acquisitions and projects - new york university stern...

TRANSCRIPT

265

AcquisitionsandProjects

AswathDamodaran

265

¨ Anacquisitionisaninvestment/projectlikeanyotherandalloftherulesthatapplytotraditionalinvestmentsshouldapplytoacquisitionsaswell.Inotherwords,foranacquisitiontomakesense:¤ ItshouldhavepositiveNPV.Thepresentvalueoftheexpectedcash

flowsfromtheacquisitionshouldexceedthepricepaidontheacquisition.

¤ TheIRRofthecashflowstothefirm(equity)fromtheacquisition>Costofcapital(equity)ontheacquisition

¨ Inestimatingthecashflowsontheacquisition,weshouldcountinanypossiblecashflowsfromsynergy.

¨ Thediscountratetoassessthepresentvalueshouldbebasedupontheriskoftheinvestment(targetcompany)andnottheentityconsideringtheinvestment(acquiringcompany).

266

TataMotorsandHarmanInternational

AswathDamodaran

266

¨ HarmanInternationalisapubliclytradedUSfirmthatmanufactureshighendaudioequipment.TataMotorsisanautomobilecompany,basedinIndia.

¨ TataMotorsisconsideringanacquisitionofHarman,withaneyeonusingitsaudioequipmentinitsIndianautomobiles,asoptionalupgradesonnewcars.

267

EstimatingtheCostofCapitalfortheAcquisition(nosynergy)

AswathDamodaran

267

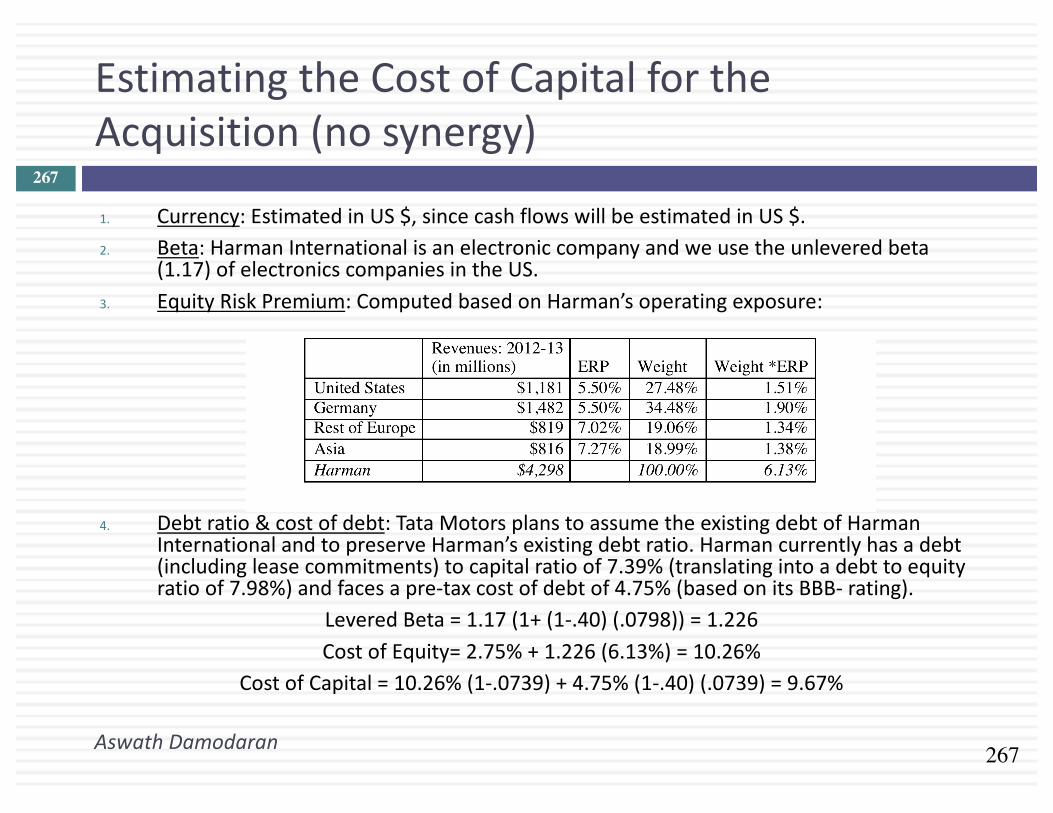

1. Currency:EstimatedinUS$,sincecashflowswillbeestimatedinUS$.2. Beta:HarmanInternationalisanelectroniccompanyandweusetheunleveredbeta

(1.17)ofelectronicscompaniesintheUS.3. EquityRiskPremium:ComputedbasedonHarman’soperatingexposure:

4. Debtratio&costofdebt:TataMotorsplanstoassumetheexistingdebtofHarmanInternationalandtopreserveHarman’sexistingdebtratio.Harmancurrentlyhasadebt(includingleasecommitments)tocapitalratioof7.39%(translatingintoadebttoequityratioof7.98%)andfacesapre-taxcostofdebtof4.75%(basedonitsBBB- rating).

LeveredBeta=1.17(1+(1-.40)(.0798))=1.226CostofEquity=2.75%+1.226(6.13%)=10.26%

CostofCapital=10.26%(1-.0739)+4.75%(1-.40)(.0739)=9.67%

268

EstimatingCashflows- FirstSteps

AswathDamodaran

268

¨ OperatingIncome:Thefirmreportedoperatingincomeof$201.25milliononrevenuesof$4.30billionfortheyear.Addingbacknon-recurringexpenses(restructuringchargeof$83.2millionin2013)andadjustingincomefortheconversionofoperatingleasecommitmentstodebt,weestimatedanadjustedoperatingincomeof$313.2million.Thefirmpaid18.21%ofitsincomeastaxesin2013andwewillusethisastheeffectivetaxrateforthecashflows.

¨ Reinvestment:Depreciationin2013amountedto$128.2million,whereascapitalexpendituresandacquisitionsfortheyearwere$206.4million.Non-cashworkingcapitalincreasedby$272.6millionduring2013butwas13.54%ofrevenuesin2013.

269

Bringingingrowth

¨ WewillassumethatHarmanInternationalisamaturefirm,growing2.75%inperpetuity.

¨ Weassumethatrevenues,operatingincome,capitalexpendituresanddepreciationwillallgrow2.75%fortheyearandthatthenon-cashworkingcapitalremain13.54%ofrevenuesinfutureperiods.

AswathDamodaran

269

270

ValueofHarmanInternational:BeforeSynergy

AswathDamodaran

270

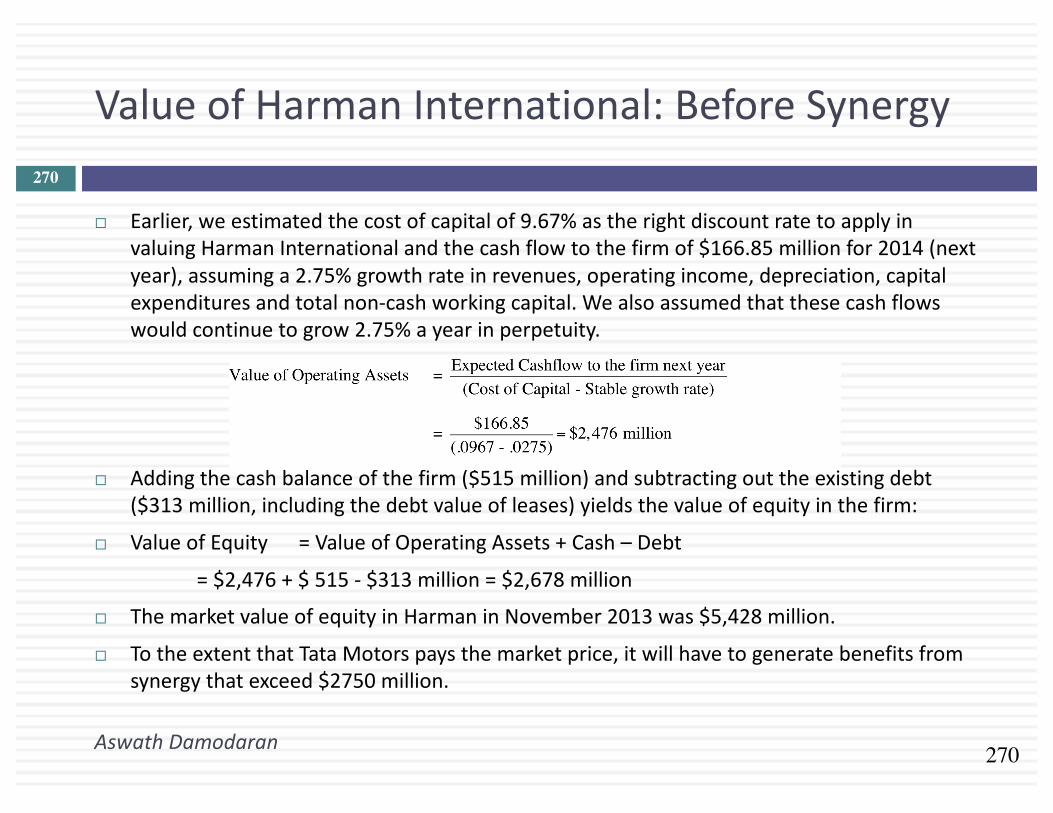

¨ Earlier,weestimatedthecostofcapitalof9.67%astherightdiscountratetoapplyinvaluingHarmanInternationalandthecashflowtothefirmof$166.85millionfor2014(nextyear),assuminga2.75%growthrateinrevenues,operatingincome,depreciation,capitalexpendituresandtotalnon-cashworkingcapital.Wealsoassumedthatthesecashflowswouldcontinuetogrow2.75%ayearinperpetuity.

