accunting research proposal

TRANSCRIPT

1

CHAPTER I

INTRODUCTION

A. BACKGROUND

According to Law RI No.10 of 1998 dated10 November 1998 on banking, it

can be concluded that the banking business covers three activities, namely collecting

funds, distributing funds and providing other banking services. Activities to collect

and distribute funds are the main activities of banks while providing other banking

services only support activities. Activities gather funds, in the form of raising funds

from the public in the form of checking, savings, deposits and deposits. Usuallyheis

givenan attractiveremunerationsuch as, interest andgiftsas astimulusfor the

community. The activity of disbursing funds, in form of loan provision to the public

.As for other banking services provided to support the smooth running of the main

activities.

The distribution of funds in the form of long-term loans and short very

helpful businessmen especially medium entrepreneurs go downstairs or small and

medium enterprises in the provision of venture capital. Current capital loan from bank

credits were very easily obtained by the process is simple. Including the products an

assortment of various sorts bank whether private or national .As credit service of

conventional banks had much cache by the very start businessman who pioneered in

the effort.

2

Credit provision that more easily this, actually gives great rewards for moves

Indonesian economy.But devoid of risk that is very high for small businessmen,

because in general all of the products conventional banks devised a system of interest

.The interest of this loan will continue to accumulate even though no effort and runs

smoothly. While the principal to be returned to the bank.

The principle of interest embraced by conventional banks this raises a

problem that is arising at that nonperformance loan bank. It is caused by small

entrepreneurs who had very easy to speculate because credit provision so easy and so

much an offer from many of the banks. When incurred losses to the company, the

company will still have to bear interest from the bank.

The act of no. 10 1998 explained that bank differentiated into two types, they

were bank conventional and islamic banks. Characteristic of the most distinguishes

between conventional banks and bank syriah is a system interest that which is

embraced leh conventional banks have nothing on islamic banks, it is one form of

solution for the problem we are talking about over. Same thing with conventional

banks, islamic banks also have a product financing for small and medium enterprises

with different systems. Using the principle, although for the results of islamic bank

financing also have the risk of a pretty heavy as conventional banks.

Before deciding financing from or using conventional bank sari’ah banks

businessmen should see a risk that may be inflicted by the financing that never

happens again non-performing. In this research, we will do the analysis afterwards

against a risk for small and medium businessmen products islamic financing and over

the use of conventional banks, then will be conducted comparison between the two.

3

B. PROBLEM STATEMENT

1. To what extent risk posed by conventional bank products financing of

small and medium enterprises?

2. To what extentrisk posed by islamic bank products financing of small

and medium enterprises?

3. How comparisons between risk posed by the product of financing of

conventional banks and islamic banks?

C. OBJECTIVE OF RESEARCH

1. Knowing risks caused by conventional products financing to small and

medium enterprises

2. Knowing risks caused by islamic products financing to small and

medium enterprises

3. Knowing comparison risk posed by the product of financing of

conventional banks and islamic bank

D. SIGNIFICANCE OF RESEARC

1. Provide information to the reader about the products of conventional

bank financing

2. Provide information to the reader about the products of islamic bank

financing

3. Giving information to readers about risk inflicted products of

conventional bank financing for small and medium enterprises

4

4. Giving information to readers about risk inflicted products of islamic

bank financing for small and medium entrepreneur

5. Giving information to readers about the comparison risk inflicted

between financing of conventional banks and islamic bank for small and

medium entrepreneur

5

6. CHAPTER II

LITERATUR REVIEW

A. DEFINITIONOF BANK

Bank derived from Italian “banque” or italian“banca” which means “bench”.

The bankers “Florence” in the “renaissans” transact them with sitting behind the

counter money exchange. Meanwhile, according to the act of banking banks are

business entities that are collecting fund from public in the form of saving and spend

that to the people in the form of credit and or other forms in order to improve the

living standards of the people at large.

According to the act of republic of Indonesia no 10 / 1998 date 10 November

1998 about banking bank has three major function of which is collecting fund,

disbursing funds, and grant the services of other bank four activities to collect and

disbursing funds event is a staple bank while grant the services of other banks only

supporting activities. Activity of collecting fund such as collecting fund from public

in saving and deposits. Usually while given for services interesting such as, interest

and reward as a stimulus for the society. Disbursing funds activities in distributing

credits to the public.

It is concluded that banks is a financial institution that was made with the

principal activity is collecting fund from the excessive capital in money with other

6

institutions lacking money. Collecting fund done in the form of saving and distribute

funds in the form of loans in various forms the product of financing.

The act of no. 10 1998 explained that bank differentiated into two types, they

were conventional banks and Islamic banks. According to statute no.21 / 2008 on

Islamic banking, explained that Islamic bank is a bank having its business activities

based on Sari’ah principle. Sari’ah commercial bank is a bank that its activities grant

the services of in traffic payment. The public credit bank Sari’ah business activities

not grant the services of traffic payment.Basic function of Sari’ah banks in general

equal to conventional bank, so that a general principle regulation and supervision

bank also true on Sari’ah banks. Nevertheless, there are some differences rather basic

in operational bank Sari’ah demand distinction regulation and supervision for Sari’ah

banks.

