accounting highlights of the aicpa's sec & pcaob · pdf fileevery year during the...

TRANSCRIPT

Heads UpAudit and Enterprise Risk Services

Do You Hear What I Hear?*

Accounting Highlights of the AICPA’s December 6-8, 2004 SEC & PCAOB Conference by Deloitte & Touche LLP’s Accounting Standards and Communications Group

Every year during the holiday season, the American Institute of Certified PublicAccountants hosts a conference featuring speeches by, and question and answersessions with, members of the Securities Exchange Commission, the Public CompanyAccounting Oversight Board, and other standard-setters. While the speakersrightfully indicate that their remarks do not necessarily reflect the views of theirorganizations, the remarks clearly provide insight into current concerns and priorities.

This year’s recurring theme? Regulators, preparers and auditors have worked hard,making progress toward the goal of ending accounting, internal control and auditingfailures that have so sapped investor trust and confidence. Nevertheless, muchremains to be done. According to Donald T. Nicolaisen, the SEC’s Chief Accountant:

Investors continue to be skeptical of management and auditor reports, andthis prolonged erosion in investor confidence remains troubling. Investors andthe public rightly demand more…I believe there is still much we can do.

The conference also provides a forum for regulators to share information and toexpress a variety of other concerns in advance of the annual reporting season. Topicsranged widely, covering matters such as:

• PCAOB’s new auditing standards, audit firm inspection matters, and internalcontrol reporting requirements;

• Convergence of U.S. and International accounting standards;

• SEC filing rules;

• Corporate governance and fraud; and

• AICPA’s Centers for Public Company Audit Firms and Corporate Governance.

While the scope and breadth of the conference is far reaching (over 60 speakers,moderators and/or panel members) this issue of Heads Up focuses only on thosespeeches (or other comments) that deal with financial accounting and reportingin accordance with U.S. generally accepted accounting principles. Further, weomit topics that cover information that is already widely available from other sources(e.g., the speaker reviewed the provisions of an outstanding exposure draft). Keep inmind that the FASB’s Web site — www.fasb.org — is an excellent source ofinformation on current agenda projects.

December 13, 2004Vol. 11, Issue 9

In This Issue:• Accounting Highlights of the

AICPA’s SEC & PCAOB Conference

• Appendix: Summaries ofSpeeches and Other Comments

• Glossary of Standards

As developments warrant, Heads Up is prepared by the National Office Accounting Standards andCommunications Group of Deloitte & Touche LLP(“Deloitte & Touche”). For further information,contact your local Deloitte & Touche office.

This publication contains general information only and Deloitte & Touche is not, by means of thispublication, rendering accounting, business, financial,investment, legal, tax, or other professional advice orservices. This publication is not a substitute for suchprofessional advice or services, nor should it be used as a basis for any decision or action that mayaffect your business. Before making any decision ortaking any action that may affect your business, youshould consult a qualified professional advisor.Deloitte & Touche, its affiliates and related entitiesshall not be responsible for any loss sustained by anyperson who relies on this publication.

* Christmas carol, original words and music by Noel Regney and Gloria Shayne.

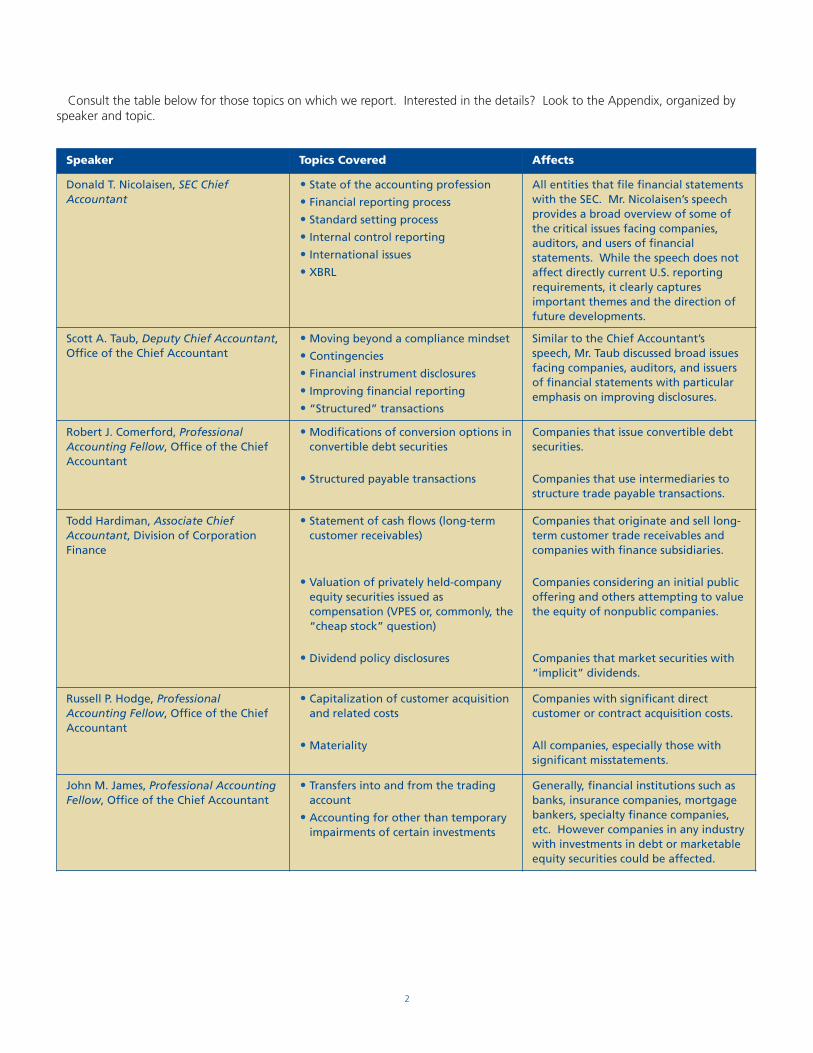

Consult the table below for those topics on which we report. Interested in the details? Look to the Appendix, organized byspeaker and topic.

2

Speaker Topics Covered Affects

Donald T. Nicolaisen, SEC ChiefAccountant

• State of the accounting profession

• Financial reporting process

• Standard setting process

• Internal control reporting

• International issues

• XBRL

All entities that file financial statementswith the SEC. Mr. Nicolaisen’s speechprovides a broad overview of some ofthe critical issues facing companies,auditors, and users of financialstatements. While the speech does notaffect directly current U.S. reportingrequirements, it clearly capturesimportant themes and the direction offuture developments.

Scott A. Taub, Deputy Chief Accountant,Office of the Chief Accountant

• Moving beyond a compliance mindset

• Contingencies

• Financial instrument disclosures

• Improving financial reporting

• “Structured” transactions

Similar to the Chief Accountant’sspeech, Mr. Taub discussed broad issuesfacing companies, auditors, and issuersof financial statements with particularemphasis on improving disclosures.

Robert J. Comerford, ProfessionalAccounting Fellow, Office of the ChiefAccountant

• Modifications of conversion options inconvertible debt securities

• Structured payable transactions

Companies that issue convertible debtsecurities.

Companies that use intermediaries tostructure trade payable transactions.

Todd Hardiman, Associate ChiefAccountant, Division of CorporationFinance

• Statement of cash flows (long-termcustomer receivables)

• Valuation of privately held-companyequity securities issued ascompensation (VPES or, commonly, the“cheap stock” question)

• Dividend policy disclosures

Companies that originate and sell long-term customer trade receivables andcompanies with finance subsidiaries.

Companies considering an initial publicoffering and others attempting to valuethe equity of nonpublic companies.

Companies that market securities with“implicit” dividends.

Russell P. Hodge, ProfessionalAccounting Fellow, Office of the ChiefAccountant

• Capitalization of customer acquisitionand related costs

• Materiality

Companies with significant directcustomer or contract acquisition costs.

All companies, especially those withsignificant misstatements.

John M. James, Professional AccountingFellow, Office of the Chief Accountant

• Transfers into and from the tradingaccount

• Accounting for other than temporaryimpairments of certain investments

Generally, financial institutions such asbanks, insurance companies, mortgagebankers, specialty finance companies,etc. However companies in any industrywith investments in debt or marketableequity securities could be affected.

