accounting for long term liabilities ch 10 – acc 1a

TRANSCRIPT

Accounting for Long Term Liabilities

Ch 10 – Acc 1a

Different Ways to Finance a Company Borrowing from a Bank (Ch 9):

Notes Payable – More expensive and restrictive than bonds.

Selling Stock (Ch 11): Gives up ownership shares, but does NOT require interest or principal repayments.

Issuing Bonds (Ch 10): Easier to deal with than bank loans, require interest & principal repayment.

Bonds A borrowing/lending arrangementAdvantages• Bonds do not Bonds do not

affect affect stockholder stockholder control.control.

• Interest on Interest on bonds is tax bonds is tax deductible.deductible.

• Can increase Can increase return on return on equity.equity.

Disadvantages• Bonds require Bonds require

payment of both payment of both periodic interest and periodic interest and par value at maturity.par value at maturity.

• Can decrease return Can decrease return on equity.on equity.

Secured and Secured and Unsecured Unsecured

Secured and Secured and Unsecured Unsecured

Term and Term and Serial Serial

Term and Term and Serial Serial

Registered Registered and Bearerand BearerRegistered Registered and Bearerand Bearer

Convertible Convertible and Callableand CallableConvertible Convertible and Callableand Callable

Types of BondsA2

10-4

. . .an investment firm called an underwriter. The underwriter sells the bonds to. . .

A trustee monitors the bond issue.

A company sells the bonds to. . .

. . . investors

Bond Issuing ProceduresA1

10-5

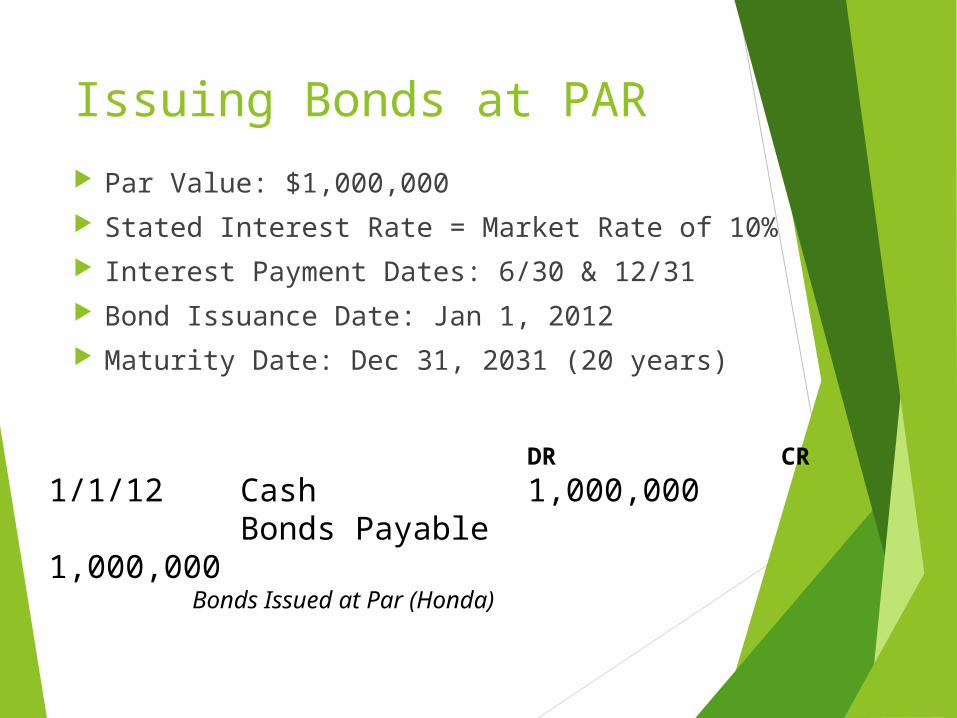

Issuing Bonds at PAR

Par Value: $1,000,000 Stated Interest Rate = Market Rate of 10% Interest Payment Dates: 6/30 & 12/31 Bond Issuance Date: Jan 1, 2012 Maturity Date: Dec 31, 2031 (20 years)

DR CR

1/1/12 Cash 1,000,000Bonds Payable 1,000,000

Bonds Issued at Par (Honda)

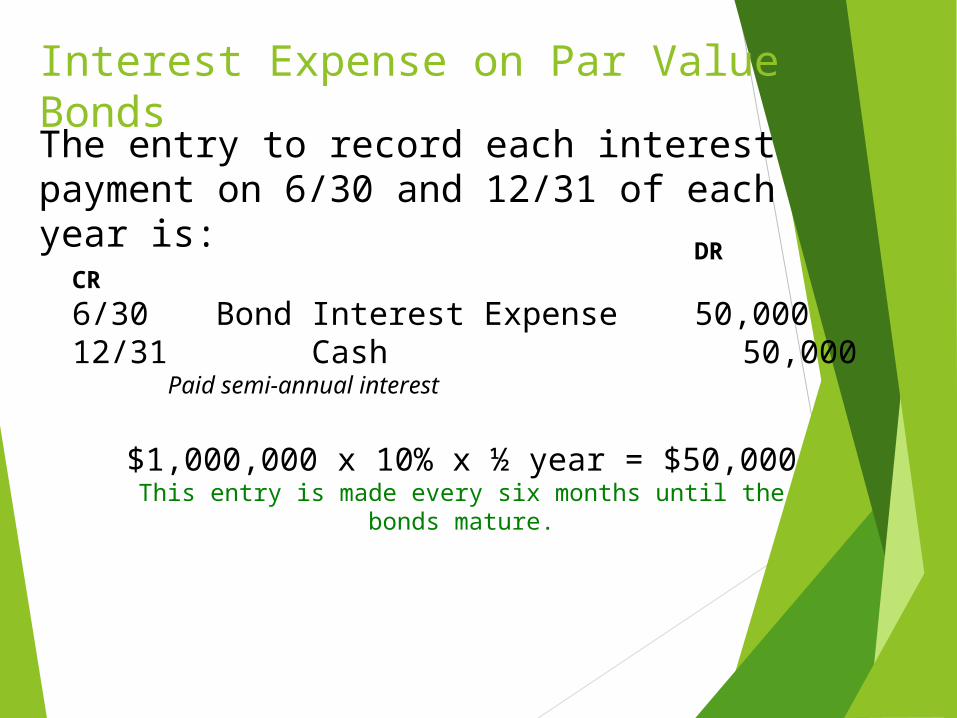

Interest Expense on Par Value Bonds

The entry to record each interest payment on 6/30 and 12/31 of each year is:

DR CR

6/30 Bond Interest Expense 50,00012/31 Cash 50,000

Paid semi-annual interest

$1,000,000 x 10% x ½ year = $50,000This entry is made every six months until the bonds mature.

