acommerce mobile world congress - new business models in southeast asia

TRANSCRIPT

Commerce + Mobile:Evolution of New Business Models in SEASheji Ho | July 2015

About aCommerce

Singapore | Thailand | Indonesia | Philippines

The Leading End-to-End Ecommerce Solutions provider in S.E. Asia

FOUNDED IN

2013With over 360 staff across Singapore,

Thailand, Indonesia, and Philippines

REVENUE

3xTripled revs in

second half of 2014

CLIENTS

100+30% are in Fortune top 1,000, 70% are recurring with 1-2 year agreements

MARKET GROWTH

30%Year-on-Year growth

for B2C and B2B Ecommerce market

in S.E. Asia

Singapore | Thailand | Indonesia | Philippines

4

End-to-end ecommerce solutions

Ecommerce Strategy & Consulting

Web & Mobile Development

Production, Photography, Copy Writing

Digital Marketing, CRM, and

Data

Channel Management on E-tailers & Marketplaces

Payment Gateways

Sourcing & Merchandising

Cross Border & Custom Clearance

ERP Integration & Accounting

Management

Customer Service & Call

Center

Warehousing and Order Fulfillment

Nationwide and Next Day Delivery with

COD

We focus on sales by providing turn-key solutions that drive a customer’s path to purchase

With our own fulfillment centers, delivery fleet, and proprietary technology we manage the entire E-commerce logistics supply chain

Demand Fulfillment

Demand Generation

Singapore | Thailand | Indonesia | Philippines

5

Raised over $15M in venture capital in 2 years

Evolution of New Business Models in Southeast Asia

Singapore | Thailand | Indonesia | Philippines

7

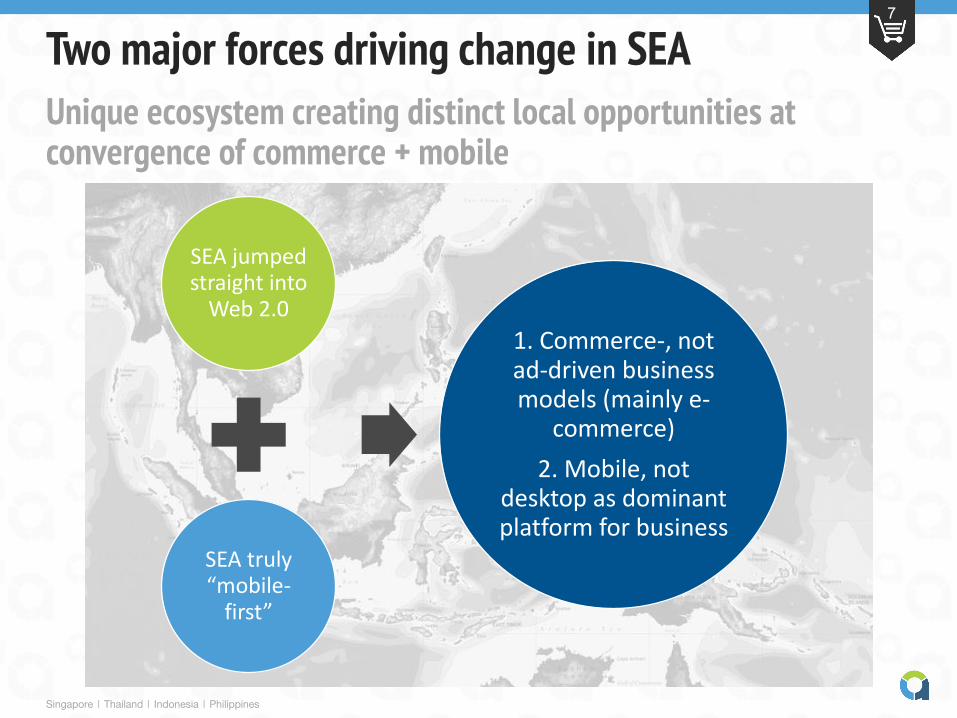

Two major forces driving change in SEA

SEA jumped straight into

Web 2.0

SEA truly “mobile-

first”

1. Commerce-, not ad-driven business models (mainly e-

commerce)

2. Mobile, not desktop as dominant platform for business

Unique ecosystem creating distinct local opportunities at convergence of commerce + mobile

