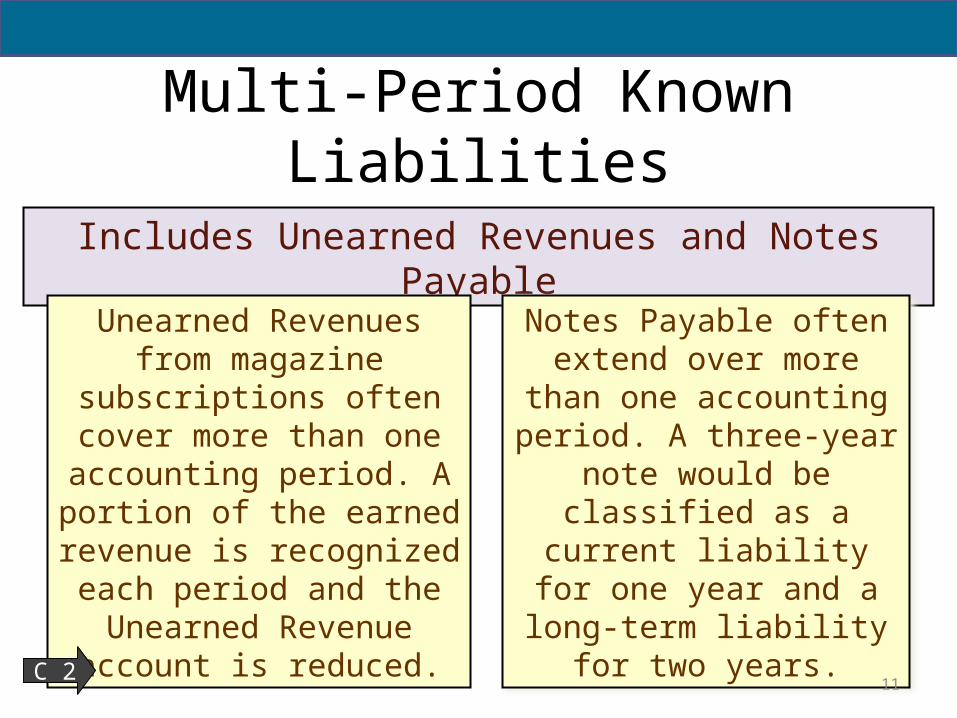

Multi-Period Known LiabilitiesC 2

8

11 - 9

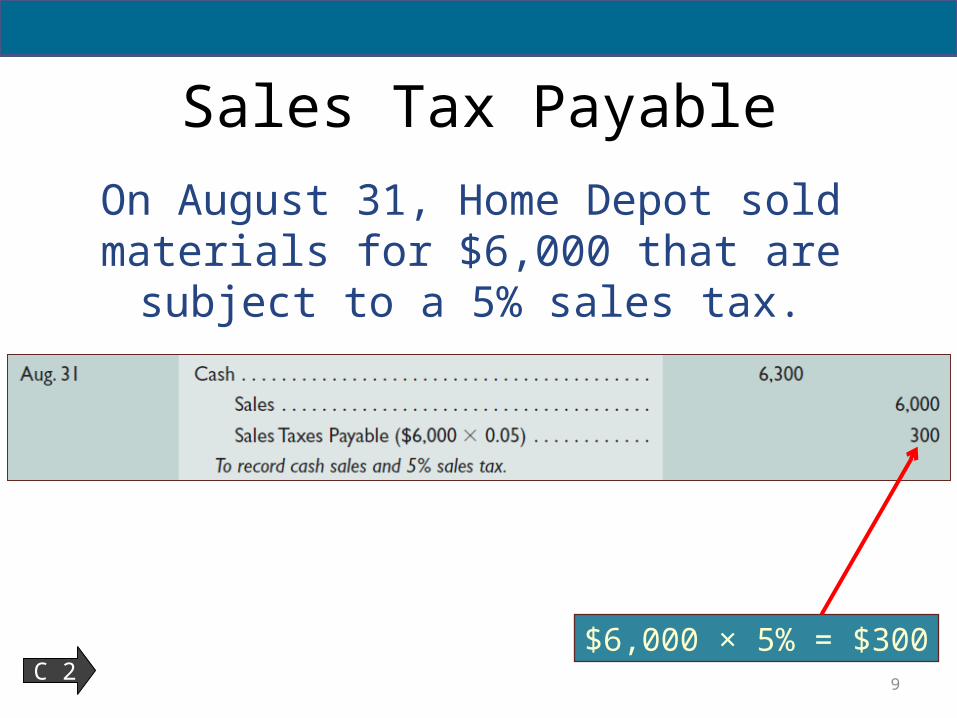

On August 31, Home Depot sold materials for $6,000 that are subject to a 5% sales tax.

Sales Tax Payable

C 2$6,000 × 5% = $300

9

11 - 10

On June 30, Rihanna sells $5,000,000 in tickets for eight concerts.

Unearned Revenues

C 2

On Oct. 31, Rihanna performs a concert.

$5,000,000 / 8 = $625,000 10

11 - 11

Multi-Period KnownLiabilities

Includes Unearned Revenues and Notes Payable

Unearned Revenues from magazine subscriptions

often cover more than one accounting period. A portion

of the earned revenue is recognized each period and

the Unearned Revenue account is reduced.

Notes Payable often extend over more than one accounting period. A three-

year note would be classified as a current

liability for one year and a long-term liability for two

years.

C 211

09-P1: Short-Term Notes Payable

12

11 - 13

A written promise to pay a specified amount on a definite future date within one year or the

company’s operating cycle, whichever is longer.

A written promise to pay a specified amount on a definite future date within one year or the

company’s operating cycle, whichever is longer.

Short-Term Notes Payable

P 113

11 - 14

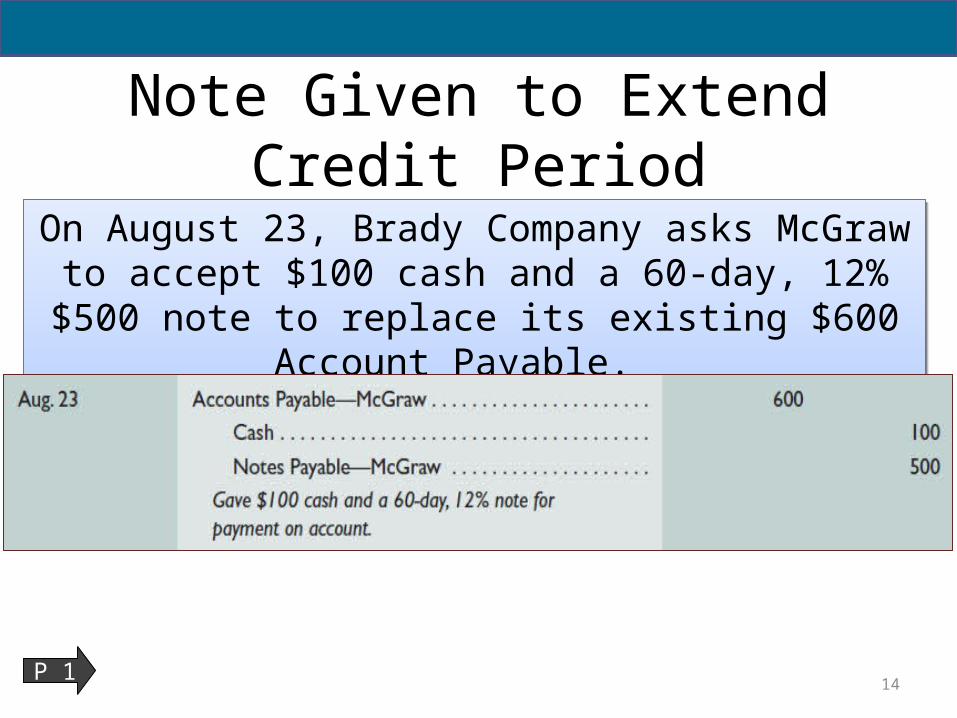

On August 23, Brady Company asks McGraw to accept $100 cash and a 60-day, 12% $500 note to replace its

existing $600 Account Payable.

On August 23, Brady Company asks McGraw to accept $100 cash and a 60-day, 12% $500 note to replace its

existing $600 Account Payable.

Note Given to ExtendCredit Period

P 114

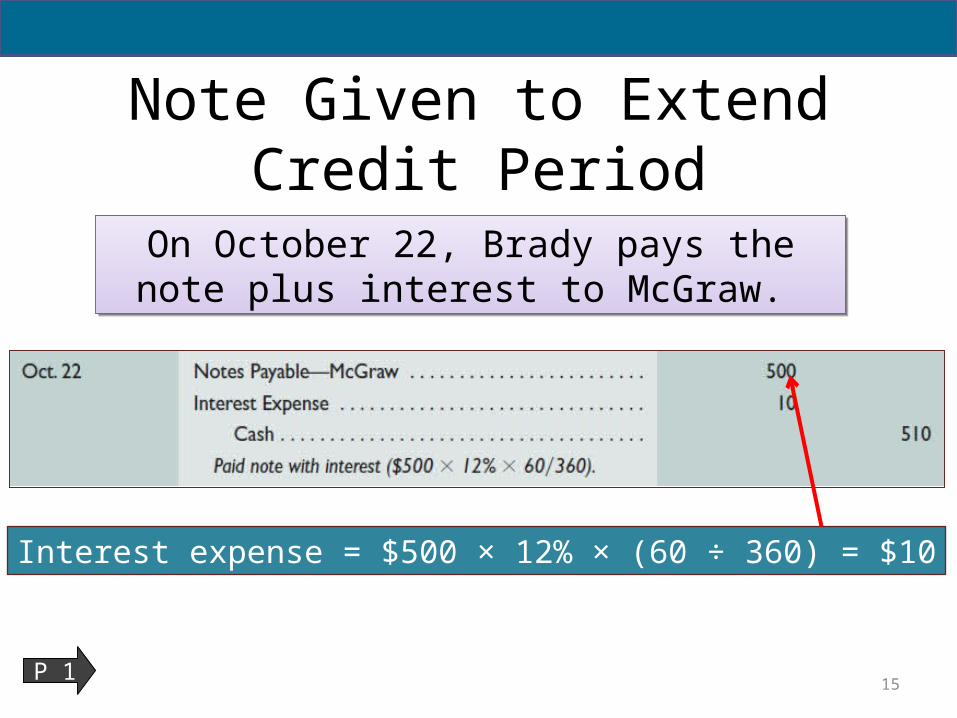

11 - 15

On October 22, Brady pays the note plus interest to McGraw.