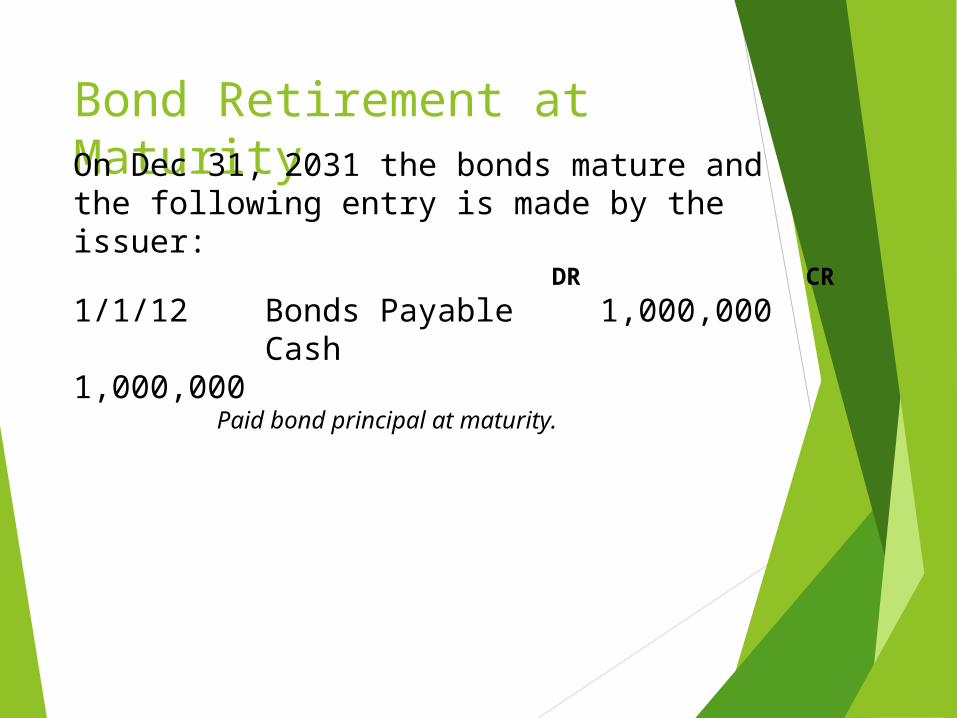

Bond Retirement at MaturityOn Dec 31, 2031 the bonds mature and the following entry is made by the issuer:

DR CR

1/1/12 Bonds Payable 1,000,000Cash 1,000,000

Paid bond principal at maturity.

Ex 10-1, Parts 1 & 2

Interest Rates & Bonds

Stated Rate: used to determine the amount of the interest payment

(par value x stated interest rate x [1/# interest pymts per year])

Market Rate: determines the selling price of the bond and is the interest rate used for Tables B1 & B3.

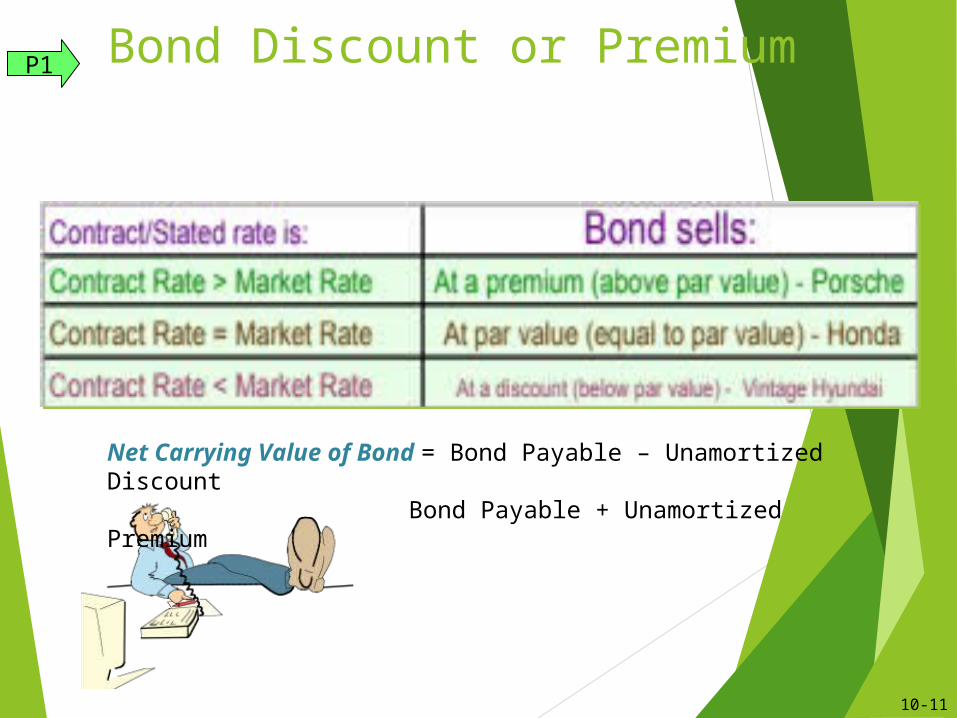

Bond Discount or PremiumP1

10-11

Net Carrying Value of Bond = Bond Payable – Unamortized Discount Bond Payable + Unamortized Premium