Singapore | Thailand | Indonesia | Philippines

8

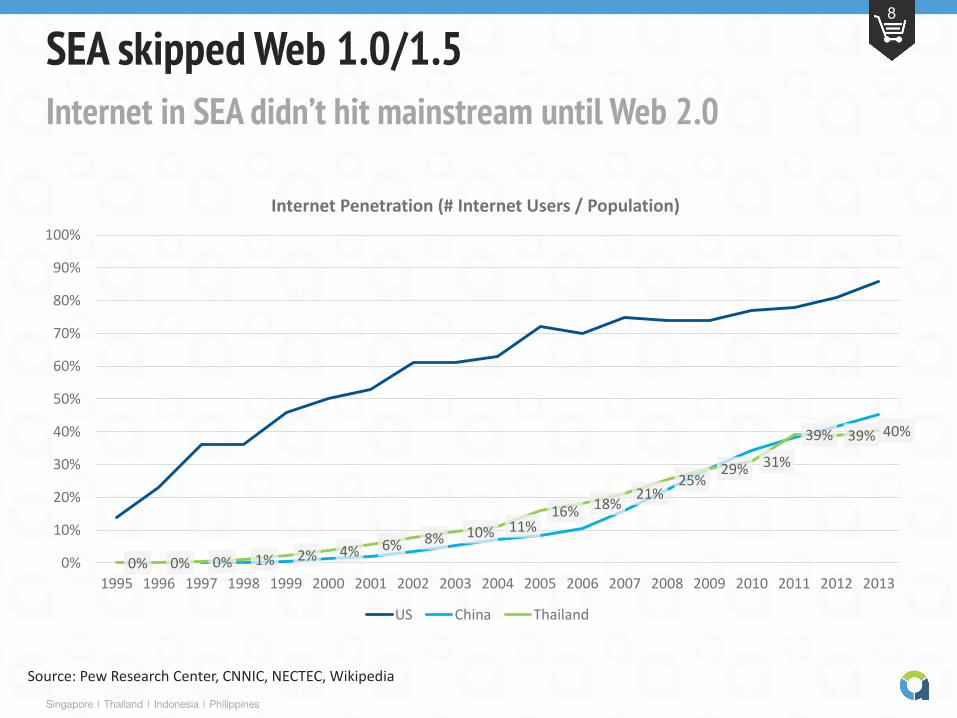

SEA skipped Web 1.0/1.5

0% 0% 0% 1% 2% 4% 6% 8% 10% 11%16% 18%

21%25%

29% 31%

39% 39% 40%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Internet Penetration (# Internet Users / Population)

US China Thailand

Internet in SEA didn’t hit mainstream until Web 2.0

Source: Pew Research Center, CNNIC, NECTEC, Wikipedia

Singapore | Thailand | Indonesia | Philippines

9

SEA skipped Web 1.0/1.5

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

US China Thailand

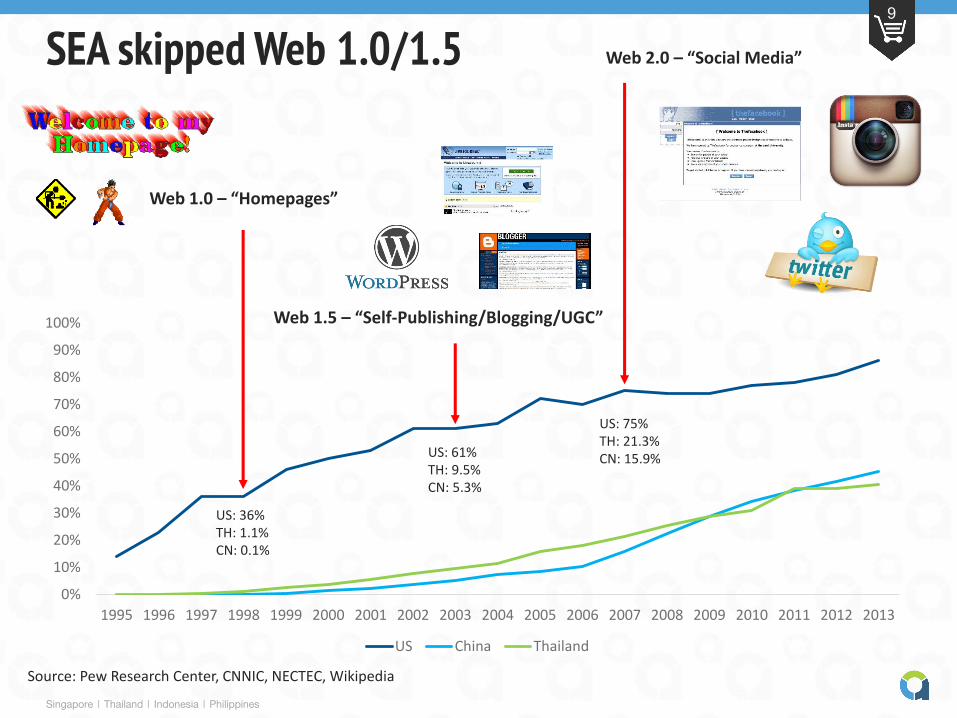

Web 1.0 – “Homepages”

US: 36%TH: 1.1%CN: 0.1%

US: 61%TH: 9.5%CN: 5.3%

US: 75%TH: 21.3%CN: 15.9%

Web 1.5 – “Self-Publishing/Blogging/UGC”

Web 2.0 – “Social Media”

Source: Pew Research Center, CNNIC, NECTEC, Wikipedia

Singapore | Thailand | Indonesia | Philippines

10

“No Tail” in SEA because it skipped Web 1.0/1.5

User generated content creation mainly happening on closed systems such as Facebook, Instagram, and Line

Singapore | Thailand | Indonesia | Philippines

11

No-Tail implications on ecosystem in SEA

• Relatively simple ad tech environment

• Affiliate marketing still nascent

• Demand-side platform (DSP) market still nascent

• Accelerated development and proliferance of e-commerce and other non-ad based business models

• “Traditional” digital agencies’ scope reduced to executing global contracts and buying offline media (in US, these agencies still have a role to play due to complicated ad tech environment)

