achieving scale in consumer and small business lending & voting structures ... the bank retains...

TRANSCRIPT

Achieving Scale in

Consumer and Small Business Lending

May 2017

2

FORWARD-LOOKING STATEMENT AND OTHER IMPORTANT DISCLOSURES

AP Commercial LLC, is a wholly owned subsidiary of Alliance Partners and is the SEC-registered investment adviser referred to herein as “Alliance Partners.” Registration with the SEC or with any state securities authority does not imply a certain level of skill or training.

Information contained herein may include information with respect to prior investment performance. Information with respect to prior performance, while a useful tool in evaluating Alliance Partners’ investment activities, is not necessarily indicative of actual results that may be achieved for unrealized investments.

This presentation is for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product, or service of Alliance Partners.

Unless otherwise noted, information included herein is presented as of December 31, 2016. This presentation is not complete, and the information contained herein may change at any time without notice. Alliance Partners does not have any responsibility to update the presentation to account for such changes. Alliance Partners makes no representation or warranty, express or implied, with respect to the accuracy, reasonableness or completeness of any of the information contained herein, including, but not limited to, information obtained from third parties. Past performance is no guarantee of future returns.

The information contained herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations.

3

BancAlliance.com Washington, D.C. Office | 4445 Willard Avenue Suite 1100 | Chevy Chase, MD 20815

Main:(301) 232-5440 | Email: [email protected]

301.232.5416 [email protected]

Wayne Gore Managing Director, Alliance Partners

Wayne is a Managing Director of Membership at Alliance Partners. Prior to joining Alliance Partners, Wayne held leadership roles in the Financial Institutions Group with McKinsey & Co. and served as Managing Director at the Corporate Executive Board focused on corporate strategy, banking and insurance, and risk management. Previously, Wayne was an investment banker with Merrill Lynch and Goldman Sachs as a member of the Mergers & Acquisitions teams. He has also served on the Board of his family-held community bank during its growth from $200 million to $1.1 billion in assets. Wayne received his A.B. from Princeton University and his J.D. and M.B.A. from Columbia University.

4

What is BancAlliance?

A network of 225+ Member Banks

o Typically $200MM - $10BN in total assets

o 15-person Board of Directors

o Independent credit policies, procedures & voting structures

o Managed by the asset manager, Alliance Partners

5

1. Community Bank Evolving Landscape

2. Avenues for Diversification

– Consumer Hybrid Lending Platform

– Small Business, In-Market Lending Platform

New Lending Platforms for Community Banks

6

The Evolving Community Bank Landscape

Community Bank’s Share of U.S. Banking Sector

Loan Portfolio Diversification of Community Banks

1

2

Source for top graph: SNL data for all banks based on total assets since 1990 year-end Source for bottom graph: SNL data for community banks $200MM to $10B in total assets in 3Q 1990 and 3Q 2016

83%

17%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Large Banks ($10BN+ Total Assets) Community Bank (Below $10BN Total Assets)

