acquiring merchandise for sale - pearson...

TRANSCRIPT

CHAPTER 6 ACQUISITIONS AND PAYMENT: INVENTORY AND LIABILITIES Acquiring Merchandise for Sale

Purchases (pp. 214-16)

Purchase Discounts

When a company takes advantage of a purchase discount, it reduces the cost of inventory. Under a perpetual inventory system (discussed below) the credit for purchase discounts is made to the Inventory account. Under a periodic inventory system (also discussed below) the credit is made to a Purchase discounts account. To illustrate, assume that you purchase $10,000 worth of inventory on January 5, 2001 with credit terms 2/10, n/30. The purchase is paid for on January 12th. Journal entries would be as follows:

Date Transaction Debit Credit 1/5/2001 Inventory or Purchases $10,000

Accounts payable $10,000

To record the purchase of inventory, terms 2/10, n/30

1/12/2001 Accounts payable $10,000 Inventory or Purchase discounts $ 200 Cash 9,800

To record the payment of the 1/5/2001 $10,000 purchase less the discount of $200 ($10,000 x 2%)

Purchase returns and Purchase allowances

Purchase returns and purchase allowances are accounted for much like discounts – the account used depends upon whether you are using a perpetual or periodic inventory system. With a perpetual system Inventory is credited. Under a periodic system, the credit would be to Purchase returns and allowances. To illustrate, assume you return $150 of defective merchandise that you have not paid for yet. The journal entry would be as follows:

Date Transaction Debit Credit Accounts payable $150

Inventory or Purchase returns and allowances $150

To record the return of $150 of defective merchandise

18

Freight-In

When goods are shipped (FOB) shipping point, the freight cost increases the total inventory cost. Once again, under a perpetual system a company will increase Inventory while under a periodic system a separate Freight-in account will be maintained. To illustrate, assume you receive a bill for $85 to cover the shipping cost of merchandise purchased FOB shipping point. The journal entry would be as follows:

Date Transaction Debit Credit

Inventory or Freight-in $85 Accounts payable or Cash $85

To record the shipping cost of inventory.

Example of Cost Flow Assumptions and Timing of Record Keeping

Perpetual Inventory (pp. 218-9) When a company uses a perpetual inventory system, all inventory purchases are debited to the Inventory account. When a sale is made, two journal entries are required, one to record the sale and the other to reduce the inventory and record the cost of goods sold. For example, the January 8th sale and January 16th purchase for Phil’s Photo Shop using a perpetual inventory system would be as follows:

Date Transaction Debit Credit 1/8/2001 Sales $60

Cash or Accounts receivable $60

Cost of goods sold $30 Inventory $30

To record the sale of three cameras – sales price $20 each, cost $10 each

1/16/2001 Inventory $60 Cash or Accounts payable $60

To record the purchase of 5 cameras at $12 each

Periodic Inventory (pp. 219-20) When a company uses a periodic inventory system, all inventory purchases are debited to the Purchases account. It is a temporary account that is used to accumulate the cost of inventory purchased during the period. When a sale is made, only one journal entries is required to record the sale. Cost of goods sold is calculated at the end of the period. The January 8th sale and January 16th purchase for Phil’s Photo Shop using a periodic inventory system would be as follows:

19

Date Transaction Debit Credit 1/8/2001 Sales $60

Cash or Accounts receivable $60

To record the sale of three cameras at $20 each

1/16/2001 Purchases $60 Cash or Accounts payable $60

To record the purchase of five cameras at $12 each

Conclusions About Inventory Cost Flow Assumptions (p. 222)

Jones Saddle Company had the following transactions during August 2002

purchased 30 units @ $20 per unit on August 10, 2002 purchased 20 units @ $21 per unit on August 15, 2002 purchased 20 units @ $23 per unit on August 15, 2002 sold 35 units @ $30 per unit on August 30, 2002

Prepare journal entries to record the purchases assuming that Jones Saddle Company uses a perpetual inventory system. Prepare the journal entries to record the sale using (1) FIFO, (2) LIFO, and (3) Weighted Average.

