acme technology and the future of auto insurance - december 4, 2014

TRANSCRIPT

IMS Inc. Proprietary and Confidential

Autonomous cars, digital, & the future of insurance

Discussion with Acme insurance, December 4, 2014

IMS Inc. Proprietary and Confidential

Purpose

• This is a point of view about how autonomous cars, and related digital technology, will transform auto insurance in the next decade

• The culmination of this is a discussion on the implications and indicated action of this emerging technology

IMS Inc. Proprietary and Confidential

Benefits

• Acme can gain a “greater share of the future” by harnessing the key technology, trends and the respective impact of these trends the following strategic choices • Enhancing current services

• Adding new services

• Reducing current services

• Removing services

IMS Inc. Proprietary and Confidential

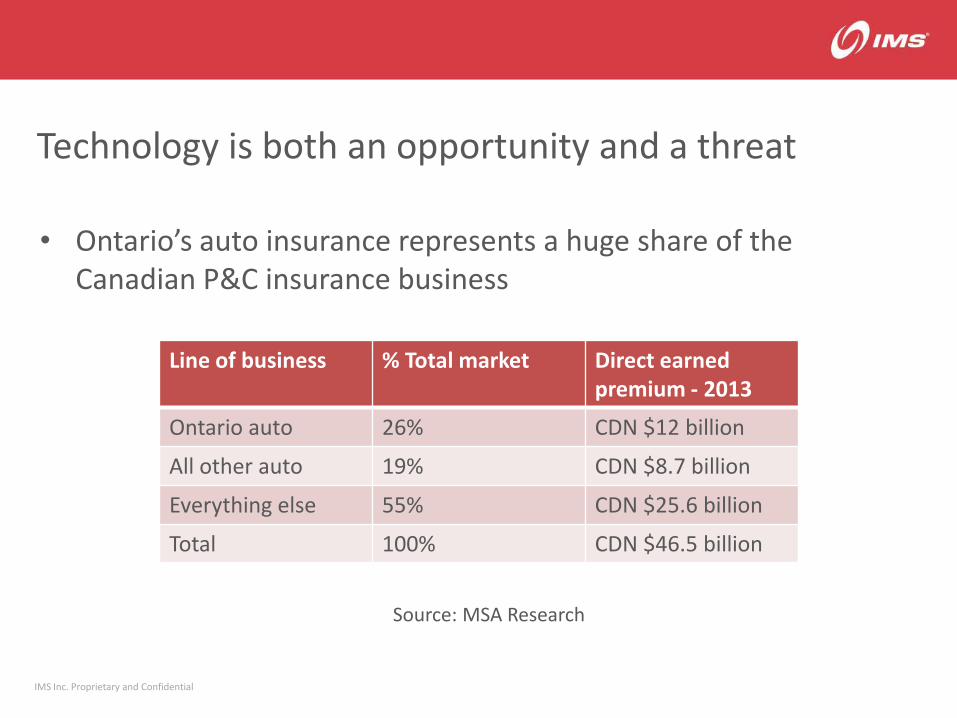

Technology is both an opportunity and a threat

• Ontario’s auto insurance represents a huge share of the Canadian P&C insurance business

Line of business % Total market Direct earned premium - 2013

Ontario auto 26% CDN $12 billion

All other auto 19% CDN $8.7 billion

Everything else 55% CDN $25.6 billion

Total 100% CDN $46.5 billion

Source: MSA Research

IMS Inc. Proprietary and Confidential

Driverless cars will have the largest impact on this business, but should be viewed in context of other, related digital technologies

Car sharing

Telematics and usage based insurance

Collision Avoidance

Automated enforcement

Autonomous cars

IMS Inc. Proprietary and Confidential

Impact of digital technology on auto insurance

Technology Social impact Insurance impact

Car sharing (B2C & P2P)

Fewer cars on the road Smaller insurance market How to insure shared vehicles?

