accounting for tax - its management sdn bhd · business goods (e.g. furniture, tableware,...

TRANSCRIPT

GST SEMINAR:

Accounting For Tax

Melaka

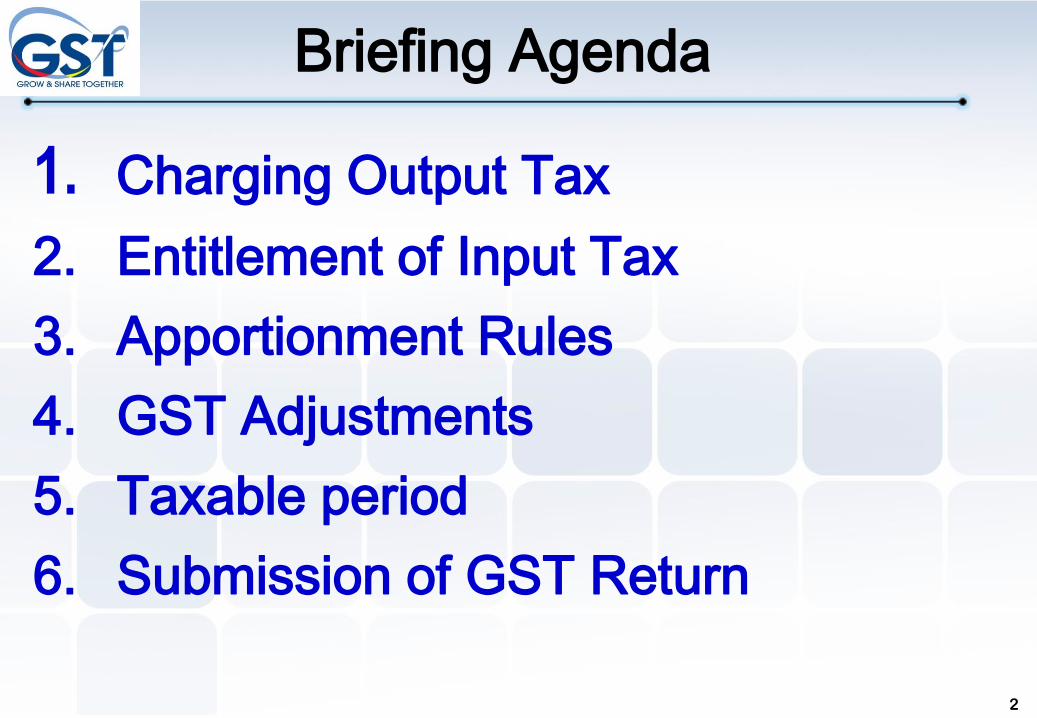

Briefing Agenda

1. Charging Output Tax

2. Entitlement of Input Tax

3. Apportionment Rules

4. GST Adjustments

5. Taxable period

6. Submission of GST Return

2

1

3

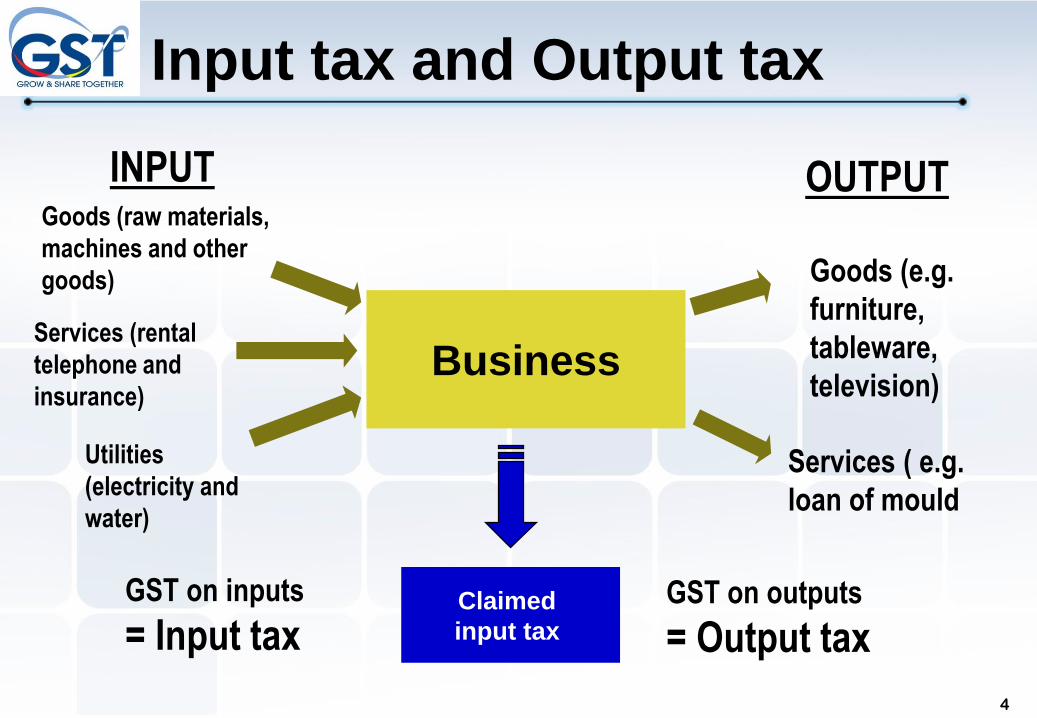

Business

Goods (e.g.

furniture,

tableware,

television)

Services ( e.g.

loan of mould

INPUT OUTPUT

GST on inputs

= Input taxClaimed

input tax

GST on outputs

= Output tax

4

Goods (raw materials,

machines and other

goods)

Services (rental

telephone and

insurance)

Utilities

(electricity and

water)

Input tax and Output tax

5

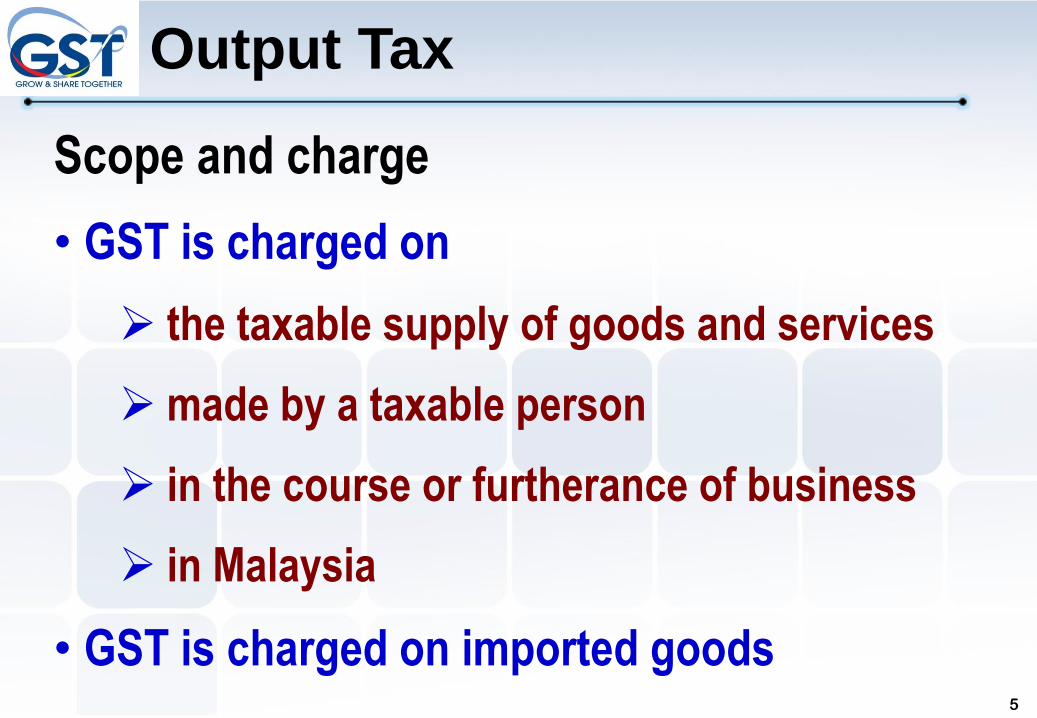

Scope and charge

• GST is charged on

the taxable supply of goods and services

made by a taxable person

in the course or furtherance of business

in Malaysia

• GST is charged on imported goods

Output Tax

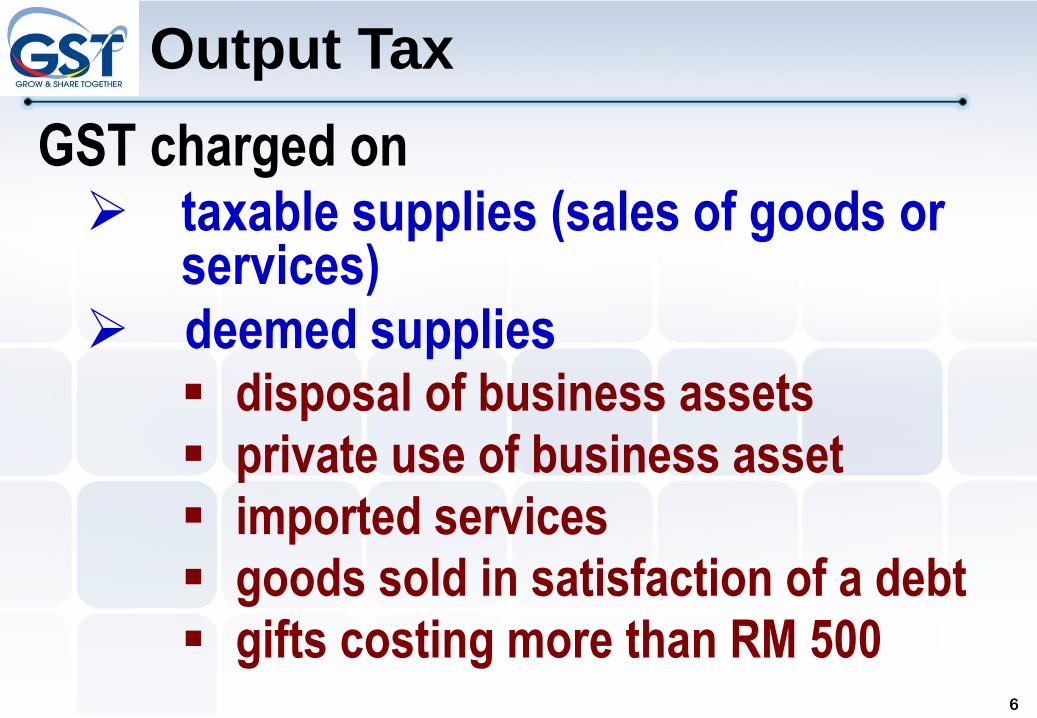

6

GST charged on taxable supplies (sales of goods or

services) deemed supplies

disposal of business assets private use of business asset imported services goods sold in satisfaction of a debt gifts costing more than RM 500

Output Tax

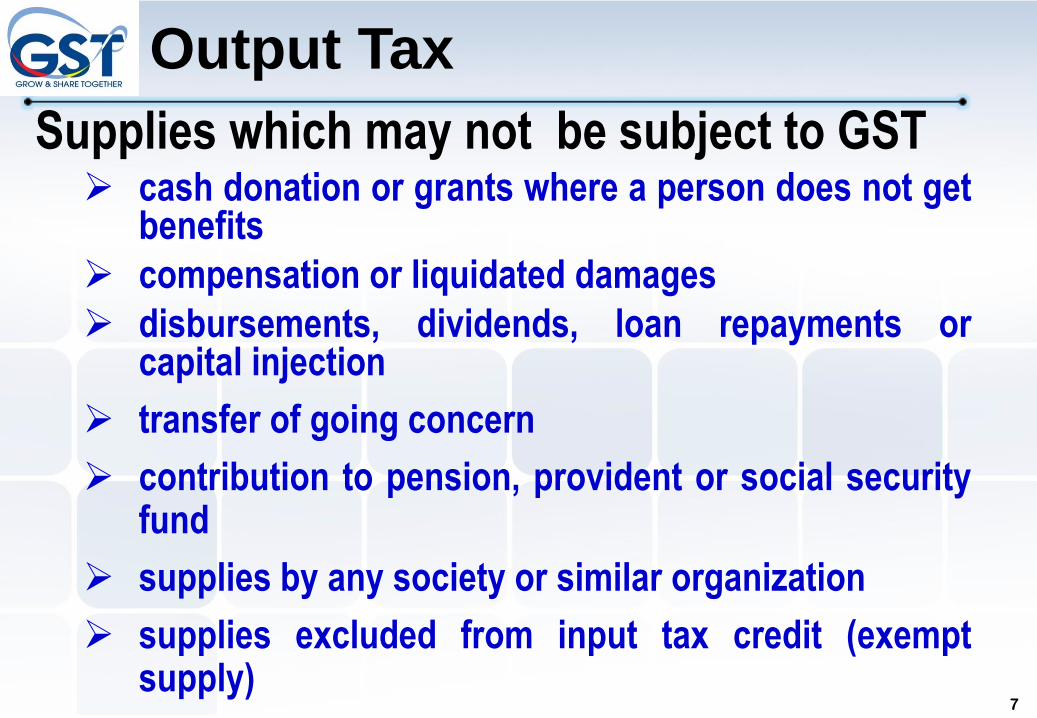

7

Supplies which may not be subject to GST cash donation or grants where a person does not get

benefits

compensation or liquidated damages

disbursements, dividends, loan repayments orcapital injection

transfer of going concern

contribution to pension, provident or social securityfund

supplies by any society or similar organization

supplies excluded from input tax credit (exemptsupply)

Output Tax

8

Issuance of Tax Invoice

Types of tax invoice when making

taxable supplies

full tax invoice

simplified tax invoice

9

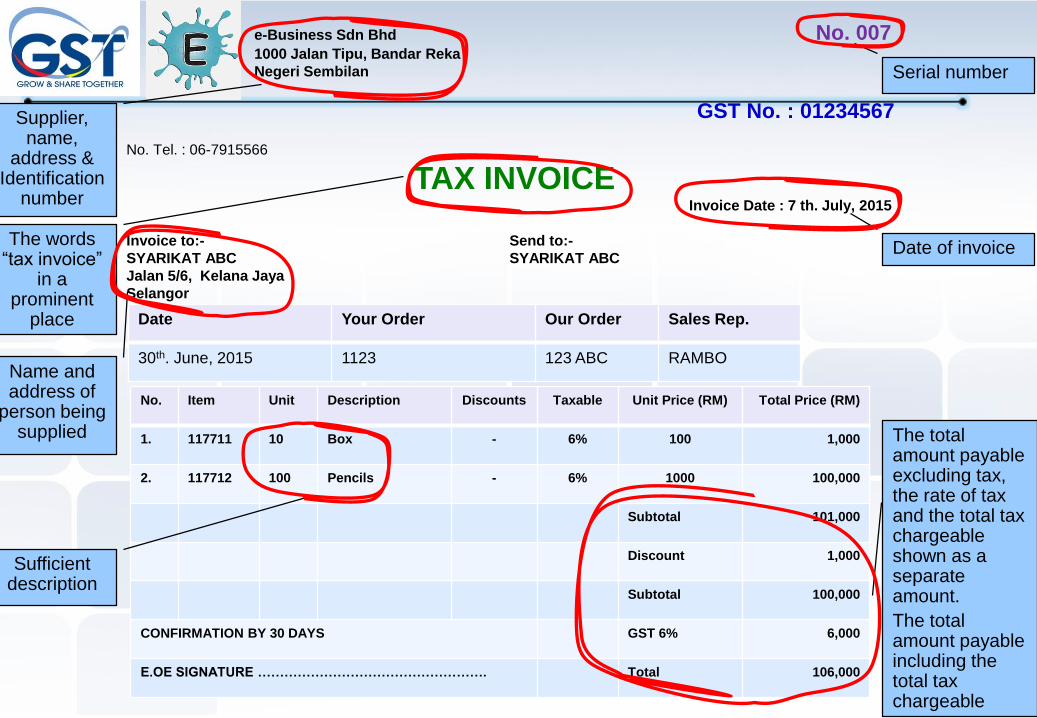

e-Business Sdn Bhd No. 0071000 Jalan Tipu, Bandar Reka

Negeri Sembilan

GST No. : 01234567

No. Tel. : 06-7915566

TAX INVOICEInvoice Date : 7 th. July, 2015

Invoice to:- Send to:-

SYARIKAT ABC SYARIKAT ABC

Jalan 5/6, Kelana Jaya

Selangor

Date Your Order Our Order Sales Rep.