Ex 10-1, Part 3b

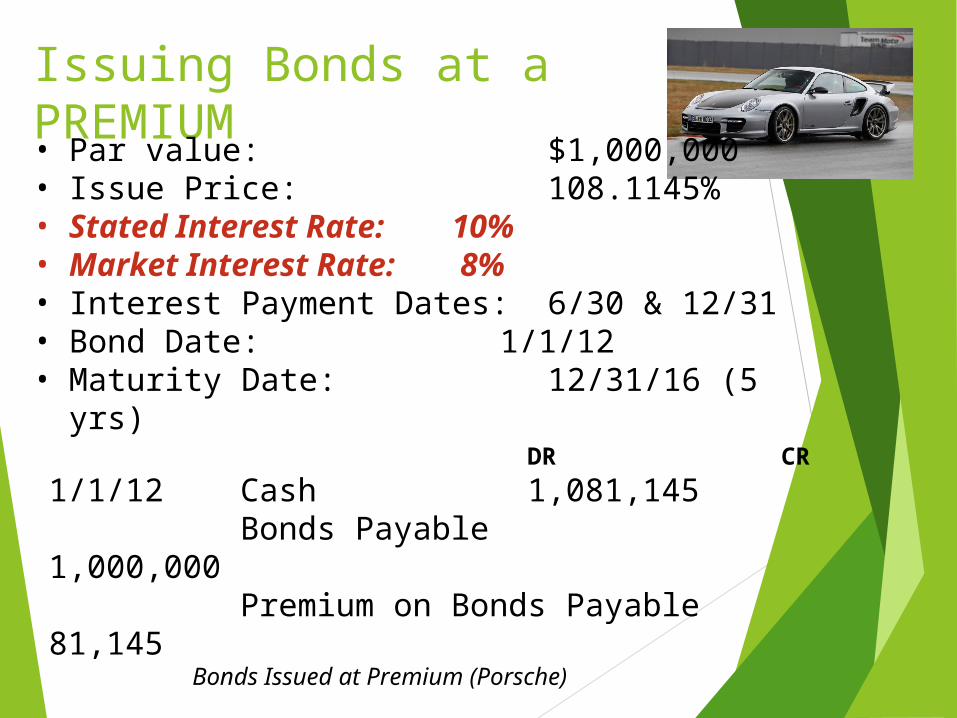

Issuing Bonds at a PREMIUM

• Par value: $1,000,000• Issue Price: 108.1145%• Stated Interest Rate: 10%• Market Interest Rate: 8%• Interest Payment Dates: 6/30 & 12/31• Bond Date: 1/1/12• Maturity Date: 12/31/16 (5 yrs)

DR CR

1/1/12 Cash 1,081,145Bonds Payable 1,000,000Premium on Bonds Payable 81,145

Bonds Issued at Premium (Porsche)

Interest Expense on PREMIUM Value Bonds

The entry to record each interest payment on 6/30 and 12/31 of each year is:

DR CR

6/30 Bond Interest Expense 41,885 (plug)

& Premium on Bond Payable 8,115*12/31 Cash 50,000**

Paid semi-annual interest & amortized premium

$81,145 / 10 interest payments = $8,115* (rounded)

$1,000,000 x 10% x ½ year = $50,000**This entry is made every six months until the bonds mature.

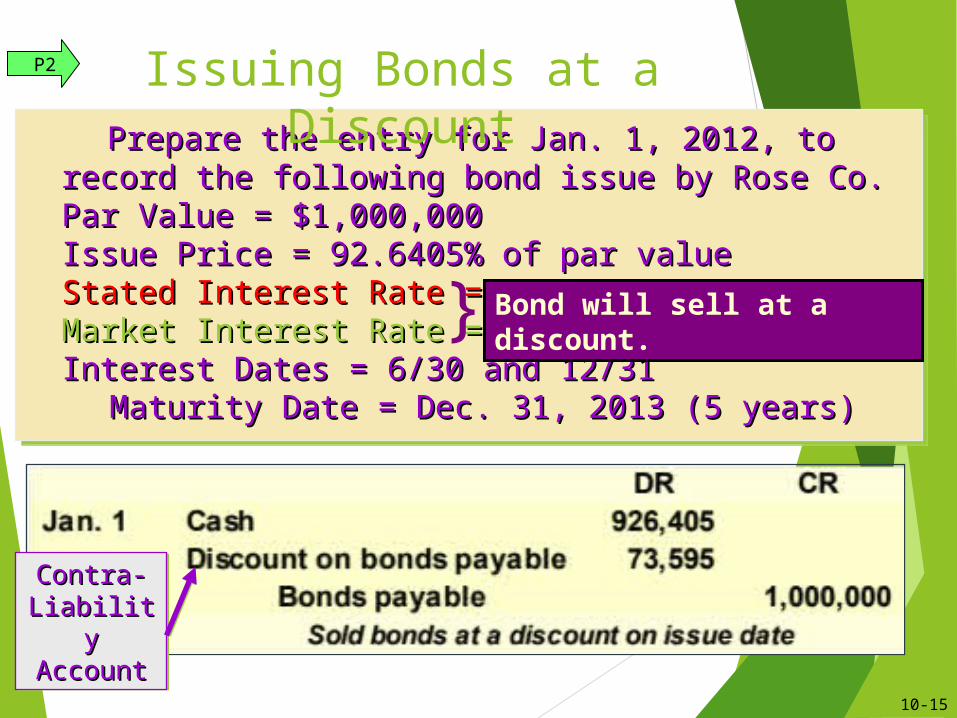

Prepare the entry for Jan. 1, 2012, to record the following Prepare the entry for Jan. 1, 2012, to record the following bond issue by Rose Co. bond issue by Rose Co. Par Value = $1,000,000Par Value = $1,000,000Issue Price = 92.6405% of par valueIssue Price = 92.6405% of par valueStated Interest Rate = 10%Stated Interest Rate = 10%Market Interest Rate = 12%Market Interest Rate = 12%Interest Dates = 6/30 and 12/31Interest Dates = 6/30 and 12/31

Maturity Date = Dec. 31, 2013 (5 years)Maturity Date = Dec. 31, 2013 (5 years)

Prepare the entry for Jan. 1, 2012, to record the following Prepare the entry for Jan. 1, 2012, to record the following bond issue by Rose Co. bond issue by Rose Co. Par Value = $1,000,000Par Value = $1,000,000Issue Price = 92.6405% of par valueIssue Price = 92.6405% of par valueStated Interest Rate = 10%Stated Interest Rate = 10%Market Interest Rate = 12%Market Interest Rate = 12%Interest Dates = 6/30 and 12/31Interest Dates = 6/30 and 12/31

Maturity Date = Dec. 31, 2013 (5 years)Maturity Date = Dec. 31, 2013 (5 years)

Issuing Bonds at a Discount

} Bond will sell at a discount.