7

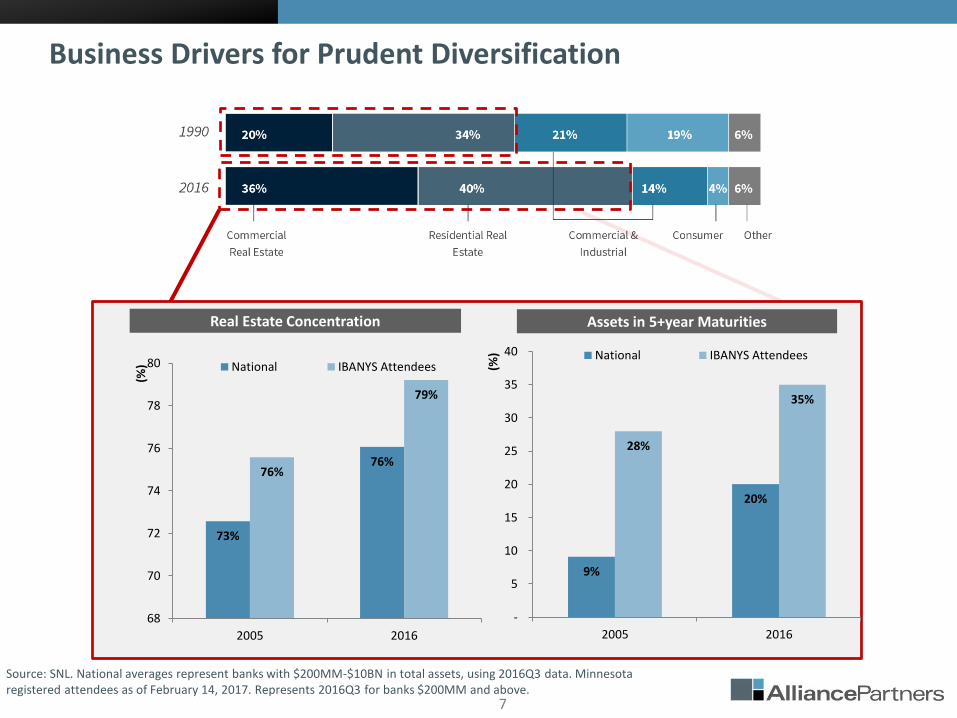

Business Drivers for Prudent Diversification

Real Estate Concentration

Source: SNL. National averages represent banks with $200MM-$10BN in total assets, using 2016Q3 data. Minnesota registered attendees as of February 14, 2017. Represents 2016Q3 for banks $200MM and above.

Assets in 5+year Maturities

“Historical evidence demonstrates that financial institutions with weak risk management and high CRE credit concentrations are exposed to a greater risk of loss and failure.” - Federal Banking Regulators

73%

76% 76%

79%

68

70

72

74

76

78

80

2005 2016

(%) National IBANYS Attendees

9%

20%

28%

35%

-

5

10

15

20

25

30

35

40

2005 2016

(%) National IBANYS Attendees

8

Business Drivers for Prudent Diversification

Represent banks with $200MM-$10BN in total assets Source: SNL. Represents data for Q3 1990 and Q3 2015 data.

Market Share of Consumer Loans

70%

30%

0%

20%

40%

60%

80%

100%

Banks Below $10BN Banks Above $10BN

8%

92%

0%

20%

40%

60%

80%

100%

Banks Below $10BN Banks Above $10BN

1990 2015

Community banks have lost market share in a $1.3 trillion marketplace they once dominated.

9

Drivers of the Shift

Most community banks

are unable to compete

independently due to

economies of scale across

the business including risk

analytics, advertising, ops,

compliance, and servicing

The Consumer Finance Challenge and Opportunity

Implications for Community

Bankers

Narrower customer

relationships (implicitly

inviting the big banks in)

Loss of earning assets

Loss of diversification However,…

Community banks enjoy superior customer relationships (consumers

would much prefer to do business with them over bigger banks)

Community banks enjoy superior cost and stability of capital

Source: Wall Street Journal, February 9th, 2015

10

Real Estate

Merchant Cash

Advance

Pay Day

Education

Financing

Explosion of New Lenders Marketplace Lending Developments and Opportunities_vFinal.pptx\31 AUG 2014\3:25 PM\2

FinTech Landscape

SMB Credit

Consumer

Purchase

Financing

All Shapes, All Sizes

11

The Opportunity

Generate Loan Growth and Diversification Hold a diversified portfolio of high FICO score consumer whole loans consistent with strict underwriting guidelines.

Deliver a Superior Customer Experience Provide access to a borrower-friendly, pre-approved loan with competitive rates.

Trusted Compliance Management Oversight With expertise in regulatory and compliance issues, BancAlliance provides comprehensive program oversight.

Limited Investment Required Partner provides marketing, services loans and creates the technology customer-interface.