30th. June, 2015 1123 123 ABC RAMBO

No. Item Unit Description Discounts Taxable Unit Price (RM) Total Price (RM)

1. 117711 10 Box - 6% 100 1,000

2. 117712 100 Pencils - 6% 1000 100,000

Subtotal 101,000

Discount 1,000

Subtotal 100,000

CONFIRMATION BY 30 DAYS GST 6% 6,000

E.OE SIGNATURE ……………………………………………. Total 106,000

The total amount payable excluding tax, the rate of tax and the total tax chargeable shown as a separate amount.

The total amount payable including the total tax chargeable

Date of invoice

Serial number

Supplier, name,

address & Identification

number

The words “tax invoice”

in a prominent

place

Name and address of

person being supplied

Sufficient description

10

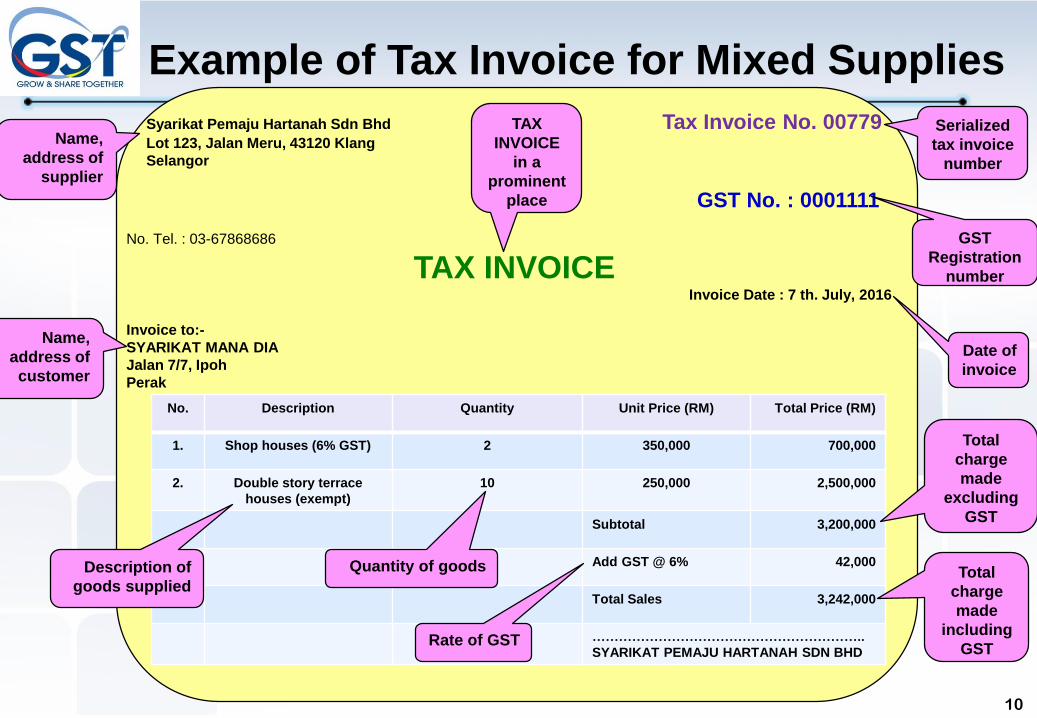

Syarikat Pemaju Hartanah Sdn Bhd Tax Invoice No. 00779Lot 123, Jalan Meru, 43120 Klang

Selangor

GST No. : 0001111

No. Tel. : 03-67868686

TAX INVOICEInvoice Date : 7 th. July, 2016

Invoice to:-

SYARIKAT MANA DIA

Jalan 7/7, Ipoh

Perak

No. Description Quantity Unit Price (RM) Total Price (RM)

1. Shop houses (6% GST) 2 350,000 700,000

2. Double story terrace

houses (exempt)

10 250,000 2,500,000

Subtotal 3,200,000

Add GST @ 6% 42,000

Total Sales 3,242,000

……………………………………………………..

SYARIKAT PEMAJU HARTANAH SDN BHD

Serialized

tax invoice

number

Date of

invoice

Total

charge

made

excluding

GST

Total

charge

made

including

GST

Quantity of goodsDescription of

goods supplied

Name,

address of

supplier

GST

Registration

number

Name,

address of

customer

TAX

INVOICE

in a

prominent

place

Rate of GST

Example of Tax Invoice for Mixed Supplies

No. Item Units Description Unit Price Total

1 2022 1 Plasma TV Somy 56

inches

8999.00 8999.00

Price 8999.00

Discount 500.00

Subtotal 8499.00

Price inclusive of GST 6% (RM509.94) Total 9008.94

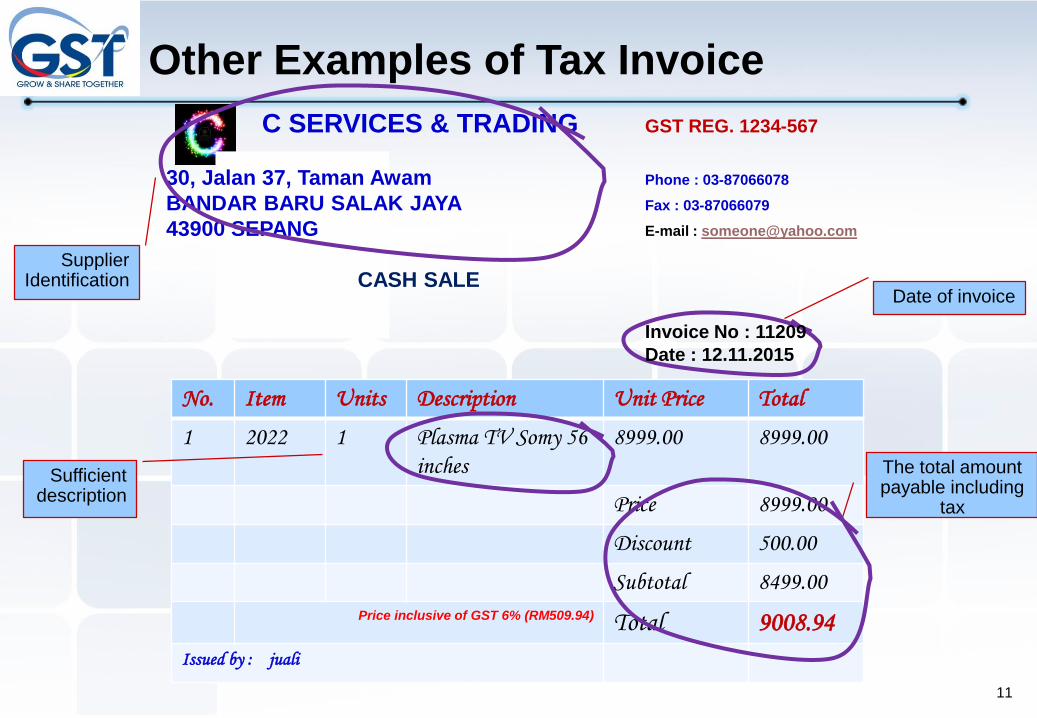

Issued by : juali

11

Supplier Identification

Date of invoice

The total amount payable including

tax

Sufficient description

C SERVICES & TRADING GST REG. 1234-567

30, Jalan 37, Taman Awam Phone : 03-87066078

BANDAR BARU SALAK JAYA Fax : 03-87066079

43900 SEPANG E-mail : [email protected]

CASH SALE

Invoice No : 11209

Date : 12.11.2015

Other Examples of Tax Invoice

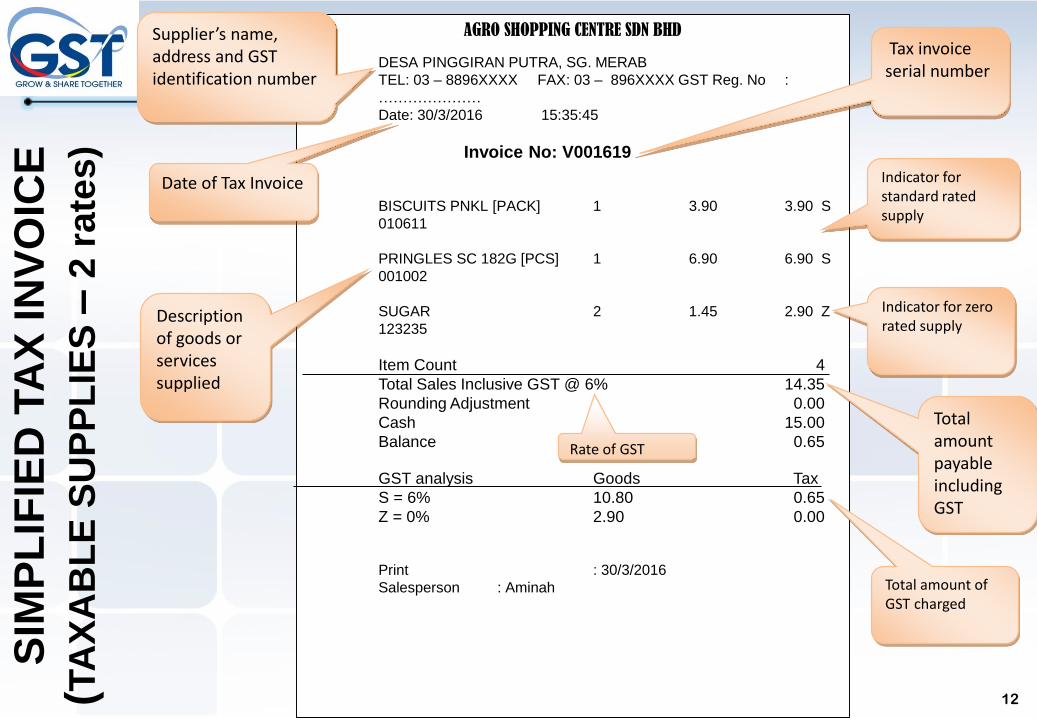

AGRO SHOPPING CENTRE SDN BHD

DESA PINGGIRAN PUTRA, SG. MERAB

TEL: 03 – 8896XXXX FAX: 03 – 896XXXX GST Reg. No :

…………………

Date: 30/3/2016 15:35:45

Invoice No: V001619

BISCUITS PNKL [PACK] 1 3.90 3.90 S

010611

PRINGLES SC 182G [PCS] 1 6.90 6.90 S

001002

SUGAR 2 1.45 2.90 Z

123235

Item Count 4

Total Sales Inclusive GST @ 6% 14.35

Rounding Adjustment 0.00

Cash 15.00

Balance 0.65

GST analysis Goods Tax

S = 6% 10.80 0.65

Z = 0% 2.90 0.00

Print : 30/3/2016

Salesperson : Aminah

Date of Tax Invoice

Supplier’s name, address and GST identification number

Total amount payable including GST

Description of goods or services supplied

Tax invoice serial number

12

Indicator for zero rated supply

Indicator for standard rated supply

Rate of GST

Total amount of GST charged

SIM

PL

IFIE

D T

AX

IN

VO

ICE

(TA

XA

BL

E S

UP

PL

IES

–2

ra

tes

)

2

13

14

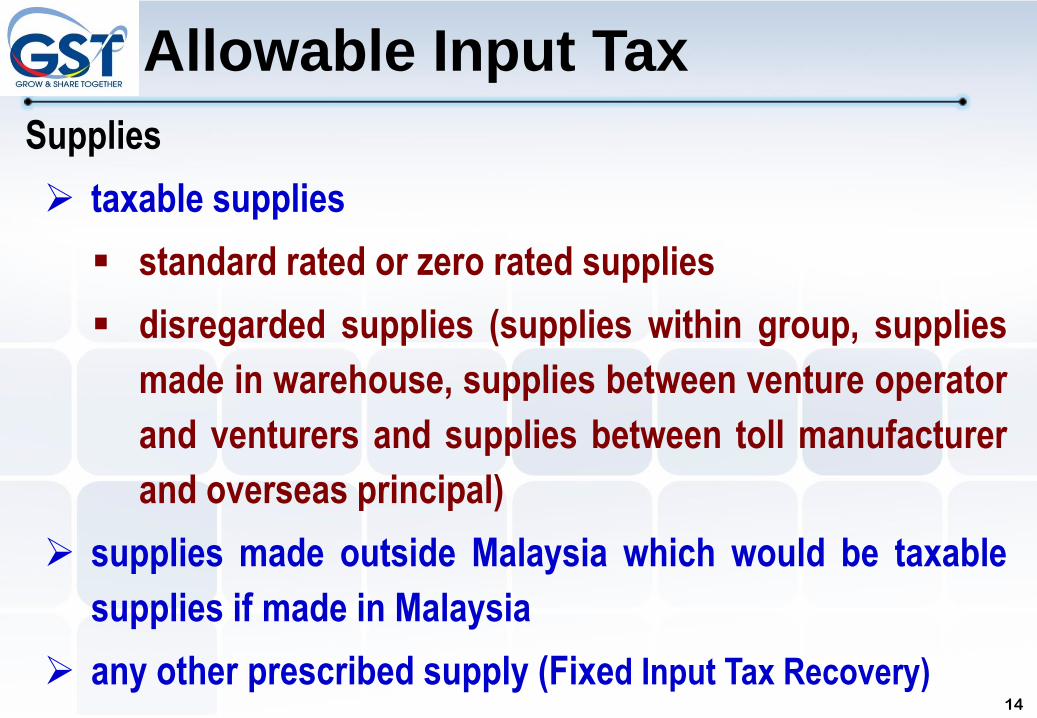

Allowable Input Tax

Supplies

taxable supplies

standard rated or zero rated supplies

disregarded supplies (supplies within group, supplies

made in warehouse, supplies between venture operator

and venturers and supplies between toll manufacturer

and overseas principal)

supplies made outside Malaysia which would be taxable

supplies if made in Malaysia

any other prescribed supply (Fixed Input Tax Recovery)