B. THE DIFFERENCE CONCEPT BETWEEN FINANCING IN

CONVENTIONAL BANK AND IN ISLAMIC BANK

Islam as a religion is the concept that regulate human life comprehensively

and universal good in its relations with the creator (habluminallah) or in relation to a

fellow human being (hablumminannas). Based on BRI sari’ah education website,

Islamic bank is a bank that the system reference to Islamic law. The sari’ah principle

is based on islamic law governing the agreement between bank and other parties for

storage funds and / or financing business activities or other activities in accordance

with sari’ah.

7

From the definition above, we can see the deference between concept of

Islamic banking and conventional banking. Cursory when viewed is

technically,saving in bank sari’ah with prevailing on conventional bank almost no

difference. It is because either at a bank sari’ah bank must follow conventional and

technical banking rules in general. However, when observed deeper, there is several a

fundamental differences between them.

First difference in contract, on Sari’ah banks, all the business must according

to rule being justified by Sari’ah. Thus, all the business that must follow norm and

rules, which prevail at, contract muamalahsari’ah. On conventional banks,

transactions, the opening of an account both accounts, savings and deposit, airman,

based on an agreement but the principle of airman this not conforming with rules

sari’ah for example, wadi’ah, because in the product of accounts, savings and deposit,

promising return with a fixed interest rate against money paid-up.

Second, there are differences in return for granted.Conventional banks, using

the concept of the cost (cost concept) for calculating advantage.It means that interest

promised in advance to customer’s depositors is charge or cost to pay by a bank.

Hence, banks must “sell” to customers other (the borrower) with interest costs

higher.The difference between both called a spread that which portends whether the

company profit or loss. If spread positive, in which a burden interest charged to a

borrower higher than that given to depositors, interest so it can be said that bank

made a profit.The opposite is also true. While bank sari’ah using approach profit

sharing it means that the fund was distribute to accept bank financing.The profit

8

gained from the funding divided by two, to a bank and for customers based on an

agreement division of profits in advance.

The third difference is a target credit / financing.The depositors at the bank

conventional not conscious of money save lent for various business, irrespective of

halal-haram of the businesses. While in sari’ah banks, distribution and mistress of

society bounded by the basic principle, namely the sari’ah principle that means that

granting a loan should not be downto business which is unclean as, gambling, a

beverage, pornography, and other businesses which is not in accordance with the

sari’ah

In the conclusion, there are 3 (three) main different between sari’ah concept

and conventional concept, the first is about the agreement, the second about the return

for costumers and the last about utilization of costumer’s fund

C. DEFINITION OF FINANCING

In etymology financing derived from a charge, namely financing needs effort.

According to invite, banking no.10 year 1998 financing is provision of money or bill

that may be like to that, based on approval or agreement between bank with other

parties that requires parties defrayed to recover the money or bill that after a specific

time in return for or for the result.

According to Antonio (2001: 160) quoted by Rezain their paper about

Financing (2010) financing facility fund provision is to parties who are short of

9

money. In the same paper, Explained that according to Kasmir, financing is

provision of funds by the bank to the other party by an agreement between two parties

where a bank obliging other parties to restore loan in a specified period by or in

return for the results of

In the conclusion that the financing is a the activity of the bank in meet the

needs of the needed funds by the party that lack of funds by agreement between the

two sides, certain whereby a party who borrows obliged to return the money of

money borrowed accompanied by return to the bank.

Definition above is general definition, because there are two kinds of bank,

and every kind has definition each against financing them. Conventional financing is

channeling funds to the General activities carried out by the Conventional Bank, in

Conventional Banking, financing, better known by the term credit or loans. In an

attempt to generate big profit the banks trying to be channeling credits to poor people

funds (deficit spending unit).In the bank, credit distribution will put this interest to

public using credits from banks. It was express by Martono (2007)in Reza’s paper

about Financing (2010) “Interest credit is an amount or compensation for services

over the use of money by customers”

Meanwhile, in the sari’ah financing an event distribution of funds held by

bank syariah a principled to the concept of syariah banking or islamic banking is

governed by a ban the religion of islam to lend and with advantage in the form of a

10

interest. Besides that in syariah banking term credit or loan cannot be used to explain

activities done by syariah banks.

Financing in sari’ah banking is a form of the distribution of funds to the real

sector.The major difference with credit situated on the concept of inters. Economics

islam categorizes interest as usury and legal unclean. Financing employed the concept

of profit and losses sharing or for the result. Both sides have approved the magnitude

of a dependent part on the agreement.