Singapore | Thailand | Indonesia | Philippines

12

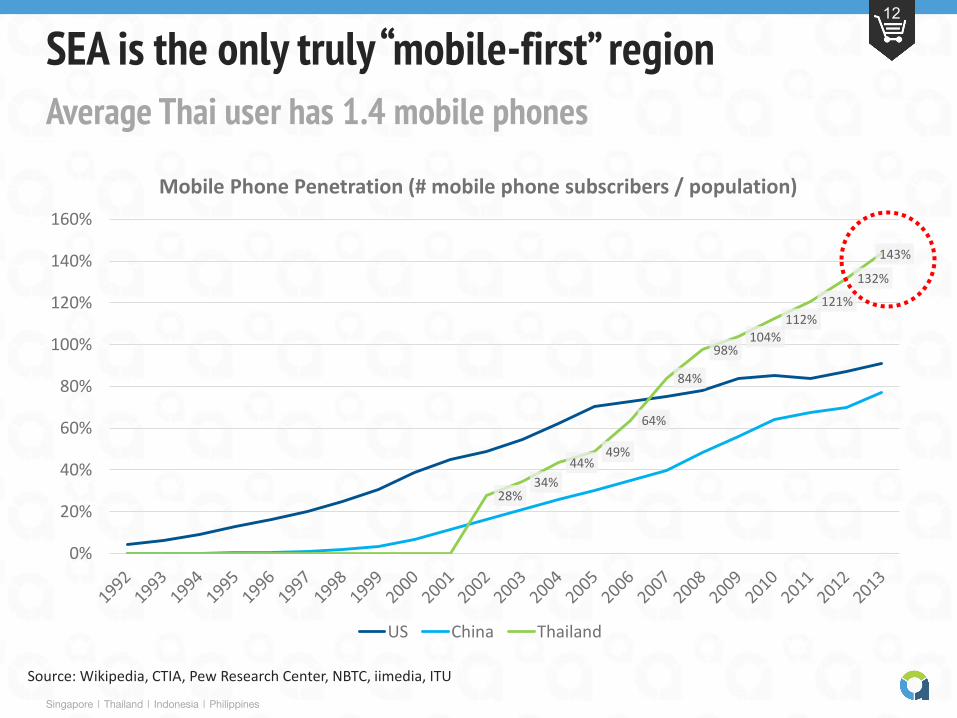

SEA is the only truly “mobile-first” region

28%34%

44%49%

64%

84%

98%104%

112%

121%

132%

143%

0%

20%

40%

60%

80%

100%

120%

140%

160%

Mobile Phone Penetration (# mobile phone subscribers / population)

US China Thailand

Average Thai user has 1.4 mobile phones

Source: Wikipedia, CTIA, Pew Research Center, NBTC, iimedia, ITU

Singapore | Thailand | Indonesia | Philippines

13

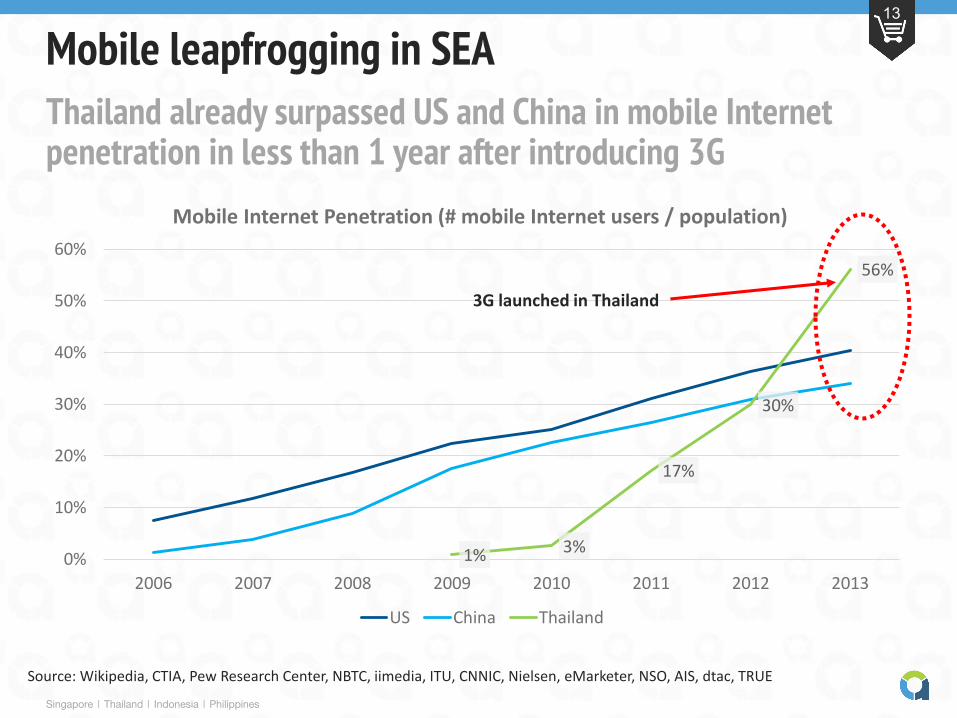

Mobile leapfrogging in SEA

1% 3%

17%

30%

56%

0%

10%

20%

30%

40%

50%

60%

2006 2007 2008 2009 2010 2011 2012 2013

Mobile Internet Penetration (# mobile Internet users / population)

US China Thailand

Thailand already surpassed US and China in mobile Internet penetration in less than 1 year after introducing 3G

3G launched in Thailand

Source: Wikipedia, CTIA, Pew Research Center, NBTC, iimedia, ITU, CNNIC, Nielsen, eMarketer, NSO, AIS, dtac, TRUE