P2

10-15

Contra-Contra-LiabilityLiabilityAccountAccount

Contra-Contra-LiabilityLiabilityAccountAccount

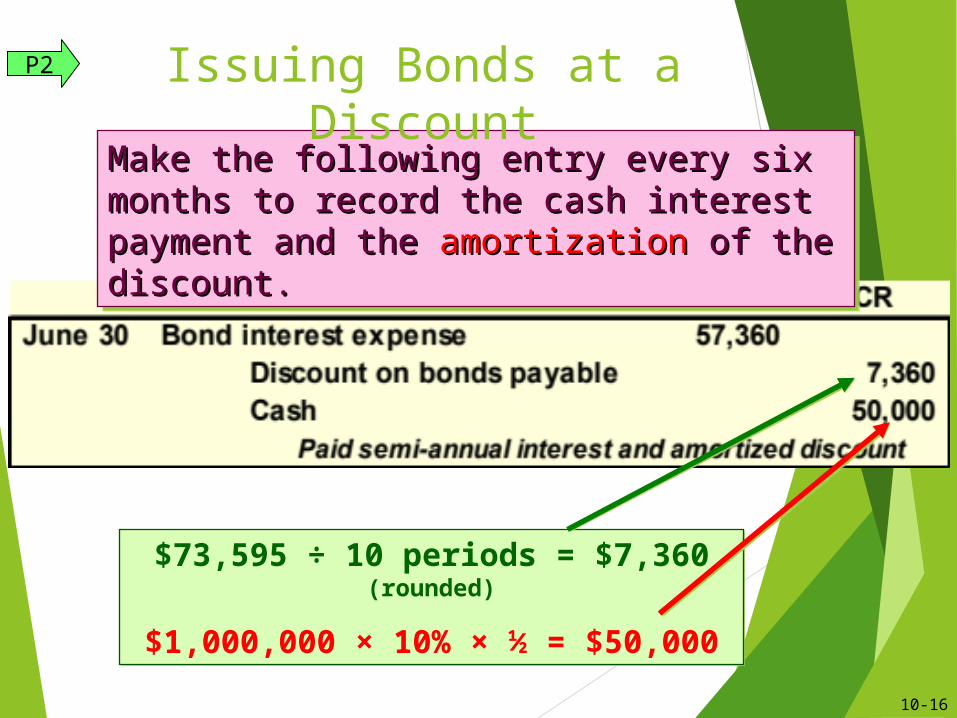

$73,595 ÷ 10 periods = $7,360 (rounded)

$1,000,000 × 10% × ½ = $50,000

$73,595 ÷ 10 periods = $7,360 (rounded)

$1,000,000 × 10% × ½ = $50,000

Make the following entry every six months to Make the following entry every six months to record the cash interest payment and the record the cash interest payment and the amortization amortization of the discount.of the discount.

Make the following entry every six months to Make the following entry every six months to record the cash interest payment and the record the cash interest payment and the amortization amortization of the discount.of the discount.

Issuing Bonds at a DiscountP2

10-16

Bond Issuance Journal Entry

Discounted Bond (Hyundai) on Jan 1:Cash $926,405

Discount on Bond* 73,595Bond Payable

$1,000,000

Premium Bond (Porsche) on Jan 1:Cash $1,081,145

Premium on Bond* 81,145 Bond Payable

$1,000,000

*The Bond’s Discount or Premium accounts are Contra Liability accounts.

Cash $1,000,000 Bond Payable

$1,000,000

Cash $1,000,000 Bond Payable

$1,000,000

Bond at Par Value (Honda):Bond has a 5-yr

term & pays interest 2x per

year

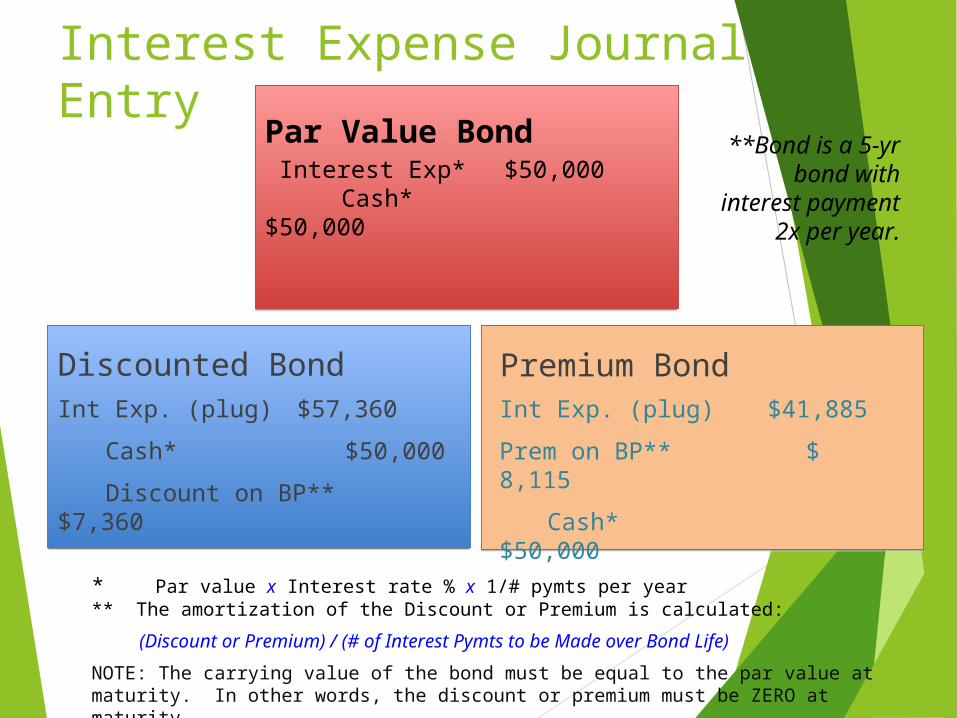

Interest Expense Journal Entry

Discounted BondInt Exp. (plug) $57,360

Cash* $50,000

Discount on BP** $7,360

Premium BondInt Exp. (plug) $41,885

Prem on BP** $ 8,115

Cash* $50,000

* Par value x Interest rate % x 1/# pymts per year** The amortization of the Discount or Premium is calculated:

(Discount or Premium) / (# of Interest Pymts to be Made over Bond Life)

NOTE: The carrying value of the bond must be equal to the par value at maturity. In other words, the discount or premium must be ZERO at maturity.