STUDY BREAK 6-2 (p. 222) SEE HOW YOU’RE DOING

Inventory and Cost of Goods Sold in Merchandising Operations

Adjustments and Closing under a Perpetual Inventory System When a company maintains a perpetual inventory system, the current inventory balance and cost of goods sold are maintained at all times. A physical inventory count at the end of the year is needed to verify the inventory balance and identify shrinkage. The following is what typical inventory and cost of goods sold accounts would look like before the adjustment and closing process when using a perpetual system.:

Inventory Cost of goods sold BB $7,500 $372 Purchase discounts BB $0

Purchases 26,580 265 Purchase returns and allowances 12/1-12/31 27,435

Freight-in 2,395 27,435 Cost of goods sold 12/31 Unadjusted balance $8,403

20

A physical count of inventory calculates an ending inventory value of $8,255, indicating shrinkage of $148.

The Inventory and Cost of goods sold accounts must be adjusted for the shrinkage and the Cost of goods sold account must be closed to Income summary, just like all other expense accounts:

Date Transaction Debit Credit 12/31 Cost of goods sold $148

Inventory $148

To record inventory shrinkage

12/31 Income summary $27,583 Cost of goods sold $27,583

To close costs of goods sold ($27,435 sales + $148 shrinkage)

After these two entries are posted, the Inventory account will contain the correct ending balance of $8,255 ($8,403 - $148) and the Cost of goods sold account will be reset to $0.

Adjustments and Closing under a Periodic Inventory System

Under a periodic system, the same company would have the following T-accounts and balances before adjustments and closing: Inventory Purchases Freight-in BB $7,500 BB $0 BB $0

12/1-12/31

26,580

12/1-12/31 2,395

Purchase discounts Purchase returns and allowances

$0 BB $0 BB

372 12/1-12/31 265

12/1-12/31

Remember that under a periodic system, no Cost of goods sold account is maintained.