Singapore | Thailand | Indonesia | Philippines

14

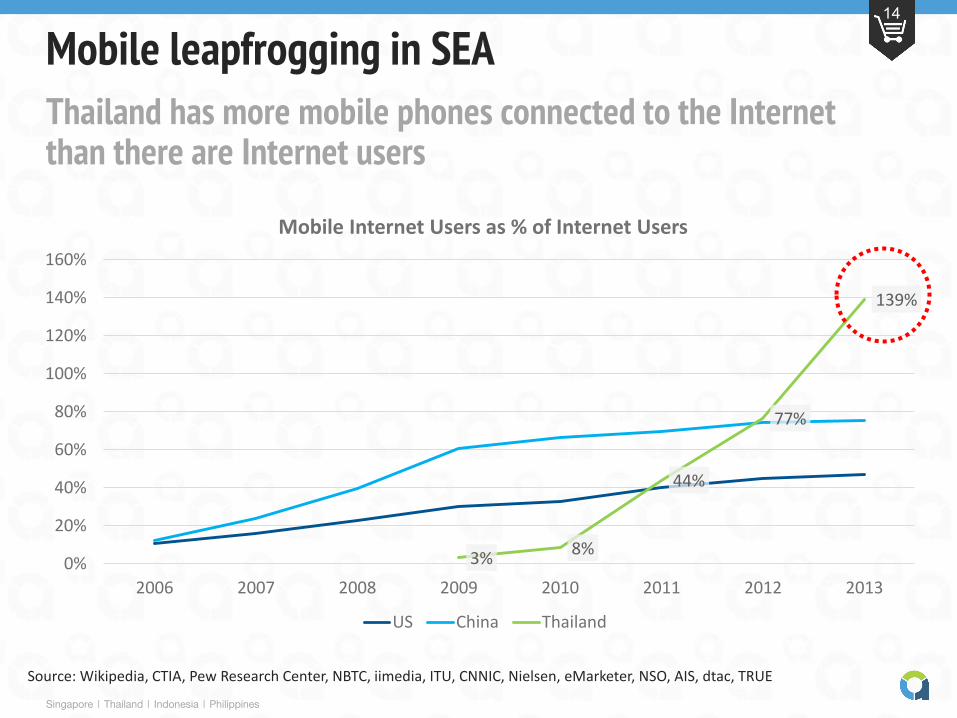

Mobile leapfrogging in SEA

Thailand has more mobile phones connected to the Internet than there are Internet users

3%8%

44%

77%

139%

0%

20%

40%

60%

80%

100%

120%

140%

160%

2006 2007 2008 2009 2010 2011 2012 2013

Mobile Internet Users as % of Internet Users

US China Thailand

Source: Wikipedia, CTIA, Pew Research Center, NBTC, iimedia, ITU, CNNIC, Nielsen, eMarketer, NSO, AIS, dtac, TRUE