D. FINANCING PRODUCT OF CONVENTIONAL BANK

Based on Wikipedia Indonesia (2011) Type of financing provided by a bank

conventional as follows:

a. Credit investment, is of credit given to customers for purposes related to

investment.

b. Credit working capital is of credit given to customers for the purposes of

venture capital.

c. Trade credit, is of credit given to customers to enlarge / facilitate the

activities of commerce.

d. Productive credit is credit investment, which can be in the form of capital

trade.

e. Credit consumptive, is of credit given to customers for the purposes of

consumption.

f. Credit profession, is of credit given to the professional

11

g. Syndicated credit, is of credit given to a debtor corporate together with

some other banks

h. credit programs, is credit granted bank in order satisfy a government

program

In general, system of the financing by the bank conventional implemented the

system of return to the bank by using instrument interest that is worn to every

costumer.The interest rate is stipulated for every type of product varying dependent

from a period of returns and the amount of financing it is providing.

E. FINANCING PRODUCT OF ISLAMIC BANK

a. MusyarakahFinancing(Partnership, Project Financing Participation)

Based on fatwah by the board of the MajelisUlama Indonesia in order in

Fatwah Letter no: 08 / dsn-mui / iv / 2000 on financing musyarakah give you

some provisions concerning musyarakah:

1. Statement ijab and qabul should be manifested by the parties to show

their will in hold contract (calneh), by taking account of the following:

a. supply and the reception must explicitly indicating purpose

contract.

b. acceptance of the offer took place recently contract.

c. Calneh poured in writing, through correspondences, or by use how-

how the modern communications.

12

2. Parties contract law, should be capable and attention to the things

below:

a. competent in giving or exerts power of representatives.

b. Any partners must provide funds and work, and every counterpart

carry out of work as a deputy.

c. Each partner has the right to regulate assets musyarakah in the

process of business normal.

d. Any counterpart confers the authority to other being partners to

manage assets and each deemed to have been given authority to

doing activities musyarakah his partner, with due observance to

the interests of without doing heedlessness and willful

wrongdoing.

e. A partner not allowed to melt or invest funds for its own benefit.

3. Profit

a. Advantage should dikuantifikasi clearly to spare distinction and

dispute in the allocation advantage or termination musyarakah.

b. Any advantage partner shall be divided proportionately on the

basis of all benefit and no prescribed amounts in early were for a

partner.

c. A partner may propose that if profits to exceed the amount

specified, excess or prosentase that given him.

d. system benefit-sharing must be set out clearly in calneh.

4. Loss

13

Loss must be divided among the partners proportionally according to

their respective capital shares in

b. Mudharabah Financing

Mudharabah is agreement cooperation between bank as the owner of funds

(hahibulmaal) with customers as (mudharib) that have skill or skills to manage any

undertaking that is productive and halal. The results of advantage of the use of these

funds being shared based on the ratio they had agreed on.

Canley mudharabah used by a bank to facilitate the fulfillment of capital for

customers’ needs to run businesses, or projects by conducting capital participation for

business or project concerned.

Harmonious

a. People whomdoing agreement:

1. Owners of capital (ShahibulMaal)

2. Implementing / businessman (Mudharib)

b. Capital (Maal)

c. Project / Business

d. Profit

e. Consent Qobul

General Terms

a. People who are bound in contract law competent

14

b. Capital requirement used to be:

1. Form of money (not goods)

2. Obviously the numbers

3.cash (not in the form of debt)

4. Directly submitted to mudharib

c. Profit sharing thirsty clear, and according to the agreed ratio

Special Conditions

a. Application for Funding

b. Data identity / personal

c. Corporate identity data

d. Project proposals are implemented

e. Warranty / guarantee

Capital / Assets

a. Capital is only provided for businesses that are clear and agreed

b. Capital must be unag cash, clearly the type of currency, and obviously the

numbers

c. Capital submitted to mudharib entirely (100%) per diem

d. If capital is gradually handed over it should be clear stages and should be

agreed upon

e. The costs incurred for the feasibility study (feasibility study) or the like are

not included in part of the capital.Payment of those fees are set by agreement

between the two sides.

15

Work and Costs

a. Bank reserves the right to supervise but reserves the right to meddle tudak

work / business Mudharib.

b. Bank as fund providers should not restrict the business / action mudharib in

the operations, except to the extent the agreement (the business that has been

establish) or that deviate from the rules of sharia.

Profit Sharing

a. The advantage gained is the result of manage funds of financing given

b. Magnitude is expressed in the form of profit sharing ratio agreed

c. Mudharib have to pay a share of the profits that belong to the bank on a

regular basis in accordance with the agreed period

d. Banks will not accept the division of profits, failures or defaults that occurred

not because of negligence mudharib

e. In the event of business failure that resulted in losses caused by the negligence

mudharib, if any, shall be borne by mudharib (into bank accounts)

F. SUMMARY

1. Banks is a financial institution that was make with the principal

activity is collecting fund from the excessive capital in money with

other institutions lacking money. Collecting fund done in the form of

saving and distribute funds in the form of loans in various forms the

product of financing.

16

2. The act of no. 10 1998 explained that bank differentiated into two

types, they were conventional banks and Islamic banks. According to

statute no.21 / 2008 on Islamic banking, explained that Islamic bank is

a bank having its business activities based on Sari’ah principle.

3. There are 3 (three) main different between sari’ah concept and

conventional concept, the first is about the agreement, the second

about the return for costumers and the last about utilization of

costumer’s fund.