21

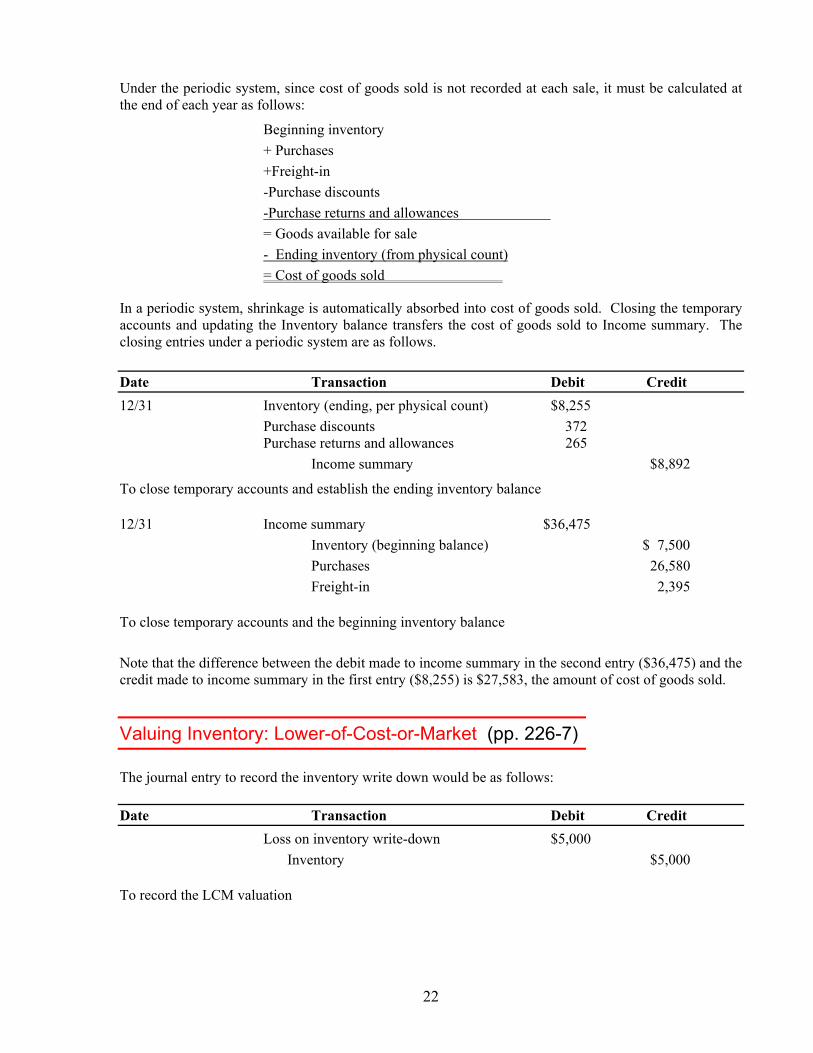

Under the periodic system, since cost of goods sold is not recorded at each sale, it must be calculated at the end of each year as follows:

Beginning inventory + Purchases

+Freight-in -Purchase discounts -Purchase returns and allowances = Goods available for sale - Ending inventory (from physical count) = Cost of goods sold

In a periodic system, shrinkage is automatically absorbed into cost of goods sold. Closing the temporary accounts and updating the Inventory balance transfers the cost of goods sold to Income summary. The closing entries under a periodic system are as follows. Date Transaction Debit Credit 12/31 Inventory (ending, per physical count) $8,255 Purchase discounts 372 Purchase returns and allowances 265 Income summary $8,892

To close temporary accounts and establish the ending inventory balance

12/31 Income summary $36,475 Inventory (beginning balance) $ 7,500 Purchases 26,580 Freight-in 2,395

To close temporary accounts and the beginning inventory balance

Note that the difference between the debit made to income summary in the second entry ($36,475) and the credit made to income summary in the first entry ($8,255) is $27,583, the amount of cost of goods sold.

Valuing Inventory: Lower-of-Cost-or-Market (pp. 226-7)

The journal entry to record the inventory write down would be as follows:

Date Transaction Debit Credit Loss on inventory write-down $5,000

Inventory $5,000

To record the LCM valuation

22

Paying for Acquisitions: Liabilities

Acquisition of Human Resources and Payroll Liabilities (pp. 230-32) Following the Risky Company example in the textbook: $500 gross salary, 20% ($100) withheld for income taxes, Social Security taxes at 6.2% ($31.00), and Medicare taxes at 1.45% ($7.25), the journal entry to record payroll would be as follows:

Date Transaction Debit Credit Salary expense $500.00

Income taxes payable $100.00 Social security taxes payable 31.00 Medicare taxes payable 7.25 Cash 361.75

To record salary expense and payroll deductions

When Risky Company pays the government the taxes withheld, they must match the Social Security and Medicare amounts. The journal entry to record the payment of the taxes is as follows:

Date Transaction Debit Credit Payroll tax expense $ 38.25

Income taxes payable 100.00 Social security taxes payable 31.00 Medicare taxes payable 7.25 Cash $176.50

To record payroll tax expense and payment of taxes

STUDY BREAK 6-6 (p. 232) Sandy earned $1,500 at her job at Paula’s Bookstore during February. Sandy has 20% of her gross pay withheld for income taxes, 6.2% withheld for Social Security (FICA) taxes, and 1.45% withheld for Medicare taxes. Prepare the required payroll journal entries assuming that Paula's bookstore will not submit the taxes to the government until next month.

SEE HOW YOU’RE DOING

23

Summary Problem: Tom's Wear Faces New Challenges in May Transaction 1 Pays $300 cash for an insurance premium. Coverage starts May 15th.

Date Transaction Debit Credit 5/1/2001 Prepaid insurance $300

Cash $300 To record the purchase of insurance Transaction 2 Collects $7,900 on accounts receivable.

Date Transaction Debit Credit 5/10/2001 Cash $7,900

Accounts receivable $7,900 To record the collection of accounts receivable Transaction 3 Pays accounts payable of $4,000.

Date Transaction Debit Credit 5/12/2001 Accounts payable $4,000

Cash $4,000 To record payment on account Transaction 4 Purchased 1,100 T-shirts at $4.00 each on account.