Singapore | Thailand | Indonesia | Philippines

15

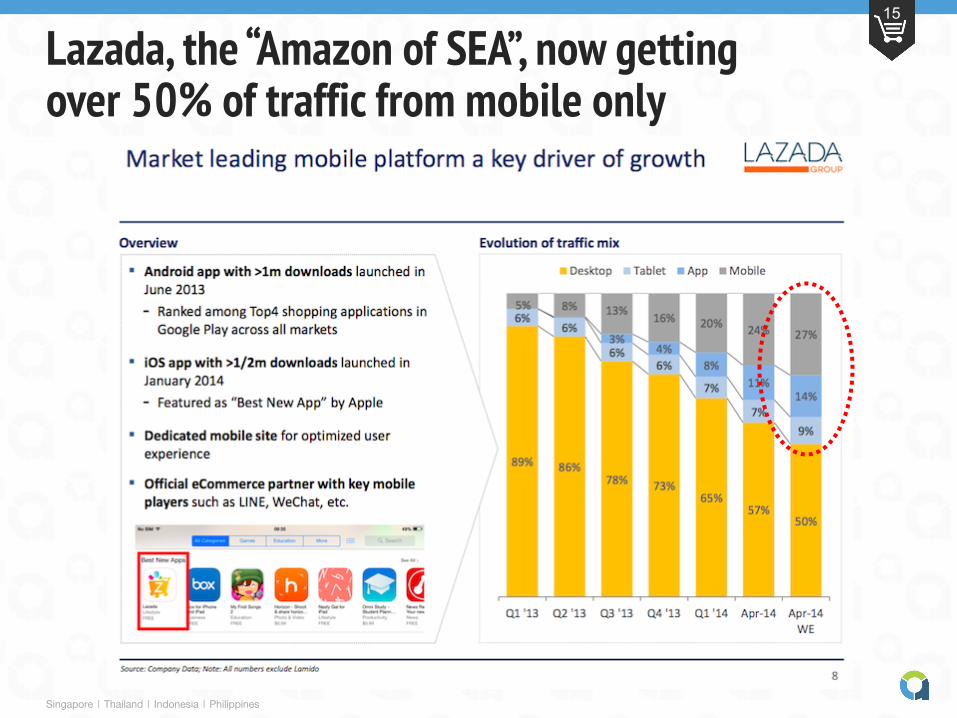

Lazada, the “Amazon of SEA”, now getting over 50% of traffic from mobile only

Singapore | Thailand | Indonesia | Philippines

16

Reading tea leaves: predicting the future in SEA by looking at China

Singapore | Thailand | Indonesia | Philippines

17

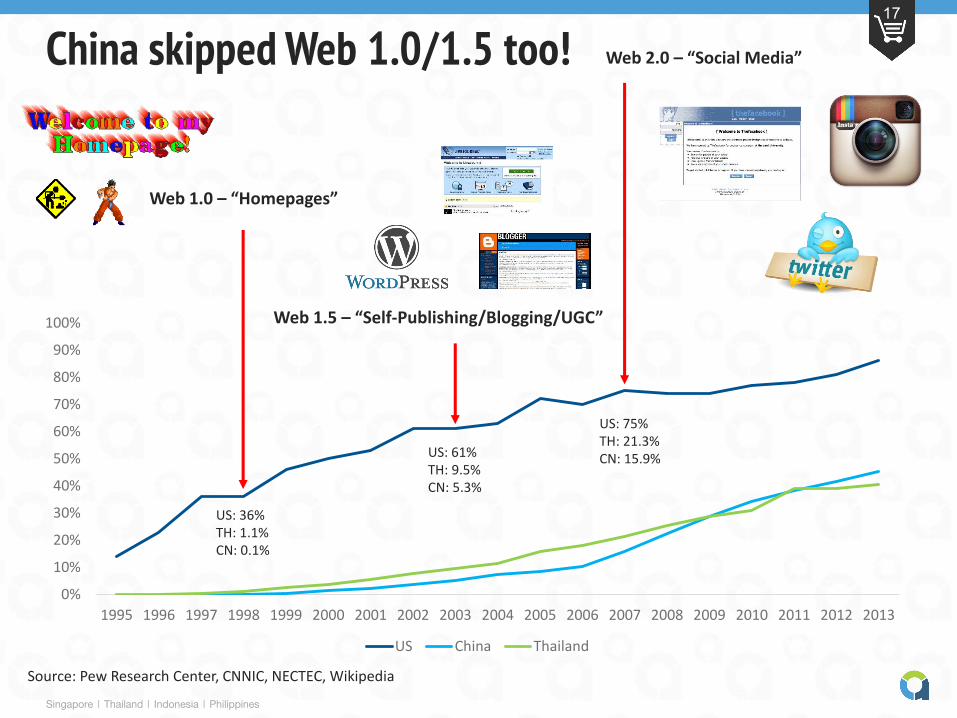

China skipped Web 1.0/1.5 too!

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

US China Thailand

Web 1.0 – “Homepages”

US: 36%TH: 1.1%CN: 0.1%

US: 61%TH: 9.5%CN: 5.3%

US: 75%TH: 21.3%CN: 15.9%

Web 1.5 – “Self-Publishing/Blogging/UGC”

Web 2.0 – “Social Media”

Source: Pew Research Center, CNNIC, NECTEC, Wikipedia

Singapore | Thailand | Indonesia | Philippines

18

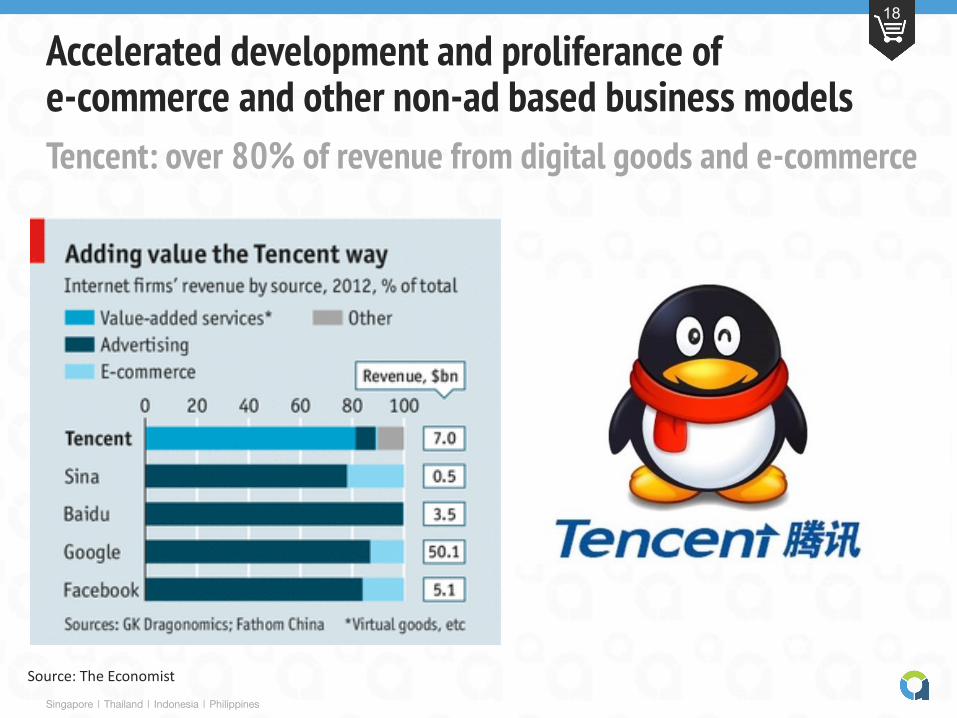

Accelerated development and proliferance ofe-commerce and other non-ad based business models