3

Speeches by the SEC staff generally are available on the Commission’s Web site at www.sec.gov. We endeavor to be asaccurate as possible and the information in this issue is our best attempt to capture the key accounting and financial reportingpoints made during the conference. Please keep in mind, however, that we have not confirmed the accuracy of this HeadsUp with the SEC staff or any other organization mentioned.

Before you dive into the details, one final word. The members of Deloitte & Touche LLP’s Accounting Standards andCommunications Group wish you a happy holiday and a peaceful and prosperous 2005.

Speaker Topics Covered Affects

Chad A. Kokenge, ProfessionalAccounting Fellow, Office of the ChiefAccountant

• Disclosure requirements foraccelerated vesting of stock optionawards

• Useful life and amortization patternof renewable intangible assets

Companies that accelerate vesting of“out-of-the money” stock optionawards prior to the adoption ofStatement 123(R).

Companies with renewable intangibleassets.

G. Anthony Lopez, Associate ChiefAccountant, Office of the ChiefAccountant

• Nonmonetary exchange transactionsthat culminate the earnings process

• Revenue recognition

Companies involved in nonmonetaryexchanges.

All companies, particularly thoseinvolved in selling products withembedded software and intangiblesinvolving renewals or extensions.

Jane D. Poulin, Associate ChiefAccountant, Office of the ChiefAccountant

• Consolidation of variable interestentities

• Accounting for income taxes

• Accounting for benefit plans

Companies with variable interests in apotential VIE with an emphasis onrelated party relationships.

Companies with contingent tax reserves.

Accounting and disclosures forcompanies providing employee benefits.

Other Items

Martin P. Dunn, Deputy Director,Division of Corporation Finance

• Proposed SEC rule on securitiesoffering reform

All SEC Registrants.

Jenifer Minke-Girard, Senior AssociateChief Accountant, Office of the ChiefAccountant

• Use of other than quoted prices in fairvalue measurements

Companies that present or disclose fairvalue measurements.

Craig Olinger, Deputy Chief Accountant,Division of Corporation Finance

• Segment reporting Public companies that are required tofollow Statement 131.

i

Appendix: Summaries of Speeches and Other Comments Financial Accounting and Reporting Matters AICPA’s December 6-8, 2004 SEC & PCAOB Conference

Speech by Donald T. Nicolaisen, SEC Chief Accountant

The Chief Accountant’s speech covered a broad variety of topics, listed in the summary above. Overall, in matters handled bythe Office of the Chief Accountant, the focus is on having the accounting profession provide better and more useful informationto the investing public; information that is timely and cost-effective.

State of the Accounting Profession

While important progress has been made in regaining investor confidence, Mr. Nicolaisen recognizes that industry-wide andcompany-specific disclosure and ethical failures continue. He acknowledged that legitimate concerns have been raised regardingoverload and resource constraints, particularly with respect to smaller public companies. Care needs to be taken to avoid aregulatory framework “that is so burdensome that it smothers the economic viability” of smaller registrants. Auditors were urgedto continue to enhance the profession’s credibility and its role in the financial markets, including a need to focus on the corebusiness of auditing.

Financial Reporting Process

Financial reporting (including but not limited to financial statements) needs to be greatly improved; it should be thought of as akey communication tool serving the needs of the investing public. In supporting the financial performance reporting initiative ofthe FASB and the IASB, Mr. Nicolaisen observed that today’s disclosure information, although it may comply with GAAP andregulatory requirements, often is insufficient, and lacks organization and quality. Disclosure requirements need to be “the floor,not the ceiling,” and preparers need to shift their focus from a compliance mindset to one that concentrates on meeting theinformational needs of investors.

The Chief Accountant urged plain English communication with investors — not an abstract population but “real people —mothers, fathers…neighbors, blue collar workers,…employees with 401(k) plans…” Companies should explain their business(e.g., use non-boilerplate MD&A, consider using the direct method cash flow statement format and expand segment disclosuresbeyond GAAP’s minimum requirements), and provide investors with the same information that the companies themselves woulduse when making investment decisions.

The Chief Accountant highlighted the SEC’s pending report to Congress on off-balance sheet activities. In addition to specialpurpose entities, it will cover leasing transactions, pensions, contingencies, and contractual obligations. He observed thatInterpretation 46(R)1 has raised the question as to whether there is a need to revisit consolidation accounting.

Topics Covered Affects

• State of the accounting profession

• Financial reporting process

• Standard setting process

• Internal control reporting

• International issues

• XBRL

All entities that file financial statements with the SEC. Mr. Nicolaisen’s speechprovides a broad overview of some of the critical issues facing companies, auditors,and users of financial statements. While the speech does not affect directlycurrent U.S. reporting requirements, it clearly captures important themes and thedirection of future developments.

1 Titles of each Standard referenced in the Appendix appear in the Glossary of Standards.

ii

Standard Setting Process

The Chief Accountant’s office will be taking a hard look at its rules to make sure, among other objectives, that they areoperational. Mr. Nicolaisen expects the FASB and PCAOB to do likewise…searching for an appropriate balance between “thequest for perfection and a common sense approach to standard setting.” He noted the following:

• FASB’s standards should include few, if any, exceptions.

• PCAOB faces the difficult issue of addressing the gap between investors’ expectations and the auditor’s responsibility to detectfraud.

• The complexity of certain accounting standards (e.g., pensions and derivatives) needs to be addressed.

• FASB will need to think “out of the box” to deal with challenging issues, such as revenue recognition, and deserves itsconstituents’ support.

• Any new standard should have a transition period that provides preparers with sufficient time to establish appropriate internalcontrols.

Internal Control Reporting

According to Mr. Nicolaisen, sound internal control processes represent a great opportunity to improve financial reporting.Improving internal control is “the most urgent financial reporting challenge facing a large share of corporate America and theaudit profession…” He recognizes, however, the burden on smaller companies can be disproportionate. While in principle, allcompanies who access U.S. markets should adhere to the same disclosure standards, the costs and benefits of compliance needto be appropriately weighed. The SEC staff also acknowledges that foreign issuers face significant challenges and resourceconstraints as they move to adopt international accounting standards.

International Issues

Based on the current trend, the Chief Accountant is optimistic that the SEC ultimately will be able to eliminate the IFRS to U.S. GAAP reconciliation requirement. The Office of the Chief Accountant is considering the steps required to achieve this goal,including a planned 2006 review of the consistency and quality of IFRS-based financial statements included in SEC filings.

Convergence is not a matter of just choosing U.S. standards; instead, the convergence project is an opportunity to makeimprovements for the benefit of investors by selecting a better model and leveraging the resources of the FASB and IASB.

XBRL2

The Chief Accountant urged the meeting participants to voluntarily furnish XBRL files to the Commission using EDGAR, hopingthat the program will be in place for 2004 year-end filers. Mr. Nicolaisen reviewed the steps the SEC staff has taken to encourageparticipation. Mr. Nicolaisen discussed XBRL in the context of his repeated statements that there is a need to consider changes tofinancial reporting “in the context of better, faster and cheaper ways to produce information for investors.”

2 XBRL is an acronym for eXtensible Business Reporting Language. It permits text based data, (e.g., EDGAR information) to be tagged, thus facilitatingautomated retrieval, analysis, and exchange.

Editor’s Note: Mr. Nicolaisen stated, “We should expect in the coming months to see an increasing number of companiesannounce that they have material weaknesses in their controls.” If registrants have a material weakness in their internalcontrol over financial reporting then their controls are not effective. However, it is still possible for registrants to have a“clean” audit opinion with an adverse opinion on their report on internal control over financial reporting.

iii

Speech by Scott A. Taub, Deputy Chief Accountant, Office of the Chief Accountant

Moving Beyond a Compliance Mindset

Like Mr. Nicolaisen, Mr. Taub discussed broad themes conveyed by the Office of the Chief Accountant. Although encouragedby significant progress in a number of key areas, the SEC staff believes that as a profession “we do have more work to do.”Underpinning almost all of his concerns is the existence of a “compliance mindset” that permeates the financial reportingprocess. In order to continue to make meaningful progress, Mr. Taub indicated that it will be necessary to stop looking ataccounting and financial reporting as a compliance activity (i.e., having an inappropriate focus on accomplishing the minimumnecessary to satisfy the rules). Rather, the objective should be to communicate openly and honestly with investors and other usersof financial information.