On October 22, Brady pays the note plus interest to McGraw.

Note Given to ExtendCredit Period

P 1

Interest expense = $500 × 12% × (60 ÷ 360) = $10

15

11 - 16

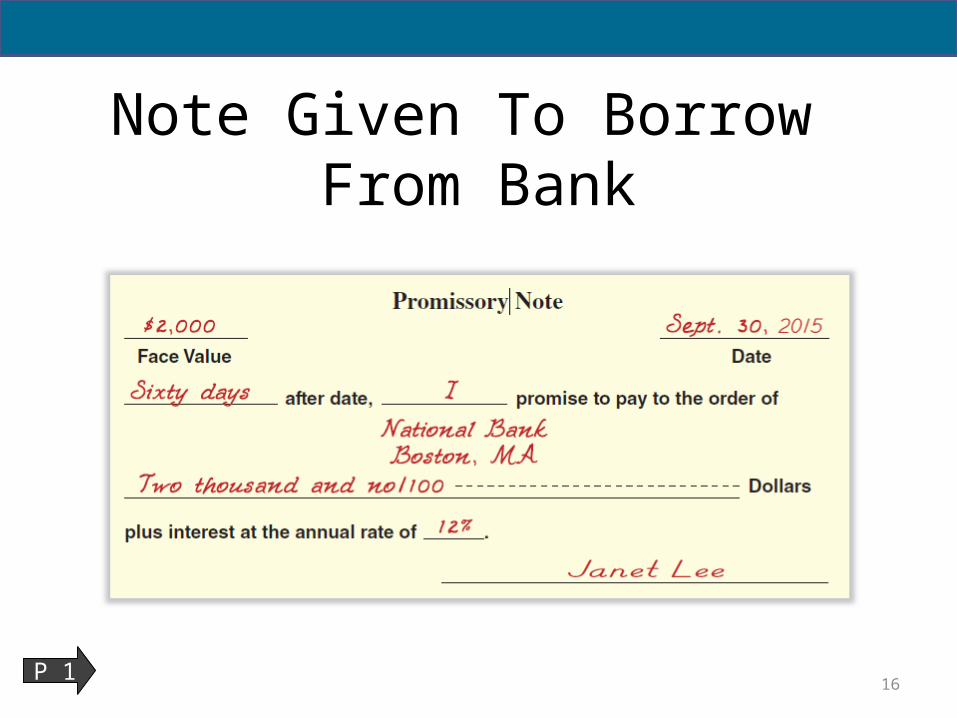

Note Given To Borrow From Bank

P 116

11 - 17

Note Given To Borrow From Bank

On Sept. 30, a company borrows $2,000 from a bank at 12% interest for 60 days.

P 1

On Nov. 29, the company repays the principal of the note plus interest.

Interest expense = $2,000 × 12% × (60 ÷ 360) = $40 17

11 - 18

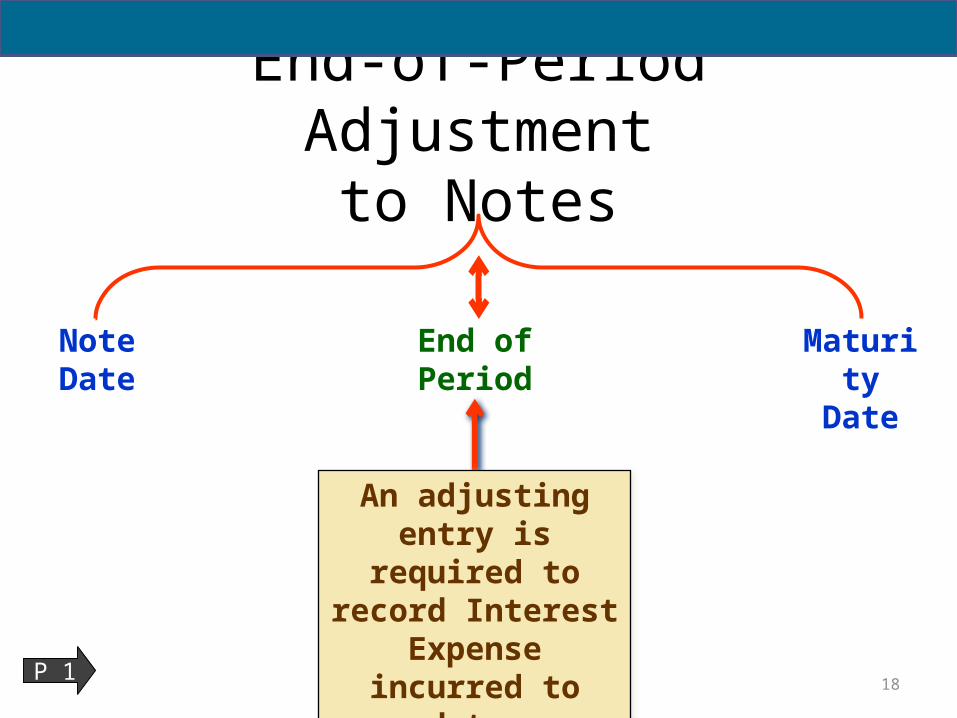

Note Date

End of Period

Maturity Date

An adjusting entry is required to record Interest Expense incurred to date.

End-of-Period Adjustmentto Notes

P 118

11 - 19

End-of-Period Adjustmentto Notes

P 1

On Dec. 16, 2015, a company borrows $2,000 from a bank at 12% interest for 60 days. An adjusting entry is needed on December 31.

On Feb. 14, 2014, the company repays this principal and interest on the note.

19

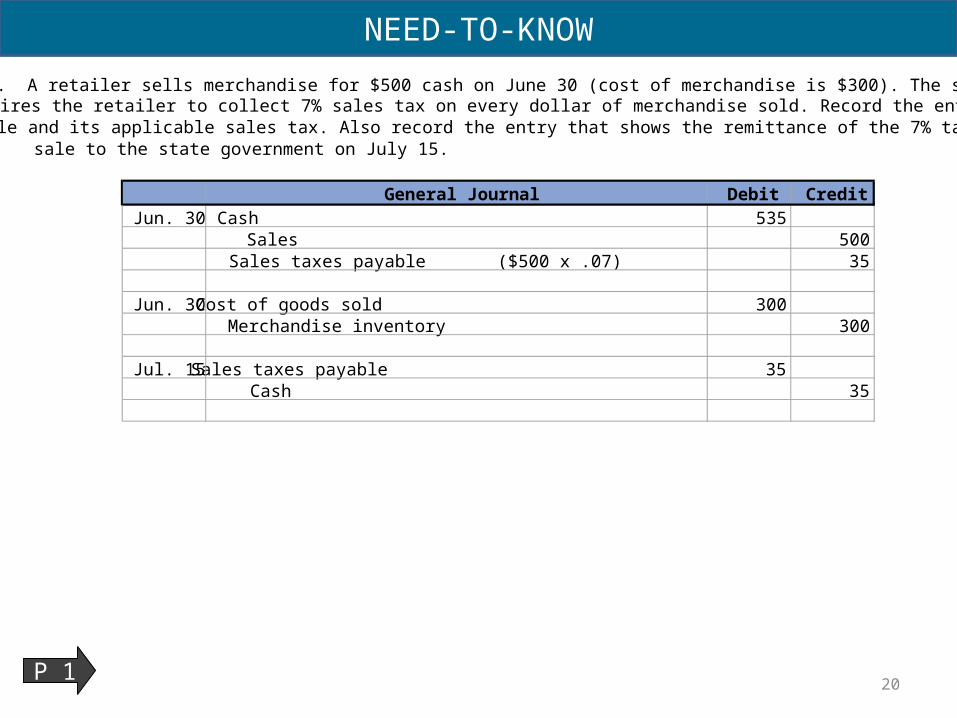

NEED-TO-KNOW

Debit CreditJun. 30 Cash 535

Sales 500Sales taxes payable ($500 x .07) 35

Jun. 30 Cost of goods sold 300Merchandise inventory 300

Jul. 15 Sales taxes payable 35Cash 35

General Journal

Part 1. A retailer sells merchandise for $500 cash on June 30 (cost of merchandise is $300). The sales tax law requires the retailer to collect 7% sales tax on every dollar of merchandise sold. Record the entry for the $500 sale and its applicable sales tax. Also record the entry that shows the remittance of the 7% tax on this sale to the state government on July 15.

P 120

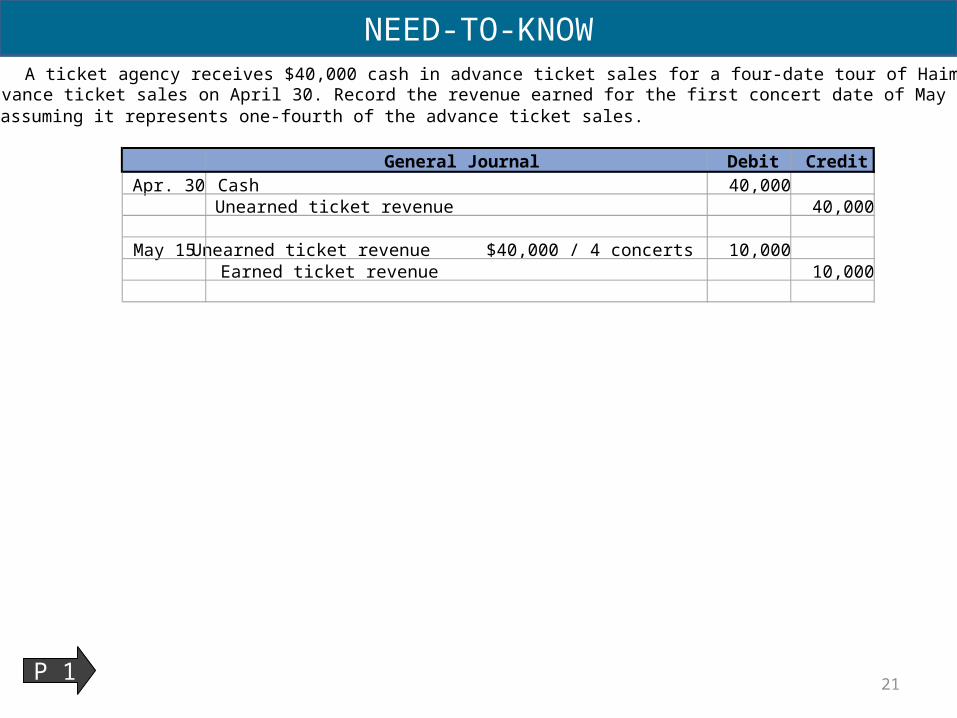

NEED-TO-KNOW

Debit CreditApr. 30 Cash 40,000

Unearned ticket revenue 40,000

May 15 Unearned ticket revenue $40,000 / 4 concerts 10,000Earned ticket revenue 10,000

General Journal

Part 2. A ticket agency receives $40,000 cash in advance ticket sales for a four-date tour of Haim. Record the advance ticket sales on April 30. Record the revenue earned for the first concert date of May 15, assuming it represents one-fourth of the advance ticket sales.