Purchase

clothes

15

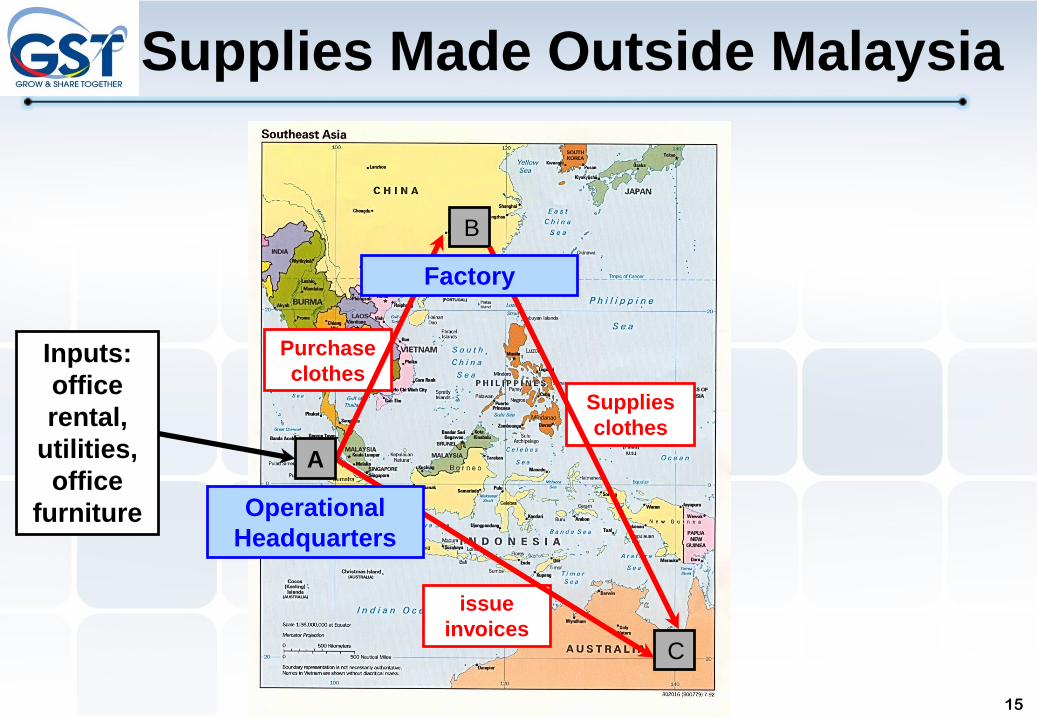

Supplies Made Outside Malaysia

issue

invoices

Supplies

clothes

A

B

C

Operational

Headquarters

Factory

Inputs:

office

rental,

utilities,

office

furniture

16

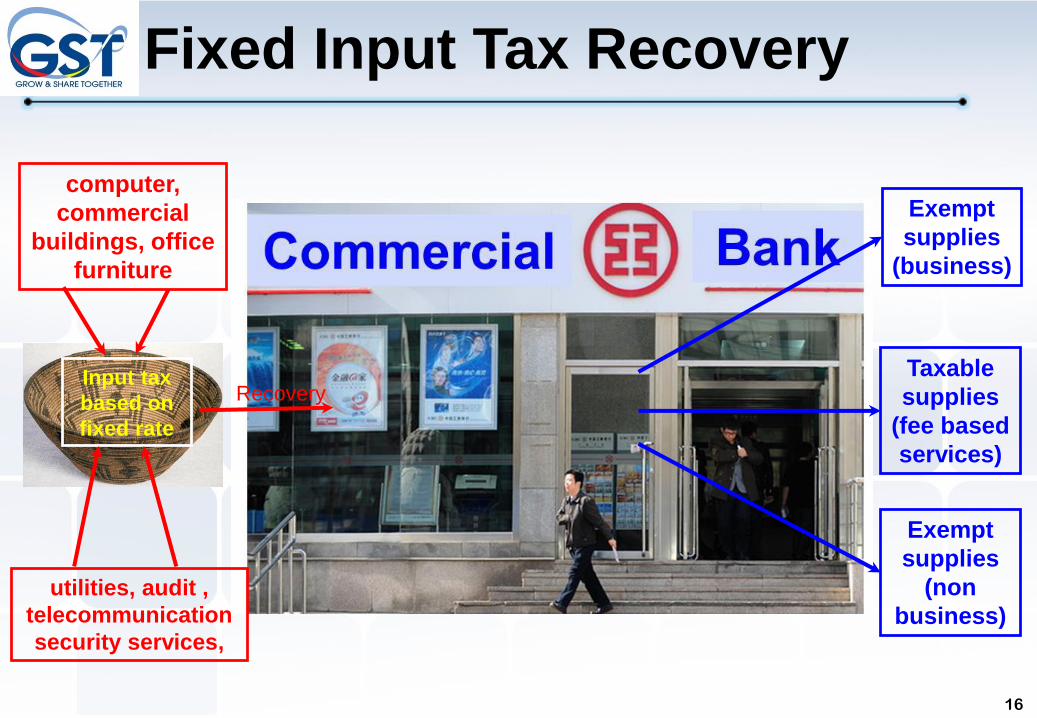

Fixed Input Tax Recovery

Input tax

based on

fixed rate

computer,

commercial

buildings, office

furniture

utilities, audit ,

telecommunication

security services,

Recovery

Exempt

supplies

(business)

Exempt

supplies

(non

business)

Taxable

supplies

(fee based

services)

17

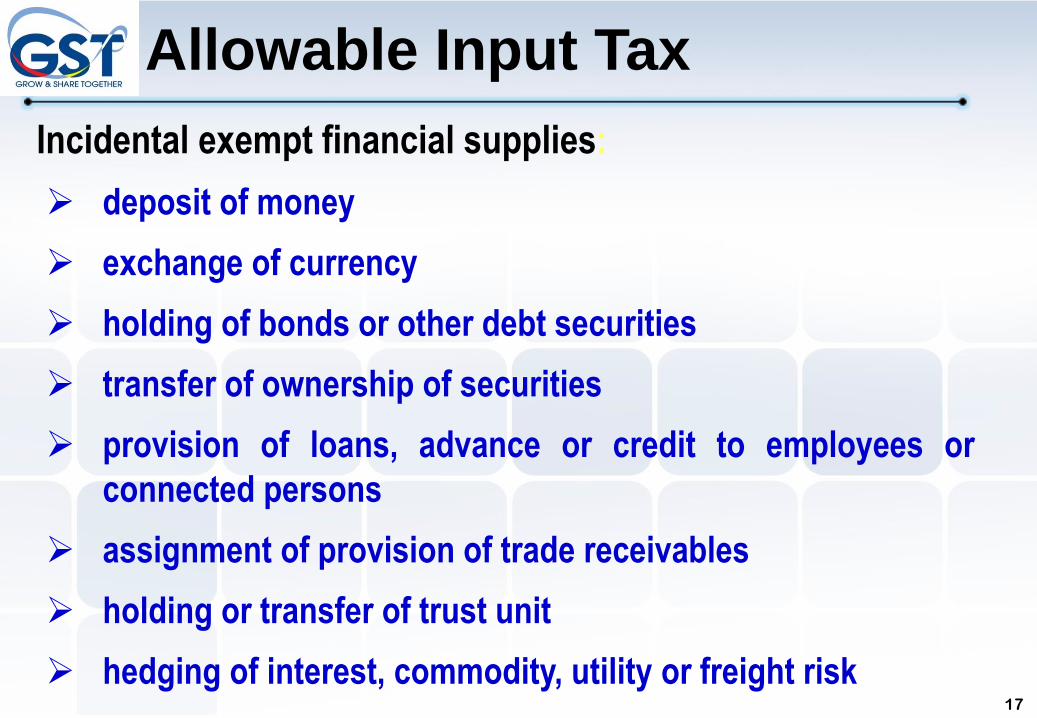

Allowable Input Tax

Incidental exempt financial supplies:

deposit of money

exchange of currency

holding of bonds or other debt securities

transfer of ownership of securities

provision of loans, advance or credit to employees or

connected persons

assignment of provision of trade receivables

holding or transfer of trust unit

hedging of interest, commodity, utility or freight risk

18

Incidental Exempt Financial Supplies

Special tax treatment does not apply to:

banks

development financial institutions or money

lenders

insurance company

stock or futures brokers

pawn broker or hire purchase companies

debt factor or credit or debit card companies

investment or unit trust or venture capital company

19

Input Tax Credit

Input Tax Mechanism

Tax paid on inputs to be offset against the output tax in the

relevant taxable period

Subject to a time limit of 6 years from the date of return

required to be made

Apportionment rule to apply for a mixed supply

Refund to be offset against other unpaid GST, customs and

excise duties

Net tax to be refunded within

14 working days for on-line submission

28 working days for manual submission

20

Conditions:

Claimant must be a taxable person

Must have a valid tax invoice full tax invoice

simplified tax invoice - claim the input tax up to a limit of RM30.00 if name and addressof recipient is not stated in invoice (GST at 6%)

invoice issued by approved person under Flat Rate Scheme

Customs No 1 /Customs 9 (imported goods)

document to show claimant pays imported services

Invoice issued under the name of the claimant

Goods and services acquired are not subject to any inputtax restriction e.g., motorcars

Good and services are acquired for the purpose of makingtaxable supply

Input Tax Credit

21

Non Allowable Input Tax

Blocked input tax

passenger motor cars including hiring of car

22

Blocked Input Tax

Family benefits

any benefits (including hospitality of any kind) provided

by the taxable person for the benefit of any person who

is the wife, husband, child or relative of any person

employed by the taxable person for the purposes of any

business carried on or to be carried on by the taxable

person

23

Club subscription fee

any joining fee, subscription

fee, membership fee, transfer

fee or other consideration

charged by any club,

association, society or

organization established

principally for recreational or

sporting purposes or by the

transferor of the membership

or such club, association,

society or organization

Blocked Input Tax

24

medical and personal accident insurance

Blocked Input Tax

25

Medical expenses

any medical expenses in

connection with the provision of

medical treatment to any person

employed by a taxable person

Blocked Input Tax

26

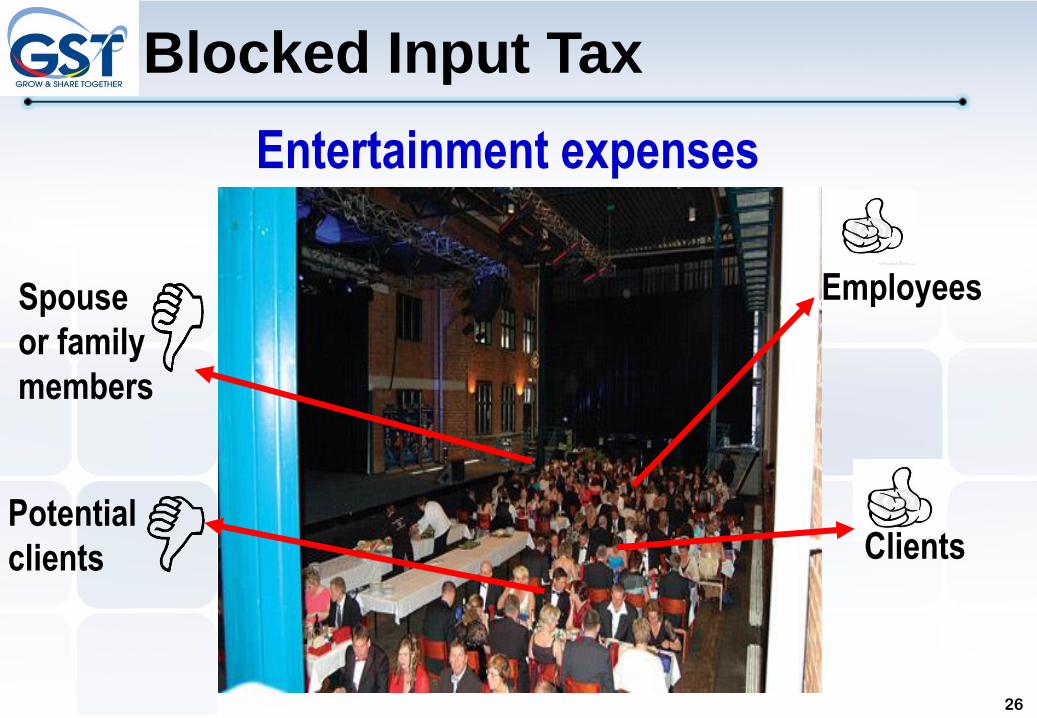

Entertainment expenses

ClientsPotential

clients

Spouse

or family

members

Employees

Blocked Input Tax

3

27

28

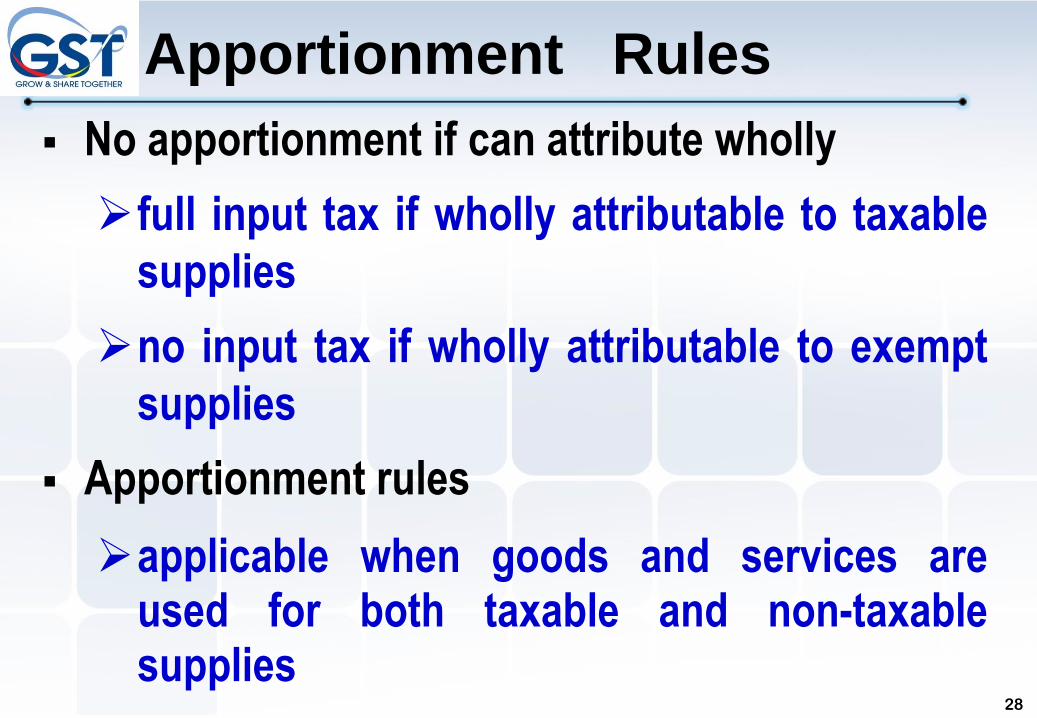

Apportionment Rules

No apportionment if can attribute wholly

full input tax if wholly attributable to taxable

supplies

no input tax if wholly attributable to exempt

supplies

Apportionment rules

applicable when goods and services areused for both taxable and non-taxablesupplies