Date Transaction Debit Credit 5/14/2001 Inventory $4,400

Accounts payable $4,400 To record the purchase of 1,100 T-shirts at $4 on account

Transaction 5

Agrees to sell school system 900 shirts @$11 each. Collects cash of $9,900 in advance. Half the shirts will be delivered by May 30 and the other half in June.

Date Transaction Debit Credit 5/15/2001 Cash $9,900

Unearned revenue $9,900 To record the collection of sales revenue in advance Transaction 6 Sells 800 shirts for $11 each on account.

24

Date Transaction Debit Credit 4/15/2001 Accounts receivable $8,800

Sales $8,800 To record the sale of 800 T-shirts on account

4/15/2001 Cost of goods sold $3,200 Inventory $3,200

To record the expense cost of goods sold and reduce the inventory by 800 x $4. Transaction 7

Hires Web designers to start a Web page - $200 for design and $50 per month maintenance, 6 months paid in advance. A full month's fee is being charged in May.

Date Transaction Debit Credit 5/21/2001 Prepaid Web services $300

Misc. operating expenses 200 Cash $500

To record payment for Web page setup and maintenance Transaction 8 Purchase 1,000 shirts at $4.20 each on account.

Date Transaction Debit Credit 5/30/2001 Inventory $4,200

Accounts payable $4,200 To record the purchase of 1,000 shirts on account Transaction 9 Repays the 3-month note issued on March 1st, with interest

Date Transaction Debit Credit 5/31/2001 Short-term notes payable $3,000

InteInte

rest payable $60 rest expense $30 Cash $3,090

To record the repayment of the March 1 note, with interest Adjustment 1 Record insurance expense for May - $25 for the first half of the month (beginning prepaid insurance) and $50 for the second half of the month ($100 month beginning May 15).

Date Transaction Debit Credit 5/31/2001 Insurance expense $75

Prepaid insurance $75 To record insurance expense for May

25

Adjustment 2 Record rent expense of $1,200 for the month of May.

Date Transaction Debit Credit 5/31/2001 Rent expense $1,200

Prepaid rent $1,200 To record rent expense for May Adjustment 3 Record Web services expense for May.

Date Transaction Debit Credit 5/31/2001 Misc. operating expenses $50

Prepaid Web service $50 To record Web maintenance services for May Adjustment 4 Record depreciation expense for the van - 6,000 miles x $0.145.

Date Transaction Debit Credit 5/31/2001 Depreciation expense $870

Accum. dep. - Van $870 To record May depreciation expense on the van Adjustment 5 Record the $100 monthly depreciation expense on the computer.

Date Transaction Debit Credit 5/31/2001 Depreciation expense $100

Accum. dep. - Computer $100 To record May depreciation expense on the computer

Adjustment 6

Half of the shirts were delivered to the school. Reclassify half of the unearned revenue as earned and record the cost of goods sold.

Date Transaction Debit Credit 5/31/2001 Unearned revenue $4,950

Sales $4,950 To record delivery of half of the shirts to the school

5/31/2001 Cost of goods sold $1,800 Inventory $1,800

To record the expense cost of goods sold and reduce the inventory by 450 x $4 Adjustment 7 Accrue Sam Cubbie's $1,000 salary for May, including the employer portion of payroll taxes (Social security 6.2%; Medicare 1.45%) and Withholding tax 20%.

26

Date Transaction Debit Credit 5/31/2001 Salary expense $1,000

Employer's payroll tax expense 77 Payroll taxes withheld $277 Other payables 77 Salaries payable 723

To record the accrual of Sam Cubbie's salary, withholding, and payroll taxes Adjustment 8 Accrue interest expense on the van note.