With these observations serving as the context, Mr. Taub addressed the following accounting areas and “ways of thinking”where there is still a need for improvement.

Contingencies

Mr. Taub emphasized the following regarding the accounting and reporting of contingent liabilities:

• Statement 5 and MD&A require disclosures of significant contingencies even when no amount is recorded in the financialstatements (e.g., a loss is reasonably possible rather than probable). Investors should not first learn about a contingent liability(when the event occurred in the past) by disclosures made later, when a material expense is recorded.

• Boilerplate disclosures do not meet the objective of Statement 5 and MD&A. Opaque disclosures, whether related tolitigation, tax, or other risks are not acceptable; detailed information about the specific contingencies being evaluated needsto be provided.

• Existing standards require an accrual for probable losses that is based on the most likely amount of the loss. While those samestandards provide for the accrual of the low end of a range if no amount within the range is more likely than any other, Mr.Taub indicated that it is “somewhat surprising how often ‘zero’ is the recorded loss right up until a large settlement isannounced.”

Financial Instrument Disclosures

Mr. Taub observed that there is significant room for improvement related to financial instrument disclosures. In that regard,compliance with the “minimum requirements” often results in disclosures that are poorly organized, fail to tell the whole storyand are difficult, if not impossible to tie out to financial statement balances. Preparers and auditors should strive to make surethat disclosures are easy to follow and that they provide the investor with the whole story.

Topics Covered Affects

• Moving beyond a compliance mindset

• Contingencies

• Financial instrument disclosures

• Improving financial reporting

• “Structured” transactions

Similar to the Chief Accountant’s speech, Mr. Taub discussed broad issues facingcompanies, auditors, and issuers of financial statements with particular emphasison improving disclosures.

iv

Improving Financial Reporting

Mr. Taub indicated that preparers of financial statements rely too heavily on standard setters and regulators to pushimprovements in accounting and financial reporting. As a way to make meaningful progress, preparers (and their auditors) shouldconsider improvements to financial statements to communicate better with investors. Mr. Taub offered the following broadsuggestions on how preparers can improve financial reporting:

• Select accounting policies that provide meaningful communication. For example:

o Companies should consider Statement 95’s preference for the use of the direct method of cash flows. Mr. Nicolaisenmade the same suggestion in his remarks.

o Companies should consider their existing accounting policies related to pension accounting. Statement 87 does notrequire policies that smooth earnings, and companies should consider other alternative accounting policies.

• Improve footnote and other disclosures to give investors more insight. For example:

o Disclose expense information by nature (that is, salaries, material purchases, depreciation, rent, etc.) as useful additions tothe information provided by function (that is, cost of sales, selling expenses, etc.).

o Disclose more detail about depreciable lives of fixed assets (e.g., the depreciable amounts remaining over 5, 10, 20 years).

o Increase the use of tables in MD&A and provide a more insightful evaluation of the metrics.

“Structured” Transactions

Mr. Taub cited highly “structured” transactions (which he characterized as those designed to skirt the requirements of anexisting standard), as another example of a compliance mindset that impairs the quality of financial reporting. Mr. Taub pointedto financial products that were designed specifically to avoid liability treatment under Statement 150, and to the number ofcompanies that restructured SPEs to avoid the consolidation impact of Interpretation 46(R). He noted, with irony, that theissuance of a new standard all too often results in attempts “to avoid reporting the very information sought by the newstandard.”

In certain cases, the SEC’s Division of Enforcement has been involved. However, in other cases, the structuring effort mayclearly comply with accounting literature. Even in those cases where the structuring effort meets the letter of the accountingrules, Mr. Taub indicated that “employing them is not in the best interest of investors, does not promote transparency, and isevidence of the fact that the focus on compliance undermines quality financial reporting.”

What does this mean for registrants? First, the SEC staff will be seeking clear disclosures about accounting-motivatedtransactions (i.e., when registrants seek to structure transactions for financial reporting purposes) even if the transactionaccomplishes its financial reporting objective. In the words of Mr. Taub, “if you really believe that it’s a good idea to structurethings around the accounting or disclosure guidance, you shouldn’t be embarrassed to tell readers of your reports that that’s whatyou’ve done.” Second, if a registrant is attempting to avoid existing accounting requirements by engaging in structuringactivities, it can expect no sympathy from the SEC staff if the accounting guidance has not been fully considered.

v

Speech by Robert J. Comerford, Professional Accounting Fellow, Office of the ChiefAccountant

Modifications of Conversion Options in Convertible Debt Securities

In response to Issue 04-8, many companies are modifying the terms of their issued convertible debt in order to minimize theeffect on diluted earnings per share. Diverse views exist as to how modifications to the conversion terms of convertible debtinstruments should be incorporated into Issue 96-19’s discounted cash flow analysis, used to determine whether the debtmodification should be accounted for as a debt extinguishment.

Issue 96-19 provides guidance as to whether a modification of a debt instrument should be considered an extinguishment ofold debt and issuance of new debt. That model generally indicates that if the present value of the cash flows of the modifieddebt instrument differs from the present value of the cash flows of the original debt instrument by 10 percent or more, themodification should be accounted for as an extinguishment.

Mr. Comerford indicated that investor behavior demonstrates that conversion features have value because “there is a directcorrelation between the fair value of a conversion option and the yield demanded on a convertible security.” Therefore, changesto the fair value of a conversion option as a result of a modification should be incorporated into the discounted cash flowcomparison, even though the change literally may not impact the cash flows on the debt. Some examples of changes toconversion options follow:

• A change in the conversion price,

• A change in the number of shares underlying the option,

• A change in the nature of any conversion contingencies,

• An extension or reduction of the bond’s maturity (i.e., indirect change to the life of the conversion option).

According to Mr. Comerford, the analysis under Issue 96-19 should compare the fair value (not just the intrinsic value) of theconversion option immediately before and after the modification. Any difference identified is included in the analysis in the sameway as if the amount represented a current period cash flow.

Topics Covered Affects

• Modifications of conversion options inconvertible debt securities

• Structured payable transactions

Companies that issue convertible debt securities.

Companies that use intermediaries to structure trade payable transactions.

Example

On July 1, 2003, Company A issues $1,000 of contingently convertible debt that matures on June 30, 2013. The debt isconvertible into ten shares of common stock (implying a conversion price of $100) and, if converted, is settleable only in shares.However, the investor does not have the right to convert unless the market price of Company A’s stock exceeds $120 for fiveconsecutive days. During the quarter ended September 30, 2004, the average price of the underlying common stock was $95per share.

On October, 1, 2004, Company A changes the terms of the conversion feature such that the debt principal must be settled incash and the conversion spread must be settled in stock. Company A also extends the maturity date of the debt until June 30,2018, indirectly extending the term of the conversion option.

In addition to considering any cash flow changes as result of this modification, Company A must compare the fair value of theconversion option on October 1, 2004, with its fair value at September 30, 2004. Any difference would be treated as a currentperiod cash flow in determining if the present value of the cash flows of the entire debt instrument differ by 10 percent ormore, resulting in an extinguishment. If the present value of the cash flows differ as a result of the change by less than 10percent, the original debt instrument is considered modified. The change in the value of the conversion option results in anincrease to debt discount (or a decrease in debt premium), which is amortized as an adjustment to interest expense in futureperiods. The offset to the balance sheet entry is recorded as an increase to equity.

vi

Structured Payable Transactions

“If a transaction walks, talks, and smells like a short term borrowing, it probably is” suggested Mr. Comerford, discussingstructured payable transactions. Regulation S-X, Article 5, requires a separate balance sheet display for (1) borrowings, and (2)amounts payable to trade creditors.

In last year’s speech, Mr. Comerford indicated that the SEC staff was aware of two transactions involving a financial institutionintermediary for which it was inappropriate to classify the resulting transaction amount as a trade payable. In the first transaction,a financial institution settles a company’s existing trade payables; the company pays the financial institution at a later date. Thesecond transaction involves a tri-party arrangement: (1) a financial institution accepts an IOU from the company, and (2) presentsits own IOU to the vendor (which the vendor may present for accelerated payment at an appropriately discounted amount). Thecompany benefits from either transaction by (1) obtaining a repayment date from the financial institution beyond the due date ofthe original payable, or (2) sharing in a portion of the trade discount received by the financial institution via the acceleratedpayment to the vendor.