4. financing is a the activity of the bank in meet the needs of the needed

funds by the party that lack of funds by agreement between the two

sides, certain whereby a party who borrows obliged to return the

money of money borrowed accompanied by return to the bank.

5. Financing in sari’ah banking is a form of the distribution of funds to

the real sector.The major difference with credit situated on the concept

of inters. Economics islam categorizes interest as usury and legal

unclean. Financing employed the concept of profit and losses sharing

or for the result. Both sides have approved the magnitude of a

dependent part on the agreement.

6. In general, system of the financing by the bank conventional

implemented the system of return to the bank by using instrument

interest that is worn to every costumer. The interest rate is stipulated

for every type of product varying dependent from a period of returns

and the amount of financing it is providing.

17

CHPTER III

RESEARCH METHOD

A. RESEARCH DESIGN

This research used quantitative method, quantitative method is method to

doing a research with systematic about section and phenomena and the relationship.

The purpose of quantitative research is developed and uses mathematical models,

theories and/or hypotheses pertaining to natural phenomena. The process of measure

is central part in quantitative research because it provides the fundamental connection

between empirical observation and mathematical expression of my relationship. The

quantitative method research is measurement and statistical objective data trough

scientific calculation derived from the sample of people or resident who are ask to

answer on a number.

This research will be comparing how big the risk that must be borne by

business financing for two types of products .This risk will be calculated by

comparing to be borne the burden of business because of using two types of financing

.This burden will give effect to company’s liquidity risk which results in some of the

company can emerge.

An Expense borne by the company with respect to this financing can be

calculate by comparing profit with dirty company interest expenses must be paid at

any period. Certainly, in this business using only one type of financing considering

18

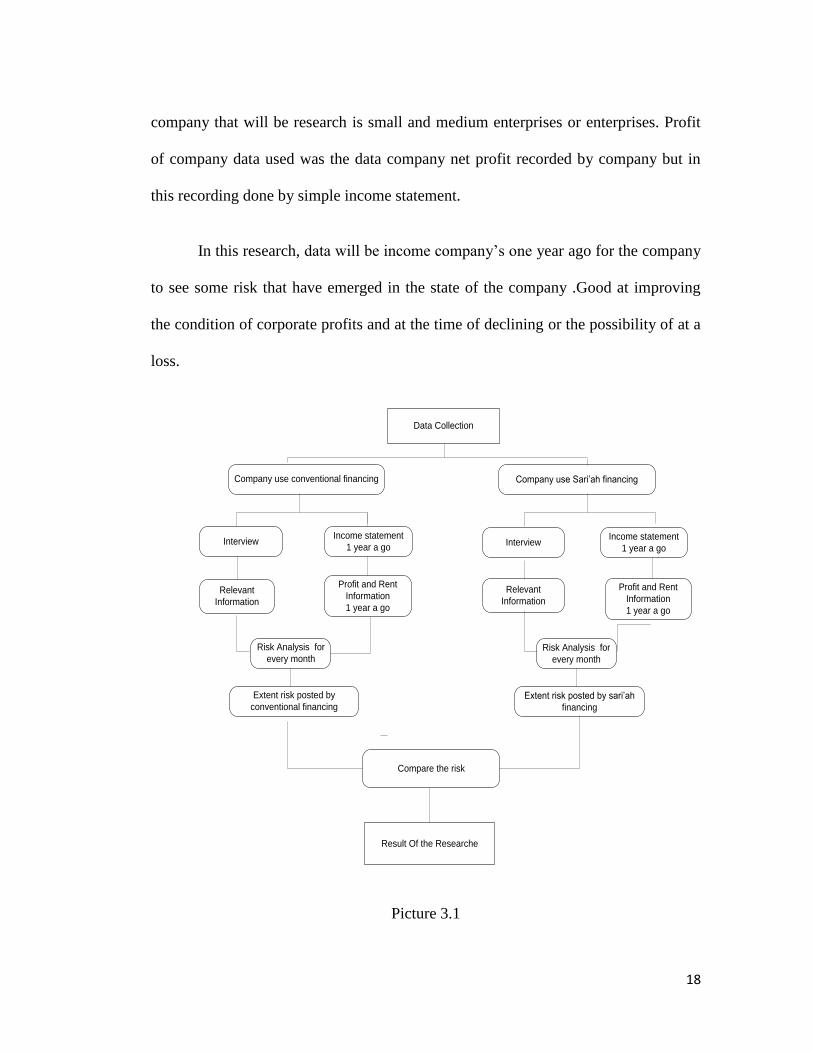

company that will be research is small and medium enterprises or enterprises. Profit

of company data used was the data company net profit recorded by company but in

this recording done by simple income statement.

In this research, data will be income company’s one year ago for the company

to see some risk that have emerged in the state of the company .Good at improving

the condition of corporate profits and at the time of declining or the possibility of at a

loss.