P 121

NEED-TO-KNOW

Debit CreditNov. 25 Cash 8,000

Notes payable 8,000

Dec. 31 Interest expense ($8,000 x .05 x 36/360) 40Interest payable 40

Feb. 23 Interest expense ($8,000 x .05 x 54/360) 60Interest payable ($8,000 x .05 x 36/360) 40Notes payable 8,000

Cash 8,100

Part 3. On November 25 of the current year, a company borrows $8,000 cash by signing a 90-day, 5% note payable with a face value of $8,000. (a) Compute the accrued interest payable on December 31 of the current year, (b) prepare the journal entry to record the accrued interest expense at December 31 of the current year, and (c) prepare the journal entry to record payment of the note at maturity.

General Journal

36 days

54days

P 122

09-P2: Payroll Liabilities

23

11 - 24

Payroll Liabilities

Employers incur expenses andliabilities from having employees.

P 224

11 - 25

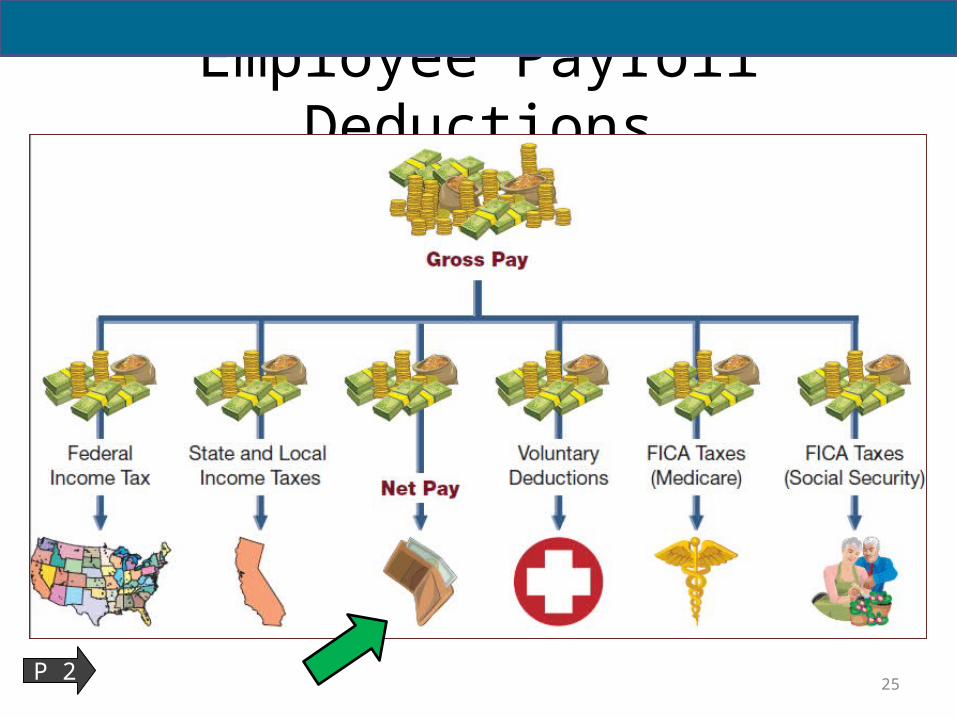

Employee Payroll Deductions

P 225

11 - 26

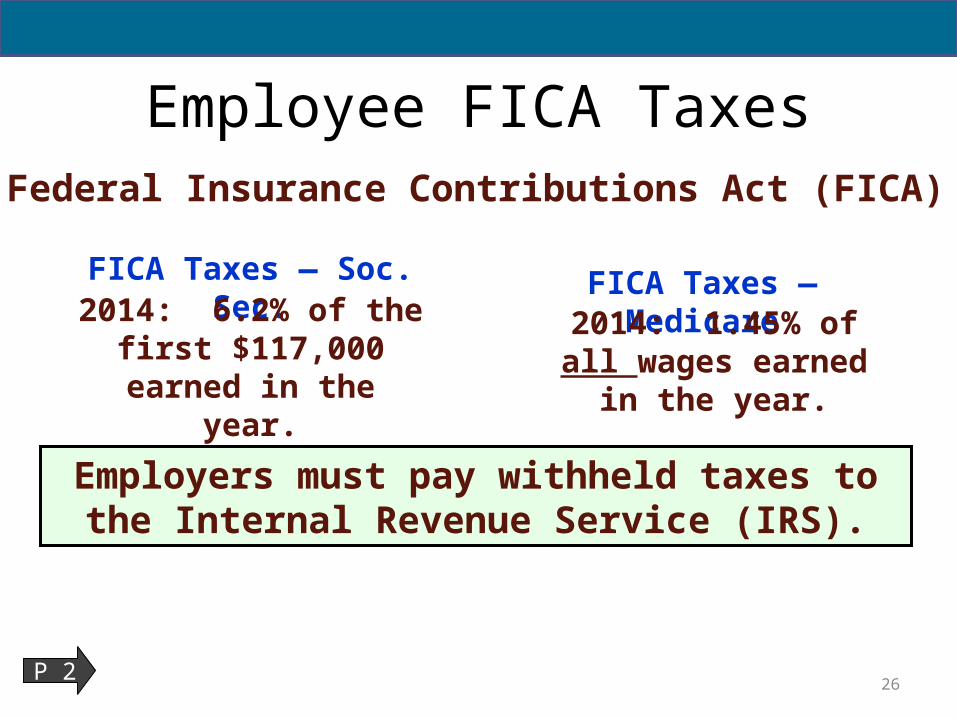

Employers must pay withheld taxes tothe Internal Revenue Service (IRS).

FICA Taxes — Soc. Sec.2014: 6.2% of the first $117,000 earned in the

year.

Employee FICA TaxesFederal Insurance Contributions Act (FICA)

FICA Taxes — Medicare2014: 1.45% of all

wages earned in the year.

P 226

11 - 27

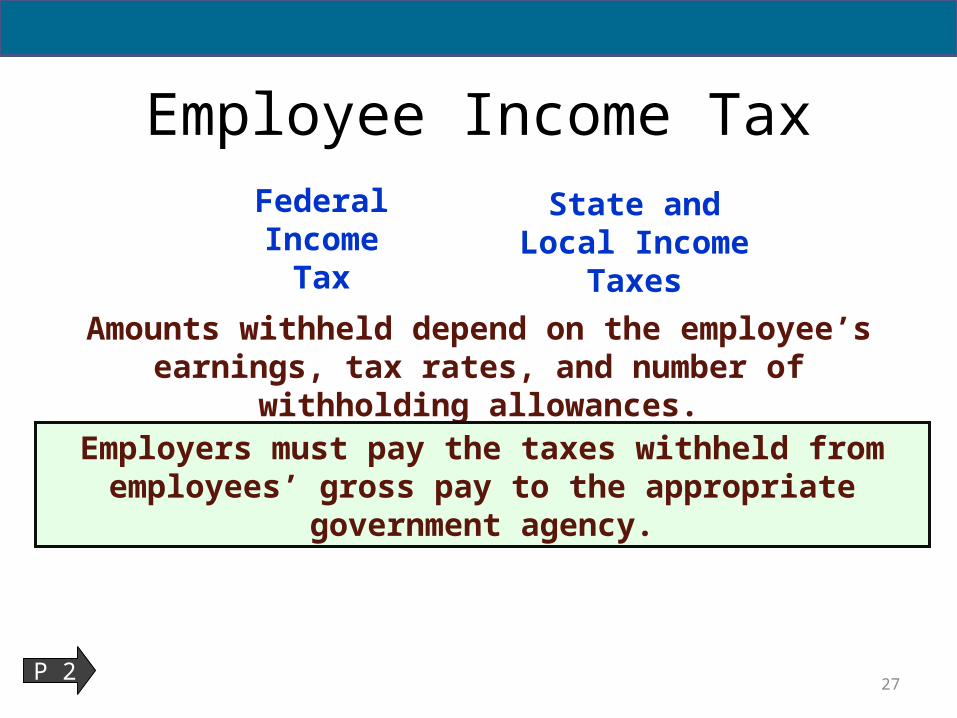

Amounts withheld depend on the employee’s earnings, tax rates, and number of withholding allowances.

Employers must pay the taxes withheld from employees’ gross pay to the appropriate government agency.

Federal Income Tax

Employee Income TaxState and Local Income Taxes

P 227

11 - 28

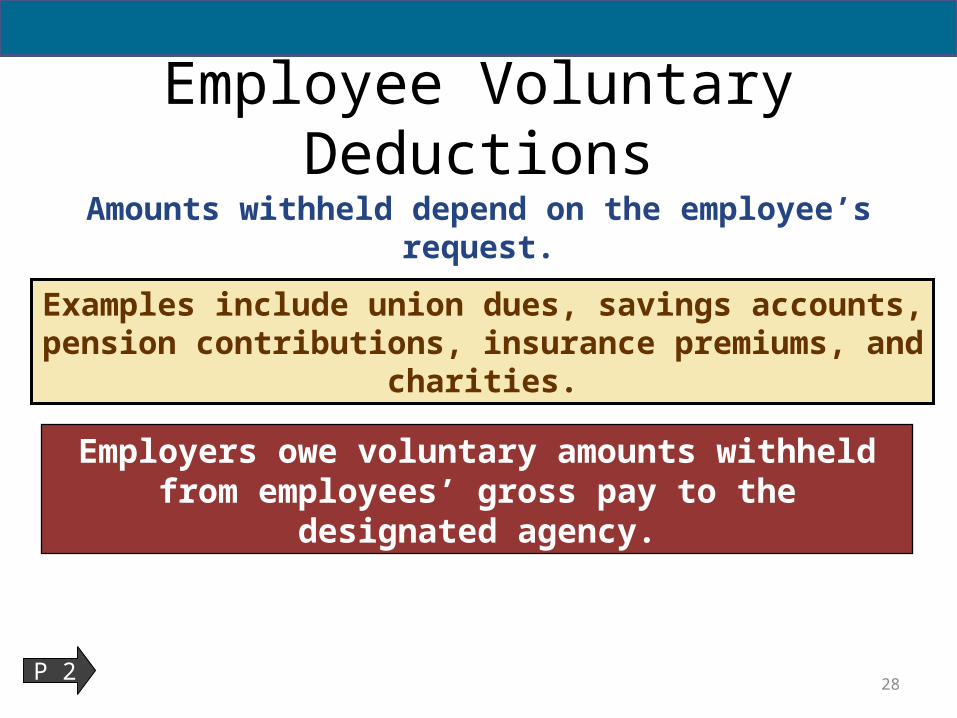

Amounts withheld depend on the employee’s request.