After last year’s speech, questions continue to arise regarding the classification of payables in other structured transactionsinvolving financial intermediaries. For example, if a debtor is involved in, or facilitates, a vendor’s factoring of receivables to afinancial institution, would the debtor continue to classify the unsettled obligation as a trade payable? In this year’s speech, Mr.Comerford warned registrants and auditors not to mistake last year’s discussion of two troubling transactions as a set of rules fordetermining when short-term borrowings may be classified as trade payables. In fact, the SEC staff does not believe it isappropriate to determine classification through a set of rules or checklists. Instead, a consideration of all the facts andcircumstances against both the letter and spirit of the accounting literature is required.

Here are some of the questions that the SEC staff encouraged preparers and auditors to consider in determining whetheramounts due may be classified as trade payables:

• What is the totality of the arrangement?

• What are the roles, responsibilities, and relationships of each party to the structured payable transaction?

• Is the creditor a “trade creditor,” i.e., a supplier that has provided the debtor with goods or services in advance of payment?

• Has the debtor participated in the process of factoring the vendor’s receivable to the financial institution?

• Does the financial institution make any sort of referral or rebate payments to the debtor?

• Has the financial institution reduced the amount the debtor/purchaser would have had to pay to the vendor on the originalpayable due date?

• Has the financial institution extended the payable’s original due date beyond the date on which the original payment wasdue?

Editor’s Note: Including the full fair value change resulting from a modification of a conversion option in determiningwhether debt has been extinguished may be a change in practice. In addition, based on an informal discussion with the SECstaff, treating the change in the fair value of the conversion option as if it were a fee paid to the creditor (assuming that themodification is not an extinguishment) may be a change in practice.

Editor’s Note: It appears that the SEC staff is setting a high hurdle to achieve trade payable classification if the debtor is notan entity that sells to the creditor specific products or non-lending services.

vii

Speech by Todd Hardiman, Associate Chief Accountant, Division of Corporation Finance

Statement of Cash Flows (Long-Term Customer Receivables)

The Division of Corporation Finance has questioned the reporting as investing activities, cash collections from long-termreceivables and proceeds from transfers (e.g., sales) of customer trade receivables. Mr. Hardiman emphasized that, in the view ofthe SEC staff, Statement 95 is clear. All cash collections stemming from the sale of inventory are operating cash flows regardlessof whether the cash flows represent:

• Immediate cash collections from customers,

• Collections of cash from receivables obtained in exchange for inventory (short-term or long-term), or

• The proceeds of the sale of customer receivables (originated in exchange for inventory) to third parties (e.g., in a Statement140 securitization).

Why does the SEC staff think this issue is clear? In support of his analysis, Mr. Hardiman noted that it is addressed specifically inparagraph 22(a) of Statement 95:

Cash inflows from operating activities are:

a. Cash receipts from sales of goods or services, including receipts from collection or sale of accounts and both short- andlong-term notes receivable from customers arising from those sales.

Mr. Hardiman also indicated that this accounting is required in situations where the extension of credit is provided by a captivefinance subsidiary.

Topics Covered Affects

• Statement of cash flows (long-termcustomer receivables)

• Valuation of privately-held-companyequity securities issued as compensation(VPES or, commonly, the “cheap stock”question)

• Dividend policy disclosures

Companies that originate and sell long-term customer trade receivables andcompanies with finance subsidiaries.

Companies considering an initial public offering and others attempting to valuethe equity of nonpublic companies.

Companies that market securities with “implicit” dividends.

Example

Company A sells a product for $500. The customer finances its purchase with a loan from Company B (a captive financesubsidiary of Company A). When Company B makes the loan to the customer, it remits $500 to its parent (Company A) onbehalf of the customer. How should Company A account for this transaction in its consolidated Statement of Cash Flows?

On a consolidated basis, the initial transaction (sale of the product) is a non-cash transaction. When Company B receives apayment on the loan from the customer, the payment should be treated as an operating cash flow in Company A’sconsolidated financial statements.

viii

Valuation of Privately-Held-Company Equity Securities Issued as Compensation (VPES or, Commonly, the “CheapStock” Question)

The Division of Corporation Finance continues to criticize the valuation of equity securities of privately-held companies. Theproblem? Valuing these securities when no quoted market price exists and when there have been no recent sales of the same orsimilar securities.

In order to assist companies, the AICPA issued a practice aid.3 Nevertheless, the SEC staff continues to have concerns andcontinues to comment on the accounting of pre-IPO companies involving the fair value of their own common stock. Specifically,Mr. Hardiman cited comments related to:

• Inconsistencies between the nature and stage of development of the company and the selection of appropriate assumptionsin the valuation,

• Inappropriate allocation of the enterprise’s value to the various classes of debt and equity securities, if more than one class ofequity securities exists, and

• Inappropriate liquidity discounts taken in valuing the equity securities.

There are a number of different valuation techniques and methods for allocating entity-wide value to the capital structure of acompany. The selection of the appropriate technique or method requires careful consideration of facts and circumstances specificto any given company.

What are the SEC staff’s concerns regarding discounts? Companies must be able to provide objective and reliable support forthe type and magnitude of each discount used in the valuation. Ultimately, there are no bright lines and the burden will beplaced on management to provide the necessary support. Absent sufficient reasonable support, companies can expect tocontinue to be challenged by the SEC staff.

Dividend Policy Disclosures

Increasingly, companies are offering securities that give the holder participation rights in significant “intended” dividends.Many of these securities “promise” to pay a regular dividend equal to all cash in excess of current operating needs (e.g., anIncome Deposit Security) even though the company may have little or no history on which to base the “promise.” Mr. Hardimanindicated that the registrant should consider providing disclosures that include, but are not limited to, the following:

• A clear articulation of the dividend policy, how the company arrived at it, and how the company expects to be able to pay it,

• An identification of risks and limitations (e.g., the discretionary nature of the dividend, debt covenants, state laws),

• Forward-looking information regarding the registrant’s future ability to pay intended dividends, and

• A company’s intentions and assumptions regarding liquidity and capital resources in MD&A (e.g., intended dividend policy andfunding source for the next year, effects of new securities and financing arrangements, effects of paying out cash as dividendsrather than reinvesting in the business).

The disclosures should address all of the relevant facts and circumstances of the specific security offering.

3 Refer to the AICPA Practice Aid, Valuation of Privately-Held-Company Equity Securities Issued as Compensation.

Editor’s Note: Mr. Hardiman did not specify where, and in which documents, these disclosures should be included.

ix

Speech by Russell P. Hodge, Professional Accounting Fellow, Office of the Chief Accountant

Capitalization of Customer Acquisition and Related Costs

The SEC staff continues to receive numerous questions on revenue-related costs. One concern is whether certain customer orcontract acquisition costs can be capitalized. Since expensing these costs almost always is acceptable, Mr. Hodge was quick topoint out that he was addressing whether it was “acceptable” to capitalize costs rather than suggesting that capitalization wasrequired or preferable. Mr. Hodge offered the following thoughts:

• Costs must meet the definition of an asset before they can be capitalized. That means they must have future economicbenefit,

• “Deferred costs” do not necessarily meet the definition of an asset, and

• Certain accounting principles strictly prohibit the capitalization of costs. For example, costs of internally developed intangibleassets should be expensed as incurred (paragraph 10 of Statement 142).

What can be capitalized? The bottom line is that the costs have to be incurred in connection with a specific customer contract.SAB Topic 13 provides limited guidance to preparers on the capitalization of these costs. Preparers may analogize to Statement91 and Technical Bulletin 90-1 to determine if a cost is direct and incremental to a contract, therefore often qualifying forcapitalization.

Measurement, Attribution, and Impairment of Acquisition and Related Costs

Once the decision has been made to recognize customer or contract acquisition costs as assets, measurement isstraightforward: capitalize the amount incurred. Regarding attribution and impairment, Mr. Hodge encouraged preparers todetermine the nature of the assets that have been capitalized and apply the accounting model that is appropriate for those typesof assets. Mr. Hodge suggested that preparers should think of most capitalized customer or contract acquisition costs asintangible assets. Therefore, the amortization and impairment models in Statements 142 and 144 would provide appropriateguidance.