Interest Exp* $50,000 Cash* $50,000

Interest Exp* $50,000 Cash* $50,000

Par Value Bond **Bond is a 5-yr bond with interest

payment 2x per year.

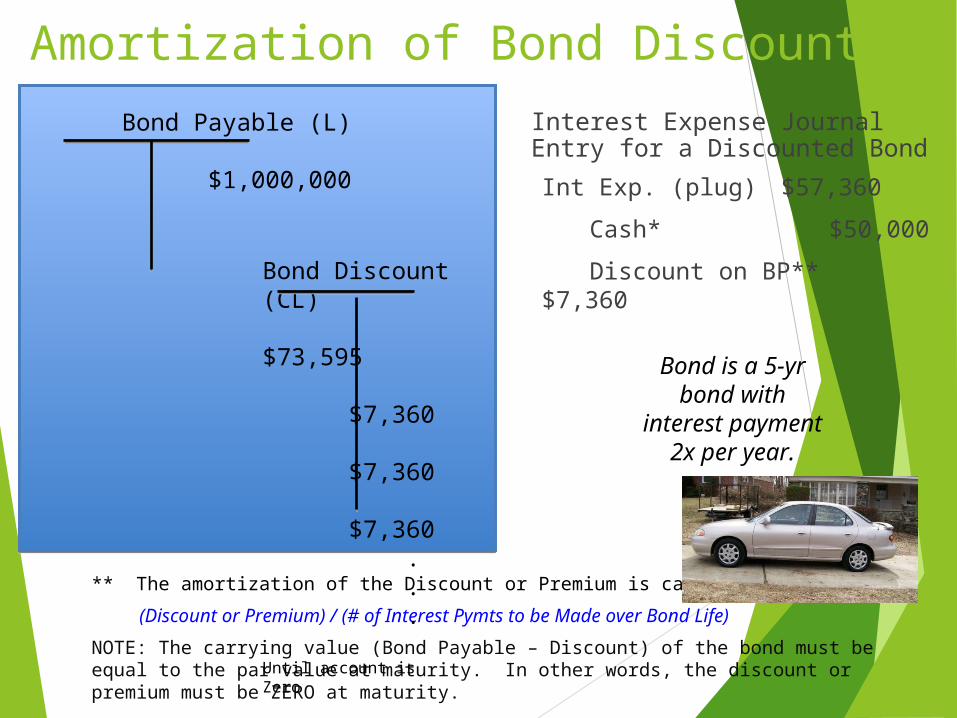

Amortization of Bond DiscountInterest Expense Journal Entry for a Discounted Bond

Int Exp. (plug) $57,360

Cash* $50,000

Discount on BP** $7,360

** The amortization of the Discount or Premium is calculated:

(Discount or Premium) / (# of Interest Pymts to be Made over Bond Life)

NOTE: The carrying value (Bond Payable – Discount) of the bond must be equal to the par value at maturity. In other words, the discount or premium must be ZERO at maturity.

Bond is a 5-yr bond with interest

payment 2x per year.

Bond Payable (L)

$1,000,000

Bond Discount (CL)

$73,595 $7,360 $7,360 $7,360

.

.

. Until account is Zero

P2

10-20

Amortization of Bond PremiumInterest Expense Journal Entry for a Premium Bond

Int Exp. (plug) $41,885

Prem on BP** $ 8,115

Cash* $50,000

Int Exp. (plug) $41,885

Prem on BP** $ 8,115

Cash* $50,000

** The amortization of the Discount or Premium is calculated:

(Discount or Premium) / (# of Interest Pymts to be Made over Bond Life)

NOTE: The carrying value (Bond Payable + Premium) of the bond must be equal to the par value at maturity. In other words, the discount or premium must be ZERO at maturity.

Bond is a 5-yr bond with interest

payment 2x per year.

Bond Payable (L)

$1,000,000

Bond Premium (CL)

$81,145 $8,115 $8,115 $8,115

.

.