Employers owe voluntary amounts withheld from employees’ gross pay to the designated agency.

Examples include union dues, savings accounts, pension contributions, insurance premiums, and charities.

Employee Voluntary Deductions

P 228

11 - 29

An entry to record payroll expenses and deductions for an employee might look like this.

Recording Employee Payroll Deductions

P 2

*Amounts taken from employee’s employment records

29

09-P3: Payroll Expenses

30

11 - 31

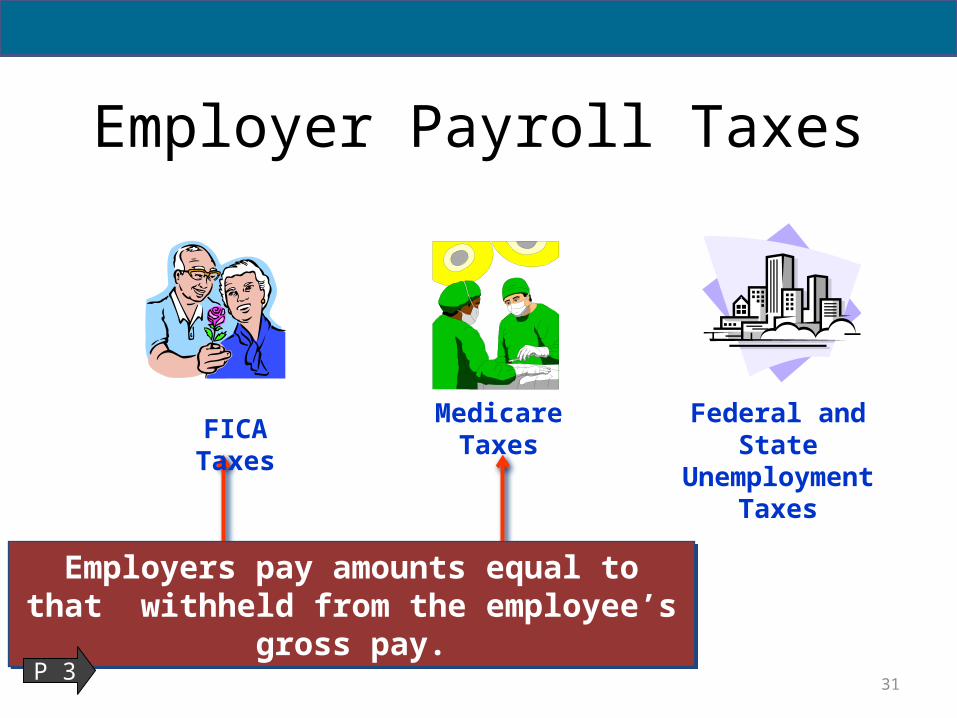

Employers pay amounts equal to that withheld from the employee’s gross pay.

Employers pay amounts equal to that withheld from the employee’s gross pay.

Employer Payroll Taxes

FICA TaxesFederal and State

Unemployment Taxes

Medicare Taxes

P 331

11 - 32

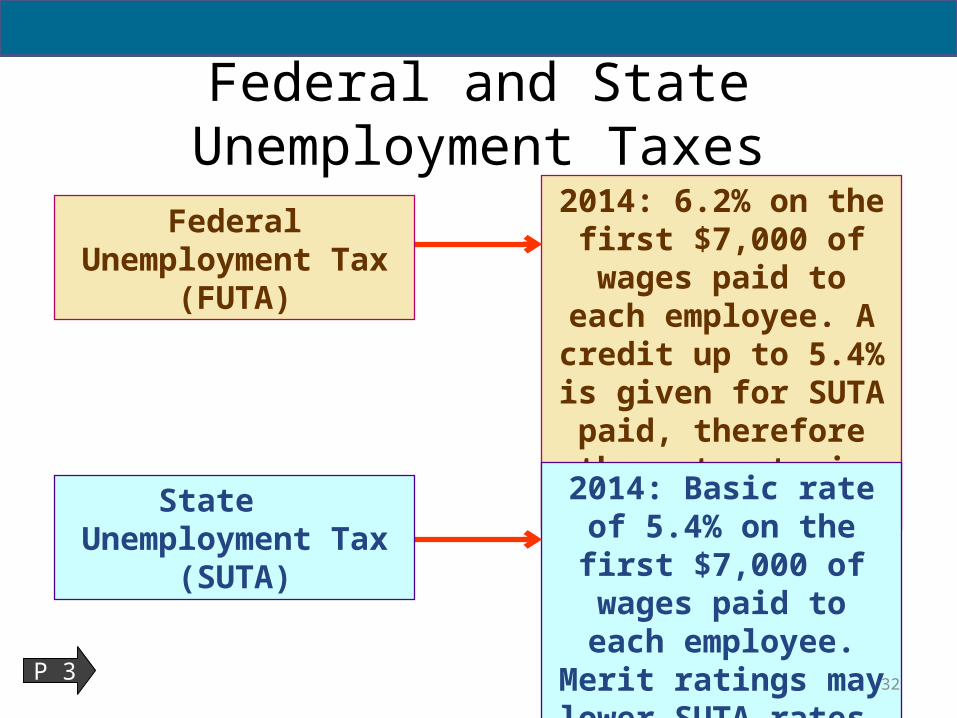

2014: 6.2% on the first $7,000 of wages paid to each employee. A credit up to 5.4% is

given for SUTA paid, therefore the net rate

is 0.6%.

Federal Unemployment Tax

(FUTA)

2014: Basic rate of 5.4% on the first

$7,000 of wages paid to each employee. Merit ratings may lower SUTA rates.

State Unemployment Tax

(SUTA)

Federal and StateUnemployment Taxes

P 332

11 - 33

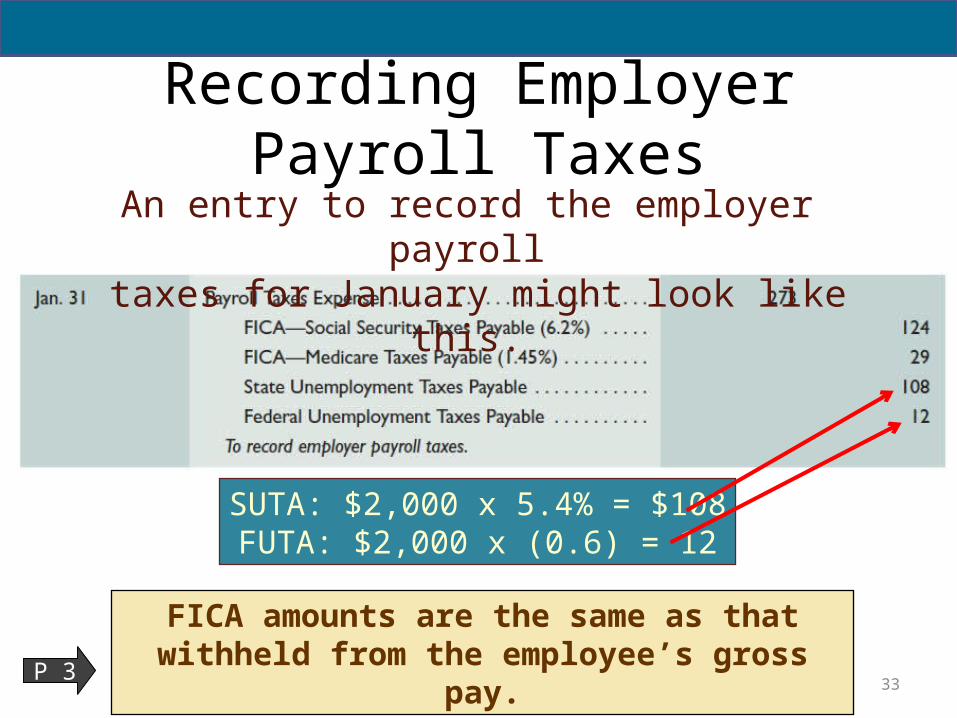

An entry to record the employer payroll taxes for January might look like this.

FICA amounts are the same as that withheld from the employee’s gross pay.