Potential for Attractive Risk-adjusted Returns

Consumer Lending: Partnership Strategic Benefits

Independent RISK Analysis*

Average Borrower FICO 706 - 727

Average Borrower Debt-to-Income 16.0% - 20.0%

Average Borrower Income 76,000 - 92,000

Gross Rates 7.5% - 13.98%

Charge Off / Prepay Impact 1.8% - 6.6%

Lending Club Servicing Fee 0.9% - 1.0%

BancAlliance Servicing Fee 0.5%

Weighted Average Estimated Net Yield 4.2% - 5.9%

* Performed by MTG Risk, LLC using Lending Club data as of 7/7/16

12

Consumer Lending: Illustrative Economics

Lending Club Risk Grade A B C

Average Borrower FICO (1) 729 713 701

Average Borrower Debt-to-Income (1) 17% 19% 21%

Average Borrower Income (1) 100,100 85,100 76,700

Projected Distribution (2) 35.0% 35.0% 30.0%

Average Gross Rate (3) 7.1% 10.8% 14.2%

Charge Off / Prepay Impact (4) 1.9% 3.9% 7.2%

Lending Club Servicing Fee (5) 0.9% 1.0% 1.0%

Alliance Partners Servicing Fee (6) 0.5% 0.5% 0.5%

Net Yield by Grade 3.7% 5.3% 5.5%

Combined Net Yield 5.2%

(1) Statistics based on BancAlliance Portfolio as of December 2016

(5) 1.0% of average principal balance, expressed in yield terms

(6) 0.6% of average principal balance, expressed in yield terms

YIELD ANALYSIS

(3) Based on weighted average of all Lending Club loans, using rates as of 4/1/17, not reflective of

BancAlliance credit criteria

(4) Based on expected prepay/default curves from Lending Club, not reflecting any potential

improvement from BancAlliance credit criteria

(2) Distribution by credit grade will vary. Current mix based on BancAlliance experience to date

13

Small Business Online Lending Capability is Increasingly Critical

19%

1%

24%

11%

0%

5%

10%

15%

20%

25%

30%

Businesses w/ <$1MM Revenue Businesses w/ $1-10MM Revenue

% of Businesses Indicating They Pursued an Online Lending Option

2014 2015

Simplicity, speed and higher likelihood of success drive businesses to consider an online solution

14

Community Banks Wrestle with Different Pieces of the Puzzle Marketplace Lending Developments and Opportunities_vFinal.pptx\31 AUG 2014\3:25 PM\2

24/7 Online & Mobile Application

Loan Analytics & Document Capture

Integrated Referral Options for Customers a Bank Doesn’t Approve

Full Solution (Incorporating All Three Options)

More Efficiently Serve Customers

Deliver a “Yes” to More Customers

Reach More Customers

15

24/7 Online and Mobile Application Marketplace Lending Developments and Opportunities_vFinal.pptx\31 AUG 2014\3:25 PM\2

Instant ability to accept applications 24/7 from any device including mobile

Hosted by Fundation – no burdensome integration, setup or maintenance costs

16

Loan Analytics and Document Capture Marketplace Lending Developments and Opportunities_vFinal.pptx\31 AUG 2014\3:25 PM\2

Reduce burden and cost for bank and customer

Enhance quality and rigor of credit decisions

Slash underwriting timelines

Improve customer experience

DIGITAL LOAN FILE • Application Data • Consumer Credit File • Commercial Credit File (PayNet) • Public Record Data (Personal & Business) • Bank Account Transactional Data

