achieving the competitive edge in the innovation...

TRANSCRIPT

Achieving the Competitive Edge in the Innovation Economy

Georgia Tech Economic Development Course

March 14, 2007

Mary Jo Waits

Center Director

Pew Center on the States

The Challenge: Responding to….

8 Big Forces

1. The Idea-Driven Economy

2. The New Business Model

3. The Talent Imperative

4. The “Big Sort”

5. New Calculation for Quality of Place

6. New Definition of Success

7. New Focus on Place-based Assets

8. The Search for Regional Stewards

1. The Idea-Driven Economy

“The first 100 years of our country’s history were about who could build the

biggest, most efficient farm.

The second 100 years were about the race to build efficient factories.

The third 100 years are about ideas.”

(and experiences)-- Seth Godin

Fast Company, August 2000

New Growth Theory: Stanford Economist Paul Romer’s Perspective

Ingredients

• Intellectual capital

• Human capital

• Financial capital

Recipes

• New ideas

• Entrepreneurs

• Networks

Results

• Productivity

• Prosperity

• Cluster vitality

Source: Collaborative Economics

“Recipes” combine resources in new and different ways

In 1971, a small coffee shop starts in Seattle’s funky Pike Place Market with a new “recipe”

“Recipes” combine resources in new and different ways

Nanotech: You start with building blocks like nanowires, nanotubes, and nanoparticles. Put together one way, these building blocks make a computer. Put together in a different way, they make a biological sensor.

Biology is another example. You have a limited number of building blocks, like proteins and DNA. Depending on how you put them together, you end up with a tissue, a worm, or a human being.

Charles Lieber, Harvard Chemistry Professor & co-founder, Nanosys

Innovation is Added as Indicator

Performance Indicators

Innovation Output

Patents

Firm formations

VC investments

IPOs

Fast growth firms

Overall Economy

Employment growth

Unemployment

Average wages

Wage growth

Cost of living

Exports

2. The New Business Model

Companies and entrepreneurs moving from “closed innovation” (in-house research capability) to “open innovation” model.

“Many companies are starting to innovate with research discoveries of others.”

Harvard Professor Henry Chesborough, Open Innovation, 2003

Intel’s “Lablets”

Small-sized research facilities adjacent to top university research centers

Intel expects to benefit from proximity –gain early access to promising new technologies

Applies to all companies, not just high-tech

Procter & Gamble names director of external innovation—Goal: 50% of its innovation from outside the company in 5 years

Why? Inside more than 8,600 scientists advancing the industrial knowledge that enables new offerings; outside are 1.5 million.

“So why try to invent everything internally?”

Global Business Model

ManilaCosta Rica

Dublin

BangaloreBombayHyderabadChennaiiPune

Israel

BeijingShanghaiShenzhenGuang ZhouHong Kong

MoscowBudapestPrague

Hsinchu

•Washington D.C.

•Boston

•Minneapolis

•Atlanta

•Phoenix

•Seattle

•Austin

•San Diego

•Portland

•Raleigh-Durham

•Denver

•Sacramento

•Salt Lake

Firms tap talent and serve markets globally, from their start.

San Diego: Rise of a BioTech Cluster

Today: 3rd Biotech hub behind San Francisco & Boston

North Torrey Pines Road: Densely packed 2-mile stretch w/ Scripps Research Institute, Salk Institute for Biomedical Studies, UCSD

“We can throw a rock and hit UCSD. I can hit a golf ball and hit Scripps. Everything is within walking distance. That means more heads get together and we do a lot of collaboration.” VP at Salk Institute

3. The Talent Imperative

With “Innovate or Die” the first rule, the second rule surely is:

“Have Talent or Die”

Skilled people, not computers or raw silicon, are the fundamental source of the ideas and innovation that drive the economy.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1940-1950 1990-2000

New Work

Production Work41%

Creative Work16%

Creative Work30%

ProductionWork26%

Service Work31%

Service Work43%

Agriculture12%

Source: Richard Florida

Re-Valuing the Right Brain….