Materiality

Once again the SEC staff is considering materiality issues and likely will be issuing interpretive guidance in the near future.

In the meantime, Mr. Hodge discussed the following:

• The method of evaluating misstatements (i.e., “iron curtain” versus “rollover”),

• The use of quantitative and qualitative factors, and

• The method of correcting previously immaterial errors that are material to the current period.

Topics Covered Affects

• Capitalization of customer acquisitionand related costs

• Materiality

Companies with significant direct customer or contract acquisition costs.

All companies, especially those with significant misstatements.

Editor’s Note: This guidance is not expected for this reporting season.

x

Method of Evaluating Misstatements

The two predominant methods used to evaluate misstatements are known as “iron curtain” and “rollover.” The fundamentaldifference between the iron curtain and rollover methods is whether the effects of prior period misstatements are considered.The iron curtain approach has a balance sheet bias in that it only includes errors that impact the balance sheet at the end of eachreporting period. In contrast, the rollover approach has an income statement bias because it considers the reversing effect ofprior period misstatements. Mr. Hodge illustrated the difference through the following fact pattern:

Assume that a registrant has a recurring late cut-off error related to revenue recognition at both the beginning and end ofthe current period of $120 and $100, respectively.

Under an iron curtain approach, the company would consider the impact of the overstatement of $100 in its period-endquantitative evaluation. Under the rollover approach, the quantitative evaluation would consider the net understatementeffect of $20, which results from the beginning of the year cut-off issue ($120 understatement) and the end of the yearcut-off issue ($100 overstatement). As one can see, the resulting analysis could be significantly impacted by the methodthat is used.

Which method should a company use? Current accounting and auditing standards do not address the issue. Mr. Hodgeindicated a preference for both. This dual approach likely would lead to evaluating misstatements using the approach that resultsin the larger misstatement. In the above example, the iron curtain method yields the larger misstatement. His rationale for acombined approach is that it focuses on all financial statements and does not favor one over the other.

Quantitative and Qualitative Factors

While quantification is important, it is only one step in an overall materiality assessment and preparers also should beconcerned about the qualitative considerations. Mr. Hodge stated:

SAB Topic 1.M makes it clear that exclusive reliance on a percentage or numerical threshold has no basis in the accountingliterature. That is, quantifying, in percentage terms, the magnitude of a misstatement is only the beginning of an analysisof materiality; it cannot appropriately be used as a substitute for a full analysis of all relevant considerations.

Correcting Previously Immaterial Errors

An issue sometimes arises as to how to treat uncorrected misstatements that were considered immaterial in prior periods, buthave become material to either the income statement or the balance sheet in the current period. Some believe that it is sufficientto correct the prior year error in the current year and provide disclosure on the nature and effect of the adjustment. However, theSEC staff’s position is that if the effect is material to the current period financial statements, the correction of the error should bereported as a prior period adjustment in accordance with Opinion 20. In other words, the prior period financial statements shouldbe retroactively restated.

Editor’s Note: Mr. Taub, Deputy Chief Accountant — Office of the Chief Accountant, made the same point several timesduring the conference.

xi

Speech by John M. James, Professional Accounting Fellow, Office of the Chief Accountant

Even though Statement 115 was issued more than ten years ago, certain provisions of the standard continue to consternatepreparers. Mr. James noted that many questions received by the SEC staff are addressed in the FASB Staff Implementation Guideto Statement 115 (the Guide). He also shared his views on two areas of ongoing SEC staff scrutiny: transfers into and from thetrading account and other than temporary impairments (OTTI).

Transfers Into and From the Trading Account

Statement 115 and the Guide indicate that transfers into or from the trading category should be “rare.” Although the SECstaff concedes that the term “rare” does not mean “never,” they still view the threshold, established by the standard, to be high.How high? Mr. James described a number of transactions for which the SEC staff concluded that the underlying reason for thetransfer was inconsistent with Statement 115’s concept of “rare.” These included transfers executed to (1) enact a change in aninvestment strategy, (2) achieve accounting results more closely matching economic hedging activities, or (3) reposition theportfolio due to anticipated changes in the economic outlook. What would qualify as rare? Mr. James provided the followingexamples that may meet this threshold:

• The adoption of a new accounting standard that explicitly permits such a transfer;

• A change in statutory or regulatory requirements;

• A significant business combination or other event that significantly alters an entity’s liquidity position or investing strategy;

• Other facts and circumstances that give rise to an event that is “unusual and highly unlikely to recur in the near term.”

Since any transfer to or from the trading account is likely to trigger SEC staff scrutiny, Mr. James encouraged preparers to pre-clear such transactions.

Accounting for Other Than Temporary Impairments (OTTI) of Certain Investments

Applicable Guidance

At its March 2004 meeting, the EITF reached a consensus on Issue 03-1, which established a model for identifying, recognizingand measuring OTTI for certain debt and equity securities, including those within the scope of Statement 115. The Task Force’sconclusions regarding measurement and recognition proved controversial, ultimately causing the FASB to defer the effective date of this guidance until constituent concerns could be resolved. (The assessment and disclosure provisions of Issue 03-1remain effective.) Prior to the completion of that project, which will not be completed until sometime in 2005, the FASB hasindicated that preparers should continue to follow existing OTTI guidance. Mr. James noted that the existing guidance includesSAB Topic 5.M, of which he clarified certain aspects.

Topics Covered Affects

• Transfers into and from the tradingaccount

• Accounting for other than temporaryimpairments of certain investments

Generally, financial institutions such as banks, insurance companies, mortgagebankers, specialty finance companies, etc. However companies in any industrywith investments in debt or marketable equity securities could be affected.

Editor’s Note: Paragraphs 20-22 of Opinion 30 provide helpful guidance for assessing whether an event is unusual andhighly unlikely to recur in the near term.

xii

Impairment Analysis Methodology

Mr. James reviewed the factors in SAB Topic 5.M that should be considered when performing an OTTI assessment, andindicated that the SEC staff expects that “registrants will employ a systematic methodology that includes the documentation ofthe factors considered.” Mr. James also emphasized that all available evidence should be reviewed when performing an OTTIassessment, and noted that the SEC staff:

…expects that the impairment analysis performed by a registrant would be more robust and extensive as the length of timein which a recovery needs to occur becomes shorter and the magnitude of the decline in value becomes more significant.

Tainting of Available For Sale Securities

Statement 115 prescribes that the sale of a security out of an entity’s held-to-maturity portfolio may call into question theentity’s intent to hold other securities in the portfolio until maturity. Mr. James addressed whether this same “tainting” guidanceshould be applied by analogy to the sale of an underwater security classified as available for sale. He indicated that:

…the staff does not believe that the tainting concept resulting from paragraph 8 of Statement 115 should be applied inthe same manner to the Topic 5.M analysis. The SEC staff believes that the individual facts and circumstances aroundindividual (or larger groups of) sales of securities should be evaluated in determining whether the hold to recovery assertionfor the remaining securities continues to be valid. [Emphasis added]

Editor’s Note: Preparers should also review OTTI guidance included in Statement 115 and the Guide, Issue 99-20, and SAS 92 (AU 332).

xiii

Speech by Chad A. Kokenge, Professional Accounting Fellow, Office of the Chief Accountant

Disclosure Requirements for Accelerated Vesting of Stock Option Awards

Companies continue to consider accelerating the vesting terms of their out-of-the money stock options prior to their adoptionof a final standard on share-based payment. The goal of making this change? Principally, companies are seeking to avoidrecognition of compensation costs in future periods as would be required under the forthcoming statement.

Rather than discuss the merits of the accounting for this type of change, Mr. Kokenge provided his thoughts on the appropriatedisclosures. He referred financial statement preparers to paragraph 47(f) of Statement 123, which states that the terms ofsignificant modifications of outstanding awards must be provided. Certainly, acceleration of the vesting terms of an out-of-themoney award meets this criterion. In addition, Mr. Kokenge expects preparers to provide their reasoning for the acceleration.Simply stating the company has accelerated the vesting of certain of their outstanding employee stock option awards will not besufficient. Companies that have consummated, or are currently considering such a transaction, should be prepared to explain itsactions in SEC filings.