Recording EmployerPayroll Taxes

P 3

SUTA: $2,000 x 5.4% = $108FUTA: $2,000 x (0.6) = 12

33

NEED-TO-KNOW

Debit CreditJan. 8 Sales salaries expense 30,000

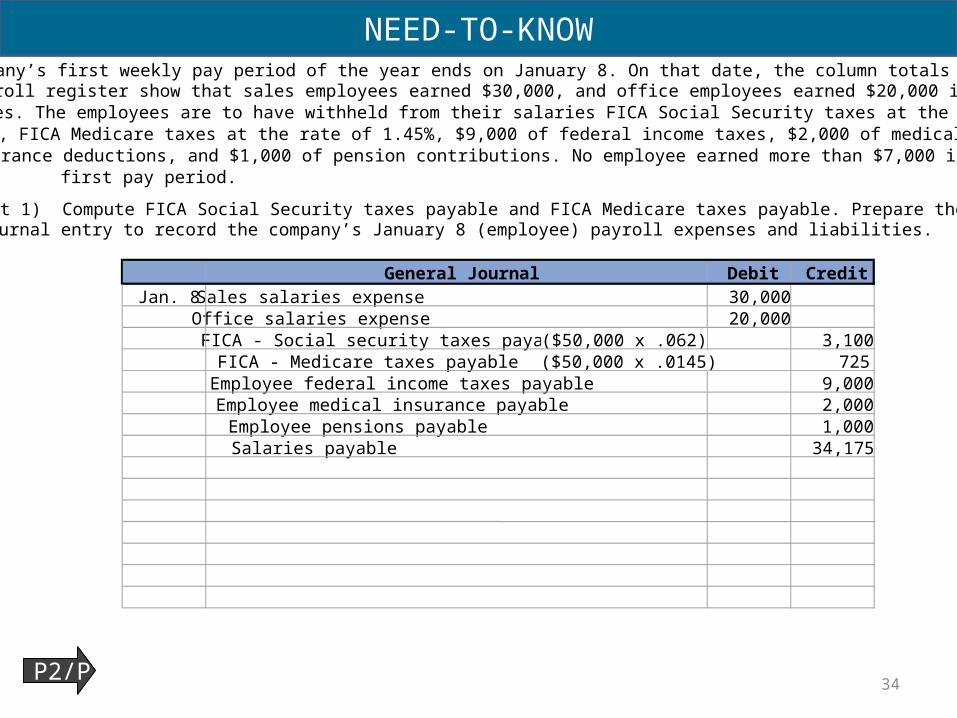

Office salaries expense 20,000FICA - Social security taxes payable ($50,000 x .062) 3,100FICA - Medicare taxes payable ($50,000 x .0145) 725Employee federal income taxes payable 9,000Employee medical insurance payable 2,000Employee pensions payable 1,000Salaries payable 34,175

Part 1) Compute FICA Social Security taxes payable and FICA Medicare taxes payable. Prepare the journal entry to record the company’s January 8 (employee) payroll expenses and liabilities.

General Journal

A company’s first weekly pay period of the year ends on January 8. On that date, the column totals in its payroll register show that sales employees earned $30,000, and office employees earned $20,000 in salaries. The employees are to have withheld from their salaries FICA Social Security taxes at the rate of 6.2%, FICA Medicare taxes at the rate of 1.45%, $9,000 of federal income taxes, $2,000 of medical insurance deductions, and $1,000 of pension contributions. No employee earned more than $7,000 in the first pay period.

P2/P 334

NEED-TO-KNOW

Debit CreditJan. 8 Sales salaries expense 30,000

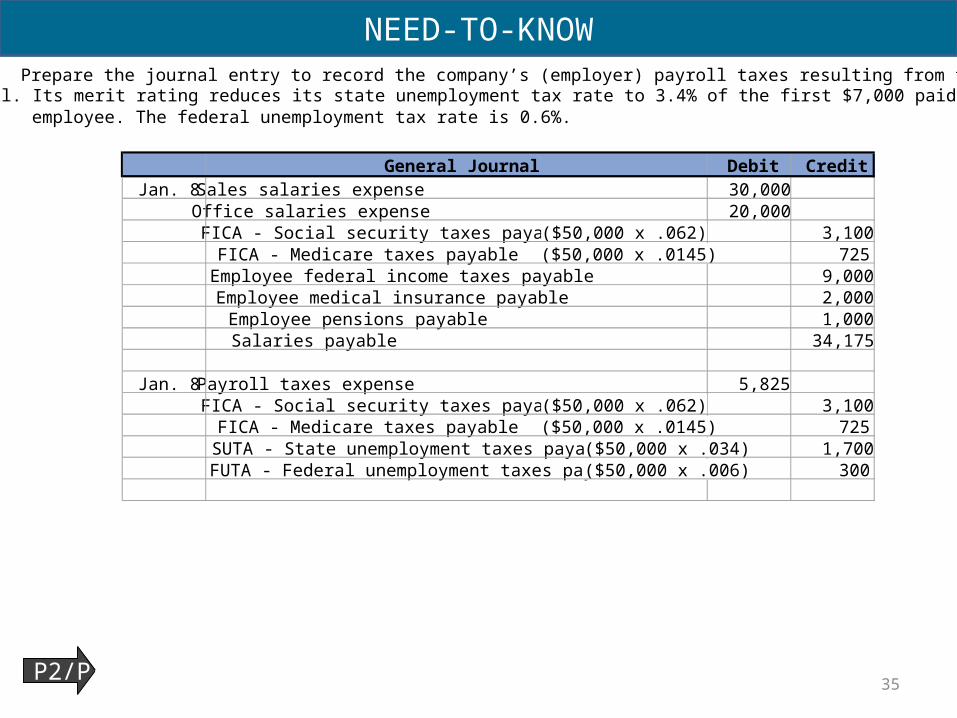

Office salaries expense 20,000FICA - Social security taxes payable ($50,000 x .062) 3,100FICA - Medicare taxes payable ($50,000 x .0145) 725Employee federal income taxes payable 9,000Employee medical insurance payable 2,000Employee pensions payable 1,000Salaries payable 34,175

Jan. 8 Payroll taxes expense 5,825FICA - Social security taxes payable ($50,000 x .062) 3,100FICA - Medicare taxes payable ($50,000 x .0145) 725SUTA - State unemployment taxes payable ($50,000 x .034) 1,700FUTA - Federal unemployment taxes payable ($50,000 x .006) 300

General Journal

Part 2) Prepare the journal entry to record the company’s (employer) payroll taxes resulting from the January 8 payroll. Its merit rating reduces its state unemployment tax rate to 3.4% of the first $7,000 paid to each

employee. The federal unemployment tax rate is 0.6%.

35P2/P3

09-P4: Estimated Liabilities

36

11 - 37

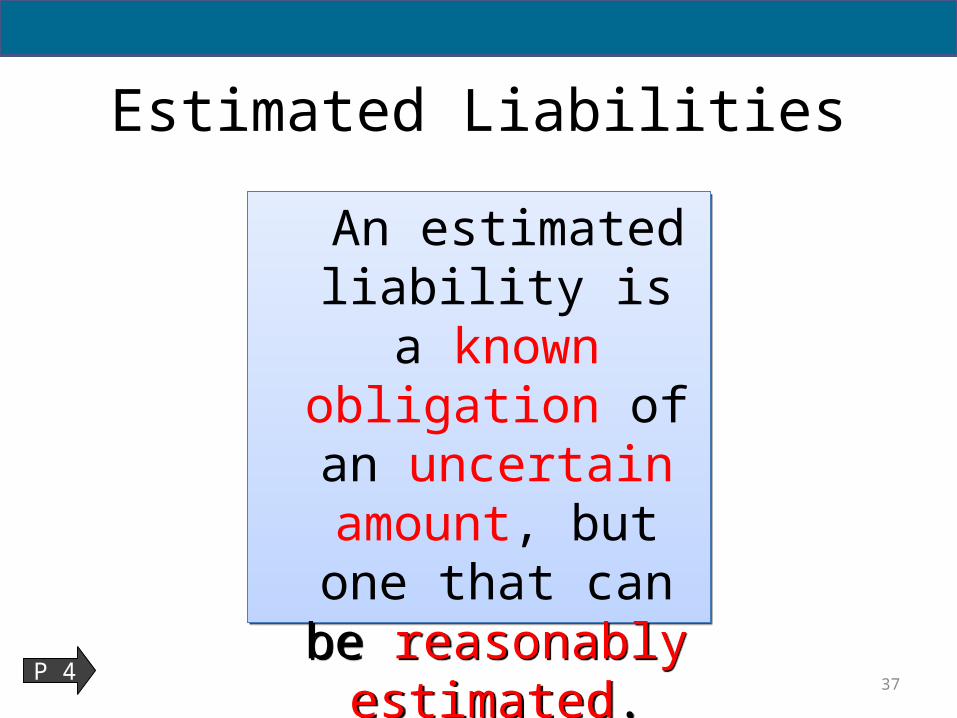

Estimated Liabilities

An estimated liability is a known

obligation of an uncertain amount, but one that can be

reasonably estimated.

An estimated liability is a known

obligation of an uncertain amount, but one that can be

reasonably estimated.

P 437

11 - 38

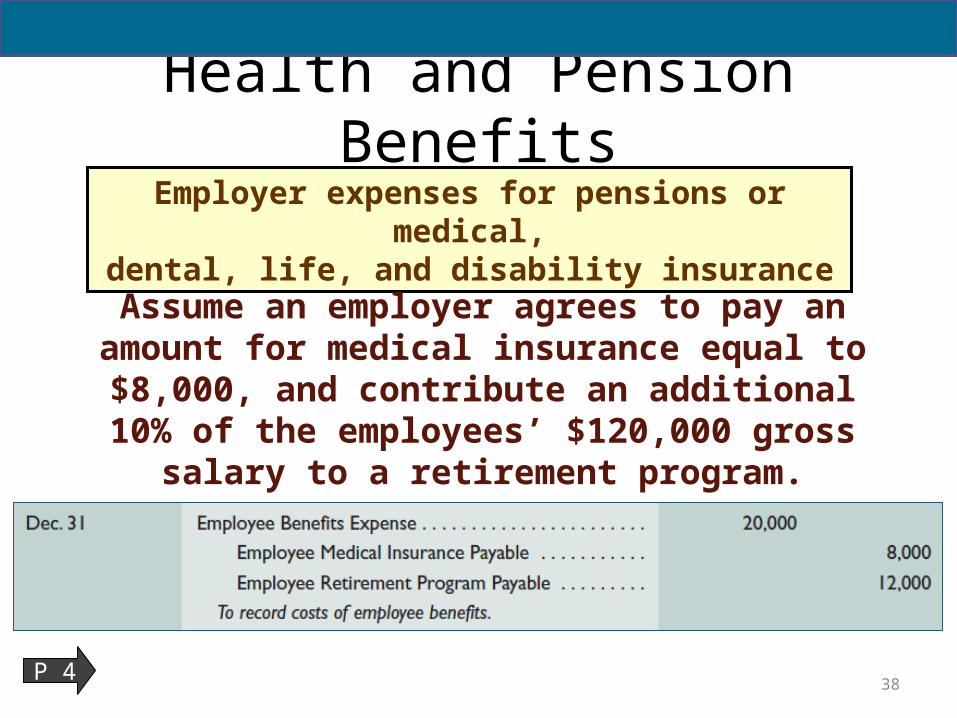

Employer expenses for pensions or medical,dental, life, and disability insurance

Health and Pension Benefits

Assume an employer agrees to pay an amount for medical insurance equal to $8,000, and

contribute an additional 10% of the employees’ $120,000 gross salary to a retirement program.