Logical

Mathematical

Linear

Sequential

Verbal

Rational

Serious

Intuitive

Artistic

Nonlinear

Simultaneous

Visual

Emotional

Playful

Can StayWill Go

See Daniel Pink, “The Whole Mind: Moving from the Information Age to the Conceptual Age”

What can stay, what will go?

Can Stay: “Right Brain”Work

Research

Design

Management

Marketing

Proprietary

Creative Core

Sand box

Will Go: “Left Brain”Work

Routine

Low Value

Cost Sensitive

Large Volume

The Challenge Ahead: Talent Gap

+20.9million

+3.5 million

Workforce Shortages Coming

2002-20121982-92

Growth in 25-54 year old population

Source: Bureau of Labor Statistics

4. The Big Sort

The 2000 Census revealed a whole new pattern in metropolitan growth—a brain-driven winner-take-all pattern

The 25 metro areas that already had the most college graduates in 1990 got more than their fair share of college graduates—twice as many, in fact.

Joe Cortwright, 2005

Talent Migration

-40% -20% 0% 20% 40%

% Change 25-34 year-olds, 1990 to 2000

50 Most P

opulous Metro A

reas

Average of Top 50 Metros

Big Shifts Among Metro Areas

Biggest Shifts in Talented 25-34s

Rank Metropolitan Area Change, 1990-2000

2 Charlotte, NC MSA 56.6%

3 Austin--San Marcos, TX MSA 56.2%

4 Portland--Salem, OR--WA CMSA 50.0%

5 Atlanta, GA MSA 46.2%

6 Denver--Boulder--Greeley, CO CMSA 40.1%

42 St. Louis, MO, MSA -0.7%

45 New Orleans, LA MSA -4.3%

49 Providence, RI MSA -7.0%

Change in College Educated 25-34s

Thinking about how you will look for and choose your next job, which of the following statements best reflects your opinion? (Asked of 1,000 25-34 year old college graduates)

Look for the best job I can find. The place where it located is pretty much a secondary consideration.

0% 20% 40% 60% 80%

Look for a job in a place that I would like to live

People now seek place

But, can’t Afford to Assume that Highly Educated Residents will “Stick” Around

Flurry of Research

Richard Florida, The Rise of the Creative Class

James Irvine Foundation, Linking the New Economy to the Livable Community

Edward Glaeser, Harvard Institute of Economic Research

Paul Gottlieb, Labor Supply and the “Brain Drain”: Signs from Census 2000

Make Sure Talented People Want to Live in Your Region

“Arugula is how I define cities. I go to a grocery store, and either you can get arugula or you can’t.”

Cindy Crawfordinternational super model

Young Talent Seeks…

Breadth and depth of employment options

Startup friendly

Intellectual vitality

Just-in-time recreation, “out & about”

After-hours spots

Diversity of cultures, thinking

Starter homes

Easy to get around town

Proximity to urban center

Source: Next Generation Consulting, 2002

5. New Calculation for Quality of Place--More Complex

Natural environment counts for a lot.

But natural features aren’t enough. Places must have distinctive urban amenities as well.

Choice (in lifestyle) matters in the talent war.

Being a smart, innovative place matters.

It’s not just about physical attributes. Intangibles such as tolerance and entrepreneurial culture are part of the calculation.

Speed is a vital amenity.

Waits, Which Way Scottsdale?, 2003

6. The New Definition of Success

1990-2000Income Growth Population Growth

1. San Francisco 27%

2. Austin 23%

3. Atlanta 23%

4. Seattle 21%

5. Tampa 21%

6. San Antonio 18%

7. Charlotte 18%

8. Cincinnati 17%

9. Colorado Springs 16%

10. San Jose 16%

59. Tucson 8%

74. Phoenix 5%

1. Las Vegas 62%

2. Bakersfield 35%

3. Austin 34%

4. Mesa 32%

5. Charlotte 31%

6. Phoenix 30%

7. Raleigh 28%

8. Colorado Springs 25%

9. Arlington 24%

10. Aurora 22%

Source: CEOs for Cities report, Weissbourd and Berry, October 2003

What Success Looks Like

Prosperity

(rising real income per capita)

Productivity/Competitiveness

(increased output per worker)