. Until account is Zero

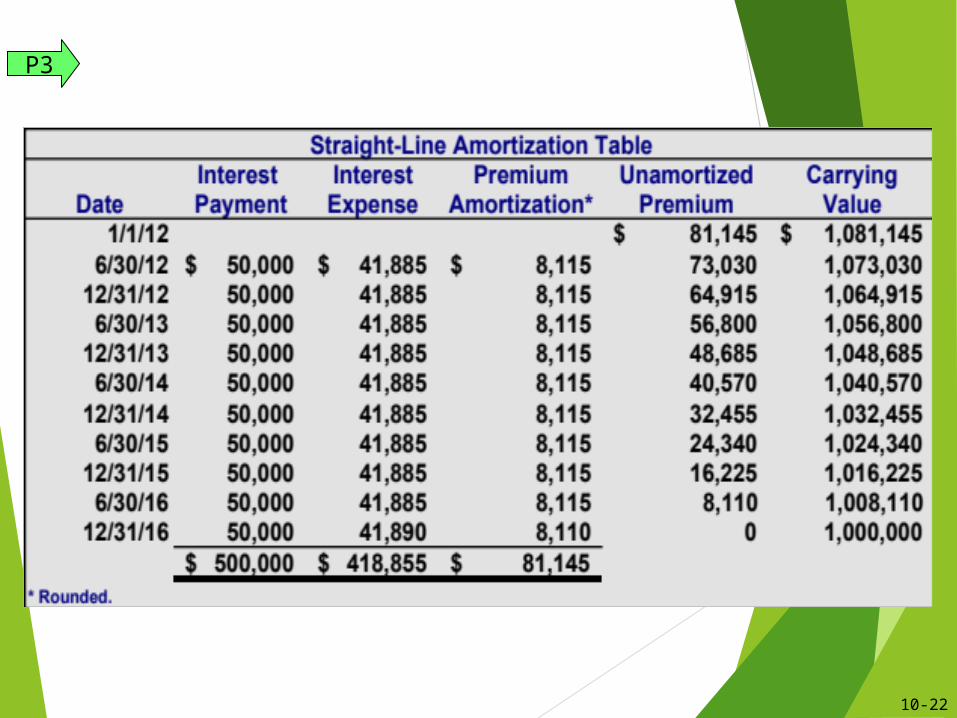

P3

10-22

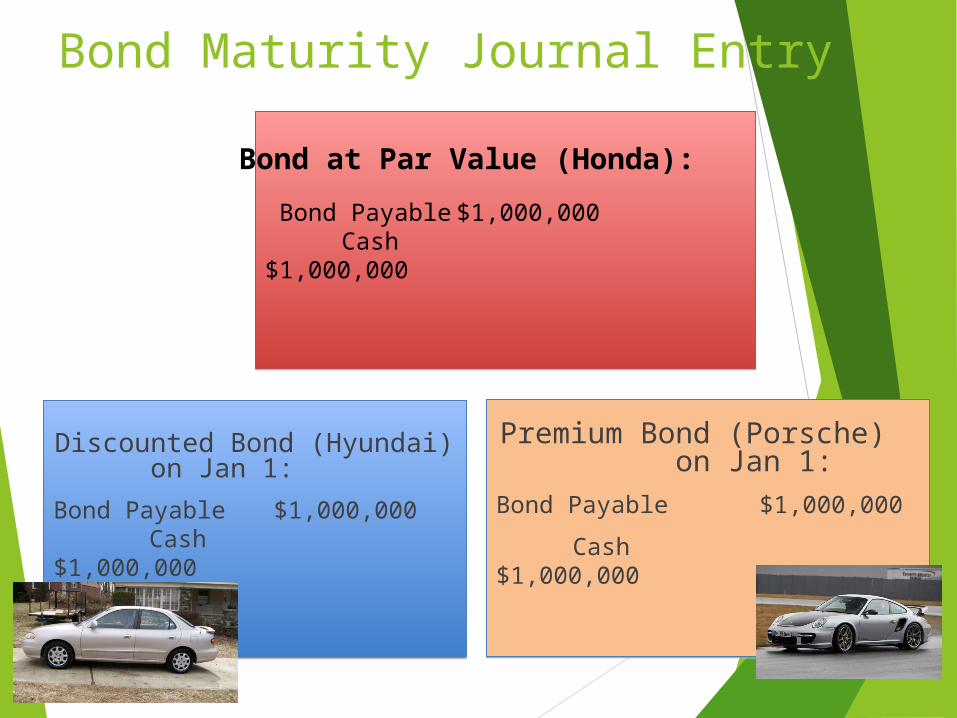

Bond Maturity Journal Entry

Discounted Bond (Hyundai) on Jan 1:Bond Payable $1,000,000

Cash $1,000,000

Premium Bond (Porsche) on Jan 1:Bond Payable $1,000,000

Cash $1,000,000

Bond Payable $1,000,000 Cash $1,000,000

Bond Payable $1,000,000 Cash $1,000,000

Bond at Par Value (Honda):

Basics of Bond Valuation

The value of a bond investment is based on the SUM of

•Stream of interest payments made/received over the the life of the bond Use the market rate interest and Table B3.

PLUS•Single lump sum payment (par value) made at the bond’s maturity. Use the market rate interest and Table B1.

The Four Components of Time Value Calculations:

PV – Present Value, what is it worth today?

FV – Future Value, what is it worth in the future?

n – number of periods (i.e. months, quarter, year)

i – interest rate % earned for each n

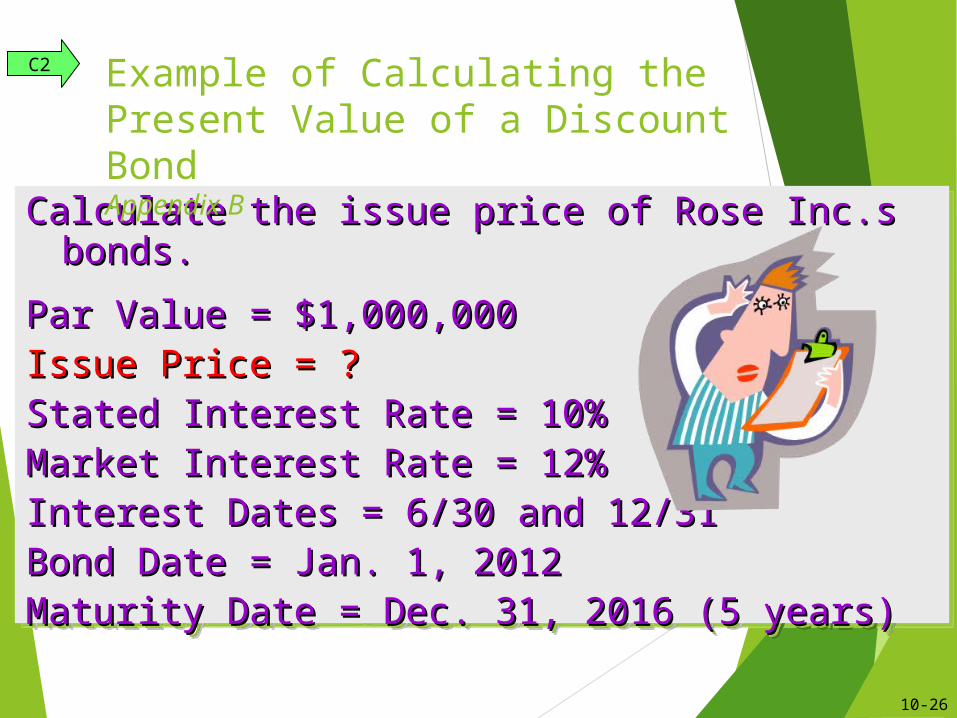

Calculate the issue price of Rose Inc.s bonds.Calculate the issue price of Rose Inc.s bonds.