Useful Life and Amortization Pattern of Renewable Intangible Assets

Companies have assigned an indefinite life to certain renewable intangibles (e.g., network affiliation rights, FCC licenses)consistent with the assumptions used in the valuation of these intangibles under Statement 141. In Issue 03-9, the Task Forcewas asked to provide guidance for evaluating how “substantial cost” and “material modifications,” as used in paragraph 11(d) ofStatement 142, affect the determination of the useful life of a renewable intangible asset.

At the September 2004 EITF meeting, the Task Force discontinued discussion of Issue 03-9. The FASB added a limited-scopeproject to its agenda to provide guidance on how subparagraph 11(d) of Statement 142 should be evaluated in determining theuseful life of renewable intangible assets. Until the FASB completes its project, Mr. Kokenge provided thoughts about some of thematters that were discussed in Issue 03-9.

Evaluation of Material Modification and Substantial Cost

Consistent with the general direction taken by the Task Force, the SEC staff believes “substantial costs” or “materialmodifications” consist of expected costs and modifications (i.e., changes to the terms and conditions) that an entity would notexpect to incur if the intangible asset was perpetual in nature rather than renewable.

Topics Covered Affects

• Disclosure requirements for acceleratedvesting of stock option awards

• Useful life and amortization pattern ofrenewable intangible assets

Companies that accelerate vesting of “out-of-the money” stock option awardsprior to the adoption of Statement 123(R).

Companies with renewable intangible assets.

Editor’s Note: Companies contemplating strategies to nullify the effect of the forthcoming standard on Share-BasedPayment should consider carefully Mr. Taub’s remarks described earlier.

xiv

Conceptual Differences Between Statements 141 and 142

This issue deals with how an assigned useful life for an intangible asset under Statement 142 interacts with the determinationof the fair value of that intangible asset under Statement 141.

The SEC staff believes that the valuation assumptions applied to the same intangible asset under Statements 141 and 142 candiffer. Statement 141 requires valuation based on a traditional notion of fair value (willing buyer etc.) Under Statement 142, theintangible’s assumed life is based on its utility to a specific entity.

Finally, Mr. Kokenge noted that some registrants truncate the life of cash flows used to determine fair value under Statement141 in order to be consistent with the asset life used for Statement 142 purposes. The SEC staff believes truncation to beinappropriate for the reasons discussed in the previous paragraph and that the resulting measure would not be fair value. Simplyput, the valuation of the intangible asset should not be changed under Statement 141 even if the useful life was limited underStatement 142.

xv

Speech by G. Anthony Lopez, Associate Chief Accountant, Office of the Chief Accountant

Nonmonetary Exchange Transactions That Culminate the Earnings Process

Opinion 29 sets forth the general principle that all nonmonetary exchange transactions are to be accounted for at fair valueunless the conditions of paragraphs 20-23 are tripped. Mr. Lopez pointed out that there is no authoritative guidance addressing“the timing of revenue or gain and related expense or loss recognition within the income statement” for nonmonetary exchangesthat culminate the earnings process. What are the SEC staff’s views?

Mr. Lopez believes that preparers should look to the guidance outlined in Concepts Statement 5 and SAB Topic 13 indetermining when revenues or gains should be recognized for these transactions. For example, if the “timing of the products andservices to be delivered differs from the timing of products or services to be received in the exchange,” then preparers mustevaluate the core principles of revenue recognition (i.e., whether income has been earned and is realizable, and delivery andperformance has taken place). These concepts are illustrated in Concepts Statement 5 and SAB Topic 13. However, thesestatements only provide guidance as to when the transaction is recognized, but not to where the resulting credit or debit shouldbe reflected in the income statement. Mr. Lopez provided the following example:

Vendor A exchanges services with Vendor B that results in a culmination of the earnings process. Vendor A receives servicesfrom Vendor B over 12 months but delivers services to Vendor B over 18 months. Assuming all other revenue recognitioncriteria are met, how should Vendor A account for this transaction?

Vendor A would recognize revenue over 18 months. In contrast, Vendor A would recognize the expense/loss related to theservices B provides over 12 months. Concepts Statement 5 states that expense/loss related to such services should be basedon the manner in which the entity’s economic benefits expire in relation to the service.

Mr. Lopez believes that Concepts Statement 6 answers the question of how these entries should be classified in the incomestatement. However, the specifics of the transaction must be reviewed. For example, under Concepts Statement 6, in order foran item to be considered a component of revenue, it must represent an inflow from “activities that constitute the entity’s ongoingmajor or central operations.” Otherwise the item is a gain. Preparers should look to Concepts Statement 6 for the expense/losstreatment. Mr. Lopez believes that preparers also should look to Article 5 of Regulation S-X, which provides common incomestatement captions for commercial and industrial companies.

Topics Covered Affects

• Nonmonetary exchange transactionsthat culminate the earnings process

• Revenue recognition

Companies involved in nonmonetary exchanges.

All companies, particularly those involved in selling products with embeddedsoftware and intangibles involving renewals or extensions.

Editor’s Note: In determining the timing of recognition and appropriate income statement classification, companies shouldconsider how the transaction would be accounted for if consideration was paid in cash.

xvi

Revenue Recognition

Changes in Circumstances and the Impact on Revenue Recognition

Due to the complexity of the accounting model for many types of revenue transactions, companies continually must assesswhether their current accounting policies properly reflect the economics of the contracts they are executing and theproducts/services they are selling.

Mr. Lopez provided examples in the context of the software industry and, in particular, the application of SOP 97-2 to productsthat contain software. One example is where products that contain software evolve over time such that a registrant’s previousconclusion that software is incidental to those products is no longer valid. Footnote 2 to SOP 97-2 includes some indicators to beused in determining whether the software is incidental. Mr. Lopez provided the following thoughts about these indicators:

• The indicators are neither determinative or presumptive, nor are they all inclusive.

• In considering whether the software is a significant focus of the marketing effort, a company should focus on whetheradvertisements promote the features and functionality that result from the software.

• In considering whether the software is sold separately from the product or service, a “red-flag” exists indicating that softwareis more than incidental if the company licenses their software to competitors.

• Because changes in circumstances also can affect costs, registrants should evaluate carefully whether costs of softwaredevelopment should be accounted for under Statement 86 or SOP 98-1.

Mr. Lopez provided some additional items for consideration in deciding whether software is more-than-incidental:

• Whether the rights to use the software remain solely with the vendor or are transferred to the customer;

• Whether the rights to use the software survive cessation of the service or sale of the product; and

• Whether the licensed software requires the customer to provide dedicated information technology support.

If a conclusion is reached that the software is more than incidental, then the preparer may need to consider Issue 03-5 todetermine whether the other elements should be accounted for under SOP 97-2. Under Issue 03-5, the preparer must determinewhether the software is considered essential to the functionality of the non-software elements. Thus, it is considered softwarerelated and within the scope of SOP 97-2.

What is the key takeaway? It is important for companies to have a process to evaluate the continued applicability ofaccounting policies in light of an ever changing business environment.

Extensions or Renewals of Intellectual Property

The AICPA issued TIS Section 5100.71 to clarify whether commencement of the extension/renewal for a pre-existing activesoftware license was a prerequisite for revenue recognition. If the customer already has possession of and the right to use thesoftware to which the extension and renewal applies, then the vendor may recognize the portion of the extension/renewalarrangement fee as revenue if all other revenue recognition criteria are met.

The SEC staff has been asked whether this guidance may be applied by analogy to extensions/renewals of intellectual property.Mr. Lopez believes that this analogy is appropriate if “(1) all other revenue recognition criteria of SAB Topic 134 are met, and (2)the customer already has possession of and the right to use the intellectual property to which the extension/renewal applies.”

4 SAB Topic 13 requirements:

• Persuasive evidence of an arrangement exists,

• Delivery has occurred or services have been rendered,

• The seller’s price to the buyer is fixed or determinable, and

• Collectability is reasonably assured.

xvii

Speech by Jane D. Poulin, Associate Chief Accountant, Office of the Chief Accountant

Consolidation of Variable Interest Entities

Considering “Activities Around the Entity”

Generally, an analysis of a potential variable interest entity (VIE) under Interpretation 46(R) involves only direct interests in theentity. However, Ms. Poulin indicated that the SEC staff has received a number of questions about whether certain contracts oractivities between parties other than the VIE, that pertain to the VIE, need to be considered when analyzing Interpretation 46(R).Further, Ms. Poulin indicated that “these relationships are sometimes referred to as ‘activities around the entity.’” Ms. Poulinoffered the following example:

Investor A made an equity investment in a potential VIE and Investor A separately made a loan with full recourse to anothervariable interest holder (Investor B). Can the loan in this situation be ignored when analyzing the application ofInterpretation 46(R)?