P 438

11 - 39

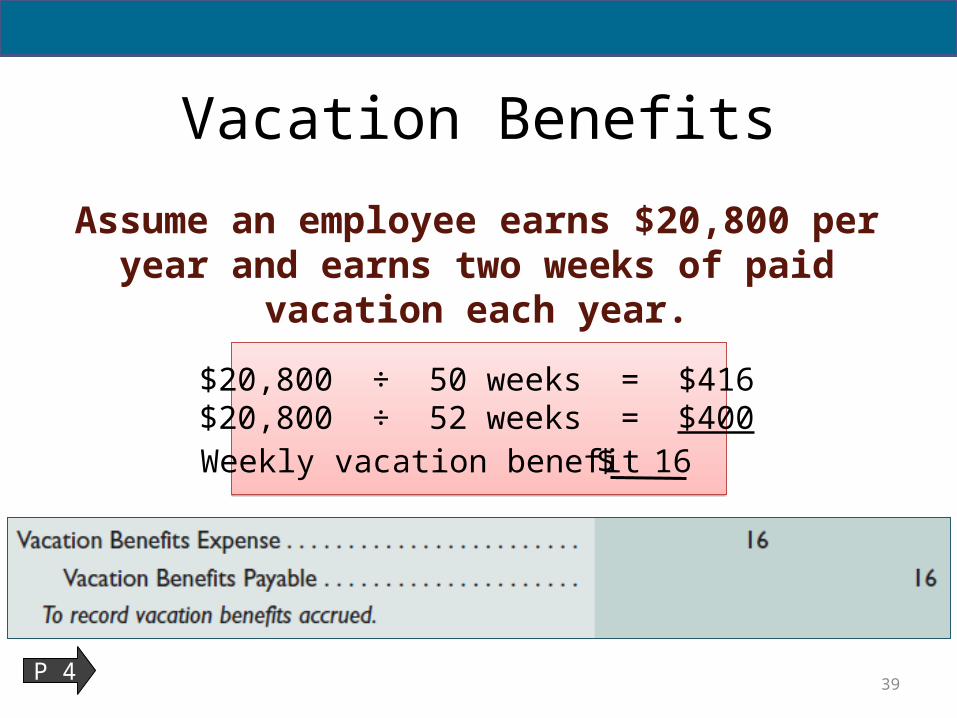

Vacation Benefits

Assume an employee earns $20,800 per year and earns two weeks of paid vacation each year.

$20,800 ÷ 50 weeks = $416$20,800 ÷ 52 weeks = $400

Weekly vacation benefit $ 16

P 439

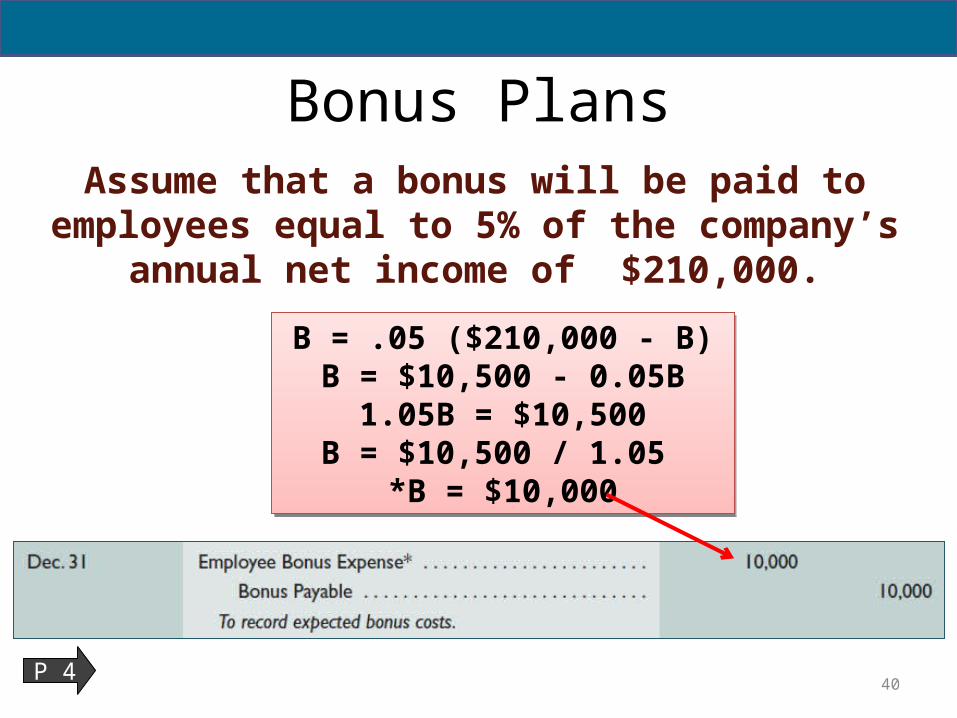

11 - 40

Bonus Plans

P 4

B = .05 ($210,000 - B)B = $10,500 - 0.05B

1.05B = $10,500B = $10,500 / 1.05

*B = $10,000

B = .05 ($210,000 - B)B = $10,500 - 0.05B

1.05B = $10,500B = $10,500 / 1.05

*B = $10,000

Assume that a bonus will be paid to employees equal to 5% of the company’s annual net income

of $210,000.

40

11 - 41

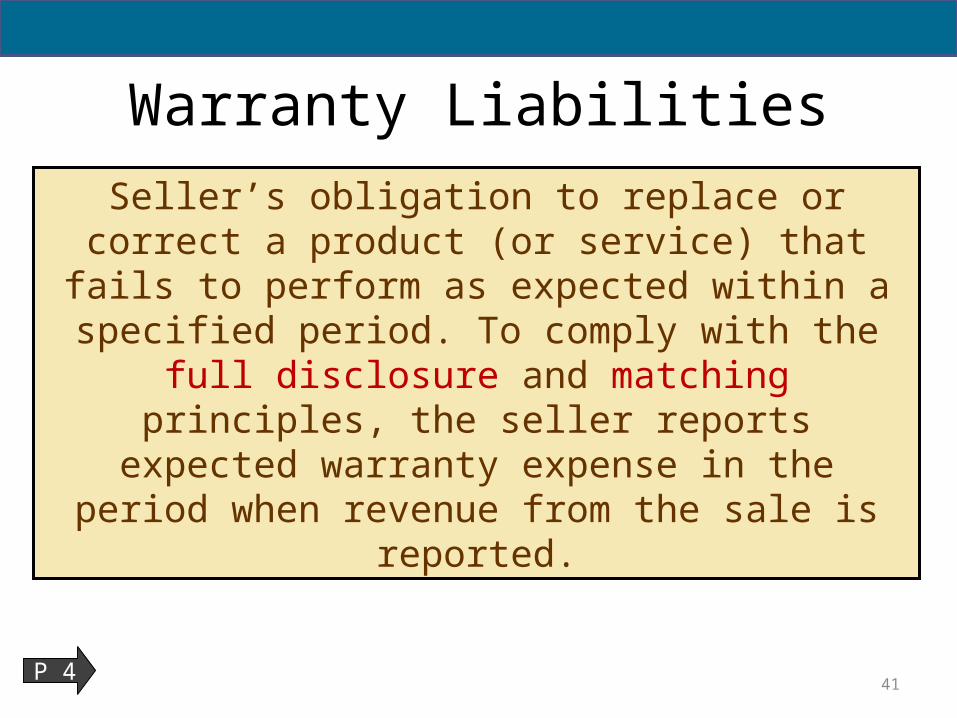

Warranty LiabilitiesSeller’s obligation to replace or correct a product (or

service) that fails to perform as expected within a specified period. To comply with the full disclosure

and matching principles, the seller reports expected warranty expense in the period when revenue from

the sale is reported.

P 441

11 - 42

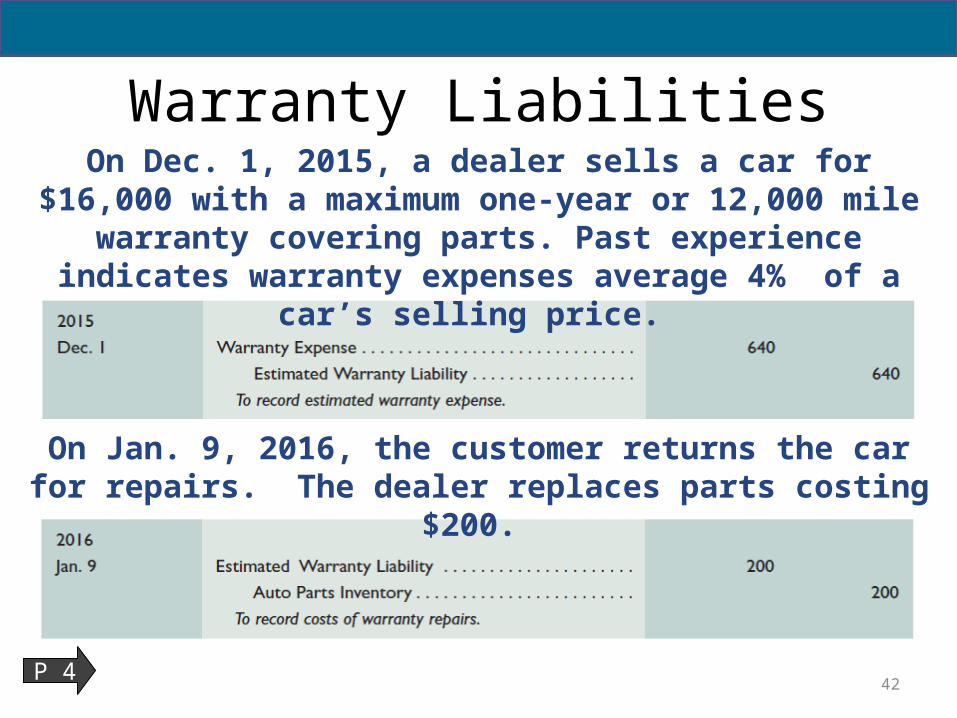

Warranty Liabilities

P 4

On Dec. 1, 2015, a dealer sells a car for $16,000 with a maximum one-year or 12,000 mile warranty covering parts. Past experience indicates warranty expenses average 4%

of a car’s selling price.