Interview

Relevant

Information

Data Collection

Income statement

1 year a go

Profit and Rent

Information

1 year a go

Risk Analysis for

every month

Extent risk posted by

conventional financing

Company use conventional financing

Interview

Relevant

Information

Income statement

1 year a go

Profit and Rent

Information

1 year a go

Risk Analysis for

every month

Extent risk posted by sari’ah

financing

Company use Sari’ah financing

Compare the risk

Result Of the Researche

Picture 3.1

19

B. RESEARCH SUBJECT

This research will be implementing at the Makassar by taking sample as two

companies. The one company using conventional financing and one others use

conventional financing.

C. RESEARCH TIME

This research will held on December 1st until December 31th 2014

D. RESEARCH INSTRUMENT

Instrument of research is a tool or facilities researchers who used in collecting

data. Research instrument used in this study is interview. To doing interview we need

a list of questions it contains some question that is relevant and in accordance with

the purpose of research and the data which does not need to and ware presented in

income statement.

E. DATA COLLECTING PROSEDURE

Data collection techniques used in a research there are two types namely

through engineering documentation and interview. Data collection techniques used in

this research there are two types namely through engineering documentation and

interview. Engineering documentation data done by asking corporate profits for one

know last (1 January until December 2014) as well as data interest expenses borne by

the company that .While engineering interviews were conducted with given the

questions to business owners some question that is consistent with the objectives

20

research. While, interviews technic ware conducted with given the questions to

business owners some question that is consistent with the objectives research. This

interview is to get of relevant information relating to their efforts to ensure that data

that will get documentation researchers using a technique relevant and know other

factors that influence da not described in the data collected remember a financial

report made by small and medium enterprises is very simple.

Problem Statement

Draft Of Quastion Data needed

Interview Collated Data

The general information

of the company

Data of Profit and interest or

cost of financing every month

Analysis the Data and Information

Result Of Research

Picture 3.2

21

F. TECHNIQUE OF DATA ANALIZING

Analysis begins the process of collecting all the data had been obtained. This

data was then classified into data obtained from conventional bank and bank sari’ ah.

The next step is sort the information company profits and number of loans must be

pay based on months of the transaction. After that, through both the information, we

see companies in capability to pay the cost of financing in use in both stamens

conventional bank and bank Sari’ah. From some results we can see how big

comparison between incomes obtained with the cost of the use of the funding is.

From the number of the cost to be borne by the company, it can be seeing how

big risk that must be face by companies. From these results can be compare between

the magnitude of risk faced by companies that use conventional financing and

funding of the sari’ah. From a comparison, we can take the results and it will answer

the problem statement.

22

CHPTER IV

RESULT & DISCUSSION

A. DATA AND INFORMATION FROM CONVENTIONAL

COMPANY FINANCING

a. Result of Documentation method

The dataobtained in the formof datathe company's gross profit andthe cost

offinancing:

No Month Profit Interest Cost

1 January Rp 8.000.000 Rp 10.000.000

2 February Rp 7.500.000 Rp 10.000.000

3 March Rp 10.000.000 Rp 10.000.000

4 April Rp 13.000.000 Rp 10.000.000

5 Mei Rp 12.500.000 Rp 10.000.000

6 June Rp 20.000.000 Rp 10.000.000

7 July Rp 25.000.000 Rp 10.000.000

8 August Rp 19.000.000 Rp 10.000.000

9 September Rp 17.560.000 Rp 10.000.000

10 October Rp 18.000.000 Rp 10.000.000

11 November Rp 11.000.000 Rp 10.000.000

12 December Rp 14.000.000 Rp 10.000.000

(Table 4.1)

b. Interview Method

Company Name : CV. Angkasa Jaya

No.Sertificate of incorporation : PP0467-3827-4536

Date of building : 1 January 2014

Beginning Financing : Credit Financing from BRI

CabangTamalanrea.

23

Kind of financing : Kredit Usaha Rakyat

Amount of Financing : Rp 50.000.000,-

Period of financing : 24 month

Interest rate : 3% /month

Additionfinancing : Loan from family and personal money

(for four beginning month)

B. ANALYSIS OF CONVENTIONAL FINANCING RISK

a. Analysis of Provability of Company

The analysis will compare between companyprofit andcharges that

company will pay the bank, because use conventional financing.Company

uses Rp 50.000.000 financing and a period is two years (24 months)base on

contract company must pay an interestthree percent from total financing.

The following is the interest that company must pay to the bank for

each month:

Interest Rate 3%

Total Loan 150.000.000

Period 24

Interest expense for two years 90.000.000

Interest expense each month 3.750.000

monthly installments 6.250.000

Total that company must pay to Bank 10.000.000

(Table 4.2)

A fee of Rp 3.750.000,- plus principal of a loan Rp 6.250.000,-is the

fees to be paid a company to the bank for 24 months.Interest costs is that it

represents a fix cost. The following is provability of company to paid the cost

of financing

24

Following is a table of analysis of liquidity of company:

No Month Profit Interest cost Analysis

Provability

1 January Rp 8.000.000 Rp 10.000.000 0,8

2 February Rp 7.500.000 Rp 10.000.000 0,8

3 March Rp 10.000.000 Rp 10.000.000 1,0

4 April Rp 13.000.000 Rp 10.000.000 1,3

5 Mei Rp 12.500.000 Rp 10.000.000 1,3

6 June Rp 20.000.000 Rp 10.000.000 2,0

7 July Rp 25.000.000 Rp 10.000.000 2,5

8 August Rp 19.000.000 Rp 10.000.000 1,9

9 September Rp 17.560.000 Rp 10.000.000 1,8

10 October Rp 18.000.000 Rp 10.000.000 1,8

11 November Rp 11.000.000 Rp 10.000.000 1,1

12 December Rp 14.000.000 Rp 10.000.000 1,4

(Table 4.3)

In above the equation can show the provability is very fluctuant,

moreover in early years the establishment of the company at such a moment

where corporate profits not capable of basic cover shall be paid to the bank

.At the time of companies experienced advantage under a fixed charge, hence

companies should cover the shortages of assets remain firm or sell investment

or even is done by adding capital from the owner .However because the fee

that stayed constant, and when companies experienced the increase in profit,

then provability increase significantly.

b. Analysis Liquidity of Company

From the data that get from documentation method, we can make the

analysis of liquidity of company.

25

No Month Profit Interest Cost Cash In Company

Beginning cash Ending Cash

1 January Rp 8.000.000 Rp 10.000.000 Rp 8.000.000 Rp (2.000.000)

2 February Rp 7.500.000 Rp 10.000.000 Rp (2.000.000) Rp (4.500.000)

3 March Rp 10.000.000 Rp 10.000.000 Rp (4.500.000) Rp (4.500.000)

4 April Rp 13.000.000 Rp 10.000.000 Rp (4.500.000) Rp (1.500.000)

5 Mei Rp 12.500.000 Rp 10.000.000 Rp (1.500.000) Rp 1.000.000

6 June Rp 20.000.000 Rp 10.000.000 Rp 1.000.000 Rp 11.000.000

7 July Rp 25.000.000 Rp 10.000.000 Rp 11.000.000 Rp 26.000.000

8 August Rp 19.000.000 Rp 10.000.000 Rp 26.000.000 Rp 35.000.000

9 September Rp 17.560.000 Rp 10.000.000 Rp 35.000.000 Rp 42.560.000

10 October Rp 18.000.000 Rp 10.000.000 Rp 42.560.000 Rp 50.560.000

11 November Rp 11.000.000 Rp 10.000.000 Rp 50.560.000 Rp 51.560.000

12 December Rp 14.000.000 Rp 10.000.000 Rp 51.560.000 Rp 55.560.000

(Table 4.4)

We can see in the accounts of the situation, liquidity in the early years

of the situation, liquidity in the event of the company it is not good to obtain

liquidity problems associated with the firm. Based on the information

collected from the public to cover the cost of fund to borrow the money to

friends and to sell the assets of a company. This has happened during the first

five months.

c. The Risk Expectation of conventional financing

1. The Provability is very fluctuation

Seen from provability analysis that has done by seen in the first month

the establishment of the company occurs stabling company profit. This

happened because company still in business conditions so that pioneered sales

turnover is very weak. In a situation like this company have to bear interest

26

costs and loan principal very not in accordance with the profit-generated

company.

Because use interest system, and although the companies condition not

in a good state, the company still have to pay the fixed interest. This in turn

requires the owner to do additional funding by borrowing from family and use

their personal funds .In this case, the company still can survive due to funds

are still available from the owner.

Early in the establishment of the companies condition is very risky

where at the time, products or services offered was still search the market

share and must compete to gain customers. However, the company has must

face with a load large enough. This certainly is not healthy for the company

and threatening the survival of companies

2. The liquidation of company did not stable in beginning year

On the first several months of establishment of company, profit

obtained not able to cover liquidity is situation where companies having a

supply of cash that optimal that can be sufficient operational needs company.

Liquidity is a component that must be possessed an enterprise, with a good

liquidity and so many benefits can get, among them:

be able to use a period of time a discount from supplier

be able to use if there are the differences in the selling price of supplier

27

Keep the good name because the payment of supplier always arrive on

time

a profitable investment be able to use avoid things that they cannot be

avoided

According to analysis has taken over, that can be seen in the first

several months, the establishment of the company a profit don’t be able to

cover the cost of the interest on the loan and that the company is not liquid.

3. The Profitability was very low in beginning month of company build

Profitability company low to the first several months’ Probability is the

ability of the company generates profit. The low profitability company

liquidity influenced by a company that low that there are several opportunities

to generate profit not capable of being use.

C. DATA AND INFORMATION FROM SARI’AH COMPANY

FINANCING

a. Result of Documentation method

The data obtained in the form of profit from the company and profit-

lose sharing to bank.