Innovationincreasingly higher-value products and services

produced more efficiently

Source: Council on Competitiveness

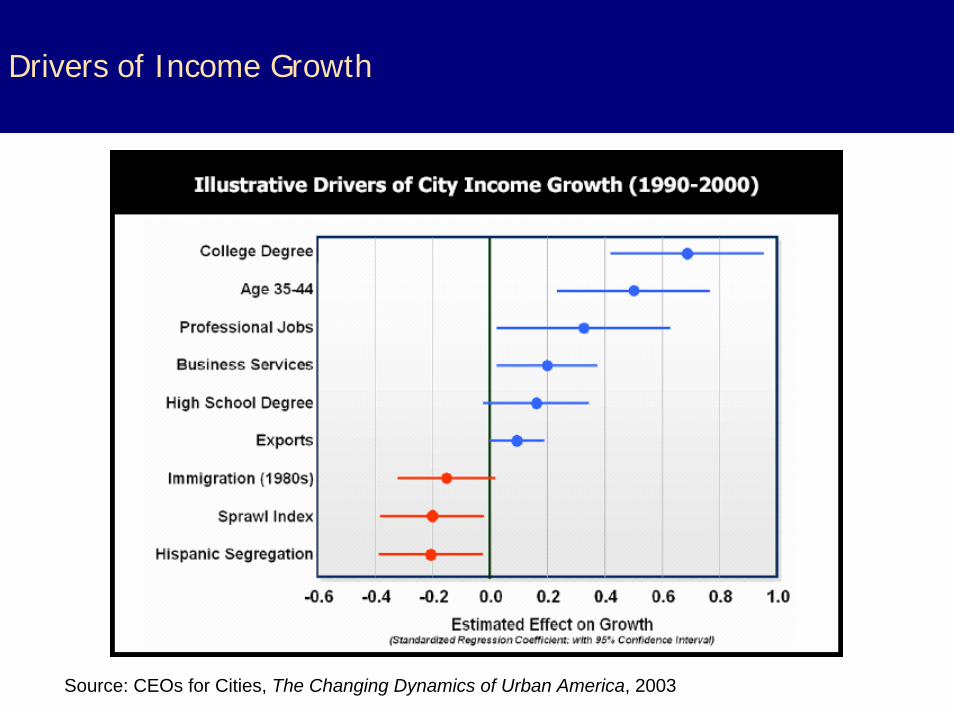

Drivers of Income Growth

Source: CEOs for Cities, The Changing Dynamics of Urban America, 2003

What Will Boost Per-capita Income?

Education Level

Science & Technology Activity

Export-oriented Industries

Entrepreneurial Initiative

Broad-based Innovation

The Creative Class

Reducing poverty and inequality

Shifting Sources of Wealth

Resources

Costs

Proximity

Clusters

Knowledge

Talent

Quality of Life

The Inherited Landscape

Traditional

CurrentThe Created Landscape

7. New Focus on Place

From Inherited Assets to Created Assets

Most Important Sources of Prosperity

Agricultural and Industrial Era

Inherited Assets

Natural resources

Geography

Climate

Population

Knowledge and Innovation Era

Created Assets

Top universities

Research centers

Talented people

Entrepreneurial culture

Networks

Amenities

Elements of a Knowledge-based Economy

5 tangible elements:

A strong intellectual infrastructure (universities and firms generating new knowledge and discoveries)

Mechanisms through which knowledge is transferred from person-to-person / firm-to-firm

Excellent physical infrastructure (high-speed internet)

A highly skilled technical workforce

Good sources of capital

2 intangible elements:

Entrepreneurial culture

Quality of lifeSource: National Governors Association

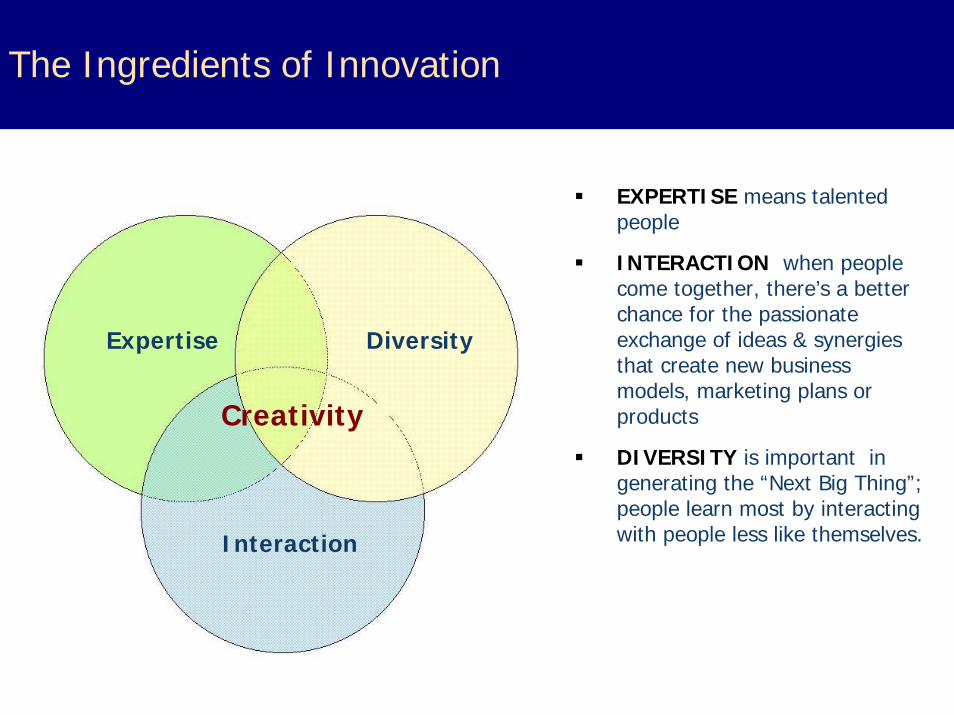

Expertise Diversity

Interaction

Creativity

EXPERTISE means talented people

INTERACTION when people come together, there’s a better chance for the passionate exchange of ideas & synergies that create new business models, marketing plans or products

DIVERSITY is important in generating the “Next Big Thing”; people learn most by interacting with people less like themselves.

The Ingredients of Innovation

Building Expertise

Focused Excellence: Georgia Research Alliance, CA Institutes for Science and Innovation

Talent: Lilly Endowment’s $100 M for “intellectual capital,” Georgia's 100 eminent scholars, USC’s goal of 100 high-profile professors, Science Foundation Ireland recruiting 50 world-class scholars by 2008

State-sponsored Research Funds: CA, TX, NJ, NY, MI, AZ, OH

Orchestrating Interaction

UCSD CONNECT “Meet the Researcher”

ASU’s supercomputer; Engineering school moves to “main street”

Innovation Districts Atlanta’s Technology Square, Torrey Pines, Research Triangle Park, PA’s Keystone Innovation Zone, St. Louis’s CORTEX 1,000 acres for medical research district

Partnerships and Networks Georgia Cancer Coalition, St. Louis Coalition for Plant and Life Sciences, BIOCOM

Putting people from Diverse fields and cultures together

AZ Biodesign Institute—co-locates 3 O’s

UC Discovery Grants

NIH starting to encourage interdisciplinary research

Silo, Solo is Passé

Where Sparks Fly

“It’s all designed for interaction.” All of us are smarter than any one of us.”

Douglas Merrill

Google VP of engineering describing the company’s space in Tempe

New Workplaces

More…

Alternative work arrangements

Dedicated meeting and collaboration spaces

Flexible work spaces

Shared amenities—campus, community

Vertical possibilities

Investment in technology/infrastructure

Less…

Office space per worker

Hitachi’s Plan: mixed-use, interaction, public spaces, synergy

Retrofitting the Suburban Business Park

7. The Search for Regional Stewards

The new century will be a highly competitive one—especially as cities and regions realize that key features are “buildable” and thus can be had by nearly any place that puts its mind to it.

But who takes the lead?