On Jan. 9, 2016, the customer returns the car for repairs. The dealer replaces parts costing $200.

42

09-C3: Contingent Liabilities

43

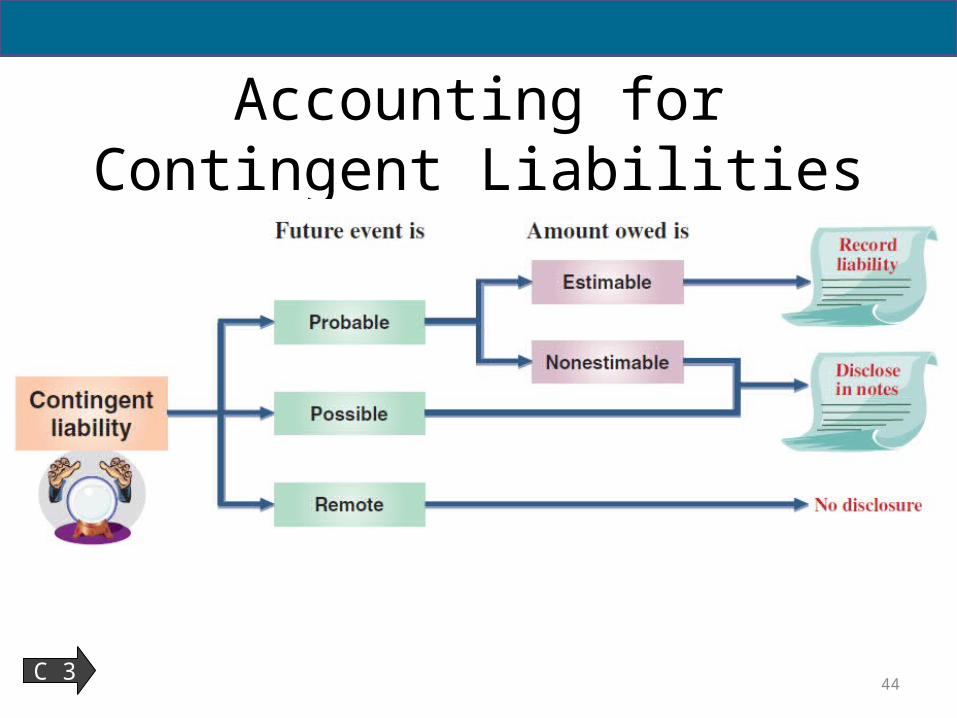

11 - 44

Accounting forContingent Liabilities

C 344

11 - 45

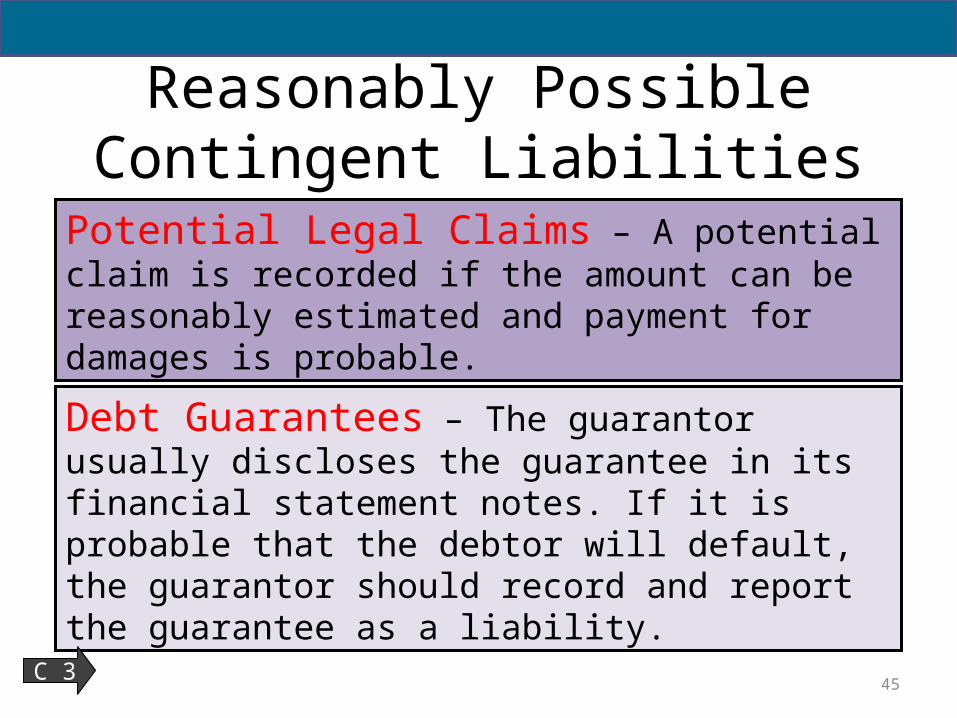

Reasonably PossibleContingent Liabilities

Potential Legal Claims – A potential claim is recorded if the amount can be reasonably estimated and payment for damages is probable.

Debt Guarantees – The guarantor usually discloses the guarantee in its financial statement notes. If it is probable that the debtor will default, the guarantor should record and report the guarantee as a liability.

C 345

NEED-TO-KNOW

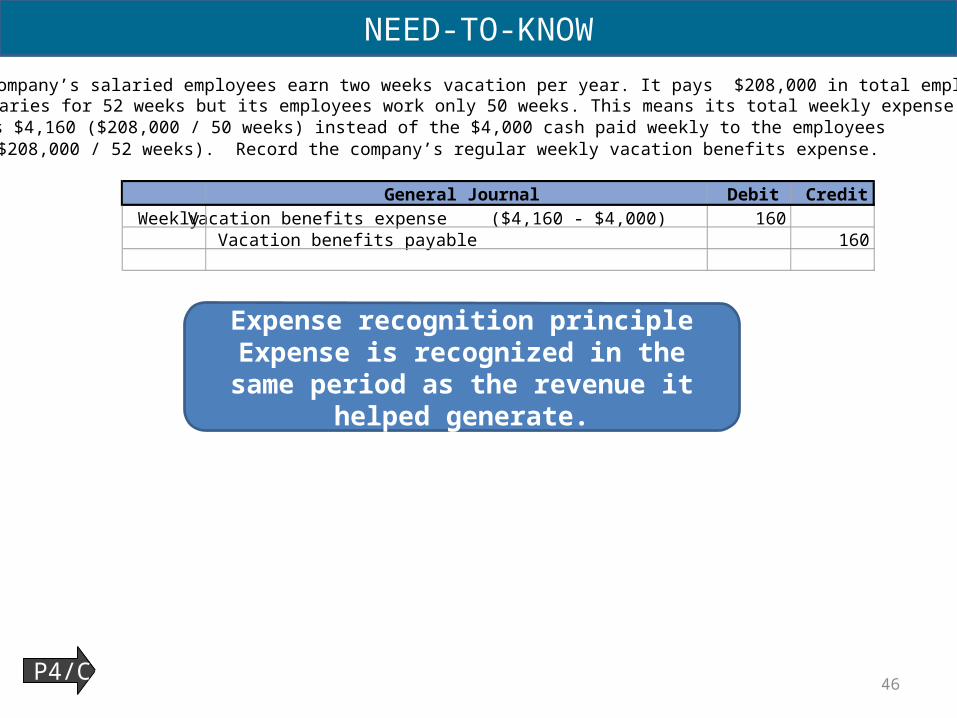

Debit CreditWeekly Vacation benefits expense ($4,160 - $4,000) 160

Vacation benefits payable 160

A company’s salaried employees earn two weeks vacation per year. It pays $208,000 in total employee salaries for 52 weeks but its employees work only 50 weeks. This means its total weekly expense is $4,160 ($208,000 / 50 weeks) instead of the $4,000 cash paid weekly to the employees($208,000 / 52 weeks). Record the company’s regular weekly vacation benefits expense.

General Journal

Expense recognition principleExpense is recognized in the same period as

the revenue it helped generate.

P4/C346

NEED-TO-KNOW

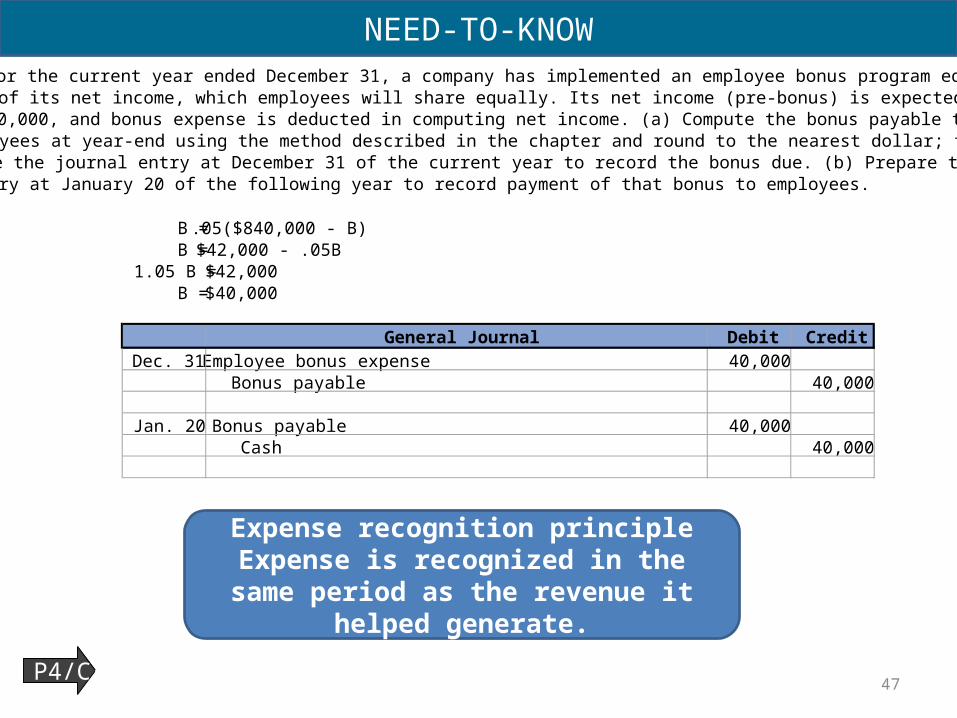

B = .05($840,000 - B)B = $42,000 - .05B

1.05 B = $42,000 B = $40,000

Debit CreditDec. 31 Employee bonus expense 40,000

Bonus payable 40,000

Jan. 20 Bonus payable 40,000Cash 40,000

For the current year ended December 31, a company has implemented an employee bonus program equal to 5% of its net income, which employees will share equally. Its net income (pre-bonus) is expected to be $840,000, and bonus expense is deducted in computing net income. (a) Compute the bonus payable to the employees at year-end using the method described in the chapter and round to the nearest dollar; then, prepare the journal entry at December 31 of the current year to record the bonus due. (b) Prepare the journal entry at January 20 of the following year to record payment of that bonus to employees.