According to Ms. Poulin, the loan cannot be ignored and may raise questions regarding (1) the analysis of whether equityinvestments are at risk, and (2) whether as a group, the equity holders have the characteristics of a controlling financial interest.While often difficult to evaluate a loan such as the one A made to B, the substance of the facts and circumstances should beevaluated.

Other “activities around the entity” include equity investments between investors, puts and calls between the enterprise andother investors and non-investors, service arrangements with investors and non-investors, and derivatives such as total returnswaps.5

Ms. Poulin cited another example of activities around the entity:

Investors became involved with an entity because of the availability of tax credits generated from the entity’s business.Through an arrangement around the entity, the majority of the tax credits were likely to be available to one specific investor.

The SEC staff concluded that the specific investor must include the tax credits (1) as a component of its variable interest in theentity, and (2) as a factor (along with other activities around the entity) in determining the entity’s expected variability.

5 The FASB has issued a proposed FASB Staff Position, FSP FIN 46(R)-b, “Implicit Variable Interests Resulting From Related Party Relationships UnderInterpretation 46(R).” Implicit variable interests also illustrate an activity around the entity that should be considered when applying Interpretation 46(R).

Topics Covered Affects

• Consolidation of variable interestentities

• Accounting for income taxes

• Accounting for benefit plans

Companies with variable interests in a potential VIE with an emphasis on relatedparty relationships.

Companies with contingent tax reserves.

Accounting and disclosures for companies providing employee benefits.

Editor’s Note: Investor B’s investment would not qualify as equity investment at risk under paragraph 5(a)(3) ofInterpretation 46(R). The investment was financed for Investor B by a loan from Investor A, another party involved with theentity. The disqualification of Investor B’s equity from being at risk may cause the entity to be a VIE. For example, if InvestorB’s investment provides it with participating voting rights, the holders of the equity investment at risk in the entity do notcontrol decisions about the activities of the entity.

xviii

Related Parties

Paragraph 17 of Interpretation 46(R) includes factors used to determine which member of a related party group should beconsidered the primary beneficiary of a VIE. Because paragraph 17 requires an overall assessment of which party is most closelyassociated with the entity, the SEC staff considers all factors that may be relevant as well as the ones listed in paragraph 17. Ms.Poulin indicated that a conclusion should neither be based on a simple tally of factors, nor based on which member of the groupis associated with the most number of factors. Ms. Poulin declined to answer the hypothetical question of whether any of theparagraph 17 factors carry the most weight or is the most determinative. Instead, she indicated that “the facts and circumstancesof the situation should be considered to determine whether one factor or another is more important than any other.”

Information-Out Scope Exception

Ms. Poulin made the following observations about the “information out” scope exception discussed in paragraph 4(g) ofInterpretation 46(R):

• The exception only applies to entities created prior to December 31, 2003. Therefore, the SEC staff expects, for entitiescreated after December 31, 2003, that all information is available as necessary to make an Interpretation 46(R) assessmentand, if required, to consolidate a VIE.

• Management should be prepared to support how they have satisfied the Interpretation 46(R)’s exhaustive efforts requirementif they use the “information out” scope exception.

Reconsideration Events

Accounting for Income Taxes

In recent months there has been significant activity surrounding the accounting for contingent tax benefits. The FASB will soonexpose, for public comment, an interpretation that will shed light on the recognition, measurement, and classification of incometax benefits resulting from uncertain tax positions. Until then, Ms. Poulin provided the following thoughts:

• Financial statement preparers should “use a consistent method and have a reasoned basis” for their accounting for contingenttax benefits.

• Companies are encouraged to disclose their policy for accounting for contingent tax benefits.

• Assume a company’s policy is to recognize a tax deduction in the financial statements only if it is probable that a deductionwill be sustained under an IRS audit. If the company includes a less than probable deduction in its tax return, it should recorda contingent tax liability for the difference between the book and “as filed” tax positions.

• Companies should disclose the amount of recorded and unrecorded contingent tax liabilities pursuant to Statement 5. Whilethis disclosure requirement may cause uneasiness for some (in that it may provide a “road map” for IRS auditors), the SECstaff does not believe that this is a valid reason not to comply with GAAP and SEC disclosure requirements.

Editor’s Note: In a later question and answer session, Ms. Poulin emphasized that it is important for a company to havecontrols in place to ensure that it routinely receives information necessary to identify paragraph 7 and paragraph 15reconsideration events.

xix

Accounting for Benefit Plans

While the accounting and disclosure requirements of Statements 87, 106, and 112 are long standing, Ms. Poulin thought it wasimportant to re-visit the concept of a “substantive plan” and the importance underlying assumptions play in the accounting foremployee benefit plans.

What is a substantive plan? In most cases it is the written plan; however, in some cases the written plan may be modified byother contracts (e.g., union contracts) or by a company’s past practices. Ms. Poulin defined a substantive plan as “the plan theemployees have come to know as the plan and the plan the employees expect from the company’s past practice.” A company’saccounting should follow the substantive characteristics of the plan; whether based on past practice, other contracts, or the plandocument. For example, if a company’s past practice indicates that it absorbs more of the plan costs than is required by the plandocument, the accounting should incorporate those additional costs.

With respect to benefit plan assumptions, the discount rate is one of the most vital assumptions and one that has recentlyreceived scrutiny in the press. Ms. Poulin reminded registrants that their selection of a discount rate should be based on anappropriate evaluation of the company-specific facts. Companies should not derive discount rates based solely on a simplecomparison to other companies.

Another assumption that has garnered headlines is the appropriateness of mortality assumptions. The SEC staff suspects thatsome current benefit plan valuations are incorporating mortality tables that are outdated (e.g., 20 years old) even though moreup-to-date information is available. Ms. Poulin also believes companies should give more consideration to the employee basecovered by the plan. For example, mortality tables derived from data on employees working in a manufacturing company maynot be indicative of the mortality rates of a service provider.

xx

Other Items

Proposed Rule on Disclosure of Unresolved SEC Comments

Mr. Dunn pointed out that the SEC has issued a proposed rule entitled “Securities Offering Reform.” Section seven of theproposed rule requires all accelerated filers to disclose, in their annual reports on Forms 10-K or 20-F, SEC comments on anyExchange Act reports that:

• The issuer believes are material,

• Are more than 180 days old at the end of the year covered by the annual report, and

• Remain unresolved as of the date of the filing of the Form 10-K or Form 20-F.

The disclosure must include the substance of the comments and may include the registrant’s position regarding the comments.In a subsequent Q&A session, Carol Stacey, Chief Accountant of the SEC Division of Corporation Finance, indicated that the SECstaff plans to inform registrants when the SEC staff has completed its review of a filing, which would allow registrants todetermine whether a comment is resolved.

Use of Other Than Quoted Prices in Fair Value Measurements

Ms. Minke-Girard noted that the current FASB Exposure Draft on Fair Value Measurement will provide a “fair value hierarchy.”Under that hierarchy, the most reliable evidence of fair value is the quoted market price of identical items, if available. While afinal standard has not yet been issued, Ms. Minke-Girard observed that there is fair value guidance in a number of places inexisting GAAP (e.g., Statements 107, 115, 133, etc.) and many of those standards contain a hierarchy similar to the one proposedin the exposure draft. Accordingly, in valuing a financial instrument where a quoted market price is available, it would be unusualto deviate from that quoted market price. However, if a registrant uses something other than a quoted market price to estimatefair value, the SEC staff would expect a supportable analysis of the conclusion, including documentation of why the methodologyused results in a better measure of fair value.

Segment Reporting

In response to a question from the audience, Mr. Olinger commented that although segment reporting was not specificallyaddressed in a speech, it continues to be a concern. The Division of Corporation Finance continues to comment on Statement131 segment disclosures with great frequency.

Topics Covered Affects

• Proposed rule on disclosure ofunresolved SEC comments

• Use of other than quoted prices in fairvalue measurements

• Segment reporting

All SEC Registrants.

Companies that present or disclose fair value measurements.