Date Transaction Debit Credit 5/31/2001 Interest expense $250

Interest payable $250 To record the interest expense on the van for May

27

28

723 0 30,000 5,000 4,985

BB $3,295 $300 1 BB $8,000 $7,900 2 BB $1,100 $3,200 6b BB $25 $75 Adj-1 5 $1,800 $1,200 Adj-22 7,900 4,000 3 6a 8,800 0 4 4,400 1,800 Adj-6 1 300 5 9,900 4,400 4 8 4,200 600

500 7 250

3,090 9 8,900 4,700

$8,805

7 $300 $50 Adj-3 BB $4,000 $200 BB BB $30,000 $725 BB 100 Adj-5 870 Adj-4

250 4,000 30,000300 1,595

3 $4,000 $4,000 BB $310 BB Adj-6 $4,950 $9,900 5 $277 Adj-7 $77 Adj-74,200 8 9 60 250 Adj-8

4,950 277 774,200 500

Retained earnings$723 Adj-7 9 $3,000 $3,000 BB $30,000 BB $5,000 BB $4,985 BB

Prepaid Web service

Unearned revenueInterest payable

Common stock

Payroll taxes withheld

T-accounts for Tom's Wear with May journal entries and adjustments

Prepaid rent

Equipment - Computer Equipment - Van Acc dep - Van

Accounts receivableCash Inventory Prepaid insurance

Acc dep - Computer

Other payables

Salaries payableShort-term notes

payableLong-term notes

payable

Accounts payable

29

$8,800 6a 6b $3,200 Adj-4 $870 7 $200 Adj-7 $774,950 Adj-6 Adj-6 1,800 Adj-5 100 Adj-3 50

7713,750 5,000 970 250

Adj-1 $75 Adj-2 $1,200 9 $30 Adj-7 $1,000Adj-8 250

75 1,200 1,000280

Rent expense Salary expenseInsurance expense Interest expense

Misc. operating expenses

Employer's payroll tax expenseRevenue

Cost of goods sold Depreciation expense

Tom's Wear , Inc. Adjusted Trial Balance

May 31, 2001

Debits Credits Cash $8,805 Accounts receivable 8,900 Inventory 4,700 Prepaid insurance 250 Prepaid rent 600 Prepaid Web service 250 Equipment - Computer 4,000 Accumulated depreciation - Computer $300 Equipment - Van 30,000 Accumulated depreciation - Van 1,595 Accounts payable 4,200 Interest payable 500 Unearned revenue 4,950 Payroll taxes withheld 277 Other payables 77 Salaries payable 723 Long-term notes payable 30,000 Common stock 5,000 Retained earnings 4,985 Sales 13,750 Cost of goods sold 5,000 Depreciation expense 970 Other operating expense 250 Employer's payroll tax expense 77 Insurance expense 75 Rent expense 1,200 Interest expense 280 Salary expense 1,000 Totals $66,357 $66,357