Telematics Initial self selection Behaviour modification

Good drivers attracted to telematics Reduced claims

Collision avoidance

Reduced frequency and severity of property damage, bodily injury, accident benefits

Reduced need for auto insurance Premiums drop/profit could increase Fewer claims employees

Automated enforcement

Reduced number running red lights and speeding due to cameras

Increased safety & reduced claims Speed not considered by some telematics programs

Driverless cars Fewer claims due to less human error.

Separation of driver vs. vehicle related risk. Reduced claim frequency and severity

IMS Inc. Proprietary and Confidential

Car sharing will affect specific market segments more than others

Car sharing programs are used most by -Urban residents -Young people -Highly educated professionals -Travel for business -No kids

IMS Inc. Proprietary and Confidential

Telematics is more than pricing

Insure issues • Programs for specific

segments e.g., YDI

• CRM e.g., Chronicle

• FNOL/Claims management

Beyond insurance • Value added services e.g.,

Roadside assistance

• Automated traffic law enforcement

• Road charging

IMS Inc. Proprietary and Confidential

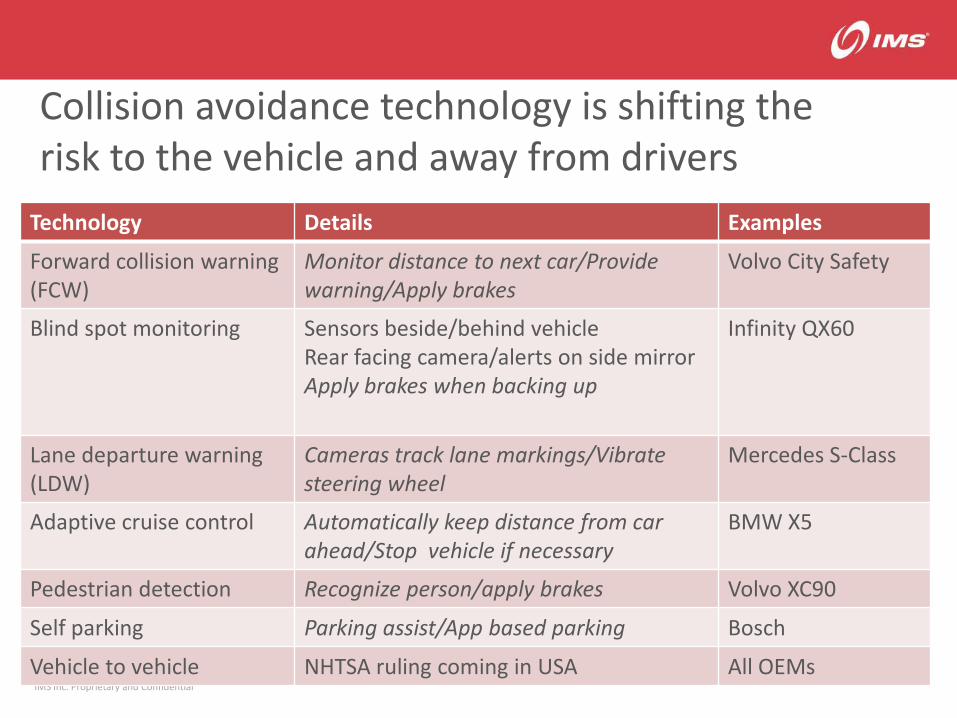

Collision avoidance technology is shifting the risk to the vehicle and away from drivers

Technology Details Examples

Forward collision warning (FCW)

Monitor distance to next car/Provide warning/Apply brakes

Volvo City Safety

Blind spot monitoring Sensors beside/behind vehicle Rear facing camera/alerts on side mirror Apply brakes when backing up

Infinity QX60

Lane departure warning (LDW)

Cameras track lane markings/Vibrate steering wheel

Mercedes S-Class

Adaptive cruise control Automatically keep distance from car ahead/Stop vehicle if necessary

BMW X5

Pedestrian detection Recognize person/apply brakes Volvo XC90

Self parking Parking assist/App based parking Bosch

Vehicle to vehicle NHTSA ruling coming in USA All OEMs

IMS Inc. Proprietary and Confidential

Traffic law and parking enforcement

• Automatic traffic law is common, albeit controversial

• Speeding is avoided as rating factor in telematics programs

• Red light and speed cameras popular

• In vehicle technology can afford automatic parking and tickets!