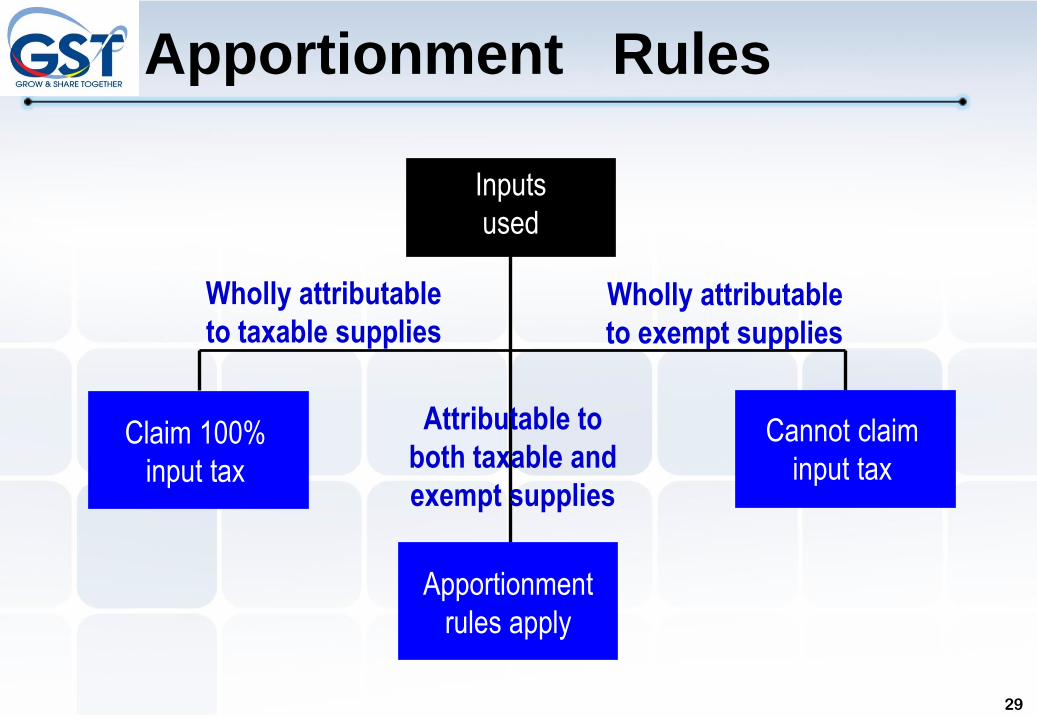

29

Claim 100%

input tax

Inputs

used

Attributable to

both taxable and

exempt supplies

Wholly attributable

to taxable suppliesWholly attributable

to exempt supplies

Apportionment

rules apply

Cannot claim

input tax

Apportionment Rules

30

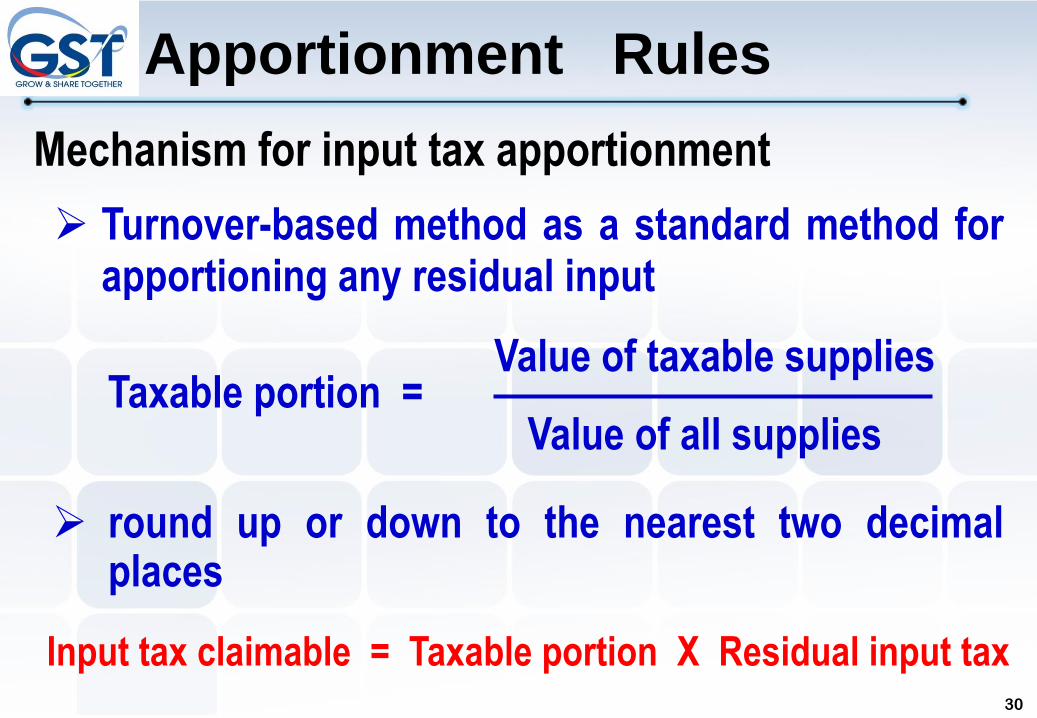

Mechanism for input tax apportionment

Turnover-based method as a standard method forapportioning any residual input

round up or down to the nearest two decimalplaces

Value of taxable supplies

Value of all supplies Taxable portion =

Input tax claimable = Taxable portion X Residual input tax

Apportionment Rules

31

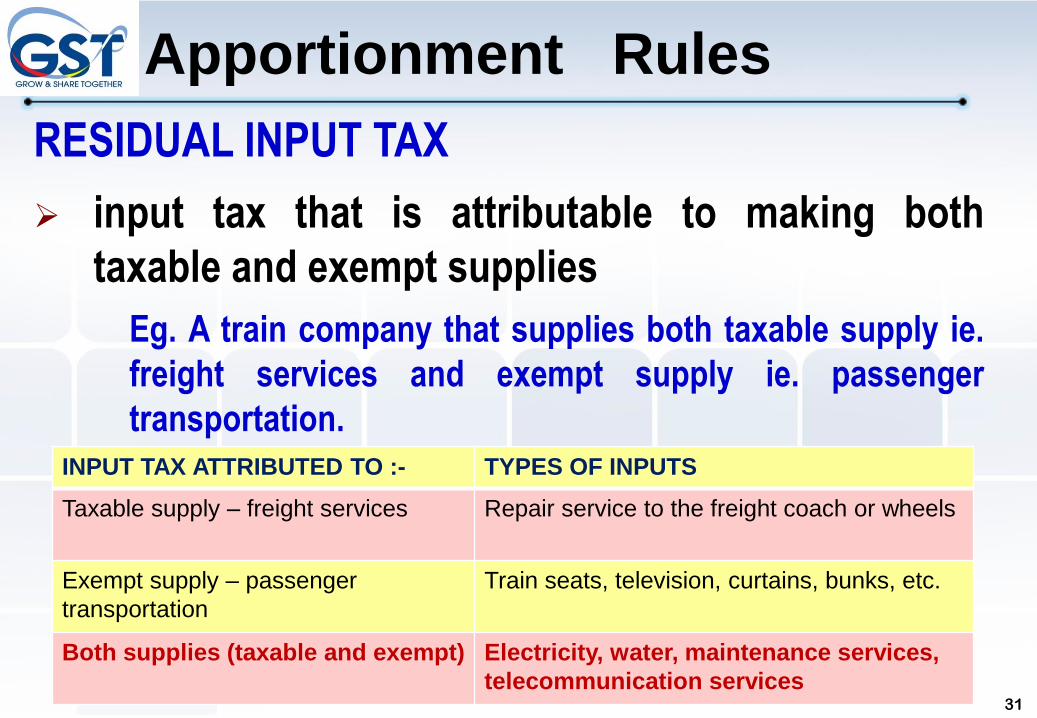

RESIDUAL INPUT TAX

input tax that is attributable to making both

taxable and exempt supplies

Eg. A train company that supplies both taxable supply ie.

freight services and exempt supply ie. passenger

transportation.

Apportionment Rules

INPUT TAX ATTRIBUTED TO :- TYPES OF INPUTS

Taxable supply – freight services Repair service to the freight coach or wheels

Exempt supply – passenger

transportation

Train seats, television, curtains, bunks, etc.

Both supplies (taxable and exempt) Electricity, water, maintenance services,

telecommunication services

32

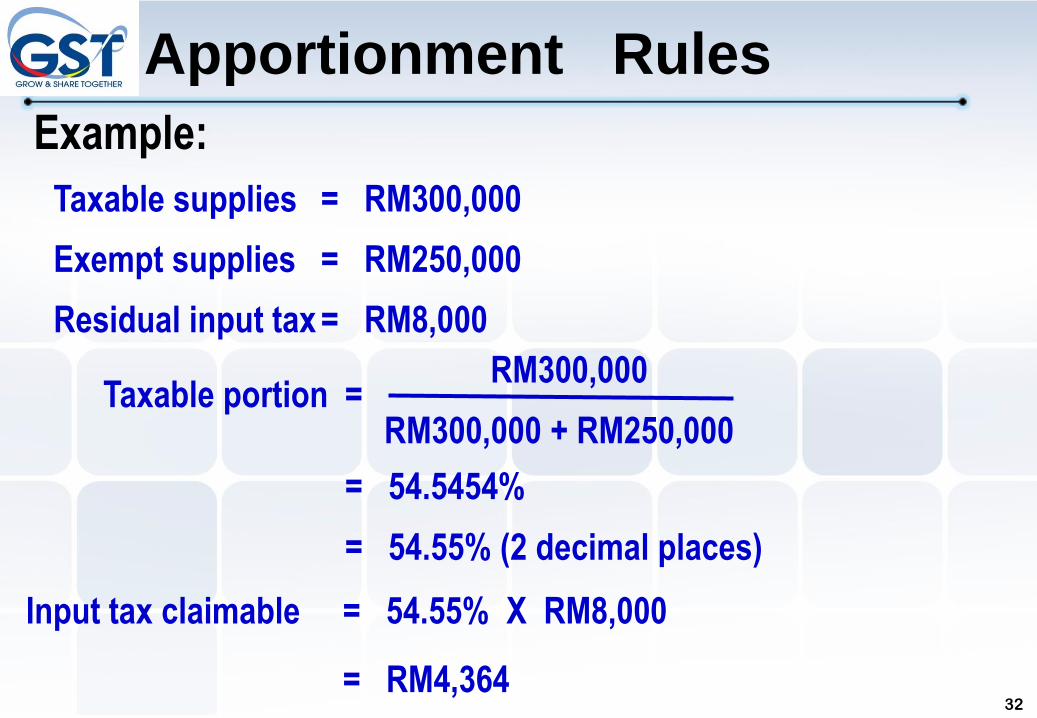

Example:

Taxable supplies = RM300,000

Exempt supplies = RM250,000

Residual input tax = RM8,000

RM300,000

RM300,000 + RM250,000Taxable portion =

= 54.5454%

= 54.55% (2 decimal places)

Input tax claimable = 54.55% X RM8,000

= RM4,364

Apportionment Rules

33

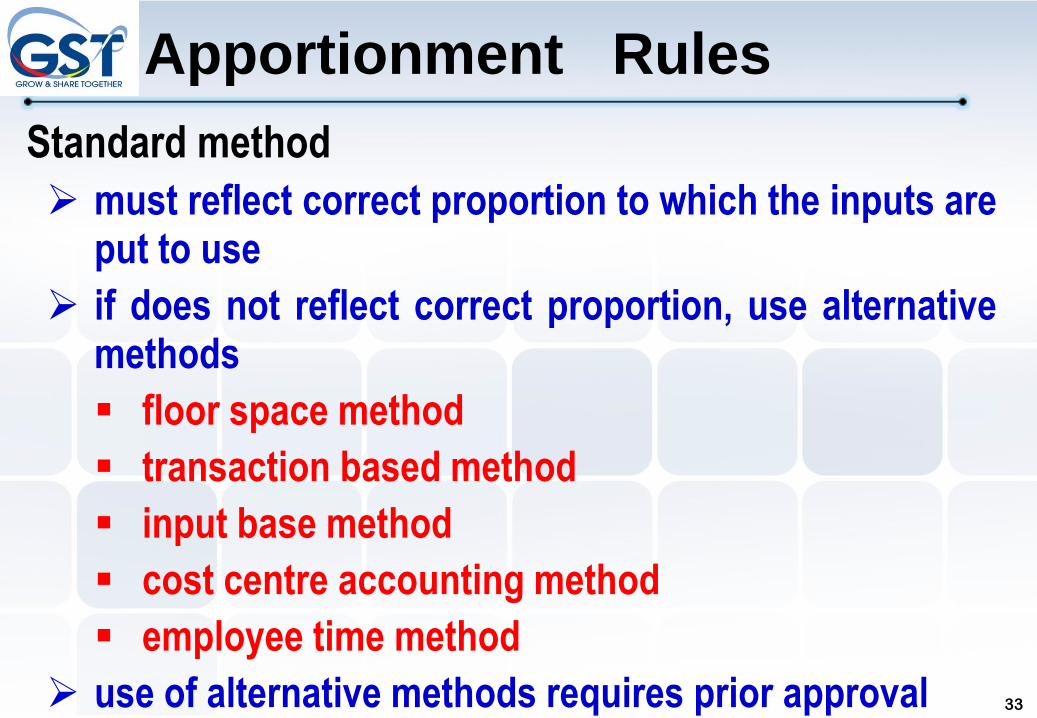

Standard method

must reflect correct proportion to which the inputs areput to use

if does not reflect correct proportion, use alternativemethods

floor space method

transaction based method

input base method

cost centre accounting method

employee time method

use of alternative methods requires prior approval

Apportionment Rules

34

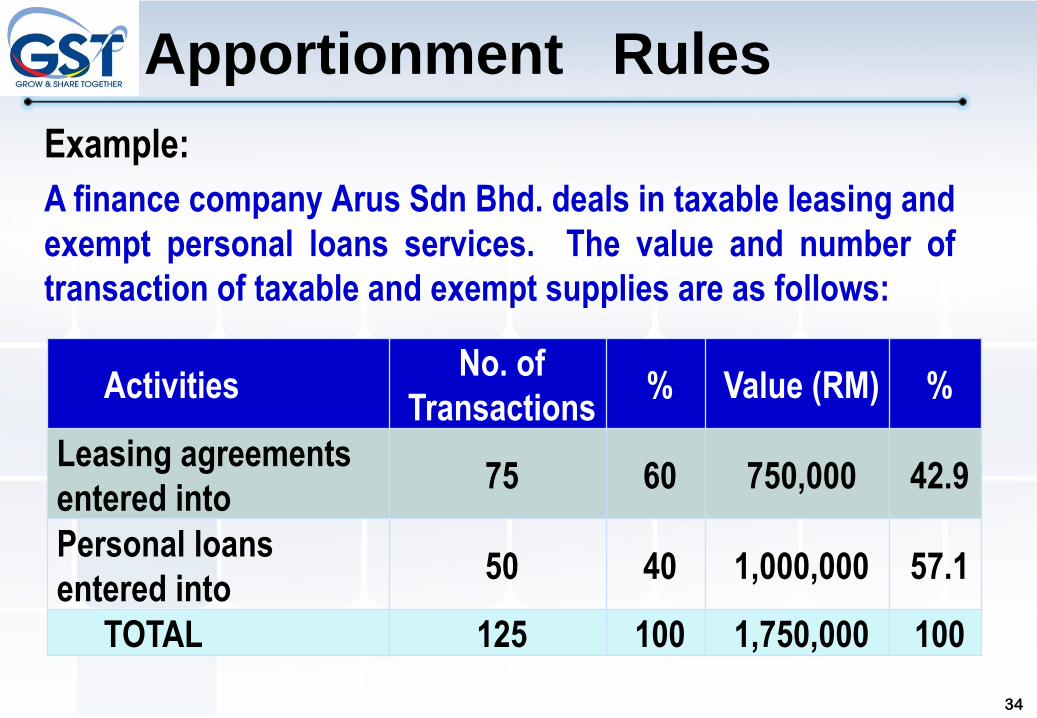

Example:

A finance company Arus Sdn Bhd. deals in taxable leasing and

exempt personal loans services. The value and number of

transaction of taxable and exempt supplies are as follows:

ActivitiesNo. of

Transactions% Value (RM) %

Leasing agreements

entered into75 60 750,000 42.9

Personal loans

entered into50 40 1,000,000 57.1

TOTAL 125 100 1,750,000 100

Apportionment Rules

35

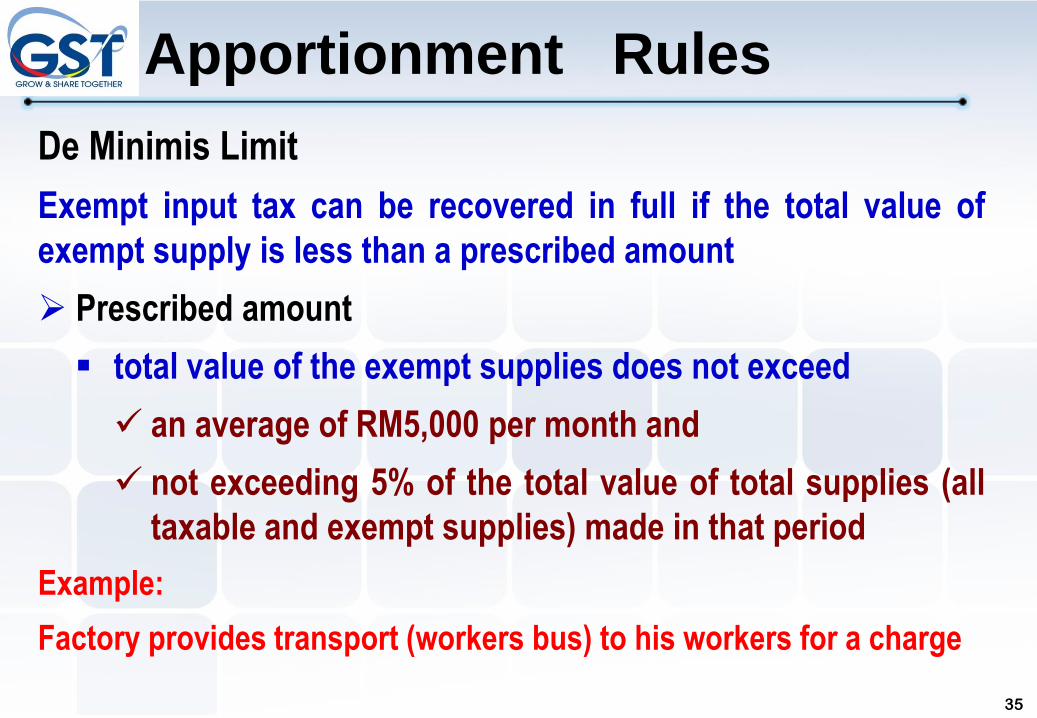

De Minimis Limit

Exempt input tax can be recovered in full if the total value of

exempt supply is less than a prescribed amount

Prescribed amount

total value of the exempt supplies does not exceed

an average of RM5,000 per month and

not exceeding 5% of the total value of total supplies (all

taxable and exempt supplies) made in that period

Example:

Factory provides transport (workers bus) to his workers for a charge

Apportionment Rules

36

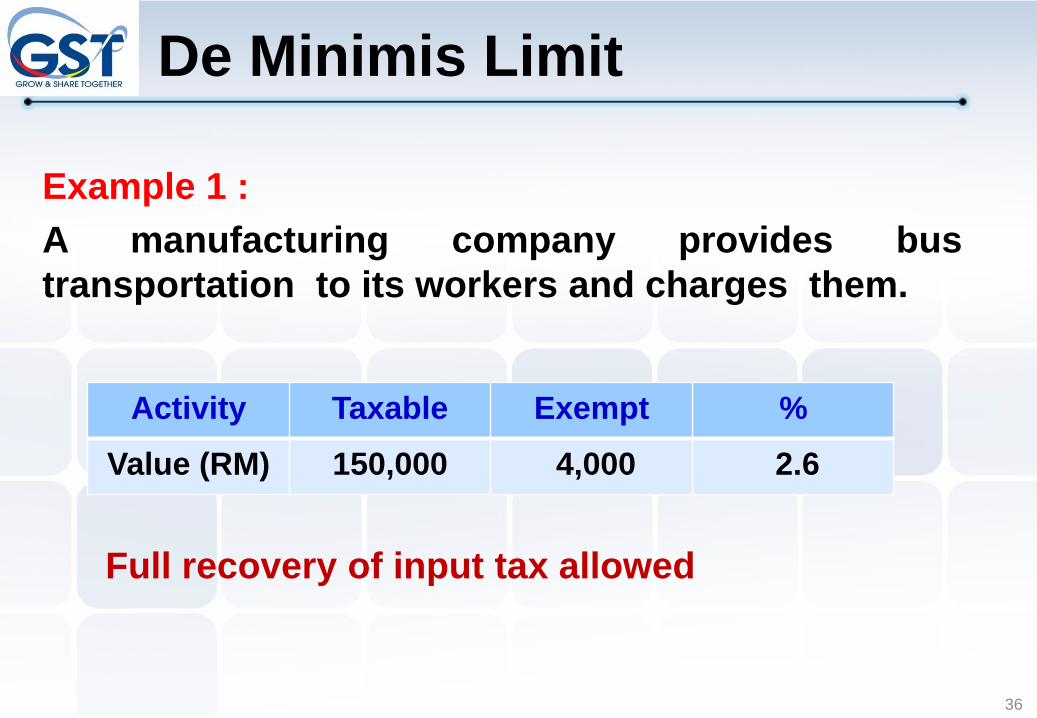

De Minimis Limit

Example 1 :

A manufacturing company provides bus

transportation to its workers and charges them.

Activity Taxable Exempt %

Value (RM) 150,000 4,000 2.6

Full recovery of input tax allowed

37

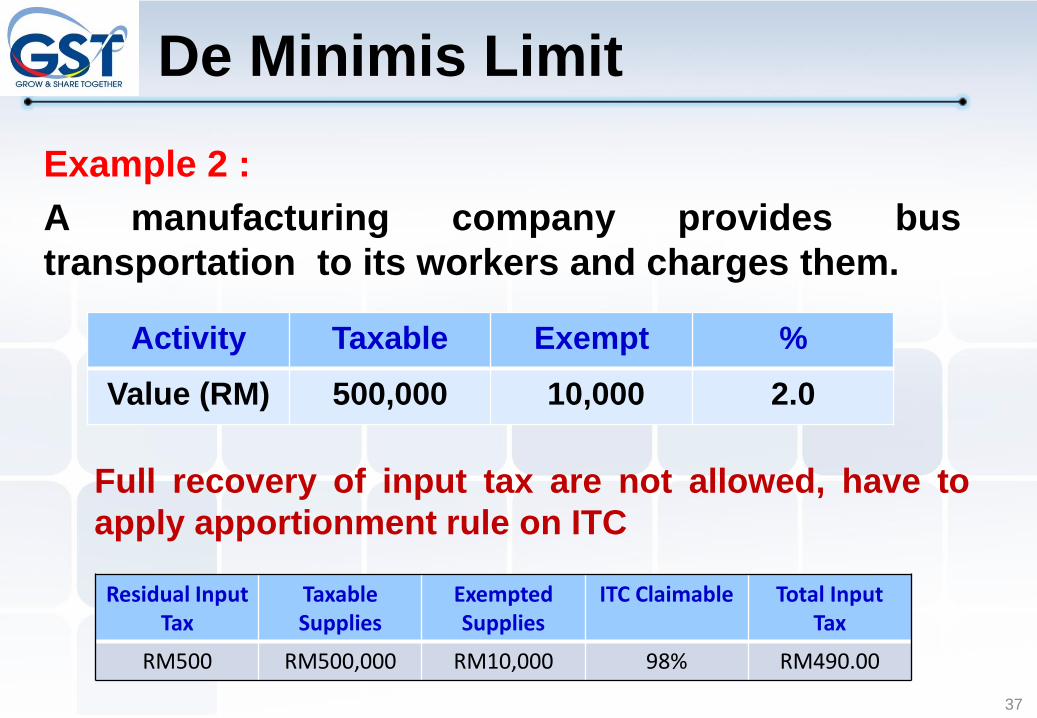

Example 2 :

A manufacturing company provides bus

transportation to its workers and charges them.

Activity Taxable Exempt %

Value (RM) 500,000 10,000 2.0

Full recovery of input tax are not allowed, have to

apply apportionment rule on ITC

Residual Input Tax

Taxable Supplies

Exempted Supplies

ITC Claimable Total Input Tax

RM500 RM500,000 RM10,000 98% RM490.00

De Minimis Limit

4

38

39

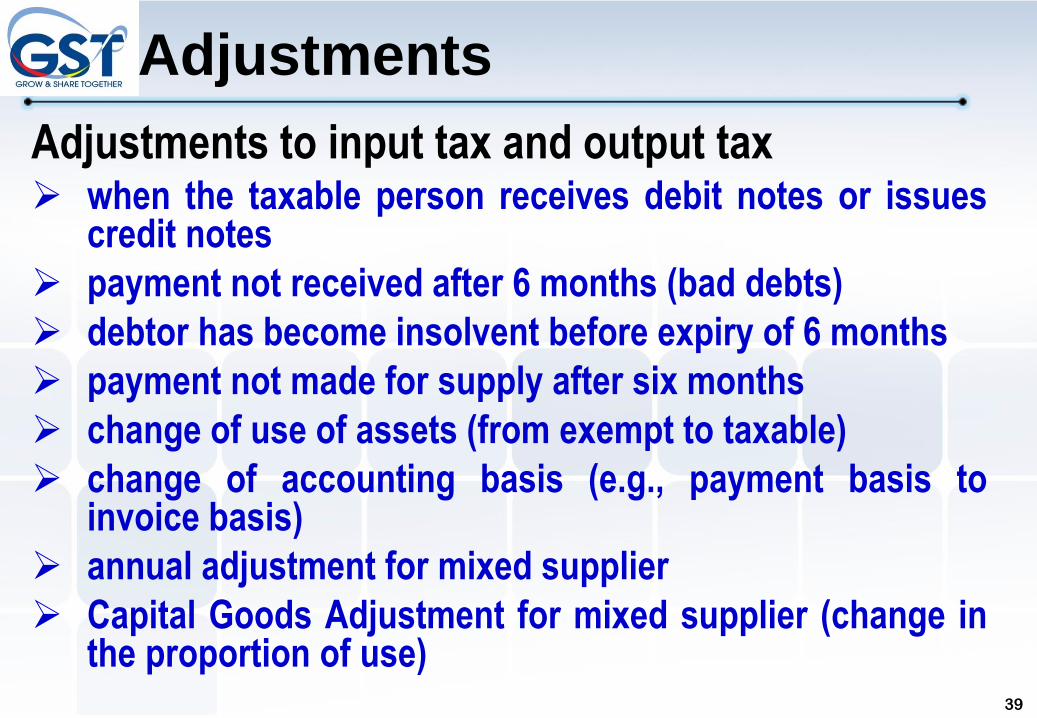

Adjustments to input tax and output tax when the taxable person receives debit notes or issues

credit notes

payment not received after 6 months (bad debts)

debtor has become insolvent before expiry of 6 months

payment not made for supply after six months

change of use of assets (from exempt to taxable)

change of accounting basis (e.g., payment basis toinvoice basis)

annual adjustment for mixed supplier

Capital Goods Adjustment for mixed supplier (change inthe proportion of use)