Par Value = $1,000,000Par Value = $1,000,000Issue Price = ?Issue Price = ?Stated Interest Rate = 10%Stated Interest Rate = 10%Market Interest Rate = 12%Market Interest Rate = 12%Interest Dates = 6/30 and 12/31Interest Dates = 6/30 and 12/31Bond Date = Jan. 1, 2012Bond Date = Jan. 1, 2012Maturity Date = Dec. 31, 2016 (5 years)Maturity Date = Dec. 31, 2016 (5 years)

Calculate the issue price of Rose Inc.s bonds.Calculate the issue price of Rose Inc.s bonds.

Par Value = $1,000,000Par Value = $1,000,000Issue Price = ?Issue Price = ?Stated Interest Rate = 10%Stated Interest Rate = 10%Market Interest Rate = 12%Market Interest Rate = 12%Interest Dates = 6/30 and 12/31Interest Dates = 6/30 and 12/31Bond Date = Jan. 1, 2012Bond Date = Jan. 1, 2012Maturity Date = Dec. 31, 2016 (5 years)Maturity Date = Dec. 31, 2016 (5 years)

Example of Calculating the Present Value of a Discount BondAppendix B

C2

10-26

Present Value of a Discount Bond

1.1. Semiannual rate = 6% (Market rate 12% ÷ 2)Semiannual rate = 6% (Market rate 12% ÷ 2)

2.2. Semiannual periods = 10 (Bond life 5 years × 2)Semiannual periods = 10 (Bond life 5 years × 2)

1.1. Semiannual rate = 6% (Market rate 12% ÷ 2)Semiannual rate = 6% (Market rate 12% ÷ 2)

2.2. Semiannual periods = 10 (Bond life 5 years × 2)Semiannual periods = 10 (Bond life 5 years × 2)

$1,000,000 × 10% $1,000,000 × 10% (stated rate)(stated rate) × ½ = × ½ = $50,000$50,000

$1,000,000 × 10% $1,000,000 × 10% (stated rate)(stated rate) × ½ = × ½ = $50,000$50,000

C2

10-27

Ex 10-9

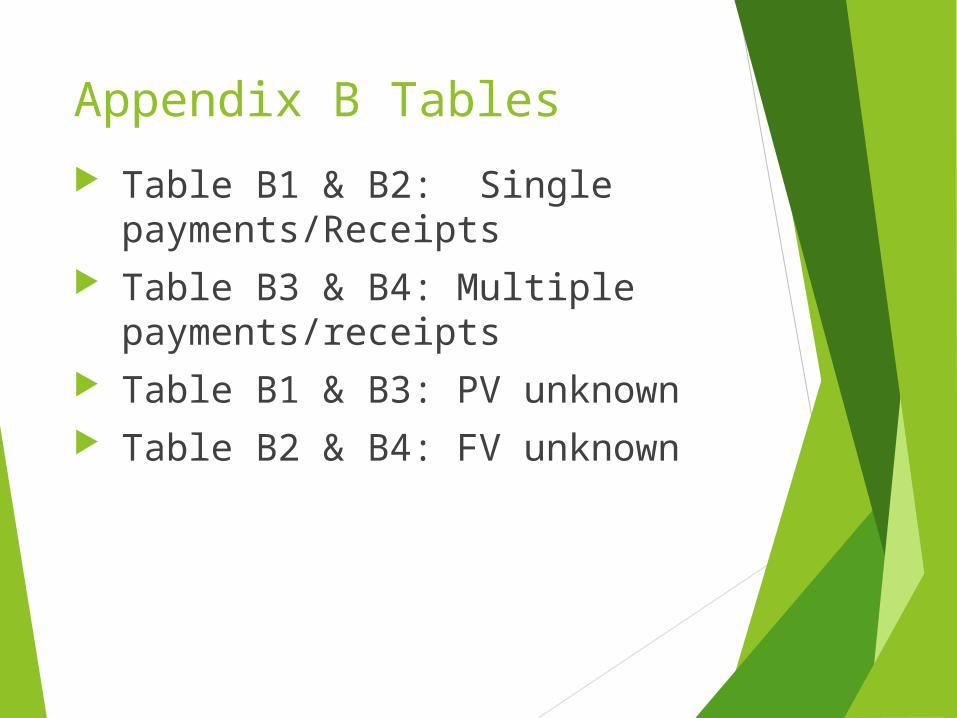

Appendix B Tables

Table B1 & B2: Single payments/Receipts

Table B3 & B4: Multiple payments/receipts

Table B1 & B3: PV unknown Table B2 & B4: FV unknown

Time Value of Money Sch B-1 & B-2: A single payment

B-1: If I wanted to have $xx (known factor) in a future period, how much would I have to deposit today? I.e., If I need $5,000 for a down payment in 2 years, how much do I need to deposit in the bank today?

B-2: If I deposited $xx (known factor) today, how much would I have in the future? I.e., If I deposit $3,000 today, how much will I have in 2 years for the down payment on my car?

Table B1 & B2 Single Payment/Receipt

Table B1 PV

Unknown

FV Known

Table B2PV Known

FV Unknown

Time Value of Money Sch B-3 & B-4:

Sch B-3: If I want to have a future series of $xx payments (known factor) in the future, how much would I have to deposit today? I.e., If I want to have $1,000 paid to me every month during my retirement of 20 years, how much do I have to deposit today?

Sch B-4: If I deposit a series of $xx payments, how much will I have in the future? I.e., if I deposit $100 every month for the next 30 years, how much will I have saved for retirement?