¨ Addingthecashbalanceofthefirm($515million)andsubtractingouttheexistingdebt($313million,includingthedebtvalueofleases)yieldsthevalueofequityinthefirm:

¨ ValueofEquity =ValueofOperatingAssets+Cash– Debt

=$2,476+$515- $313million=$2,678million

¨ ThemarketvalueofequityinHarmaninNovember2013was$5,428million.

¨ TotheextentthatTataMotorspaysthemarketprice,itwillhavetogeneratebenefitsfromsynergythatexceed$2750million.

MeasuringInvestmentReturnsII.InvestmentInteractions,OptionsandRemorse…

Lifeistooshortforregrets,right?

AswathDamodaran 271

272

Independentinvestmentsaretheexception…

AswathDamodaran

272

¨ Inalloftheexampleswehaveusedsofar,theinvestmentsthatwehaveanalyzedhavestoodalone.Thus,ourjobwasasimpleone.Assesstheexpectedcashflowsontheinvestmentanddiscountthemattherightdiscountrate.

¨ Intherealworld,mostinvestmentsarenotindependent.Takinganinvestmentcanoftenmeanrejectinganotherinvestmentatoneextreme(mutuallyexclusive)tobeinglockedintotakeaninvestmentinthefuture(pre-requisite).

¨ Moregenerally,acceptinganinvestmentcancreatesidecostsforafirm’sexistinginvestmentsinsomecasesandbenefitsforothers.

273

I.MutuallyExclusiveInvestments

AswathDamodaran

273

¨ Wehavelookedathowbesttoassessastand-aloneinvestmentandconcludedthatagoodinvestmentwillhavepositiveNPVandgenerateaccountingreturns(ROCandROE)andIRRthatexceedyourcosts(capitalandequity).

¨ Insomecases,though,firmsmayhavetochoosebetweeninvestmentsbecause¤ Theyaremutuallyexclusive:Takingoneinvestmentmakestheother

oneredundantbecausetheybothservethesamepurpose¤ Thefirmhaslimitedcapitalandcannottakeeverygoodinvestment

(i.e.,investmentswithpositiveNPVorhighIRR).¨ Usingthetwostandarddiscountedcashflowmeasures,NPV

andIRR,canyielddifferentchoiceswhenchoosingbetweeninvestments.

274

ComparingProjectswiththesame(orsimilar)lives..

AswathDamodaran

274

¨ Whencomparingandchoosingbetweeninvestmentswiththesamelives,wecan¤ Computetheaccountingreturns(ROC,ROE)oftheinvestmentsandpicktheonewiththehigherreturns

¤ ComputetheNPVoftheinvestmentsandpicktheonewiththehigherNPV

¤ ComputetheIRRoftheinvestmentsandpicktheonewiththehigherIRR

¨ Whileitiseasytoseewhyaccountingreturnmeasurescangivedifferentrankings(andchoices)thanthediscountedcashflowapproaches,youwouldexpectNPVandIRRtoyieldconsistentresultssincetheyarebothtime-weighted,incrementalcashflowreturnmeasures.

275

Case1:IRRversusNPV

AswathDamodaran

275

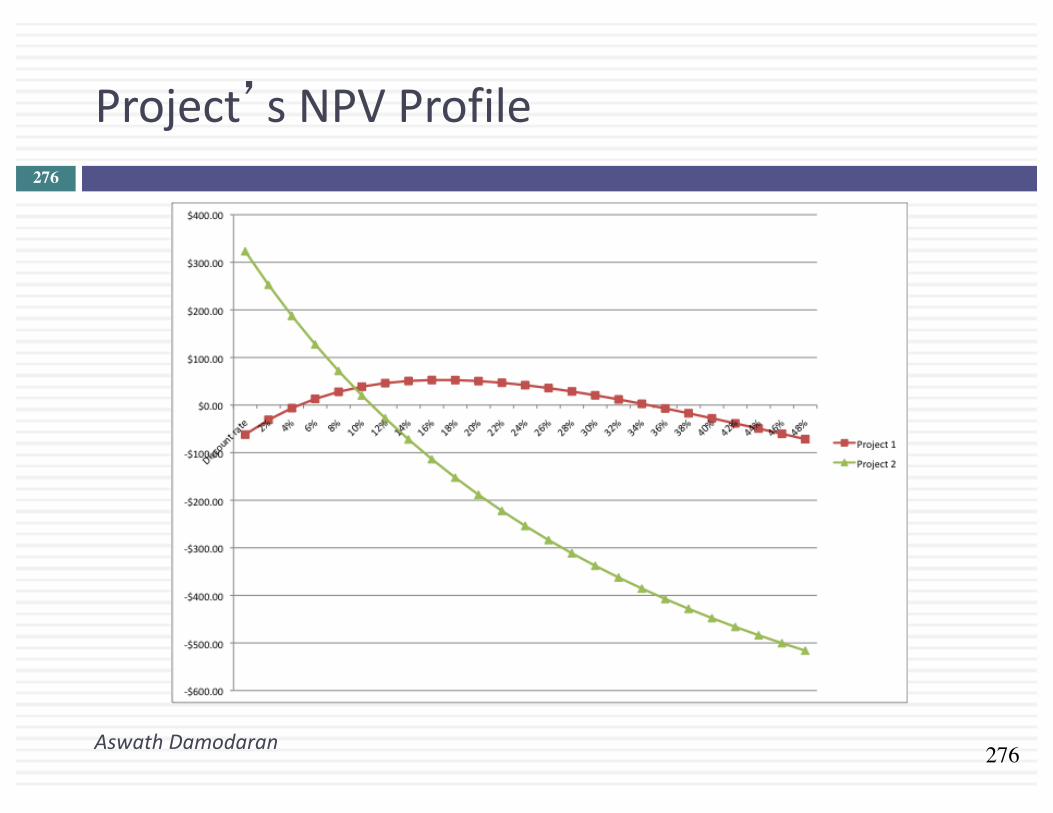

¨ Considertwoprojectswiththefollowingcashflows:Year Project1CF Project2CF0 -1000 -10001 800 2002 1000 3003 1300 4004 -2200 500

276

Project’sNPVProfile

AswathDamodaran

276

277

Whatdowedonow?

AswathDamodaran

277

¨ Project1hastwointernalratesofreturn.Thefirstis6.60%,whereasthesecondis36.55%.Project2hasoneinternalrateofreturn,about12.8%.

¨ Whyaretheretwointernalratesofreturnonproject1?

¨ Ifyourcostofcapitalis12%,whichinvestmentwouldyouaccept?a. Project1b. Project2

¨ Explain.