CREDIT WORKFLOW SCREEN

17

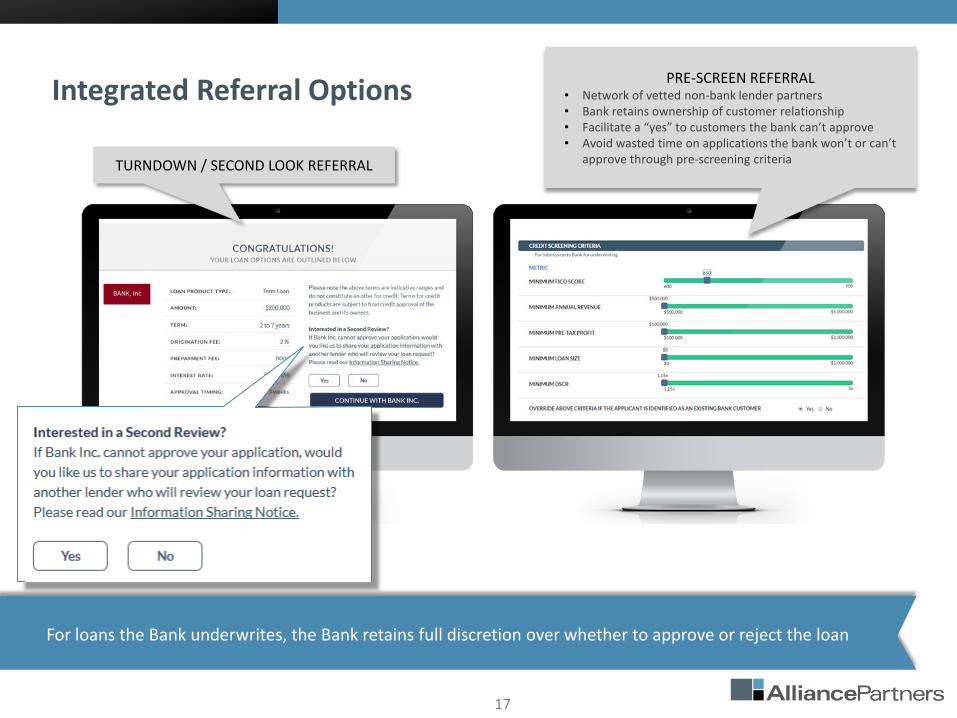

Integrated Referral Options Marketplace Lending Developments and Opportunities_vFinal.pptx\31 AUG 2014\3:25 PM\2

For loans the Bank underwrites, the Bank retains full discretion over whether to approve or reject the loan

TURNDOWN / SECOND LOOK REFERRAL

PRE-SCREEN REFERRAL • Network of vetted non-bank lender partners • Bank retains ownership of customer relationship • Facilitate a “yes” to customers the bank can’t approve • Avoid wasted time on applications the bank won’t or can’t

approve through pre-screening criteria

18

Selected Small Business Case Studies* Marketplace Lending Developments and Opportunities_vFinal.pptx\31 AUG 2014\3:25 PM\2

Speed to “Yes” “Bridge” Loan before SBA Loan Cash Flow Management Loan

Borrower need/ benefit: Customer reached out for funds to bridge the gap before an SBA loan would be approved and funding available. Bridge funding was immediately available and used to purchase materials and furniture to get the new business started while SBA funding process was pending.

Community Bank Small Business Lending Platform* *Powered by BancAlliance and Fundation

2 1 3

Bar/Restaurant Group Borrower

Gymnastics/ Martial Arts

Studios Borrower

Grocery Store Borrower

Borrower need/benefit: Customer wanted to grow into newer building as part of its business expansion, but was burdened by two mortgages that negatively impacted cash flow, which challenged their ability to raise funds via traditional community bank underwriting process.

Borrower need/benefit: Customer’s cyclical business had varying liquidity needs across the year and needed financing for incremental liquidity for day to day operations and inventory, rather than traditional small business loan for a single purpose. Traditional bank underwriting for business LOC was 2-3 weeks for approval.

Bank benefit: Deposits transferred from Regional Bank to the Community Bank that facilitated the loan; bank made up-front referral fees and receives on-going referral fees.

Bank benefit: Deposits retained by the Community Bank; successful cross-sell of cash management and other business products; bank made up-front referral fees and receives on-going referral fees.

Bank benefit: Bank underwriting efficiency improvement with the platform significant streamlined underwriting. Approval process improved from 2-3 weeks to 2-3 days.

*Sample loans are presented for illustrative purposes only to provide examples of the types of loans made available through the Fundation platform. BancAlliance members may or may not own these sample loans at this time.