Tencent: over 80% of revenue from digital goods and e-commerce

Source: The Economist

Singapore | Thailand | Indonesia | Philippines

19

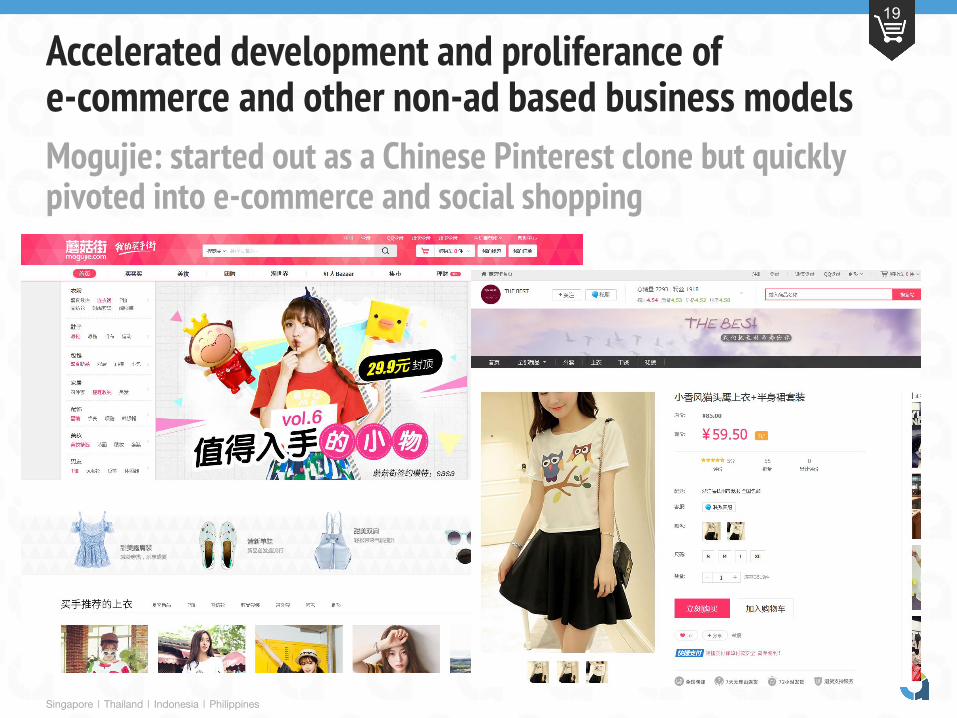

Accelerated development and proliferance ofe-commerce and other non-ad based business models

Mogujie: started out as a Chinese Pinterest clone but quickly pivoted into e-commerce and social shopping