No Month Profit Profit Sharing

1 January Rp 7.000.000 Rp 2.800.000

2 February Rp 8.000.000 Rp 3.200.000

3 March Rp 10.000.000 Rp 4.000.000

4 April Rp 14.000.000 Rp 5.600.000

28

5 Mei Rp 12.000.000 Rp 4.800.000

6 June Rp 19.500.000 Rp 7.800.000

7 July Rp 26.000.000 Rp 10.400.000

8 August Rp 19.000.000 Rp 7.600.000

9 September Rp 18.000.000 Rp 7.200.000

10 October Rp 17.500.000 Rp 7.000.000

11 November Rp 12.000.000 Rp 4.800.000

12 December Rp 15.000.000 Rp 6.000.000

(Table 4.5)

a. Result of Interview Method

Company Name : ButikNahla Makassar

No. Aktependirian : -

No.Sertificate of incorporation : 1 January 2014

Beginning Financing : From BRI Sari’ahCabangTamalanrea

Kind of Financing : Musyarakah

Amount of Financing : Rp 50.000.000,-

Contract of financing :

1. Profit sharingof 40% from company profit forbank

2. Returns of financing doing in three years, 20% in first years, the

secondyear is 30% and50% in third year

D. ANALYSIS OF SARI’AH FINANCING RISK

a. Analysis of Provability of Company

Because the company use sari’ah financing, so the cost from

financing use profit share sharing. The cost is from profit of company and

return principal of financing can paid according to the percentage in three

year.Following is a table of analysis of liquidity of company:

29

Cost in December

Profit Sharing Rp 15.000.000 Rp 6.000.000

Return of principal financing 50.000.000 10.000.000

Total cost in December Rp 16.000.000

(Table 4.6)

No Month Profit Profit Sharing Analysis of

Provitability

1 January Rp 7.000.000 Rp 2.800.000 2,5

2 February Rp 8.000.000 Rp 3.200.000 2,5

3 March Rp 10.000.000 Rp 4.000.000 2,5

4 April Rp 14.000.000 Rp 5.600.000 2,5

5 Mei Rp 12.000.000 Rp 4.800.000 2,5

6 June Rp 19.500.000 Rp 7.800.000 2,5

7 July Rp 26.000.000 Rp 10.400.000 2,5

8 August Rp 19.000.000 Rp 7.600.000 2,5

9 September Rp 18.000.000 Rp 7.200.000 2,5

10 October Rp 17.500.000 Rp 7.000.000 2,5

11 November Rp 12.000.000 Rp 4.800.000 2,5

12 December Rp 15.000.000 Rp 16.000.000 0,9

(Table 4.7)

From the analysis on the table, we can see that the provability on the

year was very stable because the character of cost is variable with the profit.

If the profit became high the cost also high and if profit decrease the cost

became decrease. It make provability became stable, but the provability

decrease because.

b. Analysis Liquidity of Company

No Month Profit Profit Sharing Cash in company

Beginning cash Ending cash

1 January Rp 7.000.000 Rp 2.800.000 Rp 7.000.000 Rp 4.200.000

2 February Rp 8.000.000 Rp 3.200.000 Rp 4.200.000 Rp 9.000.000

3 March Rp 10.000.000 Rp 4.000.000 Rp 9.000.000 Rp 15.000.000

4 April Rp 14.000.000 Rp 5.600.000 Rp 15.000.000 Rp 23.400.000

30

5 Mei Rp 12.000.000 Rp 4.800.000 Rp 23.400.000 Rp 30.600.000

6 June Rp 19.500.000 Rp 7.800.000 Rp 30.600.000 Rp 42.300.000

7 July Rp 26.000.000 Rp 10.400.000 Rp 42.300.000 Rp 57.900.000

8 August Rp 19.000.000 Rp 7.600.000 Rp 57.900.000 Rp 69.300.000

9 September Rp 18.000.000 Rp 7.200.000 Rp 69.300.000 Rp 80.100.000

10 October Rp 17.500.000 Rp 7.000.000 Rp 80.100.000 Rp 90.600.000

11 November Rp 12.000.000 Rp 4.800.000 Rp 90.600.000 Rp 97.800.000

12 December Rp 15.000.000 Rp 16.000.000 Rp 97.800.000 Rp 96.800.000

(Table 4.8)

From the table, the liquidity of company was very stable, It because

the profit from the operational of company can cover the financing cost.

c. Risk expectations of Sari’ah Financing

1. Profit Sharing can push down the Profitability of company

Sari’ah financing did not use interest system but use profit sharing

system. Profit sharing system is system that the company must give partly of

the company profit to the bank with percentage on the agreement. The

character of cost is variable cost, it always changes if the profit of the

company change. If the profit of the company was increase, the cost of

financing also became increase so it can push down the profitability of the

company.

2. Decrease the liquidity in month that the company must return the

main loan.

In profit sharing system, the main of loan will return in several phase

according to the agreement. Therefore, there are several months in period of

financing the company must pay the cost mare than other month, so the

liquidity of company in that month decreases. The company also must pay

31

attention it month to prepare more cash on that month to anticipation the

profit of company cannot cover the cost of financing.

E. ANALISIS OF COMPARISON BETWEEN FINANCING

RISK OF CONVENTIONAL AND SARI’AH FINANCING

a. Comparison in liquidity of company

From the analysis of company liquidity, the liquidity of conventional

financing was not stable, it because the cost of financing did not follow the

profit. If the profit of company decreases, the cost did not decrease so the

liquidity of company became fluctuation.