IMS Inc. Proprietary and Confidential

Driverless cars – available today

IMS Inc. Proprietary and Confidential

IMS Inc. Proprietary and Confidential

US States slightly ahead of Canadian provinces

IMS Inc. Proprietary and Confidential

Sample benefits of autonomous cars

Social

- Fewer accidents

- Lower need for vehicles (service vs.

product)

- Less need for road signage

Business

- Lower costs (delivery drones, lower

insurance)

Individual

-Better use of driving time

- Different use of your car (office, kitchen,

entertainment)

- Mobility on demand for older/very young

IMS Inc. Proprietary and Confidential

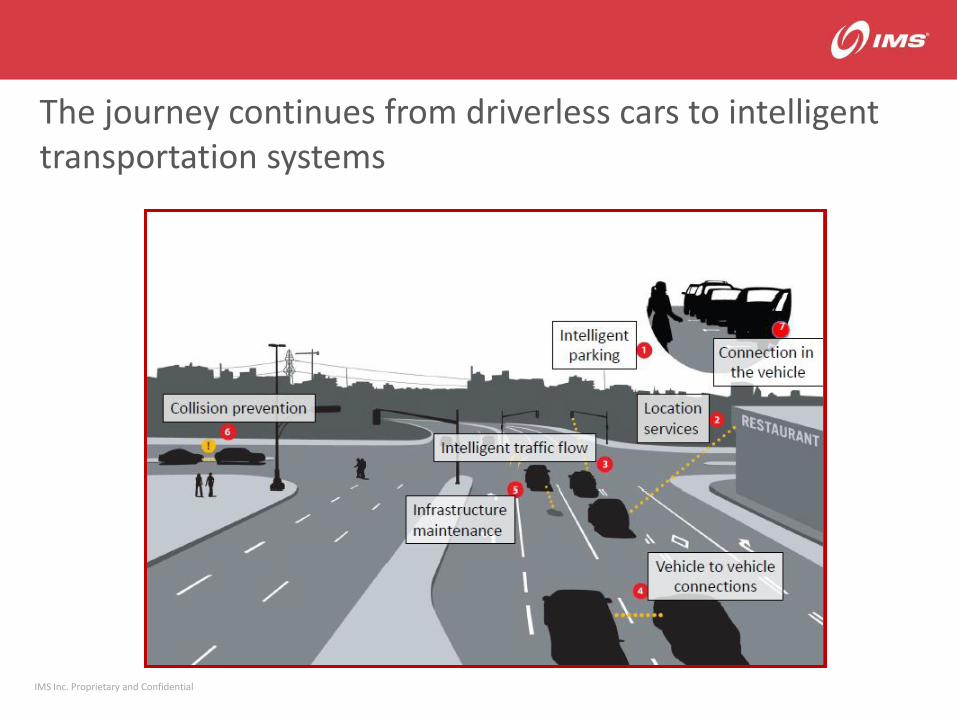

The journey continues from driverless cars to intelligent transportation systems

IMS Inc. Proprietary and Confidential

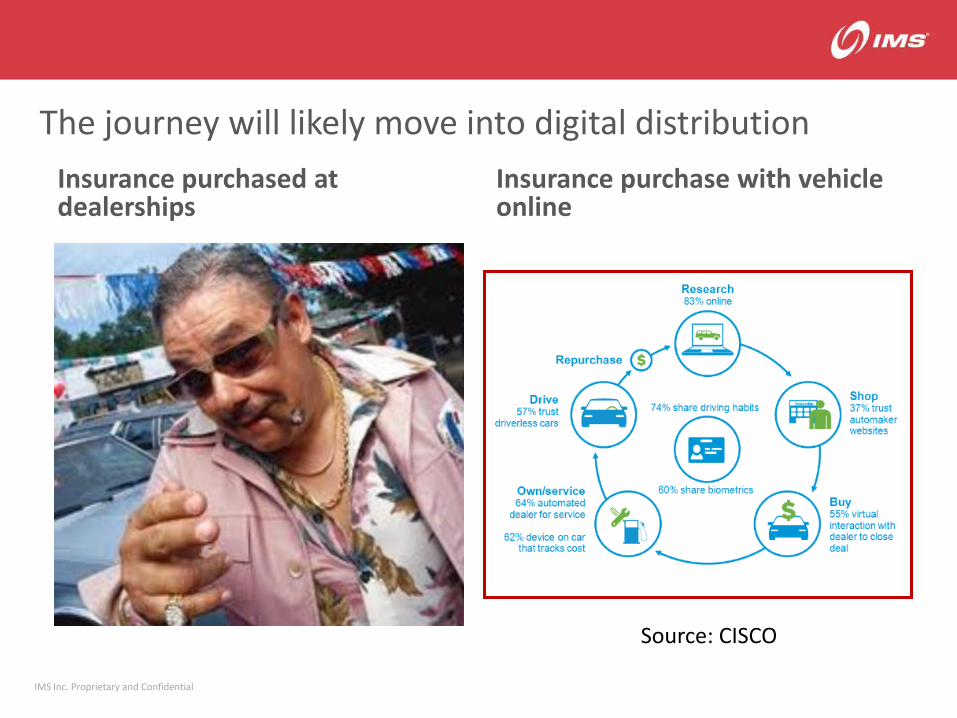

The journey will likely move into digital distribution

Insurance purchased at dealerships

Insurance purchase with vehicle online

Source: CISCO

IMS Inc. Proprietary and Confidential

Timelines: depends on the technology/region

Stage 2014 2015-2018 2019-2022 2023+

Available

Pilots

Preferred/ Incentives/ Special lanes

Mandatory/ Legislated

Collision avoidance

Collision avoidance

Collision avoidance

Car sharing

Telematics

Autonomous cars

Autonomous cars

Autonomous cars

Telematics

IMS Inc. Proprietary and Confidential

Many OEMs launching autonomous cars (sample)

2014-2017 2018-2020 2021+

2015 – Tesla cars 90% autonomous

2015 – Audi to sell low speed autonomous cars

2016 – GM offering Super cruise Cadillacs

2017– Google’s cars available to the public

2017 – Volvo to sell driverless cars

2017 – Nissan to sell driverless cars

2019– Tesla to offer full autopilot capability

2020– Audi, GM, Mercedes, Nissan and Renault to semi autonomous cars

2020– Volvo to sell “Crash free” autonomous car

2024 – Jaguar to launch driverless cars

2025– Daimler, Ford. GM release self-driving cars

2026-2035– Several source report that self driving cars will be the standard

IMS Inc. Proprietary and Confidential

Some issues related to autonomous/driverless cars

Technology

- Standards vs. proprietary

systems

- Cyber security

Legal

- Regulation

- Difficult to keep up with

a moving target

Social

- Mix of digital and analogue

vehicles and drivers

Moral Artificial

Intelligence

(M2M selects smaller objects)