278

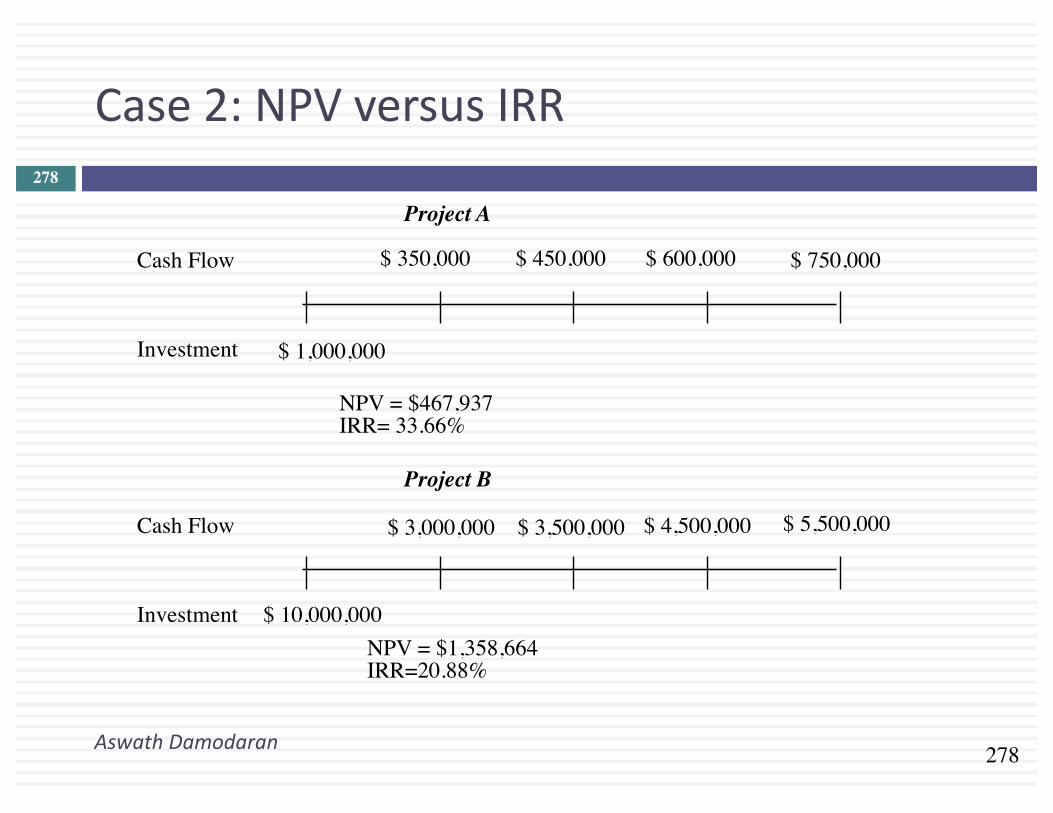

Case2:NPVversusIRR

AswathDamodaran

278

Cash Flow

Investment

$ 350,000

$ 1,000,000

Project A

Cash Flow

Investment

Project B

NPV = $467,937IRR= 33.66%

$ 450,000 $ 600,000 $ 750,000

NPV = $1,358,664IRR=20.88%

$ 10,000,000

$ 3,000,000 $ 3,500,000 $ 4,500,000 $ 5,500,000

279

Whichonewouldyoupick?

AswathDamodaran

279

¨ Assumethatyoucanpickonlyoneofthesetwoprojects.YourchoicewillclearlyvarydependinguponwhetheryoulookatNPVorIRR.Youhaveenoughmoneycurrentlyonhandtotakeeither.Whichonewouldyoupick?a. ProjectA.Itgivesmethebiggerbangforthebuckandmore

marginforerror.b. ProjectB.Itcreatesmoredollarvalueinmybusiness.

¨ IfyoupickA,whatwouldyourbiggestconcernbe?

¨ IfyoupickB,whatwouldyourbiggestconcernbe?

280

CapitalRationing,UncertaintyandChoosingaRule

AswathDamodaran

280

¨ Ifabusinesshaslimitedaccesstocapital,hasastreamofsurplusvalueprojectsandfacesmoreuncertaintyinitsprojectcashflows,itismuchmorelikelytouseIRRasitsdecisionrule.¤ Small,high-growthcompaniesandprivatebusinessesaremuchmorelikelytouseIRR.

¨ Ifabusinesshassubstantialfundsonhand,accesstocapital,limitedsurplusvalueprojects,andmorecertaintyonitsprojectcashflows,itismuchmorelikelytouseNPVasitsdecisionrule.

¨ Asfirmsgopublicandgrow,theyaremuchmorelikelytogainfromusingNPV.

281

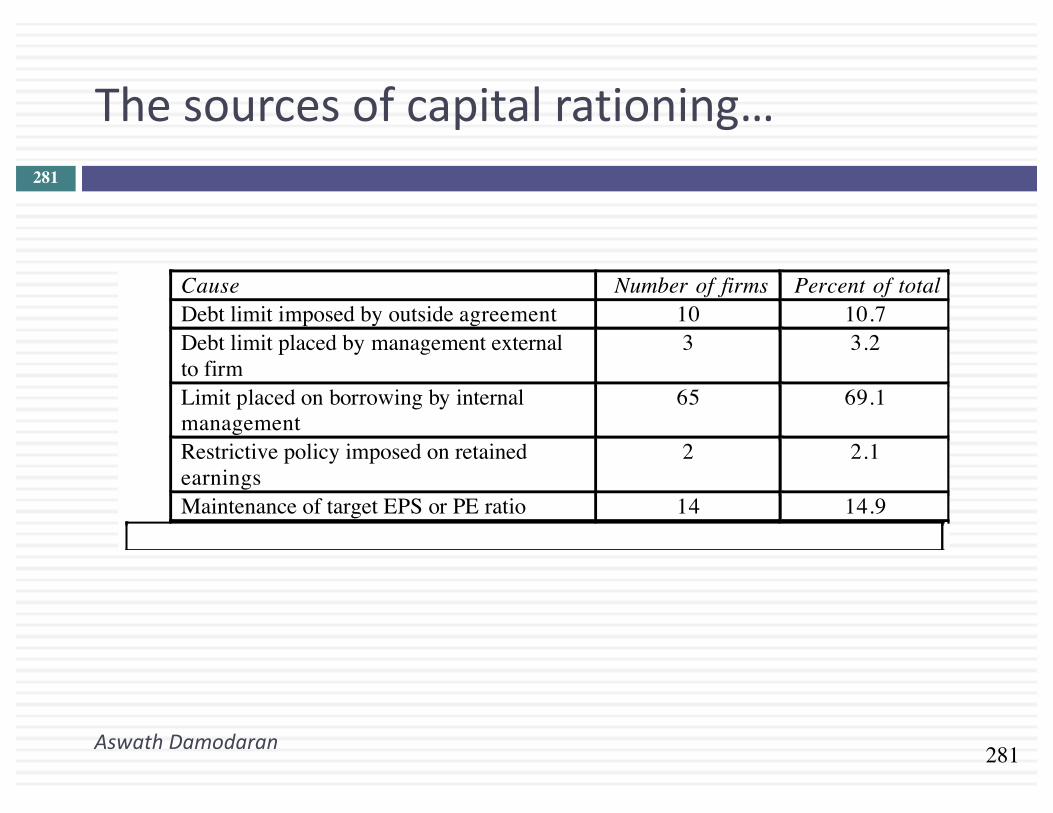

Thesourcesofcapitalrationing…

AswathDamodaran

281

Cause Number of firms Percent of total Debt limit imposed by outside agreement 10 10.7 Debt limit placed by management external to firm

3 3.2

Limit placed on borrowing by internal management

65 69.1

Restrictive policy imposed on retained earnings

2 2.1

Maintenance of target EPS or PE ratio 14 14.9

282

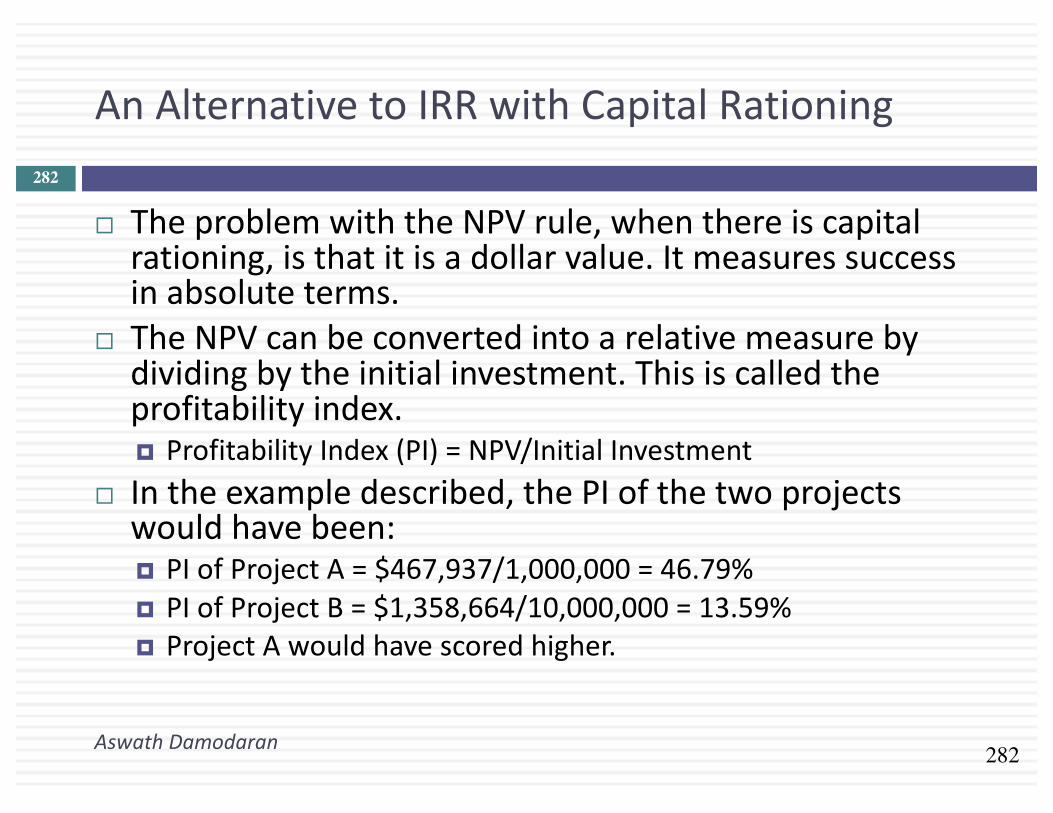

AnAlternativetoIRRwithCapitalRationing

AswathDamodaran

282

¨ TheproblemwiththeNPVrule,whenthereiscapitalrationing,isthatitisadollarvalue.Itmeasuressuccessinabsoluteterms.