Singapore | Thailand | Indonesia | Philippines

20

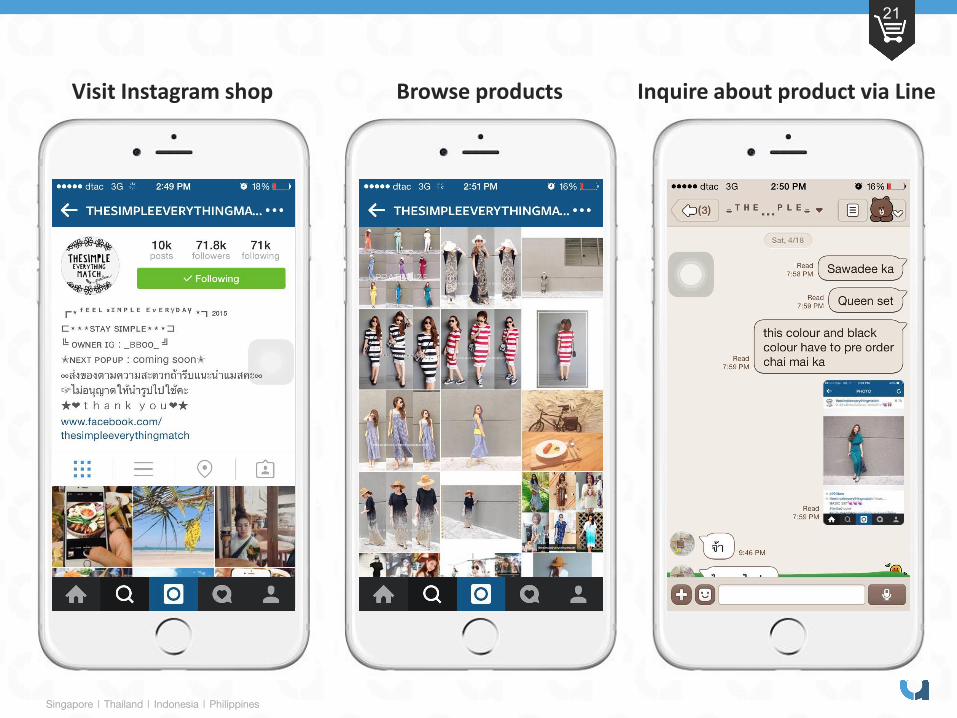

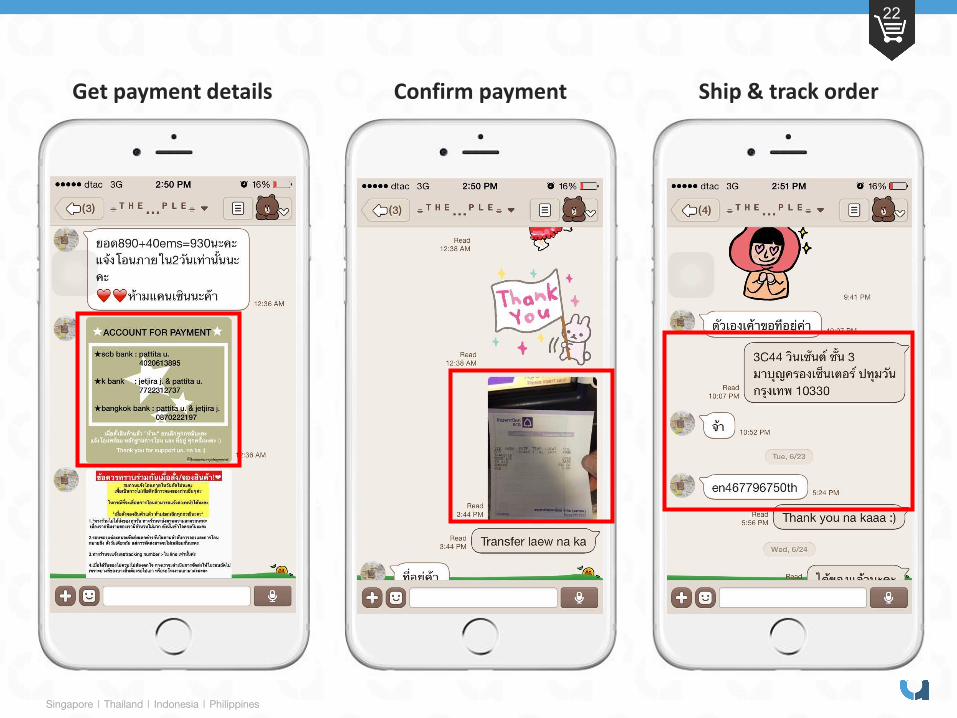

Thailand and Indonesia: social media users make money from e-commerce, not advertisingEst. 1/3 of total Thailand e-commerce GMV from transactions on “shadow marketplaces” –Instagram, Facebook, and Line