General Journal

Expense recognition principleExpense is recognized in the same period as

the revenue it helped generate.

47P4/C3

NEED-TO-KNOW

Debit CreditJun. 11 Cash 400

Sales 400

Jun. 11 Warranty expense ($400 x .05) 20Estimated warranty liability 20

Mar. 24 Estimated warranty liability 15Repair parts inventory 15

On June 11 of the current year, a retailer sells a trimmer for $400 with a one-year warranty that covers parts. Warranty expense is estimated at 5% of sales. On March 24 of the next year, the trimmer is brought in for repairs covered under the warranty requiring $15 in materials taken from the Repair Parts Inventory. Prepare the (a) June 11 entry to record the trimmer sale, and (b) March 24 entry to record warranty repairs.

General Journal

Expense recognition principleExpense is recognized in the same period as

the revenue it helped generate.

48P4/C3

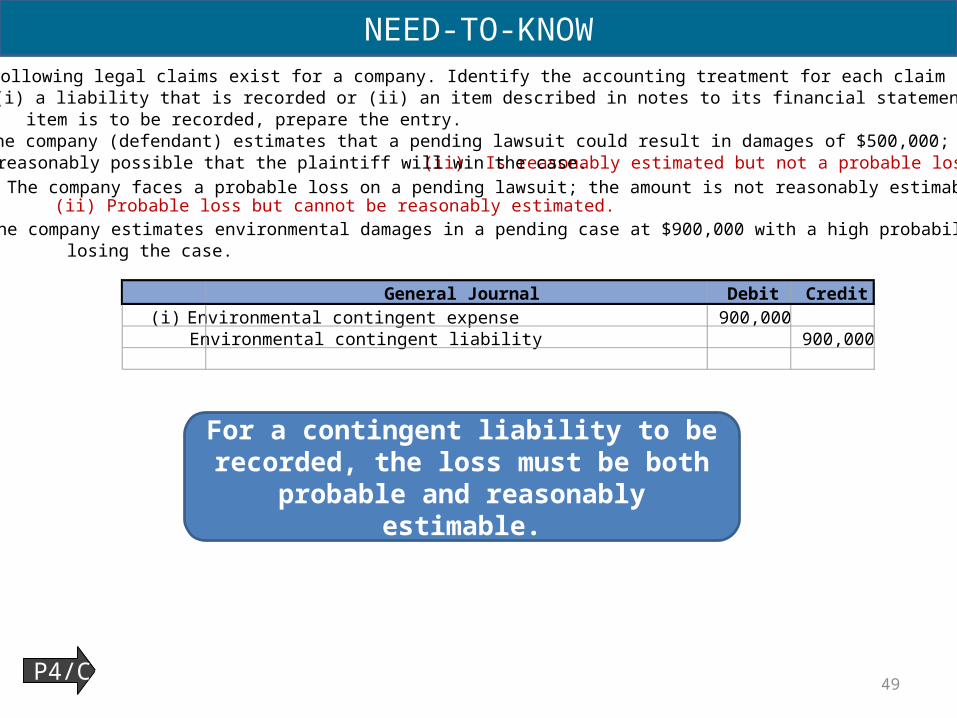

NEED-TO-KNOW

(ii) Is reasonably estimated but not a probable loss.

(ii) Probable loss but cannot be reasonably estimated.

Debit Credit(i) Environmental contingent expense 900,000

Environmental contingent liability 900,000

General Journal

The following legal claims exist for a company. Identify the accounting treatment for each claimas either (i) a liability that is recorded or (ii) an item described in notes to its financial statements. If anitem is to be recorded, prepare the entry.a. The company (defendant) estimates that a pending lawsuit could result in damages of $500,000; it is reasonably possible that the plaintiff will win the case.

b. The company faces a probable loss on a pending lawsuit; the amount is not reasonably estimable.

c. The company estimates environmental damages in a pending case at $900,000 with a high probability of losing the case.

For a contingent liability to be recorded, the loss must be both probable and reasonably

estimable.

49P4/C3

11 - 50

Global ViewCharacteristics of Liabilities

Accounting definitions and characteristics of current liabilities are similar for U.S. GAAP and IFRS. Sometimes IFRS will use the

word “provision” to refer to a “liability.”

Known (Determinable) LiabilitiesBoth U.S. GAAP and IFRS require companies to treat known (or determinable) liabilities in a similar manner. Examples would be accounts payable, unearned revenues, and payroll liabilities.

Estimated LiabilitiesRegarding estimated liabilities, when a known current obligation

that involves an uncertain amount, but one that can be reasonably estimated, both U.S. GAAP and IFRS require similar treatment. 50

09-A1: Times Interest Earned Ratio

51

11 - 52

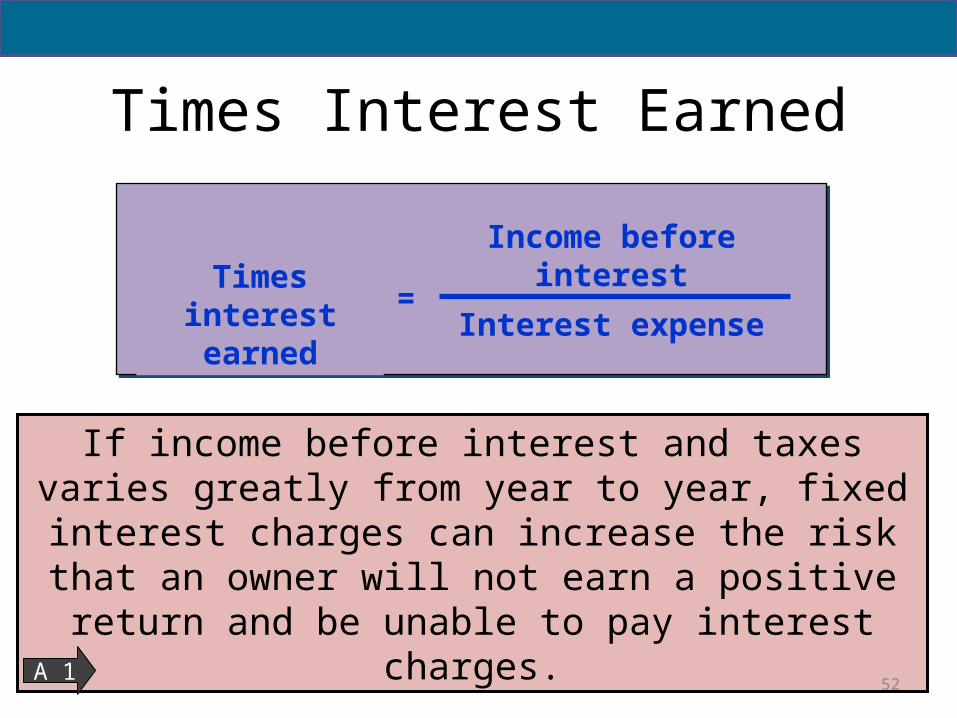

If income before interest and taxes varies greatly from year to year, fixed interest charges can increase the risk that an owner will not earn a positive return and

be unable to pay interest charges.

Times Interest Earned

Times interestearned

Income before interestand income taxes

Interest expense=

A 152

09-P5: Payroll Reports, Records, and Procedures

53

11 - 54

Appendix 9A: PayrollReports, Records, and Procedures

P 5

Payroll Reports

IRS Form 941 IRS Form 940

W-2

Payroll Records

Payroll Register Payroll Checks

Employee Earnings Report

Payroll Procedures

Withholding Tables W-4

54

11 - 55

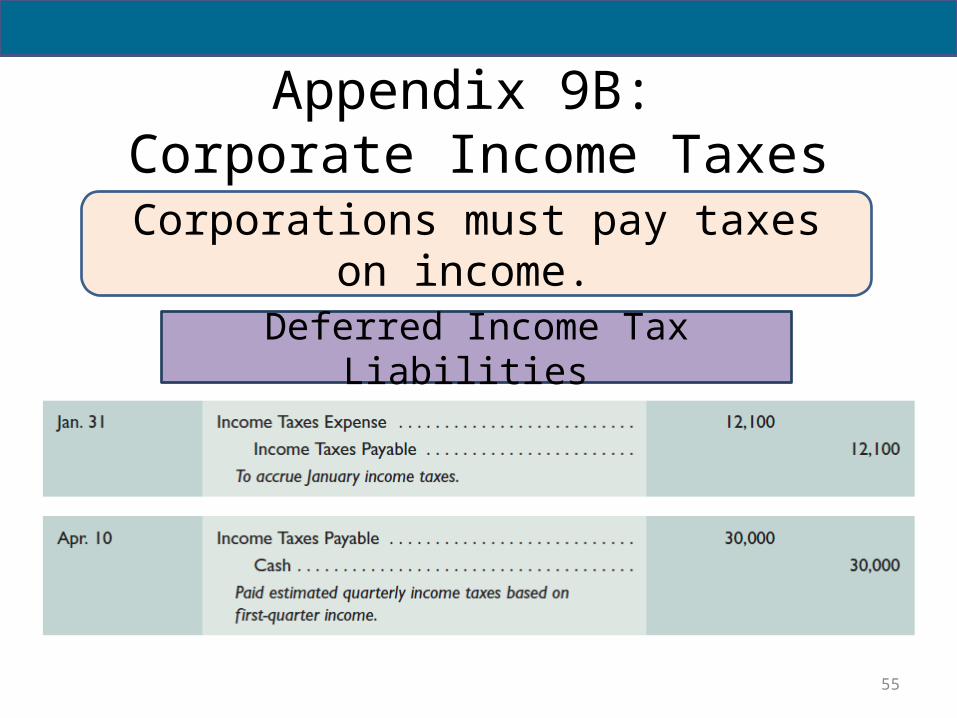

Appendix 9B: Corporate Income Taxes

Corporations must pay taxes on income.

Deferred Income Tax Liabilities

55

11 - 56

End of Chapter 9

56