¨ TheNPVcanbeconvertedintoarelativemeasurebydividingbytheinitialinvestment.Thisiscalledtheprofitabilityindex.¤ ProfitabilityIndex(PI)=NPV/InitialInvestment

¨ Intheexampledescribed,thePIofthetwoprojectswouldhavebeen:¤ PIofProjectA=$467,937/1,000,000=46.79%¤ PIofProjectB=$1,358,664/10,000,000=13.59%¤ ProjectAwouldhavescoredhigher.

283

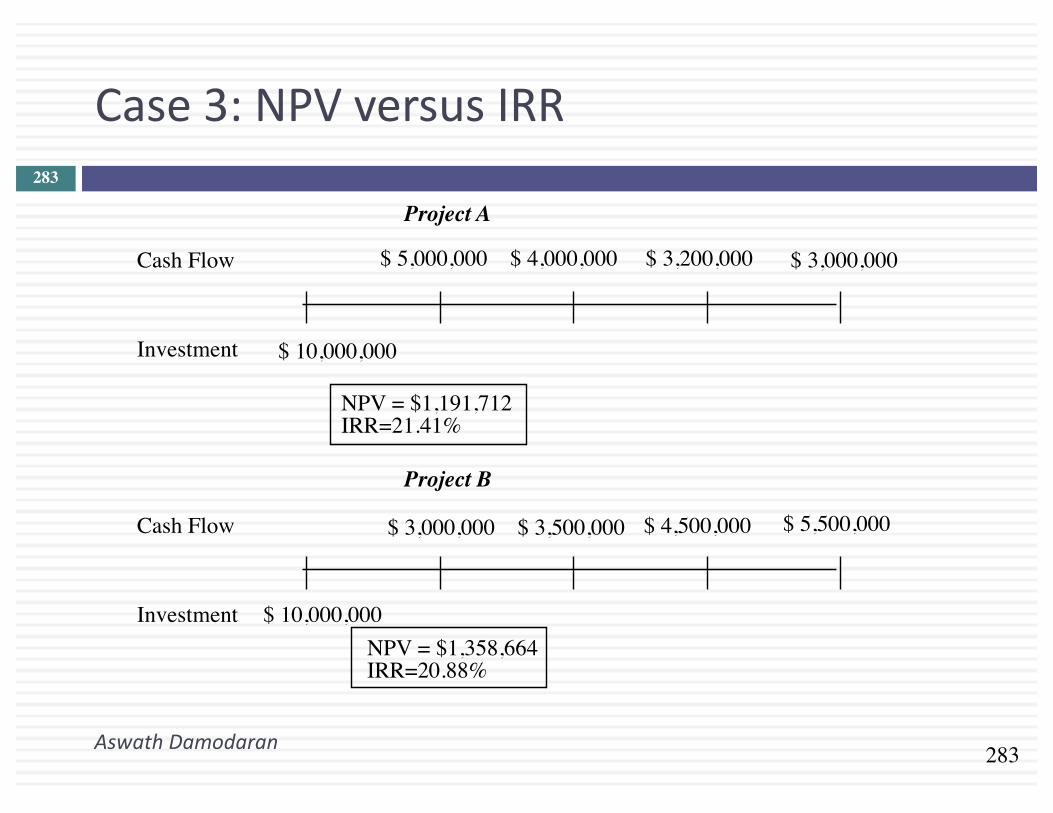

Case3:NPVversusIRR

AswathDamodaran

283

Cash Flow

Investment

$ 5,000,000

$ 10,000,000

Project A

Cash Flow

Investment

Project B

NPV = $1,191,712IRR=21.41%

$ 4,000,000 $ 3,200,000 $ 3,000,000

NPV = $1,358,664IRR=20.88%

$ 10,000,000

$ 3,000,000 $ 3,500,000 $ 4,500,000 $ 5,500,000

284

Whythedifference?

AswathDamodaran

284

¨ Theseprojectsareofthesamescale.BoththeNPVandIRRusetime-weightedcashflows.Yet,therankingsaredifferent.Why?

¨ Whichonewouldyoupick?a. ProjectA.Itgivesmethebiggerbangforthebuckand

moremarginforerror.b. ProjectB.Itcreatesmoredollarvalueinmybusiness.

285

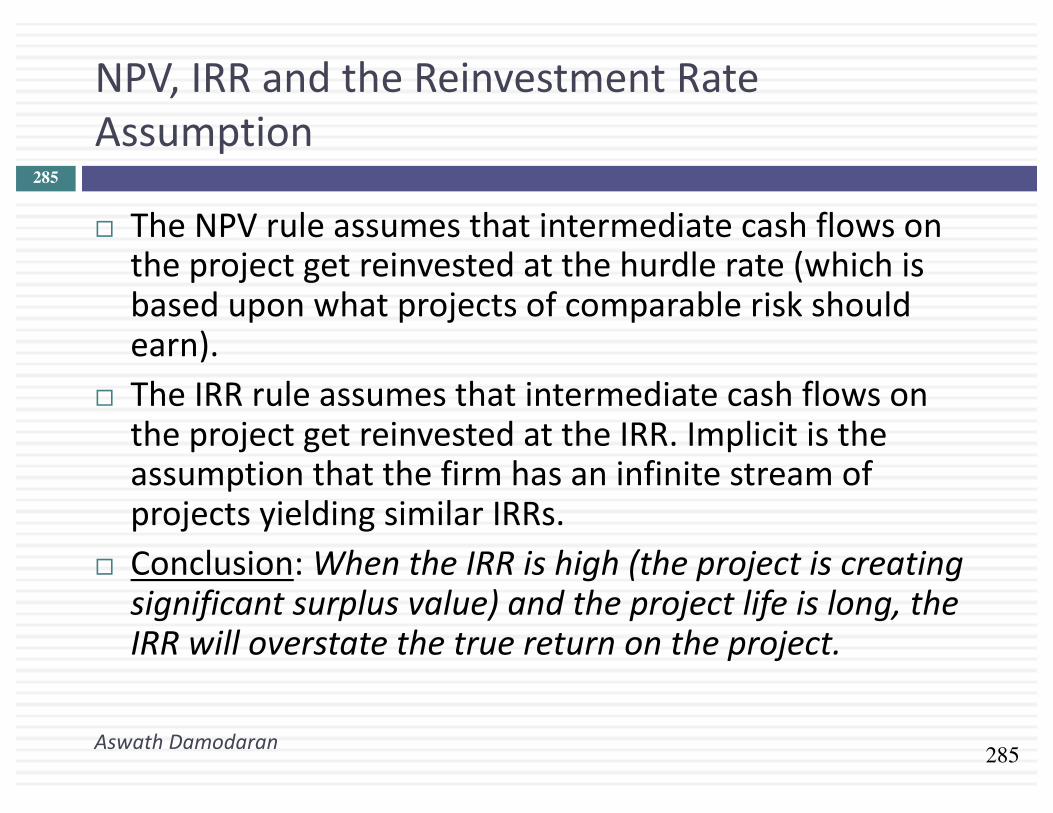

NPV,IRRandtheReinvestmentRateAssumption

AswathDamodaran

285

¨ TheNPVruleassumesthatintermediatecashflowsontheprojectgetreinvestedatthehurdlerate(whichisbaseduponwhatprojectsofcomparableriskshouldearn).

¨ TheIRRruleassumesthatintermediatecashflowsontheprojectgetreinvestedattheIRR.ImplicitistheassumptionthatthefirmhasaninfinitestreamofprojectsyieldingsimilarIRRs.

¨ Conclusion:WhentheIRRishigh(theprojectiscreatingsignificantsurplusvalue)andtheprojectlifeislong,theIRRwilloverstatethetruereturnontheproject.