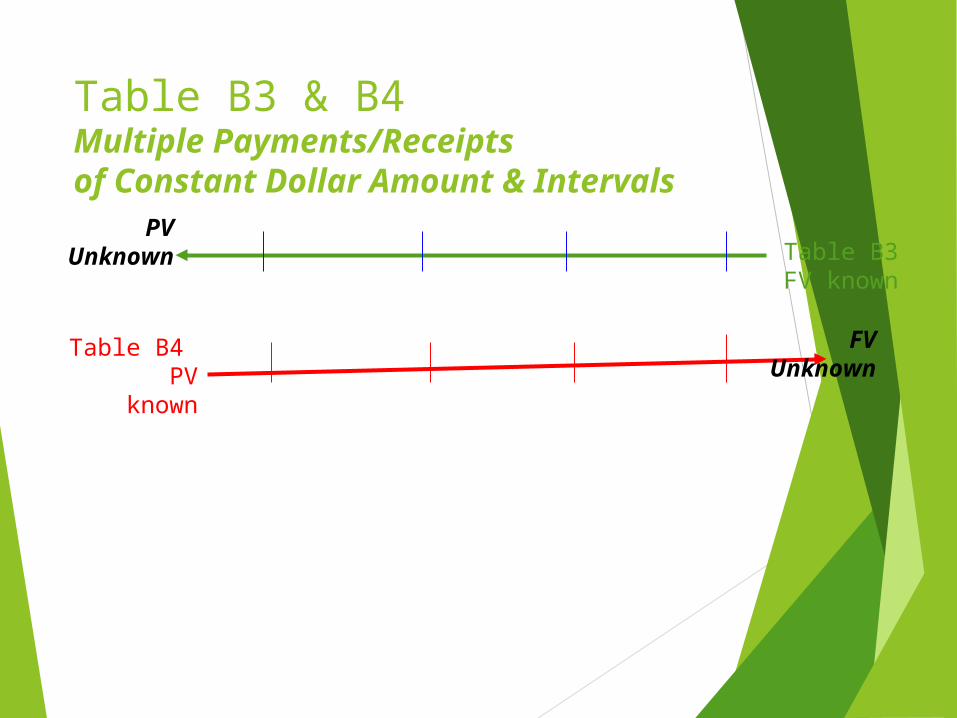

Table B3 & B4 Multiple Payments/Receipts of Constant Dollar Amount & Intervals

PV Unknown Table B3

FV known

Table B4 PV known

FV Unknown

Vocabulary

Annuity Net Carrying Value Bond Premium, Discount or Par Bond types (know what each is)

(p. 426): Secured & Unsecured; Term & Serial; Registered & Bearer; Convertible & Callable

Debt to Equity Ratio

Mortgage Notes and Bonds

A legal agreement that helps protect the lender if A legal agreement that helps protect the lender if the borrower fails to make the required payments.the borrower fails to make the required payments.

Gives the lender the right to be paid out of the Gives the lender the right to be paid out of the cash proceeds from the sale of the borrowercash proceeds from the sale of the borrower’’s s assets specifically identified in the mortgage assets specifically identified in the mortgage contract. contract.

A legal agreement that helps protect the lender if A legal agreement that helps protect the lender if the borrower fails to make the required payments.the borrower fails to make the required payments.

Gives the lender the right to be paid out of the Gives the lender the right to be paid out of the cash proceeds from the sale of the borrowercash proceeds from the sale of the borrower’’s s assets specifically identified in the mortgage assets specifically identified in the mortgage contract. contract.

C1

10-35

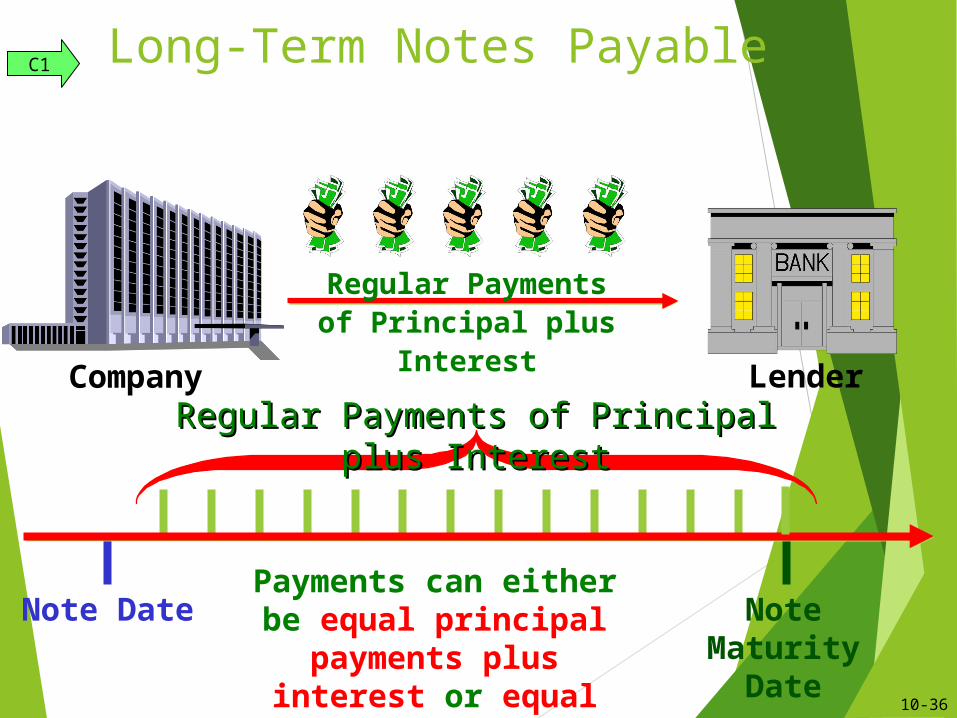

Note Maturity Date

Company Lender

Note Date

Long-Term Notes Payable

Regular Payments of Principal plus InterestRegular Payments of Principal plus Interest

Payments can either be equal principal payments

plus interest or equal payments.

Regular Payments of Principal plus Interest

C1

10-36

Installment Notes with Equal Payments

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Interest

Principal

The principal payments increase each year. The principal payments increase each year. Interest expense decreases each year.Interest expense decreases each year.

The principal payments increase each year. The principal payments increase each year. Interest expense decreases each year.Interest expense decreases each year.

Annual Annual payments are payments are

constant.constant.

C1

10-37

Debt-to-

Equity Ratio

Total Liabilities

Total Equity=

This ratio helps investors determine the risk of This ratio helps investors determine the risk of investing in a company by dividing its total liabilities investing in a company by dividing its total liabilities

by total equity.by total equity.

This ratio helps investors determine the risk of This ratio helps investors determine the risk of investing in a company by dividing its total liabilities investing in a company by dividing its total liabilities

by total equity.by total equity.

Debt-to-Equity RatioA3

10-38