In Sari’ah financing the liquidity during the year became stable, it

because the character of financing cost is variable. If the profits decrease the

cost, also decrease. Nevertheless, in end of year the liquidity was decrease

because on December company must return the main loan of company, so

the cost increase more than other month.

b. Comparison in Provability of company

To see the provability, we use liquidity as basis. Because if the

company have much cash, it can cover the short-term debt. Seen from

provability analysis that has done by seen in the first month the

establishment of the company occurs stabling company profit. This

happened because company still in business conditions so that pioneered

sales turnover is very weak. In a situation as this company have to bear

32

interest costs and loan principal very not in accordance with the profit

generated company.

In sari’ah financing the provability of company was stable because use

profit sharing. The cost of financing follow the company profit, it make the

provability became good.

c. Comparison in Profitability of company

Profitability company low to the first several months’ Probability is the

ability of the company generates profit. The low profitability company

liquidity influenced by a company that low that there are several

opportunities to generate profit not capable of being use.

Profit sharing system is system that the company must give partly of

the company profit to the bank with percentage on the agreement. The

character of cost is variable cost, it always changes if the profit of the

company change. If the profit of the company was increase, the cost of

financing also became increase so it can push down the profitability of the

company.

33

CHPTER V

CONCLUSION & SUGGESTION

A. CONSLUSION

1. The liquidity of conventional financing was not stable, it because the cost of

financing did not follow the profit. If the profit of company decreases, the cost

did not decrease so the liquidity of company became fluctuation. In Sari’ah

financing the liquidity during the year became stable, it because the character

of financing cost is variable. If the profits decrease the cost, also decrease.

Nevertheless, in end of year the liquidity was decrease because on December

Company must return the main loan of company, so the cost increase more

than other month.

2. The provability of conventional financing was not stable, it because the cost

of financing did not follow the profit. If the profit of company decreases, the

cost did not decrease so the liquidity of company became fluctuation. In

sari’ah financing the provability of company was stable because use profit

sharing. The cost of financing follow the company profit, it make the

provability became good.

3. Profitability company low to the first several months’ Probability is the ability

of the company generates profit. Profit sharing system is system that the

company must give partly of the company profit to the bank with percentage

on the agreement. The character of cost is variable cost, it always changes if

the profit of the company change

34

B. SUGGESTION

This time, so much financing products offered by various financial

institutions, including banks and non-bank types. Financing various products

with the conditions very easily also offers loans very much .But , suggested

to the entrepreneurs especially a new business will begin in the field of small

and medium businesses to analyze the financing of products using before

deciding to pembiaayan financing used can be efficient and effective and

does not cause a large risk for business survival .

Based on a research, researcher suggested t use Sari’ah financing to

begin business especialy to small and medium eterprice because the risks

generated relative smaller than use conventional products financing as

viewed from the aspect of liquidity, profitability and provabilitas.

In research that has been researcher do still so much negativity , hence

we suggest to the researchers next to do more in-depth research and making

this study as a preparation proses . The components still to increase is the

treatment of companies have been insufficient and the treatment side

variables is weak.

35

BIBLIGRAPHY

Anonim. 2008. Undang-Undang Republik Indonesia Nomor 21 Tahun 2008 Tentang

Perbankan Syariah. Jakarta;Dewan Perbankan Syariah Indonesia.

Anonim.2000. Fatwa Dewan Syari’ah Nasional No: 01/Dsn-Mui/Iv/2000 Tentang G

IRO. Jakarta;Dewan Syari’ah Nasional.

Anonim. 2010. Daftar Produk Perbankan Syari’ah. Jakarta;Islamic Banking

Anonim. 2010. Menghitung Bagi Hasil iB. Jakarta;Islamic Banking

Anonim. 2010. Syariah Education. Retrive on www.brisyariah.co.id; 13th November

2014

Ahmad Fairuza, Denes. Analisis Manajemen Risiko Kredit Sebagai Alat Untuk

Meminimalisir Risiko Kredit (Studi pada PT. Bank Rakyat Indonesia

(PERSERO) Tbk. Cabang Malang Kawi). Malang;Balai Penerbit Fakultas

Ekonomi dan Bisnis, Universitas Brawijaya

Gumayantika, Rika. Abdul, Kohar Irwanto.2010. Analisis Sistem Manajemen Risiko

Kredit dan Pengaruhnya terhadap Laba Perusahaan dengan Penerapan Model

Program Komputer (Studi Kasus PT Bank JABAR Cabang Ciamis).

Bogor;Penerbit Fakultas Ekonomi dan Manajemen Institut Pertanian Bogor

Siamat D. 2005. Manajemen Lembaga Keuangan: Kebijakan Moneter dan

Perbankan. Jakarta; Lembaga Penerbit Fakultas Ekonomi Universitas

Indonesia.

Syahputra, reza. 2012. Pengertian Pembiayaan. Retrive on

rezasyahputra32.blogspot.com; November 2014

Wendiana, Adetyas.2009. Analisis Kredit. Jakarta;Lembaga Penerbit Fakultas

Ekonomi UI