286

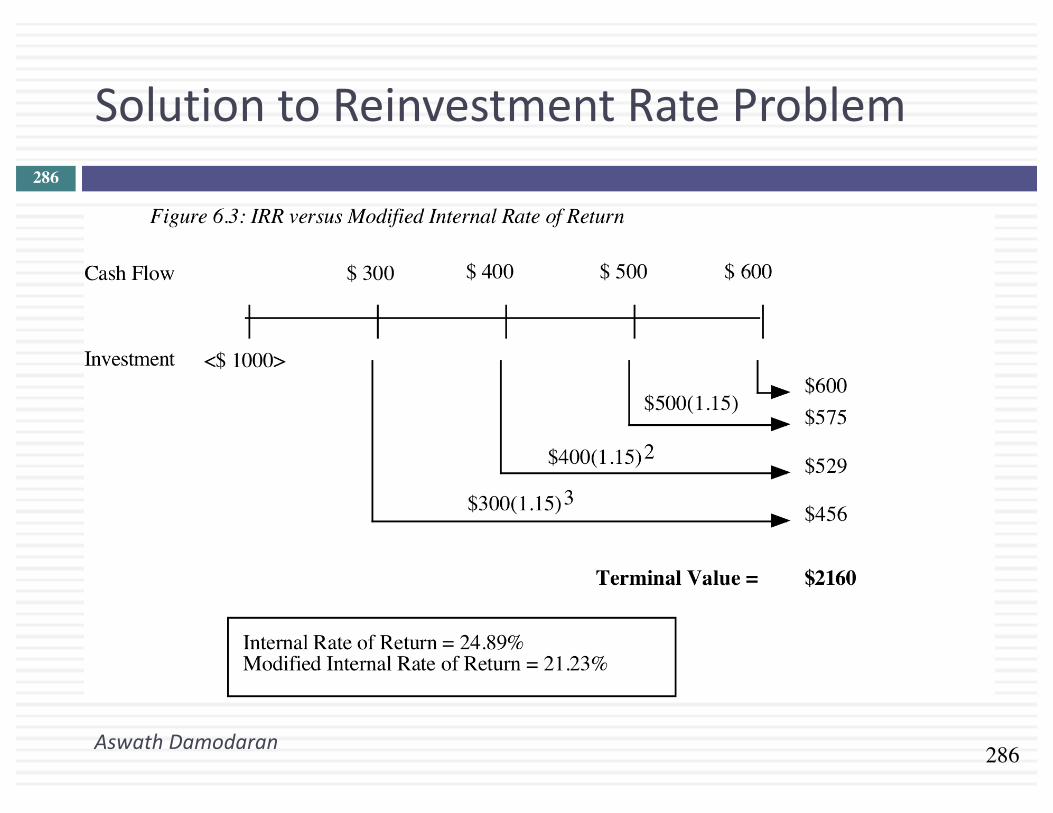

SolutiontoReinvestmentRateProblem

AswathDamodaran

286

287

WhyNPVandIRRmaydiffer..Evenifprojectshavethesamelives

AswathDamodaran

287

¨ AprojectcanhaveonlyoneNPV,whereasitcanhavemorethanoneIRR.

¨ TheNPVisadollarsurplusvalue,whereastheIRRisapercentagemeasureofreturn.TheNPVisthereforelikelytobelargerfor“largescale” projects,whiletheIRRishigherfor“small-scale” projects.

¨ TheNPVassumesthatintermediatecashflowsgetreinvestedatthe“hurdlerate”,whichisbaseduponwhatyoucanmakeoninvestmentsofcomparablerisk,whiletheIRRassumesthatintermediatecashflowsgetreinvestedatthe“IRR”.

288

Comparingprojectswithdifferentlives..

AswathDamodaran

288Project A

-$1500

$350 $350 $350 $350$350

-$1000

$400 $400 $400 $400$400

$350 $350 $350 $350$350

Project B

NPV of Project A = $ 442IRR of Project A = 28.7%

NPV of Project B = $ 478IRR for Project B = 19.4%

Hurdle Rate for Both Projects = 12%

289

WhyNPVscannotbecompared..Whenprojectshavedifferentlives.

AswathDamodaran

289

¨ Thenetpresentvaluesofmutuallyexclusiveprojectswithdifferentlivescannotbecompared,sincethereisabiastowardslonger-lifeprojects.TocomparetheNPV,wehaveto¤ replicatetheprojectstilltheyhavethesamelife(or)¤ convertthenetpresentvaluesintoannuities

¨ TheIRRisunaffectedbyprojectlife.WecanchoosetheprojectwiththehigherIRR.

290

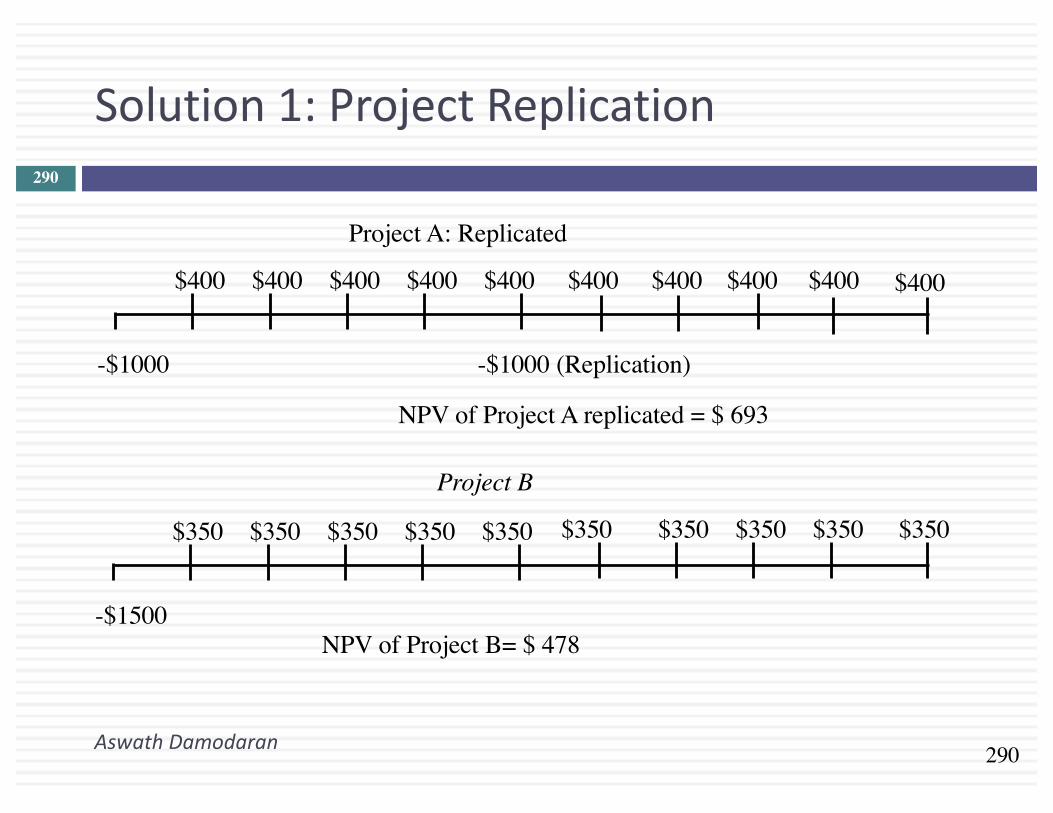

Solution1:ProjectReplication

AswathDamodaran

290

Project A: Replicated

-$1500

$350 $350 $350 $350$350 $350 $350 $350 $350$350

Project B

-$1000

$400 $400 $400 $400$400 $400 $400 $400 $400$400

-$1000 (Replication)