Adjustments

40

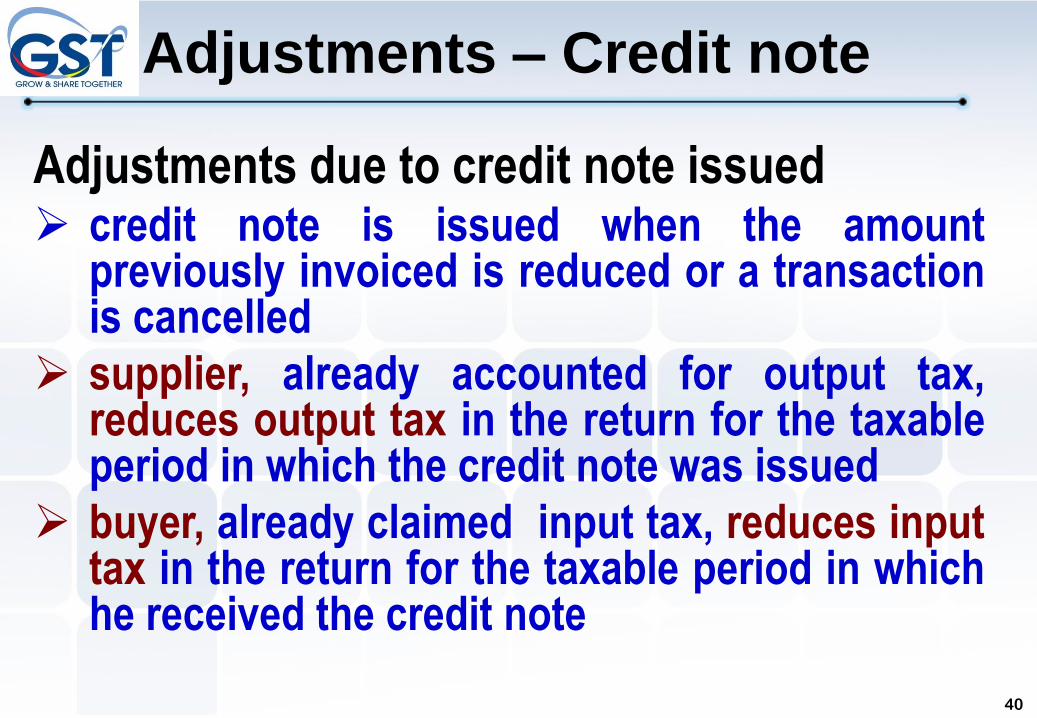

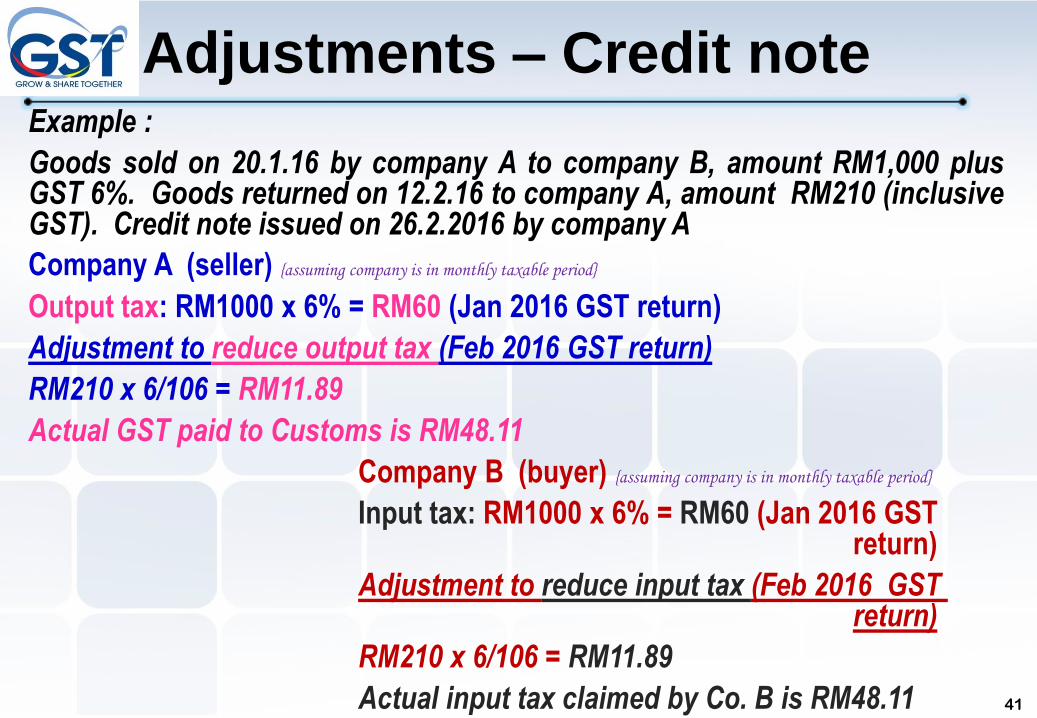

Adjustments due to credit note issued credit note is issued when the amount

previously invoiced is reduced or a transactionis cancelled

supplier, already accounted for output tax,reduces output tax in the return for the taxableperiod in which the credit note was issued

buyer, already claimed input tax, reduces inputtax in the return for the taxable period in whichhe received the credit note

Adjustments – Credit note

41

Example :

Goods sold on 20.1.16 by company A to company B, amount RM1,000 plusGST 6%. Goods returned on 12.2.16 to company A, amount RM210 (inclusiveGST). Credit note issued on 26.2.2016 by company A

Company A (seller) {assuming company is in monthly taxable period}

Output tax: RM1000 x 6% = RM60 (Jan 2016 GST return)

Adjustment to reduce output tax (Feb 2016 GST return)

RM210 x 6/106 = RM11.89

Actual GST paid to Customs is RM48.11

Company B (buyer) {assuming company is in monthly taxable period}

Input tax: RM1000 x 6% = RM60 (Jan 2016 GST return)

Adjustment to reduce input tax (Feb 2016 GST return)

RM210 x 6/106 = RM11.89

Actual input tax claimed by Co. B is RM48.11

Adjustments – Credit note

42

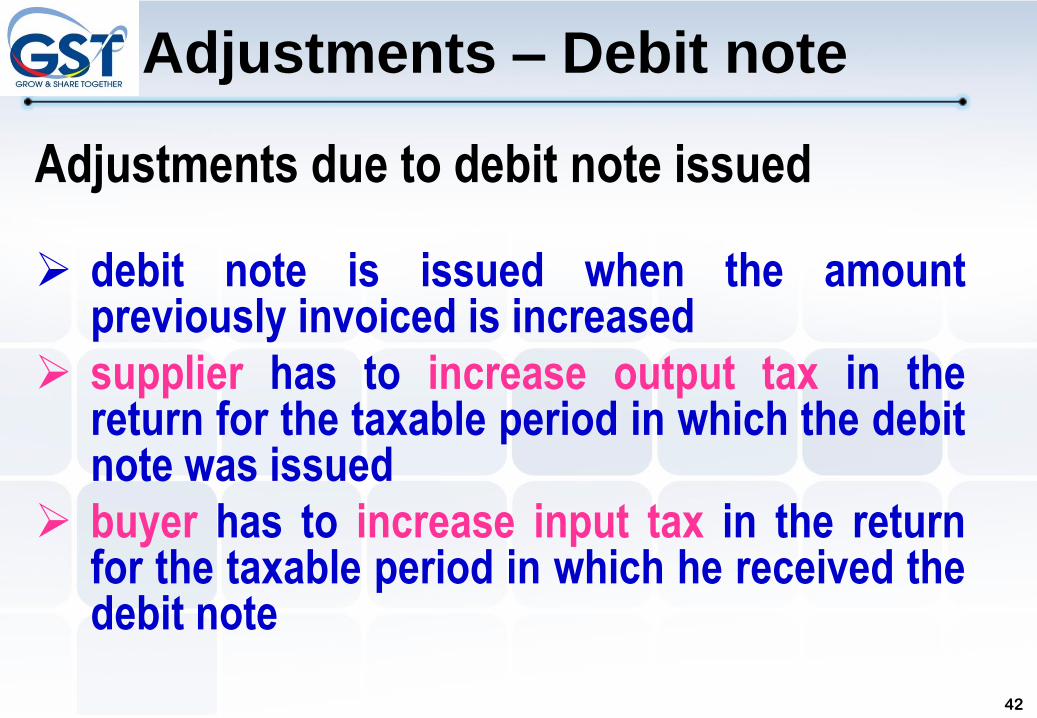

Adjustments due to debit note issued

debit note is issued when the amountpreviously invoiced is increased

supplier has to increase output tax in thereturn for the taxable period in which the debitnote was issued

buyer has to increase input tax in the returnfor the taxable period in which he received thedebit note

Adjustments – Debit note

43

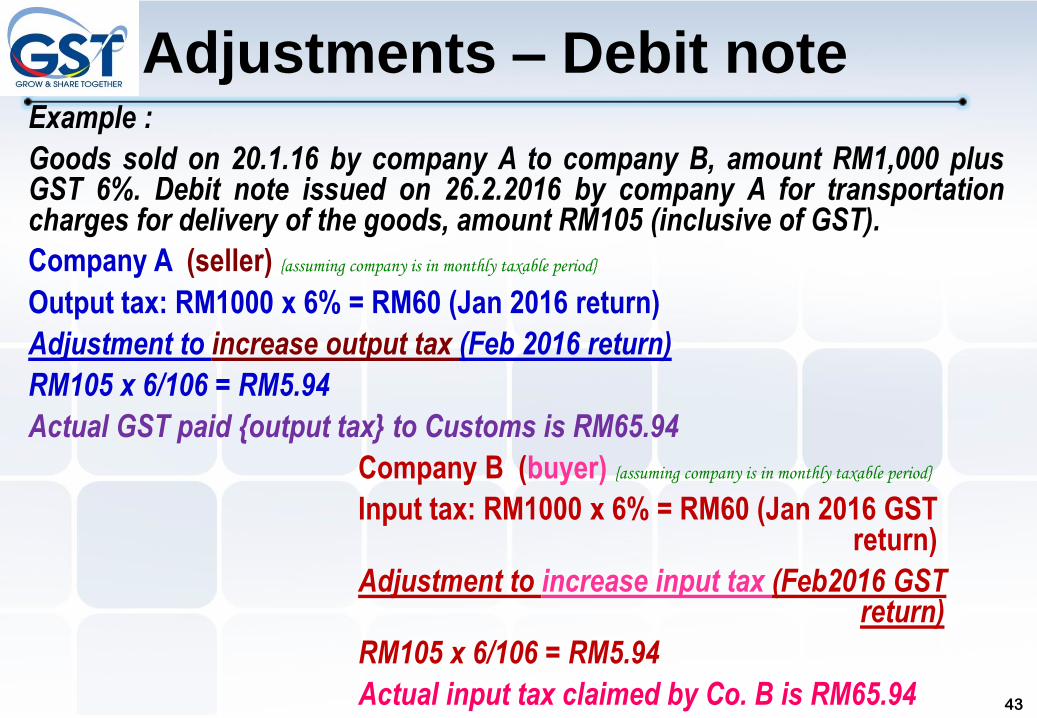

Example :

Goods sold on 20.1.16 by company A to company B, amount RM1,000 plusGST 6%. Debit note issued on 26.2.2016 by company A for transportationcharges for delivery of the goods, amount RM105 (inclusive of GST).

Company A (seller) {assuming company is in monthly taxable period}

Output tax: RM1000 x 6% = RM60 (Jan 2016 return)

Adjustment to increase output tax (Feb 2016 return)

RM105 x 6/106 = RM5.94

Actual GST paid {output tax} to Customs is RM65.94

Company B (buyer) {assuming company is in monthly taxable period}

Input tax: RM1000 x 6% = RM60 (Jan 2016 GST return)

Adjustment to increase input tax (Feb2016 GSTreturn)

RM105 x 6/106 = RM5.94

Actual input tax claimed by Co. B is RM65.94

Adjustments – Debit note

44

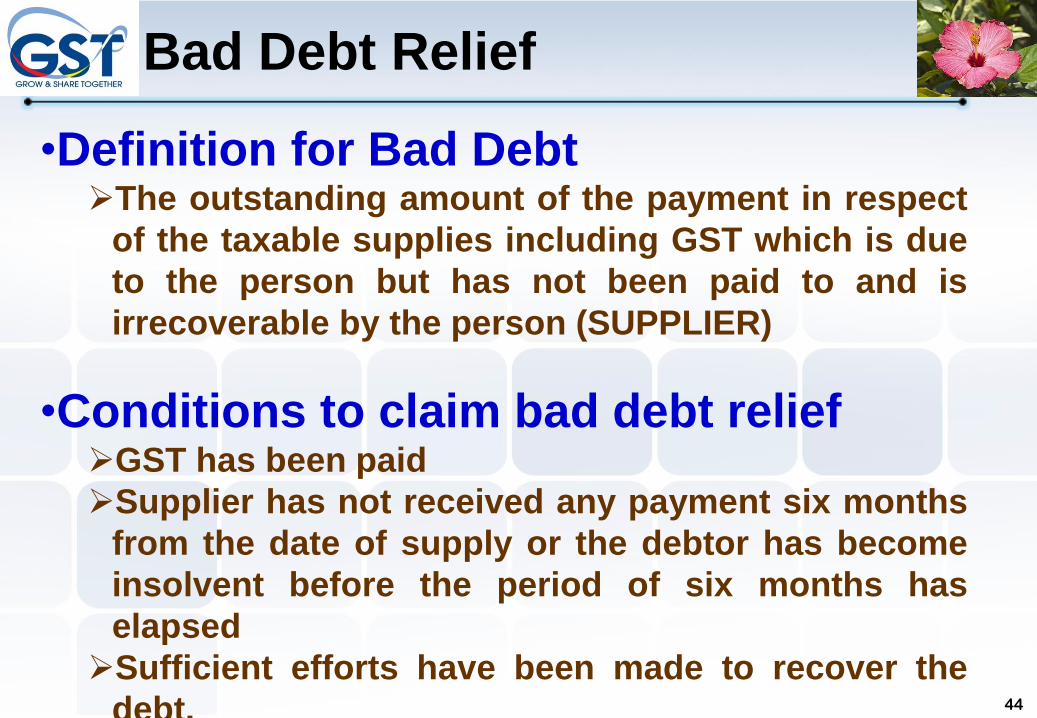

•Definition for Bad DebtThe outstanding amount of the payment in respect

of the taxable supplies including GST which is due

to the person but has not been paid to and is

irrecoverable by the person (SUPPLIER)

•Conditions to claim bad debt reliefGST has been paid

Supplier has not received any payment six months

from the date of supply or the debtor has become

insolvent before the period of six months has

elapsed

Sufficient efforts have been made to recover the

debt.