Source: AT Kearney, Tech in Asia, aCommerce internal data

Singapore | Thailand | Indonesia | Philippines

21

Visit Instagram shop Browse products Inquire about product via Line

Singapore | Thailand | Indonesia | Philippines

22

Get payment details Confirm payment Ship & track order

Singapore | Thailand | Indonesia | Philippines

23

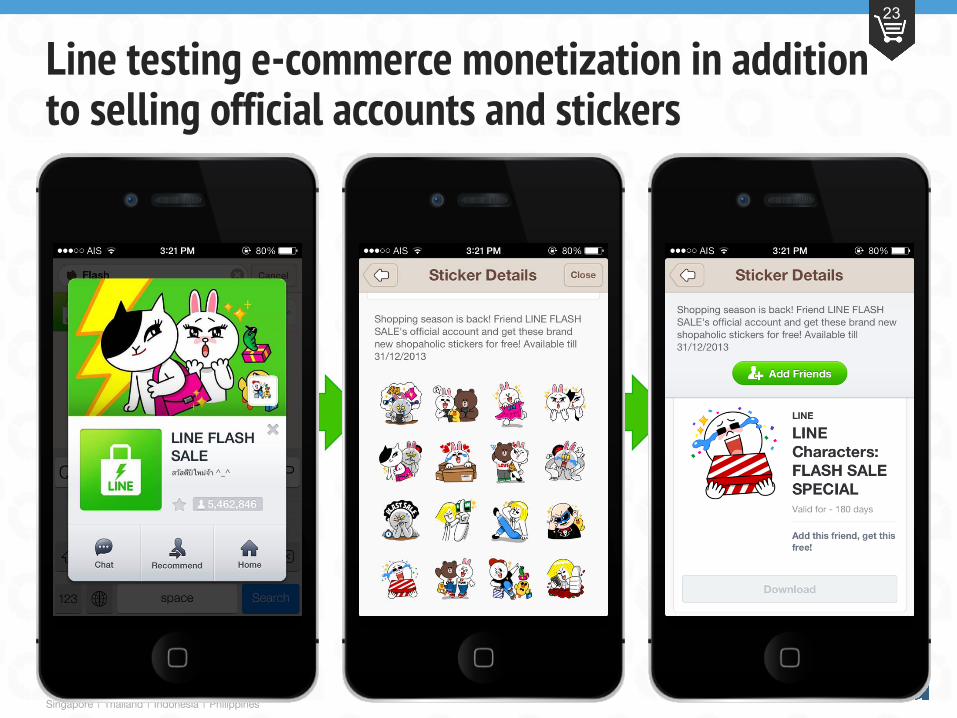

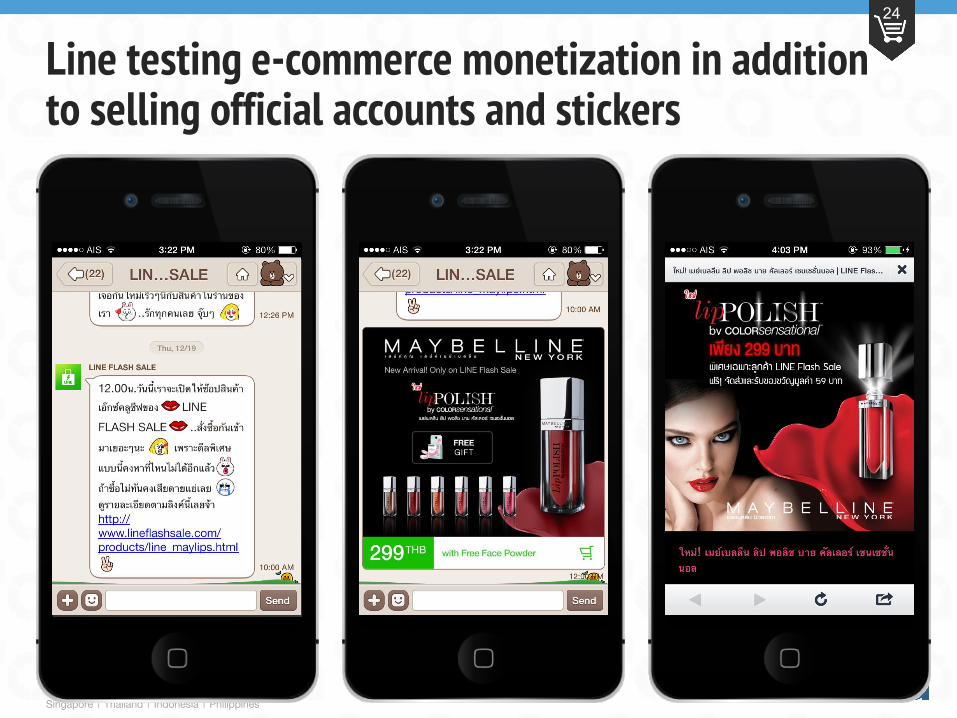

Line testing e-commerce monetization in addition to selling official accounts and stickers

Singapore | Thailand | Indonesia | Philippines

24

Line testing e-commerce monetization in addition to selling official accounts and stickers

Singapore | Thailand | Indonesia | Philippines

25

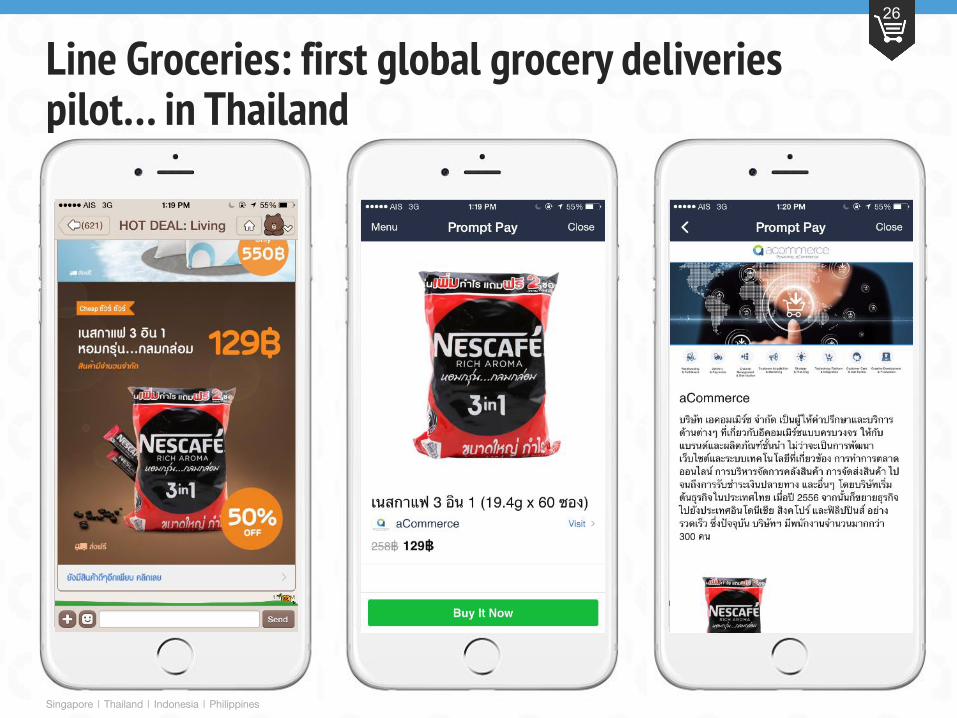

Line Groceries: first global grocery deliveries pilot… in Thailand

Singapore | Thailand | Indonesia | Philippines

26

Line Groceries: first global grocery deliveries pilot… in Thailand

Singapore | Thailand | Indonesia | Philippines

27

Key takeaways

1. “No-Tail” landscape

• Accelerated growth of e-commerce and alternative business models

2. Truly “Mobile-First”

• Mobile instead of desktop-based business models

• SEA desktop e-commerce 4-5 years behind China BUT mobile-ecommerce only 2-3 years behind

3. $$$ opportunities at convergence of Commerce x Mobile

Singapore | Thailand | Indonesia | Philippines

28

A peek into the future:Thai high school student’s homescreen

Thailand Office946 Dusit Thani Building, 4th fl., Rama IV Rd. Bangrak, Bangkok, Thailand 10500

Indonesia OfficeJalan Wijaya Timur II No. 13RT 015 RW 002, Kelurahan Petogogan, Kecamatan Mampang Prapatan Jakarta

Thailand Distribution Center951/1 Soi Preeyanon, Sathupradit Road, Bangpongpang, Yannawa Bangkok 10120, Thailand

Singapore Office#05-01, Block 71 Ayer Rajah CrescentSingapore 139951

Singapore | Thailand | Indonesia | Philippines

Thank You!29

Sheji HoGroup CMO, aCommerce

E: [email protected]: +66 (0)92-265-1700Skype: sheji_ho

Address:946 Dusit Thani Building, 4th fl., Rama IV Rd. Bangrak, Bangkok,10500 Thailand