NPV of Project A replicated = $ 693

NPV of Project B= $ 478

291

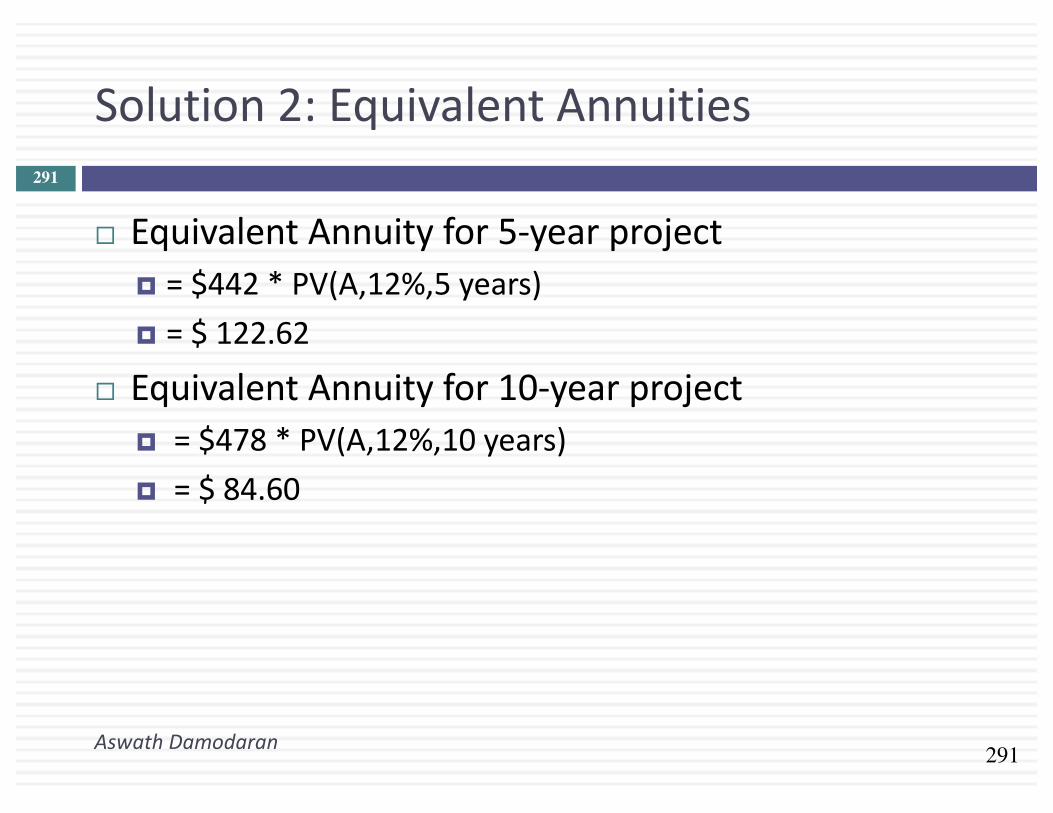

Solution2:EquivalentAnnuities

AswathDamodaran

291

¨ EquivalentAnnuityfor5-yearproject¤ =$442*PV(A,12%,5years)¤ =$122.62

¨ EquivalentAnnuityfor10-yearproject¤ =$478*PV(A,12%,10years)¤ =$84.60

292

Whatwouldyouchooseasyourinvestmenttool?

AswathDamodaran

292

¨ Giventheadvantages/disadvantagesoutlinedforeachofthedifferentdecisionrules,whichonewouldyouchoosetoadopt?a. ReturnonInvestment(ROE,ROC)b. PaybackorDiscountedPaybackc. NetPresentValued. InternalRateofReturne. ProfitabilityIndex

¨ Doyouthinkyourchoicehasbeenaffectedbytheeventsofthelastquarterof2008?Ifso,why?Ifnot,whynot?

293

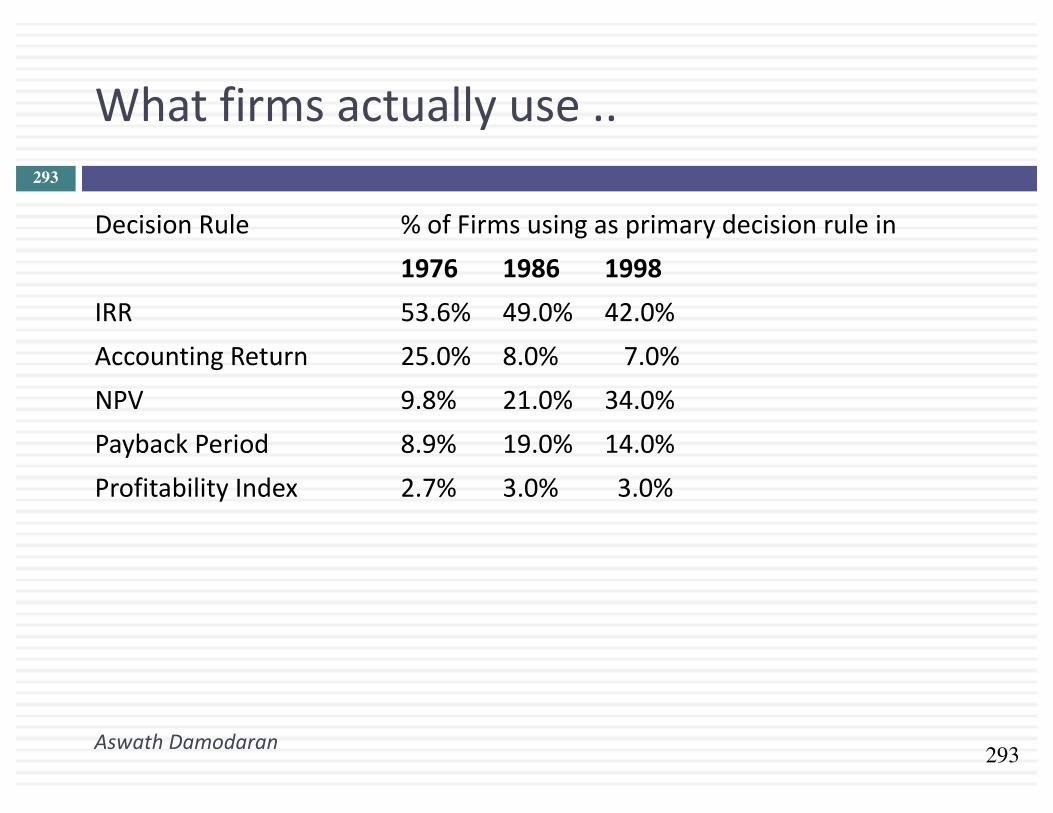

Whatfirmsactuallyuse..

AswathDamodaran

293

DecisionRule %ofFirmsusingasprimarydecisionrulein1976 1986 1998

IRR 53.6% 49.0% 42.0%AccountingReturn 25.0% 8.0% 7.0%NPV 9.8% 21.0% 34.0%PaybackPeriod 8.9% 19.0% 14.0%ProfitabilityIndex 2.7% 3.0% 3.0%

294

II.SideCostsandBenefits

AswathDamodaran

294

¨ Mostprojectsconsideredbyanybusinesscreatesidecostsandbenefitsforthatbusiness.¤ Thesidecostsincludethecostscreatedbytheuseofresourcesthatthebusinessalreadyowns(opportunitycosts)andlostrevenuesforotherprojectsthatthefirmmayhave.

¤ Thebenefitsthatmaynotbecapturedinthetraditionalcapitalbudgetinganalysisincludeprojectsynergies(wherecashflowbenefitsmayaccruetootherprojects)andoptionsembeddedinprojects(includingtheoptionstodelay,expandorabandonaproject).

¨ Thereturnsonaprojectshouldincorporatethesecostsandbenefits.

295

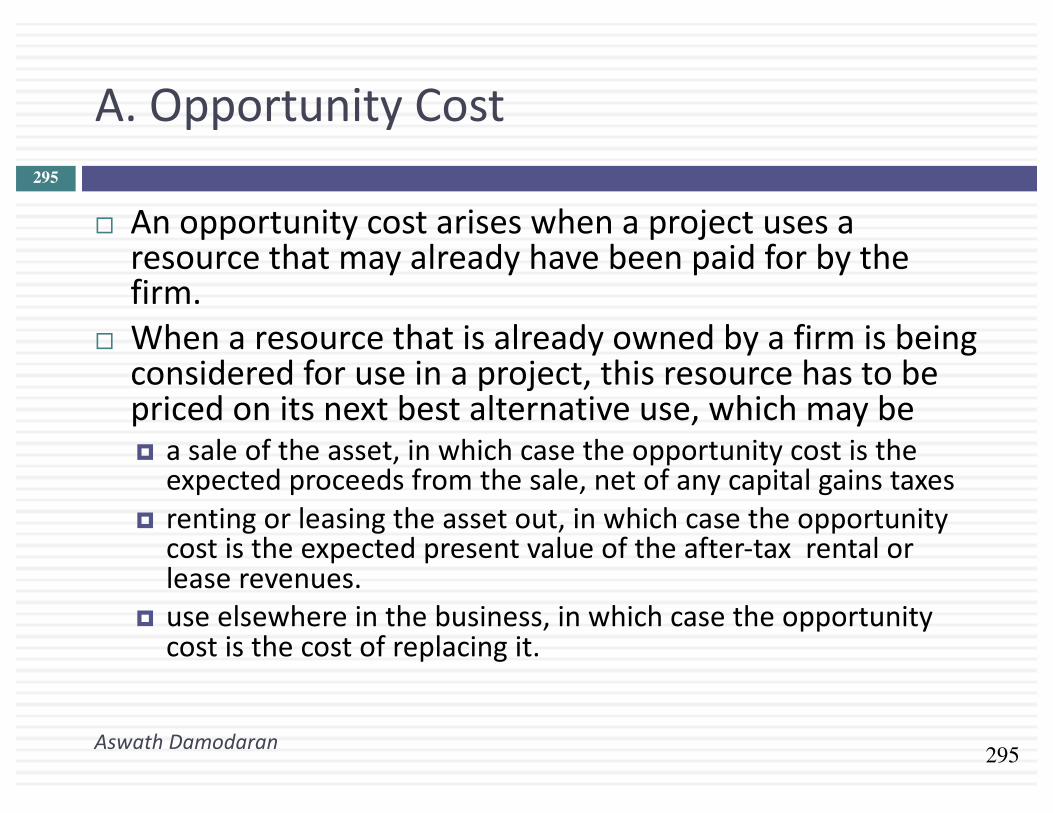

A.OpportunityCost

AswathDamodaran

295

¨ Anopportunitycostariseswhenaprojectusesaresourcethatmayalreadyhavebeenpaidforbythefirm.