Bad Debt Relief

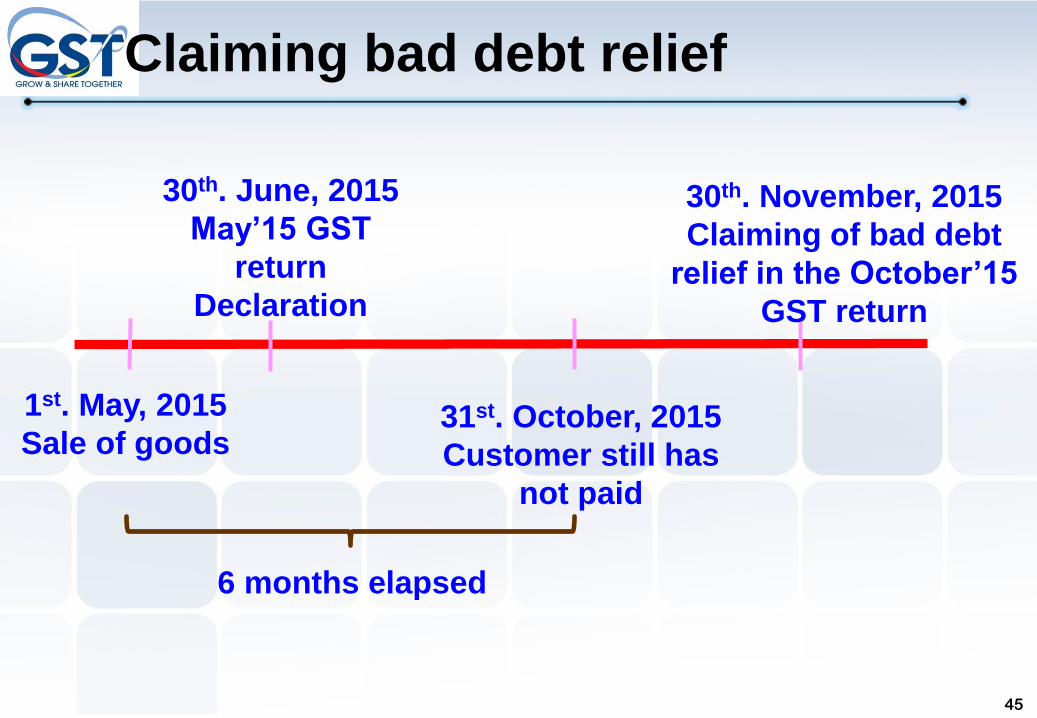

Claiming bad debt relief

45

1st. May, 2015

Sale of goods

30th. June, 2015

May’15 GST

return

Declaration

31st. October, 2015

Customer still has

not paid

30th. November, 2015

Claiming of bad debt

relief in the October’15

GST return

6 months elapsed

46

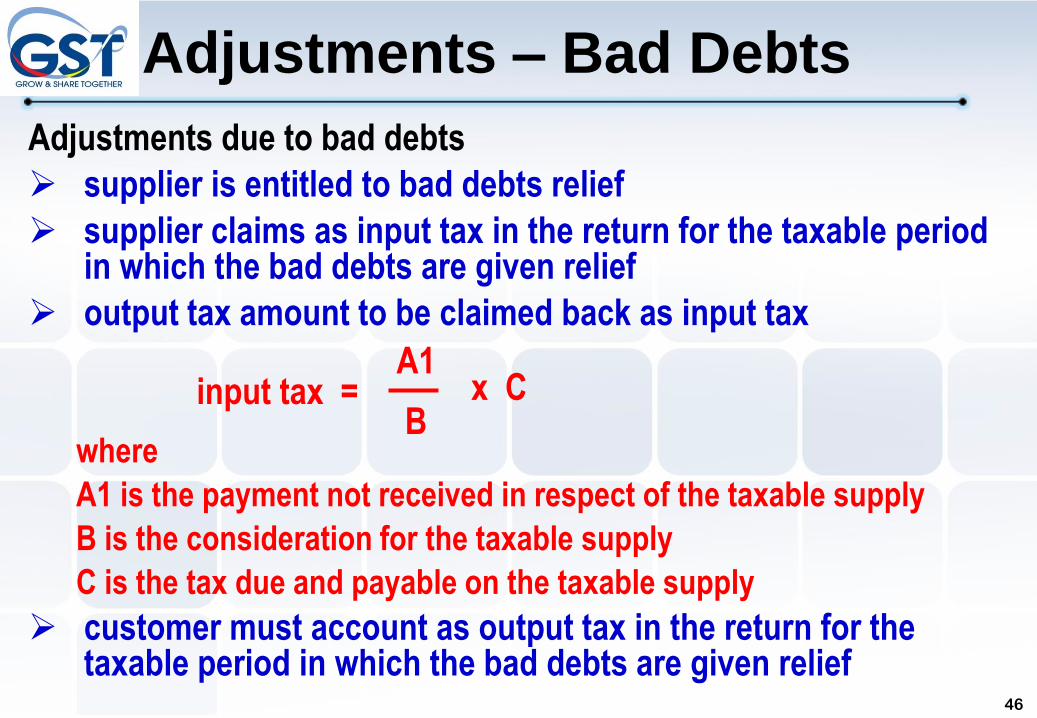

Adjustments due to bad debts

supplier is entitled to bad debts relief

supplier claims as input tax in the return for the taxable period in which the bad debts are given relief

output tax amount to be claimed back as input tax

where

A1 is the payment not received in respect of the taxable supply

B is the consideration for the taxable supply

C is the tax due and payable on the taxable supply

customer must account as output tax in the return for the taxable period in which the bad debts are given relief

A1

Binput tax = x C

Adjustments – Bad Debts

47

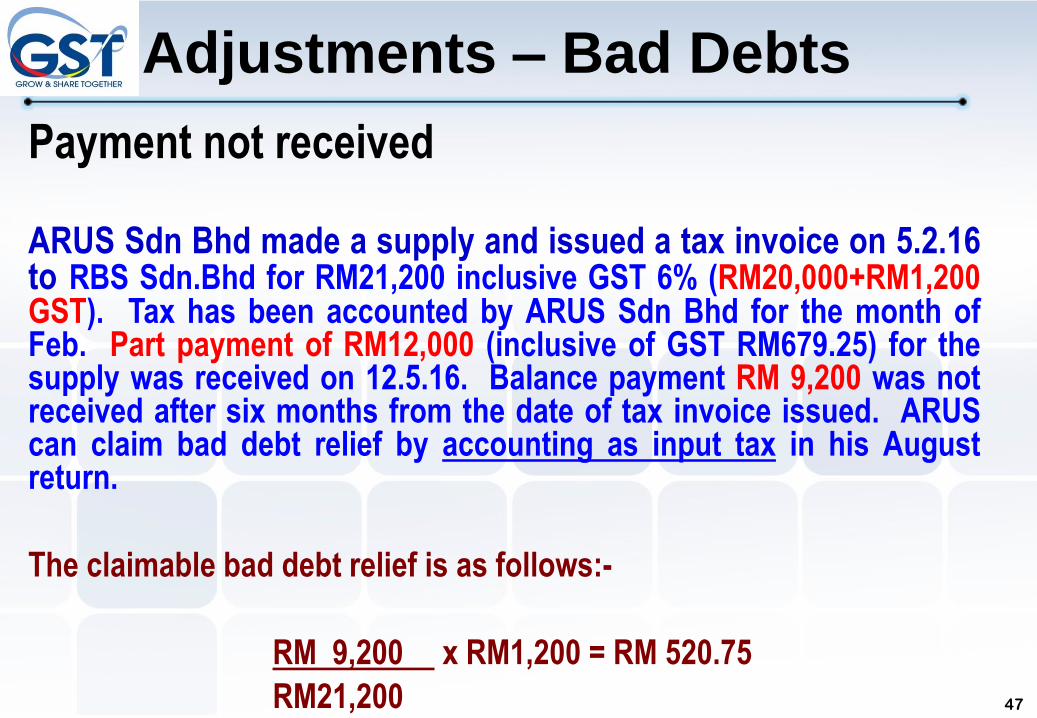

Payment not received

ARUS Sdn Bhd made a supply and issued a tax invoice on 5.2.16to RBS Sdn.Bhd for RM21,200 inclusive GST 6% (RM20,000+RM1,200GST). Tax has been accounted by ARUS Sdn Bhd for the month ofFeb. Part payment of RM12,000 (inclusive of GST RM679.25) for thesupply was received on 12.5.16. Balance payment RM 9,200 was notreceived after six months from the date of tax invoice issued. ARUScan claim bad debt relief by accounting as input tax in his Augustreturn.

The claimable bad debt relief is as follows:-

RM 9,200 x RM1,200 = RM 520.75

RM21,200

Adjustments – Bad Debts

48

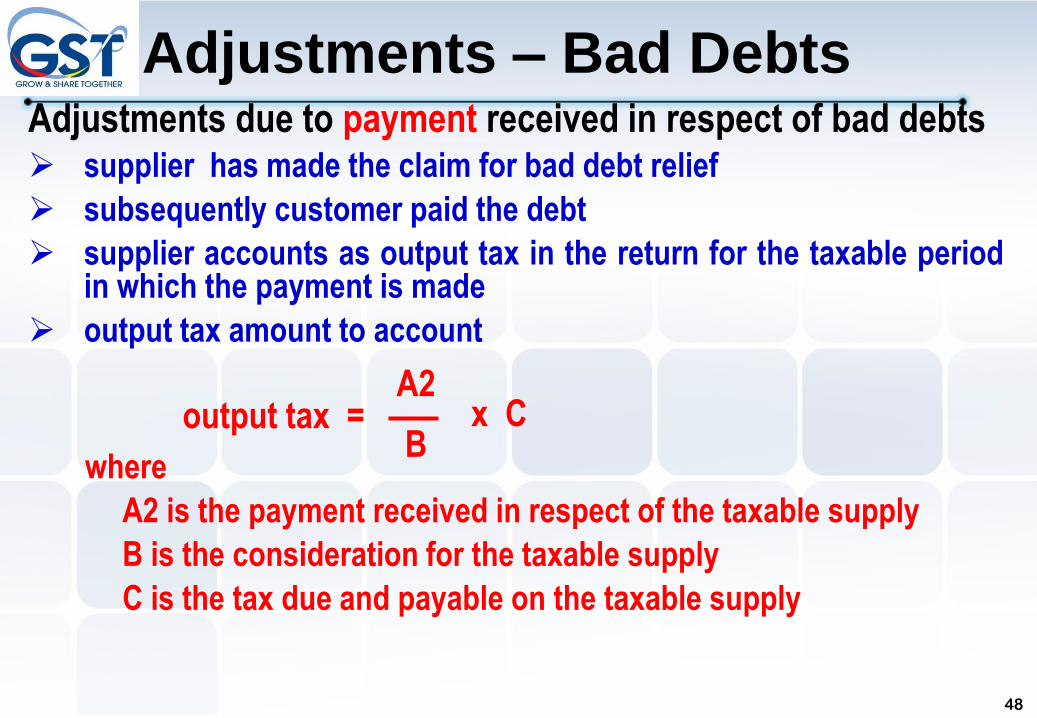

Adjustments due to payment received in respect of bad debts supplier has made the claim for bad debt relief

subsequently customer paid the debt

supplier accounts as output tax in the return for the taxable periodin which the payment is made

output tax amount to account

where

A2 is the payment received in respect of the taxable supply

B is the consideration for the taxable supply

C is the tax due and payable on the taxable supply

A2

Boutput tax = x C

Adjustments – Bad Debts

49

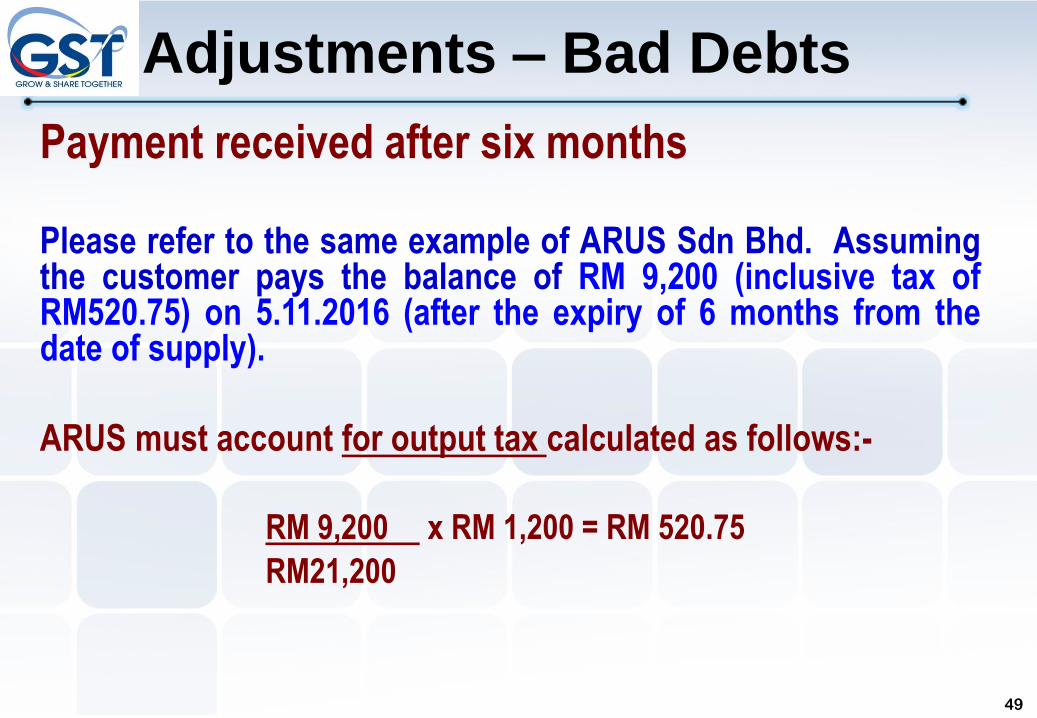

Payment received after six months

Please refer to the same example of ARUS Sdn Bhd. Assumingthe customer pays the balance of RM 9,200 (inclusive tax ofRM520.75) on 5.11.2016 (after the expiry of 6 months from thedate of supply).