19

An Overview of the

BancAlliance Platform

20

Executive Overview

The BancAlliance network is a shared lending platform that provides its community bank members with a broad array of loan programs and services, including sourcing, underwriting and managing loans that might otherwise be inaccessible.

Our mission is to enable our members, the banks that direct our activities, to prudently diversify

into high-quality commercial, consumer and other loans in a manner consistent with the

highest commercial and regulatory standards – without changing the nature or mission of the

traditional community bank.

21

How the Network Operates

BancAlliance is a Maryland non-stock corporation,

governed by a member elected Board of Directors

Eligible US banks have the opportunity to join the network by executing membership documentation. Members elect the Board of Directors, who adopt and maintain BancAlliance’s oversight policies.

Alliance Partners is an SEC- registered investment adviser

and serves as the asset manager for BancAlliance

Alliance Partners is responsible for identifying opportunities for the network, for negotiating and managing partnerships, and for sourcing, underwriting and approving all loans and loan programs prior to referring them to the network.

BancAlliance is supported and managed on a

day-to-day basis by Alliance

Partners

Registration with the SEC or with any state securities authority does not imply a certain level of skill or training.

22

Deep Expertise Alliance Partners offers a strong team drawn from industry leading firms with expertise specific to BancAlliance loan programs. In addition, members of the Alliance Partners management team have had decades of experience managing lending businesses through a variety of credit cycles. The team is in service to BancAlliance members.

Specialized Focus Alliance Partners focuses on identifying the specific challenges facing community banks and developing innovative solutions that advance the interests of BancAlliance members.

Strong Compliance Framework Alliance Partners recognizes the critical importance of regulatory compliance and designs the BancAlliance loan programs and services to operate in a manner consistent with regulatory expectations. To the extent possible, Alliance Partners seeks to minimize the regulatory challenges and costs imposed on members.

Alignment of Interests The BancAlliance Board of Directors ensures that the interests of members and Alliance Partners are aligned.

Fiduciary Duties and Oversight Alliance Partners is a registered investment advisor subject to oversight and examination by the SEC.

The Asset Manager

Alliance Partners is the investment advisor to BancAlliance members. Alliance Partners deploys a specialized orientation and set of resources to help members meet their asset and return objectives.

Registration with the SEC or with any state securities authority does not imply a certain level of skill or training.

23

We provide cash flow-based financing alongside experienced private equity sponsors to fund growth, acquisitions, expansion, or recapitalization of middle-market businesses with approximately $10-75 million in EBITDA. We typically source senior term and revolving debt facilities ranging in size from $40-250 million and secured by all of the assets and stock of the business. These loans generally have five-year terms and variable interest rates. Members always have the right but never the obligation to participate in any given loan.

We have partnered with Lending Club, a leading marketplace lender, to provide community banks access to a user-friendly consumer lending platform. Members are able to participate in consumer lending without having to maintain the expensive platform and processes that such lending requires. The program is designed to enable member banks to offer an attractive unsecured consumer loan product to their customers, and to add consumer loans to their balance sheets, generating interest income and diversifying loan portfolios.

We have partnered with Fundation, a technology-enabled lender serving the small business market. Members that elect to participate in this program have access to a small business lending platform that can be integrated into branch and online workflows. The platform facilitates the collection of applicant information 24/7 through a bank's website. The platform delivers an electronic credit file to the bank, incorporating data sources and analytics; this credit file can improve the efficiency and timeliness of decision-making. We have partnered with Personal Capital, a registered investment advisor serving the wealth management market. Member bank customers have access to leading software tools to consolidate and view financial assets, cash flow, and estate and retirement planning positions. Customers with $25,000 or more of investable assets receive preferred access to licensed investment advisors traditionally supporting the highest net worth customers.

Current BancAlliance Programs

Commercial Loan Program Small Business Loan Program

Wealth Management Program Consumer Loan Program

Washington, D.C. 4445 Willard Avenue, Suite 1100

Chevy Chase, MD 20815

Telephone: (301) 232-5400 www.bancalliance.com // www.alliancepartners.com