¨ Whenaresourcethatisalreadyownedbyafirmisbeingconsideredforuseinaproject,thisresourcehastobepricedonitsnextbestalternativeuse,whichmaybe¤ asaleoftheasset,inwhichcasetheopportunitycostistheexpectedproceedsfromthesale,netofanycapitalgainstaxes

¤ rentingorleasingtheassetout,inwhichcasetheopportunitycostistheexpectedpresentvalueoftheafter-taxrentalorleaserevenues.

¤ useelsewhereinthebusiness,inwhichcasetheopportunitycostisthecostofreplacingit.

296

Case1:ForegoneSale?

AswathDamodaran

296

¨ AssumethatDisneyownslandinRioalready.Thislandisundevelopedandwasacquiredseveralyearsagofor$5millionforahotelthatwasneverbuilt.Itisanticipated,ifthisthemeparkisbuilt,thatthislandwillbeusedtobuildtheofficesforDisneyRio.Thelandcurrentlycanbesoldfor$40million,thoughthatwouldcreateacapitalgain(whichwillbetaxedat20%).Inassessingthethemepark,whichofthefollowingwouldyoudo:¤ Ignorethecostoftheland,sinceDisneyownsitsalready¤ Usethebookvalueoftheland,whichis$5million¤ Usethemarketvalueoftheland,whichis$40million¤ Other:

297

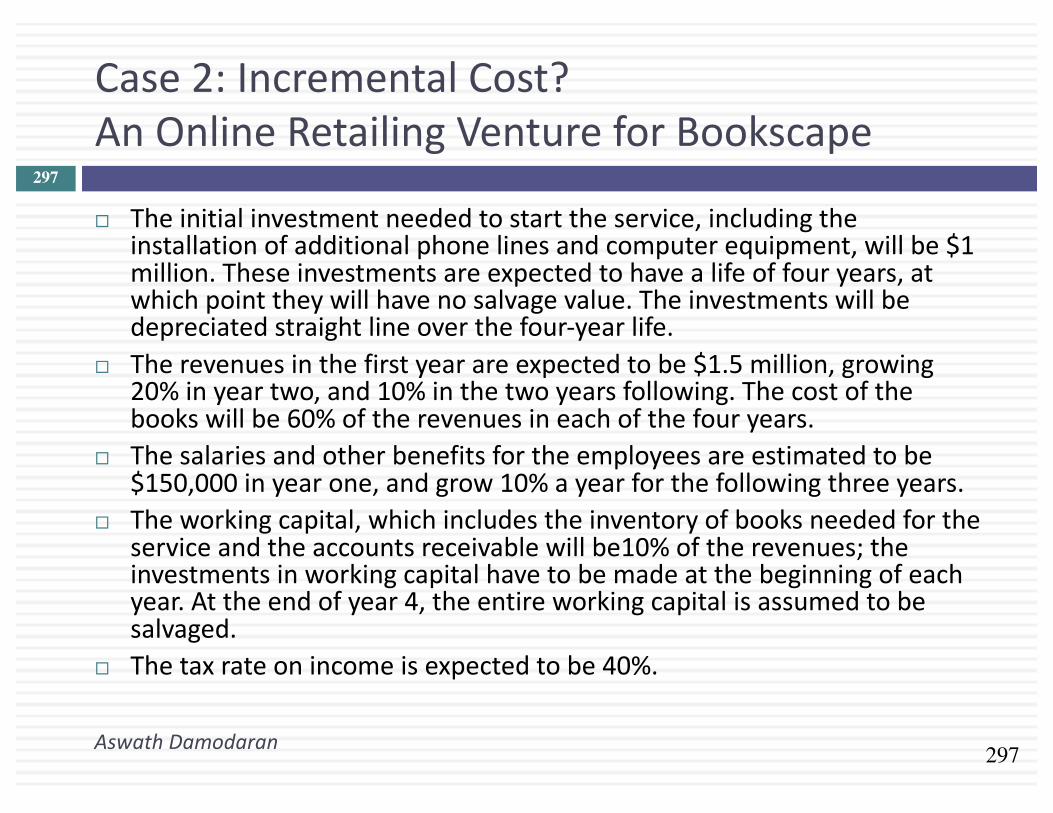

Case2:IncrementalCost?AnOnlineRetailingVentureforBookscape

AswathDamodaran

297

¨ Theinitialinvestmentneededtostarttheservice,includingtheinstallationofadditionalphonelinesandcomputerequipment,willbe$1million.Theseinvestmentsareexpectedtohavealifeoffouryears,atwhichpointtheywillhavenosalvagevalue.Theinvestmentswillbedepreciatedstraightlineoverthefour-yearlife.

¨ Therevenuesinthefirstyearareexpectedtobe$1.5million,growing20%inyeartwo,and10%inthetwoyearsfollowing.Thecostofthebookswillbe60%oftherevenuesineachofthefouryears.

¨ Thesalariesandotherbenefitsfortheemployeesareestimatedtobe$150,000inyearone,andgrow10%ayearforthefollowingthreeyears.

¨ Theworkingcapital,whichincludestheinventoryofbooksneededfortheserviceandtheaccountsreceivablewillbe10%oftherevenues;theinvestmentsinworkingcapitalhavetobemadeatthebeginningofeachyear.Attheendofyear4,theentireworkingcapitalisassumedtobesalvaged.

¨ Thetaxrateonincomeisexpectedtobe40%.