IMS Inc. Proprietary and Confidential

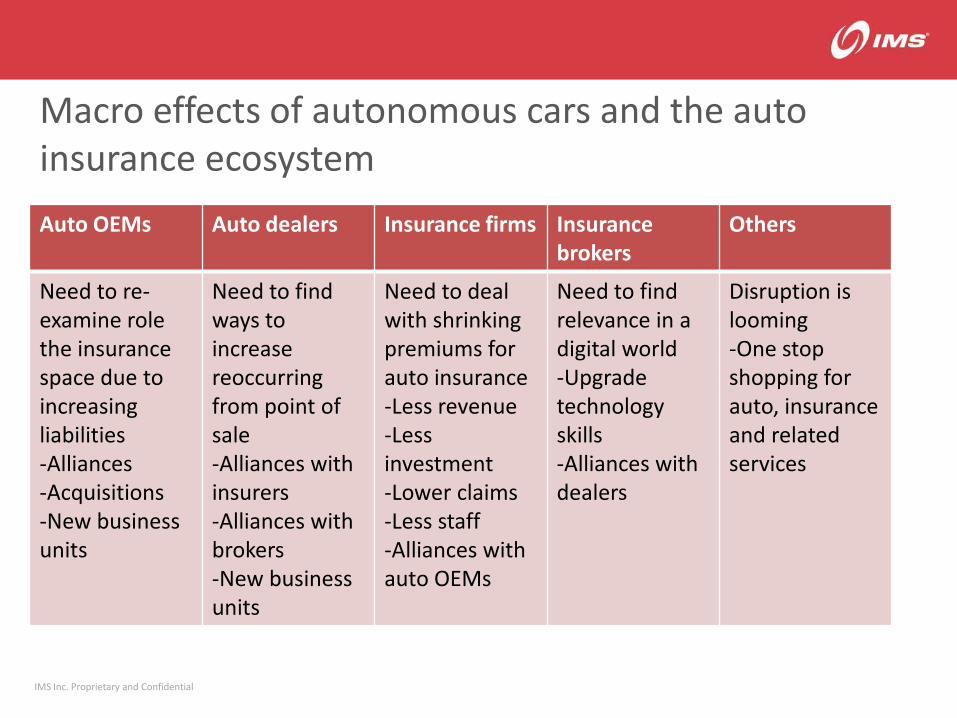

Macro effects of autonomous cars and the auto insurance ecosystem

Auto OEMs Auto dealers Insurance firms Insurance brokers

Others

Need to re-examine role the insurance space due to increasing liabilities -Alliances -Acquisitions -New business units

Need to find ways to increase reoccurring from point of sale -Alliances with insurers -Alliances with brokers -New business units

Need to deal with shrinking premiums for auto insurance -Less revenue -Less investment -Lower claims -Less staff -Alliances with auto OEMs

Need to find relevance in a digital world -Upgrade technology skills -Alliances with dealers

Disruption is looming -One stop shopping for auto, insurance and related services

IMS Inc. Proprietary and Confidential

Implications/indicated action for the auto insurance ecosystem

Auto OEMs Auto dealers Insurance firms Insurance brokers

Others

Need to re-examine role the insurance space due to increasing liabilities -Alliances -Acquisitions -New business units

Need to find ways to increase reoccurring from point of sale -Alliances with insurers -Alliances with brokers -New business units

Need to deal with shrinking premiums for auto insurance -Less revenue -Less investment -Lower claims -Less staff -Alliances with auto OEMs

Need to find relevance in a digital world -Upgrade technology skills -Alliances with dealers

Disruption is looming -One stop shopping for auto, insurance and related services

IMS Inc. Proprietary and Confidential

Implications/indicated action for the auto insurance industry with the growth of autonomous vehicles

IT Product/ Marketing

Sales/ Distribution

Underwriting Policy mgt. Claims

Need to keep up with changes in the auto industry

New products -Vehicle based -Driver based

Need to evaluate how to best sell these products -Direct -Special channel -New channels e.g., Dealers

Need to continuous find ways to price the risk of this changing technology

How to manage a change in policy with a client purchases a technologic-ally advanced vehicle

How to deal with decreasing claims