30

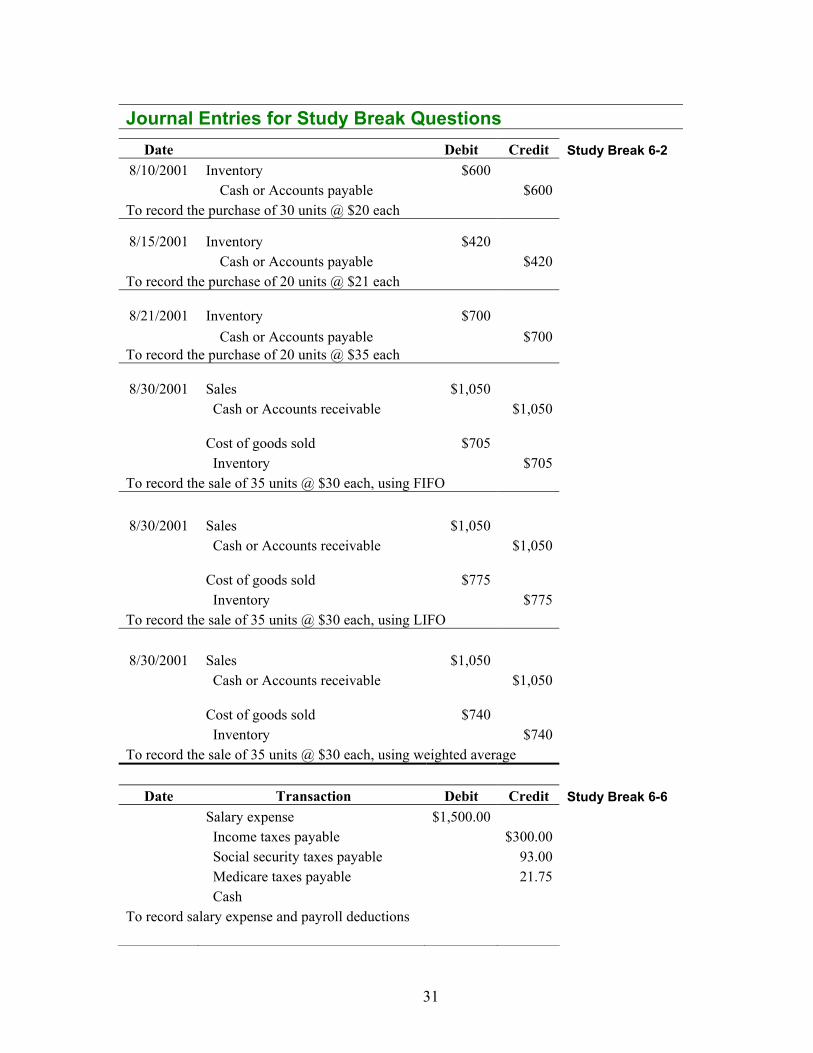

Journal Entries for Study Break Questions

Date Debit Credit Study Break 6-2 8/10/2001 Inventory $600

Cash or Accounts payable $600 To record the purchase of 30 units @ $20 each

8/15/2001 Inventory $420

Cash or Accounts payable $420 To record the purchase of 20 units @ $21 each

8/21/2001 Inventory $700

Cash or Accounts payable $700 To record the purchase of 20 units @ $35 each

8/30/2001 Sales $1,050

Ca

In

sh or Accounts receivable $1,050 Cost of goods sold $705 ventory $705

To record the sale of 35 units @ $30 each, using FIFO

8/30/2001 Sales $1,050 Ca

In

sh or Accounts receivable $1,050 Cost of goods sold $775 ventory $775

To record the sale of 35 units @ $30 each, using LIFO

8/30/2001 Sales $1,050 Ca

In

sh or Accounts receivable $1,050 Cost of goods sold $740 ventory $740

To record the sale of 35 units @ $30 each, using weighted average

Date Transaction Debit Credit Study Break 6-6 Salary expense $1,500.00

InSoMCa

come taxes payable $300.00 cial security taxes payable 93.00 edicare taxes payable 21.75 sh To record salary expense and payroll deductions

31

Date Transaction Debit Credit Payroll tax expense $114.75

Social security taxes pa Me 21.75

o record employer payroll tax expense.

yable 93.00 dicare taxes payable

T

Short Exercises

SE6-11 The Woods Company purchased 500 electric saws from the Jordan's Equipment Company. Each

Date Account Debit Credit

electric saw cost $300. The saws are to be sold for $650 each. Woods paid $1,550 for freight and $280 for insurance while the saws were in transit. Woods Company also hired two more salespeople for a costof $4,000 per month. Give the journal entry for the purchase of inventory. Assume the company uses perpetual record keeping for inventory.

SE6-21 Tone Company acquired 4,000 transformers from the Ochoa Company. Each transformer cost

e

Date Account Debit Credit

$100. Tone will sell them for $125 each. Tone paid $950 for freight and $200 for insurance while the transformers were in transit. Tone Company paid $900 to advertise the transformers in a local real estatmagazine. Give the journal entry for the purchase of inventory. Assume the company uses perpetual record keeping for inventory.

SE6-7 The Hawking Company's records reported the following at the end of the fiscal year:

Beginning inventory $ 40,000

A physical count showed that the ending inventory was actually $26,000. What is the journal entry needed to correct the accounting records?

Ending inventory 28,500 Cost of goods sold 280,000

32

Date Account Debit Credit

Exercises

E6-1 The Ribbomonth of May.

n Company began operations on May 1. The following transactions took place in the

s of merchandise on account during May were $400,000.

pany was $25,000, paid in cash by Ribbon during May.

Ribbon returned $22,000 of merchandise purchased in part a. to the supplier for a full refund.

e. alary was $3,000 for the month.