Framework for Stewardship

Innovative EconomyPreparing people andplaces to succeed

Social InclusionEnsuring that everyone participates and shares responsibility

Collaborative GovernanceFinding creative ways to govern

Livable Community

Preserving and creating places to live and work

Stewards

of Place

The Challenge Ahead:Strategic, Sustained Effort

“There was no single defining action, no grand program… no solitary lucky break, no wrenching revolution.

Good to great comes about by a cumulative process--step by step, action by action, decision by decision, turn by turn of the flywheel—that adds up to sustained and spectacular results.”

Jim Collins, 2001

Playing a leading role in the Innovation Century will take:

New Era Thinking: Move from Cheaper Here, Made Here, and Grown Here to: Invented Here. Discovered Here. Started Here.

Sustained, Resolute Effort: These new ambitious will not be realized unless they serve as a long-term guide for public policy.

Exceptional People: There is no substitute for talent—it’s the path to greatness.

The Collaborative Gene: No more silos. New ideas require collaboration. So does bold public policy.

Arizona’s Strategic Moves

Three “Big Bets” on an innovation future

Three “Big Bets”

Big Bet No. 1Target export-oriented, knowledge intensive clusters to build strengths in:

Electronics/Information Technology

Aerospace

Software

Biomedical

Advanced Business Services

Optics

Three “Big Bets”

Big Bet No. 2

Prop 301, a sales tax increase which citizens approved in 2000, earmarks $1 billion over 20 years, distributed among the state’s 3 universities

Arizonans recognized that K-12, community colleges, top-tier universities are a critical infrastructure for the 21st century

In 2003, AZ legislature approved $440 million in research facilities at 3 universities—12 new research facilities

Three “Big Bets”

Big Bet No. 3Genomics – $90M raised in 2002 to jumpstart the bioscience industry with attraction of TGen and IGC

Battelle Biosciences Roadmap to develop 3 areas: Cancer therapeutics

Neurological sciences

Bioengineering

Lots of Ownership

Biodesign Institute at ASU

BIO5 at University of Arizona

Technopolis – entrepreneurial support

Arizona Board of Regents - metrics for 301 funds

Arizona Biomedical Collaborative—3 universities

Legislature passes Angel Investor tax credit

Maricopa Community College district-- $1.5 M training for bioscience

Foundations continue to support TGen and top talent

Greater Phoenix Leadership—Bioscience Task Force

Cities connecting to Big Bets

Phoenix Downtown “Knowledge Anchors”Scottsdale Los Arcos, Mayo Clinic R&DChandler potential Intel and ASU NanoInstituteTucson’s UA Research Park and new Critical Path Institute Flagstaff’s NAU partners with TGen

More Big BetsUA/ASU Medical SchoolMaricopa Partnership for Arts and Culture

Austin: City of Ideas

Three decades ago: Sleepy University/Govt Town (per capita income 85% of US average)

Today one of 20 “Cities of Ideas” (per capita income is 107% of US average)

Started with Vision: “Poised for Greatness” - IT and quality of life

Attracts Motorola, AMD in 70s; MCC research consortium; SEMATECH-13-firm research consortium; many IT- related firms follow

UT top 10 of engineering graduate schools (1989)

Multiple startups: Dell and spin offs from UT

San Diego: Rise of a High-Tech Cluster

Geography produces tourist & military town and begets Scripps Institute (1912)

Today: 3rd Biotech hub behind San Francisco & Boston

North Torrey Pines Road: Densely packed 2-mile stretch w/ Scripps Research Institute, Salk Institute for Biomedical Studies, UCSD

Rise of High Tech Clusters

• City dredges harbor, 1907

• City gives land to General Atomics to increase HT (1956); designated S&T zone; spawns 60 companies

• Leaders get a University (UCSD)—post-grad science focus (1960); in 1990’s, spawns 69 companies

• UCSD professor starts Linkabit becomes Qualcom & Leap Wireless (1968) ; UCSD scientists founded Hybritech

• Salk Institute (1960) ; since 1980’s spawns 17 companies

• Scripps produces 40 companies in similar time

• UCSD CONNECT (1995) “meet the researcher”

• BIOCOM—informal network

• $1 B in private VC (2002) ; $ 500 M annually NIH

• UCSD opens graduate business school (PhD/MBA)