ARUS must account for output tax calculated as follows:-

RM 9,200 x RM 1,200 = RM 520.75

RM21,200

Adjustments – Bad Debts

5

50

51

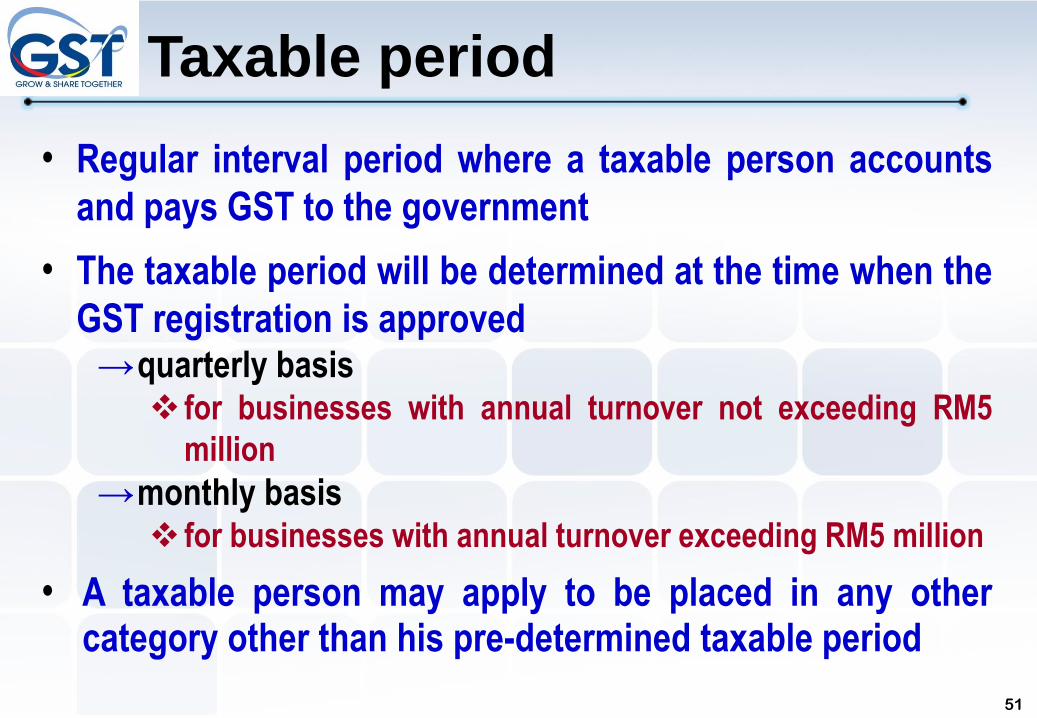

Taxable period

• Regular interval period where a taxable person accounts

and pays GST to the government

• The taxable period will be determined at the time when the

GST registration is approved→quarterly basis

for businesses with annual turnover not exceeding RM5

million

→monthly basis for businesses with annual turnover exceeding RM5 million

• A taxable person may apply to be placed in any othercategory other than his pre-determined taxable period

6

52

53

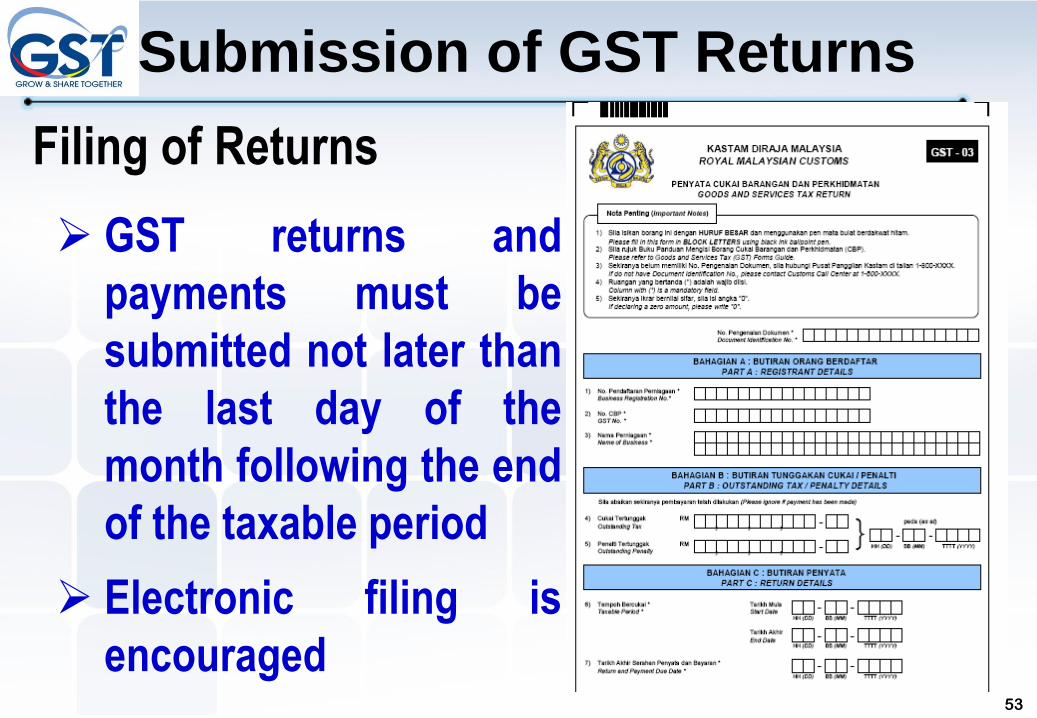

Submission of GST Returns

Filing of Returns

GST returns and

payments must be

submitted not later than

the last day of the

month following the end

of the taxable period

Electronic filing is

encouraged

54

Submission of GST Returns

55

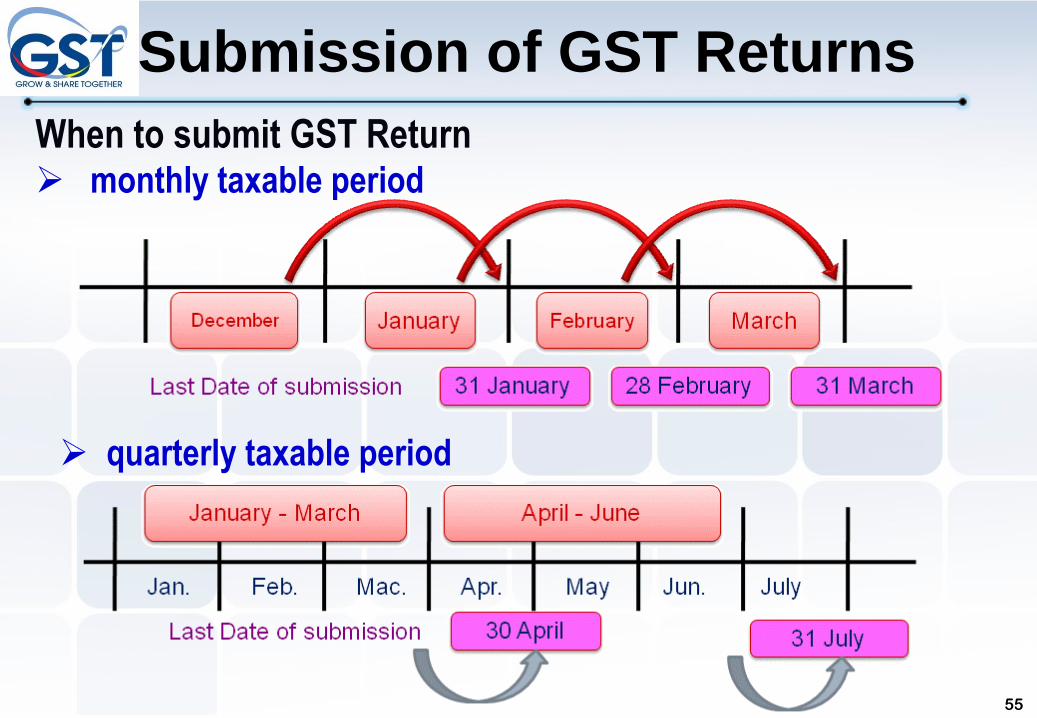

When to submit GST Return monthly taxable period

quarterly taxable period

Submission of GST Returns

56

Submission of GST Returns

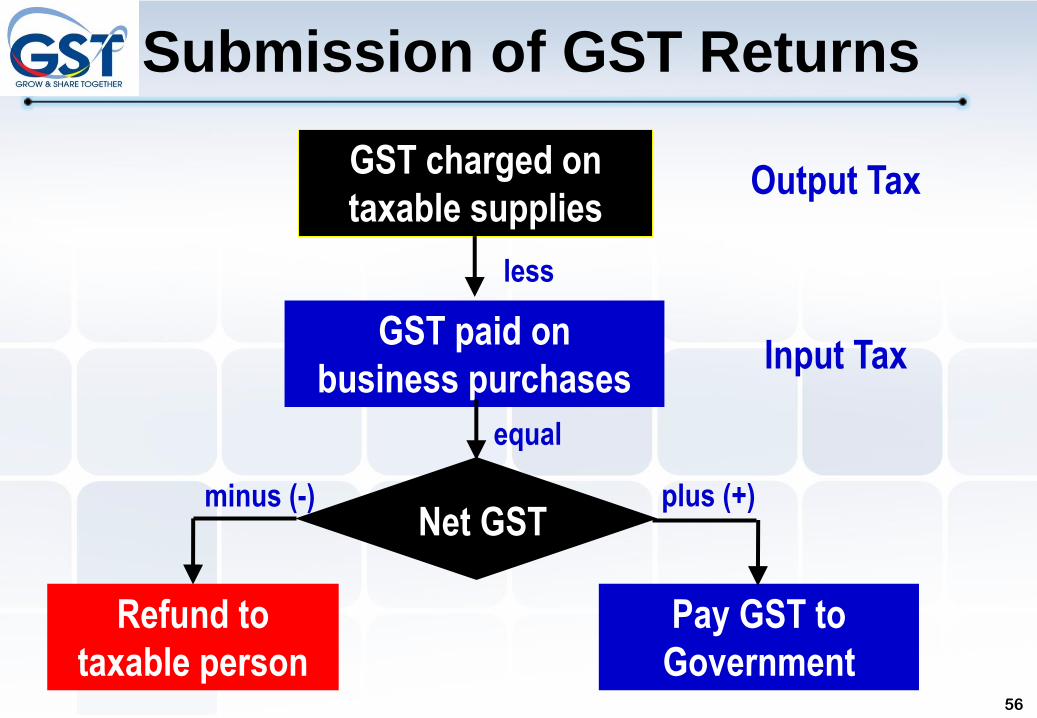

GST charged on

taxable supplies

GST paid on

business purchases

Net GST

Pay GST to

Government

Refund to

taxable person

Output Tax

less

Input Tax

plus (+)

equal

minus (-)

57

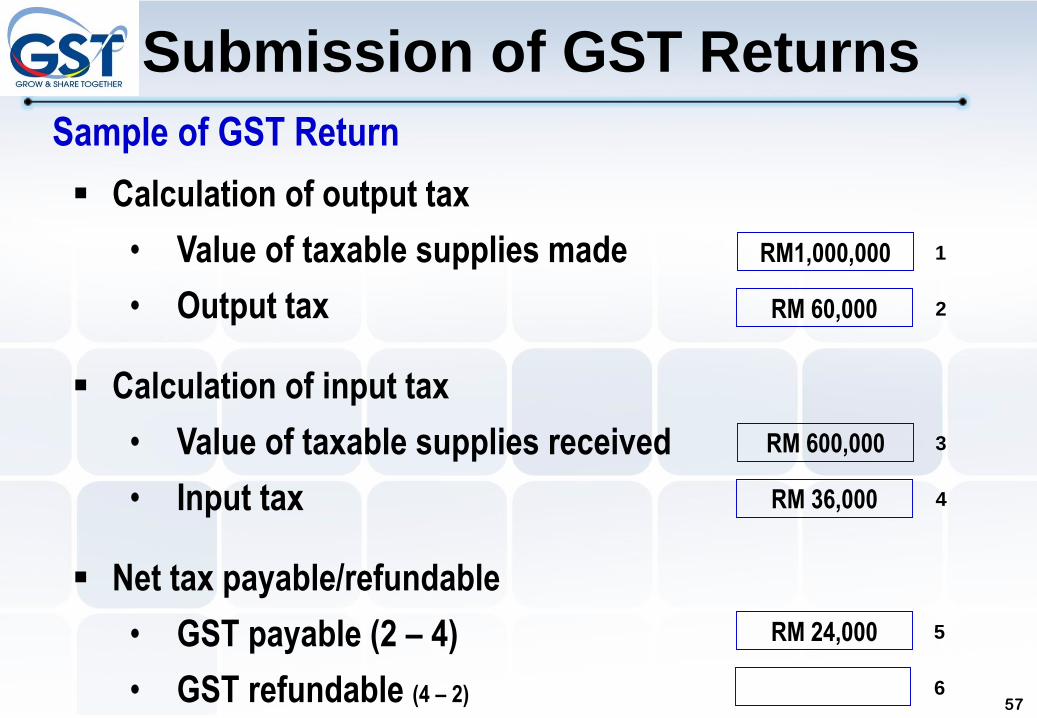

Sample of GST Return

Calculation of output tax

• Value of taxable supplies made

• Output tax

Calculation of input tax

• Value of taxable supplies received

• Input tax

Net tax payable/refundable

• GST payable (2 – 4)

• GST refundable (4 – 2)

RM1,000,000 1

RM 60,000 2

RM 600,000 3

RM 36,000 4

RM 24,000 5

6

Submission of GST Returns

58

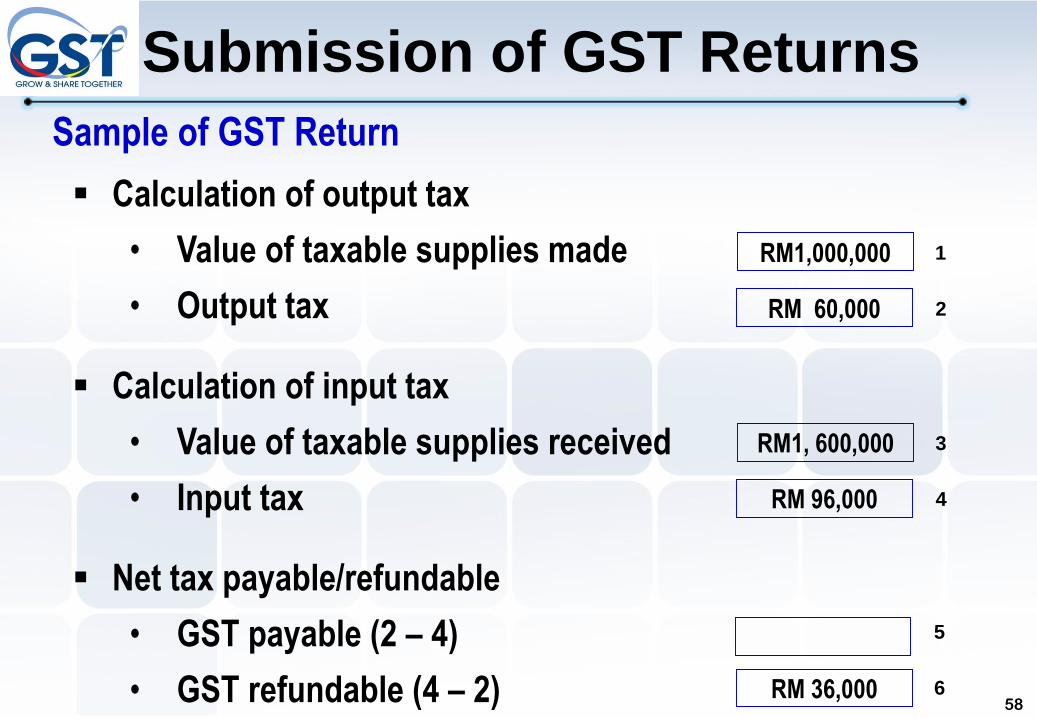

Sample of GST Return

Calculation of output tax

• Value of taxable supplies made

• Output tax

Calculation of input tax

• Value of taxable supplies received

• Input tax

Net tax payable/refundable

• GST payable (2 – 4)

• GST refundable (4 – 2)

RM1,000,000 1

RM 60,000 2

RM1, 600,000 3

RM 96,000 4

RM 36,000

5

6

Submission of GST Returns

59

i) Ketua Setiausaha,

Perbendaharaan Malaysia

Pejabat Pelaksanaan GST

Komplek Kementerian Kewangan,

No.5, Persiaran Perdana,

Pusat Pentadbiran Kerajaan Persekutuan Malaysia,

62596 PUTRAJAYA.

Tel : 03-88823000

ii) GST PORTAL

www.gst.customs.gov.my

iii) Customs Call Centre (CCC)

Tel: 03- 78067200

Fax: 03- 78067599

Email: [email protected]

Comments and Enquiries

60

End of Presentation

Thank You

GST Special Task Force UnitRoyal Malaysian Customs Department

Putrajaya

61