Asstransaction described above.

a. Cash purchases of merchandise during May were $300,000.

b. Purchase

c. The cost of freight to deliver the merchandise to Ribbon Com

d. The store manager's s

ume Ribbon Company uses periodic record keeping for inventory. Give the journal entry for each

Transaction Account Debit Credit

a. b.

c.

d. e.

33

E6-3 For each of the following situations, give the journal entry th the purchasing company would record for the inventory purchase (including the cost of the freight, where applicable). Assume any freight harges are paid in cash at the time of receipt. Then, record the payment to the vendor for each purchase.

Assume the company uses periodic record keeping. Assume discounts are recorded only when the

b. Invoice price of goods is $3,000. Purchase terms are 4/10, n/30 and the invoice is paid in the

c. eipt. The shipping terms are FOB shipping point, and the shipping costs amount to $250.

at

c

payment is actually made and the purchase discount is taken.

a. Invoice price of goods is $5,000. Purchase terms are 2/10, n/30 and the invoice is paid in the week of receipt. The shipping terms are FOB shipping point, and the shipping costs amount to $200.

week of receipt. The shipping terms are FOB destination, and the shipping costs amount to $250. Invoice price of goods is $2,500. Purchase terms are 2/10, n/30 and the invoice is paid 15 days after rec

d. Invoice price of goods is $9,000. Purchase terms are 3/10, n/30 and the invoice is paid in the week of receipt. The shipping terms are FOB destination, and the shipping costs amount to $200.

Transaction Account Debit Credit

a. purchase

payment

b. purchase

payment

c. purchase

payment

34

d. purchase

payment

F ac oll of $

E6-16 or a specific counting period, a company has gross payr 20,000, federal income tax withheld of $4,000, and FICA (social security) taxes withheld of $1,600. Give the journal entry(s) to record the salary expense for the period. Include any related employer expenses.

Date Account Debit Credit

Problems – Set A

P6–1A The Battier Company made the following purchases in March of the current year:

March 2 Purchased $5,000 of merchandise, terms 1/10, n/30, FOB shipping point. March 5 Purchased $2,000 of merchandise, terms 2/15, n/45, FOB shipping point. March 10 Purchased $4,000 of merchandise, terms 3/5, n/15, FOB destination.

Required:

Record the jour d in cash. Assume B hase discounts only uses

cord keeping for inventory.

nal entries for each purchase. In each case, the freight charges are $350 and are paiattier Company records purchases at the full invoice amount, and records purc

when the payment to the vendor is made and the discount is taken. The companyperpetual re

35

Date Account Debit Credit

The For Fish Com an w

P6–5A pany sells commercial fish tanks. The comp y began 2002 ith 10,000 units of inventory on hand. These units cost $150 each. The following transactions related to the company's merchandise inventory occurred during the first quarter of 2002:

January 20 Purchase 5,000 units for $160 each

February 18 Purchase 6,000 units for $170 each

March 28 Purchase 4,000 units for $180 each

Total Purchases 15,000 units

The c n nve tory co quarter ending17,000 units, leaving 8,000 units in ending inventory. The com

journal entry required at March 31 to record the cost of goods sold for the quarter using:

ed average

include all related i n sts. During the osts showunits totaled

March 31, 2002, sales in pany uses a periodic record-

keeping system.

Required: Give the

a. FIFO b. LIFO c. Weight

36

Date Account Debit Credit

a.

b.

c.

P6–8A Cheny Company buys and then resells a single product. The product is a commodity and is subject to rather severe cost fluctuations. Following is information concerning Cheny's inventory activity during the month of June 2003:

June 1 430 units on hand, $3,010 June 4 Sold 200 units June 6 Purchased 500 units @ $11 per unit June 10 Purchased 200 units @ $9 per unit June 15 Sold 300 units June 20 Purchased 150 units @ $6 per unit June 25 Sold 400 units June 29 Purchased 50 units @ $8 per unit

Cheny uses a perpetual, FIFO inventory system.

Required: Assume Cheny sold each unit for $20 per unit. Give the journal entries to record the sales and reduction in inventory if appropriate:

Date Account Debit Credit

June 4 June 15

37

38

June 25