Public companies that are required to follow Statement 131.

Editor’s Note: Comments on this proposed rule are due by January 31, 2005. Any filers that have comments on thisimportant proposal can submit them directly to the SEC Web site, www.sec.gov.

Editor’s Note: In recent months, the SEC staff has asked the EITF to take up two issues in an effort to improve segmentreporting. See the September 2004 Issue of EITF Roundup for a discussion of the consensus reached on Issue 04-10, and theremoval of EITF Issue No. 04-E, “The Meaning of Similar Economic Characteristics,” from the EITF’s agenda. The FASB mayissue a FASB staff position on the meaning of similar economic characteristics.

xxi

Glossary of Standards

FASB Statement No. 5, Accounting for Contingencies

FASB Statement No. 57, Related Party Transactions

FASB Statement No. 86, Accounting for the Costs of Computer Software to Be Sold, Leased, or Otherwise Marketed

FASB Statement No. 87, Employers’ Accounting for Pensions

FASB Statement No. 91, Accounting for Nonrefundable Fees and Costs Associated With Originating or Acquiring Loans andInitial Direct Costs of Leases

FASB Statement No. 95, Statement of Cash Flows

FASB Statement No. 106, Employers’ Accounting for Postretirement Benefits Other Than Pensions

FASB Statement No. 107, Disclosures About Fair Value of Financial Instruments

FASB Statement No. 112, Employers’ Accounting for Postemployment Benefits

FASB Statement No. 115, Accounting for Certain Investments in Debt and Equity Securities

FASB Statement No. 123, Accounting for Stock-Based Compensation

FASB Statement No. 123(R), Share-Based Payment (to be issued December 2004)

FASB Statement No. 131, Disclosures About Segments of an Enterprise and Related Information

FASB Statement No. 133, Accounting for Derivative Instruments and Hedging Activities

FASB Statement No. 140, Accounting for Transfers and Servicing of Financial Assets and Extinguishments of Liabilities

FASB Statement No. 141, Business Combinations

FASB Statement No. 142, Goodwill and Other Intangible Assets

FASB Statement No. 144, Accounting for the Impairment or Disposal of Long-Lived Assets

FASB Statement No. 150, Accounting for Certain Financial Instruments With Characteristics of Both Liabilities and Equity

FASB Interpretation No. 46(R), Consolidation of Variable Interest Entities

FASB Concepts Statement No. 5, Recognition and Measurement in Financial Statements of Business Enterprises

FASB Concepts Statement No. 6, Elements of Financial Statements

FASB Technical Bulletin No. 90-1, Accounting for Separately Priced Extended Warranty and Product Maintenance Contracts

EITF Issue No. 96-19, “Debtor’s Accounting for a Modification or Exchange of Debt Instruments”

EITF Issue No. 99-19, “Reporting Revenue Gross as a Principal Versus Net as an Agent”

EITF Issue No. 99-20, “Recognition of Interest Income and Impairment on Purchased and Retained Beneficial Interests inSecuritized Financial Assets”

EITF Issue No. 03-1, “The Meaning of Other-Than-Temporary Impairment and Its Application to Certain Investments”

EITF Issue No. 03-5, “Applicability of AICPA Statement of Position 97-2 to Non-Software Deliverables in an ArrangementContaining More-Than-Incidental Software”

EITF Issue No. 03-9, “Determination of the Useful Life of Renewable Intangible Assets Under FASB Statement No. 142, Goodwilland Other Intangible Assets”

EITF Issue No. 04-8, “The Effect of Contingently Convertible Instruments on Diluted Earnings per Share”

xxii

EITF Issue No. 04-10, “Determining Whether to Aggregate Operating Segments That Do Not Meet the Quantitative Thresholds”

APB Opinion No. 20, Accounting Changes

APB Opinion No. 29, Accounting for Nonmonetary Transactions

APB Opinion No. 30, Reporting the Results of Operations — Reporting the Effects of Disposal of a Segment of a Business, andExtraordinary, Unusual and Infrequently Occurring Events and Transactions

SEC Staff Accounting Bulletin Topic 1.M, “Materiality”

SEC Staff Accounting Bulletin Topic 5.M, “Other Than Temporary Impairment Of Certain Investments In Debt And EquitySecurities”

SEC Staff Accounting Bulletin Topic 13, “Revenue Recognition”

SEC Regulation S-X, Article 5, “Commercial and Industrial Companies”

AICPA Statement of Position 97-2, Software Revenue Recognition

AICPA Statement of Position 98-1, Accounting for the Costs of Computer Software Developed or Obtained for Internal Use

AICPA Statement on Auditing Standards No. 92 (AU Section 332), Auditing Derivative Instruments, Hedging Activities, andInvestments in Securities

AICPA Technical Practice Aids (TIS Section 5100.71), “Effect of Commencement of an Extension/Renewal License Term andSoftware Revenue Recognition”

Member of Deloitte Touche TohmatsuCopyright ©2004 Deloitte Development LLC. All rights reserved

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu, a SwissVermin, its member firms, and their respective subsidiaries andaffiliates. Deloitte Touche Tohmatsu is an organization of memberfirms around the world devoted to excellence in providing professionalservices and advice, focused on client service through a global strategyexecuted locally in nearly 150 countries. With access to the deepintellectual capital of 120,000 people worldwide, Deloitte deliversservices in four professional areas — audit, tax, consulting, andfinancial advisory services — and serves more than one-half of theworld’s largest companies, as well as large national enterprises, publicinstitutions, locally important clients, and successful, fast-growingglobal growth companies. Services are not provided by the DeloitteTouche Tohmatsu Vermin, and, for regulatory and other reasons,certain member firms do not provide services in all four professionalareas.

As a Swiss Vermin (association), neither Deloitte Touche Tohmatsunor any of its member firms has any liability for each other’s acts oromissions. Each of the member firms is a separate and independentlegal entity operating under the names “Deloitte,” “Deloitte &Touche,” “Deloitte Touche Tohmatsu,” or other related names.

In the U.S., Deloitte & Touche USA LLP is the U.S. member firm ofDeloitte Touche Tohmatsu, and services are provided by the subsidiariesof Deloitte & Touche USA LLP (Deloitte & Touche LLP, DeloitteConsulting LLP, Deloitte Tax LLP, and their subsidiaries) and not byDeloitte & Touche USA LLP. The subsidiaries of the U.S. member firmare among the nation’s leading professional services firms, providingaudit, tax, consulting, and financial advisory services through nearly30,000 people in more than 80 cities. Known as employers of choicefor innovative human resources programs, they are dedicated tohelping their clients and their people excel. For more information,please visit the U.S. member firm’s website at www.deloitte.com/us.

SubscriptionsIf you wish to receive Heads Up and other accounting publications issued by the Accounting Standards and CommunicationsGroup of Deloitte & Touche, please register at www.deloitte.com/us.

Dbriefs for Financial ExecutivesWe invite you to participate in Dbriefs, Deloitte & Touche’s new webcast series that delivers practical strategies you need to stayon top of important issues. Gain access to valuable ideas and critical information from webcasts presented each month on:

• Sarbanes-Oxley • Corporate Governance

• Financial Reporting • Driving Enterprise Value

Dbriefs also provides a convenient and flexible way to earn CPE credit — right at your desk. Join Dbriefs to be notified ofupcoming webcasts.

On December 16 at 2:00 PM EST, we will host a 90-minute webcast on the latest accounting and disclosure requirements forcalendar year-end companies. Register for this webcast today.

On January 5 at 2:00 PM EST, we will host a 120-minute webcast on FASB Statement No. 123(R), Share-Based Payment.Registration for this webcast will be available shortly.

Deloitte Accounting Research Tool AvailableDeloitte is making available, on a subscription basis, access to its online library of accounting and financial disclosure literature.Called the Deloitte Accounting Research Tool (DART), the library includes material from the FASB, the EITF, the AICPA, the PCAOB,the IASB, and the SEC, in addition to Deloitte’s own accounting manual and other interpretative accounting guidance.

Updated every business day, DART has an intuitive design and navigation system which, together with its powerful searchfeatures, enable users to quickly locate information anytime, from any computer. Additionally, DART subscribers receive periodic emails highlighting recent additions to the DART library.

For more information, including subscription details and an online DART demonstration, visit www.deloitte.com/us/dart.