298

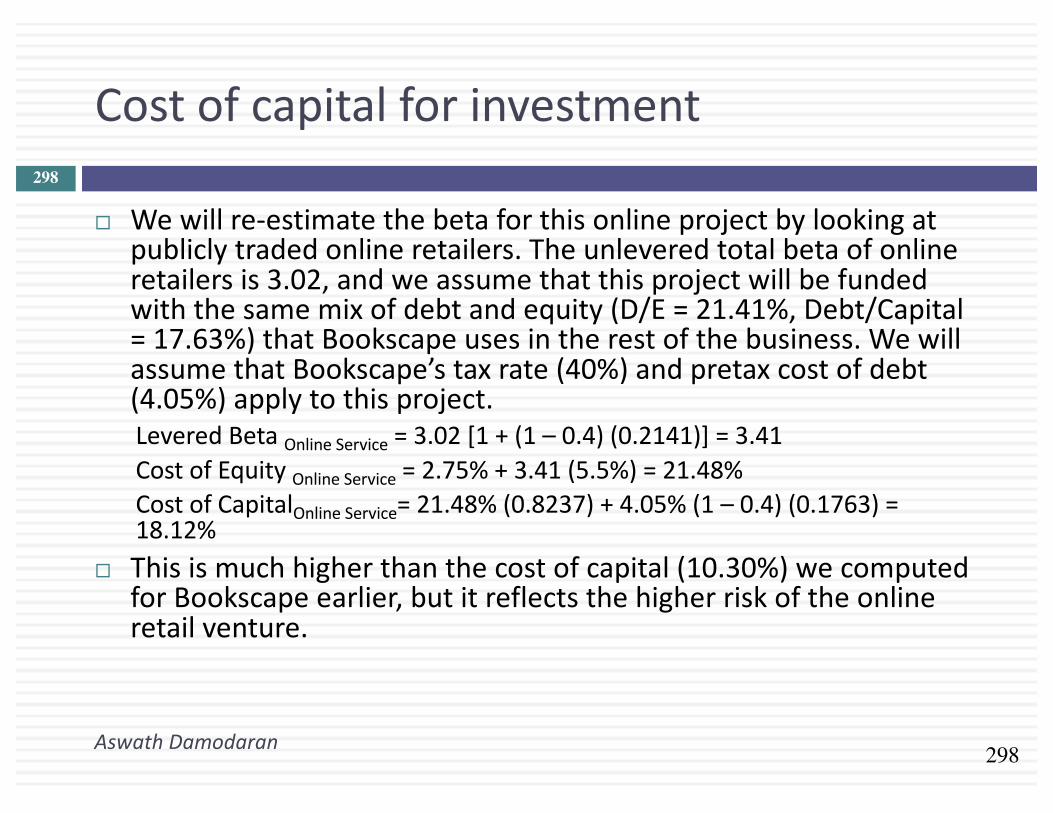

Costofcapitalforinvestment

AswathDamodaran

298

¨ Wewillre-estimatethebetaforthisonlineprojectbylookingatpubliclytradedonlineretailers.Theunleveredtotalbetaofonlineretailersis3.02,andweassumethatthisprojectwillbefundedwiththesamemixofdebtandequity(D/E=21.41%,Debt/Capital=17.63%)thatBookscapeusesintherestofthebusiness.WewillassumethatBookscape’staxrate(40%)andpretaxcostofdebt(4.05%)applytothisproject.LeveredBetaOnlineService =3.02[1+(1– 0.4)(0.2141)]=3.41CostofEquityOnlineService =2.75%+3.41(5.5%)=21.48%CostofCapitalOnlineService=21.48%(0.8237)+4.05%(1– 0.4)(0.1763)=18.12%

¨ Thisismuchhigherthanthecostofcapital(10.30%)wecomputedforBookscapeearlier,butitreflectsthehigherriskoftheonlineretailventure.

299

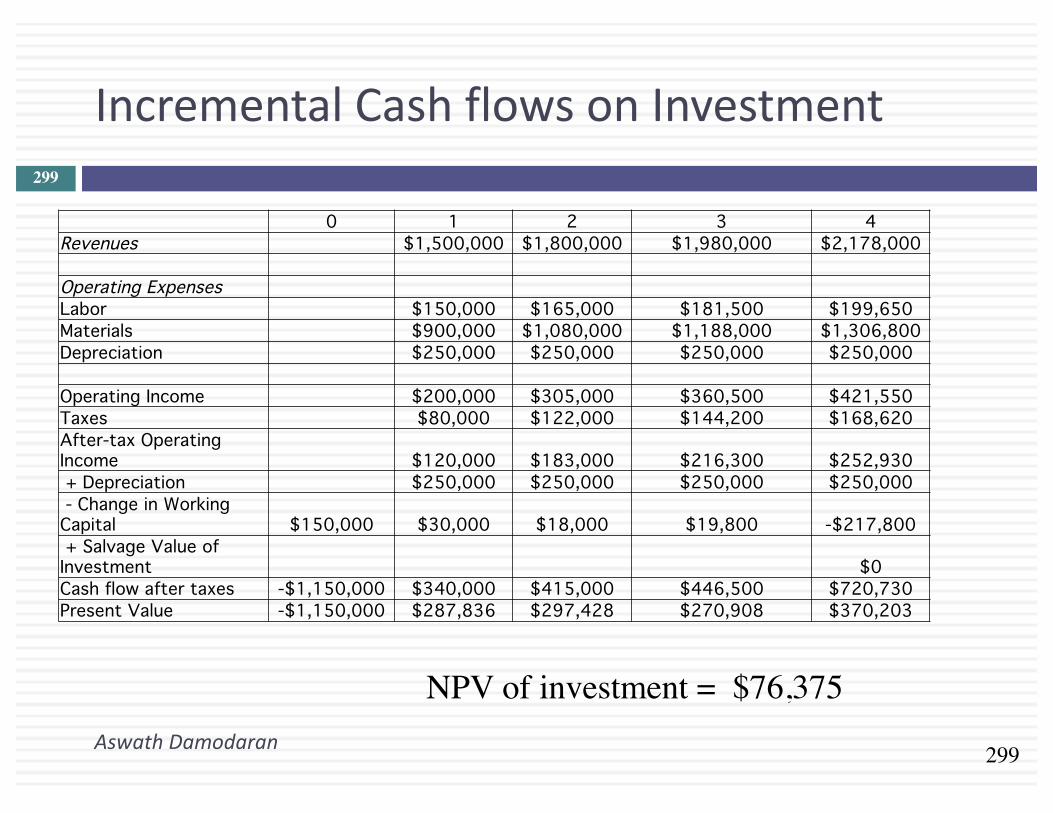

IncrementalCashflowsonInvestment

AswathDamodaran

299

NPV of investment = $76,375

0 1 2 3 4Revenues $1,500,000 $1,800,000 $1,980,000 $2,178,000

Operating ExpensesLabor $150,000 $165,000 $181,500 $199,650Materials $900,000 $1,080,000 $1,188,000 $1,306,800Depreciation $250,000 $250,000 $250,000 $250,000

Operating Income $200,000 $305,000 $360,500 $421,550Taxes $80,000 $122,000 $144,200 $168,620After-tax Operating Income $120,000 $183,000 $216,300 $252,930+ Depreciation $250,000 $250,000 $250,000 $250,000- Change in Working

Capital $150,000 $30,000 $18,000 $19,800 -$217,800+ Salvage Value of

Investment $0Cash flow after taxes -$1,150,000 $340,000 $415,000 $446,500 $720,730Present Value -$1,150,000 $287,836 $297,428 $270,908 $370,203

300

Thesidecosts…

AswathDamodaran

300

¨ Itisestimatedthattheadditionalbusinessassociatedwithonlineorderingandtheadministrationoftheserviceitselfwilladdtotheworkloadforthecurrentgeneralmanagerofthebookstore.Asaconsequence,thesalaryofthegeneralmanagerwillbeincreasedfrom$100,000to$120,000nextyear;itisexpectedtogrow5percentayearafterthatfortheremainingthreeyearsoftheonlineventure.Aftertheonlineventureisendedinthefourthyear,themanager’ssalarywillrevertbacktoitsoldlevels.

¨ ItisalsoestimatedthatBookscapeOnlinewillutilizeanofficethatiscurrentlyusedtostorefinancialrecords.Therecordswillbemovedtoabankvault,whichwillcost$1000ayeartorent.

301

NPVwithsidecosts…

AswathDamodaran

301

¨ Additionalsalarycosts=PVof$34,352

¨ OfficeCosts¤ After-TaxAdditionalStorageExpenditureperYear=$1,000(1– 0.40)=$600¤ PVofexpenditures=$600(PVofannuity,18.12%,4yrs)=$1,610

¨ NPVwithOpportunityCosts=$76,375– $34,352– $1,610=$40,413¨ Opportunitycostsaggregatedintocashflows

Year Cashflows Opportunity costs Cashflow with opportunity costs Present Value0 ($1,150,000) ($1,150,000) ($1,150,000)1 $340,000 $12,600 $327,400 $277,170 2 $415,000 $13,200 $401,800 $287,968 3 $446,500 $13,830 $432,670 $262,517 4 $720,730 $14,492 $706,238 $362,759 Adjusted NPV $40,413

302

Case3:ExcessCapacity

AswathDamodaran

302

¨ IntheValeexample,assumethatthefirmwilluseitsexistingdistributionsystemtoservicetheproductionoutofthenewironoremine.Theminemanagerarguesthatthereisnocostassociatedwithusingthissystem,sinceithasbeenpaidforalreadyandcannotbesoldorleasedtoacompetitor(andthushasnocompetingcurrentuse).Doyouagree?a. Yesb. No

303

AFrameworkforAssessingTheCostofUsingExcessCapacity

AswathDamodaran

303

¨ IfIdonotaddthenewproduct,whenwillIrunoutofcapacity?

¨ IfIaddthenewproduct,whenwillIrunoutofcapacity?

¨ WhenIrunoutofcapacity,whatwillIdo?¤ Cutbackonproduction:costisPVofafter-taxcashflowsfromlostsales

¤ Buynewcapacity:costisdifferenceinPVbetweenearlier&laterinvestment

304

ProductandProjectCannibalization:ARealCost?

AswathDamodaran

304

¨ AssumethatintheDisneythemeparkexample,20%oftherevenuesattheRioDisneyparkareexpectedtocomefrompeoplewhowouldhavegonetoDisneythemeparksintheUS.Indoingtheanalysisofthepark,youwoulda. Lookatonlyincrementalrevenues(i.e.80%ofthetotalrevenue)b. Lookattotalrevenuesattheparkc. Chooseanintermediatenumber

¨ WouldyouranswerbedifferentifyouwereanalyzingwhethertointroduceanewshowontheDisneycablechannelonSaturdaymorningsthatisexpectedtoattract20%ofitsviewersfromABC(whichisalsoownedbyDisney)?a. Yesb. No